Rates “need to rise further.” Balance sheet already shrank by 14%, more shrinkage to come.

By Wolf Richter for WOLF STREET.

The Bank of Canada today hiked its overnight rate and its deposit rate each by 25 basis points, to 0.50%. It cited 5.1% CPI inflation that it expects to rise further and faces one of the worst housing bubbles anywhere – both of them fueled in part by two years of interest rate repression and money printing. It cited “further pressures on house prices” and the additional inflationary pressures from commodities markets following Russia’s invasion of the Ukraine.

“Interest rates will need to rise further,” the BoC said in the statement, in line with jawboning by BoC officials following the prior meeting in January.

“Price increases have become more pervasive, and measures of core inflation have all risen,” it said. “All told, inflation is now expected to be higher in the near term than projected in January.”

“Persistently elevated inflation is increasing the risk that longer-run inflation expectations could drift upwards,” the BoC said.

“The Bank will use its monetary policy tools to return inflation to the 2% target and keep inflation expectations well-anchored,” it said, after having not even tried to do that for well over a year and being a gazillion miles behind the curve.

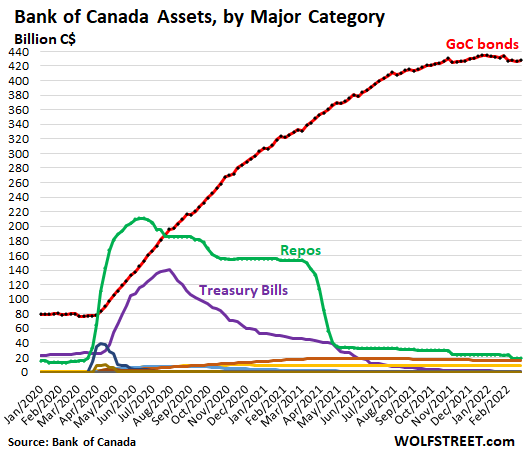

Quantitative Tightening (QT) for the BoC refers to shrinking its holdings of Government of Canada (GoC) bonds. It confirmed today that QT is being planned but provided no details on the start date and the amounts of shrinkage.

The BoC has already unloaded essentially all Canada Treasury bills (purple line) and nearly all repos (green line). Its balance of GoC bonds has been roughly flat since October last year:

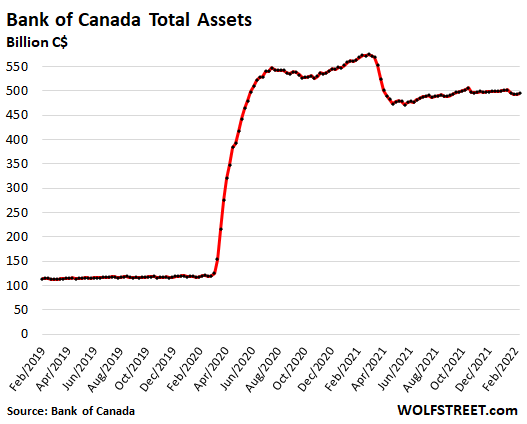

All assets combined on the BoC’s balance sheet, at C$494 billion, were down by 14.1% from the peak in March 2021, when the BoC began unwinding part of its stimulus measures, citing “moral hazard” as one of the reasons:

To keep its holdings of GoC bonds roughly flat, the BoC is reinvesting the proceeds from maturing securities to buy new securities. When QT starts, it will allow GoC bonds to mature and roll off the balance sheet without reinvestment. QT “would complement increases in the policy interest rate,” the BoC said.

“The timing and pace of further increases in the policy rate, and the start of QT, will be guided by the Bank’s ongoing assessment of the economy and its commitment to achieving the 2% inflation target,” it said.

BoC governor Tiff Macklem will give a speech tomorrow and may choose to flesh out his ideas about the coming QT.

The BoC sees the Canadian economy as “very strong,” and cited GDP growth of a red-hot 6.7% in Q4. It said that “economic slack has been absorbed.” It acknowledged that in January, Omicron dealt the labor market a “setback,” but in February, things were already recovering from it. “Overall, first-quarter growth is now looking more solid than previously projected,” it said.

This paves the way for another rate hike at the next meeting on April 13, and for more rate hikes this year.

The BoC appears to try to front-run the Fed, as it has done with ending QE and the liftoff rate hike. The Fed is on track to hike its policy rates on March 16, confirmed by Powell before Congress today. While the BoC and Powell cited the fallout from Russia’s invasion of the Ukraine as a new source of “uncertainty,” they both said that the resulting price surges in commodities were adding fuel to already red-hot inflation – and for both, the BoC and Powell, getting this inflation under control is now an official top priority.

Canada has now joined a slew of countries that have implemented rate hikes, including advanced economies, and including some shock-and-awe rate hikes, and including the mother of all rate hikes by the Central Bank of Russia on Monday on top of eight big rate hikes before then. Next in line to join the club is the Fed that is trying too little too late to mitigate the effects of policy error after policy error since March 2020.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Listened to Powell – no Taper just gradual rate hikes. The taper he did suggest was $100 Bill a month and a Senator pointed out at that rate it would take 22 years to clear the Fed books.

3 Senators wanted to find out about Powell’s efforts on GLOBAL WARMING. All of them warmly supported his nomination.

What a dog and pony show.

No Hard questions

CONCLUSION = WE ARE SCREWED!!!!!

Front-run by the BoC?

“If you’re not first, you’re last”

Well, the Fed really IS last.

ECB or BOJ will be the last :-]

forgetting Swiss cheese with current inflation 2.2%

Seattle Guy,

Listen to the hearing again. Either you misheard, or you or they don’t understand the difference between “taper” and QT and don’t understand balance sheets.

1. “Taper” is in the process of being completed. Which means QE is ending and then the balance sheet won’t grow anymore.

2. QT (Quantitative Tightening) = shrinking the balance sheet. $100 billion a month in shrinkage will reduce the balance sheet by $3.6 trillion in three years and by $4.8 trillion in four years. That would be about as much shrinkage as is possible.

3. The assets on the balance sheet can never go to zero. People who say that the assets should go to zero don’t understand balance sheets.

On a balance sheet: Assets = liabilities + capital. Always.

The biggest 3 liabilities on the Fed’s balance sheet are currently:

$2.2 trillion of currency in circulation (paper dollars) that are growing and will be higher in three years; this is a function of demand from people wanting paper dollars globally.

$1.6 trillion reverse repos that can and will go to zero;

$3.8 trillion in bank reserves that cannot go to zero. They’re now shrinking but they will likely remain above $1.5 trillion.

So add those three together, and that is also roughly the amount that the Fed will have in assets. So a few years from now maybe: $2.5 trillion in currency in circulation plus $0 reverse repos + $1.5 trillion in reserves = $4 trillion.

So $4.0 trillion will be roughly the minimum in assets the Fed will need to have a few years down the road to balance the liabilities it will have. And at $100 billion a month shrinkage, it will get there in about four years.

THANK YOU Wolf for that explanation! Sincerely!!!

Agreed, and Seattle Guy better be careful or he will be sent to the “Richter Gulag” making beer mugs for the next 10 years!

:-)

Thank you Wolf for that explanation.

So if you look back some 20 years ago, prior to GFC, the Fed had assets of less than 1T consistently for some time.

I know everyone’s favorite thing to do on this website is to bitch and moan about Fed policy and its asset purchases.

But going from 1T to today’s 9T (give or take), isn’t some of this growth at least in part due to global expansion of international growth, and the fact that every single other country in the world uses USD as reserve currency?

Like some of that growth up to today’s 9T of course is QE, but isn’t some amount of it global expansion in economies?

Any good literature on this?

Peanut Gallery,

The “normalized” balance sheet today would be around $3 to $4 trillion. The rest is excess, and QT is going to be used to shed it. The Fed is using the term “normalize” to explain what QT will do.

Same principle applied 20 years ago:

$700 billion total assets

Main liabilities:

1. Currency in circulation (paper dollars) was about $580 billion.

2. Reverse repos = 20 billion

3. Reserves = $40 billion.

But something did change: During the financial crisis, the Fed switched from a minimum “required” reserves regime (it had a 10% minimum reserve requirement for banks) to an “ample reserves” regime, meaning that it wanted the banking system to have ample cash on deposit at the Fed (= reserves) so that banks could supply the liquidity if there are issues.

Until 2008, the Fed had a standing repo facility that provided this liquidity to the financial markets. In 2008, the Fed switched to the “ample reserves” regime, and the banks then were expected to provide the liquidity to the markets, and the Fed shut down its standing repo facility.

In 2021, the Fed revived its standing repo facility, to deal with liquidity issues in the financial markets when banks refuse to supply the liquidity (which is what happened in the repo market blowout in late 2019 after reserves dropped to about $1.9 billion, and banks refused to supply liquidity to the repo market).

The standing repo facility will allow reserves to drop without something blowing up.

Thank you Wolf. I didn’t realize the standing repo facility was a feature previously available to banks in years past. I will need to do more research on that.

In a country that boasts of “checks and balances”, who checks the Fed?

“Inflation is what happens when people increase the money supply by fraud, imposition, and breach of contract. Invariably it produces three characteristic consequences: (1) it benefits the perpetrators at the expense of all other money users; (2) it allows the accumulation of debt beyond the level debts could reach on the free market; and (3) it reduces the Purchasing Power of Money below the level it would have reached on the free market.” mises.org

If paying taxes is PATRIOTIC….then what is the systemic debasing of the Nation’s currency?

Who knew, that the Fed would not answer their duties, not raise rates in quick response to inflation…who knew to be fearlessly fully invested?

For that has been the entire game since QE and 2009.

Those who gave us the gunslinging 2008 debacle are the same who seem to have been plugged in and are fully enjoying the “New Fed”.

Congratulations! We are riding the Buzz Saw. Would like yours cross cut or ripped?

Better than a donkey and an elephant.

1/4 pt?

Why bother?

Inflation just ran up TWENTY 1/4pts in 7 months……..

Where is the serious intellectual inquiry from these Congressmen?

Each Democrat seemed to be more concerned about race and gender issues than economic ones…the other party just kissed up to Powell.

Wolf –

Where you stated:

“ When QT starts, it will allow GoC bonds to mature and roll off the balance sheet without reinvestment. “

It would be interesting to know what the maturity schedule is for the BoC balance sheet. I assume (hope) that it’s weighted toward earlier maturities.

Also, the maturity schedule before the March 2020 “liftoff” in assets might be revealing. Do you expect they will try to get back to where they were then, as far as shape of their portfolio?

I’m not a financial expert but how can piddly .25 rate hikes every once in a blue moon ever hope to get on top of 6% + inflation?

Not a financial expert? Then you’d be an ideal candidate for Fed chairman 😀

My question is: what is the motivations and thinking and other aspects or processes behind the actions that have left to our current problems?

So what can be learned to do better in the future?

Or a finance manager at a car dealership

Or CEO of a EV car company

Or a SPAC founder

or… or … orr…….

Not a financial expert either, but I’m pretty sure it won’t.

It’s not quite “Erdonomics” (to borrow a term from a friend), but it’s still pretty damn disgusting.

You deserve your own Financial Show on CNN!!!

You can name it: ” The WTF Financial Hour”

It can’t. Inflation IS the goal. Ignore all talk of protecting the dollar. That’s what the military industrial complex is for. The goal is inflation.

I suggest being long $Popcorn. This show is just getting started.

This morning I thought I read that they hiked by 0.5 percent. It was a Globe and mail article titled “Bank of Canada raises interest rates by 0.5 per cent”

Looks like Globe and mail did make a mistake in their headline.. Pretty sad these guys can’t even get that kind of stuff right….

The Globe and Mail article I read said “to” not “by”, but it also had an edit after being up for 5 hrs so they may have caught the typo.

It’s amazingly easy to put typos into headlines. I can do it too :-]

We don’t need the FED or the stock market its all BS

Then what is your genius solution to it all?

Please tell

Weird statement. If rates need to rise further then why not raise them now?

I think the hope is that inflation will ease, without too hard and fast a nudge leading to panic, tipping into a market rout, waves of bankruptcies and recession. All this is fragility is not least due to the preceding Fed policies. Without true price discovery, and with cheap credit afloat, there may be a lot of zombies suddenly revealed. The medicine might kill such a weakened patient. the fed smokes a lot of hopium!

The Bank of Japan got way out on the wrong side of this sort of timid policy. This fed into a lot of drag on their economy for decades. And it looks bad from a crony standpoint.

In the military the saying is “Hope is NOT a Strategy!”

It seems to me that they had a choice here… go with the .50% rate increase and signal to the markets that they are REALLY serious about this… or go with the 0.25% rate increase as a teaser to signal that these increases really are coming down the pike.

I am not saying either strategy is wrong. It just strikes me as “weird” to go with 0.25% and say “We know we need to do more.”

50BP or 25BP, both are a joke. There is a psychological difference but in itself is not remotely enough to make a difference.

Only a definitive to the asset mania can sufficiently tighten credit conditions to restore “normality”.

“In the military the saying is “Hope is NOT a Strategy!””

Well the saying at the Fed is “Hope IS OUR STRATEGY”.

The hope was the inflation would be “transitory”

The hope was it could keep interest rates at 0 forever

The hope was it could do QE forever

The hope was by doing all this it will ensure that stock markets keep going up for ever

Inflation proved to be a mean fella!

KPL

Yep.

Powell said “we don’t want to have happen today what happened in the 70s”

I guess he meant they are not going to stand to their post.

Zombies?

Look at most of corporate America for starters. Crap balance sheets and low credit ratings even credit rating agency low standards. Yes, the same companies with market caps at ridiculously inflated prices.

It will take a while for rising interest rates alone to kill off the zombies but the end of the fake economy will do it a lot faster.

You must have missed the memo. Corps are no longer interested in old school thinking like that. Strong balance sheets are only for borrowing for buybacks and mergers. That’s how management gets the big paychecks and bonuses.

Worrying about shareholders or employees is such a quaint idea. Not heard of in decades.

There was already a small run on Canadian banks after the “emergency” fiasco, another steep spike in interest rates would spark another run from a larger swath of the population. The Canadian economy has no rare minerals to back it up either so if they push too hard, they have nothing to get back up with.

Why would people take money out banks if they are paying higher interest?

There is a lot of BS around but this takes this weeks prize.

A run on the Canadian banks? No one lost a dime in a Canadian bank during the Depression when almost 10K US banks went under.

As for ‘no rare minerals’ someone else can take that pigeon.

SpencerG,

Central banks never do that. They don’t want to lock up the markets. They say in advance what they’re going to do so markets can adjust to it, and then they’re going to do it. Every rate hike cycle takes many steps.

Powell will consult the tea leaves in his cup tonight, might change his mind by tomorrow’s meeting 🍵

The Fed isn’t saying inflation is transitory anymore, but they are conducting policy as though it is transitory. They Fed must expect inflation to come down on its own, but by then, the dollars in your pocket could be worth 20-30% less in just two years.

He thinks he can quickly tame inflation, if in his judgement the time is finally right. I think he’s nuts. The high oil prices pretty much guarantee high inflation for at least 2 more years. There are going to be shortages in everything made of oil/gas. This includes fertizer/food, chemicals, plastics, cosmetics and meds.

Usually the fed tries to stay out of politics, at least publicly. I’d love to be a fly on the wall. Fed policy guarantees the current gov’t is gonna be voted out this year and in 2024. Maybe they want that???

In the past there were 75bp rate hikes. We need an emergency full percentage increase just so the fed has any credibilty.

“the dollars in your pocket could be worth 20-30% less in just two years.”

So true. I’m withdrawing money from the guys “doing God’s Work” , and buying anything of solid value, in a category I have expertise in.

For me, it’s musical instruments (Fender, Martin, Gibson, Vox ,etc.)

Every $1,000 cash I don’t put into an instrument, will be worth $850 in 12 months. And the “God’s Work” Goldman Sachs Marcus guys are paying .5% A YEAR. Versus the 15% true blow off in the dollar every 12 months. A true no brainer, if you don’t overpay in the initial purchase.

Quality USED instruments, I should have said. Already depreciated.

Today made me proud to be Canadian born.

Not.

Oil up 17% in 2 days which will increase inflation noticeably but that. .25 rate increase will scare it

Let’s face it…Canada has nothing but resources and housing. They tried to cook resources under Justy. Think they will ever tamper with housing?

Nevaeh.

If you want a good laugh, read Garth Turner’s Greater Fool blog. He is the complete opposite of Wolf when it comes to selling his book vs. Stating the facts.

Garth Turner on his blog thegreaterfool.ca stated don’t buy gold about 6 weeks ago.

powell as much as said today that he’s never going to take inflation seriously if doing so would cause a decline in asset prices.

We Yanks have a fundamental Constitutional right to (at least a perception of) a wealth effect, didn’t you know that? Bestowed on us by the Almighty at the Battle of AMZ nosebleed heights.

That’s not what I heard.

I did wolf. I think third to last question. He said housing prices won’t come down, they’ll just stop going up so fast.

I doubt he’d say it but I can only assume he thinks the same about VTI/VOO.

not directly. but he said that the economy and markets would have a “soft landing.” i read that to mean “ideally, we’d get inflation under control without taking the froth out of asset markets, but if we can’t do that, we’ll let inflation control to run out of control to prevent the asset price decline.”

Powell’s venture captialists and their Collateralized Loan Obligations (CLOs)

would suffer if rates were real.

The one Congressman that mentioned the Rules of the Fed, how they dont seem to appear anywhere, and that the Taylor Rule would have rates circa 9% gets my vote for questions of the day for Powell.

Looking at homes for sale this spring in my city. Lowest for sale inventory I have seen in the 20 years I have lived here.

For sale inventory is about 75% below normal. Lower than last year.

I suspect we will have some nice bidding wars as people want to buy before rates get too high?

Yes I will be queuing up to buy a house right before I think they are going to drop in price!

ru82, where in the midwest are you? You can’t talk about RE without specifying the market you are referring to…

Powell has shown he has no intention of helping those hurt by inflation. I have read that in the 1970’s a barrel of oil priced in US dollars moved from $2 to $32 within just a few years. Could the US economy withstand a doubling of the price of oil, much less a ten fold increase?

I believe Powell will get no more than two rate hikes this year. I suspect QE will be reinstated even if it is briefly ended. Powell’s comments are very good for gold and oil. The Fed is intent on debasing the US dollar to keep the stock market rising.

I see no discipline in US political figures.

Comparisons of today’s inflation to that of the 70s can stop with this one fact.

In the 70s we had a Fed that FOUGHT inflation.

Today we have a Fed that PROMOTES inflation.

Look at the behavior of the US government right now with this geopolitical situation.

I’m not getting into specifics since it seems to be taboo here but there doesn’t seem to be much hesitation to sacrifice the consumer for the cause.

Same applies to the FX value of the USD. The markets will be thrown under the bus to preserve the empire which requires the USD as global reserve currency.

“To keep its holdings of GoC bonds roughly flat, the BoC is reinvesting the proceeds from maturing securities to buy new securities.”

I call this “quantitative maintaining” but I think I am the only one. Anyways, even QM is an egregious abdication of mandate by the Bank of Canada in the face of inflation 2.5x above target and runaway real estate prices.

And prices are truly runaway: my wife and I both have stable jobs with far above average incomes in Canada, no kids, no debt, no expenses, lots of savings, etc., and we are priced out in a small coastal town in BC. Can’t compete with the speculators and idiots and money launderers. Yes, technically, we could pay current asking prices and service a mortgage, but being able to do something stupid doesn’t mean it’s affordable.

What a mess. The Bank of Canada has been one or more of: useless, blind, complicit, and incompetent.

The NAV on bond funds adjusts daily to reflect the new value of the bonds, what are Central banks doing?? How are all these Central banks carrying these bonds as the interest rate goes up??!!

As yields increase the price of the bond falls…so the trillions of bonds held by central banks have to be decreasing in value every time rates go up which must/would lead to lower portfolio values. Even small 25 bp rises would likely cost billions.

Even if the banks are carrying these bonds at face value vs market value when the banks sell the bonds, then surely they’d have to book a loss/decrease in portfolio value?

I really don’t understand the math of how large central banks that have done huge QE campaigns can balance their books in a rising interest rate environment, UNLESS the gov’t is providing infusions of cash on the side to the bank, or the member banks are providing cash/equity to balance the book….but then where do the member banks and gov’ts get the cash from?

**”printing currency requires a balancing debt creation, so infusions have to be from equity or taxes

Thoughts anyone???

Central banks are not bond mutual funds. They’re banks. And they don’t adjust the value of bonds that are not for sale. Market value is irrelevant for them since central banks generally don’t sell bonds, but they keep them until they mature, and when they mature, central banks get paid face value for them.

..yea but I thought they were considering selling some of the bonds in order to shrink the balance sheet faster.

Oh well thanks for the clarification.

The Fed said it might consider it, especially with regards to MBS. The BoC heads have not said anything to that effect. And central banks have not yet sold bonds in large quantities. Only time the Fed actually sold bonds was in 2021 when it sold its corporate bonds and bond ETFs, but the amounts were small (ca. $13 billion) and it made money doing it.

It’s kind of funny here in Canada. Our Prime Minister hates oil and gas, but that is what is keeping our economy afloat right now. Housing is going crazy here. The For Sale sign on homes is barely up before a Sold sticker is added. New houses and infills are being built everywhere. But inflation is also bad, and no one believes the official government of Canada number. The question is not who’s first to hike rates, but how far or how many rate hikes before their Central Bank are forced to stop. I believe the Bank of Canada can only go to around 2% without tanking the economy, which isn’t much. There’s no way a 2% interest rate is going to stop 7 or 8% inflation, especially with oil prices on their way to the moon.

Let’s see what this will do, it might take time or it might do nothing when it comes to the insane Canadian housing market. Just read that they are still setting record price gain up there but these things move slow unlike stock especially when it comes to price reversal if that’s even a thing one can fanthom after close to decade of a half of nothing up up gravy train.

“The national average home price broke an all-time record in January 2022 as Canadian home prices continue to rise across the country. For January 2022, the average home price in Canada’s housing market was $748,439, up 20% from last year. Compared to last month, average Canadian home prices are up 5% from December 2021’s average home price of $713,542. Meanwhile, the MLS Benchmark Price increased 23% year-over-year to $825,800 for January 2022. That’s the highest year-over-year price growth that Canada’s housing market has ever seen.”

How do Canadians afford anything? Are wages that much higher than the US? I just can’t see how those prices have been sustainable for this long. Makes me scared for the future of the US housing market. How distorted can it get?

Uhm…

– less spent on health care. (single payer is cheaper)

– better social safety net (including worker rights and minimum wage)

– less spent on higher education (nowhere near as crazy as US)

– less spent on cars (smaller in general, and fewer)

– shorter mortgages – so lower rates (for now). Kid was borrowing for a house at 1.69%. A lot of 3 yr and 5 yr at fixed or variable.

Shouldn’t all that have already been priced into housing? It’s not as if those costs have fallen, suddenly freeing up more money to pay up for housing….

You should visit Toronto and Markham, Ontario. There are more Paganis than Toyotas where there are international colleges and Chinese shopping plazas.

Someone might get the idea from your post that Canadian social services don’t cost more than in the US.

Taxes are higher there, noticeably higher. The country isn’t getting anything for free.

The income distribution (reflected in some of your examples) isn’t as lobsided as it is in the US which is one factor.

My brother is a professor at a Canadian university in Nova Scotia. Yes, a lot cheaper than in the US but nowhere close to cheap. It’s still beyond the financial capacity of the median household income, by far.

Mortgage rates are lower, but this is mostly if not entirely offset by higher prices.

Not sure what the LTV ratio is available through the government’s mortgage insurance. It better to be about the same as the US or else affordability is probably worse.

Prices went up over 30% last year in Halifax near where my brother lives. Incomes are low in the maritime provinces and this market couldn’t have been affordable to most in that area even before.

Wages higher? Not to my knowledge, though maybe it’s changed since US incomes have stagnated for two decades.

My brother lives near Halifax, for the last 21 years. He just bought a house in Wolfville where both he and his wife work at the university.

They can afford it because they had some equity from their prior home and both have one of the few good paying jobs in the Annapolis Valley.

I agree with some of the points in the post below but have also often wondered how people there make ends meet, though I’m not totally familiar with their lifestyles.

Point is, it’s not exactly like there are very many good paying jobs in the area. Some have owned their houses for a long time, others (retirees) brought money with them from elsewhere but mostly to my knowledge, housing is less affordable there than it is in the US.

Proportionately there is more (or seems to be more) foreign money in the largest cities but don’t know how widespread. It’s not common to my knowledge anywhere near my brother.

Interest rates are lower but you can’t get a 30YR fixed rate amortized mortgage. My brother has had a series of 5YR mortgages with 30YR amortization since he first bought in 2010.

If rates move up noticeably, Canadian homeowners will be impacted more or a lot more than here in the US.

In Omaha ne people are starting to speak out ,properly taxes out of control,but assessor says not there fault ,increased housing costs ,watch out in a year ,when food is unavailable,CHAOS

I read an article recently and most of the experts believe if there is a dip, it will not be much. Mainly the reasoning is short supply of housing couple with a lot of immigrants arriving. Canada had 360k immigrants in 2021. They expect more this year.

I read that Canada builds about 200k new homes a year. I am guessing the average family is 2.5. So that will provide housing for 500k people. LOL New immigrants will need 74% of all new housing built in Canada.

I believe the same thing is happening in my city. 50% of are growth each year is immigrants. There are just not enough houses being built to meet this growth. The population has been growing at 8% YOY but housing is growing at 6%. Like I said, much of the population growth is immigrants. What is crazy of the 50% growth in immigrants in my city, 40% are undocumented.

On issue for the lack of homes is because builders want to build McMansions but immigrants are mostly low income. The medium family income in my State is $62k. 75% of the people in my city make between 28k to $38k. The average new home being built in my city is $505k and this is in flyover land.

What I am seeing is multi generations moving in together or the Parents buy a home and the kids live with them and pays rent or the kids buy a home and the parents pay rent.

FYI…We have never seen this many homeless in the city before too.

No, it isn’t different this time.

I saw this video which shows politicians being asked what the average house price is in Canada. The reply or rather lack of is unbelievable.

If you factor out the Chinese home prices would be a lot less in Canada than in America. Instead of buying low and selling high the Chinese only buy when prices skyrocket and then all of them pile into the trade. No one making under half a million dollars a year could ever afford to buy anything new other than a small apartment in two thirds of Canada.

Why is the govt deliberately keeping the immigration numbers above the construction numbers?

Answer: to force up house prices.

And we can’t easily vote Trudeau out because he nixed proportional representation, which makes it harder to get a smaller party bootstrapped.

So no democracy for you!

The Federal government controls the immigration rate (and they have it high because Canada’s demographics yields a dearth of young people) but it DOESN’T control the number of new homes constructed each year — that’s a function of provincial and municipal policies interacting with the developers and the construction industry.

Family members bought in Okanagan 1 year ago at 850k. They just sold for 1.35M. They bought a massive RV.

Wow nice gain. They are going to live in RV or buy/bought another property?! Tough to sell rn before you buy because where do you go with month on month price increases and minimal inventory.

I sold a townhouse in Edmonton, Alberta Canada in March 2021. After fees I just did double my money in 31 years. Bought it in 1990 and sold it in 2021.

Yardeni is out with his monthly report on big four central banks As of end of January it was $31.2 and still rising slightly. Inflation is a world wide problem, but the big central banks (BOE, BOC,BOJ, Fed) just don’t act like it’s too urgent of a problem.

Careful with these multi-central-bank numbers. The non-US central-bank balance sheets are converted from their currency (euro, yen, etc.) into USD, and so the balance changes with the exchange rate.

Of the four central banks you mentioned, two ended QE by January: BOJ and BOC. The Fed was still buying at a fairly high rate in January. And the ECB was just starting to slow down.

Rumer is that Adam Vaughan is trying to drive down bond yields to appease the Chinese foreign investors for real estate bubbles.

Energy price shocks, are in many ways, the same as interest rate rises, both strip cash out of people’s pockets and both can lead to full blown recession. For Canada and the rest of the world, I suppose it depends on where the energy price shock eventually gets to.

Will people in the USA pay $7.50 a gallon for fuel….Yes, of course…..Europeans do now, though we don’t tend to drive as many miles, as things are much closer than in North America. If I have a busy year, including a trip to the South of France (800 miles each way) I rarely go over 5000 miles for the year….

Equation for gas B÷42÷2×3=G plus 18 cents federal tax plus your state and local taxs.(B being price per barrel of oil and G being gallon of gas).

In my state we have 1 state and 2 county taxes. $115 oil tranlates to $4.58 per gallon of gas in my state. I guess wolf didnt post my other post so i wont continue with why we just poured fuel on the inflationary fire 🔥.

Powell to recommend 1/4pt.

I say to Powell.

WHY BOTHER?

Rep French Hill of AR…..in the House hearing with Powell….

won the day, IMO.

You can access this wonderful questioning at the 2:33:000 mark of the youtube video.

He mentions the Taylor Rule and where it would formulate rates currently…taking into account GDP, Employment and Inflation….circa 9%!

Also mention Fed Rules seemingly omitted from recent Fed publications…

And above all…… he said… “Inflation is a THIEF” … I hope Powell heard that and sided with that assessment. Maybe not. For the Fed to PROMOTE ANY inflation, as they do, is thus then to PROMOTE thievery. Wouldnt that be an interesting exchange?

Why do some (most?) central banks coordinate with the US Fed, while other countries to what they please (e.g. Brazil, Russia)?

Does anyone understand that dynamic?

When inflation turns to hyperinflation eventually everyone goes completely broke. The rich become the new poor and everyone is poor. I guess the goal of the U.S. Fed is too make everyone poor and at least that will make the people who are already poor happy when they see the rich all become broke like them.

If you listened to the Powell testimony today, there were mentions of Rules of Monetary Policy, usually included in Fed publications, missing from the most recent one. Powell said it was an oversight.

So I found the “Rules of Monetary Policy” at the Cleveland Fed…and I provide the link. Click on the item at the top of the list…

Fed Funds are way way way below where the “Rules” suggest they be…..curious that it was missing from recent publications.

https://www.clevelandfed.org/our-research/indicators-and-data/simple-monetary-policy-rules/archives.aspx

New biz idea for WR: making book on Fed rates for those who wish to gamble. Obviously we have several ‘fish’ at the table. One doubts there will be a rate hike at all so betting against him is the easiest money you’ll ever get. Another thinks 2 of .25 and done for the year. So it only takes the March hike to take out # 1 and a third hike in 22 to take out #3. I’ll give either good odds. # 1 at least 7 to 1.

I’ll also bet on a .5 bump in March but here I want odds. I also want to know the rake, although in the case of #1 I don’t care what it is.

BTW: I think I was first to raise the idea of .5 on WS about 2 months ago when retired Fed guy Hoenig said Fed should consider it. He is widely respected in the Fed. I believe he quit after the Powell Pivot, rolling back the baby steps after a storm of abuse from a financial genius.

Not sure about last sentence- he may have quit earlier.

Nick Kelly,

Hoenig was head of the Kansas City Fed from 1991 to 2011 and thereby also served on the rate-setting FOMC. He retired in 2011. Over the last 3 years of his term, he spoke out against and voted against Bernanke’s 0% and QE policies.

In 2012, he started running the FDIC — the Federal Deposit Insurance Corporation.

I’m betting on 3 one quarter of a percent rate hikes and inflation will magically fall coming into the midterm elections only to rise again in early 2023 and then skyrocket into hyperinflation. There will be no 18 to 24 month hiking cycle interest rates will be hiked for at least the next 7 or 8 years continuously. So the hiking cycle should last decades not 18 to 24 months.

Odds of a half point hike in March I’d put in the 20 to 25 percent range sure as hell not 50 percent range like it was. I bet horse races on the premise of what I know the odds on a given horse should be and what the actual odds are at post time and bet accordingly on the overlays. I also take the track bias into account.

Nick Kelly,

NEWS FLASH:

Financial publisher Wolf Richter arrested for illegal bookmaking. He faces 3 years in a California state hoosegow and a fine out the wazoo. Authorities are now investigating the person or persons who colluded with Richter to start his bookmaking racket. The Federal Reserve’s Financial Blogger Suppression Department, which had previously been investigating Richter, is sharpening its knives, according to people familiar with the matter.

The true inflation figures show in Canada if you look at the increases in the purses at Mohawk and Woodbine racetrack in the Toronto area. All the purses are up between 5 and 10 percent in the last 6 months.

I have heard the Canadian Mortgage and Housing Corporation (CMHC) underwrites or guarantees just about all the bank morgages in Canada. What happens if there’s a downturn or wave of mortgage defaults? Will Canadian taxpayers be subsidising bankrupt banks and deadbeat homeowners who refuse to move out?

Yes. The CMHC is funded with taxpayers’ monies. The poor on social assistance like OW and ODSP will have their benefits cut to save the wealthy paper rich home owners.

Here in Canada a 10 year GIC is 3.20%. I think rates need to be much higher with inflation, taxes so a 4.20% to 5% 10 year GIC is in the works in the next 12 months. Our GIC is like your CD in the US.

The US is a empire that is dying gasping for its last breath of air. Bankrupt and committing suicide. Fiat currency has reached its limits its destruction is written in history.

“Nations are not ruined by one act of violence, but gradually and in an almost imperceptible manner by the depreciation of their circulating currency, through its excessive quantity.” ~ Nicolaus Copernicus