The magic of ridiculously inflated home prices meeting holy-moly mortgage rates.

By Wolf Richter for WOLF STREET.

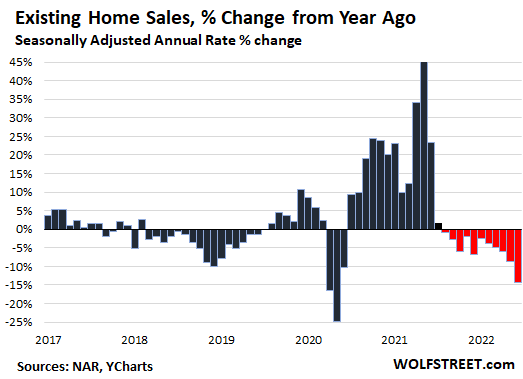

Sales of previously-owned homes of all types – single-family houses, condos, co-ops, and townhouses – dropped by 5.4% in June from May, the fifth month in a row of month-to-month declines, based on the seasonally adjusted annual rate of sales. And sales dropped by 14.2% from a year ago, the 11th month in a row of year-over-year declines.

The sales declines have been accelerating, even as all kinds of inventory is suddenly coming out of the woodwork. And the excuse for the drop in sales that there is a shortage of homes on the market has vanished.

Sales of single-family houses dropped by 12.8% year-over-year, and sales of condos and co-ops plunged by 24.7%, according to the National Association of Realtors today (historic data via YCharts):

“Both mortgage rates and home prices have risen too sharply in a short span of time,” said the NAR in its report today.

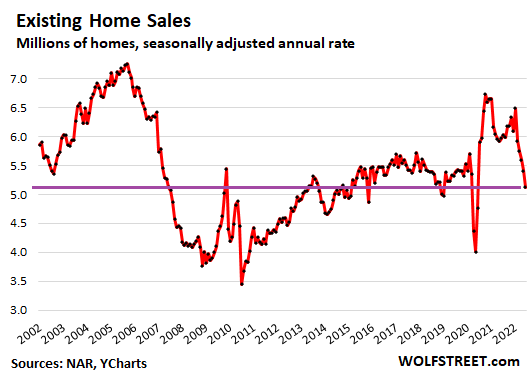

The seasonally adjusted annual rate of sales in June fell to 5.12 million homes, the lowest since the lockdown months in May, April, and June 2020 (historic data via YCharts):

Holy-Moly Mortgage Rates in the driver’s seat.

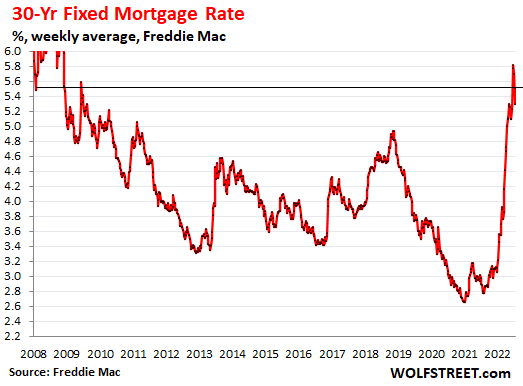

I call them “holy-moly mortgage rates” because that’s the sound potential homebuyers utter when they see the mortgage payment needed to fund the ridiculously inflated price of the home they’re wanting to buy.

The average mortgage rate spiked to 5.5%, up from 2.9% a year ago, according to the most recent reading by Freddie Mac. It breached the 5% line in mid-April and has been in the 5.5% range since mid-June.

A 5.5% rate for a 30-year fixed rate mortgage, when CPI inflation is over 9%, is still mind-bogglingly low, and speaks of years of interest rate repression and QE by the Fed, which has bought, among other goodies, $2.7 trillion in mortgage-backed securities, thereby repressing mortgage rates. But QE has ended, and QT rules, and the Fed has started to shed its mortgage-backed securities, and mortgage rates have made the first steps toward some kind of normal level, except now prices are sky-high due to years of mortgage-rate repression, and the whole thing is out of whack:

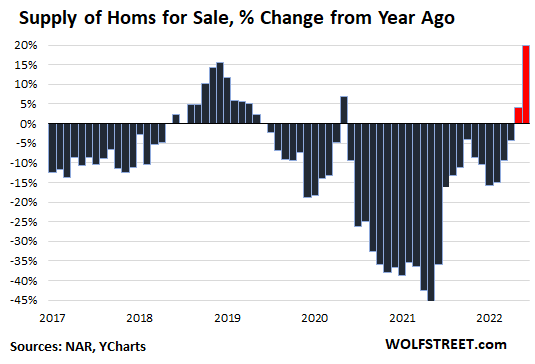

As always when the market turns, supply that no one thought existed starts coming out of the woodwork.

The number of homes listed for sale in June jumped by 110,000 from May to 1.26 million, the highest since September, after having jumped by 113,000 in May and by 100,000 in April.

All last year, the industry lamented the “housing shortage” in order to hype up the price, when it was really a refusal by homeowners who’d bought another home to put their old and now vacant home on the market because they wanted to ride up the price spike all the way to the top. This has now been accomplished, and these vacant homes are appearing on the market

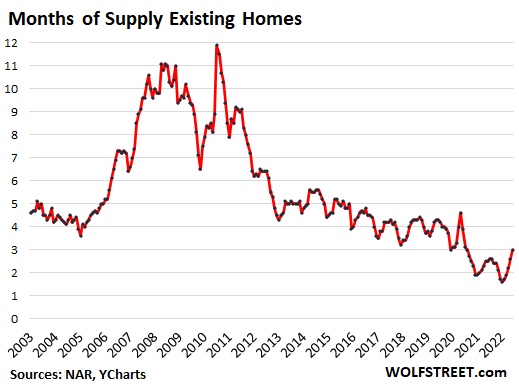

Supply of homes listed for sale jumped to 3.0 months, the highest since August 2020, and up by 20% from a year ago. (data via YCharts)

Supply nearly doubled from the low in January (data via YCharts).

Sales by Region.

Sales dropped in all regions on a year-over-year basis. Note the 21.3% plunge in the West: In California, closed sales of houses plunged 21%, and closed sales of condos plunged by 27%. To show where this is headed in July: pending sales in California collapsed by 40%.

- Northeast: -11.8% yoy.

- Midwest: -9.6% yoy.

- South: -14.1 yoy.

- West: -21.3% yoy.

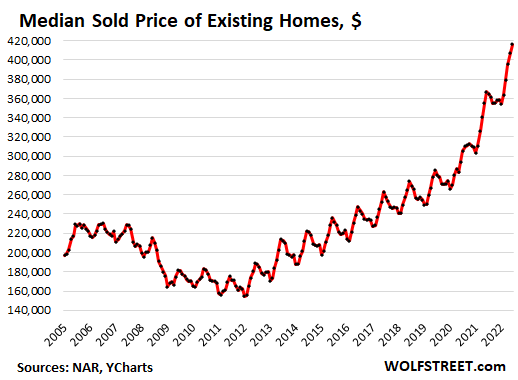

Median Price skewed by shift in mix to higher-end sales.

The median price rose to $416,000, up by 13.4% from a year ago, according to the NAR. And as we’ll see in a moment, the median price is skewed by changes in the mix, and there has been a huge shift in the mix to the higher end (data via YCharts):

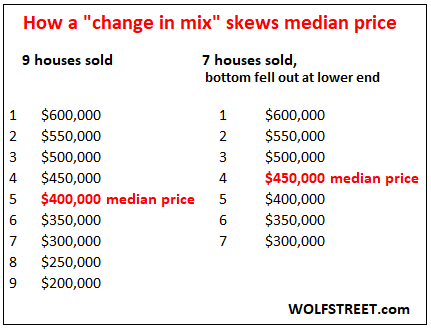

I’ll just repeat my favorite illustration: In a market where 9 homes sold, the median price is the price in the middle (fifth from the top). If only the top seven houses are sold, as the bottom fell out, the middle is now the fourth house down, or the fourth house up. This change in mix skews the metric of the median price, though the actual prices of the homes haven’t changed:

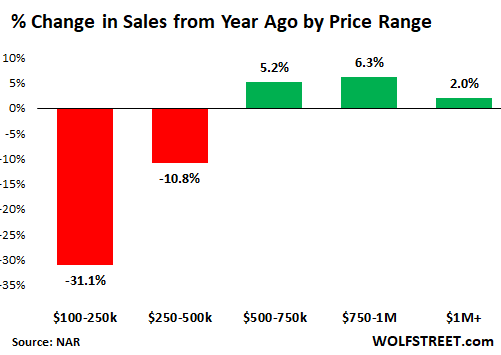

In the US market, the bottom has fallen out in sales of homes priced below $500,000, which accounted for 62% of total home sales in June.

But sales of homes above $500,000 have increased year-over-year. Sales of homes in the $500K-$750K range accounted for 20% of total sales; homes in the $750K-$1 million range accounted for 7%; and homes of $1 million and over accounted for 8% of sales.

And this big change in the mix – with fewer homes selling in the lower half and more homes selling in the higher half – skewed the median price upward. Sales by segment, according to the NAR:

And don’t blame the West for this shift in mix. In the high-priced West is where home sales plunged the most (21.3% year-over-year). Sales plunging faster in the high-priced West than in lower-priced regions would normally skew the median price down. So what we’re seeing is that the actual sales mix across the US is shifting, with higher-end buyers less impacted by the prohibitive affordability issues brought on by these holy-moly mortgage rates.

And no, investors, second home buyers, and all-cash buyers aren’t piling in: Their share remained steady.

Individual investors or second-home buyers purchased 16% of the homes in June, same as in May, and down from a share of 17% in April, 18% in March, 19% in February, and 22% in January, according to the NAR.

“All-cash” sales, which include many investors and second home buyers, remained at a share of 25% in June, same as in May, and down from a share of 26% in April. Their share has been in the same range for the past 12 months.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

More high-end buyers are also the cash buyers as you suggest and aren’t impacted by the rising interest rates.

… or discretionary inflation.

High end buyers aren’t foolish to buy now, otherwise they won’t have this kind of cash for buying homes to begin with.

Most cash only buyers today are:

1. People who have paid off this houses that were purchased much earlier at a cheaper price, now want to move. So they sell their house and use it to buy another.

2. REITs and investors who raised money from other sources and then gamble with other people’s money by now using this cash to buy house.

3. Folks who laundered money illegally from other countries to invest in US real estate.

price is IRRELEVANT when moving sideways

ie from one market to another

and paying CASH

most moving to LOWER COST MARKET and can buy EXCLUSIVE homes in new market

around 1/2 sales today in Tucson

“3. Folks who laundered money illegally from other countries to invest in US real estate.”

4. Just plain rich foreigners who have bought many tens of thousands of homes in California alone.

Superb map by zip code of Calif all cash sales

“Data dig: Are foreign investors driving up real estate in your California neighborhood?”

I live in an upper middle class area in coastal SoCal. 2 local realtors and 1 mortgage broker all say that all-cash deals are very rare in the area, it’s mostly people rolling equity from another property and maybe some stock market dough into the deal but still financing about 70-75% of the purchase.

“All Cash” was never big in Boston during the Pandemic-induced spike.

Institutional Buyers are awash and cash and trying to unload it, and financing the purchases via loans enables them to purchase more properties with their cash because they are putting less money down.

If they are concerned about not being able to service this large number of loans – they are yet to show that.

I’ve heard this argument before, but I don’t agree. If the people who were previously buying $500,000 houses can only now afford $400,000 houses, then the people who could previously afford $620,000 can now only afford $500,000, and so forth. There aren’t separate markets for high end buyers (except for the oligarch penthouses in New York or London) and normal buyers. There might be a delay, but a collapse in demand at the low end will eventually affect the high end too.

Agree. The housing bubble won’t really pop until you start to see declines at the higher end of the market. Which I suspect is why Wolf keeps showing us that last chart on price range.

Yes. At the higher end, even for cash buyers, it’ll be about psychology. Even people who have $2 million in cash to buy a house won’t do so if they think they can get that same house for $1.5 million next year. And watching prices collapse elsewhere is a good way to change that psychology.

“ Even people who have $2 million in cash to buy a house won’t do so if they think they can get that same house for $1.5 million next year”

Nope, at that level the differences for many are rounding errors in their wealth portfolio…

They care more about what it is and what it can do for their lives than the cost…

That’s absolute nonsense. There are many older people who would pay in cash for a $2 million house but don’t have so much that the $500,000 difference is a rounding error.

Sorry COWG, but Einhal is absolutely correct. People that have a few million dollars don’t consider half a million dollars to be a rounding error. Neither do people with LOTS of millions of dollars.

Of course, there are exceptions, but you won’t find many among those that earned it for themselves.

Thanks Halibut. He’s right that people with half a billion or more in net worth are going to buy the house they want, and aren’t going to care if it’s $1.5 million or $2 million. But there are a lot of upper middle class retirees (or soon to be retirees) with comfortable levels of wealth, say $5-$10 million, who are looking for a home, say on the beach or in a ski town. As you correctly point out, those people don’t consider $500,000 to be chump change.

There aren’t enough people for whom half a mil is a rounding error to have any real effect on the market as a whole.

“ That’s absolute nonsense”

Einhal,

Be nice to your elders !

I’m not discounting what you’re saying, however I think you might be having a somewhat narrow focus…

Many wealthy people will buy a house like we are talking about ( think Naples, FL) not necessarily as a primary residence ( although it may be) but more as a portfolio move…

These people think IRS first, price second… they have an army of lawyers and accountants protecting their money…

As an example, let’s say I sold a high dollar property that was depreciated out… I HAVE to redeploy the money or get killed in taxes on capital gains…Price may or may not matter… depends on what the purchase brings to my tax bill…

Without getting too far into the CPA realm ( which I’m not), my only point is that for many wealthy people, high dollar real estate considerations is not necessarily calculated on the price, but also the tax ramifications…

As an aside, I used to fly right seat on a King Air that was owned by a construction company who leased it out for charter… the owner, after the aircraft was depreciated out, had to invest in a more expensive aircraft to avoid capital gains taxes…

Wealthy people do not do anything without without consultation regarding tax ramifications…

That’s my point… but I also see what you’re saying.

COWG, I agree that that does happen, but just want to note that 1031 exchanges are limited to investment real estate (not a residence, whether primary or secondary). If you’re talking about the strip in Naples off Gulf Shore where the houses are $50 million or more, then I agree we’re talking about a different market unaffected by the rest of the housing market.

The housing market isn’t going to collapse any time soon. By early next spring, housing will be broadly down 10%. In addition, mortgage rates will slip below 5%. Due the combination of these factors, housing market will stabilize and turn north again, al beit at much slower monthly gains. We might not see real negative job losses by next spring and inflation isn’t going materially below 7%.

And, the Fed won’t be able to raise the FFR more than 3.25-3.5%. To do so, will cause competition over where investors will put their money, namely short duration treasury bills and even the 2-3 year notes. If demand for bills falls, then yields will have to increase.

So, this all will get really interesting by this fall after what may be a 100-basis point rise next week then at least a 50-basis point increase in September. By then, we’ll have a lot of economic data to see where the economy is headed, especially inflation. Look for Putin to do something big in terms of flows of petrol & NG to Europe around this time.

The difference is that cash buyers turn homes into an income stream, which they then use to make more cash only purchases. There should be laws in place that say tax breaks and exemptions only apply to individual buyers, not shell companies, and then only for the first two homes. The finalcialization of housing is the most morally bakrupt decision this country has ever made.

Absolutely. I can understand why the Republicans won’t do anything about this because of their distaste for regulations even when most of the population need these protections on a critically essential item like housing.

But I wonder why the Democrats don’t have any positions on this matter. Perhaps, the housing lobby including banks, mortgage companies, NAR, and others have a complete chokehold on the Democrats as well.

God save us!

Amen. There are reports (e.g., in CNN business) that the banksters and their Wall Streeter cronies, the financiers, are buying up US real estate. They want to make us all their rent-slaves while they collect our disposable income via sky-high rents. With access to unlimited financing from their “Federal” Reserve even if they ever go insolvent, such bets (using the credit and financial power of our nation channeled through the credit power of their “Fed”) are more ways to milk money from Americans.

Keep in mind, e.g., if they buy 1000 houses each with a loan of $700,000 for an interest rate of 7% per year (preferential, bankster-crony rate) and real inflation is running at 12%, they are getting an annual reduction of debt “gift” of $35,000,000.00 PER YEAR (12% less 7%, which is 5% times $700,000,000) just from those houses. Their ability to raise rents later far above the rate of inflation, and further profits from increases in land values, are just going to be millions more in profits.

@Sean Shasta,

What I am proposing is a *paring back* of laws surrounding housing. That is the opposite of regulating. It’s not Republicans who won’t like it, it’s the wealthy who are exploiting the law, who come in all political flavors.

All true. That’s a great description of how this latest housing bubble will likely unwind, and how it did unwind in 2007 and 2008. The capacity of buyers at the different layers go into decline more-or-less simultaneously, and the whole thing feeds on itself. All the signs are there again and this time it’s not different. If anything given the level of leverage now and the much higher rate of inflation pinning down the Fed and thwarting any monetary loosening, it might be an even more striking drop this time around. Though may still take a few years to work out all the factors.

CA only saw buying post bubble 1.0 at annual rate of about 60 pct that of the pk yrs of bubble 1.0 (although bubble 2.0 has gone on longer).

So *maybe* implosion 2.0 might not be as bad.

Hard to judge unless somebody totals up annual sales for both periods and the relevant annual median buy in prices.

Used to think smaller annual sales meant 2.0 would definitely be not as bad, but 1.0 ran for maybe 5 years and 2.0 may have run for 8 or 9.

My god, the Fed has been a lobotomized monster for so long…

Think about what that drop in prices does to leveraged MBS. And people starting to get delinquent on their mortgages.

I am housing bear, but I don’t think Wolf”s theory on people holding onto empty homes to hope for price increases is supported by data. Homeowner vacancy rates remain near historical lows. I think the issues is too many single family rentals, so it is key to keep any eye on rental rates to signal the big fall in housing prices.

https://www.census.gov/library/stories/2022/05/housing-vacancy-rates-near-historic-lows.html

40,000 homes in San Francisco are vacant. This is such a HUGE and acknowledged problem that people are trying to put a vacant-home tax on the ballot. The Census has no idea…

The vacancy data from the Census is BS. Their method of measuring vacancies by sending surveys to address that are vacant produces silly results. And then there’s the issue of how the Census defines “vacant.” Not what you think.

John Stiles

“but I don’t think Wolf”s theory on people holding onto empty homes to hope for price increases is supported by data. ”

You are 100% wrong on this. The data that I see right in front of my eyes says otherwise. About 90% of the appraised homes we have seen since the beginning of the pandemic have been empty. I’ve posted this numerous times on this Website. Obviously, you never read my posts. Instead, you’ve decided to join in with all those Lemmings who believe every piece of bull s$it published by the government.

Two thoughts came to mind when reading this…well more like three but the last one is more related to my excitement in seeing this trending in the right direction, now just to be patience and see this reflect in the grossly overpriced asking still seen in popular SoCal markets..(I am looking at you Irvine, West LA, South OC)

“Sales of single-family houses dropped by 12.8% year-over-year, and sales of condos and co-ops plunged by 24.7%, according to the National Association of Realtors today”

Looks like Lawrence Yun is going to have to work more OT to put the spin machine on full blast

“The number of homes listed for sale in June jumped by 110,000 from May to 1.26 million, the highest since September, after having jumped by 113,000 in May and by 100,000 in April”

Wonder how they are going to spin this one now…probably will still use the it’s still historical low in comparison long term trend. Well, eventually that will also not be the case, then I guess it will be back to “It’s just a gully” defense or why my area is so unique and different.

I will work with my homie, Lawrence Yun!!! There will be no correction!!! This will be a soft landing!!!

Phoenix, I’m not at all familiar with SoCal, but someone in the last articles comments mentioned a lot of Mandarin speaking Chinese buying a lot of property recently in the Irvine area. Big spenders.

Taiwanese speak Mandarin. In other areas of the country like Seattle Chinese buyers seem to be pulling back for various reasons, but with tensions over Taiwan it’s possible there may be some rich people from Taiwan investing more in some SoCal cities. Taiwan is so much smaller than mainland China that I think it’s reasonable to expect a smaller immigrating population if that is the case, and maybe only those with a lot of money.

NOT mentioning this to discourage you, but possibly give you a heads up. Maybe you can buy something that is older and needs work and have it fixed if the numbers work out. New rich immigrants sometimes won’t touch older housing. Which is smart if you don’t know the language or the local hiring or building code environment.

Yeah will have to see how it plays out. These Chinese buyers can their Irvine, San Gabriel Valley. Even if these areas are in fair value, I probably don’t want to live there. My best hope is that they stay away from some of the nicer areas not populated by the same demographics in SoCal.

Irvine and areas like that have been building homes that appeal to those who respect their multi-generational family. The homes often have a central courtyard that separates the main house from the small casita type house that has a living area, bedroom, small kitchen, and a spa type bath.

That might explain the attraction to those areas. When I lived in OC, the neighborhood we lived in turned heavily Asian due to the fact that every home had a first floor bedroom suite with access to the family room and kitchen.

And they paid through the nose to get them.

Chinese lost 50% on homes in mainland now ,another 50% haircut .welcome to America suckers

Also look for homes where someone has died. I think this is disclosed. I was told Chinese will avoid these homes. I know sounds crass but being practical for you.

Also look for homes with 4s in their street address. Chinese will likely not buy these. The more 4s the less likely.

They do not even have floor 4s in chinese buildings.

4444 main st.

There have been virtually no Chinese buyers of US residential real estate since early 2017. The CPC instituted highly-effective capital controls starting in the summer of 2015 when the Yuan went through another devaluation.

Farm land, etc. may be another story – but Chinese purchases of US residential real estate haven’t been a thing for more than five years

There may be something to this, ie. in the shrinking share of mainland Chinese vs Taiwanese doing this. China now has very thorough capital controls and it’s tough to move money out–and interestingly it wasn’t just Beijing pushing this, Canada’s government was pressuring them because it was tired of Chinese investors basically wrecking the affordability of housing in Vancouver. The controls aren’t perfect but they work reasonably well. Maybe even more important now is that more Chinese investors are wary about the potential of their property or assets to be seized abroad. Also the home market is providing more opportunities, and they’re getting more worldly, ex. a lot of Chinese investors preferring real estate in other Asian boomtowns (incl. in SE Asia), in Europe, Australia, even more snapping up options in places like Brazil or Argentina. That diversification means a lot less money for the traditional real estate bubbles in Canada and the US. It’s possible that the Taiwanese have less experience with parking money in varied overseas real estate, and so may stick closer to traditional markets already with a lot of ethnically Chinese contacts like in the San Gabriel valley, or Seattle.

Miller, I agree, especially about the concern over future seizures. When FINCeN did an ever broadening pilot program with disclosure of beneficial ownership required cash sales fell;

“According to a study by the University of Miami; “After anonymity is no longer freely available to domestic and foreign investors, all-cash purchases by corporations fall by approximately 70%, indicating the share of anonymity-seeking investors using LLCs as “shell corporations.”

They’re not only worried about potential future confiscation by the US but also about the Chinese government.

The capital flight controls however don’t ever seem to work. In fact after the first pause with tighter controls the money seems to flow out even more out of fear..

I think the bit-coin etc crash adds to it as well. I imagine a LOT of money leaves China through bit-coin etc as much of that is untraceable. At least one of the big RE development companies over there was doing double accounting and a lot of their money was found to be leaving the country to pay offshore “loans” in bitcoin before it went bankrupt.

This is all so cute. You all think homebuyers are all rational. Sure lots are smart and rational like you think they are. But not all are by a longshot. There are lots of people in CA with lots of money that just like buying homes. Some make money, some lose money but that doesn’t motivate or stop either. They just like to buy homes and live in them

Exactly!

”Connected” foreigners bring their own labor to fix or even build new housing.

Seen it in various places since competing on bids against them since 1981 in bay area, more recently other wheres.

Do you know if they’re doing that or are they connecting once they get here? When I lived in the Richmond in SF there was already a huge Chinese migrant labor pool. They might have to negotiate with the boss.. It would be more expensive to import carpenters that had any clue as to what they were doing to work on a $2+M home. Never mind someone who knew code.

Hey Wolf,

A question for you: Without all of the QE and low interest rates for the last 20 years, where do you think stocks, housing, NFTs (ok i won’t ask about them since they wouldn’t even exist without the cheap money), and the unemployment rate would be?

Its funny, you read so many articles about how the FED is making a “policy” mistake by tightening to fast or even at all and blah blah blah, but in my mind and from how society has “progressed” the past 20 years, i’d say the policy mistake was low interest rates and QE to begin with. Some of us knew when it started that it would all end in tears, and now i think we’ll have more then just tears……..

“Its funny, you read so many articles about how the FED is making a “policy” mistake by tightening to fast or even at all and blah blah blah, but in my mind and from how society has “progressed” the past 20 years, i’d say the policy mistake was low interest rates and QE to begin with. ”

You said it! But for inflation biting the Fed they might still be at 0 and QE.

Is it a crime to line up the Fed Chiefs from Greenspan on and shoot them?

Inflation is baked in might drop to 6-7% range ffor next several years . FRB bailed out rich one too many times .But billionaires wil still be eating steak ,while poor people eat grasshoppers

“Liquidate labor, liquidate stocks, liquidate the farmers, liquidate real estate. It will purge the rottenness out of the system. High costs of living and high living will come down. People will work harder, live a more moral life. Values will be adjusted, and enterprising people will pick up from less competent people.”

Next round of scandals for the elite will be the super-wealthy feverishly creating back channels to invest in Russia – which, presumably, is one of the few places likely to offer positive real returns now that the sanctions have backfired so spectacularly.

Bet on it.

“But for inflation biting the Fed, they might still be at 0 and QE.”

It looks like that’s the norm for now on if inflation can be knocked back a little. QE and 0% keep the stock and property markets hot which looks good in the news, gets politicians voted back in and the wealthy get richer.

Who needs physical production, send it overseas. That thinking is relic. Congress is having us pay someone to manufacture chips in the U.S., it’s come to that.

lol true and does kind of have a decadent “fall of Rome” feel to it. That’s maybe why the inflation right now is important in thwarting the Fed’s easy money tendencies, it’s bad for social order, bad for politicians and changes the calculations. If there’s anything that riles up populations with thoughts and actions involving pitchforks and lampposts, it’s runaway inflation, and that scares the politicians and elites too. Maybe a big reason why the Fed and central banks around the world are finally changing their tune. Their hand has been forced.

KPL

In a corrupt society, those with absolute power to destroy the lives of others, have no personal responsibility for consequences. I give you the Fed, Washington, DC, Europe and the WEF/WHO.

We are in the lasts days of Rome, although it took a couple of hundred years before Rome was sacked. But the rope got tighter and tighter every day.

Why do you think DC was so quick to put 2 full infantry divisions in DC after Jan 6?

Because of a topless schmuck wearing a buffalo head?

DC knows what they have done and how they are thought of.

Thus two full infantry divisions appear in days to defend the city of whited sepulchres.

With all this bad news, I was thinking home builders stocks would be dropping more. The home builders ETFs (ITB and HOMZ) are down around about 25% from their peak and still above pre-pandemic prices.

I just read Mortgage demand hit a 22 year low.

Hurray! Bull sentiment at all time high. Fed soft landed the rich after all…at the expense of equality, civility, decency, integrity, honesty, fairness and freedom. Enjoy the remains of your shattered major award.

Where are you seeing bull sentiment at high?

Crazy….but hotels are doing great. Some people say we are already in a recession. You do not have a recession with low unemployment and record sales in the hotel industry that is almost 100% discrete income? Anyway….average hotel rate is now $155. Crazy.

——————————————————————–

Smith Travel Research, which is the primary data source for hotel industry trends, released its monthly hotel performance report for June on Tuesday, and it was a doozy.

In June, the hotel industry reported its highest monthly room rates on record, with the average daily rate (ADR) at $155.04, up 15.3% over June 2019 (pre-pandemic). Meanwhile, revenue per available room (RevPAR) also hit a record at $108.64 — a 10.3% increase over June 2019.

Yes, San Francisco is packed with tourists throwing money around — mostly domestic tourists too.

The term you’re looking for is “Revenge Travel”. This is people booking vacations they couldn’t take for the last two years due to covid. All modes of transport are sold out or even overbooked in some cases. There are almost daily reports of chaos at airports around the world due to cancelled or overbooked flights. It also helps that Europe is now on sale with the Euro now at parity with the dollar.

So yes, hotels and AirB&B are going to be doing great right now. Good luck finding a rental car.

I would agree with you. There could be pretty big hangover coming for travel.

Wolfe has been posting a lot about a pivot in spending from goods to services. I don’t think that pivot will have legs – I think we’re going to go straight back to spending on goods (if mostly essential ones) with very entrenched “demand pull” characteristics due to expectations of higher future prices.

Not sure it is as bright as it looks. Vacations were canceled and now everyone is trying to doing something so the demand is synced and prices are through the roof. But that is not sustainable volume but a one-off peak.

FD: Currently paying the highest rate I ever paid in Europe which made us keeping the trip short.

There are fewer hotel rooms available though due to the labor shortage.

Hotel occupancy around Boston has absolutely snapped the needle off the meter.

There is probably an upward swing in the quality of hotels and motels being stayed at by tourists. Many of the lower end motels are being used partly or wholly as low income residences- either by the government or by choices of the owners. 4 of them are now rented by permanent residents and 2 of those became tun down flea bags because of that. One is entirely rented by one employer for his employees, another decent one is rented permanently by workers who had a connection with the owner- construction workers etc – so it’s not just “the former homeless” who are renting them.

So- we have more STRs but less than half as many hotels and motels accepting reservations.

Oops, meant to say out of 7 motels and hotels in my area 4 of them are rented by permanent residents.

Along these lines, I would like to see some room supply numbers…2 yrs of pandemic surely put some properties into bk…I’ve seen at least three acceptable quality motels (100+ keys each) sitting empty and idle locally (Columbia SC) during these “record” room rates.

Destroy enough supply and rates will rise, even without a great economy.

Why are people renting motels?

Are tgey transient workers?

RU82, no, they live there year round. They can’t afford or get anything else. The rates are dropped for longer term residents. Same in some vacation RV parks now.

Campgrounds are packed too, and getting pricy. The state parks here were filled up before the weather warmed, very few cancel even when bad weather’s forecasted. Not hard to imagine people are living in campgrounds to save money, or have no where else to go.

There’s something weird going on with campgrounds.. Yep, there are people living in them and switching out here and there, but there is something else going on. The 3 times I was able to get a campsite and actually go there last summer I noticed the campgrounds were only half full late night AND early morning even though they stated they were completely booked both online and in the campground computers. IDK WTF is going on. People booking them then not showing up? It’s very frustrating.

Probaby staffing issues. Stayed at a family campground resort over Memorial Day weekend that was supposedly booked solid, yet half the sites were empty. Not enough staff to maintain/turn over sites. A few of the resort’s services were slashed as well (babysitting, doggie daycare, etc) due to staffing.

Most people are still becoming poorer, technical recession or not.

It’s a hollow victory.

I think it’s mostly talk of a technical recession, mainly due to the way 2021 numbers were so crazily distorted by all the stimulus from that year (and from 2020) that changes in inventories, less hot spending and the trade deficit could lead to two straight quarters of contraction. Not a bad economy, just technically adjusting down from the sugar highs of 2021. Even then if I had to guess, I’d say that Q2 in the US will squeak out growth and still barely avoid recession after the contraction in Q1–Wolf posted retail sales numbers that were pretty good for June, and if anything the parts of the economy that raise GDP in a not so good way (healthcare costs, costs of education) may also keep the USA barely positive, even if they make things more difficult for lots of indebted Americans. I’d say a recession is much more likely in early 2023 when the full brunt from Fed tightening gets felt and start to exert its effects more obviously, which usually takes time from when the tighter monetary policy, rising interest rates and more stringent credit takes hold. And while it may be deep and difficult, it should be manageable. If history is rhymeing, I’d say a lot like the 1983 recession, and closely following Paul Volcker’s model to fight the inflation then. Only a recession would cure the current US housing bubble and other asset bubbles at this level of mania.

People spending before Armageddon commences? Plus still too much paper wealth.

@ru82: “You do not have a recession with low unemployment and record sales in the hotel industry”

Actually, that’s exactly where you are when a recession starts. Recessions start when everything is as good as it can get – and then it starts to get worse. And the “get worse” part starts small, so most people don’t notice.

Anyway, until the monthly inflation numbers come down, the Fed’s rates have to go up… There might be a “soft landing” on that flight path, theoretically — but the runway is fogged over, there’s a high wind, and the Fed’s “plane” doesn’t have proper instruments.

Wolf, typo, the subject line above your name says moly-moly … “The magic of ridiculously inflated home prices meeting moly-moly mortgage rates”

Thanks.

RE prices are the result of two factors ( twin sides of the same coin). Interest rates have been declining for 4 decades now ( forced down?) and money creation has been exploding for the same period. Everything else is just a symptom of these two. The RE pumpers love to spout things like land availability, exploding population etc. Sorry folks, those factors went as far as they can go and now they will go the other way for 40 years. The ride is over, making money on asset inflation ( of any kind) is over. Time to get a useful skill or an actual productive asset ( mine, farm, machine shop) and prepare for the new/old world.

Seneca:

I’m re-building a machine to cut shingles and took a drawing to a good machine shop to get a steel Mandrel made. The owner looked at the drawing after about 5 minutes he says “about $800, but I can’t get to it for 3 or 4 weeks.” I said “how about I pay you $1200 and you have it ready next week.”

“Yes, Sir.” was the reply.

Population and land supply is a rationalization.

Broke is still broke.

Yep. If Americans can’t afford housing, then they can’t afford it, and prices have to come down to meet that. No amount of hand wringing about supposed housing supply or creative financing can get around the basic barrier of affordability, and the need for prices to match incomes.

Tent cities!,,,

Maybe not.

If a product is not affordable it may dissapear from the market. It depend on the price point where sellers no longer make money. Ok, existing housing can go very low, but not newbuilds.

As flee says, tent cities is one possibility, shack slums another.

The pricing of money has a large psychological variable to it. It can change rapidly as in a run on the banks The public’s faith in this Government is about done. Next will be America’s debt buyers. Every great empire collapses eventually and the cause is immorality based.

Interest rates and unemployment need to double from here to get a correction of 20 to 25%. As it is now it will be only a dip lower in pricing!

Not sure about that. In the comments after another post someone had run the numbers on how much the combination of a little higher interest rate on high prices do with monthly payment.

Now, the correction in prices do only come if enough have to or chose to sell.

Yeah, plus the effects of QT and the reverse repo market effectively draining liquidity. There are a lot of analogies for the Fed right now with what Paul Volcker faced so aggressively, but one difference is that Jerome Powell’s Federal Reserve has more options to tighten now besides just interest rate hikes.

We’re already at a point where the change in interest rate has caused the amount that can be borrowed to drop by roughly 25 to 30% for a fixed payment level. And unless the Fed gets their act together soon, rates will head even higher. Prices will correct accordingly, but the RE market is very sloooooow. Like a train wreck in slow motion.

“Prices will correct accordingly, but the RE market is very sloooooow. Like a train wreck in slow motion.”

True, we were talking about that on the other thread. There’s a lot of downward pressure on the ridiculous housing bubble home prices with how high they’ve exceeded American incomes, now that the Fed is no longer propping them up. But we kind of agreed that it’ll probably still be a while before US home prices truly correct to levels that are affordable. Maybe 2024 at the earliest, more likely 2025 or even 2026 based on the record from the 2007 and 2008 corrections. The one difference this time is that with the inflation monster running rampant like this for the first time in 40 years, the Fed won’t be able or willing to jump in with monetary easing like the last time. They’ve been burned badly by the excessive looseness of the past decade, and past 40 years in general.

Yep, so the house price correction is likely to run deeper and not be so heavily concentrated in “housing bubble states” like it was last time. (BTW I appreciated your comments on prior thread and replied there too.)

Yes. They were blinded by their own hubris, in that they thought their money printing had no costs, so why not? I think they were actually shocked to their core at how bad inflation got. That wasn’t supposed to happen! And now they’re stuck.

We’re in twilight zone = shimmies spent and now rising credit card debt,not looking good . Got the jet fueled up and ready to go

I feel like a lot of the comments are bipolar, one minute there is talk of hyperinflation and next there is excitement about house prices crashing. These are two things that don’t go together either you have massive inflation or you have housing prices significantly drop, you will never have both, outside of some localization. The reality might be inflation at 8% and house price growth at 0 and in few years the house price growth over the past few years will have been canceled out by inflation without actual significant price reductions. And if you see that as soft landing then you might just get that.

It depends. First, housing price is not part of the CPI. That make it possible with CPI inflation at the same time asset prices like housing fall.

Observe, the I in CPI is «index» not «inflation». The index measuring the rate of change in price on some consumer goods, CPI, measure housing only as rent or ovner equivalent rent.

Inflation used to be defined as expansion of the amount of money. CPI may or may not have a strong coupling to inflation and the strenght of coupling may differ with time.

Sum up, hyperinflation and housing price crash can co-exist.

It certainly can…

As the Fed fights inflation by raising rates, mortgage rates also rise…

Typically, outside of manias, there is an inverse relationship between mortgage rates and housing prices…

Mortgage rates up, housing prices down…

Throw a 8% mortgage rate at housing and see how fast prices drop…

Unless you’re older than around 50ish, you have no idea…

“…one minute there is talk of hyperinflation and next there is excitement about house prices crashing.”

Different groups of commenters. Not the same people.

This is more or less what happened from 1990 to about 1995. The median house price doubled in the 80s, then went flat for 5 years realigning value with price a bit. Interest rates dropped significantly during that period, kicking off the birth of the tech bubble and house prices resumed their relentless upward march right up to the GFC.

Your scenario has actually happened before, so it’s clearly a possible outcome amongst many.

My parents experienced this and I caught the tail end.

My parents purchased a house in S. CA for 50K in 1976.

By the time I was looking for a house in 1987, the price for this house had risen to 350K. This was during extreme inflation. Mortgages were at 13-15% and were up from the 6% my parents were paying. My parents did not pay off the loan during this time since LT savings accounts were paying 10%. Why pay off your 6% mortgage when government insured savings accounts were paying 10%?

Why sell your house with such an awesome 6% mortgage rate? Times have changed when 6% is not awesome but 3% has replaced this awesomeness.

The motivation to sell was low. The home prices and interest rates were rising. Sound familiar? Volume of sales were low.

The only reason this is different is that back then, investors were not speculating on rentals. My wife’s grandma bought the neighbor’s house at a low for some supplemental income but this was not widespread and certainly not with a 25% corporate involvement. The rest of her family was anti-rental investment due to the personal involvement with bad tenants. The Fed, with low interest rates and high rental rates has driven the speculation and the investment interest to all-time highs.

It is different this time. However, not that much.

It’s called stagflation, as in 3rd world country standard of life entering.

Incomes are increasing for many and pent-up-demand is building! When housing bottoms when banana-republic Jerome throws in the the rate-hike towel there will be a holy-moly housing buy-fest!

Nope on both counts.

I’ll take the “under” on your claim.

Sorry. Layoffs.

Listened to latest interview with Steve Hanke. He got inflation right in July 2021 predicting 6% to 9%. His model says inflation will average 6% to 7% in 2023. Hope he is wrong.

“In the US market, the bottom has fallen out in sales of homes priced below $500,000, which accounted for 62% of total home sales in June.”

I want to play devil’s advocate for some fun, so here it goes:

Did the bottom fall out or did all homes become generally more expensive? Per FRED: 20 years ago the U.S. median house price was about $180k and it’s now around $450k. Did the mix change, or did the majority of houses go up in price during that time?

Here in my pocket of CA’s Inland Empire, it really wasn’t hard to find an acceptable house under $500k a few years ago. Now there are basically no sales occurring in the 400s or lower here. Did the bottom fall out, or is it that there just aren’t any houses listed here in the 400s or lower in the first place? It’s not necessarily a change in mix, but it seems that the whole range shifts upward over time, chasing the lost purchasing power of the dollar.

In the last couple years, we’ve created way more new dollars at a much greater rate than we created new houses or new people to live in them. I would like to argue that the bottom did not fall out of the lower end of the housing market, but that the bottom fell out of the dollar.

A different market a different place.

When the banks where allowed to lend people 5x their yearly income instead of 2x the price of houses did go up the same amount.

The houses are still the same, just the price and the size of the loan have changed.

I agree, I think what we are seeing is the bottom falling out of the dollar combined the expectation that is going to fall more. See my earlier post. In order to see a major correction there needs to be reversal in expectations.

Yes. A true commitment by the Fed to protect the dollar would reverse expectations. But talking about rate hikes and QT without actually following through will not reverse expectations. That’s why the next 6 months are so important.

Yes. Note that they had to start the rate hikes off slowly in order to avoid demolishing the ginormous money-market-mutual funds. 0.25%, 0.50%, 0.75%… debating now 75 vs 100 to be next, tune in for the next episode of the show next week…

*Relative* Energy Security makes the US Dollar the best-looking horse in the Western Glue Factory at the moment.

Pretty sure the Treasury Markets are signalling the Fed taps out – or at least pauses – at 3.75% or lower.

@BigAl – Treasury market has no experience with stagflation and has been losing money badly for almost 2 years now. The yield-curve-recession-signal seems about right. But rates could go quite a bit higher. The 1970s is a better guide than any more recent history, and no one expected the rates of the 1970s.

All the houses on both sides of our ”block”, actually 3 statue blocks long, were built in 1950 all exactly the same size and only mirror images if any change at all; 726SF heated, no AC, as 2/1 ”winter cottages.” Two bedrooms, one bath was still the standard then.

As those and similar aged houses in this hood beyond our block reach true ”tearer downer” status – as opposed to ”fixer upper”, and many are for one reason or another, they are being replaced by two story houses of between 2500 and 3300 SF, though I think that may include the garage, not sure. Three bedrooms, two baths is considered the minimum these days, and many are up to 5 and 3…

Anyway, that is one illustration of the very clear changes in the size of houses, especially in the times of cheap money we have been experiencing.

As someone who has been involved with construction in various areas of USA from the 1950s, I am pretty sure there has been a relentless increase in the CUBIC footage of single family houses almost everywhere, even more so that the net usable SQUARE feet IIRC.

I agree. It’s dangerous to group your data by a variable that is not stable over time, and home prices have been anything but stable in the last couple of years. It doesn’t mean that the overall conclusion is wrong, though.

Not Sure,

“Did the bottom fall out or did all homes become generally more expensive?”

Look at the data over the past 12 months. So I’ll just repeat what I said below:

In reality, when you look at shifts as huge as those depicted in the bottom chart, amid the overall sharp DECLINE IN VOLUME — meaning FEWER homes are sold — but more high-end units sold and a LOT FEWER lower-half units sold, you see that this is in large part a shift in the mix of what sells. If this happened on steady or increasing volume, it might just be price increases.

I’m not the only one that’s seeing this. The California Association Realtors has been pointing that out for months — because it’s obvious from the data.

“ you see that this is in large part a shift in the mix of what sells”

Or is available to sell…

Same as the average transaction price with autos… kind of hard to to sell lower price cars when there aren’t any available…

COWG,

That’s precisely why I love the Case-Shiller Index. It ends this entire silliness, including this false equivalence with your used-vehicle nonsense.

We went through similar shifts during Housing Bust 1: at first the median price still rose and then only flattened because the high end was still moving, while sales at the lower end dropped, because owners of lower-end homes couldn’t sell their properties because market prices had fallen below mortgage payoffs. And this decline in sales at the low end kept the price declines from showing up in the median price for a while, and people were still denying the housing bust because the shifting mix kept the median price from showing the damage.

And then median price declines did show up. And then when forced selling set in at the lower part of the price spectrum, including foreclosure sales, volume rose in that end of the spectrum. But wealthy people pulled their higher-end properties off the market because they didn’t need to sell, and sales volume of these properties fell. As a result, the mix shifted dramatically toward the lower end, and the median price plunged a whole lot more than actual prices.

That’s why I’m not a fan of median price – I’m trying to explain it and explain what it means, and people just argue, and drag in some nonsense about used cars or whatever, because they don’t want to look at the underlying data.

And that’s why I love the Case Shiller Index which compares the price of the same house over time (sales pairs method). It nails price declines, and it’s not impacted by any changes in the mix.

But the CS is about six months behind. And I’m also not a fan of waiting six months for the Case Shiller to start showing the changing market.

Actually…

I was talking about the ATP referenced in your earlier articles about how they jumped to $45k or so due to the prioritization of the higher end more profitable vehicles… new not used…

And how the ATP was higher due to the lack of lower priced vehicles…

Same with housing… the housing available at $2-300k is microscopic and will have zero net effect on your C-S numbers…

Compare the index at 6 mos intervals back to Dec 2019 and you’ll see the difference… there’s a challenge for you…

A 33% rise in the index ( thereabouts) from Dec 2019 to summer 2020…

That measured an emotional/ psychological event..aka, FOMO…

So from a historical perspective, C-S is good info…

But not enough to stake your reputation on…

As Augustus Frost proclaims many times, you can’t deliver data on an psychological event today or going forward, but you can measure it looking backwards…

ATP = AVERAGE Transaction Price. “Average” prices are NOT skewed by changes in mix; they’re skewed by outliers. Very different from “median” prices, which are skewed by the mix. Changes in the mix skewing the median price is the issue here.

This is why your argument is silly, confused, and based on a false equivalence. It gives me a headache to even read it.

Wolf

CS Is far from perfect also. It is based on the sale of some mythical average house. People don’t live in average houses they live in real houses. Declines don’t happen across-the-board they happen differently in different neighborhoods at different price ranges in different locations with different updating on different lots in different ways. I follow a real estate at the micro level and have for 30 years. I know what prices are doing around me because I can look at a specific house in the county i live in and tell you how much the price has changed. More often than not it is nothing close to what CS would have you believe.

TheOldMan,

“It is based on the sale of some mythical average house.”

Effing ignorant BS. You go from clueless to cluelesser. I’ve been talking about this forever. I’ve linked the methodology many times, and you still spout off this BS.

READ THE METHODOLOGY:

https://www.spglobal.com/spdji/en/documents/methodologies/methodology-sp-corelogic-cs-home-price-indices.pdf

Inventory has been low for the last 3 years.

I suspect that is because people are selling their houses before they go on the market. The reason I suspect this is because we did it. Trashed houses do not go on the market. They are sold to investors and flippers behind the scenes before they reach the market. My Mom’s hose was outdated and somewhat trashed. We got estimates to fix it up to the level of her neighbor’s house sold 3 months ago. We decided to dangle the house at a price that subtracted the upgrade costs for a quick sale (Utilities, water, trash, property taxes (We canceled cable but could not cancel heat and water) were at about $500/month and the estimate to upgrade was 5 months so the clock was ticking.) We were offered the lowered asking price before it ever hit the market and was never recorded as being on the market.

My brother said: ” Now the new owners can paint with whatever color they choose instead of the blah Navajo White that we were intending and were quoted.”

We were a low sale according to the market but the availability was never recorded.

Now, how many more houses are actually going to market without this “Preferred Realtor” valve?

Around here, it is hard to find a house below 500K. I see the below 500K volume dropping for this reason.

There is still money out there to buy the 500K-1M homes.

Since I’ve Seen It All Before, this has been a historical excellent long-term investment. Long Term is key.

House prices may drop 20-30% from early this year but that only means they are flat from last year. The Fed has build a buffer and foreclosures should be small so their Bank Overlords should be happy.

Unless we go into a jobloss recession where people can’t pay their mortgages from 1-3 years ago. Then we will enter 2008 again until the Fed drops rates dramatically.

Faster than the piddly drops they did in 2008. Otherwise, BlackRock, BlackStone ,Integrity Homes will have a field day taking foreclosed homes off of Fannie and Freddie’s hands. If that happens, then we will become a renter nation.

The question becomes – what is the definition of “high-end units”? Is it square footage of the residence? Lot size? Something else?

I’ll use Massachusetts as an example. Right now:

* The market around Greater Boston has cooled just to the point that homes need to be listed. There is no room whatsoever for price negotiation and properties are moving quickly. The number of listings remains very low by historical standards. A large number of W. European buyers has emerged.

* The Mass market outside of Greater Boston has relatively more properties available – but they are not being listed. Despite that, they are on the market for longer and – for the most part – they are ultimately selling for prices that reflect a larger increase over pre-pandemic baselines than their Metro Boston counterparts. This – IMO – suggests are greater percentage of institutional buying

I used to dream about living in a $1M home.

Now, I am disappointed since my house has become a $1M home and it is not living up to my expectations.

Don’t be too hard on yourself Bob. The average American will be a millionaire soon. A loaf of bread will be $100, a cheap car will be $500,000 and we’ll all be dreaming of being billionaires someday. Maybe it’ll be cheaper to heat one’s home by simply burning paper dollars than buying oil or natural gas… Should make life a little easier for the low-income folks under the $500k poverty line.

I’ll just have to reset my expectations.

Billionaire is my new goal.

Unfortunately, my savings account interest will not get me there in time for my demise.

I understand the table in the “How a change in mix skews median price” box. But it doesn’t reflect the reality I’m seeing here in southern CA. The columns drop from 9 sales to 7 sales, and fair enough because sales volume is dropping in real life. But the #1 spot stays at $600k from column to column. What I see in my zip is that everything across the board shifted up in price. Sales of lower priced homes don’t happen anymore because there are no lower priced listings. My zip is pretty much filled with the same types of houses over and over again – all similar stucco boxes built in the last 20 years. The houses selling now are the same houses that sold in 2021 which are the same houses that sold pre-pandemic. The mix hasn’t changed. What happened here is the whole right column shifted up… The #1 spot didn’t stay at $600k, it moved up at at least $50k this year and everything below it shifted up proportionally. The 2 cheapest spots at the bottom fell off because there are 0 listings at those price points, not because the cheaper houses are sitting while the nicer houses are still moving. Around here, median price increased because all prices increased. The same has happened in another very different city an another state that I am keeping a close eye on.

How will that change in the coming months? I don’t know. And I can’t really speak for the rest of California, but I can say that the change-in-mix argument doesn’t explain what I’m seeing in the greater L.A./Inland Empire area at the moment. Perhaps the “all real estate is local” mantra is all too true and state-wide or nation-wide numbers just do a poor job of describing what’s happening regionally.

Some of what you say is definitely true. After all, prices have gone up. But there is now enormous downward pressure on prices because of the relationship between interest rates and loan amount. The people most affected by this are at the low end. Their purchasing power has dropped by almost 30%, which is huge. This is why Wolf’s explanation makes sense. You’re both correct to some extent. I think the main issue is that price levels are no longer supported by the amounts that can be borrowed, which is why the market has basically ground to a halt. Prices will correct accordingly, but it takes time.

Yes. Both. Lower end homes are taking longer to sell than others, 2 or 3 price reductions and then some of them drop out of pending.

The reason is lack of maintenance and a lot of structural damage. Many of them need more work than is worth it- a black hole, and also many of them have failing septics in rural areas. Flippers have painted over major problems in some cases. In rural Ca some of these homes have no electricity except for a minimal off grid system that is very old and failing. Some have no water.

Old time buy and hold local investors are throwing their worst homes into the market right now, the ones they lose money on.

The dollar collapse upcoming, waiting for foreign fiats to collapse first. Inflation from printing needs to default everywhere. Then you will see low housing prices again. Only a renter collapse can take down the mighty and rich investor/landlord class, so that way it must go. I remember looking at two-story track homes in Moreno valley for 150k in 2009, 10. We have multiples of more debt in the system ready to default this time around.

In regards to $500k homes, they aren’t making anymore Boise.

MW: Surprise! So-called ‘inflation hedges’ like real estate, gold and TIPS ‘are not performing as expected’ as those things just continue to plummet.

Is this the beginning of 1929,because this seems to be a global contagion

I would say yes. The central bank model of debt expansion on the current fiat dollar is beyond the ability of servicing under the current setup. Only Powell cheerleading holding it together now, but reality approaches.

Looks more like the beginning of 1923 to me.

On a RE forum I lurk on some of the investors are talking about shifting to privately loaning mortgages instead of buying properties.

At the beginning of what’s likely to be a big price decline?

I hope they are requiring 40% down payments. Also be interested to know what their exit plan is to unload this paper before rates “blow out” in the future.

Holding illiquid long-dated potentially under collateralized paper sounds about the worst fixed income speculation I can come up with, maybe slightly better than junk bonds.

Private money lenders we have dealt with in the past will only loan on a ”contract” that enables them to take the property without going through the BR or or courts AF:

It becomes a simple matter of contract enforcement, and usually in rural areas is, shall we say ”facilitated” by the sheriff unless both parties are ”family,” in which case it can get really interesting to watch.

Haha, IDK. There are all sorts of schemes. I can imagine someone co-ordinating it and making bank in fees before it falls apart.

It wouldn’t be a bad idea though if someone does have 50% or more down.

Yeah, plus what VintageVNvet said. There is a scheme currently where people sell a house owner financed and then repossess the property. There’s even a name for it- a “Lonny deal”. Named after some crook “guru” who “invented” it. I’ve seen people in this area do it, selling the same property over market rate and repossessing it several times. Pretty awful.

“There’s even a name for it- a “Lonny deal”. Named after some crook “guru” who “invented” it.”

Sounds like a good way to go dirt-napping. That’s the kind of major screw that pushes some people over the edge.

That «sheriff» part quickly turn interesting when there is large scale corruption. Not only family, but also other alliances and considerstions come to play. Like if you are local or not.

Ask China how shadow banking holds up for their private rich.

One thing I like about China is their wealthy fraudsters often become involuntary organ donors.

Add crypto to your list.

Wolf,

I understand that the median hole price will rise if the bottom falls out. But what I don’t understand is how you know the bottom is falling out versus all home sale prices continuing to increase across the board – which would also explain why there are fewer <500k sales. The lowest price bracket has a combination of sales dropping and homes moving up and out of that price range, so of course that share drops by the most. The 250-500k range still has houses moving out of the range but also a big share moving into the range from the 100-250k bucket.

The relatively low 2% rise in the $1M+ range I cannot explain and perhaps is what you see as the proof for your explanation.

This is how I am interpreting the data shown in this article, and others where you’ve mentioned the bottom falling out. I’m not trying to push an agenda and I’ve RTGDFA (multiple times). Clarification would be greatly appreciated.

Chicken and egg.

In reality, when you look at shifts as huge as those depicted in the bottom chart, amid the overall sharp DECLINE IN VOLUME — meaning FEWER homes are sold — but more high-end units sold and a LOT FEWER lower-half units sold, you see that this is in large part a shift in the mix of what sells. If this happened on steady or increasing volume, it might just be price increases.

I’m not the only one that’s seeing this. The California Association Realtors has been pointing that out for months.

1) RE collapse hurt more people than SPX collapse. The Fed try to rectify the frothy RE market.

2) 3.8%-4.3% Unemployment is better for employees than 3.6% unemployment..

3) China is interested to keep US dependent on Taiwan.

4) Putin interest to keep EU dependent on Russia natgas. He can squeeze them up to a point. He doesn’t want to lose his large European market.

5) We need a stable affordable housing.

6) Russia and Europe will need each other like a married couple after a fight.

Michael,

The notion that the Fed is *actively* trying to rectify a frothy RE market is empty talk – if not outright fantasy.

Cities and towns in the USA rely *heavily* on property taxes to finance themselves. Most did *not* re-assess housing values in 2020 or 2021 because they were getting generous State aid made possible by Federal pandemic packages.

But that’s over, cities and towns are now re-assessing properties and many homeowners are likely going to get ambushed by property tax bills that are 15-25% higher than two years ago. This will lead to delinquencies, and pie-in-the-sky default on muni bonds. The Fed makes plenty of egregious policy errors – but they are well aware of what dropping home values means for cities and towns.

I am looking forward to seeing the coming crash. For the last 20 years, my family and I have always been in the wrong place/situation (SF south bay area, household moves, multiple employer layoffs, etc) to take advantage of the bubbles and pops. Now that I have a much more stable job and am in a state and area that is ripe for long-term living, I’m eagerly anticipating the average house here (and everywhere) to crash quite a bit so I can finally lay down some roots.

The median price of a home here in Sierra Vista, AZ managed to spike 23% from last year to $282k (thanks Fed, you idiots!), and is up over 50% just from 2019. Truly a WTF moment. It now takes about 4.7x annual household median income of $60k to afford the median priced home in this retirement-type area. That is just insane for the area (though admittedly not bad for other areas of the country).

Good news is I’ve already seen a ~45% increase in the # of homes for sale just in the last 4 months that I’ve been tracking inventory. It’ll likely still be years before I feel it’s worth purchasing a home here, but it’s nice to know the reckoning is finally starting.

Be prepared to haul water, if any is available. Sierra Vista will be especially hard hit.

Good point to remind. A serious water shortage from climate change might affect housing and overpopulation.

Good luck to you in Sorry Vista.

Who the hell would live there in the first place?

Is the Intel School still at Fort Huachuca?

Ford cut 8,000 jobs because of chips shortages.

And just across the Mississippi river; a bit south of my home, the Ford factory from 1925, where Rangers were assembled until recently, has been demolished. Over 320 rowhomes, built by Pulte Homes, are the centerpiece of the new set up.

Ryan Companies, of the Twin Cities, got most of the rights to develop the 135 acre site.

Where autos and trucks were once made in Minnesota, we now have retail shopping, a skateboard park, 1,900 to 3,000 square foot rowhomes that start at around a half-million, and a few single family homes that are over a million bucks per. And a bigger Lunds & Byerlys grocery store.

The whole country could be covered with houses only before someone says…now where are the jobs. Time to think ahead. Better than before.

ME: Ford cut the jobs to fund their EV initiatives and the bulk is coming from salaried people.

Had an interesting conversation with one of my former associates at the auto company I worked at. He told me that new model vehicle launches are being delayed due to the overabundance of cat and dog parts left from the prior generation vehicle. The parts are not adaptable to the new vehicle (size differences and different pans/subframes) and there’s too many to digest into the spare parts business. Looks like things are getting even messier.

I’m seeing a complete standstill in neighborhoods I’m looking at in Washington state. Inventory is rising. Days on market is increasing fast. I’m seeing many houses going unsold and dropping off the MLS so they can relist again with a fresh listing.

When I do searches on homes that have sold recently, I see a very small number of them that were executed at 5-10% below asking prices, so discounting is well underway. Those sales above asking price are long gone. The most recent July sales were likely contracted in April/May, when interest rates were substantially lower, and things have only gotten worse since then.

Anybody who bought in April/May/June likely has buyer’s remorse.

In fact, I found one peculiar listing where a house sold and closed in June but was relisted for sale by the new buyer in July. I guess they realize their purchase was a big mistake and they are now trying to correct it.

At this time, anyone who bought in last few months seem like made a mistake.

After a year or so, it is possible, anyone who bought in last 2 year or so seem like made a mistake.

There are certainly more properties on the market in the Boston area than there were 2 months ago – but they are selling very quickly. Lots of buyers from the UK, France, Germany, Netherlands….even a few from Poland. The entrance of buyers from those geographies is very, very recent (last 6-8 weeks) – but it’s not hard to figure out the reason.

Here in the Mainline area of Philadelphia suburbs, it seems similar… a bit more inventory but the (non-dump) quality houses are still selling fast. I’m not sure what to make of it… Are some local markets going to remain hot for a while yet? Is the Philly area just generally not as over-valued as other regions, so not going to see the same drop? Is the crash coming, but just taking longer to show up here?

Global investors also got wiped last housing bust remember. Never be late to the party.

I’m also seeing what looks like game-playing on the MLS. Houses are being listed with a new MLS number, less than a month after the same house was listed under a different MLS number. Sellers must be worried about their listings looking stale. Buyers wonder “why doesn’t anybody want to buy this house?”

The new MLS number also gives the home advertising status of a “new listing”, even though it’s not.

I don’t pretend to know all the games realtors play with the MLS, but I assume these games impact the statistics to a significant extent and mask the damage being done in the housing market.

Are these re-listings being counted multiple times as properties available for sale?

I doubt that. I assume only one MLS listing can be active for any given home at any given time. However, I think the continual refreshing of listings under different MLS numbers impact statistics by underreporting the number of days on market.

If Redfin says average days on market is 25, maybe it’s really 50 once you factor in all the MLS gaming that occurs.

Nobody should be betting on lower house prices.

The price of an essential good is not going to decline when its replacement cost is rising. As I’ve been saying for years – house price inflation may well be lower than that of other sectors of the economy – but it will not disappear when the overall environment is highly-inflationary.

What do I mean?

* If you reckon your house’s value in terms of its worth in the number of USD – it will increase

* If, on the other hand, you reckon your house’s value in terms of its worth as a number of gallons of gasoline – it will decrease

There have been only four meaningful reductions in median USA houses prices for as long as the stats have been kept.

– A very small decline circa 1970

– A small-ish decline around 1980 when inflation was quite high but real interest rates began to approach positive territory

– A very short drop around the time Iraq invaded Kuwait in the summer of 1990

– The large-ish drop post-2008 crash

That’s it. No others. None. Zero. Zilch. And only one of them (a small one) occurred in a meaningful inflationary environment.

The pipeline of new homes will be narrowing very quickly and there are lots of perspective buyers from Western and Central Europe who have begun to enter the USA property market (three guesses why…)

You don’t understand economics or markets.

Prices are not determined by cost of replacement, but by how much people can afford to pay which in this case mostly means afford to borrow.

If the customer base can’t afford your product, it’s irrelevant how much it costs to make it. You’re going out of business. It’s irrelevant if it is a necessity. With real estate, people who can’t afford to buy or rent will double or triple up if necessary.

Your history lesson is also incomplete. Only the GFC resembles the current market, because it was part of the same asset mania. 1970, 1980, and 1990 weren’t a bubble or mania.

Also depends upon what market you are talking about. Some markets or neighborhoods within a market will do a lot better or worse than others. Concurrently, people pay their mortgages with nominal currency units (dollars or otherwise) usually from wages, not inflation adjusted.

Anyone buying a home who is able to keep their job or has enough liquidity if they lose it will come out ahead (eventually) but a lot can happen to real estate prices between “here” and “there”.

I was talking to a close friend who is a custom builder in New England – he builds those fancy shingle style manses along the Long Island Sound on the CT side.

I asked him what he was doing and he said he just finished building a chicken coop for a friend of his and is now working on a raised platform for his dog to sleep on when he’s out in the barn.

His phone has pretty much stopped ringing and what bids he does toss out are only quoted for labor. Materials? He tells the client to “leave his wallet on the countertop and he’ll take only as much as he needs”. The example he gave was for cedar shakes (siding) for the homes he builds. He said a few years ago they were $500 a square. Now they’re $1,800… subject to change without prior notice. A doug fir stud is about $7.

He built his house in the woods…. has tillable land, chickens, horses, and can heat his house and hot water with both oil (which he says is about $6 a gallon at this time) and firewood (wood burning furnace – not stoves). He had some of his laborers splitting logs to put up for the winter. In his opinion, people haven’t seen nothing yet. Imagine buying 300 gallons of heating oil every two months at $6 a gallon during the long New England winters. Even he winces at the thought and can’t imagine how the average Joe is going to afford it.

Home construction is *DEAD* in Greater Boston.

The great pandemic home remodeling is over. It’s a lot easier to get a contractor on the phone than it was 12 months ago…

…just don’t ask him to give you a quote in writing.

Lumber Mills did not add capacity when the Pandemic lockdowns died down and they are rapidly cutting capacity now. As we’ve seen with oil refineries – that capacity may be lost for good.

Famines start when people can not afford food. Neccesary or not, if the custom base can not afford it, they do not get the product.

This have been seen several times in Africa. First the market for food seizes, then people go hungry and die. Prices of food may not rise that much when this happen.

Famines start when there is not enough food – which affects prices.

When there is a famine, food is rarely sold in market conditions because – if available – it is claimed by force and not purchase.

When inflation reaches self-catalyzing levels – replacement cost is *always* a factor in pricing.

If you do some digging, you’ll find that existing house prices in Argentina are appreciating at 35% despite the overall transaction volume being the lowest since the late 1980s and that 40% being significantly-lower than the overall inflation rate of 65%.

New home construction began to seize up last summer. It’s deader than the proverbial door nail up in Boston. It’s significantly-lower than the post-2008 and (even worse) – the 1989-1991 era when Massachusetts underwent a very severe recession. We’re still seeing near-10% annual price appreciation in Boston as of June; i.e. the market has barely cooled.

Know what? Doesn’t matter. Institutional investors are trying to unload dollars and they don’t need financing for these purchases and we’ve already seen over the past two years how few buyers are needed to sustain significant price appreciation. And – at least in Metro Boston – we’re seeing a new cohort of buyers enter the market from Europe. Now housing crash yet.

Lance Roberts said it best with regards to houses and cars.

People buy payments.

Payments.

When the rates went up along with home prices, it was like getting a sledge hammer in the forehead.

Demand started drying up quickly. And initially homes were held off the market, hoping for improvement. Too late…seeing price cuts in the SE.

And supply (IMO) will increase when reality sets in.

Similarly BA, there have been some very very deep dives of RE prior to 1970, AND it appears possible that we might be in the early stages of another and possibly deeper dive now. Only time will tell us that, eh?

Considering that grandpa sold for $2K in ’42 the house his dad had built in La Jolla for somewhere around $10k, and my dad had to sell the farm and one house cheap and cheaper to keep the house we lived in around ’56, and we don’t even want to talk about what RE in FL was selling for after the crash of that market in ’29, eh

BigAl – also note that no one lives in a “median USA house”. All housing is local. National averages conceal a lot of local variations.

The 1990s decline decimated property values across Southern California, which lost a ton of aerospace and other high-end jobs due to the “peace dividend” after the Cold War wound down.