Last time prices fell like this was during the Financial Crisis. But now, there is no crisis.

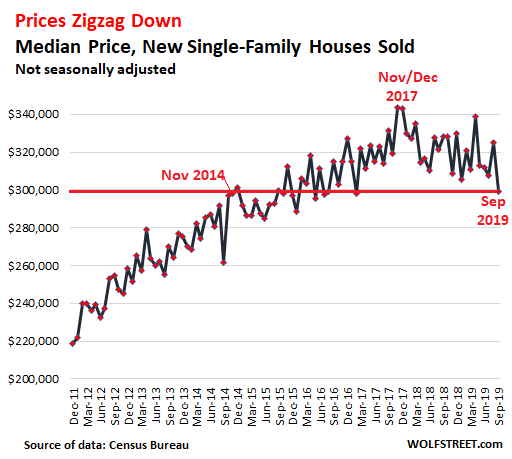

The median price of new single-family houses in September fell 8.8% from a year ago to $299,400 – down 12.8% from the peak in November and December 2017 and back where the median price had first been in November 2014, according to the Commerce Department this morning:

“Median price” means half of the houses sold for more, and half sold for less. The decline in the median price does not include incentives that are thrown in by homebuilders to close deals, such as free granite counter tops.

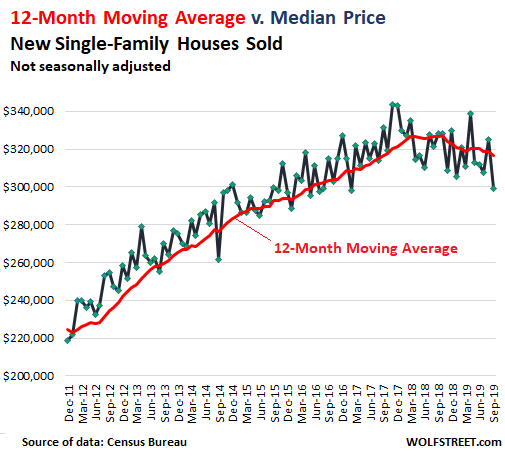

The longer-term trend via the 12-month moving average.

This median-price data – produced jointly by the Census Bureau and the Department of Housing and Urban Development – is “volatile” on a month-to-month basis. To show the longer-term trend, I added the 12-month moving average, which eliminates the monthly ups and downs. The September data point, being the average of the past 12 months, lags months behind of today’s market, but it allows for longer-term trends to become clearer.

The lag of the 12-month moving average (red line) shows up in how, on the way up, median prices were mostly above the red line, and now on the way down, median prices are mostly below it:

So the market has significantly changed, and homebuilders are responding to this changed market with lower prices – which is interesting given where mortgage rates are.

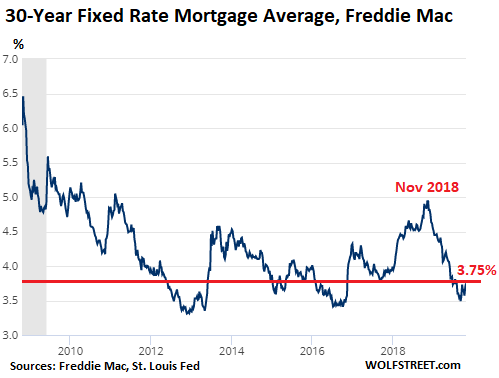

Mortgage rates tick up but remain near record lows.

The average 30-year fixed-rate mortgage interest rate rose to 3.75% for the week , according to Freddie Mac this morning. While up a tad from the near-record lows in August, it is still down over a full percentage point from 4.9% a year ago and remains close to record lows, which puts the decline of new house prices into a peculiar light as it was assumed that such a sharp drop in mortgage rates, as we’ve seen since last November, would boost house prices:

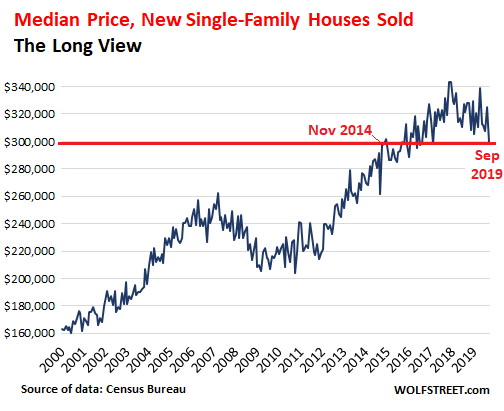

The Long View.

During Housing Bust 1, the median price of new houses dropped 22% from the peak in March 2007 to the bottom in March 2009. Then, from 2011 and 2012 through the peak in November 2017, it surged by about 55% to top out 31% above the peak of Housing Bubble 1. But at the end of 2017, it hit a ceiling and has since then dropped nearly 13%.

Lower prices beget sales.

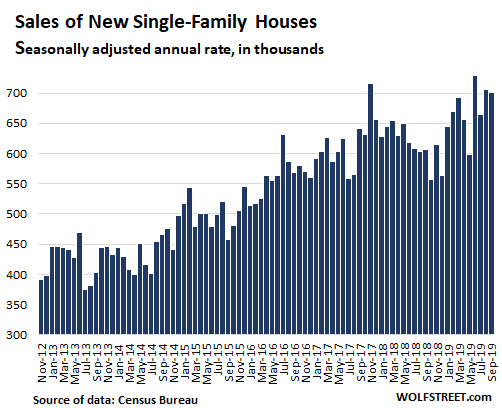

Homebuilders – unlike homeowners who want to sell – cannot “outwait the market.” They have to move their speculative inventory, and to stay in business, they have to build and sell houses. The lower prices are stimulating volume. In September, homebuilders sold new houses at a seasonally adjusted annual rate of 701,000 houses, the fourth highest since the Housing Bust, and up 15.5% from September last year:

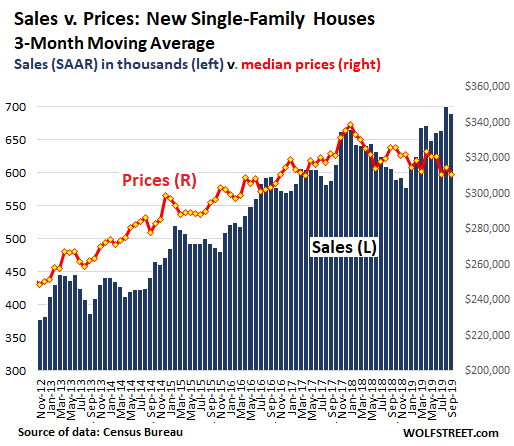

The relationship between prices and sales volume – how they behaved before 2018, and how they changed over the past couple of years – becomes clearer with a comparison of the three-month moving averages of median price and sales (median price = red line, right scale; sales volume = blue columns, left scale). The sharp drop in sales that started in early 2018 was eventually stopped and then reversed by significantly lower prices:

Plenty of Supply.

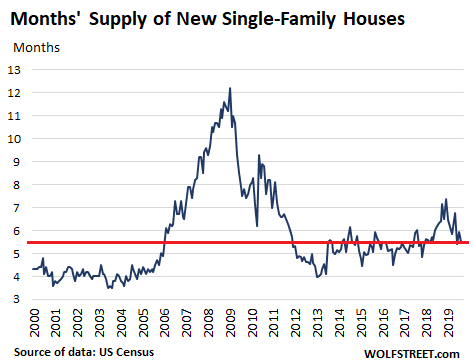

Inventory of new houses for sale ticked down to a seasonally adjusted annual rate of 321,000 houses. This is still high. But due to the increase in sales, home builders are now sitting on 5.6 months’ supply at the current rate of sales, down from the range between 6 and 7 months late last year and earlier this year. Four months’ supply would be more than enough:

Homebuilders are the pros in the housing market. They have no illusions – unlike homeowners. They have to adjust to the market so that they can continue to build and sell houses at a profit. They cannot build speculative houses and sit on that inventory for long. They have to do what it takes to move it. And they’re doing it.

The median price is impacted by cutting prices and by a change of mix. If homebuilders sell a larger number of lower-priced homes, the median price declines – because builders chose to build houses at lower price points to begin with to meet the market; and because they cut prices of houses they’d intended to sell at higher price points. One way or the other, it shows that on average, as an industry, builders have run into price resistance in enough areas to push down the national median price, despite the ultra-low mortgage rates.

In the San Francisco Bay Area, house prices dropped 16% from the peak in May 2018. Ironically, they dropped the most in Silicon Valley. Read... Housing Bubble in Silicon Valley & San Francisco Bay Area Turns to Bust Despite Low Mortgage Rates & Startup Millionaires

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It feels as though we are in the “Twilight Zone” of monetary theory…

I was going to guess “The Outer Limits”, but you might not be quite there yet. You know how famished financiers like to push the envelope.

You guys (Americans) are silly.

How can you allow housing bubble to burst?

I would strongly suggest to get in touch with multimillionaire crack shack owners from Toronto and Vancouver and gain knowledge on how to inflate and maintain largest ever (asset held in place by bug spit) bubble in the history of mankind.

Amateurs ! ….. :)

Those are all resales even doctors can’t afford new homes in Toronto or Vancouver. The only buyer of new homes was or is the Chinese. That must be the reason for the fall in new home prices in America. The rich Chinese are already here in Canada and Trump’s trade war is killing off the new homes market in both Canada and in America.

Wolf, been trying to ask you something about central bankers sponsoring assets.

Until these Banking Monkeys get slaughtered and get scared, they would never allow asset bubbles to pop. Next up — Fed gonna start OWNING stock market and junk bonds, just like BoJ and ECB. After that, they would start owning bubbly RE in USA/Canada/Europe , and then give you FREE monthly stipend through Negative Interest Rate NIR.

Renters and their kids, grand kids, would be renting for rest of their life. These Banking Monkeys are not afraid to keep screwing you and future generation, because they face no consequence, and receive only praises from main-stream media and existing bubble owners.

All the mathematics equations, equality, capitalism all gone out the window once Fed, ECB started printing unlimited Reserve currency. Your All Bubble Bursting scenarios have not occurred in last 10 years, and what makes you think it will ever burst? A few times it came close bursting, then CB started printing and printing … and even now Powell is printing again. Even recession does not matter anymore.

You can’t print forever. Eventually, you’ll get a liquidity crunch that you can’t print yourself out of and it’ll be bad.

” Eventually, you’ll get a liquidity crunch that you can’t print yourself out ..”

Really? Where have you been in last 10 years? Everytime there is a slow down in economy in USA or Europe,

1) Bernanke Monkey did QE2, QE3, … until SPX stop going down. Print Unlimited Reserve Currency across many years

2) Powell, started printing last month to resolve REPO rate issue. And this is the guy who thump chest just end 2018 saying would continue to raise rate and QT through 2020. Fxck DUMB!

3) Draghi print Unlimited Euro to buy Junk corporate bonds and pretend no default to maturity. Negative Interest rate of -0.5%.

4) BoJ is the largest shareholder of Nikkei 225 companies.

Where have you been? Until these monkeys get slaughtered and fear the people, they will just gonna continue to print unlimited to screw you and the poors.

Sean, with all due respect, it is NOT the central bankers. If you, Sean sit in Bernanky’s chair, you will become a monkey too. So will I. Power corrupts people, nobody is immune. The founder of USA understood this so well that they diffused the power through multiple branches to balance.

For me, I want to hang some central bankers too. But make the bankers fear the people won’t prevent future bankers to emerge to make the people fear the bankers. The more effective way is just do what the founders did, eliminate that central bank printer. Neuter the power, and people stop being corrupted.

So who ever goes to the screen and says “elect me, give me power and I will save you”, I will just go watch some porns. If anybody goes to screen and says “ elect me and I promise you I will do nothing other than eat and shit in the white house”, that is the one I will listen to.

Saying you can’t print forever is like saying you can’t expect the sun to keep rising every morning. I’m sorry but reality has proven you wrong. The Fed once pretended they would not print forever but now that pretense is gone, there seems to be an open admission that they will increase their balance sheet into perpetuity to fund government deficit spending even as the deficits continue to grow out of control.

The government continues to grow the deficits because they know the Fed will always show up to monetize the debt. The Repo lending market began to blow out only because there was too much government debt for the primary dealers to buy so like clockwork the Fed showed up and began monetizing the debt.

Powell can call his “not QE” whatever he wants but the fact is he is monetizing government spending and he is printing dollars even faster than Bernanke and Yellen were – he is in full on helicopter mode and there is no end in sight. “You can’t print forever” – indeed. I think what you meant to say was: you can’t print forever without destroying the monetary system – but Powell clearly doesn’t give a damn.

The Fed’s childish money conjuring, to avoid any and all austerity, needed to undo excesses and waste, has brought us unsatisfying pain avoidance in the short run but there will be unimaginable suffering as a consequence. Bernanke, Yellen, Powell, Kuroda, Draghi, cowards all – history will not look kindly on them.

Imagine the world economy without a functioning monetary system after people have lost faith in currencies – not a pleasant scenario but one central banks are willing to risk.

Even recession does not matter anymore.

Not to the Financial Industrial Complex. The real economy can still get a recession, but with the new bailout policies the FIC can’t because they’ll just pass the costs and the risk of implosion along to everybody else.

It’s always a recession for somebody, somewhere, but unless the FIC gets a recession they’ll never call it that.

I don’t see why the Central Banks can’t just keep printing and buy all the assets?

I also can see the governments paying out more and more state benefits to citizens as there are less and less jobs available due to automation, robots, databases, AI and the old continuing to work.

I believe that is the only way to prevent a civil unrest in the long term and when that gets close, create a world war for a reset.

I’m going to miss you guys, but I think I’ll get over it.

If you keep printing money up the yingyang, it becomes increasingly devalued, especially when measured against something which retains its value over time, e.g. gold. At some point, ordinary people will become aware that there money is toilet paper and a crisis of confidence will ensue.

If printing money can solve all economic society problems, Zimbabwe would have been Switzerland.

There is a limit.

Charlie Munger said it best about excessive money printing which goes something like this ‘if you don’t exactly know where the limit is and what’s going to happen you better stay a long way from where you think it is.

Instead Switzerland is becoming Zimbabwe.

You think the Swiss want to work? Guess again.

Because, for the past 170 years, it always has.

https://seekingalpha.com/article/4296904-dividend-etfs-reit-etfs-low-volatility-etfs-still-work

See the graph on Recessions by decade. Every decade for the past 170 years has had at least one recession.

Well I told my best friend to refinance his mortgage.

He made it just in time for the 3.25% rate. Yahoo.

Just like anything else in life, there are winners and losers.

Just curious: how long was your friend paying the old mortgage?

First he had a variable rate, with option to expire last year.

then he refinanced AGAIN last week.

So we did twice in a year apart. Difference was about 1%.

When you take into account closing costs, refinancing is only worth it if you plan on staying for a while. I looked into refinancing my self, closing costs would have been about $3500 in order to save $80/mo. That’s 4+ years payback. Who knows if I’ll even be in this house in 4 years? Maybe, maybe not.

When rates are as low as they are today, and have been for years, it’s a diminishing rate of return to refinance.

Although what many people do is roll over the closing costs. Which is is a dumbness level of 11. But most Americans are clueless when it comes to math or finance. So there we are.

You should have advised him to sell before the economy falls apart and the dollar loses reserve status He could buy two or three with his gain from buying gold with the proceeds of the sale

Most normal people can no longer afford houses in this country. Moreover, even if one can stretch into a house, who wants to buy at the top and be stuck in it or possibly lose it and your rainy day fund/nest egg you blew to try to make the down payment when you lose your job in the next recession? Thanks Fed! Morons.

…go to Canada, esp. Ontario and British Columbia and see, what’s going on there! 800K – just “regular price” both for the regular house and tiny condo.

Alex, should read…. “go to some places in Canada, like Toronto or Vancouver”. My 35 year old son is in the process of renting his home out and will shortly be buying another house to share with a few roommates. This is in BC. 800K buys a mansion in most of Canada….just sayin’.

Only one-third of Canada’s population lives outside of the greater Vancouver area and virtually all of Ontario which was road-killed by the Chinese.

Using median numbers $300,000 house

Median down payment 10% debt =$270,000 Median student loan $37,500 × two people = $75,000.

Combined long term debt backed by tax payer = $345,000 . Don’t know how many could go belly up but let’s say 1 million. Add 6 zeroes = $345,000,000,000. That’s $345 billion. Would take the Fed a few months to QE that much without us noticing.

I have heard comments that we are hitting the stage where we have so much debt that people are taking on debt that they don’t really believe they are going to have to pay it back. Not good.

Yeah, Old-School, it would seem easy enough to bail out many retail debtors on the face of it, but I suspect that sort of QE would be some last gasp gambit of the central bankers.

The problem is that if they give QE to people on the street, then it will flow straight into their inflation metrics, and that would render their position a bit difficult. Whereas when they give it to financiers and the top cats running our zombie enterprises, then, outside of inadequately measured inflation in financial assets and property, it only causes inflation to skyrocket in some peripheral things like vintage cars, fine wines, works of art and suchlike.

As it stands the inflation is still baked in, it’s just that we’ll possibly have to wait until financial assets start to really get liquidated as pension and social security funds seriously start to get large net drawdowns before we really see it flow into the things they measure.

I agree. I just want a home for my family. This seems like a lifelong unattainable goal, or else modern day financial slavery.

Look at the months of supply, we are nowhere near 2009.

Six months and below of inventory are signs of a normal market, wake me up when this changes.

With the Fed issuing papers in favor of negative interest rates, the housing market is getting ready for the next leg up. Nothing goes to heaven in a straight line.

Someone sounds nervous. Home prices are falling. Get over it and get on with your life

I am not nervous, I am about to close on another multifamily building. It is expensive but I can still get 4% cap rates on it. Real estate right now is the only asset accessible to people not filthy rich that are looking for some protection from the crazy experiments of the Fed and eventual inflation.

I am not comfortable to leave my money in the bank, and interest rates are close to zero anyway. Yes, prices might come down but you are having tunnel vision if you fail to consider how other circumstances might evolve. If you think that you will get real estate for 30 cents on the dollar you are deluding yourself. The Fed will never allow that. Then if prices crash, unless you have a ton of cash you wont be able to get a loan or it might be too expensive, or if you waiting for the big crash, then eventually the banks will pay the final bill and your cash above the FDIC limit might get bailed in to save the banks. I know by experience that prices of real estate don’t come down with such low inventory as we have, so time will tell how it evolves, real estate is local, I am in the san diego area and here I dont see prices coming down, and rents are still going up, we have been operating with zero vacancy for years now.

What’s your cash/debt ratio?

When did I say I expect prices at 30 cents on the dollar? I expect prices to be anywhere from 90 to 70 cents at most on the dollar in the next correction. Looking at the CA migration trends, I’d be nervous to invest in the Bay Area, where prices have fallen YoY, despite lower mortgage rates, and continue to do so. I do believe San Diego has some room to run still. I hope you’re not over leveraged on all your multi-families.

Regardless, I don’t see a NIRP experiment from this fed, nor do I see another significant leg up in real estate this cycle. I also foresee long, long periods of stagnation as foreign investment continues to dry up, and millennials struggle to pay current prices.

4%? Lol. What if the blinds need to be cleaned? This post is how you can tell RE is insane and the average RE investor believes the Fed has his back.

Long live SoCalJimbo!

Someone tell the idiots at the Fed you don’t solve one bubble bursting by blowing another even bigger one!

They already did that Obviously they couldn’t care less about bubbles Back in 2006 Bernanke said he couldn’t see any problems in housing We all know they never tell the truth

Thanks for the news. Not a good time for me to make speculative purchases in real estate. Flips may flop. Marble countertops and hardwood floors will not pay the bills. The inflation adjusted price of a home is below the last peak, but above the long term average.

In most of America’s cities the choicest land for housing has already been built on. In some places the only way to build new housing is to bulldoze the existing house and build a new one on the lot. This creates an odd looking community with new McMansions sitting next to 1950’s tract homes.

Since most new home builders ( and buyers) prefer a more homogeneous community with modern amenities some form of ‘urban renewal’ should be made available where delapidated existing homes can be condemned and made available for new housing with the sale of the land used to build low cost housing in cheaper areas for those displaced.

There is no shortage of places to build houses in this country.

There is if you want to live near the CBD. The post war push into suburbia got the land closest to the CBD. Most of those houses are now obsolete. You can drive out from the CBD in most cities and tell the age of the homes based on their architecture. The further out you go the more recent the construction.

The real key is not interest rates, its income. We had strong housing markets when the rates were 2X and 3X the current rates. The medium income has fallen dramatically adjusted for inflation. Yes, at the very bottom and top end of the income band, there has been some very nice percentage increases. For example, a person is making $10/hr and get bumped to $15/hour. A nice 50% increase, but still not enough to have even a comfortable middle class life style. Likewise, with the top .01 percent of income earners. Problem there is that there just not that many of them and they will not be buying middle income homes.

I am in IT, and outside of a few major markets, IT rates/wages have fallen considerably, mostly based on offshoring and H1B visas. In the end, if the middle class income does not rise significantly for the middle and upper middle pay bands, we will not have a robust economy. Financial Asset prices may rise, but that will not confer prosperity on the middle class.

Exactly true and with the middle class continuing to be decimated and boomers downsizing it sure doesn’t portend well for the housing markets in many areas of the western world

“The real key is not interest rates, its income”

Oh really? Do a quick amortization on a 30 year fixed at 3.5% vs 6% and tell me interest rates don’t matter.

And can we please stop with the myth that the middle class is getting squeezed or decimated or whatever? Median household income is at the highest level ever, adjusted for inflation. Yes, you read that right…highest ever. Stop regurgitating nonsense you read on ZeroHedge and look at actual data.

https://fred.stlouisfed.org/series/MEHOINUSA672N

“I am in IT, and outside of a few major markets, IT rates/wages have fallen considerably”

Is that so??

“San Jose and San Francisco still remain the top spots on the site’s list of best-paying cities for techies in 2019, according to the business research organization. But the study reveals smaller metro areas — cities like Provo, Utah, and Omaha — are becoming mini tech hubs where tech workers can find salaries that are double, sometimes triple, the average salary of the state.”

https://www.washingtonpost.com/technology/2019/07/23/ever-wonder-how-much-tech-workers-get-paid-your-town-this-map-might-have-answer/

Absolute income is has nothing to do with the definition of middle class otherwise people on welfare would be middle class as they earn more money (and gave a better house, food, health care) than upper middle class had in 1850. Middle class has to do with your share of GDP

I read JSRG’s comment yesterday and then later in the day came across this article on the middle class in my newsfeed. https://www.fatherly.com/love-money/what-is-considered-middle-class-not-income/

The author describes a correlation to the “financialization of all things” with the middle-class squeeze.

I hadn’t realized that anyone denied the middle-class was struggling (isn’t that partly why Trump was elected? To bring back jobs and wealth to the middle class?).

A crypto currency startup in my town is offering $12HR for experienced programmers. I have seen $10HR offered for IT tech jobs as well. For this money you need experience, a car, a computer, a phone, and a good credit/social score.

Are you missing zeroes there? What experienced programmer would work for $12/HR? Unless your town is Bangalore …

Last group of programmers I hired in Bangalore I paid $4.33/hr.

Post the link. I call BS

Housing historically has been around 2.5x the median household income, so it should be around 168k, or so.

Howard Marks “pendulum” tends to swing way past the median in both directions.

We’ll see.

QUESTION: Does the Fed accepts re-used (rehypothecated) collateral in the repo ops.

The collateral is assumed to be “unencumbered” because if they don’t get their cash back they will sell it, encumbered or not.

They accept collateral from the GSEs, Fannie and Freddie, and that shizz is all subprime now with DTIs approaching 50% and down payments of 3%, with assistance.

As per Morningstar :

D R Horton’s (America’s Home Builder) 5 year revenue growth was 20.75% annually & net income growth was 25.84% annually.

It seems that everything has been firing on all cylinders for quite a number of years now. I hope nobody missed the boat.

akiddy111,

You’re posting industry propaganda again, for the clueless to swallow lock, stock, and barrel. Horton’s revenue this year is up 8.6% because of acquisitions. During the first quarter this year, Horton acquired Westport Homes, Classic Builders, and Terramor Homes.

The biggest homebuilders are now in acquisition mode to increase revenues, because the market is getting very tough to grow organically, but they’re paying dearly and borrowing a lot to acquire other homebuilders.

Horton is also keeping a lid on prices to keep volume up. Their numbers are okay, but nothing to get excited about. Virtually all of the builders would have been screaming at this point had mortgage rates stayed near 5 percent. That huge drop in rates this year saved their proverbial backsides, at least temporarily.

Here in DFW the 12-month moving average of median home prices peaked out in November 2017, then dropped to about $325,000 in April 2018. Median prices in America’s largest new home market have been virtually flat for the last year and half.

https://aaronlayman.com/2019/10/new-home-sales-still-riding-wave-of-lower-interest-rates/

What’s your call regarding long term interest rates? How will lower or continued low interest rates and negative interest rates affect home prices?

Revenue & income growth. That’s nice. How about their debt service growth?

“Feddie Mac”, that is one nice Freudian typo !!

Nothing predicts a recession like falling new house prices,

FRED data…

https://fred.stlouisfed.org/series/MSPUS

I don’t see that in the data.

When prices of identical units are dropping due to lack of demand, that’s a concern.

When sales mix is changing and builders are making record volumes, that’s not a problem.

Here’s the volume chart speaking volumes:

https://fred.stlouisfed.org/graph/fredgraph.png?g=lO6i

Lumber is going down a bit on the retail level, but every time I turn around some other material has been jacked up. Any reason for electrical metal conduit to be jacked up 30% in the last few years? I don’t think so.

If people are poorer, so they’re not hiring an electrician, and looking up on YouTube how to do it themselves, they might not not notice a 30% increase because they don’t have time in the game.

I bought a 3/4 inch plumbing plug today for about $1.75. Is that price too high? Kind of low? I dunno!

Anecdotal I know, but looking around in my area, seems like every house just went to pending this past week. Like literally last week there were maybe 30 houses for sale within a mile of me, today 20+ of those 30 are pending.

I don’t know what happened, but all of a sudden, houses are selling like they did in early summer.

This is in the $350-500K range, suburban setting, mid sized city.

Yes, same thing we are noticing in Campbell and San Jose. The homes are in contract after only 3-4 days of open house.

Lower prices and lower mortgage rates will do that.

I’m not seeing that in Cupertino/Sunnyvale/Mountain View. But I watch townhouses exclusively, we may be looking at different market segments.

And yet, I just read that Trump yelled at the Fed to LOWER ITS RATES A LOT

at their next meeting. WTF. I thought Powell was gonna run the Fed, not

Trump. Does Trump care more about getting re-elected than he does getting us back to normal rates, or is that a dumb question? He didn’t get us in this mess, but I’d like to see 5% for savers again in my lifetime and that’s lookin dimmer and dimmer. It could be worse, rates could go negative and then what will old duffers like me do?

this rates have nothing to do with Trump. The fed tried to normalize, and the markets convulsed. Forget about Dec 2018 already ????

They could barely do much to their balance sheet. All bets are off, in terms of higher rates any time soon. Its likely going to take a scenario, where the fed lowers rates to below zero, the dollar plummets, stocks and bonds crap substantially, and THEN we will see hyperinflation, and THEN you see rates go up like crazy. You’ll be broke by then, and your portfolios wiped out. But the Fed will be gone too, and rates wont ever be controlled by anything remotely called the ‘fed’.

“what will old duffers like me do”?

The same thing “old duffers” did in the 1930’s.

Prepare as best you can now Sir & may the force be with you.

How do you prepare for something like THAT (see above comment)

buy silver coins? I’ve paid off all my debts (including mortgage and cars) and have savings and portfolio to see me thru old age (I’m already 80) and now THIS. And I believe it will happen. People in my

position will die, with the collapse of the banks and the markets how

would we pay our utility bills? You don’t realize until you get there how truly debilitating old age is, you can no longer work.

JV, you get super defensive with 75%, or so in T-Bills & short term Treasury Note ETF’s like VGSH, SHV & maybe BIL.

To hedge against that you own 25% in Gold Bullion ETF’s like GLD, IAU & some silver bullion as well, like SLV ( I don’t own much Physical PM’s due to the fact I don’t want to be murdered) This is pretty much my Portfolio now except for some Gold Miner ETF’s which you should stay away from at your age & some British Tobacco Stocks BTI & IMBBY that maybe you should look at for the income because they’re relatively cheap right now (might get even cheaper soon though and possibly for a long time to come) I’m not talking my book here because this portfolio is super defensive and designed to preserve your wealth, but you asked “how do you prepare for THAT?” and I felt obliged to respond with how I plan to weather this coming economic storm.

You could follow some of the Prepper advice, as well, with regard to some freeze dried food and maybe some canned food that hopefully you won’t need and can donate when close to the expiration date.

It’s the unprepared who will suffer most, as always.

Trump doesn’t care about anything but his ego

But now, there is no crisis.

Sure there is. It’s just that they decided to skip the detonation this time and instead go for a conflagration that grinds down the population with a lot less drama. The Financial Industrial Complex is bailed out continuously now, so for the FIC there may be no crisis which is instead handed off to the victim class.

Doing it this way avoids all the usual noise about torches and pitchforks, reregulating the banksters, that sort of thing.

“Where’s the kaboom? There was supposed to be an Earth-shattering kaboom!”

The Fed made $16T available last time to bailout financial institutions. It would have cost far less to bailout households.

Now we have the repo bailouts. Which will transition to more QE (already announced, though it is forbidden to call it QE). Every penny constitutes financial sector bailout.

I’m guessing the political winds are a-changing. Which will turn us just as disastrously to the opposite direction: MMT.

The smear campaign against MMT by itself guarantees that you will never know if it could have saved you. It would have taken a great deal of power away from the banks, and obviously they were never going to let that happen.

Argentina has been doing MMT for many years, it just hasn’t called it that. Their central bank is part of the Ministry of Finance (though the IMF last year pushed the government to change that). And the central bank just creates the money that the rest of the Ministry of Finance disburses to pay for state expenses, such as salaries, subsidies, etc. So you can see what kind of job that this system is doing to the currency, inflation (ca. 40%), local-currency interest rates (ca. 50%), and to the economy.

So you can see what kind of job that this system is doing to the currency

Which only goes to show how any system can be screwed up when the controls have been disabled.

Conversely, it suggests that any system might be viable given the proper controls, but I doubt bank cartel hegemony might be one of them.

Argentina has been doing MMT for many years, it just hasn’t called it that.

I wouldn’t call it that either. But it should be given a name, something catchy that can still be used in polite company.

I’d suggest La Reforma.

I was looking at Zillow and noticed house prices dropped by 8 to 10 % in San Mateo and Santa Clara, SF Bay area counties. So the people who bought in the last year are now underwater. But I guess if you can buy a crap shack for 2 million dollars with all cash (all bitcoin) you really don’t give a darn. Or maybe all the failed IPOs this year had something to do with this.

Salaries are still high and layoffs almost nonexistent so all those people can still afford the price they agreed to when they purchased. Sale prices don’t matter to you until you want/need to sell your home.

If/when a recession occurs and layoffs start, that’s when the pain of being underwater will be felt.

Home and stock prices have left rationality. People are purchasing both in the hope that they will rise to the moon.

Unfortunately, many buyers have now realized that will not happen. Investments in both will not yield returns and will likely result in real losses of principal, because if their inflated values due to “Federal” Reserve manipulation.

We are where regular, constant manipulation by the “Federal” Reserve bankster cartel and corruption have taken us. It is curious to see the similar effects of and the corruption of the US banksters and of the Chinese communists “commies.”

Similarities:

1. Both give ultra-low interest rate loans to their cronies’ entities, many of which are insolvent: the U.S. bankster’s gigantic banks and the commies entities, including state owned.

2. Both give special treatment to their cronies, who are above the law: e.g., the banksters were not prosecuted for banking fraud and the commies protect their “princelings” who are children of communist party members or people who are themselves communist party members.

3. Both sets of crooks are in deep trouble: the banksters’ banks apparently cannot get rid of overvalued real estate, which reportedly they have held since 2008 in many cases on which borrowers have defaulted; the commies have all of these state owned and commie owned entities that are over leveraged and unable to pay their loans, which cannot be dissolved due to the connections of their owners.

4. Both banksters and commies are essentially parasites who profit by frauds on regular citizens of their countries.

5. Both banksters and commies are terrified that the next collapse may see them deprived of power.

6. Both manipulate the media and attempt to censor and do their best to take it over. (Post a message critical of the banksters in certain media outlets and it will be taken down rapidly. I need not go into commie censorship here, which would take hours.)

7. Both are connected to organized crime organizations: the commies to the Chinese triads and reportedly, the banksters to the secret, successor organization to what Meyer Lansky reportedly ran. See https://themobmuseum.org/notable_names/meyer-lansky/ and see https://en.wikipedia.org/wiki/Meyer_Lansky. See https://www.nytimes.com/2012/08/26/opinion/sunday/where-the-mob-keeps-its-money.html. See also https://www.bankinfosecurity.com/interviews/how-organized-crime-uses-banks-i-1408 and https://www.rollingstone.com/politics/politics-news/the-scam-wall-street-learned-from-the-mafia-190232/. See https://www.theguardian.com/world/2017/mar/21/deutsche-bank-that-lent-300m-to-trump-linked-to-russian-money-laundering-scam.

8. Both control politicians (and thereby regulators/law enforcment authorities) in their respective country to their personal profit. See Simon Johnson’s article in the Atlantic magazine called “The Quiet Coup,” which is based on his knowledge of US affairs from his IMF experience. The IMF monitors corruption, because it has severe economic effects on countries, hurting them, of course. As to the commies too many articles exist to cite here.

9. Both have connections to the US and EU.

10 Both resort to threats or violence against persons that mention this arrangement or their corruption, while claiming that others are corrupt.

11. Reportedly, they are allied, so the banksters enabled the unrestricted commie tactic of taking over American (and EU) manufacturing by preventing U.S. action against companies moving and/or setting up factories, etc., to ship goods to the US and other countries.

“Home and stock prices have left rationality. People are purchasing both in the hope that they will rise to the moon.”

Or….they’re buying because they want a place to live. Crazy idea, right?

Purchasing RE to have a place to live is the ideal. Sadly, the problem is that too many of their RE purchases may be so overvalued and the loan terms (e.g., with adjustable rises in interest rates) so onerous that the borrowers will ultimately not complete their loan payments and will not be able to resell that RE for the same price.

E.g., supposedly, the millenial generation should be moving up to purchase higher value real estate from baby boomers wishing to move to smaller, post-retirement houses for smaller familes (after children left the nest) or to realize apparent appreciations in their RE value. However, millenials apparently cannot even qualify to buy a home, much less a mini-mansion, such as many baby boomers acquired at lower prices many years ago. See https://www.theatlantic.com/technology/archive/2019/06/why-millennials-cant-afford-buy-house/591532/

Also, I know of people who walked away from real estate, because the real estate’s value declined, so they became “underwater:” e.g., (numbers are fictitious) would you struggle to scrimp and save to pay $5000 a month on a $1,100,000 loan secured by a house (including land) which had a total FMV reduced to $600,000? If the value of the house was not going to bounce back up soon, would it not make more sense to realize the huge loss and in many cases, abandon the loan?

In California now, the lenders cannot sue for the deficit (loan principal less realized price at the foreclosure sale), not even if the borrowers refinanced their loan, which deficiency in that example (because foreclosure sales net much less than the normal FMV of a piece of RE) might be $700,000. What would you do then in that borrower’s shoes?

What will banks do if this happens to 10,000 loans? That is the problem with the RE bubble. If RE prices in enough markets continue going down substantially, will we again be in a 2008 collapse? If we are, I strongly recommend that when the US government again bails out the banks, and gets convertible securities, that it convert the loans into securities, or otherwise aquire all of the banks’ stocks and keep them permanently in the social security fund or some similar agency.

Other countries have sovereign wealth funds. An independently managed, sovereign wealth fund holding all major banks stocks (run more conservatively than the banksters currently run our banks and independent so protected from our crooked politicians and much more corrupt banksters) might be the only way to ensure that millenials and my children get significant amounts from social security when it comes time for them to retire.

As of now, given demographics, social security and government programs are really unsustainable Ponzi schemes in which the poor millenials will be left with nothing, because the government cannot ultimately meet its (per Forbes) $124 trillion in liabilities. See https://www.forbes.com/sites/timworstall/2017/04/04/sure-social-securitys-a-ponzi-scheme-but-is-it-a-sustainable-one-or-not/#6c8165c33ab6. See https://www.usmoneyreserve.com/video-library/videos/unfunded-liabilities-americas-breaking-point/. See https://www.forbes.com/sites/johnmauldin/2017/10/10/your-pension-is-a-lie-theres-210-trillion-of-liabilities-our-government-cant-fulfill/#2bc2933a65b1.

I take the time to write about this, because I hope that Americans may slowly come to realize that the problems created by the banksters and their corrupt politicians do have solutions. However, those solutions can only be implemented over the banksters’ desperate opposition. E.g., I love Elizabeth Warren, but I strongly suspect that the banksters and the most corrupt among the rich will fight tooth and nail against her election, so they can keep/elect some crook in power that will not force them to pay taxes (with a reasonable property tax), so they can keep evading taxes forever. See https://www.moneytips.com/how-the-mega-rich-avoid-paying-taxes

Social Security is easily funded by any of a number of ways, one of them being taking the “cap” off so the Richie Riches pay the same rate into it as their minimum-wage gardeners do. Or cutting back on military spending just a smidge.

Who defines ” reasonable”.

I have a reasonable amount in mind for my house.

You mean there’s room in the 650+ Billion dollar defense budget for cuts??? It’s almost like if the government throws enough money at something, it will be this gigantic great best-in-the-world achievement. So, hows about we spend a little more on education, social security, and health care????

Small town NC. Been watching new construction near me. Small 1500 sq ft 3BR, 2Bath, 2 car garage vinyl siding, nicely finished inside about $220K in small 30 unit development. In city, taxes $3000.

In Seattle and surrounding areas, the new homes are selling at a 10-30% premium to the existing homes, based on price per square foot. Maybe that’s why builders are dropping the prices. Based on what I’m seeing, they need to drop them a lot more to be competitive with existing houses.

I have been all over the country and (except for the rural SE) have never seen a housing stock as decrepit as Seattle’s. I have never been in a house in Seattle house that didn’t stink of mold – that moisture always seeps in and those old dumps rot. Congratulations to all the new Seattle home buyers – but now you have to like in it. Yuck, I’m much more comfortable living in a van.

Van, you ought to go to the Gulf Coast… talk about mold. It vies with the Olympic Peninsula for sure.

I often watch the YT Channel Cheap RV Living and wonder whether you Folks living in Vans and converted Cargo Trailers maybe don’t have it figured out.

Van down by the river, I am the same! So not willing to pay 300k for a home. There’s a reason the word mortgage means death contract.

Due to the gigantic size of the largest banks, they each now represent a risk to our economy: if they fail, their counter parties may become insolvent and the stock market and also the economy might take a nose dive.

What I do not understand is how US major banks have such high alleged real estate exposure, so that any reductions in the price of real estate are threatening to them, while allegedly having sufficient capital ratios. See https://www.frbsf.org/economic-research/publications/economic-letter/2019/april/banks-real-estate-exposure-and-resilience/. See https://therealdeal.com/2017/11/06/banks-are-far-more-exposed-to-risky-real-estate-loans-than-you-think-thanks-to-this-loophole/:

“But below the surface, banks are far more exposed to risky real estate loans than commonly thought thanks to a skyscraper-sized loophole: Instead of lending to construction projects directly, they increasingly lend to debt funds and mortgage trusts managed by private equity firms, which in turn lend to developers.”

See https://www.fool.com/knowledge-center/what-is-the-tier-1-capital-ratio.aspx. I understand that major banks also often have direct loans that are in default, which they work to avoid declaring in default (e.g., by modifying their terms, while not reducing their principal which may be less then the loans’ net, realizable amount), while not recognizing that the value of their security and thereby of their mortgage has declined in their balance sheet.

This is very important, because major banks may thus become legally insolvent if they hold “assets” (loans owed to them) that truly are not worth what is shown on their books, while their debts are shown at their true value or (in the case of derivatives and other contingent liabilities) actually understated. The “Federal” Reserve’s recent decision may indicate that reported capital ratios have already declined. See https://www.reuters.com/article/us-usa-fed-banks/fed-eases-post-crisis-rules-for-domestic-foreign-banks-idUSKBN1WP2OU.

Thus, many banks may be on the way to becoming insolvent, as real estate prices decline, even if some are not yet insolvent. However, the reported statistics claim that the banks’ current share of non-performing loans is minor. See https://www.ceicdata.com/en/indicator/united-states/non-performing-loans-ratio. If you trust the “Fed” the banks supposedly made provisions for these anticipated losses. See https://fred.stlouisfed.org/series/LLRNPT.

Based solely on what I have been told, I am skeptical. Also, I must point out that if bank insiders are trading bank stock (which I predict that they are), and not disclosing known problems with bank finances, they are violating a securities rule, Rule 10b(5), which I am sure that the SEC (which must be the most incompetent or most corrupt government agency ever) will not prosecute.

Wolf, can reported bank capital ratios (and nonperforming loan percentages reported) be reconciled with claims that banks hold more (direct or indirect) RE loans that should be in default and will likely be harmed if real estate prices declined thereby (because more underwater borrowers may then stay in the properties until kicked out after foreclosure and walk away from the properties, and properties sold at foreclosure sales may sell for 50% to 80% of what would otherwise be their FMV)?

Is the “Federal” Reserve banking cartel manipulating markets with happy talk, so that these dangers do not become patent and obvious?

I nailed the re-fi. Got my mortgage re-fi’d at the lowest point on that chart. I even took out some extra money at the time, which has been needed. Never did that before. Hopefully wont need to again. Now if we go NIRP here in the US, then maybe banks will pay me. I sure thought at the time, rates would be way higher than they are right now. The US financial system is clearly in trouble. and we aren’t even in a depression yet.

Could it be that during the unaffordable times, potential buyers got used to renting & accustomed to having a lot more disposable income, which translates to a less stressed lifestyle ??

It is hard to give up a comfort that one has grown accustomed to.

Also, don’t investors get tired of the same old, same old, & go looking for a more “deregulated” atmosphere with what might seem to offer a bit more of anything, an away from the maddening crowed escape.

Renting can be stressful as well if you can’t come up with your rent or you have a terrible landlord Trust me tenants can be bad news as well I’m a landlord and it’s not always easy

One of the biggest downsides to renting is getting booted out because the owners decides to sell, or the owner dies & the heirs sell.

Renting still makes a lot of sense for some Folks though. You just have to be wary of what I call a “placeholder property”.

In the DC area the slowdown is very apparent. Prices in newly gentrifying areas like Anacostia have been dropping around 10-20%. Even in the city itself, prices stopped rising over a year ago and are now slowly declining. My RE agent said the market has been “awful” in the last year. And this is despite Amazon coming to town.

The insanity of owning a house as your main asset you may also live in is astonishing. I am not discussing here real estate investment firms.

On a free market the real value of an asset is dictated by supply and demand. Demographics in the US are in free fall and will be for at least 2 decades, and real incomes have been stagnant while assets have been appreciating at multiples of the (fake) official inflation. So supply will be going up while demand is going down. Why participate in this mania as a private single asset owner is a mystery, unless you consider the strong ‘homeownership’ propaganda, which makes money to.. someone else.

Suburb of large southern city here. Looking to buy and watch listings constantly. No slow down in sales of existing homes – market is still hot. But price increases have moderated in the past year to a more reasonable 2-5% vs 5-10% annually. New homes are relatively scarce as the area is mostly built out. Prices for those new homes have been absurdly high compared to existing, at least 20-40% higher for less house, and I do see those prices coming down some finally. IMO that’s healthy and rational more than a sign of impending doom.