No dear, this is not seasonal.

By Wolf Richter for WOLF STREET.

Declines in house prices have turned into a relentless drumbeat. Today, the S&P CoreLogic Case-Shiller Home Price Index for “October” was released. Time frame: A three-month moving average of closed home sales that were entered into public records in August, September, and October; these are deals that were largely made in July through September.

Since then, home prices have dropped further nationwide, as we know from different median-price indices; for example, in the city of San Francisco, the median house price has now plunged by 27% from the peak in April.

The Case-Shiller Index here – it covers 20 metropolitan areas – is a more reliable indicator than the sometimes-crazy median-price indices that can be heavily skewed by a change in the mix of homes that are sold. But the Case-Shiller index lags months behind.

On a month-to-month basis, house prices dropped again in all 20 metros that are in the Case-Shiller Index. On a year-over-year basis, the price gains were further slashed, with the condo index for San Francisco now negative; and the house price index just about flat.

The biggest month-to-month drops in today’s “October” index occurred in:

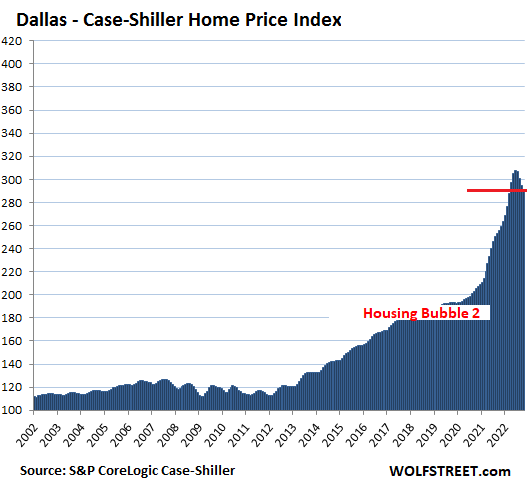

- Dallas: -2.1%

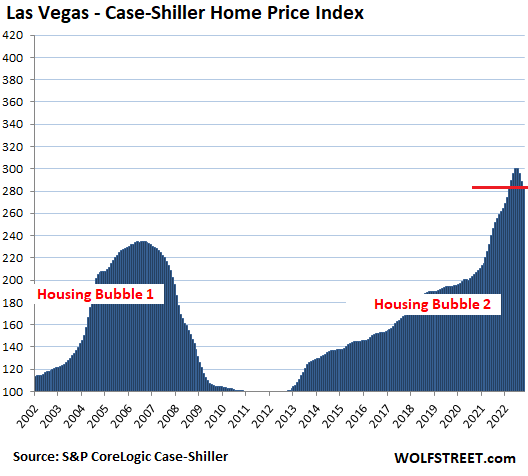

- Las Vegas: -1.8%

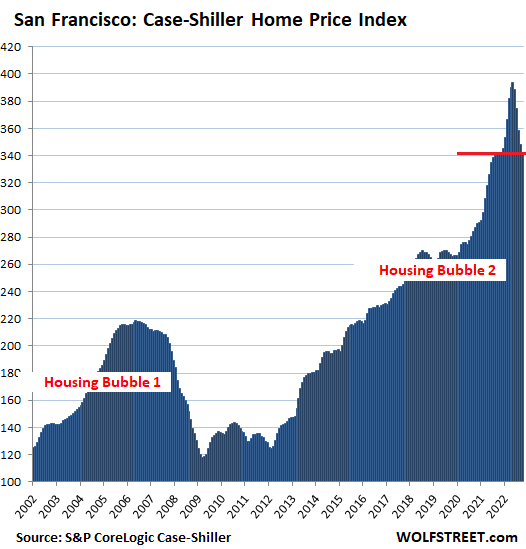

- San Francisco: -1.7%

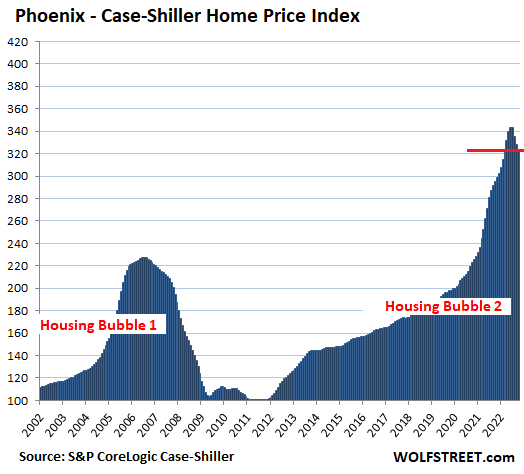

- Phoenix: -1.6%

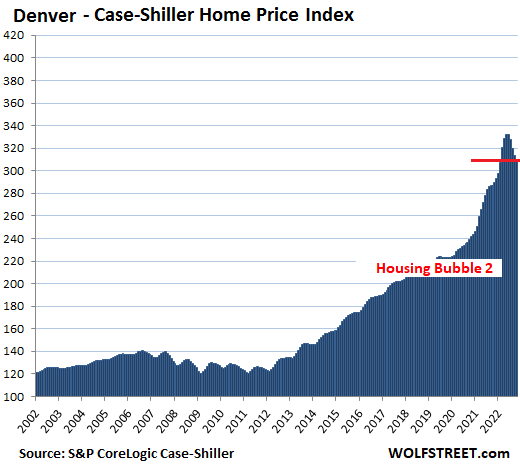

- Denver: -1.1%

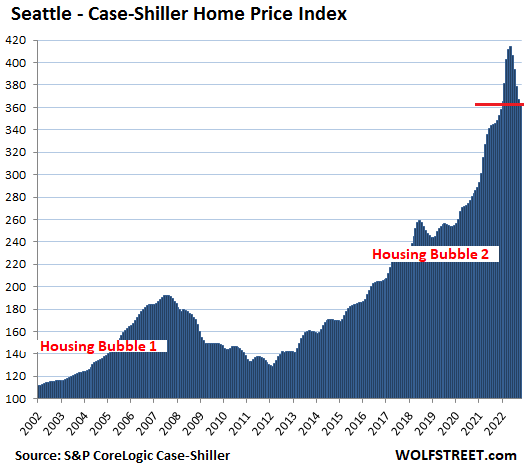

- Seattle: -1.0%

- Boston: -1.0%

- Miami: -1.0%

From their various peaks, which range from May to July, house prices dropped the most in:

- San Francisco Bay Area: -13.0%

- Seattle metro: -12.2%

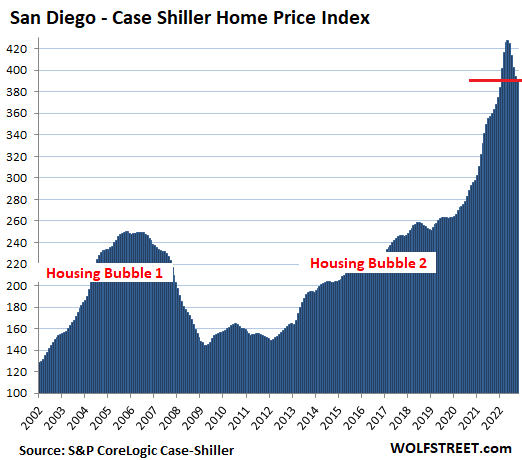

- San Diego metro: -8.5%

- Denver metro: -6.7%

- Los Angeles metro: -6.6%

- Phoenix metro: -5.9%

- Dallas metro: -5.6%

- Las Vegas metro: -5.2%.

In the San Francisco Bay Area, house prices dropped by 1.7% in “October” (three month moving average of sales that were entered into public records in August, September, and October), and are now down by 13.0% from the peak in May.

Plunging faster than it had spiked: Over those five months since the peak, the index plunged by 51.4 points. Over the five months to the peak, it had spiked by 48.6 points.

The five monthly drops from the peak have nearly wiped out the year-over-year gain (+0.6%). The Case-Shiller Index for San Francisco Bay Area condos is already down by 1.3% year-over-year.

The index for “San Francisco” covers five counties of the nine-county San Francisco Bay Area: San Francisco, part of Silicon Valley, part of the East Bay, and part of the North Bay.

In the Seattle metro, house prices dropped 1.0% in October from September, and are now down 12.2% from the peak in May.

Over those five months since the peak, the index plunged by 50.4 points. Over the five months to the peak, it had spiked by 55.9 points.

These five months of price drops slashed the year-over-year gain to 4.5%.

San Diego metro:

- Month over month: -0.7%.

- From the peak in May: -8.5%.

- Year over year: +7.5%.

- Down in five months from peak in May: -36.5 points

- Up in five months to peak in May: 53.4 points.

Denver metro:

- Month over month: -1.1%.

- From the peak in May: -6.7%.

- Year over year: +7.9%.

- Down in five months from peak in May: -22.2 points

- Up in five months to peak in May: +39.3 points.

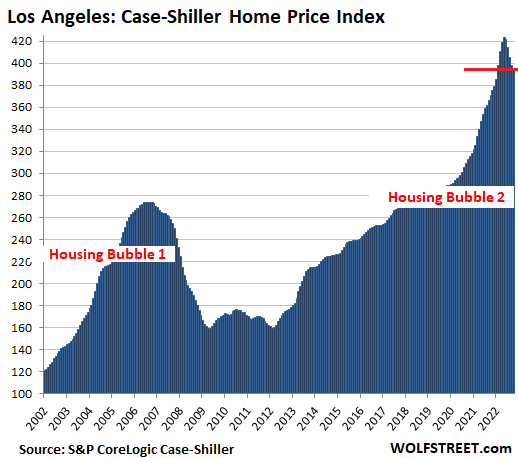

Los Angeles metro:

- Month over month: -0.6%.

- From the peak in May: -6.6%.

- Year over year: +6.6%.

- Down in five months from peak in May: -27.8 points

- Up in five months to peak in May: 44.3 points.

Changing leadership among the most splendid housing bubbles. For Los Angeles, the current index value of 395 means that home prices ballooned by 295% since January 2000, when the index was set at 100. Based on the increase since 2000, Los Angeles was the #1 Most Splendid Housing Bubble in America until February 2022, when it was bypassed by San Diego.

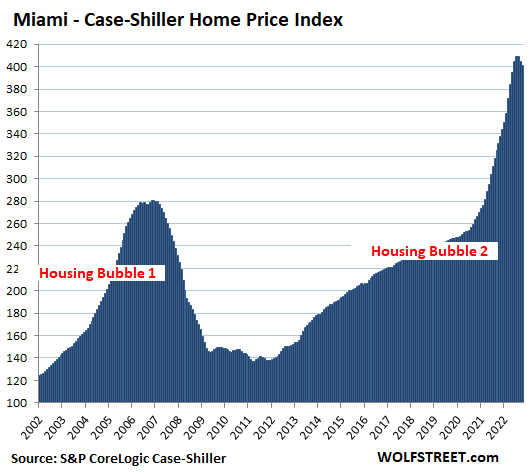

But both were bypassed by Miami in August 2022, as prices in Los Angeles and San Diego were plunging, while prices in Miami had just started to drop. So Miami has become the #1 Most Splendid Housing Bubble in America, with prices still up by 301% from January 2000. Now they’re all chasing each other down.

Methodology of the Case-Shiller Index: The index uses the “sales pairs” method, comparing sales in the current month to when the same houses sold previously. The price changes within each sales pair are integrated into the index for the metro, are weighted based on how long ago the prior sale occurred, and adjustments are made for home improvements and other factors (methodology).

Phoenix metro:

- Month over month: -1.6%.

- From the peak in June: -5.9%.

- Year over year: +9.6%

- Down in four months from peak in June: -20.4 points

- Up in four months to peak in June: +29.2 points.

Dallas metro:

- Month over month: -2.1%.

- From the peak in June: -5.6%.

- Year over year: +13.5%

- Down in four months from peak in June: -10.3 points

- Up in four months to peak in June: +36.3 points.

Las Vegas metro:

- Month over month: -1.8%.

- From the peak in July: -5.4%.

- Year over year: +9.4%

- Down in three months from peak in July: -16.3 points

- Up in three months to peak in July: +17.0 points.

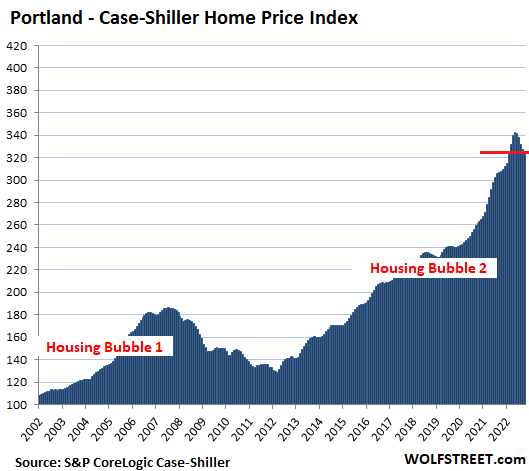

Portland metro:

- Month over month: -0.9%.

- From the peak in May: -5.2%.

- Year over year: +5.4%.

- Down in five months from peak in May: -17.7 points

- Up in five months to peak in May: +30.4 points.

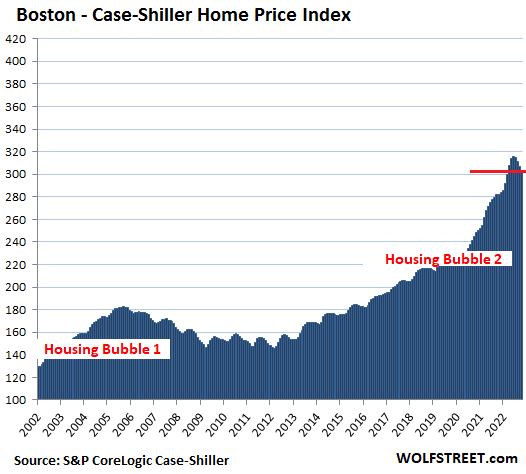

Boston metro:

- Month over month: -1.0%.

- From the peak in June: -4.0%.

- Year over year: +7.6%

- Down in four months from peak in June: -12.5 points

- Up in four months to peak in June: +24.2 points.

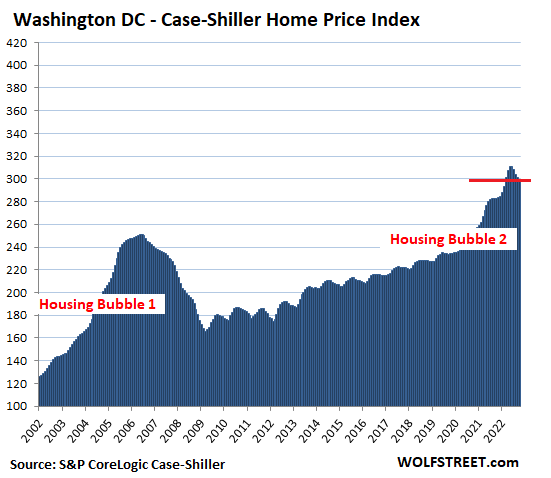

Washington D.C. metro:

- Month over month: -0.5%.

- From the peak in June: -3.6%.

- Year over year: +6.0%

- Down in four months from peak in June: -11.3 points

- Up in four months to peak in June: +17.5 points.

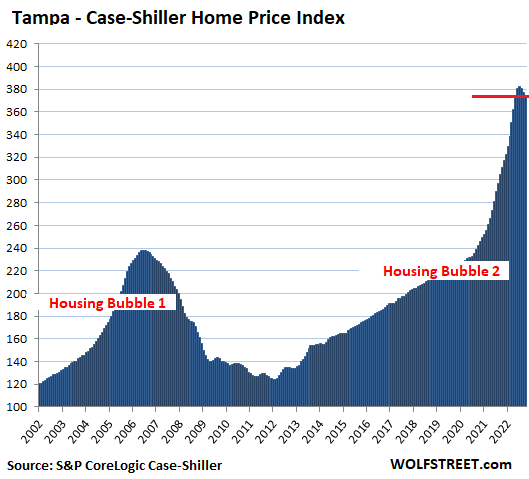

Tampa metro:

- Month over month: -0.8%.

- From peak in July: -2.1%

- Year over year: +20.5%

- Down in three months from peak in July: -8.0 points

- Up in three months to peak in July: +29.3 points.

Miami metro:

- Month over month: -1.0%.

- From peak in July: -2.1%

- Year over year: +21.0%

- Down in three months from peak in July: -8.6 points

- Up in three months to peak in July: +32.7 points.

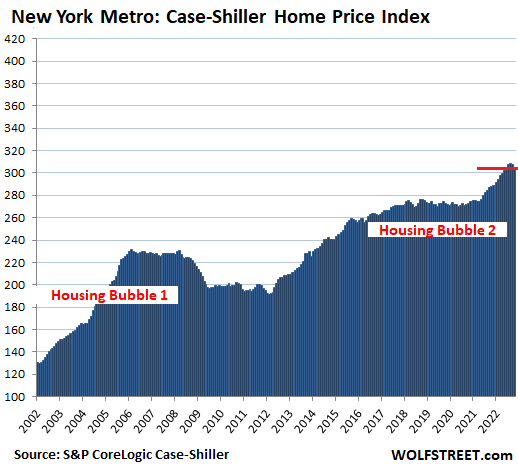

In the New York metro:

- Month over month: -0.2%.

- From peak in July: -1.5%

- Year over year: +9.3%

- Down in three months from peak in July: -4.1 points

- Up in three months to peak in July: +12.0 points.

In the New York metro, house price inflation since 2000 amounted to 172%, based on the Case-Shiller Index value of 273 today. This makes it the taillight of the Most Splendid Housing Bubbles.

In the remaining six cities in the 20-City Case-Shiller Index, house price inflation has been less, and they don’t qualify for this roster. But they also experienced month-to-month declines in the “October” index, following the declines September: Chicago (-0.5%), Charlotte (-0.9%), Minneapolis (-0.7%), Atlanta (-0.8), Detroit (-0.9%), and Cleveland (-1.0%).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

California led us up and is leading us down it seems

Exactly

Zillows quote from Aug 2022: “Not only does Zillow disagree with the “home price correction” narrative, the Seattle-based home listing site thinks the pandemic housing boom has some gas left in the tank.”

Seattle Zestimates for homes actually increased!

Seattle Homeowners that couldn’t sell their listed homes at peak may have a case against Zillow for bad Zestimates.

Funny how Zillow has removed the price history for all of the homes on its site. Things that make you go hmmm…

The Chinese won’t buy into a falling market. New home prices will take the biggest decline as the Chinese always buy new over resale when they’re in the market as buyers.

I keep seeing this “they can sue Zillow” meme and it’s time to slay it: They have no case against Zillow, the fine print on Zillow’s website makes it abundantly clear that Zestimates are not reliable for pricing your own home for sale.

Let’s not feed the mindset that someone else is there to solve your problems for you – the only person who actually knows what your home might sell for is a buyer.

I am thinking we have hit the high in housing and stocks for at least 10 years if Fed is done with easy money.

I’d be curious to see these charts extended to the 80s the last time the fed interest rates were higher than they are now. Also to see effect on inflation and what we can expect prices to fall back to. We all know it’s a giant bubble now. Interesting that denver and Dallas didn’t have bubbles but do now. I don’t think the crash will be like the 08/09 financial crisis and Fannie mae. My guesstimate will be a revert back to 2016/2017 pricing. 30 percent off the current bubble highs. Inflation and cost of materials is still real but in my current DFW area along with denver the prices people are asking for some mediocre homes is still 50 percent high.

so if I have house listed at $500,000 but it’s really ‘worth’ $400,000

and listing price drops 5.9%(Phoenix) to $470,000

should I just be laughing or ROFL

Reality takes time to set in. The “Matrix” has you. What will you choose : The red pill or the blue pill.

I take Tylenol. It’s red AND blue. 😜

The Fed led us up and now down

Gotta love Tampa & Miami, baby! Up 32.7% & 21% YoY, respectively.

Nice job, DeSantis! Can’t wait to see you in the WH!

I like DeSantis, but this was stupid.

I like DeSantis too but there are many other factors in housing prices besides the governor. I don’t think huge increases like this are healthy. It causes suffering for many people.

Higher housing prices are not a good thing. Nor is DeSantis’ attempts to stop Gainesville from taking steps to reduce them by restoring private property rights by ending single-family zoning.

Barring 1930-tier collapse, DeSantis is not going to be president.

I think many foreign investors will liquidate as their needs for capital grow: the cost of capital will only go up for years due to the retirement of the baby boomers. The CCP real estate bubble will also be impossible to reinflate much: Chinese people will not pay 20 or 30 times or more their actual annual earnings for shoddy real estate, whose value may plunge dramatically at any time.

Hence, aside from increases due to inflation, we have reached peak real estate values in real dollar terms.

It’s not just a shortage of capital, but I suspect the future will see more competition for it. Good governance and markets are spreading in places like Uzbekistan and Togo. The world is getting bigger not smaller and I hope more competitive.

the amount of decrease is so small that it is almost meaningless so far. things wont get interesting until end of next year, as stress builds on people who have purchased homes at prices above what the market will pay.

we really need some regulation of private equity money purchasing real estate to rent out. the financialization of every facet of life is the root cause of many of our problems. unfortunately, people are too stupid to do what is smart, so we need to legislate away the greed.

The problem you describe wasn’t a problem or anywhere near as big of problem until the FRB’s deranged monetary policy starting after 9/11 when the Greenspan Fed cut the FFR to 1% which greatly contributed to HB1 later followed by QE and ZIRP as a response to the GFC. Get rid of that (mostly by gutting the balance sheet) and most if not all of it would go away.

Otherwise, your solution is just another attempt to regulate moral hazard.

I’m not sure how much fiscal policy is a factor, by subsidizing renters.

Then there is also immigration policy. To my knowledge, it’s generally a lot more of a factor in the rental market but then, no one has to own the roof over their head where they live. (I’m renting now due to family circumstances.)

When the UNE rate starts creeping up, defaults and bankruptcies increase.

All bills become hard to pay. People can stay in their home after home prices start accelerating downwards, as long as they are making the same wages as when the mortgage was acquired.

It would help if 28% of income was used for the house mortgage approval, with 20% down, and a low fixed rate. Unless recent home buyers have a lot of savings, things could get rough for many home buyers on the high end of the risk scale. Secondary variable rate HELOCs will accentuate the problem of higher UNE. And we can’t forget the extra bite that inflation takes from income.

With the right stats, and historical data re what happened with defaults and bankruptcies during inflationary periods when the UNE accelerated higher would be nice to see what will probably happen.

Presently low UNE is the brake for market capitulation downwards, along with the liquidity still sloshing around from low rates and free money. It could take a while. Hope for the best , but plan for the worst.

As long as the Federal Reserve exists in its current form it will continue to funnel ultra low interest rate loans to its owners’ banks and again create bubbles as it did in real estate, and stocks to a lesser degree, in 2000 to 2007 and again in 2008 to 2022 and of course, more inflation to profit its bankster owners by shrinking their debts. We should impose a huge annual tax on it to be paid in ownership of its district banks and so nationalize it in a few years, so it truly is an independent, publicly controlled, government agency.

Secret wealth that it has enabled the ultra rich to accumulate for decades now prevents any reform. See Simon Johnson’s “The Quiet Coup.”

All told, on a “per capita” basis – immigrants provide less strain on housing. Two reasons.

Reason #1: Immigrants tend to form family households

e.g. A four person family in a 2 BR apartment is generally less strain on housing than 4 singletons who each live in a 1 BR apartment.

Reason #2: Immigrants are willing to live in denser housing arrangements

e.g. two unrelated immigrants in a 1 BR apartment

The last one is somewhat informal – but there is lots of anecdotal evidence in the Eastern USA (at least!) to support it

Reason #3: Recent immigrants often work in home construction – thus alleviating labor supply pinches.

So, yes, immigration does increase demand for housing, but not as much as other sources and can somewhat help with increased supply.

I agree without of what you said but landlord having 6 or 8 people in an apartment is much less desirable than one person.

Less wear and tear, less noise, fewer parked cars, fewer parties, etc.

If you increase occupant density, you’ll increase strain by your definition. A per capita measure (an odd metric) implies immigrants suffer more strain under their living situations, not that they somehow live better in close quarters. Nobody wants that.

“things wont get interesting until end of next year”

Tough crowd. I’d say it’s pretty interesting right now. We’re getting a peak denial-to-reality ratio!

“I’d say it’s pretty interesting right now. We’re getting a peak denial-to-reality ratio!”

Yes, in my home city of Toronto the rationalization currently is that builders will simply strangle new supply, construction will slow way down while the federal government increases immigration putting demand pressure on the market. This they say should result in mild drops and stagnation in the market for a while until inflation is sorted and then back to the moon.

Nobody wants to listen to me when I point out that at current interest, and potentially higher interest, a large chunk of potential buyers can’t even qualify, they barely could at rock bottom interest and many still needed to “cook the books” to get there with the high prices. On top of that, unlike our American neighbours, we haven’t seen the kind of wage increases while inflation spikes denting buyers capacity to save. BOC interest rates can’t differ significantly from US and by the looks of it more hikes should be coming. People there just want to believe Chinese investors run the market, even when data suggests most RE investors are domestic and they’re on the sidelines right now.

Anyway, it is definately interesting right now, I think TO RE market is in for a rude awakening. I kinda needed to write this out as a sort of self therapy in order to keep my sanity amongst the hordes of manic RE believers I deal with in real life.

I couldn’t agree more. Canadian denial of reality in realty (if you’ll pardon the pun) is akin to the denial manifested in the equity markets, not only in North America, but internationally.

Don’t worry. Everyone is in denial when it comes to their own home town. Just look at all the Californians who think they’re special because they’re close to the ocean.

It’s human nature. When people are facing potential devastation of the largest financial asset they own, it’s normal to go into denial and paralysis mode and hope for the best.

The Chinese don’t just run the market they are the real estate market in Canada as prices in Ontario and British Columbia have pushed prices upwards right across the country due to the Chinese pricing virtually everyone out of the housing market in Ontario and British Columbia. The foreign Chinese have have the biggest influence in British Columbia and the local Chinese have the biggest influence in Ontario. It takes a mere handful of Chinese buyers to drive prices into the stratosphere. The Canadian housing market someday will just mirror the housing market in China with home prices to income rising to factors of 80 to 90 to 1. When the Chinese come back as buyers in Canada home prices will rise double digits in one single month.

@The Real Tony: everything you said is complete nonsense. Pure Yellow Peril gibberish. The Chinese are a scapegoat nothing more.

My wife and I sold our house in April 2022 for 780K. 2400 Square Foot Bungalow built in 1977. Good shape but original kitchen cabinets and an older basement bathroom. The town was Port Alberni on Vancouver Island a pulp and sawmill town. Moved to Nelson BC more of a ski and outdoor recreation town with lots of Government jobs. Our old house would have probably been 850k here. Checked listings in both places last week. Prices are sky high still but NOTHING has sold. One of the top realtors is in Mexico right now because business is so slow.

my favorite denial is “maybe in your area, but not in my area”

Kind of like, I disapprove of Congress… EXCEPT my congressman (Congress approval rate now at about 22%, yet almost 98% of incumbents in Congress were re-elected)

RoDave – quintuple-check. Shake my head constantly over angst generated among many from national media coverage of say, AOC or MTG, but when I ask when they plan to move to that district to vote the rascal out (or keep them in) the looks and responses are often beyond blank (too-often the same when asked: “…BTW, who IS your representative?”).

As long as I’m astride the soapbox, the above demonstrates the weakness of wanting to impose Congressional term limits – an election IS the limiter, every two or six years, depending on the office. As you so succinctly put, Dave, scratch the surface and find someone wanting to limit those in other districts, rather than do the constant, miserable, unpaid, but necessary work of the citizen in overseeing one’s own reps in the sausage factory…

may we all find a better day.

Case-Schiller is measuring median values and not average values. Average values in the Miami MSA for example are down by about 15% from the April ’22 peak to November ’22 on an annualized basis per the MLS. Median prices have not declined anywhere close to that due to higher end buyers still paying cash for homes whereas buyers depending on financing on the lower end homes have been greatly impacted.

“The Case-Shiller Index here – it covers 20 metropolitan areas – is a more reliable indicator than the sometimes-crazy median-price indices that can be heavily skewed by a change in the mix of homes that are sold. But the Case-Shiller index lags months behind.”

Joey B,

Case-Shiller measures neither median nor average values. It compares prices of the same house when it sold previously and adjusts for the time period. This is the “sales pairs method” as explained in the article (I linked the Case-Shiller methodology in the article). Which is why it’s a much more reliable indicator. But it’s also a three-month moving average and is about 4+ months behind the reality on the ground.

Reality on the ground: For example, as pointed out in the article, San Francisco’s median price is down 27% from peak in April, but the Case-Shiller index is down “only” 13% from the peak, which is 4+ months behind. But I consider this 27% an unreliable number because the mix of homes that sold may have shifted, with more low-end homes selling, than high-end homes, which would skew the median price lower.

qt: thanks!

“more low-end homes selling”

Wolf, that is what I am seeing here in 98053 Redmond WA. Smaller cheaper houses seem to be popping up for sale everywhere. Fewer big houses are for sale/sold. The really interesting thing is to look at is the cost per square foot, which has not dropped much at all. Still about $500 a square foot.

Redmond being a big tech area might see some real price drops if the tech layoffs start to have an effect.

Easy to do but you will offend people when you challenge their tightly held long term beliefs.

Or we could just start by making sure their income is taxed the same way as anybody else’s income. Imagine of all income was treated the same with every last dollar subject to the same income tax and FICA taxes. I’d settle for that to just stop with actual labor being taxable at a higher rate than paper gains.

There is no way the social security component of FICA taxes should be applied to non-wage income. SS is supposed to be a type of pension, not a welfare program. It’s already enough of a welfare program due to the current structure.

The Medicare component is somewhat different.

Social Security is a welfare program, but I don’t think you mean it the way that the word is defined. It is structured as a defined benefit. But yes, it should apply to non-wage income. Some twit that inherits millions and invests it to make a living should pay into SS.

And the formula can still be refined so that every dollar paid in still generates an increasing retirement return that does not go to infinity, by the simple mathematical method of a function with a limit.

Speaking of limits, why is is that people with too much money have to sound so sourpussed about playing the same game as the rest of us? I’m getting awfully sick of the whining. Why not just enjoy it???

Real simple.

Take the federal minimum wage. Multiply by 2,000. That income number is the baseline for every citizen in the USA. There is no federal tax liability for anyone up to the baseline.

Now above that baseline, every dollar of income of any type sees a flat tax rate of 20%. Wages, interest carried, short term capital gains and long term capital gains are all taxed at the same flat rate.

Say the minimum wage is set at $15 per hour; $30,000 is the baseline. If you make a total of $50,000, your IRS bill is 20% times $20k = $4k. If your total income is $1 million, your IRS bill is 20% times $970k = $194k.

Real simple. Tax labor and capital gains equally. But above a living wage baseline, tax all income equally regardless of what the number is.

Ceteris Paribus

For property taxes in 2023, where I live in the Twin Cities, St. Paul will see a $14.65% increase & Minneapolis will see a 6.5% increase. That’s going to hurt on the east side of the Mississippi river.

A home near me in Minneapolis just sold for $455k. Its 2023 property taxes are $7k.

*Real simple*

Guy goes to a bank for a loan.

Banker asks “How much do you need?”

Guy answers “$50,000. And I tell you right now, I am not willing to pay a dime over 20% interest!”

Banker “Yeah, OK. I think we can do that…”

“Real simple. Tax labor and capital gains equally.”

OK, so long as cap gains are indexed for inflation. It is hardly fair to earn a negative real return and have to pay tax on a nominal gain. That’s why cap gains rates are lower than ordinary rates. It’s a crude solution to account for inflation that way, but that was the deal in the ’80s when inflation indexing was canned.

That’s still cheaper than Cook County, IL.

I gotta get out of this place.

Very good point Gattopardo.

Since I’m retired, I have no wage income anymore. My tax rate is lower than it would be if my income was from a salary paying job.

But in 2022 at the high end, 37% gets taken for wages versus 20% for long term capital gains.

PR,

It’s hard (aka impossible) to nail perfect equity in a tax code.

Can’t tell you how many friends have drooled over killer sounding nominal returns on stuff like classic cars or long-held homes, only for me to then poop on their parade by showing them that the IRR over those 30 years was actually a lot smaller than they think, and then negative when factoring in inflation. And then even MORE negative after paying even the “low” cap gains tax rate.

I think the truly egregious error in the code is allowing carried interest at cap gains rates (NOW we’re talking about a much more fair comparison between labor and capital) and lawyer structured settlements…

The home near me that sold, was not for $455k, but for $575k as I see a recent listing of sales in my neighborhood. It was built eight years ago, and clocked in at $301 per square foot. That makes more sense on property tax rate too, which is $7k. Just to be accurate …

Once the US dollar was gold backed. Today the US dollar is in part real estate backed as the counterpart for a lot of issued money, debt, is mortgages.

If real estate valye crashes, then, when it is realised that the value of the backing have crashed it may get interesting.

Once I saw that Congress was going to keep making excuses to keep spending, I am thinking Asset prices are going to get hammered.

All Powell has is the interest rate card and liquidity tools and if he has to keep going beyond 6% he is going to squash housing and stocks like a bug.

You can’t go from 3% mortgage to 8% in a couple of years without imploding housing. Same with stocks. You can’t pay 6% on t-bills in a low growth environment and expect PE ratio to be much more than 10.

Very accurate comment.

I would like to add that you can always talk about hammering capital gains with taxes until you realize that capital gains are the results of good investing [not $hit like crypto of NFT].

You over tax good investing and people are going to quit doing it. You can overtaxed productive people and capital until it goes under table, out of the country, or just retires. Then were is your tax base?

One last point for all you posters who want huge tax rates. Shouldn’t those tax rates be based on how much money the government really NEEDS rather than on how much you earn? What happens to the difference between what the government needs vs how much it collects? It gets stolen. Are the tax rates supposed to be for punishment or for the long term good of society?

I am talking about income taxes here. I believe massive inheritance taxes are fine, because clearly benifit society.

#Enlightened Libertarian:

If you look, there is a near perfect correlation between inflation, that is expansion of the amount of money, and captial gains in real estate and stocks.

Now, how much is then captial gains results of good investing?

Now, with a little bit QT, there is no inflation, rater stable amount of money or a tiny bit deflation on M1, M2 and M3 measurements of money. And the real estate and stocks turn down. Result of poor investing?

Or is the free ride up that have turned (to a roller coaster down)?

About taxing, add a transfer tax. If the government did take a % cut of every transaction, no other tax would bee needed.

“the amount of decrease is so small that it is almost meaningless so far. things wont get interesting until end of next year”

1. CSI release figures are substantially lagging;

2. % decreases take on significantly more meaning in high-cost areas;

3. Thin transaction #’s partially obscure downturn severity;

4. Things are interesting as eff right now and will get more so in ’23-’25.

Cases in point in very nice San Diego northern subdivisions I know well:

2700 sq. ft peak sale – $2.12 mil

Recent model match sale 3 doors down – $1.54 mil

That’s minus $580K. That’s not meaningless.

4000 sq. ft. peak sale – $2.64 mil

Recent model match sale – $1.9 mil

That’s minus $740K. That’s not meaningless.

And this is going to get much, much worse.

Falcon, I’m skeptical of this (no offense). Have addresses you can point to?

2243 Paseo Saucedal, Carlsbad, CA 92009

2255 Paseo Saucedal, Carlsbad, CA 92009

2894 Corte Morera, Carlsbad, CA 92009

2901 Segovia Way, Carlsbad, CA 92009

I’m getting similar numbers here in Palm Springs. And yes, low transaction numbers hide the trend. Sellers are still in total denial.

Inventory in San Diego is next to nothing which makes this very interesting. There are only 20 active house listings in all of 92115. The entire state has been rezoned to duplex but the city of San Diego took it much further by defacto rezoning every single family parcel to allow multiple units. It’s pretty much common knowledge here that as many as 5 or 6 units is very feasible. The building department fast tracks these with rubber stamp approvals. The county didn’t go this far, just the city. This is affecting property values here and will continue to do so.

Meh i know both those houses well. Part of the difference is explained by the first being much nicer and remodeled. The rest by irrational 2022 Spring exuberance with low rates and inventory. That sale over 2.1 was a joke and we all laughed at. There was one other high sale but after that no one has paid with in 500k of that. So now we are back to where we started last year having given back the insanity quickly. Nothing more is given at this point though i expect maybe another 10% give back this year before we settle back in. If you are counting on a much bigger decline you’ll be sadly disappointed

LOL of course these peak prices were driven by FOMO/low interest rates/low inventory/irrational exuberance. That’s the point.

Prices were already frothy in 2019 and then really took off late summer ’20. I think there will certainly be greater declines over the next several years. Let’s meet back here in 24 months and see what closing prices look like then.

I can also confirm this is happening somewhat in the south OC. I don’t have exact comps but 2 homes down the block sold for 1.6M in April (one 2400sf 4+3, one 1800sf 4+3).

There is now another home for sale that is 2900sf 6+3 listed at 1.3M. It’s been on the market for a month, no sale. Even if they sell for listing price, it’s a huge drop.

The problem is that the 1.6M sales were RIDICULOUS, and the new home listing at 1.3M is still sky high compared to wages in the area.

People locked in at mortgages under 3% will sit tight.

Sure, they will sit tight —- unless they experience one of the many life events that compels a sale. Examples include:

1. Job loss

2. Relocation

3. Divorce

4. Retirement downsizing

5. Death

6. And so on

This time the pain wont be for the banks, but for the people sitting tight. They will see their equity go smoke, hah ;)

About 40% of homes have no mortgage, ergo no low interest rate to preserve. Of the remaining 60% of homes, 3 out of 4 did not re-fi to catch the sub 3% rate.

So using your parameters, a massive majority of the market will not sit tight to preserve a sub 3% rate. In addition, there are those with a sub 3% rate who will certainly sell for some reason over the next few years, forced or not.

It has been a couple years since I checked, but the latest stats I am aware are of say that there are about 75 million single family homes and about 25 million of those don’t have a mortgage.

(One troubling aspect of these stats…when I look up the number of total apartments, the number falls noticeably short of a total (when added to SFH totals) sufficient to equal the reported number of households in the US (about 130 million). I’ve not be able to reconcile the discrepancy through casual Googling. Maybe Wolf would have more luck. For me, having good, macro, aggregated baseline supply stats – that reconcile – is an absolutely key starting point).

CAS127 – does that include trailer parks, RVs, vans down by the river, and unpermitted dwellings?

Apple, consider that hundreds of thousands (millions?) of California homes have property taxes based on values DEEPLY below current levels, from Prop 13. And yet….they trade hands routinely. Meaning people are voluntarily leaving their sweet tax deal for a full mark-to-market. And unlike the way you can re-fi your mortgage way back down if/when rates drop, there’s no such optionality with prop taxes.

Summary: I think the whole “I will sit tight” thing is overblown. Sure, some will. Not enough to do anything to skew the market. Otherwise CA would have had the same with no one giving up their tax base. Yet for every one of these kooky-priced sales we’ve seen over the last couple years, that seller gave up a much lower tax base….

Uhhhhh the whole I’ll sit tight because of prop 13 is exactly why prices are so high too a large extent. It greatly reduces inventory. To ignore that is silly

Yep,

The can sit tight, although the value will still decline

Those 1.7% MoM decreases will really start to add up by mid 2023, but I totally agree with your point about investor led purchases of homes to rent. There has to be a cap.

Well said. Legislate the greed away!

Meaningless? What’s 1% per month annualized? A 12% annual price drop is significant —- that’s $60K on a purchase price of $500K —- and most aren’t even putting that much down. And this is only 20 metros??? I think this is also quite meaningful given that this is lagging data.

“….we really need some regulation of private equity money purchasing real estate to rent out. the financialization of every facet of life is the root cause

of many of our problems.”

Gee you mean the end to the vulture capitalism , funded by the Fed to enrich the banking cartel and all their uber-rich friends ?

Sounds un-American to me ha

I firmly believe we should have mortgages that reset every 5 years. This nonsense where real estate investors are able to refinance huge portfolios at ludicrously low rates for 30 years is leading to increased concentration of wealth.

Properties that have no right cash flowing are making these people boatloads if money. It’s grossly unfair and should come back to bite them like in the uk and Canada. Would drop speculative investing a bit

ATL where I now live didn’t participate in HB1 but it’s in a bubble. Without cheap financing, housing is nowhere near affordable here to most prospective buyers, unless they already have bubble equity.

A long way down to go for all these markets.

Interesting.

Dallas and Denver didn’t participate in Housing Bubble I either. They have joined the crowd for Housing Bubble II.

ATL didn’t participate in HB1? Is that based on certain metrics? I remember the massive rebuild up of neighborhoods in the metro area that stood empty after the bust and were eventually turned into rental communities that accepted section 8. I know people who bought homes in those neighborhoods for 300k then had their gated community turn into the ghetto. I’d be interested to know how those two processes comport.

Atlanta doesn’t qualify as “bubble” under the definition here: large % increase from 2000. But it did increase during HB1 and then it plunged then it recovered.

This is a chart from 2017, my earliest episode of this series. I later dropped Atlanta because in terms of the increase since 2000, it just didn’t measure up and still doesn’t measure up:

Prices of ATL housing HB1 never really inflated even though many sections of the metro still crashed. Combination of job losses and an outsized proportion of financially marginal buyers.

To give you an example, I had to get my mother out of her neighborhood near the peak of HB1 and to do it, buy a house with her because she couldn’t qualify on her own.

She bought a townhome in March 2000 for $114K and sold in January 2006 for something like $105K. (Yes, you read that correctly. It lost value, even during a national bubble.)

We closed on the house in April 2006 right at the peak for $138K. I sold it in May 2017 when she had to move out for $144K.

More recently, houses in this sub-division were selling for around $330K, earlier this year but don’t know about it.

I’m confident this type of neighborhood is going to crash, again. Same thing for “revitalized” or “gentrified” neighborhoods in the city center which actually “suck” but which have increased even more.

QE = 2nd Housing Bubble

Rate Hikes = “popping” of 2nd Housing Bubble

I’m going to go on record that we will see rates at 575 bps and then a pause. How long of a pause? Until the bubble pops.

Bye Bye to equities, though. Collateral damage.

The question is “why?” WHY was the FED blowing this massive housing bubble in the first place? They had all the data, all the knowledge, all the power – everything they needed to keep pricing in check, yet they chose to blow the most insane speculative bubble known to mankind. As certain locations saw house price increases of up to and beyond 40% per year, the FED continued to maniacally buy MBS. WHY?

We need this question answered. Houses are shelter, and they stole shelter from the working class and the poor, and handed it to the wealthy with their deranged policies. We need answers. We need investigations. We need much more than rate hikes. We need accountability. We need heads to roll.

You are asking for a level of accountability which does not exist in this country.

Behind every Too-Big-to-Fail is a Too-Big-to-Account.

Why the FED maintained QE for MBS for so long in the face of Housing Bubble 2.0 baffles me.

Because corrupt congress spent money to reward contributors and buy votes the Fed was forced to maintain low rates to create false growth and keep government debt from collapsing. Of course, they should have told corrupt congress to stop – but they are all of part of the slime running this corrupt country. The people will pay for the collapse – not the corrupt bureaucrats who caused it.

MBS first bought up and now rolling off must steepen this at both ends, right? MBS’s are now dumping into a market with rising rates and falling prices? Who will buy them now. Meaning, who will lend into that pipeline? Could be a big accelerator on the downside.

Because money printing was the only quick answer to stave off a collapse of the fake financial economy. The banks were vulnerable and the powers in charge did not want to lose their fortunes. Japan 2.0

Simple it will never be repaid,DEFAULT

Like dad telling the family, “we can’t be out of money, I still have blank checks to write.” Next thing you know, they’re burning the furniture.

Looking at the the charts it seemed like they finally were figuring it out pre pandemic and reducing balance sheet, then COVID hit and things really got fun and they increased their BS in a year like 4x from what was already too high for too long

It could be simply selfish greed. Cashing in before the shatner hits the fan. They wanted to take care of themselves and their wealthy friends.

They believe they are better than the lower classes and deserve it.

Shades of a cherished lingering monarchy of rulers that feel thy are entitled.

Implicit, this certainly squares with my conviction that central banks are, by design, aristocratic institutions inimical to labour.

Exactly! This is something I’ve been wondering about for a long time. Why did the Fed allow this to get so out of hand? How could they have not known what they were doing? Why? I wish I knew or someone could explain it. Something isn’t right. If any commenters have an idea, please share it.

I would have said, maybe the Fed had cognitive overwhelm from the pandemic. But then I recall, this was well after the pandemic peaked, and the Fed was still saying, we are going to let inflation run above target. I assume they wanted to feel sure the economy had some momentum, that it was juiced up and running hot. But that was after years of juicing up, and the landscape was already full of zombies, topped up with extra handouts, and now we see them falling like rotten trees.

It is startling that price stability didn’t break before then, but like a bad addiction, it can run seemingly functionally for a long time before it topples.

Certain things numb a person to risk. One is lots of funny money. Turns out it numbs the issuer too, apparently. Euphoria (not least, easy money, the illusion of something for nothing) is a daydream that enfeebles.

It’s like the Fed sold our souls to make it unscathed through the GFC and worst pandemic in 100 years.

The price must be paid at some point.

Was it worth it? So far, yes. The saga isn’t over yet, so there will be more pain.

The answer is simple: corruption, fraud, and greed. But, it is extremely difficult to accept as the sign says “Federal Reserve Bank”.

Reading your replies here, you know the answer. But, not being a psychopath, you still can’t accept it.

Yep they stole it and continue to do so. Heads are not going to roll, any investigation will be rubber stamped, and no one will be held accountable.

Time to internalize this, let go of any hope “they” will change, and radically alter your position accordingly. It’s difficult, but not impossible, and it provides a great deal more peace.

The fed are appointees and virtually the entirety of the business sector wants housing prices to rise as they make money directly off of it or indirectly via the wealth effect. Every greedy sleazeball thinks about buying that boat from the profits and not the young family priced out by this insanity – unless it’s one of their kids in that family.

As you can see from the charts, the prices are not down much, however that might be because of “frozen markets,” ie. few transactions and homes are not receiving bids, or accepted bids.

will prices go down to 2011/2012/2013 levels?

I know of countless houses that were either “taken off the market until spring” or that sit without price cuts at peak pricing levels. People are simply waiting for the halcyon days to return, riding the market down.

The halcyon days will not return because ZIRP will not return.

Don’t bed on it. Things get bad enough there will be negative rates and QE up the whazoo.

If the 39YR interest rate cycle turned in 2020, there will be no ZIRP. Any attempt to do that will crash the currency.

There is nothing any government nor central bank can do to prevent falling living standards without cheap and loose lending, as neither produce any wealth. “Printing to infinity” doesn’t change the outcome.

#Augustus Frost:

The 39 year interest rate cycle might be a rather moth yardstick.

The fundamentals of the monetary system was completely reorganised about fifty years ago when the gold standard was left.

In later years, the switch form the banks holding the mortgages to sell them of as MBS was another major change to the monetary system.

The only bit history I would put any weight when it comes to money is that all prior fiat money systems are just history. Usually at less time than the one we have today.

not happening at-least until another year or so in markets like Dallas..unless there is severe recession. I’ve been waiting on the sideliness and I spoke to my neighbor yesterday who literally signed up for 850K house with 10% downpayment @6%..I don’t know what to say..people are just out of thier minds..That new build is absolute crap and shouldn’t cost more than 350K in my opinion. As long as such people exist and fuel the fire..things won’t change much.

To add to my previous comment, the reason he gave…his rent got bumped up to 3K and he didn’t want to put up with those increases anymore…perhaps people are between a rock and hard place???

I don’t know..I’m afraid I might be forced into such a corner come next year end.

Not where they buy an $850K house. Sounds more like a rationalization.

That’s a $4500 in P&I plus maybe another $1500 for everything else, per month.

Yikes. Add in TX property Taxes, and it’s tit meet wringer. Your neighbor seems rather innumerate. Plus…no offense, but it’s Dallas.

Knew a lot of his type from HB1…same guys who were telling me, “your house can be your job!”

I love this stupid country.

It seems to me that the layoffs will be a major factor in the next year or so. People still have savings and and a cushion from their home equity to offset the recent layoffs. I remember that after the last housing bust Bernanke was dropping rates furiously, but home prices continued to go south due to layoffs and fears of being laid off. Once the savings ran out jingle mails started, and those who had money waited to buy since the FOMO effect was reversed.

Lower mortgages may not save housing this time around. All that the Fed has done is pull demand forward for several years and nothing can change that.

The only thing that is holding up the stock and housing markets is the faith in Fed pivot. If the Fed does indeed hold the line and not pivot the whole house of cards will come down.

Unemployment is still very low at 3.7%.

Thumb in the dam, it is.

Garbage in, Garbage out.

My belief is that if the prime rate hits 8% the price of houses will drop below the top of housing bubble 1’s highs. And I believe that it’s entirely possible the prime rate will 8% sometime in 2023.

The USA will not start to pull out of this mess before before the ECB rates get within 1-2% of the average inflation rate for the EU, and they are always a year behind the Fed, so 2023 is going to be hard. And if China can’t contain their economic mess it will get worse.

People keep telling me it’s not like the 70’s, and I have to agree; back then Congress actually tried to restrict spending. That’s not happening this time around.

There was no free lunch in the guise of free money in the 1970’s, and the inflation seems an awful lot worse in the past year than I remember it being some 50’ish years ago.

Been seeing a lot more of those Redfin email blast with listing back on the market. Think there’s still a lot of funny business out there, marked sold and then over asking, probably a way to sucker in last of the FOMO sheeps.

Wonder how many of these redfin/zillow listing marked as sold is actually sold..I know a lot of contingent falls through the cracks then get relist later.

It seems that a lot of appraisals are coming in lower than the listing. Danielle DiMartino Booth made some comments on this a few weeks ago. A lot of sellers get a panic attack when this happens.

Not to worry. The FHFA raised the conforming loan limit to $1 million to assure a continued bubble in home prices.

You still need a job to quality.

10% of buyers can be the price setters for an entire market. Rich people always come out of the woodwork to buy another house, even if 30% of the population can’t even quailfy. Blame the Fed.

It doesn’t even require 10%, of buyers or sellers.

Nah. If they’re truly rich, they’re buying yachts. Houses are for little people.

also refin estimates and zillow estimates are way off too in the zip codes I’ve been looking around..The difference is almost 200K!! what kind of “Estimate” is that? It all looks like it’s fudged up.

The Year over year numbers are abut to get REAL ugly!! The real-estate cheer leaders like NAR and Red Fin have recently chosen to exclude mouth over month reporting and have instead reported “the housing market is up year over year. The current median price is compared to the median price of a year ago. As we move forward the 12 month old median price will rise almost strait up as the current value will most likely keep falling resulting in a huge year over year decline of epic proportions. This will be evident in all the future YOY numbers getting worse by the month until May or June of next year. The real knee slapper will be how the cheerleaders will put lipstick on the pig some other way.

“mouth over month” reporting. Now that my friend is hilarious!

I agree completely with your analysis and look forward to the housing crash of 2023. Unfortunately, a lot of good people will lose their winnings from the RE casino but overall a healthy crash is badly needed.

With a primary home and two rentals, I almost everything during the GFC. Now, I own a paid off 670 sqft home and only T-bills….patiently waiting for the forthcoming fire sale.

When the winning are well over 40%, if they lose 30%, they still won’t have any losses.

If they are up 40% and then down 30% they are losing money. $1* 1.40 (Up 40%) = $1.40.

$1.40 * .70 (Down 30% = $.98

$.98-$1.00 = loss of 2%

You need to cash in your chips first to win. Many will ride this to the bottom like the last time. Besides, all the equity some took out while prices were high will come back to haunt them.

You’re exactly right to a point. The 12 month old prices are now spiking while the current are dipping so the y-o-y will be very ugly soon. Let’s call it 20-30% down in a year. But that will mean the crash already happened. Then what? How much more decline will be left in the system? I say less than you think

Washington D.C. metro:

Month over month: -0.5%.

From the peak in June: -3.6%.

Year over year: +6.0%

Down in four months from peak in June: -11.3 points

This Case Shiller data give a misleading picture about what is going on in a large Metro area such as Washington DC. First of all, the data lags by as much at least 2 months. Second, the data should be spiked down to zip code to get an accurate picture. Some Zip codes are still in a bubble blowoff stage because of the shortage of available listed properties in prime locations, with good access to transportation and schools. Other zip codes (a majority) are already in a complete meltdown rivaling 2005/2006. Only when you look at the data down to zip code level do you get an accurate picture of what is going on.

Where can you find the data by zip code?

We got the data. It shows exactly what we said above. A 1,500 sq foot rambler just sold for 1.3 million in a close in suburb. It was in a great location, well constructed all brick, good transportation, access to downtown DC, stable neighborhood. That’s nearly 1000/sq foot. These are the pockets of RE that are defying all the trends. Case Shiller averages everything in the metro area and doesn’t pick up these trends in this particular zip code.

Hi,

Although I live in eastern Washington state I have occasionally watched videos by Sessa Realty discussing the Toronto RE market. To your point, his recent one indicated Toronto as a whole was down 12 or so percent from its peak (or was it YoY … I think from the peak).

However west Toronto was flat, central Toronto down 11 or 14 percent (median vs. average) and Eastern Toronto off 24%.

Again I dont recall if it was YoY or peak to current prices, but the local differences were dramatic.

I don’t own any RE.

Re: relentless drumbeat

The temp is quickening to a death march, but the good news is, you can use your crypto as collateral on the way down and see if the LTV is adjusted on the house or collateral…

“Crypto-backed mortgages let borrowers use their cryptocurrency as collateral to purchase a home. You don’t need to sell your assets to get one of these mortgages, meaning you’ll avoid tax consequences. If the value of your cryptocurrency falls too low, your lender may liquidate your assets.Apr 14, 2022”

Great! A housing market goosed with Ponzi collateral. Entertaining, at least, to to watch it all unwind.

Now, if this just keeps up at this pace for 10 more months, the Fed can claim real success, and return things to normal. Unfortunately, the Fed isn’t serious, so that won’t happen.

Wolf,

If by May18, (1) the upper bound of the Fed Funds rate is above a value of 5.0% (e.g 5.1%) and (2) the Fed has not made a credible announcement by that date that they intend to start cutting rates before June 2024, then I will be sending you an extra $50.

LOL, thanks! Will be interesting.

But when is “May18”?

If it’s May 18, 2023, why that day? What’s so special about it?

Enough time for them to feel political pressure once things look like they are going to go south “too fast”, two weeks after the May FOMC meeting. It’s a win-win type one-sided bet, however things turn out.

Rate hikes are doing their work.

Business tied to construction.

Have friends who own small manufacturing to hvac businesses.

All of us are down in numbers. No youngsters here. We all survived 08.

2023 will finally make the fed happy

with employment #’s.

Yup. Steel prices were a wild ride since early 2021. We just got Q1 estimates for 2023. They’re in the basement. Finally some relief.

Excess demand from all that free money has now completely evaporated in this area, and the half dozen metal suppliers we use are back to fighting for business. They bent us over a barrel for nearly two years so I have zero sympathy as the power dynamic shifts back to buyers.

Now, fingers crossed our top line doesn’t fall off a cliff too…customers are starting to push for discounts again since they can see commodities drop too.

The Most Splendid House Bubble (Rabbit Hole)

Maybe, this whole Everything Bubble is connected in ways we didn’t see?

” Noting that it is “rare to find ‘new’ types of mortgages in the post-crisis U.S. mortgage finance market,” Citi Global Perspectives & Solutions’ (GPS) “Home of the Future” report said that a “new crypto- adjacent mortgage product has gained prominence with a straightforward motivation: Allowing crypto investors to utilize their investment gains… Blah, blah”

Currently digging into Citi sec report to see BTC-BACKED loan valuation stuff. Essentially, these Ninja loans are probably everywhere and contagion impairment isn’t being examined (yet).

The FED appreciates your patience while they learn the limits of their systems. They are better calibrated for future once-in-a-generation events. The shareholders of all the banks are very glad. Whenever they need to goose the system they can and will go back to all the lessons learned

Housing Bubble 1 would still be a Housing Bubble today.

The Portland chart looks reasonably balanced. For insight on where this mess is heading, draw an imaginary straight line through the lows of 2002 and 2012 and extrapolate through to 2024. Then do the same for Vegas for a range of possibilities.

The lows following Housing Bubble 1 were assisted by QE and never reached their true nadir.

But the million dollar question is ..would the FED or whoever is responsible for this mess be ready to perform the reset??

When we talk about the Fed, the questions are in the trillions.

The Fed has no power to change economic outcomes; only the power to defer them. There might be some further can-kicking leeway but it would cost trillions and fail within a few quarters.

Any sensible cost-benefit analysis would conclude that history and reality have won.

Housing has already derailed the soft landing narrative.

The Most Splendid Rabbit Holes

What a mess!

I’m still confused about FTX obtaining a bank in Washington, a process that apparently fell under Federal Reserve Board jurisdiction. That act of issuing a banking license to SBF, seems criminal.

Nonetheless, as this expanding bubble pops, housing valuation is obviously linked to loan value and collateral, linked to LTV and default, etc.

Maybe I’m wrong to suddenly link crypto revaluation to home revaluation, but, there’s definitely weird stuff going on behind the curtains.

Beyond and besides the decreased value of homes and collateral, is the linkage to leverage positions and thus liquidity problems. As houses and crypto fall like lovers, in unison, that adds a new exciting layer of risk to the valuation drama, that’s probably just begun.

There’s been virtually no capitulation in any market and earnings revisions and impairment are nowhere to be seen — but I think this is like a scuba diver, deep below the ocean, with an oxygen tank running out of air. Reality isn’t that far off as all these positions explode.

Another tidbit:

We also use a portion of our deposits attributable to investor funds as the funding source for specialized lending opportunities, such as mortgage warehouse and SEN Leverage lending activities. We are comfortable with this strategy because of the short-term nature of those assets and because we can access funding at the Federal Home Loan Bank (“FHLB”) should we experience heightened volatility in the deposit balances related to these digital currency investor funds.

Let’s review, we have the SEC incapable of regulation, Federal Reserve granting bank licenses to laundry coin pumpers, FDIC doing nothing, Maxine Waters looking like a total idiot, the entire Congress looking equally corrupt and now FHLB ready to offer additional funding to a group of morons.

Obviously this insane mess hasn’t even started to unwind.

Welcome to ‘Murrica

People may downsize.

New Privately-Owned Housing Units Started: Units in Buildings with 5 Units or More, 12/20/22 FRED report:

The 584,000 units started in November is an increase from the previous month. This number is way above the 60 year average.

Let’s look at that? I want to go from a $500k home to a $350k condo. What did you say the new rate for that condo is 6.5%? Oh my! My mortgage is @ 2.95% So your saying my payment will be the same and I start over @ 30 years? No thank you.

No, John, because it is highly likely you’ll be able to refinance at rates successively lower over time.

Not if the interest rate cycle ended in 2020.

The bond mania is over.

This is from a Marketwatch, January 2020 story. It seems to me that a collateral review for LTV may be an interesting dynamic to watch. Somebody (entity) ended up with a bag of laundry tokens that aren’t performing…

“ Nearly 12% of first-time buyers indicated that selling cryptocurrency holdings contributed toward building a down payment for a house, according to a survey conducted by Redfin RDFN, -9.30% in the fourth quarter of 2021. That’s up from 8.8% of buyers surveyed in the third quarter of 2020, and 4.6% of novice home buyers in the third quarter of 2019.”

Are these year over year Case-Schiller numbers adjusted for inflation? example – if a house was 500k in Dec 2021 and now a year later it’s still at 550k, with CPI at 6-8+ percent, is that reported as 0%? I think if we factor in inflation, the drops are even larger. (If they are not including this in their calculations.)

The Case-Shiller Index IS AN INFLATION INDEX, that of HOUSE PRICE INFLATION. It’s conceptually silly to adjust one type of inflation by another type of inflation. It would be silly for example to adjust consumer price inflation by wholesale inflation, or consumer price inflation by wage inflation, or wholesale inflation by the Case-Shiller index. It’s one thing to see which inflation index has moved faster than others, but it’s conceptually silly to adjust one inflation index by another (though there are silly folks out there who will adjust anything by anything to make it look a particular way).

The rise of a pair : bought in 1995, sold in 2022, adjusted to inflation create a C/S bubble. C/S need only few pairs to skew up their positively biased charts. The banks and RE agents love these two blue zone elite enclave prof, but Gen-Z don’t.

That’s uninformed BS. You have no idea how the C/S works. I explained in the article that the sales-pairs method adjusts for time passed:

“The price changes within each sales pair are integrated into the index for the metro, are weighted based on how long ago the prior sale occurred, and adjustments are made for home improvements and other factors.”

And I linked the methodology in the article. Read the methodology instead of posting BS:

https://www.spglobal.com/spdji/en/documents/methodologies/methodology-sp-corelogic-cs-home-price-indices.pdf

That makes sense. Thanks for the explanation Wolf.

Somebody wise once said: Never ascribe to malice that which can be explained by mere incompetence…..

I’d like to figure a way to turn all of Gen Y and Gen Z against the FED. Educate them on what the FED has done to their futures and set them loose on the Eccles Building and across this entire land with protest signs to END THE FED. Tens of millions of young calling for these cronies to be hauled off to prison. That’d do it. Jerome Powell and his cronies would be finished. There’s no place in this country or world for these people anymore. They are a cancer upon society.

It seems as though everyone at this website wants to blame the Fed for the housing bubble. Many exclusively blame him. Occasionally some also blame Pandemic free money.

I can’t disagree with that, I’m not as economically savvy as the folks here. However it seems worth pointing out that politicians of all backgrounds allowed investors (of various types) go on a buying spree. No regulation … by politicians… to prevent it or limit it.

Why do none of the commentators here have a problem with that ? The silence would seem to suggest you folks don’t believe any regulation was warranted.

Separate matter:

Also… how many of the Fed-is-a-devil commentators here were complaining about their low interest rate policy in 2012 ? 2016 ?

Probably some. But as usual there seems to be a jump on the bandwagon affect (?).

Was the low rate policy terrible or was the problem a low rate policy COUPLED with large amounts of free money and supply chain problems ?

“No dear, this is not seasonal.”

Trudat. This is structural and will unwind over many, many years. Between the orgy of free money, and the NIMBY policies of lefty cities that give only lip service to housing unaffordabiity, and the shift toward work-from-home, and ordinances that seem designed to force small landlords out of business, the only surprise here is that it took this long for the tide to start going out.

Over the last 10 years, California has lost millions of middle class taxpayers, equal to the population of Philadelphia. Silly me for thinking that should have nudged prices down way before the Fed remembered what their job was, but it didn’t happen.

And instead of using the tsunami of free money for more creative building out of cities and neighborhoods, such as–just off the top of my head, I dunno–repurpose shopping malls and office buildings to multi-family housing? Replacing urban husks and former K-Mart stores with vibrant, affordable neighborhoods? Allowing investors to renovate empty theaters, strip malls, schools — into something usable by hundreds of young, growing families, and thereby give cities a great future?

But no. Lots of fun now to be had for pointing out how stupid NFT’s and Crypto and SPAC’s were, but when given the chance to truly transform the local landscapes of our most unaffordable cities, nobody wanted it to happen. So investors had to put it somewhere, even the dumbest places.

So let it go. Let the pols who listened to gentrified homeowner associations figure out how to pay levy ad velorem taxes on the same selfish people who crowded their town halls to shout down anyone who tried to do something different. Let the boomers who enjoyed a home-as-ATM machine since the Greenspan years now wonder if they’ll ever be able to tap their home for free equity ever again, and if no, what their taxes are going to be if they do sell and move elsewhere. And when the investors do come back, we’ll only be tempted by real returns of OVER 20%, and you can forget that if it’s in any ZIP code that EVER voted to let people live rent-free, indefinitely, for any reason.

“And when the investors do come back, we’ll only be tempted by real returns of OVER 20%, and you can forget that if it’s in any ZIP code that EVER voted to let people live rent-free, indefinitely, for any reason.”

That will really narrow down the choices, because there is a lot more of this coming in the future.

The banks won’t go quietly as far as housing prices going down is concerned. So the UK market, which has interest rates going up, as driven by the BoE to “fight inflation..” has base rate linked mortgage rates going up.

The banks response has been to switch repayment mortgages to interest only i.e. you no longer pay off the debt. Stimying the reduction of the money supply because now even with -higher- interest rates, repayments are now -lower- so if anything, for these property owners financial conditions are looser than before.

I realise the US is different, however for these conditions, I think the banks will be making every attempt to ease conditions for current owners to prevent a flood of properties coming on the market because basically its in their interest to do so.

There is a strategy I think thats starting to come out into the open of causing inflation as measured to come down by increasing debt. Such as the release of the US oil reserves to hold down prices at the pump, but this incurs a cost as you have to fill up the reserve again later. This higher cost is not an inflation cost, its been moved to another column.

Or the price cap on energy costs in the Eurozone and the UK, this makes inflation look lower but the cost is simply moved to another column, debt, away from the inflation measure.

Price capping strategies using borrowed public funds are fiddling the true inflation rate and making the actions of the Fed harder to proceed and I think these price caps are becoming more widespread. For example in the US the two mortgage price caps Fannie Mae and Freddie Mac are very obvious long-standing examples of US debt capping what would otherwise be interest rates. Of course there are others as well.

My summary although inappropriate for the article as posted is that there are many forces acting against the Fed tightening.

Most mortgages aren’t owned by banks.

The biggest price support is likely to be another government foreclosure and payment moratorium.

Who owns the mortgages varies between countries. The consequenses of default to the banks varies with country too.

Real wold example confirms: Sold house in Phoenix june 2021 (at zestimate) 350K. June 2022 zestimate was 411K, current zestimate 370K. -6K in last month.

Interest rates continue to climb. I think we will see, or need to- 12-18% street rates for real estate in 2024 Credit Card rates for highly qualified at 15-24%. ARM Rates ???????

1) The top 0.1% of wealth formed stocks, real estate and whatever bubbles. The 1% of wealth are $130M behind. The rest don’t participate.

2) The top 0.1% need time. The sticky inflation might osc between zero and 15% for almost a decade.

3) Alberta clipper caused death, destruction and blackouts. Tesla did’t start, Kia did.

4) Kia Forte for $230/month, $3K down. It used to be $120/month and zero down few years ago.

5) GM is fully committed to Hummer and Lyriq EV between $70 and $120K. From alpha back to Delta. Kia Forte price doubled not because of the high inflation because GM stupidity.

Most every home got up to a million clams in Southern California in the big cities, could you imagine being around 30 and looking at doing 30 to life in the big house with a monthly payment of what, $7k?

Madness

Xavier. They cannot sell it. They are stuck with what they got.There are not enough fools to buy it, especially after JP hiked interest rates, hikes that destroy buybacks, executives perks and bonuses.

Can QQQ breach Oct lows in the next few weeks : why not ?

Don’t worry, be happy, because QQQ will rise again, after scaring investors.

FED and Government created the bubbles. SAD watching this again and again.

NQ took out 28 SL all the way under Nov 11 low. If the big guys don’t care NQ will rise again. But if they do and NQ take SL under Nov 4 or Oct 13 lows and they panic the markets might plunge, at least for a while, for fun and entertainment.

My home “value” dropped about 1% since summer. I could not care less.

It is a well built ranch in a park like paradise, including a lake out back with forests in several thousand acres on 3 sides, and great neighbors to the south. No mortgage either. It is a liberating condition.

If the value drops to zero, it is still the same, modest, yet highly desirable, and deeply appreciated home.

Might I suggest all try to locate your own paradise, whatever that description might entail, and go for that to be happy. Chasing equity will drive you nuts.

I don’t even know what’s my home value is as I don’t really chase it and it won’t impact me anyway.

The last housing bubble ( and bust) is called by many housing bubble 1, or the first housing bubble. I think some time in the future we will look back on the bubble that is currently sliding down the backside and call it ” The last housing bubble.” It may be generations before we see the conditions for another housing bubble again.

The 2 things the rest of the world couldn’t undersell us on was the dirt under your feet and the MIC, and through the miracle of compounded interest created the housing bubble- the er, last frontier.

The other is self explanatory.

Housing depends upon Congress. Congress determines how housing is financed.

The “Cash / Drain” factor pricked the bubble in housing.

HOUSING IS THE BUSINESS CYCLE

If you’re not buying or selling, it doesn’t matter what home prices do.

My house has been worth $400k, $700k, $1.5m, $600k, $1.5m and recently $2.5m – all in that order over the past 22 years. It’s paper profits or losses unless I sell, which I’m not.

That said, I did start liquidating some investment properties and new construction and I still am. I missed the very top, but I’m close enough to be ok with the prices I’m getting.

It’s still not too late to get out, for those who haven’t, but want or need to. This market IS GOING LOWER. Look at the charts. I’ve been in the business for many years and been thru many booms & busts. This one’s just getting started, contrary to a lot of wishful thinking.

I treat my rental properties the way Wolf says to treat bonds – hold em til maturity, collect the interest payments and get your principle back in the end. Rental properties pay nice coupons, even though they’re a lot of work, and in the long run, unless you buy at the very top, they gain in value.

$1.00 today will buy $2.00+ of real estate in 2025.

Until recently with the price of used cars rising quite a bit, everything aside from a home went down in value sometimes drastically (I don’t mean to single out BMW & Jaguar owners…) over 10 years.

Furniture, home surroundings, sporting goods, clothes, shoes, the gamut.

And yeah I get it, that 3,500 square foot lot is pretty damned special and that’s where the value is, kind of.

Could houses drop down quite a bit in value as inflation in everything else is headed to the moon, Alice?

That’d be weird.

Agreed. I don’t see housing prices in nominal, fiat terms dropping if the replacement cost in those terms is only heading up.

If, on the other hand, you reckon the value of your house in terms of gallons of gasoline or even gallons of milk – then, yes, certainly it could drop sharply.

Replacement cost is dropping hard, as well as new home prices. Fastest drop ever, and it’s just starting. It’s an obvious consequence of Fed tightening. Interest rate sensitive sectors are getting hammered.

I have been telling my friends to get rid of their rentals but they believe it’d only go up in value. IN fact, one of my friends , bought his 4th house in san diego this March, which I guess was the peak.

I sold all my san diego rentals beginning of this year when the market was still hot and my friends though I am crazy to sell when the market is so hot.

Now, my friends are losing money in their rentals ( equity ) as well as in their stock portfolio. Some of my friends thought last year, that they can day trade and thus wont need a job. Things have changed now.

It was 82 on Christmas Day and more often than not the weather over winter is the best in the country. This isn’t to say that’s the only reason real estate will always be coveted here, but it sure is a huge factor; for that matter, all year the weather is good in San Diego. We’re bordered by Camp Pendleton to the north, mountains to the east, Mexico to the south and the Pacific ocean to the west. A tremendous amount of land is park, military, or dedicated open space. This all adds to the scarcity of buildable land. I’m not so sure I’d be wanting to sell off real estate here unless it was politically, regulation or tax motivated (ie: move to Texas or Florida).

I heard the same logic during HB1 as well.

My friends went out and bought many homes in last 1 year or so.

Going by your logic, prices should not go down at all in SD because it is different and special..

Many people told me to buy real estate in san diego saying come what may, home prices wont go down here.

I heard the same thing in HB1 as well. People usually deny using their own logic. For example, it won’t go down, worst it remains flat, It would go down but it won’t go down that much, OK it is going down a lot but it wont go down a lot in nicer areas.

Jon, after the busts the prices have always come back and shot up. What happened after HB1? Prices went up. After the S&L crisis? Up. After the massive military reductions in the early 90’s? Up. After the dot com bust? Up. The more challenging question to be answered would be when has it ever gone down and stayed down? Never. Printed money and poor economic leadership makes sure of that. San Diego is special, though.

There is a lot more to living standard than weather. The last 15 years I lived in SD I truly hated it. It is a depressing place now, compared to the SD I enjoyed in the 60’s 70’s 80’s and 90’s.

I will trade not having to look at graffiti and homeless everywhere for a little hot or cold weather any day. I can even go to Costco and drive right up to a pump, not sit in line for 30 min.

Replying to Jdog:

Believe me , I am in san diego but not by choice.

“San Diego is special, though.”

This statement made me chuckle :-). Most of my friends think the same.

It’s really not that special…I mean, it ain’t Carmel; even Carmel isn’t.

Going to another great time to build wealth from the delusional masses in the next few years.

I think the people that are going to blow the bubble are the people, that caused this shit bidding and paying millions in cash for 2-3-4 houses because everyone was doing it afraid of the inflation and losing the stolen or given money.

I know these are median home prices, but those are often purchased as rentals. The chart for more affordable rental class SFH in those metros (typically 70% of the median or so) might be even more distorted on the up and then down from the spike.

The 240 index number seems to be about where things took off in most markets (2018 / 2019). Even if prices came back down to the 240 index level, I am not sure these homes would work as viable rentals as far as cash flow – unless rents consistently rise through the recession. I’m not saying SFH should be seen foremost as rental opps, just saying the pricing metrics are bleak for future SFH rental investors. Multi-Fam housing will surely fill the void unless SFH pricing completely implodes below the 240 index level (unlikely).

“Multi-Fam housing will surely fill the void unless SFH pricing completely implodes below the 240 index level (unlikely).”

Why do you think SFH can’t go below 240 index level ?

I think it can easily go. If it can touch extremes in one direction, then it can happen on the other direction as well.

I heard the same thing in HB1 as well. People usually deny using their own logic. For example, it won’t go down, worst it remains flat, It would go down but it won’t go down that much, OK it is going down a lot but it wont go down a lot in nicer areas.

All the above proved to be wrong during HB1. This HB2 is much ore monstrous than HB2 so I assume it’d be much worse this time.

Not sure what the future holds but for housing to be affordable, it needs to fall a lot or people wages need to increase a lot and/or rates go down big time.

“I know these are median home prices, but those are often purchased as rentals.”

NO, NO, NO, these are N0T, NOT, NOT MEDIAN PRICES.

RTGDFA.

From the article:

“Methodology of the Case-Shiller Index: The index uses the “sales pairs” method, comparing sales in the current month to when the same houses sold previously. The price changes within each sales pair are integrated into the index for the metro, are weighted based on how long ago the prior sale occurred, and adjustments are made for home improvements and other factors (methodology).”