QE creates money. QT does the opposite: it destroys money.

By Wolf Richter for WOLF STREET.

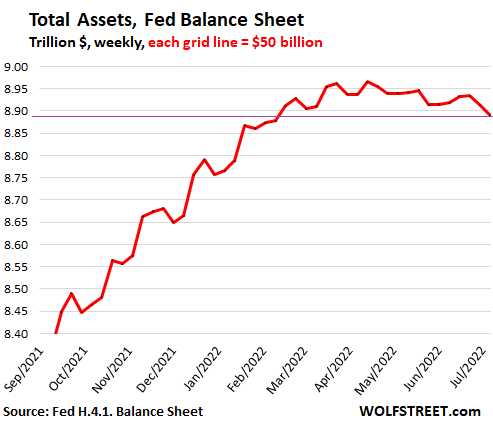

Total assets on the Fed’s weekly balance sheet as of July 6, released this afternoon, fell by $22 billion from the prior week, and by $74 billion from the peak in April, to $8.89 trillion, the lowest since February 9, as the Fed’s quantitative tightening (QT) has kicked off. The zigzag pattern is due to the peculiar nature of Mortgage Backed Securities (MBS) that we’ll get to in a moment.

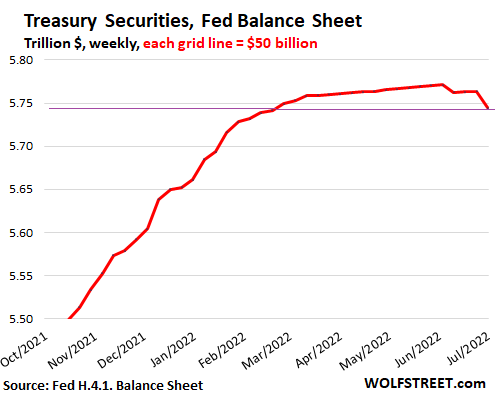

Treasury securities fell by $20 billion for the week, and by $27 billion from peak.

Run-offs: twice a month. Treasury notes and bonds mature mid-month and end of month, which is when they come off the Fed’s balance sheet, which in June was June 15th and June 30th.

Tightening deniers. Last week’s balance sheet was as of June 29 and didn’t include the June 30th run-off. However, the army of tightening-deniers trolling the internet and social media doesn’t know that, and so a week ago, they fanned out and announced that the Fed had already ended QT, or was backtracking on it, because Treasuries hadn’t dropped in two weeks, which was hilarious. Or more sinister: hedge funds manipulating markets through their minions?

Inflation compensation from TIPS adds to balance. Treasury Inflation-Protected Securities pay inflation compensation that is added to the face value of the TIPS (similar to the popular “I bonds”). So if you hold a fixed number of TIPS, their face value will rise with the amount of the inflation compensation. When they mature, you will receive the total amount of original face value plus inflation compensation.

The Fed holds $384 billion in TIPS at original face value. It has received $92 billion of inflation compensation on those TIPS. This inflation compensation increased its holdings of TIPS to $476 billion.

Over the month of June, inflation compensation increased by $4 billion. In other words, until those TIPS mature and run off the balance sheet, the Fed’s holdings of TIPS will increase by the amount of inflation compensation – currently around $1-1.5 billion a week!

No TIPS matured in June. But next week, July 15, TIPS with an original face value of $9.6 billion plus $2.5 billion in inflation compensation will mature, for a total of $12.1 billion, that the Fed will get paid. After that, the next maturity of TIPS on the Fed’s balance sheet is on January 15, 2023. And the TIPS balance will increase from July 15 through January 15 due to inflation compensation.

The thing to remember about the Fed’s TIPS is that the inflation compensation is added to the balance of TIPS and therefore to the balance of Treasury securities, at around $1-1.5 billion a week currently.

The balance of Treasury securities fell by $20 billion from the prior week and by $27 billion from the peak on June 8, to $5.74 trillion, the lowest since February 23:

- Note the two run-offs on the balance sheets on June 16 and today.

- Note the small steady increase of around $1-1.5 billion a week after QE had ended from mid-March into June, which is the inflation compensation from TIPS.

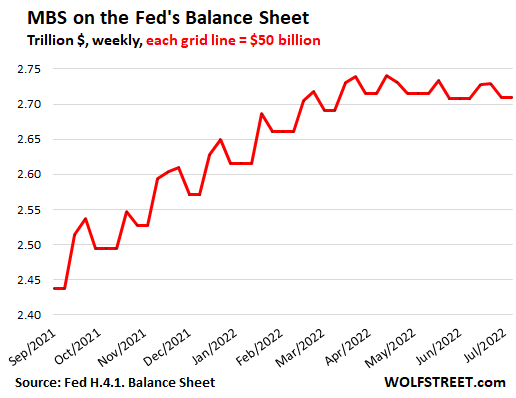

MBS fell by $31 billion from peak.

Pass-through principal payments. Holders of MBS receive pass-through principal payments when the underlying mortgages are paid off after the home is sold or the mortgage is refinanced, and when mortgage payments are made. As a passthrough principal payment is made, the balance of the MBS shrinks by that amount. These pass-through principal payments are uneven and unpredictable.

Purchases in the TBA market and delayed settlement. During QE, and to a much lesser extent during the taper, and to a minuscule extent now, the Fed tries to keep the balance of MBS from shrinking too fast by buying MBS in the “To Be Announced” (TBA) market. But purchases in the TBA market take one to three months to settle. The Fed books its trades after they settle. So the purchases included in any balance sheet were made one to three months earlier.

This delay is why it takes months for MBS balance to reflect the Fed’s current purchases. The purchases we san show up on the balance sheet in June were made somewhere around March and April.

And these purchases are not aligned with the pass-through principal payments that the Fed receives. This misalignment creates the ups and downs of the MBS balance, that also carries through to the overall balance sheet.

In addition, MBS may also get called by the issuer (such as Fannie Mae) when the principal balance has shrunk so much that it’s not worth maintaining the MBS (the issuer then repackages the remaining underlying mortgages into new MBS).

Tightening deniers. So when the tightening-deniers – including a hedge-fund guy with a big Twitter following – trolled the internet and the social media about QT not happening because MBS balance ticked up by $1.2 billion on the June 23 balance sheet, they got tangled up in their own underwear. The following week, the MBS balance fell by $19.5 billion. That’s how MBS on the Fed’s balance sheet work. These folks just didn’t know, or more insidiously, tried to manipulate the markets.

The thing to remember about the Fed’s MBS balance is that it declines due to pass-through principal payments, and occasionally because they’re called, and this is an uneven process.

The Fed’s MBS holdings fell by $31 billion from the peak.

The up-moves in the balance come from purchases in the TBA market during the phase after QE and before QT, when the Fed was trying to keep the MBS balances flat. It has since reduced those purchases to small amounts, but they won’t show up for a couple of months. When they do show up, the up-moves will be much smaller, and will eventually vanish, and only the down-move will continue, and the overall balance will drop faster:

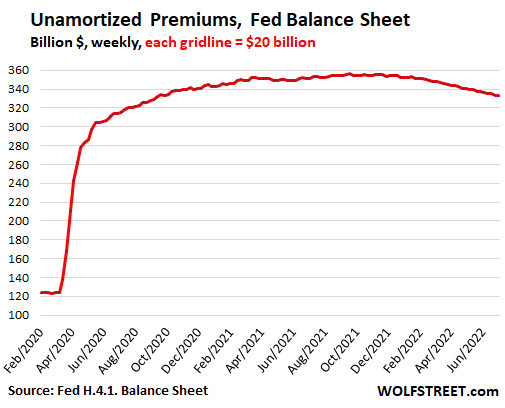

Unamortized Premiums declined.

Unamortized premiums accounts for the amount that the Fed paid in “premiums” over face value when it purchased Treasury securities, MBS, and agency securities in the market.

Bond buyers, including me and the Fed, have to pay a premium to buy securities if the coupon interest rate exceeds the market yield at the time of purchase.

But unlike me, the Fed books securities at face value and books the premiums in a separate account on its balance sheet. This adds some transparency. The Fed amortizes the premium to zero over the life of the bond, against the higher coupon interest payments. By the time the bond matures, the premium has been fully amortized, and the Fed receives face value and the bond comes off the balance sheet.

The unamortized premiums peaked with the beginning of the taper in November 2021 at $356 billion and have now declined by $23 billion to $333 billion:

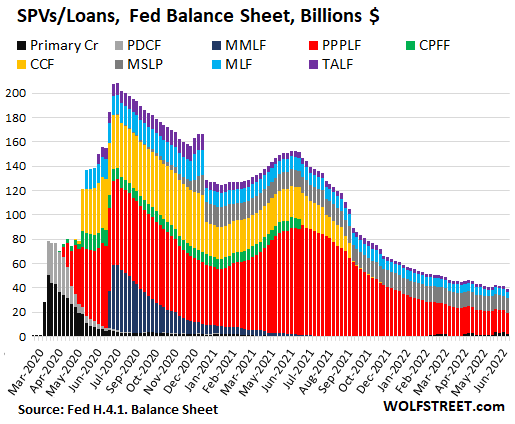

The SPV creatures almost gone.

The Fed set up the Special Purpose Vehicles (SPVs) during the crisis to do QE with assets that it was not allowed to buy otherwise. Equity funding was provided by the Treasury Department. The Fed lent to the SPVs, and shows these loans plus the equity funding from the Treasury Dept. in these SPV accounts.

Four of the eight SPVs have been completely unwound by now, and their balance has been zero.

The PPP loans that the Fed bought from the banks fell to $18 billion and account for about half of the total SPVs. The remainder: Main Street Lending Program ($12 billion), Municipal Liquidity Facility ($7 billion), and TALF ($2 billion). Also listed is the account for Primary Credit (less than $2 billion). For a total of $39 billion, down from $208 billion in July 2020.

QE creates money. QT does the opposite: it destroys money.

With QE, the Fed creates money that it then pumps into the financial markets via its primary dealers, and this money is used to purchase assets, and as this money chases assets, it inflates asset prices of all kinds, which means it drives down long-term interest rates, including mortgage rates, which further inflates home prices, etc. This is the officially stated reason for deploying QE.

With QT, the Fed does the opposite. QT reverses QE. QT destroys some of the money that QE had created, with opposite effect on yields and asset prices, and home prices, etc., driving up long-term interest rates and deflating asset prices.

The Fed is now tightening its policies – raising rates and kicking off QT – because inflation has exploded to a 40-year high, has spread across the economy and deeply into services, and is becoming solidly entrenched. This inflation is in part a result of QE. And QT is one of the tools the Fed is using to crack down on inflation.

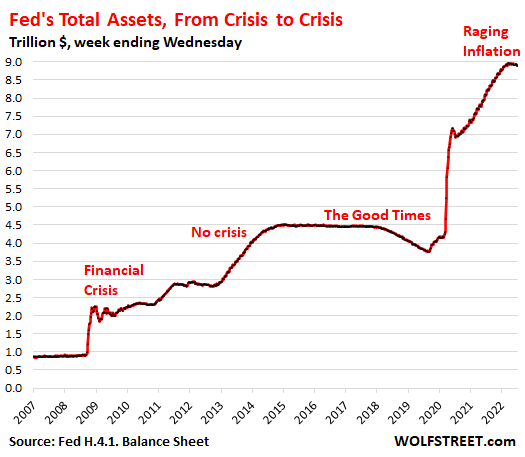

The Fed’s assets from crisis to crisis – money-printing comes home to roost:

In the 15 years of this chart, there are two crises: the Financial Crisis and now the inflation crisis. Today’s inflation crisis pulls into the opposite direction of the Financial Crisis, and dealing with it will require the opposite tools:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I’m not a QT denier, as the information is too public to argue against. However, that doesn’t change the fact that this amount of tightening doesn’t show a real commitment to fighting inflation. When they can print $3 trillion in a month, they can sell $1 trillion in a month. They just don’t want to upset the “markets.”

Sell $1 trillion to who though? Some hedge fund would have to have $1T just sitting there. If the fed wanted to sell those to someone they would take a HUGE loss because interest rates are higher now. The rolloff and going up to 90B/month is the right policy, just should have started way sooner. As soon as housing prices took off.

Greg said: ” The rolloff and going up to 90B/month is the right policy,”

—————————————–

for who? and what do you base this on?

To whom and at what price. At prices yielding 5-6% on 10-year treasuries they could probably unload $1 Trillion in a week.

Good response, this is the main issue. It doesn’t make sense to argue the Fed should (or even could) make such huge and sudden sell-offs of its assets–who would be the buyer? Sure, QT could be a little faster and more volume than current schedule, but there are obvious practical problems with such a huge and rapid sell-off. It’s likely not even doable. And as you say, it’s another reason this should have started a whole lot sooner. Better late than never i guess.

and just think ,if we were to be sale oil at 110 dollars a barrel ,we would not be in this mess at all, oh and stimulus no helping others yep my stock up 15 percent easy, now this will cost usa muchhhhh more than now

Plenty of buyers of treasuries at the right yield.

Raise the yield and buyer R available.

These are existing Treasuries with the yield already set. To do what you are suggesting, the Fed would have to sell at a discount and book a sizeable loss. Long-term, the Fed can take more money out of the economy by holding them until they mature.

Well said. I feel wolf and most commenters are too idealistic or negative to see the reality. People at the top are too knowledgeable to ignore all the issues mentioned here. Even they can’t control the economy 100%, they can distort it for a long long time.

You have (utterly and completely) failed to understand the reality that is inflation. Specifically, that the Fed CAN”T PRINT ANY MORE FUCKING MONEY.

The Fed absolutely HAS distorted the economy since 2007. What we are seeing now is the Fed trying to reverse course, because they have RUN OUT of your ‘long, long time.’

Absolutely, this is the right answer. Of all the stupid Fed distortions since 2007 (if anything more like going back to Greenspan and before, for almost 40 years), this level of QE even when inflation was threatening has been and will be the most damaging to the US economy and society. Asset bubbles have been an issue since Rome, but they’re not too harmful if they’re confined to dumb things like tulip manias or the latest dozen crypto coins to be mined–only the speculators take a bath and get left as bagholders. The US housing bubble OTOH, and similar bubbles in Canada, Australia, HK, UK and NZ, is much worse since it’s caused unsustainable rises in a basic necessity like shelter, also leading rents to shoot way up. Same with medical and education costs in America. It’s criminally negligent to allow bubbles in such absolute necessities, they’re caused so much pain that even good earning and professional younger Americans are struggling to get financially sound and start families. This has been by far the Fed’s worst blunder.

“ What we are seeing now is the Fed trying to reverse course, ”

Disagree.

They are attempting to SLOW course.

No talk of price rollbacks after an 8% spike….just MORE at lesser rates

Four times their target in one year and they dont change or recalibrate?

They have distorted it for decades, at least.

New Era Begins

ERA, a long and distinct period of history with a particular feature or characteristic.

Wolf, your title has more than a little hyperbole! Let’s see if your “era’ lasts 6 months!

According to you tightening deniers, the Fed would never taper its asset purchases, never end QE, never raise rates, and certainly never do QT. You people have totally lost touch with reality every step along the way. You people are steeped in propaganda.

Wolf said: “According to you tightening deniers, the Fed would never taper its asset purchases, never end QE, never raise rates, and certainly never do QT.”

————————————

did the FED not do all this in 2018 before it reversed course?

there is a difference between tightening deniers and long term tightening skeptics. The FED has a history of of misdirection, lying and Idiocy. The FED acts in the interests of their masters. Our job is to figure out what is in the interests of their masters. That is what will be done. As it is, your clarity of mind and foresight of competing issues (inflation arrest versus the alternative) is persuasive, even in the face of many of our skeptical prejudices.

We are lucky to have you.

The best pandemic ever, followed by the craziest mania, followed by raging inflation, followed by the worst H1. Huge gyrations and instability. Noone knows even what’s happening at the moment, much less in the future. Smell of the 1920s.

“You people have totally lost touch with reality every step along the way. You people are steeped in propaganda.”

***snorting chortle***

“This country was founded on the principle that one Corporation couldn’t hog all the slaves, leaving the rest of us [corporations] to wallow in poverty.”

-Eric Cartman

Still more of this QT denier cluelessness. Here’s a news-flash, the Fed has RUN OUT OF that time because inflation is here in the US, it’s raging and it’s dangerous. A far, FAR greater danger than a collapse of the stock market or home prices (both asset bubbles that need to go way down to be in-line with US incomes) or even a severe, deep recession (almost certain in early 2023, or starting in Q4 2022). A deep recession is rough but temporary, it cleanses asset bubbles and makes things affordable, leading to strong recovery. To contrast, runaway inflation utterly wrecks nations and their economies, and for a major power like the US, this means the end of US geopolitical importance, collapse of the US dollar, loss of confidence in US political and financial institutions. And from there, social unrest and literal blood in the streets of the United States. Uncontrolled inflation is the worst-case scenario, and like Wolf has said, the Fed’s hand has been forced.

Don’t you find it sad that the Fed only acts appropriately when it’s forced to? This leads one to hope for a collapse so big that it ends or severely curtails the role of the Fed going forward. Churchill was right: Americans will do the right thing only after they have tried every alternative.

@ yxd0018 who said; ” I feel wolf and most commenters are too idealistic or negative to see the reality”

—————————————————

bless us with your insight and tell us what the reality is ……..

(do you work for the FED?)

“ People at the top are too knowledgeable …”

interesting point of view

unique and curious

Wolf needs to do another article on the “Crybabies” on wall street who can’t survive with NIRP & Zirp

Noted LOL

The big lesson of history most of us know is when you start printing money it’s nearly impossible to stop. My guess is once a few months of full runoff is in place the consequences will be too much for central bankers to bear.

Took a look at Yardeni’s big 4 central bank balance sheet report and it looks like total QT rolloff is at a faster rate than the last episode.

Agreed. The choices are very severe recession or inflation. The Fed has to pick one, and right now, all they’ve done is slightly tapered and raised rates by a miniscule amount in the hope that they can avoid both. They won’t be able to.

“The choices are very severe recession or inflation. ”

And again, of those two, runaway inflation is tremendously more dangerous to a country, and causes long term damage that can’t be recovered from. A deep recession is rough to go through, but ultimately temporary, cleanses out asset bubbles and resets the economy in a better place, followed by a strong recovery and better allocating of assets. It’s healthy and necessary for an economy. Whereas, uncontrolled inflation utterly wrecks nations. Throughout history, inflation has been one of the major factors bringing down great empires–the Romans, British Empire, Ottoman Turkish Empire all suffered ruining internal decline and ultimately collapse with inflation a big factor in their demise. And it would be even worse for the USA with the catastrophic resulting of a loss of confidence in American financial institutions, danger for the USD and general loss of trust in US management. And as divided as the US is (with more than 400 million firearms in circulation), the resulting societal breakdown and social unrest would be incredibly bloody. The Fed truthfully doesn’t have a choice–QT is happening and accelerating, no matter how much the QT deniers try to fantasize otherwise.

@ Miller who said: “And it would be even worse for the USA with the catastrophic resulting of a loss of confidence in American financial institutions, danger for the USD and general loss of trust in US”

—————————————

I am afraid much of this has already taken place, perhaps not yet what should be a catastrphic loss of confidence, but certainly a disgusting lack of confidence.

as an aside, another reason to favor recession over runaway inflation is because wealthy benefactors get to pick up discounted assets. just part of the asset boom bust cycle the FED foments

Miller, I agree. But they need to pick up the pace or it’ll be too late.

Inflation is an effect of decay and collapse, not a cause. Nobody is even admitting those are happening, much less trying to find a cure. Our institutions are utterly out of touch and run by geriatrics with zero chance of reform. They will have to be rebuilt now rather than reformed.

The choices for FED and Govt is simple per me: Either inflate away the govt debts/entitlements or keep printing money.

IN the long run, I see Govt not defaulting on their promises and would rather print money and let inflation run loose.

Let’s see what are the outcomes of this coming mid term. If people are really sick/tired of this rampant inflation then it should show in mid term results.

The economy and the country would be better off if Fed Funds had be 2% and 30yr mortgages 5.5% for the past 12 years.

IMO.

The Federal Reserve must be held to formula guard rails….

*Inflation guided rates

*GDP guided money supply increases

“My guess is once a few months of full runoff is in place the consequences will be too much for central bankers to bear.”

And then what, they allow inflation to just rip through the economy and destroy the dollar and anger the entire populace? I don’t think so. I hear everybody grumbling about inflation these days.

We’ll see. Following this blog is more interesting than any novel. Such rich backstories and unknown twists and turns to come.

There might be a difference, the Roman empire lasted for centuries with the eastern part holding on for a long time. The USA have used less than century to become an empire, it may unravel equally quick.

The Soviet Union did disintigrate in a few years to the surprise of many people.

If they wanted to QT they would not have had increases in April and the selling would have started in April, and the reverse repos would not be in play.

I am of a similar sense, but more vocal about the fact we have, at the controls, the most incompetent Federal Reserve in it’s history. In the previous episode, they caved like a cheap lawn chair under Trump’s tongue lashing.

Powell is an empty suit for the jaba the hutt size banks that own them and are regulated by them.

Will they choke when London Bridges come falling down. Probably.

The markets have been buoyant, almost giddy, this week as the swashbucklers, devine that the Fed endgame is in sight.

They will stop raising interest rates below what we guessed at, last week.

Because, JP is signaling that the kegs are not ending, although the wait in line is likely to be longer.

The withdrawal from an addictive human tendency: ie;

The attraction of cash at zero, or below interest rates to a world that, apparently, is dominated by testosterone, which is expended complying with the plans of a dominant female.

As Hemingway reportedly imagined in the book ” And the Sun Also Rises ” which I havently verified and am relying on original reporting by random people responding to someone else’s author citation.

a character was asked, ” how does one so rich go bankrupt ?”

The reply, ” gradually and then suddenly.”

Dang it! I don’t have anything to contribute but I wanted to be the 1st person to reply!!!

You’re not first, and you didn’t reply. Good job.

At least he’s not a sheep.

Let’s round up and say QT is drawing down about $40 billion per month.

So, how long to return to the $1 trillion the Fed held before Housing Bust 1.0?

$7.8 *trillion* divided by 40 *billion*…about 192 months if my top ‘o head math is right.

16 *years* at this rate. Which ain’t never going to happen.

(Everybody ck my math…I’m not even using the back of an envelope…)

My point?

The QT rate is pretty damn slow and the amounts pretty damn small (relative to the mass of unbacked money printed).

The fact that mortgage rates have more than doubled in the wake of this, this …kernel of a reversal highlights just how addicted/dependent the mkts have become upon Fed money printing – reverse the unbacked boodle of printed money by .5% and borrowing rates more than double.

This isn’t the result of a central bank acting as a wise steward, it is the result of a CB becoming a crack dealer for politicians.

While I agree with your general point that the Fed is going too slow, your math is off. Firstly, the Fed has publicly stated their goal of $95bil/month in QT, which they’ll reach within just 3 months. This is the first month and they’re already at $75bil.

You have to look at the overall balance sheet, not just treasuries, because, to some extent, these are fungible assets: people often sell one and buy the other and both securities are classified similarly for most regulatory purposes.

Secondly, the balance will never go to zero: there is some level of balance sheet that the Fed needs to carry to manage the money needs of the economy. Generally speaking, as the GDP grows, so should the Fed’s balance sheet to provide enough money to keep the economy flowing freely.

No one knows what that level is in this new era of monetary policy, but $2Tril has been bandied about. Let’s assume that’s right. Then that means $8.9tril – $2tril = $6.9tril / $95bil per month = 72 months or 6 years. Still too slow, but a lot different than the 16 years your math comes up with.

And the Fed had to stop its first and only round of QT after about a year once it went full tilt because the repo market freaked out, the yield curve inverted and then they had to start lowering rates in late 2019.

The Fed won’t make it anywhere near $6T before it has to startup QE again, and I’m not a tightening denier. But, with a cooling housing market, I do think the Fed may have problems meeting the full $35B MBS runoff by fall. The Treasury’s won’t be an issue because of all the short-dated bills it has on its books.

By early 2023, they’ll have to start selling MBS which won’t be a bad thing. By then 30YFRM will probably be about 4.5% and it will need to rise back to 5% and stay there. Otherwise, the housing market will re-ignite.

I agree with Mish. This may well be a 1990 recession redo where we see unemployment tick up by “maybe” 1.2’ish %.

Jay,

“And the Fed had to stop its first and only round of QT after about a year once it went full tilt because the repo market freaked out…”

This is precisely why the Fed re-instituted the “Standing Repo Facilities” – repos and reverse repos – to keep the repo market from freaking out. It did this last summer before it discussed QT, and for that reason.

Now the repo market won’t freak out again because everyone knows that the Fed now has an upper and a lower limit on it with repos and reverse repos, as explained here:

https://wolfstreet.com/2021/07/28/my-thoughts-on-the-feds-back-to-the-future-standing-repo-facilities-announced-today/

Wolf, so if they did not plan for the repo freak out the first time, chances are they will miss something else this time around. They are incompetent.

Yes, something else may blow up eventually. The stock market being one of the candidates.

What they should have done is let the repo market participants blow up. There were a bunch of mortgage REITs that borrowed short-term in the repo market to fund long-term holdings of MBS. That’s a ridiculously risky bet, and those mortgage REITs along with some hedge funds doing similar things were being locked out from the repo market because they were blowing up, and other market participants were figuring out, and that should have allowed to happen. Instead the Fed stepped in and bailed them out. That was a really stupid thing to do.

Borrowing short-term in the repo market at the lowest rates available in the US, and investing long-term is super risky, and it’s done all the time because they know now that the Fed is going to bail them out.

Yes, the Fed was totally incompetent. It should have just said, OK, that’s market risk and credit risk, and you people got paid to take it, and now it’s your turn to live with it.

https://wolfstreet.com/2019/11/06/whats-behind-the-feds-bailout-of-the-repo-market/

The difference being that in 2019, the Fed didn’t have nation-wrecking runaway inflation to deal with. Now in 2022, it does–so it doesn’t make sense to try to apply 2019 assumptions to 2022. It’s totally different situation now. The Fed is between a rock and a hard place, but the difference is, as painful as may be consequences of the concerns from 2019, the consequences of uncontrolled inflation to the US would be far, FAR worse. Again, a recession and downturn may be painful but they’re temporary, and burst asset bubbles are a necessary cleansing for an economy. (Esp the housing bubble–home prices NEED to come way down be in line with US incomes, in some markets 60 to 90 percent). Whereas, uncontrolled inflation wrecks nations and brings down empires–even worse for us in the US because of our high debt and trade deficits. And like Wolf said, the Fed has taken steps to take care of the repo market.

@ Wolf who said: “to keep the repo market from freaking out.”

———————————————

the FED shouldn’t concern itself with money market funds and repos to bail them out. They are a sick joke anyway.

Miller

Agree.

Corrections are called “corrections” because they correct.

They flush the poorly financed, the over leveraged.

The Fed had rates at 4000 yr lows for how many years?

Notice also that regarding inflation, the Fed never mentions price roll backs….only lesser increases in the rate of inflation….

accumulated on top of the 8% spike, and compounded.

The Fed is indeed between a “rock and a hard place”….and the Fed brought the “rock”.

Thanks for the additional info, I guess my timeline was off by a month or 45 days.

1) But…I don’t know how much faith should be put in Fed’s “stated intent” for anything, for any significant length of time – let alone 60 months of adversity and political pressure.

A) In the fall of 2018 the Fed folded like a cheap suit in 3 months after the hugely overvalued stock mkt fell a mere 20% (after Treasuries hit a lofty 3%)

B) “Jawboning” (read manipulation of perceptions divorced from actual activity) is probably the Fed’s favored mode of “action”.

Head faking the mkts into thinking more QT will occur than really will, theoretically addresses the inflation issue while leaving the Fed-Treasury Debt incest essentially…unmolested (pretty crucial for a gvt whose debt is in excess of the nation’s GDP and is largely bought up by its own central bank)

2) As I mentioned above, the very, very quick doubling of mortgage rates/collapse of equities indicates just how much everyone knows that the mkt is utterly dependent upon Fed ZIRP. A flutter away from ZIRP and rates have more than doubled and equities are off 25%.

Those things occurred *before* the QT (apparently)…does the Fed/DC have the stomach for months 3/6/12/36/60?

I guess it’s understandable to wonder about these things because of the Fed’s past incompetence on this, but the difference is now, how inflation is forcing the Fed’s hand to move away from ZIRP and QE and towards heavy interest rate increases, QT and other measures to tighten the money supply. In the big hierarchy of threats to an economy and nation, runaway inflation is at the top–it absolutely wrecks nations and has been one of the major factors in bringing down many of history’s top powers and empires. And it leads to massive social unrest, collapse of whole nations and blood in the streets. It’s what the Fed fears most, as it should. Contrary to a lot of the misinformation that the US media has fed us, a recession isn’t something to be feared when it acts as a corrective (esp as a correction for a dangerous housing bubble and other asset bubbles like this). It’s rough, but temporary, and institutions can take steps to cushion it. OTOH runaway inflation is a mortal threat to a country and almost impossible to cushion against (Nixon’s price controls were a failure). The Fed is moving more towards going full Volcker here, it has to, and it means a deep recession in early 2023 (or starting in late Q4 2022), but it’ll be temporary and cleansing, followed by a strong recovery.

Miller,

Don’t really disagree with you, but more or less 20 yrs of ZIRP doesn’t suggest to me that the Fed was all that worried about ever causing inflation.

Heard many, many,…many more times about the (gasp) horrors of *deflation*.

Sure, DC is scared sh*tless *now*, but not during the two decades they courted the cancer (and appropriated unto themselves the savings resulting from Chinese production led *deflation*…offset by the DC money print, in all its myriad forms…for over 1000 weeks).

Cas-

RE: your point #2, the very quick doubling of mortgage rates, IMHO, indicates that banks and other people with inside knowledge know that this time, it’s different. The Fed means business. Recall that mortgage rates started skyrocketing before QT or even the FFR increases started. They knew that due to inflation, this wasn’t just a temporary 6 month blip and then back to business as usual. And they didn’t want to get stuck with 3% 15-30yr mortgages when the 10yr yield is going to be higher than that for years.

IMHO, if they thought all this was temporary and we’d go back to QE by the end of this year, they wouldn’t have raised mortgage rates so high and so quickly. Why do that and scare off business if you think this is just temporary?

Ya but there will surely be another crisis in that 6 year span. Our collective definition of crisis is the problem. As a child we had no air conditioning and slept well anyway. Now if the AC is off by a degree, we have a crisis. We are spoiled, entitled and easily manipulated into pointless consumerism. Sadly the Fed enables our addictions because politicians need votes and Corporations are people for campaign finance purposes. The best medicine is to take it all off life support. But spoiled Countries with big egos need to maintain the lifestyle. And so borrow we must and will always do. Now how to preserve wealth in that environment?

Cas127,

Nonsense. Not “a month.” This was the FIRST MONTH — the phase-in of QT. In a little while, QT will run at around $95 billion a month. So now redo your numbers.

“This is precisely why the Fed re-instituted the “Standing Repo Facilities”

Wolf, I know you understand all of this better than we do. Trust me. I get that and respect your very strong knowledge on the subject matter.

But, if the economy slips into a real recession (i.e., broad declines in unemployment (5% or higher), housing prices, manufacturing, consumer spending and most importantly wages) probably in the next 12 months or so, then the Fed will be forced to reverse course to some extent. This may be cutting the runoffs in half or even suspending it like they did back in 2019. But, the biggest question going forward is will the Fed continue to manipulate the yield curve, specifically on the long end, where housing is set. I’m like most people and fear the Fed has learned nothing from the last 12 years. When I look at the 10YT chart, it seems to me that anything under about 5% leads to a slowly building asset bubble. And periods below 3% accelerate this by a factor of 2 to 3x.

Again, I agree with your general interpretation on a very dense subject, but in late summer through the fall of 2019, the Fed lowered the FFR by about 1%. My point really is that, given the current macro environment, I’m simply skeptical that repos & rev repos will keep the FFR in its target range.

Like I said in a different post last night. Rev repos, especially, seem to be a gimmick in terms of pulling cash from the economy. I can’t say I support the idea that the Fed ended bank reserves due to COVID, but I understand why. Yet, I certainly don’t understand why they’ve chosen not to bring them back and appear to have chosen what to me is the gimmicky path.

In my view, the Fed should have set out a course that included some level of selling assets, both treasuries and MBS. I think that would have given JPowell much more credibility and, I assume, would have allowed them to not use rev repos to try to siphon off the trillions in extra cash banks and brokerages like Fidelity have that are the direct result of QE. That money needs to go away as quickly as possible without causing another Great Recession.

But, correct me if I’m wrong, the main reason they aren’t selling assets off is because of the upward pressure it would put on yields? If this is generally correct, then there’s only two reasonable explanations:

#1 They think it would push us quicker into a recession and may cause it to be more severe. Okay. I get that and recognize that nobody really wants a severe recession. But NOBODY knows what the exactly right policies are to keep that from happening while taming inflation. JPowell is on record saying something to that affect.

#2 The national debt has grown so large that it’s this gigantic noose around the Fed & Treasury’s necks. Now, I know as an economist you’re a big proponent of % of GDP. And you may well be right in its significance to my point, but I do feel that we’re at the moment in time when all the bad things lurking in the shadows are getting ready to come home to roost. If at the very least, the national debt is now one of the main drivers of determining what the Fed can and cannot do to help manage the economy. JPowell can’t put his big boy Volcker pants on and raise the FFR to 10%. It would be catastrophic to the interest paid on the debt.

As I’m posting this, employment rose in June by a whopping 372K jobs! Again, the Fed is massively behind the curve.

Thanks for your reply to the post I’m replying to.

You, and apparently a lot of other people, seem to think that because the Fed has capitulated several times in the past they will do the same this time. That in the face of a recession or severe market losses they will go right back to QE.

I don’t think so. They have touched the hot stove and they know it. They thought they could do this without triggering inflation because they did manage to do so for a long time. But now that serious inflation is here, they are not stupid. Any faltering or wavering is simply a no go, regardless of any recession or asset price tragedies.

Because inflation is truly the worst thing that can happen, way worse than even the most severe recession.

All IMHO, we’ll just have to wait and see.

“But, if the economy slips into a real recession.. then the Fed will be forced to reverse course to some extent. ”

NO IT WON’T. Again the difference in 2022 compared to every such case in past 40 years is that the US is now dealing with runaway inflation, a mortal threat to a country’s economy, stability and even survival as a nation. It’s unbelievable how much economic illiteracy and misinformation the US media has spread about recessions, as if they’re some kind of horrific monstrosity–some recessions are a necessary part of the business cycle, esp if they pop asset bubbles and reset prices to affordable levels (and housing bubble esp needs to pop and home prices go way down). Whereas, runaway inflation wrecks nations and great empires–it would mean the destruction and fall of the US as a major power, and social unrest. Try to imagine tens of millions of American families unable to afford food, rent, gas, cars or basic household items–literal blood in the streets, esp with more than 400 million firearms out there. A cleansing recession in 1982 and 1983 was rough, but ultimately allowed Volcker to save the US economy (and Reagan of course benefited politically from the recovery). It’s basically the same situation here in 2022, and same solution for it–a deep but temporary recession in early 2023 to halt inflation, then recovery.

The Fed has a third option which is pause. The do not have to “reverse” anything. And they can pause for a long time. And pausing is akin to letting the free market run its course for a time. They paused for a year while inflation went higher and higher, they will also pause to see what happens when eventually inflation slows down.

The main thing that the fed is trying to avoid is persistently higher inflation, because they know the productivity cannot keep up with 3%+ inflation in the long run. 2% is the target, unless they change the target, which they seem loath to do, it’s going to be rate increases and QT for quite a while.

Demographics suggest that employment could remain tight for a very long time, the population is aging out of the workforce without replacement. It’s an inflationary environment, and as such the Fed will use its tools to find price stability. Should the fed resist, you will have a gigantic contingent of elderly people that are unable to afford basic living expenses anymore. These are the people who come out and vote. Inflation is not an option.

“Because inflation is truly the worst thing that can happen, way worse than even the most severe recession.”

Thank you, just amazing how this basic wisdom seems to get overlooked in so many places. US schools have done an absolutely terrible job of teaching basic economics and history, and how fundamentally dangerous inflation is to a nation–and even more to a country like the United States, with our high levels of both public and household debt, and especially our high trade deficits. (Even when previous great powers and empires were wrecked and collapsed from inflation, at least in most cases, they had a trade surplus that cushioned some of the pain–the US does not.) It’s far worse than a recession. Also to blame here is US media for constantly stirring up fears about recessions as such a horror–when in fact, they’re often a necessary part of the business cycle, esp when they pop asset bubbles like the disaster housing bubble the US is currently stuck with.

Jay said: “I assume, would have allowed them to not use rev repos to try to siphon off the trillions in extra cash banks and brokerages like Fidelity have that are the direct result of QE.”

___________________________________

rev repos bail out money market accounts and pay more interest on money market funds than the market would otherwise allow. just more bastardization of markets by the manipulative FED.

Miller said: “a deep but temporary recession”

——————————————-

temporary? how temporary? how do you adjust from “runaway inflation”, as you said, to a deep recession and keep it short?

“The Fed has had reverse repos before Bernanke came along.”

According to Google, RRP’s were created in 2013. That was Bernanke, right? I thought he was the architect. Maybe Google is wrong. I know I certainly could be wrong.

“So RRPs remove that excess liquidity, and by removing liquidity they act as form of QT.”

This truly is a fundamental question. How does moving money back and forth to the Fed every day making $80B a year for money market funds actually remove excess liquidity? It doesn’t do so on a permanent basis. And I get RRPs apparently are targeted at the FFR, so they’re not created to permanently remove excess liquidity. But, I guess the follow-up question to that is what policies did Volcker use from 1979 through 87 to keep the FFR under control? What was used before 2013, assuming Google’s not wrong?

In addition, how is demand for $80B a year in free money going to go away, unless the Fed reinstitutes reserve requirements and, or starts selling assets? Then, investors would have the option to buy up big chunks of the Fed’s balance sheet with part of this $2.3T in excess liquidity that was created out of thin air by the Fed.

As always, thanks for your replies.

Jay,

“According to Google, RRP’s were created in 2013….”

When are you going to go to the source finally and quit posting this Google BS?

Go to the Dec 2003 balance sheet from the Fed where reverse repos are disclosed already. They just weren’t abbreviated with “RRP,” but were called, as today, “reverse repurchase agreements.” (Reverse Re-Purchase = RRP). They were already on the 2001 balance sheets too, though with $0.

So here is Dec 2003: Use your browser’s search function and search for – reverse – and you’ll see them in several locations:

https://www.federalreserve.gov/releases/h41/20031204/

“What they should have done is let the repo market participants blow up . . . Borrowing short-term in the repo market at the lowest rates available in the US, and investing long-term is super risky, and it’s done all the time because they know now that the Fed is going to bail them out.”

All extremely great points and for most of us, myself included, your knowledge helps us understand things better. BUT what you describe above is the very definition of a gimmick. Why does the Treasury & Congress let the Fed implement something so substantial that can be taken advantage of so easily and create such big risks to the system?

It just doesn’t make sense, and it’s borderline criminal across the board. The Fed shouldn’t create a market facility that encourages them to print tons of fake money that money market funds use to create $80B a year in fake wealth.

In 10-15 years, financial historians are going to look back and explain how screwed up the Fed policies have become. No money should be created that doesn’t result in real Treasury debt.

Okay, unless they renamed something, then RRP’s started on 9/23/20213:

“The overnight RRP operational exercise started on September 23, 2013.”

Citation:

https://www.federalreserve.gov/econresdata/notes/feds-notes/2015/federal-reserves-overnight-and-term-rrp-agreement-operations-in-financial-accounts-of-the-united-states-20150324.html

Jay,

Reverse repos go back to at least 2001 — though at that time, they had $0 balance. And the Fed disclosed them on its balance sheet, even back then. There is nothing new here, other than the magnitude.

Here is the balance sheet for Dec 4, 2003 that has reverse repos on it with a balance. Use your browser’s search function and search for – reverse – and it will come up in several locations.

https://www.federalreserve.gov/releases/h41/20031204/

Repos aren’t limited to the Fed. I remember reading up on GAAP accounting rules for dollar repos back in the 1980s, while working at an insurer. They are nothing more than collateralized loans (the Accounting rules were to treat as a financing transaction rather than buys and sells).

I think Wolf’s reference to 2001 is the use of repos by the Fed, not the first use of repos overall.

I think these numbers need to be normalized to GDP to be most meaningful.

Generational Democracy will take hold, soon enough.

We have preceding generations “infringing” on the economic liberty of succeeding generations. It’s over for Silent generation and Boomers.

Gaslight all you want, millennials and Gen Z aint buying it anymore.

“ Gaslight all you want, millennials and Gen Z aint buying it anymore.”

You’re right…

They’ve already bought it at nosebleed prices….

“millennials and Gen Z aint buying it anymore.”

Great then, if that’s the slogan, they can try to confiscate it from the wildlife fund I will it to. Or Chinese I sell it to. That’s winning!

How many revolutions led to many years at least, of nothing but blood and misery? Most of them. Good luck!

The USA won the last big round of gains (rather, our forebears did) by war. That’s what propped up the great middle class, that some gen Z and millennials seem to now want to be handed to them. Are you ready for that? Because that could well be the price tag for those tickets.

Fighting over scraps will not build a functioning society. Creating value will. Work, service, boring stuff!

Everyone forgets Generation X

😄

We haven’t been buying it either.

Not since the 1980s. The Elders outnumbered us for 40 years.

The change that is happening now, which Wolf shows us here, is a generational transfer of wealth.

But it’s more than that. It’s a shift in national priorities. We need to build the 21st century.

There is a “recession” coming, but it will hit RICH PEOPLE instead of hitting the rest of us. For a change!

They will be fine. They can lose fortunes larger than the riches of the Pharoahs of Ancient Egypt and still be fantastically wealthy.

Forgive me if I laugh when they cry.

Wolf,

Can you provide any context/background to the balance sheet expansion that kicked off at the beginning of 2013 (“no crisis” in your last chart)?

Go back to my articles back then.

Hi Wolf,

The markets jumped partially because of a $200 billion spending program announced in China.

Can you explain how that could affect us here, since they likely have something similar to the Fed there ?

No, that’s not why the market jumped. The market jumps and the market dumps on a day to day basis, because that’s what markets do, and whatever reasons anyone assigns to these short-term moves is just fiction.

If it sells off tomorrow or Monday, it’s not because China rescinded whatever program had promoted earlier.

Thanks for the great info as always Wolf. If one is to believe a one liner tweet from Burry about MBS, it’s easy to be mislead into thinking QE is just around the corner. Now since likely know what he is doing, I would chalk this up to hedge fund manipulating the market. Kind of disappointing coming from him to say the least but just like any other money managers out there…

No offense, but why on earth would you think Burry or anyone else would have your best interest at heart…

Burry would have been broke if the MBS holders hadn’t gotten scared and were trying to be the first out the door…

It was then that the CDS he had bought against those MBS saved his ass… and his fund…

Wolf-

I’m assuming these balance sheet figures don’t include the overnight reverse repos and the bank excessive reserves?

I think it’s important to include those in the overall balance sheet, because they are definitely a part of QE/QT. If the Fed reduces their balance sheet by $75bil, but also reduces its overnight reverse repo balance by $75bil, then the overall amount of money in circulation hasn’t changed.

I get why the Fed has these other facilities, as they allow them some ability to manage their QE/QT efforts (the reverse repo market allows daily fine tuning and rapid reaction to events happening faster than the biweekly market operations they conduct, and the excessive reserves is specifically targeting bank lending and credit formation). But, IMHO, real QT isn’t happening unless the balances fall faster than the balances in these other 2 programs.

Lune,

Reverse repos and reserves are liabilities on the balance sheet. This article discusses the assets. Reverse repos are the OPPOSITE of QE. They’re a form of QT and drain money from the market.

I occasionally discuss the liabilities, and I might do soon again.

Reverse repos are a gimmick created by Bernanke to let the Fed do QE. It doesn’t truly remove money from the system. It’s like a water turning into liquid, then gas over and over. And it’s free money to the banks to the tune of $80B a year or about 29% of their gross profits last year. Tell Fidelity to start putting some of that RRP money they make off my money every day back into my account. It’s criminal.

Great write up btw. I hope it all goes as planned.

Jay,

The Fed has had reverse repos before Bernanke came along. But QE creates excess liquidity, which can push short-term yields into the negative, and which tears up money market funds because they will break the buck, and that can cascade nicely into a financial panic. So RRPs remove that excess liquidity, and by removing liquidity they act as form of QT. But unlike QT, RRPs are demand-based, and if demand dies down for them, they go away. And they will go away as QT begins to remove excess liquidity.

The primary counterparty of RRPs are Treasury money market funds, NOT banks. Banks can put their excess cash into the Fed’s reserves account.

@ Wolf-

money market funds should be tore up. they are all part of the FED/Wall Street scam. They pay their depositors insufficiently for the risk, and they provide free money to the packagers thanks to the FED providing a backstop.

And they wouldn’t be so large, and allowing an escape valve for the FED’s money creation and FED created wealth disparity.

Right, but they still have an effect on the total amount of money out there. If assets decline at the same rate that liabilities decline, then the overall balance sheet remains the same. That’s why I think the overall balance sheet, looking at both the assets and the liabilities gives a more accurate picture of how much QE/QT is happening.

FWIW, this means that, with $1Tril in reverse repos, the Fed has actually already implemented $1Tril of QT by stealth. That $1Tril in liabilities counteracts $1Tril in assets that the Fed holds, reducing the overall balance sheet while not affecting the headline asset numbers.

Those things are LIABILITIES (NOT ASSETS) on the Federal Reserve balance sheet which are offset by ASSETS in order for the sheet to balance.

Good info. Could you do an article on currencies? Will the euro catch a bid now that the ECB is about to finally raise rates? And how does Japan manage to keep inflation down when their stocks and currency are in the tank? I’m guessing they didnt go on a printing binge like the west did for covid.

“This inflation is in part a result of QE.”

Why “in part” instead of”primarily”?

The other part being the Trump & Biden administrations going overboard with fiscal stimulus.

If I had to estimate, probably 60% of the current inflation crisis was caused by reckless fiscal spending (stimulus checks, unemployment benefits exceeding wages, PPP, etc.), 30% by reckless monetary policy (ZIRP & QE long past the end of the emergency), and the remaining 10% from the supply chain stuff, China lockdowns, Russia-Ukraine, and other outside factors that Democrats (as the governing party) & central bankers cite to deflect blame to others.

China and Japan, the worlds 2nd & 3rd largest economies, have stable inflation rates around 2% right now.

We always used the World Bank’s GDP calculations which use PPP, and China is by far the largest economy in the world on that measure. In many ways it makes more sense than nominal or other figures because it measures what people can actually buy. Just because something costs more in the US doesn’t mean it’s higher quality, and the only reason we care about prices and exchange of money is to buy real goods and services. So by that measure China is no doubt larger than the US now, and as you say, the relatively stable inflation rate there is very important, in part due to that fact. As for Japan, if anything they’ve wanted more inflation for a long time, so ironically, they’re probably getting the counter-balance they’ve long wanted in their own particular case.

There is also interest rate repression and government stimulus programs and some other factors, including mass psychology. The actual causes of inflation are amazingly not all the well understood — but it’s never just one thing.

QE was the primary cause of the interest rate repression. $11T in two years is the “one thing” that stoked inflation. And JPowell watched gleefully as my house appreciated 100% in four years. A 5th grader could have looked at a home price appreciation chart from June 2020 over the next 12 months and realized something was out of whack big time and needed to be done. It’s utterly insane, borderline criminal that the Fed let all of this go on as long as it did, especially the rent & mortgage moratoriums which was the next biggest driver of inflation.

Again, great post!

And, I didn’t mean to say the rent & mortgage forbearance was the fault of the Fed. That was the CFPB.

My bad!

Goldman sucks and black rock running this ship ,FEd is a puppet

” borderline criminal that the Fed let all of this go on as long as it did”

Nothing borderline about it. Straight out criminal counterfeiting.

CFPB ?

damned acronyms

There are a few variations on a theory of inflation that is well-supported by the facts and by historical experience, but it’s well outside of conventional economic thinking and rather accusatory towards large-scale finance and capitalism as practiced for purposes of exploitation. All rather Keynesian, with its deficiencies corrected, and accounting for boom-bust cycles as well. While there are numerous potential drivers of inflation, like shortages, excessive credit, and mismanagement of money supply, there are always certain other common features.

John Adams’ disagreed vehemently with Alexander Hamilton over an early form:

“All the perplexities, confusion and distress in America rise, not from defects in the Constitution or Confederation, not from want of honor or virtue, so much as from downright ignorance of the nature of coin, credit, and circulation.”

– John Adams

Accounting for extended periods of low inflation, with boom-bust cycles tamed, make for an interesting discussion of the theory. Not that it matters.

Thanks for the John Adams quote. that’s one I hadn’t heard of. Interesting how deeply the Founders thought about inflation and associated issues, they were well aware of the danger even then and took steps to keep it from strangling the young US. Any leaders of a nation that want to even pretend to be competent, need to be just as aware of the fundamental danger than inflation poses to a society.

It’s always one thing: the purchasing power of the unit of account being degraded. Inflation is always and everywhere a monetary phenomena. Indeed you can use M2 to more or less hindcast today’s inflation or so I’ve heard.

Cyto,

Thanks.

It is very easy to get lost in the weeds of various Fed operations to manipulate the money supply (in the service of ?) but the key underlying fact is that the Fed *is* manipulating the money supply (by definition shorn from any direct linkage to real asset/productivity growth).

A ton of time and energy will be lost among the trees, while spending way too little on evaluating the nature/health of the forest.

Friedman thought inflation was purely based on monetary policy. Keynes said monetary policy shouldn’t affect government spending.

When you get into the esoterica of the dismal science, it’s easy to see it’s mostly political unless the government actually slows down debt creation for new initiatives and current entitlements are properly funded.

The biggest surprise to me has been the utter failure of Gold’s price to respond to inflation and how incredibly strong DXY is now.

The Euro has had the bottom fall out and basket cases like the Turkish Lira and Argentine Peso are getting slaughtered.

I feel like the Bond market has done a lot of work for the Fed, but I also don’t think it’s going to get much more help, which means the next 1-2% of rate increases will hurt what is a strong economy. They were late, and they will be late with their pivot.

I guess the flip side is that at least it’s not Turkey or the EU.

DXY is strong because the “markets” believe that the Fed will continue. Whether or not that is true remains to be seen.

Not in any way defending the ECB’s incompetence or tardiness here, but as for the last sentence, the EU has had lower inflation than the US (in spite of, not because, of the ECB’s stupidity)–and that’s using a CPI basket that tends to overestimate inflation vs the US (there’s a lot less in hedonic adjustments. substitution or other numbers-fudging there, and they tend to put proper weight on essentials people actually need, like housing). Goes in hand with what we’ve been hearing from our European assignees, inflation has been getting bad there but it’s consistently much worse when they fly back to visit family in the USA. The European Union, at least in its core countries, does have some structural advantages in keeping inflation down, ex. a much higher savings rate and cultural aversion to debt compared to the US (a lot less household debt), view of housing as shelter more than investment and much more efficient and less expensive healthcare and education. Again the ECB was still delinquent here, as much as the Fed, but they did have a bit more of an anti-inflationary cushion.

In the grand scheme, it’s always one thing: Size of the money supply relative to the size of the economy. If the money supply grows at a faster pace than the economy and the population upon which it is built, inflation is the only possible outcome. Inflation can travel down many paths and it can be hastened or delayed by many factors. But at the end of the day, if more dollars are available to chase goods and services, prices will go up, period. We can print physical money or we can create new digits in accounts or we can generate credit money by lending out conjured-up digits, and we can even monetize debt on a national scale – a nation lending conjured-up digits to itself… It really doesn’t matter in the long run how the money is created. If we create new money that is not backed by additional products, services, or resources pulled out of the ground, we can only expect inflation. It’s perfectly well understood, but economists have a habit of overcomplicating their “science” in order to make a career out of producing mountains of inaccurate predictions.

Between Jan 2020 and Jan 2022, M2 increased by 40%. In that same time period, U.S. median home price grew 29% and the S&P500 grew by exactly the same percentage as M2 – 40%. Now the Fed has closed the free money spigot and even started to remove a little money deploying a small teeny tiny trickle of the anti-dollars they carry on their balance sheet. Surprise surprise, the housing market cooled off immediately as if it hit a wall and investors panicked as M2’s growth went flat.

Here’s the catch: M2 has never meaningfully decreased on the St’ Louise Fed’s M2 chart stretching back to 1959. It has gone flat or shrunken by absolutely miniscule amounts for a few months in a row here or there, but it ALWAYS resumed its upward trajectory within months of flattening. Add that the Fed has dropped interest rates during every single recession since WWII, and it’s fairly simple to anticipate their next move. The Fed will hold on to interest rate hikes and QT until we enter the next recession. In the next recession the Fed will abandon rate hikes and at least pause QT. M2 will resume it’s upward trend. When, exactly, will this happen? Who knows? But when the job market finally gets the memo and takes its turn and we figure out we’re in a recession, look for the Fed to change course. They always have and always will.

The actual causes of inflation are perfectly understood. Powell lied: “The connection between monetary aggregates and either growth or inflation was very strong for a long, long time, which ended about 40 years ago”.

The distributed lag effects of money flows, the volume and velocity of money, are not “long and variable”. They have been mathematical constants for > 100 years.

In my personal opinion, instead of doing 0.75% rate increases (though I certainly don’t oppose them), the Federal Reserve should have sped up balance sheet reduction instead.

Rate increases are easy to reverse: they can immediately slash rates to 0% when there’s an “emergency,” as they’ve already done twice in the last 15 years. But the balance sheet takes time to shrink. Last time QT made it to $600 billion before the markets threw a tantrum, and the balance sheet is now $5 trillion larger than it was before.

“The Fed holds $384 billion in TIPS at original face value. It has received $92 billion of inflation compensation on those TIPS. This inflation compensation increased its holdings of TIPS to $476 billion.”

This, in part, explains why the Fed is so behind the curve.

I think you were posting your comment while I was writing mine below, otherwise I would have replied to you originally. At any rate, this all seems really twisted. I never understood why the fed bought TIPS. Maybe there is a reason that somebody here can explain.

If the Fed pays extra $$$, the yield stays lower would be my guess. It’s all part of that interest rate repression business they’re in now. All they know how to do is lower rates vis-a-vis QE.

SocalJohn,

Here is the reason why the Fed bought TIPS, quoted from my article in April:

https://wolfstreet.com/2022/04/21/peak-balance-sheet-feds-assets-dip-to-5-weeks-ago-level-end-of-qe-end-of-an-era/

The Fed’s sleight of hand with TIPS on market-based inflation expectations.

Since March 2020, the Fed’s proportionally huge purchases dominated the relatively small TIPS market and pushed the TIPS yields into the negative.

The TIPS yields are called “real yields” and form a factor in the “market-based” inflation expectations (such as the spread to regular Treasury yields) that the Fed cited in its statements to show that market-based inflation expectations were “well-anchored,” when in fact these “market-based inflation expectations” were the result of the TIPS yields that the Fed manipulated down with its purchases of TIPS.

With its purchases, the Fed pushed the 10-year TIPS yield into the negative throughout the pandemic. But the Fed has now stopped buying TIPS, and TIPS yields began to rise in January (from -1.1% at year-end) to just above 0% on April 19, the first time since March 2020 that 10-year TIPS yield closed in the positive, though for only one day.

Manipulating the TIPS yield to show that “market-based inflation expectations” were “well-anchored,” though inflation had already begun to rage, was one of the cleverest monetary sleights of hand.

Thank you Wolf! I’m embarrassed to admit that I now remember your original article on this. Thanks again for reposting the pertinent text from that article, and thanks for all of your excellent work.

Thanks Wolf, had been confused about the TIPS thing for a while, that helps to break it down.

Wolf said: “Manipulating the TIPS yield to show that “market-based inflation expectations” were “well-anchored,” though inflation had already begun to rage, was one of the cleverest monetary sleights of hand.:

————————————

fraud …

that’s what they are ………… fraudster’s that stack the deck and rig the game in favor of their string pullers and the objective of servitude of the lessers

just as “clever” as their many other frauds and deceipts

Thank you for the way you break things down. I’m not entirely a novice, but I’m also no expert in the Fed’s workings. This article in particular broke concepts down to their fundamentals, which helps people like me. Keep up your good work!

The Fed creates inflation, and then the the Fed gets paid for having done so because the Fed holds TIPS, which were bought with money that the Fed created out of thin air. And the TIPS payments to the Fed increase the balance sheet that the Fed is now trying to shrink. I hope I’m wrong about something here. Sometimes I think this system is so badly broken that it cannot be fixed.

10-4 ScJ:

Been trying to explain this to family folks who are somewhere near the bottom of those understanding the Federal Reserve.

Not going to be easy far damn shore,,, but IF WE the PEONs don’t figure out how to not only get rid of the FRB, but also how to make our lives functional, or at least as function as OUR lives ( of WE PEONs ) were before the banksters initiated the FRB, when WE would put our gold into jars in the back yard “In the good times” and then take that gold out and buy buy buy!!!\

When the banksters ”’real eysed” what WE PEONS were doing was exactly when the FRB started,,, to STOP WE PEONs from getting ahead,,, as in totally ahead of the banksters..

Can’t have that,,, eh???

VVN, get rid of the FED? What (who) would replace it?

That is what the FED and their Masters would have you focus on

don’t fall for it ………………….

I would say probably something much, much more humble, Anthony….

If we lend credence to Ashby’s law of requisite variety then all these central bank shenanigans are in any case just an exercise in myopic sophistry. The failure of their system of responses is baked in.

Thanks for the detailed explanation Mr Wolf. I learned something! ( I think, if I have to, I guess ….)

It will be interesting to see how far Fed goes and how much real reduction they achieve before making a U turn. They tried doing so in 2018-19 and backed off the moment Trump threatens them.

US debt, Consumer debt, Corporate debt have only grown over time with small efforts to reduce it without any significant reduction.

I bet the moment there will be any trouble they will begin QE in full steam. May be they will reduce any another few hundred to show everyone they are trying.

When they made the U-turn in 2019, inflation was BELOW the Fed’s target. Now we have raging inflation. This is s a crisis, and the Fed understands that it needs to get this under control. People who compare 2019 to 2022 are comparing apples and oranges.

As a junior banker in the late ’70s to ’81, I saw inflation and interest rates most people today can’t imagine. I wish I still had my 1976 Ford campaign WIN button. I don’t know what he would have done, but after 2 years of Carter’s presidency with inflation getting worse, Carter hired Volcker and he swung the hammer on inflation. It wasn’t pretty, but it worked.

It didn’t work immediately… and Carter yanked Volcker’s chain in the spring of 1980. The real Volcker push didn’t come until November of 1980 after the election was over. Reagan (whose college degree was in Economics and who had a life-long interest in the subject) ignored the political pressure and “Let Volcker Be Volcker.” It cost Reagan dearly in the midterm elections in 1982 but it also led to his re-election in 1984 (with 49 states) and to 40 years of little inflation in this country.

This is the worst expansion of new money in U.S. history.

Trump took credit for the stock market rise. Biden not so much.

Powell was serving his first term. Powel now serving his last term.

Inflation was not. Inflation now raging.

Deniers about QT have been proven wrong, each step of the way, and indeed have ‘lost tough’ if they have been betting on their convictions.

“I bet the moment there will be any trouble they will begin QE in full steam.”

I’m sure you engage in this fantasy as often as you can, because otherwise you’d have to face the cold hard truth of your shack price crashing bigly with no FED riding to your rescue. You gambled. You lost.

Stocks are now going up and so is Bitcoin. RE will stabilize.

Bond market is already pricing in Fed U turn. I guess they are smarter than a few perma bears.

Asset prices will not be allowed to fall too much, and in long run charts these hiccups won’t even show up.

This is hilarious sarcasm LOL

“I’m sure you engage in this fantasy as often as you can, because otherwise you’d have to face the cold hard truth of your shack price crashing bigly with no FED riding to your rescue.”

lol and that’s so true. That’s the real motivation of I’d bet more than half of the QT deniers and the “this time it’s different” squawkers on CNBC, Bloomberg and all these Tiktok and Youtube financial vloggers–they’ve gotten themselves heavily leveraged and in over their heads with FOMO and buying at the top of this outrageous Everything Bubble, especially it’s worst part (the housing bubble) where they were hoping to get rich as slumlords by driving rents through the roof and passing on their costs to desperate working and middle class folks just looking for an affordable place. We even know several who bought multiple rental properties in the most outrageously bloated and overheated real estate markets (like Phoenix or many cities in West Texas that are all running out of water and in major drought). Or got knee deep in similarly stupid asset bubbles in crypto, SPAC’s or overpriced equities (which at least don’t hit absolute essentials for Americans the way the bubbles in home prices, healthcare and education do). They know that in any fair market, their assets are grossly overvalued and have to come way down, in some cases leaving them underwater, or forced to (the horror of it) reduce rents on their tenants already suffering from rampant inflation. Their only hope is the Fed riding in on a white horse, but now with runaway inflation raging, that hope is forlorn. And most, in their heart of hearts, know it.

Reading these great details, I wonder what is Wolf’s background to be so familiar with these dynamics

I covered the last QT in detail, and I contacted the New York Fed which answered some technical questions back then when I couldn’t figure them out myself. I dug into it because no one else was, and because it was so confusing, and the reporting was so bad on it.

What exactly was in any way ‘confusing’ about what the Federal Reserve was doing back then?

Bravo!

LOVE IT!!! Far damn shore Wolf,,,

And, budget allowing another cash send, will be coming as soon as I sober up enough to drive to the PO…

Again, many many thanks for your work.

Probably already saved US, the family US, at least several and more significant %%% ….

As I understand it the intent of QE was to suppress the longer end of the yield curve. If that’s right then I think that QE will most directly affect asset inflation – inflated housing prices. I guess it will indirectly address other facets of inflation via demand destruction, i.e. negative wealth effect. So maybe fewer imported cars and international vacations. Won’t lower grocery bills or ever increasing cost of all energy, health insurance, etc.

YES it WILL reduce all of those SR.

If too young, refer to local and other ”anecdotal” reports of what happened in all the now clearly ”out of control” aspects of our world…

Been there, done that will be a meme for the very youngsters these day,,, just as it was in the late ’70s/early ’80s.

Tough, far shore, for those who have never seen any ”back tracking”…

Have you ever seen the cost of heath insurance or anything in the heath field actually go down here in the U.S. ? I haven’t and I have been around 79 years.

Wolf,

I calculated the following numbers for the month of June, June 1 through June 29, to be exact, from the System Open Market Account Holdings table (SOMA) found at newyorkfed.org:

Change is Treasury Bills: $0.0 Dollars

Change in Treasury Notes and Bonds: -$9,301,269,800.0 Dollars

Change in Agency MBS: -$1,987,287,600.0 Dollars

With regard to the Treasury cap only, $30 Billion for the month of June, coupon securities that mature have priority and if the cap is still not met, T-Bills will roll off the balance sheet to meet the cap.

From the numbers above, why didn’t the Fed roll off T-Bills? I understand that there may not have been enough T-Bills that matured in the month of June to meet the cap, but they didn’t roll off any, as far as I can tell.

Perhaps the Fed is talking about a rolling 30-day period instead of a calendar month.

Thank you.

I understand that there were T-Notes and T-Bonds that expired on June 30th, as the article points out. I guess those were credited toward the month of June even though the SOMA holdings were not updated until the following week.

Trying to avoid the RTGDFA hurled upon me.

From the SOMA account I calculated a change in T-notes and bonds of -$31,400,708,200 dollars, June 1 to July 6, which takes into account the June 30th maturities. So looks like the cap was met after all, without the need to roll off T-bills. Sorry to pollute the comments.

There were ~48 billion in notes and bonds that matured in June, above the 30billion cap. Thats why t-bills stayed steady. The last h.4.1 was through 6/29 so missed all the 6/30 maturities (reflected in this weeks h.4.1).

See my comment below for september, tbills will need to be reduced then.

“Change in Treasury Notes and Bonds: -$9,301,269,800.0 Dollars”

RTGDFA.

At least read the 2nd paragraph!!!!!!!!!!

Treasuries roll off twice a month, June 15 and June 30. The June 30 roll-off of $20 billion wasn’t part of the June 30 balance sheet because that balance sheet cut off on Wednesday Jun 29. For crying out loud.

Fabulous article.

Some additional input.

SOMA holdings can be found at https://www.newyorkfed.org/markets/soma-holdings

Its useful to look at the UST held by the FED to determine when the balance sheet will drop. For example for July, between 2billion and 13.6billion will drop on 7/15 with the balance 16.4-28billion will drop on 7/31. Just look at the UST maturing for the month and readers can see for themselves.

September is interesting since the FED owns only ~44billion of maturing treasury notes/bonds. Since QT will be 60 billion in UST the FED wont roll over any of these and additionally the FED will have to also not roll ~16billion of treasury bills so look for the tbills on the FEDs h.4.1 to drop in september

On MBS, Fannie and Freddie pay their monthly payments to investors (the FED in this instance) on the 25th of each month or next business day if weekend/holiday (which is why the MBS balance sheet dropped so much on last weeks h.4.1 that spanned June 27th (25th was a saturday). Fannie and freddie MBS account for ~80% of SOMA MBS holdings.

GNMA II MBS accounts for most of the other 20% of holdings and it pays to the FED on the 20th of each month. GNMA I is negligible but pays on the 15th.

Those MBS payments consist of both regularly scheduled monthly payments and any principal prepayments (payoffs of the mortgage due to refinance or selling the house or winning the lottery), the regularly scheduled payments are predictable ~5bill a month but the prepayments are less so and have been slowing o. Based on May prepayments and the Feds MBS purchase schedule for MBS from mid june to mid july it implies ~25bill in prepayments + the 5bill regular payments. I havent seen prepaymment numbers for June yet but they will probably continue to slow. Meaning, so long as the FED continues to just roll off MBS balance (as opposed to selling MBS) and prepayment rates stay steady or continue to slow, the FED will not be able to meet the ramped 35billion number for September but will instead be somewhere in the low 20s probably.

Hope this additional info helps readers to understand (and confirm for themselves) some of the underlying mechanics for QT.

What I dont have the details on are detailed settlement dates on the MBS the FED is purchasing/has purchased (as reinvestments). If that information is public Id love to know where to find it.

Hope this helps.

thank you JC.

Actually helps this old boy to at least ”try” to understand all of these modern concepts,,,

Which clearly are just another way of confusing the already sufficient challenges of any of WE PEONs who want to invest, but usually don’t have anywhere close to enough information…