The wealthy got immensely wealthier. Everyone else paid for it via rampant inflation.

By Wolf Richter for WOLF STREET.

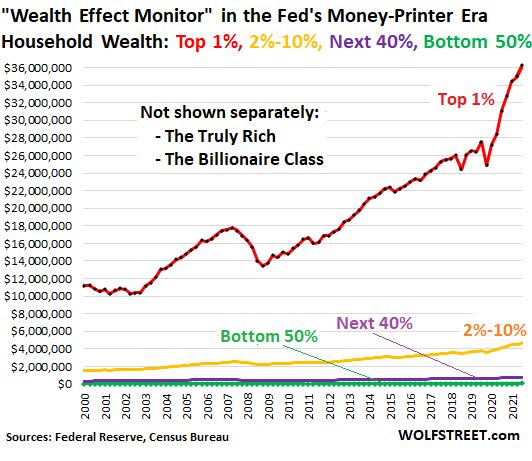

The Fed’s own data on the distribution of wealth in the US is a quarterly report card on the Fed’s official policy goal of the “Wealth Effect.” It has now released the data for Q4. The Fed uses monetary policies, such as QE and interest rate repression, to create asset price inflation and make a relatively small number of large asset holders vastly wealthier so that they might spend more. This has been explained in numerous Fed papers, including by Janet Yellen back when she was still president of the San Francisco Fed.

The Fed’s wealth distribution data divides the US population into four groups by wealth: The “Top 1%,” the “Next 9%” (2% to 10%),” the “next 40%,” and the “bottom 50%.” My Wealth Effect Monitor divides this data by the number of households in each category, to obtain the average wealth per household in each category. Note the immense increase in the wealth for the 1% households after the Fed’s money-printing scheme and interest rate repression started in March 2020:

As you can see from the steep curve of the red line, the “Top 1%” households were the primary beneficiaries of the Fed’s policies since March 2020. These policies were designed to inflate asset prices, and only asset holders benefited from that. The more assets they held, the more they benefited.

The Census Bureau defines a household by address. Each address is one household, whoever lives there, whether they’re a three-generation family, four roommates, a married couple, or a single person.

So here is the average wealth (= assets minus debts) per household, by category in Q4, 2021:

- “Top “1%” household (red): $36.2 million.

- The 2% to 10% household (yellow): $4.68 million.

- The “next 40%” household (purple): $775,000.

- The “bottom 50%” household (green): $59,000.

But wait… durable goods.

The Fed includes durable goods in this wealth. Durable goods are motor vehicles, boats, furniture, electronics, etc. They’re consumables – unless they’re art, antiques, or classics – and their value will ultimately go to zero. For the “bottom 50%,” their durable goods account for nearly 20% of their total assets and for nearly 50% for their total wealth (assets minus debts).

The Billionaire Class got more billions.

The Fed doesn’t provide separate data on the truly rich (the 0.01%) and the Billionaire Class, a distinct royalty-like class in American society whose names often have the royal title of “billionaire” in front. They’re the biggest beneficiaries of the Fed’s monetary policies.

The top 30 US billionaires have a total wealth of $2.12 trillion, sliced into 30 slices for a wealth of $70.8 billion per billionaire, according to the Bloomberg Billionaires Index.

Compare that to the bottom half of the US population – the “bottom 50%” – who have a combined wealth of just $3.7 trillion, sliced into 165 million slices for each individual. For them, the inflated real estate prices just mean higher housing costs.

Reckless usage of percentages can kill someone.

If I give my favorite homeless guy $5, and he already has $5 in his pocket, I increased his wealth by 100%, which is a huge percentage jump in wealth. But he’s still homeless and still doesn’t have any wealth.

Percentage increases are regularly touted to show that the wealth at the bottom increased, when in fact, it increased by only minuscule amounts of dollars because the bottom 50% have so little that even a big percentage increase still amounts to nearly nothing in dollar terms, compared to the billionaire class.

When the wealth of the bottom 50% increases by 5%, they gain about $3,000. And when the average wealth of the top 30 billionaires increases by 5%, they on average gain $3,500,000,000. And the wealth disparity just blew out.

Greatest economic injustice committed in recent US history.

Since March 2020, the Fed printed $4.9 trillion and repressed short-term interest rates to near-zero in order to inflate asset prices so that the asset holders would get immensely more wealthy, in line with its doctrine of the Wealth Effect.

This act has produced the greatest economic injustice committed in recent US history.

My “Wealth Disparity Monitor” tracks that economic injustice on a quarterly basis by showing the difference in average wealth between the top 1% and the bottom 50%, per household, based on the Fed’s own data.

In 1990, the wealth disparity between the average “top 1%” household and the average “bottom 50%” household was $5 million. In Q4 2021, it ballooned by another $1.2 million from the prior quarter, and by $5.1 million year-over-year, to $36.2 million.

Since the Fed’s crazed money printing binge and interest rate repression started in March 2020, the wealth disparity between the average “top 1%” household and the average “bottom 50%” household has exploded by $11.2 million per household.

More wealth for the wealthy, paid for by crushing inflation for the rest.

The Fed’s policy of the Wealth Effect operates by creating asset price inflation through money printing and interest rate repression.

The bottom 50% of Americans — who spend all or nearly all their income on housing, transportation, food, healthcare, etc. — hold practically no stocks, no bonds, and very little real estate, according to the wealth distribution data from the Federal Reserve. When the Fed purposefully inflates those assets that only some people in society hold, it says F-U to the rest.

And this money-printing binge has now created the worst inflation in 40 years. Inflation destroys the purchasing power of the dollar, and it destroys the purchasing power of labor denominated in dollars. Just to get by, the bottom 50% spend all, or nearly all, of their income on consumer items – such as housing, transportation, and food. And they got mauled by this rampant consumer price inflation that this money printing has triggered. And they’re the ones paying for this act of the Fed to enrich the asset holders.

So average wages and salaries went up a lot, but by only a fraction of the amount that rents, and the prices of houses, used and new vehicles, gasoline, groceries, etc. shot higher. And the worker bees in this economy now have to tighten their belts further even as richest asset holders got vastly wealthier, thanks to the Fed’s policies.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wow, it’s almost too much to believe, but there it is, in all its color. WTF.

Yeah, the mainstream media never covers this. Wolf does a great job with this.

America is more than the 1% that the mainstream media covers 90% of their time. God Bless America.

Give up the TEE VEE I did 25 years ago and I am doing just fine!

Even the old television networks saw the writint on the wall. Endless variations of the reality television genre were their last gasp.

I am currently on old black and white TV series, crime noir and such, borrowed from local library.

LL Rogers

IMHO, TV reporters and achair wo/men are belong to ‘previleges mob with connections’ called ‘PRESSITUTES! It is being proven everyday!

The mainstream media from MSNBC to Fox News to New York times to Wall St. journal are all owned by billionaires.

Despite all this supposed “diversity” of media, all billionaire-owned media collude to censor and distract from topics that help billionaires.

It’s convenient to scapegoat the media, but how many would subscribe to a news source that only reported on the poor or those suffering? Or a TV network that had ugly news anchors? People would rather know how much toilet paper Elon Musk uses than a heartbreaking story about someone stuck in a ghetto.

Mainstream media? What about your representatives? Ever hear them complain?

andy-it’s a p-i-t-a citizen’s duty, but too many of us don’t even consider contacting/expressing concerns to our reps., let alone be able to name them when asked…

may we all find a better day.

91B20,

That’s a fool’s errand if ever I heard one.

It is exceedingly clear to me that my duly elected congressional and executive representatives in government have no interest in considering my wishes. In this brave new world, my meek and peevish voice has no bearing on the actions of those whose job it is to serve the loud and dominating influences of the rich and powerful.

Crunchy-i seem to have hit a nerve. (Or, given your expressed logic, why bother to post your ‘meek and peevish voice’ here?Have more confidence in yourself, fellow citizen!).

My apologies, in any case, though the challenges will continue to arrive…

may we all find a better day.

Well, since there’s no armed rebellion, the lower classes must enjoy their poverty.

this fiatmoney system is just so corrupt,, silver was much better with The gold standard,, silver People was much more equal

Like Incan wealth after the Spaniards arrived.

The simplicity of your graphics is elegant and exquisite. Making a picture of the correlation between a dependent variable, like the difference between wealth disparity, and the independent variable on the X access, time. The rich have gotten richer over time. My blue collar friends, who I worked my ass off to not continue to be one of them, a story for another day, like too say, no shit sherlock.

I submit that it illustrates the “too big to fail” philosophy writ large. Swaggering, pompous financial losers calling the shots, not unlike DJT.

Now they’re telling us that they are going to save us and bring inflation down to a manageable level for the average American with zero disposable income, haven’t had a raise for 30 some years.

I think that one learns to judge the resolve of another homo sapiens. I’m not feeling the vibe from Jerome. I know you promised to quit feeding the monster but you haven’t been able to move forward in a constructive manner, yet. Let’s face it Jerome, pulling the plug to end the $120 billion per month pumping machine, rather than extend it was hopeful. Not even too mention the magnitude of effort that you expended to battle the 10% inflation monster by drawing your 0.25% dagger and waiving it our menacingly, seemed like we were on the rite trajectory.

Democracy cannot survive in a society with this level of wealth and opportunity disparity. Like hate, greed destroys the vessel that contains it.

Alas, Jerome does not have the same testicular structure as his aspirational super hero, Paul Volker. Tall Paul, kicking ass and taking names.

Jerome has a bad bosses, the banking industry, who won’t let him do anything they don’t want him to do.

Like Congress, his grateful hands are tied.

Central banks have become our worst nightmare, academics selling a new way to spin history’s greatest financial failures.

How did it become so hard to be an every day guy where my faults became an issue, not the racist, homophobic thing I was raised with, more the body shaming while pointing out that we are being screwed.

It may continue until men like me are all dead, or a better society will arise as the young people take control of the world they are all bitching about.

It is a deliberate policy to benefit the people the Fed wants to benefit. I am always surprised when anyone thinks it could possibly be anything else.

I think of it like a monopoly game. A few players for whatever reason get the good properties and build hotels and income streams. A few players end up with properties that don’t generate much income. One player is the banker who wants the game to play for perpetuity. Every time one of the players is about to go bankrupt, splash the board, storm off, and end the game, the banker gives every player cheap loans and some free cash.

The game goes on a little longer. The players with little income keep having to pay the players with the best properties and hotels. They keep getting richer. The poor stay mostly about the same until once again someone is going bankrupt and they are about to quit and end the game. Then the banker who wants the game to keep going gives everyone cheaper loans and some more free cash.

Rinse was repeat.

The next question is why does the banker want the game to keep going? I suspect the answer is because he works for the US government. In turn, the USA wants its monopoly players not to fall behind the other monopoly players that are playing separate monopoly games in other countries. In all those other countries the bankers are using the same tricks to keep their games going. None of the bankers in any of the games want their players to go bankrupt, end the game, and fall behind their competitor countries.

There is one game that rules them all happening out of Davos. However, I believe it’s Dungeon and Dragons Apocalypse. They just wrote it on the Monopoly framework. After all the billionaire geeks rule this realm and explains the odd behaviors of late. Welcome to The Upside Down 2.0!

I doubt that the Fed deliberately set out to benefit billionaires. But when it slashes interest rates to ward off a depression and sky high unemployment, things sometimes turn out that way. In any event, the families of the rich and super rich of 2022 are a lot different than the ones mentioned in Ferdinand Lundberg’s book on American wealth published over 50 years ago. Back then the Duponts, auto Fords, Mellons and Rockefellers were among the richest in the country. Now, none of these families have even one member of the Forbes 400 list.

They went private is all, you just don’t get it at all!

Absolutely correct LLR.

As has been said on Wolf’s Wonder by many before you…

Good to see others understanding this.

Thank you.

You are wrong. Ford Motor Company is still a publicly held company but has lost market share over the past 50 years and there are more heirs to split the family wealth. Here is a list of the richest people in America in 1918 as compiled by Forbes: The last of the Rockefellers dropped off the list when David Rockefeller died a few years ago at the age of 101.

Anon,

Thanks for helping to dial back the discussion a bit.

Not to defend billionaires (they can pay for it) or the Fed (which at this point is neck deep in DC incompetence, corruption, and lies), but…

1) As you point out, a lot of this is much less some intentional *plan* to enrich billionaires than it is the highly predictable outcome of how DC tries to more-or-less centrally manage the economy using interest rates (ie, unbacked money printing).

Push interest rates way, way down for two decades to “restart” the economy/employment (how’s that record really going after 20 yrs?) and assets will go into crazy valuation modes of boom and bust, unmoored from fundamentals (because unsophisticated DCF analysis views current interest rates as perpetual interest rates…) and

2) As the charts hint at, on the corners, as interest rate policies flip from loose to tight, those very rich asset holders take the biggest hits (percentage wise…even with big losses, they remain very, very rich). Again, this is pretty predictable.

That said, the main problem seems to be more or less perpetual ZIRP for 20 yrs (brief reversals triggering asset craterings that panic a hysterical DC into going back to ZIRP very quickly).

But all this ZIRP simply (financially) papers over the fundamental problem (that DC lacks the guts, brains, and spine to acknowledge) – the accelerating deterioration in America’s productive competitiveness.

Put bluntly, China has been kicking our ass for 20 years.

But DC, being mostly made up of fools, liars, opportunists, and smugly self-serving sh*ts, will go to almost any length to avoid the near term sacrifices necessary to address the real, long term problems.

Destroy the federal budget for 50 yrs to buy off key political support, no problem.

Destroy the currency for 12 to 20 yrs to buy a few more re-elections, no problem.

Tell the American people the truth, about themselves, impossible.

So the Fed “accidentally” benefitted the wealthy without foreknowledge or intent? Suuuuuure. If their actions were going to harm the wealthy elite, the Fed would be shut down by a SWAT Team in one minute.

Get rid of the fed, and put a financially diverse representation on a Treasury controlled money creation team of smart people that are forward thinking enough to get the job done more fairly.

Easier said than done, but people like Wolf, and many others here understand the system and could help change things.

We need more activism, considering a lot of people seem to know what is going on.

Roddy,

I wouldn’t say without foreknowledge (you can’t pursue the identical poorly performing policy maneuver for 20 years without eventually learning *something*).

And as for “intent”…I think the Fed would claim it is a largely unavoidable byproduct of trying to use a single lever (interest rates) to manipulate an economy of 330 million people (“We can’t re-ignite domestic primary investment/employment through lower rates, without simultaneously goosing the value of existing assets (frequently absurdly)””.

Personally, I disagree with this (20 years is a f’ing long time to endure more side effects than results from a given policy) but that is my guess as to how the Fed would defend its stupidity/impotence.

ImplicitI,

“put a financially diverse representation on a Treasury controlled money creation team of smart people that are forward thinking enough to get the job done more fairly.”

The Fed would say, “Tell us your magic policy alternative and we’ll try it. If there were a “smart policy” alternative in the age of the internet, why are you hiding it, Mr. Bigshot?”

My personal opinion is that perpetual ZIRP (versus say pulsed loosening and tightening) is what has led to the insane overvaluations in the capital mkts (“making the billionaires richer”).

The Fed could have wrung excess out of the system many times without lastingly damaging primary invt (I consider startups/expansions primary invts, and capital mkts of existing assets, secondary invts).

Alternatively, massive tax breaks could have been given solely to primary invts. (That is on the Treasury/Prez/Congress, though).

And I’m almost certain that over 7300 days, the Fed has *internally* formulated alternative tactics it could at least try/experiment with – but that DC politics (including an enormous current and worse future Fed debt) keeps them from trying anything else.

“I doubt that the Fed deliberately set out to benefit billionaires.”

Benefit? The Fed created hundreds of billionaires in just few years. Snapchat app is worth billions of dollars. So is Twilio, so is Snowflake, so is Etsy, whatever they are. Need I go on.

“I doubt the Fed deliberately set out to help Billionaires.”

And the check’s in the mail.

“interest rate repression started in March 2020” Interest rate repression started with Greenspan and continued with Bernanke, Yellen and Powell.

By deliberately stealing from poor savers and giving their tiny wealth to the very rich, the have gutted the core of the U.S.A.

Now, rampant inflation will increase taxes, via higher prices for Sales Taxes and bumping up poor wage earners into higher Income Tax brackets.

We have devolved all the way back to Princes in Castles and peasants grubbing for survival.

“ Benefit? The Fed created hundreds of billionaires in just few years. Snapchat app is worth billions of dollars. So is Twilio, so is Snowflake, so is Etsy, whatever they are. Need I go on.”

Well, if you’re trying to find something I use, you’re gonna have to…

Got cut off…

Your gonna have to keep going down the list…

Sorry…

Where are Rothschild clan

On the beach at Illuminati island…

Flea, didn’t you get the invitation?

COWG that was one of your best replies ,in top 5

There is only one Rothschild on the current Forbes list of world billionaires and I doubt that he is even related to the European Rothschilds. The source of his wealth (a mere $3.7 billion) is given as Facebook stock. Rothschild wealth was hit hard by two world wars, related inflation, many heirs and some divorces.

Correct, in free market top people will change because people consumption preferences change.

Vilfredo Pareto Circulation of elite and Vilfredo Pareto curve applies as we go up the pyramid of wealth. It always has. He found that 20% of the residents in every European nation he surveyed had 80% of the income.

So, 4% of the population (.2 x 20%) own 64% (.8 x 80%) of the wealth.

Let’s keep going. This means that 0.8% of the population (.2 x 4%) own 51% (.8 x 64%) of the wealth.

Key elements of the capitalist class display great continuity. In 1974, more than 100 years after John D. Rockefeller founded Standard Oil, Vice President Gerald Ford became president after Richard Nixon resigned. To fill the vice presidency, Ford chose Nelson Rockefeller, John D.’s grandson. This allowed Congress to look at his wealth. In a report for Congress, William Domhoff and Charles Schwartz detailed: “The Rockefeller fortune, although nominally distributed among many individual members of the Family, is actually coordinated under a central management” that was located on a particular floor in Rockefeller Plaza in NYC. They wrote that “fifteen employees of the Family, working out of this office, have been identified on the boards of directors of nearly 100 corporations over a number of years” and that “their combined assets add[ed] up to 70 billion dollars.” In 1992, the New York Times described how the Rockefeller foundation was safeguarding this wealth, which was estimated between $5 and $10 billion, for the fourth generation of the family.

What about today? In May, Rockefeller Financial Services sold a minority stake to RIT Capital Partners. (The “R” in RIT stands for Rothschild, a famous European capitalist family.) According to the London Telegraph, Rockefeller Financial Services had £22 billion, or about $35 billion, in assets. Venrock, whose name is an amalgam of ventures and Rockefeller, is a venture capitalist firm. It was an early backer of one of the emblems of the “new economy,” Apple Computer.

One study estimated that in 2000 the combined wealth of the Rockefellers, the Du Ponts, the Mellons, the Schwabs, the Hearsts, the Phipps (Henry Phipps was the second-largest shareholder in Carnegie Steel) was around $54 billion. The individual members of these families might not be as famous as their ancestors or the newer capitalists, and they probably prefer not to be in the news, especially after what happened to Paris Hilton. But they still own and run much of America. From the article, “The U.S. Capitalist Class, Past and Present- Who Owns America ?” 2012

https://icl-fi.org/english/wv/1010/capitalists.html

I wouldn’t argue that *some* very rich families have been able to perpetuate great wealth intergenerationally.

But…across multiple generations (say 3+) having multiple kids (3+) does its thing and tends to subdivide wealth down to much lower levels. The brain/money genes tend to dilute too and one playboy can terminate an entire branch of a rich family.

My general sense is that most mega rich families sink due to these intergenerational dynamics…the ones that don’t are in a definite minority.

Thanks MS for your due diligence on this question.

NAH c10,,, they just become more better at hiding their wealth in the many mountains of very clearly unknown unknowns in the financial paper,,, no matter if that paper is ”fiat currency” or ”derivatives of each and every kind” etc., etc…

Having worked for some of the ”old money” folks many decades ago,,, 3rd or even 5th generation of the founders of their dynasty,,, they were very clear about maintaining their wealth,,, maintaining and increasing their privacy,,, and especially increasing as best they could the intelligence, etc., of folks of both/all genders being married into the dynasty.

WE the PEONs should be so lucky/fortunate/blessed , eh

The Reece Committee Hearings Exposed America’s Major Tax-Exempt Foundations as Moving Toward a One-World State

In 1953, Carroll Reece, Congressman from Eastern Tennessee, had his committee begin an investigation into the American Establishment: the Tax-Exempt Foundations. (These are sometimes erroneously cited as the Reese Committee Hearings.) The hearings were held for two weeks. Then, without warning, the committee stopped them.

The Committee’s findings were summarized by the committee’s counsel, Rene Wormser. His book, Foundations (1958), has become a vital document in understanding the leftward drift of America’s elite. Fortunately, it is still in print.

for serious researchers into the secret take-over of the United States, beginning in 1913, this document will open a closed book in American history.

So the Fed props up the billionaires who own the media assets, which distract the hoi polloi from the shenanigans the Fed does…

Can anyone say ‘American Oligarchs’?

It is easy and perhaps excessively imputed, to impute malevolence, but, given the prevailing economic situation, what would you have suggested the FED do?

“What would you have suggested…”

See above.

In very brief,

1) Pulsed (vs. essentially continuous) ZIRP would have wrung out absurd asset overvaluations,

2) Focused tax benefits for primary investments (job creating startups) vs. Existing secondary investments (stock/bond/housing mkts),

3) Some/any evidence of alternative policy experiments at Fed or Treasury for last 20 failed years

As many have said, it’s more to do with stupidity and incompetence of these third rate hucksters than a plan. However, their cover-your-derriere plan is endless printing, and so we have a different level of stupidity.

“Never attribute to malice what can explained by stupidity.”

Robert Hanlon

I don’t even refer to it as public policy anymore, I consider it fraud, theft and economic terrorism against the people of the US. What Jerome Powell and Co. were doing was not even in their mandate. They should be arrested and charged with treason.

This inflation is the mopping up phase of the 40-year class war that most Americans lost while they were watching the culture wars on TV.

I figured out back in the year 2000 that many Americans voted against their economic interests and for their religious prejudices. They made their choices over the years and now they have to live with them. I am still benefiting from the Bush dividend tax cuts of 2003, even though I voted for Al Gore.

Many Americans do a terrible job managing their personal finances and it is not just people with low paying jobs.

Americans voting against their economic interests is usually the best option voters have. Take for example this last election where voting for candidates that promised stimulus checks would have been voting for the economic interests of the voter. All of those transfer payments are contributing to shortages, rising food costs, and rising housing costs.

Voting against your economic interest as a citizen at least means a vote for someone who isn’t pandering to the use of the redistributive powers of the government to pick winners and losers.

And in your case, dividends rose significantly in most publicly traded companies according to the NBER after those tax cuts. If you’re so butt hurt about it, why don’t you write a check to the government giving all of those extra dividends back since 2003?

“Voting against your economic interest as a citizen at least means a vote for someone who isn’t pandering to the use of the redistributive powers of the government to pick winners and losers.”

Brain dead comment. You really believe this? lmao news flash, they are all using the redistributive powers of government to pick winners and losers. The elites have been winning that game for decades. Did you not read the post you’re commenting on?

Government’s power is not about picking winners and losers.

It’s about creating a more stable and equitable society with equality of opportunities, but not outcomes.

With said efforts occurring against a backdrop of elites who constantly game and exploit the political system to their own benefit and to the detriment of the majority of citizens.

BB,

Not to insult you but that is pure BS…

Free market capitalism…

Nobody forced anybody to buy anything from anybody…

People bought Amazon Prime because they thought it benefitted them… not because of Bezos and the stock price…

People didn’t buy Microsoft because of Gates… they used it because it came free on their new PC… there were many alternatives out there but they were too lazy to find them… what they had basically free suited them just fine…

The “elites” as you call them, derived a benefit from people “buying” their products, not because anybody ( government) held a gun to their head…

Understand the basic concept of “ willing buyer, willing seller”….

The government didn’t game that…

People who don’t understand that basic concept have nothing, repeat, nothing to bitch about…

The majority of the citizens are dumber than a box of rocks when it comes to introspective and critical thinking…

Don’t give them more credit than they deserve…

Ask phleep…

He deals with this every day…

COWG,

“Free market capitalism…”

Hahahaha, that was funny. I’m laughing so hard my eyes got teary and I couldn’t read the rest.

On an article like this??? Hahahaha

I wish we had it. What we have is crony capitalism for the rich in normal times and socialism for the rich when things get tough and they get bailed out and made richer at every twist and turn. The Fed manipulates the most important cost of all, the cost of capital, and the Fed creates trillions of dollars to manipulate markets with. The federal government is guaranteeing many trillions of dollars of mortgages, including mortgages of landlords that own big apartment buildings, which brings the borrowing costs down. Etc. etc. There is no “free market capitalism.”

Thank you Wolf.

The Fed has deliberately violated Rule 1: “Capital must have value.”

The “cost of capital” has been driven down to zero, and lower with inflation added to the equation. Of course, not all borrowers are able to take advantage of this manipulation.

And on Rule 2: “Future capital shall have more value than current capital.”

In a few minutes this will change, but 3 Year is @ 2.58% & 30 Year is @ 2.44%.

Wolfster,

You went flying off on a tangent here…

My response was directly related to complaints about the “elites”…

And who made them “elite”…. The people who made a free and conscious choice to use the products and services ….

My point being that if you have helped these people become who they are , then you do not have a right to bitch about it…

Especially, when you have been trying to benefit from these very same “elites” by buying their stock which helped make them more elite…

So yeah, “free market”…. Nobody made you buy the products or the stock that made them “elite”… most people bought into the “elites” because they thought the “elites”were going to make them money…

The economic conditions today only came into being a short while ago…

Many non-elite have benefited from this as well…

Greed, although disguised as altruism at times, is the free market, mon frere, and that is not necessarily bad…

But let’s don’t do the greed is good thing please…

And you can’t tell me you wouldn’t be greedy either…

If the government had a program that paid you 7 million a year to dig ditches, would you not take it and leave the blog… be a fool not to… and not give a damn about those who didn’t get that job… only glad that you were smart enough to take advantage of that opportunity…

You’ve run many articles on the fall of many stocks which would have created more “elites” …what happened? …

The “free market” voted them out by not buying their products and services…

Do I have a problem with elites… not particularly… i have more of a problem with people whose greed made them that way and then complain about it…

I do see your point…. And raise you mine :)

This is easy Buffett,Bloomberg and many others bought up media companies they control content ,really not much different than China Russia

The Reece Committee Hearings (1954): How Leftist Non-Profit Foundations Undermined the Constitution

Congressman Carroll Reece investigated non-profit foundations in 1954. His findings were clear: they were run by Leftists. They were committed to the creation of a one-world government.

Dodd describes the hidden agenda of these large foundations. This agenda collapsed along with the Soviet Union on Christmas day, 1991. It was the most spectacular institutional failure in modern history. The largest and most powerful empire since the Mongols shut down peacefully. In doing so, it shut down the agendas of these foundations and related multinational corporations. They had to re-organize their agenda completely.

The West did virtually nothing to achieve this extraordinary victory. It was done behind the Iron Curtain by dedicated members of decentralized resistance movements. The looming collapse went unnoticed almost until the end, sometime around 1988 and 1989. It caught the West by surprise. Neither the internationalists nor the professional anti-Communists saw it coming.

If these same billionaires didn’t also own the media, everyone in the fed offices would have been dragged out by the hair the 1st time the fed created this boom bust cycle. (Or the 5th time or the 10th time.)

Next is part 2, the bust, where those few at the top gobble up major assets for pennies on the dollar when things fall apart and more competition vanishes. (See 2008) Eventually this path leads to one giant global montsroity which owns everything, and the billion and trillionaires each manage their own segment of it. Oh wait, were already at that part.

724 billionaires now (or recently) versus 13 in 1982 or 1983. The majority of their “wealth” is a bag of hot air because the economy hasn’t produced anything close to that kind of value add in the last 40 years, even adjusted for inflation. Anyone can verify this by looking at the ratio asset values to GDP where estimates are periodically published.

For most, it’s inflated “value” from the mania. But for many, it’s worse than that. They own large or meaningful stakes in companies that have no substance, like Uber which is a ridiculously overpriced taxi dispatch service.

If they are smart enough, they will have already diversified into other still overpriced assets that will at least hold some of its value when this house of cards collapses. My prediction is that vast majority will end up losing most of their wealth anyway, up to 90%+ in the upcoming multi-decade bear market.

It’s not possible to preserve what never actually existed.

Starting to happen. Poor Mark Zuckerberg lost 30% of his wealth in only few days. The greatest con-man of all time Elon Mask is still on the upward momentum. Jeff Bezos is suspended mid-air like Wile E. Coyote at the moment.

Exactly. The redistribution from the wealthy to working people started in the early 30s and lasted over 4 decades. All asset classes deflated together, then asset growth restarted with those owned by working folks.

Oh we’re barely there, so much further to go.

In the near future they’ll have bought up all the residential property so you can’t own real estate assets, only rent it.

They’ll take companies private so there’s no stock market to invest in. Ever wonder why you can’t buy SpaceX stock? The *right* people can and you ain’t in the club.

You won’t own anything, you’ll only be allowed to buy licenses to use products in specific ways for specific times until your rental license is up.

Neo-feudalism is our future where a small oligarchy of billionaires “owns” everything and the 99.9% of serfs are only allowed to rent pieces of whatever price the monopolists decide to charge.

Of course the stock market will survive. Where else can the hedgies dump loser companies they took private and ran recklessly into bancko? (In some cases the same companies over and over)

If all the renters of the USA work together and just don’t pay…. then what?

If it’s one person then it’s an issue, an eviction after some late fees. But if everyone doesn’t pay, then it’s popcorn time! Renter strike.

Could also build databases of large corp owned residential properties for rent and make it widely available. Then people could avoid them, or protest against them.

“ You won’t own anything, you’ll only be allowed to buy licenses to use products in specific ways for specific times until your rental license is up.”

The rise of Microsoft is your example…

Gates bought the original MS-DOS from the creator, then licensed it for what, a dollar a machine, to the PC makers…

There were several versions of DOS that were available but Gates locked up the distribution because if you wanted a different DOS, you had to pay extra…

Since everybody already had it on their machines, that’s what everybody tended to keep…

Same with the Windows follow on… if it came on your machine, you were pretty much going to stay in the Microsoft environment…

I always say the one thing Microsoft gave us was an acceptance of an 80% solution…

You computer guys who have been around since sand, feel free to correct me…

So how soon from now do the unwashed masses gather at the gated communities with torches and pitchforks?

Civil government, so far as it is instituted for the security of property, is in reality instituted for the defense of the rich against the poor, or of those who have some property against those who have none at all.

– Adam Smith, Wealth of Nations, V, 1, ii.

When they are starving and have nothing left to lose!

I was surprised that Liberal Politician Adam Vaughan was still alive after laughing at Canadians on public television and defending the rich global elite.

When there are enough starving & homeless Canadians, the one way bus ride to Bridle Path.

There were lots of Canadians riding the rails looking for work during the Great Depression but no one stormed the estates of the Eaton family at Ardwold Gate in Toronto or the Bronfman mansion in Westmount, Quebec.

Canadian stormed the White House in 1812. Anything but the British compact elite.

I think we’re heading towards Huxley’s Brave New World, where the masses will be given enough freebies to be happy while living under a totalitarian government. I always thought it would be 1984, but it now looks like the other, with all the sex, drugs and endless entertainment to keep those at the bottom happy.

The ones at the top are the ones with all the sex, drugs, and entertainment.

Have you not seen the mega yachts being consficated?

Countries like America, Canada, the UK, EU etc have a “mating crisis” where men are falling under the socio-economic ladder, and as high as 50% of men have not dated in the past year. Meanwhile, the top 1% of men have been as good as ever.

In addition to wealth disparity, there are other disparities. Dating apps have the statistics.

The media will convince the people with torches that they are the enemy of the people with pitchforks, and they will attack each other.

It wasn’t enough for them to steal your wealth, now they want to tell you what you can and cannot eat, how to live, etc. These people need to disappear.

It’s a return to feudal times with indentured servants paying outrageous rents to landowners and minor fiefdoms (such as Blackrock). Only this time around the scenery is colorfully decorated with fast cars and smartphones instead of horses and the town crier.

You mean fast electric cars, dont you?

The Ferrari SF90 Stradale has a 4 liter twin turbo V8 and three electric motors. Not totally electric, but the addition of Maxwell’s equations puts it at the apex.

It is fast. Like, really fast fast.

Dan, Japanese have trains faster than that.

Andy,

Yes, but for six hundred grand, I could drive a Stradale.

Next they want to steal your soul

I’m not using it anyway.

> Next they want to steal your soul

I’m not using it anyway.

I sold mine to the Devil with a 12 month clawback. Just ask your local Wells Fargo bank manager for details.

It would be interesting to know the median wealth of the top 1 percent.

Agree this kind of number (such as net worth by percentile of net worth) is seldom seen. And suspect that’s partly due to the press finding it variously indigestible or unappealing to its owners, but also due to difficulty in calculating.

And agree that median values are often more illuminating than averages.

So, a median figure for the top 1% would tell us something. But would it be very surprising – that is, would it upset our preconceptions? Maybe. It would improve the accuracy of our perception of the typical one-percenter.

But I’m interested in the social and political side effects of concentrated wealth, and wonder how the 1% median wealth number could help understand that.

Given the wealth disparity even within the 1%, it would be a lot more meaningful to stratify it even further.

The main point which isn’t discussed (generally, not specifically on this website) is how this money translates into power which is what ultimately matters on this subject once the numbers get big enough.

I don’t believe very many of the billionaire class are really that influential. Sure, they can buy local influence and sometimes bribe their congressional caucus, but only a very low number are much more influential than that and not all of these people are super wealthy either.

It’s still who you know or being part of a larger group. Most of the (supposedly) super wealthy are new money. My bet is that the old money is still usually a lot more influential, most of the time.

In the “next 40%” group where the average wealth is $775K. the distribution is also still lopsidedly toward the top. According to FRED, the median household net worth was $121K in 2019.

Corporations are people too. They have robotic feelings of increasing the bottom line at all costs; that’s why we have lobbyists.

It would be interesting to see where and how much each of the 1% spend on lobbying efforts.

They must pay off the politicians to help protect the noble interests of their oligarchies and monopolies.

The many industrial complexes help keep our super wealthy overlords in control, and the peons in their place.

Please send that list to my office, so we can rush a bill to outlaw lobbying and put term limits in place.

Gotta start somewhere.

Please send that list to my office, so we can publish it asap. Than-you

As Buffett said,I quote I couldn’t spend my money in a hundred lifetimes ,also think he is one of greatest investors of all time ,just bought a insurance company for 11.6 billion with a 13 billion bond fund = genius

If you buy an insurance company, you also buy the liabilities of that insurance company, including the future payouts. So you have to look at the value of assets minus the value of liabilities to see what you get. Buffett knows this because he runs a huge insurance empire.

Wolf, is there an extra zero typo in these figures?

So here is the average wealth (= assets minus debts) per household, by category in Q4, 2021:

“Top “1%” household (red): $36.2 million.

The 2% to 10% household (yellow): $4.68 million.

The “next 40%” household (purple): $775,000.

The “bottom 50%” household (green): $59,000.

No. But note that this includes durable goods. So for the bottom 50%, it includes cars, furniture, appliances, electronics, etc.

Absolute numbers matter when calculating ROI. Maintaining a minimal positive ROI is required to preserve asset values. The top 1% needs to see $360 billion in returns just to maintain an ROI of 1%, which is actually a negative return in ‘real’ terms.

Likewise, interest payments on the Federal debt are now over $3000 per working person. With total assets by all holders now estimated at $64 trillion, $640 billion per year must be paid out of earned income just to maintain a nominal ROI of 1%.

Everything is about flow. If the flows that sustain ROI go down, the foundation to the house of cards begins to quake. This has happened several times in the last 20 years or so. Once things get so top-heavy, the only options are drops in the value of assets (and probable recession) or inflationary monetary policy.

Once in that trap of top-heaviness – something that those folks in the 30s and 40s tried to avoid with all those financial regulations and progressive tax rates that have been gutted in the last 40 years – there is no painless way out. The least painful strategy is to kick the can by pumping up the money supply to support nominal ROI.

So in these ways, absolute values do matter. They only stop mattering when looking at the value of those dollars relative to commodity and labor costs, something that affects those without assets far more than those who have many.

“Beware, fellow plutocrats, the pitchforks are coming”, Nick Hanauer.

They know history quite well. The pitchfork crowd causes aruckus every once in a while, but never achieve fundamental change. In most cases, the pain inflicted on them in retribution is greater than they were able to inflict.

Violence is only truly effective when administered by those with much power. Otherwise, it’s hardly different than a toddler throwing a violent tantrum. Annoying and possibly destructive, but changes very little.

Wolf, just a remark about the wealth monitor graph that’s been really bothering me, and I’m sure some other long time readers as well.

Could you please plot the data with different wealth scales for each household category for the Y axis? I am sure that will only prove your point better. But hey, men of science gotta be rigorous.

Another way would be to plot the data with relative weight of each category in the total US household wealth or better yet, relative change compared to last quarter/year à la CPI.

In a highly inflationary environment… absolute numbers don’t mean much anymore and relative information is everything.

Merci beaucoup

> absolute numbers don’t mean much anymore and relative information is everything.

Good point. The graphics emphasize one relative disparity but I can look around me and see not everyone is in squalor, as they might be read to suggest, by the relative compression at the bottom. Something on purchasing power decade by decade would be helpful too.

Yes a logarithmic scale would be great for the y axis

I was going to ask about the “logarithmic” y axis.

It’s interesting that if you divide the the “Wealth Disparity Monitor” chart 1989 to 2021 graph into 2 equal timeframes:

1989 to 2005:

Increase from 5 Million to 14 Million (180% increase)

2006 to 2021:

Increase from 14 Million to 36 Million (157% increase)

So the last 15 years were slightly less bad than the 1989 to 2005 period?!

Also, if the “pullback” in 2007 to 2009 is any guide, the upcoming reversion in the wealth effect should be a doozy: maybe 20%, would knock the effect back to 27 Million.

Thanks Wolf for including the link to Wealth Effect” article, which succinctly reveals just how manipulative the Fed really is.

One other thing: my take is that the Fed’s ultimate goal is NOT to help the rich, but to help the Fed’s dual constituencies: the Politicians, and the Bankers. The rest of us suffer the consequences of endless deficits and declining purchasing power.

Oops: 25% would knock back the effect to 27 Million (Where I wrote 20%)

Andrew,

You’re being sarcastic, right? Log scales are used in finance specifically to hide this type of reality, namely the cumulative effects of wealth where wealth begets more wealth during times of asset price inflation. The cumulative effects of wealth is what creates this wealth disparity.

Wolf-

Probably an obtuse question, but I’m trying to understand if the problem of growing wealth disparity is getting progressively worse, as it appears visually in your “Wealth Disparity Monitor,” or if it is a cumulative but linear problem that corrects itself with the asset price correction most commenters predict?

Perhaps a different way to ask: does a major asset price depression correct (or at least interrupt) the growth in wealth disparity, or might it actually enhance the problem?

Thanks

John H.

Yes, a 50% decline in asset prices across the board would cut the wealth disparity roughly in half — back where it was a few years ago. For society overall, this would be hugely beneficial, including because it would stop inflation in its tracks and would bring down the costs of living for lots of people, including housing costs, though there would be a lot of wailing and gnashing of teeth among asset holders, who’ve gotten bailed out at every twist and turn.

I’ve been posting this monitor every quarter starting mid-2021, and will continue to do so. If we get a visible decline in wealth disparity, I will make sure to point it out in the headline.

We’ve had this discussion before. Wouldn’t that actually make the difference seem LESS extreme?

Hussman believes price to sales is better long term valuation metric because profit margins tend to mean revert. We might be going through a pendulum shift politically where labor has more power and profit margins get cut in half making stocks revert back to normal P/S of one.

Frengineer,

Would you like me to use chart tricks to hide reality? Use a different scale for each category to hide the wealth disparity between them? Use log scales to completely hide the reality? Log scales are used to hide the cumulative effects of wealth where wealth begets more wealth, which creates this wealth disparity. And you want me to adjust the numbers to asset price inflation, which would turn the top near-exponential curve into a straight line, because that’s what it represents? There would be a million ways to hide this reality in a chart.

This is the un-adjusted reality.

Look at the second chart near the bottom. This is wealth disparity in dollars between the 1% and the bottom 50%.

I know it hurts. But that’s what it is. People — including you — need to see it and understand what is going on and not try to use chart tricks to cover it up or to justify it.

Since we’re asking nicely…

Can you adjust the chart so I’m in the top 10% so I can show the lady at the bank….

A very small request that would benefit me greatly….

Thank you… :)

Working on it.

Great job Wolf. Great data. Might be getting poorer by the day but I sure love consuming your data and reading the colorful comments.

One more year of this inflation rate, and people will just start stealing as a way of life. If you are a small business owner selling goods, close your doors now.

Depending on which city you live in, this has already been transpiring.

a muffler repair shop i have frequented throughout the past 35 years and the owner said “i had my best year last year”. i was there to get a catalytic converter (not due to theft). a veteran police officer was gunned down by a 17 year old trying to stop thieves in a shopping center this week in the same large city. they were stealing catalytic converters. we are already there imo. theft and gun violence are raging in my murder capital.

I’m in Houston and this crap is going on everywhere.

JeffD,

For about the last 40 years, most illegal drugs have been purchased with proceeds from stolen goods…

I’m glad you said MOST because when my kids were buying that crap they were using my money.

Not that I know this personally…

But there were times when you needed something, say a new “dishwasher”, and “poof”, if you knew the right people, said requested item would magically be available, brand new in the box…

Effing incredible, I would say…

Just another day in paradise, would be the response…

Capitalism 101…

All for ourselves, and nothing for other people, seems, in every age of the world, to have been the vile maxim of the masters of mankind.

– Adam Smith, Wealth of Nations, III, iv

Thanks for the Adam Smith quotes!

Wherever there is great property, there is great inequality… for one very rich man, there must be at least five hundred poor.

– Adam Smith, Wealth of Nations, V, 1, ii.

yvw

Since the pandemic began, a new billionaire has been created every 26 hours. Income Inequality is deadly. It contributes to the deaths of at least 21,300 people each day— or one person every four seconds. With the massive food shortages next year (rising costs and fertilizer and seed shortages) many nations will be in absolute turmoil — the pitchforks and the mobs will be global.

@ Seattle Guy

You are absolutely correct.

Even before the food shortages related to the Ukraine war, more people died of starvation globally than died of Covid during the pandemic according to Oxfam.

The Arab Spring events are going to to look tame in comparison to what is coming if a lot of things don’t get better very soon.

Wolf,

Excellent post, and I really like what you said at the beginning:

“The Fed’s own data on the distribution of wealth in the US is a quarterly report card on the Fed’s official policy goal of the “Wealth Effect.” It has now released the data for Q4. The Fed uses monetary policies, such as QE and interest rate repression, to create asset price inflation and make a relatively small number of large asset holders vastly wealthier so that – “THEY MIGHT SPEND MORE” – (I made the last part in capitals)

Ahhhh – the good ole “Trickle Down Theory” that has been proven not to work as Pres Hoover found out and many others politicos who seem to believe it works, – but doesn’t for the common folks who get hurt the most, and bear the burden of “Champaign spending” for the rich.

Other countries have tried this and failed as many studies have shown.

A repeat of history is on it’s way, or I should say we are in the midst of a a profound correction, transition, except this time it’s compounded by unknown geo-political factors, political unrest, supply issues, monetary war, pandemic, and a war that may expand beyond Ukraine, – with devastating consequences for all.

So many dislocations have been teed up now. What is tragic is the human energy that could have gone into community, that may well now go into conflict. The young people I teach in college are willing to be reasonable and participate, if any reasonable path appears before them. I fear this will disappear, their good will and the willingness to play by the rulebook, the rule of law. What will appear will be bitterness. We at the precarious lower edge of the remaining middle class are in the thick of it — we have no second homes in Wyoming to retreat to!

For anyone falling into the culture wars and demonizing me as a gov employee: I have a law degree and many years former practice in law, and have taught college 37 years. My salary and benefits are, seriously, no exaggeration whatsoever, in the working-poor range. I do what I do (teach business law) because it makes me a contributing member of society, because it has meaning.

The cheap-seats culture war is how the masters of the universe will keep us squabbling and distracted, and set us against each other.

“The cheap-seats culture war is how the masters of the universe will keep us squabbling and distracted, and set us against each other.”

Excellent point. Media is very good at feeding people on both sides of the political spectrum what they want to hear.

Much of the rancor is over issues of little importance. It’s the Hatfields and McCoys fighting over meaningless stuff. Meanwhile the primary elections are visibly corrupt. How did the person running 9th in the presidential primaries win the nomination? The election prior to this one was also corrupt.

Never heard much about that from the media. That’s why nothing ever changes in gov’t. All the same old cronies in power.

Well, at least here in Murica – land of TV pHarma ads and big-ass pickups, the red apes fling poo, as the blue simps return the favor … All for show, of course, as they divy the gifted proceeds behind the media-wide cloaking device(s).

So the question basically becomes: ‘Who picks Your Jingo? .. and do You buy into it..

What is tragic is that the resources that went into the war in Iraq could have been used to improve life in the US for millions of Americans. Even after the fiascos in Iraq and Afghanistan, the US continued to interfere in the affairs of foreign countries who elected leaders that the US did not like.

Well this time the Europeans, Americans, Japanese, and the poor in the rest of the world are going to end up paying for in higher prices for everything.

The developed countries deserve it too.

I hope it gets so bad in the developed countries that there is real reform as a result, but too bad that people in other parts of the will face hunger and starvation.

The politicians in the developed world could care les about people in the third world and their problems.

Been listening to Lacy Hunt as much as possible. He has very unique background and phd in economics plus is 80 years old so he should have learned a little.

His basic thesis is (Japan, China, Europe and US have too much debt in that order) and demographics are poor so growth rates will be lower and lower. Central banks playing money games can’t fix the problem. Only answer is the politically unsavory one of less consumption and more savings to increase capital investment and build productivity so debt service doesn’t slowly asphyxiate us.

The problem with increasing capital investment and productivity is that economic systems are rigged to guarantee the proceeds benefit only the parasites at the top. Hunt is blinkered, promotes the interests of the <1% and is on the Ruthless Exploiter side of the class war.

More "growth" cannot be the answer: humanity resembles nothing so much as a bacterial culture that has used up its petri dish, plundering what's left of its resources and choking on its own waste production. "Growth" is the ideology of the cancer cell.

What part of "unsustainable" didn't you understand?

What part of “less consumption” don’t you understand? That’s fundamental to any notion of sustainability.

Hey Bead, ten million people die of starvation every year. They have the ‘less consumption’ thing down. Doubling that number a few times won’t compensate for the ‘more consumption’ thing on the other end of the scale. The billionaire class doesn’t tighten its belt. They order bigger superyachts. You and Lacy Hunt would never admit it, but you both know that austerity is strictly for the proletariat.

You should be noted

that the “less consumption” has to occur at the top level. Those in the bottom half are barely consuming the minimum necessary to survive.

Love your comment.

Hunt overlooked the point that all the profit was pushed up the ladder and all the debt kicked down the stairs. He’s going to need luck selling austerity to people who are broke and pissed.

We can grow wealthier and live much lighter on the earth 🌎. Buckminster Fuller devoted his life to demonstrating the principle of ephemeralization. Capital investment IS required, so we can replace harmful technologies.

I agree with Hunt on most of his points

In his interview with Danielle Di Martino booth last fall one of the more salient points of his conversations were about how trillions could have been put to far more productive use by retooling skills of Americans

Imagine if the trillions wasted from 2020-2021 went to providing free worker training and education?

We would have had far less crime, people would be far better off and in position to pivot to different jobs and industries, and perhaps even some economic growth could have come out of fewer unfilled jobs

But that would never happen. Politicians wouldn’t be able to sell that and people don’t have the personal motivation or drive to do such things due to laziness

Right. People who struggle to hold down three part-time jobs have only their own laziness to blame for their poverty, as do unemployed STEM graduates.

Blaming the victim is a form of the petitio principii fallacy favored by mouthpieces of the ruling class, and only less popular than the Straw Man fallacy.

Minus ten.

I’ve just finished prepping and planting this year’s spring vegie crop, pruned and fertilized (with polecat’s proprietary compost blend) the various berries and fruit trees, with the hens a layin .. and the honeybees having come out of winter dormancy like there’s no tomorrow .. so I Be A Richman! ‘;]

.. at least for another turn the seasons – something many ‘high ass et’ folk can’t begin to grok .. as they’ve no idea how to create/husband any of the above, should their ego-inflated lives ever falter down to depend on it! I do this on a typical city lot..

I should add that we’re on the low end of that household ‘wealth’ chart Wolf provided, and should things really come unglued .. then possession will remain MY 9/10s of the forth turning law .. the .gov pmcs will have to go pound sand!

“ I’ve just finished prepping and planting this year’s spring vegie crop, pruned and fertilized (with polecat’s proprietary compost blend)”

Polecat,

You can’t fool old country folk…

We know the septic drain field runs through the garden…

“Kids, the corn isn’t growing very good, we’re having broccoli for dinner”

:)

Well COWG, IF things get as hinky as I think they will, then .. those of us anyway who survive the fall/disruptions of both government ‘discombobulations’ and ‘essential’ goods – be they imported or domestic – may have to get over the ickyness factor of creating humanure to supplement whatever other kinds of fert obtainable to grow our own food as to not starve! Hell, some professions of old may very well become fashionable again.

‘Make Nightsoil Great Again’

Betcha haven’t seen THAT emblazoned on a cap .. Yet!

Polecat,

I want a big red cap that says on the front, “ Recycling before recycling was cool”….

And on the back , “Ask me what I mean”…

Good on ya, brother!

“Imagine if the trillions wasted from 2020-2021 went to providing free worker training and education?”

New Mexico just started a free college program for all residents at a time when college and vocational enrollments are declining. It is the most comprehensive program in the country and one to watch. I hope it is wildly successful…

training and education for what? There was a time when the best lessons learned were in the workplace. If you transfer the workplace to China, there goes that end.

cb-agree, but much of the overseas transfer followed many, many workplaces eschewing ANY serious investment in employee training/education/retention…

may we all find a better day.

Whenever I read about supposed solutions, it’s always in the unspoken context of escaping the consequences of previously living collectively beyond society’s means. That’s what has happened as evidenced by current debt levels.

There is no escaping it. Redistributing the wealth of the (supposedly) super rich makes good politics and will make a lot of people feel better. It won’t do much to keep the majority of the population’s living standards from declining or crashing. This inflated fake wealth can’t be redistributed to the population and then used at any scale in the real economy, as the production doesn’t exist to absorb it at anywhere near current prices.

In making these comments, this doesn’t mean I agree with the FRB’s monetary policy (I do not) and it doesn’t mean I agree with the ability of the rich to buy political influence either.

I just know that no matter what solution anyone proposes (here or anywhere) won’t make prevent collective future living standards from declining or crashing at this point because it will not.

There is never something for nothing. The inflated debts which substantially represent excessive past consumption must be paid through lower future living standards.

AF

“Declining living standards”….

Truly a vague statement……whatever could it mean ?

Here is something much more concrete……Prepare to live as the Amish do.

Very true. The financial economy is most sound when it is most aligned with the production economy. When they are out of whack, problems develop in the fiancial economy that can then impact the production economy, depending on how they are addressed.

The US has long been using debt to pay for the avalanche of products we receive from overseas. We will never pay off those debts. Nor do most holders of that debt expect us to. Most just want us to make good on the interest payments, thus preserving some measure of the value of those holdings.

The FRB will assuredly choose to print up more money rather than let the Fed Gov default on its debt servicing.

A grand crash that quickly resets everything is unlikely in the US. Rather, the bottom half will be slowly but steadily squeezed. Government subsidies to the bottom will mitigate that to some extent, but will also lead to more inflation. The inflation will in turn hit poorer nations and the poorer folks in the nations of major trade partners even harder.

Once wealth accumulation becomes top-heavy, at the top, it is just about impossible to reverse it without, as always, inflicting much pain on the bottom.

This is in line with the universal fact of all hierarchical systems that the people at the bottom always pay the most, one way or another, for the mistakes and excesses of those at the top.

As I’ve said before, Hunt is a former central banker who believes in central bank control, avoiding defaults and recessions, and servicing debts until the cows come home. That’s why he recommends buying 30-year treasuries that pay 2%.

Multiply Hunt’s imagination by 100, then we’ll be entering the zone of reality. It starts with a disgruntled population taking control from central bankers as a result of massive wealth disparity.

The only way to decrease wealth disparity is to let asset prices drop, let speculators default on debts, let under-capitalized banks fail, and enforce progressive tax rates. Also, all the too-big-to-fail entities in all industries need to be broken up. That would finally give prudent savers and decision-makers a say in our economy. People and companies would actually be able to invest with an expectation of reasonable return over time, without fear of a 75% price crash.

We need to take a 40% price crash to avoid an 80% price crash down the road.

Crypto offers an actual possibility of subverting the power of central banks. Hence, it will be regulated and controlled until it no longer offers that possibilty.

It should be pretty clear by now that the folks running the show here are deadset on US hegemony over the global financial system. No amount of ‘sacrifice’ by the average sorts is too much in service of that goal.

Brian Dawson,

There are now 9,849 cryptos out there. There are more cryptos out there than casinos in the entire world. They’re just gambling tokens. And bitcoin is down 18% year-over-year and 30% from November. The house always wins in casinos.

It’s bitcoin or nothing. Get the word crypto out of your vocabulary.

I bought 16 nothings today.

Glad I bought nothings. Bitcoin isn’t doing very well, as you know. It’s down 20% year-over-year on top of having lost 8% due to inflation. Bitcoin is really a shitty hedge against inflation. I prefer the nothings.

Bobber said: “The only way to decrease wealth disparity is to let asset prices drop”

—————————————-

How does that undo wealth disparity if the same entities own the assets. Concentrated wealth and power ruins free society and free markets. When asset ownership is concentrated, asset owners rule non owners.

With asset prices lower, defaults occur, and ownership changes hands. New players and new generations are able to gain asset ownership. Assets are transferred from speculators and bad players to steadier hands.

@Bobber –

I am enjoying your commentary in this thread, and you might be right. I doubt it on a big picture basis. A few assets might be jostled about, but I think those steadier hands are typically the well healed.

bobber has it correct in my very very extensive reading of her and history!

Given the opportunity to SAVE,,, each and every “Little Old Lady — of each and every AGE and gender to be sure” will save their gold in the good times/booms,,, and then buy real assets in the busts/bank runs.”

THAT was the clear message that was the foundation of the FRB; after all, we cannot have WE the PEONs literally out foxing the banksters,,, can WE???

Now that we have $600 TRILLION of ”paper wealth” of all kinds,,, this lesson should have been learned, and likely WAS and IS being learned by the LOLadies of all kinds…

Good Luck to all who will continue to gamble in the casinos of SMs, etc., etc.

And, May the GREAT SPIRITS bless us all.

I made the mistake of listening to Lacy too as he sounds very knowledgeable but he was blatantly wrong on inflation.

How can such smart and experienced people be so wrong?

Lacy had a strong narrative and nice charts showing how deflation was the way ahead and the money injected by Fed and government programs was insufficient to stall deflation.

He only saw inflation if the Fed mandate was changed and her liabilities became money.

I wish he had the courage to come out and say he was plainly wrong.

It goes to show that in those matters, no one really knows anything, no one.

“It goes to show that in those matters, no one really knows anything, no one.”

Of course they do. They just lie, that’s all…

Oldschool said: “Only answer is the politically unsavory one of less consumption and more savings to increase capital investment and build productivity so debt service doesn’t slowly asphyxiate us.”

——————————————–

What does savings have to do with capital investment in a system where money can be created at will?

It would be interesting to be able to compare asset growth rates now to the 1920s and or the 1970s

The 1920’s was a time of great asset appreciation, the 1970’s was not.

Inflation and housing went through the roof in the late 70’s in southern California.

This is the most asset inflation in history. David Stockman has dug into all this data. Michael Oliver also shows this in his MSA momentum charts. Wolf’s work shows this as well.

Ooooh,

Stockman…

Go back and read the crap he and Reagan did…

Ever wonder why his only job is to sell bullshit for advertising…

BTW, Santa Claus is real..

If that helps

Is there an end to this and if yes, when that’s going to be?

Yes and now.

“Is there an end to this and if yes, when that’s going to be?”

It does not pay a prophet to be too specific.

The Collapse is a process, not an event. TPTB are preparing for it with their own processes, and there have been numerous milestones over the last forty years: regulatory capture, assorted tax gifts and other favorable legislation, the Citizens United decision, and so forth. There are extensive lists.

They’re grabbing everything they can like there’s no tomorrow, because they know that someday soon there won’t be one. These guys are anything but stupid, and they plan to survive the worst in style.

There have been numerous explanations, going back all the way to Jefferson and Adam Smith, as well as more recent expert expositors. For example:

“… the powers of financial capitalism had another far-reaching aim, nothing less than to create a world system of financial control in private hands able to dominate the political system of each country and the economy of the world as a whole. This system was to be controlled in a feudalist fashion by the central banks of the world acting in concert, by secret agreements arrived at in frequent private meetings and conferences. The apex of the system was to be the Bank for International Settlements in Basle, Switzerland, a private bank owned and controlled by the world’s central banks which were themselves private corporations.”

Quigley, Carroll. ‘Tragedy and Hope: A History of the World in Our Time’. New York: Macmillan, 1966. Print.

It gets worse the more you look at it.

Around 90 million people die every year of preventable disease and starvation, and those numbers are projected to start ramping up about 2030. It’ll be ugly. After that, it’ll be weird ugly. You might like to consider investing in productive resources, rather than financial instruments.

What does the 1% invest in that the 2-9% does not?

Politicians

Bingo!

Govt supports big corporate spending and corporations give big donations. The latest smash and grab coming from DC should be a doozy.

Excellent! The whole situation in one word.

Yes, and it’s the only possible outcome from activist big government fiscal and tax policy.

There is no such thing as activist big government existing for the benefit of the majority.

The only option to drastically reduce (not end) “pay to play” is to radically shrink the scale of government so that it has a lot less to sell.

AF

Let’s start with the Pentagon.

Also all those overcharging military contractors.

I agree. Foreign policy needs to radically change and defense spending with it.

Yeah .. we could convert the Pentagram into one giant shopping mall instead…..

oh wait!

.. perhaps, on further thought, an enormous ashtray might be a better use of said space .. let’s do That!

Thanks for publishing an article on economics that counters the spam being put out by extremely filthy rich oligarchs and their paid professional liars.

And you can clearly see the great difference different political parties being in charge makes. So VOTE yourselves out of this! /s

Sadly, both parties seem to agree that a command economy through central banking, interest rate manipulation and monetary meddling is a workable AND sustainable solution to the economic problem.

Keynes is dead, but his offspring has grown into a giant.

OK, and what are the feasible alternatives?

Duh.

Hate to be a smartaxxe, but isn’t it obvious?

Recession, asset price discovery, followed by sustainable growth.

Contrary to central bank thinking, recessions ARE necessary. Speculative asset pricing is NOT normal.

John H. wrote:”Keynes is dead, but his offspring has grown into a giant.”

Keynes is indeed dead. But I don’t think you know anything about his theories.

He wanted to have the government to spend on the Poors during Hard Times, and balance the budget when things were good.

He never said to subsidize the wealthy and hope that it would trickle down.

Old Ghost-

Keynes was in favor of removing the mechanisms of discipline in federal spending in an attempt to preserve jobs.

Stimulative spending, though perhaps laudatory in the short run, has proved unsustainable in the long run. Fiscal stimulus, like monetary stimulus, leads to exactly the kind of excesses we’re experiencing today.

The idea of more govt spending in down cycles, and then returning to a balanced budget in good times sounds great on paper… but it never really worked that way, did it? And here we are.

“The question of Keynes’s role in history is essentially one of how his teaching could succeed once more in opening the floodgates of inflation after it had become generally recognized that the temporary gain in employment achieved by credit expansion had necessarily to be paid for by even more severe unemployment at a later stage.”

-F.A. Hayek

“The Collected Works of F.A. Hayek, Vol. 9: – Contra Keynes and Cambridge, edited by Bruce Caldwell

This isn’t Keynes, buy a Keynesian:

“To fight this recession the Fed needs more than a snapback; it needs soaring household spending to offset moribund business investment. And to do that, as Paul McCulley of Pimco put it, Alan Greenspan needs to create a housing bubble to replace the Nasdaq bubble.”

– Paul Krugman, N.Y. Times, Op-ed, August 8, 2002

Krugman, like Keynes, wanted to have the govt “spend on the Poors,” as you aptly out it. His prescription came to fruition, and GFC proved Hayek right, I’d say.

John H. wrote: “Krugman, like Keynes, wanted to have the govt “spend on the Poors,” as you aptly out it. His prescription came to fruition, and GFC proved Hayek right, I’d say.”

So…….now you have confused Krugman with Keynes. You really know nothing about economics, or the history thereof.

Krugman bailed out your wealthy friends, the TBTF banks. I would call him a trickle down guy.

Keynes wanted to put the Poors to work. Sure, some of it would have been make work. But Keynes knew it would trickle up. Big difference.

Hayek was a bought and paid for propagandist by the Super Rich of his day. Their only goal was to destroy the New Deal. Hayek’s books are propaganda. You can throw his books in the trash.

OG-

On your direction, I will dispense with Hayek. Also Hutt, Huerta De Soto, Salerno, Hazlitt, Groseclose, Palyi, and of course Mises… and that rapscalion Rothbard!

I will hang on to my copies of the General Theory and Economic Consequences of the Peace, along with Picketty, Moulton, Boulding, Samuelson (oh, I might have tossed that already), Alvin Hanson, and Heller.

Not sure what to do with Wapshott or old printings of Alexander Gray…