What the Fed did in details and charts. And, well, “Primary Credit” is starting to show up again.

By Wolf Richter for WOLF STREET.

The Federal Reserve released its weekly balance sheet this afternoon, with balances as of yesterday, October 5, that contained the month-end roll-off on September 30 of Treasury securities, which completed the first month of QT at full speed, after the three-month phase-in period.

At full speed, the pace of QT is capped at a maximum of $60 billion per month for Treasury securities and at a maximum of $35 billion for MBS. During the three-month phase-in, the caps were half that level.

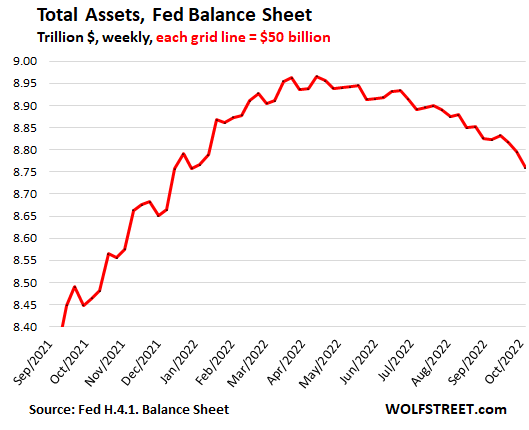

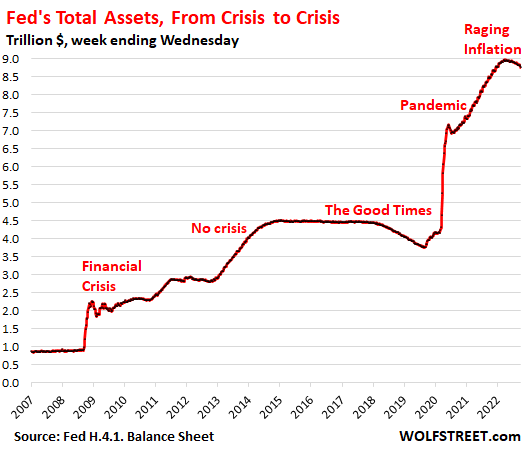

Total assets dropped by $37 billion from the prior week, by $63 billion from the balance sheet released on September 8, and by $206 billion from the peak on April 13, to $8.76trillion, the lowest since December 2021.

QT is the opposite of QE. With QE, the Fed created money that it pumped into the financial markets by purchasing securities from its primary dealers, who then sent this money chasing assets across the board, which inflated asset prices and pushed down yields, mortgage rates, and other interest rates. QT does the opposite and is part of the explicit tools the Fed is using to get this raging inflation under control.

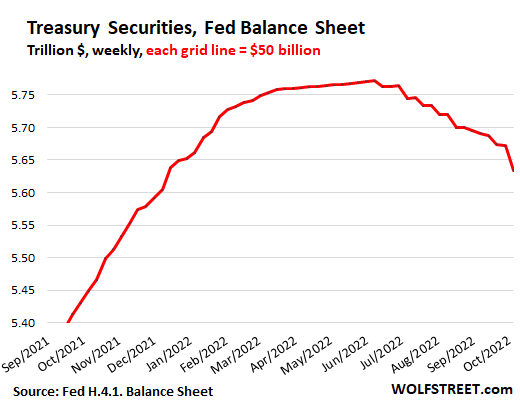

Treasury securities: Down $137 billion from peak.

Treasury notes and bonds mature mid-month and at the end of the month, which is when maturing bonds roll off the balance sheet. Today’s balance sheet includes the roll-off on September 30.

Treasury bills. In those months when not enough Treasury notes and bonds mature to get close to the $60 billion cap, the Fed also allows short-term Treasury bills (maturities of one year or less) to roll off to make up the difference. And this happened in September.

Treasury Inflation-Protected Securities (TIPS) pay inflation compensation based on CPI. This inflation protection is income to the Fed, but it is not paid in cash, as coupon interest is, but it is added to the principal value of the TIPS, and the balance of TIPS on the Fed’s balance sheet inches up until the next TIPS issue matures, which will be in January.

In total, Treasury holdings fell by $57 billion from September 7, to $5.63 trillion:

- Treasury notes and bonds roll-off: $43.6 billion.

- Treasury bills roll-off: $13.1 billion

- TIPS roll-off: none matured; next issue will mature in January

- TIPS Inflation Compensation: $235 million, non-cash income added to TIPS principal.

- Net change: -$57 billion from September 7.

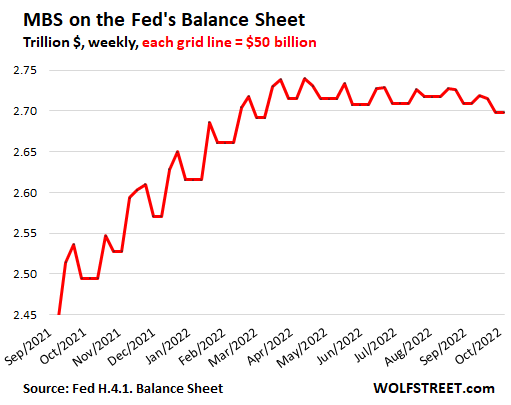

MBS, with 2-3 months lag: Down $42 billion from peak.

MBS come off the balance sheet mostly through pass-through principal payments. When the underlying mortgages are paid off as the home is sold or as the mortgage is refinanced, or when regular mortgage payments are made, the principal portion is forwarded by the mortgage servicer (such as your bank) to the entity that securitized the mortgages (such as Fannie Mae), which then forwards those principal payments to the holders of the MBS (such as the Fed). The book value of the MBS shrinks with each pass-through principal payment, reducing the amount on the Fed’s balance sheet.

But mortgage refinance volume has collapsed by 86% from a year ago to the lowest level since the year 2000; back then, the Fed had also embarked on a series of rate hikes, ultimately taking them to 6.5%. The collapse in the refi volume has turned the pass-through principal payments from refi into a trickle.

In addition, home sales have slowed, which further reduces the pass-through principal payments. Pass-through principal payments from regular mortgage payments continue at their normal pace.

The fading pass-through principal payments from the refi business is why the Fed is considering selling MBS outright sometime in the future in order to fill in the gap to the $30 billion cap.

MBS get on the balance sheet 1-3 months after the Fed purchased them in the “To Be Announced” (TBA) market. Those trades take one to three months to settle, and the Fed books them after they settle, which is when the trades show up on the balance sheet.

For a special geeky deep-dive into the Fed’s transactions of MBS in the TBA market and the delays involved, go to my analysis a month ago and scroll down to the section: “MBS, creatures with a big lag.”

So for most of the phase-in period, the MBS transactions didn’t reflect the phase-in period, but the “Taper” before it. In September and October, we’re seeing the transactions from the phase-in period.

The Fed stopped buying MBS on September 16 altogether, and so the inflow of new MBS onto the balance sheet, which is already small, will fizzle out in November.

The mismatch in timing between the days when the trades settle and show up on the balance sheet, and the days when the pass-through principal payments are booked and come off the balance sheet, gives the chart the jagged line, with flat parts in between when neither happens.

The MBS had one of those flat spots this week, at $2.698 trillion, down by $11 billion from September 8, and down by $42 billion from the peak on April 13.

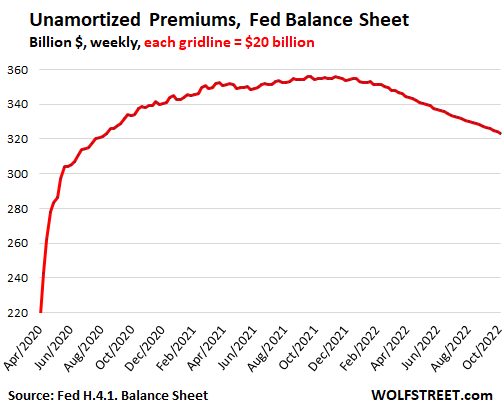

Unamortized Premiums: Down $32 billion from peak, to $323 billion.

All bond buyers pay a “premium” over face value when they buy bonds with a coupon interest rate that is higher than the market yield at the time of purchase for that maturity.

The Fed books the face value of securities in the regular accounts, and it books the “premiums” in an account called “unamortized premiums.” It amortizes the premium of each bond to zero over the remaining maturity of the bond, while at the same time, it receives the higher coupon interest payments. By the time the bond matures, the premium has been fully amortized, and the Fed receives face value, and the bond comes off the balance sheet.

Unamortized premiums peaked in November 2021 at $356 billion and have now declined by $32 billion to $323 billion:

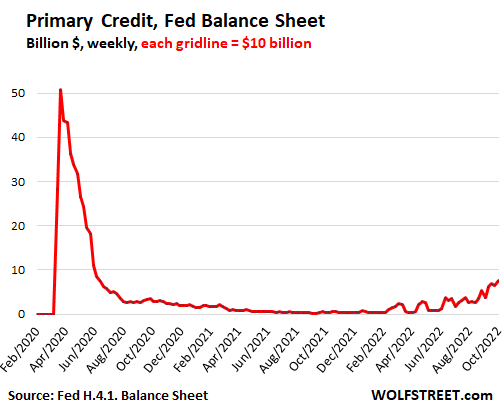

A note on “Primary Credit.”

The Fed borrows money from the banks when the banks put cash on deposit at the Fed (the “reserves”). The Fed pays the banks currently 3.15% in interest on $3.08 trillion in reserves. They’re a liability on the Fed’s balance sheet, not an asset, and they don’t belong here. I just bring them up because…

The Fed also lends money to the banks and currently charges 3.25% for it, charging more in interest than paying interest, as all banks do. The Fed does this through the discount window, called “Primary Credit” on the Fed’s balance sheet.

In March 2020, primary credit spiked to $50 billion but faded quickly and remained at very low levels. When the Fed started hiking rates in early 2022, Primary Credit began rising, though it has remained low. On today’s balance sheet, it rose to $7 billion, having doubled over the past four weeks.

It seems most banks have way too much cash and put some of it on deposit at the Fed (in total $3.08 trillion in reserves); but some banks don’t have too much cash, and borrow some from the Fed at 3.25% (in total $7 billion). In terms of magnitude, there is no comparison, but it’s nevertheless cute:

And here’s how we got to Raging Inflation:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Primary Credit’s punk ass needs to stop ‘staring’.

Good to see QT on Autopilot.

So 33% correction in Nasdaq and only 15% in real estate (extrapolating 4 month old case shiller index). Fed needs to get its MBS shit together, sell outright now before it runs out of time with falling stocks.

Real estate prices are “sticky”. All those people underwater holding out.

“Sticky” because they want the number the real estate liar told them it was worth.

It’s a great time to buy!!!!

when time comes for them to CAPITULATE

I’ll be ready with CASH

til then – keep paying that mortgage and taxes and insurance

Why would the Fed be in the business of profiting off it’s operations in the private market ?

I think that would be a criminal act.

The Fed may have their STG concerning MBS. It is not a problem for the Fed with it’s trillion dollar check book. It is certainly a problem for the private sector as home mortgage rates increase.

Where can I buy a 30 year bond, guaranteed by the US Gov’t paying 7.12 pct without a call.

Sticky because I have 3% interest and I don’t care what my house is worth because my mortgage payment for my 3000 sqft house is less than renting a 1000sqft apartment. And if I don’t need the house anymore I give it back to the bank to deal with. Play the game or be played

So…you saying a small size is cute?

“but some banks don’t have too much cash, and borrow some from the Fed at 3.25% (in total $7 billion). In terms of magnitude, there is no comparison, but it’s nevertheless cute”

Primary Credit is a measure of banks in distress. Be good to keep a close eye on it.

Also time to watch the FDIC and OCC regulatory reports on banks. They should be better off than in 2007-2009 when Bank Failure Fridays were a thing due to Housing bubble 1… except the Everything Bubble is much much bigger.

Lots of companies overborrowed on Legveraged Loan market at rates that won’t be rolling over nicely for a while. That’s going to start to leave a mark soon.

Recent analysis suggests that it is impossible to distinguish the difference between an insolvent and solvent bank, based upon their 10K filings.

At 15/1 leverage, a once in a whatever event would sink even the most compliant mega-banks.

Sleep well.

@Wolf –

Dumb question of the day: Is the argument that total assets at the Fed need to drop by roughly 50%, back to the trendline circa 2019 for us to be back in relative “health”? I would assume that total assets grow over time, so perhaps the figure isn’t quite back to $4.5, but is that a reasonable goal that officials may be aiming for?

…or, is that a completely arbitrary number to pick?

Yes, seems you’re about on target. I did some thinking and ballparking on this here:

https://wolfstreet.com/2022/09/05/by-how-much-can-the-fed-cut-its-assets-with-qt-feds-liabilities-set-a-floor/

Going by the trend line in last chart Fed never gets there!

However, now there is no option, thanks to the high inflation. So, somethings gotta give.

Either we are screwed

or we are TOTALLY BONED

I see a required recession, a deep one because the world is about to change.

John Maynard Keynes. 13. “The social object of skilled investment should be to defeat the dark forces of time and ignorance which envelope our future.”

So…with QT:

1. It’s happening! It’s really happening!!!!

2. It will continue until at least the midterms

3. It will continue until something breaks

4. You may not need a prime rate greater than the rate of inflation with enough QT

5. We are never going back to “normal” until after a hard recession

QT will continue util they double up and print the next $9 Trillion.

Agree, same as inflation.

Mindset changed, why should we work or save when we can just print money ?

The most damaging thing for any economy are disincentives to work, because production is what the economy is all about.

What disincentives do we have in the USA today?:

1) People retire early when they have large stock market and RE gains

2) People don’t work as much when they can borrow at 3-4% to get what they want.

3) Why work when the system is rigged against the worker? Not working and quiet quiting is a form of revolt against record high profit margins and foreign outsourcing.

4) With the pandemic, people have an excuse to work from home and be less productive and accountable (with exceptions, of course).

5) Heightened economic uncertainty creates volatility, which makes day trading and speculation a worthy distraction.

“The most damaging thing for any economy are disincentives to work, because production is what the economy is all about.”

So true, but the PHDs at Fed don’t care about real economy that now FUBAR, they only care about fake financial one.

Fed changed the terms of their dual mandate in August 2020 to favor employment over inflation, financial stability over inflation.

The change was cover for the Fed making a pivot earlier than most expect.

Perhaps much earlier.

“Fed changed the terms of their dual mandate in August 2020 to favor employment over inflation, financial stability over inflation.”

and the third mandate (see mission statement below) has been completely carved out due the fact if honored, the Fed could NOT have pushed long rates to the “extreme” ALL TIME LOWS as they did.

“The Federal Reserve Act 1977 states that the Board of Governors and the FOMC should conduct monetary policy “so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.”

(moderate = not extreme)

Is it a ‘dual’ responsibility? Stable prices, full employment and financial stability? That makes three. Or do the first two, automatically guarantee the third?

I think you must have meant “Quantitative Easing” or QE, not QT, which is tightening, which will be puny. The events in Asia and Eastern Europe have caused the world’s investors to flee to the US dollar, so US inflation is probably not as high as it could have been if many more nations were repudiating the US dollar as Russia and China are attempting. Nevertheless, I do agree that the “Fed’s” owners (via indirect ownership of district banks), the banksters, will not take the necessary actions to restrain inflation, because inflation is too beneficial to them and their cronies: e.g., their many, Ponzi-scheme, over leveraged companies are seeing their liabilities reduced each day that inflation continues.

For example, while the measure of inflation is arbitrary, and the current CPI method has its defenders, I opine that it is running at least at about 12% for the box of goods and services that average Americans need. Hence, like the many companies that have issued bonds at low interest rates to buy back their own stocks, thanks to inflation, the banksters are effectively getting negative interest rate loans: effectively gifts of some money with much more money to use interest free, because the interest rate that their “Fed” charges them is much less than the rate of inflation:

QUOTE FROM ABOVE:

The Fed also lends money to the banks and currently charges 3.25% for it, charging more in interest than paying interest, as all banks do. The Fed does this through the discount window, called “Primary Credit” on the Fed’s balance sheet.

END QUOTE

“3. It will continue until something breaks”

Something huge – the hugest thing the Fed is in charge of — has already broken: price stability (inflation). Everything else is a sideshow.

The day most folks realize this is going to be epic. Most do not seem to get it yet.

Wolf, inflation is a feature not a bug

Powell and the Fed want inflation right about where it is.

I do not think Powell does want inflation right where it is. (I think he is embarrassed)

However, you are very right to point out that there are reasons inflation might be welcome in certain quarters. Inflation directly reduces the true cost of paying back debt, of course. This has been discussed in the financial press, but less than I would have expected.

Inflation makes most people poorer. Most people do not want inflation. The largest debtors such as governments aren’t human beings and can’t want anything.

The individuals who compose these organizations have differing motives which do and will conflict, especially under conditions of financial duress.

Between 2009 and the initial stages of the pandemic, the decision to “print” was an easy one as it appeared to be cost free. It’s always an easy choice to borrow at or near 0%.

With the turn in the credit cycle in 2020, that’s over. Yes, there is still a minority that believes in idiotic concepts like MMT or doesn’t understand math to see the consequences of unsustainable USG debt trends. Those with the most actual influence aren’t about to voluntarily trash the USD by trading geopolitical “hard power” for fake paper wealth or to fund “bread and circus” for the public.

In a debt based monetary system with interest on money, thats right. Inflation is a feature, any interest rate other than zero inflate the amount of money. And inflation of money do soner or later translate to price rises.

Inflation is a huge thing for the Fed, but not by any means the hugest. The Fed is structured to target some inflation at all times, just not so much that it becomes a political problem. Their hugest nightmare is deflation.

Our current economy was built based on a cheap debt model. When, not if, increasingly expensive debt blows up some highly leveraged portion of the financial sector causing credit markets to freeze up, the Fed will be staring deflation in the face. They handle inflation slowly and methodically, but the deflation page of their playbook tells them to hit fast and hard, “Whatever it takes.”

Wolfstreet’s own excellent graph showing the value of the dollar over time should be proof of this. Inflation is the goal.

Agreed.

The Fed is responsible for the monster that they created and have a sacred duty to slay it. Few are aware of the pernicious nature of inflation. Worse than deflation in most cases.

I think that the recent, attempted run on the BOE and the apparent short term faltring of the long term gilt will be remembered as an iconic event as the opening event of the reconciliation between wealth and worth.

Why is it inflation has only been recognized when gas, food and other consumer goods increased a lot ? Rents in many medium and large cities, especially in the Pac NW, have gone up the last 5 to 10 years (emphasis) at a much greater rate than what was the stated inflation of two to three percent. But this was largely ignored by mainstream media and politicians.

Maybe a few sound bites and yes the homeless got media attention (still do, rightfully so).

Think Portland, Denver, Bellingham (Washington), etc.

Around 2016 or 2017 an apartment complex in Bellingham underwent new ownership.

Rents for a 2 BR apparently immediately from $1050 to $1500.

This is what I read from the renters there who were very upset by the 42% increase.

In Portland, a tenants rights group, Portland Tenants United, fought for rent control there precipitated by so called no fault (economic) evictions. Sometime around 2018 or 2019 Oregon adopted a limited form of rent control.

A 1 BR in an apartment complex near where I live in Spokane Valley, Washington went for $850 to $900 I want to say in late 2019, maybe early 2020. By 2022 it was now $1650 to $1750.

But, again, I want to emphasize that rents were going up 5 to 10% steadily in many medium, large cities in the NW going back not just to 2020, but back to 2014 or so… location dependent. Large shelter price increases certainly should qualify as significant inflation !

Someone tell the media and perhaps government officials.

“3. It will continue until something breaks”

Something huge – the hugest thing the Fed is in charge of — has already broken: price stability (inflation). Everything else is a sideshow.”

QE continued until something broke: raging inflation, as Wolf says above.

Now, QT will continue until it breaks something, as happened in England recently.

Then, QE will recommence. Then, QT. Etc.

Meanwhile, the amount of time between the two phases continues to shrink, and the Fed’s remaining oxygen levels dwindle to nothing. In other words, they are trapped.

Elements of NFCI/ANFCI are going positive which is showing that QT is starting to work. But in both measures Leverage is still negative. That’s the genie in the bottle for the Fed, so there’s still a ways to go.

And here’s how we got to Raging Inflation… Wouldn’t that also be a function of the overall government spending and not just the Federal Reserve? The cares act for starters

Nope. The Inflation Reduction Act fixes that.

Now this, “The Inflation Reduction Act fixes that.” is a laugh riot!!!

Inflation is expansion of the amount of money, simplified “money printing”.

Over time this will weaken the purchasing power of money and prices rise. Or rather the exchange rate between money and goods and services change to reflect the lower purchasing power of money.

100 percent correct!

The per child money from the government to families cut the child poverty rate in half. One in four children in America grow up in poverty. While, I’m aware that special children can overcome the adversity of a competitive society as America fashions itself as

kids growing up in poverty doesn’t seem like a good strategy to me.

Whatever we can do will help. A kind heart travels so much further than a cold dollar, as my grandfather miner used to try to tell me while I was full of myself.

Well, I’m still full of myself, aren’t we all, but I find myself remembering him.

Wolf, why do they cap QT or what’s the point of capping Treasury securities at $60 B and MBS at $35B? Why not roll off more?

I wouldn’t have, and they shouldn’t have, but they did in order to keep it predictable. There are some months when something like $120 billion in Treasuries might come off, and they think that markets might have trouble digesting that. Other central banks, such as the Bank of Canada, don’t cap QT.

Yeah, but the Bank of Canada’s QT has happened in fits and starts. You had that great article showing how they eliminated their most problematic assets first… but for market participants it wasn’t so easy to figure out what they were up to at the time because their QT started and then seemed to stall. Going forward I expect the BofC to do QT more like the Fed does.

So far, the BoC has stuck to its plan of just letting roll off what rolls off. This works OK. There are periods when nothing matures and rolls off, and then there’s a period when a lot matures and rolls off. Markets can figure this out ahead of time by looking at the maturity schedule and adjust to it. I really don’t see the problem.

But there is a difference. The BoC never bought many mortgage bonds — which are unpredictable. Nearly all of the securities that the BoC still has are Government of Canada bonds (there are small amounts of other stuff). And they’re very predictable. Everyone knows years in advance what will mature and roll off, and then it rolls off.

It’s a one-way ratchet, and I don’t like it. If the amount that rolls off is under the cap, then that’s what it is. If the amount that would roll off is over the cap, then the Fed buys to stay within the cap. If they’re going to implement a ceiling, they should also implement a floor. Otherwise, let it be as it will be.

But it’s working pretty well. Look at the markets. Prices down, yields up, housing market sagging… but all in more or less an orderly manner. I’ve become kind of a grudging admirer of this type of QT: not too fast to crash things all at once, which would trigger a Fed pivot, but fast enough to do the job (see the markets), without triggering a Fed pivot, so that it can run for a few years.

Yeah, the Fed shot themselves in the foot last time (2017-2019) not with their QT policy (which was well understood by the markets) but rather with the interest rate hikes they added on top. Nobody knew when or why the next one would happen.

Obviously they wanted to restart QT after the markets took a breather. I wonder where the Fed would be if we hadn’t had the COVID runup.

“I’ve become kind of a grudging admirer of this type of QT: not too fast to crash things all at once, which would trigger a Fed pivot, but fast enough to do the job (see the markets), without triggering a Fed pivot, so that it can run for a few years.”

I’m not. It’s a page out of Yellen’s “watching paint dry” book, and it’s ripping the Band-Aid off one hair at a time, extending the duration of the pain, especially for the working class and the poor.

We need a massive, quick crash that is extremely painful but “right-prices” everything and destroys the insolvent – both businesses and individuals. Only then can we get back to something more sustainable.

What the FED is doing right now can only be described as having their cake while eating it, too. I’m sure all the wealthy insiders are delighted.

PS – There should be no such thing as a “FED pivot.” QE should be taken away from them permanently by CONgress, and their only mandate should be stable prices, so they are forced to hike rates above the rate of inflation no matter what. F**k the stock market.

I agree – although I am just a novice compared to others at this site – and am relying on my three economics courses at Uni almost forty years ago and current reading to understand. I have read, sorry can’t site the sources, that doing QT too quickly would send too much of a shock through the system. To be honest, I didn’t think this wind down would be working this well and I am glad the Fed is taking this systematically and slowly and seem to be “starving the beast.”

When a man throws himself from the 15th floor, he says at the 14th (for now, everything is fine), the same at the 13th, 12th, 9th … 5th …

Because the problem is not how you fall, but how you land.

FED will pivot at some point and as Powell only a year ago talked about “transient inflation” (pure insanity), they will pivot before they should. It’s like Bernanke bailout of the banks.

This situation is completely new: raging inflation + everything bubble + highest debt in history + historically strong dollar against nearly all currencies (pound, euro, yen) …

There are just too many things that can spiral out of control, to make me think that Powell is Volcker. He is not. If he were, he would never have spoken about “transient inflation”. He would have acted … and he didn’t.

This FED is weak.

I guess they are stalling on more aggresive QT until interest rate hikes stop? Seems like another catastrophic error on the part of the Fed. It seems like they should be going much slower on the rate hikes and much faster on the QT, despite liquidity being the problem. If rates weren’t being hiked so quickly, then removing liquidity with aggresive QT wouldn’t be as much of a problem, right? Am I missing something? It seems people are going to “pay whatever” as long as there is too much money in the system, so clawing back a good chunk of that money as quickly as possible should be job #1. If asset prices fall, some wealth holders get burned, but they are the ones with outsized gains, so they have nothing to justifiably complain about. What’s wrong in this analysis? Politics?

Rates are only being hiked “quickly” relative to the ridiculous prior practice of quarter point increments.

Rates have been abnormally low for most of the 21st century and even ignoring inflation, come nowhere close to reflecting actual credit quality of outstanding debt which means that risk is still being grossly underpriced.

Relative to the past, aggregate credit quality is complete garbage. It only appears sound due to the distorted economy and asset mania which inflates revenues, incomes, and tax receipts.

Looking at the 3 month T-bill, the yield better rise if the fed wants to raise the effr by 75 basis points!

Essentially, you are on the right track in the sense that the so-called markets are chaotic as the paradigm changes from zirp and QE as the dominant economic policy to QT and interest rate hikes as the dominant economic policy.

Which ox will be gored remains to be seen.

So let me get this right. I deposit cash in my banks money market account and they pay me 0.1% interest, they then deposit this excess cash at the Fed and get paid 3.15% ?

Think of it this way: You are saving the financial system by way of your generosity.

It is called a “lock”.

A gift to banks beginning in 2008.

Mike T,

If you get 0.1% at your bank, it’s your OWN fault for not changing banks. Lots of banks are paying over 2% on savings accounts, and brokered CDs offer 4%+. (Treasury bills offer over 4% at Treasury Direct, designed for people just like you and me.)

Quit complaining and move your money! That will force banks to be competitive. It’s loyal customers like you that banks love to rip off

https://wolfstreet.com/2022/09/23/to-compete-with-spiking-treasury-yields-banks-now-offer-4-on-brokered-cds-of-six-months-to-five-years/

Wolf, I agree wholeheartedly with your advice and I would like to move money to a better paying account I also have, but I have a credit card (freeloader, paid off each month) with the bank ripping me off. If I move the money out of the ripoff account will they likely cancel my credit card, which I have a good cashback rate on?

No need to answer if you don’t feel like it, but would like knowing for sure if it’s wise

good point ZSG, and will reply with the experience WE, in this case the family WE have:

We continue to keep the ”savings” account with another bank from our CCs, and have had no issue FKA problems, so far…

Both banks are part of the continuing consolidation in the bank industry, so some bank names have changed more than once in the last couple decades.

So far, So good…

NOT counting on any long term stability from either bank due to the possibility, however remote, that some reality will come to that industry IN SPITE of the massive efforts to keep control of the parts of the GUV MINT that are supposed to oversee and regulate that industry.

My credit card has paid better cash back interest to me the past 14 years then any savings account. Really shows you were the priorities are in this society eh?

George Bush after 9/11: GO out and buy a car, go to the mall, shop!

Its always been a fleecing system, people only notice when a crisis happens ;)

Just keep $1,000 in that bank account for the credit card and move the rest and get that 4%+ interest.

Apples to oranges again. Banks get 3.15% overnight. To get anywhere near that rate requires a 90 day commitment by an individual.

I told you this before: You roll over repos every day, and you can sell your 3 month treasury any day if you need the cash. Same thing. That’s why Treasury bills are used for cash management.

BTW, If you buy 500,000 cars a year, like a rental car company, you’re going to get a much better price than if you buy one car every 5 years. That is true everywhere, big volume, lower price. What’s your problem?

Wolf said: “you can sell your 3 month treasury any day if you need the cash.”

—————————————

I will check this out and see what discount I have to take, what fees it would cost, and what platform I have to join …………………

Well, yes, if you want to manage your money like a semi-pro, you’re gonna have to do some basics.

The Fed will pause rates at some stage and they have made that clear.

QT is more consequential than rate increases because it will expose specious asset prices, caused by an abundance of QE, and shred business models relying on them.

Something already broke in the UK. The fragility of the bond market was laid bare, albeit fleetingly.

Something will break again.

If anyone thinks the extent of the damage caused by unconscionable levels of QE is 8% inflation, a surprise is coming.

What already broke is price stability (we have raging inflation now). That’s the biggest thing central banks are in charge of, and they went out and BROKE the damn thing. So now they’re trying to fixed it. And yes, lots of stuff is going to break along the way to fixing price stability.

When the FED pivots deploy all your cash, will be at the bottom.

When the Fed pivots is when the real crash has just begun. Read some of the Hussman articles for historical examples.

It wasn’t the bottom in the 1970s. The Fed pivoted, then had to pivot back, and then pivoted again, many times. And it got worse each time. The Fed is now trying to avoid this fate, but I’m not sure they’re able to. This will be interesting to watch.

The time to buy is when — if ever — QE re-starts. Without QE, these markets are going to have a rough time.

But QE finally broke the inflation dam, and so now I’m not sure how much appetite there will be in the future to restarting QE. Everyone is learning a lesson here. They may revert to using repos to calm liquidity issues, which is what they did before QE. And that calms liquidity issues but doesn’t pump up markets like QE does.

Restarting QE doesn’t mean stocks take off. Look at EU markets and Japan. Someone can make the claim that prices would be lower without past QE, but no one can prove it. Japan is about 33% below its 1989 peak. European markets essentially flat to down (depending upon the country) from both late 90’s and pre-GFC.

It may not be next time, but the day is coming when FRB QE will also fail to inflate stock prices.

AF,

Maybe QE has inflated Japan and European markets and their markets are still way down or flat because the fundamentals are so bad. In other words, their markets are still substantially higher than they would be without QE, even being down or flat. Since QE seems to work by bringing future returns forward, it seems possible that eventually QE stops being effective once there are no realistic returns to pull forward. Maybe Japan and the EU reached that point sooner with explicitly negative rates.

You’re right in that the end result is still that QE will eventually fail to inflate US stock prices.

I think it was 2003, the S&P index had declined to a level I was sure was the bottom. I deployed the cash I had been hording, buying at a weak support level that subsequently went on to fall in half.

I suggest that the days of pumping up the markets are limited.

just saying

1) Bills expire faster than bonds. Selling the long duration at higher speed lift interest rates, thus less inversion, while the Fed is raising rates.

2) Fed real assets : total assets minus RRP.

3) If DXY will weaken SPX & gold will popup.

4) The economy is changing. We will produce what we must have, what is really is necessary. The infantile we must have it now, creating shortages and bubbles will be on hold. Within few years we might create a global over supply. Tariff will rise to protect our “infant industries”.

5) Risk off. To reduce nuke risk munitions supply might be cut by half.

Michael,

predict me a price of gold in 6 months please. What do the charts say?

Rising interest rates and U$D correlate to falling PM prices. Historical charts indicate rising interest cycles take an average of 2.1 years to peak. So a best guess is PMs 6 months from now will be lower, barring some minor glitch like WW3 or widespread credit collapse. Reinforcing the above view, seasonal gold charts indicate PMs drop in Feb, Mar, May, June. So wait for the first FFR cuts in early 2023 to buy PMs.

No kidding, gold has failed in it’s principal purpose for inclusion in any portfolio, as a hedge against inflation.

There’s an interesting correlation between the drop in margin debt and the Fed’s QT, where the balance in margin accounts are a lead indicator, but unfortunately the data on margin account balances is monthly and delayed by 7 weeks.

$147 billion drop in margin debt from Feb to Aug

$206 billion drop in Fed assets from April 13 to Oct 5

The correlation is between QT/rates and stock prices. Then there is a separate correlation between stock prices and margin debt, which is why there may seem to be a correlation between QT and margin debt. But QT is new, and margin debt has been around for decades.

There is a scary sequence: SPIKES in margin debt are followed by sharp sell-offs in stocks that then trigger deleveraging and declines in margin debt, which trigger more declines which trigger margin calls and forced selling which trigger further declines in stock prices. This stuff can get pretty bad after a big spike in margin debt.

I call margin debt “the big accelerator on the way up and on the way down.”

This chart hasn’t been updated in two months, but you get the idea:

One would assume that margin borrowing would be correlated with a number of measures of speculation. The correlation between margin debt and QE since 2008 or so is highly correlated. I suspect that your linear regressions are limited by the small sample of statistically significant periods which typically are on the order of years or decades.

The FED is doing what they’ve been saying they were going to do since last November – Raising rates and implementing QT.

Disbelieve at your own risk.

ALL the markets believe they will continue to do what they say. Just look at real estate sales, vehicle sales, stock and commodities prices … all dropping dramatically based on higher expected interest rates. And the dollar keeps climbing as foreign money seeks safety and yield.

Disbelieve the FED at your own risk. It’s like swimming in a lake with a Beware of Alligators sign. Don’t cry if you get eaten alive.

.-._ _ _ _ _ _ _ _ _

.-”-.__.-’00 ‘-‘ ‘ ‘ ‘ ‘ ‘ ‘ ‘ ‘-.

‘.___ ‘ . .–_’-‘ ‘-‘ ‘-‘ _’-‘ ‘._

V: V ‘vv-‘ ‘_ ‘. .’ _..’ ‘.’.

‘=.____.=_.–‘ :_.__.__:_ ‘. : :

(((____.-‘ ‘-. / : :

(((-‘\ .’ /

_____..’ .’

‘-._____.-‘

Option for fun and entertainment only : the Dow gap and crossed June 17 low. It landed on Sep 30 high. Today low might be a test of Sep 30 low.

Again it’s just an option : the Dow might move higher…

If wrong sell.

On the bright side, with $2.7T in MBS’s, the Fed likely does not want the housing market to crash with massive foreclosures.

Does J Powell have room on his desk for $2.7T in home keys being jingle mailed in?

Does anyone have his address?

The Fed has trillions of skin in the game to prevent this from happening.

IMHO, this is a minor reason why house prices won’t crash too far. They will drop just enough to prevent Jingle Mail.

LocationX3 Bob:

As per the last couple dozen ”crashes” in RE,,, some places will see massive drops,,, some places will see small and brief drops…

While we can all see ”some” of the carnage already happening in ”some” local RE mkts, others are going nowhere at all…

Kinda sorta have to pay attention to the locale, eh

The home prices need to go down everywhere. The cheap money was not a local phenomenon, it was a global phenomenon.

Now all over the world, CBs are raising rates and doing QT with few exceptions.

No need for jingle mail.

Folks who bought in last 2 years have locked in very low rates and won’t sell unless they are forced to.

I guess it’d be an orderly price decrease in next 2 years or so.

No need for crash.

Prices need to come down quite a lot and I think it’d take some time.

The show has already begun, low volumes, slow dropping prices, rising rates.

For the asset bubble to come back to reality, home prices need to come down quite a lot and it’d be a slow grueling process.

People who have vested interests think this won’t happen.

Who knows ?

In a down market, paying any amount of interest for a home makes little sense. If you have flexibility, it makes way more sense to rent if home prices are declining, particularly when downsizing is attractive.

Many buyers and sellers will figure this out, and they’ll bring prices down for everyone.

If I had a 3% 30-year mortgage, I’d be thinking seriously about selling at the top and renting. The only thing you know for sure is you have a large gain now that can be captured. It might not be there next year.

People can always enter the home market again at a later time after prices fall. That’s how you build wealth.

That would have worked if you sold in 2006 and purchased again in 2012. 6 years. Timing the housing market is too scary for me.

1) You have to make enough to overcome to 10+% selling and buying costs. Including capital gains tax during the year you sell.

2) Your crystal ball has to work to time it correctly.

3) Your moving and rental costs could eat into any profits if rent continues to rise.

4) I don’t live light enough. Too much stuff to move around.

I know of one family that tried it by selling in 2005 and buying in 2014 (9 years of renting). They broke even. According to them.

Bobber – “If I had a 3% 30-year mortgage, I’d be thinking seriously about selling at the top and renting.”

That’s pretty poor advice for most.

From a practical standpoint, in most locales rent is now higher than payments on a 3% mortgage and rents are still increasing fast.

But from a pure numbers standpoint, a 3% mortgage is now a valuable asset. Selling means you give up that asset for nothing. Nobody should be giving up a 3% mortgage without some careful thought and calculation. There are many ways of valuing this depending on assumptions:

The mortgage industry when selling discount points (which builds in assumptions about holding period etc) would value a 3% mortgage vs today’s 7% mortgage at about 16% of amount financed. That is, if you have a $300,000 mortgage at 3%, in today’s world that mortgage is “worth” about $50,000. That’s almost certainly an underestimate, and mortgage companies don’t offer discounts this large because anybody paying this much certainly expects a longer than average holding period.

If you actually use and pay the mortgage for a full 30 years, the current value of 3% vs 7% is around 30%, so a giving up a 3% mortgage on $300K is a “loss” of about $90,000.

And you say you can just buy back in later. Do you realize that the increase from 3% to 7% interest requires a price drop of around 36% just to achieve the same payment on a 30-year? (reduced to about 30% if down payment is fixed vs 20%). Those kind price drops are pretty unlikely in most markets, and that’s just to break even on payments. So basically you’re betting the farm that prices and rates BOTH will come WAY down in the future, because that’s the only way to “get back in”

Everybody’s situation is different and they need to go thru the numbers themselves, but generally speaking, if you think prices are coming down, then it’s not those with high loan-to-value, low-interest mortgages which should be thinking about selling, but rather those with large amounts of equity – especially those that own outright. They not only don’t have as much “mortgage value” to loose, but should be able buy back in with cash if prices drop but interest rates don’t.

UrsaTaurus,

That is a good way to look at it now. What is the value of a 3% mortgage today? ie if you sell your 3% mortgaged home and then try to buy another house with a 7% mortgage.

You noted that you cannot buy down the 7% mortgage to 3% today. If you could, it would cost you $50K-$90K in points as you pointed out.

However, if your crystal ball tells you that housing prices will crash which will cause the Fed to react and lower rates to 3% again, then trying to time the market might work. It all depends on whether the market does crash and how well you can time the market. Also, take into account buying and selling costs, moving costs, rental costs………

Based on history, I wouldn’t bet on 3% mortgages again so buying your next home in 4-6 years at the future bottom will cost you more in interest.

I think I know when to hold them and when to fold them. I’m holding them now.

jon – the problem is different than during the last run-up. this time we have a demand-side problem and due to inflation, the Fed cant just drop interest rates and stimulate demand.

i think that there will be many people who have bought in the past couple years that will walk away – once they are underwater by 10% beyond their down payment and have lost a job.

china has experienced a mass boycott on paying mortgages – different situation – but it might become quite the trend to just walk away. people know when they have been screwed

They’re guaranteed by the taxpayer (Fannie Mae, Freddie Mac, Ginny Mae, etc.). Don’t worry about the Fed, worry about the taxpayer.

Good point.

Worry about the politicians bailing out Fannie and Freddie.

I’m not convinced that the short duration of the Fed financed housing bubble will result in a foreclosure crisis. A small group of wealthy people over payed for housing. I hear them crying to be made whole by the government as well as you do.

They were only trying to gouge the little people, provide some incentive for them to work harder.

There are fears from CEOs that Canada will be in a deep recession next year due to QT.

Will the Bank of Canada act as a plunge protection team and cause a currency collapse while the FED is tightening until 2024?

The Canadian peso is reaching 70 cent levels despite 100-dollar oil. If the Bank of Canada (BoC) lets the interest rate become lower than the US, the Loonie will go lower.

If this is a plan by the powers that be to debase the Canadian dollar to make it cheaper for foreign buyers, then why isn’t this tantamount to crimes against the country?

Canadians are suffering big time because of the greed in the housing market and the labour market is different than the USA where the economy is stronger than Canada.

I’m confused. I remember reading about the Canadian housing bubble a decade ago. And no one did a damn thing about it. And now someone is supposed to wave a wand and neutralize the collapse of the Canadian Housing Bubble. A home grown malady, worthy, but not deserving of empathy for their current dilemma.

Most excellent article. Thanks for the unvarnished view of the data as reported. I have a comment but I want to be an olf and post a portion of the commentary before the comment, a quote:

“They were careless people, Tom and Daisy- they smashed up things and creatures and then retreated back into their money or their vast carelessness or whatever it was that kept them together, and let other people clean up the mess they had made.” ― F. Scott Fitzgerald, The Great Gatsby

The wailing and moaning by the rich about the evil Fed making there leveraged assets worth less. It seems ridiculous, watching it. Reminds of something I can’t quite put my finger on….

Almost a plea: just one more shot of Uncle Ben’s elixir.

I’ve seen all this before. QT then a crisis comes around and bail outs come back, more QE. Next crisis right around the corner. Let’s see Wolf at the beginning of the year you said the FED could wipe out $4 trillion easy. The year is almost up what happened to wiping out that $4 trillion. $206 billion is a far cry from $4 trillion. And you made that statement in a comment.

Hahaha, I knew that there’d be someone that confuses “maximum” with “minimum,” happens all the time, no biggie, but it’s still funny.

This is what I actually said:

“So four years from now, based on these estimates, the floor for total assets on the Fed’s balance sheet would be about $5.2 trillion, below which the Fed could not go. At the peak, the Fed had $8.97 trillion in assets. So my calculus says that the Fed could do a maximum QT of about $3.8 trillion.”

Read the whole thing and bookmark it because it’s really important:

https://wolfstreet.com/2022/09/05/by-how-much-can-the-fed-cut-its-assets-with-qt-feds-liabilities-set-a-floor/

My Bad. And I said it was in a comment you made not a article. I couldn’t find the Quote I was looking for and my time is better spent doing other things than tracking down a comment. I believe this one is close enough and more drastic than the $4 trillion you said could be cut easily from the FEDs balance sheet.

Quote:

* Wolf Richter Dec 23, 2021 at 3:24 pm Tbv3, “..return to September 2018” Typo: September 2019. The first $1.7 trillion of Quantitative Tightening is just going to reverse the $1.7 trillion in reverse repos (RRPs). So that’s not even tightening. Anything above it would be actual QT. The Fed could easily take its balance sheet down to $4 trillion. It now has standing repo facilities, and the repo market knows this, and there won’t be any kind of repo market blowout, like there was in Sep 2019, when the Fed didn’t have a repo facility and the repo market panicked.

Not only has their balance sheet not gone down since you made that comment. It went up that’s by your own charts. So explain how is it they could easily cut their balance sheet to $4 trillion? They haven’t cut it at all, it went up. Your comment made at the end of last year. Now correct me again!

Jeeesuslordalmidy. What effing lie! First chart in this article. RTGDFA: