Cloud software hype comes home to roost.

By Wolf Richter for WOLF STREET.

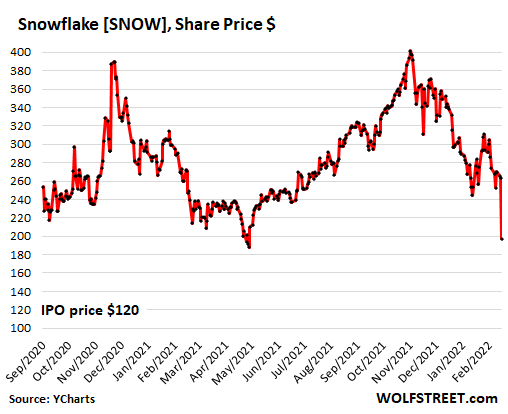

Shares of cloud-software company and Buffett darling Snowflake [SNOW] collapsed by 30% initially to a low of $184 in afterhours trading before recovering a little and is now down about 25%, at $198 a share, after it reported an operating loss in Q4 of $152 million and a net loss of $132 million, on $384 million in revenues, peppered with disappointing guidance and the announcement of the acquisition of Streamlit.

Snowflake had a steamy IPO in September 2020, the largest in the US that year, in part fueled by Berkshire Hathaway which bought about 2.1 million shares in a private placement and 4.04 million shares from former Snowflake CEO Robert Muglia in a secondary transaction, both at the IPO price of $120 a share, for a total stake of 2.2% of the shares outstanding.

For the year 2021, the company lost $680 million, compared to $539 million in 2020. Over the four years for which financial statements are publicly available, the company lost a total of $1.74 billion.

On the first day of trading following the IPO, shares opened at $245 and spiked to $319 intraday, before closing at $253 a share. They never got anywhere near the IPO price of $120.

After some sideways trading, shares spiked to $429 intraday on December 2020, amid enormous hoopla and head-scratching, in a moment that was typical for the craziest stock market ever, giving the company an inexplicable market capitalization of briefly $120 billion. Shares then sagged, but spiked again to $403 a share on November 16, 2021, after which they lost their footing, along with a whole slew of other highfliers.

From the intraday high on December 8, 2020, shares have plunged by 54.5%. At the afterhours price of $195, Buffett and other investors able to buy at the IPO price are still in the black, but not many stockholders are who bought the shares in the open market (data via YCharts):

What rattled a lot of nerves today – with the stock price still at these nosebleed levels – was the guidance for product revenue growth of 65% to 67%, down from the actual growth of 102% in Q4, reported today. This was seen as competition in the data storage and analytics sector encroaching on Snowflake.

In reality, at these nosebleed levels, in a sobering market, anything can rattle nerves.

It probably didn’t help that Snowflake announced along with its losses and soft guidance that it had agreed to acquire Streamlit, without disclosing the terms. Streamlit is “a framework built to simplify and accelerate the creation of data applications,” it said. “With this strategic acquisition, the two companies will join forces to unlock the unrealized potential of data and make it easier to build beautiful applications.” Yes, very poetic. I thought so too.

Shares of cloud-software provider Salesforce.com [CRM], which owns 6.1% of Snowflake, dipped 0.7% in afterhours trading today and are down 33% from their high on November 9, 2021.

Shares of Twilio [TWLO], another cloud software company, have plunged by 64% from their high in February 2021.

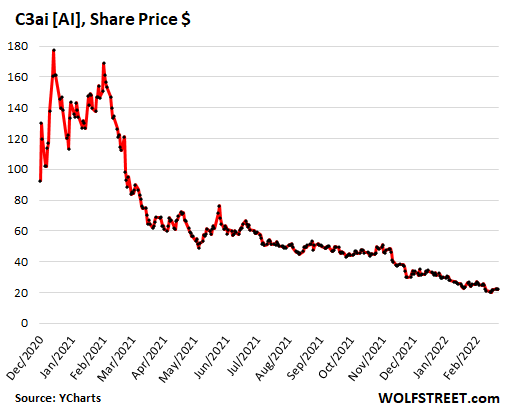

Shares of C3ai [AI], which sells cloud-based AI software, have collapsed by 88% from their high in February 2021 – yes, that infamous February 2021 when something changed and the highfliers started coming unglued, one after the other. The plunge includes the 2.8% drop in afterhours trading today, after the company reported that its net loss more than doubled to $39 million in Q4, on $70 million in revenues.

It didn’t help that C3ai also announced that it had a new CFO, the third CFO since the IPO in December 2020. The old CFO had been with the company for only four months. Just another horror show of IPO hype turned into collapse, one of many since February 2021:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I’m getting a feeling the next leg down should be significant. Maybe even circuit breakers . This last rally is running out of steam.

Those circuit breakers just notify the fed to hop in a throw some $$$ around I believe these days.

andy – I’m with you. the punch bowl is gone…where is it??

Not gone for Fed members – Powell is up to around $85 million

in his personal accounts. He started the job with a paltry $50 million or so.

Punch Bowl is there . . . no punch though.

When you run a cloud storage and analytics company and can’t make money these days… yikes.

They don’t care if they make money. Their business is doing the IPO and pocketing the investor cash.

Harrold, it seems so Dot Commy true right now, doesn’t it, for so many of the tech thingy businesses. Seems as if it could be that much of their biz strategy is more about IPO winnings. Or maybe it’s half IPO bucks and then the other half is selling to a new set of suckers? Musical chairs with profits.

Every man and his dog is doing cloud storage or security IT these days, so very many companies competing for the same space.

As with online gambling, companies in a quickly-crowded space like this as showing desperate moves — throwing money at customers or at novelty acquisitions. It has the scent of desperation, so early in a firm’s life.

Promoters say “the next Amazon,” “the next google,” but the critical fact is, these originals were pioneers and first movers who blazed a trail. Not the absolute first mover in each case, but the ones who got in early enough and had the right stuff to build a durable industry with strong network effects. Some few of the latest crop in insurance and DeFi etc., will be those survivors and it was not complete folly to out smaller bets scattered across them. But the real money in that strategy is mostly for angels and other early investors. It won’t always work as Buffet doubtless knew. But it dents his reputation a little bit.

Buffett probably sold out his position causing snowball effect ,,he’s to smart to take that big of a hit

Cloud is the 21st century equivalent of a utility company. It’s not revolutionary and these companies aren’t “disruptors”. it’s a data center with economies of scale.

The valuations on the named companies are utterly absurd; totally disconnected from any realistic business prospects where these valuations make any sense.

Salesforce is much better than the others but still in deep outer space.

“Now, the packet in front of you has our focus group research. Inside, you’ll find the breakdown including keyword association with the brand. The top two being ‘originality’ and ‘fresh,’ which I think are great things to keep in mind as you begin working on Matrix 4.”

Apologies if it has been pointed out already, but a lot of the “Buffett” purchases/sales aren’t really his, but the two asset managers he hired several years back to take his place when he finally leaves/dies.

Of course they do affect BRK’s bottom line just as if Buffett himself had done the purchase/sale. But it’s not entirely accurate to say Buffett did it.

phleep-truly original thought is the rarest commodity…

may we all find a better day.

LK,

Don’t forget “beautiful” (as noted in the article), and may I add “like you’ve never seen before”? Both have become quite popular adjectives recently.

English comp has never been easier to master.

I wish I could say the same for economics.

“ones who got in early enough and had the right stuff to build a durable industry with strong network effects”

ugh..what the hell are you talking about…?

We live in a woke world where if you did yesterday something that was right but by today standards is no longer, you may get cancelled electronically.

I am not giving an opinion if that is great, good or bad, just an observation on things that happen and even outdide your own actions.

Examples are the freezing of accounts of people donating money to protestors in Canada.

Or the Russian citizens who got stuck in the metro because visa and apple pay and whoever else cancelled them; those people themselves did not invade Ukraine but happen to suffer from bad bad Putin who is in charge because he owns the people counting the votes .

Yes, these are examples of people but same risk exists for companies (and shareholders) these days;

just ask anyone who invested in Russian companies with low valuation but high profit value instead of Tech stock with high valuation and low profit value. Those carpet bomb sanctions just wiped thrm out.

So the question is if it is still be great to put everything in the cloud or keep a bit more control over things?

I imagine the pain is quite concentrated. If you like SNOW, you probably owned a dozen other small tech companies, and they’ve all been dropping like rocks.

It seems you either love them hate them.

Will a stock market crash affect the Beijing money lawnderers in Canada? I’m fed up of seeing 18-year-old “international students” from China driving those rare Italian sportscars which cost US$2M to order.

Lol. Saw one of those guys today at a University of California campus. The out of state (foreign?) tuition, high end wheels, no big deal.

We have come a long way since I was in Pharmacy School at Oregon State, 78-79. Back then it was mostly all rich Iranians in loaded Trans Ams or Blazers.

They try hard to lose virginity. Unlike local boys getting away with a split-check dinner.

Right, because local wealthy boys don’t drive high-end cars.

Beijing money still has its own moats. Beijing tiptoes into global links and pulls back behind its walls. Right now I think its expansiveness is a bit muted because of its internal credit issues, vetoes by Xi of a bunch of business, and bizarre wrangling with COVID.

You’re fed up because someone else has money? Wow that is the most openly stupid comment I’ve ever seen on Wolfstreet.

Yes, he is upset that someone else has money. That is 100% the thrust of their message. I am stunned by your clarity of perception and insight into the minds of othera.

It’s not that hard.

The wheels are coming off the bus and nobody but those who choose to pay attention know. My architect called me a few days ago and said that 3 three THREE! of his clients decided to hold off pursuing their projects, and he only had four or five active jobs going. The buyers strike has begun. I’m not surprised in the least that the stock market is starting its turn for the worse. What’s coming won’t be recognizable to any of us, but at least those of us who know it’s coming won’t be caught off guard.

Good info!

I am not sure what will happen. Where will the buyers who are going on strike live?

There is not enough housing. My city has seen a population growth of 8% YOY the past several years yet only a 6% growth in housing YOY. This has caused the amount of homes for sale inventory to keep dropping YOY. Inventory for sale is 80% below normal.

People need housing. I guess we will just see a lot of people start having roommates?

Just read this article in Bloomberg. Eye opening

Mullen left Goldman, then founded Pretium in 2012, raising money from investors and plowing it into rental houses as well as bets on corporate credit and mortgages. In its early days, the company bought real estate at depressed prices, but as the market recovered, it learned to win deals by moving fast. These days it employs software that scans real estate listings every 15 minutes. When its acquisitions team sees a home it likes, it estimates rent and a repair budget and aims to get a cash offer out within hours of the home going on the market. Pretium also works with homebuilders to develop communities of new rental homes.

The suburban gold rush also proved irresistible to private equity giants, sovereign wealth funds, life insurers, and everything in between. Pagaya Technologies Ltd., which uses artificial intelligence software to evaluate consumer credit, started helping clients buy homes. Boston Omaha Corp., a holding company that, among other businesses, provides broadband internet to subscribers in Arizona and Utah, hatched a plan to develop rental projects. So did a water company in Denver, Pure Cycle Corp. “Adding single-family rental or something tied to housing in your company name these days is akin to adding ‘dot-com’ back in 1999,” Palacios says.

A reali In 2019 helped a client sell a house in Surprise, a suburb 30 miles northwest of downtown Phoenix, to a Japanese company. The buyer, a family-owned conglomerate called Yamasa, redid the kitchen and listed the house for rent at a price that seemed unrealistic. But it rented, and Yamasa’s agent started blasting him with emails, offering cash for other homes. Yamasa, which did not respond to requests for comment, has since become a prolific buyer of rental real estate, acquiring hundreds of homes in the Phoenix suburbs and thousands of other properties across the U.S.

Typo on my name above as it should be ru72 but does anyone have an idea how many homes in the US are owned by investors.

The article also said Blackstone is publishing public paper saying it is better for people to rent than own. lol. That seems like a conflict of interest.

Just some good ole inducing of demand by changing public beliefs and perceptions. Commercial propaganda, nothing to see here folks. Buy my shit.

It certainly has been done before in the USofA. Boarding houses, having someone stay in a ‘spare’ room, etc was not unusual in the past .

Imagine that? Like that’s never ever happened before. It used to be pretty routine to share a place when just starting out, to save money and be able to have a nicer place than by oneself.

I don’t think it can be done today due to all the “Laws”, etc. especially Zoning Laws…….

Would you really want a “stranger” living with you in today’s (lack of ) Culture.

Interesting factoid: 16 year old John D. Rockefeller lived like that when he started work in 1839. His parents lived on a farm. His dad was never home, and he was mature enough to do so. Imagine a 16 year old doing that today.

Not a big fan of implying outliers are the norm or could ever be.

One Superman is enough. A world of Supermen is trouble.

Berkshire Hathaway is up 84% over the last 5 years.

S&P500 is up 84% over the last 5 years.

Except S&P500 ETFs paid dividends over those 5 years, unlike BRK.

So is Buffet just collecting people’s dividends while index investing?

BRK is made up of lower growth, lower PE type companies. His insurance operations allows him to hold about $150 billion assets at long term negative cost that gives him a tail wind. With his cash stake he is running about 80% equities and 20% cash. He will probably out perform in a down market.

He tells you if you need cash to sell 4% of shares per year. It’s more tax efficient not to pay investor a dividend and have them sell shares if you can generate a fairly steady and growing share price.

The tax benefit is on the timing now. Tax rates are the same for the same holding period and have been for years.

Many investors don’t want the income and would rather let it compound tax free til they need the cash.

But how long could you realistically grow a share versus maintaining and paying a steady stream of dividends?

The unsavory reality is that growth has limits.

Brk has been a pretty steady grower every decade. Last time I did the numbers their 10 year growth rate was 11%, but that was 3 or 4 years ago.

No problem selling 4% of shares each year as it is much lower than growth rate, but your income would rise or fall with the share price.

Buffett recently did a share buy back. He said everything was overpriced so he was returning money. He did this by way of buyback instead of dividend because first is capital gain while second is taxed as income.

Also: everyone is up last 4 yrs. Given Buffet’s usually more conservative holdings it is actually not bad it matched the S@P which has a bunch of risky high flyers which have tripled. The test of Berks vs S@P will be the next 4 yrs.

So much of trading (betting) these days seems to be folks trotting out some fancy new unicorn and having a popularity contest over which mythical business model looks hottest and sexiest for a minute until reality kicks in.

Sheesh

Those that vote early and often, then get out quickly seem to win.

The buisness model is to made up a unicorn (cloud data analytics payment processing), and go IPO while the going is good. Billionaires minted daily. The Fed’s “wealth effect”.

The era of companies with silly names is coming to an end

How about ridiculous twitter antics by CEOs that seemed to move mountains of money and markets. Musk was only the most obvious — (arguably committing) securities fraud couched as a pot joke about TSLA going private at $420 with “funding secured”? Joke crypto Dogecoin soared when he merely mentioned it? I hope that all goes with the dinosaurs and dodos too, when the real specter of fundamentals re-asserts.

Corporate names over the last several decades have been mostly awful and someone probably paid a consultant big money to come up with it.

It’s worse for spin-offs and mergers where recognized names were replaced with something totally stupid.

Why not call the company “ponzi”? They keep raising investor money and losing it on their dubious business. All the while hoping the stock will go up enought to make them rich before the market catches on.

Imagine the IPO price for a company with a name like:

“SouthSeas TuliPonzi Data”

Symbo:l STD ?

good one MA,,, glad you are commenting here with the humour and prescients of your comments so far…

Makes for the very informative AND entertaining part of Wolf’s wonder,,, at this point, one of the best of the websites with at least some ”moderation” of the comments for us to keep on topic, bee at least somewhat ”polite” etc., etc…

Hmmm… this article explains an awful lot. If you have Warren Buffet and Salesforce as your seed money providers it gives a lot of confidence to the rest of the market that you will be the “cloud-software company” that survives the inevitable shakeout.

Buffet (and his reputation) were a backstop for seriously wobbly firms in the past: Solomon Bros. in the early 90’s scandals, and Goldman Sachs in the pit of the GFC. He has not been sloppy with getting visibly involved in projects — he rejected many (Lehman, Long Term Capital Management). It IS striking that his presence didn’t carry the day here. But being an early investor in hot tech was not in his wheelhouse before.

It’s market that should be big enough for many competitors though I expect at much lower margins later.

Unrealized potential of data? You mean they invented a better spy trap for users?

And beautiful applications? Just another whacky framework that will be the punchline to a joke a year from now. Funniest part is watching fools learn every new language and tool that comes down the pike so they can list it on their resume.

Buffet always claimed he avoided high technology companies because he didn’t understand them. So a purchase like Snowflake is hard to believe. Perhaps the answer is that Buffett is long past his prime days as an investor.

That’s what everyone said just before the tech Bust of 2000.. Je has 2 money managers running a lot of of his portfolio. If it was under a billion dollars might have been done by one of them. He usually does the big concentrated buys of $10 billion or more these days.

>> Perhaps the answer is that Buffett is long past his prime days as an investor.

According to this article, the shares were purchased at the IPO price of $120, way below the current share price. They made a killing so far.

Buffet also made a killing on that activision gaming buy-and-flip recently. The timing was so perfect prior to its acquisition by MSFT, it has an insider kind of whiff to it. It definitely was not an opportunity that would have been offered to a someone like me or you, at scale. Maybe some new people are being tested out at Berkshire.

He actually didn’t make a killing on that. Currently he has made zero profit on that deal. He bought all those shares for what they have been selling for even now after the deal was announced.

Also he didn’t perform that purchase.

Most of these big sharks hunt by insider hints.

You do not judge an investor by one purchase.

Consider WB’s record for at least the past five years to decide if he is past his prime ,or not

Richard Greene,

I was just about to comment this same sentiment before I saw your post.

I am also very surprised to see his interest (let alone investment) in this type of company. This was the same guy that said he wouldn’t invest in Google some years ago because he didn’t “fully” understand the business model well enough.

Does anyone know why Buffett is pivoting?

I would theorize that just like any “successful” wall street gambler Buffet has his sources. With brick and morter companies these sources feeding Buffet information can put some lipstick on it but not too much. But the IT turds out there are something else. This is not lipstick on a pig, this is lipstick on a turd shaped like a pig. And the people selling this are 3rd world scum the kinds of which Warren had probably never seen before. I started working in IT just at the beginning of the 2000 crash, got laid off at a consulting company. The consulting company put me on a project for a wall street firm building a trading platform software in Java. This project that could be done by 10 people had 250 people assigned to it. But that does not hold a candle to the scams going on right now…people need to take a hard look at where the “money managers” are parking their retirement cash and reevaluate. Otherwise the underpasses in this country are going to become retirement homes.

Where are money managers invest.?

Probably treasuries.

Buffet’s biggest holding is Apple. Up 500 billion.

Databricks is biting Snowflake’s ankles, with some success.

Their employees are called ‘Bricksters’…

If they get funny hats, it will really take off.

Slightly used robinhood hats are available cheap, second-hand.

I’m in IT and I have to say this is the best BS line I’ve ever read. “a framework built to simplify and accelerate the creation of data applications,” it said. “With this strategic acquisition, the two companies will join forces to unlock the unrealized potential of data and make it easier to build beautiful applications.”

LOL

Sounds like Adobe cloud- already carrying a lot of traffic for some of the big hitters. There are only three main clouds- Azure, GCP, and Amazon. Even Adobe runs their cloud on Azure (mostly- not 100% certain of back end) Cloud tech is going to displace quite a lot of data center, but not sure what else. Certain companies are in danger from cloud, though trying to move their on-prem types of tools to cloud based- F5 for example. Content delivery networks are also rushing to remain out front of cloud. Akamai- the original, most pervasive CDN should be able to stay out front because of scale. Their main competitor CloudFlare is another money losing investor supported version of SNOW, though who knows if they have a trajectory leading to profits?

MT,

Even worse is the name/brand. Would you entrust your data and software to a company named Snowflake? I wouldn’t.

Not all of us here are “computer or tech savvy”.

So, can someone kindly explain, in plain English, what SNOWFLAKE does?

What do they Sell? What exactly do they do? As Senator Bernie Sanders would say, “What do they do do?”

I can’t figure it out. I’m old school and think of companies that make things, or ship-move things, or fly you around.

When I think of “cloud storage” I visualize a cold warehouse with a bunch of servers. That sounds like something a group of high school nerds could put together, thus, what is so special?

Is it like those huge, 3 story, storage units popping up everywhere? Those are “off site storage” places for physical stuff. I can understand that.

Is that what “cloud date storage” does? Store Tweets and Facebook posts? Really? Now that would be an economy to scare the Chinese.

Marcus Aurelius,

I’ll give it a shot.

The “cloud” = gazillion servers in thousands of data centers around the world (hardware), owned by third parties, such as Google, Amazon (AWS), Microsoft, and a bunch of smaller ones. And these companies, and other companies, then provide all kinds of software and services to make this work.

Regular companies used to run their corporate and communications software and database on their own servers at their own locations. But in recent years, they switched to the “cloud,” meaning they run their stuff on rented servers at these data centers and pay for all kinds of extra software and services. There are many benefits to this setup, but also some real drawbacks.

Companies, such as Snowflake, provide additional and specialized services and software to companies that have switched their data to the “cloud.”

Google “the onion hp cloud”

Look for the video entitled: HP Offers ‘That Cloud Thing Everyone Is Talking About’

There are plenty of REITs renting cloud computing services with good dividends.

I like the reits with communication towers better. Smaller footprint, no AC maintenance, minimal staffing.

Snowflake is another Musk – a decoy for military activity to act with impunity.. It is Vanguard and Blackrocks loss maker run as a decoy for a few morally corrupt families to act with impunity. Largesse enables. University brains run snowflake.

Do a search for workday ms teams integration – HR tool and business filing system with instant messaging wrap around. All US defence employees . AND. China military. are analysed for their potential to de collaborate with their employer. To minimise risk you understand while rights freedoms removed.

This is why Gates and Buffet have shared so many fireside chats. And collaborated. On shares. Investment strategies. To create weight. To achieve what a scrutinised DARPA can not.

Nothing to see here folks. Look over there. This sheen you are seeing gives us room to manouver. You choose not to question our strategy to farm humanity for profit via war. Could not have done it without the corrupted grammar. Search

Russell-Jay:Gould post office.

Our IT company used to have that meme saying hanging in their office. “There is no cloud. It is just someone else’s computer.”

I remember when “the cloud” was called time sharing.

Is that like a “Party Line” on my family’s 1960 rotary Bell Telephone service plan?

I get it.

SET HOST

(DEC VMS)

Exactly that

I don’t know about the financials of Snowflake, but for business IT, Snowflake tackles a number of problems that have developed with database storage and data accessibility. Relational databases(SQL or structured data), like Oracle, DB2, MS SQL have dominated until internet companies like Google and Amazon started capturing massive amounts of data, for example, user clicks, which is typically stored in NoSQL databases (unstructured). This has created a bifurcation of incompatibly accessible data that businesses need a simpler why to utilize as both kinds of databases (SQL and NoSQL) are now mainstream. Snowflake has developed a DATABASE that was designed from the ground up to run on the cloud, meet performance requirements to compete with high performance warehouse/analytic databases such as Teradata, all using the widely common SQL interface. If they have done what they claim, this should be a huge money-maker. I was advocating for doing a trial of their software at the company I worked at four years ago, but I retired before I got a chance to test it. Anyway, the direction Snowflake has taken is just the next evolution in bringing cloud technology, database, data warehousing, analytics and probably AI to the next level of accessibility for the ordinary business. I am surprised Warren Buffett has invested in this because I thought his mantra was to invest in companies he could understand the product, such as See’s Candies. I oversimplified the explanation but I think the case is compelling and much more to it than I explained.

Financials make it evident it’s a bag of hot air. It’s a fantasy valuation regardless of what the technology can do. The product may be better than the competition but that doesn’t eliminate the relevance of ROI and cash flow. The purpose of “investing” isn’t to make a better mouse trap but a competitive return versus alternate uses for the money.

After losing another 17% today, market cap is “only ” $65B, down from $80B at the open.

In return, you get a company with cumulative losses of over $1B, no dividend, a (meaningless) P/E ratio of infinity, and a price/sales of 65.

Yes, paying $65 not for a $1 of earnings (which is still only an accounting number), but revenue.

Maybe it makes sense under federal government math but not otherwise.

When I looked at Snowflake, the evaluation was on what problems we were having in a hybrid database world and how that would best the solve the problem in relation to other available solutions. On paper, it meet the needs very well but, like I said I never did a proof of concept with it, meet with existing customers, i.e., got into the due diligence on whether to purchase. Part of the due diligence is if the company doesn’t look financially viable, that would be hard to overcome. That was 4 years ago and Snowflake is still around. I would say their inability to make a profit would be a concern if I were evaluating them now but that doesn’t necessarily mean their product is “hot air”. It’s going to take a while for products in this area to mature and then for the best solutions to rise to the top (and certainly to make money).

You misunderstood me. I never said the product is hot air.

I said financially, the company is a bag of hot air.

In a real (as opposed to a fake) economy and one without an asset mania, the company either wouldn’t exist or would have to price its product to actually make money.

That’s how normal economies and financing works.

If it did that, my guess is that it would have a market cap in the hundreds of millions or maybe a few billion (maximum) due to its growth prospects.

Companies can now go to a hybrid cloud which allows them to run anything in their own silos. No need to switch to SQL if they don’t want to or to pay for any other software solutions.

Snowflake could be part of a hybrid cloud as it is a cloud native application. The hybrid cloud is not a replacement for databases and the need to query them. SQL is the query language so widely known to IT professionals and business users. So it is a huge benefit to be able to use SQL in a “hybrid database” world, which is what I was talking about, which could be on-premise, in the cloud or in a hybrid cloud.

Cambric, than you for that thoughtful write up. As a former SQL DBA I know these problems well. I also know cryptic sounding company literature is a telling sign that they are trying to baffle customers with bullshit.

Since the need is great and they haven’t been able to sell the product in 4 years, this tells me it probably does not work as advertised. I would not invest my money.

Yeah, I attended a Snowflake marketing session, well attended and it was a well-oiled and slick presentation, but I didn’t hold it against them at that time. It had a borderline too good to be true feel, but we had benchmark data we developed for Teradata and others so it looked like we could run a benchmark on Snowflake with minimal effort and cost. But now, I agree with you, I was surprised to see how much has been invested in Snowflake, and 4 years hence, its huge stock valuation and yet they are still losing significant money. That definitely seems like something is amiss and I would not invest my money in them either. Too bad really, I am sure a lot of blood, sweat and tears is in the development of the product. If you are trying to scam people, which seems to be a cynical consensus here, I think there are a lot easier ways to do it…say building a little Theranos black box anyone?

Like in the 2000’s bubble, there is a lot of crap, but some good stuff in there as well.

On YouTube:

“Two minute papers – Is OpenAI’s AI As Smart As A University Student?”

It shows recent developments in which machine learnings / “AI” is able to interpret and solve increasingly sophisticated math problems. As the years go by, even advanced intellectual pursuits are going to be subject to replacement by machines. I used to expect domain-specific knowledge and graduate-level education to offer protection, but now I have serious doubts.

Capital is the best protection to risk, for them and their children. It’s never subject to automation or outsourcing, though it is at risk of depreciation and theft.

“It shows recent developments in which machine learnings / “AI” is able to interpret and solve increasingly sophisticated math problems.”

Man. I could have used this stuff when I took my Differential Equations course in engineering school!

Sorry…the name of the place should have been a tell for everyone, except for those that sold to the bag holders. Always remember what the real product is in these 21st Century “Tech” Companies. The Stock 🤑🤑

Just let this sink in for a minute:

“For the year 2021, the company lost $680 million, compared to $539 million in 2020. Over the four years for which financial statements are publicly available, the company lost a total of $1.74 billion.”

Yet another raging cash furnace.

How does one conclude that this is a good place to invest your money. Unless it isn’t your money being invested.

“a framework built to simplify and accelerate the creation of data applications”

I know! Let’s call it SilverLight!

(where’s the SELL button?)

Lol, exactly. Haven’t heard that name in years but it’s now a punchline, as snowflake is destined to become.

The stock market is nothing more than playground for seniors, who believe they are earning their “earnings,” while the rest of the country goes belly up. What could go wrong?

Softbank isn’t involved in another stinker? There’s still time to lose money!!

Ever notice how the movers and shakers in our economy are all about the age of Warren Buffett?

Nah. You just need to look around. There are lots of much younger movers and shakers: Zuckerberg is an early millennial, Salesforce.com’s CEO and founder Benioff is now in his mid-50s. Tesla’s Musk just turned 50. My wife is…

you know one can’t help but wonder if the establishment( gov) is about to throw Tesla and Musk under the bus. I know the stock has come down from 1250 to 800 something but common its a 50 dollar stock in a rational market.

Cloud-based technology in the time of block-chain. Hmm . . .

Does this remind anyone besides me of Ramses II and the Sea People?

It is our mission to authoritatively provide access to diverse services to stay relevant in tomorrow’s world and progressively build leveraged core competencies such that we may continue to collaboratively maintain enabled ideas through continuous improvement utilizing buzzwords and catch-phrases that sound important.

Hal:

That’s a “word salad” of epic proportions.

It’s a Beaut, Clark!

Since I am one, here, that has no clue what you are all talking about, your advertising “product” needs to be re-written so as to dazzle and convince my type to sign on:

Here is my Copy for such an Ad:

The Global Mission for STD, Inc (SouthSeas TulipPonzi Data) is to simplify your life with groovy office tricks to impress your network of friends. We can store your Data, like U-Haul Storage Units can store your decades of accumulated junk. Want a place for Family Pictures you would rather forget? Phone numbers you can’t remember? A safe storage place for a current list of your Medications and Doctors.?

Our STD pros can pass on to you the latest. Worried about a virus infecting your MySpace account? Your AOL email? Your ClubMed reservation number? WE have the cure. We are STD.

Only STD can protect you from the promiscuous web. Come. Join us for your Data Storage.

We have Three levels of Data Storage for your individual case:

Primary

Secondary

Tertiary.

(Ok. The above list may be beyond what some of you might know…but if you get it, I know you’ll be laughing)

For point of reference Microsoft was still at its IPO price two years later and Apple much longer than that.

Was that before or after EpsteinGates?

1980 for Apple and 1986 for Microsoft. Easy to look up :-]

SNOW is in an over saturated field. Can’t compete with the big dogs and does not offer better SLA. I would say technology needs to invest in simplification. AI can only do so much. Still need boots on ground and hands to keyboard, investment needs to go into simplifying security and process. SSO is no longer single but requires four verifications. Defeats the purpose. Simplification and lean process is The future of Cloud and Security. Look for biometric AI for future of this technology. Look to smart wears.

Cambric Finish: “I am surprised Warren Buffett has invested in this because I thought his mantra was to invest in companies he could understand the product, such as See’s Candies.”

* * * *

As I noted above, a lot of the purchaeses/sales of the last several years aren’t really Buffett’s personally. He hired two asset managers several years ago to replace him as capital allocator for BRK when Buffett dies/leaves.

It’s often those two guys who buy ans sell what the 13F shows. Buffett does the marketing bit (genuine or not I don’t know), like singing the praises of AAPL, KO, AXP, etc.

Buffett’s aversion to technology is often misunderstood. It’s not that he doesn’t understand the technology. He frequently knows a lot about it. Charlie Munger once commented at a shareholder meeting that most people would be surprised at how much Buffett reads.

It’s just that Buffett can’t determine whether a given technology has endurance as a brand, like KO or AXP have. It reminds me of Peter Lynch quoting in one of his books a passage about an electronic device to make the point that it’s hard to know whether 10, 20, or 30 years down the road it will have enduring value.

I know, how quaint. Just do HFT and get rich, and quit jabbering about enduring value.

Yeah, that makes sense and I am sure Buffett is a smart guy and is not technologically illiterate. That is what I find interesting here, BRK shouldn’t be so naive like those investors who testified in the Theranos trial and were seemingly easily duped. I am also sure he (BRK) has access to reliable technical experts who can evaluate companies like Snowflake, which is a hard-core back-end technology product. This seems to indicate that knowledgeable people think they have a viable product. On the other hand, as I have stated, something seems amiss. But as a potential customer, my problem was a lot easier, I just needed to test whether it would do what I needed at a cost I could afford.