You’re just “unsecured creditors” if we file for bankruptcy. But hey, CEO tweets: “We have no risk of bankruptcy.”

By Wolf Richter for WOLF STREET.

Crypto exchange Coinbase Global not only rattled its already tortured shareholders when it reported horrific results afterhours on May 10, but also its crypto holders, when it added new language to its quarterly filing with the SEC, explaining what could happen to their cryptos at Coinbase if it files for bankruptcy.

In the same breath, it filed a shelf registration with the SEC to raise more money by selling shares, whose collapse has made selling more shares to raise money much more precarious.

Then Wednesday afternoon, the whole situation was made worse, amid general mayhem in the crypto markets, when the CEO came out with a tweet storm and said among other things, “We have no risk of bankruptcy.” Oopsiespalooza.

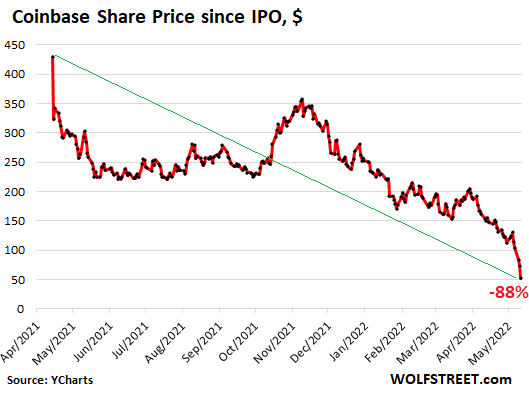

Shares of Coinbase [COIN] kathoomphed 26.4% during regular trading today and another 3.2% in afterhours trading to $52.01, down 88% from its intraday peak on April 14, 2021, thereby earning itself a prominent spot in my column, Imploded Stocks.

April 14, 2021, the day the shares peaked, was of course when Coinbase went public in a mega-hype-and-hoopla direct listing at $381 a share. The share price then spiked to $429.54 intraday and closed that day at $328.28, giving the company an inexplicable market cap of about $88 billion.

Well, let me retract that. The market cap was very explicable because these were the craziest times ever, and every bit of hype and hoopla was eagerly absorbed amid the craziest bout of consensual hallucination ever that by far outdid the dotcom bubble.

And these folks got literally thackamuffled to the point where the huge percentage thunkadunk today shows up on this chart as just another step in the stairway to heck:

Revenues, transactions, and users plunged.

Coinbase reported a loss of $429.7 million for Q1. We’ve gotten used to these kinds of horrifying numbers by now. Coinbase is following in the footsteps of a lot of startups where management somehow believes that bigger losses are better losses.

Revenues – most of which it generates through transaction fees – plunged by 35% to $1.2 billion. Both the loss and the plunge in revenues were a lot worse than analysts had expected.

Revenues plunged because monthly transactions plunged and the number of monthly users also dropped. And Coinbase said that it expects the number of transactions and the number of users to fall further in Q2.

Turns out, cryptos aren’t fun anymore. They’re money-sucks – I mean fiat-sucks. Prices are plunging. Bitcoin is now at $27,144, down 60% from the peak in November. How the heck are you supposed to have fun trading, when you get powwoozzled on a daily basis? But Coinbase needs people to trade so that it can extract its fees.

You’re just “unsecured creditors” if we file for bankruptcy.

Then folks started reading the new language in the 10-Q that Coinbase filed with the SEC. It said that if Coinbase files for bankruptcy, while it has your beloved change-the-world cryptos in custody, you and all the others could be treated as “unsecured creditors.”

The new language is in the middle of other delectable morsels and says this:

“Moreover, because custodially held crypto assets may be considered to be the property of a bankruptcy estate, in the event of a bankruptcy, the crypto assets we hold in custody on behalf of our customers could be subject to bankruptcy proceedings and such customers could be treated as our general unsecured creditors.”

But hey, “We have no risk of bankruptcy.”

That language caused enough of an uproar that CEO Brian Armstrong decided to do some damage control on Wednesday. In a series of tweets, he tried to soothe the nerves of Coinbase’s users, and extended his “deepest apologies” to them for not including this language sooner, and communicating the inclusion better to the users. He said among other things:

“We have no risk of bankruptcy, however we included a new risk factor based on an SEC requirement called SAB 121, which is a newly required disclosure for public companies that hold crypto assets for third parties.”

He called a bankruptcy filing a “black swan event.” Which was totally reassuring, given the history of black swan events.

This comes amid chaos in the crypto market. Big names are shookalacking. And stablecoins, which are supposed to maintain a value of $1, are becoming unstable. TerraUSD started careening off its $1 range on Monday and promptly kathoomphed to 30 cents, before bouncing, then relapsing, then bouncing, and relapsing again. At the moment, it’s at 60 cents.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Countdown to rate cut and QE 3…2…

Countdown to QT…

Kinda like last time?

i.e. only until the market throws a tantrum….

The Market will throw a tantrum, a “Spit the entire dummy” tantrum, However the market is greedy and will find a base on that and then bloom.

What really is a concern is inflation, it eats, like rust in metal, slowly but effectively through all assets, everything.

This Genie is out of the bottle and a 0.5 % rise in prime is tickling it with a duck feather. It needs to be contained or it will eat everything.

Unlike last time, this president never talks about the level of the S&P. Very different. Unlike last time, inflation is raging. Thunder’s description is apt.

Bitcoin is death

Don’t worry, when markets go down another Fed head will come out and use his mouth to make it go up again.

Donkry Punch,

The market has been going down, and we’ve been eagerly waiting for Fed heads to come out and make it go up again, and instead they came out and palavered about QT and 50 basis point rate hikes and actually did the rate hikes and made markets go down further. This is just an upside-down world, these days.

Ah, QT, more fed gossip on the quiet.

Fed has blown up assets by squashing rates. Start punching 3% risk premium and higher 10 year treasury rates into a dividend discount calculator and you can see it will not take much to pop market and kick off recession.

Try a 6% 10 year and you will get S&P around 800 depending on what you use for nominal growth rate. Don’t think we will get to 4% on 10 year before it all falls apart.

Don,

Who will be the last tightening denier left standing?

@ Wolf Nomi Prins?

Those of us who LIVED through the 70s inflation and the Volker days, who witnessed the grinding of the 90s, the dotcom bust and GFC, we know it’s different this time.

Inflation as you have said so many times, is entrenched in the economy now.

Low interest rates and QE are not on the horizon at the moment.

Inflation is a monster!

How da hell all the central bankers were so callous, it beats me.

“If you don’t do the right thing, the right thing will be forced upon you”

That’s exactly what is happening. They kicked the can down the road too many times.

I am very curious to see the future interactions of:

Fed raising interest rates,

Fed sales and redemptions while not buying Treasuries,

increasing national debt as we airlift cash to Ukraine,

growth of US debt interest

loss of tax revenue with falling stocks and possible recession

BTW, is the student debt an asset that offsets part of the national debt?

joe2,

Yes, the student loans held by the government are an asset on the government’s balance sheet, and therefore are an asset for taxpayers.

Yes, the $1.6 trillion that the government handed to students was borrowed and that amount borrowed is now included in the $30.5 trillion government debt. It expected to get this money back plus interest (hence an asset).

But by forgiving student loans, the government will no longer have this asset. All it will have is its own debt that funded those student loans, and it will have to continue servicing this debt. And that $1.6 trillion in debt that was used to fund the student loans won’t go away when the student loans are forgiven. Lot’s of people don’t realize this.

“thing will be forced on you”

Quantitative Easing (formerly known as money printing) has always been Savings Rape.

But hey, DC’s short term political interests always come first.

And I think a decent argument can be made that DC authored stealth inflation (appropriating most of the possible consumer savings from the 20 yr China import explosion) has been with us for 20 yrs.

But you are right that now the wheels are completely coming off…DC can’t hide/obscure explosions in auto and housing costs (although it is amazing that the MSM has complete radio silence on these core topics…an accomplishment right up there with 20 years of saying absolute zero about having bank CD returns zero’ed out).

The FED is doing exactly what they are supposed to do.

The CBs did their jobs – they maintained the status quo and propped up their job security. That’s the definition of bureaucracy. Just happens to be against the interests of the majority, which is by design in the USA. Private profits and socialize losses.

Exchange your Bitcoin for a Tesla before its worthless.

Do you mean like TERRA LUNA that was at $86.09 eight days ago and now is 0.0046

Cathie Woods is selling Tesla stock and buying GM

Wolf,

I know you are firmly in the QT-Fed-Has-Finally-Grown-a-Spine camp right now, but the QE-Fed-Has-Chickened-Out-For-20-Years camp is probably entitled to a semi-detailed debate…and what a post it would make!

I’m semi-undecided right now (although 20 years of grotesque DC/Fed mismanagement is an empirical observation, whereas continuing QT is simply a prospective, ahem, speculation…).

My sense is that your QT faith is largely based on DC’s political need to beat back current obvious inflation (vs. 20-yrs-of-steal-the-China-savings-stealth-inflation…) but you may have other arguments for why QT will stick this time, despite well deserved blood on the Street.

And what a post it will make!

This is really funny, after a while. The QT deniers will be dogging this comment section until after QT actually shows up on the charts of the balance sheet, which may be in late June or in July, given the lags and bumpiness of the weekly balance sheet, where every little bump will trigger loud screaming in the denier camp that the Fed is STILL doing QE, and where every drop will cause icy silence in the denier camp. And then, eventually, when QT is clearly visible in the chart, the denier camp will change strategy and switch to “the Fed will re-start QE next week.” It’s always the same, been that way since 2017.

I agree with Wolf on this one. We’re just getting started with the VIX ramifications of ramping up QT. JPowell won’t be the 2nd coming of Volcker, but he’ll be a mini-Me , meaning he’s got to stay the course for quite sometime to tame above 8% inflation. Even with a 1.4% decline last QTR, there’s still a ways to go with taming personal consumption / services.

The perfect storm for oil & natural gas continues to evolve. War in Ukraine, EU at chanting they’re “cuts to Russia oil & gas”, & FJB himself, who just cancelled a new oil & gas lease previously approved in Alaska. These crazy people running DC are fat, dump & happy with high oil & natural gas prices.

Inflation doesn’t go down materially without three things:

1) FJB out of office

2) Russia out of Ukraine

3) JPowell channeling his inner Volcker mini-Me.

The FED is beholden to the Stock Holders.

All corporations are to enhance the stock holders.

As George Vanderbilt said: “The Public be damned.” which, of course, was taken out of context since he followed that phrase with the fact it was the Stock Holders he served. Not the Public.

The FED is doing a very good job. Enhance the assets prices as high as “possible”. Give the Stock Holders time to sell, then make the assess drop, so that the Stock Holders can re-buy at the bottom.

Rinse, Repeat, Rinse, etc.

Thus, the QT will occur. Assets will go down, the public be damned, and the stock holders will do just fine.

Bond rates are coming down, in spite of higher than expected CPI print and record PPI. Why? Because smart investors know that Fed will make a U turn the moment there is any real danger to these loss making corporations and to the asset bubble and holdings of the wealthy. So far losses are paper losses, no real bankruptcies and bond write offs.

Remember Fed is the biggest criminal organization ever created and all this window dressing is because of the upcoming mid terms.

The 10YR has come down a whopping 20-25bp from the recent peak.

Bonds have been in a bear market for over two years, yet UST are still near the lowest rates ever. No market moves in a straight line.

Keep on believing it.

Dying bond bubbles make dead-cat bounces in the same way that dying stock bubbles do.

No, Kunal, I think rates are coming down because they think it’s not going to take 8% or even 5% fed funds to knock inflation down. The Fed won’t be making a U turn to save markets, they’ll be stopping to ensure no overshoot that crushes the economy any worse than necessary.

Theory I like is most of the debt accumulated since GFC didn’t go to productive investments as can be determined by low levels of productivity growth. Now we have auch bigger debt to service, but not the real economy to service the higher debt payments.

Solve the equation for amount of debt service society can service and you will get the maximum real rate. It’s a very low number before the defaults start.

Why are college debt payments suspended with inflation at 8%? I thought we needed to reduce demand. You get rid of debt by sticking it on the government balance sheet and financing it at a negative real rate. FHA and VA loans might be next.

Better check on China

Wolf, I hope you can write an article about the following, thank you.

Not long ago, the Federal Reserve announced that the net assets of U.S. households in the fourth quarter of 2021 rose to about $150.29 trillion, a record high. According to the population of about 332.4 million, the per capita net assets of American residents reached US $452000. Compared with 2019, the net assets of U.S. households increased by $33.5 trillion, with a growth rate of 28.7%.

Among them, the shares held by American residents reached $49.6 trillion. U.S. home ownership rose to $38.1 trillion,

This is part of my quarterly wealth disparity monitor, which looks at this based on Fed data, and categorized by household wealth.

The next quarterly update will come in about two months. This is the prior one through Q4 2021:

https://wolfstreet.com/2022/04/03/my-wealth-disparity-monitor-of-the-feds-money-printer-era-holy-moly-april-update-of-the-greatest-economic-injustice-in-recent-history/

When I checked FRED which I infer is based upon the tri-annual survey, “real” median household net worth was a whopping $121K.

Up 10% (adjusted) from 1998.

There is constant movement up and down the distribution and the median now includes people who were too young at the time.

Still, it’s obvious the typical American has gone nowhere financially (at best) during this time, one of if not the weakest performance ever.

This pathetic performance was also during the biggest asset bubble in human history.

What’s the data going to look like when the mania crashes?

It’s a rhetorical question.

I always say you can look at wealth either at market price or the amount of real cash flow the asset can produce.

By suppressing interest rates Fed blew up the first number, but you could make the case that the cash flow of stocks, bonds and real estate is going to be negative in real terms for the next decade.

What is a dividend paying utility or 10 year Treasury worth today paying 3%? Or a REIT paying 4%? Not very much unless inflation gets back down to 2%.

Wall St. bandits win again pocketing billions from brainwashed American Patriots rushing blindly into yet another scheme. 9/11, GFC, QT, COVID n now SPACs. Expecting anything different results is either stupid or madness. Ukraine will be proven in due time, enjoy the latest tale but do follow the money.

Other than letting maturing securities expire, I do not see QT in the cards. That is, unless they sell assets at a loss, which is quite possible since they creat fiat at near zero cost. It is amazing that Wolf beats up the fed with one hand and then defends them with the other. What will he say if proven wrong by the ‘deniers’? Admission?

Gilbert,

Letting maturing securities run off the balance sheet without replacement = QT. And the markets obviously understand this. As does everyone else, except maybe you.

Is that the latest thing that tightening deniers now are hiding behind, the verbiage that letting maturing securities run off the balance sheet is suddenly “not tightening?” That’s kind of funny.

I beat up the Fed for letting inflation rage and doing QE for years and repressing interest rates and thereby doing untold damage to many people and the economy for the sole purpose of inflating asset prices. When the Fed finally and in baby steps (“too little too late”) is starting to back off its disastrous policies, it’s a good thing obviously, even if it’s too little too late.

Delusional are we lol. Countdown to QE 4. Months ago you said they would start QT. Still waiting. As I stand here and breath the purchasing power of the dollar is just dust in the wind. The mighty dollar is losing purchasing power against the Russian Ruble, Brazil Real even the Mexican Peso. It so toxic nobody even will take it for oil.

Anonymous,

You’re spreading idiotic BS to manipulate. Months ago, I said they would end QE, and they have now ended QE. Months ago, I said they would raise interest rates, and they have now raised interest rates. Months ago, I said that they would do QT after they ended QE and after they started the rate hikes, and now that they ended QE and started the rate hikes, they will do QT. QT will start in June, and we will see the first effects on the balance sheet in late June.

Anonymous,

And in terms of the dollar, check out the DXY. The dollar has been red hot.

IMHO Federal Reserve will not show any real concern about the state of markets until indexes fall significantly below the levels that they were at in the fall of 2019 (right before the pandemic). For S&P, that would be something around 3000 (-25% from where it is today). And even then QE is unlikely IMHO; more likely is a temporary delay in rate hikes / QT.

The people who are claiming that the Fed will abandon the fight against inflation for this reason or that are forgetting one thing… NOBODY on today’s Fed wants to go down in the history books as having failed to contain inflation. Their PERSONAL reputations are riding on getting this right in the end.

They will obfuscate the inflation on COVID and RUSSIA. It really has become quite a comedy of failures. Origianly it was you can’t get TP because everybody was buying, then it was you can’t get computer chips because of the shutdowns due to COVID, then you had to pay through the nose for used/new cars due to chip shortages, now gas is at ATH due to RUSSIA… the blame game go round and round

Correct, but apparently, this doesn’t matter.

Reading the financial press, it’s been evident (for months) that FOMC members are “losing face”.

They care a lot more about the opinions of their peer group (economics profession) and having Congress breathing down their necks than many who post here believe.

They ‘already’ have failed to contain inflation. Sounds like ‘inflation’s increase is decreasing’. Personal reputations? HA!

Exactly.

People should read Danielle Di Martino’s book “Fed Up”.

The Fed is a bureaucracy. Nothing’s more important than avoiding undeniable serious error.

Inflation is hitting a very large fraction of the population very hard. Rents and homes at unaffordable levels. Food prices leaping upward. And diesel and gasoline. Hitting both young people and, especially, retirees.

If they don’t get inflation under control Congress will threaten their independence. As a bureaucracy they must defend that above all else.

The stock market and crypto bubble psychology is being broken. As it was dependent on unprecedented money-printing, only even greater money-printing could reinflate it. The Fed cannot start another round of even greater QE.

We’re about to see an absolutely incredible run on the crypto bank “stable coins“. The stock market crash has already wiped out $20 trillion of illusory wealth. The crypto stable coin run will probably wipe out a hundred billion plus of real wealth.

Not sure they care as long as they go as multmillionaires.

This seems to be one of those repetative statements tossed as iron clad truth.

Same as: fed is trapped, they’ll never raise rates, and they will drop rates as soon as market tanks….

If the Fed sticks to its QT and interest rate hikes, I am guessing that the S&P ends up at or below where it was in December 2018. Around 2500.

The idea that the FED is going to ignore inflation and decide to start pumping QE to save the crypto market is on of THE most delusional I’ve yet heard. Just laughable beyond comprehension.

We need an immediat rate increase NOW!

The Fed has no choice now but to taper. Powells most recent statements include gems like: “executing soft landing may be beyond our control”

“Process of getting inflation down will include some pain”

“With perfect hindsight it would have been better to act sooner”

“Inflation is just way too high”

I guess he had to wait for confirmation of reappointment before he could come out with the real truth

I see a lot of people talk about Fed doing a soft landing.

But nobody has defined what is ground level. Is that a 3% CPI? a 5% unemployment rate? Any consideration to asset price levels? Or to its own holdings (which has gone up by $1.5T since Jan 21)?

How much will the QT shed? 2020 levels? 2015 levels?

Or is it a nebulous concept to justify pretty much any monetary action?

good one NBL!

Please keep on here to share YOUR insights with us who are absolutely/certifiably ”learning” on Wolf’s Wonder.

Thank you.

and to be very clear,,, NO sarcasm at all in my comment…

SPY and QQQ can drop another 10% and they still we be above pre-covid.

The FED is not going to push the panic button yet.

These rate hikes are getting some of that margin froth out of the system in both stocks and crytpos.

I am guessing the FED is okay with another 10% drop in the stock market and maybe another 15% to get us back to normal. Coinbase stock is probably is at the level were it should have IPOd.

BTC was between $5k and $10k pre-covid. That is probably the price it should be too.

Regulate them! Wallets and crypto exchanges are just rebranded bank accounts and brokerage accounts.

Crypto coins, nfts and stable coins are still equities and money market funds / securities.

They got away with offering unregulated financial products and now people who used real money to buy this stuff were robbed by the people running it.

They weren’t robbed at gunpoint. People voluntarily bought crypto. The free market is working exactly how it’s supposed to; self regulating and purging the excess. Everyone pays for an education… Some just pay more for it than others.

Perhaps the current administration will implement a CLF program. Crypto loss forgiveness. It is being considered for student loans, so why not crypto losses? Losing money is a form of education, after all.

Fantastic joke ! Made my day, thank you.

Nice!

Thank you SnakeEater. That is how it should be. People are in control of what they do.

One thing that never ceases to amaze me, is that while riding my bicycle, I see people texting on their phone as they walk. Perhaps they would be better served watching the world around them, and not just the phone’s screen.

I ride silently at speed. Preoccupied pedestrians do not hear me until I below out a warning when they are about to walk into me. It happens far too often.

Azani, I agree: “Regulate them pedestrians!”

Plenty of bikers ride improperly on the sidewalk. A lot of blame to go around.

Pro-tip. If you toss their phone in the street they’ll run in front of a bus to pick it up.

BUY A DAMN BELL!

Hey, I ride on the streets in full accordance with the law and with logic and reason. Many miles are on bike paths that are part of the street system. The Twin Cities has very good integration of the roadways for bicyclists.

The problem, is that most people have no idea that I am going at 25 mph (or more) with any kind of a tailwind. It is deceptive speed to someone not paying attention. I’m smooth as silk in technique and form, plus my bike is whisper-quiet. So, I close down the distance in much shorter time than they assume if they take a quick glance a few seconds prior.

When I have the right-of-way, and am in my zone, I become a machine on a mission. A damn bell? Nope. “Look!” bellowed loudly works wonders.

My fingers are always ready to squeeze the disc brakes, and my bike stops on a dime. As 91B20 says, “It is combat out there.” Always be ready for the unexpected; like an idiot jaywalking with a phone in hand.

The corollary is the same as putting money into a crypto “investment” and assuming it will magically grow in an exponential manner. Look first, then cross the street.

@ Dan Romig,

I’m disappointed you aren’t on a fixie.

Gattopardo,

I have six bicycles that are all ready to go. Two are fixed gear custom track bikes made with Reynolds 531 tubing. I designed them both.

One for sprints, madisons, kierins and points races. One for time trials. Kierins are fun, for an ex-hockey player; you can hit other riders and knock them up the track! Helmet to kidney area does the job.

IMO, fixed gear bikes are not safe on the streets. If you ride a fixie, more power to you! Be safe, eh?

My two year old road bike is an engineering masterpiece, and by far, my favorite machine to ride or drive. I put more miles on it per year than any other vehicle.

There may be some truth-in-advertising liability issues…

We should now regulate what should have been outright banned as legal investment vehicles? No, this whole house of cards can crash and burn, and its many youthful cult members can join the real service economy and learn what labor is.

so sad, to bad !

I have tulip bulbs, 390 years old to sell, been waiting to get my money back, generation after generation.

I have a sale … 2 for one, $2400 for both, none taxable

I kept a Trezor wallet when I played around with Bitcoin. It was a pain but I think I would recommend a paper wallet/ledger now. Technically you have to keep track of all transactions for taxes. I passed through Coinbase as fast as possible which wasn’t very fast. I found it all a big pain for little gain and left dust wallets all around.

I looked into pirate coin but the process is like a 4 dimensional game of chutes and ladders.

Decentralization and unregulation is the point, because the regulator is the oppressive kleptocracy. Bitcoin good, mania bad.

It’s very odd that crypto assets are not the property of the accountholders, as is the case for a normal brokerage operation like TD Ameritrade or ETrade, etc.

If that’s truly the case, why would anybody hold Bitcoin in a wallet at any Bitcoin marketplace? There appears to be no safe way to hold Bitcoin.

This realization may be the death of bitcoin.

I thought the same thing. Is this coming from the SEC… or the legal department of COINBASE? It has those weasel words favored by lawyers everywhere… “may be considered”… “could be subject to”… “could be treated”

Similarly, your bank account is the property of you, but you are an unsecured creditor depending on the regulations in your country. The banks can make use of your cash, and laws have been put in place around the world to legitimize bailouts using your cash. There is a pecking order, but your cash is on the list a little way down.

…

Holding Bitcoin or others in an offline wallet is ‘secure’ – this is different from exchange holdings in an account. There are many cases of ‘exit strategies’ and hacking thefts which leave account holders with nothing.

Holding Bitcoin or others in an exchange account is not secure. Holdings of coins should be transferred from exchange accounts to offline wallets to keep your exchange holdings at a minimum.

Holding cash in a coin exchange account is not secure. Many claim FDIC coverage for account holders’ cash up to $250,000 that they claim to offload to banks in comingled accounts but that insurance covers the bank failure, not exchange failure, you have to have confidence that the comingled funds have been allocated correctly in the exchanges’ records, and there is no way to guarantee that the cash has been transferred to comingled accounts anyway. They just claim to do so. Comingled cash has a way of disappearing when custodians become desperate.

Whatever… I’m selling the small amount of Bitcoin that I have with Coinbase. Apparently, I bought it, but others can have claim against my Bitcoin in certain circumstances. It’s not worth my time to check out the details, given the small holding I have.

Plus, gold has been an imperfect but much better hedge against inflation and other aspects of my portfolio. It’s clear Bitcoin is a purely speculative risk asset with no correlation to anything, except other purely speculative assets like ARKK.

You are missing something. If a bank goes bankrupt, the FDIC pays me, and the FED backs the FDIC with ability to print money. I get paid, no matter what.

When Coinbase goes bankrupt, I would get an expensive lesson in greed and stupidity.

I’m not missing something; it’s just complicated. Usually when things are complicated you lose.

Just don’t leave any coins in any exchange account except those you don’t mind losing, transfer them to an offline wallet, and don’t leave any cash in any coin exchange account for the same reason. Then you won’t get an expensive lesson.

IF Coinbase went bankrupt, and IF they offload customers’ funds to the bank as their policy states, and IF they have allocated customers’ funds correctly, and IF they don’t dip into the comingled funds for their own use, then your funds would be available to you from the bank IF the bank accepts documentation from the exchange (IF they can provide it) as to the allocation of funds owned by each customer. No FDIC relief would be necessary unless the bank failed, then IF the customer funds allocation was audited and accepted by the FDIC, the FDIC would compensate customers’ funds accordingly.

That’s a lot of IFs, and probably a lot of time, and probably a lot of Maybes thrown in. There have been a lot of losses by customers in the past.

Also, I have commented several times on this board: try to find the physical address of any of the exchanges that people send hundreds of billions of dollars to. They’re usually mail drops in remote places, and even mail drops for other mail drops.

As I said even thought the transfer/conversion fees and delays will be ridiculous, paper wallet.

All the doorways have tolls.

“Similarly, your bank account is the property of you, but you are an unsecured creditor depending on the regulations in your country. The banks can make use of your cash, and laws have been put in place around the world to legitimize bailouts using your cash. There is a pecking order, but your cash is on the list a little way down.”

That’s because it’s not actually a deposit. It’s a loan to the bank.

An actual bank deposit used to be a custodial arrangement, centuries ago. Now the word “deposit” has multiple different meanings, another being a down payment to buy something.

If bank “deposits” were actually deposited for safekeeping (custody), then banks couldn’t lend it out (legally), the banking system would be a lot less leveraged and sounder, and no interest would be paid. The bank customer would have to pay the bank for the service.

Virtually no one wants that. That’s why we have the designed to fail banking system which exists now.

Bank customers want free account services (checking) and until more recent times, interest on their funds.

Bank shareholders and management want higher profits and stock prices which can only be achieved by lending and leverage.

Those with the most influence in government want leverage to provide credit and growth, some of it fake and some of it real.

I believe this is what basically happened when MF Global blew up. The account holders were commodity traders who owned the contents of their accounts. MF Global kept the cash balances in a bank account. Which in effect made the account holders unsecured creditors of the bank. Which made it simple for MF Global to ship the money to Europe to be rehypothecated.

AFAIK it is relatively safe to hold bitcoins in the “cold storage” (USB device that holds all the info of your crypto assets).

The obvious vulnerability here is that operating system makers for PCs / phones / tablets can easily blacklist these USB devices if government orders them to, thereby rendering these “cold storage” devices inaccessible on those Windows/iOS/Android devices (mainline Linux would be much more difficult for government to strong-arm this way, if possible at all).

There is also an option to use paper wallet/ledger as one of the commenters pointed out above.

Like a friend said, “if you don’t control your keys, you don’t control your wallet”. Friends who’ve done crypto a long time have various strategies – a couple USB keys in separate safe deposit boxes, paper copies, etc. You want to be damn sure your backup protocol is on point.

There was that story a few months back about some poor guy who lost some enormous amount of BTC because he’d recycled the hard drive and realized much later that all that BTC was worth about $500M. Coinbase offers convenience, they’ll manage your keys for you.

Bitcoin is free software, you can download it from the internet (Github) and run it on any computer as well as read the source code if you’d like. Your “wallet” is just a long password ultimately. If you can write down the password, you own the wallet and it can’t be seized. Can’t really be blacklisted period. Its just this “layer 2” systems where it interacts with currency (exchanges etc. ) which exhibit these problems with bankruptcy, seizing, etc. All you have to do to “spend” bitcoins is download and run the software, and type in your password, and your funds appear. Don’t lose the password!

I thought that was reasonable until I bumped into real world problems

1) nobody takes Bitcoin

2) Bitcoin volatility is ridiculously high and seems to be driven by whale pump and dump

3) there is no anonymity with know your customer requirements

4) transaction times and fees are very high – especially ATMs. So high they were a significant plus in mitigating taxes

5) and of course taxes

I am not a blockchain currency bear, but I am waiting for blockchain currency II. And curious as to who has a profit incentive to create it.

A Ring-a-ring o’ roses,

A pocket full of posies,

A-tishoo! A-tishoo!

We all fall down.

This whole space is one giant fraud that should have never been allowed to exist in the first place. It needs to be shut down permanently. As I mentioned in a thread a few weeks back, Coinbase will be going BK and out of business. Google “Coinbase stole my money.” It’s a fraud outfit.

That’s why China banned it

The real mayhem is in the stablecoin complex. Stablecoins are collapsing. The same stablecoins that magically, on many many occasions, stabilized a meltdown of cryptos. So who’ll save the stable coins?

A stable genius?

Genius? A stable coin? Like cow chips or horse sh-t you mean?

The latter have compost value with future yields rising

The tiny country of El Salvador was going to use Bitcoin instead of US dollars. They even had a scheme to use electricity generated by a volcano, and sell “Volcano Bonds” to finance building the geo thermal electric plant.

Alas, I think the scheme is going up in smoke.

Mr. Ed?

Cryptos will probably be known as the ultimate Ponzi scheme off all time. I still remember people who bought this crap to build wealth based on the belief that the government could never track it or tax it. Then Coinbase was ordered by a Federal judge to turn over records of users who had bought, sold, sent, or received more than $20,000 through their accounts in a single year between 2013 and 2015. If you sell your coins for dollars, of course IRS will know about it when you get into your bank account but don’t report it.

Cryptos, in my view, appealed to the most simple-minded rank and file investors. The only thing that made them feel so invincible was the monetary orgy show that Powell put on in the last two years that destroyed any price discovery.

Used to have BTC. Ditched them in 2017, when Bitcoin started to rise too high too fast. Used the profits to by my first 9999 gold bars. Never looked back in the cryptoworld.

Bitcoin appealed to many libertarian types. How many times have I heard decentralized, democratized, etc.?

In Crypto, value store you!

-Well-known crypto hustler Yakov smirnoff

What I can’t understand is, what is the risk of contagion and how many real institutions got involved in some of the riskier crypto projects. I feel like we may look back on today and think this was where it all unraveled. Not just for crypto but the rest of the market.

The funny thing about the wealth effect is that it works both ways. When people feel wealthier (even if from artificial asset price inflation), they spend more. But when they feel poorer (even if from modest deflation of ridiculously priced asset), they spend much, much less. And retreat from the market.

Dark times ahead

Research Michael Saylor and his company MicroStrategy. There’s tons of leverage out there, this is just what is known. At some unknown lower price from here, his company will be margin called and that’s when the fireworks will actually begin.

I suspect that margin calls are already taking place in the crypto space. That is why the drops recently have been so accelerated.

As I type this, DOGECOIN is down to 8 cents (from a high of 74 cents in May of last year) and is down 87% from its high in October of 2021. Both of them were twice as high in the past month.

Based on my talks with some Millennials who are really into these “altcoins” that have no real purpose in life (the altcoins… not the Millennials)… they are getting margin calls and have to sell SOMETHING in order to cover them. Welcome to the Real World kids… borrowing money to buy wisps of air is not a good plan.

Hahaha…this made me laugh..I would argue that some on this forum might disagree..

“Based on my talks with some Millennials who are really into these “altcoins” that have no real purpose in life (the altcoins… not the Millennials)”

Time for Thunkadunk coin?

Can’t wait for houses to Pikadunk.

I prefer “Splat coin”. As in the sound it makes when it hits the ground.

PonziCoin.com

(available for sale = $10,000)

Perhaps this will answer your questions.

They didn’t know until it was too late. In February 2014, the Bitcoin exchange Mt. Gox filed for bankruptcy, with an estimated 850,000 bitcoin lost and thousands of customers left high and dry.

Little has changed eight years later. A mere fraction of the lost bitcoin was recovered. Creditors have waited years to reclaim their assets, and Bitcoiners continue to gamble with their savings by leaving their coins on an exchange.

Exchange juggernaut Coinbase acknowledged in its earnings report Tuesday it holds more than $250 billion in assets on its customers’ behalf, and customers could lose access to their assets if the company ever went bankrupt.

“…Moreover, because custodially held crypto assets may be considered to be the property of a bankruptcy estate, in the event of a bankruptcy, the crypto assets we hold in custody on behalf of our customers could be subject to bankruptcy proceedings and such customers could be treated as our general unsecured creditors,” the company stated.

The disclosure made the rounds online, scaring many Bitcoiners – and for good reason. If exchange customers are designated as general unsecured creditors in bankruptcy court, they join a long line of people waiting to claim their bitcoin, a process that can get dragged out for years.

Coinbase CEO Brian Armstrong clarified on Twitter that Coinbase currently has “no risk of bankruptcy,” and the disclosure was made to satisfy a requirement from the Securities and Exchanges Commission.

But Coinbase is just one of many exchanges on the marketplace today, and there is no guarantee your exchange is in good working order. There have been dozens of crypto exchange failures over the years due to hacks, accidents, and chronic mismanagement. And you never know when an exchange could restrict withdrawals.

All this is happening as a “monkey wrench” that I said years ago about about crypto “Monopoly Money”, – backed by a handful of nothing, – helping tank the markets.

And CEO Brian Armstrong saying there is “no Risk of Bankruptcy” – that’s dripping of arrogance, – yeah he doesn’t have to worry because he’s “Madoff” with other people’s money on his yacht(s)!

The total crypto market cap stands at 1.16T, down from about 2T, and the worst is yet to come.

It’s going to be a “catalyst” that will further sink the markets because of crypto panic selling, plus some crypto accounts have been leveraged up to 5x to buy stocks, you only need 20% down to buy, and if it’s used to buy stocks on margin in a brokerage firm, as I suspect, and the firms demand “margin calls”, and there will be defaults, this could be what takes it all down, faster than the Titanic.

Like I have said before all this crypto “snake oil” should have been squashed from the beginning, – it’s pure insanity.

I have ZERO empathy for those that bought this insanity, and now they are talking of regulations, Ha, Ha – Well the Titanic has already set sail and hit the iceberg – it’s a day late and 1T dollars short, forgetabout bailouts!

Well if Coinbase got $88 billion in their IPO last year, then they should be able to absorb $2 billion a year losses for the next 40 years give-or-take.

This math only works with the real money. What Coinbase got is funny-money, and they work in a different manner – by dropping or adding digits to the number. For example, original Coinbase number (stock market valuation in funny-money) was 88 (funny-billions), they dropped one digit, and it became just 8 (funny-billions). Question is, whats next for them ? If they drop another digit, they will have nothing (not even zero).

Coinbase didn’t raise $88 billion at the IPO, or any amount. That was the market cap = number of outstanding shares x share price.

This was a direct listing, and the existing shares just start trading. No new shares were issued, and the company raised no money in the IPO.

But Coinbase had raised over $500 million from venture capital investors in the years before going public.

Keep your eye on the sparrow, Microstrategy, MSTR. CEO converted all their market cap to crypto. El Salvador has about 73M in Bitcoin. COIN holds about 200B, MSTR is about 1.9 billion while the effects of devaluation are felt more at the bottom tier.

WOW… no new money for the company… just cash for the existing shareholders??? These guys can’t even do an IPO right. Nice to know that SOMEBODY is getting rich off Crypto-Mania.

“And CEO Brian Armstrong saying there is “no Risk of Bankruptcy”

Yeah, right. Just like Hank Paulson telling us in ’07 that “the banking system is strong”.

I mailed this Coinbase 10-Q bankruptcy topic suggestion to Wolf the other day, and to my pleasant surprise he followed up on it here today.

I’ve never personally bought any crypto, yet my main concern was the fallout from the Tether stablecoin possibly unravelling (USDT).

Tether (USDT) is an $80 billion stablecoin struggling to maintain its $1 peg as I write this, currently at 98 cents.

If Tether (USDT) unravels, the potential contagion effects could be huge, including a Coinbase bankruptcy among many other nasty surprises.

I totally agree. People don’t realize they are often actually trading stablecoins when exchanging crypto into usable currency. Tether being the biggest.

There is supposed to be 1 tether per $1, which is what makes crypto have the underlying value. But tether has only had about 3% dollar reserves, which means the entire crypto platforms could literally just vanish to zero if people widely realize there isn’t any underlying value.

It appears that was going to happen yesterday, then suddenly Tether has miraculously gone back to $1, and all the wobble is gone.

Breaking the Tether:Dollar peg is nothing less than it deserves seeing as how its integrity is/was based on a pack of lies about exactly what the assets were that was actually backing Tether at any on time: https://www.cftc.gov/PressRoom/PressReleases/8450-21

Back in the days in Amsterdam, at least at the end they had some nice tulips to sooth their pain.

Modern times, i guess.

Anyone foolish enough to pay real money for the privilege of moving nothing around inside nowhere to accomplish no purpose deserves to lose the real money.

well said.

Why Warren and Charlie called it Rat Poison,but people don’t listen

The weekly DOW and SPX breached the cloud, following NDX footsteps.

It’ refreshing to see some reason in the markets. Way to go. Just look how insane the valuation of Tesla still is.

But many families will be financially destroyed. Gambling should not be seen as cool. Yes, people are greedy, but they are also mislead.

My friend,who I’ve know since we were 12 , is one of those people who gets easily success to gambling. When we were kids and we used to go to the arcades, to mostly okay videogames, he would disappear only to come back and say he had spent his whole weeks pocket money £3 on a fruit machine. When we got older and started work he would plough his entire wages into these things .

Last year he told me how bit coin was a great investment opportunity and he was going to put all of his family savings into bitcoin, and though he is still up 100% I fear, like may others, they will chase this thing to 0.

I made a lot of pocket change selling free games on pinball machines from the first day I started school. I spent more time playing pinball machines that I did going to school and sleeping. I could beat anyone on the baseball games blindfolded with just a ball and bat.

Crypto’s ethereal nature, along with it’s volatility, makes gold, (the “relic,”) look positively stable.

Paraphrasing James Grant on gold: in addition to it’s lustrous beauty, that it hurts when you drop it on your foot adds to it’s allure.

I’ve been reading a few recent tidbits about fledgling attempts to create a gold-backed digital currency.

I admit this idea intrigues me a little, considering that physical gold can’t be divvied up for tiny purchases.

I read somewhere recently about a paper bill impregnated with gold specs. Verification of content issues would be key (like an assay) was my first thought, but I suspect some industrious materials engineer could overcome that challenge.

The monetary authority won’t supplant it’s own currency, I suppose, but perhaps an enterprising industrialist billionaire?

“The monopoly of government of issuing money has not only deprived us of good money, but has also deprived us of the only process by which we can find out what would be good money.”

– F. A. Hayek, A Free Market Monetary System, lecture Nov. 11, 1977

“Verification of content issues would be key (like an assay) was my first thought, but I suspect some industrious materials engineer could overcome that challenge”

AFAIK they (Aurum) had already overcame this challenge. They

run “goldback” (the very thin gold film sandwitched between two layers of clear polyester, i.e. gold bill) through the machine that shines light through this “goldback”, and does spectral analysis to confirm presence of gold, and its amount. Takes a second, and is highly accurate.

I believe “goldback” is a legal tender in 3 states, but so far didn’t manage to gather big acceptance among merchants (but few do accept it).

By my calculation, gold in “goldback” is about 30% overpriced vs spot market price, which seems acceptable to me because these are real gold money in your real leather wallet, not some electronic record of a promise to hold some gold somewhere on your behalf.

Gold impregnated bills will never work because of Gresham’s Law. Bad money drives out good money in circulation. It would be very easy to extract the gold from paper if inflation in fiat made it worthwhile.

“Trust me, I have your gold right here, believe me, but I will sell you a claim (on or off the ummutable blockchain).” You don’t know where I am, I am in the global cloud. See the problem? Even today’s wonderful trustworthy person is transformed by circumstances. That’s why we have things like banking laws: structures of serious accountability.

LOL. There ARE gold-backed currencies, it’s just that they’re called Exchange-Traded Funds. You own them in a brokerage account (SIPC protection) and pay far smaller fees than in digital/crypto currency space.

Look into GLD, PHYS, etc.

These are divisible down to about the $10-20 level based on share prices.

The main issue would be taxation on capital gains, but that’s also true with crypto and other currencies.

Put them in Roth IRA

Those ETFs do not have the gold they say they do. They exist primarily as a gambling mechanism to divert demand away from physical.

@Wisdom Seeker

You quite literally just made the case for blockchain tech and cited the reason why crypto will never die.

In your example, you referenced the ability to walk in to any store and transact with any asset – both the consumer and merchant made whole by means of a new technology. But there are inhibitors built into our current legacy financial system that prevent this from being possible, namely: economic finality (the time it takes to finalize a transaction) as a result of the layers of beaurocracy involved in authentication. It’s 3 days to clear a visa payment right now, remember.

Enter, blockchain.

An immutable ledger technology which, hypothetically, can accomplish what you’ve posited and genuinely already has. There is a company/crypto named Flexa which has created a collateral token named AMP through which they’ve built the infrastructure using blockchain tech to do exactly what you’ve just described.

As of today, i can open Flexas app on my phone (SPEDN) and walk into a Rona or Baskin Robbins (to name a couple, out of their 40,000 partners) and scan my qr code on a debit machine and voila! I’ve just made a purchase using crypto and no one is the wiser. It’s finalized instantly, fraud-proof for the merchant, completely transparent for anyone to see via a blockchain scan, and rewards investors (instead of rewarding a central entity) by redirecting paid fees to investors via smart contracts c/o decentralization.

Hypothetically, this tech is already available to use for fiat to fiat but lacks widespread adoption. The tech could conceivably collateralize any method of payment, anywhere, anytime.

Reading this comments forum is like diving back into 1990 when everyone was down on the internet and failing to understand the ramifications of the technology. Blockchain is all about personal ownership and destroying monopolistic behaviors that create extraordinary wealth divides. This ‘look at chart and price go down must be worthless’ mindset is just as misunderstood as those who’ve invested in crypto as a means to get rich without understanding what blockchain is good for, and what it isn’t.

I could name 2 other crypto projects that have the potential to completely disrupt and replace current legacy systems (currently worth trillions) but it seems like the cool kids here just want to talk gold and Fed, believing the future will resemble the past.

Actually for MarkB:::

Agree totally with your: ” but it seems like the cool kids here just want to talk gold and Fed, believing the future will resemble the past. ”

Just EXACTLY the same as the cool ”kids” warmongers just want to fight the last war, eh

And we can see exactly how well that is working out right now in eastern Europe, eh?

Gonna continue to be a TON of very sad folks no matter if ”investors” or warmongers IMHO…

Glad NOT to be in either group at this point in time, but still keeping both kinds of powder ”dry” just in case the FFR goes above 5%,,, etc., etc.

Your fiat works great for “tiny purchases.”

Wolf & Wisdom Seeker,

Yes, I understand the flexibility of fiat for ‘tiny purchases’ along with the ETF’s, but I was thinking more along the lines of Judy Shelton wanting sound money to be enforced by true hard asset backing. No more QE on a whim because certain well-connected parties can’t stand to lose money at life’s proverbial blackjack table.

JJ I hear you.

But you know, for any transaction that a “digital currency” could handle, there’s no need whatsoever for a new currency.

Consider foreign exchange when traveling: it used to be you had to buy paper Euros or whatever with your dollars. But now your credit or debit card is set up to swap your dollars (or whatever currency you hold in your account and want to sell), through a market-maker, for whatever currency your counterparty wants to receive. And as the markets have grown, the spreads and fees have gotten quite small in most cases.

But there’s no these trades have to use dollars or other currencies. They could be shares of the S&P500, bond ETF shares, or whatever. Just need an open, active electronic market, with a “tradeable path” between assets you hold and assets your counterparty would like to hold. The gold ETF would often work. Then you could walk into a store anywhere on the planet, sell any asset in your portfolio for gold (or whatever), and then swap that for any item you want to buy from your counterparty.

It’s not barter and it doesn’t require any new currency or asset, just a new trading platform.

Goldmoney from Goldmoney.com has been one to my knowledge for years. I don’t own it and can’t confirm how it actually works.

Ultimately, if you don’t own the physical metal, there is some level of trust in the entity behind it.

It’s a function of confidence.

The problem with crypto “currency” is that it’s actually nothing. Anyone can create a new one any day of the week, regardless of whether the supply for an individual one (like BTC) is limited.

BTC has name recognition and early or first mover advantage but it’s still nothing. No “hard power” backing it, like the USG. It’s not a debt like paper assets subject to direct default, but since it’s just a bunch of 1’s and 0’s, can (and probably will) go to zero anyway.

The allure seems to be missing these days. The all powerful US dollar is kicking sand in gold’s face. The miners have been taken out back and shot as though they were all bankrupt. Precious metals are a lot less precious these days!

Since nobody knows what gold price is going to do I treat miners like I would a company making widgets. If balance sheet is good and PE gets to about 16 it’s on my possible buy list.

Whhhaaaatttt!?!?!

They can really just seize all my precious Tulips??

Must wake up from HODLer nightmare.

But wait, they are on the immutable blockchain. Wait, wait — ! The pie in the sky just flew away. You have a certificate to nothing (a bet on your peers’ belief and hope) on a ledger some kid coded into existence.

You are also merely an unsecured creditor of your bank, including the contents of your safety deposit box.

Allegedly you are insured by FDIC for the first $250,000.

But ask FDIC just what percentage of cash it has to secure the entire US bank system.

And how long it would take to get your insured savings from FDIC.

And after the Fed prints the money for the FDIC, just what is the new purchasing power of your allegedly insured savings.

This may be irrelevant, since the bank can merely bail you in as a new equity holder in lieu of being merely an unsecured creditor.

It’s called modern capitalism.

But for whom?

That’s complete nonsense. No customer is being “bailed into” any bank. In fact, when banks fail, you don’t even realize it, as another bank takes over it before you even know anything happened. Your money doesn’t go anywhere.

Well, that may be so in US. But bailing in is precisely what happened in Cyprus in 2013 and in Greece 2015. The bail-in procedure for failing banks was adopted as standard modus operandi for the Eurozone.

Every insurance system (or work of human design) is imperfect. It’s ALL relative, the way down, in this mortal material world. But our FDIC is the best among many more risky things. Do you carry around a paper bitcoin wallet for everyday finance? I thought not. All backstops are NOT created equal, all are created imperfect and unequal. Just as all assets (worth anything) are unequal and fluctuate. A big enough catastrophe can erase any of them.

Diogenes,

jeesusmoleesus, that’s a load of stuff there.

The FDIC is an agency of the US government and can borrow from the US Treasury, and the US government is backed by the printing press of the Fed, and the Federal Reserve Board of Governors (whose Chair is Powell) is a federal agency, and the US government will never run out of money. It might destroy the dollar through inflation, but will never run out of money, you just have to understand that. So the FDIC will always be able to pay off its insurance, and you can take that off your worry list.

When the FDIC resolves a bank, the stockholders and preferred stockholders and contingent convertible bonds get bailed in. The FDIC gets all the bank assets, and then pays off the liabilities based on the capital structure, which includes deposits. If there were more liabilities than assets, the FDIC pays out deposit insurance only on the amount of the shortage, which is in the worst case a small portion of the deposits.

So if you think that the FDIC has to be able to cover the total amount of deposits, you show that you don’t understand banking, assets, and liabilities.

I’ve been through three bank failures and never lost a dime. This fearmongering about the FDIC and banks is just pure BS spread by the gold sales industry.

I went through two bank failures in the late 1980s, but never even changed buildings. Bank A failed (they’d usually do this over the weekend), and on Monday there was a sign for Bank B. A few months later, Bank B also failed. Then there was a sign for Bank C.

It only cost me a new box of checks each time.

The FDIC is what kept a sharp recession (Texas in the late 1980s) from becoming a catastrophic depression like the 1930s.

From reading accounts of the 30s (and hearing them directly from grandparents), so many people who would have survived otherwise lost everything because their bank failed. Prudent savers with enough to tide them over a few bad years were tossed out on the dirt roads.

I agree with Wolf. FDIC deposit protection is the closest thing we have to sacrosanct in the financial world. Anyone saying otherwise is just fearmongering to fleece the gullible or not thinking things through.

Was one of them M Bank? That was one of mine in the second half of the 1980s.

It’s ultimately a question of what would happen in a full blown systemic crisis.

Sure, the FDIC through the government can pay off every depositor in full. If that happens, won’t be much consolation if the money isn’t worth much of anything.

It’s the same concept as to whether the USG (or any government) can or can’t default on debt denominated in the national currency.

The answer is both yes and no.

No, because of “printing”

Yes, because of what I just wrote. What matters ultimately to most people is the debtor’s (government here) ability to pay you back (with interest) in (near) full value. “Getting your money back” when it’s worth a fraction or low fraction of it’s initial value is a form of default.

That’s why the USG’s actual credit quality on any longer-term debt is the weakest since at least the Civil War. No different in much if not most of the world.

Augustus Frost,

Read what I said how the FDIC operates when it resolves a bank. Even in a systemic crisis, the amounts the FDIC pays out of its insurance fund to cover depositors are just a small fraction of total deposits because the Fed bails in the stockholders, the preferred stockholders, and the CoCo bond holders, and it gets all the assets, and then it uses the proceeds to pay off the liabilities. The capital shortfall is never huge. You’ve got to get this into your head somehow, even if it hurts. This FDIC gold-bug stuff is really tiring.

No gold bug here.

There has been no real systemic crisis since the early 1930’s. GFC didn’t last long enough and wasn’t deep enough.

A real systemic crisis will be worse than the Great Depression because leverage is a lot higher and the government’s ability to neutralize it is a lot worse too.

Most bank assets are a bag of hot air: unsecured, “secured” by what is actually debt, or in a very low minority of instances, secured by inflated collateral.

Yes, I know something like the Great Depression can supposedly never happen again which is where I presumably disagree with you.

Banking system is also currently a much lower proportion of total system credit. I get that too.

I’m a gold investor but not a gold bug. The gold bug conspiracy and catastrophe theories are truly tiring.

Would NCUA be the same in working principle as FDIC and protected the same as you described?

There’s a silver lining in this.

So much electricity has been squandered on mining this garbage that will now not be justified or needed.

Might relieve some chip shortages too.

Wow, there is a startup idea: reprocesses all the cryptos and turn them back into electricity… Instant unicorn.

I don’t know if cryptos crashing are making tech stocks look any better.

I thought Warren and Charlie responded well to Peter Thiel’s attempted put down of Warren for opposing Bitcoin, calling him “Enemy number one: the sociopathic grandpa from Omaha”. Their response, delivered to a wide audience shortly after Thiel’s derogatory comments were made, without acknowledging that Thiel even exists, which was perfect, clearly explained the absolute folly of crypto, calling it “rat poison squared”. Warren made sense, Thiel’s didn’t. It can’t be good for the “asset class”, if you can call it that, to have its champions put down so publicly and so effectively.

I think Buffet has done well because he is disciplined about not speculating. One of his rules for buying whole companies is that they have a long history of earnings. Why make it more difficult than that?

Thank you, Old School. Perfectly stated. This upcoming crypto debacle may help the current generation understand that reality. Buffett’s investing approach is brilliant in it’s simplicity.

As a refresher, Warren and Charlie on cryptos:

Warren: “rat poison squared”

Charlie: “trading in turds”

Thiel always took pleasure in being the tough guy/bad guy. He is now involved in a fund that wants to disregard all effects of its operations (drilling, whatever) outside of pure profit. OK, But remember that kind of bad boy rebel kid from school? Most of those kids I knew end up in prison or dead. There is a reason conventional wisdom is called that, and Buffet took it to a higher level, with nothing up his sleeve.

Oh, Buffett has a lot up his sleeve, including deep political connections and the ability to swing legislation in his favor in times of great need.

Charlie – “suck it up”

Bailouts and laws are only of benefit to the wealthy

Warren Buffett doesn’t see a halo when he shaves. Peter thiel and the other 1200-odd Young Global Leaders do. If you sweat for your pay, you’re less likely to listen to the larceny in every human soul and resist the temptation of something for nothing. If you got “lucky”and scored big from the Fed skew and CDC interference with the markets, maybe encryption for the sake of encryption as a speculative financial product makes sense to you. Many professional gamblers have a sweet tooth for other games of “chance” where they give back much of their take from their specialty. Technology doesn’t alter human nature so much as it catalyzes it’s potential for good or ill.

Mr. Buffett understands hard work. Mr. Thiel is a club member that doesn’t want to ever have to understand hard work, unless it’s somebody else’s.

Wolf…thank you for a great article on the madness that is Crypto. Having bought Ethereum at $700, sold at $2100, rebought, resold and eventually loosing 18% of my marginal investment swore off the Crypto path to financial madness.

The bonus to your article is the new “Wolf Words”. 🤪🤪

I think some people don’t appreciate that if an enterprise gets into a vulnerable position in financial markets, the vultures are going to try to take you out fast.

OS-a mild semantic point of nature vs. human allegory, but actual vultures have the decency to wait to eat until you have been well and truly taken out by something else…(nature’s perfect crime scene cleaners…).

may we all find a better day.

Cathie woods

I am trying to avoid an intense feeling of schadenfreude for every person who actually believed that cryptos and nfts were a legit investment.

They were not, they are not, and you can believe that “trees grow to the sky” and see how that works out for you. I’ll stick with “what goes up must come down” :)

In a interview a smart man said crypto would correct to 4-7 k ,market would see 1000 k dent harry

Or a Supreme Court and a political party that aim to “lesser human being” half of the US population.

Please keep your hands off my uterus.

“But you’re losing 7% to inflation if you hold cash.”

Well I lost 98% of my $10 play money in 12 hours buying Terra Luna. Currently at 2 cents.

Buy the Dip!!

It’s uterUS not uterYOU.

This isn’t over by a long shot. The BTFD crowd has poured in.

I’ll stick with “what goes up must come down” :)

I’ll add “the bigger they are the harder they fall”

BIT DOWN MORE THAN A LITTLE BIT…

CRAPTOS SINK IN THE ABYSS…NEARING WORTHLESS!!!

REALITY FINALLY SINKS IN TO IDIOT SPECULATORS…

More than $200 billion gone in day…

COINBASE warns bankruptcy could wipe out user funds…

Half value vanishes…

Billionaire Wealth Destroyed…

Plummet tests durability of hype-driven industry…

These made up collapse terms just make your otherwise clear reading “bumpy”- and sounds silly

You gotta have sense of humor to get through these crazy times.

Yes just thought of terms whackmuffled and muffleclubbed.

Dave – I respectful disagree. Wolf speaks closer to the truth than almost any publication. You can not make up “consensual hallucination “. I like his writing style.😉

They’re ‘gonna be just fine because as everyone knows, Fortune Favors the Brave.

/S

Most of them will be fine because they are only investing “play money” in Crypto. The ones who aren’t wouldn’t be fine no matter what they “invested” in.

The US Dollar – just as fully expected – is doing absolutely wonderfully well and is up 0.33 to 104.35 on the DXY and is headed for 120 and perhaps significantly higher as it proves its role as the world’s most important and desired currency.

If BTC gets to $20k, it’ll be 70% off its high. I’ve been through 2 previous 80% drawdowns already – this could be my third. Each time, the chorus declares the folly of bitcoin and keens its death knell. Tulips are resurrected to lay on its casket. Yet, despite it all, simply by holding, I’ve several thousand X-ed my investments.

I will say that this time really is different in that we have much more gambling by Big Money playing usual Wall Street games at the margins, often setting price because of btc’s small market cap. How that plays out this cycle is the new wrinkle. We shall see. But bitcoin is not going to zero, it’s only shaking out the weak hands and froth again – as any free market must do.

The core hodlers are rock solid. The fundamental case has not changed. The base protocol makes more converts at every economic level and in every economic sector every year. I’m just trying to figure out what else I can sell to buy more while bitcoin is priced in the $20k’s.

The last two drawdowns were both in low interest rate, QE-fueled environments. There was no inflation like we see today.

Don’t be surprised if this time is simply different, there is no rebound and it just keeps dropping toward zero.

Bitcoin is not a currency and is basically acting like a high growth tech stock. The moment it becomes a threat to power is the moment they simply ban it and it goes to zero. And if you don’t think they can do that (they can, very easily) or would do that (they would, without blinking an eye if it began to undermine the USD), I can assure you they will.

All crypto is going to zero and there will eventually be an official digital dollar that 99.9% of people will preferentially use.

That doesn’t mean we won’t see a BTC bounce to all time highs and beyond, but ultimately, all this stuff is a ponzi that is going to zero.

And before anyone says the USD is also a ponzi, yes, it is. But it’s a ponzi backed by state power and a giant military. That’s the difference.

The USD is also a ponzi, for the time beeing backed by a state with a giant military. 😉

Not sure if this passes muster as allowable content but here are some juicy “findings” by the Queensland O of T (published in various news outlets – although not a fan of the NY Post this is where the following is in print).

“The average Bitcoin investor is a calculating psychopath with an inflated ego”

“They identified that many investors exhibit signs of the “dark tetrad”, a group of four unsavory traits made up of narcissism, Machiavellianism, psychopathy and sadism.”

“in plain English, that means dark tetrads have an inflated sense of self-importance and derive pleasure from the pain of others.

They also find it difficult to empathize with others and are sly and manipulative.”

The most problematic issue for me is the gigantic need for electricity required to “mine” these coins. Plenty out there to research on this topic but basically an environmental & ecological nightmare. Its emblematic of the Human Race’s apparent race to oblivion. The irony being of course the terror of mere mortality.

The “dark tetrad” describes a lot of market participants, not just bitcoin. And it’s true of business logic generally: pump up your brand (narcissism), do whatever it takes to beat the competition (Machiavellian), squeeze your workers and suppliers to boost your own profits (psychopathy and sadism)…

Question: do such people participate in markets because of their personality failings, or do they develop that type of personality because that’s what the “market game” requires to survive?

Is playing the game bad for your mental health?

Buy the damn Dip!

Assuming what you’re saying is even true (I’ve several thousand X-ed my investments), which I happen to suspect is a gross exaggeration, you seem to fail to understand how you were even able to do such thing, and who you had to rely upon to even get there – all of the fools who just got wiped out. So now you need more suckers. Where are you going to get them with no more free sh!t from the government and FED?

You could sell the bitcoin you have now for thousands more than 20k if you think that’s going to happen.

I just noticed coinbase is 6 percent of Ms. Woods fund. That might take yet another big chunk of value. $35 and change premarket. Quite the drop, and there could be more.

Could be? WILL BE! Guaranteed.

The wolves on Wall Street are eating her alive = equals she isn’t smart enough to change her convictions. Terrible manager but still gets her cut,so still in the game

Has anybody asked Cathie Woodshed about her Bitcoin call? It’s looking more laughable by the day.

There is a story about a cat in a convalescent home. Whatever patient it decided it wanted to snuggle with would be the next to die. Cathie Woods is that cat. When ARKK buys a stock, it’s the kiss of death.

That yellow metallic junk has again plunged by $6.90 per ounce to $1845.80 per once and that gray metallic stuff has plummeted by $0.56 per ounce to a new 2022 low of $21.00 per ounce as they both are in the process of reverting to their means of $456 per ounce and $8 per ounce respectively.

I hope so. I’ll buy it by the truckload.

LOL. In generating those “means”, which “dollars” were you using?

1 year returns (in USD)

S&P minus 4%

DJ minus 7%

NASDAQ minus 13%

Bitcoin minus 41%

Gold plus 1%

Gold is hardly a junk, and seems to be quite resistant to general declines everywhere in the markets

My commodity futures fund 40%.

The yield (interest rate) on the benchmark 10 year US Treasuries is nicely back about 3.00% and headed much higher.

You are a bit ahead of yourself?

Liquidity sponge dries up.

Here is your wise guy cobalt…

Not just the bitcoin and NFT are down, all the major indices were down by a significant %. Even the giants paying dividends were down recently. I understand the FAANGMAN and nasdaq stocks. We are looking at a major pull back, bear market or a recession soon.

Nobody says “buy the dip” now. May be its really different this time. Feds will raise the rates to 1.5% by the end of this year. Inflation is so high. Not only in gas prices but food, goods and services. Again, all around the world food production, diseases, social unrest and even war is going on.

“May you live through interesting times…”

PPI just came in HOT again. 1.5% to 2% is not going to cut it.

Japan’s Softbank just reported a full year loss of $13 Billion. Pretty soon, they’ll have to ask the Japanese government for a bailout.

There should never be another bank bailout on earth. Simply make depositors whole and end the companies, distributing assets to smaller, more responsible banks. We are overbanked anyway.

They can thank their fearless leader in charge for that one..a guy stupid enough to pour tons of money in WeWork…winner winner chicken dinner

Question: Can Coinbase change the status of its “depositors” to “unsecured creditors” after the fact? Don’t the terms—or lack of terms—extant at the time of “purchase” prevail? Of course, even if this is true, it itself will have to be argued in bankruptcy court. Because nothing screams bankruptcy like stating “We’re not going bankrupt.”

At the rate it’s going, the depositors’ cryptos will be worthless anyway.

They were always unsecured creditors. Credit slips dot org discussed this a couple months back and I cited it here.

Yes, they were unsecured creditors at Mt. Gox in 2014. Nothing has changed. They were always unsecured creditors. But no one wanted to know it, and the SEC is now apparently pushing exchanges to disclose this publicly so everyone knows, even if they don’t want to know it.

I know one thing…if I had any funds (crypto) in Coinbase, my fingers would be pounding the keyboard today to get my stuff out of there as fast as I can. I suspect there is a run at Coinbase going on right now.

Coinbase simply gives users an error message like “Unable to complete transaction. Please contact us.” And then when the user tries to contact them they are unable to ever reach them. Google “Coinbase stole my money.” The only time people seem to gain traction is when they start blowing the up on a social media site. This company is a fraud outfit, and unregulated.

Bought 10 Terra Luna at $1 each, lost 98% of that overnight. Might as well had played the lottery. At least I get a free play.

You had to understand you’re just gambling. Everybody is trying to hit the lottery. Hard work and saving is how you get ahead. And yeah, it’s HARD.

I knew I’d agree with something you said eventually.

So, with all this legalese, Coinbase essentialy states that in case of bancrupcy, they’ll do a bail-in on customer’s accounts. This reminds me of Cyprus 2013 and Greek 2015.

Hi – was wondering what a few beers would buy me at your mind-place ?

Couple of questions, of course we are talking about opinions…

1. What would you think the SPY or NASDAQ finally bottom out at?

2. How long will this bear market continue, now that it’s been spotted?

3. Any sectors you actually like?

I will share my answers.. to my own questions ;-)

John A,

1. no idea. A few months ago, I started comparing this to the dotcom bust. So that’s my model. Back then, the Nasdaq kathoomphed 78%. It went one stock at a time, many of them going down 90% to 100%. It was a terrible shitshow, but our elders told us that this would happen and it happened :-] We’re on the same track so far this year, which started last year, with the first batch starting in February 2021. The S&P 500 went shookalacked 50%+ during the dotcom bust.