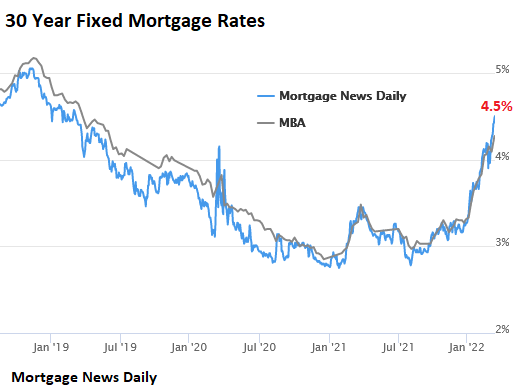

But it doesn’t yet reflect the recent spike in mortgage rates to 4.5%.

By Wolf Richter for WOLF STREET.

OK, the “existing home sales” data released today by the National Association of Realtors was for February, and in February the average mortgage rates were a lot lower than today. In mid-February, the average conforming 30-year fixed mortgage rate had just edged over 4% for the first time since 2019, according to the Mortgage Bankers Association’s weekly index.

According to the daily measure by Mortgage News Daily, the average 30-year fixed rate mortgage hit 4.50% yesterday, the highest since March 2019. Since last fall, the average rate has jumped by 1.5 percentage points, from 3% to 4.5% (chart via Mortgage News Daily):

In its report for November, the National Association of Realtors expected the average 30-year mortgage rate to reach 3.70% by the end of 2022. Now it’s only March 2022, and we’re at 4.5% already. This is moving fast. Last month, I speculated that 4% might be the magic number beyond which the housing market is going to feel it.

It’s not a secret: As mortgage rates rise, more and more buyers are priced out at these sky-high prices, and they step away from the market.

But among buyers who still qualify, rising mortgage rates trigger a mad scramble to buy something “now,” no matter what the price and no questions asked, and they’re waving inspections and are taking huge risks – even NPR aired something like a warning about that yesterday, LOL – to lock in whatever mortgage rates are still available before they rise even further.

There is a well-established pattern: Sales activity picks up in the early phases of the cycle of rising mortgage rates, and we saw some of that, but it’s getting impossible for an increasing number of potential home buyers.

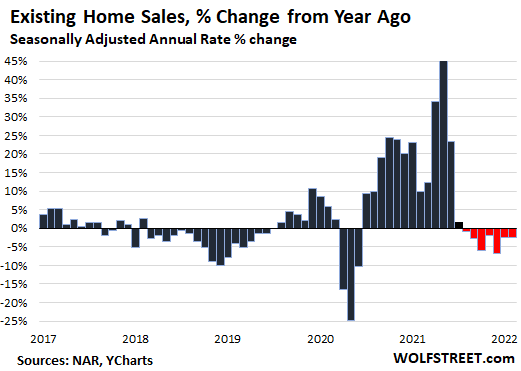

Sales of previously owned houses, condos, and co-ops in February fell by 7.2% in February from January, and by 2.2% year-over-year, to a seasonally adjusted annual rate of 6.02 million homes, the seventh month in a row of year-over-year declines (historic data via YCharts):

“Housing affordability continues to be a major challenge, as buyers are getting a double whammy: rising mortgage rates and sustained price increases,” the NAR said in the press release. It pointed out that monthly payments had risen by 28% from a year ago. “Some who had previously qualified at a 3% mortgage rate are no longer able to buy at the 4% rate,” the report said.

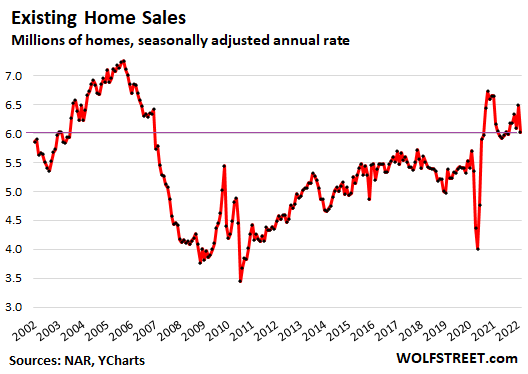

Home sales peaked in the 2003-2006 era. The current era remains solidly below that peak. The seasonally adjusted annual rate of 6.02 million sales in February was also well below the pandemic peak, but was up from the prior years.

Sales of single-family houses dropped 7.0% for the month and 2.2% year-over-year, to a seasonally adjusted annual rate of 5.35 million houses.

Sales of condos plunged by 9.5% for the month and by 4.3% year-over-year to a seasonally adjusted annual rate of 670,000 condos.

By Region, the percent change of the seasonally adjusted annual rate of total home sales in February from January, and year-over-year (yoy):

- Northeast: -11.5% from January, -12.7% yoy.

- Midwest: -11.3% from January, -1.5% yoy.

- South: -5.1% from January, +3.0% yoy.

- West: -4.7% from January, -8.3% yoy.

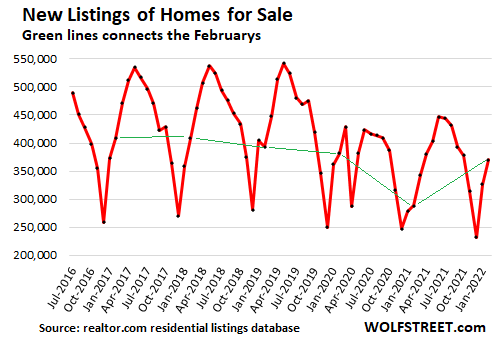

Here come the new listings. The number of homes listed for sale in February jumped by 13.4% year-over-year, after the 13.2% jump in January, and were down only 3.0% from February 2020.

New listings come out of the woodwork when interest rates rise and volume stalls — because it’s now suddenly time to put the extra house on the market before the market turns. In February, new listings essentially rose back to the normal range for a February, after having been woefully low during the past two years. The green lines connect the Februarys (source: realtor.com residential listings database):

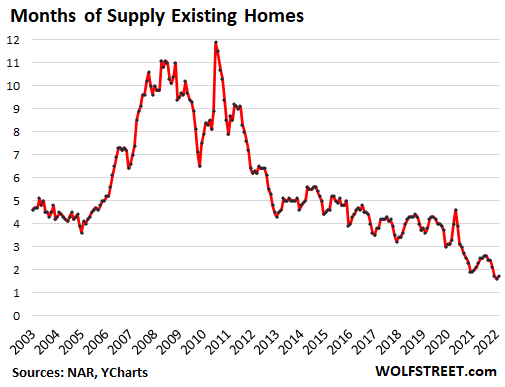

Supply of homes listed for sale ticked up from the record low in January to 1.7 months of sales. The number of unsold homes on the market rose 2.4% from record lows in January to 870,000, seasonally adjusted.

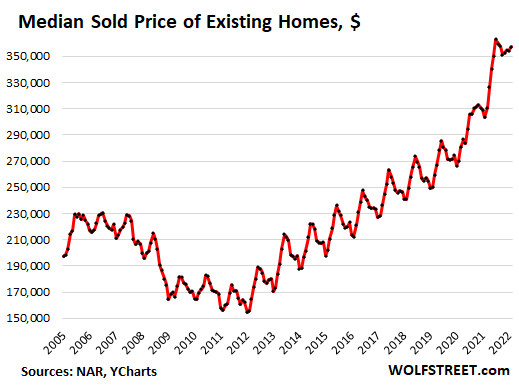

The median price ticked up from January and was up 15% from a year ago, to $357,300. The year-over-year spikes had peaked last May and June at over 23%. The seasonal peak in the median price was in July 2021 at $362,800:

Investor share of sales remains about level. “Individual investors or second-home buyers, who make up many cash sales,” accounted for 19% of the transactions in February, down from 22% in January but up from 17% in February 2021. “All-cash” sales remained in the same range, accounting for 25% of the transactions in February, down from 27% in January but up from 22% in February 2021.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“…rising mortgage rates trigger a mad scramble to buy something “now,” no matter what the price”

A broker I know confirms that has been the sentiment here in SD, accelerating over the last few weeks. Yup.

DC has created an utterly phony interest rate environment for 20 years…and by this point most people know it.

Boom/bust 1.0 relied upon the suckers – those ignorant of DC’s manipulations.

Boom/bust 2.0 is relying upon the hyper-speculating psychopaths (they know the game for what it is)…thus the rush for the door…they know their “wealth” is wholly contingent upon DC’s increasingly runny empire of bullsh*t (interest rate division).

A 0.25% higher rate with postponed QT will cause house prices to inflate further.

When inflation is at 8%, the 4.5% mortgage gives you a 3.5% return over cash, even when house prices don’t go up. However, 30 year treasuries pay only 2.7%, and house prices are jumping by 20% a year, REITs got a 17.4% return over treasuries. So, no big investor will stop buying housing.

Also, there is both a Fed put and a Govt put on house prices, so they never go down and should keep going up. In essence, US is all in on Housing, and housing markets can only correct when whole US is going bankrupt, not because of dollar debt that we can print, but because we no longer manufacture stuff and may not have anything to offer in lieu of our imports.

Great, with a Fed and Gov put on housing we’re on the same path as China.

We need forced sales. If the Fed triggers a deep enough recession that will happen.

@Raj and @makruger Exactly. And I think that is where we are headed. The only strike against that outcome is that there are no annual taxes for real estate in China, so taxes put a drag on purchases in the U.S. Also, for me, the fact that the Fed is not even pretending they want Prime rate above CPI highlights the govt wants to inflate the property market similar to China.

Remarkable that people believe 8% seems okay but dont dare raise rates a couple of % pts..

INFLATION will cause a recession. People will stop going out to eat in order to fill up their gas tanks. People will stop driving trips.

Hotels/Motels will suffer. Restaurants too. We are a service economy reliant on mobility.

2 or 3% short rates will not damage the economy as much as people think….IT WILL hurt stock and real estate, but they have had a free lunch for 12 years and the job of the Fed is not to defend spiked asset prices….or is it?

exactly

I need to SPEND MY WORTHLESS fiat $dollars before I lose anothe 30% of value

mortgage??? don’t have one called cash

Inflation is probably really 7.5% to 12% per year, so even a mortgage at 7% per year means that they are gifting you .5% to 5% per year. So in areas with reasonable property taxes, since the banksters’ “Federal” Reserve clearly is only going to pretend to try to slow down inflation, any asset that can keep its value against inflation is better than cash or bonds or CDs with their puny returns. I heard advertising about adjustable rate mortgages, now those would be crazy to get.

so i see that a lot, and a 30 year fixed at 7% per year is only a “gift” if inflation *stays* at 7.5%-12% per year. if that does happen, the us dollar is doomed.

The US dollar is probably doomed as a reserve currency in coming years albeit not for a while because our allies have now realized that the US is the only viable opponent to China and Russia, so they may keep it up for a while. The “Federal” Reserve will not raise interest rates enough to tame inflation like Volcker did.

this is the stupid lemmings running off the cliff. there is a simple reason they run to buy a home – because they think the prices will keep going up. if you told those buyers that they would be sitting on a 10-15-20% price decline over the next 5 years they would run away from that purchase.

but people are greedy.

the problem with the idea of locking in a low interest rate on a home purchase during a speculative bubble is that interest rates have not stopped moving up. and demand for homes will eventually be hit by a lack of buyers who can afford the monthly payment.

once the market finally hits that inversion point and prices start to fall, the supply will finally hit the market – at the wrong time and will drive a stake in home prices.

i see 50% declines in many overpriced markets like southern california.

i was predicting 5% interest rates by May in January and people called me crazy. we might get to 6% by the end of May.

I’m betting months supply heads lower from here for the rest of the year as CPI inflation continues to increase for at least six more months. The only thing that would change my bet is several 0.5% rate hikes in a row.

JeffD,

So just another thought here:

For home buyers struggling to qualify for a mortgage, it doesn’t matter if “real” mortgage rates are negative (below CPI).

If they cannot qualify for a mortgage because they don’t have enough income to cover the mortgage payment, now that the rate is 4.5%, that’s it… they’re not buying. Those buyers are gone from the market. It doesn’t matter what CPI is.

The number of potential home buyers that disappear from the market increases with rising mortgage rates and rising home prices. At some point, the market stalls (volume slows), and price discovery starts.

In fact, big inflation leaves less money for mortgage payments.

to add on that, the “all cash investors,” many of whom are actually leveraged, just not with a traditional mortgage, will bail the moment they see things slowing down. the investors don’t have to dump what they have bought in the past 18 months. they just have to merely stop buying new stuff, and the buying pressure is gone. and i think that’s a distinct possibility when you consider that the people you described being gone from the market will put downward pressure on prices for everyone.

After Fed’s demonstrated apathy to inflation, stock markets are roaring again.

Why should it ne different for Housing? “To infinity and Beyond…”

I agree. We have not only stopped buying, but have reduced some property that we considered to be much more than fully valued (values up over 50% in the past 2 years). We are not alone, many other large real estate investors we know have been selling for the past 18 months and we are all sitting in heavy cash positions waiting for better opportunities over the next 2-3 years. Will our cash take a hit from inflation while we wait – yes – but we feel we will more than make up for it with better buying opportunities in the next few years.

The 10-year treasury note is often cited as an important reading for the market partially due to its function associated with variable rate equity lines If that gets up around 4% it could be a hurting point It was for me until I refinanced 6 months ago and consolidated the mortgage and equity line.

10 Year Treasury Rate is at 2.14%, compared to 2.20% the previous market day and 1.71% last year. This is lower than the long term average of 4.29%.

USDA home loans have a very low bar, similar to “are you breathing?” I just typed fictitious numbers into their eligibility quiz with an approval. You would be surprised where USDA home loans apply.

Example: 47 charlottes way, muir beach is an eligible property under USDA loan guidelines.

Whoops. Showed as eligible in their tool, but violated loan cap:

Properties financed with direct loan funds must:

* Generally be 2,000 square feet or less

*Not have market value in excess of the applicable area loan limit

*Not be designed for income producing activities

For instance, anywhere in Scotts Valley is eligible that meets these requirement.

1.5% on a $300,000 mortgage is about $250 more per month.

Not sure how much the cost of financing has gone up for institutional buyers if it’s comparable, there is a limit to how much of it can be passed to the renter.

About a 20% increase in the monthly payment.

You also need to factor in the price increase as well. Those 300k crap shack is now “worth” 350K – 400K on paper.

But for investors, the CPI specifically rent CPI is an important factor because it represents the growth rate for the gross income they expect to accrue from their investment.

So even if the market stalls and capital appreciation slows, the income growth potential relative to the cost of capital (mortgage rate) may make housing an attractive investment.

i don’t know where these investors think the money is going to come from. in many places, rents have gone up 20-30% this year. anecdotally, it seems that renters are tapped out.

Jake.

I’ve wondered the same thing myself. I live in a 2BR where the rent is about $2000 which is supposed to be about average in metro ATL but I’m in much better than average location and the complex was built in 2019.

2BR units range up to $3800, depending upon location in the complex. 3BR of which there are a few I think range up to $5000.

Last I checked, the vacancy rate was something like 1%.

I’m sure many people said it was “impossible” for paycheck-to-paycheck renters to pay an additional 20-30% per month, and yet somehow they are paying it, right?

“Last I checked, the vacancy rate was something like 1%.

Not bad for an economy that has been “gutted”.

Unamused,

1% vacancy because insufficient apartments built for 7 years (reaction from Bust 1.0 blast crater).

And people have to live *somewhere* (but the longer they get rent raped, the more tolerable having a roommate seems).

And when people start doubling up, what happens to occupancy?

jeffd, most people are not paying 20-30% more. that was the average increase for asking rents, but renewals didn’t pay anywhere near that, in my anecdotal experience.

as always, prices are set on the margins.

people will start to move away from expensive areas and that will also destroy the demand in those areas.

we are sitting on a bubble still, the bursting has barely begun. watch for real pain in the real estate market in the near future.

i say that as homes come on the market in May, June, July, they start to cut prices to sell and that starts the downtrend, but the bigger downtrend happens in the Fall.

“In fact, big inflation leaves less money for mortgage payments.”

Salient point there… Rising mtg rates *coupled* with inflation is *double trouble*.

Exactly!

“In its report for November, the National Association of Realtors expected the average 30-year mortgage rate to reach 3.70% by the end of 2022.”

I would never put any stock in anything NAR has to say. NEVER.

Most likely, the magic number is about 4.5%, and I agree that certain groups of buyers will start to disappear from the market. Also, listing prices in the next 3-6 months will start to pull back a little for those final sellers that become desperate.

Since mortgage closings lag rate changes, the sales numbers will continue to deteriorate from here on out and will accelerate once rates hit 5%. If rates hit 5.25%, then the housing market will begin a 10% rollover which the FED is fine with.

What they don’t want to see is a 15% or more pullback. We’ll know by late this year if a greater than 10% pullback is in the cards.

If that’s true, it’s insane. 15% wouldn’t even unwind the last year’s price spike.

Lawrence Yun is the Baghdad Bob of real estate.

Another way inflation plays into this is that homebuyers won’t mind stretching themselves early on because the payments will stay fixed while their incomes soar at or ahead of inflation place and so will become much less of a burden over time.

Lenders might start to lend based on what the borrower will be earning next year which might make it easier to qualify. That’s part of the heightened inflation expectations we hear so much about.

While I agree with your premise to a point, it is also important to remember that in most places, overall inflation is taking a bite out of most, if not all, wage gains. Additionally, the one thing that none of us have control over are property taxes – and in urban TX you can expect these to go up the maximum allowed each year.

“ Additionally, the one thing that none of us have control over are property taxes

HB69,

Correct… you have to allow for that in your calculations if you’re buying the house to live in…

In protected tax states like Florida, the payment you had in year one was based on current tax rates and probably tax protected… in year two, it reset to prevailing values because of the property sale…

Add in some insurance increases, and your house payment can increase 20% before you blink…

If you were even close to marginal going in, with inflation, you can be hurting very soon…

Wolf. At what point do we start seeing NINJA loans again……and wouldn’t those contribute to even higher home prices ?

We were offered a NINJA loan by house builder a year ago. They had 49 houses sold in a subdivision around that time and 35 of them where closed with NINJA loans.

Beating a dead horse:

USDA loans are available to home buyers with low–to–average income. They offer financing with no down payment, reduced mortgage insurance, and below–market mortgage rates.

Not quite NNJA yet, but I expect that by year end.

Gabby Cat, what area was this?

But But But the real big question is price discovery starts for whom?

AND how does price discovery continue for certain proprietary and really proprietary AI’s for whom, and where?

Correct. Nominal rates matter, not just real rates. You have to be able to come up with the payments.

This is even true for corporations and governments. Real rates may be negative, but if interest payments are higher than revenues you could get into trouble.

Don’t forget this last booster in the arm for the market:

“A significant number of U.S. consumers will have their medical collection debt dropped from their credit report, the nation’s biggest credit reporting bureaus announced Friday.”

Thomas,

Nah, that’s not changing anything. Medical debts have been discounted for decades by lenders. So you had a low FICO score, but you had a $500k hospital bill that you couldn’t pay, but everything else is top notch and on time — all this data is in the detailed credit report — the lender just said, OK, that’s a medial default, and then went ahead and made the loan.

The credit bureaus are just doing what has been de facto reality already.

Credit scores and credit reporting aren’t punitive measures. They’re designed to predict future credit performance by that individual. And that’s why it makes sense to ignore medial debts if everything else it top notch.

It comes down to affordability. House prices in large part are based on the mortgagee paying no more than 38% of household income on housing costs (mortgage, property tax, property insurance and HOA fee). I state 38% because that is what I remember the bank telling me in regards to a VA mortgage.

I recall also the house price to household income ratio being between 4.5 to 5.5 for low interest rates (less than 4% rate for 30 year mortgage).

Wolf,

Instead, the cash buyers and wealthier middle class will buy multiple houses and rent them out. A strong substitute.

I remember buying a house in 1982 with an interest rate of 14% +1/2 for PMI. Duh ! The beauty of youth is not explainable.

Off topic, maybe, but relevent in the sense that it may provide perspective. Anyway, I overheard two OG’s discussing a mutual acquaintance this morning.

The first OG remarked that so and so recently turned 98.

The second OG remarked that apparently, even Hell didn’t want him.

Our world is dominated by the same crowd that has been making horrible decisions for the last 65 years, and now their going to fix it.

Well, the naked humanity of it takes my breathe away, and makes me want to continue believing that it’s normal.

Buy now or be priced out forever!!! I have tamed inflation with my .25 rate hike!!! The market will never go down!!! Just double your money on Bitcoin!!!! Buy now and then the house you dream of will be half price next year coz Bitcoin will quadruple and houses will double!!!! I have create the greatest economy known to man!!! Can never go down!!!

The first WHIFF of falling house prices will spook everyone into listing all at once. This is what happened in 2009. Homeowners watch thier values like a hawk. They all want to sell at the very top. The media amplifies any lower prices into a stampede to get out.

More listings at first stops the bidding wars. Later on it creates a buyers market which lowers prices even more.

If mortgage rates go up a percent or two, that is what will happen. Buyers qualify for lower loans, which means lower bids.

“Homeowners watch thier values like a hawk. They all want to sell at the very top.”

Those are speculators, not homeowners. Homeowners use their houses for shelter from the storm.

Don’t forget that many homeowners locked ino a 30 yr fixed at 3%. That means affordable payments well into the future.

If you sell your current house good luck on buying a other house at that rate.

I can see lot of people staying put.

Being able to borrow against equity to tide over a short term income loss will also help.

Then there is the shortage of housing and the huge numbers of buyers.

I don’t see any big or long term collapse in housing prices. If there is a hint of that the FED will bail everyone out again.

What the heck, it is just printed money.

We will see.

Inventory is far lower compared to 2018 and real mortgage rates are still negative.

I hope I’m wrong, but it’s probably going to take higher rates than 4.5% to see a 2018-like slow down in the RE market.

To be clear, Wolf states average rates at 4.5% which means half are lower and half are higher.

In my area, several Credit unions are still closer to 3.5 than 4.5.

The one I watch just raised 30 year fixed to 3.675.

Not 2.875 like I saw before but not that much higher either.

Data set: 13, 18, 13, 14, 13, 16, 14, 21, 13

Average (mean): Add up all the values and divide by the number of data points. Average is 15.

Median: the midpoint of the data set. Order the data points by value and pick the middle value.

13 13, 13, 13, 14, 14, 16, 18, 21 -> 14

Median is often used because mean (average) is sensitive to outliers.

Replace 21 with 100. 13 13, 13, 13, 14, 14, 16, 18, 100.

Mean is now almost 24.

Median is still 14.

That 3.675 probably includes points and I don’t think the national average includes those.

Today it went to 3.70 but no points. Still historically low and a bargain looking back a year from now.

People don’t buy a house (car), they buy a payment. They only have so much per month. And when rates go from 3% to 4.5% that’s a lot less price they can put into a payment. (also as insurance goes crazy because of insurance) and property tax because of valuations………….. Again, lot less house for the same payment.

Housing prices are sticky. Takes a long time to go down. When the time on market (can you get that nationally?) really starts to jump up, then you’ll know ti’s really starting to bust.

“People don’t buy a house (car), they buy a payment”

Not me, never. But people do and I think they are foolish for that path.

Nobody ever even looks at the total interest paid over the course of 30 years.

Interest over 30 years on 1 million borrowed increases overt 200K from 3% to 4%. If anyone looked at that we would already be in a slowdown.

“Nobody ever even looks at the total interest paid …”

For many buyers, I think that you’re spot on. Afterall, interest payments are a tax deduction. Right? Ask the realtor — that’s a selling point.

:)

People don’t think about the fact that paying cash for a home results in buying the home for tens, often hundreds of thousands of dollars less than the financed option. Well, the ones that pay cash do. People don’t understand the costs of interest over the life of the loan, even if you pay off early. In this sense they do buy monthly payments without considering the actual cost.

Accumulated interest adds enormous amounts to the cost of the home. Deductions are of course nice but they are not reducing the amortized amount of the loan.

Yes, but the money you are using for your house payment in 10-20-30 years in the future is worth far less than money today.

If your paycheck keeps up with inflation and inflation runs at 10% for a few years, you house payment, relative to your income, is going to get smaller and smaller.

Not uncommon for people who have held on to their house for decades to see the property tax portion of your payment exceed the principle and interest portion.

Enough inflation and the principal and interest will sink to near zero.

Not sure why “nobody ever even looks at the total interest paid” since I look at the amortization schedule for my loan nearly every time I log on to the mortgage account online.

I like to see the breakdown of interest and principal being paid over time. It also summarizes the total interest paid for the remainder of the schedule.

Maybe other mortgage service companies don’t offer this?

if i recall correctly, they’re required by law to offer it. but most people don’t bother to read the details.

“People don’t buy a house (car), they buy a payment”

Some people actually do “buy a house”. They do that by writing a check. Others just change landlords and now they rent from the bank.

Until the day you pay it off, it ain’t your house. It’s the bank’s house.

Even when house, anywhere in USA, is without mortgage, ya still just renting it from the local taxing authorities H.

If you don’t pay your taxes, they WILL and DO all the time TAKE your house.

Surely, you can put it off, sometimes in some states for the rest of your life if elderly,,, BUT,,,

Sooner and later, they WILL take your house.

Vintage,

I agree, especially in states that allow ‘owners’ to walk away without penalty. These are the houses that some investors pounce on. I know a guy that almost exclusively buys these as fixer-uppers. The house is trashed, the former ‘owners’ have walked away, and the bank sells it — often at a loss. He buys them, polishes them up, and then resells.

He used to be a plumber, but makes more doing this than fixing leaky pipes.

Housing is a trap.

Why? Because this is where most wealth is located. With $30T government debt and $45T unfunded liabilities (which cannot be “inflated away”), housing is where they are going to get it. There is simply no other source!

The cool thing (for government) is that a house cannot be moved. It it captive capital. First they will milk it with taxes, but I fully expect that reverse mortgages will become a big thing when gov defaults on their unfunded liabilities and people will be forced to eat their house first.

AMEN!

I’d also go as far as saying you only rent your freedom from the government.

yushan, excellent point that others including augustus have been trying to make for a while. most of what we consider “wealth” isn’t. shares in facebook won’t be worth anything if the bubble economy around us collapses. who will be paying for all of the advertising then?

there’s a reason that russia matters. it’s not because of its gdp, which includes bubble wealth and other non-productive activities, but because russia controls a huge swath of the earth’s land. that’s what wealth is.

“Until the day you pay it off, it ain’t your house. It’s the bank’s house.”

All too true.

People have been sold on the idea that buying a house constitutes an ‘investment’, when for most people it should be treated as an expense. The important thing is that the ‘homeowner’, so called, is accumulating equity for oneself, and not for a landlord.

Rule #1 in Personal Finance: live below your means. With high inflation that becomes increasingly difficult for a large fraction of the population to do, even while being tenaciously frugal, even though such persons are routinely castigated for profligacy by the predator class.

The added bonus is that, as a “homeowner”, you (for the most part) are able to keep your costs of housing somewhat stable.

This makes it much easier for you to budget…. Sure, stuff breaks or wears out. However, that can also be budgeted for (rainy day fund) and reduce the impact of any unexpected “shocks” to your living expenses.

We do something that’s thought to be weird by some people and that is we pay ourselves a “mortgage payment” every month – even though we own this barn outright. We discovered this ploy back in the 1980’s when we owned our first paid off house. We put aside over $900 a month (in 1985 money) by being our own bank as that was our monthly payment up until the time we paid it off… we just continued to pay our “mortgage” but the recipient wasn’t the mortgage company, it was us. To this day, when we make an improvement or repair, we also “finance” it ourselves and make the payment to… ourselves.

I know it sounds stupid, but it works for us…. it just takes a little discipline.

“I know it sounds stupid, but it works for us”

It’s not stupid, El Katz. Give yourself some credit for coming up with something that works for you.

It’s a tale of two worlds. Half the people spend based on monthly payments, and their buying will decrease with higher interest rates. The other half cares more about making good investment decisions. They will buy less because the other group is buying less.

I wouldn’t be putting expected home price increases in my buy/sell decision or my rent v. buy decision at this time, when mortgage rates are rising and the Fed is about to start quantitative tightening.

If you are a buyer, it makes sense to wait another year to see if the markets tank. You likely have nothing to lose, because the clear trend of falling housing transactions in place, housing prices likely aren’t going up over the next year.

that’s my feeling. even if prices don’t go down, i don’t see them continuing to go up, not unless the fed restarts qe.

but you’re so right about the tale of two worlds. whenever i’ve walked into a car dealership, the idiot sales people always start with “how much are you looking to pay per month?” they can’t wrap their heads around the idea that i’m interested in the price (whether or not I choose to finance it), and not the monthly payment.

Then there’s the “Four Square” used in car sales……

Look it up. It’s pretty clever how you can get sucked in.

El Katz,

Hahahaha, yes, the four-square is a theme in my book about the “Ford Superstore” (which is in the humor category).

On the Amazon page, click on the book cover to open the book, and you can read the first few chapters for free.

To buy: The book is free for Amazon Prime members, and $2.99 for everyone else (Kindle). I know, great business model, LOL. As you can tell, I made a fortune selling my books :-]

Click on the image to get there:

I believe Wolf is right that tapering is the main thing to watch here and not the discount rate that the Fed is slowly increasing.

Without the Fed support of MBS mortgage rates are spiking much more than the rise in 10 year and the rise in discount rates. I fear all those who bought in the last year or two because of FOMO will get their rears handed to them, and realize any gains due to low interest rates will be more than offset by the losses in home equity. They won’t feel so smart that they “locked” at 2.75% especially when they will need to sell due to a job change, divorce, or other life events.

It’s a terrible time to buy but it’s a harder decision when rents are going up so fast unlike in 2006.

Though I definitely consider the current market another bubble, I don’t think there is going to be an immediate housing crash this time. History never repeats exactly.

For this reason, I would consider buying a moderately priced home as long but then would need to commit to staying in it which I can’t do right now. Any loss would be treated as a consumption expense.

There needs to be one though because artificially inflated prices are not a sign of economic health and in the aggregate the country be better off.

There are no “moderately priced homes” when the median single family residence price is 10x household income.

To add to that the moderate priced ones are snatched up immediately with cash by institutions.

I’d buy a pos and work on it happily but they are on the market here (phx) for a day or two and then sell for asking with a cash offer.

“I fear all those who bought in the last year or two because of FOMO will get their rears handed to them, and realize any gains due to low interest rates will be more than offset by the losses in home equity.”

I don’t fear that at all, I celebrate it. These people are the dumbest of the dumb, and were responsible for driving up prices.

The corporate investors just write off the losses… Rinse. Repeat.

“I fear all those who bought in the last year or two because of FOMO will get their rears handed to them”

I fear that they won’t get their asses handed to them. The worst thing that could happen would be these batshit insane prices becoming permanent.

Someone said that stock market price has been 85% correlated to QE. I suppose there is similar correlation in overall housing. If QE is complete and QT starts, seems like like it is pretty clear the direction. But might be typical escalator up and elevator down or saw tooth pattern in markets.

LOL, divorce.

People who can do basic math understand that the FED’s 1/4 point rate hike is window dressing at best, outright criminality at worst. They could never dream of getting ahead of inflation at that rate. So the massive iBuyers and institutional investors continue to pour into housing and all hard assets because the FED has signaled they don’t G A F about inflation, so it’s going to continue roaring for many years, fueled by said criminals.

The Chinese money launderers and oil dictators are living a better life than we Canadians and Americans. This world is truly Hell.

Sorry, dude. There was a time when the filthy rich (and their antics) were small in number. Once everybody saw the grift, they sharpened their pencils and stopped living like a bunch of lushes. They got steel in their eyes and joined the contest. It was a matter of, if you are not at the table, you are on the menu. Evolution doesn’t say who is right (or nice, or neighborly, or good-looking), it simply says who is left.

Things like war and large instability (1930s-1940s) open up gaps and opportunities to move up. This may be the thing that interrupts long periods of peace and tranquility, where inequality builds up. That is not a comforting thought for me either.

Yeah, you’re right. Blame it on those 5 year olds who just couldn’t see what was going on 20 years ago, and failed to prepare.

well stated and true – truth is like evolution you can ignore it but eventually it will extract its toll

Phleep-excellent comment!

I’m sure it’s evolution when Canadian workers have to complete FINTRAC forms to withdraw from C$10,000, but a thick Chinese accent man can walk around Toronto with a duffle bag of cash to buy homes and no one bats an eye.

And the hell is just beginning for the younger generations with no assets. The FED just insulted them yet again yesterday. Notice how they couldn’t even provide any details on reducing their balance sheet after having months upon months to think about it? Yet these clowns show up in a MINUTE to hammer rates to zero, pour QE on assets, and save the stock market.

“Morale hazard” has become a 10% stonk correction.

We don’t agree on everything DC but I’m right there with you in your disgust of policy makers crucifying our young people.

They’re not doing we savers trying to earn a safe return any favors either.

w.c.l., it’s not just savers, but anyone looking to lend money period. even junk bonds trade at crap rates.

Junk bond rates are down because yield hungry investors are willing to take a chance on them bidding up the price and lowering the yield. I don’t see how lenders are limited by anything. Credit cards sure aren’t, payday lenders are only limited by law, and self financing car dealers don’t seem to be restricted. IMHO It comes down to how bad do you want the money and what are you willing to give for it.

but that’s just the point. the fed has created so much fake money that got lent out that the yields are terrible for money that anyone else wants to lend out.

I think that people are discounting the risk that the Fed will actually see it through this time.

The argument that they cannot raise rates much because there will be debt defaults doesn’t hold imo, because letting inflation roar will lead to the same result eventually, but with much greater damage. Because you would sacrifice the currency too (which can only lead to much higher real rates).

I get the feeling that they are trying to deflate the bubbles slowly but steadily, but they are failing atm because nobody believes them anymore, because in the past they u-turned as soon as stocks turned south. Hence the roaring stock market: everybody expects them to crap out again. But investors may be getting this wrong.

All the issues the Federal Reserve disregarded in the past, such as raging inflation, financial instability risks and threats caused by “elevated” asset prices, are now facing the economy in the short-term, solely because of the Federal Reserve’s long-term disregard of long-term consequences.

I agree it is going to crash soon no matter what they do. They now have to try and kick the can through a brick wall.

YuShan, I agree that the markets are discounting / underestimating the Fed this time.

IMHO I don’t think the Fed really has a choice here. They cannot go down the inflationary path any further. Their hand has been forced to go down the deflationary route.

I think the question at hand is basically: deflation, at what pace and timing? And will deflation (of any size/amount) create “panic”?

Personally I hope for deflationary overreaction, as that will most likely bring back (some) purchasing power to the cash I am holding. I realize such an event will probably only be a small “air pocket” in the grander scheme of governments debasing fiat, but still I think it will present some buying opportunity at least in the short term.

I just don’t see the Fed allowing for inflation to run any further at this point. It just doesn’t pencil in at this point.

It’s also important to recognize the inflation we are seeing today isn’t the typical flavor. It is exacerbated by supply chain issues which can’t be resolved using traditional means.

Steve Hanke says money supply ensures inflation is going to run very hot til 2024. My thought is interest rate and QT is going to take down asset inflation, but not do much on real inflation. That’s going hurt as assets go down and inflation stays high.

I think that is indeed the most likely scenario.

However, if they wanted they could dampen import inflation by raising interest rates enough to make the exchange rate rise substantially. But the paradigm of the past decennia has been competitive currency DEvaluation. They would have to do the opposite: competitive REvaluation.

I wish they could simply fire the complete Fed/ ECB and appoint people without all the historical baggage to fix this thing Volcker style.

People that haven’t moved house for years will now be seeing their property tax increase thanks to yet another crazy house price boom. The ten metros with the highest property tax growth from 26% to16% –

In Illinois, DuPage property tax is now worse than Crook County. A couple of decades of suburban school districts “arms races” will do that.

I like that area. Nice neighborhoods.

Terrible taxation though…

Sangamon county is brutal too. It’s crazy all over Illinois. It’s very expensive to fund that level of corruption.

I recently sold property there. The young couple that bought my house were a little surprised at just how much tax they were adopting.

Lost a bit on the sale, but not my property tax anymore. I will never own property in Illinois again.

I also know “expats” that sold a condo on Michigan Avenue on Chicago. They lost a BUNDLE. High taxes for high crime just ain’t tolerable.

I agree. We’ve been looking for the past 2 years and haven’t found anything worth purchasing. The prop taxes in Cook Cty are hard to digest. 1k a month for a 600k house and just average yard? I will wait and buy where the taxes are lower, since there’s only 6 years until the kids are on their own.

FOMO, BTFD, TINA, diamond hands, to the moon ….

Just a sigh of relief all my family members bought into some hard assets awhile back. And, for the most part, they didn’t try anything flashy with the financing. It is nice to be able to sleep reasonably well. Very underrated.

It would take a new Fed to do what needs to be done.

Will it happen?

My guess is more & more & more inflation until the debt is wiped out by funny money.

Good luck to the bond holders.

Cheers,

B

I try not to laugh at people who complain about mortgage interest rates rising to 4.5 percent because in 1978, I was paying 9.75 percent.

For decades, American taxpayers were paying billions in taxes to protect the country from the Soviet Union. Now, we have a Federal Reserve that behaves like the central planners of that Soviet Union. I’m not against having a central bank, but think that the Fed has assumed, and been granted, too much power over the lives of the American people. This transformation has occurred under both Democratic and Republican administrations and Congresses.

“I try not to laugh at people who complain about mortgage interest rates rising to 4.5 percent because in 1978, I was paying 9.75 percent.”

i’m really getting tired of this particular refrain (nothing against you specifically). in 1978, when you were paying 9.75%, you paid for the house the market price that 9.75% interest rates lead to. so while you were paying a high interest rate, you paid 1/10th for that house than anyone today has to pay.

Jake,

I didn’t take any offense from your comment. About six months ago, an economist in Washington, DC, opined to me that low interest rates make houses more affordable. That view arguably is true when prospective buyers are shopping for a house payment in the world of ceteris paribus. Unfortunately, suppressed long-term interest rates (and the inflation that often results) drive up house prices, so are these buyers really better off? FWIW, I’ve started thinking of economists as witch doctors.

thanks for understanding. you’re exactly right. and the disgusting and despicable janet yellen repeated the lie about low rates helping homebuyers.

no, they help homeowners who are looking to sell and downsize. that’s it.

It appears that many economists and politicians think human behavior is static, e.g. lower interest rates do not affect house prices.

I think it’s pretty obvious that for given monthly payment for the same house, higher rates make houses more affordable, for example, property taxes will be lower, insurance will likely be lower, there’s the possibility of refinancing later if rates drop, and your down payment matters more (e.g. think of $100K down payment on a $300K house vs $500K house)

“I’ve started thinking of economists as witch doctors.”

As practiced in recent government policy, it’s idiotic where it isn’t intentional.

… sorry to everyone else. I had a comment in moderation I wanted to be deleted (hopefully along with these trailings).

“ About six months ago, an economist in Washington, DC, opined to me that low interest rates make houses more affordable”

Indeed true…

Circa 2013-17…

Well, yes, houses were cheaper. But the middle class wasn’t buying a house as an investment, they were buying a home. And remember, wages were a heck of a lot lower too.

I bought my first home in 1989. I had to put down approximately one years wages (before taxes) to qualify for a 13.25 home loan. To put that into perspective, my mortgage payment then was almost exactly the same as my mortgage on a house bought in 2012 that cost 3 times as much, at a time when I was earning 5 times as much. And in 2012 the amount down was the same.

If you’re over 30 and you did not buy a house in the last 10 years you’re going to regret it, because I see this inflationary cycle running 10 years or more. It’s going to be very hard on anyone who rents, has credit card (or any other) debt, and isn’t in a position to be upwardly mobile in their chosen career path.

Milton Friedman is going to kick Joe Biden to the curb.

where do you get this nonsense? the middle class is not buying a house as an investment. they’re buying to live. and wages were actually a lot *higher* as a percentage of home costs.

how anyone can say that people are better off today trying to buy a house than in the 70s and 80s is beyond me

Back in mid eighties, I could have bought a condo for $7k. I didn’t buy it because there was no one to rent it to and the HOA because of all the vacancies would have jacked the fees to unbelievable. Denver area. Some of you don’t realize what can happen when people lose their jobs, companies shut down, unemployment rises. When you have to choose between food, gas and rent; many times rent or mortgage comes last. Just sayin’.

So, you are saying rising mortgage rates won’t matter?

Jake,

I forgot to mention a fact that often gets overlooked when people are comparing house prices then and now. Salaries and wages also were lower back in the good old days when houses cost a lot less than they do now. I think I was earning about $17,000 per year, which wasn’t sufficient to pay for a house in my area, I had to settle for a condo.

Taxes were lower back then also.

Social Security was only 5% back then.

“because in 1978, I was paying 9.75 percent”

Confused, my in-laws bought at +12% in 1978, but they were desperate for a place and simply bought — an element of desperation. Of course, later they were able to refinanced for a much better rate.

If mortgage rates rise sellers will offer to carry the note. As a seller I would gladly lock in full price at lower interest rates.

most people selling a house need the sale proceeds for something, whether for retirement in a downsized condo or a new home. seller notes are not an option for them, and indeed, most people.

i’d never recommend someone get involved in something like that as a seller unless the buyer is a family member, and even then, to be cautious.

Being a mortgage lender is not a business most home sellers want to be in, I guarantee you that. That’s why so few people are doing it. Like any business, it’s complicated, and if you don’t know what you’re doing, you can get run over.

Not that complicated – just need to know credit, get plenty of skin in the game and properly assess the risk – an excellent way to make some steady interest in a market that offers little else.

This works until the buyer stops the payments, but owns the home, and doesn’t want to leave. Start saving for the legal fees, the costs of foreclosure, and the loss after you finally get to sell the beat-up property, maybe a year or two after the buyer first defaulted.

Wolf,

I personally know of two scenarios you described, and the ‘owners’ gutted the houses before they walked away. One was intentionally trashed.

As a seller, I couldn’t do it…I gotta be able to sleep at night.

:)

Having a loan below market rates is a tremendous incentive for the buyer to keep the property. If the property value goes underwater you ride with them. The seller takes theirs up front. I approach TIP bond auctions the same way. Buy reissues while inflation expectations are low (they are always wrong) Buy at a discount, then wait for inflation to rise and the Fed is sitting on yields, (QE) You’re collecting a nice return on something you didn’t pay full price for. Powell said normalize several times, that means there is not going to be a Quixotic chasing of rates to match inflation, and consumers care about the monthlies, vendors care about price.

I carried a note and deed of trust @ 4.00 % on my house I sold about 5 years ago. The 5 year balloon is coming due and they’re paying it off. I would have preferred to roll it over, it’s been some nice income. They put $275K down a n $850k sales price (private sale, no broker) which was enough for me to build a new house on a $98k lot I owned. It took me 2 years to build the new house working 7 days a week and it went on the tax rolls at $734k. Zillow says it’s now worth $1.1M. Strange times!

Onto that, I can add, in a recession, there may be a lack of new-alternative buyers at a desired price. This happened after 2008: my neighbor defaulted on her mortgage, eventually sliding to where she brought in a druggie-felon boyfriend, and whoever held the mortgage didn’t foreclose for a long, agonizing time, for whatever reason.

I suppose maybe Depth Charge’s foreigners with sacks of flight capital, or private equity smarties, might swoop in and save the day from an owner’s perspective, but that sure didn’t happen in my neighborhood. 2008 is still fresh in my mind. It is like selling a business with provision repossess it: it can be dicey.

WOLF and DAVID

I would say you are both right. I now make my living as a lender. I absorbed about 4 foreclosures and it hurt. I learned what happens when there is no skin in the game (SITG).

When skin is required, it’s astonishing how the field of borrowers dwindles. That said, with 25% down as SITG, even in a deflationary market, I am fine with the risk and 10% annual mailbox $$.

Are you going to hold that paper for 30 years or deed it to someone who will?

If not, do you expect to sell it at a discount versus publicly traded paper because the chances are this might be necessary.

Even with the current increase in rates, it’s one of the worst possible uses for the money.

The bond bull market from 1981 might not be over (I think it is) but it’s not going to last anywhere near another 30 years from now.

Taking back long-term paper now on a property sale is the equivalent of buying a (relatively) illiquid debt security in a raging mania where the long-term economic fundamentals are also mediocre to awful.

If you borrow $300K 30 yr fixed,

At 3.5%, monthly payment is $1347

At 4.5%, monthly payment is $1520

That’s 12.8% higher in terms of cash outflow on household spending.

So a rising interest rate has an inflation like impact.

But interest costs are not included in CPI as per BLS.

https://www.bls.gov/cpi/factsheets/owners-equivalent-rent-and-rent.pdf

“”Interest costs (such as mortgage interest), property taxes and real estate fees, along with most maintenance and all improvement costs, are part of the cost of the capital good and are not consumption items either. The CPI adjusts the expenditures for

home maintenance downward before using it in the CPI weight. “””

They say it’s part of Capital Goods and not something consumed, therefore not part of CPI.

But interest costs and property taxes don’t add any value to the Capital Goods so should be considered consumption, shouldn’t they?

Rightly or wrongly, the BLS looks at housing costs as a service (“shelter”), and it uses two rent factors to approximate the costs of this shelter = 1/3 of CPI.

I guess two rent factors are supposed to capture in interest costs, property taxes, maintenance, etc., as landlords factor those costs when setting the rent.

But what about the cost of interest in a broader sense like auto loans, credit card or any other financing?

My question would be, is the cost of money captured anywhere in the CPI? If not, why not?

BLS deliberately excludes interest costs because it is circular.

Since many interest rates are linked directly or indirectly to Fed Funds Rate, it would mean that the Fed easing monetary policy by lowering interest rates is counterproductive because it will cause deflation by lowering interest costs.

Could it be said that raising the interest rate accelerates the rate of inflation?

I mean it increases cash outflow for borrowers and increases income for lenders.

There is nothing deflationary about a rising interest rate in itself.

As they say the cure for high prices is high prices, the only way a higher rate suppresses inflation is by destroying demand.

The way I see it, a rising interest rate only speeds up the inflation until we reach that point where demand gets destroyed.

I’ve bought a couple rentals in my time. Maybe 20 in my life time. All in cash now because… But simple formula. What’s the going rent for the area? $2000? times 12 =$24000. Taxes & insurance & maintenance, $6000? $18000 divided by desired rate of return (5%)?. House is worth $360,000. Not $500k.

Kenny,

You’re trying to apply theory across all classes of income…

Top 20% of income doesn’t care about interest rates… if they want it ( if they don’t already have it ) , they’ll buy it on favorable terms….

The lower 30% can’t afford anything, so they don’t care about interest rates…

The impact most felt is in the middle 50%, they will get crushed playing to play the “ look at me “ game…

That’s where the most demand will be destroyed…

One phrase that should cause shivers in a lot of men is “ the lifestyle me and the children have become accustomed to” :)

Exactly. BLS only counts the “service” value of the shelter.

Too bad SAAS is already taken. “Shelter as a service” would be SAAS.

Wrongly.

They created a category that contains something everyone needs, then made it underweight in the inflation calculation, then let banks run wild forcing the price up. They also changed lending from 3 times primary income to 3 (and more) times household income to force both parents to work and to capture the additional income.

Everyone working more for the same pile of bricks. That’s usury for you.

Curious how some areas move glacially, but with inexorable progress in one particular direction, yet no one wants to know. Like the Dr Evil employee infront of the steamroller smiling and walking forwards Austin’s steamroller,

.. instead of shrieking.

Whilst, in other news, some areas soar,crash, rise like a phoenix to fly just a little lower before they… just inexplicable trade sideways in an otter-like recumbent snooze.

Tide’s or tiredness always right for somebody, I suppose.

That said it’s about time a spring’s tide goes out and shows those swimmin’ with nothin’ on, I reckon.

While the stats do seem to be turning, there’s a big base effect going on. Last year was absolutely bonkers as people were buying homes in response to covid. Looking at the actual numbers, it looks like sales are still higher than they were in 2019 and early 2020. So we’re still only getting back to our baseline trends. That said, I understand these numbers are lagging indicators so perhaps the market has cooled off much more, more recently. But I think we have to wait for the numbers before declaring the peak has come.

Wolf wrote:

“According to the daily measure by Mortgage News Daily, the average 30-year fixed rate mortgage hit 4.50% yesterday, the highest since March 2019. ”

In March 2019, the median house sales price was $261,100 compared to $357,300 today. That’s an increase of almost 37% over the last 3 years.

Since the mortgage rate is same now as it was then, this means that monthly housing payments (PITI) are also up 37% while household incomes over the last 3 years are likely up no more than CPI – about 12%.

This is a huge drop in affordability over the last 3 years and will just get worse as mortgage rates rise further even if house prices level off.

This is not sustainable – something’s gotta give ….

What gives is people’s hopes of owning a home. The fed apparently has no concern with turning multiple generations of Americans into lifetime renters. I guess that’s just the will of the free market at play? But how free is a market when it’s controlled by fed policy?

When homes are owned by investors, how will fed policy effectuate their wealth effect on younger generations? The only channel left is the stock market.

Under this line of thinking, anyone priced out of a home should be fully invested in the stock market. You can’t afford to leave any cash in a savings/checking account, or you’ll risk being left behind and destroyed by inflation in the long run. Also, avoid pension plans and focus on employers with 401k matching.

homeless…

Dead on!

“”The fed apparently has no concern with turning multiple generations of Americans into lifetime renters.”

The Fed has lent to the mortgage industry 40,000 Million dollars A MONTH buy buying MBSs (40 billion)

For two years…..why?

In 2006 the Fed owned NO MBSs, now they own 2.7 TRILLION!!

https://fred.stlouisfed.org/series/WSHOMCB

The younger generations are having their futures saddled with debt ($30 Trillion now) and that money is being used, in part, to bid up housing and equities from them, denying any reasonable entry into either. Criminal, IMO.

It used to be young families could save to buy a house. Now savings go backwards as real estate explodes away from them due to Fed activity.

More like 168 trillion ,were being lied to

homeless,

So what’s YOUR plan for YOUR future?

Do you have one based on your best and worst economic forecasts? Short term and long term?

Just curious…

If they don’t die in it, or starve to death. What a lunatic thing to wish for.

Bro, don’t worry. Huge economic implosion coming next few years that will pull the rug out from all US asset prices.

2 key drivers: commercial real estate devaluations and US demographic cliff.

Boomers about to start drawing down IRAs en masse. But more importantly, $16+ trillion of US commercial real estate about to lose 50%+ of its value.

You think the Fed was panicking in 2020? You ain’t seen nothing yet.

And when the Fed goes back to ZIRP, QE, and “emergency accommodative policy” again, for the 15th year … someone will finally have the guts to ask JPow the only question that matters…. “Will it ever end Jay?!”

Eventually the truth will come out: No. It can’t end. Fed can never stop. Because you can’t allow deflation in a debt based monetary system, only inflation. And besides money printing, the only other inflationary drivers — population growth and productivity growth — are over for the foreseeable future.

And that will be the day the public finally realizes the emperor (USD) isn’t wearing any clothes.

And then I don’t know what happens. But it won’t be pretty!!

Hm, double checked that $16T, too high. Only $3T is office space. So the hole will be smaller, but still big enough to cause a bit of mayhem.

after was estimator/project manager in commercial RE mkts for many years PNWG, and AGREE with you, far shore…

one real hard question for investors, is where between your $16T and $3T will be THE sweet spot going forward from here with re ALL commercial RE???

another, equally hard Q might be, how much of the totally unknown secondary, tertiary, and these days likely even more obscure financialized ”paper” is connected to commercial RE in USA and else where???

really and truly from what I read on Wolf’s Wonder and elsewhere, NOBODY KNOWS at this point in time…

”going to be interesting” is the understatement of the era, far damn shore

And what does that say about the purchasing power of the dollar…in the real world,….not the Fed world?

I’ve been meaning to say this for some time. So.. no more MBS purchases , no more FED Treasury purchases. Treasuries go to sale , few buyers. Rate increases to the few buyers desires? Right? Also, the FFR is what the FED controls. But their only and recent manipulation of rates has been their ability to step in and buy Treasuries when there are few buyers. So even if they don’t raise rates, the rates will rise on their own competition. Thus, mortgage rates to stay competitive must increase. Sorry, I’m not that in the know. Thanks for your patience.

I think the number where it really slows is 6%. Then just all cash foreign buyers will be left.

According to the NAR methodology, the Housing Affordability Index reached an all-time high of 184 in Jan 2021 due to a combination of stimmie enhanced family income and record low mortgage rates.

Right now the HAI is about 132 which is down massively over the last year but still well above the all-time low of 100 from 2006.

If or when mortgage rates hit 6%, HAI will drop to 108 – a level not seen since the last bubble peak in 2007.

To set a new record low affordability, mortgage rates would need to exceed 6.6%.

We’re in the last hurrah of the baby boomers shafting the young with their cash. Not sure when, but eventually demographics will kick in, with ever smaller younger generations, eventually there will be a lot fewer buyers and potentially empty homes. Likely the first hit will be states with negative population growth.

It will be interesting to see how investors react. They don’t care necessarily about mortgage rates and still have no better place to put their cash. Rents rises will have to eventually level off, but they will have leveled off after huge increases.

I’m a boomer and I didn’t shaft anyone.

Hahahaha, I’m a boomer and I got shafted many times, and I’ve come to understand that that’s life and that you’ve got to deal with it (this kind of understanding comes from being around long enough to be a boomer).

I always enjoy it when Wolf admits taking a hit because experience is what you get after you screwed up. Anyone who only tells success stories is just locker room BS.

Being a Boomer wasn’t all sunshine and roses. I get acid flashbacks watching what’s going on today. In the 60s and 70s cities were literally burning due to race riots. 4 students were shot to death by the government at Kent state. RFK and MLK were assassinated.

My first mortgage in 1984 was about 13%. We were in the middle of stagflation. Volcker came along and cranked up interest rates to fight inflation but at the inevitable cost of recession.

It wasn’t all bad though. We had “free love” and your worst virus fear was herpes.

One of my goals is to become a financial burden on my children. One went to Duke, the other to NYU. Due to my income financial aid was out of the question. $500,000 to put them through college.

Time to collect. I also hope that at my funeral people will say “That guy owed me a lot of money”. :-)

I graduated high school (mid 70s) and law school (1981-2) in recessions. The 70s had oil shocks, lines at gas stations for suddenly pricey gas, Vietnam war loss, terrible inflation, US loss of prestige, Iran revolution US hostages every day in media, mass demoralization. We were under constant nuclear standoff, facing the USSR and China. Tell me how simple it all was. I bought a home at age 37 and had no idea before then that I ever would. It turned out to be a pretty good deal but I had to scrimp to keep it (and my balance sheet in good shape). Happy sailing!

maybe not directly, but i’m sure you feel entitled to your social security and medicare.

which is the problem.

when i tell boomers “what if the money isn’t there from current production such that the working people have to be shafted with ruinous taxes?” they say “oh, well, they have to figure it out, because it’s mine!”

You are absolutely %100 correct, Jake. I feel very much entitled to what I’ve been working and paying for since I turned 13 years old. That’s why it’s called an “entitlement” as opposed to “welfare”.

I’ll never get back what I’ve paid in, but I will never blame you or your generation for that raw deal or ever ask you or your generation for reparations.

I learned a long time ago who causes all of my problems. It’s the guy in the mirror. He’s the only one with the power to invoke change. Blaming others is a complete, foolish waste of time, Jake.

The way to strengthen and make Social Security permanently viable is simple. Drop the limit on taxable wages. Tax stock based compensation as ordinary income applicable to the same Social Security rates.

These programs are a social contract everyone enters into to become part of a civilized society. And you advocate to break that contract and commitment? Is that where your values lie?

There’s always enough money for wars and interventions and tax cuts for the wealthy. There are armies of accountants and lobbyists and lawyers who do the bidding for their billionaire masters so that they pay little or even no taxes.

There is a reason these programs were initiated and carried on for all these years. Once the house of cards the speculators and robber barons built self destructed, the pain and suffering, especially by the elderly, inflicted on the common man was so obvious and horrifying that “Civilized society” bonded to ensure there would always be a safety net. That we were all in this together.

You’re not being shafted by ruinous taxes. You’re being shafted by the predatory activities of the vultures working every angle to get as much of your earnings as possible. Blaming Hal and “the Boomers” only makes you an unwitting accomplice.

The other important ingredient to ensure SS, etc., are viable for ever and ever is to make a constitutional amendment that requires EVERY GUV MINT retirement and medical services delivery program EXACTLY the Same for each and every GUV MINT public servant as for everyone else…

Just think about it for a minute: IF and only IF every politician was eligible for the same SS, etc., what kind of shape would that system be in today???

It’s one step toward fairness and elimination of the obvious 2nd class citizenship of the vast majority of WE the Peons, eh???

hal, what if the money isn’t there, meaning the taxes that the then working people pay can’t support it? then what?

markinsf, dropping the limit on taxable wages just means that the top earners are paying 60-70% of their wages in taxes, while more than half pay almost nothing. that isn’t sustainable either.

if they’re a social contract, where is my signature on it? i don’t recall signing up for it.

there isn’t money for wars and interventions either. society as a whole feels way too “entitled” for things we can’t afford. that’s why we’ve made up the differences with debt and printing.

Not a very well thought out comment, Jake.

Frank…

“last hurrah of the baby boomers shafting the young”

Those who are “running the show” may be baby boomers, but they dont speak for that generation. That generation was comfortable with low inflation, saving, earning, and doing “some” investing. The current policy makers PUNISH such behavior.

The younger generation is being saddled with tens of Trillions in debt, essentially taking money from their future and having it used to BID UP housing and stocks out of their reasonable reach. Criminal in my opinion.

It was once incumbent on each generation to “pay its own debts”…..but the game since 2009 has been to STEAL FROM THE FUTURE….$21 Trillion worth to date.

i think it’s really the greatest generation and the silent generation that was comfortable with that.

the boomers are the most selfish generation america has ever seen.

Obviously you don’t have Millennial children.

michael, i am a millennial myself, on the younger side. all i see from my parents’ generation is gloating about how they “paid their way through school” leaving out the fact that tuition has gone up by a factor of 30x since then.

i hear them talking about the 10% interest rates they paid on their houses, but leave out that the houses were only 2x income, not 10x or more like they are today.

i hear them bragging about how they’re such “brilliant” investors for “dollar cost averaging into the indices,” leaving out that their stonks would be worth 1/5th without massive fed printing which is stealing from my generation.

other than the older boomers who served in vietnam, this is a generation that has seen no hardship, and has only known prosperity, although much of it is fake prosperity built on debt and printing that is only possible due to the patrimony that they inherited from their parents and grandparents.

Jake W,

I love you but with this line — “this (boomers) is a generation that has seen no hardship — you show the entire world that you don’t have a clue.

You have no idea what it’s like to be drafted to go die in Vietnam, and demonstrate in the streets against it and get shot. Boomers went through every recession you went through, PLUS all the prior ones, including the infamous double-dip (yes, go look it up). Check out the homeless people — lots of boomers among them. Boomers died at a young age of diseases that are no-nothing curable diseases today. Boomers died in car accidents like you cannot imagine because those cars were death traps. Boomers went through the worst inflation, and you cannot even imagine what this was like; much worse than now. Boomers had no idea when they grew up what the internet was and cellphones, and they had no way of venting by posting angry comments on websites like this. You need to get real!!!

The issues in this society – and there are huge issues – are not generational. That’s a braindead red herring. You need to look at the REAL issues.

You need to quit trolling my site with this generation BS. Your future comments on boomers will just vanish. So save your breath for something that makes sense.

Assigning elemental characteristics to generations disregards the obvious – people are people who pretty much share the same desires, dreams and destinies as the human race plays out. People will utilize the resources available to them. That will never change.

80-85% of any population just wants to procreate in an environment that will provide safety and opportunity for them and their offspring. That is true throughout the annals of recorded history.

I’m a boomer who went to Viet Nam, fiercely opposed globalization, all the Middle East wars, the destruction of unions, the repeal of Glass-Steagall and the repeal of other legislation and executive orders that paved the way for the creation of the “billionaire class” but I’m as helpless as any ordinary individual in shaping history.

Whether you like it not you have signed on the social contract. Everything you take for granted, the use of roads and highways, the power grid that provides the infrastructure that heats your home in the winter and cools it in the summer, the satellites that enable the internet, cell phones and GPS, essentially everything that allows you to live an existence that provides the relative luxury you enjoy. All paid for and built with your tax dollars by a government that has been systematically gutted by accumulated wealth.

Sorry you’re around a bunch of idiotic older people who don’t understand the plight of your generation. Sounds like you need to expand your horizons.

Instead of focusing your ire at small individuals who were just trying to survive and are currently in a fortunate position (that can change overnight) why aren’t you lashing out at the true source behind this mess?

Somebody invested in you to give you a free K – 12 experience and if you sent to a state university funded part of the bill. Teachers don’t work for free and buildings don’t construct and maintain themselves.

Do u hate tour parents there boomers I presume

wolf,

i apologize for generalizing with a broad brush. note that i did exclude those who were drafted to vietnam.

i’m just tired of hearing sanctimonious bs from people who grew up in the 60s and 70s and talk about how they saved for college and a house, when those choices are not readily available to a huge percentage of people today.

it’s one thing to recognize that you got lucky. it’s another thing to be arrogant about it and think that fed largesse and the credit bubble is all one’s own brilliance.

Jake W.

1. I agree with your #3 paragraph. What the Fed has done – creating the biggest wealth disparity ever – is causing a huge amount of societal problems. And some beneficiaries are gloating about it.

2. I’m tired of generation bashing. A few years ago, millennial-bashing was a thing, and I had to stamp it out. Now it’s boomer-bashing, and I have to stamp it out. Generation bashing is ridiculously clueless, no matter what generation gets bashed. Even the whole modern concept that people born in a specific 20-year period are a monolithic bloc is silly.

3. I’m surrounded by millennials that make huge amounts of money. Michael Gorbach, who comments here and is an author on this site, has two millennial daughters. I know that at least one of them, and her husband, are making huge amounts of money. Millennials are running companies and are becoming millionaires and billionaires.

4. Yes, this is a shitty world in many respects for many people, and there are huge problems, and there have always been huge problems, but it was a shitty world for boomers too, and they were just born into it and had to deal with it, and boomers agitated in the streets to make it a better world. Many many boomers are essentially impoverished with no retirement funds and just a small amount of Social Security that they paid into all their lives. Many live on the streets. Boomers weren’t born with a silver spoon in their mouth.

Where I live just outside Denver, we still have such a massive imbalance between the number of buyers and the number of houses for sale, that anything half-way decent continues to goes under contract in under a week at well over asking. I suspect we’ll need several more rate hikes, and/or 2x the inventory to seriously dent demand and prices. Will be interesting… as I’m looking to cash in my chips at the RE casino and geo-arbitrage by relocating to Mexico, which appears to not have a housing bubble (outside of a couple of gringo-centric locations).

One issue is the supply of housing is still at a deficit. Sure a lot of condos are being built but not enough Single Family Homes because of various reasons. Realty track said there 1.4 million zombie homes. (homes that are empty for one reason or another) Even if all those home hit the market, that supply would be gone quickly. I read about 6 million homes are sold per year.

With inflation higher than current interest rates it entices wall street to buy homes too.

Plus you have a population growth of about 1.5 million to 2 million a year. Add in another 200k to 400k illegal immigrants. Since most homes average 2.3 people, we need about 860k new living units per year. The last 8 years have been below that number and thus inventory keeps decreasing. Wolf has had some good articles and charts on the number of new homes being built each year.

Example of inventory issues. In my metro of 2 million people, in 2014, there were 14k homes for sale in the month of January. In January 2022 there were 2200. That is over an 80% drop. I did notice in March the number of homes for sale has jumped up to 3500 which will be interesting to see if this inventory trend continues.

Crazy.

Aspen is full of empty houses and condos in the summer time.

Wisconsin is full of empty houses and apartments in the Winter time.

I imagine Florida must be full of empty housing units in the good ole Summertime.

and same for florida for ever apple!

back in my ”pre-teens” and subsequent, we kids could walk down the waterfront and swim in dozens of swimming pools that had functioning equipment, but no owners or occupants present for most of the months between march and late fall/early winter…

it WAS a ton of fun,,, but mr. carrier ruined it all when the ”central air” came to most florida houses, and the results today indicate cleary what a totally clustered arrangement proceeded since

some of us native floridans used to consider making it a law for all ”seasonal visitors/residents” to go home at the end of march just like they used to do before central air,,, and now, of course, most of us have totally welcomed ALL the folks coming from where they do not have caps on property taxes, etc…

so far, from what I have seen/read recently,,, MOST of the folks coming here to the flower state have at least SOME understanding of what it means NOT to have GUV MINT ”’TAKING”’ everything they can from WE the PEONs