Holy-moly mortgage rates of 7% slash demand for new houses due to super-inflated prices, but prices are now coming down.

By Wolf Richter for WOLF STREET.

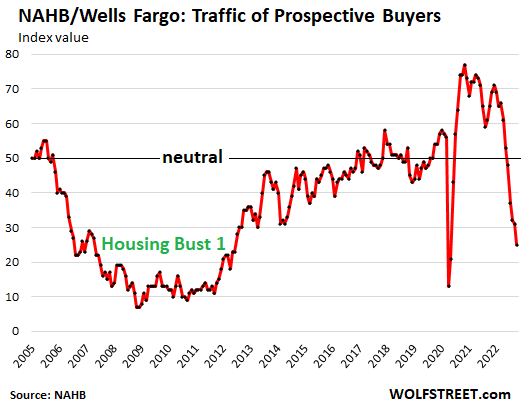

Traffic of prospective buyers of new single-family houses plunged to the lowest since 2012, excluding the two lockdown months April and May, and is now approaching even the levels of those two lockdown months, according to data today from the National Association of Home Builders.

The NAHB index for traffic of prospective buyers dropped to 25, about where it was in mid-2007, well on the way down into Housing Bust 1. From 2008 through 2011, the index hovered around 10. Only this time, the descent is happening a lot faster than in 2005-2007:

Traffic is a sign of interest among potential homebuyers, but many of them lost interest amid still sky-high prices and holy-moly mortgage rates of around 7%. The response from homebuilders is to reduces prices and offer incentives (including mortgage-rate buydowns, anything to avoid the stigma of a price reduction).

The overall confidence of builders of single-family houses fell for the 10th month in a row in October, as “rising interest rates, building material bottlenecks, and elevated home prices continue to weaken the housing market,” the NAHB report said.

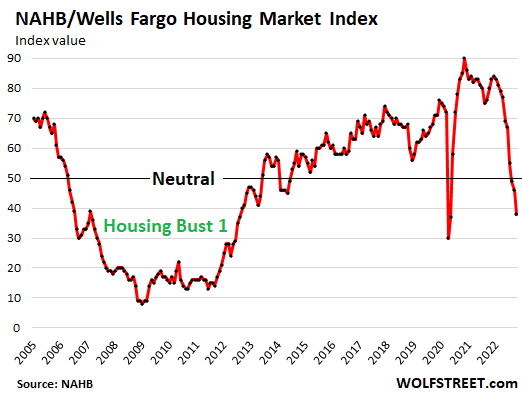

With today’s index value of 38, the NAHB/Wells Fargo Housing Market Index is now nearly where it had been in May 2020 during the lockdown, and below where it had been in February 2007, on the way down into Housing Bust 1.

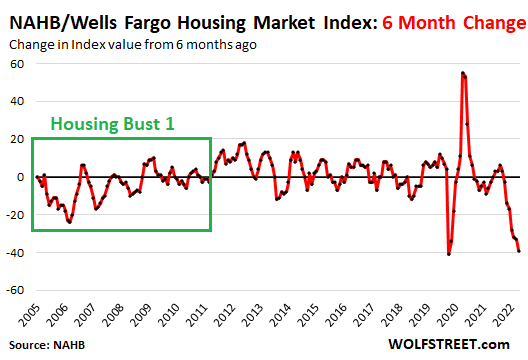

Current descent much faster than during Housing Bust 1.

From April this year, when mortgage rates began to bite, until October, the index dropped by 39 points in six months (from 77 in April to 38 in October).

When Housing Bust 1 took off for homebuilders in October 2006 (index at 68), the index dropped in six months by 17 points. There was never any 6-month period during Housing Bust 1 when the index dropped anywhere near 39 points. The fastest drop was 24 points in the 6-month period that ended in September 2009.

The current 6-month drop now nearly matches the 6-month plunge through lockdown April 2020:

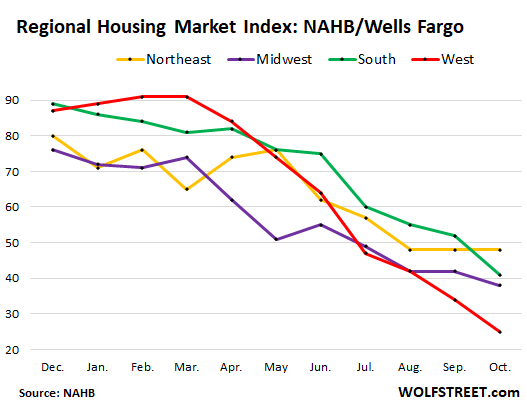

Home builder confidence by region:

The NAHB’s regional Housing Market Index plunged the most and the fastest in the West (red line in the chart below). From its high this year in March (91), it plunged by 66 points in seven months.

The speed of the descent: Since December:

- West: by 62 points (red)

- South: by 48 points (green)

- Midwest: 38 points (purple)

- Northeast: by 32 points (yellow).

The NAHB index for current sales dropped by 9 points to an index level of 45, the eighth month in a row of declines. This means that more builders rated current sales as “poor” rather than “good” (50 is even).

The NAHB index for future sales dropped 11 points, to an index level of 35, the lowest since June 2012, coming out of Housing Bust 1. And on the way down into Housing Bust 1, the descent reached that level in July 2007.

Price declines.

Homebuilders can improve sales by cutting prices and by using various incentives and mortgage rate buydowns (when the builder subsidizes the mortgage). Homebuilders cannot just sit on the homes they’ve started building or have already completed. They must sell them one way or the other.

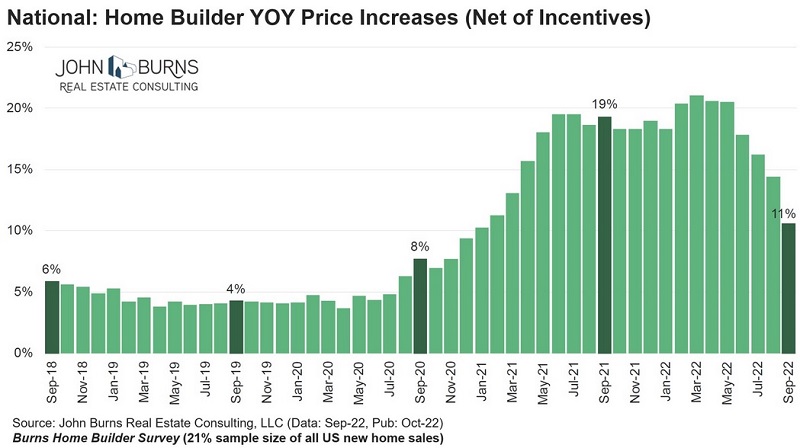

According to the Burns Home Builder Survey for September, by John Burns Real Estate Consulting, prices net of incentives had started to decline from month to month in late spring, with year-over-year price increases falling from the 20%-range in May, to 11% in September.

“Very likely this chart [of year-over-year price changes net of incentives] ends the year flat to slightly down given market momentum we’re picking up on the ground, tweeted Rick Palacios Jr., Director of Research at John Burns (click on chart to enlarge):

Holy-moly mortgage rates.

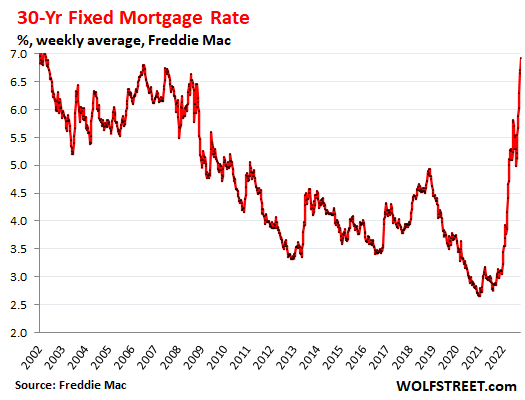

The average 30-year fixed mortgage rate rose to 6.92% last week, the highest since February 2002, according to the weekly measure by Freddie Mac, which was released last Thursday, reflecting mortgage rates earlier last week. The daily measure by Mortgage News Daily has been just above 7% for days.

“Holy-moly mortgage rate” is my technical term based on the utterances potential homebuyers make when they see the mortgage payment of the house they’re trying to buy at these still sky-high prices.

Sure, rates were a lot higher back in the day, say in the 1970s and 1980s, but home prices were a whole lot lower compared to income levels. So I can’t say that 7% mortgage rates are no big deal because my first mortgage was 8% in the late 1980s, and it was just fine. And others who’d bought their home years before with a 15% mortgage, and came out of it OK, can’t say that 7% today is no big deal.

High prices and high mortgage rates don’t go together – and prices have been inflated to ridiculous levels amid years of the Fed’s QE and interest rate repression, which are now unwinding.

At today’s sky-high prices, the 7% 30-year fixed-rate mortgage does a job on home sales and on prices, as we’re already seeing.

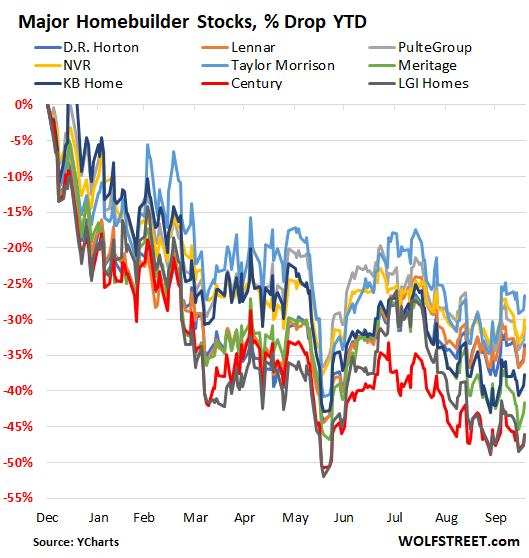

Homebuilder stocks are down between 27% and 46% so far this year (data via YCharts):

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Maybe I’m a perma-bear but IMHO, prices will decrease below the lows seen in ’08/09, mainly because the only thing that put a floor on house prices back then was the Fed drastically reducing interest rates. Even with that, housing was barely affordable even back then.

Now, with the Fed constrained by inflation, they’re not going to drop rates to save the housing market, and ’09 prices at 8 or 9% interest rates will still be unaffordable to the vast majority of buyers.

Also, 8-9% interest rates are conservative. Given the slope on those graphs, even if things started to stabilize tomorrow, we’ll blow through 8% before any sort of peak. And given that inflation is still at record levels, the Fed will be tightening for the foreseeable future. I see no end in sight for interest rate increases.

Final note. Wolf, you mentioned that mortgages tend to track 10 year Treasury rates because the average mortgage is held for 10 years. I wonder if that average duration will lengthen now that refinancing has all but stopped, and plenty of people will stay put in their houses due to underwater mortgages and /or they don’t want to give up the 3%-4% rates they currently have. And if the duration increases, would that lead to even higher interest rates, assuming the yield curve doesn’t invert?

If property values drop back to 08/09, states like Texas that rely on property taxes will be bankrupt.

How many times have you seen property taxes go down? Not here, even through 08 and beyond.

We did in Florida after the housing bust with people getting theirs revised down when home values went down. At any rate, prices won’t go back to 2008 levels. There is too much money printed out there to keep it above that. Plus politicians will likely do mortgage relief for whoever has a government-backed loan and maybe even for those without govt loans via Congress on that one. More handouts and more inflation in years ahead until an actual depression.

Assessment goes down. Levy goes up?

Of course you only see the assessment or revaluation. Then the date for a challenge passes and you get the new bill with a new levy.

I am so stupid. I should just rent. I wouldn’t own anything but the landlord would. If I didn’t like it I could move but he is stuck with the situation.

You think you own a ‘titled’ property. Hah.

Good point JR Hill, all these people “own” these homes. Where I’m at, I have a friend who just paid $4,300,000 for a home. Anyone wanna calculate property tax on that @1.23 percent? Hint: it’s a LOT of money, and it goes up 2% per year, EVERY YEAR FOREVER. Doesn’t seem sane to me, also doesn’t seem much like ownership. Try not paying that bill, the county will come and bury you, after they take back their “property”.

Interesting. I’ve been wondering about the effect of hurricane Ian on the government revenue around Ft. Myers. Can’t see how it would be other than disastrous.

If that were true, wouldn’t every hurricane in history have destroyed multiple tax bases multiple times per year?

Good point. Property taxes are a huge source of government revenue down there, especially without an income tax. Beyond that it is mostly sales taxes for govt revenue.

I’m from Ft Myers Beach. A few days after Ian my brother called FMB a graveyard. The store I used to own in Times Square is completely obliterated. Gone. The true extent of this storm is still unknown but in places like Ft Myers Beach that had tons of single level and old wooden construction. Anything on the ground floor is wiped off the face of the earth or mortally wounded.

The coastal devastation runs from Naples to Venice with major flooding inland in places that don’t usually flood due to 20″ of rain overnight. There is even major damage on the East Coast.

The only things that survived on FMB are the bland high rises and relatively new construction built to modern wind standards… and some old wooden piling cottages that sway with the wind.

My prediction is the govt deficits in sales and property taxes caused by the storm will create a budget crisis on Ft Myers Beach and Ft Myers (because govt can never shrink) and this will create the justification for ugly new high rise corporate type condo coma castles of yuck and geezerdom to sprout and fester everywhere.

Harrold,

I’m sure that CA (notoriously dependent upon sky high income tax rates…and even more notoriously volatile capital gains taxation) is going to do just wonderfully with mkts down 20% to 25%.

Not sometime in the future…*now*.

It also helps if political *expenditures* are at something less than a fire hose.

But hop on the CA high speed train to nowhere and assure yourself of the superiority of the CA way.

Just another “Minsky Moment.” The inflation impulse was well established by speculative behavior boosted by 40 years of tax cuts and tax loopholes. The pandemic just lit the fuse. Same as 10 years ago. And the ten years ago before that. And the one before that. And the one that will happen in another 10 years.

Harrold, Texas cities and tons collect property tax, not the state.

The big money for the state is oil and gas royalty revenue and that has been so good for so many years, we don’t have a state income tax.

Texas is not going broke. Not even close.

…that oil and gas revenue is going to take in the teeth when commodities follow property prices down the monetary contraction hole.

You missed the most important entities which are funded by property taxes in Texas and that’s the school system. City and county property taxes are small compared to the school district property taxes. Many states with superior school systems fund their schools with an income tax.

Also Texas has a very high sales tax with few items exempt. All in all it’s a system that favors the 1%. Overall tax burdens are LOWER in many states with an income tax than Texas.

Maybe the construction of monstrous football stadiums at TX high schools will slow down a tad…..

Well many of the Texas markets have prices flat from 2008 except Dallas and Austin areas so not much impact on the state revenue side.

“If property values drop back to 08/09, states like Texas that rely on property taxes will be bankrupt.”

I wish Wolf would someday explain how property taxes work, so that people stop with these misconceptions. Property tax totals are based on government budgets and local laws. The values of the properties being taxed have virtually no impact on those totals. Values are simply used to allocate the totals to individual properties.

Good question. It’s also possible the average duration will shorten due to foreclosures and evictions.

Read about Mel Watt during the Obama years circa 2014. That’s where this whole housing bubble redux stems from. It’s been brewing for almost a decade.

Don’t forget – there are other agents for keeping the lead balloons aloft. I remember the housing credits from back then; here in Austin, it had the effect of injecting adrenaline into a perfectly healthy heart. The key difference now is that the objective is to contain the market.

Lune, the national median house price dropped just shy of 20% by the GFC bottom, taking that median back to its 2004 figure. Some bubbly markets were hit hard while others remained pretty calm. You think that even after over a decade of QE and massive money supply expansion, we’re ever going to see 2009’s house prices (at the 2004 level) again? Can you point out a time that the median house price ever dropped anywhere near the 50%+ that you’re suggesting?

I agree that interest rates are going to have an effect and some folks are going to get hurt, but your prediction is way out in lala land. Even the great depression only saw a 30-35% average drop. There’s also a 100% chance that the collapse you’re describing would trigger significant action from both the central bank and politicians.

The figures I’ve seen (just 2) were 26 and 22% for the peak to trough drop. 22% was for the median. I calculated using figures from Dont Quit Your Day Job website.

Shows 2007 peak of 217.9k and bottom

of 170.0 in January 2012.

I dont remember what organization cited

26%.

My neighbors house sold for about a 23% loss in 1989. Dallas suburb.

My house appraised for 24% less in 1990 than I paid for it new in 1986.

Sold for 8% loss in 1996, ten years after i bought it new. Nice house, lightly

used too. Rowlett.

But yes Nasdaq might drop 78-79% in the

tech bust, but 50% for RE seems a stretch.

Well, for standalone single family anyhow.

Scott Burns wrote an article in the Dallas Morning News in the late 80s or early 90s

and claimed Boston condo owners could not sell them for half what they’d paid for them. Boston had a large run up in RE

prices in the 80s I believe.

We can be in the 80s again, we can be in the 30s again, or we can create our own version of monstrous crisis which we are.

What I observe is that the man next door thinks he doesn’t have to work hard, others can and should.

These hard working people will come and buy his speculative prices on assets.

That works for as long as there are still a lot of hard working people out there. But the truth is, there aren’t. We have become a nation of sit at home or coffee sitters generations. Sad…

The younger generations rely on older generation to pay for the niceties, but the older generations that did that (because of hard work) are dying out.

There is an old Japanese say (Wolf may grill me here):

Parents toil, children ease, grandchildren beg.

We are the grandchildren. The show is over for us, we have been begging and it worked till now. But the world always changes and it’s not friendly to beggars anymore.

I don’t understand why wouldn’t we see a major crisis, as if we are so special. It’s all lined up and we did it with the help of others.

Calvin,

Speaking of begging, I’m politely begging you to please stop peddling these lazy, tired myths that people don’t work hard and younger generations are the cause of all society’s woes. I wrote a much longer response but don’t want to get put in time out, so just leaving it at this.

Keep in mind that there’s $67T in baby boomer assets to be transferred over the next 20-30 years. This is a gargantuan amount of money that will apply steady upward pressure on home prices. Certainly, there will be some short-term drops over that period, but on net, housing isn’t going to see deflationary pressures outside of some major black swan event that creates enormous economic uncertainty. A real debt crisis that puts the good faith in credit of the US comes to mind, but something like this isn’t around the corner.

Half of that wealth will vanish amid price declines — some of which has already happened. And some of it will get burned up by inflation (loss of purchasing power). And a lot of it will get confiscated by the healthcare industrial complex that is now sinking its teeth into the boomers. There you go.

Yes, part of that price decline will be due to demographics, the birth replacement rate is well below 2.1 in the US. Who needs a huge boomer house when you have no or only one kid.

Healthcare industrial complex, indeed. My mother’s assets (including a 500k home) were pretty much swallowed up for her elder care before she died. There wasn’t much left over.

Let’s see how this supposed recession plays out which will be a good indicator. No one can really know what’s going to happen with the stock market & housing over that lengthy of a time period.

50% is nothing more than a WAG. Certainly, I agree that healthcare costs will certainly eat into the hand me downs. No doubt.

Either way, the BB generation will pass along enormous wealth that’s never been seen before.

Why would a bunch of boomers all putting their houses on the market drive “UPWARD” pressure on home prices?

Is this sarc? Or a typo?

The houses are not all going on the market all at once. But as they are sold off, this is going to create an enormous amount of wealth transfer that will allow beneficiaries to be able to afford things (houses, cars) that they wouldn’t otherwise be able to afford.

My realtor told me the same.

He also told me that home prices won’t go down, rates would top up at 8% after that rates would go down.

All else being equal, the massive transfer of wealth will be inflationary. To what extent is, I agree, hard to say. Again, if there’s some black swan event or two in the next 30 years that really changes the calculus, then people’s housing & stock values are going to be the least of their worries. Realtors are notorious for exaggeration.

The bottom of housing was in actually in 2012, 4 years later. Will be drop below those lows?

That would equate to more than a sixty percent drop in Toronto, Canada home prices from the peak in February this year. From the peak in 2022 back to the trough in 2012.

There will almost certainly be mortgage forbearance and foreclosure moratoriums first before prices decline below Housing Bubble 1 lows.

@3% which is likely “ballpark” for a high percentage of government guaranteed mortgages, it only costs $2.5B per month for each $1T.

Not going to happen, 30% REIT owned now….before they were strawberry pickers

33% at most

You are, unlike government, objective and knowledgeable. I obtained my real estate license in ’88 and a Broker’s license in ’92. I warned anyone who might listen in 2005 that the housing market was absolutely going to crash. (Spurned on by liar loans and faith in statements from the likes of the chief economist of the National Assoc. of Realtors and Fed Chief Bernanke. That was a tough few years and lots of bankruptcy and programs’ forgiveness. But nothing changed afterward beyond a lowering of rates to goose the Housing market back into trouble again. And in 2018 I again told anyone who would listen that again we were in a major housing bubble. Hardly anyone listened except to avoid me as a Real Estate Broker. Doing the right thing was important to me. I have since moved to the Philippines where my money is buying so much more. Good luck America.

The housing bubble should have burst a long time ago. But now it’s floated soooo high it’s hard to see how any of the newer buyers inside can survive the fall.

Say kids, what season is it? FALL SEASON!

Yes, good luck to those short sighted buyers.

Good, let it crash harder and faster than last time…still feels like a long shot so I am not holding out hopes, but that’s probably the only way one can afford a house in California, especially NorCal and SoCal.

As a person who lives on an area of suddenly manic house building and population increase, I’m enjoying a good dose of NIMBY schaudenfreude…

Lol we are screwed up in LA . It is more un affordable but it doesn’t want to drop a little here.

Banister Business Plan #07:

Golden business opportunity to borrow in Yen or Euros, swap for dollars and lend on US mortgages.

Done right, you capture both the US-overseas interest-rate spread AND the plunge in value as the Yen implodes!

Triple bonus kicker: keep the Loan-to-Value in the sweet spot so that when the recession hits and the borrower can’t pay, the borrower wants to walk away. Then you can harvest the collateral and hold it for a further profit when the Pivot brings rates down and house prices surge back up!

Even better, Wiz, lend that mortgage cash via hard money loans at >10%. The LTV optimization is the trickiest part.

That loan-to-value sweet spot. Would that be somewhere in Northern Alaska?

Wow, “bankster” became “banister”. Spellcheckers now automagically censor any non-approved words; toss in AI and soon Big Brother won’t need the MSM to censor free speech, b/c the software will do it for them…

@Gattopardo – can’t lend at high rates while Fannie and Freddie and US Taxpayer are willing to underbid!

@Andy – LOL re: Northern Alaska. Seriously, based on 2008 I think the LTV sweet spot today is 60-80%. Depends on the market. But predatory lender needs enough houses to drop in price just enough below the mortgage that the owners give up and walk away … just as the market bottoms. Set the LTV too high and the lender gets swept away too. Set it too low and owners can sell and walk away.

BTW, Wolf has us feeling a bit smug here b/c we think we can anticipate what’s ahead, but I think things will get out of control and we’re all going to be flailing for a while… If the bond market gets just a little more squirrelly there could be a deep freeze in credit land, and a lot of unexpected bankruptcies, even as Fed’s helping hands remain tied by raging inflation. So I’m back to looking at “diversification” in terms of diversification of cash protections: FDIC insured, NCUA insured, SIPC insured, Treasury guaranteed… bond covenants…

I can see 40 or 50 year mortgages coming. Gotta keep things rolling along.

Wisdom Seeker, Would love to see how a non Japanese citizen can borrow in yen. Keep dreaming!

Banks do it all the time. “Yen Carry Trade” is a thing.

There was some guy Mauldin who writes an investment newsletter who was figuring out how to do it himself. He would’ve saved a lot of payments on the exchange-rate plunge already.

And then you are going to get the shaft when the Yen turns around and zooms upwards………………..

The move in the Yen is being exaggerated by huge bets in the derivatives market which will cause billions of losses to those playing the game when it ends.

The banks are borrowing at 4%-5% (brokered CDs). To give Joe Six-pack 7% loan for 30 years to buy a losing asset ahead of a recession is pretty good deal on my book.

Reduced price increases are not declines. The prices are still increasing just at a slower rate. 11% YOY is still an increase even taking into account inflation.

Russell,

You misread it. There are month-to-month declines since May that are reducing the year-over-year spike. It will take till the rest of the year before the monthly declines add up to become year-over-year declines. So re-read it.

When a price is up 20% yoy, it would have to plunge by 21% the next month to be down yoy. That’s not going to happen. YoY price spikes take a while to reverse even amid steep month-to-month declines.

So you will have a few more months left to come in, soothsaying that these price declines are “not declines” because they’re still up yoy, though they’ve been down 8 month in a row.

In plenty of markets, prices are already down yoy. So you already lost the battle there. I’ve featured some of them here, and I’m going to feature more of them tomorrow. So make sure to check back.

The title of the graph is YOY price increases, since the graph is all positive, they are still increasing. Graph may not reflect reality, but that is what it shows.

There are a bunch of ways to show price changes: actual prices, month-over-month, year-over-year. They all show the same price declines from a different angle. After a 20% yoy spike, prices have to decline month-over-month for a while before prices are negative year-over-year. The chart shows you the process on the way to a negative yoy number.

Agreed, but it’s hard to feel sorry for the builder when their prices are starting to moderate when they are still 11% higher than the previous year.

Cry me a river!

“The title of the graph is YOY price increases, since the graph is all positive, they are still increasing. Graph may not reflect reality, but that is what it shows.”

This is really dumb analysis. Let’s take a certain market for instance: The median price peak was $615,000 in May. The median price in September was $535,000. Year over year, prices for the month of September still show as up. Are prices “increasing?” Of course not, they’re crashing.

Don’t go busting house humpers only golden narrative left now…the only thing they can hang on to is YoY change is still positive…I mean how else are they going to convince you housing is a no lose proposition.

But as you said, matter of time before YoY shows negative even in “invincible” markets like SoCal, I am sure when that time come when YoY is showing negative then the narrative will just pivot to it’s normalizing or we’re in gully…etc

Wolf – Any guess where mortgage rates might peak, as I’m guessing around 8-9% as that would double the payment (half the loan value) versus 2.7% previous low on the 30 year, and thus might get the attention of the Fed and Congress as houses could plummet 50% if such rates last long enough???

I really like your charts as even though the past does not predict the future, there are commonalities that show up visually in the charting..so thanks for running the numbers and making the charts, there is a good reason why so many financial sites utilize your data…

I’m speculating at the moment by dipping into VMBS at these levels, and I’m guessing we might bounce quicker than the previous housing bust (2006-2013 bounce). I’m guessing the Fed will be forced to buy, or simply threaten to buy, MBS by Congress at some point if mortgage rates get too high 6 or so months before 2024 elections. I believe the govt will be making the decisions for the Fed going forward as has been the case historically from case studies in previous money printing experiments that often turn into debacles. We might go from “Don’t Fight the Fed” mantra to “Don’t Fight Congress” motto. I’m hedged either way and personally believe it a mistake to keep printing, but we don’t have the sharpest tools in the shed running our country, and the easiest way to get votes is to “Buy” them via printing money…

What’s your timeframe?

For the first leg of this cycle (the current one) since the presumed secular trend change in 2020, don’t be surprised if rates aren’t that different from today a year or two from now.

If you are referring to longer term as in later this decade or even after, 8% to 9% isn’t even close if the cycle really bottomed in 2020.

Ultimately, rates are destined to “blow out” far past the 1981 peak. The fundamentals everyone uses as a reason why things are different vs 1981 so it can’t happen will fall into place later. These fundamentals are actually already mediocre to terrible right now but it’s not fully evident because still loose monetary policy and sub-basement level credit standards disguise the true state of the economy.

As long as inflation is in the 4%-8% range, it remains a political bitch, and politicians will leverage it to beat up on their opponents, and politicians won’t ask the Fed to create even more inflation. That would be political suicide. And bond yields would blow out if the market realizes that the Fed is just going to throw more fuel on the inflation fire. So I don’t see that as a realistic scenario.

Wolf, re “And bond yields would blow out if the market realizes that the Fed is just going to throw more fuel on the inflation fire. So I don’t see that as a realistic scenario.”

Isn’t that scenario already doomed to play out b/c their is $1.5T of Biden stimulus starting to get spent now, and city/states have at least $1T of COVID money left to spend, and the Fed’s QT will only remove ~$1.2T/yr. So that is going to fuel labor and materials inflation despite the Fed trying to crash the housing market asset inflation.

How much cheaper is EastCal than WestCal?

75% off.

I know someone is going to complain about the mortgage-rate chart above going back only 20 years, and not all the way back to whenever, so here we go:

THANK YOU!!!

No seriously, I’m trying to teach my 15 year old about money and finance. He needs to see stuff like this NOW. Trying to learn about the value of home ownership is not something people should be “learning as they go” when they’re in their 30s

Just sayin’

I bought and moved a lot of paper back then, buyers still buy cars and homes, just not at what you see in market manics as of recently

great thing about it is finally risk credit profiles will be priced properly…like in the past. Tiered credit buckets and workflows will react much different in the fast algo world of today though….

I’m going to money 2022 next week lets see what financial world has to say…Already saw the best decision engine workflow tool I have ever seen…

OK Wolf,,,( are you a boomer??)

What was the rate when family bought 3 homes in 1955??

( Just kidding to make your prediction, eh?)

Seriously, this reminds me of the first house I purchased in 1978 with 20% down and the balance of the $40K price financed at 16%.

Fixed it up with all kinds of new top to bottom and sold it very quickly in ’80 for $105K.

Zillow now says it’s worth over $1MM… or was a couple months ago..

Gonna be fun fun fun for the current flock of kids, eh?

Now just need to include house prices on the same graph to show the disconnection of price and interest rates today

How dare you not include the 1960s…

2b – that’s gold.

But to misquote: No-one who was there remembers the 60s anyway.

Can you go back to 1776 for the full picture? I don’t think 1972 is sufficient enough :P

I tried to graph this once but could not figure out whether the trail of tears should go on the x or y axis. Any thoughts?

Just a curious aside, but there is an influential investment paper that plots the long run price performance of the Herengracht district in Amsterdam since 1628. You might be asking what the heck is the Herengracht district and why should I care? The reason the dataset from it is so exciting is that it has been a residential community for nearly 400 years, the price data is captured for the whole time, and the Amsterdam population has been a relatively stable percentage of the Netherlands for that whole period of time. A near ‘timeless’ area data set over an incredibly long time period. The more interesting fact is that over that timeframe the actual real rate of return of real estate has been 0.5% and only a 3.2% real return since 1974. Over long periods of time, real estate is the most mean reverting asset in existence.

I actually studied this prior to the 2007-8 bubble and it, coupled with Manias, Panics and Crashes by Charles P. Kindleberger, was what kept me on the sidelines waiting for the crash. Data is what should be driving everyone’s financial decisions, but that isn’t the average person’s deciding factor. It’s usually raw emotions. The math will get them there; weak hands will have to fold eventually.

Excellent comment! In this context does “real return” include or exclude taxes and maintenance/repair costs?

I’m guessing few of the houses are actually 400 years old.

Also, to be fair, Amsterdam was very close to the center of the financial world in the 1600s, like New York or London is today, so the starting-point effect might skew the long-term returns. Similar to looking at Tokyo real estate only since 1989… But I haven’t seen the graph. I just figure that in a population and era famous for valuing tulip bulbs at the same price as median houses, there might be some interesting quirks in the data…

You are right. Same idea applies to stock prices.

Most people are either ignorant of history or much of it is contrary to their personal preference.

The “real” return of holding cash is a terrifying alternative. If anything, this is proof that residential RE is a reasonable store of wealth over the long haul if you’re hoping to at least keep up with inflation. If a person bought a house in the 50s, it did a decent job of keeping its real value, maybe to be lived in for a long time rent-free and then passed onto the kids. If that same person put that much cash under a mattress, it wouldn’t even buy the most pathetic economy car available in the U.S. today.

Here in California’s Inland Empire, buyers haven’t totally gotten the memo about the slowing housing market. An unimpressive 1,750 sqft house on a small 6,000sqft lot just went pending for $660k up the street. A slightly nicer house for $750k just went pending down the street. Another 1,550 sqft house in semi-rough shape went pending for $550k a block away. A seemingly long list of houses closed by 10/14/22 around here for whatever reason. I don’t know if these buyers are the dumbest or the smartest people around. Is this another mid-late 2000’s when the median price dropped ~20% or another 1970’s when house prices nearly tripled due to inflation? We’ll find out.

NotSure – The real return of “cash” is what you get in a money-market fund with interest, not under a mattress. It’s really not that bad. Was better under a gold standard…

No, you are all wrong.

The “real return of “cash” is not what you get in a money-market fund with interest.

The “real return of cash” is what you can buy by holding cash. Holding cash provides no interest income.

There were no such things as money market funds years and years ago either.

A dollar of cash held from 50 years ago will not buy anything compared to what it could buy. Your return on holding cash is near -100%.

The Dutch have records of mortgage rates and house prices going back to the 1600s.

Housing must have been cheapo during the early 80s, or was that a period of a greater percentage of people renting? I notice now that a growing number of larger cities have a growing percentage of renters verses owners.

I bought a house in the suburbs of Boulder Colorado in 1978 when in grad school for 65k. Brand new and I got to pick the flooring, colors, etc. Huge lot. Sold it in 1985 for 86k. Houses in that exact same subdivision are listing at 800k+ now.

I should add 2000 sq ft, 4 bedrooms, 2 bath, fireplace, big garage, desirable neighborhood. Party finished basement, nice decks.

It was but jobs were hard to get ,union busting . And a lot of homes lived in never updated .so they were reasonably priced in older neighborhoods.Dirty hands built equity

Only cheaper in hindsight given all the money printing. I remember buying a house in 96 for 177K with a 20% down 30 year fixed at around 7.25% and a coworker just said “thirrrrrrtttttyyy yeeeeaaarrs” and it scared me thinking about how long I could be on the hook for this (at the time) 25 year old 4/2 fixer upper. No one around back then would have ever guessed we would have gone as far off the rails as we have

Do a search for this: Historical US Home Prices: Monthly Median from 1953-2022

You’ll see median house prices for 1980s.

Hi Wolf.

Appreciate the chart going back to ‘whenever’.

In those days (early 70s) the home owner could simply sit back and pay off as scheduled over the course of the 15 or 30 year term, meanwhile for their savings get interest in the mid to high teens on t bonds, CDs and commercial paper money market. I don’t see that part coming back.

Back in the 1960s they had 3-4% mortgages just like we recently did. And, just like today, no one in the 1960s anticipated that mortgage rates would be north of 10% in just ten years, or 15% in 15 years. Time will tell!

If the 1970s inflation were so easily vanquished by Volcker’s high interest rates, how come inflation took another decade to settle down to a reasonable level, and rates had to remain well above that inflation for the whole duration? Inflation peaked around 1982 but it didn’t return to the levels we’ve gotten used to for many years after that.

I’m starting to suspect that perhaps the real underlying force driving inflation is a historic rebalancing between labor and capital. That’s a generational sea change, not simply a stimulus-response effect of the COVID money-printing binge. Viewed from that lens, it’s entirely possible that inflation might go on for 10-20 years, and given the headroom on monetary velocity, inflation might even be nearly impervious to interest rate hikes and QT for many of those years! Won’t that be a surprise!

re “I’m starting to suspect that perhaps the real underlying force driving inflation is a historic rebalancing between labor and capital. That’s a generational sea change, not simply a stimulus-response effect of the COVID money-printing binge.”

while there may be a bit more of that happening post-COVID, I doubt that will be a trend for a few reasons:

1. Wage inflation has significantly lagged CPI the whole time.

2. The Fed knows it has to crush labor’s bargaining power to control inflation. So, must induce a deep recession and asset/M2 deflation to force labor participation rate back up to pre-COVID levels.

3. High wages and high PPI costs will drive much faster Automation to replace the human labor from the production equation, over the next 5-10 years. I think Self-driving class 8 cargo trucks and taxis will be the first great example.

looking at the graph above it seems that mortgage rates have really out paced interest paying loans…CDs, treasuries…this time, is there a simple explanation to this? Are the banks expecting defaults and/or slowing of business and want to make some money now?

In Denver metro Zillow shows my home had lost $15K of value in last 30 days. Seeing prices on new construction getting cut. Still not that many homes my area on the market for sale. Folks must be staying put. Winter is coming, most people are scratching the new home off the Xmas wish list. Inflation now seems to be a runaway freight train. Housing affordability across all income spectrums coming to a grinding halt. Makes you think who really has passive income and liquidity in this economy. Excellent credit still gets you highway robbery.

The only buyers for homes in the next year will be from Corporate relocation companies, private equity cash buyers and foreclosure sales. It’s going to get ugly. Middle class buyers are priced out of home ownership. Even if they could afford to buy now, if they buy, they will get wiped out in the crash that is on the horizon and wind up underwater with their mortgage lender. They lose no matter what they do. You can thank the Fed, Congress, the current morons running the country and all this reckless spending for this. ENJOY

Do you expect housing to crash next year or the year after that?

Wolf – You can delete my above comment. I wanted to know from SC when he expected the hosing market to crash. One of his comments down the line answers that question.

I didn’t delete anything. It went into moderation for some reason, and it’s now released. However, if you want to actually get on the moderation list, all you need to do is keep pestering me about moderation.

Emperor Has No Clothes,

Your Denver Metro Zillow experience pretty much matches my Chicago Metro Zillow experience.

Which might be considered somewhat odd because Chicago SUPPOSEDLY didn’t have the huge runup in houses prices that Denver was supposed to have had.

In any case, I would be very happily amazed if my home sold for even near the Zillow value.

It’s worth a lot TO ME because it’s paid off, pretty well insulated, and I live here. Somehow I doubt Mr. Housing Market cares about any of that.

California, Florida, Colorado RE…

get much love at these web sites.

And yet, foreigners and other investors

helped propel Toronto to greater price than Denver and others.

Toronto IS correcting quite a bit.

As best I can tell it maxed out

at CA $1.34 M in February.

Now at CA $1.09 M.

About $800k US.

Canada’s RE correction is mostly in Ontario and Vancouver. No surprise I guess, they had huge run ups.

But it is perhaps interesting that Toronto, not part of an ocean coast or mountain range, has appreciated so much.

2 Points:

1. Housing is correcting. In addition to Toronto down 19%, Seattle off 9%,

San Jose 11%, others (Austin, Boise)

off 5 or more percent. Will Southeast

cities (Atlanta, Jacksonville, NC cities)

where investors have bought so

much RE correct much ?

They bought 33% of Atlanta homes in

2021. Twenty five to 30% in others.

2. While California and Florida will continue to appeal to older adults,

their future appeal to the young may

be less. Why ? Obvious reasons.

California: Wildfires, drought, super expensive housing, combination of factors.

Florida: climate change factors perhaps and the greater realization

that hurricanes and (yes) tornados are a recurring part of the landscape.

This would be to the disappointment of those currently living there. Their RE would reflect the reduced demand.

Seems to me Chicago is lagging in terms of national decline, because I see as we only have a “super bubble” vs “insane bubble” like California, which they are just now hitting. Don’t be surprised if we might not see any significant trend shift even on next Case-Shiller index update.

In my opinion, much of it has to do with lack of inventory and school district. I see raggedy shacks being purposely listed cheaper (in comparison to other raggedy shacks in current inflated market), so people end up overbidding each other. I have just learned that 18 or so people bid on $305k house way over asking price. Same house would sell for no more than $200k in 2014 and be on market for 90 days (best case).

Those are just last minute Shyster Meister tactics to pray on desperate/needy people. Its a calm before storm.

I’m one of those sitting on the sidelines. It’s not just the mortgage rates, although it’s mostly the mortgage rates. I can only speak for Florida where I live. But every single new community that is built might as well be townhomes. Why would I want to pay an exorbitant amount of money to hear my neighbor going to the bathroom? Or on the weirdest shaped postage stamp of a lot that could possibly be created by man with a weird sloping driveway to boot. It’s not like this is Colorado.

When the money is cheap and easy to get, most people are probably like why not? Because if nothing changes they can just sell it to the next person.

But finally, it’s changing. And so now as prices begin their descent everyone is thinking if I buy that postage stamp house where all the colors are a slightly different but same shade of gray-brown, with the fake trimmings, how hard is it going to be for me to get rid of this crap-shack one day?

Drove through a neighborhood in FL recently. $400k houses basically on top of each other. One house was blasting annoying rap music that could be heard down the block. Imagine paying $400k and you are stuck with that as a neighbor

Cramer just issued a buy on the banking sector.

Did he ever say it’s time to get out of the banking sector — before shares began to drop?

Goldman revenues -20%, net income -43%, CEO warning of recession and says it’s time to be careful. Cramer will likely turn out to have nailed it again. Just remember his comment for a while.

I remember that buffoon telling everybody and their mother to load up on Bear Stearns. Is he a meth head or something?

When we finally got our 18% second on our house paid off and our

mortgage rate down to 10%, we felt like we were living for FREE!

That was for a small 2 BR 1 BA house we bought in San Jose in the

80’s.

I hope we’re not going back to those kind of rates. At least the house

was under 100K then.

Now I pay cash for everything or I live without it. I pay all utilities first,

grocery bills second, anything left over goes in the bank. All my dividends are reinvested, I have never spent them. 14 years of no interest on savings has made me a little crazy.

The market here in the Swamp is deader than a doornail. No sales, no listings, no refinances, NOTHING. Had one fellow appraiser call up whining and complaining that there is no business. None. And they have to pay rent for their office space and are in debt. So, I see a lot of small mom & pop real estate businesses going belly up. We’re pretty much WFH, have no office rent, so we can ride this out until the market improves in a year or so after it crashes 30% or more. So, I say, just bring it on!

Same in my neighborhood. New listings are getting very little if any traffic. Buyers have clearly taken a step back in just the past few months.

It appears as though it will be a buyers market once prices really start to drop…it’s inevitable.

But for now, the slowdown is sudden and for many, soon to become harsh.

Appraisers can fix this situation quickly by appraising lower values. Business will pick up dramatically.

House sellers are in total denial. A large number “took it off the market to wait for it to turn around.” They are riding the price down. The rest are basically stale listings that have been sitting for months, grossly overpriced. I see houses listed at prices where even a 70% reduction would still be overpriced. The only things selling are at massive discounts.

This housing crash is already spilling over to the contractors that support housing. I recently had to call some contractors to fix a lot of stuff that was recently damaged in a recent fiasco that came out of nowhere. I had used them before, and they did good work for the money. Two of them were out of business, phones disconnected. A third (electrician) was still operating but he said the pandemic nearly took them out. No one wanted anyone in their houses for 2 years. The dude said people were using candles rather than calling electricians. Others were running 40 foot extension cords through drywall as a workaround. The dude said his company closed their commercial office and substituted a P.O. Box instead. The secretary was now WFH. This is what is going on now. It will only get worse.

Just for perspective:

Zillow says our home in the saintly part of TPA bay area is worth over FOUR TIMES what we paid cash for it 2015.

That is just plain CRAZY, and a very clear indication that RE mkt in at least some places in FL will go down as much as it did between 2006 when a 1600SF ”fixer upper” on a canal with sailboat clearance to the GOM was listed at $885K,,, then sold in 2009 for $225K.

Hold tight folks,,, stormy seas ahead everywhere IMHO, in spite of Z predicting prices here and elsewhere will go UP 5% or so…

Yeah VVNV, when has Zillow ever gotten it wrong?

Thanks Wolf. I saw a nifty chart on Zero Hedge by Market Ear comparing the NAHB index with the inverted 30 year mortgage rate going back to GFC and a caption indicating that the bottom is not in until NAHB turns around.

One other note you and others may enjoy the housing thread by Jeff Weniger (Wisdom Tree) very in terms of buyers/sellers and where the market is going. I assume the Canadian market will play out much the same way. Here is the thread:

https://twitter.com/JeffWeniger/status/1582395774121361409

In two thirds of Canada the only buyers of new homes were the Chinese until mortgage rates rose this year. In Canada new home prices will fall much more than resale home prices percentage wise for this reason.

Thanks Tony. I’m in Toronto. I had no idea 2/3 of new homes were Chinese buyers !!!!! OMG If that is true we are in for one helluva correction.

Ground report from San Diego:

No real impact on the home prices as of now.

Not sure what the future hold.

Ive watched a home in our North San Diego neighborhood drop by 300k in the last 5 months. Listed for 1.7m in June and just reduced again today to $1.35m.

Yes, prices are down from aspirational asking price. But not really down from say last quarter.

My wife sold her mom’s 100 year old, 1300 sqft, termite/mold tear down on a tiny lot in southeast Orange County CA for $1.5 million in October. Current zestimate is $1.643 million, so I interpret that as no real sign of down market yet.

As much of a cheerleader as I’ve been about San Diego’s untouchable prices, even I can’t say I’ve seen things stay the same. Stuff in areas I watch is either sitting, selling at reduced prices, reposted at lower prices, or coming back on the market when it falls out of escrow. I’m sure that the time of year is contributing to this, but it’s obvious that the biggest culprit affecting things is that the market can’t bear the higher price that comes with a higher rates on an overpriced house.

The corrections here on SFR’s won’t be as bad as other parts of the country, but there are definitely substantial corrections on the horizon. Condos are gonna get hammered, though.

Things have not slowed down a lot yet in San Diego.

My realtor told me the same the come what may sfr in San Diego won’t go down so buy now or priced out forever.

In 2009 I thought the same ie sfr in San Diego won’t go down a lot as we are special and everything is awesome to justify insane home prices but we all know what happened here in 2011 2012.

“My realtor told me the same the come what may sfr in San Diego won’t go down so buy now or priced out forever”.

Tell the same realtor that she better start training for a new career or be broke forever. Just like during last bubble, everybody was a real estate agent and they all knew it all.

I am tracking 7 northern coastal SD neighborhoods for my next buy and they are all almost down by around 15-20% now from spring ’22 prices. I believe by year end ’23 you can add another 5-10% to that so we will be looking at something up to about 30% down. I also predict further declines in ’24. It is certainly not out of the question that the ’07-’12 crash of 40% in this area will be seen again.

Hoping that the FRS raises rates to at least 4.0 during 2022! So that 2023 can be a[nother] Good Year.

Pretty fast slide in those indexes, but I agree with many who are stating people will just hunker. Prices will not crash like HB1. The rental market will likely thrive since people gotta live somewhere.

Not sure what would happen in the future. But I though the same in 2008-2009. I thought san dieog is special and come what may, prices wont fall.

My friends told me worst that can happen is stagnant price in 2008-2009.

I also though, prices wont fall as people got to live some where.

Thousands living on the streets of USA these days from what we read jon.

After all, this is freedom central, including freedom for rich folks as well as poor folks to live under a bridge, or in a tent on the streets of many cities, even while working full time from what is reported currently.

Or did that change recently where you are?

Depends on job losses. Real estate slow down will nuke a lot of businesses. Where I live every retail space that was empty 6 years ago is filled with something related to houses. Kitchens, tiles, flooring, granite, hot tubs, etc. Slow down could hurt a lot of those businesses, and many more.

The other day on Reddit people were peeking into the r/sales subreddit looking at sales people talking about the massive slowdowns they are seeing. Not all industries of course, but quite a few.

A lot of home renovation contractors are now calling me offering their services.

it was not the case 6 months back.

No meaningful decrease in price yet but I for sure see slowdown in home sales and to some extent in prices.

Read his prior posts. He’s apparently a landlord, so of course he believes this isn’t a bubble and prices won’t crash.

Based on post by individual people i can easily make out who is landlord/realtor etc vs others 😀

Me? Not a landlord. Renter scum eager for a crash (and hoping I can hold onto solid employment this go around.)

“but I agree with many who are stating people will just hunker. Prices will not crash like HB1.”

Just because fewer people will be voluntarily selling their homes doesn’t mean prices won’t crash. Yes, there will be a lot fewer voluntary sales – initially – because the higher mortgage rates at current prices produce unaffordable mortgage payments. But there will still be involuntary sales due to job changes/losses, divorce, death, etc. And these sales will have to occur at much lower prices because of the higher mortgage rates (to produce an affordable mortgage payment). Overtime, these forced sales, even at much lower sales rates than normal times, will set home valuations at much lower levels. Eventually, we should reach an equilibrium where the values of homes will drop to a level where, when combined with the higher mortgage rates, the resulting monthly mortgage payment will be roughly equivalent to what people are currently paying based on their 3% mortgages and higher purchase prices. At this point, voluntary sales will pick back up and overall sales will increase to normal levels again.

In theory.

Rents are starting to go down too. August MoM decreased by 2.5%. People can live with their parents, they can share an apartment, they can do many things to shrink the required amount of rentals.

People hunkering is totally irrelevant. Valuations are based on the transactions that occur, even if they are few and far between. So hunker if you wish, and enjoy the view of crashing valuations.

Most of the people don’t get this easily

Prices are defined on the margins.

Amen. Exactly.

Beardawg

If you follow the Fed, the MBS market is not hunkering down.

I appreciate all the opinions on this housing shift and I may turn out to be wrong. I used to be a landlord (2005-2019). Out of RE now except a couple remaining 10% Interest Only notes.

My perspective is comparing what’s happening (or going to happen) with HB1. I cashed in on HB1, buying project houses for pennies in AZ an MO and turning them into viable rentals and eventually sales.

The volume of inventory for the super deals for landlord / flippers just won’t be there, so I believe existing SFH rentals (acquired during the crazy price years of 2019-2022) are going to maintain relatively higher rents due to sheer lack of rental inventory. Some of that inventory will make its way back into the market (foreclosures etc), but nothing like in HB1.

Yes people will hunker, for about a year or two. Then reality will set in and loses will be realized.

It is the same scenario in every housing crash, and no, this time is not different. Anyone who does not think this will be as bad as 2008-2012 is not looking critically at circumstances.

In the first housing crash, the majority of mortgages at that time, were originated in the 5.5% to 6.5% range which gave room to lower rates to 3.5% and offset lower values.

Today, most mortgages being held are in the 3.5% range and new mortgages are in the 7% range with no hope of lower rates in the foreseeable future. That translates into 35% lower sales prices to keep payments in the same range. Sales can only take place when buyers qualify for loans, and that can only happen in a high interest rate environment when prices decrease.

Jdog

You make my point exactly. if you are sitting on a 3.5% mortgage and going back into the market gets you 7%, even if prices are significantly lower – means people will “hunker” for as long as is needed. Yes, job losses / life circumstances will force some people into selling or foreclosure – but not like 2008-2012 – the volume just will not be there. Also remember that inventory was plentiful in the 2005-2007 timeframe – not so in the 2020-2022 timeframe. Lower inventory = more price stability. It is my belief “HB2” (if you want to call it that – and it has not yet happened) will pale in comparison to HB1. We should know within about 2 years.

Beardawg,

You sell and move into a rental, and let prices drop, and after they dropped enough for a few years, you buy at a big discount.

I know people who are doing exactly that, including a commenter here who is a Realtor and who timed her market perfectly: she got out of it at the total peak.

In addition, folks are going to sell their vacant homes. Now that prices have dropped, they pulled them off the sales market and put them on the rental market, but that’s a very different animal. After a while, they’ll show up on the sales market again, or perhaps in a foreclosure sale.

“You sell and move into a rental, and let prices drop, and after they dropped enough for a few years, you buy at a big discount.”

The price drop has to greater than the totals costs incurred in the sale and move including taxes or you would have been better off staying and not selling.

And then you have to factor in the higher interest rates or paying interest if you need a loan.

Lots of variables and none of them are under you control.

“Prices will not crash like HB1.”

All you ever post is wishful thinking based upon nothing. You read like a housing shill. Is that you, David Liarhea?

DC

See my response to Jdog above. It is my theory, based upon reasonable suppositions as oppoosed to “nothing.”. I have no idea who David Liarhea is and I am not invested in RE anymore except for two (2) 10% interest only notes as a lender. I welcome discussion regarding the suppositions I presented, but your “go to” tends to be baseless name calling which I presume gives you some sort of internal warm feeling.

The reality is that if realtors, appraisers, insctors, loan officers, etc. want to keep their jobs/businesses, home prices will need to come down. All these professions depend on broad based affordability to generate a sufficient count of customers for sustainable cash flow. Since these people de facto control price setting, it will happen whether the sellers like it or not.

What would a 2100sqft. 15yr old SFR in a nice Cali neighborhood (4BR, 3Bath,2 car garage, living room, family room, 20x25ft climate controlled crawl space, 20×18 ft. deck, 100x150ft lot) currently sell for?

400k max

What is a climate controlled crawl space? I

Depends on if it’s in Barstow or Palos Verdes…..

Currently? In the bay area, nice neighborhood, decent community, 1.5-3 million depending on locale.

@ any given time around 25% of listed houses are unsaleable for a variety of reasons, but that rachets up substantially in a market trending down, the nice turnkey homes still sell, but everything else is a struggle.

In my area, we are NOT at all seeing actual sales comps drop. The overpriced “dream” list prices are being cuts, dogs are sitting longer, etc. However, decent homes are still gone very fast. Inventory is crazy low. I think a lot of areas will not drop in comps at all.

This has been my argument in these comments, several times over the past year. It doesn’t matter how many homes they plan to build. What matters is how much available inventory is built and on the market *today*. I seem to get pooh poohed for pointing that out, and I still don’t understand why. The phrase, “a bird in the hand is worth two in the bush” has withstood the test of time for a reason.

JeffD,

New houses in inventory, available, for sale, and on the market, most since Housing Bust 1 — what is so difficult to understand here? Open your eyes and look at the data:

Population in the USA in 2008 was just under 305 million people, population in 2000 was 282 million, and population in 2022 is estimated at 338 million.

I would expect that as population increases there would be more homes on the market in both boom and bust times.

Hi Wolf

Have you ever done an analysis of the average mortgage payment to the average yearly earnings of homebuyers in the United States. I often hear “mortgage rates are lower now than 1981”. And yes, this may be true but have earnings kept up with home price appreciation?

You’ve got to do local median household income v. local home prices. That’s the the only way this has any validity. I think I dabbled with it a few years ago for some cities. Doesn’t seem to be very helpful, and it’s not what I’m into.

One of our new developments had open houses for 8 different homes this past weekend! They are still way over priced, IMO.

The house next door to ours went under contract (pending) in two days after hitting the MLS. It’s as plain Jane as you can imagine, but fairly well maintained. It will be interesting to see what the selling price is when (or if) it closes.

All you need is one or 2 homes to sell at reasonable price for any neighborhood to follow suit. It’s a lot closer than you think.

Wolf a couple thoughts/questions –

1. What is the RE price to income numbers look like over the last 40 years?

2. How does housing price patterns differ in denser urban areas vs the rest of the country? You have shown how condo prices have been much flatter than home prices in the SF Bay Area and NY what thoughts do you have on what that shows us about these places that really have almost no new single homes being built. Thanks as always for your work.

Just the other day someone from the Biden administration was pointing to the falling price of housing as a good thing. Can’t remember her name. This indicates that they know what is coming and that nothing can be done to stop it, so they have to spin it as a good thing whether they believe that or not.

This is not intended to be a criticism or a complement of the administration. It’s just a report on something I saw on Bloomberg.

Time to wake up and watch the Movie Wolf’s charts tell it all

” the housing market in Las Vegas is slowing faster than any other U.S. metropolitan area, second only to Seattle”

Air Bags may be needed for landing

Seattle was propped up by Chinese money but the Chinese don’t buy into falling markets housing or anything else. So in theory home prices should fall to the level of the local’s income. When all the Chinese money exited Vancouver back on April 20th 2017 I told everyone all the money would go to Seattle and told everyone to buy homes with 8’s in them and homes as close as possible to the elementary schools and all properties on corners and don’t buy any homes with fours in the address.

As a mid 50s father of 20 something’s looking to achieve the American dream, it is astonishing how resilient the Midwest market is in spite of the referenced declining buyer traffic and market indices in this article, coupled with the increasing mortgage rates. My 20 something’s keep asking when will housing become affordable for them? I don’t know what to tell them because prices in our area seem to have the ability to defy gravity.

Probably never tbh

You need to wait at least a year or more.

This post should be mandatory reading by every scumbag FED member and CONgresscritter. Taking away affordable shelter is one of the most disgusting things a government and unelected bureaucracy has ever done.

A new study this week in the UK — where retail mortgage rates are currently hovering around 4% (variable) to 6% (fixed) — suggests that the relative price of mortgages in 2022, adjusted for much-higher debt and tax burdens in the modern age, is not far off the crazy 8-15% rates last seen during the 1970s to 1990s.

In other words, you might be paying a 5% UK mortgage… but it feels like 10%.

How are home builders, sellers and buyers doing in Venezuela and Turkey? I am guessing they have been dealing with high interest rates and inflation for some time.

Slightly off base, but in the same ballpark:

Conversation with local equipment dealer

Buyer: Geez, the prices are way up from just a year ago!

Seller: Yeah, about 20% or more, but can’t be helped, everything we order is more expensive to produce and ship, just can’t do a thing about it.

Buyer: I hear ya, my costs for fuel, food, insurance, taxes all up, way up too. Just can’t afford these prices so guess I’ll have to pass.

At what point in these interactions on equipment -or homes- or anything, become so prevalent that the result is no one is buying or selling anything. In other words, recession.

The usable resources of both the seller and the buyer are being reduced by inflation at rates much higher than the Gov’t will publish. At some point on the graph of each, they have crossed. I’d think at that point, recession became a fact, and will deepen until those two graph lines once again are nearly the same.

Just a dinosaur here, watching the passing parade.

Not until all that money that’s sloshing around is exhausted. Dealers still don’t have much inventory on the ground, I don’t care if it’s cars and trucks, tractors, excavators, dump trailers, or anything else. There is money chasing everything, STILL.

I heard FED mouthpiece Bullshitard was flapping his lips again today, talking about how inflation will be coming down “next year.” I didn’t know this guy was Nostradamus. But in the meantime, everything is UP, still. And it looks to be accelerating.

In fact, I was just checking out new Toyota prices and WOW is all I can say. Some models seem to be up close to $10,000 in the past couple years. Did incomes go up that much? Who, in light of the increase in health care, food, gasoline, insurance, etc., has an extra $10,000 for a new car? This clown show is unreal.

Did you see where he said he want’s the Fed’s rates to go at a minimum to push down inflation: 4.5% to 4.75%, and then wait and see.

And he also said that the Fed should not be concerned about the stock market. Essentially, to heck with stocks.

This was a very hawkish appearance.

Thank you. My interpretations are sometimes a little skewed by my hatred of the subhuman scum that is the FED.

I had a 10.5 % mortgage on my first house 33 years ago. My fifth and final house, which I bought a little over 5 years ago for retirement I got at 3.99% on a 15 year loan. My first house was tiny. My current house is tiny. My first house was brand new in the countryside. I hated living in the countryside – it was far from everything. My current, retirement house is in the city and close to everything. On top of that, it has now survived 2 major hurricanes – Irma and Ian. Both times I only lost my fence. My house is 65 years old, a year older than me, but it is a solid house.

I’m a noob in this space.. but I’ve been learning as much as I can. Thanks wolf for these articles and insights! I saved a lot of money in the past decade and couldn’t buy a home for personal reasons.. unfortunately now I’m not comfortable dipping my feet in this environment.

I wonder how long I would have to wait :(

Coming from Long Island, prices still remaining flat, or small reductions in price followed by taking it off the market and posting it again the following month as ‘new’.

Did find a nice home that was just about 100 yrs old but the seller ‘knows what he got’ and refuses to budge from his sky high asking price. It’s been on the market for 367 days at this point.

Im a Homebuilder from South Carolina, buyer traffic is very slow compared to even 60 days ago. Contemplating a 10% price drop to get remaining inventory sold. Doesn’t feel to good for the Fed to take a dump on the whole industry…

Thank you for sharing your experience. Much valued here.

Let me remind you that the Fed has “dumped” on yield investors, savers, and retirees for 14 years, has destroyed their cash flows, and has wiped many of them out. We’re talking about a HUGE number of people, some of whom comment here. Now we’re on the somewhat rough trip back to where it was before QE. 7% mortgage rates should be the norm when inflation is 2-3%.

Thank you, Wolf. As a saver I’ve been getting destroyed for almost my entire adult working life. At this point the damage is permanent.

Let’s review…

It was Late 2020-early 2022…

Just like car dealers continue to be today

home builders told us they “didn’t have time for us”

-“because-(insert lame excuse here) and we are sooo booked up and busy”.

Now look, they need us. Got cheap lumber? Yeah, buddy— bet you do now.

No true comparison to early 2000s housing bust and 2014 slump. The world is totally different now, trusted theories and predictions are mere conjecture.

Look around: there’s so many shortages

Short people shortage, tall people who are getting shorter shortage, clown college graduates shortage, the trees are quitting because the leaves left. Wood shortage has us stumped. There’s no water left, but the Earth is mostly water…o it’s salty…yeah we’ve known that for at least the last 4 or 5 years, just build it , you can do it. Ask the aliens for help.

I am sorry for those were have lost so much of their retirement funds/savings due poor management of this economy-that is no laughing matter. We all need each other, help one another- but somehow that is not in fashion these days- that makes me sad.