Undeterred by spiking prices and shortages.

By Wolf Richter for WOLF STREET.

Consumers borrowed bravely in December, amid shortages of all kinds, particularly new vehicle shortages, and amid skyrocketing prices of new and used vehicles, and sharply higher prices on other goods and services. Undeterred, consumers bought not what they wanted to buy, but what there was to buy. And enough consumers borrowed to do so in order to make banks smile again.

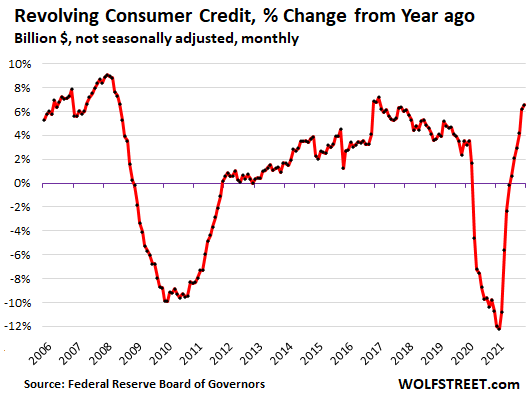

Balances on credit cards and other revolving credit jumped by 6.6% year-over-year, to $1.04 trillion, not seasonally adjusted, according to the Federal Reserve Board of Governors today. This has come up a long way from 2020 and through mid-2021 when consumers, awash in free money, slashed their rip-off-credit-card balances to the detriment of the banks that suddenly weren’t earning 29% or whatever on those slashed credit-card balances. But consumers are now atoning for those sins:

In reality, the people that charge up their credit cards and pay usurious interest on their cards are a subset of consumers because a lot of consumers carry no credit card debt. They just use their cards as payment devices and pay them off every month.

But still, even these efforts in December 2021 didn’t beat the borrowing binge of December 2019 because enough people were still flush with cash, and they were earning more money too, and they didn’t need to borrow as much on their rip-off credit cards. Credit card balances in December were 4.9% below December 2019.

I’ve been screaming for a year-and-a-half about the seasonal adjustments during the pandemic when the well-established seasonality was upended. So here we go.

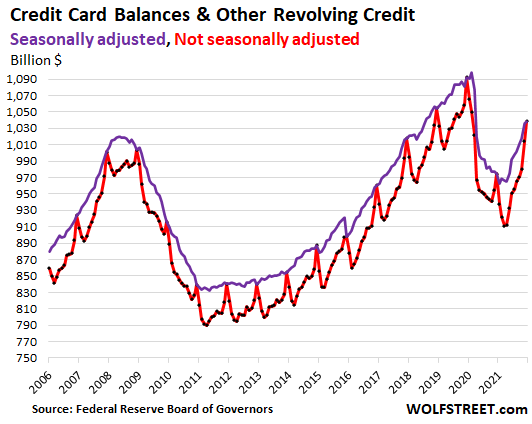

On a seasonally adjusted basis, revolving credit balances rose to $1.04 trillion – yes, same as not-seasonally adjusted because December is the month when seasonal adjustments get pegged to not-seasonally adjusted data, as you can see in the chart below. In the not-seasonally adjusted data (red), the peaks are in December. The seasonally adjusted data (purple) rides on top of all the Decembers:

What happened with auto loans & leases is truly amazing.

The number of new vehicles sold in December plunged 28% from a year earlier, amid the worst new vehicle shortage in history, as dealers had very little for sale on the lot.

But vehicles were sold for ridiculous prices that often included addendum stickers of thousands of dollars on top of MSRP. In addition, automakers, having gotten hammered by the chip shortage and not being able to produce large numbers, prioritized their costliest models and equipment packages. As a result, the average transaction price, as tracked by J.D. Power, spiked by 20% year over year in December, to $45,700:

![]()

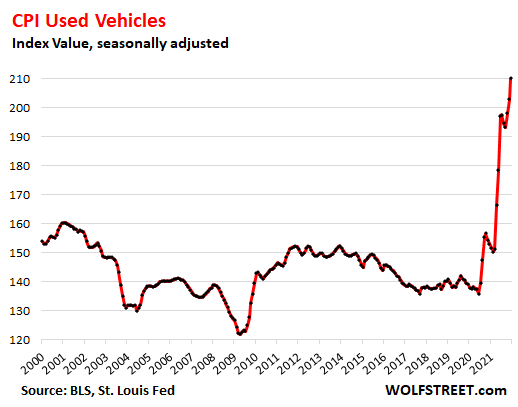

Used vehicle retail sales declined about 6% year-over-year in December, according to Cox Automotive. But prices went even crazier than new-vehicle prices and jumped by 37% year-over-year, according the CPI for used vehicles:

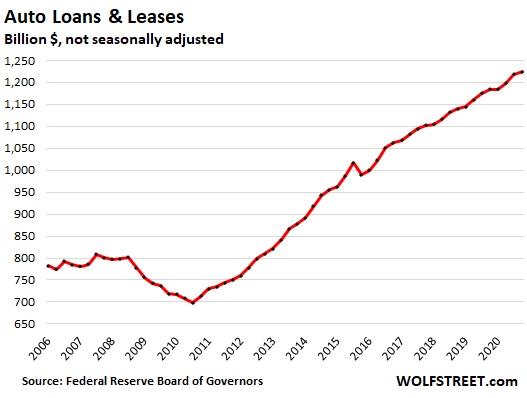

The amazing thing is how this collapsed volume in unit sales – down 28% for new vehicles and down 6% for used vehicles – and the huge price increases fused into the phenomenon of consumers borrowing more to buy a whole lot less.

Total auto loans and leases outstanding in the third quarter rose 3.4% from a year ago, to a new record of $1.22 trillion, despite the plunge in volume. This is another aspect of inflation: consumers borrow more to buy less:

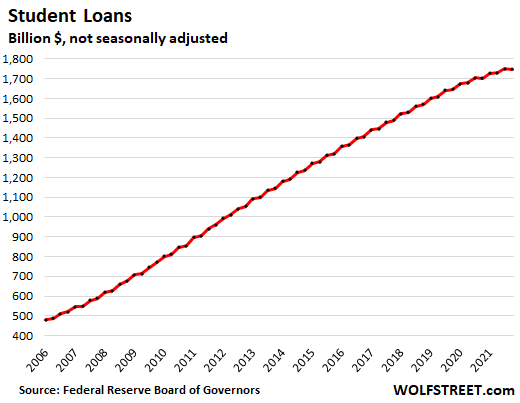

Student loans still in forbearance.

Automatic student loan forbearance has been extended for the umpteenth time, this time through May 1, 2022. We’re going to call it the Spandex forbearance program. It means 0% interest on balances and no payments due. Global loan forgiveness has been averted so far, but numerous specific student-loan forgiveness programs have been in effect for years, and more have been added during the pandemic.

By now, no one is paying down their student loans anymore. They just borrow, betting that they’ll never have to pay off those loans. Even in prior years, loan payments were often so small that they didn’t even cover the interest, and the balances kept growing, despite years of declining enrollment, and even more sharply declining enrollment during the pandemic.

In Q4, balances ticked down by a tiny $2 billion from the prior quarter, not because anyone made any payments, but because various programs of loan forgiveness removed more loans from the tally than new loans were added.

The balance in Q4 of $1.75 trillion, the second highest ever, was nevertheless up 2.7% from Q4 in 2020:

All these forms of consumer credit combined – revolving credit, auto loans, and student loans – rose 5.9% year over year in December to a record $4.43 trillion, seasonally adjusted and not seasonally adjusted (December is the month when seasonal adjustments get pegged to not-seasonally adjusted credit). So consumers did their part flawlessly. They’re borrowing more to buy less. And little by little, they’re making sure that banks and auto lenders are once again able to maximize their profits.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Something like 80% of cars are bought on credit. 1/4 are leased. So, most folks don’t even notice the sticker price or extra add ons.

You don’t win the game of life by being this helpless. Most managed to get thru 12 years of school without basic understanding of money.

If I had a sheep station (ranch), I’d stock it with Americans. Feed on grass, shear each Spring and slaughter the old rams. Good business, no complaints…

Ah, the good old days when men were men, and sheep were nervous ;>{)

Unfortunately most young people were on the lesson hard regarding interest rates. You would think the negative feedback would leave an indelible impression..

There is no cure for an irresponsible sense of self entitlement, except maybe true poverty.

Bankruptcy isn’t enough anymore. Within no time, it’s rinse and repeat.

That’s what happens with the perverse incentives of systemic moral hazard.

unending student loan forbearance = student loan forgiveness

Federal Reserve critters never learned the interest rate lessons, why should “we the rabble?

@JGarbo

“I’d stock it with Americans.”

—

The mainstream of any population are a mathematical product of their circumstances. Some individuals switch out over time.

I bet ancient Athens was very similar to prosperous, post-modern America in the way you describe.

This doesn’t contradict your post however!

Would be interesting to see a graph of the length of the lease period over time. I’d imagine it’s gone up to keep the monthly rate the same.

Leases don’t work like that. Since you are basically renting the car then unlike a car loan, extending the term of the lease doesn’t lower the monthly amount. Also, the leasing company wants to make a good profit on the returned vehicles and they normally don’t want to mess with cars which are too old.

With respect to car loans, the average length is now about six years for new cars and 5.5 years for used cars. It’s important to note though that cars are lasting longer. The average age of vehicles on the road now is 12 years.

Auto leases are the new baby house mortgages.

Fair point on the dynamic of leasing vs loans, thx.

A book could be written about student loans. I think it is a symbol of the distortions caused by easy money. They also remind me of Japanese hangover. Didn’t want to acknowledge bad debt.

It’s going to say a lot about society if they are written off, because a lot of people worked during college to ensure no debt and a lot of people did the Ramsey style and did without for years to pay it off

Who cares. There are thousands of other areas in this godforsaken country to make the same moronic stand. I didn’t vote in the politicians who put us trillions in dollars in debt to fight pointless wars. Same goes for wall street scum standing next to the money spigot etc etc. Fertility rates are going through the floor and people can’t afford to form families but at least we learned a moral lesson while the country falls apart and we are unable to fund the ponzi scheme afloat any longer because the demographics are upside down. Nothing would ever get done if everything had to be perfectly fair. Also, student loan forgiveness will never happen. It’s too convenient a method of control for the elites. They’d rather let it all burn down before forgiving any debts

Stop saying “elites” and you will be less of a serf.

Prayer helps, too.

Student loans were Obama’s stealth welfare. No place to go except grad school. The Boomers made absolutely sick money from it, especially university “administrators.” And it’s the usually sneak, give it away now and we’ll forgive it in a decade or so. I feel bad for the chumps who actually paid the loans back.

“I love the poorly educated!”

Could there be a corelation between our failure to provide “consumers” a basic financial education and our failure to teach the fundamentals of a functioning democracy to our “citizens”? It seems that ignorance is highly valued in the USA and we have far more consumers than we do citizens.

Someone must have told him that line might make some of them think, so he started saying “You are the smart ones” at his rallies.

The end of this cycle is at hand, not because of consumers getting wise but because we are in a diminishing returns curve. This is going to be a doozy when we hit the next recession, it is not going to be a pretty sight.

I expect massive debt forgiveness in order to stave off the social uprisings.

“I expect massive debt forgiveness in order to stave off the social uprisings.”

I don’t. There’s no free lunch. Can’t pay? So sorry.

Bailing out reckless borrowers by punishing savers has been going on for full 2 decades now. Yes there are free lunches everywhere in this corrupt system, specially for the rich.

Kunal-

Is it the rich who are consumer credit balances? Or who are referred to as “debt slaves?” Not in the main, IMHO.

The alter at which we pay homage to the gods of economic growth and stabilization are spattered with the blood of the debt-slaves who might have been rich in their old age.

Or maybe I misunderstood your last sentence…

exactly, just look at TNX since 2008…you will see the fed masterpiece of illusion….

Wise rulers will forgive debt, provide bread and circus to the population to stave of social unrest. I sometimes doubt the wisdom of the rulers in the USA.

We have been leaning towards totalitarian socialism for the past few years. The next elections will have a lot of young folks voting for debt forgiveness, and a substantial amount of the rest of the middle class too.

The “mob” will also support the forgiveness offered by the politicians. “There is a hard rain coming” Dylon

The problem with this idea is that expectations keep on increasing, eventually making it unaffordable.

American expectations are totally detached from reality. Look at how most people live, even those who are supposedly poor. The country doesn’t provide these living standards with its own production but from others. Over half the population is also feeding at the public trough, in one form or another. It’s unsustainable.

These living standards are only “affordable” with artificially low interest rates, an overvalued currency, and the loosest credit standards ever.

The entitlement heavy Federal budget is nothing less than modern bread and circuses. It’s been going on for decades and get worse every administration.

There’s not one politician in the USA who has the balls to suggest ending subsidies or entitlements.

“Entitlements” is a misnomer. People pay into Medicare and Social Security. Over the past 20 years, people paid more into SS than SS paid out. So bread and circus?

There are however huge subsidies for entire industries, and for farming, and even for “farms” that are nothing but suburban homes of lawmakers that get farming subsidies, etc. New subsidies of $100 billion are now being put together for the chip makers, including Intel. Boeing and the airlines got huge subsidies during the pandemic. The Defense and intelligence budget, which is spread around multiple departments so you don’t see all in one place, including the DOE which handles the nuclear armaments, enriches the military-industrial-intelligence complex. These are the things that need to be slashed.

Wolf

‘These are the things that need to be slashed’

Without serious campaign contribution reform, nothing will change and no lawmaker can afford to bite the hands that feeds them via K-street, for their elections.

In 2014, SCOTUS declared a Corporation is a citizen too and money is free speech! They are in control! They will continue to have ALL the subsidies, whether needed or not!

Implicit,

“It’s a hard rain, gonna fall” -DylAn.

Attempting to spin someone you are the antithesis to just isn’t very bright. Although I got a good laugh out of it.

IMHO this isn’t how the establishment thinks.

You have a country, your rival country is your competitor. How do you “win”? You force people to work for as long as possible for as little as possible. Okay! Get the whips out? No, that doesn’t work medium term. Use soft power. Make them want to work. Make them have to work.

How do you force someone to work? You use debt. What if debt gets too much and people become demotivated? Forgive some of the debt. You can always get them in debt again.

The key to this open prison is to make sure you don’t get in a situation where a majority can refuse to work. How can they refuse to work? If they own their own home and have no debt.

The establishment can forgive debt fine without violating this rule.

Property Taxes enter the chat…

“What if debt gets too much and people become demotivated? Forgive some of the debt. You can always get them in debt again.”

Made me think of the historical Jewish implementation of “Jubilee” (Yovel) circa 600 BC, in which every 50 years it was mandated to forgive all debts, and free all slaves. What is not usually mentioned is that all the designated landowners in the designated tribal lands kept their land permanently, regardless of what happened. Even if a landowner had gone into debt and sold their land, they got their land back in Jubilee year.

So the Jubilee deconstructed the evolving tangled web of debt activities, and that benefited many indebted non-landowners in various ways. But the landowning class endured. And the new cycle of debt began again.

> property taxes

No that’s a very basic error. Land value tax means taxing the unimproved value of land, not the property on it. Maybe know that before dismissing an entire idea, unless you have no intention of comprehending it because you are a landlord.

Who owns this debt you speak of forgiving?

The govt guarantees them all, clearly they can’t nullify privately held assets without recompensing the holder.

“A Christmas Carol is the heartwarming tale about how rich people must be supernaturally terrorized into sharing.”

From my WS folder…..probably Unamused.

That is how the CCP’s tyrannical leaders rule China. The USA has been operated more like Mr. Bean operated his car: recklessly and avoiding disaster only by the grace of god.

In the US, deceit and manipulation are used by the ultra-rich to the same effect: to keep wages paid low and to try to avoid taxation by transferring US jobs to countries that do not tax their income significantly, while the US foreign income exclusion from taxation protects them from having to pay US taxes while they keep that foreign income outside the US. (That is technically “keep it out of the US,” because actually, they can put the money in Irish or other foreign companies that in turn invest the very same funds in the US.) As a result, the ultrarich effectively armed the PLA, indirectly.

The key thing that most Americans fail to realize is that the ultrarich in the US and EU (often the same trillionaire family members) are coordinating their tactics via their control of US media, US politicians, etc., but do not appear actually to have an intelligent plan for the future, except to steal all that they can while they can and avoid paying taxes. That is why extractive industries, for example, just want to get out all the oil or metals or other things that they can at the lowest cost while avoiding paying for the polluted rivers or land: e.g., in California, if you want to buy undeveloped land as an investment, you better have it carefully tested first, because for decades, a lot of California companies just disposed of their toxic waste by driving it to some deserted area and dumping it on some neighbor’s land.

Now, if you unknowingly buy that contaminated, California land, and the toxic waste is discovered, you may wind up being required to pay more than the value of the land to clean up the toxic waste and also pay damages as it spreads to neighbors’ land. On the other hand, you can have a lot of other, dangerous conditions in land in California and the courts will not force you to fix them, if your lawyers pre-bribed the right judges by contributing to their campaigns. (However, a little research will reveal to you that those who discovered that there was toxic waste on their land suffered for it even if they were not the dumpers of the waste.)

I expect militarized police to stave off social uprisings, should they occur.

New jobs program: work off your student loan by getting in uniform and taking a truncheon to the angry peasants who mismanaged their financial lives! Dog eat dog.

Meanwhile, don’t these student loans have creditors? Aren’t they upset and willing to pull their capital, going forward? Doesn’t this dismantle the colleges? For some, that is overdue, the system has lots of waste and fraud, but the college where I teach is extremely affordable. I willingly take a persistently low wage.

It’s called capitalism, I mean fascism, I mean capitalism. What’s the difference, you ask ? Neither one is capable of providing justice, peace or compassion. What’s the solution, you ask ?

Self determination in the form of participatory democracy wherein the fruits of our labor are not stolen from us in the form of wage slavery and blood sucking rentiers. Some call it socialism.

General Strike,

If you were about 75 you would known that socialist countries had horrible standards of living compared to Western democracies. I don’t think Poland or Hungary will be going back to socialism.

No, it will be Fascism, just like the man said. Corporations ALWAYS do best under that system. For now they have to infest and destroy democracies as best they can,,,,,,,,

I’ve been paying on my (private) student loans this entire time. Never got payments stopped for covid. I damn well better get something for that if all the loans get forgiven, but I know I won’t.

Shout out to the guy I work with who used his money “saved” from loan forbearance to get a mortgage on a house, then flip it for a profit a couple months later.

I paid my 50k plus private student loan off in a little under 2 years. I don’t care if loans get forgiven. Everyone in this country views everything as a zero sum game where everyone is their competitor. This is a societal sickness passed down from the sociopathic wealthy elites who actually believe that. We have no community anymore. Everything is money, money, money.

Depends on the numbers…

Option #1 : Forgiveness no strife.

Option #2 : No forgiveness, lots of strife.

The banks have a problem this time with the # of loans and people who hold them.

If the Dems don’t give trounced at the polls over forgiveness we’re lost. But nothing surprises me anymore. And I’m OK with forgiving $10K for the community college crew. That was an obvious ripoff.

There is already a solution to unpayable debt. It’s called bankruptcy. It doesn’t usually cover student loans but that can and probably will be changed.

The actual intent behind loan forgiveness is frequently more disguised income and wealth redistribution.

Claim these deadbeats are “victims” (of something), use regulations to mandate “lending” to them, and then forgive it. It’s no different than directly stealing.

In the past, most of these deadbeats never would have obtained a loan to begin with. It was also embarrassing to default or file for bankruptcy. Now, people typically aren’t embarrassed by anything.

If lending wasn’t so detached, those who default or file for bankruptcy wouldn’t ever be able to borrow again, except at actual loan shark rates.

The trouble with bankruptcies is that if the debtor nothing have, the creditor lose it all. And that is really bad, the bank then loses money.

Never giving loan to those defaulting again also harm the banks, they loose customers that way. ;)

“Claim these deadbeats are “victims” (of something), use regulations to mandate “lending” to them, and then forgive it. It’s no different than directly stealing”

70% of student loan balances are carried by the ladies. They are a protected class. As such they have no agency and are bona fide permanent victims. They expect no repercussions for their actions.

moonbat

now that’s empowerment for you.

August Frost

‘ It doesn’t usually cover student loans but that can and probably will be changed’

All debtors except student loan holders can declare bankruptcy.

Wonder Why?

Banks campaigned to make sure specifically that there is NO bankruptcy protection law for student loans. This was intentional!

Prez Biden when he was senator and or VP was a key figure and instrumental in passing this legislation. Then the LOOT began by the (irresponsible) banks and the greedy universities in raising tution fees. Now Taxpayers are on the hook! Everything online. Crooks are in charge and sheeple keep complaining and moaning! Go figure!

The banks have created their own monster. Let me give you an example:

Someone I know borrowed $1,100 on a credit card. Made over $800 in payments on the debt, but then then their business imploded and they ended up defaulting on the debt. By the time the debt was finally discharged in bankruptcy, the bank claimed that they owed over $5,000.

How did it get there? First, once the account went into arrears, the interest rate jumped to the 29.99% APR “penalty rate”. The account also accumulated a $40/month “late payment fee”, and shortly thereafter a $60/month “over credit limit fee”. With fees and interest, the balance exploded until the bank finally charged off the account and stopped bothering to add to the balance.

When offered the $600 that would have paid both the original balance and interest on that balance at the original interest rate, the bank refused and demanded the $5,000 instead.

This account and several others were discharged through bankruptcy because once somebody gets “behind”, the behavior of the banks and the buyers of distressed debt collectively make it impossible to get out of the hole any other way.

If you want to “reform” bankruptcy, you could start by making the predatory practices illegal that drive people into bankruptcy.

Why do people end up in bankruptcy? Top three: Medical Bills, Extended Unemployment and Divorce.

Market is behaving different for sure. QQQ rolling over. Conservative dividend payers and gold miners up. Maybe the big rotation people have been waiting for.

I own an old early 70’s f350 dually with a utility body. Paid $2600 for it in 1992. It gets 6 miles per gallon on a good day going down hill and continues to run like a top. I only keep it as a back up truck to pull my trailer. I bet I could get more than what I paid for it back then, rust and all. Best part about it is there’s no loan on it.

Something’s seriously wrong with this economy.

We’ve got 20 year olds buying $75,000 diesel trucks on a pauper’s wage.

The demographic you suggest will some sense that they are poor, I’m sure, but youth needs achievement.

If real achievement is unattainable, it will be replaced with baubles. Cars, houses, University degrees increasingly, the just right for now partner, etc.

Then when the shine fades, bitterness, relationship breakdown, mental health problems develop.

Some will move on to new baubles and repeat the cycle.

Some will move in with someone new, perhaps someone who has kids, and so life will stabilise, but at a financially poorer level.

Some will land hard and stay there, bewildered by the change and unable to move beyond the hurt.

Some will reinvent themselves, but but remain wary of financial and relationship commitments (they are also more likely to be shunned socially as they will lack common social problems over which to bond with their now aging demographic)

But some will be totally fine. Their kids on the other hand…

I fall into that last group, but jokes on you! Not having kids.

I was leading-edge in my boomer generation. No kids. But liberty and integrity all the way down. I am a contributing member of society, and my “kids” are students I strive to toughen up and smarten up.

My new camaro z28 5900$ in 1977 on 7$ a hour wage ,lots of overtime

$7/hr in 1977 is the equivalent of $32/hr in 2021.

I suspect that 75000 diesel will be sold for a hefty discount in a few years. Nobody knows when this coming recession will hit, but it will, and it’ll be ugly. Maybe that diesel will be my next truck and the old f350 will get retired (replaced by my current 14 year old daily driver truck). I sure hope this recession doesn’t go to a depression, but it probably will. Regardless, a couple of years into the down cycle and there will be all sorts of vehicles on the market people shouldn’t have bought. I figure there’ll be all sorts of good deals on motor homes, too.

That also will come to roost when gasoline and diesel go well over $5/gallon. Around here (Houston, TX) I am seeing way more $75 K trucks and BMW’s than I have seen in 30 years.

DC

All this new generation wants is a good iPhone a good vehicle a couch and a big TV

Don’t forget DoorDash and GrubHub deliveries.

So the bare minimum of the every prior generation from the last 50 years?

God forbid.

Yep, paid $2,800 for a 2005 Mazda bought 6 years ago, and $5000 2001 X5 BMW 7 years ago.

I’ve averaged about $1,350 each year to keep them in decent shape.

Bought a whole driver side front door a month ago for the BMW for $300 that was kept at temperature controlled building just to get the handle, inside cables, and locking mechanism. They give a 10% discount when you pay cash.

The first replacement handle I bought on eBay was cheap plastic, and broke during 5° temperatures. A BMW dealership would have charged me over $400 for all the original parts.

My mechanic doesn’t mind when I supply the parts for the cars. I pay him cash, so Just being charged for labor. Original parts work much better, and last a lot longer.

I’d rather spend my money on fun things, vacations, eating out etc

The engines on both cars run well; both head under $100,000 miles on them when I bought them. Obviously I don’t mind putting up with the grief of getting the cars fixed. I’m 70 years old and only had one loan for a car when our four kids were young.

Funny…while I read this, I was served an ad for DriveTime.com. Their whole pitch was centered around a down payment and the monthly payment to get a car.

The business of debt slavery is alive and well.

Poor people have been in the “payment only” world for decades.

No debt, no problems….

I bought two cars off lease.

Second that

What kind of interest is being paid on auto loans? Seems like I remember back a while ago seeing auto dealer’s adverising low interest rate loans. If you get a loan with interest at one third inflation, aren’t you getting a cut of the lending agency’s profits?

Nope, chopped, diced, mushed, into canned pork packages and sold on to investors as assets.

The end investors take the haircut, a pension fund nearby perhaps.

Which leads me to; how many pension funds have been struggling due to student debt non-payment?

TimTim. The USA Fed Gov (as of 16 Nov. 2020) owned 92% of the Student debt.

While I paid off my own college debts back in the 70’s. I could tolerate the gov’t zeroing out the debt if it got the Younguns back on the track to being productive citizens.

But then the Gov’t should get out of the market for student debt, and remove the prohibition against it being canceled in bankruptcy.

Fair point. Thank you for that.

My point then would seem to apply to the packaged and sold on auto loans only.

Hmmm… I am not seeing the big increase in auto loans in that last graph. It seems like loans are rising pretty much at the same pace as they have been since 2011. Granted there are fewer cars being sold… but because of chip problems and other COVID-related issues, automakers have been limiting their production to the most expensive vehicles.

So it is not so much that people are borrowing more to buy less as it is that they are borrowing a third more to buy slightly more. Perhaps the trade-in value they are getting makes these numbers work for them???

New vehicle unit sales down 28% and used vehicle unit sales down 6%, prices spiked… look at the charts. Consumers bought 20% fewer total vehicles and borrowed more to do it.

I cringe every time I think about having to buy a new/used car.

My 2004 Chevy Cavalier is the best car I have ever owned.

It is a 5 speed stick with nothing powered. No power windows, door locks etc. It gets 30 miles to the gallon and gets me to work which is all I need it to do.

I pay 40 dollars a month for liability insurance and use full synthetic oil.

I use milk and butter in my old 1st gen Chevy small block. Creamy goodness.

– Based on my (limited) information, it seems that car inventories are actually starting to grow.

– There was a RECORD spike in inventories in the last 3 months of 2021:

I deleted your link. Here is the real story (it’s helpful to read my stuff on auto inventories):

https://wolfstreet.com/2022/01/21/when-can-we-finally-get-our-glut-back-new-used-vehicle-inventories-rise-but-for-the-wrong-reasons/

What’s going to happen to all those auto loans when used car prices go dow ?

jingle mail? ;-)

The Repo Man Cometh…

When or if used car prices go down?

New car sales December 2021 was down 28% from December 2020. Maybe the worst month, but if the numbers of the rest of 2021 is similar there will be quite a few less used 2020 cars on the market in the future.

If car manufacturers decide to and manage to tailor production to a level where new car prices stay high there may be a if used car prices go down.

That’s a pipe dream, and a failed business model. Everything I read these days is about how there’s this new paradigm where all the bubble prices stay forever. You think house and car prices will just remain at a plateau where the masses can’t afford them? Why would a business owner want fewer customers? Makes no sense.

Capital owner want the largest possible return on their investments. And there is a balance between absolute return, return ratio and risk. Less customer giving a better return ratio with less risk may be preferable. Especially if the car manufacturers can get, buy, a little legislative help.

Have you been to Africa? A lot of countries with a lot of people. Not that many that can afford cars. Do that make cars in the African market cheaper?

The price instantly drops the moment you drive it.

That won’t be a problem, the only question is can people keep paying it.

The hassle of defaulting to “cash in” on a cheaper price won’t be worth it.

A lot of buyers have to buy gap insurance to get financed. This protects the lender incase the resale value is less than theloan.

“consumers borrow more to buy less”. For autos as you point out the cost increase from $30k to $45k is in part due to people buying more expensive models or more expensive packages so technically they are buying “more” as well. Then there is the hedonic adjustments since 2014 as well. There is no doubt that inflation and people paying above MSRP is playing a role but it would be interesting to see what percentage is really inflation vs. people buying nicer cars. If 50% of people who would have bought Civics bought Accords instead, that’s one thing. If Accords are now selling 20% more than before, that’s another. Of course it’s a combination of both.

just read an article on CNBC. It said the Fed may have to raise rates higher to keep wages down. What? They want to keep wages down?

———–

Seven hikes? Fast-rising wages could cause the Fed to raise interest rates even higher this year

Leisure and hospitality, the hardest-hit sector from the pandemic, has seen a 13% earnings gain over the past year. Wages in finance jobs are up 4.8%, while retail trade pay has risen 7.1%.

They didn’t mention reducing asset bubble?

Why would they ever say that to their target audience?

See my comment above about a country using its population to extract the most work for the least outlay.

If there is a labour shortage labour will bargain up their share of their surplus value. If that approaches 100% of their surplus value then capitalists get nothing.

100 jobs, 90 people. Why should I work for you? Ah you’ll give me 75% of my surplus value. This guy says he’ll give me 80%. 85%? okay but no out of hours work, I finish at five.

> they want to keep wages down?

I really don’t understand how this is news to people. Just think back over the past 20 years. The establishment understate inflation on goods/services. The basically excluded house price inflation as they only account for the monthly amount and they moved the definition from main income to “household” income. They have totally ignored price inflation for 20 years.

Wage inflation allows labour to capture most of their value, which allows them to then refuse to work, medium term, as they will escape the tax of rent by paying off their home.

We live in a post-scarcity world. Land is used to force us to work.

So the Fed will stop this by raising rates. This will cut off credit to businesses who will stop hiring and start to lay people off. This will restore the balance to more labour than jobs.

90 jobs, 100 people. Why should I give you this job? I’ll work extra hard! So will this other guy, he says he’ll work until 7pm. You’ll work weekends sometimes? Okay but remember I can replace you any time.

This is the game. If you can’t see that the laws of supply and demand apply to you as much as they do wheat then you are going to have a bad time.

But if they induce a recession won’t that hurt the establishment?

Yes it will, but it will hurt them a lot more than if loads of people pay off their home and are able to refuse to work. You can’t force them back into the factories without breaking the spell that we live in a “free society”.

So the trick is to not get into that mess. They got into it in the 1970s when the boomers had their housing debt deflated. Look at the state of the country now, the boomer age of 1980s to now has seen the USA fall so far.

Great insights, one nit. It was the Greatest and Silents who had their housing debt deflated in 70s. They never had any debt in their lives except the 6% 15 year mortgages they got back in late 60s – early 70s, but as things turned out, were never going to pay them off early when the could get 12% to 15% in money market fund. That’s not going to happen again.

The original No Money Down guy, Robert Allen, was all about buying with seller financing on firsts and/or seconds. That was when bank and S&L mortgages were in the high teens, but price of most houses was still at about 2 to 2.5x annual income, still by a single earner in the household.

Great point, a whole history book in a comment. That describes one big step to greater financialization as the old postwar guardrails on money and credit ceased to function.

The Greatest and Silents maybe got a payoff for being drafted. But I see a big precedent there to my (Boomer) early adult financial life.

There has been widespread social decay since the 1960’s and it’s due to a lot more than just a conspiracy to keep the serfs on the plantation.

The culture is falling apart.

The elites are culpable but the plantation serfs were also willing participants in many ways. For starters, no one forced them to waste their resources (and therefore, life) buying useless baubles. It was a lack of self-discipline and entirely of their own doing.

They could have used these resources to do what you suggest, buy a home and pay it down or off faster.

Both of my hide paying extra ,on mortgage every month ,must have taught them well

Stop saying “elites.”

I assume you use a cell phone. I believe that has been one of the biggest spends by capitalists in the world. You just grew up in a world of stuff provided by the capitalist system that you think are part of nature.

Go to backwoods South America if you want to see a world without the benefits of capitalism. People still picking up milk can deliveries by horseback. It isn’t so nice living without capital investment.

They’re trying to avoid the economic phenomenon known as a “wage-price spiral” which puts inflation on overdrive.

That’s why there raising interest , JPMorgan crying about increased labor costs ,but never mentions cutting executive pay,which will cause civil unrest

Leisure and hospitality, the hardest-hit sector from the pandemic, has seen a 13% earnings gain over the past year. Wages in finance jobs are up 4.8%, while retail trade pay has risen 7.1%.

Ya and they still have less purchasing power due to galloping price inflation.

Was buying dog treats at Trader Joe’s – 3.49 for Charley Bears.

Saw them for 13.99 on e-bay- apparently people are cleaning shelves on stuff ( pharmacy stuff a lot) ….. and then posting them for sale on e-bay etc. for 4 times what they paid.

Thanks Fed. You destroyed a nation. A carny, grifter nation now, full of desperation.

House prices are set by bidding against one another, as demand exceeds supply.

Student loan forgiveness will immediately allow people presently excluded from the home market to bid more than before.

Three points:

1. forgiving student loans will move money from taxpayers to land speculators

2. Former students will not be able to buy “more house” as it will be priced in.

3. Forgiving student loans will be held back as a policy choice until house prices are about to fall. The govt will then “give in” to popular demands to forgive student loans as other house price boosting policies are now as unpopular as they are transparent transfers to the rentier classes. It will fool americans as they don’t understand how prices are set

Interesting theory, but it seems like forgiving student loans carte blanche would be deeply unpopular across a wide swath of the electorate. I think the reason they would forgive the student loans if it was needed for their political base. But I suspect that even the liberal base is split on this issue. So if they do that I predict they lose big in the midterms and beyond.

Every single policy since 2000 has been the answer to the question: how can we keep house prices up without basically saying “yep our entire economy is a complete sham”.

Well student loan forgiveness fits that pattern. It maintains the pattern of an open labour camp through house prices with total enclosure.

Wise rulers would forgive student loans on the reasons Georgist voice. Now, in USA today you may be right that the rulers will not.

No I’m saying just forgiving student loans is a bad idea as it will be transferred to land speculators.

Tax land, then forgive student loans and pay for future education using land taxes, not labour taxes.

Stop encouraging rentier activity by taxing it out of existence.

Stop discouraging real activity by taxing it less (or not at all).

In my opinion, people who get underwater in the magnitude and the paying off of their student loans, and cry for having their loans forgiven, are not the type of people that will be the best candidates for maintaining a budget required to pay off a home, and contribute to the overall economic health of society.

> not the type of people who budget well

Mortgage lending creates credit and forces people to work, creating the credit costs nothing. They want more of this.

“Mortgage lending creates credit and forces people to work”

I must not be understanding because that seems like a strange assertion. The basic thing that forces people to work is to put food on the table, and improve the quality of one’s life, as well as the lives of those one cares for.

People are not forced to have a mortgage, it’s a choice. And if they are in debt from a mortgage, or something else, they are not suddenly forced to work where they were not forced to work before.

Wise rulers never would have had a student loan program or any guaranteed loan programs, at all.

The government shouldn’t be in the student loan business at all. But then, much of higher “education” (the academic drivel they supposedly learn) is actually “adult” day care since many of these people can’t function independently in the world at this age.

In the USA if a $100,000 loan is forgiven, then you will have to pay taxes as if you earned $100,000 unless Congress makes special exception.

In the US a government student loan is on the books as an asset of the US government. Forgiving the loan transfers the cost to the general taxpayer, mostly the upper middle class.

All the comments below this either miss the point or are wrong

> people work for food

Food is far less than rent in most places, and food itself has rent built into it. Half of food is thrown away, we are post scarcity

> Wise rulers never would have had a student loan program

Debt is used for control, so yes they would.

> pay tax on $100k forgiveness

Clearly they wouldn’t make people pay the tax. Even if they did the point still stands for the net amount.

I said wise rulers, I did not mention their motivation nor their interests.

Maybe choosing the word wise was wrong altogether as that implies that the intend behind the actions are good. The word strategic, tactical and expedient may have been better.

With all due respect Augustus, as someone who is paying a good deal of tax as a result of government assistance, loans, and grants seeing me through a rough period and allowing me to pursue higher education that landed me a six figure income job and improve my conditions to the point I’m considering a real estate purchase, I disagree.

But I have always been an exception, it seems. I did look to my left and right and saw many who shouldn’t have been at college, so a qualified disagreement.

Forgiving student loans would be the most unfair move ……

If you recall, the first thing Obama went after was the student loan mechanism. Curious.

What of all the people who…

decided not to go to college because the debt was too high

the families that did without to pay for college

the people who worked two jobs to pay for college

the people who actually paid off their debt

and…

those who could pay but don’t.

Who have parents with two homes, a boat, swanky vacations, etc….and choose to indebt their children with debt they hope will be forgiven some day….by the likes of AOC, etc..

The PROBLEM IS college costs too much for no reason. Learning carries little cost. Dispensing knowledge and facts is a repetitive process ….recorded lectures and teaching assistants getting tuition breaks isnt expensive.

The Dept of Ed budget in 1978 was zero…it is now over $63 BILLION a year. That increase in spending is in exact and direct proportion to the increase in the cost of higher education. Imagine if each state could KEEP $1 Billion A YEAR for their schools. For simplicity of argument, $1 Billion per state (times 50) would still leave $13 Billion for some trimmed back Dept of Education in Washington.

Nice strawmen. How about state funding of higher education? Pull up those charts and see how previous generations got subsidized and then pulled up the ladder behind them

wrong. look at any polling on the issue

I wish someone would come and forgive all my foolish financial choices.

Wish granted.

You are now financially astute. Any other foolish deeds bothering you?

My neighbor

3 20 somethings with student debts

Just put 6 figures into his kitchen

then off to his ski time share

bail out?

votes Dem hoping for bailout

How many out there like that?

Nice of them to share all their financial and personal data with you, though.

Must be a nice neighborhood. Don’t wreck it by spray painting GOP messages on their garage door.

Georgist,

At my current 75 years, I cannot recall an organized debt forgiveness…I live another 75 and I suspect it still would not occur (Debt forgiveness is akin to other Biblical wet dreams).

HOWEVER, consider that if a debt forgiveness incident did occur, that the IRS would then tax those unrealized gains.

Rather stiff the bank, or the IRS?

Don’t answer that Georgist, it’s a disguised patriotism test…he might be NSA.

A decade ago I studied the McKinsey International report – Debt & Deleveraging (2010) – and then the follow-up report entitled Debt & Not Much Deleveraging (2015). Several other updates appeared thereafter.

The 2010 paper had some great long-term (7 decades) charts showing U.S. total systemic debt as % of GDP, including gov’t, corporate, consumer, and financial. So you could see the unhealthy debt growth trend. The alarming thing to me was how a doubling of systemic debt had taken place over those decades.

In 2010 paper there was an implicit assumption that debt levels would revert toward prior averages. As the papers progressed, they stopped using long-term charts and only presented data back to 1990… AS IF the long-term rise no longer mattered. They made the (then) 20 year average from 1990 2015 the focal point.

Our systems (banking, education, housing, federal and muni financing, etc.) are all designed to encourage debt accumulation.

“Neither borrower nor lender be,” indeed!

“Let them eat debt.”

Author and financial leader Raguran Rajan, who read the riot act to assembled global finance grandees at Aspen in ’06 (all the usual suspects, plunge protection team/”committee to save the world,” etc.), and was ostracized for it, coined that phrase in his book “Fault Lines” after the GFC.

Yeah, but debt must hit limits some day. We are testing those limits even as the consumer society dances along its little songs of infantilizing idiocy. But for now, that life of piffle I suppose is better than combat for every sandwich. Unless the one leads to the other. Think 1920s-1940s.

My take is about $8 trillion of government debt has been monetized by Fed and never will be worked off. Was it free money? No. Just deceptive money. US economy prompted up by inflated stock certificates saying company is worth a $ trillion. Might not be worth anything in five years.

Will be rolled off, not worked off.

Nope. They will never roll off more than a $ 1 trillion.

Here is a question for Powell or any Fed Gov or regional President

If a billion seconds is 32 years, how many years is a Trillion seconds?

Answer: 320 Centuries

1) There is a bubble of debt and the Fed job is to delicately decay it in stepping stones and not to shock the nervous market with 5 rates hikes, create an Anti.

2) Student loans : the last dot is a lower high. Debt jubilee up to $40K

will send total debt lower. Many useless woke colleges will shrink or close, because there are not enough students around.

3) Home buying panic is fading away with the vaccines.

4) Ford lost money. Pickup trucks are number #4 in Manheim. EV for $100K with a down payment $200 today.

5) Auto loans and leases at $1.2T – 2/3 of student loans – will fade away with the repo trucks.

I think the Fed should have a “stable prices” mandate and NEVER promote any inflation.

They should NOT have unbridled power to goose the money supply in increments that exceed GDP expansion.

I think the Fed should be kept within the rails, held to mandates and agreements that ALLOW their existence.

I notice the Fed began to SOLVE a problem and they now are identified AS THE PROBLEM.

The Fed don’t issue the money, private banks do.

We have delegated the function of credit creation to private companies who are not democratically accountable.

Make banks intermediaries, distribute credit by setting democratically agreed limits. And tax land / rentier activity.

“The Fed don’t issue the money”

Then you dont understand QE. They bought Treasuries and credited accounts.

Though banks can create by lending, Banks making loans did NOT expand the money supply $4 Trillion in less than two years

the fed issue reserves, not credit money

georgist,

Nope. The “reserves” on the Fed’s books is cash that the banks deposited at the Fed to earn 0.15% interest. These accounts are also used to transfer money between banks, and between the Fed and banks. When the Fed pays the banks for something, such as buying securities, it “credits” the amount to that bank’s reserve account at the Fed, and the bank can then do with this cash whatever it wants to.

The cash is an asset for the banks, and when they put it on deposit at the Fed, they still call it cash on their own books, but the Fed calls it “reserves,” and for the Fed, they’re a liability, namely what the Fed owes the banks.

“Make banks intermediaries, distribute credit by setting democratically agreed limits.”

If this were possible, then the optimal strategy of getting the government out of the “money business” entirely would also be possible.

It’s another type of government economic micro-management.

I can think of a lot reforms in finance. For starters, no central bank monetary policy (at all), no government sponsored moral hazard (FRB “put” and government loan guarantees), and a regulatory framework designed to inform and protect customers and taxpayers instead of everyone else.

What did the Fed use to purchase all those MBS, wampum?

historicus –

Lords of Easy Money briefly mentions an interesting theory regarding why there are such a lack of government mandates to control central banks.

“They [central banks] had become the anchor of economic development as democratic institutions were increasingly mired in dysfunction around the world. The problem with this arrangement was that central banks weren’t built for this job. All they could do was create more money. ‘Somehow, the world was now depending on the one set of institutions—central banks—with one of the narrowest sets of instruments at their disposal given the task at hand,’ El-Erian wrote. ‘And the longer such policy was in play, the greater the probability that the costs and risks would start outweighing the benefits.’

That implies that the root of the problem is dysfunctional democracies (i.e., gridlock, etc.). The central banks filled the vaccuum in needed management of the economy. And a dysfunctional democracy can’t solve the problem, since it is the problem.

It is clear that with each “emergency” the Fed accrues more power.

The problem is that they seem to cause or exacerbate these emergencies.

If the Fed was FORCED to stick to their mandates…..instead of the Fed FORCING investors to take more risk, maybe things would work out better.

After “Lords of Easy Money”, next read is “Unelected Power” by Tucker.

The elected institutions are in gridlock. That is one reason the Fed steps in. The other obvious alternative is outright authoritarianism. It is our failure to function collectively as a democracy that leads down this path. I always look at myself first. We have met the enemy and it is us. Or rather, a species too stupid to manage the complexity it has blundered into.

The Corporate Legal Construct is the current peak of “Unelected Power”, and getting stronger, IMO. It allows the money extraction required to build dynasties, which are also “unelected power”, and also getting stronger.

Phleep’s last sentences are, sadly, true. Fits my Biologist world view, anyway.

And advertising just being “assumed” to be a “business expense” has caused more damage than almost any modern “complexity”.

Really good (if off topic) discussion here.

If by democracy you mean one with a universal franchise, it’s inevitable to be dysfunctional since the typical citizen is a moron who has no business having a say in anyone else’s life.

What people call “democracy” is also implicitly contingent upon a “reasonably” informed electorate acting in “good faith”, not one where competing factions usually if not always working to feed at the public trough at their “neighbor’s” expense.

I have heard that theory. But Fed could have made the democracy work by not giving it free money. A severe recession would have been good for US sometime in last 20 years and that might would have made DC function better with new players.

first of all we’re not a democracy we are a representative republic

secondly we’re supposed to exist in a system of checks and balances but nobody checks the federal reserve.

And to the comment that our elected bodies are in gridlock, that is a good thing! The system is designed so as to have agreement on important issues and gridlock where there is contention.

A perfect example, the infrastructure bill. Only about 15% of it is dedicated to bridges roads and the like. Oh, and the Fed would have to but the bill on the Balance Sheet.

How about just some reasonable degree of friction instead of this absolute gridlock stuff?

Historicus-

There are two big problems with a “stable price mandate”

1. What do you do when prices move different directions – e.g. oil up and auto prices down, or food down and real estate up. What monetary levers do you pull then?

2. Fluctuating prices serve an important function in resource allocation, as Hayek so eloquently explained

Many other disadvantages to stabilization policy could be added. How is this different from price fixing by the Authorities in a command economy?

Well John, they should reword the mandate of “stable prices”.

But I think it is very difficult to defend the promotion of ANY inflation when that mandate is on the books.

If soybeans rise because of a draught, logically that should not bring on a monetary response.

If the price of a used car doubles, that would bring a response IMO.

Fed will be shown to be the fools they are by diverging from empirically based monetary policy to experimental policy when the experiment blows up the economy.

They took off in an experimental airplane hoping they could figure out how to land it. Expect some crazy, crazy stuff as they try to stick the landing.

historicus –

The Fed’s primary directive was the “wealth effect.” The asset boom was supposed to trickle down and boost employment, wages, and everybody.

Investors being “forced” out the risk curve was collateral damage. Investors had the CHOICE to be more conservative, taking a hit, or greedily grasping for higher risk assets.

Why should you give a rat’s arse about the hedge funds and other organizations going out on the high risk curve limb?

Gridlock and cultural war are the main roots of the problem. And if you are part of that, you are part of the problem.

(I will check out the reading you suggested)

I think the youths are being walked out onto the plank of the greater risk curve, along with the hedge funds. If the youths do not see the standard opportunities I saw (or even more, my parents postwar), they do see the grifters who jumped ahead in line. Or so it is claimed on TikTok, a thing I was never exposed to, and never will be. What a cheap, exploitative substitute for fellowship, peer relations and actual life-tested role models. The flow of data there is more noisy than the crude samplings in days of old. And the youths’ subjective time horizons are compressed into silly video clips.

great comment phleep

in my view you hit a home run on that one

The funny part is its narcissism that is being exploited.

We are way past the point that further government spending can grow the pie. In fact further government spending is going to shrink the pie unless real rates get positive. No more real investment without positive returns. No investment means ever declining size of pie to fight over.

“Investors being “forced” out the risk curve was collateral damage.”

It was intentional and admitted by the Fed.

“Why should you give a rat’s arse about the hedge funds”

Did I say I did?

“Gridlock and cultural war ”

If expecting the Fed to obey the mandates/instructions/ and agreements that allow their existence, if expecting the government to be fiscally responsible, and for the Constitution be a guide….then I guess I’m part of the problem you suggest.

“if expecting the government to be fiscally responsible”

Expecting the government to be fiscally responsible has absolutely nothing to do with the Fed.

As I stated before, the primary directive of the Fed was the “wealth effect” (i.e., trickle down theory). You keep dodging that fact and claiming that their primary intention was to force “investors” to take more risks. Fisher acknowledged that forcing more risk was a problematic side effect, not the primary intention.

The wealth effect was the original sin. And yes, if you don’t understand that you are part of the problem.

“Expecting the government to be fiscally responsible has absolutely nothing to do with the Fed.”

Fiscal and monetary policies are closely linked…in fact since QE, the Fed has bankrolled the fiscal end to a great extent.

” Fisher acknowledged that forcing more risk was a problematic side effect, not the primary intention.”

Here is what he said…PBS “The Power of the Federal Reserve”, 8:40 mark of that documetary…

“This is what we thought would happen. When you drive interest rates down all the way out, it FORCES investors into taking bigger steps on the risk spectrum.” Fed Regional President Fisher

You can decide what the original sin was, and you can hold your accusations. I provide proof, his own words, on video.

“this is what we thought would happen” = INTENT

I think our legal system is based on the adversity model where both the defense and the state makes their case and then public jury decides truth. Our two party system is built on the same model I think. Supposed to be the best modern man can come up with.

Whenever I hear “trickle down” I think of a Calvin peeing sticker on a tinted truck window.

VA has a 4.15% sales tax on autos for example. An average increase in sales price from $34K to $46K increases the tax by $500 or 500/1400 = 36%.

Not a bad take, if a little over the official inflation rate.

This compounding of taxes occurs across the board and I don’t see it being analyzed by anyone.

One key to Warren Buffet’s success is you always have to consider the drag of taxes when figuring the cost of a transaction. Most people don’t.

I enjoy following the thread of conversations on Wolf’s post. In this particular case, the discussion about car prices left the room and it wandered elsewhere…

:)

Cars are tools — they’re means to an end. They’re not an asset. Buy used, buy cheap, avoid brand status and loyalties, and learn to fix them yourself. At the very least, oil and filter changes. Anymore tools are cheap and maintenance has never been easier. They’re very mechanic friendly. And the money saved is very satisfying.

Just my thoughts.

Even as cheap as I am, I will not do oil changes anymore on my car.

Scooter is different story. Can do it in five minutes without crawling under car. No filter. Drain out 2/3 quart. Put in 2/3 quart. You are good to go.

I enjoy your descriptions of rambling around on the 50. Made me remember of my stoner days. I wasn’t a motorcycle person, but one time an Irish-American pal showed up when I was high, and gave me a ride on a Honda 50. Whoa boy, he started pulling wheelies and scared the shite out of me. I clung on for dear life and was thankful I survived the ordeal.

Sad that the the guy eventually committed suicide by crawling out on a freeway drunk. His father would beat the crap out of him regularly, I’m not sure why. And the nuns at his Catholic school told him he was an embodiment of the devil.

Terrible situation ,very sad story

Killed by soul sucking nun induced ennui. Happens all the time.

Drifterprof

I am wondering what that makes me … raced Yamaha TZ 350’s and TZ 750’s for 6 years in the 1970’s. 218 mph at Daytona … just rubbed my head … no horns … at least yet.

Been riding everyday even down to 28 degrees F.

Bad childhoods are tough to get over. Best thing you can do is give a child a happy childhood

Just watched Audrey Hepburn documentary where she had bad childhood partly due to lousy father and part due to WWII. She never got over it.

Made her a good actress. The Nuns Story and Breakfast at Tiffany’s are two of her best

So beautiful on screen, but couldn’t conquer her childhood nightmare in personal life.

The new car price increases over the past few years are jaw dropping indeed just like home price gains. This scenario truly points to a FED run amuck and without an regard to moral hazard. A 5th grader could have done a better job.

Ford announced more vehicle production cuts at North American assembly plants due to chip shortages.

A local restaurant started adding a 17% gratuity fee to the dinner tab after waitresses walked off the job due to low tips.

Price is where the action is. We all have to make it tens of times a day. Sometimes you have to walk. Price makes us choose. Choose poorly you usually end up in a bad place.

Your seasonally adjusted chart is another reason why I don’t believe any data coming out as official data. The new new math is total crap.

For those of you who are math challenged, the purple line should be under the red peaks, in the seasonally adjusted chart. It should be a smoothing of the peaks over the time frame.

Oh hm, good eye Petunia…

Paging Wolf Richter…

Good observation – the seasonally adjusted is basically a straight line connecting the annual peaks.

Look especially at 2016.

Look at 2008-9, the adjusted numbers are higher than the real max.

Petunia,

Yes, that’s why you got the red line so you can see what’s going on and how it works.

As I pointed out in the article:

“…because December is the month when seasonal adjustments get pegged to not-seasonally adjusted data, as you can see in the chart below. In the not-seasonally adjusted data (red), the peaks are in December. The seasonally adjusted data (purple) rides on top of all the Decembers”

Unfortunately, some data are so horribly seasonal — such as retail sales — that not seasonally adjusted data can be very hard to deal with on a month-to-month basis.

Nevertheless, in my retail articles there are usually one or two charts with NSA and SA data overlaid, particularly ecommerce sales where I believe the seasonal adjustments are particularly misleading.

The truth is shown in year over year non adjusted data that can’t be fudged like total retail sales or tax revenues.

Hey, look, we flattened the curve on used car CPI index! Well done, folks.

Mind boggling.

So, what happens if you are in an accident that’s not your fault, hit by an uninsured driver, or one with great insurance, or anything in between, your car is totaled.

Does your or their insurance cover the ever escalating cost of a replacement used vehicle, or a rental until one cannot be found?

My policy does not answer that question as to escalating replacement vehicle costs.

Tony22, that would depend on what type of insurance you have. If you have full / comprehensive insurance, your insurance company “should” compensate you for your vehicle at its current fair market value. Of course if it is determined that you are not at fault.

If you have liability only, then you are SOL…

If your vehicle is 3 years old and has 50,000 miles on it when it is totaled, the insurance may offer you a settlement equal to the price of an equivalent 3-year model with 50,000 miles on it.

These settlement offers are negotiable.

If the other driver is at fault, you or your insurance company may have to sue the driver and their insurance company to get a settlement. Insurance companies are litigation machines.

2weeks ago I visited Honda & Toyota in Duluth ga ( metro atlanta), dealership for new vehicles. Both did not have any new vehicle in the stock; for Honda only available was pilot base start from $40k+tax & fees.

Took the quote for 2022 crv exl gasoline non awd base price $33k + fees & tax came to $42k. Asked for Hrv small suv base model $24k + all the fees & tax . No discount no change in the fees. And you have to pre order. Some stock was coming in by 14th feb for some Hrv’s. Crv’s pre booked almost 100 people before me. That’s what Salesrep showed me sheet with customer name and estimate delivery dates goes mid March to April.They did not ask anything above msrp but unwanted additional items you have to pay one cannot remove it almost 2k and even though their website says doc fees included in msrp it is still added in the fees. When pointed out he said it only for in stock vehicles. His manager acknowledged that lot of dealerships are charging more money above msrp as addendum we are not doing it coz larger dealerships network.

Went to Toyota dealership nearby had same experience answers nothing in the stock pre order wait 1 to 2 months. Only readily available was highlander & 4runner. Asked quotes for

RAV4 xle premium gasoline

Msrp $34k + $4k addendum (premium)+ tax & fees.

Corolla le base msrp $22k + $3k premium + tax & fees.

Compare to last year or before this mania started

Crv exl or rav4 xle premium was less than $30k including taxes & fees now it is $10k to $15k more. Wondering where the luxury vehicle prices will be if the non luxury vehicle are selling at these high prices?

The 10yr is at 1.96% . Oil is consolidating around 90 fixing next leg up. I feel like the oiler down in the engine room watching the bearings fail while the captain is focused on glory.

Full speed ahead is the call from the bridge.

It’s a very difficult time to know what is what until major stimulus gets through the system. Money supply dropping from really high 20% y/y rate to 10% and where it stops nobody knows. Long term average is 6 – 7%.

Old School, which money supply measures are you looking at?

Dude. Am I high?

“On a seasonally adjusted basis, revolving credit balances rose to $1.04 billion .”

I think you mean Trillion. But what the hell is a couple of zeros between friends?

As an aside posting the average loan per imbecile, not the aggregate, gives better insight into the stupidity of those who can’t delay gratification.

The power of FOMO for those of weak mental fortitude.

The student loan situation: any debt forgiveness doesn’t have to be a discreet amount, nor does it have to start and stop at any particular point in the total owed per borrower. Just have to make it palatable to enough voters. At a politically fortuitous time, like late summer 2022, the administration could say that every loan will be adjusted to remove the bottom $5000 of debt and balances exceeding a $100k base would be multiplied by a fractional amount to reflect a new lower total owed. Just numbers thrown up in the air, overpaid admin eco-trolls would do the bogus figuring. Means-testing will be there for congressional show and tell. Scheduling out the consequences of our past indiscretions far into the Glorious Future has always been popular. Rescheduling student loan debt is individually appealing and relatively inoffensive on an agregate basis. This is about the optics of a putatively “necessary” move. Also a bribe to come back to work, disguised as govt largesse? The Eye of FedLoan knows and sees all. it’s somewhat easier to stomach a governmental screwing if the screwee sees everybody else walking funny too.

Car loans: for new at seventy+two months is pretty bad, but sixty-six months for a used car is unsustainable. Some may last longer, but the owners won’t. They want a new car in the driveway while there’s years left on the old one. My ’07 e-250 and the Japan-built tacoma don’t need OEM diagnostic gear to fix, the newest vehicles are slaves to proprietary software requiring revision upgrades like every software product since before MS-DOS. CANBUS is going to be really troublesome down the road, so to speak. Automotive electrical connectors are extremely well engineered today, but it’s to a price point and it’s still an vibration-prone electrical connection, and some will inevitably leak and allow corrosion to penetrate the mating surfaces of the connection and cause a voltage drop across the connection, and a fault condition. If it was some electrical device operating at 12vdc, pretty easy to troubleshoot. Board-level voltages can be much less, and may require a dedicated simulator to diagnose a fault. And someone to operate it, who doesn’t really exist in significant numbers yet in car repair, more expense. if your half-paid-for car is waiting to be serviced often you won’t be happy about it. Thousands of new immobile, chipless cars sitting in the weather right now waiting on a CARE package from Intel may be troublesome for the owners later, it’s not plug and play. Add a note stretching five or more years….pay cash for cars.if possible. These days to come will be evil for those who carry debt. Debt is very narrowly a moral process.most humans and all governments lack the moral infrastructure and self-control to use debt correctly. Appropriately, the german for debt and guilt are derived from the same root word. It would benefit society if imaginatively serviced debt was once again a source of guilt, and not tolerated to excess or without rock-solid financial servicing. And lots of people would have to learn how to work for their keep, rather than sponging off of others.