Sales at the Top are strong. Bottom falls out in rest of market. “Rising interest rates and higher home prices depressed housing demand.”

By Wolf Richter for WOLF STREET.

Sales in the US of previously-owned homes – houses, condos, and townhouses – fell by 2.4% in April from March, based on the seasonally adjusted annual rate of sales, and were down 5.9% from a year ago, with a much steeper decline in condo sales (-13.9% year-over-year), than in house sales (-4.8% year-over-year), the National Association of Realtors reported today.

It was the ninth month in a row of year-over-year declines, even as supply of homes listed for sale continued to rise (data via YCharts):

“Higher home prices and sharply higher mortgage rates have reduced buyer activity,” the NAR’s report said. “It looks like more declines are imminent in the upcoming months.”

The seasonally adjusted annual rate of sales, at 5.61 million, was the lowest since June 2020 (data via YCharts):

Sales of single-family houses dropped by 2.5% in April from March, seasonally adjusted, and by 4.8% year-over-year, to a seasonally adjusted annual rate of 4.99 million houses, the lowest since June 2020.

Sales of condos dropped 1.6% in April from March, seasonally adjusted, and by 13.9% year-over-year to a seasonally adjusted annual rate of 620,000 condos, the lowest since July 2020.

By Region, the percent change of the seasonally adjusted annual rate of total home sales in April from March, and year-over-year (yoy):

- Northeast: +15% from March, -10.7% yoy.

- Midwest: -3.1% from March, -1.5% yoy.

- South: -4.6% from March, -5.7% yoy.

- West: -5.8% from March, -8.1% yoy.

In California, sales plunged, except at the top.

According to a separate report by the California Association of Realtors (CAR), sales volume of houses dropped 8.5% in April year-over-year; and sales of condos plunged 20%, “as rising interest rates and higher home prices depressed housing demand,” the CAR said.

Sales in the coastal metros of California plunged by the most, and this is where prices have long entered the astronomical zone. Something serious is going on there:

In the Los Angeles metro, which includes San Diego:

- Sales of houses: -16.8%

- Sales of condos: -22.4%.

In the San Francisco Bay Area:

- Sales of houses -18.1%

- Sales of condos: -13.8%

Central Coast:

- Sales of houses: -21.3%

- Sales of condos: -22.4%

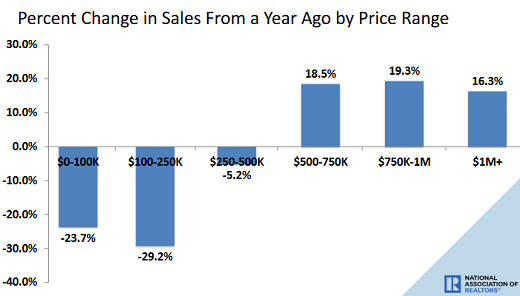

California’s median price was skewed by a change in the mix, with strong sales at the top and weak sales in the rest of the market, which changes the mix of homes sold. Median prices are very sensitive to changes in the mix. The CAR pointed this out: The median price (+8.7% year-over-year) rose “primarily due to strong sales at the top end of the market.”

And the CAR added:

“A change in the mix of sales continues to play a role in statewide record-setting home prices as sales in high-priced markets remain stronger than their more affordable counterparts.

“The share of million-dollar home sales increased for the third consecutive month, reaching the highest level on record at 34.7 percent. Home sales priced below $500,000, meanwhile, dipped again in April and hit the lowest level ever.

“Sales dropped by double-digits for price segments $750,000 and below, while sales above $2 million remained on the rise on a year-over-year basis.

“The shift in the mix of sales toward high-end homes is expected to persist in the upcoming months.”

Sales volume hit by Holy-Moly Mortgage rates and mega-prices.

The average 30-year fixed mortgage rate this week (with conforming balances and 20% down) at 5.49% was about 2.2 percentage points higher than a year ago, according to data from the Mortgage Bankers Association. The last two weeks were the highest since 2009

But we haven’t seen anything yet. The sales figures today are based on sales that largely closed in April, and were negotiated in March, with mortgage rates from January through March, when these buyers applied for mortgages and obtained guaranteed mortgage rates (rate locks) that are good for a period of time, such as three months, to buy a home with. The green box shows the mortgage rates that applied to purchases that closed in April, roughly in the range from 3.2% to 4.8% (rate data via Investing.com):

The plunge in applications for mortgages to purchase a home indicates that over the next few months, sales volume will decline further. In the latest reporting week, purchase mortgage applications were down 15% from a year ago, and were back at the low points in late 2018 when the housing market started to crack under QT and rising interest rates (with mortgage rates just above 5% in November 2018).

At the time, inflation was below the Fed’s target, and the Fed pivoted in December 2018. But that pivot isn’t going to happen this time, with raging inflation being the biggest economic problem in the US – and the Fed has barely started to raise rates and won’t start QT until June.

Inventory for sale and supply rise.

The number of homes listed for sale in the US jumped by 100,000 homes to 1.03 million in April, the first time over 1 million since October.

Supply of homes listed for sale in the US rose to 2.2 months, from the low in January of 1.6 months (data via YCharts).

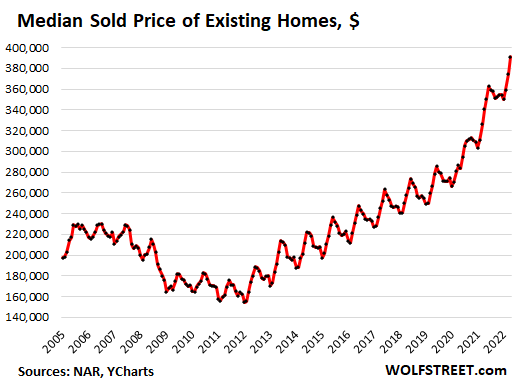

US Median Price pushed up by top-end sales. Bottom fell out below $500K.

In the US, the bottom has fallen out with homes selling for less than $500,000. But sales are strong at the high end, just as in California, which changes the mix, which skews the median price (= the middle price, with 50% of homes selling for more, and 50% selling for less). Image from the NAR:

The median price in the US rose by 14.8% from a year ago, to $391,200 in part due to the shift in the mix, with sales at the top end surging. The year-over-year spikes peaked last May and June 2021 at over 23% (data via YCharts):

Investor share of sales and all-cash sales dipped, stayed in the same range.

Individual investors or second-home buyers, who make up many cash sales, according to the NAR, purchased 17% of the homes in April, down from 18% in March and from 19% in February and from 22% in January, but same as in April 2021 (17%).

“All-cash” sales fell to 26% of total sales in April, from 28% in March, and were up from 25% in April 2021.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I’m curious where San Diego sits exclusive of the Los Angeles numbers. Strange things are happening here indeed, though.

I recall that the last crash had peak sales around 2005 abs peak price around 2006 because people didn’t realize the party had ended and kept buying.

San Diego has interesting upzoning issues going on right now that are quite a bit different than the rest of the state, which is driving up land costs like crazy.

Regardless, this can’t continue as too many purchasers have been eliminated from the pool including both first time buyers and investors.

I watch this closely in SD. Top end is still setting records, despite what should be happening. For example, in Cardiff, a 2020 build with an ask price at $5.5m got 8 bids. It closed at $6.75m. Note that, with one incomparable exception on the bluff, the record price in Cardiff had been $5.0m, the next one below that $4.7m. So was this $6.75 place that spectacular? Yeah, looks nice, but there are MANY homes around that area of similar quality….they just aren’t listed for sale.

This is SAN DIEGO, not Newport. Sad to see this formerly somewhat anachronistic and affordable area become crazy$$$.

Lots of recent new money coming from the younger social media class with stupid buying practices, stupid money to spend, and no experience of any kind. Jury still out as to whether they are able to keep the advertising income streams sustainable.

Did my 8 years in San Diego (’75-’83’) and even then it seemed all people talked about was real estate. I remember reading (some time back in 79′-80′) that San Diego was the 1st city where the average home price was $100k – the highest in the nation.

So none of this is surprising.

Austin was anachronistic and very affordable when I moved there in 1980. Sounds like it’s meant for other types now. Cheap and always something to do or music to go to, gone forever i suppose. I remember San Diego as kinda easygoing and pleasant fifty years ago. It was always the first stop in the States every other summer.

I am in San Diego and own two homes. Home prices would never go down here because we are special ( as you listed one reason: zoning issue ) and this time is different. :-)

Oh you are special alright, just not sure it’s in a good way if your statement is not sarcastic in nature..

Been two ‘short term’ dips in San Diego in the last 30 years which were Good Buying Opportunities. Dipped in 91 and didn’t recover until 97 then went up like crazy until 07 when it dipped again and seemed to recover in 3 or 4 years. It has risen steeply since. I expect another dip but long term the trend is up. I’ve been here long enough that I bought my home for 50 cents and a Ham sandwich according to most Z-Gen’ers.

San Diego County, sales, yoy

Houses: -12.6%

Condos: -24.9%

This is in line with what we’re seeing here, but I would attribute it mostly due to the lack of inventory, especially on the house side. Look at any zip in the city and you’ll find barely 10-20 active sfr listings. Folks who’ve been there a while will stay because of prop 13. Folks who bought at 2.5-4% loan rate are probably gonna stay. Also, if a house is what you want and you already have a house, best to stay as there aren’t hardly any worth while one’s coming up, unless you don’t mind spending 1.5 mil plus.

This is going to be interesting to watch over the next few years.

Been in SD almost 40 years. Place is completely disfunctional now as a community, and the only thing that can save it is a big price correction. I think that will happen. The funny money is going away. That could do it on its own. If the kool aid supply diminishes even slightly, then the correction will happen rapidly.

Prop 13 still allows residents to move within CA (to most counties) and carry their tax base with them. Sort of, with limits. So I don’t think it’s quite the anchor many believe it to be. The bigger drag is the cap gains tax + commission. That is pure loss, money gone when you sell. For the older folks, it’s better to leave it to your kids tax-free.

Apple and a few other major techs are opening big centers in SD, bringing in lots of high paid people with stock options, lots of dual earners. I don’t see pricing going down in any decent areas of SD with an ever increasing rich population. Sales decline is lack of inventory more than anything else.

The trick will be vacation rentals and secondary investment homes. There are lots of empty homes in San Diego that were bought on the way up as investments.

Remain to be seen how that situation will end up as prices stop rising and no property makes sense in SD based on sub 2% cap rates.

Why put money at 2% cap rates in a property if prices stop rising when you can buy a 10 year bond at 3% without any tenant or vacation rental headaches?

San Francisco active listings now at 11-year high for this time of the year. So yes, suddenly the inventory comes out of the woodwork.

This is happening pretty fast.

Supply is low… until it’s not?

Apple is trying to compete with Qualcomm in San Diego. I interviewed and was asked if I was willing to relocate to the Bay Area for more opportunities. The tech job market is still not great in SD relative to cost of living.

My bro and his wife are buying a peculiar but pretty SFH converted to duplex with his son & daughter in law…..in El Cajon (20 min from SD) for just under $1M (2+ acres, nice views).

They said San Diego proper is la la land but the son in law is a lawyer and has to be near SD. All 4 of them will be spending a good chunk of their income / pension $$$ to make this happen. Both ladies are real estate agents and they understand they are buying at a crazy point in the market, but they are all telling themselves it is the forever home and valuations be damned in the future.

I kinda like the fact they are going multi-gen wit their home….return to family values, but debt slaves for sure. That part worries me.

They were each paying over $3K / Mo for their respective 2BR apartments, so I guess this is just a lesser of two evils.

What exactly is different about San Diego’s zoning laws vs. the rest of CA? All I know is that my Mum said if I ever want to return, I could now build something in their backyard. I picture her street lined with cars.

Bonus program for ADU’s. Build an “affordable” one and get a bonus market rate one. The code specifically says the amount you can build is unlimited. The only limiting factor is the floor area ratio. But at a minimum of 150 square feet to be legal that’s a lot of units.

This is just the city of San Diego not the county

City of SD has some really generous ADU laws. Basically, you can jam stuff into all the open space. That is not the case in other SD towns and CA in general. In those places you have SB9 allowing subdivisions by right (with some limits) and a single ADU by right.

Remember when real estate was cyclical?

Yeah just like the economy is suppose to have recession from time to time as a nature cycle..

I think the FED has retired that Dodo bird long time ago and maybe they are thinking about resurrecting it through some Jurassic park DNA experiment but so far has been pretty tardy to the party

Given the fact that millions have refinanced to much lower rates, it won’t make sense to them to sell and move given the cost of selling and much higher rates.

Could this keep inventory low for years to come? It seems it could unless massive unemployment or other events force owners to sell.

In “normal” times, about 7% of all homes go on the market for all sorts of normal things.

Like job changes, growing family, deaths, divorce, etc. In normal times, they sell because it makes no sense for the holding costs.

The problem with housing bubbles is that folks hold on to unneeded housing cause of crazy appreciation of sweet equity outpacing holding costs.

Now they will hold on for 3% mortgage. And will pass on 3% mortgage to their kids.

Depends on the length and depth of the recession. An early 1980s level recession would be a game changer.

People usually don’t want to sell homes but they are forced to. and These homes decide the prices, fixed at the margins.

Agree. There is housing bubble and a bigger asset mania in place now and for years.

There will be a lot of involuntary selling later.

Yeah just like stocks shouldn’t go down because over the long run they will go up. Or bond etf prices should not fluctuate because you could just hold and make the interest. Or bitcoin should always go up because it’s not a fiat currency.

Then there is the price of stuff, decided by supply and demand. During the pandemic lots of demand for houses because wfh and low interest rates, not a lot of supply. Prices went up sky high except Bay Area which lost demand. Now less demand because financing is going up dramatically. Not hard to figure out what happens to price.

You will still have the 3 D’s of Real Estate:

Death

Divorce

Default

The areas I’m watching in SD have had inventory 4x in the last 4 months, but it’s still half of what it was pre-pandemic. The inventory numbers have been growing pretty steadily since February.

There is a lot of tech coming to SD, but something to keep in mind is that a large part of your compensation at a tech company is tied to the stock price of said company. As the stock prices go down for these tech giants their employees liquidity and their compensation go down.

That being said I am still seeing some spectacular up bidding in the $1.4 mil and up price range. These homes have doubled in value over the last 2-3 years, And there are only mild signs of slowing down, where as everything below the 1.4 mil has been significantly slowing down.

Maybe not the beginning of the end…

But, maybe, the end of the beginning.

Considering that the interest rates hikes (clearly and utterly the trigger and fuel for all the falling numbers) only started perhaps 2 months ago…this is barely the dawn of the beginning.

One small saving grace, the volume of suckers/speculators in House Bubble 2.0 was only perhaps 50% that in Bubble 1.0 – (some) people learned and refused to be taken in.

The very speed with which declines are occurring (see condos) is a massive indicator that a *lot* of owners knew just how vulnerable they were to Fed policy but wanted to ride the lightning anyway.

But don’t be alarmed. Real estate after real estate guru from Zillion, Redfin, Opendoor & most importantly the REEA have been telling us for two years that “this time it’s different.” There’s no way housing can collapse. We’ve got a lot better lending standards and underwriting. Well, guess what, subprime mortgages only made up 12% of loans back in 2007 just before the collapse. Never mind the grossly over inflated home values and all of those 90% cash out refi’s over the last two years. Oh NO! That’s a totally different situation. Everyone can afford their house with debt to income at 40%.

The problem is that folks who bought anything these past few years got a very good price at potentially a very good rate. Combine that with sky high rental prices and they really don’t have a incentive to sell, regardless of what the price does( and right now the price is only going up).

The reality is, for most, selling would be a dumb idea. In a high inflation environment, where can they put their money to preserve wealth? Government bonds, the stock market? Many, including myself, would rather rent the property and receive a decent return + appreciation value. Even if they could time to “top” price wise, the question becomes where they put their money post sale that would safely preserve wealth.

I agree that this has barely begun to unfold, but I think there could be as much or maybe even more speculation than last time, at least in so cal. Actually, the details don’t matter. Once a bubble forms it’s all about herd psychology. My sense is that the herd realizes something is changing.

And…coming soon.

The implosion of “tech” stocks and the resulting less crazy stock option monies for housing.

Look at Nasdaq 100 or Russell 2000 since November – already significant cratering.

But 2021’s idiot bubble stacked overvaluation on top of overvaluation.

Pre-pandemic, the SP 500 was already overvalued by 40% (post-pandemic, likely 50% or more). And the SP 500 is much less tech heavy than something like the NASDAQ 100.

It’s even worse.

The 40% overvaluation you are using is based upon inflated earnings from fake “growth”.

For anyone who is interested, pull up a list of the Fortune 500 decades ago. One site I found has data from 1955-2005.

Some of the increase is due to population growth, globalization and (maybe) increased efficiency but most of it is credit expansion and financialization.

The country and the world aren’t that much wealthier.

Not just tech, but every industry outside of energy is getting smashed. Layoffs are going to be coming from every direction and plenty will sell their homes and take jobs elsewhere or just retire

What we have seen speaks for itself. Time to panic. This is Kent Brockman reporting.

I think the international influence on the West Coast makes RE prices hard to predict. I did a search on home sales in my neighborhood for the past three years, and 100% (yes, 100%) were purchased by persons with Asian or Eastern European cultural names. Granted, some of these folks may have been in the country a long time and may be citizens.

In any case, it’s clear the Coasts are a different type of market that attracts international demand. I can’t tell if the money comes from foreign earned income or US earned income, but a lot of these folks likely have tech jobs and stock option compensation, and they may have different perspectives on RE investment. Does the connection to stock compensation make these markets susceptible to quick price drops? I don’t know, but I’m thinking about big tech stock price drops of late, especially Amazon, Facebook, and Google. More pain could be on the way, given the meteoric RE price rises these company’s encouraged.

I can show you recent home sales that reflect a 100% gain in two years in some hot areas, largely because of Big Tech job growth. I imagine such prices could go down just as fast in the right circumstances, without any concerns expressed by the Fed.

China at minimum has its own massive debt and real estate mania.

it’s not going to end well there either. Already signs of the housing mania there cracking according to the reports I have read.

I’ve heard the Chinese government wants to lower home prices in China to increase the birth rate.

Food for thought: apparently Chinese apparatchiks are being told to divest Western assets, including real estate.

WSJ:

“China Insists Party Elites Shed Overseas Assets, Eyeing Western Sanctions on Russia”

The Chinese would be the highest end buyers so that could be the reason for the highest end of the market not falling. In Canada all the Chinese bought cities are already cratering as most of the Chinese are completely leveraged all in on real estate and then some.

This is a classic stagflation in the real estate. Volumes stay flat or drop while prices stay flat or rise continuously, may be slowly but steadily. The trend will continue because construction cost, materials cost, labor cost, permits, fees, etc. are all growing substantially. This cost will be passed on to the buyers, just like PPI feeds into CPI.

This sounds really bad for most non tech people in Bay Area, even tech single earning families will struggle.

“This cost will be passed on to the buyers”

What buyers! they are already dropping out of the Market and rates are not even finished climbing and stuck market no where near a bottom. By the time this is over no buyers will be left. Doesn’t matter how much it cost to build a house if no one can afford it.

House prices are not set by construction costs.

When demand for houses drops, and prices fall, construction stops. Houses keep selling below construction cost.

Example: Detroit 2008-2010. Phoenix and Vegas have also had crashes. In all of them, at the bottoms you could buy houses with a credit card if you were brave.

Ridiculous. Buyers have to be able to buy. This is changing in enormous ways right now, and there is no indication that the trend will stop any time soon. RE is a slow, backward looking market. Just consider the appraisal process. Prices will respond anyway, since transactions need buyers. Once prices head south, things will really start changing.

Or, every other house will have a ‘for sale’ sign on. It’s almost like I’ve seen this before.

If prices are to stay the volume have to drop a lot. Anecdotal from a property market far from the USA, I did just sell. I am quite sure the price is flat from last year as there are many similar flats around and there are a few on the market every year that make it easy to trace the price. The number of houses on the market seem to decline.

Another thing that is very pronounced here as a lot of people do not move far geographically. Young people buy their parents or grandparents house off market as they move to something smaller and easier to keep. No real price discovery then as there is a question about tax too.

Its the last push of buyers that get wrecked, pulling down the rest of the market like a slinky.

Poetically stated.

And what’s the deal with “Arrived Homes”? Would love to hear Wolf’s take on this.

Got in my email a press release yesterday from a similar company — “Appreciate” as in house prices appreciate — announcing their deal to merge with a SPAC. They’re wanting me to promo it, hahahaha. Lots of startups out there wanting to lure investors in with the promise of investing in the red-hot SFR boom through some other way rather than the hard way. There will be lots of blood in the streets, and even then, those companies won’t be worth buying.

Re San Diego

The first signs of a change in the appreciation trajectory are appearing as some inferior properties are not getting bid up, and in fact are not selling at list but instead have reduced price. Interestingly, when there are price reductions they have been swift and steep, which is good advice from the realtor.

When the self-satisfaction of genius owners becomes too much to bear, it’s usually a sign of an impending humbling of these people. At least that’s true in my unscientific opinion. The Smug-o-Meter needle has already reached the red zone, so i feel San Diego prices are in the peak zone.

Many San Diegans (typically transplants) have a superiority complex because “everyone wants to live here”. They couldn’t be more wrong. San Diego suffered in ’90-’95, got body-slammed in ’07-’11, and is nowhere near immune from the upcoming downturn, and the one after that, and so on.

I was in SD from 89 to 06, called the top in RE in 04 and sold my place in Cardiff for 3.5x what I paid for in 96. One of the clues that led me to think the top was in was a big build in inventory in rancho Santa Fe in late 03. Has anyone seen that yet? By the time of the first rate hike in spring of 04 my hood had topped on a price per square foot basis. By fall inventory had jumped 5x, but bidding was still nuts in summer 05 in places like north Park.

When I look at what prices are at now on Zillow, it blows my mind. Absolutely junk areas want 750k and up. I moved to another state in 06 and it was one of the best things I ever did. SD was a magical place up until about 98, then it started getting lame with the dot com scam.

RSF was a fascinating case. Peaked early, 2003 or so as you said, maybe even earlier. Realtors bitched about how hard it was to sell a house all the way up until Covid, which is when prices finally recovered. 17 years. Crazy. Now the # of listings is about 1/5th of that ’03-’19 era.

One change there is that most everything built pre-’03 was junk. Big, and sometimes truly giant, but trendy over the top Mediterranean (or ranch) junk. Hard to sell. Many of those homes are getting torn down now. What has been built in the last 3-5 years has mostly been extremely high end, high quality, many $10m+. Totally different.

In 2007-2008, my friends told me that real estate in San Diego can never go down and they laid out the facts ( which are kind of truth). They were:

1. weather is awesome which is true.

2. Everyone wants to live here: Tue. A lot of rich people have second/third home here.

3. Lots of golf courses here. I know it sounds weird.

4. People are usually rich inn San Diego. ==> kind of true. Teslas as dime a dozen here.

5. You can’t create land anymore and san diego is locked between ocean and desert.

we all know what happened afterwards

Same here, have a old co worker that bought recently paying over asking in SD. When asked, the general assumption is that price will just level off. Somehow the irrational exuberance is always normals but a price reverse just as fast and just as violent is never possible. The disconnect is simply amazing, especially when you don’t have to look that far back to what the stock market did back in March 2020. This level of logic reasoning is something I would expect from my 5 yr old but not what I would expect from people in their 40s..but then again this is Murica after all..

Perhaps it’s still an evolution gap in human, but the level of emotionally driven FOMO, mix with hot hand fallacy and keeping up with the jones are a perfect toxic cocktail to get people in trouble and probably end up dooming us all..

No, it’s not due to evolution. It’s cognitive dissonance in unchanging human nature.

People don’t believe it due to linear thinking, ignorance of history, and the implied outcome is contrary to their personal preference.

No one wants to believe they are destined to become poorer or a lot poorer and their life could fall apart or turned “upside down”. I see similar sentiments on this blog, all the time. It’s obvious the country has experienced decades of extensive social and economic decay, but apparently that doesn’t make any difference.

After all, this is America and somehow someway, the country and population are exempt from reality which applies to everyone else, now and in the past. The country has a birthright to minimum perpetually increasing living standards.

Left SD in 2019 and will never look back. Everyone does not want to live there. It is massively overcrowded, has a huge homeless problem, People are basically aholes and idiots, about as rude and intolerant as they can be. Traffic is horrendous, the overall quality of life has deteriorated to the point where everyone is trying to live a narrative of what CA used to be, but has not been for decades. Ridiculous utility bills, forced blackouts whenever the wind blows, water rationing, threatening firestorms every year. On top of everything else, the entire State is a lost cause, and will never even begin to turn itself around in my lifetime. All of its current problems will continue to get worse for the foreseeable future as its incompetent collective governments will continue to sacrifice the good of the citizens to promote their idiotic political agendas.

Totally correct. Been in SD almost 40 years. Leaving soon.

California has a huge budget surplus now due to the asset mania which it can temporarily use to partially paper over it’s awful long-term fundamentals.

If the bond mania from 1981 is over, so is the stock mania though there has been a divergence up to January.

The end of the asset mania means the end of California’s bubble economy.

The state will soon be broke again, just as it was during the GFC and after the dot.com bust. Like the rest of the country, it’s in long-term structural decline but worse than average.

Jdog,

This sounds like Montgomery County Maryland where I live. I put a couple of “STUDENT DRIVER” stickers on the front and back of my car to keep these f$ckin morons from running me off the road. It worked for a while but no more. DC, Swamp is even worse. Its like a third world country. No law enforcement whatsoever. The civil society has broken down.

A lifelong resident of SD tells me that she’s seen poop all over the place downtown.

It’s still a beautiful place with the best weather in the country. It’s certainly not what it was, but you can say that about every place in the country that is scenic and has recreational amenities and decent weather.

But for me, the other homeowner and taxpayer expenses make CA off limits. Prop 13 means that long time homeowners pay essentially nothing and new buyers get the shaft. Sales taxes and utilities are far above average, as are gas and insurance prices. And income taxes on an income required to pay for that mortgage and those costs are above average and poised to go even higher the next time the economy dips because Newsome is spending the surplus now like a drunken sailor when most nearby Western governors are looking to cut taxes. That’s what keeps me from moving to coastal CA more than anything (as a former CA resident).

Is there a lot of international money in SD, like San Fran and Seattle?

I think that’s been growing. There’s definitely a lot of stupid money.

The Chinese are heavy in Seattle as a lot of the money moved from Vancouver, Canada to Seattle, Washington about 5 years ago.

In Seattle, I get cold calls in foreign language all the time. I have no idea what they are saying, but I assume it has something to do with real estate. I think the foreign realtors like to blanket whole neighborhoods that are attractive to their clients, and where a cultural base has been built up.

Massive gentrification continues and may be accelerating in West Coast cities. At least the historical departing residents get a nice wad of cash as they are kicked out the door. The people mainly being harmed are younger folks who rent, and have little chance to stay in their homeland.

Listen to Spanish language radio real estate program every Saturday for last two years. Jubilation now because the number of low end houses, the kind that gardeners buy, is increasing by double digits from last week. “There are 14 more houses for sale in Pinole this week than there was a week ago.”

Same thing on AM English language real estate promo stations. “Rent is going up, so you can ignore the higher interest rates”.

kerbloodbathrocksplatsmashblackdeath? For stocks? I agree. (Wolf, is that the word I heard you tell Adam??).

Back to real estate… Anyone willing to pay my Zestimate wins. Don’t wait. CALL NOW!!!

Good riddance Greater Fools!

I clearly remember the Northerners flocking to Florida to overbid US$50,000 for a home in the middle of swampland in Western Florida & Key West.

Saw a trendier clicking on the contact form for a home being advertised for US$125,000 and typing that they are willing to pay US$200,000 right away!

The west is dropping? Say it ain’t so… Can’t be invincible SoCal. I guess I will believe it when I see invincible neighborhood like Irvine or Culver City start dropping then I’ll say the fat lady is ready to sing.

On the other hand, still seeing crapshack pop up in my email from Redfin..seller asking for $850k for a not so decent jointed condo in Placentia when price history shows paying half that back in 2018 or $775k smallish condo in Ladera Ranch sold for $400k in 2020..simply amazing

I think the entire West Coast has been sold to foreign money. When you think of all the manufacturing profit that shifted overseas the past several decades, you know it has to come back to the US in the form of immigration and skyrocketing RE prices. It’s big money, and as long as the US continues to buy foreign goods and rack up debt and trade deficits, there will be no end to it. People displaced from these areas will find their new home in Oklahoma or Arkansas, with a view of scrub brush or the backside of a Walmart.

Seeing lots of tearful people on social media talking about how grandma, or the entire family is being priced out of the place they rented for decades.

I guess they aren’t willing to share the place with two other families the way immigrants do.

All the Chinese bought cities are cratering in Canada but they’ve been bought to the tune of about 3 times what any local could afford on a $45,000 a year salary. Make that 3 times what a couple both making $45,000 or $90,000 a year could pay.

Do not forget the 4 billion in illegal drug money looking for a home. Our cities fill up with fentanyl zombies, while profits buy up our national assets.

And our borders facilitate this trade along with the plethora of disease once eradicated in the US. Stupid policies have stupid results.

it is all built on funny money and will end. the piper is coming around soon.

But don’t be alarmed. Real estate after real estate guru from Zillion, Redfin, Opendoor & most importantly the REEA have been telling us for two years that “this time it’s different.” There’s no way housing can collapse. We’ve got a lot better lending standards and underwriting. Well, guess what, subprime mortgages only made up 12% of loans back in 2007 just before the collapse. Never mind the grossly over inflated home values and all of those 90% cash out refi’s over the last two years. Oh NO! That’s a totally different situation. Everyone can afford their house with debt to income at 40%.

Looking at Zillow listings in the northern part of Orange County, CA – I see a bit more inventory today. Out of 251 active listings within my search parameter ($1M-$2.5M single family), 40 showed prices cuts (~16%). Most of these cookie cutter tract homes look alike, no character. I can’t believe they are even listing for $1M+

Definitely seems to be some regional variations in real estate trends over the past few months. In my neck of the woods in New England, there is still a decent inventory of single family homes in the 400-700k range and demand remains relatively strong (MA buyers continue to flee to NH for affordability reasons). Lots of buyers are resorting to ARM mortgages (Per realtors in the family) which *slightly* softens the blow of higher interest rates. Also interesting to note some short term weakening of 10 year yields. Have to wonder if the stock market continues to sell off, it could provide some short term support for lower mortgage rates. Long term the uptrend in rates is inevitable. My guess is more stable RE markets will see a plateau in home prices while the hotter markets that saw a surge in wealthy remote workers might see modest price corrections. Until the job market flops and more people are forced to sell for employment reasons, historically low inventory levels should provide a floor even with deteriorating demand.

This reads like a press release from the NAR. Good luck with that, the bubble has burst and I haven’t read of a single market in the country that hasnt been bid up to the moon. Now it’s all over but the crying.

I don’t think the NAR would even address the risk for a correction in certain markets until prices had already corrected by 10-20%.

JoshWx

This sounds like some NAR (Lawrence Yun) talking points.

Year resorting to ARMs is usually the last gasp of mortgage approvals trying to keep the churn going.

I said it here at 3.2 that tnx will find its way back to 2.48 area. 2.79 yesterday. The fed will back off, rates will ho under 5 in a short time. The bond market front ran the fed

Watch the bond market once the Fed actually does QT, rather than just talks about. It’ll start in a couple of weeks. Give it a few months to start seeing the effects of QT.

Be interesting if the incomes of the buyers could be graphed out.

It would show which quintiles were effectively banished from the real estate market.

I kind of get the flight to safety, dumping stocks to go to treasuries and pushing down yields. Where is the new money coming from to buy the stocks that everyone is exiting? It seems stupid or at least confusing. Exactly, how many greater fools are there? Is this number in the census statistics?

It’s no different than any other time. Most of the source is from selling of other assets which is used to bid up something else. There is new money from QE “printing”, but most new “money” is just debt.

There is (and never was) any “cash on the sidelines” because it isn’t cash. It’s debt.

Just take Wolf’s charts and go back to 2016. That’s where we are headed. Major implosion coming. Even Seattle. I’ve said this many time, no one talking about the now worthless tech RSUs. Look at it as an opportunity.

A lot of these fake tech companies are going to go BK. Never made a penny in profit, options handed out like candy, spend like drunk sailors and laughable business models. I’m in tech, so I saw back in the dot com bomb a lot of peers chase the shiny object only to have funny stories of their companies imploding. Maybe f-ed company can come back and document the melting of the snowflakes as reality crushes them.

And do any of these snowflakes have sketchy mortgages? You betcha ;)

Wow. I feel like I stumbled into a blog on real estate in Southern California. :-)

Everywhere else in the USA (outside of California, anyway). SD is the postal abbreviation for South Dakota.

Cuz ain’t no place blow up and hit da fan like Cali. We be SD, OC, LA, SF all day long, bruh!

How do you know when the housing market is about to crater: when the banks are pushing 10 year ARMs on first time buyers! Yes I saw literature on this from a credit union yesterday.

Let’s see if 40 year mortgages become a thing. I have no doubt that people would sign up for that bondage in a heartbeat.

Snag that $1.2 mil cottage across the auto shop before it’s too late! You don’t need a second bathroom.

Make the mortgage a 100 year and tied to the property. Not that bad to the «owner», the lender then become landlord with the assosiated risks.

Interest-only mortgages have been around for a long time (they’re a standard option in commercial real estate). There is not a huge difference between an interest-only mortgage, a 40-year mortgage, or a 100-year mortgage.

My credit union called this week to ask if I needed a cash out refi. First time I heard from them…ever. I told her to start looking for a new job quick.

The numbers are numbers, but what is blowing the balloon is speculation, buying for 2m and selling for 4m in 3 months, the mortgage percentage and inventory doesn’t matter.. It’s like the toilet paper, ammo and baby formula, it’s in fashion. But soon or later these people are going to realize that they can’t eat the house they can’t sell..

More proof that either SoCal market is absolutely insane or extremely late to react because look up 8705-Neardale-St-90723. Pending, $800K house in Paramount…just wow…

That’s $405 per sq foot. I’ve seen a LOT more insane pricing in Seattle and suburbs.

But this is Paramount, if you know the neighborhood you’ll see how insane this is…

Wow! That is insane. My Grandfather was a janitor at Paramount High from the 60s to the 80s and it was an iffy area then. However, that price suggests gentrification. When you think of Seattle and suburbs, you don’t think of Compton, Lynwood, and Paramount.

In football they had some ballers we lined up against, they did have good soccer teams back then as it was the Hispanic hood in that region

“However, that price suggests gentrification.”

No. That price suggests a massive housing bubble. I assure you, Paramount is not being gentrified.

Prices will fall once supply rises a bit further and there is no demand. Just give it another couple months to really get going. Some sellers are pulling their homes from the market when they cant sell them instead of lowering the price because they believe that inflation means higher home prices (which it does not). Higher inflation means higher interest rates which means falling prices. But supply and demand are the metrics that set the prices and those are still being held up by psychology. Wait for the psychology to change and that is when prices start to drop.

People won’t sell because they can rent for a good amount compared to their purchase price and mortgage amount.

Even if people could time the top here, where do you put your money in a high inflation environment for wealth preservation. Most people would rather have a physical asset vs the fed funny money. Look at the 70’s and 80’s, high inflation -high interest and property prices only went up during that time.

The number of listings will shoot much higher once prices begin to fall. Sellers have been deluded into thinking that holding onto their properties is the long term strategy, when in fact, the longer owners hold, the lower the price they will get.

Inflation will peak in June. The downhill it will see

It peaked in March and will re-peak at a much higher rate later this year. Look at the huge variations and fake peaks in the 1970s through the early 1980s. That’s the model. Year-over-year and month-to-month inflation rates are NOT a straight line. They go up and down a lot, in part due to the “base effect.”

Services CPI is now spiking, even as some of the goods CPIs are coming down. So watch the services CPI blow your theory out of the water.

ok, we shall see, services will back off with many high paying white collar jobs that you even elude to in mortgage, RE, Auto and tech pretty much imploding….I’m in the drivers seat of growth for economy as CRA….so I will let you know…I will see it first

There are no longer any houses below $500k to buy in our suburb of Tacoma. A simple house on the corner bought 3 years ago for $400k is listed now for $800k. Another house, much nicer with a water view, was listed for $1.2M and sold quickly, but “only” for $1.0M. So there are some cracks forming finally. Sellers see the dam breaking and want to cash out. Hopefully rates keep rising and start a biblical flood.