In terms of diversification between stocks and bonds, there is none. Not anymore. They even nailed the bear market rally in lockstep.

By Wolf Richter for WOLF STREET.

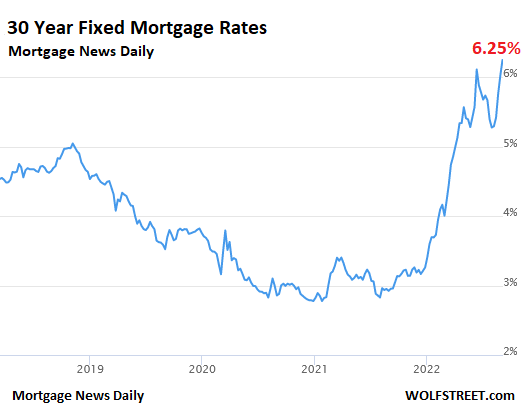

The average 30-year fixed mortgage rate, after weeks of enormous day-to-day volatility, was back at 6.25% on Tuesday, according to Mortgage News Daily. Today’s rate was just about even with the June-14 high of 6.28%, before the beautiful summer bear-market rally set in and turned everything upside down for a couple of months. With mortgage rates, that rally has now unwound.

I call them holy-moly mortgage rates because that’s the sound people are making when they figure the mortgage payment at those rates to buy their dream shack at today’s ridiculous prices (chart via Mortgage News Daily):

Treasury yields jumped, some to multi-year highs.

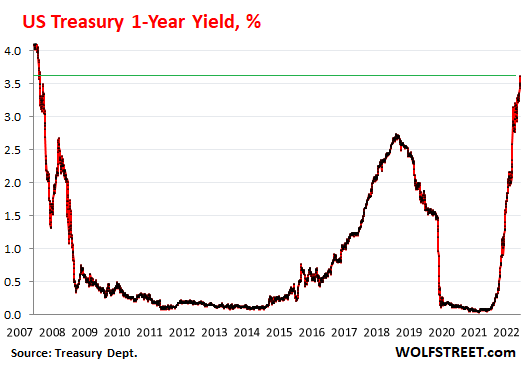

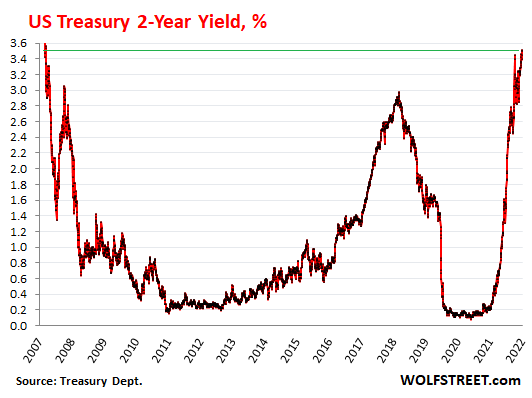

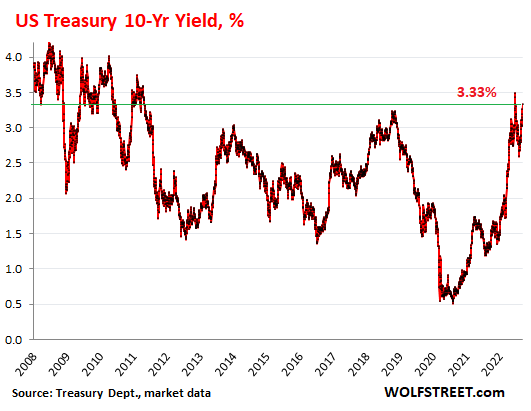

The bear-market rally was quite something. It started in mid-June and ran through mid-August. Both bonds and stocks surged, and then began unwinding the surge. While stocks have only partially unwound the bear market rally, mortgages and Treasury securities have unwound all of it already.

The 1-year Treasury yield jumped by 14 basis points, to 3.61%, the highest since November 2007. The spike started in November 2021, from near 0%. The summer bear-market rally was shallow and is barely visible in the long-term chart:

The 2-year Treasury yield jumped 10 basis points today to 3.50%, nearly matching the 3.51% last Thursday, which had been the highest since November 2007. The spike started in September 2021, when the Fed had its infamous pivot, the real one, and the 2-year yield reacted instantly. The summer rally was a little more pronounced than with the 1-year yield:

The 10-year Treasury yield jumped by 13 basis points today to 3.33%, the third highest since February 2011, behind only a couple of days in mid-June before the summer bear-market rally kicked off, which has now been wrung out of the 10-year yield:

The 30-year Treasury yield jumped by 14 basis points to 3.49%, the highest since September 2011, having squeaked past the November 2018 high. The summer bear-market rally is nicely visible in the chart, but right in line with other short-lived rallies:

So now there is all kinds of hand-wringing about the end of the bear-market rally that had been so much fun over the summer and that ended in mid-August at which point stocks and bonds began to spiral down again.

In terms of diversification between stocks and bonds, there is none. Back in the day, there was. But not anymore. They were going up together – when bond prices rise, yields fall. And now they’re going down together – when bond prices fall, yields rise. They even nailed the summer rally in lockstep. It’s just a question of which moves faster.

In terms of the bond market, corporate bond issuance came back to life as companies are trying to lock in still relatively low interest rates. According to Bloomberg, about 20 companies – including Lowe’s, Walmart, Deere, and McDonald’s – are lining up $30 billion to $40 billion in bond offerings this week, looking for buyers. And this apparently has caused Treasury yields to spike, or whatever.

There is always one reason or another that we can cite why yields are rising and unwinding the bear-market rally.

At the most basic level, markets spent two months, from mid-June through mid-August fighting the Fed, blowing off its hawkish statements, and citing stuff out of context to conjure up delusions about the Fed being in fact dovish and on the way to a pivot. As the tightening deniers fanned out and spread the gospel of the pivot, enough folks took it seriously, and so there was the summer bear-market rally.

But by mid-August, under steadfastly hawkish Fed comments, the rally petered out. And then came Powell’s Jackson Hole speech on August 26, which cleared up any remaining confusion.

So now we’re back to basics: The path of inflation, QT ramping up to full speed this month, the coming rate hikes, and still way over-inflated markets, along with speculation about when the Fed would pause to let the higher rates sink in – at 4%? – and let them and QT do their magic hopefully on cooling inflation and the labor market.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

As you’ve discussed before, it’s the collapse of the everything bubble. Bitcoin is going down just like everything else. Honestly I could see the S&P 500 going down to March 2020 lows. This is purely crystal ball speculation.

Anyway, thanks for the detailed info to add more context to everything Wolf.

How about S&P 500 to 2009 levels?

At least.

People just aren’t getting this. The stock market has moved in lockstep with the Fed balance sheet since the beginning of QE.

It is easier to just look at the 10 year Treasury rates – as they rise (providing a riskless return at decent levels) they provide a better and better alternative for that universe of hugely overvalued assets (drawing money away from said assets).

Average people don’t think in these terms (because rates have been absolutely gutted for so long and because most people don’t put asset values in historical context) but institutional investors (70%+of the mkt) do – interest rates form the absolute core of their discounted cash flow analyses (DCF) which is exactly how pros evaluate investments.

666

That would make sense if the Fed dropped their balance sheet to pre-QE levels, which they won’t… Wolf just wrote an article on the Fed’s minimum liabilities and pointed out that the Fed has a hard floor at $5+ trillion after 4 years of QT.

Here’s the thing… Is there a realistic chance the Fed holds strong on QT for years to come? Nope. The system has already shown that it can’t even handle a 2.5% FFR with slow QT back in 2018. That same system is clearly breaking again with faster QT despite a still deeply negative real FFR and we haven’t even crossed over a 2.5% nominal effective FFR. The Fed would have to hold strong into a deflationary depression, and there is a 0% chance of that sort of behavior by the Fed.

Please stop. There is every reason to believe QT will continue for quite some time. A deflationary depression is not on the horizon.

There is no deflationary depression, not even a hint of it. Could come? Sure anything can happen. But right now, labor markets are still overheated, with way, way more job openings then even the hottest economic expansions of the past 25 years, and inflation higher than anything in 40 years.

That is why, This Time Is Different. It really is. Inflation has tied the Fed’s hand, and what’s more, even the President is on board with higher rates because inflation kills his approval ratings much more than a bear market in stocks and housing.

I see your point, and those that disagree with you and still really don’t know which way to lean. This will be interesting to watch.

A huge portion of our productive economy is dependent on debt spending on cars and houses. If that dries up, so do many good jobs building and servicing those things. It doesn’t take long for those industry downturns to bleed over into others and the contraction feeds on itself.

Yes employment is strong now, but how strong will it be after a year or two of “high” interest rates choking off demand for big ticket items?

I know our economy is mostly services, but we can’t all just sell each other lawn mows and hair cuts forever.

The FED will do whatever it’s owners tell it to do. Whose wealth are the owners of the Fed interested in growing?

Cyto and Lune, I didn’t say there would be a deflationary depression. I implied that the Fed would never allow one, that they won’t hold to tight monetary policy for a period long enough to cause deflation. Inflation is the only thing they know, they just want to keep it to 2% so the torches and pitchforks don’t come out. As the effects of QT and increased interest rates set in, we may see inflation moderate pretty quickly in 2023, at which point the fed will let off the brakes a bit. This smoke and mirrors economy can’t survive the 2 or 3 or 4 years of QT necessary to meaningfully shrink the Fed’s balance sheet. The Fed is going to be in a position to ease up well before their balance sheet can shrink by much.

QT and a higher FFR are already working, and their effects are going to become amplified. If houses aren’t selling and products stop flying off the shelves, and services stop being rendered due to demand being choked off by the Fed, the job market will weaken and inflation will abate quickly. The Fed won’t have tight monetary policy beyond that point.

I fully disagree that this inflation is really long-lived. Here is why.

Inflation is based on two things – supply chain disruptions and high demand for consumption.

The high demand part is in large part based on 1) bank balances that got pumped up with free stimulus money 2) housing equity that got pumped up 3) credit card balances that got paid off with stimmie money 4) stock market gains and now are heading back to previous balances. The bank balances are headed back down, the housing prices are plummeting (although it will take time to fully see this) and credit card balances are getting back to levels where they are maxed out (or back to normal levels).

The supply side still has some issues, but many of those are going away as port traffic normalizes. There are only a few areas, like autos, where there is still supply constraint that is preventing a return to normal pricing conditions. The auto market is highly competitive and prices will return to normal in another year max. There will likely be an overshoot of production in the next year and then the prices will fall on autos.

The only real area of sustained price inflation is in services, and these might be areas where people have less choices – higher education, rent, etc. That will be the toughest area to turn around inflation. But I still see it happening within the next year.

As far as a strong employment market, sure maybe for a little while, but keep in mind that a large number of people had left the workforce. As all that free money runs out, stocks lose their value and home prices fall, those people cant afford to believe they are “retired” anymore. For every job, there will be an applicant.

The Fed is going to continue to talk a tough game, raise interest rates and sell off the bond portfolio. Give it another two or three months of this tightening and inflation will be really gone in most areas. That doesnt mean we will return to normal prices, just stop the inflation.

Keep in mind that inflation in rents is measured in lagging indicators that wont initially show the downturn. Home prices are also on a bit of a lag, as the price being negotiated for a home today is different from even one month ago, which is where the comps are.

BTW I looked at the price of lumber and it is almost down to normal range of the past years. I imagine that there is still strong demand from home builders trying to finish the projects they had previously started so once those are built, the pace of new home starts is going to be much lower and lumber will fall to a range even lower than normal.

I’m not saying that inflation is dead or the Fed will reverse course right away, but it wont require rates to double from here to get inflation under control. Mortgage rates at 7 percent is going to kill the housing market and all the areas of household formation that are tied to it. Selling off 1 trillion of the bonds would have a massive impact, and yet, still not get us close to where we started before COVID and also going back further, where we sat before the first housing crisis.

Random-vis your observation on the general economy’s great reliance on debt-perhaps there could be a bit of a shift coming socially (can one reverse-boil a frog?)-since WWII we, in many ways with our consumer society, slowly moved away from ‘taking care of/servicing/repairing the amount of stuff we owned’ to ‘just toss/break the out-of-fashion and buy new ones/perceived higher-status (if not actually superior) ones’ (i think of the T-shirt emblazoned with a cartoon of the prototypical ’50’s housewife and the caption: “I’d like more things, please!”-and please, this doesn’t infer women only!) Amp the effect up with the advent of insanely-cheap (by US standards), and therefore easily disposable-replaceable mostly-Chinese-manufactured consumer goods (financed in no small part by massive export of U.S. industrial pollution/labor costs to China and/or ‘Third World’) placed on an easy-to-obtain domestic credit card and-here we are, with the mindset affecting matters far beyond the initially financial. Given personal debt pressure one might think some would start to question (have seen this among some of the commentariat) how many things does one really need? (Not that you shouldn’t have them if you want, but are they truly affordable or mission-critical?). Different times will dictate differences in ‘wants vs. needs’ (the emergency liquidity of dry-powder cash vs. the satisfying heft of a purchased good vs. the happy result of a rendered service), and the more prosperous a society, the more difficult the differentiation becomes.

my, do i ramble…

may we all find a better day.

This must cause a sharp plunge in real estate prices in desirable areas as fewer buyers qualify. For example, average house prices in California are reportedly $816,804 per the website Fool.

If house mortgage payments just were of interest, total annual payments at 6.25% would be a minimum of $51,050 on an average, California house, and such low, house prices are unavailable in many areas because that state average must be getting lowered by real estate prices in undesirable cities. Only the interest on the first $750,000 of the new mortgage loan can apparently be deducted. (The 2017 Tax Cuts and Jobs Act limited the deduction to the interest on the first $750,000 of a mortgage.)

To keep with historical fundamentals such as wage growth, productivity and sound banking/lending…

Stocks and housing need to drop by 2/3 to get into a “normal” historical range.

And with every major downturn, it will overshoot.

2/3 down is still overvalued imo.

I suppose they will never let us see that…Even 10% drop, the media scream like the world is falling apart.

Yes, because comparisons to historical valuations using revenue, earnings, and dividends are still based upon artificial prosperity from sub-basement level credit standards.

Hussman reports on this regularly, but it doesn’t adjust for removal of these distortions.

The country is presumably somewhat more affluent versus the past (arbitrarily early 80’s when the secular market advance started) but nowhere near to the extent reflected in asset values. 735 billionaires now vs. 13 then reflects mostly fake wealth.

No, that is not ‘fake wealth’ those billionaires created wildly positive advances and innovation. The issue isn’t ‘fake wealth’ but misallocated wealth.

What are you talking about?

Market is down 17 percent or so.

Its gonna go more down

With everyone talking about inflation there has been a paradigm shift in FED

Don’t fight the FED

Agree with the sentiment but I think it is wishful thinking. Alot of fiat out there and the federal government just started deploying the COVID relief stimulus to state and local governments.

Fed tightening/QT while federal government dispersing funding will in the short term cancel out. Need to see job numbers come down to signal the end which paradoxically will be the same signal what others say the Fed will use to end tightening/QT. Personally think the Fed will focus on inflation and not necessarily the jobs numbers. Reason is, inflation is losing wealth folks money AND poor/working class is getting crushed. Jobs figures don’t affect the wealthy nearly as much as working class; so if they have to pick between the two, it will all be about lowering inflation

1. The dollar is what gives the Fed omnipotent power all over the world. They will never sacrifice it.

2. Finally the worker bees were starting to feel that may be they can ask for raise and get it…..the rug must be pulled…that’s the amerikan exceptionalism!

State and local governments have been deploying COVID stimulus money for a while now. Yes, there is definitely still more to deploy, but to characterize it as “just started deploying” is misleading.

With respect to “Fed tightening/QT while federal government dispersing funding will in the short term cancel out.”… that’s a bit misleading as well because the point is that increased government spending will now have to be funded by the private sector rather than monetization by the central bank. The resulting reduction in liquidity is the big change for the markets.

I don’t know that it will get that far, but I won’t be a buyer until it reaches the level of January 2020 again, and I might not be a buyer then, either.

Only 6.25% ?

Long ways to go to get to 20%.

But it is a start.

Can the market be wrong? All financial news believes in the postulate that the markets are always right and apparently will sniff out (if you listen to CNBC). If we hold that assumption, then markets should behave rationally. This implies that the average action of all market participants lead to rational decisions. What if all of the participants drink the same koolaid? Till what time period can markets be irrational? Is it kosher to say that the markets are just plain wrong at some point in time, even if you believe that they get rational over the long term?

A free market is never wrong.

But it can change, in a minute, with new data.

Sometimes massively in a short period of time. And a free market is full of human emotions, which can change massively in a nano second.

Government intervention to pick winners and losers greatly distorts a market, until it implodes as the graft gets too big even for a central bank.

“A free market is never wrong”

Insane statement

phoenix wrote:

“A free market is never wrong”

Insane statement

———————————————————————-

Agree 10,000% percent with the Insane statement.

Mr Market has been focused on finance to get rich. Manipulating money may enrich a few individuals. But it does nothing to make a country more productive.

OldGhost-triple check.

may we all find a better day.

The market averages were wrong last year, inflation expectations, etc.

“Right” or “wrong” when speaking about the future (thus markets) is an artificial category, an awkward forced binary model. The future is a wide array of possible states. A market discounts and probes along many axes for various versions of the future in various ways (thus bets), all at once, like an amoeba fumbling its way into the future. The market is not one right-or-wrong guess about the future. It is an array of guesses. The present-tense price of any asset is an aggregation of guesses about an uncertain future.

Markets being (as some supposedly fixed binary “truth”) “rational” or else “irrational” is, IMO, another forced, simplistic, artificial category. The rational markets models sure can be pretty though!

Never wrong, but changes quickly? That sounds like wrong, but trying to be less wrong.

What, in the history of humanity, would make anyone believe that humans make collective decisions that are wise, far-sighted, and successful?

The founding of USA and subsequent Constitution and focus on “Rule of Law” might be a good start Cyrus, even though it is not perfect and never will be.

Seems clear enough that the overall trend/line of maximum personal freedom for everyone is positive for the last couple thousand years or so, even though equally clear that the second derivative of that line does go up and down as the pendulum swings.

To pretend otherwise is to ignore the ”improved” realities of life everywhere for the vast majority of people, even if that improvement is just a wash tub instead of having to use the creek, etc.

Have tried living without running water or electricity, and while it is definitely possible,,,

it ain’t near as much fun far damn shore.

I wouldn’t count 55 men writing a document a collective decision, but I guess I didn’t make that clear.

I mean the masses, such as the market (which is what we were talking about) that has an untold number of participants.

The “rule of law” is a bit more tricky of an issue. You might try reading more history, or even looking at modern events, to determine if we truly have that for all.

“A free market is never wrong.”

There is no such thing as a ‘free market’. It’s a capitalist myth meaning ‘freely rigged’. All markets are rigged or regulated with varying degrees of both.

Free just means unregulated by the government. There are many examples of free markets. You could argue crypto is a free market. It does not mean there will be no grifters, or no one will take advantage of a knowledge gap.

More freedom equals more inequality.

The concept of a “free market” in economics is akin to the concept of a “frictionless plane” physics. Neither exist in reality, but provide useful frameworks for analyzing certain aspects of observable phenomena.

@ElbowWilham

So free market basically means one can, for example, point a gun at someone else to try to acquire their possession — law of the jungle.

Crypto is not a free market since it operates within certain criminal jurisdiction.

Glad you too have made it there una, just as we did when we realized we had only made money in the SM with what is now called insider knowledge based trading –( and didn’t have that connection any more. )

Focused on the RE mkt since 1980s where any individual who cares to can Real eyes the steps needed to rig their local mkt, or at least skip though a good part of the red tape hoops required in modern times.

“A free market is never wrong”

If true, then why do I and many others have capital gains from buying and selling securities that the market priced incorrectly?

Viewing the market in terms of “right or wrong” is silly. It is a man-made game, with man-made rules. We put numbers representing value on things. The values are set in a game of negotiations. It’s like if enough people agree that a clear sky is pink, we can start using that color when expressing a beautiful day.

intosh – great point, markets are is simplest term a “man-made game”, neither good nor evil, neither right nor wrong…just a game with rules that change constantly due to govt and Fed interventions and other manipulative behaviors of those in financial power. For example, having the SP500 bottom at EXACTLY “666” in 2009…HA, kind of proves the point, does it not???

It took me about 15 years of learning and experimenting to be able to trade “The game” successfully without having my human emotions and/or my extreme logical mind trick me into thinking the financialization of everything is anything more than humans continued attempts throughout history to make “something from nothing”…in summary, just a complex “Man-Made Game” as intosh stated…

So have fun playing the “Game” as else what is the point???

Good luck with all your investments!

The Efficient Market Hypothesis is nonsense.

The price is what it is, and in this sense, “the market” is right, but not because of any supposed market efficiency or rationality.

“The market” doesn’t have independent sentience. It’s not alive. It’s a collective abstraction.

The individuals who compose a market can’t behave rationally in the context described by academic theory and they can’t have full knowledge, whatever that is and as if it would make any difference.

Prices aren’t based upon information, data, or “fundamentals” anyway, as there is no “correct” price, for anything. The price just is what it is.

What appears “rational” at one point like now in a mania will in retrospect be condemned as reckless when the market crashes. There is also an overwhelming rationalization to justify absurd prices because everyone likes to believe they can actually become wealthier even as they produce nothing.

Good one AF!

Thanks for your ongoing efforts to help Wolf educate WE the PEONs who want to ”invest” either again as in my situation, or for the first or early times…

Came on here to learn if it was at all possible to invest in a rational manner as WE, in this case the family WE, had done for decades before the obvious ”crony” part of crony capitalism became SO clear to us in 1980s, and we got out of SMs and focused very successfully on the RE markets.

Now too old to rehab and do the work to maintain RE,,, so WE have been hoping,,,

Looks like I-bonds and maybe even regular Treasuries going forward,,,

Time will tell us a lot,,, most likely by spring of ’23.

Old dogs like you and I have no place in the stock market with our “family” or retirement savings. It’s too easy to lose it all, or most of it.

Buy I bonds, even at $10 K per year, $20 K if your wife opens an account. Also, buy short treasuries at current rates and buy all you can get if they ever yield 5% again!

“The Efficient Market Hypothesis is nonsense.”

Not entirely. It’s a useful first approximation which cannot be exactly true, which does not make it untrue.

I’ve explained this in some detail in previous comments. You’re more than welcome to go back and try to rebut it if you’re into exercises in futility.

If you know of actual evidence (no, not theory or your opinion) to support that EMH has any validity, you can provide the source and where to find it here.

No, it’s not incumbent upon me to factually disprove it. It’s incumbent upon you to prove it.

“It’s incumbent upon you to prove it.”

You can ‘prove’ your assertion first. Then I’ll discredit it, which will prove mine.

Take your time. I’ll wait.

I agree with Augustus. The burden of proof is on those who believe/claim that the market is efficient — not on those who don’t believe it is. It is for you to prove it has such quality, not for someone else to prove the lack of it.

Uncertainty and unpredictability will always remain the most fundamental attributes of human existence.

Haven’t heard about the inevitable ending for each being that is born, completely predictable at birth, eh?

So far, it is seen as certain by most folks, no matter how long and slow that slippery slope may be for any individual.

““The market” doesn’t have independent sentience. ”

You really torched that strawman, and demonstrated that you don’t understand markets.

Markets are a way of optimizing vast streams of different kinds of data to satisfy desires, and it is by far the most efficient way of doing it. Works perfectly when we let it.

You clearly misunderstand the meaning of “efficient market.” Let me try to explain. Market prices are based on future expectations. The collective expectation is reflected in the market price. That is the efficient price. For example you are drilling for oil. If you hit oil, that oil well is worth $1M. If there is no oil, the well is worth nothing. Only after drilling is complete do you know the right price. The right price is either $1M or $0. During drilling, the price of that well will vary as new information becomes available. That price is the efficient price. For example if the chance of finding oil is 30% for similar wells, then the efficient price for the well is $0.3M. It’s not the right price, but it’s the efficient price.

Again confusing the actual basis of economics as stated by Smith in a completely different situation back then compared to the current markets today.

Back then one could have perfect information and act rationally as the markets were limited.

For example, if you lived in a small village in England that had two sources of supply for sugar, you knew the price that was being charged for the sugar by both suppliers. That was full knowledge.

Your entire market for sugar was limited to those two suppliers as you had no other access to other markets (IE,suppliers because it was too far to walk, didn’t have time to walk, etc.).

Based on the price at those two suppliers you could make your decision.

I think that you’ll find that traditional Economic theory still works in many third world countries and markets and not in current markets in advanced economies such as the USA.

My favorite recent example is all the blather about how the “bond market” “thinks” that the Fed “will pivot” in the fall, winter, sprint, whatever, because some futures prices seem to anticipate lower interest rates in some future date.

What’s fun is then watching that story change, as those market prices change. Inflation + global events + The Fed have been bludgeoning those market expectations for the past 2 years since the bond market peaked.

The market’s predictive capability is better than economists’, but both break down badly at significant economic turning points. Anyone who invested in bonds or stocks 1-2 years ago based on “the market’s predictive capability” has had their portfolio decimated.

Back when I was day trading a lot, I used the analogy of a herd of cattle. Watch the S&P 500, its basically a herd of cattle on the floor of the NYSE. It reacts to the loudest bangs, biggest pops and most absurd news that would not get a flinch from a rational cowboy. Often this herd runs headlong off of a cliff, and most of the cattle are slaughtered before the last few cows in the herd can stop. Look at the major market indexes this way, and you’ll begin to see that “the markets” are quite irrational in how they behave.

Free market dynamics as it pertains to capitalism are a completely different topic, for another discussion.

Has MBS QT ramp up to 90B already begun, is that the reason we’re seeing higher yields on MBS?

Or is this purely market driven?

“Has MBS QT ramp up to 90B already begun”

MBS full-speed QT is capped at $35 billion, Treasuries QT at $60 billion. Combined $95 billion. And yes, we’re in it.

Technically, the Fed has options for removing liquidity from the 10-year market beyond selling Treasury paper.

For example, the Fed could start selling “Fed Notes”, which would be zero-coupon bonds due in 10 years. These would have the practical effect of attracting money which would otherwise have purchased T-Bonds.

Another method would be for the Treasury to sell T-Bonds directly to the Fed, who would then sell them into the market, as needed.

While either of these actions would upset various people, I do not believe that they are prohibited by current regulations.

re: “Treasury to sell T-Bonds directly to the Fed”

Today, that is illegal. The Treasury’s “overdraft privilege” ($5b of emergency borrowing at any one time of securities purchased directly from the Treasury), was discontinued for good reason. The Treasury-Reserve Accord of March 1951 is prima facie evidence.

It’s about the “Scorpion and the Frog” fable. Treasury-Federal Reserve collaboration exists in its present state, because whenever in the past the FED’s responsibilities were subordinate to the Treasury’s, this country experienced intolerable rates of inflation – which is why the Fed’s $5b “overdraft privilege” (direct purchases from the Treasury), was not extended or reinstated.

The monthly MBS roll off is not expected to meet the $35 billion limit. Is there any word if fed will sell MBS worth the remaining amount? I could not find any information. Going forward, because of limited sale and refinance activity, I see MBS roll off getting smaller every month. I so wish they will sell the remainder.

I would recommend going back and reading some of Wolf’s articles on QT, the three most recent ones should do. I was under the same false impression about MBS. Instead the truth of the matter is that MBS “rolls off” (amortizes) when any form of principle payment is made (just like a mortgage). It need not mature, in fact when it does mature the value is most likely be almost completely amortized.

The MBS cap will likely be hit frequently enough during the first year of QT. It’s the later years that are a real problem.

But a surge in foreclosures will cause payoffs to increase and pass-through principal payments to increase, and a dip in mortgages rates two years from now, from say 8% to 6%, will trigger a new wave of refis which will also trigger a wave of pass-through principal payments. Both of them will cause MBS to come off more quickly.

So nothing is set in stone.

But the Fed is talking about selling MBS outright and may do so in a year or two, to make up the gap to the $35 billion cap.

Wolf stated “And yes, we’re in it”…

Deeply “in it”…:D

And to think this is just the top of the first inning of the economic depression ball game. Thank the good lord I’ve invested in arable land and water.

I know. The interest rate cycle has barely turned from sub-basement levels, interest rates are still historically on the very low end yet look at the early results.

Yesterday I got a flyer in the mail from “Better Homes Real Estate”. It was a nice glossy flyer with two nice looking real estate agents shown. In quotes next to the agents picture it said

“Now is a great time to buy a home!”

I chuckled.

Maybe thank. Probably better to wait until you see if the future prices of your land and water are higher or lower than what you paid. Your thanks may turn into exultant joy or wails of despair.

After committing the original sin and displeased with the gospel of the pivot, I can’t help but think the Fed stands ready to rain fire and brimstone on the deniers.

It must be quite satisfying to be proven correct. I remember the comments section every time Wolf spoke about the FED absolutely not pivoting while the summer rally was in progress, it’s gotten much quieter recently 😂. I really do wonder about the motives of the people pushing the “pivot” narrative though. Was it actual conviction? Panicked/wishful thinking/delusion? Was it an exit strategy for someone?

“Panicked/wishful thinking/delusion? ”

I’m going to have to go with “All of the Above”.

It’s delusional to believe that the Fed is actually doing what they could be doing to reign in inflation. There’s still more yield to be found in the snp and crypto than there is in less risky assets and as such, the ‘bear market rally’ will continue until it makes a new high thus negating the bear market thesis and inspiring the Fed to action.

Only on this site does the narrative exist that the market is ‘a mechanism for the Fed to convey its monetary policy to the economy’. Gibberish. The market is a reflection its participants who are in a relentless search for yield and until the Fed acts meaningfully and provides an avenue for higher yield in less risky assets, it’s risk-on.

I observe with great interest the phenomena of very smart people losing money in the market because they’re more interested in being right than they are in making money. So bring on the denier rhetoric so you can all feel better about how smart you are as the market rallies.

“It’s delusional to believe that the Fed is actually doing what they could be doing to reign in inflation.”

The Fed is doing what it can to rein in inflation without collapsing the economy, which isn’t all that much with blunt instruments like interest rates and QT. It’s most likely to settle on an unhappy medium between the two and therefore fail to either control inflation or prevent a recession because excessively-low interest rates, for too long, as well as other factors, have made the situation unmanageable.

“So bring on the denier rhetoric so you can all feel better about how smart you are as the market rallies.”

Go buy some stocks. I dare ya.

una-from a strictly semantic (and it’s ever-more apparent that that horse has fled the stable) viewpoint, thanks for pointing out that under its ‘reign’, the Fed’s attempts to ‘rein’ (in, that is) the financial beast that we all have connection with (one way, or another…). (…and does ‘loosing’ something ultimately resulting in ‘losing’ it? ah-more likely i’m losing it…).

may we all find a better day.

91B20 1stCav (AUS):

We are seeing that a lot these days as the spell check, or whatever, knows more spelling than the human, eh old boy?

Same with arithmetic far shore,,, don’t even ask a young cashier to make change when their fancy machine is not working.

”This younger generation is going to the dogs!”

VVNV-the answer, of course, will be: “…but i LOVE my dog!!!…”.

best to you, and…

may we all find a better day.

(p.s.-said long ago that i was still teaching new hires how to count change in the moto-shop in the late ’90’s-aughts, mostly to protect them and the firm from the ‘i gave you twenty’ when given a ten scam run by some).

again, a better day to all.

Wolf, any reaction to MarkB’s comment?

There is no panic in the markets yet, could the seaonal mid terms rally play out after September and lead to new highs before it goes south?

Thank you.

No reaction. Waste of time.

Didn’t the very smart and knowledgeable and experienced hedge fund guys lose money lately?

Are they looking to make money? Or to be seen as right?

It hasn’t been a credible market for a while now, but people sure feel smart when dumb luck makes them money.

Mark B—

Exactly. I expect a strong counter rally in the market and in bonds (despite the Fed) in 2023 and perhaps early 2024-with new highs—before the Fed is forced to get real serious.

Everyone here thinks being a bear will “be easy money”. Not yet.

“I really do wonder about the motives of the people pushing the “pivot” narrative though. Was it actual conviction?”

You’re talking like it’s “a done deal”. That the Fed is not trapped, or that the Fed won’t pivot.

I think Bob Dylan would say –

“The Wheel’s still in spin”.

The extent of the fraud that has transpired for decades is so great now that I think anyone who claims to know how the future will unfold is dreaming a little.

Could not agree more. So J-Pow does some jaw-boning at J-hole and somehow this is now proof that the Fed will not pivot? Meanwhile another nearly trillion dollar spending bill has been passed and the strong consumer with an exorbitant war chest is given a student loan bailout. I shall hold off on the confetti parade until something really breaks. We haven’t seen anything yet.

And accept it that soon you’ll be drenched to the bone.

Hey, the FED can’t stop the vote buying, right?

The government is certainly tripping over itself to spend money and will likely continue. However, wouldn’t that exacerbate inflation and push the fed to continue tightening beyond where it may have otherwise been able to ‘pivot’?

Seba

The FEDs moment of truth hasn’t arrived yet. We’ll see how much of an inflation fighter they want to be when they’ve destroyed everyone’s pension. That’s the moment of truth.

It makes me think of the French Revolution. The people were hard working, God fearing people. And yet look at what they did to the aristocracy, the source of all their grief. The people wanted their revenge even if it sent them to hell. You can only push people so far before you inherit the whirlwind.

I guess I’m pushing the moment of truth not the pivot. I have no idea how the FED reacts. Maybe they do choose to inherit the whirlwind as the French aristocracy did. Maybe they choose to pivot. I don’t really know.

I used to think along similar lines, but the majority of people do not get pensions. Most people do not even own stocks. Destroyed pensions would do nothing to someone like me.

Inflation is what is stealing money from most people’s pockets. If they do not get that under control, you will see real food riots, which is what the French Revolution was mostly about.

“Let them eat cake” comes to mind.

First step would be not eating out at restaurants. Restaurants in my area are still packed.

Joined at the hip stocks and bonds will likely soon be successfully separated. The lagged effects of the rise in yields across the maturity spectrum – rising rates – in combination with higher labor costs, will soon weigh on corporate earnings. Until recently it’s been primarily a story of the time value of money, which affects all assets dependent on future cash flows similarly. But corporate earnings affect only corporate securities … Treasuries are likely to rally as stocks continue lower.

Finster

“But corporate earnings affect only corporate securities”

NO!

Earnings decrease also affects a Corp ability to pay dividends!

Look at all the ‘buy-back shares so far?

I started buying back my 3X leveraged short ETFs in mid July. I was a little early, but they’re looking good now. I hope a trap door opens and markets tank, but we’ll see.

Can you share the names of those ETF? I am relatively new to shorting. I want to short nasdaq (SQQQ) but I suppose I am late now. Any short ETF still worth buying?

Good lord.

ETFs are meant for day trading. They have a decaying time premium that will kill you if you hold them over weeks.

I wouldn’t say all ETF’s are meant for day trading. You are right about leveraged ETF’s having a decay, but holding for weeks is a pretty solid hedge. I’ve been doing well shorting the bond market on the long end and short end… PST & TBT to be precise.

Not if there’s a strong directional trend during the period of holding. In that case, gains are amplified slightly more than 3x

nabil

“strong directional trend during the period of holding.”

Yes. One has to be right – TWICE – Trend and timing, just in option trading.

For leveraged ETFs, I tend to buy some Long ones compared to short ones, to reduce the ‘whip lash’ . Not always successful but swing trading does reduce the risk, but only in tax deferred accts.

It is continuous fight between the powers of perception vs Reality!

This all depends on where you think the market goes from here. The time premium you pay to hold inverse leveraged ETFs is real. Go look at 6 month prices of the SQQQ versus the QQQ and you can figure out what the time premium you’re paying would be. Less volatile ones like SPXU won’t have as much time decay or there is always shorting Cathie wood (sark) or short Bitcoin (biti).

If you feel strongly about nasdaq tanking then SQQQ could work just know the longer you hold it the less effective. I’m talking months tho not days like some people suggest. Say you hold it for a month or two and the market does go down 10% you likely won’t get the expected 30% return you’ll still get more then 10%🤪.

SOXS, TECS, SPXS, TZA, SARK. The best so far has been SOXS and SARK. I buy chunks of 5 or 10 shares of each on days when the market is up and they are down. Scale in and you minimize your risk. SARK doesn’t use leverage, so it’s less volatile.

Bubba

Buy the their opposite ones in very small quantity, to reduce the back lash, like today!

I do have some money in a (what I call a) pseudo-short ETF: VIXY.

It holds (and rolls over) short-term futures in the VIX, which spikes when there is a panicky event. This could be a big fast market dip, or any of a range of things like, say, a nuclear mess-up in the Ukraine war. What I like is, this is so amorphous and psychological: it just likes (the appearance of) trouble. It really disliked interest rate suppression (the previous era). Look at the history though, the behavior is weird (it topped at like $45,000 but that was eons ago in modern trading history, before the all-powerful Fed regime really took off). It sits forever at a price around the mid-teens like a snake in the grass for an indeterminate time and then spikes through the roof for a very short time. I see it as tail risk insurance, but for me, a genuine asset class.

It does not expire like an option, which is really nice. It rolls options, so it dribbles away some money on the decay. It may take patience. It is worth some due diligence, to familiarize with the dynamics.

The stocks swoon heading into June, plus VIXY, paid for my summer. I am holding at an average buy-in of about $14.50 at this point, which seems more or less flat with a $4,000 S&P.

All that said,listen to the wise voices around here: not investment advice, etc., DON’T DO IT! ;)

Do not buy and hold leveraged ETFs!!! They are not what you think they are. Please read about them in detail and you will learn why.

They are products meant to only multiply the DAILY return of the market. You should only hold them for a very short term (a few days at most). That difference may seem small but when you do the math it leads to wildly different results than what the actual market does.

Here it comes

It is the only choice for those who don’t know or cannot trade in options. Daily decay is real. So I buy the opposite kinds in very small quantity to reduce the back lash (swing trading). I also buy a lot of Div paying ETFs in numerous sectors across the globe, part of counter measure.

A continuous fight between Perception power vs the hard Reality.

BEAR will be the ultimate winner in the end when this surreal Bull mkt is unwinding!

Have bought those ETFs in the past, but I decided the roulette wheel at Caesar’s was faster and they offered free drinks.

Short-selling both sides of levered ETF’s may be a risk-free way to make money. I’ve run the sims a hundred times. And the only reason I don’t do it, is because I know that as soon as I lever up (gotta be done in a margin account) and put the trades on, I will discover that doing so is not risk-free after all, and I’ll be the guy you read about in the Journal next week.

And yet . . . . sure seems like time decay works on both sides of the levered ETF’s and . . . can’t lose.

Wolf,

Can I request your overview on the UK.

We have a new govt.

Gilt yields have soared in the last few days.

Pound is hovering 1.15 to dollar.

New PM plans to cut taxes with inflation heading to double digits.

Yes, that will be interesting — if those new policies actually happen. But I don’t cover politics :-]

Here’s your Overview:

per Bloomberg, the first ratings agencies have labeled the UK an “emerging market”.

In plain english a third world country.

I watched Liz Truss’ first PMQ. Can you believe that she flat out refuses to tax the economy into prosperity!? She also believes that incentivizing oil and gas companies to supply more energy out of the north sea is going to reduce energy bills! Fool!

The Federal Reserve enjoys more mobility in monetary policy. The purchase of Treasury securities and the injection of trillions of dollars into the capital market push up the prices of financial assets. “How Long Has this being Going On”…….QE has left the building. It’s all Over but the crying. What goes Up? Must come down….Winter is Coming…..The Bear is wide awake.

Warren Buffett advises retail investors never to short and never to use margin. Probably has to do with being forced out of your position if you are wrong.

If you buy a broad long stock index that pays a decent dividend income then you get paid nominal income even if you are wrong in your timing. You can in theory hold position forever collecting the dividend.

It’s probably good to to decide how you are going to keep score on investing. One way is the market price and the other is the value of the future dividends. Trying to predict market prices can drive you crazy whereas dividend income is less susceptible to market forces.

While I agree with you in principle, the dividend yield on good companies is pathetic. Most people would not be able to save enough money out of their earnings to build any kind of decent retirement income doing that, and at low returns the magic of compounding doesn’t really kick in until you’re about 200 years old.

For your average person they will have to eat the capital value of their investments to support themselves in retirement, so they do not have the luxury to ignore this.

Agreed.

> your average person

… has, as a thought experiment, $1,000 locked up in a Treasury security that (now, finally) pays 3.5%. So the person gives up the liquidity and use of the money, to get $35 a year, not even a quick trip to the supermarket.

This is not rational until one has a lot of thousands. Sadly though, the person may jump too far out on the risk curve and take some wild bet on a short term pop like a 3x leveraged short ETF, with a mathematical expectation of return at sub-zero. If one “must” do it, tiny bet-sizing (affordable in brokerage accounts these days) can help to not make a very regrettable blunder, while getting experience in the real-world effects.

Better to hold cash, IMO, until one has good enough reserves to not be treated to the experience of sleeping on a sidewalk, in a time of shifty prices and investment returns. Inflation is the “insurance premium” one must pay for that relative certainly.

People who buy leveraged financial products are gamblers, not investors. I’ll take my 3 – 4% in interest and return of my principal and sleep well at night.

Most corporate balance sheets are also mediocre to terrible.

“advises retail investors never to short…”

Short. Isn’t that the deal where the upside is finite, but the downside isn’t?

“For a limited time for well qualified buyers”

I’m thinking 5% Wolf to get inline with the inflation levels at this point, but definitely 4% and a bit up.

Wholly 10 year Spike with no support from the fed. Closer to the 8 percent mtg rate call next summer that Wolf says is floating around the real estate world.

The financial websites I track and one of my financial salesman pushed for bond purchases in May and June and I refused.

They were siting all the narratives about how the markets and economy are dependent on ever decreasing interest rates and the need for more and more debt to fuel the GDP growth including housing. What is missing in the analysis is the willingness of the fed during full employment and what I believe is the retirement of the baby boomers to raise rates to fight inflation regardless of the impact on GDP and asset pricing.

Nothing moves in straight lines a wonderful quote from Wolf.

Technically, it looks like a bunch of weird tea cups forming with their depth inversely related to their duration. If people start buying bonds now due to the increased yields, there will be the forming of the handle prior to a continuance upwardly to higher yields.

Sometimes I wonder about the ‘inflation’ figures, especially regarding the negative impact on nominal wage increases. In the past several months I’ve seen some wages double in nominal value: From $12 per hour to $24 (Wal Mart warehouse centers). People who made $12.50 an hour six months ago are now getting $18-$20 per hour. These are service jobs mainly. As for production jobs, the wages appear to me adequate, at minimum ($30 and up per hour). Plus 401K and decent insurance too. About the only group I see getting royally screwed is anyone on Social Security. SS doesn’t even cover subsistence costs. You can have democracy or you can have billionaires. You can’t afford both.

“About the only group I see getting royally screwed is anyone on Social Security. SS doesn’t even cover subsistence costs. ”

From one who is in that particular group, I feel the screwing is ongoing and getting worse. Our house and car insurance renewal was up 25% for the coming annual period starting 10/1. Shopping the market resulted in no cost benefit and most others quoting were actually higher cost (discounts all in).

The kind of democracy inferred in your post isn’t affordable even without billionaires.

Most of their wealth is from the asset mania, not the result of production which can be mass distributed to the population at anything close to current market value.

Last I checked, 735 US based billionaires maybe a year ago.

Number in 1982 or 1983? 13

No, it wasn’t mostly inflation and no, the country isn’t anywhere near that much wealthier.

Re “You can have democracy or you can have billionaires. You can’t afford both.”

Stripping the elites of their wealth and Robin-Hooding it to the poor wouldn’t do much to improve the lives of the poor. There’s not enough meat on that bone. The true wealth of the nation (and the world) isn’t on balance sheets that can be given away, it’s in the daily production capacity to sustainably meet everyone’s needs at reasonable prices.

However, the huge wealth disparity is a glaring sign that something else is broken in the economy. Policies which strangle production capacity, or allow just a few companies to hog all the earnings from a given sector without any real competitive pressure, destroy the national wealth.

Breaking up the corporate monopolies and too-big-to-jail syndicates would help to regenerate legitimate business competition throughout the economy. That competition would mean lower profit margins (which in turn implies more pay to workers for each unit of production), and that would do wonders to stop inflation and give workers the earnings (and products!) to have a better life.

CEO pay is 360 times worker pay,corporate boardrooms and ceo all from Ivy League schools . Greatest frat party ever

Exactly. Barriers to competition is the biggest problem in government right now, even bigger than the rigged tax code. Something needs to be done to diffuse the near-monpoly status quo found in every sector.

I built my first house in 1974. Barely able to qualify for a 30 year mortgage, I recall the rate on that mortgage was 10.25%. Somehow we all survived, you will too.

You forgot the price

Income to asset price ratios are what matter. See credit cards and their 22% rate, do I care? No. Because it is paid off every month. A 10.25% mortgage, but the payment is only 25% of my take home? Sign me up for that reality.

These out of touch oldsters are broken records. They’ve been saying financially ignorant garbage like this for a long time now. It’s almost like their feeling smug and smart depends on them not understanding.

That’s not financially ignorant garbage, it’s the time-tested Gospel of Sweat Equity. When rates are high, your own labor has greater value because credit is too expensive. So people work to build what they want in their lives.

People mistakenly thought houses were “investments” for the past 20-30 years. It almost worked because the house pretty much “paid for itself” (equity appreciation) while rates were trending down, decade after decade, and as more people kept buying into the “investment” meme.

But rates are no longer going down. So houses are no longer equity-building investments that “pay for themselves”.

If you want to pay for your house, you have to do it the hard way, and sweat equity in your own place is a big part of keeping the cost of ownership down.

BTW, the cost of nearly everything is up 20-100x since 1971 (end of gold standard), so $18K back then is equivalent to $360K-$1.8M today.

Wisdom Seeker,

I hope typing out that non-sequitur was cathartic for you. Obviously, I was not referring to sweat equity as “financially ignorant,” but to the common old person trope of “back in my day it was so much harder…” in regards to rates while ignoring asset prices and incomes. I see the shoe fits you as well. Rates matter a great deal less when you can pay off a 30 year mortgage in 7 years with scrimping and a median income.

I’ll make it very easy for you since you seem intent on your ignorance.

Median price of a house in the US in 1983: $75,300

Median income in the US in 1983: $24,580

Ratio of 3.063 earnings to price

Mortgage rates were ~13%

Monthly payment of $218, which is 10.64% of income.

For the first two quarters of 2022 we have:

Median price of a house in the US in 2022: $436,700

Median income in the US in 2022: $83,895 (2021+5% wage increases thus far)

Ratio of 5.205 earnings to price

Mortgage rates are 6.25%

Monthly payment of $2,151, which is 30.76% of income to mortgage.

If only us kiddos had it as easy as you did when it comes to purchasing assets. Don’t let the door hit you on your way out.

From late 1986-1990 one might have had a ~10.25% mortgage, or in ’78, or ’74. I’ll leave it to you to see if you can cherry pick some data that paints you less of a fool.

Cyrus you over-represented median household income by 20,000. It is actually 62,000. That puts closer to 40% income to mortgage. Also that is 60% of the monthly take home pay. Things are much worse today.

@Cyrus –

You misread CreditGB as saying “back in my day it was so much harder”. I don’t see that in his comment. Also, he was referring to 1974, not 1983. I think the non-sequitur is on you.

P.S. Houses were smaller then, with fewer features. There was a reason for that, which you might want to think about. One might almost say that people made it easier on themselves by not trying to buy that which they couldn’t afford, or something…

Still Seeking–

I’m sorry you can’t read between the lines. Good job sidestepping your ignorance once again. You can lead a horse to water…

Maybe. My parents also built their first house in the Summer of 1974 when I was 8 years old. They borrowed $18,000 at, I think, 9% interest, and my father and my maternal grandfather built it doing all the work themselves. $18,000 dollars to build a 2000 square foot ranch house with central air and heat.

We’ve made it to just about where my first loan on my first house was back in the 90’s. I was pretty happy with that rate. I get it that this would be a shock for those who have become used to or were born into cheap and free money, but for me, I was thrilled I got that rate and don’t see this as something horrible. The market needs a correction very badly, despite the fact that that it will be painful for some. If this correction continues to delay it’ll be really really painful for virtually everyone.

All prudential reserve banking systems have heretofore “come a cropper”.

Wow, the 13 Week Treasury bill is up 12 basis points. The yield is 3.01%. Does this mean Wall Street is reluctant to give up hope on the stock market? They can temporarily deposit their money into a short-term bills and notes in hopes that they can get the money out fast for another stock rally?

My wife and I bought our modest 3bed/2br home way back in 2013, at the very bottom of the market here. We had all the usual “sky is falling” doom and gloom stuff and nonsense from literally everyone we knew. We went ahead, and bought, and we are glad we did. Where we live, we literally couldn’t afford a double wide right now for what we paid for a house back then.

I feel awful about everyone who bought at the top of the market, and who will be deep underwater very soon, if they are not already. But the alternative is even worse: millions who can’t afford to buy, and are now being hard pressed to afford rent. We can’t have all those folks living out of doors, it’ll tear the country apart.

We need SANITY in the markets. ALL the markets, including RE

Welcome back Pablo.

The one year T Bill is paying 3.61% and the 10 year T Bill is paying 3.33%. Both are well under the inflation rate and the yield curve is inverted.

It seems the yields need to go higher in order to beat inflation.

Any predictions on when the 10 year T Bill rate will go over 10%? In 1981, at the peak of that inflationary period, the 10 year T Bill was paying over 15%.

I should have taken my paper route money and gone all-in on 10 year and 30 year T Bills back then. I am better prepared now.

The one year T Bill rate is tempting at 3.61%. It pays better than most of my dividend stocks with less risk.

“one year T Bill rate is tempting at 3.61%.”

one month is 2.17% which could be also interesting.

Does anybody know if you can buy T-Bills on the auction in Merrill (IRA acct)?

You can at Fidelity or at Treasury Direct, so if you want to and you are motivated there are ways even if Merrill does not.

Crap I somehow missed the IRA part, I do not know if you can buy at auction in a IRA at Treasury Direct (I buy outside of my IRA), but I am sure you can at Fidelity.

Thanks, but the question was about Merrill.

If you can’t get the service you want move your money, it yours and fully portable.

You can’t buy T Bills on auction at Merrill. I tried but only secondary market were available. Wanted to park my saved down payment for a future home in 1 month T Bills until better home buying opportunities presented themself so I moved it to Vanguard where you can buy them on auction. They don’t allow you to automatically purchase new ones each month so I’m just logging on once a month to purchase new ones once they mature.

If I were to switch to 3 month or longer bills for the higher yield, can anyone estimate what sort of loss I might expect to take if I needed that money suddenly and I were to sell them to the secondary market before maturity in a rising rate environment?

Clearly varies by lender, to answer your question J.

We, in this case the family We, have been studying that along with studying on Wolf’s Wonder…

I work in IT not finance so trying to understand some basics here. Why is Treasury yield rising a bad thing? Is’nt it good for fix income folks to get some interest? Seems like Treasury yields are inversely proportional to stock market. Does that mean Treasuries are a secure form of investment, where everyone who was gambling in the stockmarket goes to take a breather. If you had 10 million lying around, why would’nt you put it in Treasuries and sleep at night?

Why are rising yields considered bad?

Because the country (and much of the world) has collectively lived above its means for decades and the current artificial prosperity requires cheap borrowing and the lowest credit standards in history to continue.

Everything nets out to zero with debt and credit. That’s why you may or have heard that “we owe it to each other” or “we owe it to ourselves, which would be true for the US if it weren’t the world’s largest debtor.

But everyone’s debt is also someone else’s “wealth” and when defaults and bankruptcies occur at scale, then a lot of “wealth” disappears, credit gets (a lot) tighter, and actual investment and employment decline because it’s mostly contingent upon borrowed money.

The financial system and economy are only designed to prosper with perpetually expanding credit and debt. Without it, it falls apart. Look at the GFC in 2008 for an example.

And credit and debt can only expand forever on a planet with limitless resources, which we most certainly do not have (that anyone on the planet knows of). So like yeast in a petri dish full of sugar we consumed until nothing was left and now are left with a lot of yeast that needs to be fed ;)

But hopefully stocks will give me a comfortable retirement \s

We have barely tapped the resources of out planet.

“The financial system and economy are only designed to prosper with perpetually expanding credit and debt.”

That much is certain. Worse, debt is increasing faster than GDP, making the present situation a financially-unsustainable debt trap. The quants see disaster coming and assume somebody will prevent it but have absolutely no idea how and have decided to ignore the problem and make dinner reservations.

Worse still, the present situation can only continue by overexploiting nonrenewable resources, which makes it an existentially-unsustainable trap as well, meaning it must inevitably collapse.

It’s been years since I’ve advised people to Save Themselves. Now I tell them to Enjoy it while you can. A late-summer vacation in Europe would be ill-advised because it’s on fire but you could make dinner reservations while considering other options, although you wouldn’t want to wait too long.

It’s bad for people that had bonds already. If they want to sell them, then they will receive less than if the rate is lower.

This is why bond prices are inverse to rate changes. Bonds are not priced on what the bond would produce after the coupons are clipped, but what the bond sells for now in the open market.

Best analogy is GPU cards. Every time a new model comes out with faster speeds, prices for the previous model take a big hit, even the ones never used or slightly used.

Nate

For those willing to venture out there is a laddered ETF on bonds of different maturity. Start with small # shares and add slowly when it drops. This is only for those with patience.

somethingstinks,

“Why is Treasury yield rising a bad thing?”

It’s not a bad thing for people who are going to buy the 10-year Treasury in the future; for them, it’s a good thing because they buy it at a lower price to lock in a higher yield. The yield should be much higher. It should be above the rate of inflation.

But it’s a bad thing if you already own 10-year Treasuries because you locked in the lower yield you got when you bought them, and if you try to sell them, you will have a capital loss.

But it’s not that simple. If you bought a 10-year Treasury at auction in 2020, and you get a 2% coupon per year, and you hold to maturity (2030), you will get your money back, for sure, and you will earn 2% each year, for 10 years.

So that’s not a bad thing if inflation = 1.5%. But if inflation = 8% over the 10 years, then you will lose a lot of purchasing power to inflation.

Of course, if you put this money in the stock market, you get an even smaller dividend yield, and you might lose 50%, and in addition, you will lose purchasing power to inflation. So the calculus is complex, and the outcome is unknown. That’s why different people do different things, which is what makes a market.

Thanks Wolf,

This is a good explanation.

For retirees and conservative investors, US government insured bonds seem to be the safest for guaranteed fixed income.

somethingstinks

Higher rates are good for lenders, bad for borrowers. Now who are the big borrowers? They are the ones saying high rates are bad.

RedRaider

Lenders also have to face default and BKcy!

This is going to be a slow multi-year price reduction process for RE, which is bad for sellers. I’m already seeing sellers drop the price of RE incrementally, as they follow the market price down. Once it’s on the market too long, people won’t touch it. They wonder why nobody else wants it.

Better to take a big gulp and get the home sold, avoid maintenance costs, etc.

Whatever you think your home is worth, it’s worth 15% less in a market like this. And I predict this market is not going to trend upward again for a LONG time.

I’m still seeing properties sell for k-razy prices throughout the multiple different cities that I track for my own amateur market analysis. I saw a place in Bakersfield which sat for five months, going in and out of pending, finally go under contract at ~500K…in Bakersfield! I saw another property in Port Angeles WA languish for a month before selling for 74K over asking. Wild.

The trend I see in a lot of cities is minor price cuts but with asking prices still well over anything “normal” based on prior sales histories for the same or similar neighboring properties.

I think it’s going to take a long time for the perception on-the-street (not WS) to come into phase with reality. The popular delusion remains that the gains we’ve witnessed in assets like RRE is organic and ineluctable. Nothing in almost any market has made sense to me in years…I still sense a a kind of EZ come/EZ go fatalistic attitude among consumers; welcome to the casino-at-the-end-of-the-world

A co-worker during housing bust 1 made this mistake. Rode the market all the way down.

He went with the agent who recommended listing at $580K instead of the other one at $500K. If he listed at the lower price initially, probably would have sold close to it.

This was in 2007 shortly after the peak in PHX. He ended up selling at $350K in 2009.

I think the trick is not to sell if the market is down.

Sell high, buy low.

My co-workers in the Bay Area rode it out and by 2016, they were above water again.

Today, they are multi-millionaires on paper.

Tomorrow never knows.

As a side note, I think if you look at the historic house price charts, if you purchase a house and lived in it for 15 years, you have been always guaranteed a gain on your house.

ie purchased in 2006 and sold in 2017 was about the break-even point.

Purchasing a house is a long term place to live that should beat rent eventually. Historically, it has been very questionable as a short term investment. Especially given the buying/selling costs and holding costs.

When my mom passed away, my brothers calculated that every month we didn’t sell the vacant house, it was costing us about $800/month for minimal utilities, property taxes, insurance, yardwork, etc. There was no mortgage. She had purchased in the 70’s so Prop 13 had cut that down significantly.

A optimistic would view $800/month as a great rate if they could rent for that amount. Landlords take their cut. A pessimist with a vacant house could view that as a constant drag on income.

Hello Augustus,

I saw this happen to a family member’s neighbor in the east bay SF during housing bust 1. Listed at around $650k and rode it all the way down to $325k (50% drop). I also remember the 1990’s downturn that dropped a family members house from $235k in 1990 to around $175k in 1996 (25% drop). Worst case scenario, mortgage rates continue to rise for years and housing bust 2 is somewhere between housing bust 1 and the 1990s downturn (between a 25% to 50% drop). If inflation gets under control and mortgage rates level off by next year, then you are looking at prices recovering what they have lost, and they will continue the next leg up if mortgage rates drop.

Americans need to recover from their collective interior decorating fetish. A home is a fine thing, but mobility is a lot more attractive to me as I get older.

As for prices recovering next year – I just don’t think so. This was a mania and the underpinnings of that euphoria and FOMO are being worked through, albeit slowly. I anticipate a period of sobriety following all the after-after parties. I know I’ll be hitting snooze a few more times before taking the plunge. Welcome to the snoring 20’s.

Some negative correlation is better than no negative correlation.

Nate,

“Negative correlation” is the definition of what diversification is supposed to accomplish.

Bonds and stocks used to have negative correlation. If the price of stocks went up, the price of bonds would go down (= yields rose due to hotter economy, higher inflation, etc.). When it got rough for the economy, stock prices would fall, and bond prices would rise (= yields fell because of lower inflation, rate cuts, etc.).

That model has stopped working since QE was kicked off in 2008. Since then, stock prices and bond prices have gone up together, and now they’re going down together. Their correlation is “positive” – meaning, no real diversification is possible. You’re just betting on the same thing in the same direction, but with two different instruments (stocks and bonds). This feels great on the way up (because both are going up), but on the way down, it hurts (because both go down together).

Wolf, it allows one to short both markets at the same time, and you get a New Age form of diversification by shorting two very different financial markets at the same time. With so many flavors of Short ETF’s out there, it is like being in a buffet line with so many choices.

One can try to trade the counter-trend rallies like this summer, but better to take 20% to 30% profits when you have them in any position and wait patiently on a desert island for the main trend to reaffirm itself. No glory without risk. Not talking $100’s of thousands of dollars here, how about $10’s of thousands.

Yay, I get to chat with wolf about diversification, one of my favorite topics to read about! Happy dance.

So, I did a bit of googling and this is not apparently the first time people have experienced a period of positive correlation between stocks and bonds. I will cite the link since it’s a bit dense and I know you can read the dense stuff better than I can : https://russellinvestments.com/us/blog/is-the-stock-bond-correlation-positive-or-negative

My thinking is that while you are right that correlation has become more positive, which sucks because you’re already trading return but still getting a lot of short term volatility.

BUT! If your time horizons are long and you cannot predict the next phase of negative correlation, then it still may make sense. I guess correlation phases are difficult to predict. Maybe we get a knarly recession in a year or two that finishes inflation, and then fed cuts hard, and negative correlation returns. Likely? Who knows! But after seeing the interesting times we’ve gone through through already, possible.

So, to be more clear, what I meant is that some possible negative correlation probably better than no negative correlation.

Open to hearing about better correlation bets but from what I understand everything has been getting more and more positive over the years. Globalization, more consumer access, and arbitrage are the likely explanations.

Also, some folks value holding less volatile but positive correlated assets even though they sacrifice some overall returns – for example placing less volatile assets you may need in a shorter window, like 5 to 10 years – with a more conservative mix of stocks to bonds, and stuff earmarked for long time horizons (college funds for toddlers; retirement) with their hyper volatile stuff.

Adam Smith’s “invisible hand” has not existed for decades. I know it never really existed at all, but compare that to today where all “prices” are driven by mathematically engineered forcing functions adjusted by computers at microsecond speeds, rather than by true price discovery.

Nate

Ideally, diversification with ‘uncorrelated’ assets as I have mentioned many times, before. See my comment below

9/28/21 Warren called Powell “dangerous” citing banking regulatory issues. He was “dangerous” for BBB as well being unwilling to carry the “transitory” ball across the goal line.

Hes about to get “dangerous” again with a rate hike this month. I forsee narrative escalation to “extremist” in the wake.

I dont think he will be renominated for another term. The Powell Pivot will be to a consulting gig at the Workd Bank.

“I dont think he will be renominated for another term.”

I doubt if he would even consider another term. With his millions ($$$$$), he should retire and live the good life for his remaining years.

Warren and Trump are on the same side when it comes to cheap money. Kinda makes you wonder if the whole thing (Dem vs Rep) is nothing but a sideshow…..

Wolf – Any thoughts on the European energy derivatives market?

Let it blow up. Let some hedge funds blow up. Get it over with.

My sentiments exactly.

But many European Countries are buttressing these energy economies with loans and special funds, b/c of their derivative exposure (1.5 Trillion). How long they can kick this can down? Thanks.

I agree with Wolf. Countries, including the US, will learn the lesson to not be energy dependent on another country for the sake of Climate Change and ECG which is a farce!

Harvest your natural resources and keep your Nuclear Plants. If Germany didn’t shut down their Nuclear Plants for the sake of ECG, they would be energy independent today!

But, but, but………….. you are on record as stating that sanctions on Russia would have no impact on the world economy at all.

Care to revise that now?

I’m on record stating that this is a WAR in Europe, and there are costs to a war. Putin invaded a European country. Look at a map. What is Putin going to take next if you let him? Poland? Former East Germany (which he liked so much)? The Czech Republic? He already took part of Ukraine in 2014. Putin’s territorial ambitions must be stopped. And so far, the Ukrainian military, support from the US and Europe, and the sanctions are doing a pretty good job at stopping him. But there are costs too.

Because real estate is such a slow and sticky market, the holy moly IR effects maybe not have even started.

All those unlocked in need of refi may drown quickly as the recession is already here.

Watch out below.

The effects of the higher interest rates have started. One just need look at markets like Phoenix, some in CA, ID and more to see price cuts galore needed to bring in buyers.

“In terms of diversification between stocks and bonds, there is none”

This is a well known fact for those who have undergone Bear Mkts in the past. Now, in this 3rd largest ‘everything bubble’ mere diversification won’t protect one’s portfolio. The ravage of the Bear will be a lot worse than previous bear mkts.

One diversification with ‘uncorrelated’ assets including measures to go AGAINST ‘the mkts, in whatever form one is comfortable. Unfortunately many retail investors loathe to do this. Hence many will end up holding the bags, just like in the end of each Bear mkt.

Re: Lack of Diversification between stocks & bonds and the comment “This is a well known fact for those who have undergone Bear Mkts in the past.”

Not true! In 1987, 2000-2003 or 2008-2009, bonds, especially Treasuries, were an excellent diversifier for bear markets in stocks. “Flight to Quality” was a meme back then.

You have to go back to the 1970-1982 timeframe to find periods when bonds didn’t provide diversification insurance against bear markets in stocks.