Rents, houses, used and new vehicles, gasoline, groceries, forget it, hahahaha

By Wolf Richter for WOLF STREET.

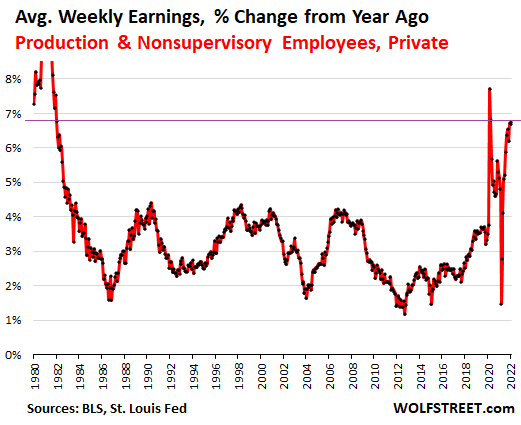

One of the results of the very tight labor market is the surge in hourly wages, particularly for workers in the category of private-sector “production and nonsupervisory employees,” where average hourly wages jumped by 6.7% for the third month in a row in March, compared to a year ago, according to the Bureau of Labor Statistics. Other than the lockdown distortions in April and May 2020, this was the biggest gain since early 1982.

These are workers in all industries and in all jobs that are non-management jobs, ranging from waiters to Facebook coders and Goldman Sachs traders. In dollar terms, the average wage of Production and Nonsupervisory Employees increased by $0.11 from the prior month, and by $1.71 from a year ago, to $27.06.

The distortions in average wages that occurred in April and May 2020 reflect the effects of the lockdowns, when many lower-wage employers, such as restaurants and retailers, were shut down, and their employees were laid off. Their relatively lower wages fell out of the averages, while many people in higher-paying service jobs, such as those in financial services, tech, and other sectors, switched to working from home.

As millions of lower-wage people were laid off, the higher wage earners became a bigger proportion of the earners and pushed up the year-over-year gains in average hourly wages. In April and May 2021, the low year-over-year gains reflect the high base a year earlier.

Average hourly earnings in the private sector overall increased year-over-year by 5.6% in March. In dollar terms, the average increased by $1.67 year-over-year, to $31.73 per hour.

But these big wage gains were out-spiked by prices.

Despite the biggest increases in average hourly wages for production and nonsupervisory workers since 1982, these folks are worse off. They might feel better about their higher wage for a little while, until they try to buy something – and discover that prices have out-spiked those wages gains by a wide margin:

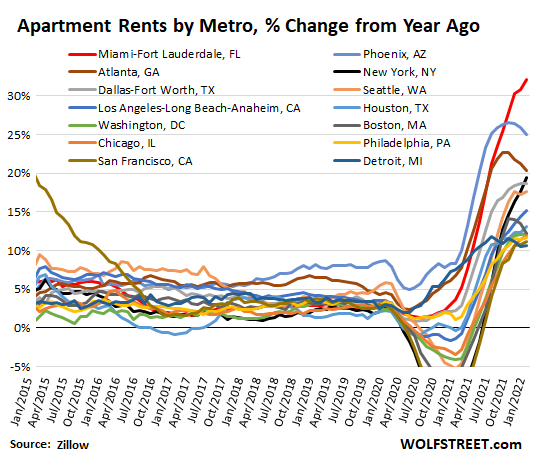

Rents of apartments and single-family houses across the US, according to Zillow’s Observed Rent Index, spiked by 17% from a year ago, two-and-a-half times the pace of the wage gains.

Rents spiked by 11% or more in all of the largest 14 metros, at the top: Miami (+32%, red line), Phoenix (+25%, blue line), and Atlanta (+20%, brown line). The smallest spike of the largest 14 metros was in Detroit (+11%).

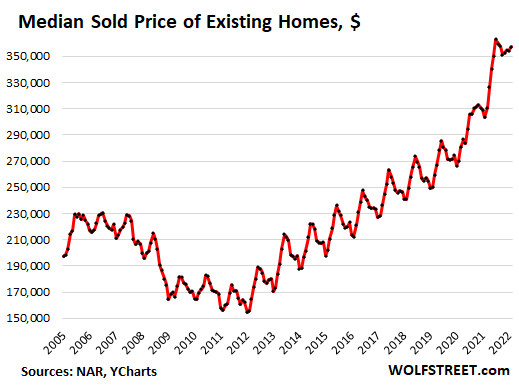

The median home price across the US jumped by 15% from a year ago, to $357,300, according to the National Association of Realtors. This was more than double the pace of the wage gains:

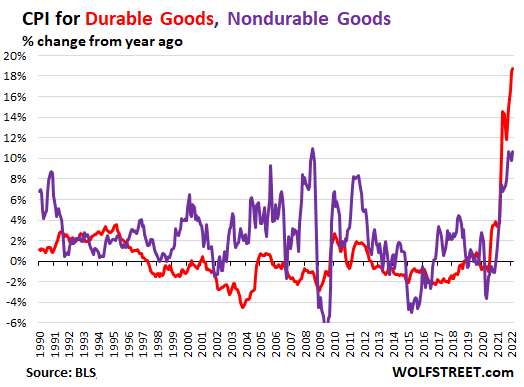

Prices of durables goods – dominated by new and used vehicles, but also furniture, consumer electronics, etc. – spiked by 18.7% in February, according to the Consumer Price Index for durable goods, by far the worst price increases in the history of the monthly CPI data going back to the 1950s (red line in the chart below).

This spike was over two-and-a-half times the pace of the wage gains. It was fueled by prices of used vehicles (+41.2% = 6x wage gains) and new vehicles (+12.4% = nearly 2x wage gains).

Prices of nondurable goods – dominated by food, gasoline, other energy, and household supplies – spiked by 10.7%, the worst price increases since July 2008 (purple line):

This is why inflation is an insidious force.

The biggest gains in compensation occur at the top, executives of major companies are getting raises that amount to millions of dollars, in addition to massive stock compensation packages. And many highly-paid employees at these companies are getting massive compensation increases in dollar terms, along with their stock compensation plans. Their stockholdings have ballooned since March 2020 in line with the Fed’s money-printing orgy. Those folks might grumble about higher costs, and shake their heads at the gas pump, but they will be fine in this crazy inflationary environment.

But the people that earn hourly wages, they will not be fine. Their raises might make them feel better briefly – until they have to go fill up their car, buy groceries, pay for the rent increase, or buy a car. And if they want to buy a house, well, forget it. In addition to home prices having run away from them, mortgage rates have now jumped. And those 6.7% in wage increases are going to look ludicrous compared to reality.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

i should’ve asked the question i asked in the earlier article, here, because this is where the most blood is.

It’s actually worst when you account for in-hand wages after subtracting taxes, Social Security etc. A 6.7% wage hike results in ~4.5% in-hand increase, that hits a 7.9% inflation wave and topples, only to be plunged deep by “Hedonic quality adjustments” and BLS “BS” weightages.

So, in reality, workers are getting poorer.

Wolf, if possible, we should atleast account for federal and state taxes while comparing hike in wages with inflation.

As long as the tax brackets are adjusted in line with inflation, then a 6.7% wage hike means 6.7% higher taxes and 6.7% higher after-tax amount. There might be a bit of variation, but nothing like what you’re suggesting.

Yes, I miss calculated.

Same here. Consistently two weeks early.

> Despite the biggest increases in average hourly wages for production and nonsupervisory workers since 1982, these folks are worse off

Not so fast. Those who were able to leave NIMBY areas thanks to remote work are still enjoying massive deflation. I’m one of them, great times!

most people who are paid on an hourly base, in my experience, are not the ones who have the ability to work remotely.

so what — YOU MAKE LIVING WAGE(as defined in 2020)

I find those IN REAL WORLD, ie door to door workers

continue to do and service said POPULACE – even takers

we get paid or WORK IS NOT DONE

of course OUR PRICES have now doubled from 2021

oh, take it or find someone else

Not correct again.

Most folks who moved to work remotely had their salaries adjusted via new offer as per “Cost of labor” of the new zip code (please note that this not cost of living).

While companies were a little generous in not reducing salaries by more than 30% initially to keep the offer attractive, HR software will automatically adjust all future hikes downwards to bring employees down to real cost of labor in next 3 years.

Not to mention that , it’s in human nature, that most bosses will promote the guy that they meet over lunch, and not that remote audio feed!

The only silver lining is that even adjusted “Cost of Labor” still provides slightly better living standards when moving from tech hubs like silicon Valley or Seattle to certain destinations that have “Lower cost of Living”.

Your reply is actually the most generous option. The reality is that most hard core WFH jobs will soon be moved to Manila or Mumbay. If you can do work and no one needs to see your face live, it won’t be long until they figure out that they can find a smart, motivated, grateful employee amongst the more than 2 billion English speakers on the Asian continent.

To think that Americans have such special skills that replacements can be found amongst more than 2 Billion Asian English speakers, that really is the height of American hubris.

Actually, I meant

“To think that Americans have such special skills that replacements CAN’T be found amongst the more than 2 Billion Asian English speakers, that really is the height of American hubris.”

Sick-hubris (could be portrayed as a civilization reading, and then without serious reflection moving on to believing its press releases in their entirety) being that which ultimately undoes any empire, American or otherwise.

Beware ‘exceptionalism’, the DNA of our human population is common, at once magnificent and miserable…

may we all find a better day.

Although I agree with your general point, having worked in basically this capacity a few years ago (part of team scouting thru India, Pakistan, Philippines and spending much of 2 years there) there aren’t anywhere near 2 billion English speakers in Asia, incl, in S and SE Asia. We were linking people up both for call centers and back-office work and in most of India, we needed translators and interpreters to communicate just about anything of significance. Even in Philippines to our surprise. Seems like Americans esp in our history classes place way too much emphasis on the British Empire period in South Asia, which in big sweep of history was little more than a tiny little blip (a couple centuries tops) in millennia of history there.

And even then as we learned from our hosts, the UK only had a major presence in around 40 to 45 percent of what’s now Indo-Pak, depending on maps, with most of it still under a local rajah. By the time they got kicked out in 1947, the Brits just weren’t there long enough or broadly to have much effect on the language or culture of India or the surrounding countries–the in depth estimates indicate somewhere around 2 to 3 percent of Indians speak English at anything similar to working level now, a little more in Paki and Bangla and almost never at native level unless they’re lived for decades abroad. It’s why there’s been huge push in every Indian state to get learning and working materials in their local languages (and similar across the subcontinent), the English medium education efforts have been a total failure because there’s just not enough of a base and learners wind up not knowing any language very well. They said maybe around 8 to 9 percent true working English ability in Philippines, they did seem to have an easier time in our meetings but we still had to get our main training materials and manuals translated in to Filipino or Ilocano, just like we’d done with Hindi, Kannada, Tamil and Malayalam in India or Punjabi and Urdu in Pakistan. (Or they just used auto-translators on their browsers for web-based or pdf documents).

Sure a lot of people in those countries take classes but very few have actual working ability in the language, same with the Chinese and Japanese, they can’t speak or use English anymore than we Americans can do serious business in French even after all the years we took in middle and high school. (The leaders of our overseas teams always spoke the local languages fluently, in the Philippines members of the leadership had to know Ilocano and Capampangan along with Filipino based on where we were working, in Sri Lanka she had to speak Sinhalese, in India it was mandatory for all of us to speak at least conversational Hindi–it was considered an insult if we didn’t–and our leaders spoke Tamil and Kannada when we got posted there). And just like in South Asia we had to translate the English-language documents, or just have them auto-translated which fortunate for us, is getting very reliable.

There’s this weird confusion in a lot of world history classes in the US (and I mis-learned this too Tbh) where Americans equate “being in someone’s empire” with “switching over to speak their language”, when in reality this almost never happens. Sure it did for ex. the Dutch in Aruba (partly because the place was barely settled before), but the Dutch were in Indonesia for many centuries and the Indonesians don’t speak Dutch today because of it. And even less of a cultural effect for ex. the Brits in India or Americans in Philippines, and the same reason almost nobody in Mali or Senegal actually speaks French even when they study it and it’s used in some gov. documents (they all use their local languages there), it’s too difficult to get fluent and the imperial cultural roots of the old colonial power just aren’t deep enough.

I’ll just add, I still do agree at least partly with your overall point. Obviously we were stationed in South and Southeast Asia because we were outsourcing some work there, and some of those offshored operations stuck, but it wasn’t because of English ability. (And even then it’s not like there’d be enough jobs to outsource to employ even the tiny minority of solid English-speakers there–we’ve actually gotten more mileage out of outsourcing Spanish-language sales and documentation to Panama and Colombia for our US Latino clientele, which is fastest growing customer base). It was more just, we could do a lot of things cheaper and get work done during after-hours in the US and Canada (after we got key info translated), so made sense on our balance sheet.

Turns out some other problems later emerged though, for ex. some of the power grid and other infrastructure in India and Bangladesh often went down, communications failed and we missed critical deadlines. And then everything went to heck when the delta Covid wave hit India and the broader region. So offshoring sometimes works but scope tends to be a lot more limited than a lot of companies (incl us Tbh, before we knew better) assume at start. Which is maybe a good thing, if it was too easy to outsource backoffice and IT, then there wouldn’t be many good white-collar jobs in the US anymore and Americans wouldn’t have money to actually buy our products anyway. Wolf has been pointing up eye opening graphs about how Americans buying power has been falling like a rock and another hit to that is the last thing we need, that’s when the pitchforks probably would come out.

Like you, I have been able to work remotely, which has been a financial plus for me, though the price inflation in basic items has eaten into those overall gains.

The majority of Americans are destined to become poorer or a lot poorer over the indefinite future.

Yes, I have written this so many times it sounds like a broken record. Looking at the actual US long-term fundamentals (as opposed to the fake ones most want to believe), it’s also obvious.

I don’t think you are wrong. Like the saying, the rich gets rich and the poor gets poorer. Now, it’s just much quicker! Thanks central bankers!!!

It’s not like I am happy about if that’s how it comes across.

It’s going to be really hard to escape the downdraft and I don’t assume I will be exempt either.

the rich aren’t going to be exempt either. americans aren’t going to be willing to live as chattel slaves the way many in the world were in the past.

No, they won’t, contrary to what I read from so many comments here.

724 billionaires now versus 13 in 1982. The lopsided proportion are destined to have their wealth collapse. Their wealth is mostly a bag of hot air and they lack the political influence to avoid it.

not just political influence, but the ability to quash a social rebellion.

all of the wealth in the world and a gated compound doesn’t do you any good unless you can pay enough people to protect you, and trust that they won’t turn on you.

Just ask Jack Ma.

So says John Calvin as channeled by AF.

your posts are getting really irritating.

J

Excellent !

Thank you for verifying their effectiveness.

The majority of Americans became much poorer in 2008. Now they are mostly wealthy again.

My point is that people who had enough income to buy a house and invest in the stock market since 2008 did extremely well. I think 2008 could happen again and the majority will become poorer again. These are typically professionals, CEOs, VPs, doctors, lawyers, engineers, nurses, electricians, plumbers, and successful business owners.

The people who did not have enough income since 2008 to buy a house or invest in stocks became much poorer with rapidly rising rent, food, transportation, childcare and all of the other necessities of life. If they fell into the credit card/Payday loan trap, they fell even faster. Having enough income seems to be a losing battle for these people. These are typically hourly wage people working in services or fixed income people.

I don’t know what the percentage difference between the number of people in each category above.

Just as in 2008, wealth can be fleeting for the first category. Stock market crashes 50%, house prices crash 50%, job loss causing foreclosure can send many of the first into a spiral. 50% loss in wealth, no home due to foreclosure, and no job due to layoffs.

Without the Fed propping things up, I think this would have happened already.

As long as the part you like isn’t broken, I don’t see the problem…

The chip shortage is causing rising new vehicle prices and used car part shortages. Too many supply chain disruptions. Oil and gas prices are cyclical except in hyper inflationary periods. Wars were often times of inflation.

David Hall,

I understand that you’re human, but many of your comments sure read like those of a bot whose algo has been unsuccessfully repurposed to composing comments.

OK, so RTGDFA…

… and you will see that the biggest inflation items in the article — rents and home purchases — have nothing/zero/zilch to do with chip shortages, supply chain disruptions, and oil and gas prices.

It is our mission to authoritatively provide access to diverse services to stay relevant in tomorrow’s world and progressively build leveraged core competencies such that we may continue to collaboratively maintain enabled ideas through continuous improvement utilizing buzzwords and catch-phrases that sound important. [Hal9000_BOT_Error_Severity_HIGH see stack trace]

Especially given your username, hilarious post!

Your WTF real estate bubble has not burst yet? Didn’t you called a home price top or two already?

Good luck if your local home improvement center ordered parts from China. Covid shutdowns are clogging ports. Could that affect home prices?

Now your getting silly.

“home improvement center”????

And you still didn’t read the article. Did I say anything about new houses or new construction or remodeling? Nope. The charts I showed were RENTS (those buildings have been around for a while) and the median price price EXISTING homes, meaning USED homes that had been built a while ago, not new homes. You’re just way off in no-man’s land with your supply-chains and ports when it comes to rents and the price of existing homes.

IIRC from a few months back, David is trying to build a home in the Tampa area and may be having issues with a builder…

i.e., some misinformation…

Wolf, in fairness to David Hall, even though you mentioned the rise in prices of rents and existing home sales, people still need or want to make improvements to their residences, so that’s probably what he means by “home improvement centers”. There are still needs to buy durable goods like stoves, refrigerators, washers and dryers, bathroom vanities, etc., plus even people buying existing homes are probably going to do their own home improvements unless they’re moving into a rare move-in ready condition house at which point they will be paying even more inflated prices to buy the house.

Good lordy!!!!!!!!!!!!

Sounds like we have been brain washed to wait for the burst. for the last week period, I see sold houses with 20% over asking price, in my area, Los Angeles.

RTGDFA?

May I ask?

I Googled, but no definitive answer.

Read The blank blank blank Article

This is a WOLF STREET special. One of the commenters here came up with it. If you Google it, you’ll get the comments here.

“Read The blank blank blank Article.”

Huh???

I put blank blank blank into your search, here on this website, but over 4500 matches?

I’m even more confused…

OK, here we go. You asked for it: RTGDFA = Read The G*d D*mn F**king Article

Ok…

I think I get it now.

By the way, I’m an Australian and dyslexic.

I’m not saying there’s a connection between being Australian and dyslexic… hahaha.

But I always check out your website, because of the graphs.

Even though they are American based, they’re still interesting to look at.

(Thank God for voice-to-text software)

The following is from Forbes, Feb. 8, 2022.

“During the last three months of 2021, credit card balances increased by $52 billion to $860 billion—the largest quarterly increase in the 22-year history of the data, according to the Federal Reserve Bank of New York’s quarterly report on household debt and credit.

Overall, total U.S. household debt increased by $333 billion during the fourth quarter to $15.58 trillion, according to the New York Fed. Throughout 2021, debt balances—including mortgage, credit card, auto, and student loans—grew by $1 trillion, largely driven by mortgage balances.”

People just keep going deeper into debt. Some simply have no choice, but others have just become comfortable with it like those who live at the base of an active volcano or a failing dam. I keep wondering when the creditors will stop extending more credit to these people who can’t or won’t pay down their debts, but to date only the poorest amongst us have faced a day of reckoning. People may be complaining about prices, but as long as they can buy on plastic they don’t seem to be changing their behavior.

It seems to me that there is a very big difference between mortgage debt and consumer debt.

Mortgages are secured by [hopefully] a stable or appreciating asset, consumer debt us spent on food, gas etc.

Re – Mortgages as stable collateral.

Take a look at how much faster alleged home values have grown relative to alleged median incomes, and you become a lot less sanguine about the stability of that home value collateral.

If incomes rise 2% per yr and home “values” 8% (invented numbers but accurately illustrative), compounding ensures that things get delusional pretty fast.

The only reason that housing has seen perhaps 20 years of its greatest appreciation (with one massive coronary) at the exact same time employment/wages have seen 20 years worth of some of their worst, is that the G disemboweled interest rates (via unbacked money printing) in order to foster an “affordability illusion”.

Once they are forced to stop ZIRP, the houses of cards collapse.

It happened in 2007 to 2009, when a 2% increase in mortgage rates triggered one of the worst housing collapses in American history. And a 1.5% increase in Treasury rates in 2018 triggered a 20% fall in the SP 500.

Good comment. It’s all part of the Financial Cabal’s (Bankers/FED/Wall Street) purposeful and government backed effort to create a debt society. Most efficient form of slavery there is. Must keep the servants serving the masters.

Cas 127

I am 67 years old and I have seen a lot of ups and downs in the last 45 years, since I got out of college.

As I keep saying, population goes up, the amount of buildable land goes down goes down, and everyone has to live somewhere.

So I think real estate….over the long run… is going be okay.

We will see.

Enlightened,

Re: Buildable land – The US has an astronomical amount of buildable land, even when government restrictions (often phony baloney, mainly in the service of existing RE owners) are taken into account. Tiny, tiny subsets of America (Manhattan, SF city proper) have a true land supply issue…the other 99.9999% of America’s acreage doesn’t (one look at any US map illustrates this). And with internet tech being 25+ yrs old, willful hyper-density is starting to look economically perverse.

Re: Population – Slowing to an absolute crawl due to true, underlying economic cratering and the Baby Boom finally being carted off. That leaves immigration – mostly illegal, again “oddly” servicing the interests of existing RE owners (who might otherwise be under real pressure due to birth implosion and internet relocations).

The cheap mortgage debt helps to make the ever increasing consumer debt possible.

Rumpled Bemused,

Household debt overall increased because of surging mortgage debt due to exploding home prices. Duh.

Here are the credit card balances that you refer to. Note how LOW they are compared to before the Pandemic, and how little they have changed from 14 years ago, despite population growth and inflation.

Why do you drag Forbes into here when you could drag WOLF STREET into here and get a gazillion times better info? So yes, go click on my article and learn something:

https://wolfstreet.com/2022/02/07/consumers-did-their-part-borrowing-more-to-buy-much-less-what-happened-with-auto-loans-is-truly-amazing/

Wolf,

Do you think the non-increase in credit card balances could be due to cash-out refinances paying them off as house prices increase?

That’s an interesting question. And I don’t know the answer. There were massive refi’s in 2020 and 2021. But I’m not sure that there is a big overlap between people with high credit card balances and homeowners doing refis.

We do know that lots of people used their stimulus checks to pay down their credit cards, and credit card balances plunged as the stimmies flooded the land.

“We do know that lots of people used their stimulus checks to pay down their credit cards…”

Almost like a debt jubilee ascribed to a disease.

Hmm.

I suspect some of the decline in CC balances was due to stimmy checks. Regardless, we are a whopping 5% off the prior high and the rate of increase is steep..

Rumpled Bemused,

But here are the auto loan balances, which you didn’t mention, with prices up by 41% for used and by 12% for new:

https://wolfstreet.com/2022/02/07/consumers-did-their-part-borrowing-more-to-buy-much-less-what-happened-with-auto-loans-is-truly-amazing/

As we used to say in the meetings with the credit folks when they worried about the escalating amounts financed, “You can live in your car, but you can’t drive your house”.

Thank you, I have read your previous articles. Regarding Forbes, no one is my sole source of information. I wasn’t being dismissive of mortgage loans or auto loans. My concerns are with the rising collective private debts, of which credit card balances are a part,and the public’s willingness to assume more of every variety. Perhaps, I shouldn’t have used the phrase “buy on plastic” as it makes one think of a specific type of debt.

Frankly, I find your response to my comment unnecessarily antagonistic.

Rumpled Bemused,

I work very hard to give people the data and charts, along with perspective, and two months after I’d published my article on credit cards and other consumer debt and delinquencies, you drag this perspective-less misleading nonsense from Forbes into here. Compare what Forbes said about credit card debt to my chart. Do you see what I’m talking about?

What goes on at Forbes, stays at Forbes.

You bet I’m antagonistic when people drag this misleading Forbes crap into here. There was zero reason for you to do that.

“I keep wondering when the creditors will stop extending more credit to these people who can’t or won’t pay down their debts”

Not until the defaults start piling up and they have to get bailed out again. Some lenders figure federal bailouts into their risk calculations and find ways to launder away the profits from their balance sheets.

Moral hazard my ass. The Financial Industrial Complex has way too many ways to game the rules so corporate officers can’t lose.

When you can create credit from nothing, why not extend it? Particularly when you get backstopped by the government.

Nice racket, huh? Guess who’s paying for it.

@ unamused –

it ain’t the rich ………………

Just like WeWork and others with no hope for anything but massive losses, credit issuers will continue to sell their bad deals to an eager investor, until the entire debt foundation collapses. Until then, they can peddle this bad debt on and on to buyers with no end in site..

This is smelling a bit like the old S&L debacle. But hey, probably not.

“ credit issuers will continue to sell their bad deals to an eager investor, until the entire debt foundation collapses”

My friend,

You never expressly stated which end of that transaction you didn’t like…

Yet all you here over and over is that household balance sheets are in great shape

Household balance sheets are supposedly in great shape but it’s actually due to an asset mania. That’s the only reason household net worth is at record levels. It’s fake wealth as there is no possibility of spending it at scale in the real economy.

The flip side of this coin is that the aggregate data says nothing about the distribution.

There are some (maybe many) very wealthy people who owe a lot but it’s presumably at very low rates secured by ample collateral. A purported example is Larry Ellison whom I read owed $2B to finance his lifestyle. But my guess is that he probably pays something like FFR plus a very low spread, like a few basis points. I presume he had a LOC from banks but at that scale, he could also do a private placement with an institutional fund.

It’s the lower end of the distribution where it’s the biggest big burden. Mostly what many here would classify as (relatively) low balances but at high rates.

exactly. there’s not enough productive capacity in the world to buy all of today’s “assets” at anywhere near today’s prices.

Not everyone pays 29.9% on their credit cards. If your score is 750 or better you can frequently get long term rates as low as 6.9% (Though 9.9% is more common.) If a durable product category is inflating at double-digits(Think appliances or furniture), then it can be worthwhile to buy at today’s price and pay down with cheaper dollars.

Not unlike buying rapidly appreciating RE at 3% rates. And unlike RE, that refrigerator will likely never be cheaper.

Disclaimer:

My own credit score is over 800. Last year I decided to buy a new central AC system. About a year or two sooner than I had planned. Got a 6 year note at 5.9% Inflation has already boosted the cost of my unit more than the 6 year interest charges.

Inflationary expectations, how do they work?

Bakes,

Apples to peanuts…

Did you calculate electric savings from a perhaps newer efficiency rating…

This would affect your ROI over a 10 year life cycle ( depending on where you live)….

Expected life cycle… amount paid…efficiency savings…expected inflation over the term… not for just one or two years…

But then again, if you’re happy, don’t worry about it… :)

800+ means that you are exceptionally talented at producing profits for bankers.

I mean no offense; that’s just how THEY see it. Like Vegas sees a whale.

@COWG

Good point!

Comparing electric bills prior and subsequent to the installation, I can see an additional savings of $240 by installing a year earlier. I also neglected to figure the ongoing maintenance cost of an out-of-warranty HVAC system ($360 in the final year).

@Hal

No offense taken and you raise a very valid point! Though in my admittedly unusual case, one might be surprised. I’ve never earned more than $40K in any given year. I’ve only had one mortgage of $100K. Credit cards are used for bonus points and paid monthly. I don’t own a car. I couldn’t possibly have netted that much profit for the banks. Though maybe via retailer’s fees!

But your larger point stands. One does not get any credit score at all unless you play the banker’s game.

I appreciate what you’re saying, but I think that it’s a rare consumer who is giving this much thought to their purchases.

Well, Banana Republic is now introducing “Banana Republic Baby” presumably for the credit-addicted public to adorn their offspring in designer clothes. So, yeah… maybe consumers ain’t thinking at all.

Ding ding ding ding ding.

And a terrible salesperson that would allow them to.

Arm’s length deals. You get not what you “deserve,” but what you bargain for. Anyone who makes a more foolish deal falls into another saying: “a fool and his money are soon parted.” It was never different.

The troubling part for me is the bailout waiting for the fools, which rewards and encourages folly (and the galaxy of problems we are talking about). It makes others’ self-inflicted problems MY problem. Moral hazard is the Achilles heel of our times, because peopole vote themselves bailouts (and then blame the bureaucrats such as Powell who carry them out). Do you REALLY want things to get fair?

A postcard from “the other side”:

Don’t care what my CC rate is. Its paid in full before charges. The minor annual fee is nothing. They are merely convenient payment methods, nothing more.

Retirement comes damn quick folks, and unless you have ties to a political family, the cash flows slow way down for most.

Can you pay off all debt by the time -your- cash flows slow down?

“…the cash flows slow way down for most.”

The cash inflow slows down agreed but the cash outflow is the bothersome part.

Agreed pay off credit card debt monthly (and be a credit card company slug) and pay off debt before retiring is a good practice.

Even better when they pay you back a percentage! We won’t hold any cards that don’t offer kickbacks. Although lately I’m holding more cash than usual. ‘Legal tender for all debts public and private’ and all.

RB-

“ I keep wondering when the creditors will stop extending more credit to these people who can’t or won’t pay down their debts”

James Grant said somewhere that the markets have lost their “gag reflex.” Seems to be your “creditor” question.

Very pertinent…

And price discovery is lost too, without sound credit risk in the picture. Prices include vital information. That used to be a beef about failing communism.

I am not sure “ludicrous” is the right word here. Wage gains are a good thing… and to be expected considering the low unemployment rate and the limits that are possible to further offshoring. And poorer people can make substitutions that cost them less money (eat at home versus eating out, meat as ingredient versus as main course, etc.)

That said I think this all ends pretty tragically. Most people who will need to make such cutbacks have already been doing it for years. Oil prices are twice what they were two years ago… and unlikely to collapse on their own (absent action by the Saudis). Food prices are elevated as well. Housing prices are about to be.

Most importantly of all… inflation is sticky. When you buy a pickup truck or SUV thinking little of it because gas prices are low.. you are stuck with that decision longer than you would like when gas prices spike. Housing is the same way.

Yes, poorer people can just become poorer. insightful

Small expenditures add up over time. As one example, I’ve read that lower income groups are the primary buyers of cigarettes. Those are expensive. Daily visit to Starbucks is a luxury that adds up fast.

Every time I go to any nicer restaurant, the place is at high capacity (if not packed), and in the metro where I live, usually with outsized representation by one demographic group who constantly bitches about what a raw economic deal they get in this country. This isn’t just recently but for a long time.

Back in 2006, I subsidized the house in a starter subdivision for my mother. When the market crashed, I’d see residents with cars worth about the same or more than their house. That’s completely nuts.

With a median net worth of $120K (2019), most Americans will never build meaningful wealth if a noticeable percentage of their assets is tied up in a car and depreciating. Recent experience is an aberration and won’t last.

When I see evidence and data that Americans have noticeably reduced this type of discretionary expense, I’ll believe they are cutting back.

Not even close to that, yet.

I agree. When I get out, I see all the restaurants are full, all of the time. And, honestly, it astonishes me. That many people can’t actually afford to spend that much money. I would bet that most of these folks are on the south side of that median net worth figure. Enjoy your meals, you math wizards.

Yet another comment that lumps the financially challenged into a causation bin labeled “poor choices.” Please don’t generalize and assume everyone who is not well off is that way because they’re throwing money at booze, cigs, lottery tickets, and the cliché Starbucks.

I am poor. Not because I wouldn’t like to have a good bank balance, but because I’ve spent nearly a decade as a full-time caregiver for a relative who has no money to hire care or to go to a care facility. It’s exhausting and leaves few options for making a living, even working remotely.

I don’t smoke, I don’t drink, I don’t do drugs, but on the rare occasion when I want a break from my depressing life, yes, I do drive through Starbucks. And, yes, before the pandemic quarantined me at home to protect my immunocompromised relative, I used to eat out at fast-casual places. I cherished those brief respites. Do you expect people who are hugging ground level to give up everything and lead a completely joyless life so they can save $300 a year from not getting coffee?

I don’t doubt that there are plenty of poor people who blow money on stupid stuff, but for every one of them, there is a single mom trying to make a life for her family on a low wage and people in their fifties and sixties who have been extruded from the better job market due to age discrimination. Everyone is an individual. They all have their stories. They aren’t stereotypes.

Now, on the bright side, I’ve nursed the same tank of gas in my car for almost six months because I have no life.

Dorothea- Thank you very much for your comment. I’m looking after my 91year old mother. Doubt I would ever have moved here otherwise. It’s not traditionally a good place to make a living. I don’t use tobacco or alcohol, i do drink good coffee, ordered from a roaster. Starbucks tastes burnt to me. Be good to yourself to the extent you’re able to, others often forget that you are sacrificing your time and money to care for someone else. These people making self–righteous comments about the real or imaginary failings of other people say much more about the commenter, and what they’re afraid of.

You’re to be admired, and I hope that better times are ahead of you.

@ Dorothea Lange –

Don’t distress over the smug comments of others. Some of them where born on third base and think they hit a triple. Others suffer from Stockholm syndrome.

“Delayed gratification, self sacrifice, you don’t deserve a cup of coffee”

and other battle cries to keep the servants serving the masters

The beatings will continue until morale improves

-Powell

LOL… I first saw that sign in a Massachusetts auto repair shop. I thought it was funny and mentioned it to the manager who sighed and responded “If only it worked that way.”

Reuters: Parts shortages, high gas prices weigh on US auto market

Major automakers are expected to report on Friday that first-quarter US car and light truck sales fell sharply compared to a year ago, with more uncertainty ahead because of parts shortages, high fuel prices and rising interest rates.

JD Power and LMC Automotive forecast that January-March US car and light truck sales will decline 18% from a year ago, and predict the annualized sales pace for March will slump to 12.7 million vehicles, down from 17.8 million a year ago.

Cox Automotive said earlier this week first quarter US auto sales would be the weakest in a decade.

I have absolutely zero problems in the last three years getting parts for my 06 BMW 750…

Pretty damn reasonable, too…

On the other hand, if you’re trying to buy parts with chips for a recent year, yeah, I can see that…

Real personal income declines for the 9th time in 10 months – Mish

Basement vacancy declines – PK news

Home prices under ‘full-scale attack’ as interest rates, taxes rise – GN

Recent homebuyers fear “greater fool” shortage… PK news

Love your wit.

Economist who called housing bubble warns of market ‘roll over’ ahead – BI

Economist who called housing bubble sells 900sf studio in San Francisco for $9 million -PK news

“As millions of lower-wage people were laid off, the higher wage earners became a bigger proportion of the earners and pushed up the year-over-year gains in average hourly wages.”

A fine insight. It suggests that things are not at all as rosy for working stiffs as the statistics would have you believe. And a lot of people will buy the con instead.

“the biggest inflation items in the article — rents and home purchases — have nothing/zero/zilch to do with chip shortages, supply chain disruptions, and oil and gas prices.”

Another fine insight.

Shortages and supply chain disruptions make excellent cover and great excuses for straightforward price-gouging – in addition to motivating consumers with fomo. People are way too easily suckered with a good con job – er, straight-faced story.

And no, I would NOT like to buy an insurance policy for that replacement DVR. Or for any other common appliance. But they’re always up for weaseling me into falling for the grift.

“And a lot of people will buy the con instead.”

The whole reason MSM nozzles exist…to half or quarter “inform” the casual, low info, channel hopping, drive by voter.

Or to give the illusion of having done so (if you are cynical about the true degree of democracy the US actually employs, with its rather obscure election administration processes).

(Isn’t it odd that CNN, which has enough dead air to expend thousands of hours on an overseas missing jet or to have Michael Avenatti live in their colon for months on end, has never managed to generate a 60 minute “explainer” stepping through US election administration procedures and their invulnerability to gaming/abuse? Should be simple, since CNN itself seems so utterly, utterly sure of it and never, ever shies away from telling the public so.

But is never “here’s why”…it is always “trust us”.

Yes, very fine insights. Wolf, with his excellent and tireless mind, does us great service. Thanks.

The guy is an athlete of the intellect.

Don’t say price wage spiral though, we still have lots of high priced assets to unload before the public catches on to this sham. Fiscal and monetary policy hamstrung by inflation, it’s going to be a long time before the new regime of austerity ends. Fed/congress might try to blow another mini bubble after this one pops, but the labor market tightness won’t allow it without another spurt of inflation

What austerity?

I know you aren’t referring to the USG government budget.

If anything they’ve upped the corporate handouts.

Bonuses are expensive.

Hey Tom, I reckon that if they are genuinely hamstrung then holders won’t be able to unload without most becoming engulfed. I suspect there is yet another shot left in the liquidity pump before the flames taker over, though, even if it’s only based on declining inflation rates and not on deflation. I guess this year might eventually get quite interesting for a few prices if the tightening continues unabated…

The inflationary strategy for wage earners is cut back on discretionary spending, and since wage earners now have a lot more of that the cutbacks should be easier. Short interest in consumer discretionary stocks is increasing. The real pressure is lower income contractors. (landscapers, housecleaning) and that all comes back to their customers.

Let them eat cake!

m.a. and just about any politician you care to name

$27 per hour median wage in manufacturing…

APRIL FOOL MOTHERF…ERS !!!

According to UAW-GM Master Agreement,as things stand in 2022:

1. Tier 1, now making $32.32 an hour, with a pension and retiree health care

(Tier 1 are like Hindu Brahmins, rarely seen, never heard, soon to become totally extinct 😀)

2. Tier 2 hired 2007-2019, to reach $32.32 after four years, with a 401k instead of a pension and no retiree health care.

3. Tier 2 hired after 2019, to reach $32.32 after eight years, with a 401k instead of a pension and no retiree health care.

4. Workers in parts warehouses (CCA) hired before November 2015 will top out at $31.57 in 2022.

5. Workers in parts warehouses (CCA) hired after November 2015 will top out at $25 an hour after eight years.

6. Workers at four Components Holding plants, who progress over eight years from $16.25 to a max of $22.50

7. Temps, making $16.67 an hour, can be laid off at any time and have no dental or vision insurance

8. Flex temps

9. Part-time temps

( Temps are GM’s Future !!! )

10. Workers for GM Subsystems, who aren’t under the same contract as other GM workers but work alongside them in the plants. They make between $13 and $14.85 an hour.

11. Workers at an electric battery plant to be established near Lordstown, Ohio, reportedly to make $17 and not under the GM master agreement.

This list doesn’t include workers for contractors like Aramark, who do jobs inside the plants that used to be done by GM workers: janitorial work at under $16 and skilled-trades work for $25.

Non-union shops pay less.

According to the personal observations of unknown and not very influential statistitian Brent median US manufacturing wage is $17 per hour.

Very insightful if true

we live in con-game times

the younger workers being gamed by the system, with a whole lot of the older generation complicit

Brent,

Seems you confuse “minimum” with “average.” Most of the workers listed on your own list earn over $17 an hours, up to twice that. So the average cannot be $17 an hour. You need to redo the math.

GM is top payer in manufacturing.No matter how corrupt UAW is they have much more bargaining power than ANY individual smart-a$$ worker with Harvard degree in Applied Negotiation Sciences.

There is an old wisdom “You can bargain only collectively.Individually you can only beg.”

During my business travels I see a lot of small CNC shops located in the middle of nowhere, making parts for the likes of Ford & GM.Going wage rate there appears to be $15 per hour.Even less in poor states like West Virginia.

Brent,

Also, you only show GM manufacturing workers. If you pretend to say that your average wage of $17 is reflective of all US workers, you’re spreading BS.

The category “production and nonsupervisory employees” includes ALL workers in ALL industries, EXCEPT managers, and includes the $220,000 a year Facebook coders and the Goldman traders that make a gazillion.

So you need to include the GM engineers, and the GM coders and the finance specialists and all the other other GM employees who are not managers.

Here are some of the major industries whose workers are included here:

Mining and logging

Construction

Manufacturing

Wholesale trade

Retail trade

Transportation and warehousing

Utilities

Information

Financial activities

Professional and business services

Education and health services

Leisure and hospitality

Other services

Mr Richter;

I am a blue collar so my field of vision is limited.I have no idea whether Facebook coder makes $250K because I will never interact with him socially.And he will probably balk at my demand to show me his bank statements with the amount of direct deposits.

UAW-GM Master Agreement covers salaried employees too and can be downloaded from UAW website.

GM White Collar Pecking Order:

Junior Engineer = Level 5 (College grads usually) receive in 2022 starting salary $72K + $8K bonus (which is not guaranteed)

Engineer = Level 6

Senior Engineer = Level 7

Lead Engineer = Level 8 (this is when you get a company car)

Engineering Manager = Level 8

Technical Fellow = Level 9 (most advanced technical position)

Senior Manager = Level 9 (level of useless fat that has grown immensely since 10 years ago.)

Each level has sub-levels, so they can give you little mini-promotions that don’t really mean anything. They’re more used to thwart advancement. “Sorry, you can’t apply for that next level because you’re not at the top of your current level”. That is where you hear 7A, 7B, 7C and so on.

Good life begins above level 9, there are the unclassified ranks where the bonuses are bigger than peon’s salaries:

Director

Executive Director

Vice President

Executive Vice President

So yes-with white shirts thrown in GM median manufacturing wages exceed $31 per hour.

And every small pathetic CNC shop must aspire to grow as big as GM, build their own caste system and, being too-big-to-fail, get bailouts from Almighty Gov when things go sour.

Interesting data.

Personally, I started out at level 5 at GM in 1984 at 25K.

Raises were rapid at that time with inflationary COLA at 7%.

Interesting that almost 40 years later it is at 80K. 80K is actually very low compared to Silicon Valley salaries I know a new college grad hire started at 120K in CA last year.

I left at Level 7 since at the time, I couldn’t see going much higher in the next decade. There was a traffic jam above level 7. I gave up a lifelong pension that is not available anymore to new hires. I had to try to make my own pension.

Wolf said: “The category “production and nonsupervisory employees” includes ALL workers in ALL industries, EXCEPT managers, and includes the $220,000 a year Facebook coders and the Goldman traders that make a gazillion.”

—————————————–

Thanks for this clarification. Somehow, like Brent, I thought production employee had to do with producing something. I laugh at the concept of a Goldman trader producing anything ……… well, other that graft and corruption.

I thought Forbs was now a Chinese publication?

A big part of Forbes is just a blogging platform where they pay independent writers a fixed sum per article (small) plus a commission on the clicks. Years ago, they approached me and explained this to me. Much of the Forbes content you read online is from these independent authors. I have run into a lot of BS from them, and anything with “Forbes” on it instantly goes into the Ignore File.

I am in a fortunate tier where, despite my low earnings, I have a house, a paid-for well-functioning car, and can severely limit those expenses that are spiking. I can ride out a lot.

But I feel for those who do not have this setup in place. I can only hope supply and demand distortions even out. I do not relish the idea of severe stress and social conflict, or the aggravated politics this may bring.

68% of Americans own homes. Even if only half of them ATMd the house in 2018-2021 via Refi, that is a S*** ton of extra $$$ out there available to pay off monthly CC bills for quite some time.

You can blame the Fed, but those homeowners will be fat / happy for years to come. They don’t care about monetary policy.

The renters are losing about 4% annually to inflation per Wolf’s calcs on non-durable goods (6.7% wage gain vs 10.7% inflation on non-d’s), and they can double up in apartments, live with relatives etc (it’s already happening). Pretty much everyone else rides the housing high to infinity.

This can go on a lot longer, especially with .25 / .50 rate hikes every 2 months. Int rates mean nothing when 1/3 of Americans can refi (again). Monthly rate higher, but some of the cash can be used to pay that higher monthly mortgage rate.

no, they will only be fat/happy as long as the value of their homes don’t drop. if they do, they’ll owe tons of money on a deflated asset.

but the flip side to 68% (it’s actually more like 65%) of americans owning homes is that 35% don’t. and those that don’t aren’t too keen on being thrown under the bus to protect those that overleveraged themselves.

He obviously doesn’t or claims not to remember the housing bust or GFC.

In GFC, my home price went from $350k to $160k. I was never underwater. But others lost their perch in the middle class. Which fueled angry populism since then, I think.

In 2008, every bank in the country along with GM, Ford, and Chrysler all required a $1 trillion government bailout.

This after years of being told to work hard and look down upon those living on government welfare.

That fueled the angry popularism.

> I am in a fortunate tier where, despite my low earnings, I have a house, a paid-for well-functioning car, and can severely limit those expenses that are spiking. I can ride out a lot.

Same! For me the gift that keeps on giving is not to have to spend on US healthcare, I get universal coverage from my home country.

I’m Canadian and yes we get universal coverage and yes I believe in Universal Healthcare but the system is not sustainable and to think otherwise is irresponsible. Canada like most western countries has a massive spending problem. The country is in debt up to it’s eyeballs. We should be the wealthiest country in the world in my opinion. We have a small population and are the second biggest country in the world with massive amounts of resources. My wife is American and She has good medical insurance in the states. She makes more in the USA than she would in Canada and housing is cheaper where she is compared to British Columbia. During the 08 Recession the crash in house prices allowed her to get in. House was worth 350k and it went all the way down to 150k which is when she bought. In Canada we haven’t had a proper crash and I have friends who are trying to leave the country and work elsewhere, because housing is to high, they also have good jobs.

Maybe it’s just me but I see perfect storm brewing. Stock market way overvalued. Runaway inflation. All debt increasing. Recession looming. Recessions mean layoffs. You’re not re-fi if you lost your job. Besides lots have re-fied several times already. Car payments, need food, gas. I’m having trouble bringing the old optimism up to speed.

Imagine a speed bump that is square, not rounded.

I’m guessing the pain will get a lot worse once the student loan payment moratorium (supposedly) ends in May. 43 million borrowers at an average of 460 dollars a month, (totalling 20 billion dollars in monthly payments.) I wonder what that will do to credit card debt, consumer spending, etc… 460 dollars is a significant amount.

Lawmakers are already urging President Biden to continue forbearance through the end of this year. I’d be surprised if he doesn’t.

They’re going to have to learn the meaning of “loan” and “debt.”

There appears to be the misconception among young people that “loan” and “debt” mean “freebee.”

@ Wolf –

I think a lot of bankers that get to create money from nothing and collect interest on it share a similar same vision as the students.

freeloading, society ruining creeps ….. (the bankers, not the students)

i think there’s a good chance he extends too, but on the other hand, there’s no longer the good old virus as an excuse anymore. so any forbearance is purely a welfare handout.

The biggest rewards would go to the most careless.

the biggest rewards go to the biggest thieves ……

the ones who steal legally and lie truthfully

all made possible by the state

the state being largely comprised of bought politicians doing the bidding of those who bought them

That’s what concentrated wealth and power does …. it buys continuous advantage, and ruins free markets

then buys pontificators to assure you the concentrated wealth and power is all done in the name of freedom ……

some of the pontificators don’t even know they are bought

forbearance is just kicking the can, so those 43 million people might as well get busy paying their loans off. The other 289 million of us have no intention whatsoever of paying their debts.

yeah that’s the problem with democracy. those 43 million can vote themselves our money.

Kick it long enough, coupled with inflation, you get to pay with worth-less dollars

Wealth of America’s richest 1% reached a record $45.9 trillion at the end of 2021 – more than the bottom 90% combined – as booming stock markets fuels the ultra-rich

The top 1 percent added $6.5 trillion to their net worth last year as stocks and financial markets soared, according to the Federal Reserve’s latest report on household wealth.

Thinking it is time for the new WOKE to be about obesely wealthy people. About 15 years ago the macho man in Hollywood got all the ladies and used his / her power to get what they wanted. That generation is gone. WOKE away. Perhaps the public sentiment about being Musk rich will go out of vogue

Maybe our temporary FED chairman would also be discarded

Do you even know what woke means?

Re: woke

Woke seems to be a anti-pejorative word. Whatever woke is, it must be better than non-woke.

It’s a way of patting oneself on the back when declaring wokeness.

In Buddhism, being awake is the highest enlightenment.

Some smart propagandist has tied the word woke to their cause.

part 2 from previous post (spreading my percent across two direct topics):

so Wolf, what i’m talking about is this:

many would agree that the private equity model and the pump and dump and illusion b.s. thing is so out of hand that it’s what’s killing america. i don’t have the statistics but the general consensus here and where i go, among both (for everything’s binary now) sides, is that America is Over.

you can recite stats about manufacturing but we don’t even loom our own cloth anymore.

i’d read an article in the nytimes awhile back about a fashion designer who’d made a killing in his first venture but now his financiers were into …was it, “destructive properties”?

making money in the breaking down and destruction of companies.

so i was asking you: in this model of destructive investments, has anyone planned for the thinning out of the american dream where your best bet is to hope to one day RENT a house from a corporation who owns most of ’em?

but the HUMAN element is overlooked as if we are continuous cogs and that is where i hope to jack this up.

i was afraid there was no plan. that’s why i no longer believe the WEF is as powerful as i’d heard and see… being The Bad Girl, and MIXED, i see both sides the in between…

and i don’t think there’s a plan when i think of the REALITY of people. everything goes tits up in a hurry especially with power people. i think we’ve been–as you say–amazing and evil– at the same time. that’s humanity for ya.

so i’ve given up the demon idea the mass psychosis the EVERYTHING as i read history and realize, “oh, we’ve done all this before.”

and as for being on the bottom i’ve said it before, you see the worst in humanity. but also the best, right?

that said: i don’t believe there are nefarious plans anymore, only opportunities because people will never miss a chance to make a buck.

and i’m reading Barbara Tuchman’s book on the Black Plague, which is a playbook for every single thing that’s happening now. from the fear the panic to the deaths and to the impoverishment of the lower class of people.

so WEF guy writes a book called RESET or something and i think “reset THIS” because as the other side opposite girl, it may be a fine time to amass some of everyone’s wealth (as in the black plague –and unions were even formed), but it’s also a fine time for We The People to Reset some of the things that need adjusting.

because look at these stats and if you’re gutting the future’s wealth and the dollar might not be the reserve currency and people don’t trust not getting their accounts confiscated at whim or retroactively…

TRUST is gone.

so what next? that is what i was asking and that was a bit MUCH i know, dear friend!

and no one’s planning but i think we’re entering the dark ages (also according to history) and it makes sense if business a whole economic world view is based on gutting the real economy the real world, which no one’s in because they’re on the magic phones.

so then back to PEOPLE… the quirkiest most unpredictable part of this equation. the young people when they feel it’s hopeless and there are less of these “service” jobs because of Ford’s idea that someone’s gotta BUY the cars…

well, what of an economy where the corporations no longer –as with the tech revolution– it changes the human and makes us nothing when the corporation deals business directly with the government (tesla pfizer etc) and then WHO ARE WE?

i mean We the People.

we can’t afford our own homes or keep our own money and it seems it FEELS, for i’m a touchy feely person, it FEELS like they’re against us.

and if it’s true that we’ve been divided all along to keep us bickering among each other for the rancid fetid diminishing spoils, then my aim my overly-ambitious new goal that i share hear to see how far i get, my goal as mixed complicated girl, to try and get us to better understand each other and our human needs, even if in the most utilitarian enlightened self interested way of having FUN.

because if a fashion designer cannot get backing because he needs to LOSE money so they can kill him off and go do the same with another biz, then WE WILL CONTINUE TO NEED THESE BLUE PILLS, ya dig?

they are related.

and this is the very one and only reason i am alive. to remind you here in finance of your humanity as well as ours, down here.

my father is/was a player in his day and i learned the best players love each and every woman they deign to even look at! they bring women back to life.

so i try to love that way as a female but i am quite surprisingly chaste for my ways my tolerances my mouth. i try to go BAM! to your heart and make it start again so you look at what we’ve got here and go, “there has GOT to be a better way” and stop waiting listening for others to tell us when to act riot love sit pray scream.

i’m trying to do the human part of this equation because this is a soulless financial system unattached from anything ALIVE. and yet we’re slaves to understanding it serving it.

oh! the most important part of my history lesson in Barbara Tuchman’s “A Distant Mirror: The Calamitous 14th Century”, is that it was when the CHURCH went too far and started losing its credibility and power.

if you see the CHURCH as the corporate bureaucratic system losing power (just when it thinks it’s gained it via direct gov subsidies…but who’s paying the taxes???)

this ALL happened before so we do what we know to do. no conspiracy theory needed; just PLANS. because whatever you believe, 100% of survey respondents (mine) say “we’re screwed.”

no one’s going zippedy do dah. not even tech people. never before have they looked so haggard so… niggrified.

THIS is why you think you need those blue pills. i know because when i used to spread my legs in the sun i’d think about WHO i was doing it for.

when i just was in the sun a few minutes ago, the entire time i was thinking about WHAT I WAS GONNA WRITE ON WOLFSTREET.COM.

that’s why i’ll need those blue pills. NOOOO! the beat’s wrong on those things. have you seen the porn on blue pills? it is like a Phillip Glass soundtrack on repeat.

x

I’d suggest we are in the dark ages now. We live in societies that are completely lacking in vision, only striving to consume more, without any concept of where it will or should lead, or what it harms. And any single human life therein is also without goal and meaning, it’s just a grind to stamp the tickets and move along, or fall behind and be scorned.

Frankly we are a species gone insane after leaving natural restrictions to our expansion in the past. Our subsequent exponential growth has also lead to the accelerating decline of the surrounding natural environments, climate systems, resource base, and also the currently observed crumbling of the social binds and contracts as we descend into a dog fight for the declining per capita resources.

okay i suppose you’re right about us being in a dark ages. and you said it ALL. but i’m always trying to put off the worst expectations until sometime in the future because you can psych yourself through all kinds of hell that way.

i think that’s really why everyone needs blue pills. how do you get amorous over The End of America when you might end up in a roving RV and eventually unable able to fight off the state’s nursing aides with your walker if you don’t invest wisely TODAY this MOMENT. AHORA. NOW.

but i’m trying to remember my position my vantage point my PREFERENCE and thus this is the opportunity a lot of us have been waiting our entire lives for.

when the lockdowns i heard a voice in my head said, “it’s here now. you’re up.”

i think we each have parts to play and my little one is trying to quickly be the freaky weird art teacher like some of us had in the 70s and 80s. i’m trying to LIVE out philosophy. i leave the apartment early enough to ask questions with really long open answers because Saltcreep, you’d be amazed at how fast people can wake up. they often revert back because there’s no support.

that’s why i wanna start a local thing if i can and inspire others to do it where they are. it takes over you like music, being around people and losing track of time and laughing and messing up and going too far so you have to apologize but then no one cares. that’s the fantasy part.

but i’m trying to do the artist’s job. flap our butterfly wings in the darkness and hope we cause tsunamis on a sunny morning in Idaho.

that’s why no time for secrets glam holding in stomachs. must share mistakes lessons ideas. apologies assumed ahead of time.

that kinda thing.

x

Hey kl, just the other day I was discussing with a guy at work about the relative merits of actively fighting the inevitable or just passively accepting it. He was firmly in the Don Quijote camp and I’m more in the nihilist vacuum. So pay no attention to me!

When we watch a movie, we see what the director wants us to see from the the perspective of how said director wishes to manipulate the scene to trigger a certain response…

Whether it be happy, sad, horror, sympathy, empathy, etc…

Regardless of how you got here, you didn’t have a choice…

What you did have a choice in was whether or not to steal the tires you made sandals from…. )

Are you not entertained?

Saltcreep-

I hear you saying that there was a much better past, and a better future for our world is not possible. But was the past really better? And must the future really be dystopic futility?

Kitten L. is onto something.

I like the line from Cool Hand Luke: “you got to get your mind right.” Now, like always, is the time for self discipline.

Read Will Durant’s Lessons of History for a cosmic vision of humanity’s road… in 90 pages.

Hi John. As I sit down here on a sunny afternoon to read your book recommendation whilst sipping wine and nibbling cheese and olives I guess I can see how other views are still prevalent amongst those of us who are fortunate enough to live in certain places and circumstances.

But I hope you will forgive me for being a droning bore and contending that we live in a blip in time that is not sustainable and that is fading before our eyes. Even for those whose lives are materially seemingly secure we are struggling for place and purpose in a society where our only real function is to consume, and where only those close to us care if we’re there or not. In the atomised world we live in loneliness and isolation has become an epidemic. We have tried to use the moment of excess to eliminate risk from our lives, and end up with a pretty controlled and powerless existence.

And we have largely ruined the natural environment we live in and strained energy and other resources beyond the breaking point. The massive boost we got from fossil fuels is gradually fading with the passing years, as we pile on debt in exponentially growing terms in order to try to paper over the declining productivity and increasing discontent and stratification, as we sober up to be faced with the size of the bill for our excesses.

Salt-eloquent, as always. Life will go on. Specific forms of life-or their lifestyles-won’t…

John H.-the Durants were giants of their time and the Western/Eurocentric viewpoint. Planetary geographic science/ history data since then has greatly expanded, however, and should be a backdrop to all prior students of human history as they are now inseparable from that ‘cosmic vision’.

kl-engage, adapt, and overcome-i have no doubt this is what you’ve always done best …

may we all find a better day.

I enjoy your posts kitten, please keep expressing yourself

thank you. i try and Wolf really is important to me because he keeps bringing me back.

funny because it’s the WHITE GUYS who say “more! more! more!” and let me think and be as complicated awkward and weird as i am. it’s always been that way.

always.

anyhow, thank you No 1 for saying the same blessing to me.

xxxxx

Did you accidentally paste part of your Match profile in here?

I also think you’ve read “Howl” by Allen Ginsberg a few too many times, especially Part II about Moloch.

BTW I believe your father wasn’t a player. IMHO he was probably a love bomber. Look up the term.

Love bombers are manipulators who use overwhelming attention and affection to build trust, as a means to gain control, and ultimately sucking the emotion and joy for life right out of their partners. Once they set the hook, they turn into angry control freaks.

The online dating sites are chock full of love bombers looking for prey. It’s a target-rich environment.

Sorry about the detour Wolf. Moloch made me do it. I’ll toss in some Moloch financial stuff to make it legitimate:

Moloch! Moloch! Robot apartments! invisible suburbs!

skeleton treasuries! blind capitals! demonic

industries! spectral nations! invincible mad

houses! granite cocks! monstrous bombs!

Michael Gorback-

you’re confused as hell.

i’ll be back. i’m your fan so i’m gonna take extra time and think about you as i spread my legs in the sun and think of YOU howling like a coyote.

the proper response to ALL of this will come from that…

more later.

x

p.s. and people like me never had “match” profiles, dated online or done personal ads in the old papers. there’s no analogue for someone me that’s why i’m still here in The Real World.

it’s magical here. when i used to dance outside all the time i knew “my next man will be the one with the courage to come up and kiss me.”

it sounded bizarre. but a year later or so IT HAPPENED.

i’m for real and no, my father was not a love bomber. he IS a motherfxckin ANGEL. and all who’re like me are secret unknown angels taught to live according to these financial societal and all the RULES here that we are forced to conform to , barely understand, yet live by.

and they are anti-human against YOU. you especially Michael Gorback, you are too hilarious for Them. i know you are kin even if you think not. i KNOW YOU.

—

more later after i slip back into my muumuu and tire sandals and get my martini or whatever COWGrrrl says i drink…

(at the very bottom i’ll start my mass response anew because this is a very important conversation. it is EVERYTHING.)

K-Lo

The old story is if someone guesses its 12:00 pm he/she will be correct once per day no matter how many bad guesses.

Well……JP has guessed that we did not need to raise rates and sell securities to slow inflation lots of times…….guess what…..he may be right.

The inflation he has created looks like its starting to slow consumer spending……which will eventually slow the economy and slow inflation.

Of course before we have a real slow down Congress will be going ape like in its efforts to pass more spending…..which will goose even more inflation…..and my fear of hyper inflation.

All the while JP wonders if his 5 iron can really go 180 yards.

I went to a farm action yesterday….land that would have sold for $7500 per acre two years ago…… sold for $16,000 per acre.

The danger is there……..if the morons don’t let up……..any further spending will be like gas poured on a forest fire. No central bank in its right mind will hold a reserve that is melting in value…….these sanctions against Russia are also giving the world a real look at just how stable and secure their dollar assets are if they do anything opposed to our morons.

Bottom line….nobody liked 1929……..but……..at least we survived as a nation……..see Germany in the Weimar years.

As inflation rages upward, it will cut the financial legs out from under an ever expanding group of working people. The lower incomes are already cut to only high priority expenditures and nothing else.

The endless “refinancing” someone mentioned will become unavailable to ever increasing numbers of “comfortable at the moment” folks, not due to mortgage rate increases, but their grotesquely eroded ability to service debt from wages that are a “joke” as compared to the outlays they are facing.

Food, fuel, energy, housing costs, and soon more taxes, absorb more and more of a barely increasing annual budget.

The impact of this mess, compounded by massive policy errors, will be felt for decades to come.

An economy where the average wage is $65k per year is one that 99% of the world’s countries can only dream of…

R

Now that is a silly comment.

Compensation minus cost of living is the economically correct way to evaluate such things.

Americans can only dream of the vastly reduced costs of living that are enjoyed by so many countries in the world……

An economy where the average disposable income PPP is $55k per year is one that 99% of the world’s countries can only dream of…

Averages are irrelevant. The US median household income is about $67K. That’s before tax.

Depending upon family size, it’s middle class in Topka, KS and much of “flyover country”.

It’s working class or lower on much of the east and west coasts and many larger cities in-between. A noticeable majority of households in NYC, DC, SF and LA are actually poor, unless they are feeding at the public trough and often even with it.

The percentage of US households that are actually middle class (or higher) is probably somewhere in the vicinity of 20% to 40%, once again depending upon location and household size.

This number is destined to shrink once cheap credit, lax lending standards, and government subsidies no longer suffice.

R

You are repeating yourself.

The good ole USA is a very expensive place to live. The vast majority of humankind doesn’t live here and just aren’t interested in moving here.

That income you quoted is pitifully inadequate when weighed against the cost of housing, transportation, health care and education. You know, the actual staples of life.

Word is out. The few trying to get in by any means are typically under educated about the true reality of the USA.

What AF and OTB said. The supposed high salaries and wealth of Americans is an illusion, too often fails to account for differentials in cost of living. Most places I’ve worked overseas have much lower costs for everything, esp the basics like housing and food, so even though they mostly don’t make as much as we do they also can frequently afford more. Most things in the US cost way more than elsewhere in the world, esp. healthcare and schooling but more and more, also housing and food. Potential immigrants are in fact more aware of that and it’s why there’s less and less interest for skilled workers to come here.

Even if the starting salary looks higher in the USA (and even that’s lower than many other places), it’s useless if you can’t really save up your earnings, buy a home or improve financially, which inflation and the housing bubble are making super-difficult as Wolf’s charts are showing more and more. Sure, we still get immigration from places that are so full of poverty and corruption that people really don’t have much alternative, But when workers and specialists with skills have options, the US is looking less and less attractive. It’s another heavy price of the Fed’s policy failures and the inflation and asset bubbles resulting from it.

Please search for the word “pave” in the article and replace it with pace.

Darn Anti-Pave-ites! Always expecting us to tend the planet to keep up with the “pace” they set. Next, they’ll be wanting us to fix NASA by building a whole new generation of shuttles that don’t implode everytime a space monkey cuts a fart. And they’ll want it accomplished on a reasonable budget including $12.95 per toilet seat cover regardless of the extra cost of an anti-gravity sealing system (i.e. common magnets). What’s the world coming too? 🙀😹😹😹😹

He’s pointing to a specific period in time, such that it might read: “There, relatively lower wages fell….”. But who gives a shiva’s ass about the rules of American English anymore. Half the damn population can’t even express themselves coherently. Most are mumblers. Seinfeld’s “low talkers”!🤐

You are truly gifted, brother BuySome. But you ask, who cares? I care. I, Prophet. Now, it shall be written into law: These articles shall be sanitized, transcribed to parchment and preserved, and archived so that generations yet born might benefit from these glorious writings.

What if nobody cares that you care? Do you care?

And BuySome: there’s only one Shiva. You can’t give “a” Shiva’s ass. You can only give “the” Shiva’s ass. Keep up the good work with those Hindu studies.

Curious? Where does the increasing talk of no paper dollars come into play here? Controlled digital spending based on your social credit score. Is that really possible in the next decade? Or will there finally be a citizen revolt before they gain that much control?

The past 2 years would indicate no revolt.

We have keyboards to release our frustrations.

Wait

And in the next recession, the drop in hourly wages will look equally ridiculous when compared to prices. Yes the later will drop, just much slower than wages.

Won’t someone please think of our billionaires?