Refinance mortgage applications collapsed to lowest since year 2000.

By Wolf Richter for WOLF STREET.

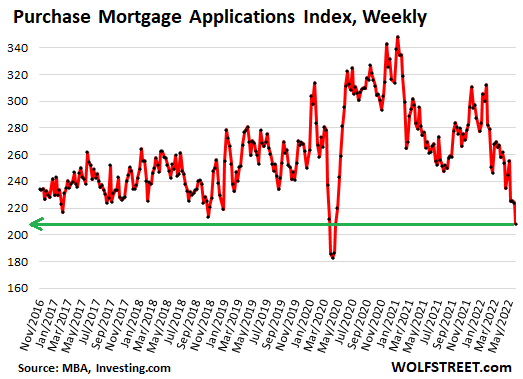

This just keeps getting worse: Applications for mortgages to purchase a home dropped 7% for the week, and were down 21% from a year ago, the Mortgage Bankers Association reported today. An indicator of future home sales: Potential homebuyers try to get pre-approved for a mortgage, lock in a mortgage rate, and then start house-hunting.

Mortgage rates have soared this year, and home prices have soared for years to ridiculous levels, causing layers and layers of potential buyers to abandon the market, amid “worsening affordability challenges,” as the MBA called it. And these applications to purchase a home hit the lowest point since the depth of the lockdown in April 2020 (data via Investing.com):

The MBA’s Purchase Mortgage Applications Index has now dropped below the lows of late 2018. By November 2018, the Fed had been hiking rates for years (slowly), and its QT was in full swing, and mortgage rates had edged above 5%, which was enough to begin shaking up the housing market. Home sales volume slowed, prices began to come down in some markets, and stocks were selling off. But with inflation below the Fed’s target, and with Trump, who’d taken ownership of the Dow, constantly throwing darts at Powell, the Fed signaled in December 2018 that it would cave, and instantly mortgage rates began to fall, and volume and prices took off again.

Today, raging inflation is the #1 economic issue, and the Fed is chasing after it, with backing from the White House, and so this issue in the housing market is just going to have to play out.

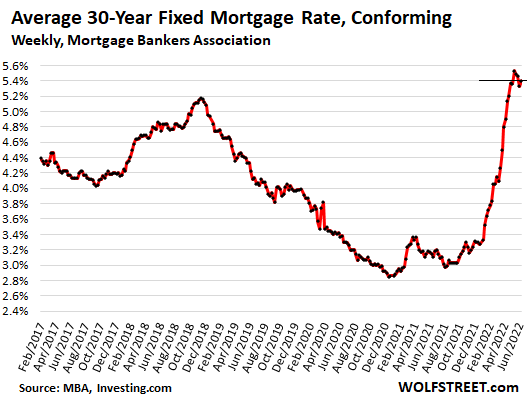

Holy-Moly Mortgage Rates.

The average 30-year fixed mortgage rate with conforming balances and 20% down rose to 5.40% this week, according to the MBA today, having been in this 5.4% range, plus or minus a little, since the end of April, the highest since 2009.

I call them holy-moly mortgage rates because that’s the reaction you get when you apply this rate to figure a mortgage payment for a home at current prices and then accidentally look at the resulting mortgage payment (data via Investing.com):

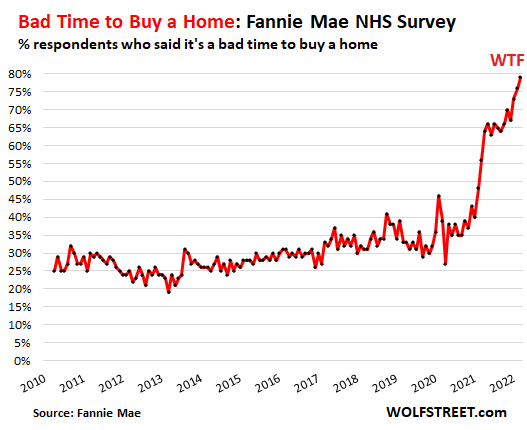

“Bad time to buy a home.”

Turns out, sky-high home prices to be financed with holy-moly mortgage rates, plus uncertainty about the economy, dropping stock prices, and inflation eating everyone’s lunch make a toxic mix for homebuyers.

The percentage of people who said that now is a “bad time to buy” a home jumped to 79%, another record-worst in the data going back to 2010, according to Fannie Mae’s National Housing Survey for May. Sentiment has been deteriorating since February 2021:

“Consumers’ expectations that their personal financial situations will worsen over the next year reached an all-time high in the May survey, and they expressed greater concern about job security,” according to Fannie Mae’s report.

“These results suggest to us that increased mortgage rates, high home prices, and inflation will likely continue to squeeze would-be homebuyers – as well as those potential sellers with lower, locked-in mortgage rates – out of the market, supporting our forecast that home sales will slow meaningfully through the rest of this year and into next,” said Fannie Mae.

Sagging stock prices keep getting blamed.

The stock market is on the front pages every day. Only a small percentage of Americans own any significant amount of equities, but that doesn’t matter. Stock market declines, with many high-flying stocks plunging 70% or 80% or even 90% since February 2021, have rattled a lot of nerves. Which is in part why Fannie Mae pointed out, “consumers’ expectations that their personal financial situations will worsen over the next year reached an all-time high.”

The MBA also had previously pointed at the financial markets as one of the reasons for the plunge in purchase mortgage applications.

In the tech and social media sector, the big declines in stock prices have now triggered the first hiring freezes and a few layoffs. And this too – just the idea of nirvana being somehow over – is shaking up some folks.

Sharp increases in stock portfolios, stock options from employers, or cryptos empowered potential homebuyers and enabled many to borrow against their portfolios to come up with down payments. This option has either vanished or is looking very shaky for many.

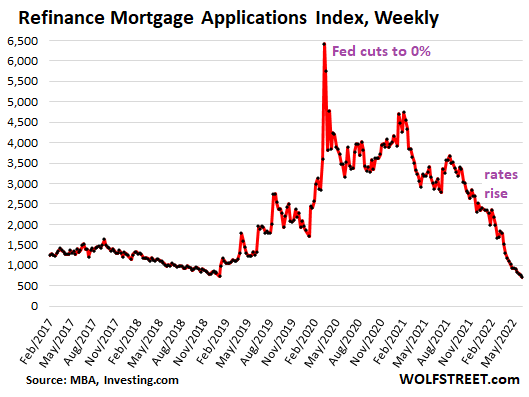

Refi applications collapsed to lowest since year 2000.

Applications for mortgages to refinance an existing mortgage dropped another 6% for the week, and have collapsed by 75% from a year ago, to the lowest level since the year 2000, according to the MBA’s Refinance Mortgage Applications Index. The MBA obtains this data from a weekly survey of mortgage bankers.

With these holy-moly mortgage rates, just about the only reason to refinance is to extract cash from the home via a cash-out refi (data via Investing.com):

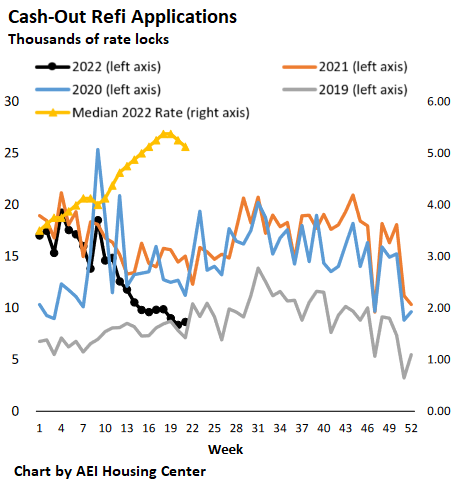

Cash-Out Refi mortgage applications.

According to the AEI Housing Center, which tracks mortgage applications by the number of rate locks, no-cash-out refi applications have collapsed by 92% from a year ago. But cash-out refi applications are primarily driven by the desire to extract cash from a home, with mortgage rates being a secondary issue – and so they continue but a slower pace.

Cash out refi applications in week through May 30 (black line) plunged by 42% from the same week in 2021 and have stabilized roughly level with 2019:

A cash-out refi provides a big lump sum for the homeowner to spend on all kinds of things, from cars to home improvement projects. They are also used to pay off high-cost debts, such as credit cards so that these credit cards can then be used for more purchases. The plunge in cash-out refi reduces the availability of these lump-sums, and therefore reduces the stimulus to the economy they provide.

No-cash-out refi mortgages at lower mortgage rates also boost consumer spending, as the lower rates reduce payments that then leave some extra every month to spend on other stuff. But the spike in mortgage rates, and the subsequent 92% collapse of no-cash-out refi mortgage applications ends this program.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Winter is coming

It really isn’t coming, considering how high prices were. Just because it goes down doesn’t mean it’s weakness considering how high it has been. Markets don’t have to go up and down….they could also go sideways for long periods of time. It doesn’t have to always be doom and gloom. There is also neutral.

Housing is now TOTALLY TANKING even in Beverly Hills, CA.

The ghetto parts of LA still have houses listed around 800 k. Insane

It is absolutely not tanking anywhere in Los Angeles. I’m rooting for it to do just that, but it hasn’t yet begun.

I read a realtor study saying that LA prices were down on a quarterly basis, but not on a yoy basis yet. Interesting because spring is when the opposite trend is expected. Also interesting because it came from a realtor (in OC if I remember correctly).

Not sure about LA but Santa Barbara market has turned, what would take a day to sell is sitting for weeks with no offers and price cuts of 100k per family that live there.

Real estate markets just take time to play out. There are still some idiots that are willing to buy at high prices, maybe they are selling one property and buying another.

Supply is still pretty low, so it will take time to build. By this time next year we will have a very different market, one where sellers know they must sell or lose more in the future. Home prices are all about psychology. If you own a home and want to sell, do it now. Be willing to cut the price. Because the longer you wait, the worse it will get. You will not want to take a 50K hit on profits and will take a 500K hit 3 years from now.

Not a bubble. Completely different than 08. May flatten but wont tank across the board. Supply and demand….with rates this high, who is going to sell their home with a 3 percent interest rate only to enter a turbulent market that offers 6 percent. Rates are way more important than people give them credit for. 3 points may as well be $100k cost differential…when it comes to your monthly mortgage. If you’re waiting for a return to pre-pandemic prices, you will die waiting.

WRONG. Demand in areas that gained 100% are going to burst like a baloon. Depends on what part of the country you are in.. CA, WA, MA, NY won’t lose so much. But the AZ, TX, NV, ID, FL, UT’s of the world are going to free fall

I love the sideways for a long periods of time line, I believe every RE agents is mandated to repeat that talking point to every one of their clients. Not saying you’re a RE agent but do like that logic of it can only go parabolic on the way up but never down. I wish I can say the same about my income for the rest of my life too.

Real estate agents I know they tell me , prices can never ever go down in southern california. With these negative news about the housing in the recent months, they have the same line what Tony has: Prices may not rise but won’t go down for sure. So, it is prudent to buy now at these price/rate then buy later at the same price but at much higher rates :-)

Phoenix_Ikki, That’s cuz everyone & their dog wanna be & are RE agents & when it all collapses they get fired, so they lie like crazy, plus most are ignorant & have no knowledge about finance, economics or history. How anyone can read these articles & see these charts even if ignorant & not see what’s coming is beyond me.

Now you are twisting my words and taking it out of context. In reality, you don’t know whether prices will go down, up, or sideways, but for some reason your crystal ball is better than mine? Come on. I’ve lived through 4 recessions. Rinse and repeat. This isn’t the END of the world like you doomsday commenters always spew the same narrative when things look bad. Inflation is the hidden tax and you think that all the Covid stimulus and vaccines were free as well? The govt writes stuff off all the time just like any other business. Sure it’s a loss, but when you have fiat currency they make the rules.

“It’s just a gully.”

well I believe listings will come out big time – thereby increasing supply of UNSOLD homes

2nd with those NEEDING MORTAGE(now over 6% and RISING)

there won’t be market unless you have all cash

and there is A LOT OF CASH BUYERS LEFT

—

it’s ok – I’m patient for my vacay home – 2+ year horizon

all cash – no issues – just motivated seller

Tony, try 50% plus property collapse, affordability is they only thing that matters & foreign buyers will not buying to get sanctioned, a downward spiral is coming. Anyone not seeing this is brainwashed by recency bias.

The front page of the Spokesman Review (Spokane’s daily paper) showed a chart of rising house prices in Spokane County. Prices have doubled (!) since 2017 to $450k. Five years…

We’re talking Spokane and the surrounding county — not particularly prime real estate. Those prices are not sustainable and definitely not affordable on local wages.

Re Spokane: the prices might not be sustainable but they are successful. In my working-class neighborhood, prices were about $150k before 2020, now about $350k. The $350k houses are selling fast.

50% at a minimum. In Australia plenty of places can lose 65% and be fairly valued. Ofcourse the central planners will try to swing out of the tight corner they are in, but it’s hard to see any way they can relate their bubble from here…. spoiler, they don’t want to. The trillions they throw next time will come to late, just like they started to fight inflation too late.

There is no downward spiral. The banking laws have changed. The rules in which they approve loans have changed. The market will slow because the Feds is raising rates to slow down inflation. There’s no bubble to burst. Some markets will get a small correction but not like all the chicken littles think occurred in the 2000’s. Been in the industry 20+ years. It’s slowing because with the rate increases client aren’t getting approved so many contracts are cancelling. This is a hodge podge of data that doesn’t tell the hole story.

Grasshoppers can’t see Winter is coming until it’s too late.

Haha! Sure! 50%! Please stick to your day job? People don’t have any clue yet there are people like you out there saying oh my God the world is over. We’re leaving a time where the Fed pushed down rates artificially now we’re merely going back to where they should have been the price run ups are because people saw an amazing opportunity with low interest rates. There is still significant demand and household growth creates demand, and wages have gone up, people need a place to live.

Anything that can go up 30% in a year can go down 30% in a year. Why do so many people think housing prices are different, at a time when mortgage rates are rising fast?

I do find it surprising that purchase mortgage applications are down only 21% from last year. With the huge increase in mortgage rates, and prices, you’d think mortgage applications would be down 50% or more. There must be a significant amount of FOMO remaining in the buyer pool at this time.

Those FOMO buyers will be making their conversion to bagholders very soon. Sellers are still filling up the bags as we speak.

So far , we still have overasking prices for lower and higher end markets in Los Angeles

Check the sold houses and apartments for the last week days in Zillow , use the appropriate filters to see what I am talking about.

Bobber,

The irony is that something that goes up 30% has to go down only 23% to get back where it was. If it goes down 30%, it’s 9% in the hole.

At Mortgage Watch Daily it’s interesting that most of these quoted 5.4% rates also require 10K in extra fees to get this rate. The “pure” rates are closer to 6%. And surely going higher.

Just wait for the June / July / August numbers. They will be down way more than 21%. I think you are right on @bobber.

“Anything that can go up 30% in a year can go down 30% in a year”.

YES! That all day! I don’t know why sone fail to grasp this basic market truth

Here’s a fun word. Naivete.

Good. Maybe regular, hard working people can afford to buy again. We got priced out of the market despite a very healthy income and amazing credit rating. It’s getting to the point that the American citizens that make up the majority of this country can barely afford to live in it.

Sure, for the forseeable future demand will fall off a cliff but everyone holds because they don’t want to book a loss. If it was that simple, no one would lose money on anything.

That’s not how markets work, even housing. People sometimes are forced to move. Or they die. Or they cannot service their debts. Or they bought many years ago and some profit is better than no profit. Or institutional investors withdraw because the numbers don’t make sense. Or builders can’t afford to sit onto the homes that are already being built. Or all of it.

And then, prices go down. Typically after that, more people decide they don’t want to catch a falling knife and they sell, and so on.

Another way to think about this is if you look on eBay, sometimes an item that would normally sell for $1k with an open not reserve bid for a $.01. if people are that rational and everyone wait and only bid last 5 secs, the winner will likely get the item at much lower price than normal value but we all seen that’s not how the normal world works.

Gaming theory help explain this type of perceived orderly behavior that’s not grounded in reality.

Except rents have continued to go up 10, 20% or more, when rents go down 30%, then there is room and opportunity for home prices to go down 30%. Who really thinks rents will go down 30 or 50%?

totally wishful thinking.

This is a mania, the biggest US housing bubble ever. There will be no long-term sideways flatlining, especially if the bond mania ended in 2020 as appears.

The headwinds for housing now are worse than 2006 at the end of housing bubble 1.

“The headwinds for housing now are worse than 2006 at the end of housing bubble 1.”

Nope. Not even close. That was a credit anomaly and far different. I agree the mania is subsiding and flattening to small drops are possible, but lots of skin in the game and lots of cash floating around… still.

Back then we had bartenders getting no doc loans and leveraging on 10 rental properties at a time. This time around it’s still rather difficult to obtain financing… as it should be.

Many hoping for 50% off just aren’t going to get it.

Funny thing about these bubbles is that each one is different, and that is one the reasons that so many people get trapped. It’s true that it’s different this time in so many ways. But that doesn’t matter. The only thing that matters is the herd mania, and that is the same.

“Back then we had bartenders getting no doc loans and leveraging on 10 rental properties at a time. This time around it’s still rather difficult to obtain financing… as it should be.”

Here we go again, braindead people posting things they have no clue about. I have posted links that show it has been SUBPRIME this whole time. Fog a mirror financing is around this time just as last time. Wake up and learn a little bit instead of posting from whatever stupor you are mired in.

It is different this time, but the credit anomaly is still present. My husband and I make a combined gross of 130K. We were approved for a 750K loan in Southern California. We have 75K to put down and on a 4.3% rate we would be paying $5,000/ a month on a 700K home. We decided against any purchases at the moment. We net about $6,500 a month once you factor in taxes and insurance. How many people out there are being approved for loans they realistically cannot afford. If either one of us loses our job we cannot afford our mortgage.

2006 was a worse situation, but the problem now is that the Fed cant cut interest rates to stop price declines, once they begin. so we have a much longer downward spiral in home prices coming in my opinion.

markets that crash and then bounce back result in smaller losses. markets that just keep moving lower and lower and eventually noone wants to buy them at all are the real problems. that is what will have. but the people who look at their real estate holdings as their assets will deny it for a long time.

It was different last time is a common refrain right before the pop.

It was different. Then, we had liar loans and out to lunch lending standards. This time we had a temporary demand spike because of COVID/WFH, a building slowdown because of COVID, a ban on foreclosures and evictions, and a flood of stimulus to avoid layoffs and safety net those who were laid off. Honestly, it’s hard to envision a crazier set of circumstances to juice demand and suppress supply.

No one can see the future. But something has to give because income vs. price ratios are completely out of whack. The best case scenario is flat prices with massive inflation in pay. But this is America where raises are bullshit so I don’t like those odds.

The economic cycle has expansion and recession…. cyclically, there is no neutral over time.

That comment comes from someone who perhaps is in real-estate and doesn’t see the world changes that are forthcoming and certainly doesn’t want to realize anything that would jeopardize “sales” as it there revenue. Rose glasses on . Time will smear the shade of glasses on.

General Contractor here has made this comment / reply

i remember rates when i was a child at 16% that was the 70s then great for investment then when i worked in banking in the 90s rates were around 8.25% our seniors complained of their time deposits barely being worth the money

…. do they still even have time deposits anymore? idk but i remember mtg rates being of acceptable rates then, now to hear holy moly rates at 5% is a funny thing….i did loans for manufactured homes rates were between 9 – 11% ….. people didn’t complain then, i don’t get it

You’re assuming 10 to 20% correction. Superbubble means 60 to 70% off current home prices.

Can it be a Nuclear Winter instead of the regular flavor Winter for the housing market?

Haha winter is coming. If you didn’t sell its already to late. Better start learning how to speak mandarin.

Yeah. Because everybody knows- if there’s one people on the planet who don’t have a bigger system-wide property bubble right now….it’s the Chinese.

lol.

“Brace for Impact”

Here’s what is not being discussed….and what makes this situation different..

the replacement cost of these homes is soaring……

this wasnt the case in past housing crashes…

and there is still corporate money saddled with the objective of buying housing and renting it out…looking for a fair return vs the current inflation.

IMO.

the key issue here is the investors driving up prices in the real estate market. investors need renters, with no more free money and inflation we will see renters cannot afford these inflated housing costs (look at the costs of housing versus median incomes) investors will pull the trigger to offload properties soon and flood the market. Different cause versus the 2008 foreclosures but the same outcome. Crash.

You hit the nail on the head. Investor accumulation has caused this market manipulation and squeeze. The panic sell offs will create a crash. It will also trigger increased foreclosures of those who will walk away from homes they excessively paid over fair value. Supply will soon not be an issue. Expect 25% price drops by 23

Wait for the Wall Street boys to exit when they have to liquidate to cover their losses. OpenDoor still buying shit in AZ and trying to sell for 50k more 3 weeks later.

Spot. On. As I am not a realtor, but rather have a masters degree in global science, I have already noticed an increase in the homelessness rates since the moratorium on evictions has expired. If so many are opting for the roadside, renters are not actually collecting on these vacant investments. Considering that the average household cannot absorb a $1,000 emergency, yet food costs have soared over 10% gas about 50% year over year— we’re looking at a household deficit of between 5-9,000 this year if trends continue. Homelessness or housing adjustment—these are hard facts. The hyper-inflated technology bubble is already bursting. This is absolutely going to roll over the housing market like a steam roller. Pricing will adjust accordingly, and hard. Even Zillow had the foresight to get the heck out of the buying market and start unloading it’s inventory. It’s always those who have the most to lose who are the blindest. Will this market recover? Of course— it always does. Markets always recover, but I would expect that buyers stop rolling over immediately and own their power, and sellers understand that it’s not 2021 anymore.

1) Isn’t it funny how costs/replacement cost just “happened” to double over the very same 20 years that ZIRP halved interest rates, keeping monthly pmts roughly constant? I wouldn’t take it as gospel that claimed “costs” are anywhere near bottom line true production costs. Builders have heard about the Fed too…and quickly reprice accordingly.

2) Institutional ownership of SFH is still pretty small – maybe 5% to 15% (very maybe) of new build and unlikely to be much over 1 million cumulatively (in a 75 million+ SFH market nationally).

And nobody knows better than institutional investors just what interest rate movements do to asset value/affordability/resale value – so they will move on a dime.

Just ask Zillow – which dumped its home flipping operation last November (after losing tens of millions). Not many entities are as plugged into SFH supply/demand dynamics as Zillow.

Cas, what are you on about?

Investors are about 30 percent or more of the home sales TODAY and have been for the past couple years. You’re taking the inventory that is just sitting there not on the market makes zero sense. They are responsible for driving prices up.

Zillow exited buying houses, still sitting on 4 billion or so in houses (read its balance sheet on its 2021 10k). Cost of lumber is still elevated but has dropped 50% YoY.

Apparently you lack a sense of history as well the economics of pyramid Capitalism. Speculation or the action predicting the future doesn’t have a good record in the investment of Real Estate or Stock Market. As a young adult in the 70’s I remember having inflationary and recession pressures on economy at same time. In the early 80’s Home interest rates were 18%

Didn’t think I would ever be able to purchase a Home. At that time thinking your home was an financial asset that you could flip into a higher price home was not a thing. A home was a place to live and raise a family or not. But even as mortgage rates dropped and economy improved. The so called Wolves of Wall Street have kept up their Speculation, informing their consumers of the future disasters when anything happens that might hamper their right to capitalize on their prey. In the year 2000, we were able to refinance our house from 6. 5 per cent to 5.00 %. That was considered great. Currently interest rates were raised to ease the pressure of inflation. Also, no one can predict the future. Especially the false prophets of Capitalism. More like Coyotes than Wolves.. Plus the Government has no control over real estate prices or oil prices. They are private businesses. But like all bully Capitalists, they must blame the GOVERNMENT when their predictions fail..

Thanks for making us all dumber. lol

Not tanking in Phoenix…….

Treasury yields rise, 2-year hits highest since Dec 2018 ahead of Friday’s U.S. inflation report

Yep, shorted the correction and focused especially on the spike in junk bonds. Thinking that may have been related to the Luna/terra crash somehow.

That why I think it isn’t going to take that high of a rate to roll the economy into recession. Ten year between 3% and 4% and a flat yield curve and mortgages at 5.25% – 6.25% should be enough in my opinion. It’s not written in statute that inflation has to be 2%. Volker was satisfied with 4% I think. Market is already baking in 2.75% average next 10 years.

The 10 year should be up near the rate of inflation, anything else would result in continuing the same old crap.

10 year inflation breakeven is exactly 2.75%…so 10 year bond is already above where it should be according to you…

The vast bulk of the inflationary impulse is from commodity price inflation NOT wage growth. Pretty much every commodity globally is well above its incentive price so to assume commodity inflation will be contributing meaningfully to inflation next 10 years from the current extremely elevated position is overly pessimistic.

Inflation has shifted to services — healthcare, rents, insurance, travel services, etc. And 70% of consumer spending is services. Your commodities theory was widely held a year ago, when they still thought that inflation was “transitory,” which turned out to be wishful thinking.

Inflation has moved into services, where inflation is now spiking. 70% of consumer spending goes into services — rents, healthcare, insurance, travel services, education, etc. Your theory was the reason Powell dismissed inflation as transitory. This has turned out to be a horrendous mistake. I think it’s time you update your theory.

So many people looking at only one side of the picture regarding real estate crashing. The term crashing can only describe 2008 from faulty ARM loans given without income verification to any person on the street who applied and stated they made all this income. When a friend who was a furniture delivery guy can take out a home equity loan and use it to buy a high rise condo worth twice as much as his primary home and the HOA dues are high like another mortgage can get a stated income loan we’ll yes the market will crash eventually. But since 2008 the SAFE act was implemented to deter from bad loan practices. TODAY people are sitting on lots of equity in their homes and staying in them because they’re still shell shocked from 2008 therefore even though demand is shrinking the supply is still low. My opinion there will be a corporate crash first then other markets will decline as well but not Crash. That word is too extreme and promotes fear in people rather than educating them.

Vickie,

It all comes down to monthly mortgage payment affordability.

If home prices doubled/tripled over the last 20 years only because mortgage rates went from 8% to 4% to 2.6% (last year), then a *lot* of that gets unwound now that rates are 5.4% (and likely heading higher in DC’s panicked fight against the inflationary cancer it long courted).

A $400k house at 2.6% rates ain’t worth $400k at 5.2% rates…far too few potential buyers have the income to qualify for the monthly payments that go along with a $400k house at 5.2%.

You mean like every other president before and since?

So, why did he re-cave?

“But with inflation below the Fed’s target, and with Trump, who’d taken ownership of the Dow, constantly throwing darts at Powell…”

“Every other president before and since” didn’t get on Twitter and issue very thinly veiled threats to fire the Fed chair if he didn’t cut rates.

LBJ actually physically assaulted Fed Chairman Bill Martin. Does that count more than a mean tweet?

No, because it wasn’t public.

If Trump was tossing darts at Powell I would surmise that Biden is indiscriminately and without any regard tossing lawn darts in the air.

The Fed’s independence means lawn darts in the air are better than darts from (any) Pres thrown directly at the fed chair. There are reasons institutions, like people, have boundaries. Now just mouthing it on twitter is worse than LBJ privately manhandling William McChesney Martin, who served in uniform in WW2 and could certainly handle it.

Yes, the Fed fumbled, but more pressure from various sides only stirs the mess worse. We all make mistakes and then hopefully set things right. No part of the USA or person in it is exempt from this natural state of uncertainty.

And note: Trump’s darts were all toward opening the floodgates to cheap credit constantly, mainly to crank up stocks, something now bemoaned by many of his fans here.

But I know plenty of folks don’t care about facts, they want to feel angry and powerful and cutting and on top of it. Like a tough guy. Clue: none of us are on top of it. We are in the worst moments, helpless tidal creatures floating in whatever it will do now.

With clearly equal ”certainty” pleep,,, many places in USA continue to be ”exempt” from the uncertainty brought on most of WE the PEONs in USA who have debt.

Not to reveal too much to the banksters and others of their ilk who have done SO much damage to almost everyone who has ANY DEBT,,,

But, in fact, there are many folks in USA and likely elsewhere who have NO debt,,, and have not had debt for years, maybe decades, maybe ever…

That is EXACTLY ”WHY” the Federal Reserve ”bank” was started in the first place:::

All of us LOLs, in this case little old ladies of each and every kind, kinda/sorta learned, usually the hard way,,, to put our excess gold in jars buried in the yard when times were good/booming,,, and then take out our savings and buy for pennies on the (gold) dollar when the ”bust” arrived.

Because SO many, if not ALL ”banks” went bust in almost every recession/etc… the FRB was started by the usual oligarchy types to make sure ”their” money/investments would not suffer, again and/or ever, etc.

Foundational basis for ALL the ”issues” that continue to haunt and rip off all LOLs who are savers and thrifty folks…

The Fed reports to Congress not to the president. Thus only Congress can remove a the Fed Chairman.

The US is bankrupt & Japan will soon show the world ya can’t engage in fraud any longer, Japan got away with it so long only cuz they were the only ones, now everyone is doing it. A collapse & total collapse is coming, a good lesson that QE, market manipulation & fraud at the highest levels will be paid for in total ruin, even uttering the words “We’ll do whatever it takes” is the height of , what ever takes results in ruin.

Why are there rules in the first place? Doing whatever it takes has consequences, if not, let’s all be criminals, fraudsters & thieves to get rich, let’s all do “whatever it takes” to be wealthy, the arrogance, hubris & delusion is unprecedented.

Alan Greenscum, Ben Berstanky, Granny Yellen and Jerome Bowel should all be in prison. Just look at a chart of the FED’s balance sheet over the past 100 years to see what a filthy, vile sham they perpetrated.

This kind of doomer talk is around all the time… I remember it well from 2008… but life goes on in spite of the hoarding of beans. When I was young and impressionable, I was more likely to get caught up in the nihilistic fever dreams.

The broken-record tough guy stance must sure feel good, though. But nobody can show the alternative: what the world would be without these moves. It is sheer conjecture. It is too complex for anyone, tough or not, to calculate.

This talk has been floating around for years, closely followed with ‘buy gold’.

Things turned out to be pretty nihilistic for the 8 million households that got foreclosed out of their down payments/equity/houses in the wake of 2009 (out of 50 million SFH with mortgages).

Just because the MSM takes orders not to talk about it, doesn’t mean it ain’t happening.

Quite usually the opposite in fact.

LOve your nicknames. Very Appropriate

Meh you don’t need look at future Japan. Just look at past Japan. Their asset.price bubble was no joke. Japan is why the refrain stocks always go up is simply not true.

Funny, I have been playing around with data you can download from Realtor.com and charting out SoCal areas and what not…what I noticed is that huge spike up in price reduction YoY and yet median list price and average list price is still extremely sky high…just funny to see how sticky home prices is, hopefully will see that crack and drop in the latter part of this year

Very sticky, and some people will follow the market all the way down. I knew someone during the last collapse in SoCal that initially listed their house for $1.04M when the market had already turned down and that was peak pricing. They followed the market down with price cuts for well over a year, though I don’t remember the exact length of time, before finally selling at $720K. Those same sellers are out there now, they just don’t know it yet. I’ve owned a house for 22 years in the same neighborhood and have watched it go way up, way down, way up above the previous peak, and now what? I’m not a complete pessimist though, I don’t think it’s going below the previous bottom.

The last housing bust took 5 years. In the first year of it, people didn’t even know it was a housing bust. Afterwards, with hindsight, they knew. But the underlying dynamics were spelling it out already.

Yup, one thing that’s eerily similar to that mortgage app line on the way down is when I charted out price reduction count YoY and that line is pretty straight up, looks very much like that mortgage application drop line in reverse, with some areas worst than others, what’s a little surprising is seeing that line spiking up in all SoCal metro areas as some would like to believe it’s impossible out there cause the weather is so nice.

Will see how this hold up over time as you said it took half a decade last time but the pattern is there for sure and that denial and never ending hopium will take quite a while to work through, need a black swan event to help the price stickiness to come down faster I hope.

Oh as some others will like to believe this might just level off or we’re in a temporary gully..there’s no impossibility just probability right?

“need a black swan event to help the price stickiness to come down faster I hope.”

I don’t think you need a black swan. If interest rates keep ticking up, that should do it.

It’s going to crash much faster than last time thanks to social media. Plenty of RE agents, lenders and investors on Twitter and YouTube are bringing lots of good data from the trenches which we didn’t have during the last bubble. It’s why things turned so quickly from the beginning of the year. Very few bubble deniers left at this point.

It should crash faster than last time because the overvaluation and fundamentals are far worse.

Conversely, since history never repeats, I’m anticipating it won’t and I’m probably the biggest pessimist on this blog. I expect the crash to be bigger – eventually – but it might take longer than these posts expect.

First, I expect market rates (including mortgages) to hit a preliminary peak (the first of many only) and temporarily move contracyclical to FRB monetary policy, maybe six months to a year.

When?

Don’t know but nothing moves in a straight line forever and rates have already been rising in anticipation of FRB tightening, both QT and FFR increases. 30YR UST has already lost 55 points from 191 to 136 since March 2020. That’s a huge move even though rates are still very low.

Second, when real estate starts falling noticeably, unemployment increases “a lot”, and foreclosures with it, I’m expecting another mortgage moratorium. Many politicians almost certainly believe it’s mostly cost free and of those who don’t, still might conclude it’s cheaper than bailouts and reverse wealth effect.

It’s going to be worse this time, but probably not particularly soon.

A F,

“A mortgage moratorium?”

Yeah, that’s what we will surely need. Contract law and property rights are so passé. /s

I dont agree that it crashes faster. Last time the banks had to foreclose on may properties. This time there is not that issue.

This is going to just be a lack of demand that will slowly wear away at pricing. It will take 1-2 years before there are any people underwater on their mortgages. It will take 2-3 years before people start to realize that if they dont sell they will lose more money. 5-7 years later, the prices are at 50% of peak, that will be when plenty of people walk away from homes.

The Fed wants a soft landing.

The Fed absolutely does not want housing prices to crash 30-50%.

Especially if it happens suddenly. Too many people may decide to mail in the keys to their lender when the beautiful 30% gain they achieved in their home evaporates and they are underwater. The Fed works for the banks.

However, if housing prices only drop 10% over 3 years while the Fed is making a half-hearted effort to control 8%/year inflation, people will still be able to sell their house for a 17% gain and won’t walk.

Nevermind that 8% inflation times 3 = 24% and a 10% loss totals to roughly a 34% effective loss.

Inflation is the Fed’s friend to avoid another 2008 housing crash.

At the moment the RE market has gone from 100 over-asking offers with inspections waived for homes to “only” 4-5 offers at list price or slightly over.

The last time during a market that was rising with inflation around 2014, we offered 5% lower than asking on a house that was on the market for 2 months. One other bidder had tried a 10% under-asking number and we “won”. We still had buyer’s remorse for a short time because it is costly to make your house the perfect home for you.

I consider that a normal market.

2008-2012 with the 30-50% crash was not normal either but we are still a long way from that.

Bingo. It seems that until sellers see price cuts and/or lower appraisals no one realizes that the trend has reversed.

This time IS different than last time in that sellers will not be forced/foreclosures so much as those wishing to downsize or moving for jobs, with the former being the big driver as boomers retire and move. (What is the vacancy rate for homes owned by this group?)

The big question mark that I see is the institutional owners of single family homes. How will they react? Mark to market does not have to be published in order to be public knowledge and smart people may realize that their investments in this sector are losing value and they rush to cash out of the fund.

The last housing bust actually started here a few months after the sub-prime lenders in California got into trouble. In late 2005 I noticed the days new listings sat on the market started going up. That turned into an avalanche in 2006. 2009 was rock bottom.

What did the data from 2006 to 2009 look like?

Bubbles build over time, but pop very, very rapidly – because 1) the herd only knows to follow the herd (not understand the fundamentals) or 2) speculators think they can outrun the herd.

When holding an extra home becomes much more expensive than the sweet appreciation, there will be a housing inventory glut.

When rents, alone, don’t cash flow to cover holding costs and there is no sweet appreciation, there will be a housing inventory glut.

When corporations can no longer find cheap and easy money, there will be a housing inventory glut.

A lot of second/third home owners won’t even wait for cash flow.

I have friends who owns multiple homes and have the conviction that home prices won’t ever go down. So far, they have been proven smart and they for sure have the right to gloat over it.

They are cash positive but if their home prices drop by 15% or so , say, they won’t hesitate to sell it.

Won’t hesitate to sell but will be unable to, greed is a terrible thing, why wait. If ya not prepared to hold down 50% plus you should’ve sold 6 months ago.

Do these 2nd/3rd homes sit empty, rented, AIRBNB?

Did they pay cash or are they making payments on houses that just sit empty

I think they mostly sit empty. According to the Census, there are 16 million empty houses in the US.

Harrold,

On a semi-related note, “normal” active listing inventory averages about 1.2 million in a given year.

In 2021, it was between 400k and 500k (thus the goofy, post 1 million Covid dead, price spike – less than 50% of the normal inventory was available).

With rates now up to 5.4%, inventories are back up to about 600k…before peak selling season.

Once pandemic paranoia fades, for sale inventories will normalize.

And that 16 million, negative cashflow heap o’empty houses, can surge active listing inventories in an instant.

It does not matter. Even if they are rented and producing positive cash flow, a lot of people just can’t see the value of their real estate holdings going down. They’d rather cut prices and sell it. This is true even more these days because of proliferation of media and real estate holding is a psychological process.

The more gloom and doom stories you have ( as it is currently right ow, ) the more people want to get out.

There are now mass vacancies on vacation rentals, etc. A large part of the shortage of for sale inventory was due to the rapidly increasing prices. Who sells a house that’s increasing in value $10,000 per month, and faster than the loanowner’s actual income?

All of these speculative shacks are going to hit the market en masse as soon as these greedy speculator scvm realize they’re depreciating $10,000 per month. The carnage is going to be unreal.

And I am also expecting these same people to put the barely used pickup trucks and SUVs up for sale as well.

“ And I am also expecting these same people to put the barely used pickup trucks and SUVs up for sale as well.”

You can have my truck…

When you pry my cold, dead hand from the gas pump nozzle….

I see home values dropping but not rents. I think most renters are trapped by increasing circumstances of ownership being well beyond their ability ever. Landlords won’t give in to lower rents unless they absolutely have to.

They will not have to lower rents until it becomes cheaper to buy than rent.

Which is why the bad tax policy that encourages speculating in residential real estate has screwed people who need a house to live in and also those who want to rent.

Yet nobody wants to change tax policy. They want to blame the FED, when really all they do is try to compensate for the bad policy coming from congress.

The answer is to abolish the income tax, go to consumption taxes and remove inducements to speculate in residential housing.

I discuss that in the link associated with my name above.

Tax policy isn’t even close to the primary driver for either housing bubble 1 or housing bubble 2, this one.

It’s primarily artificially cheap money and lax lending. I’ve read this sentiment here before (I think from you) and it’s totally wrong.

Do the math yourself. The tax code didn’t change meaningfully since 2006 to benefit real estate. If anything, the major increase in the standard deduction in 2017 had the opposite effect for most taxpayers.

Median house payment has increased something like $800/month in the last year from the combination of rising prices and higher mortgages. This increase dwarfs any tax benefit for most homeowners or prospective buyers.

Hi Augustus,

Thanks for the reply.

Real estate boom bust cycle has been going longer than since 2006.

And I think tax policy is just a contributor to the effect.

But if we change policy to make real estate speculation more expensive, would we not have less competition for houses people need to live in?

“They will not have to lower rents until it becomes cheaper to buy than rent.”

Nope.. rents only go up as far as people can pay. When they can’t, they will double up/move in with family/etc. Rents are controlled by what people can afford.

It’s a factor but not the primary factor.

The point I was making is that there isn’t a material tax policy change that led to a lack of housing affordability or the two real estate bubbles. This equally means that reducing tax benefits for real estate alone wouldn’t make much of a difference.

In my last post, I also forgot to mention the SALT cap. The combination of the SALT cap and the much higher standard deduction means that most homeowners either get no net tax benefit or it’s marginal. Even with higher home prices and higher interest rates, any incremental benefit after the $24K standard deduction is modest at best and it’s not much better for many higher income people due to the SALT cap.

For investors, shorter depreciation schedules probably make the most difference, but it’s been 27 1/2 years to my knowledge for a long time. The $250k/$500K exemption isn’t available to them but doesn’t help homeowner occupants on the front-end anyway which matters most.

I don’t think tax policy is driving up house prices or rents..

The 2017 Tax cut doubled the std deduction which greatly helped renters. They had more cash (24K per year) to burn.

SALT cap hurt homeowners since they can’t deduct their state and property taxes. It should have driven RE prices down.

Rental landlord deductions did change in 2017 and if your rental is a business, you can deduct a certain percentage of the rent collected. I don’t know the details on this but it benefited landlords and corporations that have properties as part of a business. This should have been passed on to tenants.

I think rents went up because:

1) Low interest rates cause higher prices. More people can afford a more expensive home. They purchased available rental property to live in. Including a couple of neighbors who are happily living in former rental properties to the dismay of the former renters who were thrown back into the limited rental pool.

2) Limited investment options for ROI. Rental properties, stocks, and REITs that purchased a large amount of homes and rented them had a great ROI. They had to make a return after purchasing a former rental so they raised the rents. Safe treasuries and bank accounts did not have any ROI.

3) The “Flipper” craze. If you are handy, and have some cash, invest in a fixer home and automatically make 20+% while the bubble was rising. That took away low priced un-gentrified rentals.

4) The AirBnB craze. Short term rentals for fun and massive profit. That drove out long-term renters in some areas.

5) The Covid migration out of cities with people buying up former suburban rental homes. I think Wolf stated that city rents have been flat.

6) Rental property churn. Long-term landlords who had low mortgages and lower rents sold for a massive profit to new landlords who had to raise the rent to have an ROI.

Rents are always a lagging indicator. They always have been and always will be.

When unemployment rises sufficiently and people can’t afford it, rents drop.

Landlords who refuse to reduce rents will find themselves with high vacancies and negative cash flow as their renters move out and “double up”.

AF,

Generally agree with you here, but 30% to 40% rent hikes over 1 or 2 pandemic years has me thinking other factors may be in play.

(Also recently found out that 150 to 200 MSAs (out of 380) in the US lost population from 2010 to 2020…hardly conducive to soaring rent prices under normal supply/demand conditions).

If national apt complex landlords are riding yield optimizer software hard, they might be willing to eat abnormally large vacancies under protection of abnormally high rent rates – see above.

On tools like rent.com, etc. I’m seeing 75th percentile rent pricers apparently happy with dozens of vacancies…while 25th percentile pricers are utterly leased up.

I agree that you can’t get blood from a stone…but they can try.

AJD,

All it takes for SFH speculation (and general inflation!!) to end is for DC to allow mortgage rates to rise from their money-printer-poisoned 2.6% to today’s marginally rational 5.4% to an honest-risk-adjusted 9%.

The rapid 21% decline in mortgage applications (yr over yr) happened within 2-3 months of rates going to 5.4%

In last 24 hours, front range Colorado MLS shows new listings over 400. Price reductions (same period) 263. Seems to be accelerating every day.

I’m also seeing price reductions in my metro Denver neighborhood, it looks like the peak was probably last month, there was no inventory here since about March 2020 and things were selling in days, now some homes sitting for weeks with reductions from the peak pricing of earlier this spring. Not dropping like a stone yet. One house sold a month ago for about 25% higher than any comp, and everyone rushed up to list at that number, but it appears to have been a weird outlier peak, nothing sold within 15% of that one sale. Really interesting to watch first hand. Homes have roughly tripled in value in our neighborhood since we bought in 2001.

I would say they tripled in price, not value.

Value is the same, a house.

I do think we should discourage investors from speculating in residential real estate.

What would it take?

Require payment in full at closing, no leverage, no borrowed money if corporation is buying?

If not a corporation, 25% down on second house, 50% down on third house, 100% down for more than three?

Requiring more capital should reduce competition for homes from people who do not plan to live in them.

House flipping is not a value adding activity, it is a disease that merely extracts wealth while providing no value.

It’s getting so hard to sell a house in my town that sellers now actually have to put up For Sale signs on the property.

2banana,

“When corporations can no longer find cheap and easy money, there will be a housing inventory glut.”

Ten or fifteen years ago I was visiting an aunt in Pleasanton, CA (where I had attended high school). She had gotten her RE license just to have something to do.

Pleasanton Valley homes were selling for a 800k and I asked her how the average couple could afford to buy there. She told me that when companies like People Soft transferred someone to the corporate office in town, the company bought the house for them to live in.

All true

Wolf’s article provides another nail in the coffin for the 40-year bull market in bonds: “The average 30-year fixed mortgage rate … highest since 2009.”

But it’s odd that the 30-yr mortgage rate is “highest since 2009” while benchmark Treasury Bond rates are still about 1% below 2009 rates. Typically the 30-year mortgage rate is about the 10-year Treasury rate plus a “spread” of about 1.5%. The current spread is unusually high, well over 2%. It’s the wide spread that’s pushing mortgage rates to “highest since 2009” ahead of Treasuries.

Unfortunately, since 2000, “wide mortgage spreads” have only been seen in times of financial crisis (Spring 2020, Fall 2007-Spring 2009)…

Alternatively, spreads could be wide not because of tight financial conditions, but because, in a time of rising interest rates, mortgages are now more likely to be held longer. During an era of falling rates, mortgages were often refinanced early at lower rates, so the loan was of a shorter duration for the lender, and they could offer a cheaper rate. With a rising rate trend, the effective duration of the mortgage loan will be larger, and lenders maybe want a higher return to make up for the risk of sustained inflation?

I should do another piece on the spread between the 10-year yield and the 30-year mortgage rate. This is really interesting in a geeky kind of way.

I’m geeky and very interested! Thanks Wolf!

Other than the late 70’s and early 80’s, have we had rapidly rising mortgage rates over multiple years? Please go back that far if possible.

Homeowners, like my parents, made out very well in the late 70’s and early 80’s. 5% mortgage rate while earning 10+% in LT bank accounts.

They didn’t have to move so they didn’t and had no incentive to pay down the mortgage. House prices were relatively flat compared to high inflation. They also had awesome COLA (6-8%) raises every year.

Renters did OK also until the mid 80’s when rents skyrocketed.

Of my HS class of the early 80’s, my friend’s parents who owned homes in S. CA are still there. My friend’s parents who rented are long gone.

Please do riff on the spread between 30-yr MBS vs. 10 Year T-notes.

The proposal I heard 6 months ago was:

Sell 30-Yr TBA MBS against Ten-year Notes in the belief that (even if you don’t know which way interest rates will go) you’ll make money shorting MBS against Notes because the Fed selling its MBS.

FRED says the spread was tightest in April 2021 at 1.35.

By January 2022 when I heard about it, the spread = 1.76.

Now the spread = 2.33.

So, the trade idea is working, but very slowly.

It feels like everyone and their mother has it on.

I heard an interview of a former money manager who theorized that the fed wants to make rates at the long end high but keep them low at the short end to reduce speculation while maintaining liquidity and not kill off good businesses.

Might be some truth to it.

It would seem like they could do this via QT, which just began, so time will tell…

Spreads have also widened significantly in commercial real estate lending. CMBS is functioning but with wide spreads, the Debt Fund lenders, who have become a big part of commercial lending, have been doing much much lower volume the last 2 months.

“But it’s odd that the 30-yr mortgage rate is “highest since 2009” while benchmark Treasury Bond rates are still about 1% below 2009 rates”

Mortgage rates are set by the market.

Treasury yields are played around with by the Fed.

It’s called “being behind the curve”.

Wait until QT kicks in. You ain’t seen nothing yet.

Uncertainty/risk/fear widens spreads.

Everybody and their dog in the business knows that the Fed has been “crack dealer to the masses” for 20 years.

Banks have re-priced mortgages quickly and blown out spreads to offset the fear of what happens now that the Fed starts cutting back on the interest-rate crack supply.

The banks know madness is likely to come – near term price crashes (as buyer supply evaporates with higher rates), general macroeconomic mayhem, cats and dogs sleeping together, etc.

Ok Wolf whatever.

I read that inventory was growing in Seattle. Is that wrong? If not, it is normally a leading indicator of market cooling. The stock thing will fade unless we revert to more monetary insanity.

In Seattle, houses are still selling, though not as fast. I don’t see any dark winters here tbh. A lot of cash buyers. Lots of RSU money has to flush through imo. Idk how long before it collapses. Perhaps it won’t when the Fed reverses course and the printing presses start firing again.

I agree, the outlier RSU company money has crashed but there are plenty more companies who haven’t crashed (yet).

FYI, RSU’s are typically paid in lieu of a salary increase. Instead of a salary increase, you may be paid in stock that vests over the next 3-4 years. You take it and eat ramen on your current salary with no cash raise.

If you received RSU’s in 2019/2020 (Vesting in 1,2,3,4 years), and the company stock is still up significantly since that time, you have no motivation to move this year.

It is hard for companies to lure people away from other companies who have greatly appreciated RSUs since then.

The stock market has to normalize away from Pandemic highs for this to happen. What company has appreciated 5-10X in 3 years? The worthless ones have crashed.

If your company gave you 30K in RSU’s as a 3 year raise back in 2019, and now the company stock is up 5X, that is worth 150K. That is hard to walk away from and when vested, would provide a good down payment on a house.

In many ways, this is a good retention program for employees during tough hiring times. However, it is likely costing the company more than they expected by giving stock instead of a cash raise back then. They have to buy back stock at an inflated price to pay their employees the RSUs committed.

The old saying for startups is: “You can’t eat stock”. However, today, you can buy a house with it.

The Tech companies have crashed though. Those RSU issued at $30k are now only worth $3k in many cases.

As Wolf pointed out, many profitless tech companies have crashed.

I work with profitable tech companies who have not crashed yet….. They are still up 2-3X from 2019. These companies are probably not worth 2-3X more than 2019. (Look at Nvidia, AMD, Apple, Microsoft, )

We are still early. All it will take is one bad quarter to send these company’s stocks plummeting. Just like in 2001.

All the money funneled out of Vancouver, Canada and into Seattle Washington on April 20th 2017. I told everyone buy all the homes with 8’s in them. Don’t buy homes with 4’s in them. Buy every house you can get near elementary schools all the corner lot homes closest to the elementary schools. Anyone who listened to me and bought next-door or directly across the street from the elementary schools would have tripled their money.

The last place I would want to live is near an elementary school. The traffic before and after school is ridiculous. At a school near my house, people can’t even get out of their driveways at certain times because the cars are backed up.

Mormons build their churches as close as they can get to the local elementary school.

Watching your little ones walk to school from the kitchen window is worth a lot of money to some people.

I read that inventory was growing in Seattle. Is that wrong? If not, it is normally a leading indicator of market cooling. The stock thing will fade unless we revert to more monetary insanity.

FRB has about 30 points on the DXY if they decide to restart QE. They might be nuts enough to do it again when financial conditions tighten meaningfully and markets really start to crack.

Soft-ish landing my ass.

He still says landing don’t he, yet people say prices will never fall, landing means down down down, with so many speculators it will be the hardest landing ever, the Fed can’t go back either with inflation soon to be 10% & people raging. I mean to say “landing” is a big deal for the Fed, do people think they’ll say it’s gonna collapse? 2007 they didn’t even admit prices will crash while already falling.

I think Flippers are now working 24 hour shifts to finish their flip. I would be “flipping out” to finish asap.

Which also means that part of the buyer pool has dried up.

Japan is still landing from its peak in 1989.

I have nagging suspicion that nothing will pop – ever.Because house prices aka principal does not matter (just like $30T US Gov Debt).Nobody in his right mind plans or tries to repay it. Pay interest only then flip it to the bigger sucker or live in for free as long as you can.

Out of 10 biggest mortgage originators 7 are non – banks but quasi-gov entities.

Banks which STILL write mortgages dump them ASAP as hot potatoes.

The question is: who’s financially pressed to evict “homeowners” when they don’t feel like paying off their >$500K crapshacks ? Auntie Yellen, Uncle Jerome ? They could not care less…

Also if RE bubble starts deflating how our retired Sacred Cows (cops, teachers, firefighters) will continue to draw their $200K pensions funded mainly by property taxes ?

Found the website for you, Doubting Dorothies:

transparentcalifornia dot com slash pensions slash all slash

$200K pension sounds like f… peanuts.Honor Roll begins with a $1.5M pension drawn by former cop.

Just wow in your reply…I think my brain broke a little just from reading this..

I have an article in my scrapbook dated 2010.One guy “bought” a home sweet home with NINJA loan which was quite popular in 2005-06.

After 5 years of almost free living (interest only) he sent a jingle mail and assumed it was the end of it, since his state was “no-recourse”

Well, his former state hounded him down in another state and garnished his wages for unpaid PROPERTY TAXES !

IMHO that’s the deep meaning of RE bubbles.Fed Gov inflates bubbles so that increased property taxes cover State Gov fat salaries and even fatter pensions.

Because if Feds take over bankrupt state retirement funds no f… way they will keep paying $1.5M pensions of retired CA cops.

What planet are you living on?

Average Texas teacher’s pension: $24,921

Average Texas police and fire pension: $47,000.

California isn’t Texas, and averages are misleading because many people don’t stick it out to properly milk their pension system.

Pension spiking based on overly-generous formulas is a financial art form, not so different from creating cryptocurrencies, private equity shenanigans, or overhyped IPOs…

He lives on the planet California.

I knew a couple (worked with the wife)… he was a statie in CA…. “retired” from CA after 20 years, with a vested pension and then went to be a cop in Huntington Beach and worked long enough to get a second pension. The trick is that they “pack” overtime and raises in the last year that has some kind of effect on the overall pension amount. Plus COLA.

They have a mountain ski house (Mammoth). A beach house (Huntington Beach). A motor home for their trips to AZ towing their ski boat. Everything is top notch.

As a patrolman. Not a captain. Not a chief. A patrolman.

I live on the next best planet – IlliNoise.

It appears that our planet learned a lot from your planet 😀

I always wondered why state workers (not sure about Gov) get to retire after 20 or 30 years and start receiving a pension when the rest of us smucks have to wait until 65 or longer.

They have unions who negotiate on their behalf.

To ru82. I’m a federal officer and can help with your question. The pension and health benefits are a recruiting tool, as long as the retirement age based on year of birth. Starting salaries are very low relatively speaking. There is matching 401k for first 5%, but we also pay in towards our pension. The government promotes a three-legged stool of pension (now only about 30% of average high three salary for most), TSP 401k, and social security. I’ve never received stock options, sporting event tix, and have to refuse even a dinner invitation from private firms due to any potential conflict of interest. I also have to submit to a background investigation every five years to demonstrate good standing with financial and personal relationships. Though the pay eventually catches up to provide a comfortable life, you never get rich as a federal employee, so the trade off is early (ish) retirement.

My friend in CA retired as a high school teacher with a pension of $100K. He owns a 2 million dollar home, has a RV/Bus, paid $550K to roam around :-)

Plus they get gold plated medical, Rx and dental for life. Shhesh…

Don’t overlook the pay and benefits of lifeguards in California. Also, if cops scam the state by claiming a disability when they retire. This means their pension payments are exempt from state income taxes.

Oy Vey

How much does a Public School Teacher make in Texas? The average Public School Teacher salary in Texas is $53,853 as of May 27, 2022, but the range typically falls between $44,980 and $65,661. Salary ranges can vary widely depending on the city and many other important factors, including education, certifications, additional skills, the number of years you have spent in your profession.

https://www.salary.com/research/salary/benchmark/public-school-teacher-salary/tx

Sorry Wolf, forgot about the link thing.

What about school principal’s salaries ?

It is no secret that at schools and especially institutions of higher learning non-teaching administrators grossly outnumber those who teach.

It’s not a secret, it’s false. The ratio of staff to admin in public primary and secondary schools is higher than any other industry in the US, (@13:1 employees to admin.) For example, the ratio in government/public admin is more like 3:1.

Texas teachers also do not pay into Social Security or Medicare, so they will not have that when they retire.

TX doesn’t have a massive pension problem generally. CA, IL, NJ, and weirdly, KY do though.

Texas has a huge pension problem.

Brent, does that pension mean total $$ given to person per year, or just total $$ to be disbursed to them? Thanks

Pension amounts are usually always given per year.

MR RICHTER DOES NOT APPROVE OF POSTING LINKS IN COMMENTS – PERIOD !

But… in my first comment I used a loophole 😀

Substitute . for dot and / for slash and see for yourself.

Top 20 are drawing >$1.5M YEARLY

If you click Heroes’ names there are additional entries like additional lump sum payment ( another $1.5M, sort of retirement gift ?)

FOLKS FROM TRANSPARENTCALIFORNIA WEBSITE – THANK YOU !!!

Let me see.

It’s different this time, right?

There really is something for nothing?

The US is exempt from the economic reality which applies to everyone else, both now and since the beginning of civilization?

The answer to your question on pensions is that they won’t, not in the same purchasing power.

As much as I want to believe an old wisdom7 that it’s not gonna be different THIS time – I am awestruck and deeply amazed by the craftiness of Financial Devils.

Ross Perot in 1992 made polite noises about balancing Fed budget…

Then Paul Krugman proclaimed “Deficits dont matter !”

And it is onward & upward since then, with no end in sight…

Brent wrote: “Then Paul Krugman proclaimed “Deficits dont matter !”

Wrong. If Krugman did say it, he was just repeating talking points from others.

“Reagan proved that deficits don’t matter,” Vice President Dick Cheney said when the Bush administration sought a second round of tax cuts …”

Cheney’s sidekick is also reported to have said ” “Stop throwing the Constitution in my face,” Bush screamed back. “It’s just a goddamned piece of paper!”

You all might want to keep this in mind, it is what the .01% think when talking up stuff like “mandates” that might restrict what they want to do.

In theory, it’s “onward and upward” until the USD FX rate starts crashing. This is the ultimate limitation on what you are describing, and the US isn’t any different than anyone else.

In the real world, it’s also based upon psychology. Look at the performance of the major asset classes in other major economies. The only universal mania since the late 90’s is bonds, credit and debt. This is the “mother of all bubbles” (reflective of currency expansion) and without it, the other bubbles have no oxygen and die.

In a highly leveraged financial system, no government or central bank can keep the financial markets and asset values from collapsing. They can only reflate after the bust, as they can’t act fast enough to prevent it.

In Japan, it’s been over 30 years and stock prices are lower. Real estate, I don’t know but at most only somewhat higher in most of the country. In Europe, the credit bubble didn’t reflate the stock market, though recently some markets have exceeded the 1999 and 2007 highs, nominally. Real estate is somewhat in a bubble in the sense of recent appreciation. China has a massive real estate bubble, but stock prices are off by more than half from the 2007 peak. Credit has expanded by a factor of something like 5X.

The point is, it’s not a mechanical process with a guarantee that the money will go where we think.

@Old Ghost

“Important political fact, which is that whatever you would do with the deficit, the public won’t notice. In 1996, a majority of Republicans thought that the deficit had increased under Clinton, even though we had in fact been on an incredible run. So no, I mean, the deficit doesn’t matter. The economy matters. And that’s why somehow or other, Obama has got to get jobs being created.”

Paul Krugman, “This Week with George Stephanopoulos” show, Nov 29, 2009, ABC transcript.

Don’t you realize that almost 50% of the US government debt of $30 trillion matures each year and has to be and is repaid in full and that new US Treasuries have to be issued to float the total debt again at whatever the prevailing yields (interest rates) are?

Wolf,

You stated “Only a small percentage of Americans own any significant amount of equities…….”

That is misleading. A decent amount of Americans own lots of equities INDIRECTLY through their 401k funds/annuities/pension plans/etc. These are ETFs, mutual funds, Target Date Funds, etc. The 401k plan at my current employer offers about 10 different types of mutual funds that are not index funds and only 2 of them did not have Facebook/Amazon/Microsoft on of their top 25 holdings.

It’s not misleading when understood as a percentage of total stock value. 2019 data from the Federal Reserve shows that 70% of all stock value is owned by the top 10% of income earners. The bottom 60% of earners only own 7.3% of total stock value. The 60-80 and 80-90 percentiles own another 11% and 12%, respectively. A stock market crash does not impact the vast majority of American households directly. The Fed data includes both direct and indirect stock ownership.

Also, far fewer Americans have employer based retirement plans than you seem to think.

Nunya,

The bottom 50% of households in terms of wealth hold essentially zero stocks, directly or indirectly. Their major “wealth” are durable goods (cars, phones, etc.) and small amounts of home equity.

The next 40% (to round of the bottom 90%) hold very modest amounts of equities.

Most of the equities are held by the top 10%.

https://wolfstreet.com/2022/04/03/my-wealth-disparity-monitor-of-the-feds-money-printer-era-holy-moly-april-update-of-the-greatest-economic-injustice-in-recent-history/

Yes, from a $ standpoint, but that’s a narrow way of looking at it. Marginal utility matters a great deal.

For that 50-90% bracket, for instance, losing money on their investments has an outsized financial impact on their lives compared to the top 1%– even if the top1% lose far more in $-terms.

There’s a psychosocial component as well, but that’s another discussion.

Were they somehow incapable of reading the stock prospectus of any stock or fund they ever bought which clearly states THERE IS A RISK OF 100% LOSS IN EQUITIES (stocks)?

Good chart.

About a year ago I came across a chart that had the cumulative bailouts (TARP, COVID, etc) plus the QE added together since 2009 and it was between to 25 trillion to 30 trillion. Anyway, this would have been the equivalent to handing out $80k to every person in the U.S. which would also be about $210k per family. Instead, it mostly all went to the top 1%.

IMHO. That is partly why we did not see inflation during many of the early bailouts. One person can only wear at one time on shirt, pants, and shoes at one time and can only eat 3 meals a day. They can only buy so many kitchen tables, lazy boy chairs, or bicycles. They can own several cars but they can only drive one at a time. You get the point.

So those kind of things did not go up in price. It is the things that were rare, like collectibles, land, etc that were going up faster than inflation as the top 1% were chasing those items over the past 13 years. Finally when the Government started to give everyone some money and forebear their debt, inflation eventually took off as supply could not keep up with this new pent up demand with free money.

There is all this talk about supply chain issues (which there are), but somehow China had an all time trade surplus record in 2021 and after 5 months this year, China is ahead of last year. Looks like the supply issues is because they cannot increase production fast enough?

People talk about a shortage of chips, but the chip makers are setting records on how many chips they produced and sold. Also you read about a shortage of truck drivers but there more truck driver on the road than ever in any other past years. Part of the inflation issue is certainly demand.

Just try to book a hotel on the beach this year or last. People are paying record prices.

Crazy. Hopefully higher interest rates will cool things off.

The net amount was noticeably less than your numbers, not even close. The USG didn’t give anywhere near that much away and the FRB doesn’t give any at all, except as interest rate subsidies. Look at the national debt.

Where do you come up with such wild and false numbers?

I got the numbers from talkmarket.com They had table and listed bailout amount in a spread sheet.

I was off. The total is 36 trillion. I was being conservative. That was enough for 270k per family

https://talkmarkets.com/content/economics–politics/the-rescues-are-ruining-capitalism?post=284508

It’s true that stock ownership is very heavily weighted to the 1% and even more to the 0.1%.

But a 50% decline hits people lower down the economic scale much harder. A billionaire with 50% lower net worth will have no appreciable change in lifestyle. A 60 year old aiming for retirement on a portfolio of a million or so is looking at 5 extra years of work. And the 30 year old working for the company propped up by speculation in stocks is unemployed in that scenario, so stock ownership is only part of the equation.

“Their major “wealth” are durable goods (cars, phones, etc.)…”

The slowest of depreciating assets ;P

And what about the poor government property tax income, when property values plummet! /s

Well it’s not happening in beach towns like westerly RI or margate NJ or South Florida like Boca Or Delray Beach. In fact still multiple offers and prices still sky high. Higher rates in luxury vacation markets aren’t having any effect. All cash buyers.

You’ve discovered a correlation between learning disability and coastal living. Excellent work!

A few months ago I was in Orlando at a Disney resort and started talking to a home remodeler from Miami. He was telling me 80% of the work he has been doing the past 2 years has been for people moving from New York. They had money flowing out of their pockets. Tearing down $1 million dollar homes and building $3 million dollar homes. Tearing down $4 million dollar homes and building / renovating them into $10 million. He said he has a rental and 3 years ago he rented it for around $2k and now he rents it for $3.9k.

He was traveling with a buddy who did not believe he was renting his rental house for almost $4k as this guy lived on the same block but had not been checking out current rents. We went online to several places that rent homes in Miami and sure enough, the going rate was about $3.7k to $4.5k.

The buddy said holy cow, I am going to rent out my home as my payment is only $1500 and I will make bank and pocket $25k to $30k a year. But then the remodeler said….where are you going move your family to live? You will not be able to afford to buy in the your neighborhood or Miami anymore. You would have to move to the Midwest. LOL

Randy these are early days. Coastal RE will not be immune.

Love,

San Diego 1990-1995 and 2007-2012

You do realize real estate is lagging compared to the stock market? Are you expecting demand and prices to fall off a cliff overnight? Or are just a realtor?

Its happening in Florida. Everyone is slashing prices by 10%, tons of inventory flooding the market. Things are starting to sit.

My 1st mortgage, way back in the 80s, had a high rate of interest. So we bought what made sense and paid down principle as fast as possible. We started from the premise- let’s not get too much house and worry about the loan. Today they start with how much monthly payment can I get? Even car dealerships start with negotiating the payment. We have lost our way and deserve what we get. My Grandfather used to say – we need a good old fashioned recession. I’d like to rates go up to reflect risk. Maybe T bonds would yield more. Maybe even keep up with the cost of living?