“It is of paramount importance to get inflation down,” she said to get markets to prepare for what’s coming. And they’re preparing.

By Wolf Richter for WOLF STREET.

Fed Governor Lael Brainard, one of the biggest doves on the Fed’s monetary policy committee, explained this morning in detail that inflation is hitting lower-income households much worse than higher-income households, and that it is hitting disadvantaged households, such as those with limited access to online shopping, even harder, and their inflation rates are far higher than the national average inflation rates because the basket of goods they’re buying is systematically different, and that they’re spending nearly all their money on necessities, and that they often cannot substitute items whose prices have jumped with lower-cost items, because they’re already buying the lowest-cost items to begin with, and there is no way to go lower on the ladder. They can only buy less, such as buying less of the cheapest store-brand cereal, which is the example she used.

It was an indictment of Consumer Price Inflation, depicting it as the scourge that it is for the people at the lower half of the income scale. And then she said that the Fed would have to, and will, crack down on inflation to get this under control.

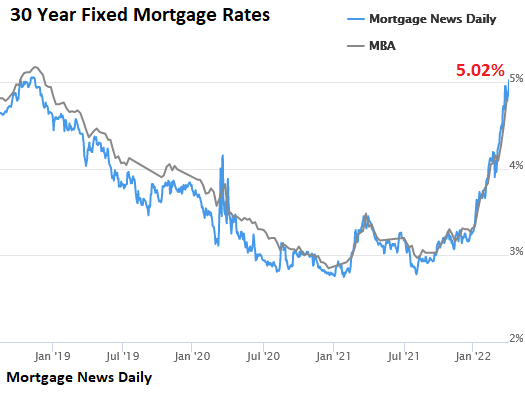

Upon the speech, whose text was released in advance earlier this morning, the average 30-year fixed mortgage rate spiked by 18 basis points to 5.02% today, the highest since November 2018.

But back in November 2018, this measure of mortgage rates by Mortgage News Daily, had peaked at 5.05% briefly, before the Fed buckled under Trump’s withering attacks. But back then, inflation was below the Fed’s target, and now inflation is spiking and out of control, and it’s the White House that is now under withering fire from voters over the spike of consumer prices. There isn’t anything in recent years that compares to this. The comparison has to be to the 1970s.

And instead of fretting about the spiking mortgage rates, Brainard agreed that the market was beginning to price in the coming “expeditious increase in the policy rate” and “a more rapid reduction in the balance sheet” compared to last time:

“Consistent with these expectations, we have already seen significant tightening in market financing conditions at longer maturities, which tend to be most relevant for household and business decision-making. For instance, 30-year mortgage rates have increased more than 100 basis points in just a few months and are now at levels last seen in late 2018,” she said.

Brainard’s comments today added a new political reality to the Fed’s policies: Inflation is a horror show at the lower end of the income spectrum, with much higher inflation rates among these households than the national average inflation rates that are more reflective of inflation rates experienced by higher-income groups.

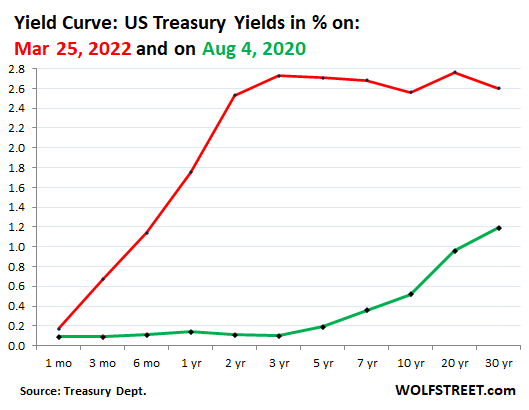

The two-year Treasury yield spiked by 9 basis points to 2.53% by noon, the highest since March 2019, having exploded in six months from 0.2% last October, which is a huge move. Another 30 basis points will take the two-year yield to 2.83%, which would be the highest since 2007. And the Fed hasn’t even seriously begun to raise rates. It is just telling the markets to get ready for it:

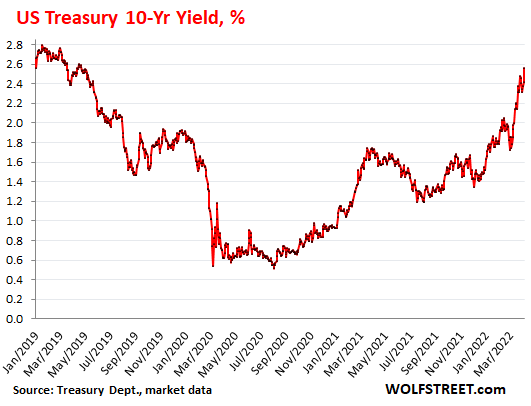

The 10-year Treasury yield spiked by 16 basis points to 2.56% by mid-day, the highest since April 2019:

The yield curve re-un-inverted between the two-year yield (2.53%) and the 10-year yield (2.56%), after the 10-year yield outspiked the two-year yield.

But the yield curve retains its kangaroo-shape: very steep from the one-month yield (0.17%) to the three-year yield (2.73%) and then essentially flat, with a small dip at the 10-year yield, a rise at the 20-year yield, and a dip at the 20-year yield:

The longer maturities – the five-year yield to the 30-year yield – will feel the Quantitative Tightening when the Fed will shrink its balance sheet by several trillion dollars. And this will levitate the yield curve at that end, even as the short-term yields are coming up with the Fed’s rate hikes. The green line is the yield curve at its historic lows in August 2020:

This is what the market reacted to:

“It is of paramount importance to get inflation down,” Brainard said in her speech today.

“Currently, inflation is much too high and is subject to upside risks. The Committee is prepared to take stronger action if indicators of inflation and inflation expectations indicate that such action is warranted,” she said.

“We are committed to bringing inflation back down to its 2 percent target, recognizing that stable low inflation is vital to maintaining a strong economy and a labor market that works for everyone,” she said.

The FOMC would “continue tightening monetary policy methodically through a series of interest rate increases and by starting to reduce the balance sheet at a rapid pace as soon as our May meeting,” she said.

“I expect the balance sheet to shrink considerably more rapidly than in the previous recovery, with significantly larger caps and a much shorter period to phase in the maximum caps compared with 2017–19,” she said.

As reminder: Last time, the caps after the slow phase-in, were set at $50 billion per month in balance sheet reduction. This time, the caps would be “significantly larger” that $50 billion a month.

“I expect the combined effect of rate increases and balance sheet reduction to bring the stance of policy to a more neutral position later this year, with the full extent of additional tightening over time dependent on how the outlook for inflation and employment evolves,” she said.

And so far, the “outlook” of the Fed has evolved drastically, to now seeing much higher inflation for far longer than a year ago.

For the consequences of the Fed’s policies, read: My “Wealth Disparity Monitor” of the Fed’s Money-Printer Era: Holy Moly. April Update of the Greatest Economic Injustice in Recent History

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Jawbone the market into pricing in what they now wish they had done awhile ago. I get it.

FYI, Lael, this inflation can crush anyone, regardless of income level. Consider the many people wanting to buy a home, or those in a tiny started home who did the “right” conservative thing and are now totally priced out of the next tier up.

No. Inflation is not going to crush Elon Musk. Or Jeff Bezos. Or Jerome Powell. Or Lael Brainard.

Depth Charge wrote: “No. Inflation is not going to crush Elon Musk. Or Jeff Bezos. Or Jerome Powell. Or Lael Brainard.”

Inflation may not get them. But the upcoming Panic, err, deflationary Depression may hurt them a bit. But it is more likely to hurt the bottom 80%.

I was reading up on events preceding the Panic of 1873. Lots of eerie similarities to what has been happening lately.

The Republicans stole the Election of 1872. The only reason they failed in 2020 was because the former guy is a total incompetent. Then you have all the corruption in business (and government) after the Civil War.

Even the so called “Stimmies” some people like to call “socialism” is eerily similar the stimulus given back then to the railroads. The recent stimmies also went mostly to private businesses…..even the money given to states and local government looks like it will now be used to give the 1% “tax relief”.

The “New Green Deal” also sounds eerily similar to the subsidies to railroads in the late 19th Century.

Then you have the similarity to the strikes, and general labor unrest. The US military was used to crush Labor then, and I suppose it could happen again.

Hmmm…….and there was a lot of immigration after the Civil War as well. But nobody complains today about immigrants (or do they?).

Just my 2¢…….

Inflation does not crush people with significant assets. The assets go up. If their assets and income exceed their expenses, they gain.

Also, those same people — investors and asset-holders — have been enriched by Fed policy already over the last 20 years. This is freely admitted by the Fed. They implemented a trickle down rescue.

If the interest rates are dependent on inflation and if the affordability assets are dependent on interest rates then assets would go down with interest rates going up.

Yes, some assets (not all) are likely to fall temporarily.

But people with significant assets will not be crushed by that. They won’t be forced to sell those assets at a low point. Nor will they be greatly inconvenienced by higher prices.

People without assets or with relatively few assets are in danger of being wiped out by either or both of those possibilities.

Ed

Top 1% hold 50% or more of Wall St wealth, top 10% more 90% of wealth and the bottom 90% less 7%!

Is it their trickle down wealth effect? Good Lord!

If those assets are leveraged they very much get crushed.

If they are leveraged, then they don’t really own them. Whoever supplied the cash to purchase the assets are the true owner.

the housing market is a bubble, but housing market bubbles take time to burst – like 3 years. interest rates will need to rise more and home inventories need to rise for 3-5 months solid before we get a real significant oversupply of houses.

my guess is that once prices start to drop, alot of owners will finally rush to sell their home – at the same time, so they will be competing for buyers, who will not be showing up.

the first step is for demand to fall and inventories to slowly rise during the summer, while mortgage rates go to 6% or more.

I suppose the word “crush” is a relative term, like most everything else. However, there is a significant difference from the human toll perspective from being “crushed” that you can no longer afford your dream home or can’t move up from your current one… and being “crushed” because you can’t afford to feed your children or get them proper medical care or pay next month’s rent.

I have a neighbor who complains incessantly about the inflated cost of new wood flooring for his large, restored home… but never about the inflated value of the home itself. People tend to see what they wish to see, and (in my experience) most are hopelessly myopic when it comes to economic/social issues.

And in this financial system the homeowner can extract that inflated value from their home. Very similar to 2008, home values were rising, homeowners felt pressure to improve their homes (to stay current with rising values) and they were incentivized by the home ATM to REFI and extract those gains. While some of them were living large, many were paying (rising) medical costs, there was no ACA then and HC insurers were raising premiums. Now the social safety net is tighter and the home equity market is looser and people really really hate the Democrats? If gasoline went back to half what it is today nobody would be complaining about inflation, and that is a function of the 2020 oil market collapse, which took capacity offline. They can stop selling oil to China and send LNG to Europe and Japan and the circle will square.

The student loan payment pause is inflationary.

Pause was just extended yet again. It’s looking unlikely that it ever resumes.

Federal student debt is 1.6 trillion. This is like dropping an extra 1.6 trillion dollars of stimulus into the economy.

Your handle says it all: not smart

What part of his comment is “no smart”? He’s exactly right. The Dems are going to continue to provide loan relief for continued pauses until either Biden caves or they’re voted out of control starting in 2022.

And, he’s perfectly correct in stated these pauses are inflationary. It’s like telling 1/6 of the $10.5T in mortgage debt to permanently take a break.

I’m pretty sure he meant that extending the pause forever is equivalent to just handing out the money.

Correct. I meant to say that the politician’s “solution” was “not smart”

Is it too late to get student loans? I’m 41 but just curious LOL.

They should be retroactive, and adjusted for inflation.

When I went to college in the 70’s, it was $4 per credit hour. A Semester, Full Time, was 12 credit hours, cost $48. This was/is a well known State University.

I remember writing the check.

i am SO TIRED of hearing the whining students about their student loan debt.

first off, noone can actually run up much debt for undergraduate studies. the max you can borrow is around 30K, so it is like the debt on a car.

second off, if you go to graduate school and cant get a job to pay off your student loan afterwards, then you are an idiot. just because some mediocre university will accept you to study some worthless graduate degree does not mean you should get the degree. go get a job in your field and get experience working. make sure you graduate from undergraduate with plenty of internship experience, so you can get a job when you graduate. my oldest daughter had 6 internship, took a gap year off and still graduated in 4 years. she took courses at community college and took 18 units every semester (because the price is the same as the normal 16 units), so we saved one full year of college ($85K). we had a plan from day one to fund it.

the problem is that kids believe that an education is their right and should cost nothing, so they dont look at the hard numbers of the cost and benefits. unless you are rich and money means nothing, getting a degree that doesnt lead to a job is a luxury you cant afford.

honestly, with my younger daughter, I am going to push her to start a business in her area of interest BEFORE she goes to college, or during college. i mean, does the world need another employee? no, the world needs another freakin Elon Musk. maybe we use her college funds to start the business.

it is time for our whole society and kids to grow the heck up and stop asking for a free ride.

EVERY industry where government gets involved in funding – higher education, healthcare, housing – is highly inefficient and prices are unaffordable. healthcare is going to be revolutionized by DTC telemedicine. higher education is unfortunately not being forced to be cost efficient or to lead to good paying jobs.

gamnetv, loved your post until this part…”the world needs another freakin Elon Musk”. No, the world definitely doesn’t need another Musk. Hell no. And he has been the ultimate free rider from EV subs.

Musk’s companies currently employ over 100K world wide. We don’t need one other Musk, we need 10.

Elon has achieved more than you.

You said it yourself: “we” made a plan. “I” am going to push her.

Without you presiding over your daughter’s decisions she probably would have done the same thing you’re lambasting everyone else for doing.

Good for you and for her that she has you, but not many students have a similar adult supporting their decisions.

I think you are missing the more important part of post-secondary education isn’t that you get a better job (which is still true), or that you gain access to better future connections, but that a well-rounded education and development of critical thinking at a high level leads to better human beings with better outcomes for subjective happiness and fulfillment without regard to earning potential. Access to post-secondary education is a human right like access to basic healthcare. I can see why US people get salty about it because it is not provided. I am Canadian by birth, raised in US. I paid $6000 a year to go to undergrad in Canada in 2002-2006. My sister paid $40,000 a year in the US.

Agree. Education has great worth beyond affecting earning capacity. A society which believes in educating its children – and creates sensible policies to that end – is where I’d rather live.

And you touched on what may be the unconscious backdrop of Gametv’s remarks: The US has wandered into a higher education cul-de-sac that is both overcrowded and too costly to be practical for a great number of young people.

no, neither health care nor college education is a human right. the only human rights you have are to be left alone for a number of things. there’s never a “right” to have someone else forced to pay for your stuff at gunpoint.

A human right?

Your “right” demands somebody else provide it and pay for it.

Rights are not a product. Rights are free. If a “right” has a monetary cost, then it is not a Right.

“Critical Thinking?” Really?

If you most college students get “a well-rounded education and development of critical thinking at a high level” you’re smoking crack.

Your sister could easily have paid similar tuition at her state school in the US. Only a chump pays 40K a year for undergraduate tuition.

“Access to post-secondary education is a human right like access to basic healthcare.”

Access to post-secondary education is MOST CERTAINLY NOT a “Human RIGHT” Bobble.

That is a completely ridiculous statement to make.

What percentage of adult humans alive today have ‘post-secondary education’? I can assure you it is under 10% of the global population.

You have just invented a “Right” that doesn’t exist!

My community college nursing school loans were no more than $18k. 1.5% & 3.5% interest rates, fed loans.

Deferred a few times when I was under employed: graduated nusing school in the GFC recession hiring freezes, and twice while out of work due to complicated pregnancies/childbirth, VERY briefly defaulted during the divorce (he timed it well–at 2 weeks postpartum SAHM. Don’t be a SAHM no matter what ladies, trust me, the law is not in your favor and you can end up homeless with infants before you’re legally allowed to return to work, like I did. Doing great now though).

Paid religiously in between all that static on Income Driven Repayment. Loans which still got sold to several servicers that tacked on $10k each and jacked up the interest.

Now owe $50k. On $18k loans that were already half paid off.

I was no Philosopsy major but I dare say the bootstraps and avocado toast philosophy doesn’t account for notoriously bad legal contracts like student loans for medical degrees, or marriage for that matter.

I’d gladly pay the prolincipal and interest rates I closed on the loans woth, but, well, silly spoiled Millenial doesn’t wanna quit eating to pay $30k in tacked on arbitrary servicing fees.

Good for you for staying afloat and not dumping the problems on others! That is virtue, we need to rediscover! Those are the unsung heroes.

I am timid and patient, and fine with that. I finished law school more than 10 years before I got married. (It turns out a divorcing spouse who contributed during school could claim a piece of my law career — yikes!). Undergrad through law school was all-in less than $20k back then. Even so, I strained early to pay off my student loan but did. After divorce, despite being the only one who ever paid a dime on our house payments, I had to buy out the departing ex. But I kept the house. A great trade.

Contracts have risks, especially in light of future events, yes. (I teach that at community college.) I am proud of teaching community college and not gouging people on tuition. And marriage is an open-ended constantly-reshaping “relational contract” beyond my comprehension or competence. So I don’t sign on.

I went to college the old fashioned way.

I went to fight a war in the mid 1960’s and came back home and used the G.I. Bill to get through engineering college. My $222/month covered everything, but I did work nights and weekends to pay my way through the rest of the expenses (apartment, food, junk car, etc). It was tough, but it was over in just 4 short years.

The G.I. Bill (in its new form) is still available to veterans. Also, one can go into certain colleges like Texas A & M under the ROTC program and have tuition paid all the way.

My granddaughter went thru college on grants and scholarships. She didn’t owe a dime when she graduated the University of Texas five years ago. The money is there, and all she had to do was apply for it. That even surprised me that it was so easy to get the funding.

Bless your heart. I was not happy to hear that the government paused re-payment yet again on student loans. Loans were requested and granted and backed by the Federal Government. The people should pay back what they owe. My gut feel is these will all be erased by executive order.

What a gift to give the voters

Agree. It’s inflationary.

So, what happens to people like me who have privately financed student loans, and have been paying the entire time covid has been going on?

You must be “Privileged”.

So pay up. Pay your fair share.

i can only testify from personal similar experience LC:::

when i paid the last $3K to my private lender, he broke out a $3K bottle of cognac, and we shared it with a TON of wonderful memories for him and me:

He finally ”opened up” about his experiences parachuting behind the lines, twice in WW2 after TPTB found out he had spent his HS Jr year in Germany and was completely fluent,,, walking out the first time with the help of the French ”partisans” ,,, stealing a plane and then crash landing it the second time and had the scars for the rest of his life…

Hope your pay off won’t be quite so dramatic, but encourage you to PAY OFF your loans,,,, NOT for the lender, but FOR YOU and YOUR health…

”some folks” think they can do a or the dirty deed, including reneging on their word, and get away with it without ANYT recriminations:::

Most folks suffer for years until they real EYES that is NOT true,,, some go ahead and ”pay the piper” and go on to happiness of each and ever kind

others continue to suffer — at their own hands/minds to be sure

All I hear is talk out of these people, with no action at all. “We understand that inflation hits the lower income households the hardest,” said Jerome Powell as he continued to pour hundreds of billions into MBS purchases for another 6+ months after uttering such hollow words.

Shitcan the entire lot of these creeps. That Jerome Powell still has a job after such a horrific performance is very telling of the systemic rot we are currently dealing with. Not only was he 100% wrong in his “transitory” BS, his group of fraudsters were frontrunning the stock markets on their own insider information. These guys are anti-American financial terrorists destroying the standard of living of the masses for their own personal financial gain. Yet they sit back for months upon months arguing over a measly 25 basis point rate hike. What a JOKE.

How many different ways can you say the exact same thing in all of your comments?

Would you please add something of value to the conversation?

GFY stands for good for you right?

How many times did the Fed say it would normalize interest rates? Surely, the harm caused from that is 1000x worse than anything Depth Charge has to say. It’s interesting what bothers you, and what doesn’t.

+1 PG! I was dreaming many times of the option to hide “bash the FED” comments” – would save a lot of time to read just information

Jawboning is one of the most powerful tools the Fed has. That’s how it gets markets to do what it wants them to do, in both directions.

So now the average 30-year fixed mortgage rate is over 5%. That’s is going to start working.

The two-year yield is over 2.5%, while banks are sill paying near 0%.

Look, there is a two-year Treasury auction coming up on April 26. If yields stay on the right track, I’m going to put in an order to place some extra cash that is now earning near 0% at the bank.

Jawboning works!!

I am confused. The Fed should not be required to Jawbone if the free markets are working.

E.g. Fed stopped buying treasuries => no one else should buy it at negative real yields (yields – inflation) => new auctions will need to raise real rates to positive territory => yields snap overnight to 8% => No Jawboning required.

Does Fed needs to jawbone only because other entities buy treasuries because they still believe in Fed Put that they cannot lose money, and Fed would bail them out by lowering rates again?

“The Committee is prepared to take stronger action if indicators of inflation and inflation expectations indicate that such action is warranted.”

Did we not get this indication 6 months back? Yes we did and they said “Inflation is transitory.” If dumbnuts like us could figure it out, what were the PHDs at Fed doing?

Also this comment has an “if” that indicates that Fed “STILL doubts” whether “Strong action is warranted”.

Raj,

Jawboning happens in real time. Markets react instantly, as we can see.

Actual monetary policy transmission to the markets has a long lag, many months, but it will eventually get there. That’s why jawboning is an official tool in the Fed’s toolbox, known by official names such as “communication” or “forward guidance.”

The Fed used jawboning massively starting in March 2020. Every time it made any kind of announcement of what it is thinking about it might do, markets spiked. That’s how jawboning works in real time.

Its whole corporate bond buying thing was one gigantic jawboning exercise that caused the biggest corporate bond bubble ever, and then the Fed ended up buying almost nothing (just $12 billion of the $750 billion it said it would buy). I covered this at the time. It was an amazing thing to see it being played out that way.

“Look, there is a two-year Treasury auction coming up on April 26. If yields stay on the right track, I’m going to put in an order to place some extra cash that is now earning near 0% at the bank.”

Me too.

Jawboning works! But how long?

Global Conditions are ideal for rip-roaring inflation, unlike anytime (even in 70s) before b/c record in Public and private sectors, ZRP kept too long, stimulus more than needed, chain supply problems still lurking, Covid is still here. Current economy still neeeds fossil fuel, whose production being reduced. ESG is ‘castle’ being built in the sky! 30M barrels being released Stragic Reserve is a joke, since USA uses almost 20M barrels/day!

We are in uncharted waters!

“Jawboning works! But how long?”

Until the slow-moving monetary-policy transmission catches up.

Jawboning is effective in real time, as we can see. The transmission of monetary policies to the markets takes months, and its impact on inflation is known to take about 18 months.

You sure you want to lock in two years at 2.5%? (asks the guy who has said that many times over the last decade, and sat in too much cash because of it).

We are holding out for when the FFR goes to at least 7%, then going to buy the TIPS with that as the ”base” rate that stays at that for the whole enchilada of time…

Otherwise, as others on here have said, once the FRB does go back to it’s clear corrupt decreases, at the end of the 2 year, you’re back to where you started, getting nada at the bank.

Or just ”invest” in diamonds, unicorns, perpetual motion machine, gravity mirror, etc., etc.

@ Wolf –

If you succeed at getting two year Treasuries at 2.5% on April 26th, what do you project happening to the purchasing power of that money spent for the Treasuries?

How much better or worse off will you be two years later?

Why are you willing to tie up money for two years at 2.5% when inflation far exceeds 2.5%? What do you happening with inflation?

So if I do nothing, and the cash earns nothing in the bank, the purchasing power also declines, but I don’t get the interest. And if I buy stocks, and they plunge 50% in two years, the purchasing power gets double-whammed by the plunge and by inflation. The calculus is always the same. In this environment, I’m trying to find a mix of the least worst options. Inflation is a shitty thing :-]

Do you think DC is factually incorrect ?

If so, where in his statement is he wrong ?

DC does have a tendency to emotionally charge his posts,

but that is just his style.

Actually I think Depth Charge is completely true in everything that he says.

But seriously, when you’ve made your point once, why make it again? Or three times? Or like, fifty times? At some point you have to add value to this conversation by talking about something else that adds to the corpus of knowledge.

We know the Fed is late. We know the US elite repress and steal. We know it’s not fair.

And besides it is a ton of crap to have to scroll through. The more garbage people post here the more junk you have to sift through in order to get to the good stuff.

Seriously, posts from really intelligent helpful people like Yushan and Gametv (and Wolf?) get buried because of “powell! inflation! rabble rabble rabble” comments.

Peanut G.

Why not ask the Fed to stop repeating?

“The Committee is prepared to take stronger action if indicators of inflation and inflation expectations indicate that such action is warranted.”

This comment has an “if” that indicates that Fed “STILL doubts” whether “Strong action is warranted”.

So how is this statement different from previous statements that essentially meant “Fed may do something stronger, sometime in future, to address inflation?”

Don’t be too hard on him.

He had a terrible misadventure with a nail gun.

He keeps saying the same thing.

He keeps being right.

They don’t like the straight forward truth, and people who don’t acquiesce to their narcissistic demands.

YES trmrd!

And one can skip through whom so ever one wishes NOT to read again and again when so ever one chooses, eh?

I will testify that I DO do that when I have read any of the frequent commenters on here once per article and they post over and over again.

Please feel free to skip anytime YOU CHOOSE!!!

”All generalities are false, including this one.” MAY apply???>

Coming to WolfStreet to read the article & commentary is like going to your favorite café in the morning to sit at the big table with all the regulars whose company you enjoy. It’s comforting. It’s a community. I look forward to the personalities & byplay of ideas. I appreciate thoughtful commentary & that Wolf manages the site to the rules he stipulates. I don’t want Depth Charge to shut up or VintageVNvet or phleep or any of the other regulars, but I may choose to skip Peanut Gallery for awhile.

Like TeacupDragon said, this is a place to get good information from Wolf and the community members.

In the short time I have been reading these articles and comments, I have learned a lot, and that knowledge has been real helpful to me. Actually, I wish I had found Wolf’s site years ago.

even “righter” would be to simply end the Fed

“How many different ways can you say the exact same thing in all of your comments?”

As many ways as possible to ensure that markets get it before the action. Markets have still not got the memo. May be the Fed’s pussyfooting around rate hikes with a 25 bps in Mar did not help.

Jawboning is Fed’s way to make sure the action (rate hike – BTW likely to be 50bps in May and QT > $50B) that follows does not crater the market.

There is nearly a month of jawboning left till the next meeting.

It might be that they’re doing exactly as they’re being told.

Yes, I would guess these jawboning sessions are test runs to get the market’s reactions. It’s more than likely all planned.

Perhaps, all this is intentional.

If it is, then this “Plan” is brilliant, and being executed brilliantly.

Look at it “backwards”. If this is intentional, ask “why?”. Ask, “what is the poin”t? What is the “goal”? Why would this be intentional?

If you do that, everything becomes so clear it will shock you.

Connect the dots for me. Seriously. I just now reading this article gained an intuitive understanding of what a yield inversion is. That’s how new I am at this.

So seriously, lay it out for a financial newb.

can you help me with this as well?

you are 100% correct. The Federal Reserve needs to exposed every second repeatedly for the crime they have committed and are still committing. One of the few people who knows who is the worst culprit behind all of this mess. It is a very corrupt system that will meet its own demise from the inflation monster it has created.

continue your good work man! The Fed needs to be exposed every day for the massive crime they are committing. We can never forget who is the biggest culprit.

Ha! We know the Fed is lying! The Fed says one thing, but contiunes to do the other. Principal is being reinvested in MBS rather than being allowed to roll off.

No, it most certainly is not.

What is the FOMC going to do when most of the inflationary drivers come from supply side economics?

You can destroy demand all you want but monetary policy can’t create more oil and wheat…

It doesn’t matter whether the inflation comes from demand side or supply side. Either way, you have to raise interest rates, even if it causes a recession and temporary drop in corporate profits.

Speculators will suffer. Everybody else gains.

This is going to be unpleasant for a lot of people for a long time.

Milk in my area is now north of $7 a gallon. its $10 a gallon at whole paycheck.

I paid $3.09 last week.

This is like driving a car with the “pedal to the metal”, and then realizing you need to slow down.

So, don’t adjust the right foot, but not stomp down HARD on the brakes.

Gee, what could go wrong?

That is the state of our economy.

I paid $1.99 yesterday. Usually it is $2.99 in Seattle.

You need to pack up and move.

Shells, where do you live where milk costs $7?

Are you buying an over-marketed, over-priced organic milk from Whole Foods?

Walmart has gallon 2% milk every day for $2.39. Yes it used to be $0.99 on sale in years past…

Milk is the perfect food for a baby cow.

I stopped drinking it altogether about 40 years ago. Cheese or yogurt would be a better choice.

It will still matter. There will be no “soft landing”. This recession is going to be a doozy.

Somewhat lower inflation for everybody and unemployment for many.

I can’t wait to get a 2022 C8 for $20,000

Marcus, my thoughts run the same way. I’m afraid so many people are thinking that, it will become a self nullifying fantasy.

It does not matter if the reason for a famine is no food to purchase or no purchasing power to buy food. People die anyway. That may be the end game quite a few is in for.

Naw… Euell Theophilus Gibbons ate tree bark.

Bobber, I do think it does matter where inflation comes from? If it is supply side, then monetary policy cannot alleviate it.

I do agree that rates must rise for a multitude of reasons. But to think that demand side impacts from rate increases solve all problems – that’s too simplistic right now in this economy.

> where inflation comes from? If it is supply side, then monetary policy cannot alleviate it.

So, buyers for whatever reason, interest rates or exhaustion of cash, reduce demand. Prices adjust downward, more in line with supply. I suppose the word “recession” pops up.

PG –

To me there’s interesting corollary to what you said which I haven’t seen mentioned all that much – high rates actually make investing in productive capacity MORE expensive. So raising rates and promising to tamp down future inflation both dissuade investment.

So policy is actually going to hurt supply side, the only way it works is if it hurts demand side more.

inflation comes from digitizing too much money, suppressing interest rates and extending too much credit. It is the creation of gobs of money, which in accordance with the cantillon effect first pushes asset prices and eventually pushes the cost of living. (Notice no mention of the phony CPI)

It is all part of the creation of a debt society where servants are kept in service to the masters.

I am adjusting my standard of living downward, even as my debt inches downward. This is to preserve my liberty. Freedom isn’t free. And it certainly doesn’t correlate necessarily with gobs of cheap and free stuff, whether that stuff is credit, cash, student loans, iPhones, avo-toast, or whatever. (Not that you said that.)

So how long can we continue living on our grandchildren’s projected income?

Only as long as the grandchildren of the elite convince the grandchildren of the masses to pay a portion of their produce to support old deals. I suspect a few deals will be re-written.

“Fed Governor Lael Brainard, one of the biggest doves on the Fed’s monetary policy committee, explained this morning in detail that inflation is hitting lower-income households much worse than higher-income households”

This is partially true. We are not high income but are not affected by this Bideninflation the way most people are. Home mortgage paid off, semi vegetarian diet, no debts, still in the workforce with fees going up and adj for inflation, WFH 85%, limited gas usage, most expenses deductable, 8 computers humming along doing most of our work. People need to stop whining about this inflation and do something constructive to deal with it. Its only going to get worse.

Do people come to this website to just continuously brag about their amazing life situations?

Also, which administration printed 4 trillion in stimulus and gave it to anyone and everyone?

I honestly wish the previous administration was still in office just to see what kind of bs would come from their mouths to try and justify these price increases

Instead we get short sighted idiots here who go around making completely stupid comments about “BiDeNfLaTioN”

Troy, it is true that this inflation doesn’t impact some like it does others. They are allowed to speak their minds.

If you don’t like it, go somewhere else. And Swamp is not bragging. He has been posting here for a long time and is objectively telling us about his lifestyle as is so we can learn from him.

Inflation doesn’t touch me either, but I don’t go on here talking about how people shouldn’t be purchasing anything because I myself don’t buy anything, because I know that’s not constructive to 90% of the population

He lost his credibility after mentioning bidenflation anyway, people who blame one political party on the work of another are shortsighted goldfish

I say this as an independent, couldn’t care less about either party

Troy, the problem is 90% of that population that you refer to overconsume.

Hence Swamp’s point: don’t overconsume and you won’t be impacted by inflation as much.

I do agree with your point that to make inflation a partisan matter is foolish. Just look at the politician voting on the profligate spending from the CARES act. Everyone voted for it. Both teams red and blue.

OK PG, Both teams red and blue voted for this. So why defend the the inflammatory partican playground throw-down “Bideninflation”? That is worthy of Zerohedge and FOX. It cheapens and coarsens the discussion, unless it makes a meaningful point, which you conceded it does not.

Read FOX comments to see how brain-dead and shouting they are.

The cognitive dissonance really is amazing. Damn that Joe for not going back in time and preventing QE Infinity and PPP and Stimmy 1 and Stimmy 2 and…

Yes, that cognitive dissonance truly is amazing. Joe wasn’t extending rent moratoriums, child credits, unemployment benefits, tuition deferment, now was he?

No, Joe is off the hook because he didn’t ‘go back in time’ and undo Trump policies. Besides, now it’s Putting fault, not Trump. Get with the narrative.

At this point it blows my mind that people are still taking sides looking left and right when they should be looking up and down. This is class warfare.

;-)

Troy,

“Also, which administration printed 4 trillion in stimulus and gave it to anyone and everyone?”

One after the other — with the first one being the bigger overall:

1. Trump administration: 2 stimmies, PPP loans, corporate bailouts, mortgage forbearance, eviction bans, etc.

2. Biden administration: 1 stimmie, extension of the programs inherited; mostly expired now

Wolf, come now… dollars attached to those unit counts??? ;)

Just kidding. I know total dollars probably come more from the Trump admin.

But still.

Trying to keep you on your toes…

True but lacking context.

1. During the height of a complete lock down of the economy the entire world for 8 weeks in a situation of almost complete economic uncertainty. At least for much of those programs.

2. Vaccines are available, lock downs almost completely resolved, and remember he tried to pass a 4 Trillion dollar spend a palooza stopped only by a few sane people in his own party.

I don’t think either was completely correct but the failed spend a palooza would have been the single most unnecessary and inflationary bill in US history.

Swamp, I have to agree with you. If everyone can see the reality is 10% interest rates and 10 inflation then the first step is deal with it as best you can and then fight for change.

Just complaining about reality is a waste of your life.

What would you suggest? Buy more leveraged real estate? or what?

Depends on what you’re trying to do…

Circumstances and your psychology dictate how you proceed…

Enlightened Libertarian went from zero to 20 million in 15 years. I am wondering if he still thinks there is a prayer of repeating that.

Troy,

I think you missed my whole point. I wasn’t bragging about anything. I was trying to let you and the other lemmings which constitute 85 to 90% of the American people of things they can do to combat this Bidenflation or TrumpInflation whatever you want to call it. Staying in the workforce is one of them. It’s a guaranteed winner. Making yourself more productive is another, by using technology to leverage your skills. Having a better diet is another. I’ve posted many times before that most produce and seafood hasn’t gone up much at all in the last few years in spite of this inflation. Go look at all the junk food that people are putting in their checkout carts. And the price of red meat is out of sight. So I’m suppose to feel sorry for all these folks who don’t make good dietary choices. Sorry I don’t. Maybe they should take a dietary course. And maybe they should get rid of their gas gussling cars or use public transportation once in a while.

Swamp,

He didn’t miss your point…

He couldn’t understand it…

You were speaking French…

He was listening in Spanish…

I’ve also started boycotting vendors who are not comenserate with my values. Like WOKE companies just for starters. I will not buy any products from them unless I am unable to find a replacement. Examples, AT&T, Comcast, Verizon who are all crooked monopolies which I use because I have to just for survival. My enemies list includes companies like Amazon, Whole Foods, Disney, Starbucks, American Car companies, Big Banks, Safeway, etc. The list is getting longer every day.

I know, I know!

If everyone would just live like me we would all be much better off.

Your lucky to be working,inflation is killing my retirement

Exactly. We are in our late 70’s and inflation is hitting us in all expense categories.

Even my wife’s PCP (Her doctor) is pulling the stunt of calling between quarterly appointments to “discuss her medications” and bill Medicare for a “telavisit” (which will cost us $35). They are thieves.

There is NO REASON to try to pull off a telephone call with her to “discuss her meds” when they know exactly what THEY have prescribed for her at any given moment. Plus, in two weeks she has a booked appointment for a visit with the Doc. Crooks.

In addition, cable has gone up, the gas/electric utilities have higher “fuel costs” added, groceries are up a lot, gasoline is up, car insurance went up, and so on.

Rant over.

Anthony A.,

Dump the cable, brother…

Grab an antenna for the Houston locals…

Way, way lots of free tv out there…

Literally, tons of it…

You’ll never miss cable…

(Unless you like 15 religious and 37 shopping channels)… :)

COWG, I would dump the cable in a flash if it weren’t for the wife wanting to watch “certain” shows only broadcast on the cable. Plus, she is an Astro’s fan and can only watch the games on the special sports channel here in Houston that is part of the cable package.

Me, I care less about cable or watching the Astros. But, for peaceful coexistence, I’ll pay the cable bill.

Flea

Forget retirement. That was for the last generation. You ain’t got none. Get over it.

I’ll bet FED shorted market ,before comments Braenard , what a shitshow

Obviously not. The Federal Reserve is not involved in stock markets at all and does not own any stocks.

Yet. Just wait til stocks react to rising rates at some unknown future level.

It was not so long ago that they had never purchased mortgage securities, and they’ve recently experimented in the corporate bond market, no?

SoCalBeachDude

Have you heard of PPT?

Plunge Protection Team refers to the Working Group on Financial Markets. The group, formed in the aftermath of the 1987 ‘Black Monday’ stock market crash, provides financial and economic advice to the U.S. President during market crises.

In recent years, some have had suspicions concerning the methods of the Working Group, as it does not release records of its meetings and recommendations. Plummeting indices have rebounded in a day, leading to speculation that the Plunge Protection Team manipulates markets.

Sweden central Banks have bought US euities including Apple! BOJ has and still buying ETFs of Japan! QE was a ‘seat of the pant’ origin from Barnake, with no prior research or record! Fed NEVER bought MBSs in it’s ENTIRE history(since 1913) prior to 2009!

Hank Paulson, and his PPT, has been called to warm up the bullpin. Word has it that the recent plunge in the Transportation Index is a leading indicator of a stock market meltdown. Usually leads by 3 to 4 months. Add in the possibility of a new Covid variant, and its game over.

The so-called PPT was entirely disbanded in 1993.

SoCalBeach

‘The so-called PPT was entirely disbanded in 1993.\’

Wow!!

Explainer: ‘Plunge Protection Team’ to convene amid Wall Street rout

WASHINGTON (Reuters Dec 24, 2018 ) – The Trump administration is arranging a phone call on Monday with top regulators to discuss financial markets amid a rout on Wall Street.reasury Secretary Steven Mnuchin will host the call with the president’s Working Group on Financial Markets, known colloquially as the “Plunge Protection team.”

sunny129,

Please read the whole article that you cited. It’s pretty clear what these people did and didn’t do. And they didn’t buy stocks, or anything else.

SoCalBeachDude

RE PPT (investopedia)

How the Plunge Protection Team (PPT) Might Work

On Monday, February 5, 2018, the Dow Jones Industrial Average (DJIA) experienced a drop that was twice as large as its biggest point decline in history. However, arbitrary and aggressive buying cut the decline in half in one day. On Tuesday and Wednesday of that week, stocks opened lower, and each time aggressive buying buoyed the markets. That aggressive buying, some say, was being orchestrated by the Plunge Protection Team.

Or, to take a more recent example: The Plunge Protection Team’s aforementioned teleconference on Dec. 24, 2018. That whole month, the S&P 500 had been heading towards a record decline—the motive for the team’s meeting—and the DJIA dropped 650 on the 24th alone. But when trading resumed after Christmas, the DJIA rallied over 1,000 points. On the 27th, it lost half those gains, until a late-day reversal stopped the slide, and caused the market to close 600 points up. That’s no coincidence, conspiracy theorists argue.

With these interest rates spiking like they are doing right now, and the Transportation Index (which CNBC doesn’t show anymore) signaling market crash, along with the inverted yield curve Bernanke and Tim Geitner may also be called out of retirement to join the PPT. Hank Paulson was out bird watching, his favorite passtime, when his cell phone started ringing off the hook.

SoCalBeachDude, I recall when GM went BK several years ago, the “Gov” ended up with a pile of the “New GM stock” and subsequently sold it over the years. Someone, maybe not the FED, in the Gov was buying and selling GM stock.

Yes, that was the US federal government, not the Federal Reserve.

SCBD-

It appears that the dead corpse of the Working Group On Fin’l Markets (akaPPT) issued a report on Nov, 1, 2021. Its on Treasury website.

Just goes to show you how hard it is to kill a federal government department, once it’s up and running!!

Aside from that I believe that THE FED will buy stocks (or equity ETFs), some day, due to:

A. Other banks have done it (as Sunny129 discussed above)

B. The “mission creep” that it has applied to it’s variety of policy tools” every decade of its existence.

C. Its over-riding compulsion to protect the markets from volatility (which it’s own policies have enhanced).

The FOMC needs to move the Federal Funds Rate up to 9.5% ASAP.

That’s what the NRA has been saying.

That would make it a great time to buy.

Or sell.

Ms. Braindead sounded like she was going to handle all this tapering herself…..”I expect, I expect, etc.”

What egos these make believe leaders have.

I’ll bet she has never been in a grocery store or pumped her own gas.

I’m guessing she has done both, actually.

Anthony A.,

You misunderstand the meaning of “I expect.” I expect that my wife will be home tonight at 7 pm. That doesn’t mean that I am able to make that happen or that I even have any say in it :-]

Wolf, that’s certainly one expectation that will never change! 😅

Husband said something very similar to our young boys recently. Smart guys! :]

Exactly Wolf. These interest rate hikes and tapering actions are not going to go exactly as planned.

Yes, they were accomplices in terrible overspending in 2020-2021 but there are many things out of the Fed’s control right now.

Read an article just yesterday that was speculating how long it will take for mortgages breach 5%. The author speculated it could take months.

Hilarious that it only took 1-2 days. The question now is how high will they go? I posed this question to Wolf last week: what’s causing the recent spike in mortgage rates?

I was surprised that he didn’t have a few ideas, but to his credit we all can agree that this is playing out much faster than most of us expected.

My thought process says the mortgage industry / investors are pricing in the flood of MBS and 10-yr treasuries that will start hitting the market in 1-2 months. The FED has created massive fake demand over the last two years, suppressing yields and driving up prices along the way. As such, investors expect the FED to give them significant discounts on price & higher yields as compensation for absorbing all of these FED owned assets that they’ll then carry on their books for years to come.

Translation: the mortgage industry is right-sizing rates, driving them up, so they can afford to purchase all of these MBS at much lower prices than the FED purchased them at.

Just my $0.02.

Yes, this has been very fast moving.

Refis have died. The first layoffs in the mortgage industry (PennyMac, etc.) are already happening.

And so it starts. There’s no telling how many people are going to let go who work in the mortgage business.

And from there, the contagion will spread.

But don’t worry, America! There won’t be a recession by the end of 2022, easily a year earlier than what’s currently “the guess” by the experts.

Feature, not bug; more workers are needed in the productive economy. Need more output to break the supply chain bottlenecks driving the inflation. Alternative is to break the inflation by killing demand, but that’s destructive to living standards. Increasing production and diversifying supply chains makes everyone wealthier (except for the monopolists).

USAA is laying off 90 in their mortgage division.

Wolf, Mrs Swamp has seen refis dry up since the 1st of the year. But no matter. Condo sales in the city are booming and making up the difference and then some. A lot of multi-family buildings and 2 and 4 unit townhouses were converted to condos and now are on the market and selling well even at the higher interest rates. They are the only game in town as traditional townhouses are too expensive for the average 1st time homebuyer. We are working 18 hours/day including weekends.

Friend in the mortgage business was told by leadership today to begin to prepare for the cascade of mortgage defaults. They still make money in the mortgage business on the way down as well

Could you expand on this?

I have a coworker with a husband who’s a VP at a well-known lender and they already made huge cuts with more planned.

He told her that they were front running huge anticipated plunges in the industry’s customer base.

Why would there be a “cascade” of mortgage defaults?

Please explain.

Cascade of mortgage defaults: if people are running out of money or jobs or both, having bought in at the top, it’s easy to imagine. So many were out over their skis in 2008.

But it is weird that the economy and jobs are said to be running hot, even as stocks are sputtering, and bonds rates rising. When does Wall Street echo to Main Street?

Remember, they don’t even have to be underwater to default, just not able to make payments. It’s not difficult to imagine that as inflation eats up more and of the paycheck; maybe student loan payments start up; car payments rising etc. – that all of a sudden that mortgage payment that originally was stretch but doable no longer is.

And that’s not even including more dire scenarios like longer-term un(der)employment. Or actual big declines in home prices.

Just a week or so ago either NAR or realtor.com was saying rates would hover around 4.5-5% thru the end of the year. I mean I suppose that could happen but seems highly unlikely. Are they forecasting lower rates so as not to increase the FOMO already in the market. Maybe they know the crash is coming and want to limit it spiking any worse. You can tell by the drip drip drip of bad headlines that people are individually getting bolder in making more negative forecasts based on what everyone else is saying.

Abomb

I wouldn’t pay any attention to what Realtor.com or NAR are saying. I get some of their pubs. In 2007 while the Real Estate market was in full meltdown mode with much more to follow, they said that “This was never a better time to buy a home”. These people paid hucksters and liars.

Trust me, I don’t. If I read something from them, I immediately start busting out laughing. Most anyone associated with the real estate business in terms of sales is mostly a cheerleader. Kinda reminds me of JPowell.

I mean, you’re asking a barber whether if you need a haircut…

You know what he’s going to say ;)

We just did an inspection of a 1.2 million 19th Century townhouse in the heart of the DC Swamp today. The Realtor never showed up to let us in and sent a lock box code that was invalid. It turns out the number they sent was the serial number of the lockbox instead of the code to unlock the box. These people have to be the dumbest people on the planet. Total morons.

“ was surprised that he didn’t have a few ideas, but to his credit we all can agree that this is playing out much faster than most of us expected “

Jay,

Most of the things you read from the “pundits”

are going to be a load of BS…

No one, and I repeat no one, under the age of 50, has experienced or has a practical understanding of high inflation and what it can do to an economy…

Think about that for a minute next time you read what some “guru” thinks…

When even the HMFIC stumbles into the house like a clueless drunk rube, it should be a warning …

Looks to me while she’s not at the podium, Brainard’s now in charge…

You all hear that giant pop of the housing market?

Only for the masses. Expect an even larger share of cash/investor-purchased homes.

Why? If home prices go down, why would they buy?

If rents go down (e.g. recession), and home prices are going down, why would investors buy?

There are at least 2 Million new Americans entering America every year.

Expect 50,000 a week.

They need housing and the Government will pay whatever the Hedge Funds and Private Equity companies demand.

Brilliant Plan.

Maybe Publius meant they will buy ‘when’ house prices are lower.

Marcus These are not Americans entering US ,more like no income refugees ,

> If rents go down (e.g. recession), and home prices are going down, why would investors buy?

Faith-based, that the Fed put will refloat them again, as in the last 15 years. That’s the 1% everybody talks about: they can time market swings this big. They built up enough dry powder (and the contrarian view) to do it.

MA

Two million a year ? Really ?

Of course, you don’t supply number for how many die or emigrate.

You insinuate USA population is increasing.

It isn’t.

More like Braindead……..she and her crooked friends are playing a dangerous game. Tightening now……no way this end up a soft landing unless oil drops to 40 bucks and corn drops to 5 a bushel…..both for other factors. They will have to hit the brakes hard.

Just goes to show that when one of these morons gets a call from someone who has the super power big bucks…..ordering them to raise rates…….the show must go on. She got the call……and suddenly Ms Dove is Ms Hawk. After two years of watching this mess unfold.

fred flintstone,

You need to get ready for much higher interest rates. Inflation is going to hit 10% here pretty soon. And the Fed has gotten the message. It doesn’t matter where the economy is going, inflation MUST come down or else the whole economy will turn into a giant shithole.

Yes Wolf I fully agree they raise til they break but will the next QE be even larger or will they actually act responsibly in the future?

That’s the zillion dollar question…

It will be larger. One last mega pump before the entire system implodes.

They will go full Japan and just start outright buying ETFs.

Not for a couple of years though. This market still has to drop by 60%+ first.

A question often discussed here.

My position is that monetary policy will not jeopardize USD reserve currency status.

The public, markets, and economy will be thrown under the bus to preserve the Empire. Look at US policy toward Russian energy imports. Yes, it’s somewhat symbolic (limited imports from them) but an indication of elite thinking. Americans are already being told of the sacrifices they will have to make supposedly to “stand with” a country most of “us” couldn’t even find on the map prior to February 24th.

It’s no different in Europe, where the EU elites will throw everyone and everything under the bus to save the European Project.

Augustus,

Ironically, the actions of the US/NATO/Europe in this conflict have done more to undermine the status of the USD as the global reserve currency than anything the likes of the Fed have done at home. Other nations are now looking at it as a liability and forging closer trade ties with each other and settling more and more transactions in alternative currencies.

Internal monetary policy won’t matter a jot compared to the consequences of geopolitical recklessness such as freezing Russian assets and driving them into the arms of China. We’re already seeing countries like India, Brazil and even Saudi Arabia starting to stick a middle finger up to the Global American Empire.

AF,

Empires require a stable energy supply…

My thoughts are short term pain for long term gain…

Positioning the US influence with a) natural gas exports and b) the US military protecting ME oil…

That would be the long game that I would play…

People are forgetting a huge factor: If the Fed’s policy rates are 5%, and inflation is heading down to 3%, and there’s a run-of-the-mill recession, the Fed can CUT rates serially by a whole bunch, to something close to zero, and doesn’t need to do QE. That’s the classic model. Lots of Fed heads have said they’d like to return to that model.

When rates are near zero, and then a recession hits, that’s when QE gets dragged out, because the Fed’s policy rates bump into what the Fed calls the “lower bound” (near 0%), and the Fed can’t cut any further because it won’t cut into the negative.

@Augustus Frost

“…My position is that monetary policy will not jeopardize USD reserve currency status…”

I fully agree.

However, I live in Europe, and I can assure you that everybody and their uncle is getting sick and tired of the way the USD is being used to force policy decisions. The US is behaving more and more like the schoolyard bully, using the USD as a stick.

This weaponizing of the USD is a much bigger threat to its role as a reserve currency than any pure monetary decision.

Jos Oskam,

As long as the US military keeps Belarus and Russia from marching through the Suwalki line to Gdańsk, that’s the way it’s going to be…

Sorry, bud…

I think drifterprof can give you some ideas if you want to relocate…

@COWG

Nobody I know is afraid of the Russians marching anywhere into Europe, since it is more than obvious they would spread themselves too thin doing that.

Lots of people see this kind of fearmongering for what it is, the last gasps of a failing empire.

And they hate sitting in the cold and paying through the nose for everything because of it.

“…inflation MUST come down or else the whole economy will turn into a giant shithole….”

IMO it’s already a giant shithole, it’s just being masked by the trillions in stimulus washing over everything. I am seeing more businesses, specifically restaurants, fold over the lack of employees and the rising prices. Inflation destroys business. The PTB screwed the pooch. There’s no going back.

It will be a lot more evident when the asset mania crashes (regardless of future monetary policy), cheap borrowing ends, and borrowers have to quality under any credit standards actually resembling prudent lending.

Lending and credit quality standards are and have been a complete farce for years.

Why would u bust ur ass in a restaurant job when the pay doesn’t keep up w the minimal expenses it takes to survive? Give up, lay down. Thanks JPow and Co.!

Quick shops in my area closing at 4:00 pm no help

TWEIAPS –

I’m still trying to understand how a person just quits working and resigns themselves to a life of zero income. I’ve been working since I was 11. No work = no eat.

Just imagine how many nails he has pounded !

This for DC:

It’s actually quite easy to quit working and get by with Zero INCOME — on the books at least, and at least for ”a while.”

This from one who started selling newspapers in the streets at age 7, because I could and dad said I could buy a new football or anything I wanted WITH MY OWN MONEY…

Several entire years in my 20s and 30s show NO income on my SS summary in case I forget the freedom I had and I suspect many folks have and have had, BUT,

Ya gotta be thrifty in all things: housing- NO payments of any kind, so tent or a couch or ”squatting”; transportation either ”shanks mare” or hitch hiking; food — tons of free food all over, especially USA, but other places in world too; medical services, tons of free med services, especially in USA, but other places too, esp. in what was Great Britain; entertainment, free books almost everywhere.

Of course, when one tires of that lifestyle, one can always find work of the lowest cash paid manual labor kind, and I washed a ton of dishes, pots and pans, dug miles of ditches, etc.

”Work is the curse of the drinking class.” May apply???

> how a person just quits working and resigns themselves to a life of zero income.

In my area, there are plenty of guys around who steal. They are combing through the parking areas at 3:00 a.m. I do my jogging at night, so I see it.

I’ve seen this career path before. I’ve seen guys go through the whole arc from young and fairly fit to wrung out and then dead. But more show up.

And those guys shooting up the bars and concerts? drug dealers fighting for turf.

Consider a Mind Experiment, a la Einstein.

What if THAT is the goal?

There are those who believe in EVIL. They really do. They think there is EVIL and EVIL forces. But, when you bring up a really EVIL scenario, they call you a conspiracy nut case……then, I ask again, is there EVIL or not?

There is, or there isn’t. Can’t hedge that one, unless that is part of the EVIL “plan”. Deny the existence of EVIL?

If there truly is EVIL, how would it play out? Like today? Like what is happening now?

I suggest you all track down a 5 hour video by a “famous” Australian singer named ALTIYAN CHILDS. It will answer your questions. It is the most frightening video I have ever watched. Truly Evil.

No, Marcus…

Truly evil is watching “Keeping Up with the Kardashians” without realizing it….

Evil spelled backward….Live

Wolf, Thanks for your site and comments……lots of good info…….yep to your comments……I would love for them to do the right thing and tighten…..in spite of any recession threat…….I do believe rates are going higher permanently for several reasons.

Personally I would welcome higher rates but my comments are not aimed at achieving that goal. I view this site as academic economics….not personal.

My issue is Brainard changed like a chameleon…..it is my fear there is no Volcker today or very many other patriots who care more about the country than their short sighted personal interests…….its mostly politics…….and I fear them giving up on inflation at the earliest hint of weakness…..bad for the country……but…..politically there will be tremendous pressure once the unemployment rate and poverty rates start to climb.

We’ll see. Right now I don’t see an FDR, Reagan or similar leader that would stand up and say no to all the various lobby group and have it stick.

Wolf

The whole economy is already a giant shithole. I don’t care what government economic figures say.

That’s not what I see when I use my eyes.

If just a small increase in rates has such a quick and appreciable effect on the economy, do you think Fed increases of more than a quarter percent are likely?

But what happens if the Fed hits the brick wall of recession while raising rates or it is not able to raise rates much before economy craters?

Wolf –

If I understand it, the Fed has two main levers it uses to influence the the speed and direction of economic growth: FFR, and balance sheet.

The FFR lever is limited on the downside by the zero rate bound when trying to stimulate the economy. When fighting inflation, the balance sheet lever is limited by the current size of the Fed’s balance sheet.

Does either the “zero bound” or the “balance sheet bound” provide a challeng in our current bubbly predicament?

Do you chart the size of Fed balance sheet against GDP, and could you provide some historical perspective on it compared to where it’s been and how it compares to other central banks and where they’ve been?

Apologies if this has been discussed in past and I missed it.

If the BLS properly captured housing prices rather than surveying rent, inflation would be 12-15%. My Kroger boneless chicken finally shot up 25% after two years. The only thing, food wise, that I can think of that hasn’t gone are the Costco Kirkland protein bars: $17.99 for 20. What a deal.

Wolf said: ” whole economy will turn into a giant shithole.”

————————————————-

What would we the call the economy of the last decade(s) as interest rates were suppressed, money was pumped, offshoring was rampant, wealth gaps were widened, health care – housing – and education prices exploded, debt slavery expanded ?????

It’s been a hole for many. Now others are falling into it, or recognizing they are in it as well. Deferred recognition because of debt, stimulus and forbearance.

Cb:

US economy became a “giant shithole” in April 2009!

I’m getting ready for the Fed’s Austral plan.

Texas Tea hits $102 as I write…..

Yep. Those planned strategic oil reserve releases don’t seem to be having much effect.

Those crude oil reserves have to be sold before they can leave the reserve. Most crude oil sales are contracted out for several months, and this release will take many months to get into the GLOBAL system.

It’s really just a political stunt at best, and possibly, the repurchase of the release in the future will be at lower than current sale prices. Such a good deal? Not…

After listening to these morons for 25 years ( I was too young to care prior) I have learnt they are full of it. They will never do the right thing let alone keep to the rules they themselves set. It’s like being paralyzed whilst someone extracts all the money from your pockets.

The older I get, the more full of it I realize people are. Actions truly speak louder than words, no matter how much the words are liked, subscribed, retweeted, shared, or other absolutely meaningless performative signal boosting happens.

Today’s world needs more put up or shut up.

Unless it is intentional.

Unless? If you cannot rationally see it by now, you are not paying attention…

twinkytwonk

As the former Archduke of Austria Hungary, Ferdinande once said in 1914:

“Trust no one. Assume everyone is a scoundrel until they prove otherwise. Then you can take them into your circle of trust”

This is the best advice I’ve ever heard for your personal and professional life.

He had a righteous mustache for sure.

The Archduke F. got that right but still got assassinated in Sarajevo the same year. Obviously not paranoid enough. Sometimes they are really out to get you.

Didn’t Wolf’s ancestors come from Austria/Hungary? It once was a great proud empire for 300 years.

Swamp Creature,

Very close. Bohemia. At the time, it was part of the Austrian Empire, now in the Czech Republic. Grandfather went to school in Pilsen, location of the original Pilsner brewery, which competed with the original Budweiser, which was (and still is) brewed in the city of Budweis (German name). That’s why I have beer in my veins! Grandfather served in the Austrian Navy in the late 1800s when Austria still had a navy. The whole clan was run out of there in 1945 amid a huge bout of ethnic cleansing that expelled all the German speakers that had been there for thousands of years and that even the Romans dealt with and wrote about. Those folks lost everything. However, my grandfather (as a younger son, no farm no inn) and father were engineers designing machinery for Siemens in Germany, which is where I was born.

Wolf,

does this mean active, outright sales and not passive roll off? is that what Lael is suggesting with respect to treasuries and maybe MBS?

ace,

We’ll find out more tomorrow in the minutes, maybe.

Passive roll-off alone is going to amount to a reduction of over $100 billion a month, or over $1.2 trillion the first year. It may be more than that. That’s already quite a bit.

I suspect that they’re considering selling MBS outright because they’re so squirrely and unpredictable, especially with rising interesting rates cutting off refis.

They will also cap the maximum per month, maybe at $100 billion a month.

And there will be a phase-in, as last time, but shorter.

That’s interesting that you think they want to sell the MBSs not that I think you’re wrong. I have no clue other than to think that if they sell MBSs mortgages rates will crush the housing market, and I have a hard time seeing them do that.

Sorry should have said “considering” not “want” in the first sentence

They have already publicly suggested it (Bullard among others). There are technical reasons for doing it. MBS are just funny creatures. They would roll off mostly through the pass-through principal payments, rather than maturing securities.

I’d like to see what happens to the long term Treasury and Corporate Bond funds when interest rates start spiking to Paul Volcker rate levels? I think there will be a run on these funds when investors open their monthly statements and see declines in their principle of 30% or more. I wonder how anyone can be so stupid to buy these funds in the first place just to get say another 1% yield. I’m on the verge of dumping my own fund because of their sorry performance on short term muni bonds.

Swamp Creature,

Going by futures prices, 30 YR UST has declined from 191+ to about 146 since March 2020. That’s 45+ points or almost 25% already (less the pitiful coupon payments) and this is just getting started.

It’s better for shorter maturities but still bad.

The future losses for currently issued debt are going to ginormous.

I watched Bullard’s interview a couple of weeks ago, and he did say that balance sheet reduction will be Passive.

Thing is even at $100 Billion/month it will take 3-4 years to get rid of all the excess they’ve printed over the last couple years. that’s a really long time of high inflation/recession.

While I do have some fond memories of the 1970’s the inflationary policies from then didn’t fade away until the 1990’s. The home mortgage rates in the 80’s were all double digits. And credit cards (which nobody is talking about) were over 25%. It took decades for people to dig out of those holes.

Imagine what the impact would be if student loans were 15-25% interest. We have two generations of citizens who’ve been taught that they need not save, but should live on credit.

This depression is going to hurt.

Not only living on credit, but they seem to have learned to avoid any capital accumulation. They live in their cash flows.

Reading this the image that comes to mind is a 16 year old, high as a kite, driving dad’s 1968 Wildcat during a snowstorm on an icy road, knowing the brakes have failed, dash a glow and trying to will the car to a safe stop.

“Oh my god, what have I done.”

And these clowns sleep well at night and feeling secure and “safe.”

Does the FED have security like the President?

let the dow go down another 1000 and they’ll walk it all back( after they’ve covered their shorts).

US Fed is such a disgusting organization. They openly lied about inflation, CPI, blatant robbery from poor people and now that they are caught naked, they are doing more and more lip service, while still printing and still keeping interest rate at near zero. This lady and Fed mafia has no common sense and compassion left and its sickening. Every night must be thinking of millions of ordinary Americans she screwed. And more lip service. All Fed members must be fired. Every economist said that unhinged printing and interest rate suppression will cause inflation but these clowns did not get it, are they brain dead or simply corrupt?

“Keeping rates near zero”

Hahahaha…

Mortgage rates over 5%

2-year Treasury over 2.5% up from 0.2% six months ago. Open your eyes, Kunal. This is happening a lot faster than anyone expected.

If the 2-year yield keeps on keeping on, I’m going to buy some 2-year Treasury notes at the auction on April 26. Time to shift money out of the bank into something that pays a little interest.

Pure wisdom dispensed daily. If you think there is a better place to get investment advice, you are mistaken, IMHO.

Wolf may be willing to get 2.5% for cash over the next two years but I never make a capital commitment longer than minutes without the expectation of at least doubling my money. Wolf has elegantly demonstrated how the markets are driving interest rates straight up. Asset prices will be going straight down.

Remember, he who loses the least in a bear market if the winner.

Since now cash is trash, just like 1999, I want cash to pluck the diamonds after the crash.

Of course, you can profit on the way down, with our suggested SRTY and SQQQ. As always, don’t get greedy and go back into cash as your account balance hits new highs and re-enter the positions on market rallies.

Bid for authentic Wolfstreet Beer mug $250. Wolf, I have not had a single human offer to sell me a Wolfstreet “Nothing Goes to Heck in a Straight Line” glass beer mug at any price. So I am asking again for anyone holding an authentic mug to send me an email with your asking price.

HarryHoundstooth at yahoo dot com.

I already sent you my ”ask” HH, but didn’t hear any counter offer, so thinking you’re not serious???

(of course, my one million wasn’t serious either LOL)

Harry Houndstooth said: “Wolf may be willing to get 2.5% for cash over the next two years but I never make a capital commitment longer than minutes without the expectation of at least doubling my money.”

—————————————-

and how has that worked out for you? Are you a billionaire yet?

there are a few newbies on this site. They might actually believe you. If it’s not complete BS, name a few of your extraordinary trades …………………

Would consider a 1 year or 3 year lease (provided I can get reasonable insurance). Please make an opening offer.

@ Wolf –

It sounds like Kanal has perfect vision. His comment is 100% correct.

Kunal

The Fed screwed more than just poor people. They screwed middle class people who played by the rules, and watched their savings get depreciated by 20 to 30% over the last 10 years. This is robbery. Worse than some thug who steals your hubcaps off your car. And for what gain? The whole sh$thouse will collapse anyway. ENJOY

What the heck are “hub caps”? : -)