“Recent stock market volatility” catches some of the blame.

By Wolf Richter for WOLF STREET.

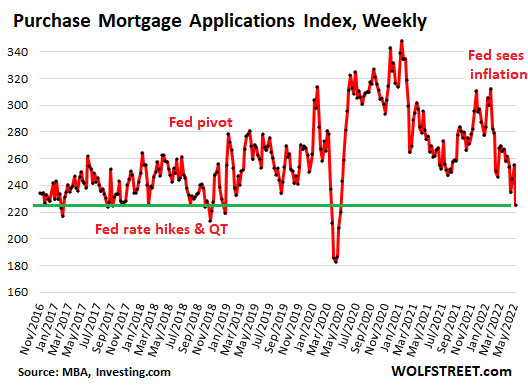

Pieces of evidence are lining up in increasing density. The number of potential future homebuyers that need a mortgage has been thinning out for months. Today, another milestone: Applications for mortgages to purchase a home dropped 12% from the prior week and were down 15% from a year ago.

In its report, the Mortgage Bankers Association today added that “prospective homebuyers have been put off by higher rates and worsening affordability conditions” – namely the ridiculous spike in home prices over the past 18 months, on top of the surge in prior years, combined with mortgage rates returning to what would have been still very low rates a couple of decades ago.

The MBA’s Purchase Mortgage Applications Index dropped to the lows of late 2018. Back then, the Fed had been hiking rates, and its QT had pushed mortgage rates to a hair over 5%, volume was drying up, and prices had started to wobble and were coming down in some markets. But inflation was below the Fed’s target, and Trump had been keelhauling Powell on a daily basis. Powell caved, mortgage rates dropped again, and volume and prices took off again. Now raging inflation is the dominant economic concern, and the Fed is determined to get it under control (data via Investing.com):

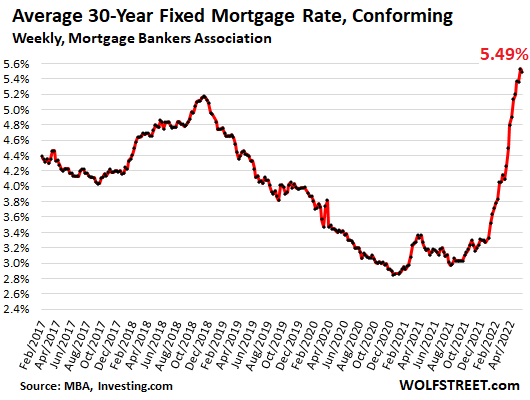

Holy-Moly Mortgage Rates.

The average 30-year fixed mortgage rate with conforming balances and 20% down this week eased a tiny bit to 5.49%, according to the MBA today, from the prior week’s 5.53%, both the highest holy-moly mortgage rates since 2009 (data via Investing.com):

Croaking stocks get blamed.

And it’s not just mortgage rates: The MBA added that “general uncertainty about the near-term economic outlook, as well as recent stock market volatility, may be causing some households to delay their home search.”

In this context, “volatility” always means sagging stock prices, because no one complains about upward volatility, and stocks are croaking. I mean, not every day, because we’ve had some sharp bear-market rallies, but they don’t last long, and then stocks skid to lower lows. It’s unnerving for people who’ve come to expect eternal and easy riches from stocks, and had built their whole future on this theory.

If you were going to borrow your down-payment by taking out a margin loan against your soaring stocks, you may now have second thoughts, that’s for sure. I mean, look at the sh*tshow going today, with the Nasdaq down 4% at the moment, subject to change.

Cryptos were not mentioned by the MBA, and that’s a good thing because they’re just gambling tokens. But some bigger cryptos have already collapsed to essentially zero. Others are on the way. Bitcoin has plunged about 58% from November, and is down 25% from a year ago.

And that’s not confidence-inspiring for people who’d expected to use their crypto gambling wins to buy a house with. Those that got out early, made it. And those that believe in HODL (“hold on for dear life”), well, they’re going to have to keep believing.

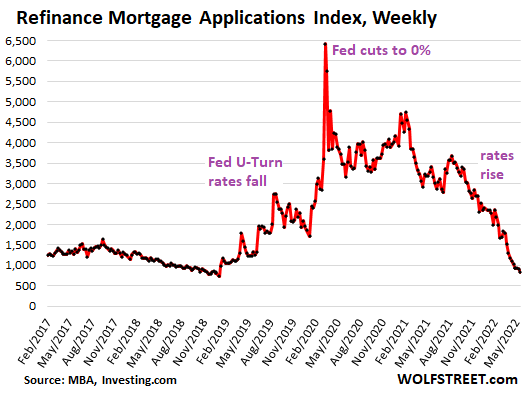

Refi applications have collapsed for months.

Applications for mortgages to refinance an existing mortgage dropped further, having plunged all year amid these holy-moly mortgage rates, with the MBA’s Refinance Mortgage Applications Index hitting the lowest point since the end of 2018.

Cash-Out Refi vs. No Cash-Out Refi.

But there is a split between cash-out refi, where needy homeowners are still feeding at the trough of the home-price spike, and no-cash-out refis, where homeowners are trying to lower their monthly payment by getting a new mortgage with a lower rate.

The AEI Housing Center tracks this split, using a different methodology than the MBA to account for mortgage applications.

Cash out refis are motivated by the need to take a big chunk of cash out of the home, and mortgage rates are a secondary issue. So cash out refis are continuing, but have dropped by 42% year-over-year, to the lows of early 2019, according to the AEI’s Housing Center.

The share of cash-out refi mortgages insured by the FHA – includes subprime mortgages and low down-payment mortgages – rose to 27% of all cash-out refi mortgages, up from a share of 10% at the beginning of the year.

“This indicates that higher risk borrowers are experiencing more stress due to inflation – not a healthy trend,” the AEI said. They’re doing cash-out refis with holy-moly mortgage rates to pay for inflation? Oh boy… Thank god that only the taxpayer is on the hook here from get-go, and not the banks, which means that the Fed can let this one rip.

No cash-out refis are motivated by lower mortgage rates to reduce the mortgage payment and save money every month. And those lower mortgage rates are now history. In the current reporting week, no cash-out refis have collapsed by 93% year-over year.

This means the end of the monthly savings from lower mortgage payments, and the end of these savings getting spent on goods and services, and thereby another pillar of support under consumer spending has been kicked out from under it.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I’m very very interested in what happens with all the 2nd homes that people have been hoarding for the last few years because “the price just keeps going up 10% every year so it would be stupid to sell.”

Look at Truckee and South Lake Tahoe. Both inventories have increased in the past 1.5 months. Mammoth Lakes, another affluent second home market in CA, has seen inventory increase with more price cuts. Inflation will drive up costs of HOA’s and a decreasing asset valuation will tempt more people to sell.

I was in SLT 2 months ago and swung by Harvey’s Casino on a Saturday afternoon and all the gaming tables were closed – no action whatsoever. The hotel was booked to capacity. One of the staff told me there was no gaming until 5 pm every day because they could not staff the tables during the day. Many employees had left the area, some in 2020 due to the covid shut down but many more recently due to egregious rent increases and COL. Confirmed by a blackjack dealer across the street at Harrahs, who planned to relocate out of the area after the ski season due to crazy rents.

I am watching this area. Agree that inventory is ticking up but price cuts still small. At the speed things are evolving I think it is wise to wait this one out and see. I predict that people will start with price cuts when the boat has already sailed completely….

I was there 17 yrs and sold in july of 2021. People are fed up with the bay area people. The anger is everywhere, from your bartender to the ski shop guy. It’s becoming a second/3rd home owner’s place that is not where you want to live. Good luck to all the people overpaying for their weekend getaway, you’ll have nowhere to eat, shop or enjoy.

As Meibion Glyndwr might well have put it: “Every home needs fire insurance”.

And a good attorney who’s specialty is working with you to prepare a LONG list of all the valuable things you had in the home…..”priceless” heirlooms, etc.

After the 2017 Fountaingrove fire here, the “fire-chaser” ads were non-stop for a year or more.

The poor bastards in Coffee Park couldn’t afford their fees, I knew two of them.

As far as the Tahoe “servants” go, it’s a long damn drive to the trailer parks around Carson city to SShore, and a real nasty (especially winter) drive over the hill to NShore.

Its happening just like that in Sonoma too. Homes sit empty after greedy rich people sell their rental homes to out of towers. Mind you the sellers already have plenty in their portfolio but its just never enough. Now the people who work here like my husband who works in the local hospital will be forced to move away. I hope none of these 1%ers need medical care when they visit because the hospital will close if they have no staff. It’s already staffed by travelers. It’s disgusting chain of events brought on by greed.

Yeah. My sister lived in a trailer outside Truckee and worked at the hospital there, early 70’s or so. Not sure what Tahoe has now for the vacationing rich folks.

Guess they can do what Aspen did and run a private bus service to “elsewhere” for all their servants?

Some areas saw 30% increases in a year’s time, which should never, ever happen with house prices. This is why Jerome Powell should have been removed from his position long ago. All of these signs were there, yet he stood up and boldly proclaimed “we’re going to let inflation run hot.”

The FED’s mandate is stable prices. How in the world was this thieving cabal allowed to do this? It is morally reprehensible, and is exacting an impossibly brutal toll on the middle class and the poor.

Bernanke came out and said Powell and Co. “made a mistake,” and that they were “scared” of another stock market tantrum. I have not been able to find anything in the FED’s mandate that says their first concern is the stock market.

Jerome Powell and his grifter buddies should be in shackles.

Their other mandate is employment. Both conditions can rarely be met at the same time. Hence the FED can justify doing whatever they want to do.

5+% is pretty good, my first mortgage was 9.5% and I was cheering.

So if house prices are high Why in the hell is the FED still buying AT LEAST 35 b a month in mortgage back securities .They have no business being there other than stocking house price inflation and no body is blaming the FED that matters that is talk about a free market BS.The FED is a criminal organisation that is there to empower the 1&2%ters they have never been richer. They couldnt go negative interest rates so they did the next best thing. Stoke the hell out of inflation and suppress interest rates give the negative rates they are look for and screwing the average joe blog along the way. The US is a crisis driven debt based ponzi scheme run by the FED .The US has no money its all debt and at some point it must implode by design

The Fed mandates are low unemployment and low inflation, but the Fed’s policy of supporting high asset prices has violated both mandates!!!!!!

High asset prices cause both CPI inflation AND unemployment. People have left the labor force because their net worth has exploded due to huge stock price and RE gains. The Fed doesn’t get it. This type of unemployment doesn’t show in the statistics, but it’s there. These same people will be begging for jobs if and when the stock and RE markets tank.

The Fed has really screwed this up, and the huge monetary mistakes have been made for at least the last 15 years.

All of it was absolutely foreseeable and expected.

I but home prices were much lower at 9.5% interest.

Is the FED a Stock Corporation?

I have heard, somewhere, that the FED has actual Stock Holders.

If this is so, their mandate is to serve the Stock Holders.

Supposedly, in 1913, the FED raised it’s Capital by selling Stock to the member banks. They, thus, would be the stock holders.

Common misconception here. The Fed is a hybrid organization.

The Federal Reserve Board of Governors is a government agency, and all its employees are federal government employees with a government salary and a government pension, including the seven members of the Board, including Powell and Brainard. The seven members of the Board are appointed by the Prez and confirmed by the Senate.

The 12 regional Federal Reserve Banks, such as the New York Fed or the San Francisco Fed, are private organizations that are owned by the largest financial institutions in their districts. All their employees are private-sector employees.

The FOMC – the policy-setting committee – consists of the 7 members of the Board of Governors (federal employees) and the 12 governors of the 12 regional FRBs. The governor of the NY Fed is in a permanent voting slot. The other 11 governors rotate through voting slots; they vote one year but cannot vote the next.

If you are a State Chartered bank you elect to become a Federal Reserve Bank(RRB) member or not to become a FRB member. The difference between the two options is the regulatory examination agency. RRB member- you are examined by the FRB and the State Department of Banking – alternating. Non FRB member- you are examined by the Federal Deposit Insurance Corporation(FDIC). if you are a Nationally Chartered Bank( big guys like Chase or any bank that has National in it’s name) you automatically are a member of the FRB. You are examined by one agency- Office of the Comptroller of the Currency(OCC).

Yes, if a FRB member, the bank has to own FRB stock. it pays a modest dividend annually. If the bank sells to another bank ownership group or PTC they are required to sell their shares back to the FRB. It is my opinion, having owned a FRB member State Chartered Bank, one can do much better owning equities vs FRB stock. Don’t lose sleep thinking FRB stock owners are manipulating the economy for gains. They aren’t.

If you want to learn about the worthless FED

Their origin

Who owns this crime syndicate

Read

The Creature from Jekyl Island

You will get your answer

These worthless scum are idiots

The FED

They care nothing about you or me

Their bottom line is

The Dollars

Words ended

D

DZ,

If I read “The Creature from Mar el Lago” will I find the reason Powell cut rates to zero before the election?

Your “book” is just someone’s opinion about lobbying, who wasn’t there. I have seen a lot of lobbying at and around my uncle’s beach house in Hilton head..(and other places)…It’s just a ways south of your Edgar Allen Poe style island and book. They usually don’t have to be quite as sneaky about it all as you want to believe, but it seems you love just deep dark secrets. I find that very sad.

DZ,

Also , as you didn’t even cite the author, I’d bet YOU never even read it…just had it “explained’ to you by another outraged idiot who never read it….likely at a bar.

I would include Mr. ‘All Is Contained’ within that group of perps. His recent comment re. Powell & Co. is just cma from a usual suspect. Throw ol’yellen inside the hoosegow extra good measure!

‘for’ extra good measure ..

“How in the world was this thieving cabal allowed to do this”?

It’s by design. Rates were decreased to ATL to get everyone on board. What happens to a stock when you have one or two major institutional shareholders with the same agenda? The answer is whatever they want. It will be another too big to fail scenario with the USD being saved by central banks, IMF and world banks. The only stipulation is to revise the US constitution and granting WHO complete global control in any health crisis they deem necessary.

The next pandemic will be queued shortly and it’s likely to be a bird flu variant. Same play book as COVID but building upon the hoax of H1N1 earlier last decade. This will be the nail in the coffin. The general public will be duped into believing it was all natural. No one is at fault, it’s a public health crisis.

You have to give it to them, it’s the best mind F yet. The sheer patience required is unfathomable. Only We the People are left to defend the human race.

@.@ oh dear, that is some story…

Yeah, but he left out the UN, the Rothchilds, etc, etc.

Wonder how he plans to “defend the human race”?

My suggestion is an immeadiate MASSIVE and Comprehensive Green New Indusry….but Climate Change is likely just another “plot” to him. He’s as sad as DZ.

“If we have a credit crisis, the Fed would intervene. We know the Fed views financial stability as job #1. Time will tell how bad things would have to get before the Fed steps in but what is clear is that we’re not there yet.” ?

Agree 100%

You have to be careful what you read, there’s always some underlying narrative. For example, this article would have you believe bitcoin is down by indicating its down 25% from a year ago. What is not mentioned is that in May 2020 bitcoin was $9k+, in May this year it is $29k+. That’s a 210% increase or an average of 105% increase/yr. I’ll hold my coins thank you and buy that house.

MXmike,

I’m sorry to hear you’re hurting because you lost so much fiat on your crypto holdings. I know that’s tough, and my thoughts and prayers go out to you.

Not necessarily so. Ex. my house in CA was worth $500K in 1992,market turned around and we sold for $340K. Just like my Upstart Stock was worth almost $200 and now it’s $41 a share. Housing prices do not always go up. Look at the stats from 2008 to 2012.

I have noticed that the number of listings in some Orange County areas is starting to explode higher now. I would think that by June or July, it will finally be back to a market that has a normal number of homes for sale, but demand will be much lower, so by end of summer, those home sellers can either cut prices or they will not sell the home.

Going to be some real carnage later in the year and in 2023.

I live in the same area and get updates from the MLS. Prices are still wildly insane, but I’ve seen homes coming back on the market and some price drops. It’s still just in the early stages but anecdotally it does look to be tapering off.

People have been badly, badly underestimating the macroeconomic significance of “small” interest rate movements for 20 yrs now (“How can going from 6% to 3% change asset values by hundreds and hundreds of thousands of dollars?!”).

If anybody in the MSM had ever spent 15 minutes in the last 20 yrs explaining the essentially simple discounted cashflow formula, recent American history would have been very, very different.

Whut Willis? Are you suggesting net present value? That’s not a real thing. No one needs a real rate of return or to factor in inflation. Nothing to see here. Please move along.

Here in nash.tenn. never.have I seen so many people move in here from out of state..calif.texas..ohio..Illinois. new York. All out of states trying to get out of high taxing states.with no income tax.laws..and of course.buying up all the homes.everwhere in town. 250k houses going.for 950k..it is just totally stupid till all the money runs out..r

Nashville, …sigh.

They don’t call it a Tennessee tuxedo for nothing. The newcomers probably stand out like a sore.

I have never seen so much glistening vomit in the morning sun in one place as I saw splattered all over downtown Nashville. Mullet powered chunky vomit and purple and hot pink girl vomit.

Nashville reminds me of Phoenix. Sprawl and a few boulders. Nonsensical prices. Except TN also has ticks, chiggers and so much vomit.

I live in California and know a lot of people who made this move. A few real down to earth normal people, but a lot of them have no sense of reality and really couldn’t fit in anywhere but Beverly Hills, Orange County or Silicon Valley. When they’d tell me their plans, part of me would be like yes, please go, just leave. But being from Sacramento and seeing how a couple housing booms have completely destroyed the culture there, I honestly hate to see people with so little character moving to places with so much of it. It’s a tragicomedy in every place where it happens.

Well, not moving to Nashville, but in all fairness, some of us have to move, like the normal, not rich, working people. So my partner and I live a couple hours north of NYC, in a nice, quiet, rural area, nothing like southern NY. He’s a vet, was about to use his VA loan to buy our first house with our new baby. Was renting a big 2 bdr for $1200, right in town. Market hit, immediately the homes in the area skyrocketed beyond our reach, and our rent went up to $2150 a month. He’s a VA hospital employee. So we’re all being driven out and need a new place to go. Sometimes its no disrespect to another community. Ours was broken up too. All the people from the city bought 2nd, 3rd homes up here, or stock piling them for high rentals.

Oh no, never in precious Irvine or South county.. Prices will never come down or will just stabilize, at least that’s what all my old co workers used to tell me as they are all conditioned to think this way based on the recovery from 08.

gametv, are you a buyer over there in orange county?

We are also looking there too. It is still ridiculous

When you add the ridiculous housing price inflation and the steep rise in mortgage rates, the cost of buying a home just went up over 40% in one year. That’s made housing unaffordable for a large segment of the population, especially 1st time home buyers. Nothing on the interest rate front will change in the next year except to make things even worse. Both buyers and sellers are going to be big losers as this housing bubble pops.

Great charts!

Everything is currently back to Pre-Pandemic 2018 normal. Purchase mortgage applications, refi mortgage applications, and mortgage rates (OK those are 0.3% higher than 2018). All are highly correlated.

Will mortgage continue to go higher? Or will the Fed throw in the towel and drop rates like they did in 2019?

I want to know who were the 800 refi mortgage applications last week? Have they been asleep for the last 2 years when rates were sub 3%? Or are they the world is ending types who want to pull out as much equity as possible at 5.49% because they want to sit on expensive cash (or buy gold). Do they believe rates will go even higher?

Seen it all before, Bob,

FYI, those 2 mortgage application charts are indices and show index values, not the actual number of applications.

Thanks for clarifying, Wolf!

> FYI, those 2 mortgage application charts are indices and show index values, not the actual number of applications.

Awesome charts!

Have you seen a similar one for reserve mortgages?

* reverse mortgages

Is there a way to see what % of reverse mortgages end up at auctions?

I don’t have any data on this at my fingertips. But I’ll keep my eyes open.

I’m signing up new reverse mortgage company for our credit API today, they have unique model where they rent back to older homeowners after giving them full bid on house while brining in other senior services via the platform….doing well and now taking next big step to automate credit application

I meant to add that all are currently back to 2018 normal.

Except for house prices.

Just give it some time Bob. All “good” things come to an end. But housing prices down move like a slow-motion trainw… you know what.

Check China,50% haircut were next ,if China-Russia succeeds there endgame is bankrupting America

Hopefully the pendulum effect will be at full play when the RE market corrects. As they say, there’s always over reaction on both sides, on the way up and hopefully on the way down as well.

“Will mortgage continue to go higher? Or will the Fed throw in the towel and drop rates like they did in 2019?”

It doesn’t matter what they do. If they raise rates enough to contain inflation markets collapse, insofar as they’ve been levitating on cheap credit since at least 2008 and will no longer have that wind beneath their wings. If they don’t raise rates inflation has its way with the economy and markets collapse when consumers start running out of anything to spend.

You might expect The Fed to split the difference so you can have the worst of both worlds, and then cultural specialists will amp up comments on finance/economics blogs blaming the situation on the evils of gdless socialism, which we are assured is the root cause of Everything Bad from corporate greed to big bank bailouts to juvenile sarcoidosis in pre-adolescent teens.

Laugh about it, shout about it, when you’ve got to choose, every way you look at it you lose.

In my opinion, we are only at the start of the correction in mortgage applciations and they will plunge much farther.

The people buying houses in the past year were correct in the short term and very horribly long in the long term. So if you flipped houses for a quick profit, congrats. But if you are holding long term, you better have gotten a really terrific deal.

What many of those people who bought didnt understand is that even if they can afford to continue paying the mortgage on their low interest loan, the price of the house will depend upon a market where other people must pay a much higher interest rate and therefore cant afford to pay the same price. So prices will adjust down. And when you combine that with alot of investors selling houses as quickly as they can and a new cycle of foreclosures hitting the markets in the next year due to people being underwater on their mortgage, well, you have a pretty bad scenario.

It can be an ok decision if the person actually likes the home, plans to stay in it, and didn’t buy it as an “investment”.

Problem is, at least a noticeable minority look at it as “investment”, they are financially marginal and won’t be able to keep it under adverse economic conditions or personal circumstances, and many areas are headed into or already in long term structural decline; the long-term “slumification” of America which is turning into a third world country.

Most of my friends in southern CA have second or third homes as investment. They bought homes in last 2-3 years. They believe, home prices won’t go down drastically.

No adverse impact on home prices in CA yet.

California real estate prices have defied gravity far longer than I thought possible.

I’m still taking the “under” on the bet your friends have placed.

The end of the bond market mania will make SoCal hopelessly unaffordable. Working Americans can’t “afford” it (renting or buying at current prices) without fake “growth”, artificially low rates, and the basement level credit standards we have now.

Foreigners will also have less money, as a country like China has its own massive bubble to contend with, though this may take longer to become evident over here.

Homes and cars are expenses. period. Sure the value of my house doubled over 20 years. But that is about right for inflation assuming I never spent money to maintain. But I spent lots of money on upgrades. Not for investment reasons but because my Wife likes them. I am an amateur craftsman so the cost of fancy woodwork included my free labor. We never intended to recoup those expenses. But we like our house. The problem at large is that people watch those reality fixer upper shows and forget simple logic. We deserve what we get as we are so gullible and easily manipulated by that stupid TV.

If people bought a home to live in, and the payment is in their budget then they are in good shape.

Those buyers might have bought next year at a lower price with a higher rate but the total payment is roughly the same.

Nobody seems to be pointing out that for the buyer their is little difference in scenario a (low rate) or scenario b (low price)

Recent home buyers bought a payment, not a price, and they will be OK if they stay employed.

Buying based on payment is the issue… if they have to sell for whatever reason within the next 10- 15 years, they’ll be upside down. They’ll never have the option of refinancing at a lower rate. Buying by price is the way to go.

Isn’t this called Deflation

Now do any/all of Canada, New Zealand, Australia, Germany etc! In Canada, our bubble is–compared to the US–bigger, broader, and has diverged significantly from fundamentals (depending on how you measure) since 2011. A bubble on a bubble in the face of <1% population growth supported mainly by immigration.

Imagine New Zealand real estate prices the day after any nuclear power says they have targeted one (1) ICBM on NZ.

Instant end of TEOTWAWKI bugout location pricing power.

Canada is taking 400,000 immigrants a year (population 39 million), so >1% just from immigration.

That does not sound like much but it means 1,000+ new people EVERY DAY (7 days a week) need a home to live in.

Per capita Canadian home starts are well above US levels, yet we still are short.

Solution?

Answer: Sow immigration. Cut by 50% and the problem easily becomes less of a problem.

Canada’s population falls significantly every year without immigration.

Canadians think they have a perpetual motion machine. They do not.

Most of the immigrants coming to Canada are now from Nigeria. The ones coming form Pakistan and India have fallen dramatically. The rich Chinese stopped coming here around 2016. Canada is mostly now importing poverty.

I would propose another solution – make immigration levels aligned with levels of homes under new construction or available for renting. The problem is, large percentage of Canadian population (majority ?) will reject this approach because they are very happy to see their homes go up in value, and know that immigration is one of the major drivers of this (along with low interest rates, lax money laundering laws and enforcement, etc.)

A lot of plans are probably going into reverse as housing shifts, and equities slide. Lots of ambitions were shaped around those trends.

An acquaintance of mine quit her nursing job after COVID burnout, and she and the hubby aimed to become landlords this spring. Time to re-think the re-think.

Yeh exactly. The wealth effect certainly had an influence on the real estate price run-up. Now we get to see the “anti-wealth effect.” Or in Warren Buffett’s terms, we get to find out who has been swimming naked.

Here in the midwest I have observed an increased level of inventory on the market, more price reductions and longer selling periods. More to come….

I’m a bit older ,u have to realize FED giveth,FED taketh it’s always a cycle . Zero interest rates were dumbest idea ever ,never happened in all of history ,now pay the PIPER

Weren’t the dumbest idea ever to the rich in the know crowd. They’ve cleaned out. Only us Stoopid peasants hate it.

I think the Swamp posted a few days ago that the current stock market crash is doing wonders for those thinking of liquidating their investment portfolio to come up with a down payment for a house. The way things are going on Wall Street there may be no portfolio left to liquidate.

There is no stock market crash yet. Individual stocks have crashed as documented here but the major averages are nowhere near that. Dividend yield on DJIA and S&P 500 is near the lowest ever, far lower than on the eve of the Great Depression.

Today’s -4% suggests that the “croaking” stocks are starting to croak in a new key, though. In my mind that marks “the end of the beginning” of the bear market.

Last time we saw -4% was just after the COVID panic in mid-2020.

In the 2007-2009 bear, there wasn’t a -4% day until Sept. 2008, shortly before the real crash got started.

The Bear is definitely here now.

The S&P500 rarely goes down -4% or more in one day. Those days are so rare you can catalogue them.

This list looks back to Jan 1, 1980:

October 1982 (oddly enough, during the recovery from the Volcker plunge – there were no -4% days during the 1980-1982 bear markets themselves).

Sept 1986 (a one-day correction).

October 16, 1987 (The Friday before the Big Crash on 10/19)

October 19, 1987 (The Big Crash, -20%)

January and April 1988 (hiccups in the recovery from the Big Crash)

Oct 1989 (a one-day correction).

Oct 1997 (quick US correction linked to Asian Financial Crisis).

Aug 1998 (Long Term Capital Management blowup. See “When Genius Failed”).

April 2000 (Dot-com bubble topping process)

March 2001 (Dot-com bear market – Breakdown of major support levels)

September 2001 (9/11)

Aug 2002 (Dot-com bear market)

13 instances from Sept 29 through Dec 1, 2008 (the major crash during the Great Recession…).

6 more instances from Jan-April 2009 when the bottom was finally set.

4 bad days in Aug 2011 (Euro Debt Crisis)

Feb 2018 (steep market correction)

8 instances in Feb-March 2020 (the COVID panic)

June 2020 (one-day correction after the COVID bottom)

And now, May 18, 2022.

S&P 500 going down -4% is a 3.6 sigma std event

The stock market has grown progressively rigged since 1993. Now its nothing but a three ring circus sideshow.

So, they’ll pull money out of the stock market after it has already lost 20% in value and buy (overpriced) real estate… only to watch it decline 20% over the next couple of years. It’s a brilliant plan I must say!

It’s called a box-barrage. The crowd surges forward, they drop some shells up in front, crowd panics and run back, some shells drop there too, they crowd stop, and then all guns are firing “for effect”, right on top of them.

So, 20% loss in the stocks, investors move to real estate, immediate 20% loss there, they go “fuck it, we will live on beans and never sell”, then property taxes, unemployment, insurance hikes, and energy costs are unleashed, all at once.

Then someone like Blackstone makes them a “sale & lease back” offer they cannot afford to refuse, or maybe they wait and buy them out at the bankruptcy auction.

I would die a happy man if the housing bubble would pop fast this time around and as hard as Target is right now at close to 30% down…

In SoCal, would be nice to see these hot areas get corrected by 40-50% to bring it closer to what’s consider normal. After all, when you see crapshack goes for $900k in Placentia or $1M in Inglewood or $1M in Chino hills…there’s only so much eye rolling one can do…

Many areas need a drop of 80% to get back to what wages support, and the higher rates go, the more they need to drop. The FED has absolutely destroyed the economy.

Completely agree with you but even though I am fantasizing I like to keep it more realistic, 40%-50% down from current level would be good enough for me to buy. Still overpaying compare to fundamental value but compare to the insane level it is at now, it’s a sacrifice I am willing to make especially since I am looking for a long term home to live and raise my family in and not some flipping opportunity.

Phoenix, you should see all the muscularity around my eyes from years of eye-rolling hypertrophy here in So Cal.

haha I don’t doubt you…personally I have been eye rolling at these prices for last decade, I had to do some HRT just to keep those muscle nice and strong…really up my does when the craziness of the housing market exploded after 2020

The fact that purchase money apps have dropped 15% yoy is in line here in SoCal due to 15% less listings . LA COUNTY where I live I see 20% in the first q1 appreciation. Total insanity still alive in 91326 zip code.

Houses will not drop past 30%. First, most MBS is held by the FED and not banks. Many protected by pension funds. Second, Dodd and Frank allowed up to 4 individuals, on a single family mortgage application, to ensure one job cut does not destroy the home mortgage note. Finally, the labor market is hot. Not the case in 2008. The problem is the new salaries are far below the COL. Much of that is due to the dollar being less then 42% of worth then in 2000. Inflation will either cool or organizations will need to being COLA. Only time will tell how this will end.

Labor market is shifting from employee power to employer power rather rapidly.

Hey wolf how about a chart of expat’s,what will happen to them when market crashes . And they lose pension,SS and savings while living in a foreign country.Bad situations

What kind of BS are you posting here? Americans do not lose their SS benefits, pensions, and savings when they live overseas. Sheesh!! Lots of retirees live off their SS benefits and pensions overseas just fine.

“Lots of retirees live off their SS benefits and pensions overseas just fine.”

Heh heh heh.

Medicare will not cover expatriot retirees, unless they fly back to the U.S. for medical care.

No one needs medicare in other countries, medical costs are reasonable.

IMO, if you’re healthy and have a little extra income in addition to Social Security, expats can live fine in many places. In Thailand, I pretty much self-insure. I keep paying Medicare premiums as backup for major stuff, for which I would return to the U.S. if possible.

A few years ago I got sepsis (blood poisoning) which I could have easily died from if undiagnosed or lived in some remote area (the body’s harsh immune response to the bacterial infection in your blood is what kills you). My Thai wife was out-of-country, and I barely made it to an expat-oriented hospital via Grab taxi (too sick to drive). Lucky for me, one of the doctors suspected sepsis right away. A couple weeks in the hospital, with antibiotics and full 24-hour monitoring by nurses as well as daily visits by doctor, including a full-body CT scan, and a few hours physical rehab, cost about $9,000.

Since then, nothing really costly. So if I average over the years, my medical spending is only a relatively small fraction of what I would have spent on getting expat insurance (prohibitively expensive at my age).

I’m on my wife’s Thai government pension insurance, in which costs are extremely cheap. But I’m uneasy about the doctors, as well as rubbing shoulders with the masses, in socialized medicine hospitals. However, other places might be okay. I’ve heard that Columbia has a pretty good socialized medical system that you can buy into very reasonably as a retired expat.

Wolf, unamused and David Hall,

I am one of those expats who have relocated to a very inexpensive English speaking country. My SS and my pension are doing just fine. I just cancelled my Medicare part B which puts my $170 more in my SS check every month. Part B pays for doctors visits and part A – which is free – pays for hospital visits. I am fortunate to be very healthy.

Which country are you in MG?

I’ve lived abroad in Asia and healthcare in Bangkok was very high quality and reasonably priced.

I am sure we will hear the same old nonsense out of CONgress once prices are crashing. Out of one side of their mouth they will say “we need affordable housing,” and out of the other side “we need to keep house prices up.”

I find myself wondering if “cash out” refinancing somehow artificially drives up home selling prices.

No, but it drives up consumer spending.

Cash-out refi money sometimes gets used to buy second homes (vacation, rental, investment)… so it could help to drive up home prices generally.

Same idea as how high stock prices enable greater margin debt, which gets used to buy more stocks, which makes high stock prices even higher…

And of course the refi money could also buy stocks, and the margin loans could also buy houses…

Too many pro-cyclical features in the system. The Fed’s supposed to be the counter-cyclical stabilizer, but instead of taking away the punch bowl they drank the kool-aid…

It does if people are taking cash out refis to buy rental properties so they can get rich like those guys on TikTok.

Indeed, that is a smart move.

Having hundreds of thousands of dollars in equity in your home is counterproductive.

Buy rentals with cash, and let tenants restock your equity position.

Rinse. Repeat.

I retired at 34 financially independent and began with $0.

America is the land of opportunity.

The elusive Housing bubble crash has been predicted numerous times over last year or so and still prices keep pushing up.

Every data indicates a crash but really seems different. I have a feeling that Fed and Govt this times will not allow a RE crash because a lot of wealth of politicians and billionaires are tied in RE against which they have taken lot of leverage. Falling RE may cause the house of cards to fall entirely.

Couple of years ago fed wouldn’t have allowed the NASDAQ to fall 30% but this year they don’t even notice or mention it, and that’s where more of the billionaire money is compared to Real estate. So no I don’t think a 25% drop in home prices to where they were just 2 years ago would bother the fed much this time.

A 25% RE price decline would hardly bother anyone. There are a few people in crazy markets that bought RE the past couple years. They are the only people to be escorted behind the woodshed. Everybody else is playing with quick gains, and they won’t be surprised to see a portion of them vanish quickly.

Bobber

I say 25% or maybe 30% because I don’t think the fed would undo all the printing they did or sell all the MBS they bought during the last two years and considering the inflation that we will continue having for next couple of years at least, 2019 Prices would be reasonable in 2024 over all even though some markets could and should drop more. On average houses appreciate 4.5% yearly therefore flat prices for four years while the $ loses purchasing power wouldn’t be a bad or a good deal depending on which side of the equation one stands.

Bobber-

“A 25% RE price decline would hardly bother anyone.”

I know many retired and elderly folk in SW Florida who want to sell in not too distant future to downsize or get extra benefits from a retirement type community, or to move closer to family. They (or their children) are VERY nervous about the downward turn they fear is eventually coming. Most do NOT want to leave their Florida home for the kids to bicker over or be burdened with.

They don’t have forever. 25% will prompt them to pull the trigger, and to chat up their decision with their friends to do the same. “First mover advantage” of a different sort…. Move out first or face much lower prices.

You could wind up with many more sellers than expected, IMO.

I think the RE speculators know things could end badly. A lot of the houses I see for sale now were purchased later than 2019, less than 3 years ago. They want to capitalize on the ridiculous price rise before it goes away. There are a few bagholders willing to accomodate them, but not a lot of them. Plus, once price start dropping, the supply of bagholders diminishes quickly.

My guess is they’ll let housing fall 20 percent in price.

They can’t stop real estate from collapsing either, only cause it to freeze due to a lack of activity by distorting market even more.

Contrary to posts I read here all the time, government and FRB aren’t going to destroy the USD as global reserve currency to preserve fake paper “wealth”, whether in the housing market or stock market.

FRB has 34 potential points of latitude on the DXY to “print”, so I can’t accurately state they won’t try at all, but we don’t live in mechanical world populated by robots. If we did, then “print to infinity” might have some validity.

The days where “printing” seemed “free” are over. Now it’s time for the “blowback’ and hard choices.

There could be a catch. The position of the US dollar as a reserve currency may be tied to the US dollar being the world number one finance currency.

If both US real estate and stock markets crash, the finance part of the US economy has pretty much crashed. The reserve currency is then left with a lot less “reserves”, that is financial assets. How do a reserve currency work then?

“I have a feeling that Fed and Govt this times will not allow a RE crash because a lot of wealth of politicians and billionaires are tied in RE against which they have taken lot of leverage.”

If that were true they’d never allow a crash at all – assuming they could and would prevent one.

“Falling RE may cause the house of cards to fall entirely.”

It’s possible. It very nearly did in 2008. They never did clean up the mess left over from that. Or from the bursting of the dot-com bubble, for that matter, at least not very well. Instead they put the pedal to the metal and waited a few years for the engine to rev up until the push rods flew through the bonnet.

If the dot-com fiasco, the 2008 RE fiasco, and The Plague fiasco didn’t flatten the house of cards, you have to wonder what would, exactly. Continued exhaustion of nonrenewable natural resources (NNRs) and renewable natural resources (RNRs) will do it eventually, but that’s still a few years off. Still, there are existential threats, like thermonuclear war and a worse pandemic. Food shortages would if sufficiently severe. The Rhine, Rhone, Loire, and Po are drying up, so food shortages are in the cards for Europe.

I used to care about these things, but I take a pill for that now.

RE crash is exactly what they want. 40% of current inflation is coming from shelter expenses (mortgage or rent). A housing bust takes that out and unlike 2008, doesn’t take the economy down with it.

I am from Seattle area and since amazon stock drop, things are considerably different. Almost all prices are back to summer 2021 level which is about 25% correction in itself. And nasdaq is hovering around Nov 2020 values right now. That effect will be visible in a month or so.

It is simple economics really. When economy is neutral, all asset prices reflect their true value. Houses dont fall from sky with their prices written on them by god. House is just another financial asset and will stabilize at its true value. A process well underway already in seattle area for last few weeks.

I am also familiar with the Seattle housing market and there has definitely been a shift. I think your observations about prices moving backward to summer ’21 are correct – that is definitely what my naked eyes are seeing.

Of course there will be good deals and bad deals, but I think the moving average has gone backwards 1 year

I got the summer 2021 price information from my RE agent. I trust him because he doesn’t give the buy it if you can afford it bs. He is asking his buyers to wait it out.

And I found this eerie similarity between Seattle housing market and nasdaq (a proxy for tech stocks). Housing market follows nasdaq with a delay of 6 to 8 weeks. And 6 to 8 weeks ago nasdaq was at summer 2021 levels. Now it is at Nov 2020 level. If I am right, a further drop in housing will show up in next 6 to 8 weeks. And amazon stock crash is something nobody saw coming. It is definitely weighing on the market.

Since you’re in a Chinese bought area it should fall the hardest. The money only came there because the Canadian government tried to push down housing prices in Vancouver, Canada back in April 2017 and then all the Chinese money went to Seattle from Vancouver.

Chinese money in Seattle was a few years back. I doubt it is a main catalyst now.

They keep hoping it will crash. Hope never made you money.

See housing market 1975-1990

This was an inflationary period.

High interest rates.

Prices went up and never returned to 70s levels, despite 12% mortgages.

How this plays out is not obvious

Yes, but the ratio of home prices relative to median income was 4.3 to 1. Now it’s around 8 to 1. Last time it was this high was in 2008/2009. Historically, it’s been in the 4 to 5 range.

Bailey from the Bank of England said at a news conference a little while ago that workers should refrain from asking for big raises as to avoid making the inflation problem worse.

They have interest rates at 1% and inflation is at 9% and according to him, they are “helpless.” Helpless or careless? Ah, you thought the inflation was “transitory”? No, they didn’t…

Then I also read this morning that a quarter of Britons are skipping meals due to inflation and the cost of living crisis.

I wonder whether these elites read history books, or whether they just think this time is going to be different just like stock investors…

The UK is in even worse shape than the US. That’s my explanation for the Governor’s comments.

The housing bubble is worse, I’m inferring consumer balance sheets are worse, the country is more reliant on imports, and it’s probably the most financialized economy on the planet.

I’m an Anglophile (for the old culture, not the current one) but believe the UK is going to fare the worst economically of any major economy in the upcoming major bear market.

Your comment about the UK housing bubble reminded me of the Horace Rumpole quote:

“An Englishman’s gin bottle is his castle.”

“Bailey from the Bank of England said at a news conference a little while ago that workers should refrain from asking for big raises as to avoid making the inflation problem worse.”

Whopping bonuses for the City Boys: still okay!

Asset inflation: still okay!

Full speed ahead on the Brexit disaster: still okay!

Will Bailey be refusing his perks to help out with inflation?

Not a chance!

Austerity is for the masses, not the masters.

Don’t say elites. Say kleptocrats, plutocrats, rich scumbags, wealthy predators, etc.

Calling a fellow smelly human an elite is so cringe.

The do! It’s just that life is supposed to be shit in England and the English people very much like to keep it that way. Charles Dickens describes The Good Old Times!

They have: Drafty homes, flat beer, nasty pub food, tossers snot-rollers and navel de-fluffers in government, leaky and unreliable cars, endless queuing everywhere, incompetent staff all over the place, bureaucracies that has to be seen to be believed lording over all aspects of existence – and yet – zero fucks given over practical aspects like plumbing, building and electrical work (because anyone can do that and indeed they do :), and every holiday everything immediately goes to shit because nobody can figure out that people would like to travel on this occasion like the did on all the previous ones.

The big lesson today for speculators is: don’t speculate in retail stocks that cater to pooh folks. Target is now down 27.4% for the day!!!

That huge loss only takes TGT’s stock price back to Sept 2020 levels. TGT is still up about 20% from pre-pandemic levels. More pain can come for TGT and lots of other companies.

There really is zero reason why stock prices should be higher than pre-pandemic. The world economy has more structural problems now than it did back then.

Yup

The “Buyer’s Market” vs the Seller’s Market” is real. Each transaction requires a motivation allocated to each of the participants. Death, Divorce, job loss, shelter, wages, affordability, etc. These are what determine prices.

“But inflation was below the Fed’s target, and Trump had been keelhauling Powell on a daily basis.”

Thanks for the vocabulary lesson Wolf. This word seems tailor-made for Trump.

Keelhaul:

HISTORICAL

punish (someone) by dragging them through the water under the keel of a ship, either across the width or from bow to stern.

HUMOROUS

punish or rebuke severely.

And depicted on History Channel’s oh so historic show Vikings

Been saying this for a couple years, Seattle has built the BIGGEST housing bubble. It will take a century to work through this inventory

In just one six block area, 10,000 units are coming on line right now, in the form of a dozen high-rises. Context – Seattle proper, is a medium sized provincial hub, thousands of miles from somewhere, with a 600,000 pop.

Rents start at 2 grand for a TINY studio. One bed is 3500$. You want a second half bath – your rent is 5 Gs. You can imagine that vacancy rates are 25 percent, which is a lie. One of the buildings I delivered to is only 25 percent full after being open for three months. Six more towers ACROSS the street are now opening.

Greatest (and last) overbuild EVER

Banks are still making deals right now, into a steepening interest rate invironment. Pure insanity!

I joke that when the FED bails out all these guys, AGAIN, every domicile in Seattle will worth 10 mil, and all of us non-banksters, will be homeless.

Some of my Canadian friends who studied Computer Science & IT at Waterloo got jobs in Seattle.

They were offered to work in the tech hubs like Microsoft. Lots of Canadians are being hired. I thought America was Americans first?

“I thought America was Americans first?”

Some Americans are more equal than others, and the more equal you are, the more first you get.

For example, Cheap Labor Conservatives like cheap labor, which is why they replaced two million American IT guys with cheap foreign imports twenty years ago. Hackware – buggy, over schedule, and over budget – is highly cost-effective, and still good for firms specializing in software project salvage operations.

Keeps profits up and “keeps prices down”. Everybody wins, except the two million former American IT guys who have trouble holding down their Amazon warehouse and Uber driver jobs. Those are losers. So are the software engineering clients who contracted with foreign imports who did deploy the software but won’t deliver the actual source code because they wrote it, so it belongs to them.

Long story, very sad. DTMB spent two years suing them but gave up trying to deport them as undesirables.

So Canadians working in the USA are like the Indians who work in Canada? Cheap labour?

Easier to hide because the Canadians from Waterloo look & speak almost like Americans?

“Easier to hide because the Canadians from Waterloo look & speak almost like Americans?”

Language skills in software engineering become important when you’re having root-level discussions of unabstracted asynchronous pseudoparallel hyperthreaded secure phantom-finessed client/service implementations and you need to figure out which scapegoat is taking the fall for locking up the California state payroll system for two weeks. Hence the resort to non-EFL/non-ESL Manitobans with provable high-end credentials.

Canadians are the guys who lack facial hair, speak in complete sentences, and don’t pack heat. That’s always a giveaway.

Extra points if you can figure out how to parse this comment into an accurate English translation.

Easy…

See these guys over here… they suck…

See those guys over there… they don’t suck…

Choose wisely…

“Canadians are the guys who lack facial hair, speak in complete sentences, and don’t pack heat. That’s always a giveaway.”

Such boring, fabricated stereotypical BS.

So true! I am one of those American IT workers who saw wages and quality disappear down the black hole of outsourcing on the dot com bust 20 years ago. It’s not worth it to major in CS anymore!

Are the Canadian workers being paid less than the American workers?

A lot of Canadians are working in tech in Seattle and San Francisco for some reason.

“I thought America was Americans first?”

Not at all in the IT industry. Federal government contractors and smaller local companies still hire a lot of native-born Americans like myself. But in the big-name corporate environments where I have worked in the past, we are a small minority. There are *lots* of H-1Bs in the larger companies.

I have been in IT for 30 years and I can say most Americans that can’t find jobs have a bad work history. Either they do not show up, don’t work well with others, or expect double for the privilege of working with them.

I fought through those times and continued to work in IT (started 1999 left in 2017). I worked at Intel, Microsoft, Mutual of Omaha to name a few of the big corporations. I know very well the H-B1 scenario. My career stagnated. I was replaced by them a dozen times or more. I had invested my whole life into that industry I did not see an out. Eventually age being over 50 did me in so I had to leave. I was probably one of the most knowledable and capable people at my sites but the politics and favoritism given to the majority not me the minority. I was a fool to stay in the field as long as I did. Now I have PTSD from all the years of being bullied there. On disability because of all the trauma I endured for nearly 20 years. I was born in this country. I worked hard and sacrificed everything for a pipe dream.

Rents are so high because many of the Chinese who bought there leave every house and apartment empty with no renters which tends to push up the price of rents.

Seasonally, this time of the year is the beginning of the house buying season because of many reasons such as kids being off the school, etc. And, if the mortgage applications are dropping, lets see what will happen in winter just around Christmas time.

Re “… end of the monthly savings from lower mortgage payments, … getting spent on goods and services…”

Those cash-out and lower-rate refis were probably the main “wealth effect” transmission channel. On one side: Tons of middle class homeowners needing every dime they can scrounge. On the other side: a very few truly rich people spending an extra $100K on bling just because their stocks were up.

The party is over and the punch bowl of hopium is empty. Time for folks to start dealing with actual reality!

We’ll see, I expect PPT to come back from their vacation tomorrow and along with those hopium dip buyers the market will have a rip your face off bear trap rally tomorrow

The bar where the PPT hung out today during trading hours, instead of doing their job and buying everything in sight, ran out of booze, according to sources familiar with the matter. There are now concerns that top-ranking PPT members are already scouting for another bar with a larger supply of booze for tomorrow as morale at the PPT office has collapsed due to the hopelessness of the situation, according to another source whose existence could not be independently verified. According to the source, there was wild clapping and cheering as they were watching on the screen above the bar how the Nasdaq was careening lower and closed down 4.7%. There is however a core group in the PPT that promised Yellen and Powell in a personal Zoom call from the bar that they would show up at their trading desks tomorrow, if they’re not too hung over, and use the $16 trillion in secret money that the Fed has secretly made available to them to buy every stock in sight.

Hello, my name is PPT…

and I’m an alcoholic

:-(

This is becoming concerning as PPT is too important to fail at their job. I have called the right people and a AA intervention will be held soon…first step to help is to acknowledge there’s a problem.

“The bar where the PPT hung out today during trading hours . . . ran out of booze”

Those must be the guys who use Wolfstreet root beer mugs for shot glasses.

“use the $16 trillion in secret money that the Fed has secretly made available to them to buy every stock in sight.”

Are rush startup IPO services still available? I’d like to crank up a hyperdisruptive vaporcorp and send its stock price on an all-expense-paid round trip to the moon.

That’s all good.

They ensured in advance that there was not enough supply and bought derivatives that more than offset the bar tab. They also owned the bar. Win Win.

Further on down the road at Buffalo Wild Wings, one rookie PPT inductee was forced to reconsider his undying devotion to fearless leader J-Pow when hazing rituals got a bit out of hand. Local PD were alerted to the scene where duct tape and blow darts left unsightly marks on the poor boy’s nether regions. Analysts from CNBC were flummoxed and dismayed by a lack of cogency to the proceedings. Markets did a quick U-turn and bonds seesawed in a typically illogical but by now predictable fashion towards bondage as rent slaves lifted the palanquin of Elon Musk out of the squalid mire. Martial law was quickly instated to quell the proletariat seated at bar benches and the Pow doused the inflation-haters with a freestyle lyrical hurricane of financial prowess putting all nay-sayers in their place. The fuzz were confused and alarmed but also slightly aroused by the evening’s display of bacchanal with just a tasteful dash of homoeroticism. Trump-appointed Federal judges with zero judging experience presided over proceedings and handed down a hearty bum paddling for all involved, and there was much rejoicing.

The PPT should only be there to prevent people from jumping off of buildings like in 1929.

Maybe last chance (this summer) to sell before home prices go south.

I’m very confident the bond mania is over. It’s the one that matters most.

I’m less confident the US stock market mania has ended (yet) and global stock markets have peaked.

The housing market will take longer than stock markets.

I agree completely. The housing market is slow moving and is quite likely in the topping process (which can take a year or more).

The stock market index charts, when looking from a sentiment charting perspective, make a very strong argument for one more leg higher.

Stock market sentiment isn’t actually bearish. I’m aware that many technical measures are bearish, but the overwhelming majority (individual and institutional) still believe in buy-and-hold forever.

Heavily “oversold” is also a traditional set-up to a market crash.

I wouldn’t bet on another advance. I’m staying out instead of shorting because of the manic psychology.

Just wondering how much of the lower level non-institutional flippers have all these 2nd homes riding up the higher prices on margin loans. And what percentage of the institutional investors will dropout once the fever breaks.

Stonks only go down for a few months, prices sag, everyone tries to unload. Population hasn’t exploded 20% every year, nor has a so called demographics shift convinced me. I hear a whole lot of snotty middle aged women bragging about a second home to each other or cash out refis while grocery shopping or running errands. Something I’ve never experienced except when I was a kid in the mid-2000s.

Only time will tell though. I’m eager to see how much this current economic climate will shake out for my work. Being boots on the ground; anecdotal observer of America’s road trip vacation destination.

But remember what the MSM is telling you…there’s not enough supply of houses and we’re still short of supply and also Gen Z and Millenials will continue to keep price steady and strong….

Not this Gen Z.

My Millennial siblings barely have C$15,000 in savings after working in contract jobs for a decade (since 2011). The GTA rents eat up most of the paycheque unless one wants to live in a room located near the furnace of a Boomer’s basement for at least C$800 a month.

Anecdotal evidence, but I’ve been watching a specific luxury housing development in the suburbs of Seattle that has about 150-200 homes. Up until about 2 weeks ago, houses would sell within 2-4 days, and inventory would be 2-3 homes for sale at any one time. Two weeks ago, it’s like a switch flipped off. Ten homes hit the market and all of them are still for sale after 8 days, except one that is pending.

Things appear to be turning in some frothy areas, as expected. The price declines will likely appear soon.

One comment……for years we have been screaming for higher rates……nobody listens…….

Now that the Walton and Dayton families are taking it in the shorts……..it don’t matter how many get unemployed …….Jay is going to raise rates…….

Another all-time high for RRPs. Waiting to see it bust through that 2T ceiling any day now.

RRP demand swells to new all-time high of $1.973.4tn; 2tn barrier within reach

18 May 2022

And this in the absence of EOQ window-dressing by the banks.

“In this context, “volatility” always means sagging stock prices, because no one complains about upward volatility, and stocks are croaking.”

So true. You’ll never hear of a class action lawsuit with an increasing stock price. The lawyers are going to be working overtime for the next few years to come.

And the Vix just means up or down, not magnitude of recent change. Something is fishy with the vix.

We need an instant rate increase of 2%, and 1% on mortgages! But, can the system junkies handle it?

Can Warren Buffett swim

of course not, he’s from nebraska!

Ace !!

Ayyyy!

Jay stayed up all night adding two and two and kept getting 7……..so he had to state today……it might not be so soft a landing after all….its going to be challenging…..going down with transitory as one of his comedy act best. Just a week ago it was strong employment will insure a soft landing.

I truly believe that the last fed chair we had that had an IQ above 110 and did not sell his office furniture was Volcker. Since him its been one used car dude after another.

Whats the trifecta going to be……..it has to be a word that describes a depression that does not hurt……how bout…..statistical depression.

There you have it…..transitory inflation, challenging landing and statistical depression.

Yep…..he will go down as a great one……I can see why he was renominated and confirmed……just last week……he fits right in with the leadership in dc.

Well summarized FF.

Didn’t the FED just announce yesterday that the rate hikes were already priced in? The wipeout today is just more egg all over these clowns’ faces. How about they STFU and go away for a while? Just raise rates and quit yappin’ your jaws, boy! If we want to hear more out of you we’ll squeeze that puny neck. We’ve reached “peak FED.” These self-important aszholes have ruined everything they touch.

My question is: How long will the institutional investors, at least $55 billion worth over the past two years, stay in the market with capitalization rates declining due to increased taxes, inflated maintenance costs and lower rents due to turnover, add in declining market value and compare it to investing in an MBS fund?

Anecdote: Spoke to three young men, two engineers and one financial analyst between 28 and 34 last week. All are married, and have or are expecting children. All three said they are happy to rent until prices come down to meet cost of interest , better to pay rent for a while than to “buy” $100,000 + worth of “equity”.

Institutional RE money is not “hot” money like with mom n’ pop investors. Most of the investment is done in funds that have a 10 year life, and the manager can usually extend the fund if the circumstances warrant it.

And even if the cap rates/yields tank from falling rents, they’ll still likely be above 0%, which means no forced selling. Finally, those funds aren’t constantly marked-to-market like equity/FI funds.

I wouldn’t count on much action coming from institutional investors.

Pension funds and insurance companies can become hot money if equity holdings are too low to unload.

My logic:

Equities down 20%, SFR up 15%. Which do you sell? Which do you hold? If you sell the equities your loss is permanent, if you sell the SFR investment your gain is locked in.

Remember that you have an annual report to provide to your stockholders/stakeholders coming up and need cash.

A friend at a retail investment brokerage sent this to me last week. Interesting stat:

“An investment fund backed by Goldman Sachs recently purchased an entire community of 87 single-family rental homes in Palm Bay, Florida, for just over $45.7 million, according to Fox Business. Data from ATTOM shows that institutional investors purchased 530,025 homes in the U.S. in 2021, a new record high and more than double the 205,934 homes purchased in 2020, according to Housingwire.com. The 530,025 homes accounted for 8.4% of all home sales in 2021.”

To your point, Bobber, these investors are not necessarily “long-term.” As investment partners, they are not to be relied upon when the going gets tough.

What you describe is this: Entire portfolios of existing rental homes are dumped by property developers and management firms, and bought by PE firms and pension funds. Meaning, one company sells is existing portfolio of rental homes to another company. There is a lot of that going on right now.

Don’t confuse that with investors buying homes that weren’t rental homes but were sold by homeowners. There isn’t a lot of that going on right now, given the very unattractive prices.

If the Bank of Canada mandate is to keep inflation within 2-3%, then the BOC should HIKE rates beyond the current 8% inflation rate to tame inflation.

I could care less of those speculators, money launderers and well-off Millennials who bought overpriced million dollar homes in rural Ontario. That’s not my problem.

Jim Cramer will be s$iting in his pants during his morning show on CNBC tomorrow morning. Total diharia. He may need to bring a change of pants to get through the whole hour.

This has to be one of your best lines.

“Thank god that only the taxpayer is on the hook here from get-go, and not the banks, which means that the Fed can let this one rip.” Wolf Richter

1) SPX : suppose May 12 low hold. May Monthly might be red, or green, but it doesn’t matter if the markets will move higher from June on. Q1 GDP was positive. Q2 might be, no recession in 2022. Case closed.

2) JP might hit another 0.50 for the third time.

3) The third 0.5 bullet will strike the economy and injure it badly.

4) JP emergency room will nurse the economy with RRP band aid to save the economy.

5) JP will pray for miracles.

I almost feel sorry for the folks who over leveraged to bid up prices way above listing. ALMOST, but no.

Get ready for real estate agent mass layoffs. During the good times everybody with a pulse gets licensed and can sell what ever comes to market. Soon only the old pros will be left. Happens over and over again.

During the last RE bust, my old realtor actually showed up at my house one night. He was wearing a funny polo shirt and hat and he had a pizza and some hot wings for me.

That’s the least he could do for 6%

When I opened the wing container, there were only 9 wings instead of 12. And the pizza looked awfully light on toppings. Hey former realtors have to eat too.

I didn’t know realtors could count change. Color me shocked.

I thought GDP was negative and Wolf had a great summary of why that number would turn back positive. Regardless no recession in 22.

Stock market prediction I can not . I am consistently wrong in fact if I just use my emotions and trade opposite better results.

Stock prices don’t move with GDP. Or else the S&P 500 would have never gone over 1,800. Stock prices move with money printing and interest rate repression. Money printing has ended, interest rates are going up, and QT will start in a couple of weeks. It’s not a mystery.

The economy can do just fine with stocks going down. No problem. China’s stocks peaked in 2008, and now are about 60% below the peak despite a lot of GDP growth since 2008. Stock market bubbles are fake values and those values vanish.

China’s economy detached from the stock market because the credit bubble expanded exponentially after 2008, mostly into real estate based upon the reports I have read.

If the bond mania from 1981 is really over, the US (and global) economy will absolutely not do fine.

It’s not going to happen overnight (retracement with a countertrend rally in bond prices to partially offset 2YR bear market) but interest rates are going to blow out in the next advance. Junk corporates are already starting to “suck wind” with rates having doubled recently. Other new borrowings will be next (especially for corporates where most have garbage balance sheets) and then it’s refinancing at higher and higher rates for everyone as debt matures.

This has been the biggest asset bubble in the history of human civilization and it’s one that is going to take decades to unwind, unless there is a complete crash.

The actual long-term economic fundamentals totally “suck”. No soft landing with the end of this mania.

Wolf hilarious PPT bar instead of buy! Secret rooms secret money and secret ownership!

Like you Ben I thought it was clever high parody and had a laugh. But then I thought… could that really be the way it is? is it so far fetched? Started reminding me how I am reacting to each episode of Gaslit.

My little slice of flyover the phones are quite for mid may. We will tip into recession this fall.

Waiting list , even with cancellations, will keep us busy until the fall.

As prepared as we can be with cash and no debt.

Road kills could get scarce by winter.

Here in a NYC suburb, good houses in good school districts are still getting sold in a couple of weeks. but houses with issues (near highway, flood risk, very old, no yard etc.) are sitting in the market longer. Last year, these were asking for ridiculous prices and selling with multiple bids for ever higher prices. Nevertheless, prices are still DETACHED FROM REALITY but I have seen some price drops. may be things will be a bit normal soon.

How did you end up in the farmer’s field?

Stupid deer wouldn’t stay on the road!

Great article, thanks.

Mohamed El-Erian spoke on CNBC this morning. Some time ago he seemed to become motivated about the size of the asset bubbles the banks were instructing the Fed to blow so that they aren’t a systemic problem for the financial health of the United States any more.

As I understood what he said, my interpretation was that Fed should resist, by his count, the fourth and most dangerous policy error identified during the Fed keggar.

His recommendation, don’t move too fast and destabilize the financial markets while assets are being be repriced. The results are baked in the cake. Don’t make it worse by instigating a crash. I think house prices have a similar future as the stock and bond markets.

I’m not sure I agree completely. Economic policy is completely emotional, gut level intuition, backed up by a variety of estimated outcomes and a list of winners and losers.

I suspect that Mohamed’s point of view is that the bets on the felt, the masters of the universe whom have constructed this disequilibrium but need to be rescued again because if they lose, mama won’t be able to find work to buy the formula that her new born needs.

Meanwhile, the goddamn inflation is reducing the buying power, and savings and pay, of 95% of the citizens by 10pct per year, every year that it persists. Duty as a patriot, demands an immediate stop.

They should raise the rate by 0.75 pct in the June meeting. Screw em. Give the wall street wise guys the losses, not give them time too continue to screw the population with their entitled games.

The ivies are trying to tell us how the whole economic picture is complicated because it’s determined by marginal components of the result, the dependent variable. Furthermore, it’s scientific so that, even though it may seem untoward, it really isn’t.

Lately, they’ve been on the path preaching that inflation really isn’t the fault of there darling, Fed, that feeds them.

Unfortunately for me, I don’t believe them because I have been cursed with the delusions that arise from being a citizen of the US for many decades.

I am going to say out loud what I think is the cause of inflation:

Policy by an incompetent and reckless Federal Reserve.

dang

Add in reckless spending by Congress which has been largely monetized by the Fed

dang,

In my opinion, it’s a good idea for the Fed not to go too fast. This needs to be spread over many years, not 4 weeks of total mayhem. If there is a huge meltdown and financial crisis, that’s not a good idea. I think at this point, 50 basis points a couple meetings followed by 25 basis points and $95 billion in QT per month sounds about right. And give markets some time to reprice themselves in a more or less orderly manner.

The Fed is already 12 months late to the party. Many years sounds like more than 3 or at least 4. You want the Fed to unwind the housing market & financial markets over 4 years? That’s completely unrealistic in terms of returning to acceptable inflation. Moreover, that would mean housing doesn’t decline more than 10% over the next 18 months. At that pace, it will barely scratch the increases we’ve seen just from 3 months ago. And, it may mean continued price increases for 6-9 more months in markets like Phoenix. The housing market needs at least a 25% correction, with 35% over the next 3 years being a very reasonable decline which is only 24 months or so of appreciation in most markets.

Currently, the markets are repricing themselves at a very reasonable pace. The DOW has sustained an orderly decline of 4,000 points in about a month, and that’s with the Fed doing nothing but raising the FFR 75 basis points. Once it sheds another 1,000 points or so, we’ll see a sustained rally for part of June. Then, it will be time for it to keep dropping. The best-case scenario is for us to find the bottom within 12 months. Protracting it out longer than that ensures housing doesn’t reset to the extent in needs to in a timely manner nor does it ensure inflation is brought under 5% which is still high (2.5x the Fed’s target).

And, JPowell can’t control all of the inflationary inputs the current administration is creating and plans to accelerate in the coming months.

Inflation has to be tamed to avoid Trump.

That will dictate how aggressive the Fed is.

“And give markets some time to reprice themselves in a more or less orderly manner.”

The sensible approach. And yet there are other pressures on the US and global economies which are not financial pressures and may be important:

– There’s The Plague, resulting in lockdowns in China as well as inefficiencies generally.

– Some shortages have not abated, and additional shortages are likely, starting with food, because of drought in the US west and in Europe, and because of increasing weaknesses in non-renewable natural resources.

– Debt is high and will continue to need to be serviced, under conditions that have deteriorated.

– Political situations are unstable and promise to contribute adverse effects of their own, some serious.

And so forth. I started to write a paragraph on how each of the moving parts is going to be adversely affected but there are a lot of them and it got to be confusing and then I remembered that I’m lazy so I gave it up.

Mohamed El-Erian and others are starting to talk about stagflation, and that’s bad, but I got in ahead of them weeks ago, so that’s good, but only for me.