The numbers are already baked in and will show up over the next 24 months.

By Wolf Richter for WOLF STREET.

Two rent factors account for 32% of the Consumer Price Index. Despite the massive spike in “asking rents” across the US, those two CPI rent factors have been much lower than CPI and have thereby repressed CPI so far. Unlike asking rents, these two rent factors track the average rent that tenants are actually paying across the entire stock of rental units in US cities, including in rent-controlled units.

On the other hand, “asking rents” reflect current price tags on units listed for rent that people have not yet rented, and it takes a while for people to rent these units and pay those rents in large enough numbers to where they move the needle of the average rent actually paid across the entire stock of US rental units, which then gets picked up by the CPI rent measures.

But those two CPI rent factors are bound to catch up with asking rents and they will then fuel overall CPI – which was already 7.5% in January, WHOOSH.

But when will the spike in asking rents drive up CPI? And how much will it add to CPI?

The short answer: The current spikes in asking rents that have already occurred through January 2022 will add more than 1 percentage point to overall CPI for the year 2022, and will add more than 1 percentage point to overall CPI in 2023, even if asking rents don’t rise further from here. This is already baked into the numbers. CPI is going to catch up with a painful reality spread over the next two years.

The asking-rent spikes are brutal.

Rents for single-family houses and condos on the rental market exploded by 12% year-over-year in the US, varying widely from city to city, the worst increase in the data which starts in 2004, according to CoreLogic today. Miami was on top of the list, with a 35% spike in rents. In the years between the Financial Crisis and the pandemic, rents of single-family houses in the US had been increasing in the 2.5% to 3.5% range.

Rents in apartment buildings – does not include single-family houses and condos for rent – jumped by 12% for one-bedroom apartments and by 14% for two-bedroom apartments on average across the US, according to Zumper data. In 20 of the 100 largest cities, rents spiked by 20% or more, and in 11 of them, rents spiked by 25% or more. This is based on median asking rents, which are the rents landlords advertise for their listings. They’re similar to price tags in a store.

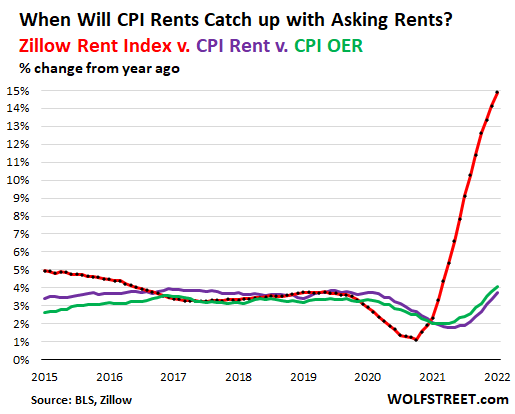

By a different measure, the Zillow Observed Rent Index, rents in January spiked by 14.9% year-over-year across the US, varying widely among cities.

All these measures show the same thing: On average, rents across the US spiked by over 12% year-over-year, varying widely from city to city, with some cities experiencing astronomical rent increases.

Asking rents take 24 months to spread across CPI rent inflation.

Asking rents are the current price tags. They don’t show up in rent inflation until enough people signed leases for units at those rents, and are actually paying those rents in large enough numbers to move the needle for the entire stock of rental units in US cities.

This makes asking rents a leading indicator for CPI rent inflation. Turns out, according to a study by the San Francisco Fed, these surging asking rents that have already occurred will push up CPI rent inflation for the next 24 months.

The two rent measures in the Consumer Price Index that together account for 32% of the overall CPI show this lag, though they too have started rising. The CPI Rent of Primary Residence (“CPI Rent”) in January was up 3.8% year-over-year, and the CPI Owner’s Equivalent of Rent (“CPI OER”) was up 4.1%.

These two CPI rent measures track what tenants are actually paying in rent across the entire stock of rental units in the cities. This includes tenants in rent-controlled apartments where rents don’t rise sharply, and it includes tenants on still active leases where rents cannot be raised, and it includes tenants whose landlords are slow to raise rents for a variety of reasons, including to keep good tenants.

So, the CPI measures will not spike in the same magnitude as asking rents. Between 2017 and 2019, the CPI measures tracked closely with the Zillow index. But in 2015 and 2016, there were large differences: In January 2015, the Zillow index showed rent increases of 5%, while the CPI measures showed rent increases of 2.6% and 3.5%.

When will these asking rents start fueling overall CPI?

So far, the rent factors in CPI have repressed overall CPI. Overall CPI in January jumped by 7.5%, despite the low readings of the two rent factors – rent of primary residence (3.8%) and owner’s equivalent rent (4.1%).

The San Francisco Fed has now come out with a staff report to estimate when these asking rents would filter into the CPI rent measures, and thereby into overall CPI. And this is going to happen over the next 24 months bit by bit.

The asking rents that have already occurred will likely push up the CPI rent factor by 3.4 percentage points in 2022 and then again in 2023, and given the 32% weight of the rent factors, will add 1.1 percentage points to whatever CPI will be by the end of 2022 and will add 1.1 percentage points to overall CPI in 2023, even if no further rent increases occur in the market.

So any leveling off or even declines in the CPIs for new and used vehicles will pale, because of their much smaller weight, in comparison to the coming surge of the CPI rent factors.

In terms of the measure the Fed uses as inflation target, “core PCE,” whose housing components are smaller than in CPI, the asking rent spikes that have already occurred will add 0.5 percentage points to core PCE in both 2022 and 2023, according to the San Francisco Fed, even if no further rent increases occur in the market.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

In Canada, when a long-term tenant pays below market value, there is ALWAYS a loophole to evict them in Toronto. ALWAYS. Nobody pays below market value rent anymore. Hear that Tiff Macklem and Chrystia Freeland who OWN properties?

In California the loophole is to ask them to leave in order to do a major renovation, which many landlords are doing. You need to give them proper notice, maybe 60 days, and rebate them a months worth of rent as relocation money (I’m not sure the exact details but this is close). Before rents spiked like crazy landlords kept tenants in place, but the lure of a thousand or more for increased rent has started the “remodel” evictions.

Good ole renovictions. I guess the greedy feudal lords want to rent the apartment to a dozen desperate international students cheating their way into the country?

No cheating in good ole free market capitalism where everything is for sale.

The foreign students have millions and that can buy you a degree and a house. Theres always poor and homo es to drive up prices in every city. And since money is all that matter we will all be poor and the world’s rich will own our houses like feudal lord’s.

We can stop it but that means getting rid of capitalism. Otherwise you’re just changing who your lords are.

This exact thing happened to my MIL in another state. She rented faithfully for 15 years. She did not get anything when she moved, not even her original deposit. Apparently, they were renovating the whole building.

Anyone who protests gainst the asset bubbles and the Liberal policies are labelled as a “white supremercist” and a future Hateler.

Meanwhile, Adam Vaughan was laughing on TVO when moderate Liberal TVO host Steve Paikin was concerned that Canadian real estate was unaffordable for Canadians.

Canadians are too passive to do a French Revolution. When Canadians are starving and homeless they rather attack someone who is going to work their dead-end job rather than the elite in Bridle Path or Ottawa.

Google “globeandmail mom pop landlords” and “bloomberg trudeau immigration targets”.

Canadians are watching their future slip away in front of their eyes, and they are totally passive. Quite incredible.

Inflation is like 7-14%. The central planners’ talking heads mull over 0.25%-0.5% raise in rates, perhaps in the next meeting. They won’t stop till we’re all broke.

Not all of us. The banksters and other ultrarich parasites are getting more and more wealthy. They are making huge profits by charging us 25% on credit cards using money that they are getting from their “Federal” Reserve privately owned bankster cartel at 2.5% or so. For the ultrarich parasites, these are the good times. See also “The Cantillon Effect: Because of Inflation, We’re Financing the Financiers” in fee org.

It is just a question of how poor Americans want to get, while the parasites get richer and richer, before they start to look for solutions in history: e.g., the French Revolution and its unique, speedy, humane method of punishing the ultrarich, which like our ultrarich, did not pay taxes in pre-revolutionary France and had parasitized France for centuries.

Correct. Those at the top are keeping their gains well beyond inflation. Example, Elon Musk, who did absolutely nothing in the past 24 hours of any note, yet recorded a one-DAY net gain of 4.66% in value on Forbes’ “Real Time Billionaires” list. Not bad!

(And he claims that his stock is overvalued…) But get this- since almost half Elon’s stake in Tesla is held as collateral for loans, Forbes doesn’t even count that in his net worth of $249.1 Billion! So…what’s he REALLY worth??

Let’s all send him a cake when he becomes a quarter-trillionaire, (that right, a quarter million millions), shall we? I bet it happens tomorrow.

Like John Lennon sang, “Strange days, indeed…most peculiar, Mama, WOAH!”

Side note on Lennon;

Was reading Playboy in rented bedroom (yeah..reading it….rare) interview with him and thought, “this guy is really arrogant, someone’s going to shoot him” and it happened about a week or so later.

Only premonition I ever had…..but it still means I have some psychotic abilities.

“…but it still means I have some psychotic abilities.”

Your Freudian slip is showing.

Good one DC I have to say

Ouch! That was painful.

Quick to save MARKETS

SLOW to save the citizens from INFLATION

that seems perfectly true, and deliberate.

House affordability is way down. House prices up 20% plus monthly payment per $100,000 up 20% due to mortgage rate.

I would think the above is going to put additional pressure on rents as alternative just exploded higher.

Steve Hanke says this high inflation is going to be with us for two more years just based on the Fed monetizing the debt and increasing money supply. Takes 18 – 24onths for the money drop to work into prices.

He got the inflation number exactly right 6 months in advance, so I think I will listen to him and invest accordingly.

The rich puke bankers and their ilk have a plan to buy up all the real estate once the plebs can’t make payments anymore. They will own everything, you will own nothing. They want society living in Soviet era housing blocks eating bugs while they show off on social media with all their trillions.

Bugs have lots of good protein….they are basically just little crabs or lobsters. Some good “goo” outfit should be making tasty burgers out of them. Beats “dead burnt cow”, as a hippie GF of mine used to say.

Have you seen how many regular non-rich bankers have been investing in real estate? Answer is a lot.

Tons of regular buyers that are not rich, investing in RE for cash flow. Taking advantage of the low rates and loosened loan programs.

Just sayin…

It is not just the house price itself that is making home ownership unaffordable for so many.

Homeowner’s insurance premiums and property taxes have also exploded higher, adding insult to injury.

“Inflation is like 7-14%.”

Certainly a lot more than 7.5%

Since the calculation of CPI has changed significantly over time, historic comparisons are like comparing apples and oranges. And, miraculously, every time the method of calculation was made “more accurate” the CPI decreased. How about that?

Rent control laws in California dictate that any unit 15 years or older is subject to rent control. Asking prices for vacant units isn’t controlled, but rent increases on existing tenants is controlled. Here’s the part that makes no sense, max rent increases in a 12 month period are limited to 5% plus regional CPI. I believe that any spreadsheet program would call this a circular reference or something like that. Because CPI is part of determining rent increases and rent increases are part of determining CPI you’ll never get a true number. I’ve pointed this out to friends and colleagues who all agree that this could be grounds for a lawsuit to remove rent controls from CA. I should also mention that the max increase regardless of CPI is 10%. All of this leads to very large errors in reporting of what the actual CPI number is and is just one more thing that makes the whole metric unbelievable. Regsrdless, rents on new to market stuff are, as you’ve said, absolutely insane.

Politicians acting to buy votes always make a mockery of econ 101 supply vs demand curve price intersection.

When the CA apts I was in started charging (c 2007) for gas/elect “hook-up”, water, sewer, and garbage, I was told a class action suit was filed and it was shot down. I forgot what the “fee” was called, but it was mailed to a three letter outfit at P/O box, supposedly some 3rd party. It varied month to month, too, as if something was being “monitored”. $30-60 in the 2 years was there.

Don’t know if it’s in effect now, I split for Tucson and the over 55 hotel style low income place I’m in now in CA doesn’t have it.

Also, before I left, they were going to mandate renter’s insurance (which they could provide for $25/mo). Was large complex next to Bennett Valley golf course, Santa Rosa, forgot name.

Wolf’s RE contact Tom is in SR…he would know all about it. Although it’s possible one apt mgr was screwing me because I’m stupid.

In SF Bay Area, where rents dropped a bit in the middle of pandemic, rents are now rising rapidly even before offices are fully open and population actually shrank. Think what would happen when offices open in a couple months and massive immigration begins.

In a year from now, I expect SF bay Area rents be 50% higher than pre-pandemic levels, which was already insanely high.

If you’re going to make a snarky comment at least know what the hell you’re talking about. SF a ghetto? Give me a break

SF Bay Area is not a ghetto even if many neighborhoods in SF city is.

Well rents are exploding here so clearly people still want to live here.

You have obviously not spent much time driving around they bay area. There are lots of ghetto places here.

Every large town has ghetto/homeless areas. In Tucson, you could head south from River Road, and the closer you got to the VA Center at the far south of town the more bars on windows. The rich people all lived in the hills on the fringes and in a few other pockets.

Maybe Wolf will let me add this 1% chart to the one for the USA he puts up a lot…..income inequality seems to be the worst in the “land of the free”.

“..income inequality seems to be the worst in the “land of the free”.”

Everyone knows that. It’s a feature, not a bug. You don’t need a Wikipedia to prove it :-]

No one lives in SF anymore, it’s too crowded.

Apple,

That’s a great Yogi Bera-ism.

Lol!

Kunal,

If a year from now, the Nasdaq is down 25% or more from the Nov peak, instead of just 15%, rents in the Bay Area are going to tank.

Here is San Francisco’s rents that rising “rapidly,” and are “exploding,” to use your terms:

I meant SF Bay Area excluding the city.

According to zumper rents in Sunnyvale are up 37% in last one year. Same in Mountain View. It’s now already approaching pre pandemic levels but what’s astounding is the rate of growth in spite of tech offices still closed and population decline.

So it’s rational to assume rents will explode post pandemic. Tech Wages are up. RE costs are up. Inflation is at ridiculous levels. I don’t see any reason rents will not keep rising rapidly in Bay Area. And btw Fed will not let the market crash.

Maybe for apartments (I’d like to see you post a real link), but in the East Bay, I’ve seen a number of rent reductions on SFH for rent on Craigslist.

If the shift away from money losing “tech” companies continues, it’s very easy to see lower rents in the future all over Silicon Valley.

How about a 80% tech Bust like in 2000? When you have 10,000 plus cryptos you know somebody has gotten carried away a little too much writing crypto.

Steve Hanke has good foundation on money. Says crypto trying to provide banking services so they are going to get regulated like banks.

Please post the link.

I’ve lived in the Bay Area for 20+ years; the rents in Sunnyvale, Oakland, etc have always been in the same rough range as SF (lower but not significantly lower) unless you live in an actual war zone.

So it would be interesting if rents there are *higher* than SF – which they would have to be if your comment is correct.

Those who are sitting out hoping and wishing for a crash will keep losing big time. Sitting out is losing trade for good 15 years. Even more so now. 7.5% compounded per govt., 10+% in reality. And still growing.

EVERY financial asset experiences the same effects of inflation as cash. All of them lose 7.5% in purchasing power. The hope is that either yield or asset price increases will outdo that 7.5% loss in purchasing power from inflation. But if your asset loses 10% in price plus 7.5% from inflation, you’re down 17.5%.

Cash has been better this year than stock indices.

Not sure what will happen in the future, but I’m sure about what happened over the past six weeks. And cash won.

Here is the Zumper link that states Sunnyvale rents are up 37% in last one year:

https://www.zumper.com/apartments-for-rent/sunnyvale-ca#guide

Kunal,

According to your link, looks like Sunnyvale rents have come up from the trough and are now flat with 2017, and well below 2018 and 2019 levels.

Kunal must be a landlord with an agenda. Paid rents are not increasing in Silicon Valley. Heck, even asking rents are not increasing. A quick trip to Craigslist showed that asking rents have not gone up since the great panic and the great escape. I see plenty of 1-bedroom under $2000 in prime Silicon Valley locations (near google), and they used to be $2300-$2700 or even worse two years ago.

All those 4-story uglybox buildings that got built in the last 5 years probably still are trying to overcharge, but the small-landlord apartments are holding steady. It is the big-complex big-landlord corporate apartments that are trying their luck with wildly overpriced offerings. They will learn eventually.

I think touting high asking rents is a double-edged sword. On one hand, it might cause the Fed to be less crazy. On the other hand, it might cause greedy landlords to become more crazy.

“Kunal must be a landlord with an agenda.”

My money is on “speculator with negative cash flow who needs rents to increase, and is counting on it to remain solvent.”

I’ve been guilty of that sort of cognitive dissonance … trying to rationalize my bad choices instead of get back on the right side of the market …. seen a lot of that sort of discussion on forums in the past…

The market always remained “irrational” (to me) longer than I could withstand the pain.

When there’s always someone on the other side of every trade, the market ALWAYS seems “irrational” to half the population.

In my opinion, the market always pukes down to where you can buy it on fundamental value and you can expect to earn about 6% – 7% more than inflation for the long haul. Don’t think it will be different this time. That’s sub 2000 on SP500.

There is saying in Silicon Valley which has been true for last 50 years.

Never bet against Silicon Valley and Silicon Valley real estate. There are some ripples but in the end it only goes one way – up.

They said the same about Detroit.

So the Fed Funds rate should be at around 9% right now? And we’re at Zero…. And they’re still debating between 0.25% and 0.50% on the next meeting.

Bizarro World.

Who knew that the Fed would NOT , THIS TIME, answer to their mandates/instructions/agreements that ALLOW their existence?

For, in the past, prior to 2009, the Federal Reserve would FIGHT inflation, NOT PROMOTE inflation….and Fed Funds would rise to meet the level of inflation…..to discourage irresponsible debt creation, protect the holders of dollars, and tamp down the inflation itself.

https://wolfstreet.com/wp-content/uploads/2022/02/US-CPI_federal-funds-rate-2022-02-10.png

But NOT THIS TIME. Who knew they would not? Who got the nod that they will promote inflation and “Let’er Run”? For those waiting for the Fed to show up lost out, and now are punished at 7.5% clip. Those who went with the “cattle drive” (bought and held assets)…. somehow were NOT concerned the Fed would actually stand to their post, won.

We wouldnt have the issues we have today if the Fed had kept to their duties. Oh, the markets might be lower, but maybe they never should have shot up like they did.

Quick to save markets, Slow to save the citizen (and businesses) from a punishing induced inflation.

I think death spiral for Fed is house prices and stocks crashing as banks would be insolvent, so they decided to goose price levels up with monetizing government spending.

Congress will act like they care and try to buy votes by doing a little inflation assistance just making things worse.

Barrick is doing press releases this morning saying they are increasing dividend and buying back stock. It is a fitting end to Fed policy when you print so much money that digging up the alternate to fiat is such a profitable business you can do what everybody else in the stock bubble is doing.

Wage deflation and rent inflation are already happening. “International students” are working in those warehouses and factories for minimum wage. Next will be international students doing welding, plumbing and construction jobs for minimum wage.

The public sector has hired “international students” to work in the hospitals and municipal offices, which can explain why Canadians are getting threatening scam calls from Asia.

Funny how international students are not being hired as overpaid bureaucrats like teachers, politicians, school administrators and cops.

“overpaid bureaucrats like teachers … and cops”

Oh, am I an overpaid teacher? Less than $20k/year gross in coastal CA. And I pay for everything I need to get there and do it, most supplies included. Have missed 5 workdays total in 37 years. Make up some more stuff.

And try being a cop with today’s complexities on the streets. You should find someone at least vaguely reasonable to demonize. But nowadays that is asking way too much.

I’m thinking of a Goya painting (yeah, like educated people know about). Two characters flailing each other while both are heedless that they sinking in quicksand. That’s what happens when one strikes out blind and doesn’t know who true enemies or friends are.

What? You make less than 20k per year? Or Month? Bullshit. Btw teachers work 9 months a year.

The average teacher salary in the California public schools system is 84k per year in 2019-2020 school year. That’s per the the California department of education. Even the beginning salary of first year teachers is 47k. That’s not including benefits such as healthcare, sick/paid leave, pension, and the fact that you have entire summers off.

While I don’t envy school teachers because they have a tough job that I sure wouldn’t want to do, I think it’s pretty easy to see you are definitely fudging the numbers here. Either A) you work super part time to the point of barely working at all, or B) you are completely lying about the numbers.

Not sure what your point is.

A large part of California by area is not high rent, at least compared to SF Bay Area/LA.

Plus the AVERAGE includes 50% of the incomes below that.

Our granddaughter, a 2nd grade teacher here in Texas, makes $42 K with benefits and she just started teaching. What’s this “less than $20 K/yr gross” stuff about?

Maybe ”international students” working for ”minimum wage” in Canada GZ,,, but long long time in USA, such folks been working for cash ”under the table” for far LESS than minimum wage in my clear perception of those in the construction industry in various locations, SE, CA, even into midwest places where the international students had no presences previous to 21st century…

Time and enough to really and truly clean up the act and actions of the vast majority of so called general contractors in many states who just ”sub contract” down the line to those who then ”sub contract” down the line to the ”labor contractors” who put bodies on the project earning less than minimum wage and are almost always subject to the same shameful activities of the Gallo Brothers who worker their illegal immigrants for 90 days, WITHOUT ANY PAY,,

just promises,,, and then called the immigration services to send them back,,, etc..

That was the main reason this old boy marched in the streets to support LA RAZA and the United Farm Workers/ Chavez…

And IMHO, that is the reason that ALL,,, REPEAT ALL,,, OF WE the PEONS should be out in the streets sooner AND later…

Not to be arrogant, did any of you ya hoo’s go to school 1.87 gallon gas now in vicinity of 5.00 what is the real increase , jBONE HEADS

But Jerome Powell and the lying Tiff Macklem from the Bank of Canada refuses the gas prices because it’s “volatile”. These banksters are robbing us blind while making the rich richer.

CLARK,

Hahahaha, gas was already near $5 in 2008 in California, same as now, “you ya hoo” – to use your elegant term. So do the math, since you’ve been to school: What’s the increase over those 13 years? And what is the increase in rent over those 13 years

and what percentage of price at the pump is actually taxes, not producer price? Amazing that gasoline can be produced with all this tax at lower price per gallon than milk, with its subsidies.

And beer is even cheaper than either milk or gasoline!

Where I live, the state tax on gas is a percentage of the price…

higher price begets higher tax revenue

2banana

“And beer is even cheaper than either milk or gasoline!”

So, are you saying Drink don’t Drive?

Just take last years $2.50 gallon gas compared to today’s $5.00. That’s your comparison. The past 12-Months rents are also up 50% in many areas.

You and clark are trolling.

If you are a conspiracy theorist you could say:

1. Government plan was to finance massive debt a real negative rate for years to come.

2. Government plan was to inflate gas price to make EV more affordable.

Constituents don’t like it and will detail plans by voting out current crooks for new crooks.

Inflation adjusted gas is cheap. Gas compared to other country is super cheap. Not sure where your seeing $5.00 gas but its not the US.

Yes. Across Southern California $5+ gallon is normal. Yesterday I filled up in what I thought was a very low income neighborhood and it too was over $5/gallon. Depressing to think that it costs nearly $100 to fill the tank in an average compact SUV

Very happy to be a full time remote worker, doesn’t have to get clothes dry cleaned and can make meals at home

As a remote worker, do you worry your employer will outsource your job to some place even more remote?

I filled my car and it cost $62.50 at $3.59 per gallon. I have decided to see how long that will last as I only use the car for a weekly 50 mile visit to my parents and maybe an emergency trip during a rainstorm. Should last about 2 months.

Everything else is a scooter at 95 mpg. Probably will upgrade this to a Honda 125cc for some additional speed and 120 mpg.

Just downloaded gasbuddy and regular gas in San Diego is $4.25

“Inflation adjusted gas is cheap. ”

Wait. Is that some type of circular calculation gimmickry?

Take away inflation from the calculation…..when it is inflation that is the cause of the higher prices?

BTW, Nothing is ‘cheap’.

If you are saying other items have increased more … perhaps.

Cobalt again with his moonshine postings…

1. If WFH made people to move away from cities, how come the rent is spiking?

2. Why people are protesting about rents? Can’t they buy a home? Million dollar starter homes with 5% rates for 30 years are available? Higher officials are scratching their heads…

3. Do you remember? Detroit sold $1 homes with $10K property taxes? Now homes of that kind are selling for more than a million dollars

4. Fear not. Rates will not be raised.

5. Even if rates are raised, it will be “a day late and dollar short”. A 2% increase over 2 years. As usual blame it on the white house.

6. I brought a lot of stuff expecting a tuckers strike. Please stike. I dont want to return those items.

7. Swamp area gas prices are slowly creeping to LOL, OMG and WTF. I feel sad for those gas guzzling trucks and SUVs.

8. Do you laugh at me for believing in the cryptos. Look in the mirror, you believe in the feds.

“I brought a lot of stuff expecting a tuckers strike. Please stike. I dont want to return those items.”

What did you buy that you won’t have to have in a few months, after more inflation? If inflationary expectations are high, the thing to dump is cash, right? For things?

The one reason I’m not dumping cash is, I want to have liquidity no matter what, to pay for necessities and fixed costs.

Actually we’re reaching a point where a returned product almost costs too much for the seller to pay for the return shipping.

I wonder when online sellers will no longer offer free return shipping. There’s a sneaky little bit of inflation that CPI doesn’t track.

Michael Gorback,

Yes. We have experienced many times that the seller doesn’t even want you to return the product. They just ship another one. Even — or especially? — pieces of furniture. We now have two nice pieces from Wayfair, for the price of one. One of them is slightly damaged on a corner. I asked for a replacement panel, just the panel, and they sent the whole entire cabinet. We have duplicates of electrical equipment that I was able to fix after they told us to keep it and sent us a new one. Shipping is too expensive.

> I bought a lot of stuff expecting a tuckers strike. Please strike. I don’t want to return those items.

I had my short bets in place for a Kremlin incursion in Ukraine. Today’s relief rally came so fast and breathlessly, the White House didn’t get a chance to say the Russians’ latest move was unclear. Why won’t the world cooperate with my fantasies and shower me with money? Even depreciating money will be graciously accepted. I should do a GoFundMe for my upset condition.

I can answer number 1. It is tough to get a company to give you a commitment that you will be permanent work from home.

My son has been teaching remotely for more than a year living with me, but NYC wanted him back so they made him teach one class in person. It has six students. That means he will be spending about $5000 per month in NYC that wasn’t being spent there before.

He had to get fully vaccinated as well, even though New York was testing him periodically for antibodies because he got Covid early on.

My favorite Liberty gas station just upped their price of regular gasoline to $3.99/gallon. I couldn’t care less. Up it to $7/gallon and get it over with.

Just where do you think all those folks coming through an open border are living?

Yeah, you are competing with them for available limited rental stock.

They also double, triple and quadruple, etc up.

Yea, they took our jobs (and rentals).

A decade ago it was illegal to have more than three tenants in a one-bedroom apartment in Toronto. Today, a dozen “international students” are in that one bedroom apartment and are paying a premium while working a minimum wage former unionized factory job.

A dozen or more is commonplace in the greater Toronto area today The old Scarborough bungalows have as many as thirty living in them today. 15 upstairs and 15 downstairs.

You never want to compete with government money. Live near a military base you are competing with government housing allowance. If you are retired and on limited means your best bang for the buck is to go live rural where few government dollars circulate.

When Will the Brutal Spike in Rents Drive Up CPI Inflation? As soon as accurate inflation stats are reported by the Gov. In other words, NEVER. CPI is already 15%.

BS. 15% inflation means that the average American income has to double every 5 years to maintain their standard of living and has to quadruple every 10 years to maintain it. Do the math yourself.

Meaning that if the average American made $40k in 2012, they’d now have to make $160k in 2022 just to maintain their standard of living. This is just BS. Get a calculator!

Sorry Wolf, I have to agree with JM. Inflation is way above double digits right now for the average working stiff.

Wolf doesn’t like it when we disagree with the government stats. But it’s hard to trust a government when they manipulate data to try to support their narratives.

I just bought Peet’s coffee during my last trip to the grocery store. It used to be a pound. Then it went to 12 ounces. Now it’s all 10.5 ounces. They are trying to hide the inflation through shrinkflation, but to me they’re just annoying me. Give me back my pound of coffee you assholes. I don’t want to increase my trips to the store because of a shrinking basket so you can pretend like you’re not charging me more.

I don’t believe the 7.5% CPI number. My own inflation calculator is WAY higher.

No one ever talks about the price of coffee when it drops as a commodity — and it does quite frequently. It only shows up in the news when it spikes.

I just bought 6 pounds of whole-bean coffee of my much-liked brand (2 bags), and it was the same price as a year and longer ago. That’s the problem with this anecdotal stuff. My coffee didn’t go up, yours did. So what’s the average price increase of coffee across the US in February?

Wolf – it’s quite possible I’m just getting ripped off by Peet’s coffee, or the grocery store is gouging me? I’m really not sure where inflation ends, and price gouging starts. I suppose I could make a spreadsheet of all my regular foods and things, and start tracking them. But I’d need historical records which I don’t have. Bottom line, shit’s getting real expensive, far more than 7.5% for everything I want and need.

SC, et alia:

Inflation hits WE the PEONs, (thanks Unamused ) in different deltas in different places and different situations within those places to my clear experience over the last 70 years or so since daddy had to sell the farm to be able to keep us in the house/home in the small city where HIS 5 kids were going to get, at least, a somewhat decent education..

While WE can continue to speculate as to whom will be the biggest losers from the clearly corrupt and cronyisms currently occurring, as I and many on Wolf’s Wonder do, sometimes daily,,, WE cannot know in advance what the FED and their clearly oligarchic cronies are going to do NEXT!

Now a days, WE the PEONs can only HOPE,,, and do our best to do the same or similar to our grandmas etc.,,,, who put their gold in jars buried in the dirt until the crash came, as it always did and always will,,,

Certainly, all the current ”fads” of ”cripts” and ”bloods” will continue for at least a while: long or short while will be subject to SO many possible ”outliers” that WE the PEONs will have to be, like totally dudes and dudettes, ON OUR TOES, ,,,

Seems like ”for eva” but NOT, because ”’they”’ will play out their hands/projects,,, as always,,,

And then, also like always, sand bag for A while,,, and then come again with their work to make WE the PEONs slaves and/or serfs again similar to the last couple thousand years…

BUT,,,, ONLY IF WE LET THEM GET AWAY WITH IT!!

I’ve been watching the recent senate confirmation hearings for Biden’s recent slate of FOMC Governor nominees.

Never once has a political party sounded so out of touch with American consumers. The Democrats repeatedly ignored the elephant in the room – 40-year-high inflation – to focus on climate change (changing bank stress tests to account for climate risk), disparities in economic outcomes between racial/ethnic groups, and other issues that are historically outside the mission of central bankers.

Sen. Menendez of New Jersey, one of the few Democrats to bring up inflation, had Philip Jefferson publicly state inflation was caused by supply chain disruptions, without acknowledging any of the other causes on the demand side.

In contrast, Republicans have been pushing hard on the inflation issue. Lisa Cook gave a bunch of rambling non-answers to Ranking Member Toomey (R-PA) when asked whether she agreed with the accelerated QE taper & faster interest rate increases to combat inflation.

TL;DR: I think Biden nominated 3 super-doves who don’t really care about the inflation problem. And neither does the Democrat Party as a whole. In short, expect more of the same for rest of 2022 – a few token rate increases followed by continued kicking & dragging their feet on normalizing policy.

Jackson

Even the Chairman of the Senate Banking Committee…the overseer of the Fed……focused on social issues in the last hearing. (Sherrod Brown)

Forgot to focus on 40 yr high inflation.

The preceding president with all of his faults tried to put two people on the Fed board that had harder money views than current Fed board. Their names had to be pulled because Fed is captured by group think post Keynes theology that any other monetary view is unacceptable.

Congress knows that easy money is their key to buying votes and that isn’t ready to change. They know that if the Fed fails, Congress can go into emergency session and do whatever it wants with fiat.

I guess you guys have an alternate history:

Remember a Pres called Trump? Well he advocated for a looser Fed policy than the one that was already the loosest in history. When JP took the first baby steps towards normalizing rates he went nuts (nuttier) violated his oath to respect the independence of the Fed, and castigated JP.

Oh but NOW the GOP is all worried about inflation. NOW it’s the Bidenflation. Ya that’s because the polls etc. tell them it’s the public’s big worry. But where were they when Trump was blowing up? Where were they when Trump wanted negative rates ( nominal, even deeper than real)?

They have airbrushed history and you fall for it.

Why don’t you stop thinking minute- to- minute and realize that today’s inflation was sown a year BEFORE Biden took office.

When parents first help junior to grow a garden, they plant radishes. Even the 1.5 months seems like forever to the kid, but he learns. So later in life when he buys some young grapevine varietals, he understands he won’t be harvesting grapes that fall, or next fall.

Some things take time to happen and perhaps more important after the bizarre stewardship after 2016, time to get over.

These idiots will lose mid- terms by a landslide

Instead of OER, why not have the property tax appraisers provide the estimates of market rents instead of asking clueless owners? Or simply extrapolate from actual rents among rental properties in the same neighborhood/ ZIP code?

Of course, the government isn’t interested in accuracy; they’re interested in understating actual inflation which means lower SS payments, lower interest rates, lower chance of population rioting, etc. Chances are the BLS is brainstorming ways to understate inflation by even more in future release cycles.

In the information age they could use real data to generate an accurate and timely number if they wanted to.

1) US10Y = 2%, mortgage = 4%, cpi = 8%.

2) The cost of mortgage is low. The value of debt today will be nothing

tomorrow, because the cpi is 8%. 2022 is better than 1980’s. We need a new Michael Milkman.

3) Comatose TY, the 10Y futures price, might wake up.

4) Inflation will decay, gov debt in real terms will be chopped and pain businesses sustain will ease.

5) Can we have a negative cpi : why not. This inflation looks like the

1982 inflation. That doesn’t mean that we are on the cusp of a 40y bull

market. Negative cpi doesn’t indicate a new 1932 depression. It means that covid scru-edu everything. The old signals are defective.

6) Once equilibrium will be found with the European rates and Chines

import JP will be able to raise rates.

7) JJ will cut gov debt, woke the woke when the radical house will be lost, avoid bloody wars, lift real wages.

8) Shi Shi Ping lift the middle class from zero to 700M, built a thriving economy, avoid wars.

During one long and uneventful drive I was wondering – will that piss-ant 0.25% Fed rate hike produce desired inflation-curbing effect, or any effect at all ?

Then I had an epiphany.Reasoning by analogy if you wish.

When large amounts of prescription drugs and doses of radiation fail to cure the patient (allopathy) – some substances diluted to 1:20,000,000,000,000,000 will heal the patient in no time (homeopathy).

“And He saith unto them, Why are Ye fearful, O Ye of little Faith? Then He arose, and rebuked the Winds and the Sea; and there was a Great Calm.”

Godspeed Our Father of Easy Money Who Art in Eccles Building !!!

Paraphrasing Ronnie Reagan – dont worry what they think about you right now.You should care what they will be thinking about you 100 years from now.

AI:

10Y = 2%, mortgage = 4%, cpi = 8%.

Mortgage cost is low. The value of debt today will be nothing tomorrow, because inflation is 8%. This ids better than the 80’s and the 90’s.

Good logic.

The only drawback I can see is, unlike the 80s and 90s, the government’s balance sheet (since GFC and over-boosting markets and pandemic) is spent to the brink. In the 2000s, it was the household balance sheets that had underwater (negative) savings, and look how that went for their mortgages. Plenty of folks rode that mortgage right out of the middle class (and now, it seems, some of those frequent website comments, hurling vinegar and blame everywhere). If we tip into a deep recession, the US gov still has Uncle Fed to bail it out (just create money). But the bond markets might balk this time at government’s attempting to bailing out profligate mortgage holders. How many times can we rinse and repeat a bailout of that scale?

“spent to the brink”

There is no “brink”….unfortunately.

The money supply, and the Fed balance sheet, should be tied to the demand for money as a result of an expanding GDP, not the whimsical decision making of the hijacked Fed and their network of insiders.

Pretty interesting how Berkshire had developed since the GFC:

1. Cash

2. Insurance

3. A railroad

4. Apple stock

5. An electric utility

6. Other

Please tell me that the Zillow Rent Index is make-believe, and is someone’s dreamed up imagination!

I rased rent over 20% this year, and appartment rented in a day, Austin TX.

It is not dream, renters are f**** up.

Hedonic adjustments are someone else’s head on your body, telling you how you are supposed to feel.

They should just put THC in our drinking water. With everyone thus becoming super happy and chill, the hedonic adjustment of water will cause a deflationary watery collapse of CPI and the FED can ease into the negative. Problem solved.

Such a weird time. A million extra deaths of mostly old people. Everyone fleeing to SFH and housing skyrocketing. My neck of the woods 40% yoy increase in all housing. Higher for lower income. Yet somehow rentals and namely apartments on long waiting lists and massive price increases.

Something doesn’t add up. Oh wait yeah it does, real estate is being subsidized. Anyone that can throw around a few tens of thousands can participate in the speculative bubble. If the FED wouldn’t have kept rates so low and subsidized the real estate market with buying MBS none of this wouldn’t of happened. Or am I missing something.

Less people, high numbers of new construction (granted, limited completions), housing in a bubble yet rentals are also in a bubble and it is scarcity from top to bottom. I can’t help but think there is mountain of uninhabited shadow inventory that completes the story. I’m just some nobody who’s not in the know but I still suspect a major housing crash.

Plus if your stock holdings went up by 5X since the GFC why not sell some and buy your dream home. It’s how asset inflation eventually becomes real inflation

Wolf,

I recently listened to your interview with Adam Taggart from December (good stuff), and it prompted a question: Do you think that the FFR will have to be raised above the inflation rate to beat inflation (as in the 70s/80s), or do you think that rate increases combined with QT, along with the likely result of those actions loosening the labor market, would defeat inflation without the FFR necessarily needing to go higher than inflation? If reversing inflation requires FFR>Infl. (WITH inflation at 7+), I’m afraid that the whole economy is about to get a world-scale beat down.

I asked a similar question last month, and you suggested that a major QT dump might rip off the band-aid without recessional chaos, but wouldn’t that wreak havoc in the bond market, which can cascade into other realms?

QT is a huge tool. They didn’t have that before. I think they understand that they can use it to push up long-term yields and raise short-term yields only moderately. I think shedding $5 trillion in assets over the next 3 years and push short-term rates up to 3% or 4% can probably do the job. Big asset price declines will take the wind out of inflation, and lots of people will go back to work, and the labor shortage will disappear, and things will balance out…. if the Fed has the fortitude to do that.

Wolf, help me here… the spread between 2’s (or 1’s) & 10’s has never been more than like 3%, right? If inflation is running at 7-10% wouldn’t it take quite a bit more on the short end to quell things?

The Fed only controls the FFR and during the 80’s they had it up to 18% to crush inflation. If you are saying a FFR of 4%, well that’s really no higher than what we saw in like 2005. Isn’t inflation running hotter than that?

I’m not questioning your infinite wisdom, just wondering how high you think the FFR will have to be to get this under control? And yeah, maybe the answer is time will tell.

Just seems we’re in uncharted territory that doesn’t even look like the 80’s… yet!

WolfGoat,

Short-term rates have little impact on the real economy because they don’t impact borrowing costs for consumers and businesses. But rising long-term rates increase borrowing costs for consumers and companies and put downward pressures on asset prices (bonds and housing for sure, and stocks to some extent). So to cool this overstimulated economy, the Fed needs to use its tools to nudge up long-term rates.

The new tool for pushing up long-term rates is QT in large amounts, and the effects of much higher long-term rates will change the inflationary mindset and remove the fuel from inflation.

An EFFR of 3% and a 10-year yield of 6% or 7% might do that. Or maybe an EFFR of 4% and a 10-year yield of 7% or 8% might do it. Maybe it will require more.

It’s hard to say off the cuff how far long-term rates would have to rise to shock businesses and consumers out of the inflationary mindset. But QT is the perfect tool of doing it without having to raise short-term rates into the sky, like Volcker had to do.

Thanks Wolf… makes sense! And keep up the good work, much appreciate your insight!

That’s a very big IF!

My guess is that they will continue easy money policies because the alternative is political suicide.

However, one thing is clear. The Fed employees including the board will continue to trade their accounts with great results…for them.

Bottom line: we’ll see

Cheers,

B

Best evidence, according to academic research, is that QE had a very weak effect (aside from its more difficult to measure psychological effects), so it stands to reason that QT would have similarly weak effects, although it might possibly frighten investors, most of whom seem to equate it with adding money to, or subtracting it from, the real economy, which is not the reality.

Hey MikeSmith, you had me with the “weak effects”. I can see that QE (and QT) would have minimal impacts over time because there is soooo much more quantitative money that has been added to the economy, that the impact of what the Fed does there is reduced. Kinda like crack!

But you lost me at “adding to, or subtracting from the real economy, which is not reality”? Can you explain that? I think adding $25T “dollars” to the world economy since 2008 has had a significant impact on ‘reality’.

In fact, as Wolf is trying to explain to folks, the ‘reality’ of the US Dollar being the defacto medium of world exchange may be changing. There’s just too much of it around to be worth anything.

Bitcoin anyone?

mike

” so it stands to reason that QT would have similarly weak effects”

Holding things up, like bond prices looks like little effect or motion.

But when you remove the stilts, the platform collapses….

collapses from the unrealistic to equilibrium…..and the question is ” will we ever see equilibrium levels with Fed policy neutral?”

If QT has such a weak effect, why is Wall Street so frazzled about it?

If the Fed unloads its bonds at the same pace it put them on its balance sheet ($5 trillion in 24 months), I doubt that there is a “weak” effect. I would expect fireworks. Even a small amount of QT created some fireworks last time.

John Hussman has claimed that QE had a negligible effect on economic performance in the real economy, aka “growth”.

This is entirely different than the impact it had on asset prices.

You never know when a long term trend will get broken, but long term trend would say Fed will not get very far in rate hikes. I will vote that the third one will be all it takes to roll over the economy.

The economy can handle way more rate hikes than the markets can…

The Fed, in addition to promoting inflation, has also quietly and uncontested shifted greater focus to markets ……

What will the markets think?

IMO, fluffing markets then defending the “fluff” is a fools errand…and expensive one for those who are not getting the fluff benefits….for it is they who are being stolen from to support these markets via the NEVER BEFORE seen disparity between rates and inflation.

You cannot look at the past 20 years and draw lessons to be applied to the current situation. The last time inflation was spiking like this was in the late 1970s. That’s where you have to look for inspiration.

Rents are going up because people want to live here, and do business here.

Lol!!!

Sometimes the shortest, simplest posts are the best.

Ah, but cardboard boxes, while also going up in price are much cheaper than apartments, condos, townhouses, and single family homes. All averaged together, as more people live in cardboard boxes, rent inflation will actually turn negative.

Most Americans live pretty high on the hog as far as housing. Most of the world probably thinks we are nuts complaining about house prices while we prepare food in a quartz countertop and have $15000 HVAC system.

$15K next year… $11K this year… just bought one!

It is difficult to hold a job while living in a refrigerator box. There was a homeless man in Fort Myers on the local TV news. He had a job washing dishes.

Remember an old song by Roger Miller, “King of the Road.”

Nationwide rental vacancies are low at 5.6%. That is the lowest since the 1980’s.

A good example of how it is that the CPI is a lagging indicator of inflation. We will see more upside pressure filter into consumer prices as the many items in shortage begin to come into balance. The price of an item you can’t buy is infinite … but for that reason also isn’t yet reflected in the CPI.

I wonder whether the reweighting of shelter in CPI-U from 33.3 in 2021 to 32.9 in 2022 is just coincidence. It may not sound much, but for an item that is expected to increase so vigorously above the the rest in the coming 2 years, the 0.4% difference in weighting will have an effect that can actually reach a 0.1 difference in the rate of inflation. To be honest, I am not entirely sure what the methodology is how these weights get determined from past data and how much this can become a directional fudge metric used to down-calculate CPI.

The January CPI used December weights. The December CPI used November weights. We won’t get the new weights, which will be for January, until the February CPI comes out. Every two years, the BLS re-calibrates the weights and implements them for January.

But Weights always adjust a little every month throughout the year. I just happened to track this in preparation for the Feb CPI with the new weights:

Shelter:

Oct: 32.425% (Nov CPI)

Nov: 32.393% (Dec CPI)

Dec: 32.946% (Jan CPI)

These monthly adjustments up and down are too small to make any noticeable difference. The once-every-two-years adjustments are bigger.

1) If next year cpi = 5%, y/y = minus 3%. // If next year rent rise by 3%, Zillow rent y/y = minus 12%. The dreaded N-word : negative 12% rent doesn’t mean 30% vacancy, deep recession or gluts.

2) It means that the Wimmer inflation was beaten. The economy is not shrinking, it became normal & stable will less extreme charts and crazy spikes cluster together. With less poisonous remarks against JP.

3) Great economy.

4) Get used to negative/ positive y/y cpi and rent, up and down for 2-5 years, until the system decay, have a normal pulse.

I wonder why the gov cannot step in and keep oil companies and landlords under control

I will not address landlords (the answer is too complex), but I will address oil companies. Oil companies do not control the price of oil. If they did, the big drop in oil prices in 2014 would never have happened. The truth is that oil is getting more expensive to find and extract than ever before, and the oil prices that have prevailed since the Great Recession have not been high enough to finance it. For example, even when oil was hovering around $100 a barrel for several years prior to Nov 2014, the fracking industry as a whole had negative cash flow. Oil prices MUST go much, much higher, or there will be no oil. And when it does, energy switching by industry will drive other energy sources much higher too. Get ready to pay through the nose for energy and for products that require energy to produce. Geologists (some of them anyway) have been warning us since the 1950s that this day would come, and the wolf in now at the door. For a long time, oil was, relatively speaking, cheap and easy, like the girl you don’t take home to mother, but those days are about over. There is still oil in the ground, but it is increasingly expensive and difficult, like the girl you will probably marry.

….like the girl you will probably marry! That’s hilarious!

I like your assessment Mike, pretty spot on. And with global tensions rising, that oil is going to be bartered and fought over like no tomorrow!

Is that really true? Oil is getting more difficult to get, but there has been a lot of capital investment and innovation. Are you forgetting that oil price is measured in devalued fiat?

Good one.

mikesmith

I don’t know if oil is getting more expensive to drill for, very probably true but I do know that oil investment has dropped. It takes, on average, around seven years to get from starting to actually getting the black stuff. They say we are coming to the end of oil, rubbish, we are still in the age of coal (world wide) If they don’t invest in new oil fields you can almost guarantee that by 2025-30 we will be running out of available oil in greater numbers and they are not investing.

Interesting times ahead

All true but the short answer is rents can be controlled by local govts but the price of oil is set in the world market. The only way a local (or national) govt could provide a lower than world price would be to subsidize it.

OR tax it less. In Canada a third of the price at the pump is tax. What ever, the govt is elected, but part of the final tax appears to be a tax on a tax. The product is valued and taxed as it leaves the ground and this value appears to be the base for taxes at further stages.

BTW: some gas stations used to have a pie chart on the pump with several ‘slices’ showing the breakdown of the price with a relatively small slice going to the station. Haven’t seen one in years.

The same argument could be made for housing.

KZ-

Are you talking price controls?

Does gov’t price control ever work?

The fed has attempted to control the price of money, and the prices of bonds…. And here we are.

What do you mean by “keep landlords under control”?

Sorry to sound blunt but the price of housing is up 30%, so why shouldn’t rents (of said houses) not go up commensurately? Landlords aren’t running a charity.

The mortgages they pay on rental properties have not magically spiked by that much for assets they already have as part of their portfolio. I’d bet the majority of their holdings they have had for longer than the last 24mo.

If asking prices went up that much it’s because landlords have universally raised rents..

Who knows what landlords own on which building. Rent/cap rates are typically a function of the asset value. Also, property taxes, repair costs and other costs have risen too.

The point is that it’s not landlords’ that have caused houses to go up 30% in value, it’s mostly the result of insane govt./Fed policies.

Max: sorry but that data is available. Most apt owners are long term. They held some for decades then suddenly ‘renoviction’

Now, I’m not saying its unusual to love money but this is the purest example of Fed policy making the rich richer at the expense of the middle/ lower/ poor. It doesn’t directly hurt anyone if the FAANGS double but it does if rents double over five years.

MP- Weren’t many landlords legally compelled to charitably forfeit their rental income through CDC”forbearance”? Haven’t many landlords taken cynical advantage of circumstances lately to raise rents beyond their debt-servicing and profit requirements? There’s two sides. As a renter, I accept given conditions. But as I’m financing your wealth formation as long as wealth is being”invested” in houses instead of some other, more appropriate goods, it’s not unreasonable to ask that I don’t have to finance 100% of your asset if it’s appreciating much faster than it’s value as shelter to the average renter. The rent paying the mortgage and maintenance is often true in boom economies like the oil patch, but worker bees in a regular hive can’t afford to buy real estate empires for the queen, the daily honey is burden enough. If one covers the other, other than credit or time limits there’s no reason to rent, and bad credit gets flushed regularly. I’ve worked on other people’s houses for decades, and the last thing I want to own is a house. Doesn’t mean I want to buy anybody else one. Rent should be reasonable. It’s certainly not temporary ownership.

“Rent should be reasonable”. Well, by that same token house prices should be reasonable also but they’re not. If stupid govt. and Fed policies hadn’t made house prices go up so much, rent, which is a function of the, wouldn’t have gone up as much either.

The landlords tripped all over themselves to buy up the housing at too high of cost. They can try to pass on that cost, but you can only extract so much from the wage earners. They are also under the belief that they will be bailed out which is why they bid it up so high.

The government screws everything up -stay out of government control things would be better

Why do you trust the government to do anything right?

They are the primary ones who screwed everything up. They created this inflation problem through monetary and fiscal policy.

We can also debate whether lockdown should have happened and if so, the extent but it was a voluntary political choice.

Apart from the baked in CPI increase that Wolf describes, I think that inflation has now truly been ingrained in people’s minds. For many it is their main worry now. And that is a self-enforcing spiral that needs either a big crisis or massive interest rises to fix.

Keeping interest rates far too low for far too long has been the policy error of the century.

Inflation being truly ingrained in people’s minds means they will spend less. A lot of demand was brought forward during the health scare. The current demand for products can’t hold up, nor the prices.

There is no strong economic foundation for this demand. It is born of profligate government spending on perpetual emergencies that never amount to anything.

If people spend less it does not mean prices are going down. We are not in free capitalist economy anymore.

Are you expecting government to stop printing? This is a very slipery slope for both parties. Path of least resistance is printing.

When you see me stacking precious metals and buying a gold miner which I did this year then you know some of us are worrying about inflation getting out of control.

The policy error of the century was the very existence of monetary policy.

Monetary policy is a form of central planning. No one knows the “correct” interest rate (there isn’t one) and no central planning committee can possibly “manage” an economy of 330+MM individuals.

It’s the ultimate economic hubris,

As Wolf has said, The Most Reckless FED Ever.

1) JP cannot raise EFFR to 21%.

2) US10Y = 2%. Mortgage = 4%. CPI = 8%.

3) The cost of debt is low. Today debt will be nothing tomorrow.

4) US corp will pile on new debt.

5) Individuals will finance themselves with higher debt.

6) US gov will increase the debt ceiling, because today debt will be

nothing tomorrow.

7) A new bubble was born : debt binge charts.

4% inflation and 2% yield = -2% real yield

10% inflation and 8% yield = -2% real yield

Same real yield, but are these the same situation for a debtor? NO!

In the second scenario, the debtor has to come up with significant cash to pay for debt service. Will he have access to that kind of cash? Most people overlook that point.

Interesting in this context is also Japan, which has a gargantuan debt pile but pays very low interest rates. Still despite of the low rates, a massive amount of tax revenue goes to debt service. Rates don’t have to rise very much there for debt service to eat up 100% of tax revenue. Will they then resort to print the interest too?

They may get away with that, but maybe not. What will such a scenario do to the value of the currency? If the currency falls and import inflation makes things worse? Questions…

In my opinion, higher inflation has changed the game. And not for the better. Central banks should have counted their blessings when inflation was “too low” and they were still able to expand their debt without getting punished by the markets.

Good saying about the real economy “The Fed can change how things look, but can’t change how things are”.

Taxes also change the above two alternatives. The negative yield is higher on the second option, after tax.

So it used to be that the interest rate controlled government spending by increasing the debt servicing cost. With low interest rates in recent past that debt servicing cost is relatively low so the debt has ballooned. I would think that the current debt is already financed at lower rates so rising interest rate would impact future government spending more directly than current debt.

TXRancher,

“… rising interest rate would impact future government spending more directly than current debt.”

Yes, that’s how I see it. I think much higher interest rates will have a salubrious effect on Congress.

Nuto closed end fund

Why should landlords and realtors tip the homeless? Because they graphically demonstrate what happens if you don’t pay the extortion money.

Banks are notorious for borrowing short and lending long. Let’s imagine they’re borrowing at the 2 year yield and lending at the 10 year yield.

The 10 year/2 year yield curve would reflect this. Over the past 30 years this yield curve has been slightly negative only twice for very short period of time. The rest of the time it has cycled between 0% to 2.5%. Now subtract 7.5% from that range to reflect inflation giving us -7.5% to -5.0%.

Historically, Americans have been willing to lend to a credit worthy borrower at 3% real return. This protects him from the risk of borrower defaulting and provides him with a small gain. That means unless the lender gets 8% to 10.5% he is not doing it. The current mortgage rate is what? 4%? That’s a shortfall of 4% to 6.5%. Lenders aren’t going to do it.

And by lender I don’t mean the banks, they’re just intermediaries. Savers are the lenders. But government comes along and guarantees these loans. This puts the taxpayer on the hook. And the taxpayer, wearing a different hat is, you guessed it, the saver.

So government is forcing savers to make loans that they don’t want to make.

Is it any wonder everyone’s poor except the 1%ers?

Pensions and insurance companies have offsetting liabilities, so it makes sense for them to lend long.

It doesn’t for anyone else, except to speculate on interest rate movements.

Moral hazard from monetary policy and government guarantees has turned the financial system into a casino where TINA and FOMO make it profitable or “necessary” to become a gambler.

“TINA and FOMO make it profitable or “necessary” to become a gambler”

Yes. I don’t want to gamble in the stock market, it’s a poor use of my time in terms of real production, but it seems necessary to maintain my purchasing power. If all the time and effort spent speculating were redirected towards real production, we would all (except the FIRE economy) be better off. However, to make the change, a non-inflationary currency system is needed.

the term for this as used by anyone around the time of Adam Smith was “rentier”, someone deriving unearned income.

As productivity has risen the “slack” between our current productive capacity and the capacity required for the necessities of life has widened. This opens up more and more room for rentiers to siphon off surplus without most missing out on anything really serious (food/shelter). Yes there are homeless but you get the point.

The more productive we become the more room for parasitic behaviour. What ought to be happening is the suppression of rentier activity, which would then allow us to cover our necessities more efficiently, leading to a 4 and then a 3 day week.

Instead we see surplus siphoned off, meaning we never get to work less. The lack of a land value tax enables the privatisation of collectively created value, driving up rents, which saturate wage gains.

Why is nobody asking the question “how come we have computers and amazing tech now and we are not working less?”. The more progress, the more slack after necessities, the more rent is bid up. This also exacerbates inequality, leading to more poverty for those left out.

In the current system no matter how much productivity gains we enable, we will always have rent take up all the extra value created. The more efficient we become the more necessary it becomes to join in on rentier activity, or you will be left behind.

Why is it that wealth always accrues to the top 1%?

Consider a game of Monopoly. All players start out equal with same amount of money and equal chances to succeed in the game. Utopia, right? However, if played long enough one player will own the board. Why is that?

It is because the game, while providing equal chances, is not symmetric. You are out of the game once you hit $0.

Our economies work on a similar principle. Regardless how much money you give to the bottom 50%, it accrues immediately to the top x% because the money is spent as they receive it. It is spent on goods and services that are provided by the top x%. This seems to be a universal law regardless of economic philosophy (capitalist, socialist, communist, feudal,…).

The only way to change that is to encourage savings. That is the silver bullet to reduce inequities.

Saving is for losers as things stand now.

Everybody knows the true inflation rate is around 15-20% @ a minimum, and what kind of interest rate can you get on your savings, 1%?

The entire point of the game of Monopoly was as a demonstration of the teachings of Henry George, as detailed in the second best selling book in the 1890s after the bible, “Progress and Poverty”.

The original game was called “The Landlord’s Game” and had two sets of rules. One set of rules is the set you know today. The other set has land value tax and UBI.

For those who want to know more, google “guardian secret history monopoly”.

Isn’t it amazing that:

1. nobody has ever heard of the second best selling book of a decade

2. nobody understands the point of a game we’ve all played for hours

For more information on land value tax itself google “Frisby youtube simple guide land value tax”.

Regarding your point of the money “flowing up”, as per Churchill “land is the mother of all monopolies” and also see Ricardo for “the Ricardian theory of rent”. Plus perhaps read up on how monopoly prices are set (by the highest bidder thereby saturating all income).

Nobody has replied to your comment at the time of writing to point out this about the game Monopoly or any of the other points I’ve raised.

georgist,

I just watched Frisby, simple guide to land value tax.

I just read the secret history of Monopoly and learned about Lizzy Magie, the true inventor of the Landlord’s Game a/k/a Monopoly.

And I downloaded the pdf Progress and Poverty and just started reading it.

Progress and Poverty looks like it will be thoughtful soulful reading.

Now I think I understand your name.

One yank down, 300,000,000 to go…

Actually 150,000,000 to go as over 50% are at 6th grade reading level or below, so I’m not including them.

Please for the love of god, after you read about it and think for all of 5 minutes, tell other people on this board how prices are set on monopoly goods.

Actually just to say about P&P, Henry George was an absolutely amazing human being. His love of fairness just shines through in his writing. He does so without malice. Really the only historical figure I’m aware of who exuded this quality is Nelson Mandela.

It’s a lovely read for the deep sense of justice alone.

For those seeking a quicker read, Bob Drake did in the present century a modernized/abridged version of Progress and Poverty, Free pdf or audiobook at

When playing Monopoly, if you get hotels on Orange or Red, you will win.

Two requirements to level the playing field include ending the buying and selling of government favors along with sound money.

The overwhelming majority are in favor of activist government. They just want to strip their opponents of their political defenses to plunder them.

Rich or poor, most at least dislike inflation, but most in modern society concurrently love artificially cheap money and ultra-loose lending standards.

You can’t have one without the other.

Without low rates and ultra-loose lending, most American’s living standards would decline or plunge and would have been lower for at least the last half century.

Without big government and the loosest credit standards in history made possible by central banking, the 1% would be a lot poorer.

I totally disagree with this.

Cheap money and the financialization of land has 100% made the poor way poorer.

Your logic ignores how prices are set. The looser money is the more people can bid up housing. This hurts the poor as the cost of carry makes it viable, month to month, but the principal still requires paying down against stagnant wages.

Georgia-

I think you’re missing AF point. He’s pointing out that the average joe wants both low inflation AND low interest rates.

Seems to me you’re disagreeing by saying that rate manipulation (“looser money”) lead to higher house prices, and he agrees.

Where I suspect you might disagree is in the degree of how “activist” the government should be in the market pricing of all assets, and other questions of redistribution of wealth.

Maybe the 1% AF, but IMHO MOST of us would be and would have been better off if we still had 5 or 6 per cent interest on our savings, as my grandma lived on her last decade or so, etc.

The point of the loose money is the direct transfer of ”real wealth” to those who have the most access at the least cost, i.e. hedgies, PE, the very ”old money folks”, etc.

As we saw personally in 2015 bidding for housing against big money, even as a cash buyer we could not get a couple of banks to deal with us because they were in bed with their big boys pals… and this information came from an actual competent and honest realtor we worked with at that time…

From many reports, this time is worse, and likely to continue to get worse.

One of the dufus fed heads came out this morning and stated…..lets not overdo it with rate hikes…….hahahaha……..they have not done a thing yet except talk about nothing…..still stimulating to beat a bat out of hell…….with inflation raging……..and he want to not overdo it…….hahaha……what a bunch off limp d—-s.

The main effect of rampant inflation is that people get scared. When people are scared they just stop spending and bang, you are in a recession. If inflation goes mad and if people get really scared, (bang times 2) you are in a depression.

Works every time….

Which one will the USA choose…..

or can the Fed print its way out……

No, of course not…..don’t be a Silly Billy

I remember a chain of events of the S&L Crises, Black Monday, Gulf War and recession that had alot of people scared heading into the 90’s, and SoCal RE lost about 15% of its value during the first part of that decade. It wasn’t until the second half of the 90’s that confidence started to return.

Then of course the 07-09 RE bubble popping, stock market crash and recession. FOMO turned into FOBWO – Fear of Being Wiped Out. As stocks plummeted, instead of buying for the long haul at cheaper prices, many people stopped their automatic 401K contributions. Fear.

Fear of one kind or another drives markets up, and drives markets down. Fear is an emotion, and unregulated emotional responses shuts down the brain’s rational thought center.

1) Zillow rent = 15%.

2) UST cheapest rent is 2% – 8% = minus 6%. o/n = 8%.

3) US Treasury collect rent from the smart money, China & Japan…to park in the basement garage.

3) The higher the inflation the higher China and Japan rent collection.

4) US trade deficit with China have peaked in 2018.

5) Despite shutting down the whole economy in 2020, being comatose for one year and hopelessly dependent on China’s infusion, until we know what we don’t know, our trade deficit with China is getting better.

6) US gov charge China high rent.

7) JP pay the primary banks low rent.

8) To cover daily expenses the poor and middle class are pay c/c banks 30% rent.

9) Vacancies hover around zero, demand for credit is high. Today 25% – 30% debt will be nothing tomorrow, ex zombie accounts who have no tomorrow.

Stocks are again rising after FOMC minutes. Fed is doing what it’s supposed to do, pump up stocks and assets.

They will keep printing through March.

QE eternity is going.

Kunal,

Stocks “are rising?”

Dow -54 points

Nasdaq -16 points

S&P 500 +4 points.

Your trolling gets really copy-and-paste boring and old. Come to grips with reality that QE will end in March, that we’ll get our first rate hike on March 16, and that there will be more rate hikes this year, and in the 2nd half accompanied by QT.

Nitpick: there’s a 5% in the text that should be 15% (Zillow).

Thanks for the useful explanation.

Seems you misread it. This is the sentence: “In January 2015, the Zillow index showed rent increases of 5%,..” This refers to the left part of the chart, year 2015, when rents increased 5%.

Powell’s not going to act boldly until his job is secure for a few years.

But by taking Raskin’s Fed nomination hostage, for what appears to be reasonable cause (to me at least), the Republican senators from Wall Street have also put Powell’s confirmation on hold.

One suspects they may also have some “if you want our support…” requests of Powell as well?

Wonder what the negotiations are like in the back channels here!

Politically and on paper Powel’s no 1 job should be to control inflation.

However his and both parties REAL masters in Wall Street want him to keep foot on the pedal and inflating the economy and asset and stock prices. As long as he keeps doing this he keeps his job.

Measuring rent inflation only by the average of current rents is a bad choice for assessing current inflation. It lags the reality by months.