But wait… Many home buyers had mortgage rates that were guaranteed when rates were much lower.

By Wolf Richter for WOLF STREET.

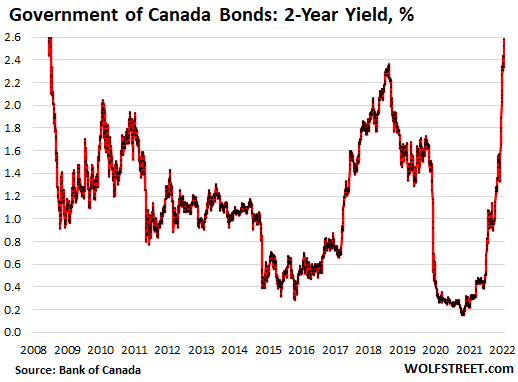

The rate of inflation in Canada spiked to 6.7% in March, from 5.7% in February. The Bank of Canada hiked its policy rates twice so far this year, including by 50 basis points in April, and announced that QT would start on April 25. Government of Canada bond yields have spiked. And home buyers, after home prices have surged for years, now face much higher mortgage rates, triggering the worst affordability crisis ever. Home sales volume fell 16.3% in March from the record a year earlier, according to CREA. And supply of homes listed for sale rose from historic lows to 1.8 months.

In Canada – where mortgages are mostly variable-rate or fixed-rate with relatively short terms, such as two-year fixed or five-year fixed – the shorter-term interest rates impact the housing market more than long-term interest rates.

The spiking yields.

The two-year yield of Government of Canada bonds spiked to 2.58%, the highest since 2008:

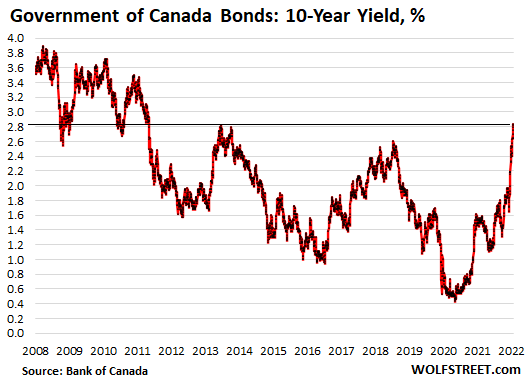

The 10-year Government of Canada bond yields spiked to 2.82%, matching the one-day high of 2013. And beyond that one day, it’s 2011:

But wait…

Many home buyers still got mortgage rates that were guaranteed when they first applied for a mortgage some time ago before the most recent spike in interest rates. They’re still buying with those lower rates. But buyers applying for mortgages now to buy a home in the near future face those higher mortgage rates.

The most splendid housing bubbles.

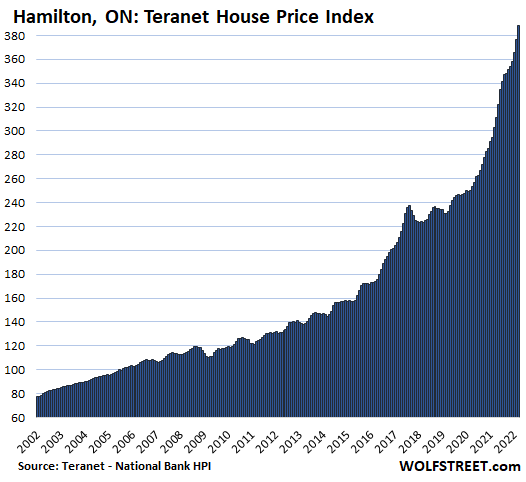

Now we have the housing bubble data for March from the Teranet-National Bank House Price Index, which represents the three-month average of closed sales in January, February, and March. So it covers sales where buyers had mortgage rates that were guaranteed in prior months, including late last year and early this year, when mortgage rates were still far lower. The impact of those higher mortgage rates has not yet shown up. But the impact will show up over the next few months.

On this backward-looking basis, home prices spiked ridiculously in some cities, rose in others, and declined in one of them.

Hamilton, Ontario, now the number one most splendid housing bubble in Canada, blew by Vancouver and Toronto in terms of the price gains since 2002. Prices spiked by 3.2% in March from February, and by 28.5% year-over-year. The index is up 307% from January 2005.

Prices had dropped in late 2017 and then hobbled sideways until May 2020, when the BoC’s money-printing orgy and interest-rate repression kicked in and re-ignited the price spikes to become utterly ridiculous:

House price inflation. The Teranet-National Bank House Price Index is based on the “repeat sales” method that tracks the price of the same house each time it is sold over time. By tracking how many Canadian dollars it takes to buy the same house over time, it is a measure of house price inflation.

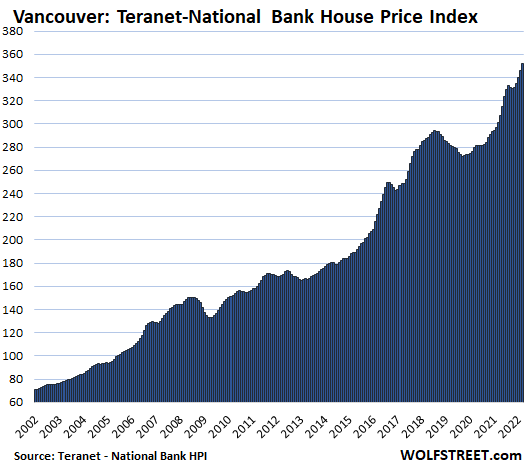

In Greater Vancouver, house prices jumped by 1.8% for the month, and by 16.7% year-over-year. Prices started falling in mid-2018, and the market remained soft until the BoC’s miracle handiwork began bailing it out in the spring of 2020.

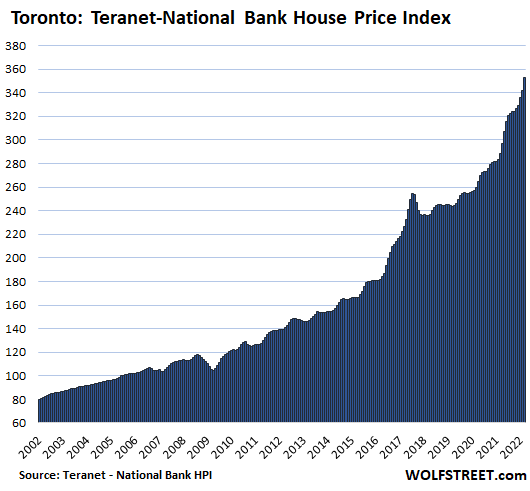

In the Greater Toronto Area, home prices spiked 3.1% for the month and by 22.3% year-over-year. In 2017, prices began to unwind and then hobbled sideways until the BoC’s reckless monetary policies performed a miracle:

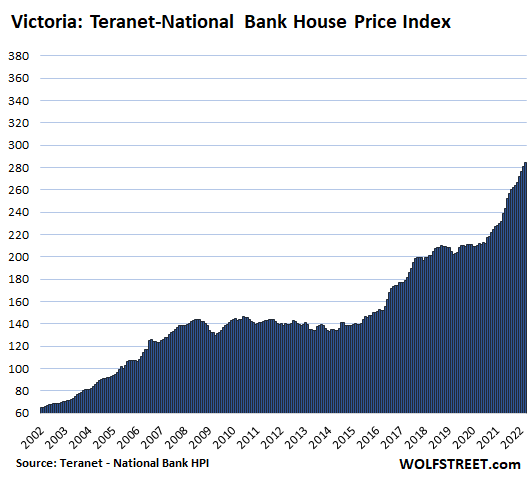

In Victoria, house prices rose by 1.2% for the month, and by 22.8% year-over-year. Prices had flattened from mid-2018 until money-printing by the BoC re-ignited it:

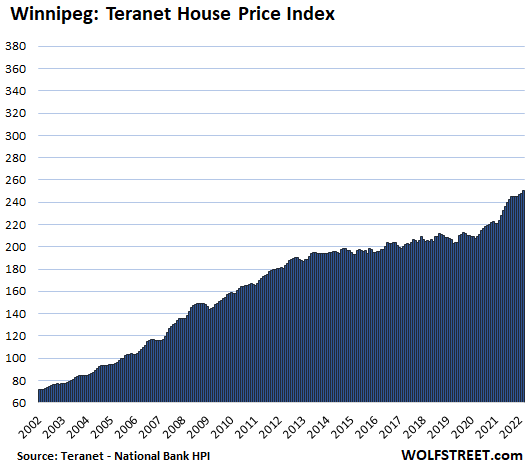

In Winnipeg, house prices rose 0.8% for the month and 11.9% year-over-year. Even here, the BoC’s miracle was able to fire up house prices that had wobbled sideways for seven years:

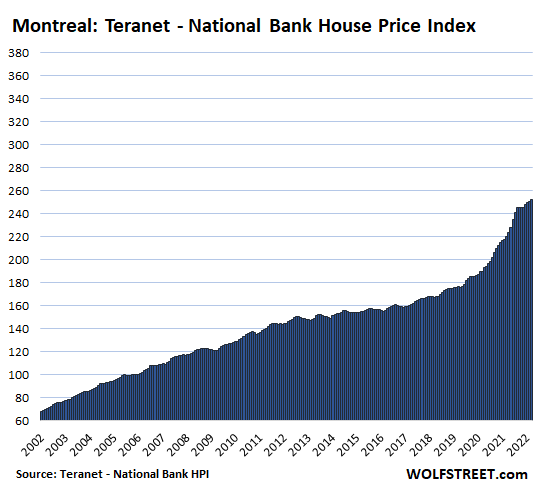

In Montreal, house prices rose 0.7% for the month and 14.6% year-over-year:

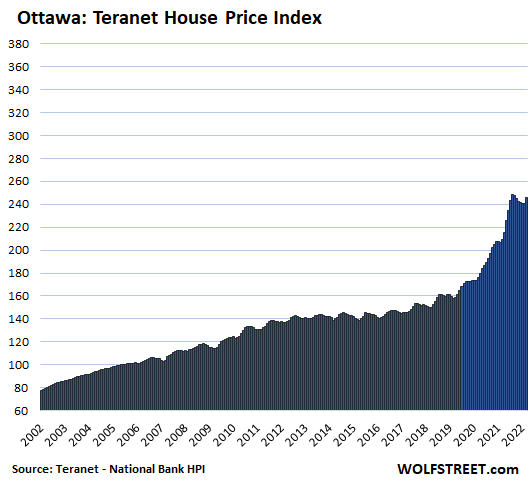

In Ottawa, house prices rose 2.3% after six months of declines. Year-over-year, prices rose 14.6%:

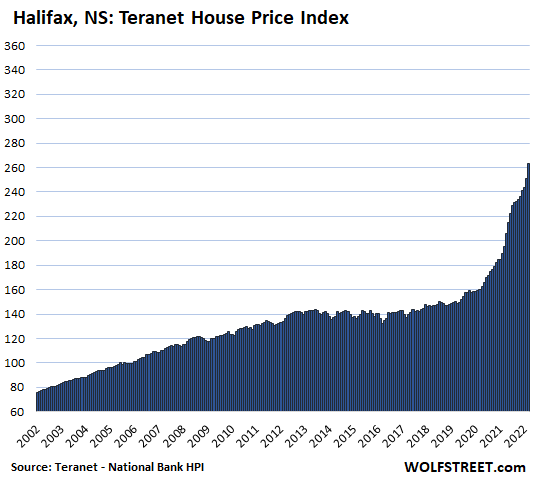

In Halifax, house prices spiked by a ridiculous 5.0% for the month, and by 34.7% year-over-year, the 11th month in a row of year-over-year price spikes of around 30% and higher:

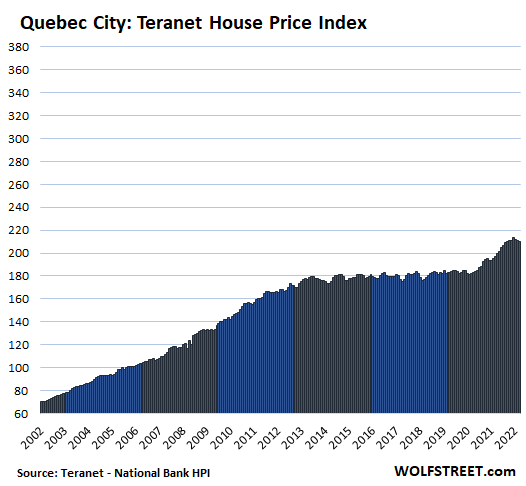

In Quebec City, house prices fell 0.6% for the month, the third month in a row of declines, which whittled down the year-over-year gain to 6.6%:

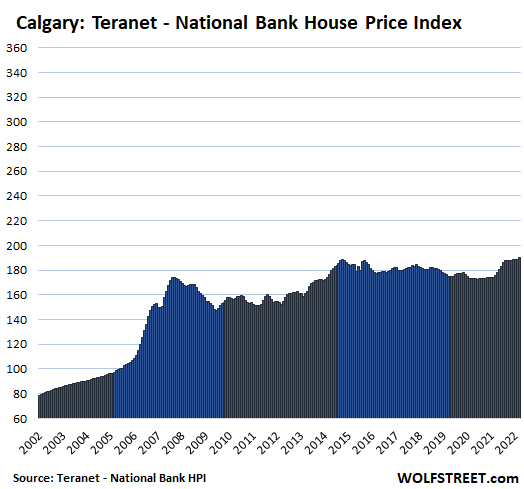

In Calgary, where house prices had been essentially flat since 2007 until the money-printing started in the spring of 2020, the index rose 0.5% for the month and 7.9% year-over-year. At this point, the index is barely above where it had been at the peak of its oil boom 14 years ago.

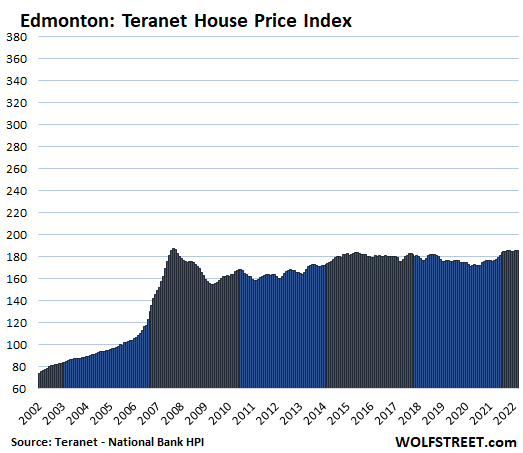

In Edmonton, house prices rose 0.3% for the month and 5.3% year-over-year but remain below the oil-boom highs of 2007:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Where is Canadian cat Paulo and his dispatches (or rather mini-essays) from Vancouver Island ?

WTF charts must be spiced up with gory details !

I’m kinda worried he is hassling extra heavy rains. Said he had a creek on his land. Climate change. Most of my HS friends up their have died, and many of their wives have sold high and moved out, but we still see and talk with one guy’s wife a lot (she comes down here to get away from winter, but is getting scared of the drive). She is on much higher ground and well south and inland of where he is. Still says the rain is excessive, but many people still moving up. Even joined the local NIMBY club.

THKS NBay !

As long as he’s not on casualty report that’s all that matters.

If he decides to chime in while being under extreme duress his posts will carry quintuple weight 😀

Got report from area. Friend’s wife says Sayward (Paulo’s “sorta town”, more like a suburb) is a “microclimate for extreme weather, way worse rain and snow than Campbell River”, also on the east coast and only 40 mi south. Also said it is a Mecca for island hopping lost grizzly bears and becoming and eco-tourist Mecca. She never knew him, but said if anything bad happened there it would be in this paper

In fact, you can probably look at Real estate in the paper if you want prices.

Link deleted- a Newspaper link is probably more Wolf hassle than a website is…but Paper is Campbell River Mirror.

I’ve been getting blown out by 6 figures for a year and a half now in Canada. Something interesting is starting to happen here in Ontario an hour outside GTA.

1. Seeing homes that sold 6 months ago get listed for 200k higher than the owner paid. Then they sit. And sit. Usually they delist them after a month.

2. I see homes list for prices that I consider to be high, but not insane. Made an offer on one, went 200k over asking. Was rejected. Next day house was relisted for 350k higher than original asking. 3 weeks later it’s still sitting there.

3. Many more houses on the market than this time last year. Sales not keeping pace.

The party is almost over, but these idiots don’t want to believe it. Bring the pain!

AT least they still have the beautiful weather there.

It is similar to what happened in 2008,

I spoke with many self claimed greedy people that lost a lot back then, where they said they refused to sell it on time before chasing down the declining prices.

I think what you see is the denial stage that these seller are in right now.

“3 weeks later it’s still sitting there.”

They don’t really want to sell those houses. They’re doing Research to make sure people are still gullible enough to get suckered by all the up-and-coming worthless tech/financial/political/educational/lifestyle enhancement fads they have in the pipeline.

Hey, marketing guys have to eat too ya know. Don’t they?

Until I found out here, I didn’t even know marketing is a COMPLETE TOTAL tax write off just like the building a business is in or labor and raw materials and tools needed to “create” whatever is “needed”.

Tried to find the law where it became tax write-off but seems it has always just been assumed.

Real shitload of damage done to society because of that assumption, (and apologies to Wolf).

Like Dick Gregory said;

“If you got something really good you don’t have to sell it to people, they will steal it from you”

The Millennial bulge will keep pressure on home prices for awhile, at least not drop too much. But it could be housings last hurrah once Millennials had had there fill. The following generations are smaller.

With the demographic replacement rate being 2.1, all but some African countries are much less than that . Some at 1.4 or 1.2. The demand for housing will start drying up like it is in Japan, and will be in Europe, China , Canada and many others. U.S. is the “cleanest shirt in the hamper” but still not at replacement rate.

When? 5years, 10 years, 20 years maybe?

Canada’s housing is in a mania which is contingent on loose lending, artificially low rates, and buyer sentiment. Demographics = potential wants, not the ability to afford.

Most of the sellers would chase down the market. I saw this in SoCal to many of my friends.

The peak in prices was 6 weeks ago. They’ve been falling ever since.

There are a couple folks with podcasts in Vancouver that comment on the market pulse and wow what a change. Average mortgage is $800-900k with low household incomes. Can just imagine what the variable rate shock will be for people.

Can’t speak for Canada, but in the UK and NZ, the government offers huge amounts of money to support renters (we call it landlord welfare). Something like £30bn in the UK (1/3 the amount spent on state pensions). They also have elaborate deposit assistance and equity sharing schemes to support first home buyers – mostly for the purchase of new builds (we call these homebuilder welfare).

Is it too much of a stretch to believe they won’t offer some sort of ‘mortgage assistance’ if things gets bad. I could see them easily getting away with stuff like adding a mortgage interest tax rebate to take some of the sting out of interest rate rises, for example. Or they could offer low interest govt loans on parts of your mortgage.

The UK just gave £6.4bn to homeowners in the form of a stamp duty holiday, and there always seems to be money to ‘help’ home prices.

I think you are right that governments will try all sorts of schemes to prop up housing market, on assumption that this burst of inflation will subside on its own soon (the “transitory inflation” narrative), and therefore this propping up will only be needed for a limited time (say, a year or two). I also suspect that central banks will be coming up with all sorts of stalling tactics in order to postpone the necessary interest rates increases, hoping that inflation will fizzle out by itself soon. So I wouldn’t be expecting full-scale housing collapse in the near future. But if inflation will indeed become deeply entrenched (as Wolf had argued in recent articles), then things may get a lot more dramatic for the housing market.

Inflation is set in. Do you think that the dollar general store is going to go back to dollar items. No. We just hope they don’t have to change the name of the stores to $3 General. Inflation doesn’t give back. It claws wins and continues to claw until beaten to a pause. It will not go down from the new highs. The hope it to stop the MoM increases

Interest rates have had a big run up though it’s from a very low base. I don’t track Canada as I do the US but infer the pattern is roughly similar.

Partial retracement is coming at some point. Assuming the 39 year bull market ended in 2020, it’s the next leg of the bear market that will more likely wreak havoc on both the economy and asset prices.

Trudeau is already doing this. They have TFHSA – tax free home savings account. Announced recently by Trudea under cover of a fake foreign buyer ban (fake because full of holes).

The will do more props, but like the UK they are running out of road. The UK recently had record netflix cancellations as people struggle with fuel costs.

You are spot on with “help” for buyers, it’s really a subsidy for sellers. Most people don’t understand how prices are set.

90 percent of the new mortgages are either one year mortgages or variable rate mortgages. That was the only way they could qualify.

What units is the vertical scale in (y-axis), and is it the same scale for all cities, or how does it relate to prices?

It’s an “index” and the values are index values. The scales are the same for all charts so you can see the relative price growth since 2002, one city compared to another.

An index value is not dollars. For example, the S&P 500 index now has an index value of 4,433.

but the units for S&P are dollars

No they’re not “dollars.” Do you you think all 500 stocks combined are worth $4,393? Which is where the S&P 500 is right now. It’s an INDEX, and it’s called “S&P 500 Index.” And the values are index values.

The SPY, which is a tradable ETF that tracks the S&P 500 Index, is in dollars. And it’s currently trading at $437.84, which is the price you can buy it at.

Why are you implying I was thinking like this? :)

I ONLY mentioned the units in which S&P is measured.

From Investopedia:

“The calculation for the S&P 500 is: Index Level = ∑i Pi×Qi / Divisor, where: Pi=Price Qi=Free-float shares”

So the units for the numerator are dollars.

And per my understanding the Divisor is dimensionless:

“… index divisor … scales the index down to a more manageable and reportable level. The divisor is a proprietary value that can change with stock splits, special dividends, spinoffs, and other variables that could affect the index’s value”.

so the units for the quotient are dollars then (dollars/dimensionless)

“but the units for S&P are dollars” is what you said, with which I thought you meant that the units on the axis are in dollars, which they’re not, and you now clarified your thinking on this now.

So looks like we had a misunderstanding. Looks like we’re on the same track.

What’s the point of all this? To boost the wealth effect and keep the consumer economy going?

Yes, A primary reason indeed.

The PM background is a school teacher, the FM a journalist, the defence minister a lawyer.

How can things go wrong, if you see what i mean?

InExcess:

Really? As if the economy in the US is very different with our career politicians and revolving door Fed bureaucrats. Come on!

Yes, but their “wealth effect” is actually a completely bogus hypothesis – or outright fraudulent lie – which does nothing but impoverish the working class and the poor. We have a disease of central bankers. We need to clean house on all these scvm. GET RID OF THEM. They are failures.

It’s what happens when a country has given up on growth and decides to just do the equivalent of drinking itself to death.

I’m in Canada and it’s actually that Canadians have gone insane.

Here is one sample comment from another forum the other day:

> Toronto has much further to go, compare the prices to London and you can see that.

This is deluded. London! Next to Europe. Masses of theatres, restaurants, culture, next to Europe, hundreds of years of history, etc.

Salaries in London are far higher too. But none of this matters to the financially illiterate Canadian.

The blabbermouth is talking right now…….after Israel central bank yesterday (a Friend) cut its holding of US dollars and for the first time is holding Chinese currency as a small part of its reserve………if this dude and his idiot friends don’t get these rates up the hyper we have been talking about is about to become possible.

Israel stated they need a currency in their reserves that pays a real yield.

I suspect after all the crap he poops out today….its going to be as hawkish as this weak limp political tool can stand.

There may be a bear in gold short term as rates increase but as soon as this pack of morons makes their widely anticipated turn (at the first sign of weakness) gold is going to explode.

Money has no friends

Rate increases are already causing the market to roll over.

The 1-5 year bond yields rose first last year (before the Bank of Canada rate changes this year) so for the past year or so, people were rolling their fixed rate mortgages into variable ones to keep their lower rates.

So now that variable rates are rising sharply (75bp in the last couple of months with more to come), they are immediately passed on to a big percentage of the market that is sitting in variable rate mortgages. In addition, people coming up for renewal no longer have ‘anywhere to hide’ – whether they choose fixed or variable, the low pandemic era rates are no longer available.

It is always an interesting question on measuring the impact of rate increases, is it the absolute change that matters, or the relative one. That is, if rates go from 1% to 2%, is that the same as going from 4% to 5% (up by 1%) or going from 4% to 8% (doubling).

Given that mortgage payments are a mix of interest and principal, I guess the answer is somewhere in the middle, but the more it looks like a doubling in terms of impacts, the faster and more severe the housing (and by extension economic, since to a large extent housing *is* the economy in Canada) downturn will be.

Wolf – it’s your site, and it is fantastic, so ignore me as you see fit, but from a Canadian housing market perspective, the big bond that everyone watches is the 5 year. The majority of the market (outside of recent times when so many switched to variable) sits in 5 year fixed rate mortgages and this is the bond that sets the tone for the whole market. So it would be nice to see the 5-year chart in your articles on Canadian housing market (could drop the 10-year since it is not as relevant to the housing market).

Not a big deal, obviously I can look up the 5-year chart myself easily enough, just trying to help.

P.S. The last article had lots of comments on the acronyms for the high flying NASDAQ stocks (e.g. FANGMAN et al). I’ve started to see people throwing around acronyms for the housing bubble countries that may suffer in this round of global inflation and rate hikes (Canada, Australia New Zealand, Sweden = CANS as the new PIGS and and so on) so maybe something for people around here to start working on :)

US CANS?

CANSUS?

CANSUSLOL?

CANSF-UK-US

CANS-FRANCE-UK-US

ROLF…

I keep thinking housing bubbles may be global this time around. Loooong Acronym if that’s the case.

PIGS = Polish Irish Greeks & Slavs

Thats my former HS 😀

Acronym PIGS is considered obsolete.

Probably still used by the RCMP insensitive brutes in private conversations.

In Europe, Pigs stands for the Southern European countries, ie, Portugal, Italy, Greece and Spain…. Countries that live off their richer EU member friends, mainly Germany and Holland…. The Germans are so generous……you’ve got to love em….

also PIIGS

“The Germans are so generous….. you’ve got to love em…..”

Grew up there. Yes, emphatically

Got busted by the RCMP at a big (somebody’s parent’s vacation home) party in Penticton in ’63. We were all underage and still in HS so they took names, the booze, and left.

Tried to scare us a bit, but mostly just called us all “stupid”.

Also had them take our joints from us in ’66 at Stanley Park. Just crushed them into the grass, and said “stupid” and left.

Things are much different now, down here, too.

90 percent of the new buyers are in one year mortgages or variable rate mortgages.

ROFL…I mean

Anecdotal. But….

My subdivision of about 80 homes had ZERO homes go up for sale in the last 2.5 years. Pre-covid, our neighborhood averaged 2-3 home sales per year.

My friend who runs the HOA board indicated we have three homes going up for sale next week, with a potential 4th in the next 2-3 weeks. That’s what we know about so far.

That alone is back to the pre covid rate in the next week.

There could be a mass increase in inventory over the next 2-3 months as people try to cash in as rates are going up.

The people are completely clueless the top was put in 6 weeks ago everywhere except in Alberta. I already shorted Home Capital and EQ Bank. Some of the private home mortgage insurers are also listed on the TSX.

Careful with the private insurers, I doubt the government would let them fail, last time one failed was in the 90’s recession and it was bailed out (arranged buyout) then.

A Canadian blogger wrote:

“Record numbers of Canadians are sucking greater amounts of equity out of their homes, even as the value of that real estate faces declines. In February HELOCs totaled $162,000,000,000 (that’s billions). This was the fifth consecutive month of expanding home equity debt, and the fastest rate of increase in a decade.

HELOCs almost always carry variable rates. As the prime ups at the chartered banks, so augments the cost of these lines. Lately that prime jumped from 2.45% to 3.2%, on a path to 4.5%. By the way, $162 billion at that rate means households would pay just under $7.3 billion per year in loan interest.”

Thanks that’s some nice future forced sellers!

Trudeau should get some more props lined up fast.

C$1M for a cottage in the middle of nowhere, Ontario.

Home prices doubled went up 100 percent in the last 2 years in Gravenhurst, Ontario Bracebridge, Ontario and Bancroft, Ontario as well as other other fringe Ontario cities.

If it’s on a fresh water lake it’s not middle of nowhere- it’s on water and worth the money. Canada has rule of law, minimal violence and riots, foreign investment and a welcome mat for global criminals to park their wealth.

Prices may slide but they won’t crash.

They will halve… atleast!!!

There will be no soft landing

FOR ALL THE FINANCIAL PAIN COMING SOON…..YOU ARE NOT ALONE….OTHERS SHARE IT ……

Shock and denial.

Pain and guilt. …

Anger and bargaining. …

Depression, loneliness and reflection. …

Acceptance and finally paying in RUBLES….

These are stange times….

Fred Flinstone you wrote … Israel stated they need a currency in their reserves that pays a real yield……….

Disagree…..China and Israel and everyone else just learned money in Dollars can be stolen …just ask the Russians and the Taliban. When we decide Israel is an “Apartheid regime” …USA will also steal their money

I am an American and even I want my few tiny $$ overseas…..lest Trudeau and Biden and any other politician choose to grab it for sins ..like liking a FaceBook post they deemed subversive.

Mortgage rates have gone up more than the 75bps hike. 5 year variable mortgages in Canada were going for prime minus 120 (1.25%) a few months ago and are now P-70 (2.5%). People avoided the spiking CA5Y yield by going 75/25 for variable/fixed. The old ratio used to be less than 50/50.

I’m in the market for a locker in the GTA and came across this listing on Zillow:

Lockers for sale for $C6,000.

11 Charlotte St, Toronto, ON M5V 0M6

“We Have Lockers Available On The First Floor Level 1 (Mainfloor), P1, P3 & P4. Must Be Occupant Of 11 Charlotte Street. Buyer Is Responsible For Seller’s Lawyer Fee Of $750.00 + Hst Payable To Goldman Sloan Nash & Haber Llp.”

It is in instances like this…and what is happening in the US…

that it is time to ask…

Why is the government involved in mortgages at all?

To keep the consumer spending merry go round going, that is why.

Also there are other factors a 2 year moratorium on foreign purchases and in Nova Scotia a 5% tax on out of province purchases and a 2% additional property tax on out of province owners. that will be a surprise to some when they get their tax bill. The timing is perfect as housing crashes send the buyers away. I personally have no skin in this game. higher prices just mean higher taxes as you still have to live somewhere.

The most splendid housing bubbles in Canada. Great! All this means is soon Wolf will release the most splendid housing bubbles in the US. I can hardly wait, it’s that time of month again.

Thanks for the heads up!

Coming April 26 to a theater near you :-]

Please, the US housing market can’t hold a candle to the Canadian market in terms of insanity. PS BoC hinted at a possible .75 rate hike in June today.

Bombs away!

I live in Markham and the Chinese are now listing their homes for sale. Every Chinese person does the exact same thing at the exact same time no matter what it is. They have no one to sell to. The peak in prices was 6 weeks ago. A good percentage of them are leveraged all in on real estate. One has only to look at what home prices do in Markham, Richmond Hill, Unionville and Stouffville to get a barometer for what home prices will do in the future for the entire golden horseshoe. It’s always been this way since 2015. In Markham new townhouses sell for 40 to 45 times annual income and they have no basement.

40-45x income? That can’t be. 10x maybe

It’s correct the average new townhouse in Markham is about 2 million dollars. The average wage is at best $50,000 a year. One or two rich Chinese can skew the figures. The real gross annual income in Markham is around $45,000 a year if they get tossed out.

Here’s the average income for for 2022 in Scarborough the city that borders Markham to the south. It says about $39,000 a year.

https://ca.talent.com/salary?job=scarborough

This web page has it at even less $40,000 a year in Markham in 2022.

https://ca.talent.com/salary?job=markham

Jesus. I didn’t imagine townhouses in Markham would be so expensive. average household incomes are higher than $50k, probably more like $80k. That’s still a big multiple though, around 25x

They can always sell it to an oil dictator from Angola, Equatorial Guinea, or Russia.

Fentanyl and meth dealers from Hong Kong are also buying up mansions in Canada.

Unless you’re a Toronto top 5%, who else can afford current real estate prices without the Bank of Canada giving away free money to the upper middle class?

Meanwhile, Ontario Premier Doug Ford wants to do a Mike Harris and gut social assistance, while the fallback will become subway murder statistics.

INCREASE the interest rates.

INCREASE social assistance rates for OW + ODSP.

INCREASE the OAS and GAINS

The housing bubble is just insane in Canada! Glad to see a few cities like Edmonton not participating in this madness. Crazy to see a city like Halifax get swept up in it though.

Don’t give the Edmontonians more credit than they deserve. The oil patch has been a shit show for a long that’s the only reason it’s not experiencing a housing bubble. Halifax is being bid up by Ontarians looking for a pretty place to retire. I know several people who sold their homes in Ontario and retired to the east coast in the last 12 months.

have you heard about cities in saskatchewan?

I’ve been mulling over the prospect that Putin may trigger a wave of europeans looking to emmigrate to Canada. I don’t have much hope that things will be very stable in the future in Ukraine, Poland, Lithuania, Latvia and Estonia. Historically, citizens displaced from those areas made their way to Canada in the post WWII period. Housing policy wonks, don your tin foil hats and start planning for the onslaught of new Canadians..

Thanks for the article Wolf, big fan of your intelligent work! I think the near term movement of prices may be dwarfed by what happens when all of the buyers who bought at record high prices and record low interest rates face mortgage renewals at what will potentially be much higher rates. Even though many sales have been full cash, I suspect a considerable amount of those funds were pulled out of existing properties to finance the new purchases. Seems like there really is no escape from the impact of significantly higher rates. I wonder if this will lead to further huge rent increases as landlords try and recover the additional costs?