California special: Pending sales collapse by 30%, prices begin to “moderate,” San Francisco condo prices decline year-over-year.

By Wolf Richter for WOLF STREET.

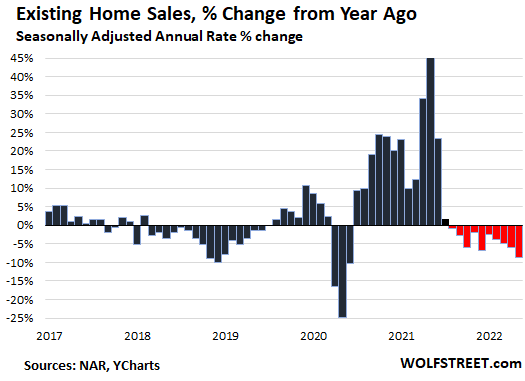

Sales that closed in May of previously-owned single-family houses, condos, co-ops, and townhouses fell by 3.4% from April, based on the seasonally adjusted annual rate of sales, and by 8.6% from a year ago, the National Association of Realtors reported today.

Sales of single-family houses alone dropped by 7.7% year-over-year. Sales of condos and co-ops dropped by 15.3% year-over-year.

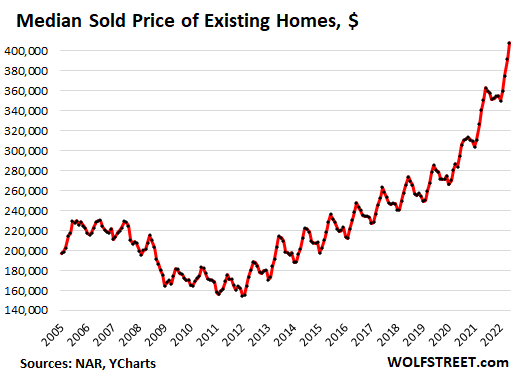

May was the tenth consecutive month of year-over-year declines. The old saw that there’s no inventory for sale is no longer an excuse because supply jumped 12.6% in May – so sharply falling sales on sharply rising supply (data via YCharts):

“Further sales declines should be expected in the upcoming months given housing affordability challenges from the sharp rise in mortgage rates this year,” the NAR report said.

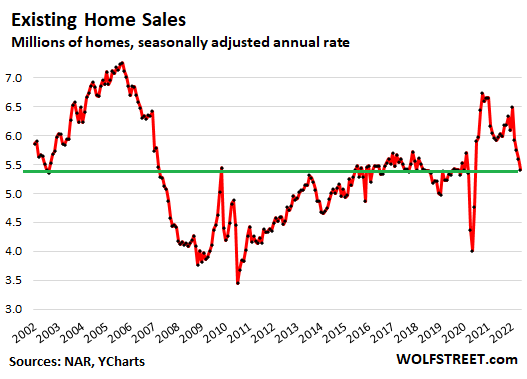

The seasonally adjusted annual rate of sales in May fell to 5.41 million homes, the lowest since the lockdown sales rates (data via YCharts):

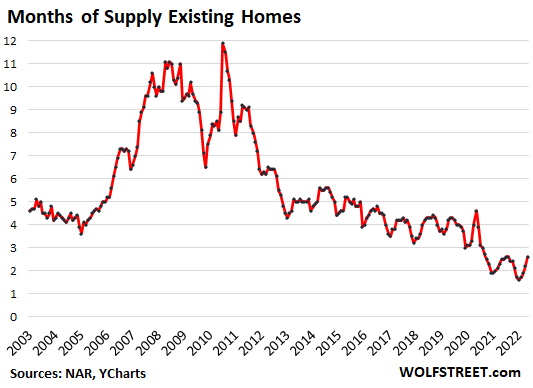

Inventory for sale and supply jump.

The number of homes listed for sale in May jumped by 12.6% from April, or by 113,000 homes, after having jumped by 100,000 homes in April, to 1.16 million, the highest since November.

Supply of homes listed for sale jumped to 2.6 months, from 2.2 months in April, and from 2.5 months in May last year, the first year-over-year increase since the lockdown. This is quite a change from the low in January of 1.6 months (data via YCharts).

Sales by Region.

Percent change of the seasonally adjusted annual rate of total home sales in May from April, and year-over-year (yoy):

- Northeast: +1.5% from April, -9.3% yoy.

- Midwest: -5.3% from April, -7.5% yoy.

- South: -2.8% from April, -8.4% yoy.

- West: -5.3% from April, -10.0% yoy.

In California, closed sales plunged, pending sales collapsed.

According to the California Association of Realtors (CAR), sales that closed in May of houses plunged 15.2% in May year-over-year; and sales of condos plunged 12.3%. These are closed sales.

Pending sales – a predictor of closed sales the following month – collapsed by 30.6% in May, “likely due to eroding affordability, rising mortgage rates and home prices, and the increased risk of a recession,” the CAR report noted.

Holy-Moly Mortgage rates.

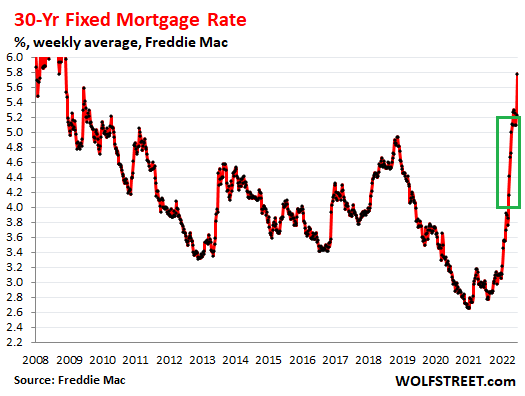

The average 30-year fixed mortgage rate spiked to over 6% last week for the first time since 2008, according to the daily measure by Mortgage News Daily. According to the most recent reading by Freddie Mac last week, the average mortgage rate spiked to 5.78%.

These mortgage rates are so named because “holy moly” is what people say when they look at the mortgage payment for the ridiculously inflated price of the home they want to buy.

But sales that closed in May are based on mortgage rates of the prior month or two, when they were much lower. Until mid-April mortgage rates were in the 4% to 5% range. In May, mortgage rates were just a little above 5%.

It’s in June, when the spike took off with renewed vigor, and we haven’t seen much housing data on June yet, except that luxury sales in Manhattan plunged by 70% year-over-year in the week through June 19, but that was mostly due to the sell-off in the stock market.

The closed sales in May are based on deals that were largely negotiated in April, with mortgage rates from April and before, when these buyers applied for mortgages and obtained mortgage rate locks that are good for a set period of time. The green box shows the mortgage rates that roughly applied to home purchases that closed in May, around 4% to 5%.

Median Price pushed up by shift in mix to higher-end sales.

In California: The median price rose to $899,000, up by 9.9% year-over-year, according to the California Association of Realtors. But the median price is sensitive to changes in the mix, and according to the CAR, this price increase in the state “can largely be attributed to the mix of sales, with the high-end market continuing to outperform the more affordable market segments.”

The change in mix show up in the share of million-dollar homes, which jumped to a record share of 35.3%, while the share of homes priced below $500,000 hit an all-time low.

“Home prices could be leveling off though, as the monthly gain in price appears to be moderating,” the CAR said. And this is already happening in San Francisco.

In San Francisco, the median price of condos fell 0.3% year-over-year. The median price of single-family houses in San Francisco rose 6.1%, the second lowest gain of the big counties in California, behind Contra Costa county (East Bay), where the median house price rose only 1.0% year-over-year.

In the US of A: the median price rose to $407,600, up by 14.8% from a year ago, according to the NAR. And here too, as we’ll see in a moment, there was a huge shift to the higher end (data via YCharts):

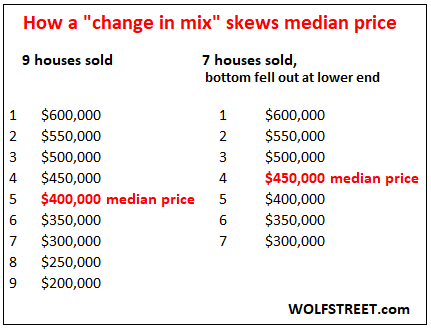

The median price is skewed by changes in the mix.

My favorite illustration: To get the median price in a market where 9 homes sold, you list them by price from the highest to the lowest, and the price of the fifth house from the top or the fifth from the bottom (same house) is the price in the middle = median price.

But if the two cheapest houses don’t sell, and if the remaining seven homes sell, the middle is now the fourth house down, or the fourth house up. This change in mix skews the metric of the median price, though the actual prices of the homes haven’t changed:

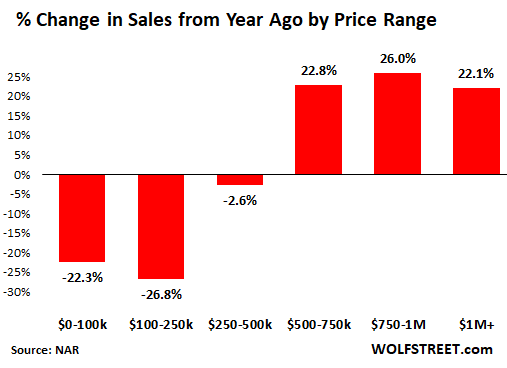

This change in mix is what happened in the US too.

Sales of homes priced below $500,000 have plunged, while sales above $500,000 have surged year-over-year, and these dramatic changes the mix have skewed the median price upward, according to data from the NAR:

Investor share of sales and all-cash sales dipped, but stayed in the same range.

Individual investors or second-home buyers purchased 16% of the homes in May, down from 17% in April, 18% in March, 19% in February, and 22% in January, according to the NAR.

“All-cash” sales, which include many investors and second home buyers, declined to a share of 25% in May, from a share of 26% in April, but were up from 23% a year ago.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It’s not different this time.

It NEVER is!!!

I never paid attention to mortgage rates

I HAD to buy 3 houses – 1031 exchange

closed on 1 in march and 2 in april

all cash, 100% free cash flow

and rented at market rates

The game is the same … only the sheeple getting fleeced are a different generation, sporting a full “coat” freshly-printed credit, ripe for the wolves to harvest…

Amen. It is an organized fleecing. Right on WS!

Actually, it is. Given enough pressure, there WILL be rent & mortgage forbearance in the mix again. People act like it was the sub 3% rates that caused the final spike in the housing bubble over the last two years.

Hogwash! In large part, it was the rent & mortgage forbearance that stopped a full tip into a recession, resulting in a free for all to push home prices up rather than down through foreclosure.

It was always has been rates. It’s always will be rates.

It is both. Low rates increase demand by increasing the pool of eligible buyers. Forbearance and moratorium decreased supply. When demand increases or supply decreases, you tend to see an increase in prices. When both happen, you can get a bigger increase.

Supply, demand, and price are pretty basic concepts. In real terms, prices are almost certain to go down. The only question really is what happens to nominal prices because inflation might soften or hide the blow, if we see a lot of wage inflation.

Home buyers rarely make their decision on fundamental value, they buy based on what the banks will lend them. Homebuilders don’t build like they are an opec cartel, they build based on profit expectations. Inouts for building going down suggests new supply won’t nearly be cut off as much as some think.

It was a free bridge loan for “someone I know”’ selling a house in IL with $14,000 property taxes and buying the same size/age/condition/3x lot house in IN for less than half price for cash, latter with $3000 property tax.

False dichotomy. “Forbearance” is/was/will-be mathematically equivalent to converting all mortgage and rent debts to adjustable rate loans, all adjusted to 0%, for some period of time, then returning to the prior contract levels.

Never let sophisticated economic language get in the way of the financial substance!

Mortgage rates are INCREDIBLY LOW at only around 6.00%, so just what are any imbeciles whining about regarding mortgage interest rates?

I agree they are low but I guess it all depends on your perspective. My mortgage in 1972 was at 7.5%.

My first house was in 1976. I begged, borrowed, and stole to get enough down payment to assume the old 1973 mortgage which had a 7.5% rate. Five years later I looked like a genius, except I bought in Decatur Illinois. In 1982 I was laid off and Decatur was one of the top ten unemployed areas of the country.

I also lived/live in Decatur,IL. I moved there in 1982 and bought my first house in 1984 with a 12% mortgage. So 6% is nothing.

My lifetime of mortgages:

8.0% – Conn. house 1976

18 1/2% – (Calif. move – 1981)

10.0% – (refi CA mortgage)

8.0% – Ca 1986 (new house)

8 1/4% – Texas 1994

6.5% – Refi Texas house

Now in the paid off house….until the bitter end!

Looking back on all of this is it more satisfying to live in a more modest paid off house or in a flashier or bigger house that is mortgaged?

@Dan: In my experience, paid off wins every time. Peoples’ needs vary, though, but we’ve never been this content.

Anthony, you can also have a glorious end too – if you want ; )

Dan, none of my houses were bigger than 2,500 sq. ft. and that was plenty big even with two daughters. The home we are in now is 2,000 sq. ft. for the two of us. A modest house with a small or no mortgage worked for us.

We had no desire ever to get a huge place with a big mortgage. But we always looked at a house as a home and not an investment.

I did buy a 2,000 sq. ft. brick ranch in 2011 for $62/sq.ft. (thank you sub prime fiasco) and deeded that to my daughter and her husband.

been in a relatively modest 1 story 2232 sq. ft for 25 years. i would not be in the financial situation i am in if i had not sat in it and paid it off. i was able to hold investments longer term and assume risk that i probably would not have with a bigger note or more debt. granted, i put down 5 percent and took out an 80% note and a 15% note to buy a home and paid off the 15 in 3 years. plenty of months and years of living paycheck to paycheck mixed in 25 years, i read “the millionaire next door” back in the 90s when it came out and it was great for someone trying to break the poverty cycle.

But the dollar was stronger and your spending power higher in 1972. Average income was ~11k in 1972, now $100 in 1972 is worth ~$700 today. Average house was 27k. Adjusted for today that means average income was about 77k.

Average cost of a house now is ~$425k and average income today is approx ~$70k. Obviously need 2022’s numbers, so that is one obvious obstacle to my point.

Simple way to put this, the cost of an average house is about 15x greater than it was then, when average spending power is actually down a little bit (if not in line with taking 2022 numbers when the come) with income then. That more than accounts for the difference in rates from the 70s to now, in my opinion.

$183/mo in 1972. 20% of total income using above numbers

$2548/mo in 2022. 43% of total income using above numbers.

To be fair though, some homes are larger than the 70s though, but it doesn’t change the fact of average and what is available.

average home in 1981 was 68,900 and average income $22,400.

Mortgage at 18.5% as posted above is $1067.

That’s a whopping 57% of income for 1981. Glad you didn’t drown Anthony!

In today’s terms, it would take approx 11% interest rate to hit the same percentage of income as Anthony had in 1981.

But when the housing market corrects, then 6% wont look too bad.

Wolf is better at this stuff :)

And your home adjusted for inflation was much cheaper. In fact, the median and average mortgage payments were lower too. The real judge is your monthly mortgage.

Prices and cost of living at all time highs, still increasing in middle TN, wages sideways, impossible for 1st time home buyer without an inheritance. In 1972 were prices at all time highs and monthly payment 120% of avg house hold income for avg home?

“Mortgage rates are INCREDIBLY LOW at only around 6.00%, so just what are any imbeciles whining about regarding mortgage interest rates?”

Not when you combine it with the most ridiculously priced homes.

The homes *became* insanely overpriced because,

1) The G has destroyed interest rates for the last 20 years (to “fix” the economy!) by,

2) Printing money backed by nothing other than DC expertise/wisdom (!), creating

3) The illusion of home affordability as gutted interest rates offset/drove the sub-moronic escalation of homes prices during the worst macroeconomic setting the country has likely ever faced.

GDG!

Not to worry, your Corporate Salvation is just around the corner.

You are correct that it is still low, but housing is at a historic high.

I’d rather pay a 9% mortgage on a $50k home back in the 70’s then a 6% mortgage on a $450k home today.

As DC ZIRP Bubble #1 showed, they ain’t going be $450k houses for long.

At today’s semi-honest mortgage rates, a tiny fraction of potential home buyers can qualify in underwriting…the only fix (other than “Return of ZIRP 2 – The Re-Re-Screwing”) is for SFH list prices to fall dramatically.

Otherwise…no sale…just SFB carrying costs…forever…

Wolf said Blackrock was buying unfinished subdivisions and putting up SF designed especially for Build to Rent……zero SFB carrying costs!…..proving PE corps may even be better than public corps….probably why they are disappearing fairly quickly, anyway.

Relax and enjoy the coming salvation from GDG!

OOPS! My bad. They went public in 1999. It’s rare for a corp to make mistakes (like the GDG), but they must have run out of money for their original business plan.

I guess some useless money wasting branch screwed up, but I’m sure was promptly closed.

I agree. My parents paid $52,000 for a house in Cerritos, CA, in 1976. The house next door, slightly smaller at about 1450 sq ft but very similar, sold for $1 million a couple months ago. I’d rather pay a reasonable price and higher interest rate too. But $50,000 to a million shows how absurd real estate is in CA.

CA RE IS ”absurd” far shore rojo:

But other places are catching up at least somewhat lately, that’s also far damn shore!!!

Our 900 SF house in the saintly part of the TPA bay area is now allegedly worth FOUR TIMEs what we paid for it 7 years ago,,, and all or almost all the others in our ‘hood the same or similar…

NUTSO,,, AKA ”’HOLY MOLY MR. ROLY POLY”’

We remember well the last crash when a couple waterfront houses – absolute fixer-uppers both, were listed at $885K in mid ’06, then went to auction in ’09 for $225K…

Hope for all the young folks who actually NEED a home that exact scenario happens again,,, and the sooner the better!!

and BTW, the ”feeling” of living without rent or mortgage is the very very best, and I encourage all to do their best to pay it off asap.

VVNV………….”and BTW, the ”feeling” of living without rent or mortgage is the very very best, and I encourage all to do their best to pay it off asap.”

Well stated, and those who get this done will sleep better at night and be less stressed.

When comparing historical rates, yes 6% is not high. But at today’s valuations, 6% is high.

You’re right rates are still historically low but that means nothing at all. The market gets used to certain rates lets say 3%. A lot of debt is issued at those rates. Therefore, if the cost of debt rises it will have very negative effects for anyone who is dependent on those low rates. For example anyone who did a cash out refi at 3% and is now trying to sell their home in a 6% environment may have a difficult time paying off the original loan since people can’t afford the price (in monthly payments) that the homeowner would need to pay off their debts. This happens all over the place in diffrent ways but the point is that historically low doesn’t mean low enough to avoid serious pain.

I think the guys with huge mortgages at 3% bitching about inflation are not thinking things through. You WANT inflation, just like you want a boatload of SFR zoning, fruity environmental laws protecting insects over people having roofs over the heads, and nimby multi-family development.

If I had 8% inflation when I had my student loans at 1.65% interest, I would have thrown a party.

Right on Nate. Inflation destroys debt.

The bigger the debt the more the destruction.

If you can hang on to your property, of course.

Inflation doesn’t destroy debt. A higher income due to inflation destroys debt as long as the income gain outpaces price increase in consumer staples.

6% mortgage rates are normal when the interest on passbook savings accounts is 4% and credit card rates are at 9%. No need co be name-calling. That’s immature.

Extended ZIRP contributed to suppressed mortgage interest rates, far too long too low. These extended low rates are the “holy-moly” for me, not the current more historically typical rates. We’re finally getting back into the low end of the range we previously had for decades – the low end of the range we had for decades i say. If i was a betting man and i am, i would venture 6-8% will be prevalent going forward. So we’re going up from here.

“Holy moly” is what people say when they look at the mortgage payment at the current rate and price.

Key is …and price. Money ain’t for nothing and your chicks for free!

but in this day and age, I really don’t want my MTV

“Holy moly” is what people say when they look at the mortgage payment at the current rate and price.”

Agree except that they may add a word between “holy” and “moly” that starts with an “f” and ends with a “ing”.

Hi Wolf

NBC bay area.com has some interesting reading.

“The monthly mortgage payment on a typical home in the Bay Area jumped more than 50% from a year ago, soaring to over $9,000 in San Jose and above $8,000 in San Francisco, according to a report from Zillow.

The online real estate marketplace reported Tuesday that housing affordability across the nation is at a 15-year low, adding that buying a typical U.S. home at the current average mortgage rate of 5.78% would mean monthly payments of $2,127, 51% higher than a year ago.”

Maybe Biden can eliminate the taxes on property just like gas? /s

We’re just returning to absolutely and perfectly normal mortgage rates that are still on the lowish side, so why any complaints or hesitancy at all in any of the real estate markets?

Obviously you’re rich

Because prices are very, very, very, very, very, very, very, very, very, very, very, very, very, very, very, very, very, very, very, very, very, very, very, very, very, very, very, very high.

“Because prices are very, very, very, very, very, very, very, very, very, very, very, very, very, very, very, very, very, very, very, very, very, very, very, very, very, very, very, very high.”

That’s what happens when mortgage rates are 2.5%.

6% is pretty darn healthy.

Now let’s see some prices come down.

The convention is no more than 35-42% of your net income as mortgage. I make $158K a year. This equates to $2900-$3400/month. For a 2000 sq ft home, prices here start around $700K, which with today’s “low” 6% interest rate, and 20% down is about $4200/month. To require 2 people making that much money having to work together to afford a single home is beyond a dangerous indication of an imminent fallout.

Loss of one job would sink that boat.

Yes, sir. Something’s gonna break when higher earners are uncomfortable with the mortgage on an average home. Not a luxury home; a typical home. And there are people with less means spending that much. Good luck to them.

It’s simple arithmetic! To buy the same house in 2019 compared to 2022 is a little over 2.5K a month. When interest rates went low the cost to buy/build a house is high. They just haven’t come back down to normal prices. The question is will they ever?

No one’s going to take that bet Mr.Falcon, we’re already at 6%. The fed just hiked the fed funds rate by 0.75% and several more hikes scheduled along with QT.

Damnit Harvey I was hoping you would take the action!

Look at the demographics.

The whole world is going Japanese.

US pop growth of the working age is NEGATIVE. Last year total pop growth was 0.12%. And the US looks v. good compared to most developed countries!

There is ZERO % chance that the US household sector can bear 6-8% mortgage rates long term without tipping into recession.

There is a HUGE bullwhip effect that will see goods inventories drag massively on growth next couple quarters. With that will also come a downdraft in business capex.

Housing construction as a % of GDP is at all time highs when pop growth is at all time lows. Equals MASSIVE overbuilding probably more egregious than early 2000s when factor new homes vs new people to fill those homes. Prices went up because housing demand is PROCYCLICAL both for renting and owning (think people living by themselves rather than roomates, people owning vacation homes etc). US has more homes under construction than any time since 1973. I.e. when pop growth was >3m per year not 0.5m now.

In fact it is almost certain that the US (alongside UK and EU) will be in recession by end 22 if they are not already in a modest technical recession this quarter.

Only decent investment currently is US T’s. 3.2% for 10 years at a time when the Fed, ECB and other CBs are just about to plunge the economy into a HUGE recession is an absolute gift.

It’s continuing to get worse. Here’s California data updated daily from active MLS reports

Active/pending ratio has gone from 1.24 on May 31st to 1.61 today driven by both a 7% rise in active listings and an 8% drop in pending sales – those are big numbers for only 3 weeks, especially as pending deals should be rising due to seasonality.

In only two months, priced reduce listings went from 14% to 26% and there is no slowdown in this trendline.

A $875K loan (the average home sale price in Los Angeles) has gone up by about $1000/month (from $4300 to $5300) on principal and interest alone in just three months. It’s even worse in the Bay Area given higher prices.

Few months ago I thought 6% rate would bring the Market to a sudden halt but apparently still not high enough to shock the market let alone halt it.

This may take a long time to play and if the fed keeps rates high beyond 2023 we may actually see a substantial price decrease in prices.

Ghassan,

RTGDFA

None of these sales happened in June when mortgage rates hit 6%.

You need to get the timing right.

Pending sales in California in May: -30%. That’s based on deals made in May, when rates were in the 5% range.

The national sales = closed sales in May for deals made in April mostly, when mortgage rates were much lower.

We don’t have much data on June yet, when the rate hit 6%.

So be patient.

ALL THIS IS EXPLAINED IN THE ARTICLE.

Yes. 60 day locks average. Thus you have 40 plus days left until you see current sales at 6 percent plus rates

I understand what you’re saying wolf but still even for 5% there is a lot of activity, my assumption was that people see it coming and step back when rates were 5% and the housing market halts completely at %6 considering current prices.

But I was wrong, maybe buyers started to step back as you mentioned now that the rate is 6% and it comes to a halt when rates are 7 or 8%. I definitely hope so.

No one should buy a house in this environment, and I mean no one even if they have the cash.

And I always read the article.

“No one should buy a home in this environment”

The only people that think so read wolfstreet and zerohedge. Poll 100 realtors and likely have 90 say it’s a great time to buy a home before rates go up even further. And it’s the realtors that normies rely on for professional advice when purchasing a home.

Relitters .. and I am using the pegorative.. can be the worst!

I swear with My Own Eye they have forked tongue.

Misfit, I think the sentiment about it being a bad time to buy might be really widespread. I recall a big survey finding that… It might have been the U Mich survey. I’m going on memory here… might be mistaken.

Socaljohn,

Yes, very widespread…

You know things are seriously bad when even Fannie Mae is using “WTF”! ;-)

Prices are falling now on a m-o-m basis. Just like they are in NZ, Australia, Canada and basically every western market that got a pandemic boost.

Just the stats for the US are total garbage. I mean corelogic publishes DAILY indices in Oz and NZ. US publishes case schiller which is 2 months delayed and an average of three months prior. A joke.

The daily price indices in Australia are fiction. I looked into those years ago, and I covered them at the time. Housing is too slow-moving with too few transactions to come up with meaningful daily indices. Every house is different, and in a different location, and prices vary from house to house for those reasons. Those daily indices are just concoctions made by algos, similar to the Zillow Zestimate.

Monthly indices are more reliable, but still not very reliable. It’s very difficult to get pricing data that actually shows price changes, not other factors, such as changes in the mix of houses that sold.

The Case-Shiller in the US uses “sales pairs”– meaning it compares the price of each house to when the same house sold previously, so it tracks actual price changes. But yes, the disadvantage is the long delay and the three-month average. Another huge disadvantage is that it covers only 20 metros.

Yeah that’s my assumption too, apparently 6% rate and a $1M mortgage is no problem for a lot of people around here…or at least on the surface that’s the case. If you compare median price sold to median wage, that gap is pretty comical.

Why would anyone care in the least? Don’t worry. Be Happy! It’s only a tiny little bit more money!

It’s hilarious that families earn $80K in SoCal while houses are going for $950K. The writing is on the wall, again. It’s just a matter of when.

Don’t underestimate how misinformed many buyers are. Many families have zero financial knowledge in the household. They read an article from the NAR and they think buying a home today is a great idea.

There are so many platitudes circulated by the pumpers, the average homebuyer has no clue what is really going on.

Lots of people will buy at every RE top.

You are absolutely right bobber.

ButBut NAR .. CAN

Thus Family saved!

Bobber,

People do learn, if slowly.

The home sales volumes in Idiotic Bubble #2 were only 50% of those in idiotic Bubble #1.

By the time the Fed re-soils its pants and launches Idiotic Bubble #3, maybe only 25% will get suckered in.

This is a good point. I feel like some commenters are a bit smug and assume that Americans are big idiotic overgrown children with negligible intelligence.

I think many people actually do learn from experience and progress through life, such that yes many have resistance to bubbles.

Of course younger people and the older ones who didn’t learn may have lessons coming.

My brother works as a loan officer in home building and while it’s a narrow sample set there is a constant stream of desperate would-be buyers trying anyway they can to squeeze out down payments that work on absurdly overblown home prices. Granted the stream has moderated in the past month. But they are still there, barking at him over the phone. If an opportunity presents itself in the future to permit debt well above 2.5 times income at record low rates the torrent of applications will resurge. Though lending standards have tightened in some respects (albeit not really in others), a debasement of monetary policy, fiscal policy, or even said lending standards will unleash the tempest. While biased and jaded, I’m of the opinion that most buyers have absolutely no clue about real estate, and they have good reason to given the precedent established for the past 20 years. It’s not that they are stupid. Most people have to specialize in their lives and cannot or chose not to devote time to a hobby such as financial literacy. Or have external forces such as marriage, health, divorce, etc. dictating their home purchasing. He can’t even get anybody to lock a rate right now, that’s how convinced would-be buyers are that rates will drop. It’s so bad that the company has a large facility at a locked rate just to mitigate the turmoil and spoon-feed their future buyers, who they know will refuse to lock. But to their credit, why wouldn’t they expect rates to drop any second if recent memory prevails? They sure as heck do not pay attention to FOMC meetings I can deduce that much. Sound monetary policy pre-dating the 2000s? That’s for losers.

That is a possible explanation for the mess we have now… anecdotally when I talk to (generally we’ll educated) people they are utterly unaware of any dark clouds brewing. “Housing always goes up”. I think these beliefs in the population delay price adaptations for some time until economic forces become overwhelming.

A whole lot of REALTORS(TM) are going to be jingle mailing the keys to their Lexus lease now that the punch bowl has been taken away. Perhaps they should learn to code.

Unfortunately for most families, even if prices fall, they probably won’t be enough to compensate for the increase in mortgage rates, so the cost of housing will remain elevated.

I can remember a time when selling real estate was a side hustle.

My teacher friend just quit ,to become a realtor ,nice gal but terrible job change .Wished her luck

This is when a lot of smarmy sales people learn that opening a door and saying here’s the kitchen isn’t really a high paying skill set.

“And this very special house has a…bathroom! You better hurry! There has been a ton of interest!”

I’ll never forget the time my cousin sold a ONE BATH house for $1,200,000. That’s, like, the achievement of a lifetime.

It wasn’t even near the beach. You’d have to spend a full hour driving through LA traffic and finding parking.

Give it time, a lot of coders are going to get the boot as well.

AI coding for mundane tasks will be along soon enough.

There is a ton of what I’d call pointless jobs that could all disappear tomorrow and the world would be fine.

Ie, pension comms hehe

Funny, I do AI coding for mudane tasks. The problem is industry is scared to adopt it, and costs to get the pro-simple builder is the cost of a coder. The time you pay someone to assemble on the builder is high.

I offer my services with my employment to amplify my effectiveness.

That the median priced home is up 150% in ten years (160k -> 400k) is a stark visualization of the disgusting econo-centric, centrally-planned, corporatized, materialistic Amerika. Truly despicable.

S&P 500 Dec 30th 2011 = ~1257

S&P 500 Dec 30th 2021 = ~4791

380% for the markets over that time… I’d saying housing hasn’t kept up! Or maybe the Fed has pumped too much into the stock market! Take your pick! Bottom-line… money ain’t for nothing!

While SP500 is still overpriced, it’s much lower now than at ATH.

S&P 500 3,764 after today bear market rally : -)

It’s actually about 280%. You need to subtract the initial value from the final value before dividing by the initial value to calculate the return percentage ((4791-1257)/1257*100=281). Still better than most real estate in that time period, but much closer.

Thanks… missed the subtraction of the original price level. Interesting comment though, is there a correlation between the stock market run up and the price of housing?

Main point being that people don’t need to raise families, make memories, sleep comfortably, etc in the financial markets.

This is a good point. Never thought about it that way.

More than *anything* you mentioned, Idiotic Bubble #2 is a measure of DC’s ZIRPed willingness to destroy the economy in order to “save” it.

People have always been materialistic, but DC worked 20 years to empower the most moronic at the expense of the most prudent.

Yes, absolutely. Those prudent with their wealth have been taken to the woodshed while those who went along with the debt-slavery program have been able to indulge ANY superficial desire.

So who wins? The banksters duh.

Tim r- those are a few of my favorite things about the United States. forgot domination of the worlds money exchanges and ownership of the best reserve currency that is necessarily more flexible than Gumby and Pokey. It’s no wonder people are falling all over each other to emigrate from this veritable hell. Can’t even get enough pilots to fly refugees far from our inhospitable shores. Oh, the humanity. etc.

You may not like the US, but it’s easier for someone who wants to make a better life for themselves and their families to do it here than in most of the world. It’s been that way long enough to establish staying power among societies, a solid valuable physical base of constructed infrastructure, and a populace of productively employed citizens. Naturally house prices reflect the increasing valuation of any capital goods in a vibrant, long-lived market economy. How much they go up is less indicative of anything of significance, as inflation as well as location makes real estate a multivariable equation. The trend matters. The attraction of Wolf’s charts is instant trend comprehension, at least to me, probably because it’s all I understand. Percentage can just be a show and tell number, and judging from recent comments about percentages changing depending on which way the discreet numbers are moving and the resulting changes in the percent base, there appears to be room for confusion. Besides, things are cooling off already in some areas. As soon as people start leaving their cards at home and their wallets in their pockets, prices should soften quickly.

Seems logical to figure that cash buyers will become a higher percentage of total closings — but the median prices will be lower too, right?

Cash buyers are NOT stupid. They don’t want to overpay either. And they can see what’s going on too. From the article, last section:

Investor share of sales and all-cash sales dipped, but stayed in the same range.

Individual investors or second-home buyers purchased 16% of the homes in May, down from 17% in April, 18% in March, 19% in February, and 22% in January, according to the NAR.

“All-cash” sales, which include many investors and second home buyers, declined to a share of 25% in May, from a share of 26% in April, but were up from 23% a year ago.

I think that’s what I was trying to say (but I didn’t express it well). My theory is that *even* as prices fall, fewer people will be able to obtain or afford mortgages because of the accompanying economic effects — so more (like 40-50% of) transactions will be cash deals.

I happened across a story in bloomberg or WSJ that said all cash in March might have been well over 30%.

What it did say is many buyers used companies like Better.com to make it look like a all-cash but Better.com makes the borrower pay something like 2.5% extra on the loan. They interviewed someone who used better.com to make an all cash offer

Also, it said many cash buyers sell all their stock….or borrow against their 401k to make the cash buy and then soon after take out a home equity loan for liquidity.

——————————————————

From better.com

Make your best all-cash offer

Once your mortgage has been fully underwritten and pre-approved, it’s time to determine your bidding amount and submit your all-cash offer. Your Agent can help you navigate this process, but as a cash buyer you’ll have a number of things working to your advantage. For starters, all-cash offers typically have a quicker closing period—the time between when a purchase contract is signed and when the sale is finalized—which is very attractive to sellers, especially in hot markets. The Better Cash Offer program also allows buyers to waive financing and appraisal contingencies, which gives sellers more confidence. Buyers who are also trying to sell their home won’t be stuck having to pay multiple mortgages or adding in a home sale contingency.

Step 4: Move in and buy back your home

After your offer is accepted, Better Real Estate pays cash for the home. You can move in as soon as Better Real Estate closes on the sale, and live there while your mortgage is processed. Once your mortgage is finalized, you can buy back the home from Better Real Estate at the original sale price.

This will soon become one of the sleezy characteristics that gets cited as evidence of the latest housing bubble after it collapses and the masses are looking back in horror.

@ru82: Interesting, thanks for posting. I wonder whether the state and local transaction fees have to be paid on both ‘sales.’

@SocalJohn: yep.

“According to the California Association of Realtors (CAR), sales that closed in May of houses plunged 15.2% in May year-over-year; and sales of condos plunged 12.3%. These are closed sales.”

This is why it’s good to look at macro level data to draw conclusion rather than anecdote evidence. If I go off anecdote, wouldn’t have notice any major shift in the market other than seeing some price reduction here and there but the last min FOMO buyers still somehow buying houses close to $1M in SoCal, often listed for less than a week or two, at least based off listings I have saved.

Still wondering where the heck these people are coming from? Do they truly believe in RE agents one way truth of good time to buy? Next time, I see one, I am going to ask them when is it not a good time to buy? Interest rate is low, sky high price, good time to buy. Interest rate has since doubled, sky high price, still good time to buy….

Btw $500K for the bottom end? I think you can buy a closet for that much and nothing else, at least in the somewhat desirable part of town, even undesirable part like Lynwood is still asking in the $700K and up…insane..

Phoenix_Ikki,

California pending sales: -30% in May. That’s that activity in May.

Closed sales in May, which you referred to, reflects activity in April.

We have no sales data on June, when rates hit 6%.

Hey Wolf. I understood your last two comments when I RTGDFA.

Ok got it, so perhaps over time, I will likely see less of these anecdote listed then under contract / sales pending even in my neck of the wood. That’s good to know, I do still expect to see certain demographics still buy now if they qualified regardless of sales/price trajectory. Looking at macro data both sales pending, inventory listing, price reduction…etc all point to a pretty fast reversal even for housing market timing standard.

“$500K for the bottom end” is obviously not meant to be a local Los Angeles number.

Just for fun lets say you’re in CA and you need a 30yr fixed mortgage. Last year with mortgage rates at 3.5%, you monthly payment would be $2,694. Right now at 6% your monthly payment would be $3,597. Lets say next year mortgage rates are up to 8%. Your monthly payment would be $4,402. Then you add in property taxes and homeowners insurance and holy moly.

This could be quite a show!

Sorry I forgot to add that these numbers are based on a $600,000 mortgage. I need to start reading my posts before hitting send.

And don’t forget the Mello-Roos. It is California you know.

And qualification criteria roughly means that 3% requires $9000 per month income. 6% requires $13,200 not counting Taxes & insurance.

600K Doesn’t even buy a crappy condo out here. Need 750K or 1.1M for a SFR

For the complete recipe, just add no *water..

*unless you’re a pupfish, or a Deadpool owner .. or both!

Mushman,

If only the payment math could have been done *in advance*!!

But as we all know, the Realtor Foresight Impossibility Theorem states that no interest rate can exist other than the *current* interest rate.

So math is physically unable to function in advance.

The change in median price since 08 can been viewed via the fact that credit was shut off to only the most credit worthy plebs and has only been flowing to those most worthy or with other assets for collateral. When i worked at BNY Mellon (not the best example because of their clients) they were only extending Jumbo loans and some of the people were using their stocks and such as collateral. Wake me up when those people get cut off from the credit spigot.

I don’t see the point of your post. You state BONY clients aren’t representative (which is true) while at the same time claiming mortgage credit after 2008 was cut-off to all but the credit worthy, which isn’t. Unless of course, you are only referring to the jumbo loan market which is a minor fraction of the total since 2008.

If you are commenting generically, mortgage standards since 2008 aren’t even close to being strict. For starters, borrowers frequently make down payments below selling costs with the MBS buyer relying on a government guarantee, which in turn is supported by currency debasement and asset inflation to maintain loan quality.

Spoke to a realtor that insisted now’s a great time to buy a home. When asked their thoughts on high interest rates, they reminded me of the interest deduction: “You’re not really paying 6% since you deduct all the interest.”

This bubble is far from being popped. We’d need 9% rates before home prices even begin a meaningful drop in the highly desirable areas.

“You’re not really paying 6% since you deduct all the interest.”

Yeah isn’t that funny? Except i have to pay taxes on the 10 bucks in interest i earn on a savings account. Its almost like the system is designed to discourage savings (freedom) and promote debt (slavery)! But not conspiracy, just the best and brightest leading us into that way too bright future.

Ha, “The System”

Obvious issues, should be re-engineered.

Drop income taxes. Stick to transaction taxes.

Much better inflation constraints.

It is amazing how debt becoming “normal” has caused people to think debt is good. Heck, people even BRAG about their debt these days like they’re some genius for paying out six figures in interest on their low rate mortgage. Sometimes they even brag about having two mortgages on two properties, as if that’s a smart position to be in.

“Debt is normal. Be weird.” – Dave Ramsey bumper sticker

It’s amazing how many financially illiterate people think that a “deduction” is a dollar for dollar write off against your taxes. It’s value depends on your marginal rate, so it will be about a third in the best possible case. And don’t concern your self with that pesky standard deduction, which is running about 25K for a married couple :)

If I hear one more rube say “I did it for the tax writeoff” I think I will have an aneurysm.

Yes the actual benefit is about of 1/3 of the interest amount beyond the $25.9K standard deduction. Not a calculation that FOMO buyers are performing of course, they gotta stay focused on winning the bidding war.

I *did* have an aneurysm.

I did it for the tax write-off…

I doubt it will take 9% to pop it, but that’s just my opinion. I think the more important factor is time. RE is an incredibly slow moving market. My guess is that the soonest we will see declines in yoy statistics is this fall, but I saw one report from a realtor in socal saying the decline has already begun when viewed on a quarterly basis.

We haven’t seen the impact of 6% rates yet. Patience! We’re barely seeing the impact of 5% rates.

I’m kind of excited, Wolf.

I would like to ask a realtor under what scenarios is it a bad time to sell.

When it’s another agent getting the commission?

Even the Titanic took three hours to sink after an iceberg ripped a gaping hole across its bow. Don’t be listening to the band; get to a lifeboat.

@HD – That’s great – love it!

No impact on prices in so cal but I see sellers inspirational asking price being reduced.

I think it’d get accelerate in the NeXT few months.

Peak home buying season is upon us. Let’s see

Terrible time to be a realtor. Crocodile tears…

80% of Realtors may have sold 1 or 2 houses last year. Most are already starving.

My bad. Mea culpa. Shouldn’t pick on ’em.

Apologies to all the realtors on WS.

What realtors?

Oh, SocalJim.

Worse time to be a mortgage broker?

No more easy refi’s.

What’s crazy is that some NNN properties have seen no drop off at all!! Just saw two new Chick-fil-A’s go under contract at 3.50 cap rate!!

It’s not supported by any data like Wolf puts together, but down here in my neck of the woods, the San Jose/south Bay area:

I’m seeing homes going on the market for prices only attainable 6 months ago.

I’m seeing dozens of homes up for sale in neighborhoods that had only one or two homes for sale, just a month ago.

I’m also seeing homes in San Jose proper in the 800k-900k range. That’s something I haven’t seen since 2019.

Homes in the 1.5-3 million range are taking some big price reductions(not all of them, but there are many). I’m talking 200k+ price deductions.

And the best part? I’m not seeing much of any sales. Nothing is moving, we just get more and more inventory everyday as people run for the exits.

This is what happens in a Bubble. People buy, buy, buy but they don’t sell or they buy second, third investment shacks.

So you have shortage, shortage, shortage, then GLUT!!!!

Everyone is trying to time the market to sell at Peak. The problem is when it’s peak and going down, it’s too late. Yall missed the boat!

You’re exactly right. I watch the market pretty heavily in my area, and it’s amazing how many wishful thinkers there are at the moment. It’s amazing how brutal the monthly payment numbers are now as well.

What I find fascinating is being surrounded by $3 to $5 to sometimes $10 million dollar homes, but the average and median incomes in my town are like $130k/year. These people are all bubble riders. Very few earn high six figure to seven figure salaries. Who would have ever thought that $130,000 salaries wouldn’t support $5 million dollar home prices?

Every time a citizen gets into suicidal debt, a Fed employee gets his wings..

@cas – Nice!

We’ll have to see how fast the knife falls this time. Some day it’ll be faster because of technology, but who knows. Who knows if it’ll even fall. Things have been weird for a couple years now. So refreshing to start seeing some sanity return to the markets.

I’m really hopeful Turtle. The income to affordability ratio has been so out of range, for so long that entire generations of young-ish people (myself included) are a lifetime of non-home ownership. Just sad. Financial repression is the term I believe.

Yeah on my street the (nice) house next door with space in the back house for a tenet sold for $800k maybe 5 months ago?

The house a few doors down, a total POS doesn’t even have landscaping and is smaller with no additional tenet housing just listed for… $1m.

Sorry folks, but that train left the station last fall. Can’t wait to watch the $25k reductions coming in every week for 6 months.

Hi John, I’m looking in the Bay Area including near but not in San Jose (e.g. Los Gatos, Saratoga). What I find strange is that the house prices in the last 6-12 months went from $2M to $3M without fail. If you look at the Zestimate chart, you can see the numbers creeping up from $1M to $2M over the last 10+ years and then suddenly a large spike to $3M. So now the house are being listed at $3M, then have a big $300k price drop to $2.7M but are still 30+% more than they were just 6-12 months ago. I don’t understand the spike at all. I think even the 2021 prices were crazy but this recent spike makes no sense. Can anyone explain it?

The one thing that will have an effect will be increasing inventory. Given the tech stock/IPO issues and the extreme prices in the Bay Area I think this is a setup for a correction. I see that some sellers are coming in at slightly lower prices now but not nearly enough. Give it 6 more months…

Josh,

Yes, what’s happening in and around Los Gatos (my home town) is that people think their homes are worth 6 months ago prices. Peak mania prices. Yeah it’s a nice place to live, but a house just down the street from me went from 4.3 million asking, to 3.6 million after just 2 weeks on the market. It’s still at 3.6 million.

Interest rates are the killer here. At 3%, if a tech couple put down 1.5 million from the sale of their old home, it’s do able, not cheap but do able. At 5-6% interest the monthly cost after putting down 1.5 million goes from 10k/month to 16k/month, and that’s just not attainable, for the average tech couple.

Also Zillow and their “Zestimates” are just plain wrong.

To answer your question, the 2020-2021 run up saw tons of IPO/crypto/stock money move into nice south bay homes. It absolutely obliterated the market here, punching prices up another 30-40% from their already insane prices. I expect this to change massively as we enter recession.

From the Intermountain West, in my tracking of some non-resort towns that had little construction in the last three years, the prices are being reduced by a nominal 5-10% in the under $500K market, a minor concession given the increases in recent years. A few more contracts are falling through. Houses sit longer. My realtor is bending over backwards because there has been little inventory since last fall and the flippers are gone. I have heard the same from realtors in my current town because they don’t have millionaire clients for the high end. Brokers will generally take the big money clients for themselves, so newer agents need a lot of luck.

While it is all a game, I laughed at just being told that an April appraisal ordered by a seller should still be good for my bank. Someone else did bid nearer that appraisal, at a price above all comps since January. One credit union here loans at 50% DTI without counting insurance, HOA, or taxes, with 20% down required. I truly believe lenders like that drive up prices across the board locally. Of course the appraisal will come in right.

I agree with the comment that most buyers playing right now are not well-informed, at least where I look. The workers are still buying their maximum payments on lower-quality fixers. These towns got hit hard in 2008-2016, when they weren’t even the bubbliest locations, but there are more retirees buying now. Unemployment is low, all services, government and extraction. I’m still optimistic about increasing pessimism.

1) The 30Y Fix Mortgage rate reached : 0.886 with the 2008 high. It’s going to be very volatile. Mortgage rates might drop to 2012 lo/ 2013 highs, to 3.3% – 4.6% area.

2) Bear market rally #1 : sideways : 2018 high was > 2013 high.

3) Bear market rally # 2 : a sharp rally a zigzag up : from 5.8% down to 3.3% – 4.6%, before rising to 7% – 7.5% area : (5.8% – 2.6%) + 4% =7.2%.

Why would the biggest run-up in history not be followed by a crash? [confused emoji] R to TGDFA that’s what I say all night all day. Hold dat cash den make dat switch, listen to my words and y’all’ll be rich!

Here in formerly red hot sequim on the Olympic peninsula, RE has been stopped cold as of about three weeks ago. Still some obvious cash sales But my Zillow daily updates are now 50 to 75 percent , price reductions. Window has slammed shut

Will the costs of building a single family home decrease as inflation starts having an effect in the 6 – 12 month term? Will lumber and associated materials prices be affected?

Yes, eventually. It will take time for material prices to come down though. Everyone will fight that as long as possible. The steel mills will first have to lower prices, then the distributor, then the fabricator, then the contractor, etc. Just one example. We do sell and fabricate steel for residential & commercial. Our costs have not come down yet.

I should add we have not seen any competitive pressure YET.

I’m a weldor/fabricator/engineer, and what we pay for steel plate is out of control right now. Hopefully it comes down soon.

Lumber prices have already plummeted 50% this year and are continuing to plunge in the US and globally.

Always did during my 50 years as cost analyst/estimator DEL.

Certainly remembering one project that had some costs almost double after 4 weeks of preparation, then fall almost that much during the year it took to negotiate the final contracts/specifications, etc., (“Design-Build” project.)

Must keep in mind this was inflation/deflation of construction materials/equipment, including from dirt to final finishes.

I just saw a house a block away from my house sell in a week for $230,000 over asking [10% over]. For what it is worth.

I was talking to another realtor at an open house pointing out that a lower price but a higher interest rate might not be as good a deal as you think. Even with the price drop you still might end up with a higher monthly payment.

Since everyone agrees that interest rates are going to be going up for the next year to year and a half that fear may still push the housing market along and slow any big drops. The buyers might be thinking that a 6% rate now is better than an 8% rate in two years. Plus you can always refi that 6% loan if rates drop again. If we have a recession what will the Feds push rates down to?

Sure wish I had a crystal ball.

U in new your or California,that’s crazy

Just outside Redmond WA 98053. My daughter [98052] had a house go up for sale, owner got a tech offer in FL. Two weeks, no offers. Owner pulled it off the market to do some upgrades/repairs. Before they could put it back on the market they got an offer to rent for $9000 a month from some corporation that needed short term housing for workers.

Two year lease? Don’t know.

If we have a stagflationary recession, which many expect, rates will have to remain elevated. It is quite possible that we will never see the ultra low rates again in our lifetimes. Just look at the history of rates to see how long the cycles can be.

Well, considering the debt-to-GDP ratio of the US is as high as it is, default/dilution risk premia *should* be higher for a long, long time.

And it would have been for the past 20 yrs, had not the Fed traded ultimate inflation for temporarily lower interest rates, by buying up the Treasury’s engorged debt paper using unbacked money.

“If we have a recession what will the Feds push rates down to?”

So, they screw around and create inflation. Then, they try to stop inflation by raising rates. A recession happens. Now they lower rates to juice the economy but cause more inflation which perpetuates the recession.

Rates ain’t coming down any time soon, no matter what, if you ask me.

Basically only folks with cash are going to benefit from what’s probably coming. That is, the rich get richer. Still, there’s room for some of the more patience little guys to get a leg up.

You’d have a bad case of FOMO if you couldn’t wait a few months to avert a potential home buying disaster.

Well, that’s what I thought in early 2020. A pandemic! Pity the fools who just bought. But, then the unexpected happened? Prices blasted into the stratosphere! But maybe now, finally, a correction will occur.

Salado Tx smaller market bedroom community on I35 45 min. N of Austin.

In 2021 homes sold in 1-2 days with sometimes zero inventory.

Nephew bought a new home from DR Horton Nov 2021 contract with finished home closing on June 8 2022. Street has about 50 homes that had sold 95 percent but not built. Nephew reported that at least 5 folks of the 45 sold homes have backed out. The homes are 3000 sq feet and sell for 550k to 600k. More anecdotal evidence of slowdowns.

How much do those people lose when walking away from a new construction like that?

Talked to several folks who walked away from their deposits on new construction waterfront ”condos” in FL in last crash PG.

All said they ”made out” much much better by buying either in the same project or nearby for less than half what had been original price.

Watched a specific project with many buildings stopping at half or so of their approved height.

Many ”builders” and subs went BK, and even heard a couple of ”developers” had to go that way — of course with the developers it was just the corporation that had been set up for the project that took the loss,, no personal losses for developers from what I was told…

Lots of people have SADS and others are no longer able to work. Obviously a drag on buying. Mechanically.

Anyone notice how the grain commodities got hammered today. Good news for future food prices.

A lot traders take profits at the end of June halfway through the year. It was probably profit taking by the ones long.

I really continue to be entertained to see what happens in the cities in terms of metro and inner city stuff. Then it wasn’t so funny.

Then it came to the “sticks”. People wanting to get out of the city, a retreat for the big crash and burn or just a twice a year cabin started buying land in this far rural place. The price per acre has gone nuts. The country tax assessor and commissioners are beside themselves with the windfall. Needless to say our assessed value has gone through the roof WITH NO ADDITIONAL SERVICES. Nothing, Nada.

We must be RICH now! What a joke. This is a paper chase with unrealistic valuations which will never go down. But the county is having a blast for the moment.

6 says build on our street since about late 2018. 1st one sold for about 260k, with #5 at 360 .. I think ..

Lucy Abode #7 has siding/roofing completed, contrator appear to be trenching for waste/sewer to street, with stuff happening indoors. Sells through a prefered reagent. I have no idea where he’s at regarding the ‘markets’ etc. and as to what price said unit will unload for.

I hope that things don’t unravel for my new(ish) ‘neighbor’s. May they be buckled up, and ready for a plunge on but one Society’s Rollercoasters. I perceive things getting rather hinky going forward. “Weeeee!”

‘says’ should read sfh

Rollercoasters are fun! Except when the track has alot of flaws and the cars end up going airborne. Even then, it kind of feels like flying for a bit. Hey look, we’re flying, aren’t we amazing?!

Is this the calm before the storm, or are home prices still rising? What is a 0-$100,000 home? Is that a small Airstream trailer? The larger ones are over $100k. Lot not included.

There are cheap fixer uppers in some of the rust belt cities of Ohio. They are listed on the realtor web site.

A double-wide mobile home on a private lot is the new aspiration of the working class — even the middle class. They are very livable, but do not age well.

Down the road from me is a 20-year-old one for sale on 1.86 acres of land and with a shared well (four families tied to the same well). Asking price of $499k.

Having completely gutted and rebuilt 2 of them.. They are much more difficult to work on than a regular house. Plus very few tradesmen want to work on them for any price, especially plumbers and electricians. Anyone buying one best be handy..

Viewed a 1987 doublewide on a super tiny lot a few weeks back. Had soggy & uneven floors, doors/windows didn’t close, nothing updated, on blocks, rotted decks, HOA fees over $700/month not including utilities, water or septic. $230k. Such a deal.

*And*…you get to pay monthly lot rental, forever. At rates only the mobile home community landlord gets to decide.

Not so much a home as a hostage situation.

Kinda like homeowners’ relationship with the local property taxing authority…

That sounds fairly typical of my experience ”inspecting” older mobile homes/trailers Lily, with many even worse.

Codes and subsequent quality changed a ton after hurricane Andrew in August of ’92 showed how really really vulnerable mobile homes were — along with many changes to all the building codes too.

Would NOT recommend buying any mobile home older than ’94 when the new codes went into effect,,, but also better be very very aware of old houses in FL for the same reason, clearly shown by newer houses OK, older ones next door flattened by Ivan and subsequent ‘canes.

Houses built in the period of approximately 1970 when most labor went from hourly employees to ”piece work”, are relatively the worst,, until ’94 when codes and especially enforcement of codes changed due to Andrew.

VintageVNvet, I looked at one several months ago that was a 98 I believe. Never maintained, roof leaked and the tenants may have poured cement down the toilet before they disconnected the sinks and tub and let water just run over the floor. The floor, roof underlayment and exterior siding were all some sort of particle board. The thing had basically melted in large areas except for most of the framing.. It’s pending now. Haha, I hope the buyers know what they’re getting into.

The old ones generally all need all new electrical and plumbing, but at least the floors were built out of plywood and the siding is metal.

1.86 acres? Hey, that’s better than the 0.05 acres of asphalt you get in SoCal.

One theory. House prices are about 30% of CPI. Even if the supply chain is screwed and other prices go up – a dip in housing alone will be enough to level out inflation and the Fed can go back to being mostly dovish without having to solve for anything. Just sell the MBS and scare rates up for 6 or 7 and on paper your work is done.

House prices are not included in cpi. They use something called owner’s equivalent rent.

Interesting thought…why is housing CPI weight only 30% if bank underwriting

is allowing 40% of income to go to housing costs?

Shouldn’t that make housing’s CPI weight 40%?

Even worse, there are certain “flavors” of CPI that weight housing only 20%

No because only some people who are just in the process of buying are paying 40%. Others are not borrowing up to their limit, others have had raises since they took out their mortgage, some have paid it off, others are renting or paying nothing (living with parents etc.). So the average share of housing in consumer spending is well below 40%.

US 10y minus 2y = 3.27 – 3.20.

Adjustable rates will play more and more into loan decisions as inflation peaks. PCE might bavk off but 30th, Seemed 1993-5 was similar rates with folks using 11th dcoa and libor

1) The Dow futures daily, the downtrend channel, L1 : Jan 5 high to Apr 21 high. // L2 : a parallel from Feb 24 low.

2) Today green bar touched L2 from below and was instantly rejected.

3) Fri June 16 close was the lowest close in the last 6 months, since Jan 5 high, a setup bar. June 17 low was a trigger. In order to cont down, there must be a lower close under the trigger low. June 17 trigger reached Feb 1 2021 low. Jan/Feb 2021 was the congestion area low.

4) Today fractal low is a signal that the Dow might hop above L2 and move higher, inside this channel.

There’s a few new listings in my area that seem to be much lower- but still too high for what they are. Fewer sales, more inventory.

a townhouse across the street is sitting for over a month. They cut the price 200K already. OTOH the starting price was 1.2M. Last time it was sold in 2020 for 720K. This is a pricey area (98005).

I hate to sound like Lawrence Yun on this website in particular, but 1.2-1M for a town house in Bellevue doesn’t sound ridiculous actually

Especially if it is a decent size and recently/well built, I don’t know…

built in 1990. 2 years ago 720K also seemed overpriced to me…

Good. I think the large majority of americans would like to see housing costs drop significantly.

If the AirBnBs of the world were outlawed, how would that affect housing affordability? No impact, or would it make a difference?

The question is, for the USA, are fewer people this year going on vacation(I think yes?) and will the AirBnBs flood onto the market as well…………probably is the answer, especially if they borrowed to buy

A better money making idea than AirBNB for those who can possibly get permits through- is building new campgrounds in vacation areas. The campgrounds everywhere around me are chock full.

Most private campgrounds have a central public bathhouse, coin operated showers, a coin operated laundry room with WIFI. Electrical and water hookups for some spaces. Nothing except a picnick table for other spaces as tent sites. RVs renting hookup spaces pay more. Gravel road and site parking.

Maybe 1/6th the infrastructure, if that, for almost 1/2 the rent of a AirBNB for a full hookup RV site.

Buying an older one usually doesn’t look worth it though..

Anecdotal: we live in a ski town where STR buying has driven prices up 200+% in four years. The total number of STRs is way, way up, nightly rates seem to be dropping because the market is flooded, and traffic is way down from the last two summers. Taxes are doubling as well, and if this winter is slow, I think we’ll have a bloodbath.

I think it would make a difference in most places, at the margin which is where prices are set.

Homes bought for AirBnB remove local supply, as the vacationers using it aren’t living there which means there is less supply for those who do.

Not sure about Wolf’s example of “how a change in mix skews median price”.

It’s true that if the two cheapest houses in a group of 9 priced from 200 to 600K don’t sell, the median price goes up 12.5%, from 400K to 450K, even with no overall price change.

But who’s to say that’s what’s happening? If all 9 houses actually go up by 12.5%, the median price also goes up 12.5%. And since the cheapest houses go up with the rest, there are fewer houses sold below any given “cheap” price.

To really show that the bottom end of the market is being disproportionately affected, you would need to see sales volumes over time on the same actual houses, not just sales volumes on a given price band of houses.

“But who’s to say that’s what’s happening?”

From the article, sales by price range:

1) There are more houses between 100K and 500K than 750K and

above. Their weight is important. The saving rate might be falling because owners of new houses had to fix a lot of stuff, at peak contractors prices. In the last two years transaction costs, interest, taxes, insurance cost…and repairs, for new owners, might be higher than price increases.

2) A project engineer interviewed a young software engineer. His

asking price was higher than her salary. That might explain why

there are so many job opening.

Hi Wolf,

Thanks for responding and yes, I did notice the graph.

However, say for a simplified example, we assume that below 100K houses are the cheap end of the market and above 100K houses are the dear end of the market.

And in year 1 we have seven houses sold at 60, 70, 80, 90, 100, 110 and 120 K.

Then prices go up 20% across the board in the next year.

The same houses are then re-sold, but this time at 72, 84, 96, 108, 120, 132 and 144K. There has been no change in composition, and no failure to sell houses at the cheap end of the market. All the houses have been sold both times, just with a 20% increase in all their prices.

But we still see the same effect as in your bar graph, because sales in the “cheap” below-100K range have declined from 4 to 3 (a 25% decline) whereas sales in the “expensive” above 100K have increased from 3 to 4 (a 33% increase).

See what I mean? Just taking sales by price tranche doesn’t prove there has been a failure to sell whichever houses happen to be the cheapest, or a “change in mix” as presented in your table. It could just mean that, due to a general price increase, there are fewer houses left to sell in what price range is considered “cheap”.

To prove a change in mix, you would need to first index your thresholds by the general increase in prices, and only then compare the number of sales in each band in periods 1 and period 2.

Wolf is spot-on that we haven’t seen the impact of 6% mortgage rates yet.

Not only are May sales data reflecting April mortgage rates, but people are still today walking around with locked-in mortgage offers at April and May rates. They see asking high prices, but they know that if they don’t buy now they will have to get a new mortgage offer at 1-2% higher than the one they have in their pocket. So a lot of them will make an offer on a property at 5% or 10% under the asking price while they still have access to that cheap mortgage; and buyers, if they have any sense, will accept it.

But this won’t last for long. As soon as rates stabilise for a couple of months – say at 7% – then every potential buyer will be facing that rate, and interest-rate FOMO will evaporate, to be replaced by a near-certainty that prices will fall. That’s when volumes will really dry up.

I’m getting ready to buy a house in two years!

Expecting that RE will be at least 20-30% cheaper, but in

this wicked world there are no sure things, except, Death

and Taxes!

Bargains are no bargains if you don’t have the funds ready

to pounce. Let the lemming be lemming and support your local

Fools’ Club, where passive investors make a killing without some MBA financial wizards hovering like vultures from above, trying to scam you out of 1-2% of your nest egg.

Saw the same thing in 2018 during Fed tightening

-Longer days on market

-Supply increasing

-Higher rates

-Lower ReFi’s

What followed?

More money printing, lower rates and far higher home prices.

When the Fed offers ultra low interest rate loans to Blackrock, Blackstone and Invitation Homes to cash out bid all the plebs paying 6% on a 30yr fixed, it’s an engineered wealth transfer. Home prices will not materially drop because the Fed always protects friends of the cartel.

Back then, inflation was BELOW the Fed’s target, and the Fed could U-Turn. Now inflation is MULTIPLES of the Fed’s target, and it is the biggest economic problem the US has, and the Fed has now acknowledge that it’s the biggest economic problem the US has, and betting on a Fed U-Turn = fighting the Fed.

The Fed will pause once inflation comes down substantially. That’s the thing to watch, not a U-Turn with CPI at 8%.

Wrong.

The primary purpose of the FRB is to support the banking industry and FX value of the USD as global reserve currency to maintain the US global Empire. It isn’t to protect fake paper “wealth” which provides zero “hard power” in the real world.

The USD also provides the basis of the FRB’s global influence. Destroying the FX value and purchasing power of the USD as your “handle” infers is the equivalent of the FRB committing voluntary institutional suicide.

That’s never going to happen voluntarily. It’s insane.

Since Mar 2020 :

1) Case Shiller 20 cities : up from 222 to 306, up 38%.

2) Real Disposable Income : up from 14.84K to 15.15K, up 2%.

3) 38 : 2 = x19.

4) It’s a RE bubble.

5) CPI rent of primary residence : up from 339 to 365, up 7.7%.

6) Case Shiller : Rent = 38 : 7.7 = 5.

7) It’s a RE bubble.

Seven Survival Rules:

1) Don’t run out of money

2) Doesn’t matter

3) Doesn’t matter

4) Doesn’t matter

5) Doesn’t matter

6) Doesn’t matter

7) Don’t run out of money

The 21% Fedrate of Dec 1979 caused two severe recessions. The oil glut that lasted between the 80’s and the 90’s and the two severe recessions of the 80’s beat inflation.

Raising rates by 0.25% or 0.75% and the $2.2T RRP are not good enough.

Use all what we got, including nuke and coal.

BBB agenda going along smoothly.

Western Europe is firing up the coal plants.

Peasants are told to start gathering firewood…winter is

on the way. I’m sure the Davos crowd will have a emergency

jet zoom meeting. Problem solved.

Anecdotal ‘evidence’ from North East – MA.

March/April were complete madness. Nice family homes in good neighborhoods that were ~800K 2 years ago have been advertised for ~1M and sold for ~1.2-1.3M.

Playbook was: advertised mid week, with open house on weekend, offers due by Sunday 8PM. 10+ offers on every home, house delisted in few days.

Fast forward just 2 months. Houses have open house days for few weeks in a row, no offers. I’ve never seen price drops in previous few years but now probably 10-15% already gave at least one drop. Advertised for 100-200K less then Zestimate. Quite few people trying to sell after they bought it less then a year ago – change of circumstances, flippers, trying to capitalize???

Realtors who were smirking on you if you would not offer 200K above asking suddenly becoming very nice to buyers – if nothing else, that feels good.

Definitely HUGE change of sentiment! HUGE! And this is all before 0.75 points interest rate rise! Everyone I talk to, buyers or sellers realize the time is up. Only realtors are still singing the song of there will be no stop in prices just slow down in rising.

very similar to what I see around me – see my post above

What other song can a real estate agent sing?? LOL

I have 3 realtor friends- actual friends, in both of the counties I’ve been looking at to buy a home in. All 3 have been telling me to wait for quite a while and now both say wait just a little bit longer. It’s going to happen :)

I just saw the absolute perfect fixer I could afford, but it’s in a neighborhood even I wouldn’t want to live it. Surrounded by serious murder-tweaker-ranchers. Prices are not quite right yet, but creeping down and I’m hoping it will happen.

I live in a rural county of 24,000, and it hasn’t hit here yet. There are still so many new custom home construction builds going on that you can’t get more than one dump truck at a time.

Working family homes get bid up and sold within hours. Retirement and vacation-type homes sell within a few weeks. This county is 1/3 65 and older.

I need 3-4 dump trucks for a couple of days to haul off ~50 loads of dirt from an excavation on a barndominium and home build and have no idea when I can get trucks in that quantity.

Concrete is only available to the trades here, and even they can’t get it more than two days a week if they can get it that much.

I know alot of people that will probably lose their house if we get a deep recession within the next 6 to 12 months. They are too reliant on their house and the whole using it as a debt, ATM machine have not taught people that you need separate savings, investments at least equivalent to value of your primary house, condo etc. This is not right away but withing a decade or two. Meaning, if you have a big mortgage and not much savings now, at least 25% value of your house, condo in Canada this is $150,000 to $200,000, you are taking too much risk like a disability, sickness, job loss, hours cut, lower income part-time versus part-time etc. then you are in real trouble. If you have all your net worth in housing, real estate and are in deep debt, somewhat debt, you are not going to be a happy camper the next few months, years.

Here in Canada, I explained why I have not bought a house with my wife since 2016, I am 27 years old right now. I told my uncle, aunt to sell their house last year during the pandemic when they were tricking everyone in a false sense of security. They did sell it made their $300,000 profit after 10 years from $575,000 paid for and sold it for $875,000 after all real estate commission, fees, closing costs etc. owning it and are renting since a similar house for $2,800 a month. I am seeing 20% to 25% price reductions just in 5 months here in GTA. Their mortgage, property taxes, insurance, maintenance, repairs etc. came out to about $3,900 a month. This means $1,100 a month is going in their pocket and have been living in about the same lifestyle renting their house. This is now building their investments in RRSPs, TFSAs. Just this alone over the next 10 years would easily build up an extra nest egg of $175,000.

They are still working and have $2,000 a month after paying all their taxes, cost of living, expenses etc. Basically are sitting in cash for the last 9 months. They were not making alot interest 2.1% short term promo savings account but now with 4.5%+ GICs fixing to interest compounding is a good idea since rates have not been this high for 13, 14 years now. Their $300,000 can easily turn into $375,000 in 5 years in GICs. Since they are both 49 now and have already $700,000 in savings, investments with CPP, OAS coming in the future few years, rent will be all covered just by that and they will have at least $1.5 million to $1.75 million just in savings, investments by retirement in 10 to 15 years

If interest rates rise further and hold their rent will probably fall a lot because they started renting near when home prices peaked. $2,8000 a month will probably drop to $2,000 a month in a year to 18 months as there’s a lag for rents when home prices fall.