First signs the juice is coming out, with several months lag.

By Wolf Richter for WOLF STREET.

Signs are now everywhere that the crazy housing market is turning the corner. Earlier today the Census Bureau reported some chilling data on new house sales and prices, which plunged in June, as inventory surged to the highest since 2008. The National Association of Realtors reported last week that existing home sales in June also plunged, even as inventories jumped. The trio of national housing reports was rounded out today by the S&P CoreLogic Case-Shiller Home Price Index.

All real estate indices lag reality on the ground. But the S&P CoreLogic Case-Shiller Index lags the most, though it is perhaps the most reliable index for actual changes in home prices.

Today’s release of the Case-Shiller Index was for “May,” which consists of the three-month average of closed home sales that were entered into public records in March, April, and May, of deals that were made a few weeks earlier, roughly in February, March, and April.

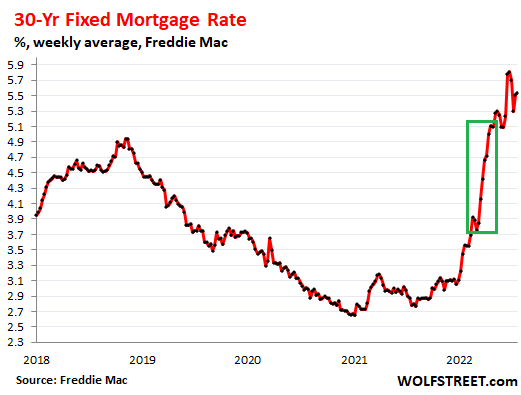

In early February, mortgage rates were 3.5%. By mid-April, they pierced the 5% mark – roughly the range that applied to the deals in today’s “May” time-frame of the Case-Shiller Home Price Index (green box):

But the first signs of a slowdown are creeping into today’s S&P CoreLogic Case-Shiller Home Price Index, with declining month-to-month price gains: In “May” (average of March, April, and May), the index gained 1.5% from “April,” down from the gains of 2.3% and 2.6% in the prior two months.

In some markets, month-to-month price gains were still huge. In others, they were much smaller: +0.5% in Seattle, +0.6% in San Diego, +0.9% in San Francisco house prices, with condo prices being flat.

The year-over-year gain of the National Case-Shiller Index slowed to 19.7%, after having been above 20% in the prior three months.

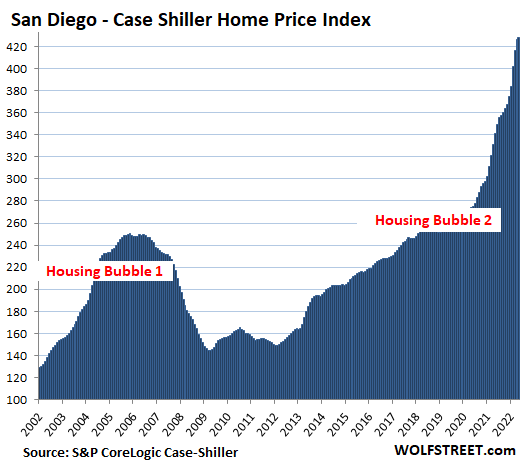

San Diego metro: Prices of single-family houses rose by 0.6% in “May” from the prior month, which was just a pale imitation of the 4.5% jump in “February” and the 3.7% jump in “March.” In the chart, you can barely see today’s tiny uptick compared to the spikes in prior months.

This 0.6% gain whittled down the year-over-year gain to 25.6%, which is still ridiculous, but down from +29% a few months earlier.

The index value of 428 for San Diego means that home prices shot up by 328% since January 2000, when the index was set at 100, despite the plunge in the middle (CPI inflation amounted to 75% over the same period). This crowns San Diego the most splendid housing bubble on this list, followed by Los Angeles and Seattle.

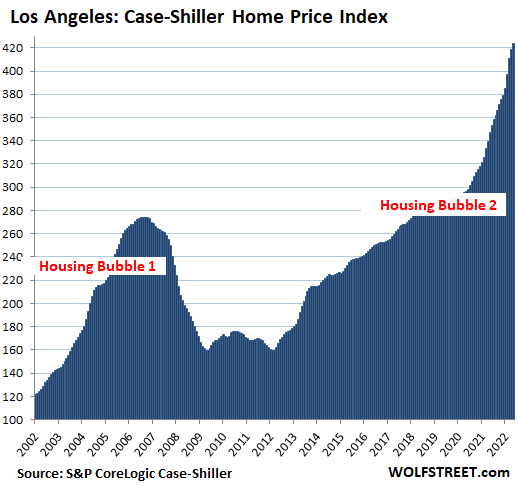

Los Angeles metro: +1.1% in May from April, still huge, but down from jumps of over 3% in February and March. This whittled the year-over-year spike down to +21.7%.

The index value of 423 indicates that house prices surged by 323% since January 2000, making the Los Angeles metro the second most splendid housing bubble on this list:

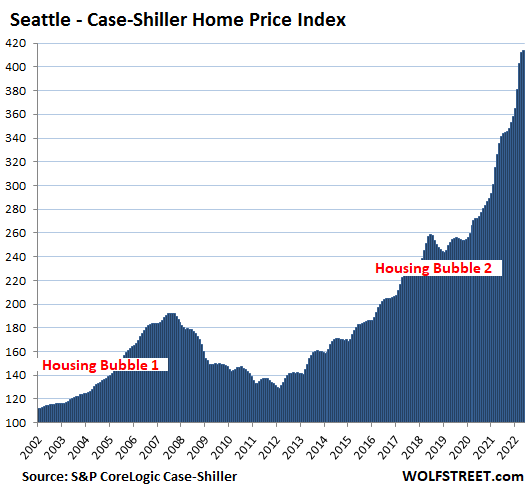

Seattle metro: +0.5% for the month, compared to the 5.6% spike in March and the 4.4% spike in February. This whittled down the year-over-year spike to 23.4%, down from 26.1% in April and 27.7% in March:

Not a miracle but house price inflation. The Case-Shiller Index uses the “sales pairs” method. The sales in the current month are compared to when the same houses sold previously. For example, the five-county San Francisco Bay Area has between 3,000 and 5,500 of these “sales pairs” each month, depending on the season. The price changes within each sales pair are then integrated into the index for the metro, and adjustments are made for home improvements (methodology). In this way, the index tracks the change in dollars it took to buy the same house over time, which makes it a measure of house price inflation.

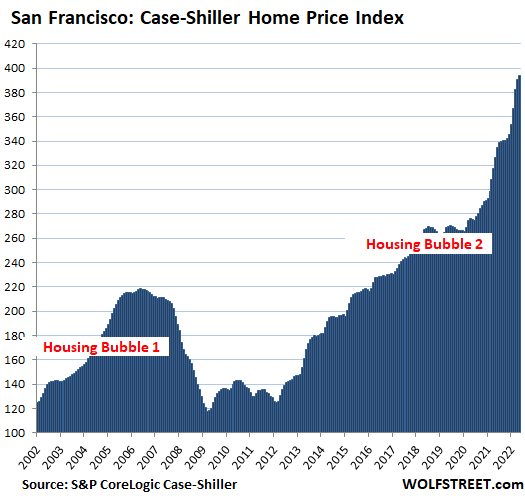

San Francisco Bay Area (five-counties covering San Francisco, part of Silicon Valley, part of the East Bay, and part of the North Bay): +0.9% for the month, down from gains of +2.1%, +4.3%, and +3.7% in the prior months. This whittled down the year-over-year spike to +20.9%, down from +22.9% and +24.1% in the prior two months:

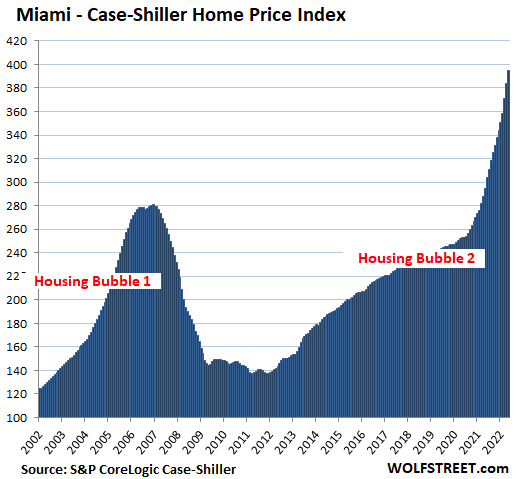

Miami metro: + 2.8% for the month, down from +3.4% and +3.6% in the prior two months. But no whittling down, in terms of year over year: +34.0%, up from +33.3% in the prior month, fastest craziest year-over-year spike in the data:

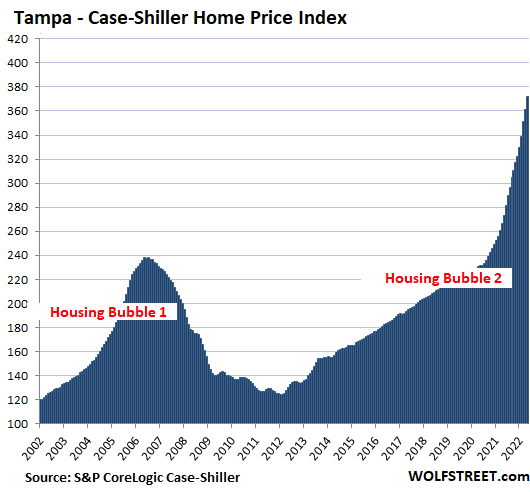

Tampa metro: +2.8% for the month, down from the 3.0% and 3.7% spikes in the prior months. Year-over-year: +36.1%, up from +33.3% in April, a new record in the data:

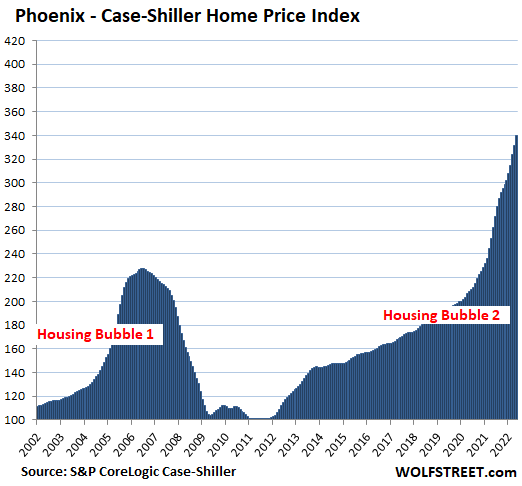

Phoenix metro: +2.5% for the month, same as in April, and down from +3.0% in March. This whittled down the year-over-year spike to +29.7%, the first month since June 2021 below +30%!

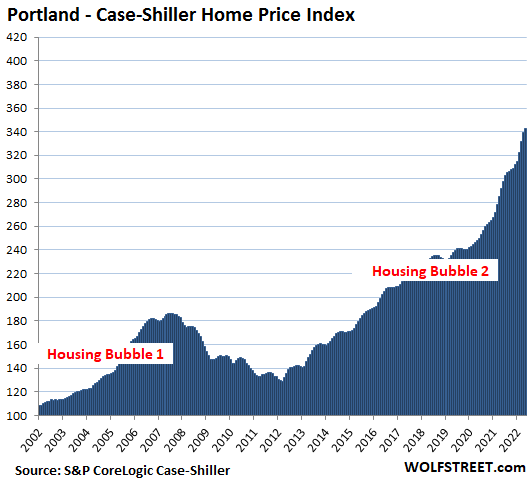

Portland metro: +0.9% for the month, down from +2.2% and +2.9% in the prior months. This whittled down the year-over-year gain to +17.4%, from +19.1% in April:

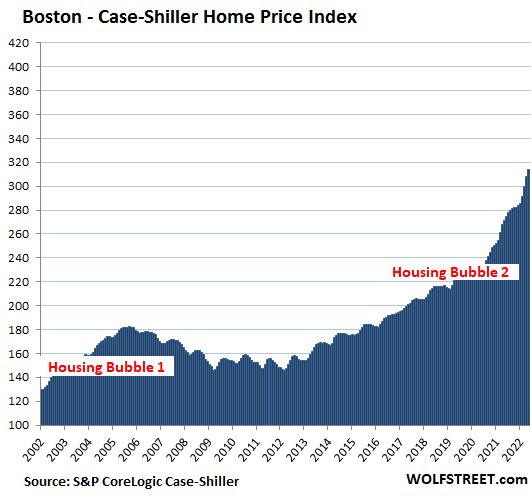

Boston metro: +1.9% for the month, down from +2.8% and +2.6% in the prior months. Year-over-year, the index jumped 15.7%, compared to 15.1% in April:

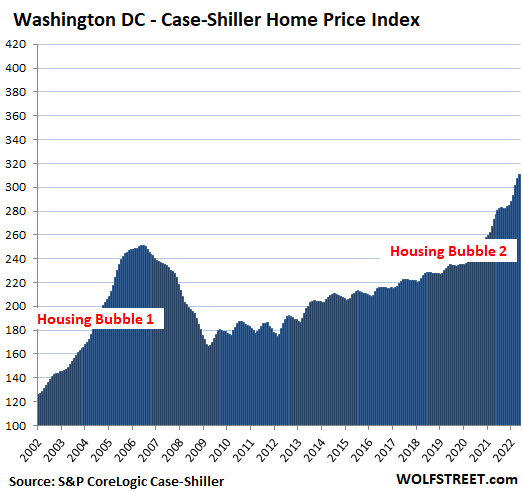

Washington D.C. metro: +1.1% for the month, down from +1.9% and +2.9% in the prior two months. This whittled down the year-over-year gain to +12.2% from +12.7% in April:

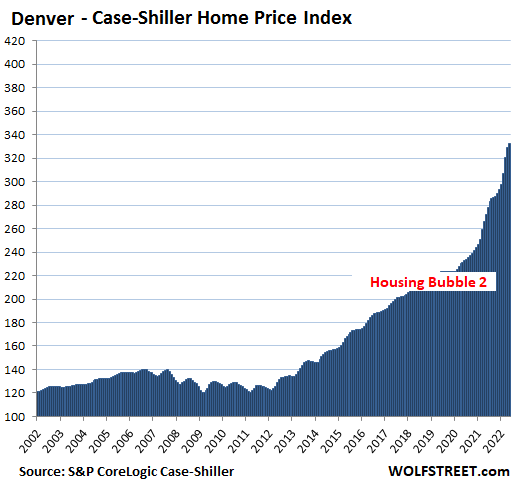

Denver metro: +1.1% for the month, down from +2.5% and +4.5% in the prior two months. This whittled down the year-over-year gain to +22.2% from +23.6% in April:

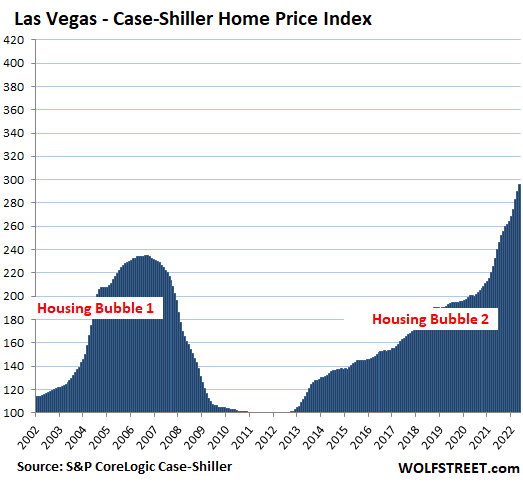

Las Vegas metro: +2.1% for the month, down from +2.3% and +3.1% in the prior months. This whittled down the year-over-year gain to +27.4%, down from +28.4% in April:

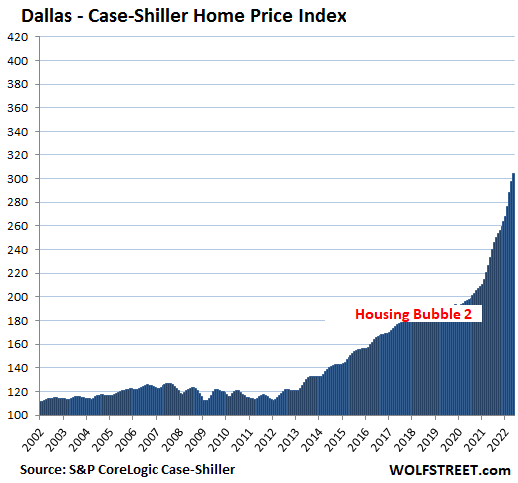

Dallas metro: +2.6% for the month, down from +3.2% and +4.3% in the prior months; keeping the year-over-year gain roughly flat at +30.8%:

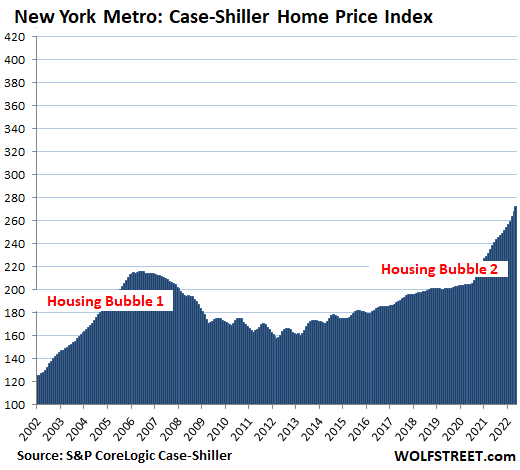

New York metro, the vast market within commuting distance to New York City: +1.6% for the month, down from +2.0% in April. Year-over-year, the index gained 14.5%, roughly the same as in April.

With its index value of 272, the New York metro has experienced 172% house price inflation since January 2000. The remaining cities in the 20-City Case-Shiller Index (Chicago, Charlotte, Minneapolis, Atlanta, Detroit, and Cleveland) have had less house price inflation and don’t qualify for this illustrious list.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Market just frozen and illiquid where I am and where I would choose to move.

The Fed skews all they touch

It will get liquid when seller drop asking prices enough to where the buyers are. The sellers are just slow in accepting reality.

I heard many real estate agents are advising buyers to take taking credit from sellers when appraisals are coming low or when other contingencies are hit.

They do this so that listed sale price doesn’t drop and they prevent panick from spreading and get higher commissions!

It’s an old scam but a good one.

Next level is under the table payments so the buyer has a down-payment.

In a Chicago metro area including Crook County better for buyer to have lower sale price recorded for property tax purposes.

I’ve heard getting a credit to buy down the rate, not the price.

SS,

Back in the Stone Age, real estate agents invented the term “creative financing” to describe the process whereby the seller took back a second mortgage and bore the risk of loss.

One really funny thing is that now it’s a norm in US to take photos of homes from a height of 40 inches, the same height from which a 5 year old sees the world. It makes standard homes look like mansions in photos.

When you walk into this home, you realize how much smaller it is in reality and probably build like a mansion for hobbits

You don’t seem to understand. Buyer can’t take credit from a seller due to low appraisal and keep price the same. If appraisal comes in low, that is the value the bank will lend on. Buyer cannot agree to keep a higher price unless they make up the difference between appraised value and sales price with cash.

I couldn’t agree more but reality is coming home to roost. I am a 15 year Realtor and I call it out as greed, we will all pay for the greed and the stupidity!

MBS rolloff from the Fed balance sheet seized as a result.

Thankfully the Treasuries side is doing fine.

“MBS rolloff from the Fed balance sheet seized as a result.”

Nonsense. MBS don’t “roll off.” Pass-through principal payments (from mortgage payoffs, refis, and regular mortgage payments) are doing just fine.

What is now showing up on the balance sheet are the Fed’s purchases of MBS done months ago in the To Be Announced Market (TBA), that take months to settle, and that are booked only after they settle. So there is this lag on the balance sheet. Current purchases – to replace the excess passthrough principal payments – are much lower but those purchases won’t settle until 2-3 months from now, and won’t show up until then.

Read this, esp. the section on MBS. It explains this in detail:

https://wolfstreet.com/2022/07/07/feds-qt-kicks-off-total-assets-drop-by-74-billion-from-peak-new-era-begins/

Just wait for few months or quarters

Sellers would come out in droves 😀

Very clear from these graphs that only the top formation in housing bubble #1 took 2-3 years. Then it dives at same rate as it ascended for another 2 years. We are looking at 2026-27 to see the bargains.

Rather than years I think it takes layoffs and unemployment. That leads to missed payments and jingle mail. When the banks reposes more homes than they want they will start to make deals and prices will normalize.

Danlxyx,

Most of the mortgages today are govt owned…

The govt will create all kind of schemes to avoid absolute foreclosure at taxpayer expense…

Honestly I have no idea how things would turn up bit wolf provides fact based analysis and he has been right so far on macro basis.

He rightly anticipated asset bubble crash and we are seeing it in stock and cryto so far and looks like housing is next.

COWG,

I’m expecting mortgage and foreclosure moratorium too and not just for financial reasons either. The potential foreclosures will almost certainly be demographically concentrated and the political sentiment is to transfer wealth to these groups.

Yes. I feel like most of us have trouble imagining how different things could be within a year regarding asset prices. Just look at the house price history. It’s caused by cheap money leverage, not real income growth.

It seems to come down to how tight will money have to get to kill inflation and when will Fed pivots?

my guess is the “sellers” will be those in the RE industry who’ve had their incomes slashed or no income and this time around there is no PUA to prop them up like in 2020. Agents, mortgage brokers, and everyone else in line who earn their living off of the transaction.

RE agents are going to have to start pressuring sellers to lower their asking cost so that they can get a transaction through and put food on the table.

You know I can’t resist to comment on a housing bubble article from Wolf. I think the take away from the inventory numbers now to 9 months level is the velocity and speed of the trajectory of the reversal. Isn’t 6 months the normal market equilibrium? It’s giving me some hope that perhaps the price reversal might happen much faster than last time given all the other signs are also happening faster this time around.

It will be interesting to see what the month to month price decrease count numbers look like when Realtor.com release the monthly number next month, so far the last 3 to 4 months is a like a straight line up when I charted it out even in SoCal.

“Much faster”

Many, many, many more housing mkt participants know that interest rates are the whole game – and then some – when it comes to sales prices, relative to implosion 1.0

Mortgage rates are followed religiously now, week to week, Fed meeting month to month.

And rate history, yr by yr is known like the bible.

So, there was zero chance that the rapid undoing of decade long ZIRP wasn’t going to create a speedy and sustained rush for the exits.

We ain’t seen nothing yet.

Many banks still providing mortgages at 75% of take home salary in no-recourse states.

Makes me wonder who will hold the bag in the new crash.

Because banks don’t eat their bad loans.

Taxpayers do.

BS

Gomp, I am talking about a city where Median single family home is valued >1.5 million dollars and median income is >130K.

If you look at housing bubble 1 (and many other examples from science and nature), the decrease pattern/rate is for the most part an inverse mirror image of the preceding increase pattern. In nature this often follows the ‘logistic distribution’.

As such, the rate of decrease may very well mirror the rate of increase. This may serve as a guide to the future as far as prices go.

New home builds in Central Ohio are sticking to their prices, which is $40 more a square foot, compared to 3019. If you go back to 2016 it is doubled! Unfortunately, you get less for the price too – due to demand.

the Debt market will drive the price of housing to the rent equivalent pmt price. Just like in Canada. Existing homeowners that paid the high prices won’t be eager to sell with the drop in price or with no equity can not afford to sell. The 10 year treasury is dropping which may bring down the borrowing cost. Who is buying these 10 year treasury notes? Not the FED maybe foreign buyers.

Actually, net-on-net, due to timing effects (Fed QE earlier in the year, burgeoning tax collections, April tax deadline, taxes due end-of-quarter) there has not been much net new treasury issuance this year until now. That will change as we progress through August, September and October and it will be interesting to see how the market handles this change in the treasury market. Some say the RRP balance will reverse to take up the slack but it’s difficult to tell what the actual effects will be.

You seem to think sellers have some magical options in a declining market.

Eager to sell? Can’t afford to sell?

Reality doesn’t care. Homeowners sell for a myriad of reasons; job loss, promotion, new job, growing family, divorce, death, retirement, etc.

Jingle mail was a thing in HB1. So was sellers bringing cash to the settlement table to get the monkey of their house off their back.

Fires seem much more common then too.

Builders’ best friend in a slow market. Plumber forgot to turn his blowtorch off and the painter spilled his thinner.

Linseed oil soaked rags are all that you need. Gotta refinish that woodwork!

Agree

Common fantasy that government or any individual is in control of reality.

People may not want to sell but they may be forced to pay.

The name of the game is inflation which is dictating Fed’s policy.

Remember Fed inflation target is 2 percent and it is currently at approximately 10 percent.

So Fed would be hiking rates and tightening till inflation reaches say below 4 percent.

Also Remember nothing goes in a straight line.

Lets see

If the Fed hold the course Canada will have significant unemployment.

30% of the “economy” is tied to housing. Unemployment will mean forced sales at cut prices. There are many “investment” properties that will be transitioning to “dead weight” properties.

Canada will be late to the party as most of the population are insane about housing, but when the penny drops you will hear it.

Presently in two thirds of Canada there are no workers for minimum wage jobs. Residential rents are higher than wages and no one will work those jobs.

GOOD point TRT!!!

Time and enough for all, repeat ALL WORKERS OF THE WORLD,,, AKA ”Wobblies” to make their ”needs” front and center in ALL of these negotiations, etc.

Will they do so, unlikely.

Most will understand the precarious condition of their ”work” as broadcast daily and repeatedly by MSM, etc., MSM doing what their owners, the oligarchs demand/insist…

WE the PEONs must insist unto our last kick of the bucket that at least SOME TRUTH prevails on WWW,,, otherwise, continuing slavery by any name,,,

WAGE Slave,,, etc., etc.

I wonder what the percentage of foreign buyers is in the stock market too.

Inflation, which has been underreported for years, must be considered in evaluating real estate prices, NOT the manipulated CPI but real inflation: inflation, IF measured by the more accurate, 1980s method, which did not involve subjective opinions or gimmicks, is reportedly over 10% per year. If the house prices are only keeping up with the decades-long inflation, then demand may cause the prices to remain high.

After all, other investments are not as useful to owners and are perceived as riskier. If the Uganda reports of a huge gold discovery are true, gold will become cheaper and almost ubiquitous. Too many companies now are run like Enron was, so too many have stock values that are far in excess of their true values, even if their stockholders do not know that.

Bonds and treasuries are effectively paying negative interest rates if you compute in real inflation. If prospective purchasers are looking at renting as an alternative to buying real estate, as they must, then real inflation may force them to lower their sights and buy cheaper, less impressive real estate rather than wasting the opportunity to get some equity by renting, if that is all they can afford: [Below is a quote]

…CPI doesn’t reflect this huge increase in housing costs.

“Rent of primary residence” is the government’s estimate of rental costs and it makes up 7.6% of the overall CPI. It ticked up just 0.3% for the month of August. It has been running a monthly increase of 0.2% all year. Over the previous 12-month period, it rose a mere 2.1%. That’s just slightly above the 1.9% year-over-year increases in prior months.

But if you’ve actually searched for a place to rent, you know prices have skyrocketed far more than a couple of percentage points. The data bears this out. Apartment List’s rental index increased by 2.1% from July to August. That’s in just one month. Since January 2021, the national median rent has increased by a staggering 13.8%. To put that in context, rent growth from January to August averaged just 3.6% in the pre-pandemic years from 2017-201

Quote from Shiffgold’s “CPI Housing Cost Calculation Hides True Extent of Inflation”

Hence, in many areas, real estate may not be in as much of a bubble as other assets, because inflation may have made its price increases modest and justified in areas with limited houses, and compared to renting, it is useful, if you can reside in the real estate even if you pay extra, because of the tax deduction for home mortgage interest. Furthermore, because CCP crooks and other foreigners view real estate in the USA as a very safe investment, their beliefs create a self-fulfilling condition: like the traditional love of gold in some societies, like India, gives it a value that its inherent usefulness (e.g., in electronics) could not provide by itself.

Of course, areas that lack access to enough water may become less desirable with time and crash in prices, like Phoenix, since the utility of such real estate may be less for those who do not want to have a cactus garden instead of a lawn and water rationing instead of a pool.

Yet another attempt at rationalization.

How many are basing their purchase and sale decisions using anything like your theory?

The US housing market has never been more overpriced than it is now and less affordable.

“Who is buying these 10 year treasury notes? Not the FED maybe foreign buyers.”

Great question, and I’d like specifics, not hidden behind some nebulous category name such as dealers and brokers, investment funds, or foreign.

What else are you going to buy? Stocks and lose 50%?

NYC is the least bubble of all the bubblicious metro areas.

But still a massive bubble just the same.

A 75 or 100 basis hike tomorrow will help!

NYC’s crime and $5k/month average rents are going to keep the suburbs and exurbs RE from tanking. Prices are going to have to come down, its unsustainable here even by East Coast standards, but probably not like Boston or D.C. will see.

As landlords are squeezed out by high rates renters will become owners at cheaper prices. Rents are only so high because so many are locked out forever.

The money made in housing was because they kept cutting rates. That’s over.

They claimed the other night on the news that NYC rents hit $5k a month average from all the people moving back into the City after they left during the pandemic. Apartment shortage, you see. Damn near snorted my beer laughing.

No one is clamouring to move back into NYC. Sure, some got reluctanly dragged back to the office and discovered how much it really, really sucks to commute on the Taconic/Bronx River Parkway. They are mostly maintaining weekend homes out here and clogging the highways on the weekend, or renting out/AirBnb-ing their quaint new country homes at a premium killing off the locals.

But NYC apartment shortage? In a time when the highways out of the city are jam packed in all directions because crime is so bad no one can feel safe walking to the corner store? Wolf surely has data insight to this, but from the eyes on the ground, naw. The Brooklyn trust fund kids aren’t as hardy as the 70s and 80s- era city folk they gentrified away. Folks want out, not in.

Could be all the delibrately unrented NYC apartments keeping rents hyper inflated, and sure, the prices will soften sooner or later and they will get rented in some controlled quantity eventually. But the endless stabbings, shootings and car/catalytic converter thefts, robberies, subway shovings and slashings are keeping the dazzling urbanites pushing outward and that keeps the greater tri state area excessively pricy. Anyone can tell you NYC, like San Fran & LA will never not be ungodly expensive, just eventually less so than at present but the crime is dragging it out.

Its not like there’s a ton of virgin land to expand into/develop around NYC. They’re doing their damndest to pile in and build upward even in the quaint Westchester towns, but the ripple has long been felt in the 2 hour radius and I’m under no delusions we’ll see sanity as long as the crime spree continues no matter how high the interest rates go. Competing factors, certainly, but not holding breath for a huge crash unless something beyond catastrophic happens to Wall Street.

Boston is beyond stupid. I live in a rag-tag little industrial town within an hour’s drive of Boston. The stupid rents in Boston plus the FOMOs who wanted a grill or something have led to more people moving here, causing prices for single family homes to rise above $400,000 (median) for the better part of a year now. Rents are up to $2000+/month for a dilapidated 3-bedroom, too. The median household income in my town is about $75k. My husband and I make pretty good money on paper, but we’re struggling to save enough for a down payment. I can’t even imagine being a median wage earner or below. You can’t pay rent in a safe neighborhood AND feed your kids on the median wage here. I’ve been donating a lot of diapers to our local food pantry recently.

People can save a fortune with cloth diapers ,I used them for my kids . But u have too get off your ass and do a little work

“Rents are up to $2000+/month for a dilapidated 3-bedroom”

You are describing Utopia for Californians who pay $3000/month for a studio apartment.

Used to live outside of Worchester in the early 00’s. Housing was almost as bad as the NYC area price-wise, but worse in ways from complete lack of public transportation, no sidewalks, and of course the weather.

Cars are mandatory so if you’re horseless in suburban MA you’re up the creek. If its worse now and surely it is, I really pity the locals.

Flea – broke people with kids aren’t all lazy. Shocker, to be sure.

Cloth diapering is lovely for folks who have ready access to on-site laundry facilities and/or lots of time to be elbow deep in diaper wash all day. Neither scenario is typically applicable to poor working parents renting crappy apartments.

The NYC market is dependent upon the FIRE sector and foreigners.

An end to the global asset mania will create large scale unemployment in FIRE and make wealthy Americans and foreigners both a lot poorer.

Historically, we can mathematically determine where housing prices should be based on what used to fundamentals before government buying/guaranteeing of all mortgages, ZIRP and easy money QE.

An average house should cost about:

2.5x average household income. Slightly higher for waterfront

100-120× average comparable rental

Total housing expenses (mortgage, taxes, insurance, maintenance) no more of 30% of NET (take home) household income.

And remember, on the way down it will shoot through that “floor.”

If I buy something during next recession it’s probably going to be an almost new mobile home, because used mobile homes are tough to finance so it’s a cash market. Not that many people with $50k – 100k cash walking around in a recession that want to live in a mobile home.

Stick built home pricing all built on monthly payment buyers, not cash.

S&P futures up over 1%. What do these rats know that we don’t?

Bad news is good news. This economy is tanking at a rate much greater than the lagging charts show. Had a front row seat last time around.

This time….fishing poles & gear are ready for an extended vacation.

They know nothing. It’s game-playing by big traders to suck you in.

The market isn’t going anywhere as long as the Fed is committed to its QT program, which barely started. Decent news from Microsoft and Google today only gives the Fed more confidence to tighten.

Yeah I’m rooting for the stock market to hang in there. The longer it holds the line the longer Powell has to hike!

actually, I’m noticing more houses hitting the market every time it goes down and slowing when it goes up. There’s a lot of leverage there. Could have a lot to do with bitcoin etc too.

Lynn,

I rode around yesterday on my scooter through our high end residential areas and saw very little for sale. I was surprised. Still a lot of new home construction and major remodels going on. I’m 45 miles outside of Raleigh, NC.

Still a very tight labor market here.

Old School – local economy is still strong. We are sort of the Mexico/China for tech jobs. A lot of late (or even post) cycle construction (institutional, bio labs, etc) typical for this market is normal. It will deflate, but probably a bit slower tgan elsewhere. “Advantage” of relatively poor, highly educated folks I guess.

Old School,

I too am in Raleigh. I drive through all sorts of neighborhoods here for work. The number of signs are recently increasing. Agree that labor remains very tight. When I ask people’s sentiment, all I hear back is “well you know, Apple’s new campus is coming & …,” I hope they are ready for announcements of construction delays. That’ll kick off the erosion in pricing.

My sense is that most people here believe that our region’s economy is as resilient as the prior downturn. It is. It’s the nature of the downturn that has changed. In a word, inflation. Too many are trying to fight the last war (GFC), I think we lost that one.

Well if it’s anything like last couple of times, FED announce rate hike, market goes banana and rally up the day off, then tank the next day…perhaps same pattern is repeating itself again

Seems to me that for the very short term the S&P is acting range bound. We tested the resistance once and just tested the top. What happens next, who knows, but the trend is down, as well as negative macro, negative geopolitical, negative monetary policy, and a Sisyphean fiscal policy (the rock just keeps getting heavier and heavier).

Nothing goes up or down in a straight line.

Don’t lose the forest for trees.

It is just a sucka’s rally being orchestrated by the big players and whales

Or the S&P 500 is priced based on 6 to 9 months out and the current economic downturn is expected to be very short-lived.

That’s because the “market” is convinced the Fed will pivot and start printing again come December or January. If they’re wrong, they’re going to get their clocks cleaned.

Futures don’t matter.

I agree. The future does matter, but futures?

The right words were used in the conference calls (“doubling of revenue in 2040”, “positive outlook”, “light at the end of the tunnel”, “upbeat expectations”) to trigger the artificial idiots. There were no brains involved. No big secret here. It’s all just a shitshow now. Musk is a genius at that. Inconvenient for him that his “Head of AI research” just left.

It wouldn’t surprise me to see the Florida graphs above (Miami and Tampa) go down at the same rate they went up in this Housing Bubble 2.

As usual, another great article by Wolf Richter.

The slope on these graphs are incredible.

Just remember that those slopes represent the complete end of any financial planning or hope for the future for many people under 40, for many, many years.

And the destruction of genuine productivity (not fake GDP housing numbers “productivity”).

The financial/retirement plans for a lot of “people under 40” is to inherit their parents’ hard earned retirement accounts and real estate portfolios. Til then, they complain about how their parents’ generation ruined their digital nomad lives and reduced the number of counties they travelled to by age 30 from 100 to 50

Any way we could get a block on these generation warfare comments? It’s not conducive to discussion, just pointless blood pressure raising all around. We’re all on a sinking ship, regardless of age. The poorest, the youngest, the oldest, and the disabled are on the lower decks.

CCCB—

Their parents will probably screw them in the end by taking out reverse mortgages on their homes to fund their lifestyle. The banks will then get their homes when they die.

So much for their heirs.

“hard earned” lmao

Tony, and the following generation may screw the banks if they do not have many children. A shrinking population is poison to an economy founded on exponential growth.

I wouldn’t either. A lot of people moved to Florida in anticipation of working from home forever. Unless their jobs stay that way, they’re going to have to go back.

A neighbor’s fire damaged home was purchased by a flipper for $200,000, in a $370K neighborhood. The flipper did an OK job, spending at least $100,000 on updates. The flipper put it up for sale at $540,000. I and my neighbors were in disbelief at the price. After a week, price dropped to $539K, then $519K, then $499K. It is now $479K, and dropping $10K every four days. The flipper (in Salem, OR) hoped to get a sucker moving from Portland or California. Didn’t work. Interesting to watch.

They just left it too late…. lol

I’m seeing houses like that coming onto the market here, although they don’t look to have spent anywhere near $100K on them.

A tell tale sign of a flip in my area is cheap really ugly and BUSY zebra looking hickory laminate flooring. The very same flooring a liquidator constantly has on sale because it’s so butt ugly. You see it in a lot of upscale very expensive houses on 20 acres of unusable land 10 – 25 miles out on dirt roads in the worst fire hazard zones. With unmaintained 1/4 mile dirt driveways. With the mold just painted over. But they forgot to sandblast the water damage from leaky roofs on the wood paneling. Oops.. My God. What a deal!

My favorite though is exterior T-11 used on interior walls as “upscale” “wainscotting”. That means the lower part of the framing is rotten from the house being used as a blown out pot grow and the T-11 is used on the rotting frame to add stability and keep the drywall from warping too fast.

We lived in Salem for quite a few years. Purchased a home in a nice part of town in 1992 for $230,000 when the average home price in Salem was about $150,000. Saw its value appreciate to $540,000 at the peak of the 2008 bubble and then collapse back so that we only got $285,000 when we sold to move out of town ( for job reasons) in 2012. So I think your flipper neighbor better get ahead of the curve or they will be toast.

Statistics are fine.

However, anybody with some background or experience in real estate knows the absolutely last thing a bank wants is to have a foreclosed property on their books. First, it’s not their business. They are about creating money out of thin air and collecting the interest on it, they aren’t realtors. They simply do not know what to do with them. Second, a foreclosed home on one side of the balance sheet and a loan/mortgage on the other side that is way higher than the value of the property is a serious solvency risk for a bank. Better to keep the illusion going for as long as humanly possible and keep the garbage off the books.

That means you can bet your behind there are a considerable number of houses out there that factually should be foreclosed, but the banks jump through all kinds of hoops not to have to kick the bums out. That’s of course a ticking time bomb for the banks.

Banks sell most of their mortgages to government-sponsored entities and government agencies and collect a fee for writing the mortgage. The amount in mortgages that banks hold on their books is just a small portion of total mortgages. Most mortgages have been securitized into MBS and are held by investors, global bond funds, global pension funds, the Fed, other central banks, etc. And the US taxpayer is bigly on the hook.

So the whole foreclosure process is now fairly complex. But it’s not the banks that we need to worry about. It’s the taxpayer.

I’m a Bay area techie who moved to San Diego and purchased a home in Dec 2020. I love the beauty and friends in the Bay area, but consistently felt unsafe and abused by the gov’t there. The upped level of anxiety and social posturing was too much for me. Most of my friends have now also left.

Currently there are 24 applicants for every available rental in San Diego. The difference between the 2008 crisis and now seems to clearly be that rents did not justify the higher prices back then. I tried to find a “good” rental at the premium end in 2020 ($2500 1bd), and It was easier for me to buy a home and pay the $4200 PITI for a 3bd. The rental quality in San Diego is just abysmal compared to any city I’ve lived in, carpet everywhere, lack of garages/parking, never updated.

The rumors I hear are that mom and pop landlords are going out of business and it’s all being acquired by REITs (I’d love to see references that support this) and financed by cheap debt. This presents an opportunity for collusion in rent setting. I know for a fact that a majority of these properties are using dynamic pricing software from a single company.

The quality of life in San Diego simply better than other high-earning cities in a new economy where remote work is permissible. And you get to live in a state that seems reasonable with respect to what’s going on in the rest of the country.

Until rents fall, homes here are still “good value”. I fail to foresee a circumstance that would cause all of these investment firms to offload rental properties or get into such a situation that they would need to decrease rents. The pace of construction is slow, and 2.5% housing is used as STVR/AirBnB, and that is unlikely to change regardless of the new STRO rules. For home prices to fall, there needs to be more supply and transactions happening but who wants to give up their 3% rate? My mother is looking to downsize her home but it makes no sense to do so at 4x the payment. She is “locked” into her large home. How do you address a market inefficiency like that? She’s more likely to move out of the country and rent the home.

I suppose job loss could force them to sell and for people to move away from rentals. Or more favorable tenants rights in California. I don’t think any of the froth has really been removed from the top of this market, the layoffs I’m seeing at layoffs.fyi are exactly what I expected. The 1% who are highly employable can keep this market going for for the foreseeable future. Most of these studies point to the reversion to mean affordability for the average person, but the middle of the bell curve for earnings has been hollowed out due to the wealth disparity. I don’t think we’ve seen this before in a modern economy.

I am in San Diego and I hear the same that this time is different and San Diego home prices won’t go down more than 5 or 10 percent.

Of course peopel in San Diego are crazy about real estate and think it is God’s gift.

Personally I dislike San Diego but stuck here for few years because of kids.

Also inertia kicks in.

The neighborhood is San Diego has really gone down in last decade or so but homes are super expensive

Also home prices are determined at the margins so even small number of transactions can bring down the price of whole neighborhood.

You do remind me of my friends who has firm belief in real estate and think it can’t go down at least in San Diego. So far they have been right.

Btw.. investment first would be the first to sell and they are less emotionally attached.

If the yield are good then why deal being a land lord

This is the magic of real interest rates.

Prop 13 is a huge reason for continuing high prices in coastal CA. My mother in law is in a home in SF she paid 77K for in 1977. Her property tax is 3K a year and she is in her 80s now. In any other state she would be selling and moving, but in CA you keep the house and the valuation and pass to a kid when you die.

Anyone over the age of 55 is eligible to transfer their tax payment (of equal or lesser value), in CA. If she’s selling her current home for about the same price as the one she’s purchasing then her monthly payment should be very low.

Thanks VitaminJ for sharing – a very good insight.

“who wants to give up their 3% rate?”

I think the reasoning like this only works well in a stable market, but I am afraid there will be some drastic (and unpredictable now) moves when the system is going out of a state of some quasi equilibrium it is in now. Mortgage rate doubling in no time may be just a foretaste.

Since when is San Diego a high earning city?

But yes, San Diego’s standard of living is better than San Francisco.

FOR HIGH EARNERS!

The typical family taking in the median of $85K has just about the same buying power of cousin Jeffro in Kentucky. The standard of living is crap thanks to the real estate bubble and now even more so due to general inflation of goods. A correction is sorely needed or they’re all going to end up in Texas clogging up our roads!

1) If China cut our Nerd #1 by 80% SPX might drop to an uptrend Channel from : Sept 30 1974 resignation to Aug 8 1982 recession low // a parallel from Sept 1976 high.

2) The channel top is higher than 2020 low, but below yesterday close.

3) It supported Oct 1987, 2009 and 2020 plunges.

4) Next time SPX might breach it for the first time.

5) For entertainment only.

Careful comparing the stock market of the 70’s and 80’s. The DJIA had a great deal more manufacturing firms in America providing decent wages to the community. Today, all we really manufacture is technology, finance, health care, food and tourism. We live and die by services. Perhaps our dollar is weaker because we do not have a foundation of manufacturing behind it anymore. We no longer produce quality steel from places like Wheeling, WV. I believe the rust belt is the biggest clue to why out golden years passed us by. We allowed globalization, aka cheap labor, to ferry our future away.

Well, if the suffix is “metro”, avoid it like the plague. You might get some appreciation in the real estate, but the problem is you gotta LIVE there.

After 60 years, learned that it is far far better to live among real people than among the always angry “metro” dwellers. They’d literally video you bleeding to death rather than call 911 or help you. Left them in the rear view mirror, the best move of my life.

And guess what, my rural place has appreciated 10% in one year. Nice, but, I won’t be selling.

Interesting aspect of these charts… if you sold back in 2019/2020 when all the chicken littles started crying “real estate bubble – crash coming” you left over 40% worth of gains on the table, more in some markets.

After booking that 40%, I’m happy to lower my asking prices by 5-10% now to beat the bottom chasers out of this cycle (and yes, I know a 10% reduction of a higher price equals more than 10% on the way up) I’ve transitioned from building starter homes to putting new double wide trailers on my developed lots to meet buyers’ and renters’ reduced budgets and expectations.

It’s still not too late to sell, sell, sell, but remember that your cash flow won’t change much, if at all, when you buy back in. Your replacement properties in 2024-2026 will likely have higher mortgage rates/payments, a huge stepped up tax basis, and you may or may not be able to get affordable insurance depending on where you live.

But then I treat my real estate more like Warren Buffet treats his stocks. I don’t try to trade in and out of every dip. Once I buy, I usually keep them forever and they only get more profitable with time. The really big money in real estate is made in the long run.

Comments like this are really tiresome. Those who sold in 2019 or early 2020 were not “chicken littles.” Many of them sold for reasons unrelated to thinking a crash was coming, and even those that were, they were ultimately right based on the financial conditions at the time.

Nobody in 2019 or early 2020 could have foreseen such an obscene amount of monetary and fiscal “stimulus” that artificially inflated all asset prices, and anyone who did benefit from those things merely got lucky. You’re not nearly as smart or clever as you think you are.

CCCB: thanks for those excellent, highly valuable words of wisdom. Note that your perspective echoes what Old School said above.

For you younger folk wondering where and how to get a real estate asset of your own, take some time to think about what CCCB just said:

a. I bought a piece of land, put in some infrastructure (driveway, water and power)

b. I put a series of mobile homes on that lot

That plan can be executed on a very small scale.

The investments can be small to start: a down payment on the land.

Then gradually do the site improvements (road and utility lines), and much of that can be done yourself if you’ve got construction talents.

Buy a mobile home. There are a lot of used ones. Fix it up if you can, or buy one that’s already in good shape.

Put that mobile home on your land, and live in it a while.

Buy another mobile home. Choose your neighbor carefully.

Repeat.

That’s a gradual, modular, manageable plan. Something you can do.

CCCB, if I said anything you don’t agree with, please jump in and set me right. I’m trying to actually help these younger folk. Old School, if you happen to see this, please add your 2c.

I remember by Grandma talking about some relatives who were told to save and buy land then build the basement. Live in the basement! Save fro building the house. The land appreciating and not paying a rent, etc. Little by little you get ahead until you’ve arrived.

My cousin is a house painter. But he’s quite affluent in SoCal with a small rental empire. It started with buying a crappy duplex at a young age, renting out one half and having three roommates crammed into the other half with him. These six or seven people paid for it all while he was out painting houses. He scaled up from there.

Probably less people today want to live gritty, though. Look at the shortage of plumbers and other tradesmen, for example.

The problem is zoning codes. Most land in rural America, especially around Central Ohio, have rules against this scenario. Land in the country with well and private sewer (aka Septic) must have at least 1800 sq foot built on it. You are not allowed mobile or modular (unless grandfathered in) in Franklin County. The closest places to work to allow this is a 45 minute drive with no traffic. Land that once allowed mobile home parks have been zoned as multi-family single buildings. My parents use to say the same thing. Buy land, build your basement as a walk out and live in it. Fix it up as you have money. Paid in full by 30. This is the price the new generation faces thanks to friends from main builders and bankers running city councils. Not to mention many sit on the boards of organizations that employee most of the citizenry. Nope. While old school was working and building, they had no time to keep an eye on politicians that wrecked our society.

Right you are. The Tiny Home folks have a pretty hard time finding a place to settle down near work.

But at least in San Diego little Billy can construct an ADU in Mom and Pop’s backyard, if it’s big enough.

In Oakland, CA, where I live, I already see Condos that have dropped the asking price below what they sold for in 2019-2021

That’s interesting. Few seem to remember in 2019 the housing market was actually showing signs of slowing with some price drops. Then COVID brought forth all the free money and the bubble got a second wind.

Interest rates should be 10%+ already, so we can get back to 2015 and sanity.

Powell floated another dud. He had every opportunity to raise 100 basis points but instead showed his yellow belly. The stock market bubble is roaring, knowing this pathetic clown is as timid as they come.

Time being of the essence has no meaning for him. And neither do people living month-to-month just simply trying to eat.

Imagine if we actually had regular every-day people running the show.

2 more weeks!

Expect the return of making loans to anyone who can fog a mirror. People will be sitting at their desk and will have to make a choice: (1) Lose their job, or (2) make a loan, any loan in order to get the fees and quotas, even if you have to look the other way at falsified “income” documents. Some will even be so desperate that they will help falsify the documents.

Already been going on for the past 5 years.

Well, if that’s the case then,we’ll see some type of implosion relatively soon. Hmmm

It’s amazing how quickly housing prices can change in America. Just a few years ago, many people were struggling to keep up with their mortgage payments and now prices have skyrocketed. It’s important to stay informed about the housing market so you