And in terms of “housing shortage” or “underbuilding?” Well, we’ll just go ahead and sink that meme.

By Wolf Richter for WOLF STREET.

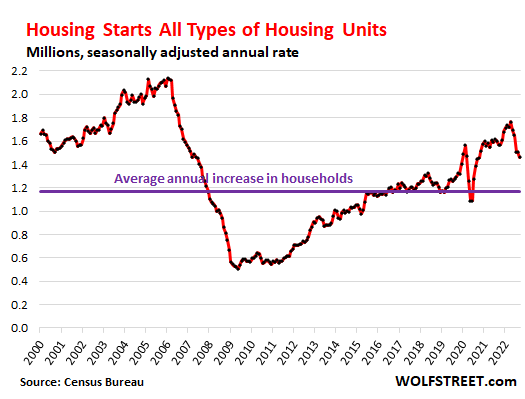

The total numbers are somewhat dismal: Construction starts of all types of privately owned housing units – single family houses and units in multifamily buildings – fell by 8.1% in September from August, and by 7.7% year-over-year, to a seasonally adjusted annual rate (SAAR) of 1.44 million housing units, according to the Census Bureau today.

These initial estimates tend to get revised sharply up or down, and are very volatile. For example, in August these housing starts had spiked by a revised 13.7% from the prior month, following a veritable plunge in July. The September decline only worked off part of the August jump.

But there are important trends underway that these month-to-month ups-and-downs distract from:

- A boom in construction starts of multifamily (condo and apartment) buildings at highs last seen during the multifamily bubble in the 1980s;

- A plunge in construction starts of single-family houses that started in April as mortgage rates began to spike.

I’m going to show these trends by converting the volatile month-to-month data into three-month moving averages (3MMA).

The three-month moving average (3MMA) for construction starts of all types of privately owned housing units fell by 3% in September from August, by 6.9% from a year ago, and by 8.6% from the recent high at the end of 2020, to 1.46 million housing starts (SAAR), the lowest since October 2020. Residential construction did a U-Turn in April and hasn’t look back since.

The purple line reflects the average annual increase in households from 2000 through 2020 to shed light on the so-called “housing shortage” and the so-called “underbuilding.”

In terms of this “housing shortage,” well…

The real estate industry uses the term “housing shortage” to justify the home prices that have ballooned to ridiculous levels, which created the bizarre world where there is now a shortage of homes people can actually afford to rent or buy, but a glut of homes people cannot afford. If you have lots of money you can rent and buy lots of homes and just leave them vacant if you wish.

Turns out, there is no shortage of housing, just prices have been inflated beyond recognition. And some folks try to get some tax benefits by converting their vacant homes into vacation rentals.

In terms of the purple line above: Housing starts fell behind household growth only from 2008 to 2015. But in 13 years before then and in the seven years since then, housing starts have out-run the growth in the number of households. And in 2020, the number of households actually fell, even as housing starts boomed.

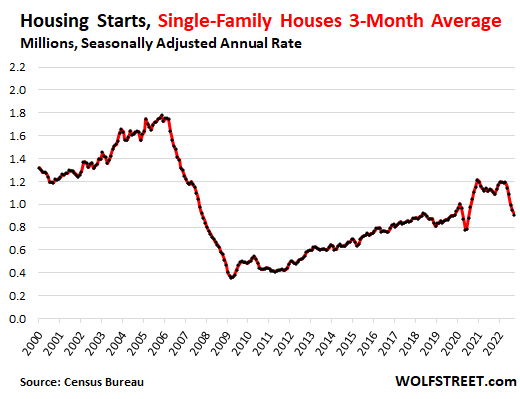

The plunge in single-family construction:

Construction starts of single-family houses fell by 4.2% in September from August, and plunged by 17% from a year ago, and by 25% from the peak in December 2020, to just 909,000 houses (SAAR, 3MMA), the lowest since July 2020.

Construction had peaked in December 2020 amid the mind-boggling free-money boom orchestrated by the Fed’s QE and 0% interest-rate policy, and by the government’s efforts to throw as many trillions of dollars in as many directions as possible. And housing got some of it and boomed.

But by 2021, inventories of houses in various stages of construction began to pile up. And when mortgage rates began to spike earlier this year, demand began to fizzle.

Homebuilders are trying to unload massive inventories as demand has plunged and as traffic from potential buyers has collapsed to Housing Bust 1 levels. Homebuilders have said that they’re going to manage these inventories from both ends: By reducing construction and by trying to boost sales somehow.

But even at the peak in December 2020, construction starts were far below the historic boom during Housing Bubble 1 that created an enormous amount of excess inventory that took years of household growth to work off.

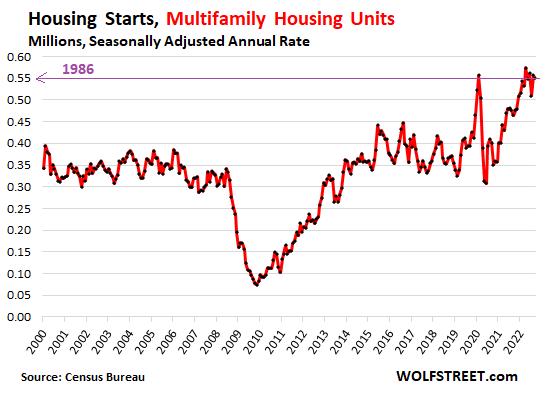

The boom in multifamily construction.

Construction starts of multifamily buildings of two or more units, such as condo and apartment buildings, dipped by less than 1% in September from August, to 551,000 units (SAAR, 3MMA). This was up by 18.6% from a year ago!

Over the past six months, construction starts had been in the range between 477,000 and 632,000 units (SAAR, individual months, not 3MMA) the highest range since the multifamily construction bubble in the 1980s, that began to unwind in 1986.

In many densely populated cities and urban centers, multifamily is just about the only type of housing that is getting built, such as in San Francisco, Boston, Manhattan, etc.

In San Francisco for example, there are currently 69,365 housing units in various stages of the development pipeline, and nearly all of them are in multifamily buildings, many of them on tracts of land to be redeveloped: Candlestick Park/Hunter’s Point Shipyard, Treasure Island, Parkmerced, Potrero Power Plant, Pier 70, etc., on top of numerous fill-in projects.

In big cities, this has been the trend for years, and people can choose where they want to live: in a new house further away, in an older house in the city, or in a new or older condo or apartment wherever it’s the most convenient for them.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“where there is now a shortage of homes people can actually afford to rent or buy, but a glut of homes people cannot afford.”

How long will it take for this to change, that is, these unaffordable homes become affordable? Years maybe?

Inevitable, I suppose.

Feels like never and probably will be never…I am being dramatic here and I know it suppose to take time but with so many stats and charts all pointing the wrong way and prices are still barely budging and there are still idiots out there buying somehow at least in certain “hot” California markets. It sure is frustrating seeing how prices are no where near the toilet yet with this kind of outlook, feel like the RE market and stock market can now just survive forever on hopium.

Majority of the sellers still time traveling and looking for prices from a year to 6 months ago and some are still getting them. Really feels like there’s no hope there for any potential home buyers looking to buy without over leveraging for a crap shack and add insult to injury with this level of interest rate even with a 800+ credit score and plenty of down payment.

Ground report from san diego: Although no perceivable change in price, the market has slowed down a lot here, home staying longer and better homes coming in and staying in, instead of bidding war.

A lot of price reductions in my hood.

If the mortgage rates stay high and go higher, I’d expect more fireworks.

Patience would pay but not a lot of people have it

just passed huge building of NEW sub-divisions in boomer retiree town of Green Valley

cement trucks, contractors and loads of lumber,etc.

of course we’re talking about few hundred homes for CASH BUYERS

I really wish that I could find some of these folks continuing to buy no matter how “hot” the market is. Because I really, Really REALLY wanna know what they do for a living, that they can afford to keep on buying right now

Sammy,

Since you REALLY want to know what these buyers do for a living; I’ll tell you about the woman who bought my brother’s house in April.

His realtor advised him to list the home for 849k even though that was about 30k above the Zillow estimate at the time.

When his buyer came to look at the house the first time, my brother was a little late in leaving so he got to drive past her Maserati as she pulled into the driveway. She offered 70k above asking and it was accepted.

What does this early 40s woman do for a living? She is paid 500k per year as a data transcriber for a hospital inputting the Medicare and Medicaid codes for the hospital to get paid.

Isn’t the hospital coding a shell game so that the patient can’t figure out the actual cost of anything?

I just had dermatologist remove mole

$1,000 for 20 min out patient

She’s married to a doctor. Transcribers do not make $500k.

I’m currently looking to buy. I been buying consistently for more than 20 years. I don’t buy homes to live in, flip or leave vacant. I buy them to rent. The income to pay cash for the new properties is generated by the existing properties. It is harder for me to find properties than fund them at this point.

Apple,

She is a single mother of a twenty something daughter. Not married.

“She’s married to a doctor. Transcribers do not make $500k.”

yeah that was my thought too, no way she makes $500,000 a year doing Medicare or Medicaid billing. That’s even more than most surgeons make. She must be married to a popular cosmetic surgeon in Beverly Hills maybe, and even then she probably has a lot of inherited family money and could borrow against it on the cheap thanks to ZIRP and QE, which is part of what’s fueling this stupid housing bubble. Healthcare costs in the US are ridiculous but that’s mainly due to the way health insurance works and the cost of drugs (the pharma companies are making bank), no way could she afford a Maserati on a biller’s income.

Medical auditor here. Nope, she is definitely not a transcriber and there is only one coding system, the ICD-10. At most you’re looking at $120k/year, $135k maybe, assuming you’re a departmental director with an RN and about six thousand initials after your name who’s been coding since the days of chipping into stone tablets. Cool story, but she’s either fronting or born wealthy.

As for the rest of us, I’m still on the market. The future of my current rental is on shaky ground so its either drop 6k on deposits for a new rental, or put the money toward the least trashy property in the garbage dump that is the current middle class housing market. Even overpaying–even catching a falling, rusty knife if you will– will work out much better in the long run, and I won’t have to worry about flakey landlords (increasingly flakey and inexperienced thanks to the new crop of clueless ‘passive income’ types) or not being able to keep my dogs. At my age, after 2 decades of renting, that all got old LONG ago and has only gotten worse.

Of course keeping a wise eye and negotiating like all hell, but the thought of throwing perfectly good cash out the window being yet another someone else’s tenant again and likely having to move yet again next year makes me physically ill. If I’m going to lose anyway, it will be for stability. Some of us can’t wait it out unfortunately.

I dated a girl for a short time years ago that did medical billing from her home. She worked 4 hours a day and sat at the local coffee house 4 hours a day.

VA loans and 15 year loans have lower interest rates. Just closed in September on a house in Hawaii with a 4.25% 30 year fixed VA rate

There was an article in Kaiser Health News (Funded by Kaiser family who were just into steel and maybe a bit guilty about what they helped start, i.e., “Managed Health Care”) by Eleanor Rosenthal, about 3-4 years ago. (PS: A Good mag!) It said if single payer health care were adopted on the Medicare model, over 2 million people in high paying (and totally useless) insurance related jobs similar to this lady (whatever she makes) would LOSE THEIR JOBS. (likely a LOT more now) When the Dems were in control, this is why we got the ACA mess (keeping the insurance corps in the game) instead of single payer, which they COULD EASILY have done.

Sadly, a lot of big donors to the Democratic National Corporation are from the health care industry, just like Republican National Corporation gets most money from fossil fuel and chemical industry.

Who wants more nightdipper rentier types around, anyway? Even if he is probably a lying troll just trying to stir things up.

Be patient. Seller anxiety is setting in. Look at the asking price drops.

There is nothing more anxiety-inducing than owning a vacant home that is falling in price and causing expenses such as RE tax, interest, maintenance, etc. Builders and second home owners are dealing wtih this now. Why make their pain your pain?

If you want to buy, I would plan on waiting 2 years to avoid losing a lot of wealth right away. Impatience is not a good virtue for wealth-building.

until we get inventory – like 5x what we have now

don’t expect much price action

“until we get inventory – like 5x what we have now

don’t expect much price action”

That’s coming online faster though, partially for uncomfortable reasons ex. COVID causing the loss of so many Americans (and millions more with long COVID). The US has had one of the most drastic drops in life expectancy in recent history, it’s now below even China and Cuba. And that’s led to a lot of homes becoming unoccupied. Even if Boomers kids inherit the homes, that just means fewer on the market as buyers elsewhere.

I hope Bobber AND Wolf are right. But unfortunately there are too many with too much money, who are not subject to the “economic logic” at lower levels……but that doesn’t get all the rich and STILL over consuming boomers (or younger) here off the hook, IMO.

Price drops like what I think you’re looking for take a long time to materialize, we’re not quite a year into this inflation crisis. You have to remember that sellers are not obliged to meet buyers at an agreeable price point if they can simply pull their property and hold it for the time being. They want to get paid and think there are better days ahead. So, the only way prices pull back is when a seller has no other option but to sell, or if they’re still ahead at a lower price and want to move the property. If people start to lose their jobs (recession) and/or higher interest and inflation start squeezing their budgets then prices may move lower. I say may because last time a lot of people held on until foreclosure and then often regular buyers were shut out from buying those heavily discounted properties, but I know someone who made out like a bandit picking up a penthouse in Miami dirt cheap, she was very flexible and bought it even though she was living in Canada.

On the positive side, once house prices broke downwards, there was a fllood of inventory competing to sell placed of the market. I could not believe some of the prices once that happened, and I also couldn’t believe how rapidly the inventory panic happened. Like one of the commenters has said here repeatedly, it only takes a few (dozen?) sales way below market price in a neighborhood to make that panic selling dam burst.

“Price drops like what I think you’re looking for take a long time to materialize, we’re not quite a year into this inflation crisis.”

Right, if history’s any guide here, it’ll prob. be around 4-6 years before home prices truly hit a bottom from this housing bubble, and there could be drops of not only 50%, but more like 60, 70, even 80 percent or more in the frothiest markets. That’s about how long it took when the Great Recession hit the country.

People/Sellers are used to high prices

They won’t sell until they have to.

But since home prices are fixed at the margin like stocks hone prices would go down.

You need to wait.

I saw somewhere San Jose off 11% from its peak. Seattle 9%. Others (including Austin) down 5% or a bit more.

Oh and Toronto off 19% from February.

Admittedly the sales prices in these cities are still very high but a 10% drop is not trivial.

Since the composition of homes bding sold in a city is always changing this would seem to, in some instances, make it a challenge to capture the true nature of price gains or losses.

Example:

For one month homes sell that have been flat for a while…its mostly the low end of the market though that sells (fluke) so it appears home values have fallen.

Next month the value of homes actually goes down a little (as best can be determined) yet the overwhelming majority of homes sold that month were from the high end of the market.

So it appears home values went up.

Again a fluke but it can happen especially as the samples (number homes sold) get smaller.

How is this sort of thing accounted for ?

Minimize short term trends yes.

I’ve seen this concern brought to light occasionally before. Am I missing something here ?

“Feels like never and probably will be never”

Hey, let me get your hope up! Seems like AirBnB owners are having a hard time booking lately and this might mean they will either lower monthly rates or take them off of AirBnB totally so they can rent them.

https://www.dailydot.com/debug/airbnb-booking-decrease-facebook-superhosts/

GOOD!

There are also some neighbor complaints about loud parties…..hope that slows it down, too. The only social good I see is if the renting party LIVES in the home and just rents a room to a kid traveling around the country…..kinda like a youth hostel.

And I’m still not sure how they beat the “running a hotel” thing.

We’ve only just entered a recession (despite claims to the contrary). Be patient.

yes, time will tell. and yes, years. but, it’s happening more rapidly than previous bubble deflating events.

locally in my western gateway tourist town (read conservative incomes), prices are coming down. It depends on how stiff/willfully ignorant a seller is, but certain single family starter homes are being reduced by huge amounts. $50k reductions on several <$350k properties and they're not moving either after weeks on market. I have hopes for a expedited "recovery"

3 years at least. The sellers in housing will need to learn the lesson that there is bid and ask. And sometimes there is no bid at all.

andy,

As a former stockbroker I like the last line of your comment. Even in the stock market there is sometimes no bid at all.

Sell Mortimer, Sell!!!

Ok, but to who

The housing market had a massive stroke and has not regained consciousness. Instead of providing first aid, the FED left it on the side of the road to die. More big rate hikes incoming, of the 75 basis point variety.

In a certain bubblicious town I’ve been following, the median hit $615k – a laughable number given local incomes. At Jerome Powell’s ludicrous 2.75% mortgage rate at the peak (valley), assuming 20% down, the monthly payment would be about $2,300. At today’s current rate of 7%, the person who used to be able to afford that $615k house can now only afford a $375k house to have the same monthly payment with 20% down.

The 20% down is actually pretty much fantasy, because almost nobody has it. 3% down, oftentimes borrowed and rolled back into the loan, is more likely.

This is why the housing market is laying on the side of the road blue. Rigor mortis will be setting in soon. This one’s DOA.

Not DOA enough apparently. Friend of mine showed me a a nearby condo in Ladera ranch, 1600 sqft sold for $783K. In talking to the previous owner, the new owner will apparently pay $6K a month (mortgage+tax..etc) not sure what kind of loan term is that. You really can’t cure stupidity at this level. The old owner made out like a bandit though and will move out of state and probably buy later.

You need knifecatchers to take the fall all the way down. But, ahem….

“The summer’s collapse in Orange County homebuying pushed the median selling price below $1 million and cut the number of seven-figure neighborhoods by six from springtime.

Since the spring’s peak, drops out of million-dollar status were found in Anaheim 92807, Anaheim 92808, Foothill Ranch 92610, Garden Grove 92845, Huntington Beach 92647, Irvine 92614, Ladera Ranch 92694, Mission Viejo 92691, and Orange 92867.”

Seems “Ladera Ranch” ain’t that special given the news earlier this month.

Why reach conclusions based on analysis of outliers? That’s FOMO behavior.

Housing prices are dropping. That’s a fact, so why get distracted by some bagholder who overpaid for a home. There are wide variances at the individual transaction level, but the downward trend is clear.

Bobber, you are the voice of reason. Much appreciated in our patience.

The home prices are just insane now. In Auburn Alabama, with a median income of about $23K, the median single family residence home price is about $425K. Explain that to me how that works, sustainably?

Hi Jeff,

Reventure Consulting had a Utube presentation maybe a week or so ago in which the average home sales price to earnings (sorry I forget if it was individual or household) ratio for various cities was examined. He compared it to its historical average as more desirable areas had a higher ratio it seemed.

The numbers you quote definitely would have resulted in one of the larger ratios if my memory serves me well.

Boise was one of the larger ratios.

I believe he used sales price but he might have used some form of average (median) valuation placed on the city’s homes.

I just don’t remember.

I failed to mention: the ratios in most of the cities were above their long term average. There were 3 or 4 quite a bit above, but he did present one that was in line with its long term ratio.

It might have been Chicago or some east coast city.

Definitely would not have been

anything near where I live, Pacific NW.

This isn’t new. Also, this looks like a national trend, rather than regional. Some may go first.

https://www.longtermtrends.net/home-price-median-annual-income-ratio/

If you look at price to income, this bubble looks super bad. Let’s hope the tighter lender standards will do what they’re supposed to do and just trap people rather than a wave of foreclosures.

@JeffD Geo-arb from more expensive locals. In the area we are looking in the south, buyers are all from NYC, Boston, PA, Chicago and of course California. Our target market is up 50% since 2018-2019. Lots and lots of cash buyers dumping $1.5MM condos and buying beautiful high-quality homes on GC for $350,000 to $400,000. I the houses we have targeted cost the same as a downpayment on a comparable home in SoCal. No place is perfect.

Say the same thing in Spanish Springs north of Sparks-Reno. Low median HH income and $700,000 houses, but the buyers were from out-of-state with many California transplants.

“Rigor mortis will be setting in soon. This one’s DOA.”

In a country completely owned and locked down by the rich , there’s going to some real sleazy tricks emerging …… stay tuned.

I think it is nearly impossible to get off the crack once you go down that road. The landing is not going to be soft. My understanding is monetary crack by central bankers is supposed to be for a year or so, not for a decade.

Now Powell got religion and is going to fix it all in a year. I think there is something big going on behind the curtain. Russia, China, Great Britain, IMF, World Bank, ECB. Geopolitics, monetary policy and fiscal policy plots all around. Powell fighting MMT crowd? Drill baby drill fighting Net Zero crowd?

I think the bad news has been successfully kicked until after election. Winter is looking like when we are going to “soft” land this plane.

Do you read wolfs articles = no way out for fed ,until interest rates are at least 12% . Then we have friends Russia,China,Iran,North Korea maybe India trying to strangle USA .Not feeling good about world or economies

I don’t think any country is trying to strangle USA.

They are just looking at their own interest than toeing the line with uSA.

It’s pretty obvious now, re BRICS etc etc etc , that a majority of the world’s population is now totally tired of “being strangled” by the USA ….

Russia, China, Iran, and North Korea are in a bar somewhere drinking hard liquor, laughing, and watching America self-destruct on a huge TV.

I remember reading articles a couple of years ago mentioning private equity firms like Blackstone were buying residential real estate during the last housing bust at deep discount prices and turning them into rentals. Blackstone alone owned $300 billion in real estate (if I remember correctly). I guess it doesn’t matter if they paid cash or mortgaged them because even if they financed 70%, the interest rates had to be extremely low. For this reason, I would think the current housing bubble will not hurt them, especially if more people are renting. However, I am thinking they could really destroy real estate prices if they decided to trim their housing inventory. In lieu of doubling their profits, they could afford to sell their inventory at a 70 or 80 percent profit. That could put pressure on people who bought one or more houses and are not in a position to take that much of a hit. What I am I missing Wolf? :)

It is unlikely that BLKROCK would pay cash when they can borrow money directly from FED and most likely created some type of Mortgage Backed Securities package and sold it back to the FED or sold it off to other institutions. Rest assured, BR knows how to leverage capital.

They are not likely to be impacted significantly, most likely not at all, by turn down in the real estate market.

They could sell 10% of their holding at below market value, creating insanely low comparable listing prices, sink home prices for the area, cause a sellers panic, and swoop in with Fed money buying everything at a deep discount. There’s your mother of all hedges.

That’s what they said about Bern Stearns, Lehman Brothers, Wachovia, Washington Mutual, Citibank, etc..

Wait a minute, is Citibank still around?

“They are not likely to be impacted significantly, most likely not at all, by turn down in the real estate market.”

The rich never are impacted in a society they own “lock, stock, and barrel”.

Right down to the government, The Fed, and all the media.

And that, my friends is the real story today concerning America.

Did you wolf say they bought properties in Spain,then everyone just squatted in them .police couldn’t get them all to leave ,then gave up.Blackrock sold at a huge loss,karma couldn’t happen to a bunch of nicer people

Nah…..Blackstone will not crash the market. From Blackstone site, we should be thankful to them for pulling us out of the housing market swoon.

”

Blackstone’s role after the 2008 housing crisis

Following the subprime mortgage crash, Blackstone swooped in on the mass amount of foreclosed homes that were selling at a low rate. They used this opportunity to prop up pricing for the sake of the overall market.

Some people credit Blackstone for balancing the market during a time when prices would have otherwise remained low. Now, the situation is reversed. Prices are massively high and Blackstone’s involvement could teeter the market even more toward high prices.”

Agree with Depth Charge. A simple comparison of median income buyer affordability and median house price at any level – national, state, county etc. – shows that there is a huge gap which is unsustainable without another round of stimulus. At national level price is down to $389k but the median income buyer barely affords a 250k house. That is even assuming excellent credit and minimal debt. An average buyer affords more like $210k at this point. And 210k is a 50% drop from peak of 420k nationally.

Just a function of time. One can live in la la land for only so long.

la la land is crazy. I was at visualcapalist site and they had a graphic of the average salary you need to buy the average priced home in 50 cities. Of course San Jose and San Fran were above $300k, If you look in the midwest and the south east there seems to be affordable housing. 4 or 5 cities were in the $50k range and 26 cities were under $75k. Honestly it did see a bit low but I do have a 3bd rental that would probably sell for $140k. 4 years ago it would have sold for $70k. LOL

Blackknight August report has indicated there has been over a 10% drop from peak home prices for many west coast cities. I suppose that drop will be bigger in the September report. In the Midwest, the drop has only been about 1% to 3%.

Here is an excerpt from the report:

“- According to the Black Knight Home Price Index (HPI), median home prices fell 0.98% in August, only marginally better than July’s upwardly revised 1.05% monthly decline

– July and August 2022 mark the largest single-month price declines seen since January 2009 and rank among the eight largest on record

– The monthly rate of home price decline is now rivaling that seen during the Great Recession – the question is how long it will continue to do so, and how far off peaks prices will fall”

I am from Seattle so I can confirm the drop in my area. Median sale price is now 870k down from 995k two months ago. And for higher priced houses, many have seen a 30 percent or greater loss. I am looking at a house right now which is sitting on the market for 1.1M when similar houses in that area sold for 2M in March. And that is a 700k house to begin with. It should never have gone to 2M.

NW wildfires surely not helping Seattle RE.

Ditto here in Spokane other end of the state. We get smoke from every direction: Idaho (more fires than usual this year), Western Oregon, Washington North Cascades and North Central Washington (every single year for the last 5 or perhaps more years) and some years British Columbia and California.

If you live here and you don’t know what AQI stands for you must be very very busy with work or something.

Prices just don’t seem to be dropping around my neck of the woods. Every new listing just makes me shake my head.

Crappy (in the eyes of this beholder) starter homes for 300K in flyover country. Whuuuuut? Oh lookie… “Luxury vinyl plank”.

Good grief.

Off topic, sorry, but I think Tesla will set some kind of record tomorrow in daily trading volume. The dollar amount could be a crazy number like $50 Billion.

Andy, you’re gambling….

Not at all, actually. Sitting tight.

It will be interesting to see what happens. I bought this dip all the way to $208 and think long term will be good prices, but I don’t trust it’s done dropping. I’ll likely sell the next pump, assuming their is one.

I think there’s a flaw in comparing the median house prices to median income since buying a home is not for every income level.

My guess is that it makes more sense to compare median house prices to top 35% income or something around there.

Not historically. Take any point before march 2020, and you will find that median income buyer has always been able to afford median price house except bubbles like 2007. And I expect that in a balanced market. Buying a house is for every income level. There is a house for every level, you may not like the house but it does exist. We haven’t reached a point where houses are just reserved for the rich.

I don’t see any reason why it would not return to that level of stability once stimulus is out of the system.

“We haven’t reached a point where houses are just reserved for the rich.”

I think we’ve reached that point now, and agree it’s not sustainable or healthy for the housing market.

If your premise was accurate (which it isn’t), then it means that the pool of potential buyers is lower than ever which means that prices are still more overpriced than ever.

I state “more than ever”, as it is obvious that in the past, the percentage who could afford to both quality for and afford the median priced home was higher or a lot higher than the top 35%.

HawaiianKing,

Only if you don’t care about revolution, as the people overthrow the government.

If you buy now there’s a very good chance you will be able to refi later at a lower rate, and of course prices are down. The housing shortage prefigures a growth in population, and open immigration policy. And as long as wages are climbing you can look forward to paying a fixed rate with your rising income. This period looks a lot like the 1950s, inflation, growth, and the Fed working off old debt. The real inflation didn’t hit for another 20 years, which might also be the case here. The deflation bogey, systemic collapse, is going to be met with liquidity liquidity liquidity. Money might not be worth much but there will be plenty of it. Investment decisions refer to the inflationary macroenvironment and are not difficult.

“If you buy now there’s a very good chance you will be able to refi later at a lower rate”… if you can live that long. It’s looking like we are beginning a new cycle in the bond market. If so, the wait for lower rates could be many years or even decades.

The best middle class, blue collar investment for the last 100 years has been a house. (the rich often overpay for their amenities) Technology is the real threat to home values, you can live off the grid, and innovations in materials and labor (3D) all make the frame house and the 16oz framing hammer a thing of the past.

No, not unless you do it soon, as in the next few years. The bond bear market is about 30 months old now and due for a pause at some point, probably sooner than most think.

After that, I’ll repeat it again. If the interest rate cycle bottomed in 2020, rates are destined to “blow out” past the 1981 peak.

Even on this site, most posters who express an opinion share the implied fantasy that there is going to significant financial stress but that magically, it is temporary and somehow someway American living standards will emerge on the other side mostly unchanged.

That’s not going to happen. We’re in the biggest asset and credit mania in human history, right now. The only reason Americans can supposedly afford current artificially inflated living standards is because of a fake economy from government deficit spending, fake wealth from an asset bubble, and the lowest aggregate credit standards ever.

The end of this mania is going to be life changing where the majority of Americans are destined to become poorer or a lot poorer over the indefinite future. Reduced housing affordability and lower housing prices are just one outcome.

:..destined to become poorer or a lot poorer..”

I think this already happened. The poor do not stand in line for the latest iPhone X anymore; they moved on to online ordering Tesla 3. As counter-intuitive as this sounds.

I’m referring to a much larger segment of the population.

If you have never seen it, look at changes in net worth and incomes over extended timeframes. I’ve posted about the 21st century but if you go back to the 60’s, it’s evident that much (if not most) of the wealth of the top 1% (or 5%) isn’t the result of a much wealthier society.

Assets that used to sell for far more modest prices now sell for hugely inflated prices due to expanding credit, as in a multiple of dozens to hundreds. Some of it correlates to inflation but not all or even most of it.

A home should be a place to live. Not a speculative investment, which it has now turned into. It’s turned into the latter by way of the greed and moral decay of much of the population and media, who believe home appreciation is a sign of wealth. It isn’t. If you want to speculate and gamble there are plenty of ways to do that. Sports betting, casinos etc. Sorry to say, this is not going to end well.

Sometimes I wonder if your comments are written by a faultily programmed bot that just lines up words that appear to make sense but don’t. Your emails, on the other hand, are always lucid. I don’t quite get it, tbh.

Booked business at my Fortune 500 has been -5% YoY or more for a few weeks now. It was 30%+ in Q1. That’s $10s of millions less that large companies are willing to spend this year vs last year. That eventually starts hitting S&W which usually means lay offs at those companies and further down the line, my company.

Prices will have to come down just due to competition of supply. buyers will only dry up more not even factoring in rate hikes and prices will need to follow. Be patient my fellow millennials.

Wolf – excellent work on deflate the myth of housing shortage and underbuilding. If the population is barely growing why must housing stock increase at 4 or 5 times population growth, or similarly high unrealistic multiple? I argued against the existence of the so called housing shortage before the meltdown of 2009 and during the runup to 2021.

US does not have a housing shortage. The RE industry advocates and spreads unsubstantiated claims of housing shortage when such facts are not supported by data. One can argue that a housing shortage exists if ‘shortage” is defined as not living in the house of one’s dreams – 7 bedrooms, 10 bathrooms, game room, media room, beachfront, price, $5.0mil. If one lives in a house commensurate with his/her income, no house shortage exists.

So no housing shortage exists, rather personal income deficiency exists.

“If the population is barely growing why must housing stock increase at 4 or 5 times population growth”… It’s not unreasonable because:

1. Weaking purchasing power in the general picture that outruns salary increases.

2. Private investors and firms need such return for their book to ride up the stock and so forth.

3. Also as houses build further and further away from locations like downtown for example, better spots are taken, while more open spots are worse in terms of location/convience.

There’s plenty of vacant lots in the inner cities in the Eastern United States as well as the Midwest. There are even “cheap” homes available to those that don’t demand a palace of granite and marble on a barista’s income.

But those come with compromise that many are not willing to make.

To offer a reasonable picture of the housing market, your first chart should include an estimate of units lost to demolition or other destruction. If the average unit lasts 100 years, that’s 1% annually.

That 1% would only make sense if there was no growth in homes from 1922 to 2022. There are 150 million housing units in the US, so 1% would be 1.5m, when demolitions is typically 150k to 300K. But I think it is highly unlikely the garbage they are building today will last 100 years.

Depends mostly on the level of maintenance JS:

An old time ”land lord” told me 50 years or so ago to figure 10% of value of property for ”proper” maintenance.

He claimed ALL of his properties got that, and were in just as good shape as when he purchased them, including some 50+ years old at the time.

We live in a hood built out in the late 1940s, early’50s, and while some houses are absolutely ”tearer downers” others are just fine, with updates to exteriors clearly seen, etc.

REITs overall are down ?about 33%. How low do you think the REIT index will go down? ? invest now some amount, cost averaging monthly over the next ten months, or wait? Some smart aleck probably will respond that I need to invest monthly for 60 months to break even.

My guess about 240 months look at Japan ,the fraud game is OVER

JGBs recently had a string of days with no bid. Coming soon to a govt near you. That’s the indicator to watch.

Scary

Combine that with a sinking currency and it’s the end of “can kicking”.

“And some folks try to get some tax benefits by converting their vacant homes into vacation rentals.”

This may be turning, as well. AirBnB is having troubles as of recently.

I could never understand AirBnB business model. In place of hotel you go into stranger’s home. And it’s not like it’s cheaper. I get Uber, but not AirBnB.

Right. I have never stayed in an Airbnb, and I never would. When I pay for expensive accommodations, I want room service, fresh linens, no cameras, etc. I don’t want to go to work cleaning somebody else’s house.

Airbnb = real estate speculator desperately trying to cover the nut

You and the statement above are simply ignorant. Vacation rentals are much less expensive and have significant amenities not found at hotels, primarily privacy. I’ve been using VRBO since inception and love it, just like tens of millions of others which is why they’ve done so well.

My daughter gets TDY all over the U.S. and uses Air BnB’s / VRBO for her housing. The catch is that you have to stay longer than a few nights. The $150 – $200 cleaning fees are a deal killer for me on anything shorter than a week and with multiple sleeping accommodations to spread the cost is a must.

The one I will never understand is a motor home. For the few weeks out of the year that you use it, it just doesn’t pencil.

do you travel alone?

If I get away from my hot Asian girlfriend. Which is not often.

@andy

So I guessed.

When you will travel with kid(s) you will feel the difference :)

touche :)

I was a part of three households sharing an AirBnB at Hilton Head.

It was well worth it to share a kitchen, have far more room than a hotel with no kids running down the hall, a private pool, and still be on the beach with an amazing view.

If it were a business trip, a hotel would be a no brainer. However, a week long stay on the beach with other families? Renting a house was a nice touch.

It all depends. When reading Bletchley Park decrypts at the UK National Archives I stay in the spare bedroom of a lovely couple’s apartment less than a quarter mile away. Half a mile to Kew Gardens station and several excellent restaurants, a quarter mile more to several more. A quarter mile to a shopping center with Marks & Spencer. Less than a hundred dollars a night. There are several somewhat larger alternatives nearby for a little over a hundred. This is a quite upscale suburb of London, about 40 minutes by train to the city center. One stop down the line to Ted Lasso’s Richmond, very upscale. Cheaper, quieter and more convenient than the hotel I stayed at on my first trip there in 2016.

AirBnB is down only 30% YTD

Only -47% since Fed 2021

Love your typo: FED 2021 instead of Feb 2021!

I would love to see Airbnb crash and burn and the houses that have been converted to resort rentals re-enter the long-term market for regular people who are now living in tents and RVs – a lot of resort towns in my area can’t get or keep the people who make a place civilized because they can’t find housing or it’s too expensive (nurses, police, teachers, etc.).

Odds are the resort rentals will still be unaffordable to locals of limited income. This is not a new phenomena. Places like Jackson Hole and Lake Tahoe have been like that for more than a decade that I know of.

Bend, OR’s nickname in the 1990’s was “poverty with a view”.

Really would hate to be a first time homebuyer in this market. To have to sit around and choke on a few more years of rent in hopes of a major decline in housing prices sounds less than appealing to me. Better off waiting 10 years to pay off that 100k in student loans and maybe another 5-10 years to save for that down payment. By then the average life expectancy will reach parity with the baby boomer generation and housing inventory will be at all time highs. Hang in there and be patient!

Off topic but noteworthy.

I removed the link. Violation of guidelines: one-line tease plus link. Not gonna happen.

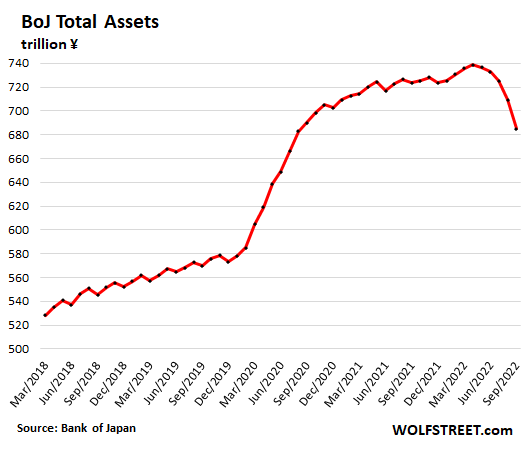

But I want YOU to know that the media always hype the BOJ’s “bond purchases,” if any, without ever looking at the actual purchases and the balances sheet. Here is the BOJ’s balance sheet. Details at the link:

https://wolfstreet.com/2022/10/07/shock-awe-balance-sheet-reduction-at-the-bank-of-japan-assets-drop-7-3-from-peak/

Read this yesterday news.

“Home Buyers Flock to Florida Cities Devastated by Hurricane Ian”

Too much greed and money sloshing around. Lot of people from out of fl state trying to capitalize on it.

Thank you. WSJ article … I wouldn’t have believed it, but there it is… buyers rushing in looking for distressed properties.

Obviously, we are nowhere close to a bottom yet.

Oh, By The Way… Rick Scott’s house is 12 inches above sea level.

Re: FL properties:

Wait until they try and insure their trophy. There are stories about people who have a moderate home with insurance bills of $7-8K on their last renewal – and that was before the last storm. The insurance companies are also requiring roof certification, nothing older than 15 years, and they must have storm shield (not tar paper) underlayment or they won’t write a policy.

Wolf you have spoken for some time about the glut of housing that is available but do you have any data sources you can share to show this? I’m a certified RE appraiser in Oregon and while inventory initially went up 4x, it’s plateaued at 2 months which is not even balanced. We’ve seen lots of price reductions and the median sale price come down a bit, but there is no glut of homes in any of my markets. Appreciate any data you can include.

You’re not a “certified RE appraiser,” you’re a “hit-the-numbers hack” who had as much of a hand as any in this speculative bubble which is now in full collapse mode, and now you’re living in a state of denial. Hope you saved your money, because it’s curtains.

You went beast mode, but I say that is needed in these crazy times.

Harsh but true.

Sorry angry old guy, I’m not your whipping post . Your comments are incredibly ignorant and misguided. I’m the only thing between mass manipulation in the market, but when people with more money than brains pay $400k over ask for a LP of $1.8mik and waives the appraisal and inspection like over 25% of people did in the last 2 years, that causes the issue we have. When investment firms come in and buy their 60,000 unit of property that gets traded on the NYSE with no appraisal, that’s what’s causing this situation. When Trump handed out $15 trillion in free money starting with his cronies, that’s what started this situation. You are likely old enough to recall the SNL debacle but are likely to dumb to understand it, but that is why my career exists. O never said anything about the market staying propped up, but you can’t wait to make a rash judgement on here to entertain your would be club house wanna be cronies, but you just got checked you loud mouth punk.

RTGDFA…..

Dano,

Don’t you read my articles about the glut of new houses? New houses in inventory, available, for sale, and on the market, most since Housing Bust 1. I’ve been showing you the progress here for a long time:

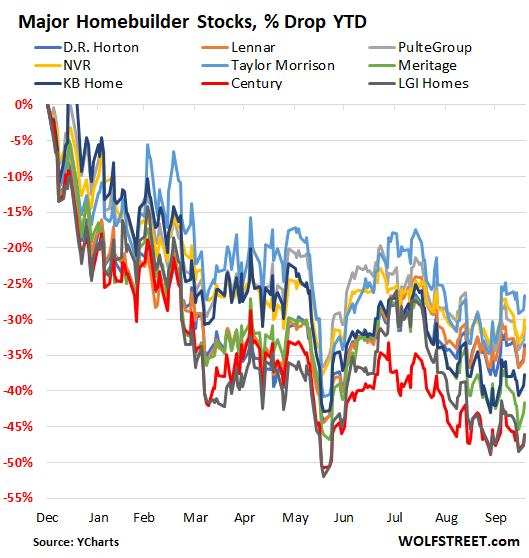

And Dano, do you ever look at homebuilders stocks, down 26% to 47% YTD:

And Dano, here is the traffic of prospective buyers reported by homebuilders:

Dano, I can’t repost all the article I’ve written about this issue, and all the data and charts I have shown you. You just have to go find an read the articles. You can find them here:

https://wolfstreet.com/category/all/housing/

Yes I read them all, but where is this data from? I know sentiment is poor and I personally think housing prices will be much lower in a year. As I’ve stated, my local prices are declining but inventory isn’t coming up, not in several months now. I think you and that other grumpy old guy above misunderstood what I said. I’m simply asking about inventory and it’s source. No appraiser in any state I speak to see these types of inventory increases. Your stats above that show housing increases do not show how many months of inventory there is in the nation and not sure you can even do that with those numbers. Each market is different.

You’re probably doing RE sales as your main profession and masquerading it with this RE Appraisal gig. Always hyping the market creating illusions of shortages when there ain’t none.

Depth Charge is right on the money recommending the dude above “saving his money because it is curtains.” We’re in the RE Appraisal business here in the Swamp. There is no business whatsoever. The market is dead. No refis, No sales, No listings, NOTHING!.

What ever happened to Network Capitol Funding, in Irving Calif? There are probably out of business like many other mortgage lenders waiting on deck to join them.

“In big cities, this has been the trend for years, and people can choose where they want to live: in a new house further away, in an older house in the city, or in a new or older condo or apartment wherever it’s the most convenient for them.”

The trend I am seeing in my area is these mutli-unit building going up are only rentals. During HB1, developers were building condos for people to buy and also they were converting Rentals to Condos that could be purchased. This time it is different and just all rental. I know people who would like to buy a condo downtown which is experience big growth but everything is rental.

FYI. I just happened to read a report on sfplanning.org and it said 65% of people rent in San Fran. I did not realize so few people owned their property in San Fran. Maybe that is the case with most big city downtown areas. Are most of the new multifamily units being built rentals units?

You’re surprised 65% rent in SF?

Where are they supposed to get the money to buy at these insane prices, even when mortgage rates were 3%?

I used to live in Midtown ATL which covers 1.7SSQM in the city core. There are SF homes but most of it is condos and apartments. I don’t remember the specifics but the reported incomes for this area made it difficult for someone to qualify to buy, even though prices are a lot lower versus SF.

Based upon the reported incomes, my guess is that most have roommates, either “attached” or not.

Wolf where do you get the “people sitting on vacant homes theory?” I am a housing bear, but I have only seen data that shows housing units (rental and owners) are pretty filled and have historically low vacancies. Do you have any data to back up your theory?

https://www.census.gov/housing/hvs/files/currenthvspress.pdf

The Census data is total BS. No one knows how to count “vacant” units by surveys that are sent to the vacant units. There isn’t even a consensus what a “vacant” unit is. According to your Census chart, the homeowner vacancy rate will be negative in 7 years, which would be a hoot and prove my point, which I have made for years, that the Census vacancy rate is BS.

New houses in inventory, available, for sale, and on the market, most since Housing Bust 1:

Just because a house is for sale doesn’t mean it is vacant. And even if it does 500K over 150m housing units equals = 0.3%, so maybe the census isn’t such B.S. If you don’t have any data to support your hunch, I think you should stop claiming it. That is if facts matter anymore, or is this just another opinion/feelings blog?

John Stotes,

“That is if facts matter anymore, or is this just another opinion/feelings blog?”

For example, according the Census Bureau’s OTHER data on vacancy rates, based on the actual census in 2020, the vacancy rate in the US was 9.7%, down from 11.4% in 2010 during Housing Bust 1.

https://www.census.gov/library/stories/2021/08/united-states-housing-vacancy-rate-declined-in-past-decade.html

You RE trolls are a handful.

Go onto Zillow’s website and view the photos of a random sample of homes in some area. You’ll find many are completely empty, and many others are look very much “staged” with rented furnishings and wall art. Homes with people actually living in them usually show signs of being lived in. Not as picture-perfect as a staged home. Exercise equipment and cheap sofas in the basement, etc.

There’s quite a lot of homes in my area that look vacant by those criteria.

Hi John,

Dont recall where I read it but it stated that

1. 59.x% of housing units were owner occupied

2. 30.x% of housing units were rented

3. 10% of housing units are vacant

Don’t know what their exact definition of vacant was.

I live in Spokane Washington. About a year ago, maybe less, it was stated that the rental vacancy rate was less than 1% here. This may still be the case although I’ve heard they are building apartments here.

A woman was transferred by the military here (or she was just enlisting ?), again maybe a year ago, and she had considerable difficulty obtaining an apartment !

A local free newspaper wrote an article detailing her plight. Took her 2 or 3 months (longer ?) with assistance to get a blasted apartment.

Ridiculous, but true. I rent.

I have seen charts from Wolf and Reventure Consulting indicating the rate of apartment construction is as great now as it has been going back to the 70s or 80s.

There is no housing shortage in the US, not how most people think of one. In most of the world, most people do not live in their own housing unit, especially of the size in the US. The only other countries where I know US type housing is or might be common are Canada and Australia.

As Americans become poorer or a lot poorer, they will double and triple up.

This will definitively end any supposed housing shortage.

This is exactly where I see things going for our country. In my SoCal neighborhood, I see no glut of unoccupied houses waiting to go on the market. The only empty houses are the very few that are for sale. The bidding wars are gone and the mania has softened, but I still see houses routinely going pending 1-2 weeks after listing for $550k-$750k. Only the junked houses or houses priced way over comps are sitting. I moved into my neighborhood in late 2019 and there were almost no cars parked on the streets. Now as families pack 6, 8, 10 people to each house, you can’t find an open parking spot along a curb in the afternoons here. 3-4 cars per house is the norm now, and 5 is not uncommon.

There’s still just way too much cash sloshing around. We increased our money supply by around 40 percent over a couple years, and house prices rose in lock step (big surprise /s). House values didn’t go up, Americans are just getting poorer, robbed of our wealth by currency devaluation. The idea that house prices HAVE to collapse due to affordability is bogus… The vast majority of human beings around the world can’t afford to buy a big house for their immediate nuclear family in their country, so they live in larger extended family units and pool resources to keep a cramped roof over their heads.

It would be nice to see average household formation broken down annually in the chart. It’s not like there are only 1.2m permits available with a waiting list.

We know there was a lost decade of college grads not finding work and living in parents basement. Or did they all make up for lost time the last five years..

Household formation can and will reverse.

As the asset and credit mania end and the housing bubble with it, it will decline noticeably or even go negative.

it is a lagging indicator.

Good point AF:

Last time we lived in FL, there were 3 houses across the street from us; when we moved in, early 2004, one house had two couples with six children, others had two folks each.

By time we left, late 2006, first one still had 10 people, others each had 12-14 people living in them.

All three were relatively small houses.

SO, question is, what constitutes a ”household?”

Current hood, all ”working class” from what I can see, has many homes with 3 or 4 apparently unrelated folks, and a some single folks living alone, including one 96 yo who looks and works as though 56ish.

Same question, what constitutes a household?

Wolf, always enjoy your articles. Note there is a typo “69,3654 housing units”. surprised no one commented on it.

Thanks. Yes hugely huge boom going on in here.

Investors will set the bottom in the coming market. I don’t expect home prices to drop as much as they did in 2008. Investors will enter the market when they can get 6-7% ROI. A key point is the cost of renting relative to buying is higher now than in 2008 and this is directly related to what an investor would consider Fair Market Value (FMV=NOI/CAP). Home prices need to drop less now than in 2008 to draw investors into the market and that is when the bottom will be set. What makes this all work for the investor is that rents don’t go down. Rents may stabilize at a level for a while but they don’t go down over time.

Rents can and will go do down dramatically if there’s a recession.

And in many areas (Silicon Valley), it’s much cheaper to rent than buy an equivalent home.

No surprise here. Having gone through 08 with our business,

this was easy to predict that housing would be in recession by fall.

No debt this time around personal/business. Fishing gear is ready

for Florida. Been a great fall for hunting. Freezer, and canning …the cupboards are full.

This will not be contained to home construction & sales. From retail – manufacturing in my little slice of America the breaks are getting slammed.

Hi Wolf,

But what of Dano’s 2 months of inventory ?

Sessa Realty does very good presentations of the Toronto RE market. Down 19% from February peak, it had quite the run up.

But in his most recent Utube presentation in Toronto the inventory is only 2 to 4 months. And he was seemingly reluctantly calling this a balanced inventory. Well that’s what I gathered. But balanced is supposedly like 5 to 6 months. I think he just felt compelled to call it balanced even if …historically… it isn’t.

Sort of because well how could it be a sellers market, i.e. only 2 to 4 months inventory, if home prices are down so much ? Other factors obviously, very high prices relative to local incomes being one I guess.

Well for all i know maybe 2 to 4 months inventory will become the new “balanced” ?

Makes sense I suppose considering so few

buyers can now qualify… limited supply becomes much less relevant.

And, over here in the UK, peddlers of homes and their accomplices, the finance industries, are declaring that now is a golden opportunity to buy. Not only do they parrot the “Shortages of Homes” myth but compound it with the “Housing Ladder” imperative.

When one climbs a ladder it is usually necessary to climb down it.

People are still dying. Probate will lead the housing market lower.

And people are still being born and there is immigration as well.

They aren’t forced buyers.

Look at that 10 year yield.

Whohoo !

Must be the Japs dumping their treasuries.

And the chinese.

And the Saudis.

And – everyone.

Jay will have to go big just to keep up with the Jones’es.

Soon – when greed turns to fear – the last thing anybody in the “housing market” will care about is price. It will be a fire sale – without the fire.

“Must be the Japs dumping their treasuries.”

Nah, it’s 8% inflation. And there’s a LOT more inflation where you live. So do some navel gazing.

I can’t wait for the yield to go high enough to where I want to buy 10-year notes. If yields go high enough, I might give the 20-year and 30-year a good look too.

Rising yields are a GREAT thing for future bond buys, after the hell we’ve been through.

BTW:

Japan’s holdings fell as it’s selling dollars and buying yen to prop up the collapsing yen.

China’s holdings increased

Saudi Arabia’s holdings increased.

The entire foreign holdings, at $3.9 trillion, are relatively small — just 12.6% of the $31 trillion in total Treasuries. The remaining $27 trillion are held by US entities.

Inflation does not sell bonds

Eliminate the tax deductions on selling a house…

The $500,000 tax free deduction only helps wealthy individuals.

I am tired of hearing from home builders that say they can only make a profit building McMansions.

Go get a job at Taco Bell and soon you will find a way to manufacture homes, mortals can afford.

How much of the profit that a company like Blackrock reports, simply be a reflection of bad tax code policy?