Record supply of LNG from the US and other sources. Record supply from Norway via pipeline. Conservation, power production shift… It adds up.

By Wolf Richter for WOLF STREET.

The price of natural gas futures in Europe continues to plunge off its crazy spike last summer. Dutch front-month TTF Natural Gas Futures – a benchmark for northwest Europe – traded today at €82 per megawatt-hour (MWh), down by 77% from the high on August 26, and back to where it had first been in September 2021 (data via Investing.com).

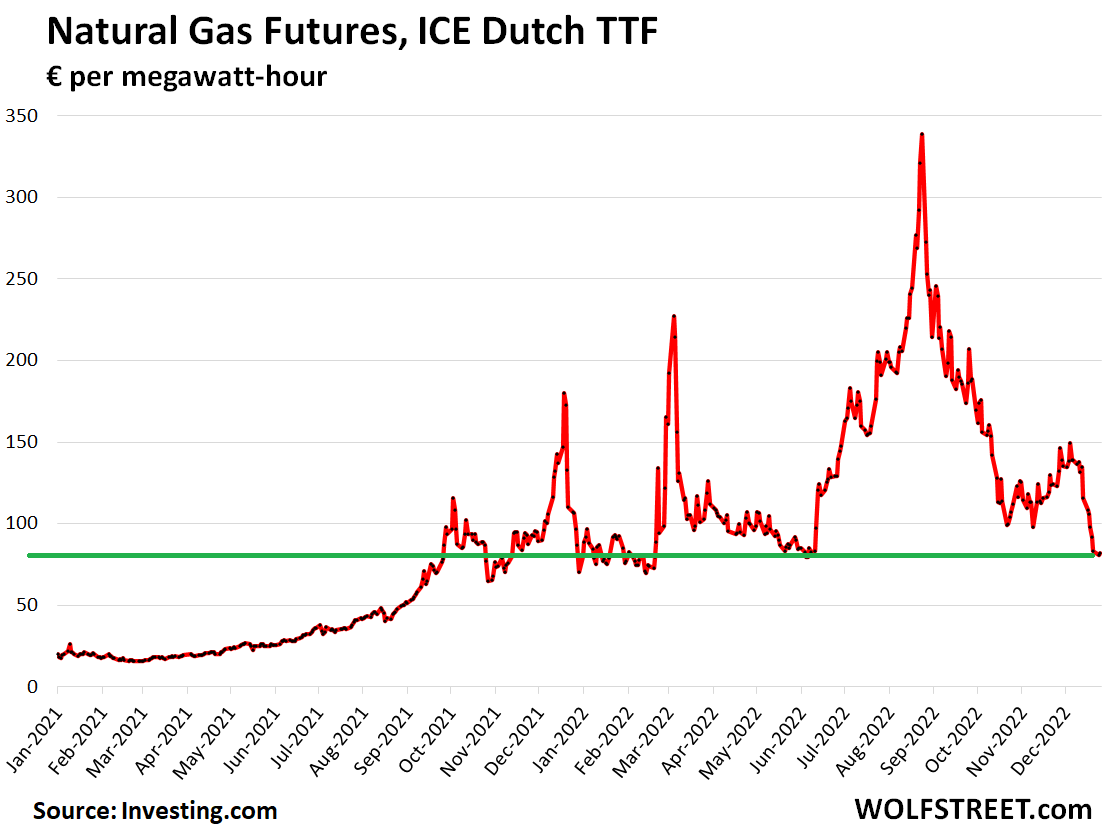

This plunge occurred amid a dual strategy in Europe: Reducing demand for natural gas and lining up new supply to replace pipeline natural gas from Russia.

The result on the supply side was a surge of LNG imports from the US and other parts of the world, that are offloaded via existing LNG import terminals and a growing list of floating storage and regasification units (FSRU).

And Norway, now the largest supplier of natural gas to Europe, increased its production by 8% from a year earlier, to record levels in 2022, according to estimates by Norway’s energy ministry in August. The gas is delivered via a network of pipelines.

And on the demand side, there are ongoing efforts by consumers and businesses to reduce consumption of natural gas and power, strongly motivated by the spike in energy costs. In addition, some power generation has shifted from natural gas to coal. Demand reduction was helped along by a relatively mild winter so far.

As a result, natural gas storage facilities are in good shape for this time of the year, especially important for Germany. In the European Union overall, storage facilities are 83.2% full, which is above the five-year average for this time of the year. Gas storage facilities data from Gas Infrastructure Europe, as of December 26:

- Germany: 88.6% full

- France: 84.0% full

- Belgium: 84.0% full

- Austria: 90.1% full

- Denmark: 89.6% full

- Netherlands: 77.4% full

In an amazing feat in Germany, where construction delays of years are common, the first floating LNG import terminal and a 26 km long pipeline to the existing grid opened on December 17, after only five months of construction. How Germany could source and install the equipment and put 26 km of pipeline into the ground in only five months is a miracle. Similar miracles are in the works. When it comes to keeping the industrial powerhouse fueled, previously unimaginable miracles are being performed on a daily basis.

In the Netherlands, two floating LNG import and storage terminals entered operations in the port of Eemshaven in September. Others are in the works.

Capacity of these floating LNG import terminals is relatively small, but enough of them will add up, and supplement increased pipeline supplies from Norway and other parts of Europe.

The shutdown of natural gas supply from Russia is a particular and spicy issue for Germany, which had become recklessly dependent on cheap pipeline natural gas from Russia, dating back to the Cold War. Every Chancellor had to be supportive of enhancing this reckless dependency further. Gerhard Schröder took this dependency to a new level with the Nord Stream project. After he left office in 2005, he got cushy jobs at Russian state-owned energy companies, Nord Stream AG, Rosneft, and Gazprom. Germany is now trying to make his life miserable. And it’s finally weening itself off that dependency.

And Russia is out of a lot of money on the natural gas that it didn’t sell to Europe, because it cannot sell the natural gas to other customers because the pipeline system cannot be moved, and there are no LNG export facilities linked to these production sites.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Even more of a miracle is that it didn’t spontaneously green itself.

“How Germany could source and install the equipment and put 26 km of pipeline into the ground in only five months is a miracle.”

It’s not really that amazing what can be accomplished when a sense of urgency exists.

Yes, we can go from burning Natural gas (70% efficiency through combined cycle cogeneration to coal (30% efficiency of ranking cycle).

Next step in this direction would be wood instead of nuclear power.

When developed economies last used coal, their energy consumption used to be far lesser. It would be interesting to see the effects of this change.

The un usually mild weather hasnt hurt Here in Warsaw its scarily warm.

Frederick – did you leave Turkey?

may we all find a better day.

Did an American make that opinion? Because I can see how that might seem a literal pipe dream with what it takes to build anything here.

In US, if you talk about putting a new gas pipeline, you will start getting called as the devil.

Gas was greened by the EU last year. Provided that the country it applies to wasn’t running on gas before, like The Netherlands, but was transitioning from dirtier fuels to gas, like Germany was doing from brown coal to gas. So it is green for Germany, but not for The NL.

What you think of that?

Commodity futures do not deliver or trade the actual commodity. Dutch TTF futures are in no way in this universe linked to real world supply and demand. What is actually occurring in the real world is unknown because there is no real market for these products. Why did Exxon reinvest all its capital into stock buybacks and not more rigs? Because oil prices are completely unpredictable and stock prices are not. Bring back delivery in commodity markets if you want investment in real things, because real investment requires real price discovery.

California nat gas prices have been hundreds of percent higher than Henry Hub futures, recently. One is a physical market – a real spot market, and one is a futures market – sell to open and buy to close or vice versa. Offsetting trades to settle instead of exchanging the actual product creates distorted realities. Dutch TTF is no different.

I voted for Trump twice and a lot of the stuff that came out of his mouth made me wince. But his remarks about German dependence on Russian gas were spot on. Even my sister and brother-in-law from Germany who can’t stand Trump were forced to agree. How one country can become this dependent on another after two vicious world wars and an extended occupation and Cold War just makes you scratch your head.

Globalism has some unexamined / ignored assumptions / opinions about political economy and what the world order ought to be.

Hard to say how much of that was ideology favoring certain parties or elements naturally sourced from changes in the economic environment due to the massive savings in international logistics from technological advancements.

Here’s a fun diversion, and topical! See how much you own / wear was Made in China / other low-cost labor Southeast Asian country. Count it twice if you bought it from Walmart.

“Here’s a fun diversion, and topical! See how much you own / wear was Made in China…”

That’s a hobby of mine, that I like to share with everyone around me at Xmas. I would say, from my N=10+/-, that the China factor is running around 80%. Every year I say the same thing…”how about next year we do a China-free Xmas?”

Rick

I believe the American position has been quite consistent for years. Trump doesn’t own it.

America has also placed too many eggs in one basket in recent history.

This article is pulling me into political commentary. Have to stop there.

Hi Rick, under Trump and Biden administration, they have overlooked the seriousness of inflation by the time it reaches you, it could be recession while the interest Rates surge to 5%. If nothing positive measures is achieved, it could skyrocketed 5.5%, goods and cost of living will surge as well.

The trend of increasing LNG exports seems like it will bode well for US balance of trade and GDP.

All the flight cancellation would not bode well for the GDP (unless passengers are forced to rebook at 5X prices).

Wait a minute, weren’t these airlines bailed out with billions of dollars of taxpayer funded debt to support the GDP in first place.

I would prefer to have a better price per therm instead of worrying about the trade balance. Until June, I was on a 2-year $0.38 per therm plan that jumped to $0.74 per therm.

Yep, it will be a strong NG market for couple more years, Europe NG issues will be more pronounced next year. Long winter and they will be in trouble this year. NG is now sitting on long term support. I started scaling in slowly on Ung today

What LNG worth is still not in the league of oil. It only makes the previously unprofitable LNG terminals a much better investment and actually valuable, but the market is still 1/5-1/6 the size of oil and profitability is possibly even lower. Major boost to African economies dealing in natural gas exports, but not a significant portion of the US GDP.

Care to share what you are looking at? Personally I like Baytex Energy.

My wife is hurrying me when I’m taking a shower and this is the result!

No gaspocalypse in Europe? Phooey, there’s so much ruination in a European Union.

Hello . I have two points to add.

This can be taken as good news. If this stabilizes the price of gas, it is good news. If it is one more of the big spikes in price variations, it is not good news, because it implies more uncertainty at the moment of making the costs and the sales prices of the products in general.

On the other hand, it unequivocally shows that Germany, being one of the largest producers and users, and more advanced in the development of “alternative energies” could not face the lack of gas with these, and the answer is simple, there is no way to store large amounts of energy to balance demand, then gas-fired power plants are used.

There’s still no near/mid-term energy transition plan for EU. Kinda like US once one examines the details.

We’ll just ignore how much coal Germany is now burning, right?

No one ignores it. Germany has always burned coal for power generation. That’s not new. So now it reactivated some older coal plants, and it has shifted some power generation from gas to coal. An economy cannot function without electricity.

So, the price of natural gas goes down significantly, as it already has started to do, but it still might not offset the financial attractiveness of moving to increased coal imports and the firing up of legacy plants beyond current EIA estimates.

Question is whether US coal miners will participate and to what extent. Some have already set aside some volume to that end.

Coal is a big export product for the US. In 2021, the US exported 85 million short tons of steam coal and metallurgical coal.

Northern Italy is burning more coal. My daughter tells me the air is pretty dirty. You can tell with every breath. Hopefully as the winter moves forward and gas storage stays above seasonal norms they will cut back on coal for District Heating.

So guessing from your comment about both US thermal and met coal exports, you are thinking that met coal will be increasingly diverted to energy generation in export markets because there will be a significant economic slowdown which usually implies less steel production?

That view would also imply that US met coal producers and US steel mills are in for a rough ride.

The wind blows towards Russia.

Germany burns a lot less coal than China, who has to generate power for it’ s Coal cars (known elsewhere as EV’s).

Until recently, Russian oil was being sold to India and then resold directly to Europe; Russian oil was being sold to China, refined, and refined products sold to Europe. Nothing is ever what it seems.

Lotta money being made in non-US exchanges investing in coal mining equities. As the Global financial system bifurcates, one dividing line will be fossil-fuel supported economies versus alternative energy economies; commodity based currency/trading systems versus petrodollar/fiat systems. It’ll be interesting navigating through these investment waters. One target in all of this is dollar as global reserve currency – divided opinions among the “cognizant” how this high stakes global power play will end.

Maybe the pandemic shock ultimately resulted in more efficiencies and higher levels of resilience globally. However, global sentiment seems weak, as we all ponder the possibility of more economic shocks. The Fed and various fashionable experts point to the jobless unemployment rate telling us we aren’t headed to recession, as the ignore the structural trend in the participation rate, with Boomers retiring early, as well as demographic changes that distort prior metrics. The other tribe (which I belong to) beats the drum of earnings decay, overvaluation, impairments from operation cash flow burn from inflation and higher interest rates.

It’s great Europe dodged the natural gas bullet, but things definitely don’t look rosey going forward…

it would “seem” investing in us natural gas companies /pipelines would make sense – BUT when you look at the price if everything natural gas related since fall/winter began are getting crushed ! anyone who got invested in the sector in the last 6 months has been “bitcoined “

You need optometrist visit, I’m banking 11% yield and all symbols comfortably above buy price

NG always gets hit end of year

NatGas contract prices are profoundly volatile. This is doubly-so during winter months in the northern hemisphere.

Recently I clipped an article from NYT (which is now $7 for a paper copy, Sunday edition is $12 ! My first NYT clippings dating Oct 1987 say 30 cents).

“Germany’s Energy Crisis Is a Cue to Chop Wood and Stock Up”

Pictures are absolutely comical.

60 y.o. retirees chopping wood, skinny-dipping in the morning instead of taking shower, stocking food (but no ammo ?), trying to catch some bleak winter sunrays with a small pathetic solar panel…

And all this with the expression of grim determination to win – or survive – or to prove something – or whatever (look at Herr Leo Bäumler in the pic #1, was he the guy who played Tin Man in “Wonderful Wizard of Oz” ?)…

I will screenshot those plummeting Nat Gas Futures, print it later on when I chance upon a printer, and paste it at the bottom. The Future will tell which mirror reflects the reality best.

And my scrapbooks will outlive all your goddamn Internets and will be unearthed in 2987 A.D. where Chicago used to stand.

I dimly remember one article somewhere describing how one mysterious entity domiciled in Holland trades (and manipulates) all Nat gas futures in Europe.

I gave it a passing glance and did not screenshot it. No big loss I guess. Probably the same modus operandi described in the book “The Smartest Guys in the Room: The Amazing Rise and Scandalous Fall of Enron”.

Enron used to be a World Nat Gas Empire…

Dutch Title Transfer Facility (TTF).

Also referred to as NLD-Europa.

79% of European NatGas Mkt Traded there.

Habeck the Greentard Philosopher and Children’s Book Author wanted a Storybook Scenario where Long-Term Contracts btwn Suppliers (which need them to commit the Time+Money to locate+extract) and Consumers would be Trashed and the NatGas thoroughly Traded as Short-Term Futures Contracts like those on NLD-Europa.

Makes you wonder if NLD-Europa are funding the “Greens” along with the CIA/MI6 – because NONE of the DEU Greens’ Policies are Environmentally Sound and they don’t have anyone with a BioChem-Leaning STEM Degree in their Leadership.

Hello Brent, great comment! As an American living in German since the 80‘s, I can attest to the German propensity to engage in activities that are individually very small impact, but with their social mindset, most Germans will „pull together“ to creat a net very large impact.

On the topic of storing ammo: being from Oregon, I miss that aspect of being able to defend your home and life with lethal force. In Germany, the monopoly for the use of lethal force lies with the state – it is rare for Germans to own real weapons and ammo and keep them in their homes. On the balance though, I prefer the strict gun ownership requirements here in Germany. I feel much safer than living in the U.S where mass shootings, armed home invasions, and armed car jacking seem to be the order of the day.

=As an American living in Germany since the 80‘s, I can attest=

😁

As an American rowdy piglet stationed in Germany during mid-80’s, I can attest that not all Germans were created equal.

Back then Greens were as psychotic as now (remember Gen Gert Bastian and Petra Kelly ?). Deranged f…ck Yoschka Fischer complained that Germans have too much money, large part of which must be given to the rest of the f…ng World ASAP(???).

On the other hand we befriended fine members of Gremlin Motorcycle Club, 100% sound and sane in mind and their 6’3″ fat-free muscled bodies. As a supply clerk (E-4) I made considerable contributions to their safety and material well-being, because, you know, US Army depots were full of useful stuff. And our generosity was fully reciprocated.

Now, my friend, watching yet another BS emanating from Bundestag (as I do watching yet another BS emanating from Washington, DC), always remember the wise advice from the “Black Book of E-4 Mafia Wisdom”:

The first question I ask myself when tasked to do something that’s not obviously and overwhelmingly in my own best interest is:

“EXACTLY WHAT HAPPENS IF I DON’T DO IT?”

=in the U.S where mass shootings, armed home invasions, and armed car jacking=

Never happened to me nor to anyone I know. So why bother ? Besides, living on Chicago South Side, I acquired a taste for German classical music.

Midnight burst from AK, followed by the wailing of police sirens, sounds exactly like the rhythm of the opening phrase – “dit-dit-dit-dah” of Beethoven Symphony #5.

And petrochemical and electrochemical production and output is cut to half it used to be in europe?

Aluminium smelters, fertilizer plants and such have shut down due to high energy costs.

Around here a petrochemical plant stoppe half of the owens and then output. They made considerable more money selling the electicity they had bougt on long contracts on the spot market…

So that’s why New England couldn’t keep the lights on last week. Makes sense now.

There is simply no possibility of LNG from the USA or Qatar (or other sources – e.g. Scandanavia) meeting EU nat gas needs in the near- or middle-term. Under the “best case scenario” the USA can meet about 20-25% of that demand and it doesn’t take much (e.g. the Freeport-McMoRan shutdown) to wreck that scenario. And let’s not forget that seaborne LNG supplies are locked into contracts that must be negotiated months in advance.

Even if it were somehow possible – the “best case” pricing scenario is that LNG (which must be processed) is about 20-25% more expensive than terrestrial pipeline gas. Recent comments from Germany suggest the actual price being paid is 3x-4x as much.

So whether the problem is availability or price – this is going to result in substantial de-industrialization of the EU.

And let’s not forget that Russia didn’t turn off the spigot until mid-summer, thereby enabling Europe to fill it’s underground gas storage facilities for this winter. They will not have that privilege next year and, therefore, next winter will be much, much worse.

Some sort of re-approachment between the EU and Russia seems inevitable to me and it’s painfully-obvious which party will get to dictate the terms.

So, what about US producers setting aside 15-20% of their production to sell into floating storage provided by trading houses at prices locked in over the next couple of years? The traders would be thinking that by the time it is needed, you will have customers that are very happy to lock in supply at a higher price providing the traders with a good margin. Just a thought.

BigAl…agree with your line of thinking.

What do you think happens to shipping rates?

Shipping transport industry somewhat like oil & gas in that no new construction (throughout the four tier structure of capacity types) has been added for well over a decade (not driven by ESG scenario like oil & gas).

Yes – right now “reliability of supply” is the highest priority.

In September the USA was able to export 11.5 bcfd/day of LNG. Nobody I’ve talked to suggests this figure can rise much beyond 15.0 bcfd/day in the next several years.

Depending on what “several years” implies, you are looking at a pretty interesting uptick in export sales that can be locked in at interesting prices. Maybe, you think hydrogen will replace natural gas in that time frame? So, what are the other options?

Natural gas right now is being marketed as the means to transition away from traditional energy sources to greener ones as I understand it. Otherwise you are looking at scenarios that involve coal and oil or distillates. I cracked a smile over an earlier comment about burning wood!

All of the aforementioned options are really popular with the politicians, the climate change lobby and the E in ESG … (irony OK? )

So, if you do not have access to hydro, then nuclear is your other option for non-intermittent supply to balance off your renewable (ie. wind and solar) energy production capacity that continues to be heavily subsidized by the state, whenever it is introduced. We’ll see what happens when the long-term 20 year contracts, play out.

Right now, the focus of corporate energy players is on paying dividends and share buybacks, not increasing reserves, at least not in the USA. Some could characterize that as a “bribe” of the public, which results in it being is starved of economical energy resources, as development is arrested.

At some point, energy will be required and if the technology is not there to keep everyone cozy and warm at an affordable price, well things will get interesting and it may not be an unreasonable assumption to predicate that governments will step in.

Fascinating topic.

Hats off to your great comment. Sensible, well researched but unfortunately will be ignored by most people.

BigAl,

BS, from A-Z. Norway is by far the largest supplier of NG to Germany. There is some NG in Europe, there is lots of NG in North Africa (just across from Spain), there is a huge amount of NG around Cyprus that can get produced, there is NG everywhere. What there isn’t enough of are PIPELINES and LNG terminals. And they’re now getting built.

“Deindustrialization” my ass. Building all these LNG facilities IS industrialization. And it feeds further industrialization. They’re spending hundreds of billions of dollars to industrialize their energy sector.

You’re clueless about how Germans feel about Russia’s war on Ukraine. What is Russia going to take next? Former East Germany? This war shook up a lot of peacenik Germans.

Germans getting fearful of Russia taking over East Germany… LOL Somebody should remind them about Austria and Czechoslovakia…

And about building Nord Stream 1 + Nord Stream 2 behind everybody’s back. I get that business is business, but victimizing Germany is ridiculous.

“Somebody should remind them about Austria and Czechoslovakia…”

Yes, reminder: Prague, 1968. I was a kid then, seeing the shock of the adults around me.

“victimizing Germany….” Hahahaha. Braindead BS. Read the G*d d**n F***ing Article (RTGDFA)

“What is Russia going to take next? Former East Germany? ”

IMHO Russia is seeking to take eastern part of Ukraine, up to Dniepro river, plus southern part of Ukraine, Odesa – Mikolaiv, plus Kharkiv in the north-east of Ukraine. I doubt that Russia want to take Kiyv, and certain that Russia doesn’t want western parts of Ukraine (but Poland and Romania may be interested in returning these territories).

As for Germany, Russia highly values German technological capabilities, and would love to sell its natural resources to Germany at half price in order to be able to buy German machinery, medicines, scientific instruments etc. This is all that Russia wishes for; it doesn’t have military muscle for any ventures outside eastern Ukraine (and Russian leadership knows this very well).

I second what AK said. A very sensible, measured comment based on what Russia said they where going to do in Feb and what is actually happening on the ground.

One of the reasons Putin invaded Ukraine was to secure the huge LP supply in the ground there just waiting to be tapped. AND, the pipeline infrastructure to Europe is already in place.

Things have backfired on Putin on many fronts.

The local papers states different. Yara have shut down fertilizer and other petrochemical plants. I do not have the exact numbers, but about half of production have been cut.

Norsk Hydro have similary cut aluminium production as have others. All in all about one fift of the production according to Reuters 25 of august.

Elkem have shut down some of the silicone smelters locally, citing high energy cost as the reason.

New pipelines, sure, from Russia to China. Then, with China buying Russinan gas at pipeline price to their petrochemical industry european petrochemical industry may be at a disadventage if they have to pay LNG prices for their gas.

LNG 5:0 Fun/fun: down from May 2022 high to July 2022 low. Up to

Nov 2022 high, before making a round trip to May 2022 high.

“1) Norway production is down. They are buying wholesale US LNG.”

How are you measuring this? The article Wolf linked from Reuters says production is up 8% from 2021 and may exceed the production record from 5 years ago. So perhaps production will be down from that record, is that what you mean?

I did see an article that Norway’s Equinor plans to buy US LNG starting in 2026, but nothing currently. Maybe another Norwegian corporation is purchasing US LNG currently, but providing a source would be useful where your bullet point appears inconsistent with the article.

Putin waited too long to shut off Nordstream to seriously affect Europe this winter. Isn’t next winter going to be a better test of how Europe fares natural gas wise when there won’t be any Russian natural gas to be had (absent the end of the war)?

There is a lot of new supply being lined up at break-neck speed. And other changes in the energy markets are taking place as well. Europe will be better prepared for it next winter. It will still be a strain, but it won’t be a surprise and chaos, as it was in 2022.

They will be in bigger trouble next year….

chaos will come with a longer winter and looks guaranteed for 2023-4 winter….

NG has years to run high, they will shut production and no new production will come. Africa is not a reliable source, North sea production is waning

What is happening now if fairly irrelevant. It is what happens next summer when the stores of gas need to be refilled that will matter. Gas reserves are filled in warm weather, and used up in cold weather. Europe started this winter with its tanks pretty much full of cheap Russian gas.

Next year they will have to refill those reserves with much more expensive LNG. That is when we will see the impact of all of this on their economies. US gas prices are already higher as a result of exports, and when it has to ramp up exports, we will see what the real impacts are.

The price of LNG has also plunged.

Yes, but it will always be much more expensive tan piped gas .

Would love to see a 77% crash in US NG prices. Not likely to happen anytime soon without a nice, real recession.

Yes, would be nice. So far, US natural gas futures have plunged only 50% from the spike in July. Now at around $4.70, from $9.98 in July.

you will miss out on another great run like 2005-2011

I have 3 symbols paying 11% yield and above, it will be this way for years….

All the naysayers were out in 2004-5 too and I banked cash for 6 years….

Frugal consumers, abundant supply and warm winter are definitely major contributors to the low prices, but the EU also launched a scary investigation looking for anti-competitive behaviour on the energy markets. Given the LNG trading field is full of dirty players like Glencore, Vitol or Trafigura it’s not that impossible to imagine the EU might be able to find some interesting trading patterns around the price hikes – or at least a scapegoat. The announced gas price cap likely also discouraged traders to engage in any kind of further price fixing (even if it’s actual use is questionable).

USDOJ found not only very interesting but also very very fraudulent trading patterns 13 years ago.

In re Amaranth Natural Gas Commodities

United States District Court, S.D. New York

Apr 27, 2009

612 F. Supp. 2d 376 (S.D.N.Y. 2009)

In common parlance this Nat Gas futures fraud is called “Banging The Beehive”

WSJ dedicated an article to this fraud in 2012.

Yes, a chart like this tells you that there’s some interesting stuff going on that you might want to investigate, LOL

Measuring nat gas in megawatts has me stumped. My whole life I have heard and used mcf or similar such when talking about gas. I guess I have to get me some new education on the new world market for gas.

I’m confused then, so why is the FT running articles on BASF etc. and how they want to slash capacity in Europe and move overseas. This take sounds quite panglossian.

Hahaha, BASF already has a number of large facilities in TEXAS! Has had for years. For the same reason I’m going to tell you in a moment.

The FT article you cite sounds like some young clueless reporter just saw another BASF press release, thought it was the first press release ever, and made some clickbait out of it.

Here’s why:

Lots of companies that use natural gas as feedstock have FOR YEARS expanded from various countries, including from Germany, to the US to produce fertilizers, chemicals, etc. in the US.

The petrochemical industry in the US is HUGE (largest in the world) for the same reason: cheap petroleum and petroleum products in the US.

Fracking in the US caused the price of US natural gas to collapse in 2009, and this has been a theme on this site since the predecessor cite in 2012. Fracking then also caused the price of oil to collapse starting in 2014. This attracted a lot of companies from Germany and other countries that use natural gas and petroleum as feedstock.

The U.S. is now the world’s largest exporter of natural gas. Poor Ukraine is living in a state of oblivion with frequent power outages. The price of real estate in Hong Kong is at a five year low. Vegetation spreads over the abandoned city of Houtouwan, China. The U.S. continues to draw down its SPR emergency oil storage. The Permian Basin produces 5.5 million barrels of oil/liquids a day. This is more than the production of Ghawar, the largest oil field in Saudi Arabia. Fifteen years ago people worried about oil wells running dry. There was a race to build LNG import terminals in America. Now they have converted import terminals to export terminals. Appalachia produces natural gas like Qatar. New England still copes with shortages of NG. Floridians are worried about global warming effects.

In agreement with Arthur here.

I have to disagree because the article doesn’t say buying Russian gas is reckless. The article actually says, repeatedly, Germany became “recklessly dependent” on Russian gas. In other words, it’s not buying Russian gas that’s reckless, it’s Germany’s DEPENDENCE on Russian gas that’s reckless. Arthur is using a straw man in order to make an unrelated comment about American actions in Ukraine.

All due respect, your response is equally straw-like.

Dependency is a security concept. Supply risk perhaps more accurate? Either way, the concept has its roots in politics and not price. GE was buying cheap gas. Pure and simple.

This whole thread is avoiding the context of sanctions, Green Energy policies, gov’t renewables policies/market and investment impacts , etc., that move the discussion out of normal market/price considerations and into politically engineered results.

Those politically engineered circumstances can change also very quickly. Any peace settlement in Ukraine would open the door to Europe dropping sanctions and beginning to purchase the inexpensive energy it needs to stop the decline in its economic and living standards. Without that happening, Europe is going to experience real pain and that in itself will cause political changes.

No argument from me!

I was responding to two comments that have been removed, so the context of my comment no longer makes a lot of sense. I wasn’t disagreeing with the article, just a previous comment, and one agreeing with it, that I thought blatantly misread the article in order to inject an unrelated political viewpoint (I did not express an opinion on that viewpoint). I screwed up by not imbedding my reply properly. That said, unless you read the two comments I was responding to it’s impossible for you to know if my argument is “straw-like.”

You’re certainly correct that “supply risk” is often rooted in politics more than price. As it relates to Germany, I think this article was focused on the economic consequences of being overly reliant on one source for a critical commodity. I don’t think the political reasons that reliance is causing problems now was the focus of the article. That’s just my opinion anyway.

Thank you for pointing this out. Seems people got confused.

Norway has been ‘encouraged’ to slow down its electrification of heating and transport, so it can increase pipeline NG rather than use it in its own CCGTs. Unlikely this will continue in 2023.

Qatar has been largest supplier of LNG to Europe ( inc UK) 2022. Second largest supplier…Russia. US trails in third. Russian supplies have included shiploads earmarked for China, but these were off loaded in Europe instead when China replaced LNG with increased coal burn at the time of peak prices. Unlikely to continue in 2023.

Two major reasons for supplies holding up in Europe so far this winter. Far warmer weather than usual coupled with demand destruction. Most of the demand destruction is not residential customers turning stats down, its industry shuttering up. If this continues next year de-industrialisation is real.

Of interest and concern is the growing contact between Gazprom, the Iranian National Gas company and the Qataris. A NG ‘OPEC’ is on the cards. After all Qatar’s north field is shared with Iran , they have to plan its development in cooperation to a large extent.

Europe is not in a good place.

Yes. Middle Eastern countries becoming interesting middlemen!!

Few noticed that is was through UAE (and not the traditional Switzerland conduit) that the Bout for Griner prisoner exchange was negotiated.

If trashing industry and economies saves gas, shorted by imbecilic energy policies, then, using the same logic, CO2 emissions could be greatly reduced if we all just stop breathing.

How Germany could source and install the equipment and put 26 km of pipeline into the ground in only five months is a miracle.

It isn’t a miracle.

The government was forced to stay out of the way, and the contractors were given a deadline. This is how construction should also be handled here in the States.

It, major GUV MINT projects sometimes IS here in USA similarly nemo.

This from one who was an estimator/construction manager for many years, at the end focusing on FED ITBs and subsequent work up to $4BBs level.

IMHO as a now retired guy, USA FEDs would absolutely ”get out of the way” and actually HELP when they wanted a project done yesterday..

OF COURSE most of these kinds of projects were kept fairly quiet, as in NO press releases that are now the vast majority of ”news” available to WE the PEEDONs…

Kinda, sorta off topic, but this is an interesting energy related rabbit hole, that includes natural gas consumption in Texas, where taxpayers seem to be subsidizing crypto mining. The politicians apparently are creating legislation to benefit mining farms, as many Texans wonder why their utility bills are climbing.

After all, it’s Texas and who cares, but as a recession unfolds, cost of living challenges for everyone in that state will cause a tsunami like burden, as home prices fall, unemployment increases, etc, etc.

**

ERCOT offers some of the cheapest power in the country, often as little as $20 a megawatt-hour. While the price can go up to $5,000 a megawatt-hour when demand overwhelms supply, ERCOT will pay industrial users to shut down during those periods.

… thanks to the way Texas power companies deal with large electricity customers like Whinstone, Harris’s bitcoin mine, one of the few owned by a publicly traded company, didn’t suffer. Instead, the state’s electricity operator, the Electric Reliability Council of Texas (ERCOT), began to pay Whinstone — for having agreed to quit buying power amid heightened demand.

for those as perplexed by megawatt hour pricing of natural gas as i am, 1 mmBTU = MWh * 3.412142

To put a few of those numbers in context. There were 6 floating regassification plants free in the world (out of 48). 3 were moved to the Netherlands and Germany. Another 10 billion or so of orders for more of this type of floating factory for just Europe. And 10 billion in LNG transports seeing that there is also a shortage of those.

That said problems are not over. One of the reasons that most of Europe managed to top of their reserves is that for more then half of the year they still received gas from Russia. That is gone for 2023, China is going to import more now the COVID restrictions are lifted while the pipelines from Russia are full (and as Wolf said you can’t just move a pipeline) so China will be competing with Europe, the largest exporter of gas in the Middle East is Qatar which is royally pissed that the EU did not hush hush, as they demanded, the bribery scandal going on now (it doesn’t help that even before that it seems that Qatar started favoring China).

And depending on how cold it gets in Germany it can get worse. They need to basically end February with a 40%+ reserve to not enter the October/November 2023 with the next emergency stage (they are currently on stage 2 that basically mandates a 20% reduction of gas use across the board). Worse is that they are only on target for that 40% due to the temperatures being above average for most of December.

Also one of the initial reasons for the Nordstream pipelines was to cut out a Russia-hostile Ukraine after it showed it had no problems with disrupting Russian gas transport to Germany and the rest of Europe. Another one was that despite the higher upkeep of a underwater pipeline the Nordstreams would be cheaper then the pipeline through the Ukraine and Poland.

Then a few people got the bright idea that they could shutdown coal and nuclear power due to the expanded transport capacity instead of the intended switch from one set of pipelines to another.

It’s really ironic when someone writes about German dependency on 30 USD gas and call it freedom at 180 EUR.

Evil Russian gas for 30 USD, but Good american gas at 180 USD.

Seems like a fair trade: as the poet said – freedom is expensive. We should all tell it to our local baker in Italy, who said that now it is impossible to sell bread with a profit. Before the gas crisis the prices were 2,6 EUR/loaf, now it should be 5,8 EUR/loaf. The baker said: “But at that price … who would buy it? No one. So we’ll close the bakery in 14 days.”