The question is particularly hot because Treasuries are now ugly instruments with the worst punishment yields ever.

By Wolf Richter for WOLF STREET.

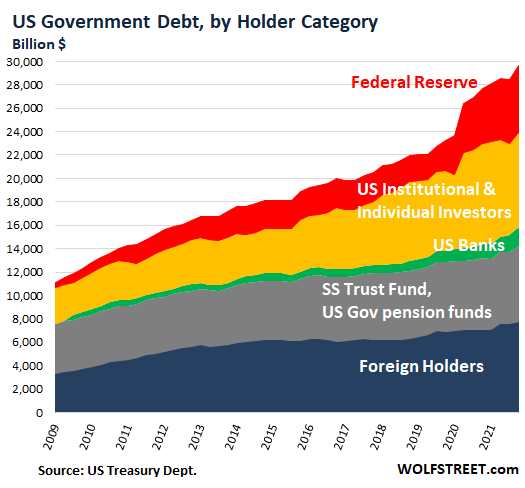

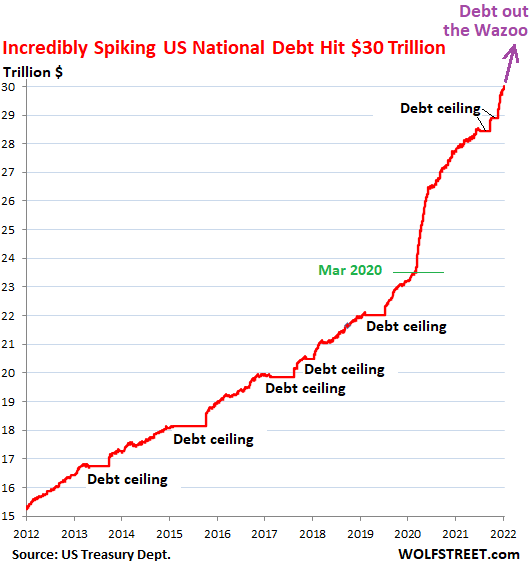

In face of the incredibly spiking US gross national debt that just hit $30 trillion after having spiked by a mind-boggling $6.5 trillion since March 2020, the steamy-hot question is this: Who the heck is buying and holding all these Treasury securities?

The question is particularly hot because these are very unattractive instruments: Yields are still well below 1% for most short-term Treasury bills, and even the 10-year Treasury maturity yields only around 2%, while CPI inflation has blasted off and hit 7.5%, creating the worst punishment yields ever. To top it off, the most reckless Fed ever is still repressing interest rates and is still, though at a much slower pace, printing money.

The whole thing is a tragic clown-show, and yet every single one of the Treasury securities was bought and is held by some entity. Who are they? This is my quarterly update on who is holding this debt, and it’s an increasingly important question for increasingly iffy times.

Foreign Creditors of the US government.

Foreign holders of Treasuries: $7.74 trillion, a record, up by $790 billion (+11%) since March 2020, and up 9.5% year-over-year, according to the Treasury Department’s Treasury International Capital (TIC) data.

About $4.1 trillion of it is held by foreign central banks and government entities; the rest by foreign institutional investors, corporate entities, banks, and individuals.

But their holdings have increased more slowly than the incredibly spiking US gross national debt over the years, and in December accounted for 26.1% of the debt, down from the 34% range in 2012 through 2015.

Dollar amount of holdings = blue line, left scale; total foreign holdings as % of total US debt = red line, right scale:

Japan: $1.30 trillion at the end of December. The largest foreign creditor of the US has increased its holdings since March 2020 by $31 billion.

China: $1.07 trillion. The second-largest foreign creditor of the US has cut its holdings since March 2020 by $16 billion:

Given the incredibly spiking US gross national debt and the relatively stable holdings over the years of Japan and China, their importance as creditors to the US has been declining for years. In December, Japan’s share (purple) dropped to 4.4% and China’s share (red) dropped to 3.6%. So they’re not the ones that are bailing out the US government:

Other big foreign holders don’t measure up to the task. Not so ironically, most of the 10 biggest foreign holders after Japan & China are tax havens and financial centers, some of them small countries that cater to US corporations that want offshore mailbox entities where some of their Treasury holdings are registered.

The UK’s “London Laundromat”: $647 billion, about 2.2% of the total US debt outstanding, and growing rapidly, up 47% from a year ago. The Number 3 foreign holder of US Treasury securities is concentrated on London’s financial center, lovingly called, “London Laundromat,” holds $647 billion in Treasury securities. The ultimate holders of these Treasuries registered at accounts in the London Laundromat could be anything from Russian oligarchs to US corporations.

The top 10 foreign holders behind Japan and China:

- UK (London financial center): $647 billion (+47% year-over-year)

- Ireland: $334 billion (+5% year-over-year)

- Luxembourg: $323 billion (+12%)

- Switzerland: $288 billion (+13%)

- Belgium (home of Euroclear): $272 billion (+7%)

- Cayman Islands: $262 billion (+17%)

- Taiwan: $251 billion (+7%).

- Brazil: $244 billion (-5%)

- Hong Kong: $226 billion (+0.5%)

- France: $224 billion (+101%)

But big trade deficits don’t mean those countries have to hold a lot of Treasury securities: Germany and Mexico, the two countries outside China and Japan with which the US has had gigantic trade deficits for years, hold only $83 billion and $46 billion respectively in Treasury securities.

Domestic creditors of the US government.

US government “internal” holdings: $6.47 trillion, a record, up by $327 billion (+5.3%) year over year, and up by $461 billion (+7.7%) from March 2020, according to Treasury Department data (blue line, left scale).

US government pension funds for military personnel and federal civilian employees, the US Social Security Trust Fund, and other federal government funds invest their massive balances exclusively in Treasury securities. This “debt held internally” is often and ridiculously described as debt that the government “owes itself”; but that’s malarkey. It’s owed to current and future beneficiaries of those funds.

But even this increase couldn’t keep up with the incredibly spiking US national debt, and the share of the US Treasuries held by these funds, at 21.9%, remained near the multi-decade low of the prior quarter, and was down from a share of 45% in 2008 (red line, right scale):

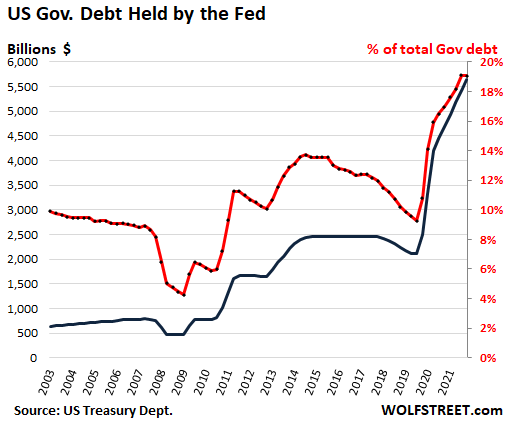

Federal Reserve: $5.65 trillion at the end of December, up by nearly $1 trillion (+20%) year-over-year, and up by a gargantuan $2.31 trillion (+69%) from March 2020, the result of the most reckless money-printing binge ever (blue line, left scale).

The Fed’s holdings of Treasury securities reached a record 19.1% of the incredibly spiking US national debt in Q3 and held at that record in Q4 (red line, right scale):

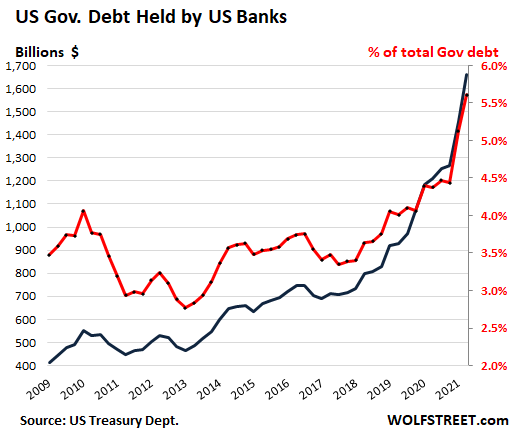

US Banks: $1.66 Trillion, according to the Federal Reserve Board of Governors’ data on bank balance sheets. This was up by $450 billion (+37%) year-over-year and by $690 billion (+71%) from March 2020, as banks, loaded up with cash, are gorging on Treasury securities. They now hold 5.6% of the incredibly spiking US national debt:

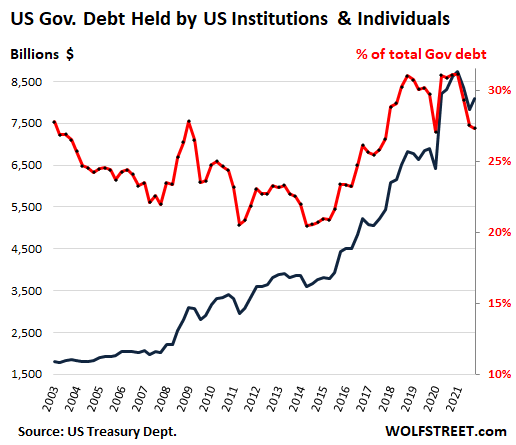

Other US institutional and individual investors: $8.09 Trillion, down by $522 billion (-6.1%) year-over-year but up a whopping $1.68 trillion (+26%) from March 2020.

These include bond mutual funds and money market funds, US pension funds, individual investors, US insurance companies, state and local governments, and other US entities. The sharp volatility of these holdings indicates that some groups dumped Treasuries in March 2020, and then, when the Fed made clear that it’s going hog-wild, they jumped back into the Treasury market and bought everything in sight. Their holdings hit a peak in Q1 2021. Since then, they backed off.

In summary: the major holders the incredibly spiking US National Debt:

And the incredibly spiking US national debt itself:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Well, I am certainly not holding or buying any of these certificates of confiscation!

Wes,

The problem though, is that many (most/all?) other assets’ value is directly impacted by the Fed’s interest rate manipulation (downward for last 20 yrs at least).

Here is why –

1) Essentially all professional investors and institutional investors are going to (at a minimum) weigh the value of an asset/investment against its projected future income stream, discounted to the present by an *interest rate*

This is the famous Discounted Cashflow Formula (DCF)

2) And a lot of professional investors are going to use the DCF to more than weigh values…they will expend a ton of analytical energy doing highly detailed DCF analyses for explicit valuation purposes

3) The problem? Every DCF valuation (by mathematical definition) is profoundly impacted by the interest rate used. Lower interest rates (by definition) spike asset valuations (because future asset income streams are less heavily discounted to present).

4) And guess what the Fed has been f*cking with for 20 years? Interest rates, (downward) by printing money.

5) This is precisely why almost every asset class is overvalued…because the Fed has artificially manipulated interest rates downward.

6) The problem? All these asset classes’ value has become more and more “anchored”/correlated to nothing other than these artificially low interest rates (as opposed to their own internal pros/cons financially).

7) As assets’ values become less and less responsive to their own internal financial prospects (and more responsive only to manipulated interest rates) these assets become more and more vulnerable/volatile to changes in gvt interest rate manipulation policies.

8) And the Fed is no god emperor with access to infinite free lunches…ultimately its interest rate manipulation (via money printing) is constrained by other macroeconomic factors (like turning its fiat into toilet paper).

9) So when the Fed is compelled to let interest rates freely float (upwards) asset values collapse (see above).

Adding to all your good points is the fact the FED has officially turned the corner to being fully MMT-based. By the time the FED pushes the funds rate to towards 3%, there’s a very good chance our economy will be ready to enter the next recession. At which point, the FED will immediately slash the funds rate back to .25% and restart QE. The government will step in with more rent & mortgage forbearance, and the craziness will start all over again. Raising rates is the easy part.

Unwinding all the MBS and enough treasuries to get the FED’s balance sheet down to a reasonable level of $3-4T is the hard part, and I don’t foresee the FED successfully maneuvering a soft landing with regards to its balance sheet.

There’s just too much money to be absorbed by the system when we’ll be running $1-1.5T annual deficits for the foreseeable future.

Simple. It is a balloon. Now that they have stretched the limits of the financial system to the new MAX. It can deflate a little but will only grow from here. $30T today $40T in two years. They can’t escape the easy money

Why is $3-4T considered reasonable? Before 2008, I think the “reasonable” amount was much lower, wasn’t it?

“ 6) The problem? All these asset classes’ value has become more and more “anchored”/correlated to nothing other than these artificially low interest rates (as opposed to their own internal pros/cons financially).”

cas,

Generally agree with all…

However, we can’t quantify for FOMO, panic, mania, herd mentality, casino/gambling mindset, and just sheer stupidity…

In todays world, if you can think past next month, you qualify for Mensa…

Don’t disagree it is a casino, but the Fed heavily, heavily influences probably the primary macroeconomic variable that determines the environment the casino exists in (interest rates)

cas127:

Yes, the Fed has been fiddling with the price of money (interest rates) for a long time.

Without knowing the true price of money, the market has no idea what is the real price of assets.

The danger is someday the market might discover, too late, the real price of assets.

That is why I think we are in some rype of crack-up boom, but just don’t know it yet.

Don’t limit your estimate of future value to only interest rates. Use real expectation value to include interest or income cash flow value, inflation loss or gain, and risk loss.

Perhaps financial instruments are too limiting. Commodities, recyclables, distributed utilities. And small companies, although targeted for destruction by the government, can still return disproportionally if filling a niche for honest services abandoned by big businesses.

Of course for max profit, service the MIC, preferably intel services.

The problem is as badly priced as US treasuries appear, when you look at Hussman’s and Grantham’s long term return projections they are competing with all other US choices including stocks, cash, corporate bonds. If you believe in reversion to the mean the best places to invest is outside the US especially when dollar is strong.

It’s not just believing in reversion to the mean.

It’s also a question of believing in something for nothing which is the biggest possible lie in economics and finance.

It’s possible for one segment of the population to plunder another if the plunder is limited. That’s what governments have done since the beginning and what exists under populist democracy.

The current plunder (through income transfer payments and negative interest rates) is growing exponentially over time.

It isn’t sustainable.

AF: I can see locally the impact of transfer of wealth. The local economy is harvested and sent out to Wall Street. Road Bond is replacing Parasitic local Gov’t feeds on what remains and talk about affordable housing. The electorate that’s harvested however does not give a shit if gas is cheap. Gas ain’t cheap. On top of high gas prices Gov’t shit in its mess kit by removing the baby sitting/ youth warehousing that in person public education offers. I over heard two very nicely dressed and articulate ladies go medieval on this subject at a local over priced bistro.Red pills and blue pill are pissed off and it ain’t transitory.

If you believe in reversion to the mean you buy treasuries now and when inflation reverts to 2% you have a positive real rate of return.

Old School

“Reversion to the mean” is a powerful gravitational theory, for sure.

The problem I always find with it, though, is WHICH mean: 3 months?, 3 years?, 3 decades?

This is especially important when considering the Fed which a) has been around for over 100 years, and b) has shape-shifted into a larger and more omnipotent agency each decade.

It’s powers have grown after each decade, especially grown after each crisis: WWI, Great Depression, WWII, Korean Conflict, end of Bretton Woods, 1970’s Inflation Spiral, major market corrections of ‘74, ‘87, ‘00, ‘09.

More insidiously, consider all of the financial crises related to the huge systemic debt build of the last 40 years. Systemic debt (gov’t/household/corp/fin’l) has grown from under 150% to over 300% of GDP from 1960, and probably is much higher than that if all the debt in the “shadows” is included.

Through these crises the magnitude of the balance sheet and the powers to act granted to the Federal Reserve System have gradually and dramatically grown, all in the name of “stabilizing” the system.

A return to the debt/GDP number of 134%* of 1960 will be one hell of a reversion!

___________

* McKinsey Institute, Debt and Deleveraging, 2010, p.54

Foreign value stocks may not decline as much as US stocks, but that does not mean they will go up. I think Wolf has laid out the case that US stocks are headed south (albeit an extremely turbulent ride – Wolf’s airplane analogy of hitting downdrafts with sudden upbursts is dead on). The fastest capital appreciation is likely to be on the downside with SRTY and SQQQ before we hit bottom.

Get back into cash after the major downlegs and get back in on the rallies. You will stay way ahead of inflation. Don’t get greedy.

Have you checked to see what retirement funds of businesses, educational institutions, etc. where you have worked are holding? You know – the ones that you expect will be sending you money some day. I’d guess you’ve seen articles about Orange County, most of Illinois, etc. not being able to pay retirees what they had promised. With the current levels of interest it’s going to get worse, especially if the stock market goes down like it should.

Foreign holders are still net buying this evaporating asset, incredible. Hats off to the power and influence of US Govt. and military.

Cleanest dirty shirt, their own country assets are evaporating even faster

It’s indeed a matter of the cleanest dirty shirt, at least that’s my opinion. As a European I diversified my portfolio by holding US cash, some treasuries and some US equities. Do I like the dollar? Not particularly, but exposure to euros alone is neither what I like.

Speaking of dirty shirts: Bitcoin now 39, 800.

Clumsy old barbaric relic: Gold 1895.

So we’ve known for years that BC is not and can never be a currency ( max speed 7 transactions per second) so then came the fall- back marketing plan: ‘a store of value.’

Wonder how the guys who stored at 60+ K are feeling. But most ‘participants’ actually didn’t. Bitwise reviewed about 80 exchanges and found the vast majority of the action was ‘wash trading’ the same guys buying and selling, moving coins back and forth to create the illusion of a market.

“Cleanest dirty shirt”

An economic Dark Ages, descended over the entire world.

Authored by political neo-feudalists.

One rationale: the negative return on US instruments is an insurance fee. I hold depreciating dollars because, if things dip at a WTF-steepness into a Recession/Depression, dollars are still king. And I owe my liabilities in them. So do plenty of others, as it is the dominant currency in international deals.

The relative awfulness of governance in other parts of the world supports the “best house on a bad block,” “cleanest shirt” idea. Look at Russia, about to pull a mid-20th century style heist. Look at the Ruble. China meddling top-down with its system is not helping them there. Love the “London Laundromat” phrase. Back at Brexit vote time I mused the UK might become a lot more like its tax havens.

And, we are the captive holders, strapped in the seats to see if our pensions survive. Everybody, banks, etc., is captive to this system — is this what the Defi folks are raving about? There is no “outside” anymore on this tiny planet. None for our trash and emissions and none for our assets. Escape is a pipe dream.

“Cleanest dirty shirt, their own country assets are evaporating even faster”

That’s not necessarily true anymore though, certainly not in 2022. I used to agree with this and be a firm subscriber of the cleanest dirty shirt theory but again, I feel like that’s a lot more tenuous argument now and perceptions are way behind events, unfolded with unexpected rapidity in the last 2 years. Wolf’s charts have been having the WTF label so much because the US fiscal and monetary environment has deteriorated into a mess much faster than probably anyone expected, so the old assumptions can’t be counted on so easily. I think it’s more like there’s no obvious safe haven, but that just means broad diversification is more important than ever. And I don’t mean crypto or bubble real estate or the Nasdaq super-bubble 2.0–things like reliable commodities (which are about as sure a storehouse of value as anything) and, yes some level of metals (you don’t have to be a gold bug to consider it smart to balance the portfolio with them).

As for cash and bonds, even there, it’s not so easy to make the cleanest dirty shirt case for the US anymore. Besides the small players that can help to round out a currency basket (won, franc, forint), for all the flak it gets, the EU finances look to be in better shape now, with far less debt and fewer obligations. The structural mess with the PIGS poses a challenge but right now, AFAIK the US debt to production ratio is even worse than Italy–that again is a very recent development and perceptions haven’t caught up. And our cost curve in the next few years is worse because we’re still trying to fill the shoes of the 21st century Rome. (Besides our higher healthcare costs, the war burdens are still staggering–the Iraq, Syrian and Afghan wars are still draining our treasury with all the veterans’ costs and some ongoing deployments for no obvious security value, if anything the Iraq War made things worse and cost us trillions.) And while I’m no fan of China or their system, they’ve handled some recent crises objectively better than we have, we’re now approaching 1M COVID deaths while China’s had it under relative control. As for Evergrande–wasn’t the point that China *didn’t* do what we did in 2008 (ie. China’s at least making actual efforts to make the fleecers pay up rather than blindly bailing them out)? Not in way saying they’re a model or that the RMB is on more solid ground, it’s just that it’s harder to make the case that the US obviously has the most effective working model of govt. or financial management anymore. Thus undermines the cleanest dirty shirt theory. Other than some smaller economies with better managed systems I’m not sure anyone really has a clean shirt, but again that’s why more diversification is the rule of the day, and this over the medium term probably doesn’t bode well for US treasuries, certainly not with inflation like this.

‘or that the RMB is on more solid ground’

It isn’t on any solid ground. It isn’t money outside Russia except in a few failed states/satellites like Belarus. In the last ruble crisis (2014- 16) it lost 50 % of its value. No one in Russia keeps rubles as a store of value.

RMB is definitely not on a more solid ground. Unless we want to take into the account the amount of physical gold China is holding.

On the other hand, China is definitely on a very shaky sandy ground. It has too many internal and external issues to contend with. Besides, it has to deal with all the inherent flaws that comes with a totalitarian system.

China is spending a massive amount of its budgets on maintaining internal security. Freedom is only what the Communists Party allows you to do and may change at any given moment. The people are under extreme pressure and there’s no real stability and assurance for the future. It is like a crock pot pressurized and waiting to blow.

China’s internal debt situation is also very serious. Evergrande is only the tip of the icebergs as they say. They are trying very hard to have a “soft landing” or “soft bursting” of the bubble, but that’s not very likely.

Internationally, China has made enemies everywhere, especially among its neighbors. India, Vietnam, the Philippines, Taiwan, Japan, Australia, US, etc….is forming an alliance against China. China is being isolated with only Russia as half a friend.

So the US maybe coming down from its high and mighty horse, but Communist China does not have a bright future ahead of it as well. It’s repressive and oppressive totalitarian regime and system has to fall some time in the future, sooner than later.

In the aggregate, non-US entities must accumulate USD assets as long as they collectively run trade surpluses with the US. It’s math.

As to owning Treasuries versus another asset (class), it’s not like there are many compelling alternatives.

The one that makes the most sense would be hoarding commodities since it at least has practical usage as opposed to choosing another asset inflated by the mania.

But if that were to happen on any large scale, prices would explode into the stratosphere with substantial “knock-on” effects.

How about obtaining land that can produce food and build a community that can be self-sufficient as much as possible? Food will be the ultimate commodity and will always be needed. Owning land and owning means of production of food would be a good investment for the real long term.

Why are we, the “People”, not provided with a list of the individuals and companies to whom we owe this money?

I would like the names from the off-shore accounts.

Why the secrecy?

Not sure who’s holding it, but I sure know who’s holding the bag.

Yes, we are!

Bankrupt republic

And our children and grandchildren and their children, too.

Wolf is right. It’s a tragic clown show.

Perhaps this will all just turn out fine.

The mathematical probability isn’t zero. :)

The Fed has surely been off its lithium.

…making too much money selling the pills to Tesla….

Mister Market is raving and dancing wretchedly. My hedges are holding but barely, engines overheating and puffing like a Star Trek scene ….

“Fed Eyeing Potential for Faster Rate Increases to Ease Inflation” (WSJ)

LOL, give us a break! Now I know why they are called ‘minutes’.

“The question is particularly hot because these are very unattractive instruments”. I guess this is relative. If you believe the stock market is going to continue to go down and housing is in a bubble this may be the best of the unattractive instruments there is.

Bitcoin anybody?

Far worse than UST.

It’s literally nothing. At least with USD is required for US taxes and USD debt servicing. Also a lot of demand from doing business with or paying for services provided by US government entities.

Bitcoin showing its colors for now: a meme asset, rave baby, runs at the first sign of trouble. Just another glittering nothing-unit in the sky. Oh yeah, value for traffickers.

It is an electronic entry in some computer somewhere.

It’s value is ONLY based on what the next person will trade paper currency for.

Wow.

If the computer goes down, what then? If there is a Solar Flaire, then what?

If the Gov orders the shutting of the internet to stop the Trucker’s, then what?

Bitcoin? Sure, US government is just begging to be extorted by a bunch of geeks. Oh, we’re too indispensable to the financial system now give us your dollars for our fancy numbers. Or else!

Bitcoin (and other cryptos) need to become a currency, i.e. owner should be able to go to supermarket nearby and buy groceries with it. Without having to pass through any BTC/USD exchanges that government can choke off at will whenever it wants to.

That would be true for “cash,” such as Treasury bills with maturities of up to 1 year.

But if you buy a 10-year, you get 2% for 10 years, and if you sell a year from now when market yields are 4% or higher, you’ll lose money.

At 4% yields next year stocks are sure to be flat to lower. So which investment has the larger downside? 2% and your capital after ten years against a possible 100% loss. The strategy in a rising rate environment is to ladder up. Assume the possibility of yields being 1%, is the same as 4%, (a 50% loss is a 100% gain) Call it 50/50. Laddering up means you keep most of your cash in short term liquid accounts, maybe FRN to capture the rise at the short end of curve. Should rates drop, buy TIP bonds.

“More money has been lost reaching for yield than at the point of a gun” Raymond F. DeVoe, Jr., of Legg Mason Wood Walker Inc., in February 1995

A.I.

Today debt will be nothing tomorrow with the accumulated inflation.

US gov finance itself with minus 5% interest rate.

Agreed. US government is having a heyday borrowing at these ultra low rates.

If someone offered you money at negative rates, wouldn’t you take it?

Yes, but it’s an unsustainable policy. Like saving money by cutting back feeding your mule. He eventually will not pull the plow.

Innovations will bear inflation.

Meh….

Personally, I’m about innovated out…

Yep if they’re not bought out too quickly by the monopolies, or stifled by tons of paperwork and restrictions that are required due to the oligarchs lobbying for barriers to entry that prevent competition, unless you’re already rich.

Accountants and lawyers cost a lot of money. Building a business up from the ground ain’t what it used to be

Very interesting overview.

It clearly shows that the often heard narrative of foreigners bailing the US out doesn’t hold. By far the biggest bag holders are savers and (future) pensioners. And that last group seems to be ignorant about this fact!

This should also put to rest the idea that you can “inflate away” the debt, because it is simply a big transfer (steal) out of savings and (future) pensions. Of course the MSM would never point that out!

This blog should be mandatory curriculum for kids.

Yes, but start with basic interest rate education, the categorical imperitive

You want to start with Immanuel Kant?

Yes I thought it was appropriate.;>)

Gimme Fed Cant.

I’ve always looked at the categorical imperative as a long-winded version of the Golden Rule. ;-)

You could start the kids off with “Actually, there are 2 Golden Rules”:

1) Treat others as you’d like them to treat you.

2) Whoever has the gold, makes the rules…

I would only add one more MG:

No matter if the language of ancient societies in USA ” early peoples ” or european, middle and farther eastern/SE or asian, the message is the same:

”As you sow, so shall you reap.”

What goes around comes around…

etc., etc.

May the GREAT SPIRITS in all of their names, etc., BLESS us all!!!

Seems like WE the PEONs really and truly need some help from the Great Spirits these days, eh

In spite of all those words of clear wisdom,,, I still like, ”Act such that you can at the same time wish your act is universal.”

What a challenge, hey whot??

They would need to learn basic reading comprehension and basic arithmetic and number sense first.

It was me. I bought all that. And I’m laughing all the way to the bank, but then, I’m also laughing all the way to bathroom.

I knew it was you!

“The whole thing is a tragic clown-show” …….

Anybody else out there find it incredible that these Fed arsonists still intend to pour gasoline on the fire they lit , all the way until their March meeting? Then they expect to change into their “fireman” outfits, and go on TV and tell us what a great job they’re doing in putting out the fire they lit.

Anybody else out there that would love to see a second party emerge in the USA , in addition to the War Party Of The Rich multi-miilionaires ?

One that would eliminate this group of predators from power, eliminate their criminal Fed, and investigate jail time for all the Fed criminals that pulled this theft off?

Well at least wait until they adopt some ethics boundaries. Then I suppose they’re off to Tahiti with the loot.

Who bought the bonds is not important.

What was done with the money gained from selling Treasury bills, notes and bonds is important.

Interest expense on the debt is important, since the debt will never be repaid.

The effect of rising interest rates on the debt is important too.

Richard

“Interest expense on the debt is important,”

Indeed.

The interest on NEW debt should have a cost that is discouraging to reckless spending.

Only new debt will carry the cost of higher interest rates.

The debt will be repaid indirectly through lower future living standards, mostly for Americans.

It’s already been happening somewhat for the last 20 years. The explosion in the national debt since 2000 (5X increase) and concurrent flatlining of real US median household income and net worth.

It’s not a coincidence.

Over half the US population is feeding to some extent at the public trough. Without these subsidies, much of the supposed “middle class” would be evident for what they actually are economically, the working class or working poor.

There is never something for nothing.

So the Fed forcing lowest lowball interest rates and asset inflation has sucked big money out of Social Security funds, which can only invest in pissant Treasuries.

The resulting windfall profits of asset inflation go into pockets of the richest people, along with their windfall tax reductions.

And the same political forces that enabled this huge widening of the wealth gap between rich and poor, will be raging about how bad and evil government is to “waste money” on Social Security.

SS purchases special notes, not garden variety treasuries.

Still, the result is similar: SS funds consist of a drawer full of federal IOUs.

Thank you Reagan and Greenspan for diverting SS funds to the general fund.

Michael Gorback,

“SS funds consist of a drawer full of federal IOUs.”

Hahaha, yes, just like my treasurydirect.gov account — same thing, I even have some “non-marketable” securities in it, similar to the securities that SS invests in, namely I-bonds.

Except, neither my account nor the SS Trust Fund is a “drawer” full of paper, but electronic records on a server. Just like your brokerage account or your bank account. Modern times :-]

But more seriously, you’re very right: SS should be set up as a stand-alone fund that is off-budget, with all SS revenues going into the Fund off budget and all payouts coming out of the fund off budget. So the SS receipts wouldn’t show up as tax receipts and the SS outlays wouldn’t show up as US outlays. If and when in the future the Trust Fund is depleted, if SS doesn’t get tweaked, and the outlays are a tad larger than the receipts, the government can supplement the receipts, and the supplement amount would then show up as outlays on the US budget. That’s how it should have been done from get-go.

I’d like to see the same for Medicare. They need to be stand-alone units whose receipts and outlays are off budget, and only amounts supplemented by the US government, if receipts are not enough, show up on the budget.

Stand-alone units would also make it easier to issue timely monthly and quarterly reports that are meaningful and show us what is going on — instead of hiding the whole thing in the budget.

Splitting SS off from the rest of the government, like Fannie Mae or the Postal Service or the Federal Reserve, does make a lot of sense.

But then the debt of the rest of the government would look much worse! The underlying Fed Gov would have to show more debt due to owing to the SS trust fund, and it would also be supported by substantially less tax revenue. The debt/revenue picture for the Fed Gov would be a lot bleaker.

SS was a standalone until Reagan and Greenspan concocted the current scheme, which siphons off FICA income into the general fund. In addition they increased FICA taxes to create a SS fund “surplus”. What they pulled off in 1983 was a tax increase on Main Street,, channeled into the general fund to cover up the decrease in taxes on the rich. I read somewhere that it transfered about $2.5 trillion.

Just another wealth transfer. Nothing to see, move along.

And gimme a break on the drawer thing. I’ve seen the drawer. All it contains is a url and username/password written on a piece of paper.

That’s why we should have never trusted the government with “social security” to begin with. The creation of the Social Security only expanded the power and reach of the federal government and did not truly benefit the general public in the long run.

“$5.65 trillion at the end of December, up by nearly $1 trillion (+20%) year-over-year, and up by a gargantuan $2.31 trillion (+69%) from March 2020, the result of the most reckless money-printing binge ever ….The Fed’s holdings of Treasury securities reached a record 19.1% of the incredibly spiking US national debt”

And Powell said “The government doesnt have any problem borrowing at these low rates.” I think they call comments like that “intellectual dishonesty”. The FED is the lender! What a scam.

Debt jubilees and tyranny conundrums.

So who is going to soak up all the budget deficits when the Fed (red) stops purchasing in March …and Fed even thinks they can start selling off their accumulated treasury holdings…again to who?

jimbo,

Yields will rise until there are enough buyers. Yield fixes demand issues. If the yield rises enough, I will be a buyer.

There WILL be higher yields, meaning higher interest rates and higher cost of funding, and higher mortgage rates, etc. That’s what rate hikes and QT are all about.

And recessions

Debt jubilees and tyranny conundrums.

In general, people don’t seem to mind that they don’t understand the interest rate manipulations. If you’re committing the crime you want to at least pretend not to know about it, but when it’s happening to you you in a negatively way, you should understand it. It is the major variable causing the gap between the wealthy and the poor.

In fact many embrace socialism/ communism as the answer. However, Justice balance scales are not just 2 dimensional. Debt jubilees, tyranny, socialism, capitalism etc…there s a lot to consider. Where is the puck going to be?

Me.

Oh, you have not been voted in yet for another term. You are in LIMBO!

February 04, 2022

Federal Reserve Board names Jerome H. Powell as Chair Pro Tempore, pending Senate confirmation to a second term as Chair of the Board of Governors

No news on the topic since. Hmmm.

It is interesting to me that (according to the graph) the percent of US Government Debt held by the Fed was lower at the end of QT in 2019 than in 2003 -2005. I hadn’t realized the Balance Sheet drawdown had been that effective.

They did a big runoff so it wouldn’t look as bad when they did the next big hockey stick move.

That’s not a measure of effectiveness. The national debt just increased at a faster rate.

The FRB’s balance sheet was still much larger as a percent of GDP in 2019 than in 2005.

Interesting, we are only about 5% of points higher now than we were in 2014 five years after the banks got ALL the money.

Just goes to show you, they gave the banks a lot of money both times, just some extra during the pandemic QE for their best customers.

SpencerG,

As August Frost pointed out: There are two parts to that ratio, and both happened:

1. the US debt soared during that time (2018/2019).

2. The Fed’s Treasury holdings declined during that time.

Yeah. Thanks to both him and you for making that clear. I am still a bit surprised because of the Negative Nellies who claim that the Fed achieved very little with that effort… but your points put it in some perspective.

When you see the list of top foreign holders, one feels revolted.

The City and a string of tax havens. What a filthy, corrupt mess the USA presides over.

Humanity can do a lot better than this “leadership”.

You first to the barricades and trenches! I’ll be right behind you. (No, I’ll be at home eating my allotment of soylent green.)

If anyone wants to start a piece of software to coordinate government policy and replace government with grassroots democracy, be my guest. It would have to bubble-up issues based on the population’s ranking, provide for informed discussion of and layout of alternative courses of action, and provide for voting.

I really think something like this could operate both at the institutional and governmental level and would reduce/eliminate the disconnect between population and government action.

agree totally ivan:

First and foremost, return to ”Local” over ”regional/state over multiregional/nation over ”global” as it clearly was for thousands of years, in reality if not in the fantasies of writers of propaganda, etc., which continues to this day.

One of the first things is to make ”time” local by SUNTIME,,, while keeping the only,,,

ONLY other time what is now called zulu time,,, FKA GMT or global mean time,,, and formerly to that, Greenwhich Mean Time.

These last three are what the world really runs on, no matter the incredible continuation of ”time zones” and other such anachronisims.

In spite of it all,,, time continues to be just one more of the ”agreements” that have allowed our species to progress in certain ways, while absolutely limiting or completely denying progress in other ways.

Time and enough to move on, eh

I use Scotties ultra soft US Treasury debt rolls in my bathrooms.

About as WTF as it gets.

I hold about 15% of my net worth in money market and bank accounts. Am not sure why I think it is secure, in as much as inflation takes big bites out of it.

Years ago I bought long term BBB bonds at 5-6% yield on cost. They lose compared to 7.5% inflation, but they lose less quickly than cash. The Ark Innovation ETF is down more than 50% in about a year. It was one of the best performing ETF’s the year before.

How fast do you want to bleed? 7-9% per year for years or 50% per year in a stock meltdown like ARKK?

I know people are gloating over ARKK’s 50% drop from its all time high (about 1 year ago this month it peaked), but if you bought it in 2019, you’d be up from $45 to $68 for a 50% gain over 3 years. That’s not crap performance in my experience, which is based on almost 40 years of investing. Way before GameSpot, AME, and Robinhood a 50% gain over 3 years in the past marked you as a good investor.

Time in the market is more important than timing the market. My buys are usually with a time to hold of at least 3 years, usually 5 if it’s a startup with a long runway. That’s what’s hurting the ARKK stocks. Many have bright prospects but have long runways they might need to raise more funds. With the possibility of higher rates that runway gets more expensive. Scary talk about 0.5% rate hikes is disproportionately driving ARKK down. BTW, not an ARKK owner but I own some of the same stocks.

Long term I worry more about the dollar. Get your cash out of the system, whether crypto, gold, land, art, or a warehouse full of copper (but not a warehouse owned by Jon Corzine or anywhere in China).

A loss of confidence in the dollar would have much more profound effects. Cash in the bank is also the easiest target for confiscation.

For the truly paranoid, think about gold confiscation and get your gold offshore to one of the many gold banks where you will have allocated gold and can trade on their platform. The US can’t confiscate that gold, as the banks will usually not allow physical delivery. They’ll liquidate your gold and deposit the proceeds to your US bank account.

Crypto in cold storage. Hard to confiscate. Even in a wallet no one is getting it without that string of characters you taped under your desk along with your other passwords. /sarc off

As a hedge I do keep some gold in off shore bullion banks. I also keep a physical cash stash not located on my residential property in case the ATMs go dark. Sometimes paranoia is a good defense strategy. You might lose money to inflation and/or gold storage fees but I think of it as insurance premiums.

Crypto only exists if the electricity stays on.

What’s to prevent the US government from making a deal with the Government(s) of the country where you have your gold stored? What is to prevent ANY government for creating a “Mandate” where you are required to be injected with a solution….oh, sorry, wrong blog…….where you are required to turn in your gold?………….or your account has a “2 week Lock-Down”…just saying……

There is nothing to stop a Government from declaring buying and selling GOLD to be “terrorism”. Sure, you can own it, but it is illegal to transfer it without a Photo ID, 10 day waiting period, back-ground check, and One Ounce a month limit……………(gee, where have I heard this before?)

10 ounces will be legal, but a 30 round roll of Maple Leaves is an assault vault…………..

No. Never. This could never happen here.

Maybe a “Gold Passport”?

We are not seeing the beginning of oppression. “They” have been working on this for decades, if not centuries. We are seeing the end results and consolidation.

Just a matter of time before the government says enough of this non-government managed/run digital money. And that will be an ugly run on the banks. It would have to be done softly to blunt the blow. Approximately $2T in digital currencies is what it was recently but with unprecedented price volatility it is difficult to guess the value on any given day

$2T in crypto versus an alleged $600T in ”derivatives” equally guesstimated amounts???

gold, silver, etc., of completely unknown amounts

guns, bullets, bombs, etc., equally unknown how much or where

etc., etc…

”Eat, Drink, and be Merry” for tomorrow we dine.

You just have to know a little bit of history to know government starts getting oppressive when they get in financial trouble. In general I would say government officials see the wealth in the country as their own and when in trouble will pass laws or invoke emergency powers to fleece you.

For an individual you have to try to not be late to the exit door.

Having said that, countries usually ally with big business and a person having some assets in the big corporate backbone of a nation will survive most situations even better than government debt. Gold always survives if you can keep it

You think the US can really do that? Play whack-a-mole with the Caymans or the Channel Islands to grab your bullion vault gold?

What about mutual funds that are backed by physical? Even after FDR confiscated gold you could still own shares of Homestake Mining. De-list Barrick?

Do you think the people who operate these businesses are powerless wimps? HSBC holds bullion for the GLD fund. The largest non-governmental holder of gold is the IMF, with 189 member nations. George Soros, David Einhorn, John Paulsen, Stanley Druckenmiller – all have bought and sold gold.

They can try to limit amounts to 1 oz but how are they going to stop you from buying or selling 30 oz privately? You and I could transact that at a neighborhood barbecue.

Do you know what that is? Freedom. Governments hate privacy.

Same with crypto. Do you think Elon Musk, Mark Cuban, JPM, USAA, Ally and Goldman will just lie down and let the government control crypto?

What else disappears when the electricity is off? Is it just crypto?

Your money and credit only exist if the electricity stays on, other than any paper currency you might have stashed. ATMs and credit card readers don’t run on dilithium crystals. How about a Zelle payment?

You don’t have gasoline (electricity to run the pumps) or EV transportation if there’s no electricity.

Physical gold and silver don’t require electricity. Home grown food doesn’t either. And just to pre-empt the inevitable comment, neither do guns.

Don’t hide behind “they”. Provide names and motives.

The control of wealth has been being on for millennia. This isn’t a culmination of anything. It’s a continuation.

You better have food,water can’t eat gold

Can’t eat stocks, bonds, bank savings, real estate, FX, paper dollars, IOU’s nor bits/bytes, neither…

And food spoils, damn it.

Now what?

That applies right now, everywhere. If you have a house full of gold but no food, you starve. But I can see the point you’re trying to make.

Silver would be better for small transactions. Even at its peak around the GFC silver was only about $50/oz. I think that a few ounces might get you a few gallons at the pump.

The gas station might accept an ounce of silver but not a bag of rice.

If there’s no rice to be found and you have some, offer to pay with rice. You’re in barter country.

Gold is a different story. I can’t imagine standing there at the pump filing gold off a bar. Even a 1/10 oz bar costs about $250. Gold is for bulk storage in a very small package. Running for your life carrying 10 oz of gold worth about $20,000 is easy. $20,000 in silver weighs over 50 lbs.

You know what’s excellent for barter? Alcohol. Stock up on the little bottles so the customer can see they’re sealed. If you try selling out of a big opened bottle there will be suspicion about dilution. Vodka is best, because it also has survival uses. And it doesn’t go bad. Like silver, it’s bulky and low-density value-wise.

A bag of dry white rice can last years for nutrition but you have the same value density problem and once the bag is opened people will wonder what else has it been cut with? Moldy old rice?

Diversify your survival assets. Some of them will be both food and money.

In paragraph two you said “The question is particularly hot because these are very unattractive instruments”, and then explained why they’re so unattractive. So if these instruments are so unattractive, why do these people and organizations buy them? And if inflation continues to be well above the yields will they continue to buy and hold them?

“why do these people and organizations buy them? ”

Because the (USD denominated) alternatives are worse – badly overvalued due to artificial gutting of interest rates by DC for last 20 years.

(see my post near top for step wise explanation).

Being in USD, you can either get inflation eroded by 5% per yr or own something that might lose 50%+ in a week.

Most people prefer the former.

Plus there is the whole theory of duration matching. If need money tomorrow you better have it in cash. If you need money in five years you better have it in a five year secure instrument. If you need your money in thirty years stocks are the way to go.

The person actually buying it is mostly doing it with someone else’s money. It belongs to someone else.

This (financial intermediation) along with the asset mania explains why so much garbage exists and sells for such ridiculous prices.

Circle jerk.

Charles Hugh Smith recently wrote “…large-scale capital can borrow billions at 1% (lower than inflation) and then buy bonds yielding far more.”. How much of the Treasuries have been bought using this method? And what will the effect of rising interest rates have on these purchases?

Funds can borrow in the repo market at near 0% and invest in long-term securities. Done all the time by hedge funds, mortgage REITS, etc. And the leverage ratios can be big. But borrowing short-term to make highly leveraged long-term bets is very very risky, and it’s what caused the repo market blowout in late 2019 (by hedge funds and mortgage REITS).

You may recall that from 17 September 2019, the United States Federal Reserve injected massive amounts of liquidity into banks due to a quite abnormal situation on the repo market [1]. The repo market designates a mechanism used by banks to obtain short-term financing. Oct 28, 2019

The banks these days mostly LEND to the repo market to earn a little extra interest on their cash. And they did that back in 2019. And then they got worried about the hedge funds and the mortgage REITS borrowing in the repo market, and a few of the big banks then stopped lending to the repo market, and that’s when the whole thing blew up.

For additional detail…

On Monday, September 16, SOFR printed at 2.43 percent, 13 basis points higher than the previous business day. With pressures in the repo market spilling over into the fed funds market, the EFFR printed at 2.25 percent, 11 basis points above the Friday print and at the top of the FOMC’s target range. On September 17, the EFFR moved above the top of the target range to 2.3 percent and the SOFR increased to above 5 percent.

This is wrong, only mmf can use rrp to buy short dated treasuries. Institutions have to pay cash for long duration treasuries

Repos not reverse repos. And not involving the Fed.

Notice how many off-shore institutions hold these bonds? We don’t know who they are, nor the terms of their purchases.

Are they getting paid something more from the Central Banks? World Bank? IMF? Is there a “rebate” or income tax credit to the purchasing institution? A “Depreciation formula”? A Depletion Allowance as in Oil companies? Any Off-shore Tax credits for interest-inflation losses to be applied to your off-shore income?

Who says they are losing money?

What if these off-shore accounts are other central banks buying each others paper?

Is our own Fed loaning trillions to off-shore banks, who in tern, loan the credit to their large investors, who agree to buy the bonds?

We have no idea. Since none of this is based on the transfer of gold, there is nothing to stop any scheme. The “Banks” can issue credit any time, any where to anyone, and by the terms of their Charters, it is secret and can not be audited.

Can anyone provide some examples of possible doomsday scenario that would put this excessive debt as a risk to the US defaulting? Many have been saying this cannot go on forever (mostly since 2009) but it has been 12 years now and counting…

1) It isn’t so much outright default (since Fed happily prints money with one hand to buy other hand’s Treasury debt) as it is

2) the inevitable hidden or explicit inflation caused by said efforts to “avoid” default and

3) therefore temporarily immunize DC habitual and utter fiscal dysfunction.

With US fiat system the only default you need is with Fed monetizing the debt. It’s a soft default. It’s happening as we speak. You are getting back less real money than you loaned out.

Lacy Hunt has eloquent theory they are just getting the economy with non productive debt, therefore the ability to service the debt goes down therefore interest rates must stay low like Japan and Europe who have bigger debt servicing problems than US.

getting should be gutting.

“like Japan and Europe who have bigger debt servicing problems than US.”

Is that really true though (for Europe at least)? As of late Sept. 2021, EU national debt was about half that for the US national debt, with the USA then at around $24 trillion which of course has spiked up to $30 trillion in the few months since then as Wolf has been charting out–a much higher rate than EU or most other places, and United States might be around 2.5X the EU level now. Yes, there are structural issues specific to the usual suspects (PIGS) and not having a central budget authority for them, but the USA’s debt to production ratio AFAIK is now even worse than Italy’s which (at least until recently) was one of the worst laggards in the block.

So yes, the EU has debt servicing issues too, but the American challenges are on a greater scale now–this has only happened really in the past few years and I feel like the US obligations have swollen up so fast that perceptions still lag behind events. Plus the EU and most of its members are trade surplus countries. As for Japan, yes, their burden is higher but also structured very differently from ours (and it also seems to be following the new mercantile script with its trade surpluses). Seems like the US position is a lot more precarious than just 2 years ago, and with inflation at this level and no end in sight, IMHO either the yields have to surge a lot more to make our instruments worthwhile or the dollar as reserve currency is eroded bit by bit.

There is no EU national debt because the EU is not a country.

The national debt of the individual EU members varies widely. It’s not a problem in Germany and in a few others such as the Netherlands, yet.

It’s a problem in Italy and Greece.

The problem isn’t directly just a function of the outstanding debt but interest rates which in turn are based upon market perception.

The ECB has distorted interest rates through QE, even worse than the FRB.

At some point, either the debt will be federalized by the EU becoming a unified political entity or the financial system is going to “blow up” as the current arrangement isn’t sustainable.

My bet is that some countries will leave and the rest will form a United States of Europe, mostly the “core”.

My understanding is the EU has two problems that make it in worse shape than US:

1. Demographics

2. They have a different structured financial market more dependent on bank financing. US finances more through equity and bond market.

USA was printing and exporting dollars the moment WW2 ended. But we had such an incredible position (factories, not bombed, good healthy work force, sweetheart energy deals) it didn’t start being publicly discussed as ugly (outside of a few old school conservatives) until sometime in JFK’s reign I think. Started well down the slippery slope through LBJ, war on poverty and Vietnam paid with air-dollars. Hence the 1970s inflation. Deficits started ascent in Reagan 80s. And so on. The American broad public was cashing in and partying on our exorbitant printing privileges the moment Japan surrendered. Here we are.

Reagan and Greenspan changed our economic course from “tax and spend” to “borrow and spend”.

I’ll give you one.

The “doomsday scenario” is going to occur when the USD loses global currency reserve status or maybe loses any reserve status (such as that held by other currencies now).

This will happen at some point after the US loses its unipolar status as the world’s only superpower. It’s really one of two now, China being the other.

Loss of its current geopolitical position also eventually means the end of the Empire. Yes, the US is a modern empire, just different from the others read in history books.

No one (hardly) ever hears about this topic or thinks about it. It seems too far in the future, as if the current US led order will last “forever”.

That’s not going to happen. Britain held its leading role from about 1815-1914 or a century. The US led order might last another 23 years (to reach a century from 1945) but I consider it dubious. Despite its larger resources, the US is far more overextended geopolitically and the economic base to support this position has eroded noticeably.

We’re living in the twilight of the Anglo-American era.

Before or as this happens, I expect the asset mania to crash back to earth. The loosest credit conditions that go with it will also end, making it much more difficult and expensive for (practically) everyone to borrow, meaning that it won’t be possible for so many to live above their means.

The majority of Americans (and many others elsewhere) are destined to become poorer or a lot poorer over the indefinite future.

Surprising the think tanks haven’t already started planning better than they do now.

In the science fiction book “The Foundation” by Isaac Isaac Asimov- a physicist, future plans and outcomes were weighted logically, economically,psychologically, ethically, etc…using massive computer power. Decisive paths for the future were planned out for optimal survival and prosperity

Right now they just want to make sure they have the most guns and power/influence. We all are really quite primitive.

Scientism: a quasi-religious reverence for gizmos and their outputs. There is a time for guns and a time for probability distributions. The world is too complex to be captured or ‘computed” by any technology outside of wildly nonexistent sci-fi fantasy. Read Benoit Mandelbrot and/or Kurt Godel to begin to see why and how. Or watch Terminator for an intuitive illustration.

If the Fed had not done QE, where would the 10y and 30y and mortgage rates be. ?

Currently the Fed is still doing QE

Where will the above rates go if the Fed is no longer a buyer ?

Where will the above rates go if the Fed actually does QT.?

Where will real yields go without the Fed buying ?

There are different opinions on where rates would be, but it’s all counterfactual. If you look at 10 year rates vs. QE the results were not what the Fed said they would be.

I fully agree with your thesis that doomsday scenario is the loss of reserve currency status. I suspect it will happen after US will start and then lose major war (or at least fail to win it). Rabid warmongering going on in US give me feeling that this major war may be close.

Similar versions are mentioned in this space several times a week.

US Govt can never default. They can ask FED to keep printing. The effect would be devaluation of USD which is what we are seeing first had for last few decades.

Also, other CBs are also printing like crazy. So, USD is the cleanest among dirty currencies.

Doomsday to whom?

Those who anticipated our Great Depression, and got out of the market in time, held cash, re-bought later, did fine.

Those in Germany who owned gold, or had access to US Dollars during their hyperinflation did fantastic.

Doomsday to whom? You assume the Fed is not aware of what all this means. Why are they the “stupid” ones and we average people so smart? The US defaulting on their debt, or run-a-way inflation, just may be the goal and extremely beneficial for those in the know.

So, what should you know? Keep healthy, keep sane, keep going to work , keep married, keep your job, stay out of trouble, and only have enough cash in a bank to meet your expenses a few months ahead.

Own, with no debt, assets you are hiding (gold & silver and proven art).

OWE as much as you can on your home, etc., as long as you have a secure job or “income” so that you can benefit from high inflation. In 10 years your debt will be nothing to pay off. This is how “those in the know” in Germany, Venezuela, Zimbabwe, and now Turkey and Lebanon, ended up owning it all for pennies.

Have this discussion with your entire family. Tell them what you are doing. Make sure your spouse is in on it.

It can not go on forever, but it can go on for a long time. It is when it can no longer go on, that it stops. So ask yourself. Can this go on?

Can the FED really increase rates to significantly decrease inflation? No

Can “we” afford a stock market crash of 50%, or even 40% or even 30%? No.

Can any Pension fund survive with a 30% market crash? No.

Can America absorb 2+ million unknown people, from 100+ countries, with no skills, no money, no housing, no food, no health care, no clothes, no identification, etc., crossing our border, every year? No

Can Social Security continue as is? No

List every financial situation today? Can it continue as it has? You have your answer. It is going to snap any moment. Please be “5 years too early, than 5 minutes too late.”

Nice summary MA,,, been doing my best to communicate similar to family and some friends for eva; some have heard it and have understood and have acted accordingly.

Would be nice to be back on the farm in an area where ”dry farming” is the norm 9 years out of 10, with similarly inclined neighbors etc…

Fortunately, we older than boomer folks don’t have to worry about it for very long if at all…

Good Luck and God Bless!

Not sure about owing as much as you can on your home unless you are ok with moving out if things go south. Thirty years is a long time to have a secure income in one location.

‘Those who anticipated our Great Depression,’

Who would that be? It sure wasn’t the banksters, with almost ten thousand banks going under by 1934. The VP of the Wall Street exchange went BK and to jail. Charles E Mitchell was arrested twice in one day. The largest private dwelling in Canada went to the gov for taxes. The lender to the new Empire State building could have foreclosed but chose not to, because what would they do with it. It wouldn’t break even until 1954.

Obviously, the rich didn’t suffer like the middle class. As most people fell several rungs on the ladder, the lifestyle of the well- off

increasingly came to resemble what had been that of the middle class. Relatively they may have been better off. This was not because they anticipated the Crash.

3 times ten to the thirteen. Sweet Mother of Pearl Jam.

National debt -DOUBLED- in ten years. Incredible…

As toilets flush, things accelerate near the bottom of the bowl.

In a corrupted, destabilized system, ever more destabilizing tactics have to be used by the corrupt to “stabilize” the system.

And it will never go down. Only higher.

As the wealth disparity keeps growing….and when more than 50% on the population is on some type of government handout, more handouts will require as the majority will ask for more.

The politician who make those promises will be voted in.

What will be the national debt 10 years from now. My guess is at least $45 Trillion?

Wasn’t the history in Great Britain that when they got in financial trouble that they had to tax the rich so high, that the rich actually blew up their inherited estates to get out from under the tax burden.

Old,

Post WW II, the UK did have a lot of tax exiles *and* it was forced to do two large currency devaluations. WW II ended the Pound’s role as primary reserve currency, necessitating tax hikes and large currency adjustments.

But the aristocrats being forced to sell their estates really started to happen 50 to 75 years earlier – as the ending of agricultural tariffs allowed much, much cheaper foodstuffs to be imported into the UK…which put those aristocrats out of business (while keeping estate upkeep prices unaffected).

Get the Feds out of the money business.

I would be happy if only WE the PEONs could get the FED out of the ”monkey business” that they certainly appear to have been in since for eva,,, but most certainly most recently increasing every decade since WW2, as commented above…

Really quite shameful for ”old boys and girls” AKA owners of the world, to have let your employees at the FED AND the various and sundry political entities around the world do such evil deeds and so many, especially considering the clear lessons of 1216, 1315, 1789, etc., etc.

NOT GOOD,,, and no way in heck gonna end GOOD for the old money folks, AKA oligarchy,,, AKA ”Grandees”,,, AKA ”Peninsulares”,,, etc., etc..

Fair warning.

History repeats! When America had little debt we thrived. Our entire debt sits mostly on taxpayer shoulders. The last graph is why we should be on our politicians to be fiscally responsible. Instead, they are lining their coffers with outside money crashing the entire system. All roads are starting to lead to a Rome style downfall. Thanks Wolf. New to finance and you are an excellent teacher.

Gabby…

and the great enemy to your logic is the embracing of MMT….

“debt is good” nuevo economics

Agree with you….but I fear Powell has been corrupted….and perhaps his lack of economic education allowed him to be swayed.

Debt can be a good economic engine if throttled….now unthrottled.

The great flaw in our system is that those who allegedly oversee the Fed, Congress and its committees, are the profligate debt creators seeking fame and reelection.

Historicus…

Thank you for proving additional details, such as MMT, to add to the growing list of terms I am trying to understand. Looking into investments and fiscal policies in America is like untangling Grandmas 50 year old knitting stash. The Fed has such a big closet of old yarn skein’s it is a little overwhelming how knotted everything is.

Powell is a puppet look at what trump did to him = weak

Just as with individuals, national debt makes the cost of living more expensive. The massive increase in the past few years guarantees that the jobs will never return to America. The cost of doing business is too high.

WOLF- fantastic graphics, as always.

As long as the Fed stops QE next month and begins tapering thereafter, the world sees again that the cleanest dirty shirt at least does what they say they will do. It is a pause of the inevitable decline.

No danger of losing “reserve currency” status, so more of the “same ol’ same ol’ ”

It’s not doomsday, more like dooms-century.

Fed added $50 billion to their Open Market Account Holdings this week but not ta worry – it’s all gonna stop…soon…maybe later sooner…

wulfgartheberserker,

Quit posting this braindead manipulative BS. You keep doing the same shit over and over again. I’m getting tired of having to waste my time shooting down your BS.

The Fed has a weekly balance sheet, which goes UP and DOWN from week to week. In the week through Thursday, total assets went up $33 billion, after having gone DOWN in prior weeks, which you willfully ignored.

Over the past four weeks, total assets increased by $43 billion, down from $120 billion per four-week period during regular QE.

Your next comments containing this kind of manipulative BS will be auto-deleted.

Deep breaths Wolf. Breathe in the goodness. Hold for a few seconds and exhale the badness.

Repeat until the weird breathing makes you pass out. When you wake up go hug your wife. Or just go straight for the wife.

It’s your blog. If you think someone is screwing it up just delete the post. Not a fan of cancel culture but I’d rather see this kept off the general discussion. At least by taking the discussion offline you’d be showing more respect and discretion than the big social media. If you block them at least you tried.

After I don’t know how many years here I know some of your triggers and try to avoid them, so for me it’s sort of a self-cancel culture.

However, the readers like Good Wolf way more than Angry Wolf who steps out of character to use obscenities. Good Wolf won’t even use “Hell” on the beer mugs.

I think Angry Wolf should try to keep these issues off the threads. In this instance I don’t feel like I have any background to understand your extreme response.

If you disagree but can’t respond with a calm reasoned argument don’t let Angry Wolf take over with public insults and threats. Bad for business, and this is a business.

As you know I love and respect you but please for the Nth time I’m asking you to just let Good Wolf speak here. It’s what people come here for.

GO GET ’em WR!

your blog/site, your rules,,, and I am QUITE certain that I am not the only one who comes here BECAUSE of your ”moderation” efforts, NOT inspite of those efforts…

MG needs to go back and re watch 2 and a half people to see how it works out between ”good” and ”bad” Alan, and have a few more laughs at himself.

(disclaimer: my comments been moderated OFF more than once on here,,,LOL )

If people didn’t post so much absolute horseshit here, over and over and over and over, I don’t think you would see so much of Angry Wolf.

@ Vintage and Pea Sea. Believe me understand the stress of moderating this blog. The curating takes an immense amount of time and energy.

I’m simply saying that I don’t want it to bleed through into the the final product.

This is a business. The popularity of the blog is a result not only of its unique content but the moderation. An informative well-curated blog is rare.

However, when moderation – especially in a hostile form – contaminates content you’re hurting the business. All I’m saying is keep the moderation out of the content, behind the scenes.

Moderation is tough for this business structure. This isn’t Twitter where you can be shut down. You can block me or block my IP here and I can come back with a new name, email address, and hide my IP with a VPN, Tor, etc. I can torture Wolf 24/7. I can make him my special project.

Furthermore, if you humiliate someone on your blog guess what they’ll say about the blog in other forums?

One pissed off customer can cost you 10 or 100 new ones.

Better to take it outside and resolve differences in private.

DC is so insulated from reality they are about 20 years behind where the general population is. Same is true for the Fed, they use inaccurate modeling of economy and are always late to the bubble.

I predict before this is over saying things contrary to the Fed narrative will get you kicked off major social media sights.

Haha The pandemic of “mis -informed thoughts”.

The Tibetian monks are being fixed now in China.

Fed denial will lower your social score.

You need a bottle in front of you, but you get a frontal lobotomy

Reading lots of Thomas Sowell right now.

Isn’t interest rate suppression just a form of price control?

Yes, absolutely. The price of capital and by extension, the price of risk. That’s one of the big problems with interest rate repression.

Who in their right mind would invest in treasuries … especially in a rising rate market. 2.0% taxable interest plus guaranteed loss of capital????

I read a lot of Buffet. He loves t-bills and hates long term treasuries. If you are good at what you are doing you should be able to pick some conservative stocks that are going to generate more free cash and dividend income than a 10 year Treasury.

T-bills are to allow you to handle unexpected financial crises and to profit from them.

National debt = $30T but the amount which must be serviced (gross debt less interagency and FRB holdings) is still “only” about $18T.

Just trying to make sense of this foreign holding part. Japan holds 1.3 trillion. Isn’t that country up to their neck in depth? An it has trillion plus of money to lend to someone else, whom is slightly less in debt?

Japan isn’t nearly the basket case that Western media make it out to be. It’s an industrial powerhouse and a huge exporter of all kinds of high-value goods. It’s also a big importer of raw materials and fuels, similar to Germany.

Last I looked Japanese per capita long term growth was superior to US. Demographics are terrible, so central bank does extra ordinary things to manage the debt.

And now the mantra is..

“If Russia invades Ukraine, the Fed can’t raise.”

So inflation will get worse (higher oil and wheat and fertilizer, etc) and the Fed won’t focus on those costs, but will do all can to fluff the markets.

The markets over the citizenry is their order of concern.

historicus,

Hahahaha. This is hilarious. There is always a mantra in the markets. So now Wall Street is rooting for Russia to invade Ukraine so that the Fed won’t raise interest rates??? The desperate BS out there is getting really thick.

I’m still waiting for Dolly Parton to come out and thank the markets ;-]

Hi Wolf!

Have you though about producing your own index regarding Main Street cost of living? We all know the numbers released are outright egregious and fluffed for positive news. I hear coworkers (and aging relatives) state that inflation is much bigger then what is reported. Perhaps a good niche to start?

Look up the Big Mac Index, a/k/a Burgernomics. It’s a light-hearted index invented by The Economist to compare relative pricing since Macs are sold in dozens of countries.

Our household inflation is lower than reported.

Inflation is an average for all dollar-using consumers in the US. It’s not “my inflation” or “your inflation,” which vary. So everyone can come up with their own number. For example, if half of your income goes to rent, and rent goes up 20%, than that causes “your inflation” to spike. But the couple down the street own their own home, and spend 50% of their income on mortgage payments, which don’t change, so “their inflation” is small.

Wolf as you know mortgage payments are excluded from OER so OER can stay stable even with a variable rate loan, a HELOC, a refi or whatever. OER is blind to mortgage payments because houses are considered assets, not just shelter services. They back out whatever isn’t shelter service. IOW what OER seeks to do is is ask “What would be the shelter service value for your house, unfurnished, and excluding maintenance, taxes, and loan interest?” That’s bullshit. No one can afford to rent their house for that.

Neither can a landlord renting a property to a tenant. A landlord has expenses that contribute to the shelter service value, but in reality the rent usually is set to cover taxes, maintenance, loan interest, and other things that OER excludes as asset related. The survey ignores this. Rent is rent under CPI, but OER excludes the homeowner’s expenses.

If I were to rent my house my ask would include all of my overhead – loan payments, taxes, maintenance, and improvements. OER ignores all of these things. It’s unrealistic.

Michael,

I agree on your rent assessment. I like using Michael Bluejay’s on-line rent vs buy calculator. The number of inputs is more than a dozen to spit out an answer and some of them are guesses like future inflation of house and future return on your investments.

Or Miley Cyrus swinging on the ‘wrecking ball’!

Wolf

The talking heads on cable (Bloomberg) are suggesting just that.

If the invasion happens, does the Fed still raise in March.

Just reporting.

What if:

Each time someone close to Putin probably buys calls prior to him expounding how they’re retreating,, conversely, every time the United States and Europe say how bad things are getting getting,they in turn buy puts ahead of the news

What if the Fed does a QE with Russian bonds?

To bribe Putin from not going in?

Why not?

Problem solved.

Kinda like the skid of money Obama sent the Iranians……but much larger.

You don’t understand geopolitics, do you?

But then how would both these players justify their military budgets, a.k.a., big socialist job program that dare not speak its name? Gotta rattle sabers SOME time. Though from that DID come such things as freeways (autobahn), commercial airlines, transistors, radar, space technologies and the Internet.

August…

in jest

and I do understand….

and what is for certain, neither you nor I have all the details to make informed commentary

Someone has to own that debt, and the Fed does care who owns their debt, so lately they have taken it upon themselves. The junk bond market seems to be holding its own, even while Chinese RE developers scramble for cash. I would say government having extra savings, (even if it is in the form of debt) is positive and prudent in these uncertain times. A recession is likely if the money isn’t needed, which is another positive. The negatives are that the US cannot handle the impact of retooling her own industrial base after deglobalization plays out. A lot of people who retired at 50 will have to go back to work at 60.

> A lot of people who retired at 50 will have to go back to work at 60.

Where does it say a person can or should retire at 50?

nowhere, yet

how some ever, after ”retiring” 3 or 4 times and being bored out of my gourd,,,,

IF one chooses to ”retire” one really MUST plan carefully for something to do that is sufficiently challenging.

Most of my old buds who declared they were going to do nothing but play golf or nothing but fishing, etc., did not last very long, and at this point I am convinced it was because of boredom.

True Dat.

Many people have to have something to do. A lot of those things bear close resemblance to work.

OTOH plenty of people are happy being drunken slugs.

I am still working nearly full time at 75 and really enjoying my work. Not sure what I would actually do if I eventually retire..

Can the Federal Reserve simply retire its treasury bonds? Why not?

It would be a “selective default” by the US government. Kiss the markets goodbye and assume fetal position.

Federal Reserve monetizing debt is a form of default too and yet they have gotten away with it for 13 years.