Last week sinks in, and WHOOSH go yields.

By Wolf Richter for WOLF STREET.

The average 30-year fixed mortgage rate spiked to 6.39% today, according to Mortgage News Daily, having bounced by 40 basis points in two days off the low of 5.99% on Thursday, giving up a month worth of declines in two days.

Gone are the hopes for “stability” in mortgage rates – meaning lower mortgage rates with smaller moves – that the housing industry has been hoping for and talking about, including homebuilders that just gave their Q1 guidance based on mid- to late-January sales orders, when mortgage rates were a lot lower and apparently heading lower still. And now the wild ride has started all over again.

The two-year Treasury yield has jumped by 37 basis points since the close on Thursday, the day after Powell had spoken: 16 basis points today and 21 basis points on Friday, to 4.46%, unwinding in two days more than half of the 65-basis-point decline from the high in early November:

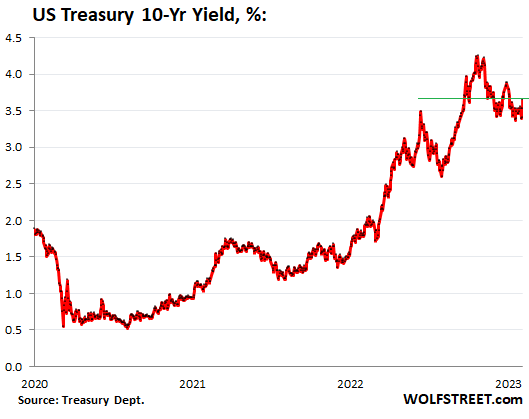

The 10-year Treasury yield has jumped by 25 basis points since the close on Wednesday, Powell-day, including 11 basis points today so far and 13 basis points on Friday, to 3.64% at the moment, unwinding in three days over a quarter of the large 88-basis-point drop since late October.

In an amazing feat, the bond market blew off – temporarily, so to speak – Fed Chair Powell’s discussion about inflation last Wednesday, how “core services inflation without housing,” which constitutes 55% of the core PCE price index that the Fed uses as its inflation yard stick, was not subsiding at all; how further rate “increases,” plural, meaning two or more, would be coming, and how no rate cut was on the table for 2023.

They looked at his slumped posture and heard his soft voice, and heard how he struggled to politely answer the same stupid leading questions over and over again, instead of just Tasering the reporters one after the other, or something. (I listed these stupid leading questions at the bottom of my What-Powell-Really-Said article.) And markets, whoever they are, thought Powell was promising a pivot or whatever.

I mean, it’s the markets, and they’re a crazy bunch and they do whatever for whatever reason, and a big bout of short-covering might have had something to do with it last week. That willful misreading of what Powell actually said was funny nevertheless.

But the honeymoon ended on Friday, when the jobs report drove home in vibrant detail what Powell had said about the labor market on Wednesday – that it was still feeding into “core services inflation ex-housing,” and that therefore a pivot wasn’t on the table this year. And today, it sank in further, and WOOSH go yields.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Last week the chance that the Fed hiked rates to 5.50% by June was priced at 4% probability.

Now it’s at 30% probability

I’m hoping my brokerage money market goes to 6% this year and I’m happy with average 3 month yield trending higher.

Deficit battle will help nudge that higher (again).

Thank you for putting this report out WR!

MSM would never tell these reports out.

Personally, I think if Powell was more serious about taming inflation, he would have done 50bps hike and also not said that ” deflation is under way” which was what market in general picked up.

It’s the FOMC that votes on the rate hikes.

What is startling about the FOMC statement is that it was completely oblivious to the end of COVID-Zero in China. It’s very hard for me to see that as a deflationary development.

I think Powell as Chairman has veto power and can override all decisions.

Maybe it was “disinflationary”.

right. he said disinflation.

disinflation is still inflation.

In terms of energy demand, definitely inflationary. In terms of crappy Chinese stuff sold at Wal Mart, deflationary, because they need to export or die, sell cheaply, to pay for imported food and energy. Probably more inflation to come, if you look at Shadow Stats, which assesses inflation using 1980 CPI metrics. Just a little Fed head fake, folks!

Jon : YES

He would have done 50bps hike / >>>>>> BUT <<<<<<<<<<<<<>> ” Results ” <<< Daily Info Sheet /

Publishing the " Cause " : Can be seen on the Daily News / upcoming Court Trials as example on and on

I believe he “disinflation”, not “deflation”.

All I can say is, I love reading The Wolf

Me too. Wolf is the only one I know of who saw Powell’s latest speech as hawkish. Everyone else (incorrectly) interpreted it as announcing a pivot. Not just those who want a pivot, even those who want interest rate hikes to continue, such as one of my favorite writers Doug Noland, saw it as a dovish speech and he seems really depressed about it…for nothing it would appear.

‘instead of just tasering the reporters one after the other’… LOL

I would enjoy that immensely. Instead it seemed he tasered bbby stock and it shot the moon!

Yes, the sudden jump in treasury yields has certainly caught our attention.

Still – I’m not convinced that the market’s anticipation of a Fed pivot has anything to do with the Fed’s desire to avoid a recession. I don’t think there’s ever really been a question that the Fed is willing to accommodate a downturn in order to try to fight inflation (whether it’s realistic to expect Fed interest rate adjustments to be able to effectively fight the current bout of inflation is a separate question that I won’t tackle here).

Rather, I think the market is anticipating the arrival of a Black Swan – whether it’s a crack up in the credit markets or a sudden loss of liquidity in the Treasury markets, or something related to a global conflict – as the event that prompts the pivot. And I can’t say I strongly disagree – the Fed’s tightening actions are a bit like walking a tightrope whilst juggling molotov cocktails. Expecting to walk back 40 years of ever-increasing monetary accommodation without significant and serious consequences just does not seem reasonable to me.

If FED has to pivot because of some events like you mentioned then first market would crash then may go up.

It means FED pivot would bring bad news for market before it pivots.

“…anticipating the arrival of a Black Swan….”

Then it’s not a black swan. Not to pick nits, but this is an important point. A black swan is a completely unexpected and unpredictable occurrence which in no way can be “anticipated.”

The events which most people describe as “black swans” aren’t really black swans.

Reminds me of a lunch conversation with one of the Big 4 accounting firms while I was in India in early October 2008 right after Lehman blew up.

Someone asked, who could have seen it coming?

My response? It’s hard to believe it took this long. (No, I didn’t specifically know or anticipate the Lehman collapse. It was still the biggest asset mania in history. until it got even bigger the last 14 years.)

grey swan events, in the parlance

I think that black swans should be available for purchase. Then you could send them to people you know who are very composed and sanguine. The arrival of a black swan would be equivalent to the Monty Python routine where the Spanish Inquisition shows up at a most inconvenient time.

I imagine that there’ll be a host of black swan wannabes: black ducks, pink swans, polka dot wildebeests…

I knew people who were talking about AIG before Enron blew.

There are book cookers, and there are chefs.

How/Shiloh – “…no one expects the Enron Management Team!!!…”.

may we all find a better day.

True. Partly depends on what variable for an event is considered unpredictable (i.e., uncertain). In order to discount an expected future event one has to stake the event to some time window.

There can also be positive or negative swan events.

Depth Charge,

You are, of course, correct.

A more apt description would have been “emergence of a new large-scale problem the timing of which cannot be precisely-anticipated”.

But I stand by my observation that investors are expecting some form of cataclysm to prompt a pivot and are willing (however dangerously) to place positions that front-run it.

Markets cannot anticipate black swans. Greys, maybe depending on where you stand on EMT that is none too popular in these comments, but not black.

Black swans happen and then hindsight boas makes us think they were predictable all along if we were smart enough and/or listened to the right people. Grey swans are somewhat predictable but resistant to modeling as they are low frequency or low probability events, generally lost in the din of daily noise.

Black swans, meaning unpredictable? I am surprised that treasury purchasers are still reportedly buying at such low, effective interest rates that appear to be below the rate of inflation. I understand why the bankers and financiers want ultra low interest rates, below the real rate of inflation (whose measure is admittedly arbitrary based on the goods/services whose prices are selected): they get their liabilities, e.g., owed to depositors, reduced over $1 TRILLION a year.

Why have investors been accepting effectively negative interest rates, after accounting for inflation, given what I opine is a real inflation rate higher than those interest rates? That is my question. I would not, because rates required to be paid on rolled over treasuries might spike a lot as baby boomers retire, events may make lenders more cautious, and capital becomes more dear.

Big Al,

Guess everyone got sarcastic about credit crunches. I would suggest the fed won’t sell mbs because it’ll demonstrate some unwanted price discovery that may lead to other issues of over leverage discovery in many other markets. Call it a platypus but such an event has very obvious potential for contagion.

Reduction in Corp earnings, refinance costs and inflated multiples could precipitously slam equity and bonds. CdS tank, Down goes gold, btc and then we’re off folks, on a very ugly drop.

Everyone is crowding into short term treasuries ,I’m almost out this boat is too crowded . Usually doesn’t end well

The great thing about 4-week T-Bills is that it can *only* end well. Zero risk, extremely short time frame, decent yield relative to other Treasuries.

A few years ago I would have laughed if anyone suggested that a Fed Chair’s slumped posture and thin voice effected markets – rather than the words he actually spoke – but here we are.

I’ve read similar thoughts elsewhere, and – yes – I’d now be willing to bet his demeanor is absolutely a critical part of the story.

Is this what they call a teachable moment?

ZZ – (first the Pythons and now SNL, today) mebbe “…it’s more important to LOOK good than to BE good…” (thank you ad, entertainment, and financial ‘industries’…).

may we all find a better day.

As the saying goes,

“When you fall off a skyscaper, it’s not the fall that kills you,

it’s the sudden stop.”

Today’s much higher interest rates are really taking their time to pressure business people, because the reality of the situation is only felt when old debt needs to be rolled over into new, much higher interest rates.

Denial is especially rampant in the commercial real estate industry, which is filled with trust fund babies who have been getting their way their whole lives. They can’t believe that they are finally about to get steamrolled, and no one cares about their wants or needs on this particular matter. They don’t want to believe it’s happening, so they just commit to acting like it’s not happening.

Generally, in past rate hikes, it has taken up to a year for the effects to become noticeable in the economy. This is about the fastest series of hikes ever and I expect nearly all of the effects are still ahead of us. On top of that, the Fed is burning $95 billion per month. Even alone, that amount of reduction in money supply should begin to show up, despite the commercial banks pumping activity.

@GrassRanger Are the commercial banks pumping? What is the source of your opinion?

Grass Ranger,

The Fed burn rate is actually closer to $75-80 billion. Even so, the M2 did fall for the first time in 40 years in 2022.

@The Sick Economist,

Yes – I’d forgotten about a Commercial Real Estate implosion. Seems inevitable to me – as would a Muni Bond crisis – but I think there are cataclysms that will emerge to prompt a pivot before those force one.

Pushing up EFFR serves to move bond investors to the short end of the curve, and they’re still there. Saving desposits are dropping, a signal no one left who has not gotten the word. The 1Y is trending higher than the 20Y. There are only hostage investors at the long end, pension funds and insurance companies. Counter intuitively rates will rise when the short end collapses (implied message from the FED – YES we’re going to pivot). Investors will demand higher return further out the curve. How they effect that I am not sure. The Treasury can’t continue to misprice their paper without consequences, when Bids in the secondary market start to push the envelope.

6.39 mortgage rates. Oil is down now, projected higher too. They say that oil is volatile, so will everything else be. Inflation and rates IMO. Like you said before Wolf and all along.

Haha the market.. I keep picturing in my head if this collective as a market is a person.. it would be the most douchebagish obnoxious know it all person one can ever meet..

Everytime someone preaches about market (both stock and bond market) wisdom.. I just get this thought if wanting to punch the market in the face… guess the 10 years yield new is doing that.

The market is an idiot. Back in 1841 Charles Mackay wrote “Extraordinary Popular Delusions and the Madness of Crowds”. Nothing has changed since then.

You can look around and see that the unemployment rate is not going up.

Practical action question: I have a Vanguard acct. I bought some tbills through them. Is there any benefit to buying it directly vs. going through Vanguard. Also bought a bunch of short-term brokered CDs.

Thanks.

I may be wrong but per me, you can’t buy tbills directly from anywhere esle but from treasurydirect.

You can buy TBills ETF but you pay some fee on them.

PLease correct me if I am wrong.

I was able to buy them on the vanguard site — they are listed as BROKERED CDs and Treasuries —

That’s not correct. You can buy directly from TD Ameritrade. I did, I started out on treasurydirect, really hated their portal and the hoops they make you jump through if you want to sell. Not so much of an issue on short term Tbill but a huge PITA for individual trying to sell Tnotes early. Doing it on TD is so much easier, not to mention you can also buy new issue there as well.

These are actual Tbills. I did make the mistake of getting an ETF before. Won’t make that mistake again.

@elbowwilham,

I buy T-Bills through Fidelity and through TreasureyDirect. The only negative experience I have had with TD is when I needed to download some tax forms. I couldn’t remember my security questions and got locked out of my account. So I had to call their customer support phone number. I was on hold for 1 hour and 20 minutes. They are swamped right now because everybody and their Grandma wants to buy I-bonds. I did get thru though and they unlocked my account. Other than that, all of my buying of T-Bills through them has been online, and has worked very well.

Not correct.

E.g. I am buying from Fidelity(BrokerageLink), Merrill and TD Ameritrade.

Moreover, I recall Wolf (?) said is is least convenient to buy treasuries from TreasuryDirect, don’t remember why though.

Use their website and look up how to sell your Tbill/notes and you’ll see why

Thanks, I didnt know this.

I buy form treasurydirect.gov.

Phoenix: perhaps “convenient” was not the best word choice… (and they had their website reworked recently)

The problem is – had to look it up – if you want to sell before maturity, you have to do via a broker.

Alku,

The sign-in process is a hassle with its on-screen keyboard and emailed pass-code. I think that’s what I said. It’s trying to be very secure. Security means less convenient.

But once in the site, I find it OK to use. The info is good. It’s easy to buy stuff. It lists the upcoming auctions, so you can choose at which auction you want to submit your bid, etc. That part is just a breeze.

We have a bunch of i-bonds in our accounts, which is buy-and-forget-for-30-years stuff. You don’t even have to deal with a 1099. I-bonds were the main reason we opened accounts there. You cannot get this stuff at your broker.

There are things that are a hassle. I’ve heard horror stories from people that closed the linked bank account and want to link a new bank account (don’t do that!!). If you want to sell securities before they mature, I think you need to transfer the securities to your broker. I’ve never done this, but that’s what it looks like to me. There may be other hassles that suddenly hit you if you want you try to do something a little different.

But I think its ideal for “buy at auction and hold to maturity” transactions, for money that you really don’t want to lose. I consider this account a little more secure than my brokerage account — even if it has the same securities in it.

If you buy through a brokerage, are the TBills held in your brokerage’s name?

Buy them at your Broker.

Take a look at other forms of guaranteed certs. I’ve been buying GIC’s. 5.05% on 1 and 2 year terms.

Last time I owned one of these boring assets, 2000, ahh.

What are GICs? Haven’t seen that abbreviation before!

I was interested in purchasing short-term Treasury stuff, through Treasury direct, but decided to not lock myself into any specific bills or bonds and be more liquid with the right brokerage account.

Buying directly from Treasury gets you a higher yield versus, primarily because there are various fees associated with services and management costs at a brokerage. The brokerage doesn’t charge you for the purchase, but it’s wise to look at annual fees.

The thing I don’t like about Treasury is the super clunky website they provide. It also made me nervous, that if you screw up your login, they can suspend your account. I’m not sure how that process works, but Treasury is not exactly customer friendly.

I decided I’d rather lose a little in fees at a brokerage and have a smoother experience. The best way to look at fee costs, is to look at the interest rate your bank offers (close to zero) versus like paying a money market $40 a year on a money market making close to 5%+.

This is not advice, but many traditional banks are seeing lots of customers move deposits into mutual fund money market accounts.

Last thing, make sure you’re in government like Treasury funds that are NOT gated! If things head south and markets fall apart, you want liquidity and some money markets are GATED.

Do your DD!!!

I’m sure they snag some pennies, but I buy EZ through my Schwab account. Point. Click. Done.

I buy treasuries at auction and hold to maturity at Schwab. No commissions to buy at auction, or to buy or sell in the secondary market. I think Vanguard is the same, but I find its website to be buggy. With Treasury Direct, you have to transfer treasuries to a broker if you want to sell before maturity.

As for I-bonds, Treasury Direct is the only game in town. It’s website is archaic, and crashes if their is a rush, usually a rush to buy I-bonds. It is a typical government website, poorly designed and down too often. If you like websites from the 1990s and enjoy playing hide and seek when looking for information, you might like it.

Tonight the president will sink buybacks, tax billionaires and cont to cut entitlement. The Irish gang will not split. The dbl McD will not rip

his speech.

Maybe why the money dropped hard at the close today. He has to go after the rich. A 30% sales tax on groceries? Hugely inflationary, just not sure Wall St will lose its access to easy money.

America already ‘goes after the rich’ who are saddled with so high a proportion of the cost of American government. The Rich are one of our most oppressed minorities.

“The Rich are one of our most oppressed minorities.”

I love your sarcasm LOL

Yes, please take a moment to pity the rich.

Show me Warren Buffet’s tax rate. Or better yet, show me how much Buffet’s Marginal tax rate changes when he sells a billion in stocks

Oh wait, his secretary has a higher tax rate than he does

‘A 30% sales tax on groceries?’

Are you getting authors mixed up? It was the other guys who proposed that tax.

‘Bumbling’ – huh? Acting in a confused or ineffectual way; incompetent.

The president who just saw the best performance of their party in an off-year election in memory is bumbling. **insert eyeroll .gif**

Cutting SSI and Medicare will not win over the AARP.

Voting to layoff IRS agents is not the same as funding a strong defense.

It’s amazing that the correction in rates hasn’t seemed to have a dramatic effect on the stonk mocket. BBBY was up 100% today too! Something has to give.

BBBY collapsed afterhours. Funny story coming.

I wouldn’t buy BBBY if the sweet lord Jesus came down and asked me himself.

Nah, in that case The Lord just wanted you broke for some reason, gotta trust that.

Lol!!!

Apes getting shanked once more. Nothing new, they’ll gladly do it again and take it up the ass again.

LOL there is no market anymore! It’s all speculative gossip. Real earnings don’t matter. PE ratios don’t matter. It’s all about debt/credit, interest rates, what the Fed will or won’t do. Total and complete clown world. 3M laying off thousands. Dell laying off thousands. 2/3 of Americans living paycheck to paycheck and can’t come up with an extra $400. Interest on the debt is approaching a trillion dollars. Oil is going to spike just watch. It’s an economic hurricane coming. And housing prices have barely budged. People spending like crazy. New cars, restaurants packed, Starbucks record sales.

“People spending like crazy. New cars, restaurants packed, Starbucks record sales.”

Yes!!! This simple and correct line at the end contradicts much of what you said about consumers before it.

“2/3 of Americans living paycheck to paycheck and can’t come up with an extra $400.”

LOL. Lots of Americans have lots of money. here’s the average wealth per household, by wealth category in Q3, 2022.

The top 50% of households (= 65 million households = 132 million people) are in bold. Look at their wealth.

“Top 0.1%”: $132.4 million

“Remaining 1%”: $19.3 million

“Next 9%”: $4.4 million

“Next 40%”: $768,000

“Bottom 50%”: $70,800.

https://wolfstreet.com/2022/12/21/fed-tightening-reduces-horrendous-wealth-disparity-that-qe-and-interest-rate-repression-have-wrought-fed-data/

That’s the average. Median is probably a lot worse.

Will 3M become the next JohnsManville?

And I see talking heads on tv ,one says market down 40% . Next one says market up 40% in 10 months. Figured out no one kKNOWS SHIT. Except 2 nd guy is winning so far it’s early in the casino.GOOD LUCK

Clearly no one knows what’s going to happen re inflation. So goes inflation, so goes the FED.

Makes sense as we’re commonly off a low frequency event (post-pandemic global shutdown of economy), with some newer modern twists (supply chain, globalization, redomestication of work force).

We have some historical parallels, but scant data, at least readily accessible to the “smarts” who comment and/or trade. Decision making by historical analogy always rather dangerous.

“Clearly no one knows what’s going to happen re inflation.”

That’s what I think.

Powell comments tomorrow will be interesting as will the inflation data due on the 13th. Which way the 10 year? Back to 4.5 or heading down to 3%?

My guess is that the 10 year is going up. I can’t claim to understand the current level, but it seems too low.

The slow witted shot ballooned entitlements he loves so much. Fred : Federal gov Transfer Payments down from $5T in Q1 2021 to $2.9T. More balloon will cut.

In 1960 Ike and Nikita had a fist fight because Gary Powers, a weather

man, Parachuted in Russia.

Yes, I suppose that JP’s demeanor is one explanation for the seemingly troubling gyrations in the “financial markets”.

There are other plausible explanations why a synthetic market would gyrate in such an unexpected fashion.

Meanwhile, a bottom feeder hedge fund makes $16 B. Go figure.

I guess that, after 20 years of monetary policy laser focused on, not only controlling the interest rate, but dedicated too doing whatever it takes to drive it too zero.

That the interest rate curve doesn’t seem rational too me. Let alone the loud closure of the vacuum that had formed in the bond market, home of the so called ” bond vigilantes”.

Now they are known as the ” bond wimps”, hammered into submission by an unrelenting ” bond villain”, the Fed.

Of course by “bond wimps” I am referring to 90+% of the population that are likely to hope for a positive interest rate on their, frankly, savings.

The rest of them are part of the ” winners circle”. The golden stream emitted by the Fed’s largess in rescuing their arrant children, the criminal banks.

I have lost more sleep over Dimon’s all clear than I ever did about the warning of an impending financial hurricane. The all clear makes my blood run cold that the criminal banks have reached an agreement with their regulator, the Fed, a rescue plan that indemnifies them and covers their losses, like the last one only better.

The crazily low volatility index at low volume on the equity exchanges. Reminds me of the merchant’s block where the proprietor is offering an asset that is more likely to decline in value than increase, at a high price.

Powell on Bloomberg tomorrow noon time.

According to GasBuddy, gas prices at the pump during January are up from $3.20 to $3.50, or about 8%. Natural gas prices have doubled in January according to Southwest Gas in California. I’m looking for at least a .3 to .4% increase in CPI for January reported the middle of February. We’ll see what that does to the markets.

Thanks to Wolf Richter, I am making money.

Why is the 10 year so CHEAP??? 3.5% is way below yearly inflation/budget deficits for the next 10 years! The market still has plenty of juice to run!!!

“They looked at his slumped posture and heard his soft voice, and heard how he struggled to politely answer the same stupid leading questions over and over again, instead of just Tasering the reporters one after the other, or something.”

LOL gold. Hilarious and accurate. Just want to say thanks – I check this blog every morning and night. I always feel like I’m reading something valuable here that is almost always disconnected from a narrative or opinion and based on real facts. That’s rare in todays world. 👍

Wolf, what constitutes these mortgage rates? Is this some real time aggregate from banks, a federally set rate, or? Speaking as someone who has never been nor will ever likely be in the asset class.

Thank you in advance.

Mortgage News Daily has been collecting this data for many years. In their chart, they overlay their daily data with the weekly MBA and Freddie Mac data, so you can see how close they are. Obviously, the daily data is a lot more volatile.

from MND: “The MND Rate Index has become the industry standard for tracking day-to-day movement in mortgage rates. Unlike surveys, our index is driven by real-time changes in actual lender rate sheets. This means we can update it any time rates change during the day and that it will be much more accurate than survey-based indices. Lastly, it is highly objective as we are not quoting a rate nor attempting to influence any audience for any purpose. The one and only goal is to capture the real movement in mortgage rates as quickly and as accurately as possible.”

https://www.mortgagenewsdaily.com/mortgage-rates/about

Wolf, You de man!!!

Kinda sorta wish I were still in the market for mortgages based on this link, but mostly on your Wolfstreet.com Wonder!!!

Thanks again for ALL your very clear reporting; just wish every site/blog were anywhere near as clear…

I like it when rates are going up, that means I can put my funds into a “sleep easy” high yield savings account, knowing they are FDIC insured rather than getting slammed in equities’ bi-polar state. Many people have been conditioned to think over the past 15 years that ZIRP is the norm rather than a tool in extraordinary times. I suspect folks who are under 35 even under 40 are living in economic lalaland. Cost of money should not be zero as we’ve seen the destabilization this has caused, not to mention the endless stimuli flowing out of DC.

Excellent breaking out of 12 month Treasury, @ 4.922%

Five percent very soon and definitely headed higher. Watched a YouTube yesterday with two ex-fed desk traders and they see higher for longer. The women being interviewed thinks terminal Fed fund can go to seven or eight, and she believes the pivot crowd is going to be boiled like frogs. Her reasoning is related to Taylor Rule, but the mechanics of that aren’t totally supportive, as that’s often been a useless model of economic activity. Maybe this time is different? I think a bigger force will be deficit liquidity weirdness that impacts supply demand dynamics (during a liquidity freeze).

Amen

And finally,:

“It will be a couple of years” before reaching the right level of banking sector reserves, Powell said, adding selling bonds rather than allowing them to run off passively is “not something on the list of active things” officials are considering…

I guess that’s a greenlight for buying meme stocks (for some) but as money market rates stay elevated for a long time, the oxygen supply for speculation will decrease. The choice is to be patient making money from higher interest rates, or burn up money speculating.

Basically, if you have a house for sale, do not miss the last train, it’s leaving now.

Well, real estate fared pretty well all through the 70s…as well as 2000-2003, when the stock market obviously did not.

Ok, one final post for rate forecasting:

Goldman Sees 10-Year Treasury Yield of 4% or More Through 2024.

That was there story November 22.

I forecast that early 2024, the Ten will be around 4.5%

That value is derived from an old Ed yardeni post where a case was made, that the current 2 year Treasury is correlated to where the 10 year Treasury will be a year from now.

However, if that framework is somewhat reasonable, it provides confusion as to where the 3 month yield will go to a year from now.

This all gets into inversion and recession dynamics, but with inflation higher than we’ve had (for decades) and the pending deficit chaos, things might get stranger and weirder.

If you look at prior ranges for the ten year, getting around 4.5%, the 3 year is always higher, indicative of financial stress and liquidity problems.

As an example, December 1999, the Ten was 6.45% and Three near 5.82%.

If we take my buddy Jay at his word, about higher longer, with at least two more hikes going into summer, what will your favorite meme stock do, if inflation remains high and we get more hikes in the fall, with an epic recession?

Most likely, the final thought to smoke in your meme crack pipes:

“ By the end of 1999, the average rate on a 30-year fixed mortgage was 8.06%, more than two percentage points lower than at the beginning of the decade when rates were hovering around 9.83%”

Yes, we have different mortgage pool composition and various mechanical dynamics in 2023+, but if the yield curve heads higher, mortgage rates will go along for the ride, and more than likely the housing market will not be filled with easy liquidity.

It’s also highly likely that all the meme stocks will be footnotes at Wikipedia and I seriously doubt crypto will go to the moon.

Nostradamus