But wait… Supply suddenly burst from the woodwork when mortgage rates surged before the Housing Bust. And for a reason.

By Wolf Richter for WOLF STREET.

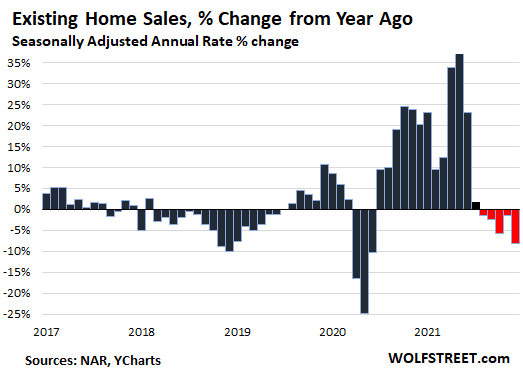

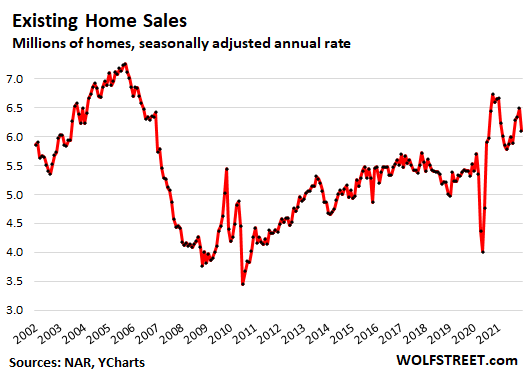

Sales of previously owned houses, condos, and co-ops in December fell by 4.6% month-to-month and by 8.3% year-over-year, to a seasonally adjusted annual rate of 6.1 million homes, the National Association of Realtors reported today. It was the fifth month in a row of year-over-year declines, amid very tight supply and rising mortgage rates (historic data via YCharts):

Seen over the long term, the seasonally adjusted annual rate of sales in December of 6.1 million homes wasn’t only below the peaks of 2020 but also well below the peaks during the 2003-2006 era.

Sales of single-family houses dropped 5.9% for the month and by 8.1% year-over-year, to a seasonally adjusted annual rate of 5.44 million houses.

Sales of condos plunged by 7.0% for the month and by 9.6% year-over-year to a seasonally adjusted annual rate of 660,000 condos.

By Region, the seasonally adjusted annual rate of total home sales dropped year-over-year in all four regions:

- Northeast: -15.7%

- Midwest: -2.6%

- South: -5.3%

- West: -10.2%.

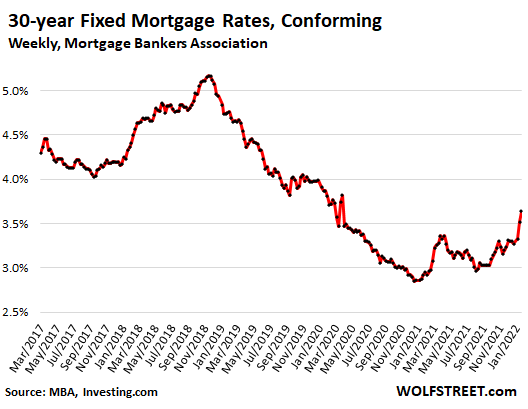

The scramble to lock in still low but spiking mortgage rates.

The average 30-year fixed rate of conforming mortgages in December was around 3.30%, which was up from November’s range of around 3.20%. But in January so far, mortgage rates have spiked. In the reporting week through January 19, the average 30-year fixed rate hit 3.64%, according the Mortgage Bankers Association (data via Investing.com):

The National Association of Realtors, back in its November report a month ago, expected the average 30-year mortgage rate to reach 3.70% by the end of 2022.

But the average daily 30-year fixed rate already kissed 3.70% on Wednesday, according to Mortgage News Daily data.

There are now two dynamics at play: As mortgage rates rise, more buyers are priced out, and they step away. But other buyers are accelerating their efforts to buy, no matter what the price, to lock in the still low mortgage rates.

“With mortgage rates expected to rise in 2022, it’s likely that a portion of December buyers were intent on avoiding the inevitable rate increases,” the NAR report said.

Buyers will do this until mortgage rates reach a magic level, at which point buyers begin to pull back. Mortgage rates beyond the magic level have the effect of cooling the housing market, which is what happened in the second half of 2018 and in 2005/2006.

Mortgage rates hit 5.0% in November 2018. And they hit 6.6% in the summer of 2006. And that was it for the housing market.

By the end of 2018, the stock market was in turmoil. The housing market was cooling off. All heck was breaking loose. And the Fed, which had been hiking rates and was reducing its balance sheet all year, was getting publicly hammered on a daily basis by President Trump.

At the time, inflation was right near the Fed’s target of 2.0% “core PCE.” So it in 2019, the Fed began signaling its infamous U-turn. It called off further rate hikes. By mid-2019, it ended its balance sheet reduction. In September 2019, it began bailing out the repo market that was blowing up.

Now it’s a different scenario: the worst inflation in 40 years.

In November, “core PCE” inflation hit 4.7%. The December “core PCE” inflation rate, to be released next week, will likely come in around 5.0%. And the Fed is starting to crack down on it – way too little, way too late, but it’s starting. So the Fed is unlikely to make a U-Turn while inflation is this red-hot.

Buying a home “now” to lock in a lower mortgage rate is a classic reaction to the initial phases of rising mortgage rates, also promoted by the real estate industry. It’s only when mortgage rates reach a magic pain level that sales volume dries up.

The NAR today also expressed this view that higher mortgage rates this year would hit the housing market and that existing-home sales would “slow slightly in the coming months due to higher mortgage rates.”

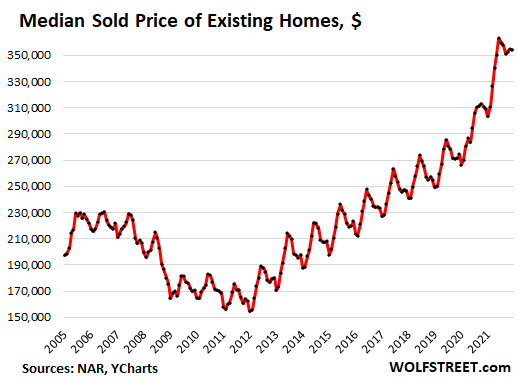

The median price spikes less.

At $354,300, the median price was unchanged for the month and was up 14.6% year-over-year. The year-over-year price spikes had peaked in May and June at over 23%. Since June, the median price has dipped 2.3%, a seasonal dip in the second half.

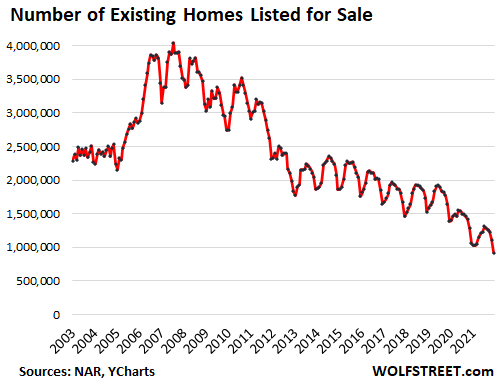

Supply of homes listed for sale declined to a record low of 1.8 months of sales. The number of unsold homes on the market declined to 920,000, seasonally adjusted.

But supply always comes out of the woodwork when interest rates rise and prices stall or decline. We saw that during the housing crash: All kinds of supply sudden hit the market, with investors that owned multiple homes being among the biggest group to just let the banks worry about those houses when buyers didn’t show up.

“Individual investors or second-home buyers, who make up many cash sales, purchased 17% of homes in December, up from 15% in November and up from 14% in December 2020,” according to the NAR.

Once homes are treated as investment products, like stocks, and not as homes, there can never be enough supply during a bull market. But when mortgage rates surge and when the market turns, those investors and second/third home buyers can easily put their vacant homes on the market — and they do. And suddenly, there’s supply coming out of the woodwork.

Note the storm surge of homes suddenly flooding the market in 2005 and 2006 as mortgage rates surged just ahead of the housing bust:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Sure hope that magic number is lower than 5% this time. I am not sure the Fed has the guts to let it even get that high.

From everything I read it sounds maybe a 3% 10 year treasury and a 5% mortgage is the upper limit before economy rolls over. Might be 2.25% 10 year and 4.25% mortgage.

Just wondering. Where are you reading this information? I haven’t see anything from a real economist that’s put upper limit numbers out there. Even Wolf just calls it the magic number without giving a value. Not that I disagree with the information your passing along, btw.

don’t care

I just purchased property

with CASH – a depreciating asset

Jeff Gunlach is one source, but there are others. Fed funds rate most likely will not be able to get to as high as last time because overall debt is higher.

Jay,

If you go to a site like multpl.com, you can track historical interest rates by month,

https://www.multpl.com/10-year-treasury-rate/table/by-month

And compare them with monthly SP 500 numbers,

https://www.multpl.com/s-p-500-historical-prices/table/by-month.

You can see that once 10 yr Treasuries were allowed to hit 3% (after many, many years of being strangled well below that – via Fed money printing/Treasuries purchases) all sorts of bad things happened to the stock mkt (which benefits when DC murders interest rates via Fed money printing/Treasuries buys).

There are a sh*t ton of investors who don’t want to be in the volatile, badly overvalued equity mkts…but they have been prodded there at bayonet point by a Fed which has kept 10 *year* interest rates at 0 to 2 measly percent for f’ing forever…the abuse goes back to at least 2002 and played a huge role in House Bubble 1.0…just like it has been playing a huge role in House Bubble 2.0.

Once rates are allowed anywhere remotely near true mkt rates (probably at least 9%-10% given the US’ 100%+ debt to GDP…) those investors run away from overvalued equities as fast as they can.

In the Fall of 2018, still pathetic 3% rates were enough to trigger a 20% decline in equities.

Gundlach thinks it could be as low as 1.5% fed funds rate that makes the market nosedive and the Fed stop. How that equates to 10 year treasury and mortgage rates can vary some, but 3% and 5% seem reasonable. Ultimately, these are all guesses and nobody knows anything about the future.

“I haven’t see anything from a real economist”

Me either, lmao.

Thanks for an end-of-the-day light hearted belly laugh.

A squeak from the IMF: ‘Fed tightening threatens world recovery’ CNN

Not sure what to make of it. Always associated IMF with tough measures on spendthrifts.

Guess it’s a case of them worrying about more fragile economies. Turkey might be a candidate for a BIG loan that the Fund wouldn’t want to make. In addition to usual, Erdogan might take IMF staff hostage when they tell him he has to raise rates.

Plus the usual SA customers.

nick kelly,

Wasn’t it just a couple of weeks ago that the IMF said that the Fed and other central banks should tighten to get a handle on inflation?

They’re STILL trying to re-re-re-bailout Argentina again again.

It is almost certain to be lower since the median home price has spiked since 2018. Higher rates + higher price = unaffordable monthly payments.

Buy now! Supply is tight (read: investors), rates are low (you’re welcome!), and for some reason people will just pay more to live in [enter city name]! Don’t lose that bidding war! Put down 100k and waive your financing and inspection, so you can be sure to land the house of your dreams! According to NAR and Zillow, houses will appreciate 17% this year!

Hahahahahahahahjajajahahahahahaha!!!!!

Thanks for the great article Wolf. A much needed reminder especially amidst a constant hoopla of real estate bulls. I’ve paid off my condo in Phx and am getting married in April. Likely going to start trying and will need more space at some point. Can financially afford it but tough to justify in this environment.

How great! Fyi, i recommend moving before any births-

Hey Tony! Congratulations! Nothing like a Spring wedding!

My daughter got married in April three years ago!

Eff you, J-Pow…

My fake Zillow estimate just dropped a fake $4000…

I.Am.Pissed…

You’re a loser… get away from me…

No, NAR forecast 5.7% and Zilllow 11%

Will easily be double digits price appreciation on real estate this year. Most of that due to inflation.

Thanks Zillow we sold our $385k house for $650k with no inspection and cash … we loved our sale proceeds $$$.

J-Pow versus Jeremy Grantham, Begin!!!

Jeremy Grantham (Jan 20, 2022):

U.S. households own real estate worth $41 trillion. Current Census data on median household incomes and median home sale prices suggest a price to income ratio of about 5.5 after accounting for a considerable estimated increase in incomes in 2021 (last datapoint was 2020). If this ratio returns to 4.0 – which is well above any levels prior to the mid-2000s housing bubble – this would be a 27% loss of value, over $11 trillion.

J-Pow:

“Don’t look up”

Jeremy Grantham has good letter out on where we are at with everything bubble. Big takeaway is house prices and stock prices always return to long term trend after bubble pops and sometimes overshoots a bit.

Wolf,

Thanks again, almost perfect timing, rolling over!

Tomorrow Delta options! Fed meeting next week, Powell appt. Feb.

Quick! Somebody scratch that fed dog’s underbelly before it pees $green$.

What will the median price be when it regresses to the mean? Not sure if Wolf’s chart goes far back enough…

Long term charts of price to income ratios will give you an idea. We would need about a 30% decline to go back to the average. My guess is, we’ll overshoot.

https://www.longtermtrends.net/home-price-median-annual-income-ratio/

No shortage of tents amidst this tight supply of homes..

Speaking of, FiNCEN/the Treasury is looking for comments on regulations they are proposing (that are a good thing &) that will effect housing prices- but currently those proposals miss the mark. They’re proposing requiring buyers of RE to disclose the real owners (beneficial owners) of any offshore or opaque LLCs buying property in the US. The regulations are designed to catch offshore money laundering.

When they required it in certain areas as a test program it effectively halted all cash sales by 70% in all areas tested.

The reason it might miss the mark is because it only requires disclosure of buyers for properties valued at more than $300K. So- it funnels money into lower end properties. & yes, there is a ton of hidden foreign money going into a good amount of lower end properties in the US. The only sort of properties that might possibly be affordable for working people. Re: comments FINCEN-2021-0005-0217 and RIN 1506-AB49. regulations(.) gov – till Feb 7.

So far, almost all of the submitted comments I read were RE agents, bankers and lobbyists asking for less rigorous standards… This is only going to put more pressure on working people if the -$300K exemption stays .. And increase homelessness.

Then what happen if (when) social unrest make foreign investors turn away from RE in the USA?

One can only hope

david calder,

Maybe an untapped market is luxury tents aimed at the average jo. A regular tent may be too much of a jump for the average jo, to drop from a house.

If we can put a touch screen in these luxury tents, we can make our own app ecosystem and get venture capital from silicon valley to start up the operation. The touchscreen will be hooked up to a solar panel making the operation green as well.

An I-yurt! A Mercedes dealership across the border in AL is running Sprinter ads to live in, seems like someone buying an overpriced utility vehicle could make the rent. The right boat, sure, but driving around in your house seems like a daily compromise.

The I-yurt will have an extensive range of options for purchase. It will start with a simple yurt equipped with a touchscreen retailling for $1,999 (yurt is a type of tent, often used in nomadic villages). The base I-yurt is sold at a loss.

Some of the available options include a heating rug specially measured to fit your I-yurt that has integration into your I-yurt touchscreen, this rug has integrated heating coils powerful enough to heat the entire I-yurt. If damaged the I-yurt rug cannot be repaired, but is replaceable. The heating rug requires an I-yurt power station. Available power stations include the I-yurt solar solutions and the I-yurt ultra green gas generator. All official I-yurt power stations integrate into your I-yurt touchscreen.

Also available is the I-yurt drop fan, this fan fits into a special attachment point in the ceiling of your I-yurt. This fan can be controlled only by the I-yurt touscreen or I-yurt display expansion. The I-yurt display expansion is a display that can extend the functionality of your I-yurt touchscreen and offers remote control access for your I-yurt devices.

The maxed out I-yurt costs only $49,999 and can only be purchased at official I-yurt showrooms and can be delivered to most target stores across the country for pickup.

The iYurt heating rug requires a proprietary power cord. For the first three years it will be called Lightning, then it will change for no reason to something called USB-c. Eventually, there won’t be a cord at all, anyway to control it, or the ability to turn it off or on. At that point you can only control it by speaking to it nicely and calling it Siri. At some point, that will no longer work either. Then, it will learn your heat habits by observation and decide on its own when to provide heat.

We all gonna be in a world of yurts!

Polecat,

Very nice…but probably too subtle for the room.

Thanks Wolf! Hubby and I are pulling back on a house we wanted to build due to some shady practices with the builder. Your analysis is giving us confidence in this decision. To explain in 2006, when we built our first home, we were part of that crazy bubble. I remember the predatory lending practices they were using in the showroom. On Tuesday, they did the same thing. They offered $0 down, proof of employment for 3 years, and a 4% payment. This is after the General Manager could not guarantee the house we picked would be the house we get. Due to supply issues – he is finishing houses with temporary doors, the walls are not poured correctly, and what we choose for color is not guaranteed. Then he upped the basic price by 35K due to lumber issues. I did not run away in 2006, but I am today. This all happened after he found out how much we could borrow. Yikes! There are some predators still out there!

An ignorant borrower does not equal predatory lending. If it’s fraud, that’s one thing but that’s not predatory lending but fraud. Signing a mortgage contract someone cannot pay back is their own fault, not anyone else’s. No one is responsible for anyone else’s economic ignorance or lack of self-discipline.

“Ignorant borrower does not equal predatory lending”

What would be defined as predatory lending?

I am afraid you are wrong August. Predatory Lending by definition according to Marriam-Webster is: the practice of lending money to a borrower by use of aggressive, deceptive, fraudulent, or discriminatory means. Deceptive is definitely the key-word. What they did is considered bait-and-switch.

Just my opinion, but I don’t think average person should get involved in a construction project. I have known too many that went wrong.

In my opinion the safest thing is to buy what is already finished and seller is in distressed situation due to life situation such as divorce or job move. You see completed project and can determine if it’s worth asking price

You are absolutely correct OS,,, but, after fixing many many new homes and remodels ”started” by amateurs as a licensed, etc., GC for many years,,,

”These times are different” DOES apply,,, for SOME folks who are willing and able to do their homework via the tons and tons of instructions videos, books, etc., some of which are really good IMO…

Without extensive study, in advance of the first tiny bit of work, forgeddaboutit already, bite the bullet and hire a pro…

Years ago, when getting $50/hour as a licensed carpenter/supervisor, I calculated I was saving money for anyone making more than $12.50, by doing the work SO much more efficiently, including acquiring materials, design modifications needed, etc., etc…

OTOH, seen some mighty pretty homes built by folks who had never picked up a hammer before building their own home…

Due Diligence,,, careful planning,,, attention to detail,,, patience, patience, and more patience,,, etc., etc

Seven “D’s” of property purchasing. Divorce. Distress. Debt. De bank. And some others I can’t remember.

And big tech anti-trust, forgot that one going on in the senate.

Out here in flyover, little inventory.

We have been buried in new construction.

After 08, have no illusions how this ends.

Its January and we have over a 100 jobs on the

book for 2022. For a Mom and Pop shop we will

soon have to cut off job requests for 2022.

We will see what % cancels plans with material cost increases, and

interest rates.

This sounds like the supply that comes online just in time to contribute to the crash, but what do I know?

Same in my small town. Minus 7% rates tell me that we are in unsustainable stimulus situation. Will not go on for very long because politicians like getting re-elected.

Some interesting things happening in SF East Bay, based on my observations (on SFH and condos < $1M):

— Craigslist rentals offering free rent. Not all lot, but I've seen one with 2 weeks free, another with 4 weeks free.

— A couple homes listed for sale that went off market. A couple more that went pending, and then back on the market.

— Quite a few homes listed for substantially less than the Redfin estimate.

— Increasing inventory (but still low, yes), especially compared to the week of 3 Jan.

— On the flip side, some houses are selling quickly (4-7 days), in general the competitively prices ones.

When you buys you a crib!

You puts money down!

My homie Too Short!

Be from the Oaktown!

City of Dope, I call it Oak

Can’t be broke, selling coke

Oh we pimp them ‘hos

When I make them sales

Got liquidity

To make Freakytale$

They say there is no there, there

But they weren’t talking about drugs.

Takes many nails to build crib, only one screw to fill it.

gotta say ”CLEVER” g!

thank you…

Better get in now….I see more fuel to light that FOMO fire..

The next two top selling points will be, interest raise is rising so get in now, to inventory is historically low and it will be this way forever.

Throw another bonus one in there…house is a perfect hedge again inflation so don’t miss out.

Buy NOW, suckas! Hold this bag for me! Take my troubles off my hands! Catch the falling knife!

Wolf, in your “By Region” section, I think you meant “Northeast” instead of “Northwest.”

surely did, thanks.

Northeast by Northwest

Rushing out to by moarrr

Before slipslidin down the maw

Of that inflated fed boar

Same ole story. Smart people buy when prices are cheap, and sell when expensive. You can always refinance a mortgage later, but you can’t pay a lower price after you purchased. The heard of sheep now being led to slaughter. History repeats, over and over again.

Wolf,

Update the copyright year on the bottom of your pages to protect the copyright. Currently lists 2011-2021.

Ha, thanks. Good catch. Done. I had no idea anyone was actually looking this far down EVER!

Condos are really hot here in the Swamp. Anything in a good location sells. Buyers want to get into a starter home and sellers want to get out before interest rates rise. It’s a marraige made in heaven. Investors are in there too as rents are playing catch up.

The current year can be done with javascript so you never have to change it again. Just google it.

Just takes 3 seconds to do by hand, once a year. No biggie. But thanks.

It’s really just as easy to do (3 seconds) this by hand (ONCE). Email me, and I’ll send you the code (can’t post here because it will be seen/blocked as malicious due to the script tags). It’s really just an easy TINY bit of code. Do it once and never have to worry about it again. Just saying…

I kinda sorta figured out Fed’s Master Plan which is “two-prongs approach” actually.

1.Median house price skyrocketed to $340K reaching “permanently high plateau”

2.In 2022-2023 median family income will skyrocket from $60K to $160K and will reach “permanently high plateau” too

3.Median house price/median family income historical ratio will revert to 2.2X and those looking at Case-Shiller charts (starting in 1890) will not suffer from cognitive dissonance.No need for paradigm shift,just a little patience…

4.And every family will be able to pay off not only piss-ant %% but the principal too.

Uncle Jerome,way to go,my heart is with you,stay the course !!!

And-shame on you,Fed bashers !!!

Genius!!!

Oh,and dont forget-money can not only be created but destroyed too…

“I was lucky enough to see with my own eyes the recent stock-market crash, where they lost several million dollars, a rabble of dead money that went sliding off into the sea.”

—FEDERICO GARCIA LORCA

A few points from the report:

“Both the total supply and month’s supply are at all-time lows on the NAR’s inventory count, since it began tracking in 1982.”

Note the total supply is at an all time low. 40 years ago, the economy was much smaller, so this is a huge statement.

This all time total supply low happened before the FED talked about aggressive rate and QT actions … so this is much bigger than buyers trying to beat the announced rate increase.

Also, the median price was reported 15.8% MoM, which is higher than your number and shows an acceleration in prices, unprecented for a holiday season, and 17% YoY.

My point remains as long as MTG rates remain far below inflation rates, buyers are in the market to take advantage of that arbitrage. While the FED and other central banks may raise rates to trim that spread, the arbitrage should still remain in place. The world’s central banks are woke and have no political ccourage. That arbitrage will overpower any FED speak.

“40 years ago, the economy was much smaller, so this is a huge statement.”

I think it’s just fueled by the price appreciation. Was it faster at any time during these 40 years?

I agree with Wolf that when it stalls the situation should reverse

“Supply” in NAR-speak ain’t supply as explained in any other market. In NAR-speak, “supply” is just the number of unsold homes sitting on the market. That’s low because transactions happen much faster than they used to, because internet.

The true “supply” to the market is the number of homes put up for sale in any given time period (NOT just the unsold ones!). Since most of those do end up selling, supply is very close to the total sales number.

Never doubt the ability of economists and marketers to distort language to your detriment!

Put more simply: If NAR ran grocery stores, they would say there’s “no supply” of food whenever there’s nothing on the shelf – ignoring the million bags they just sold, and the next million being unloaded behind the store.

Oh, and they’d also hype the shelf-shortage with “buy now before we all starve!”

There is no shortage whatsoever of supply. There are over 100,000,000 housing units in the country, many of which are under-occupied. The only shortage is one of willing sellers, and that’s a reflexive function of price history (aka momentum) – as Wolf explained.

The internet has made RE transactions faster, but right now, there is an actual shortage of homes available. Just like any other market, as demand rises, with supply constrained, the price will rise until quantity demanded is roughly equal to supply.

The total demand for houses is rising because of how many people are staying single or getting divorced. Without fixing this problem, the only way to fix the issue is to build more houses, cheaper. Current building and fire codes prevent more affordable houses from being built. A famous example of what some of these housing projects could look like is Riverdale (a large neighbourhood in Toronto, Canada).

There are many other options as well, such as building better apartment complexes. It’s important to note that as the booomers retire and pass away, they will also flood the market with houses.

The NARwhale seems ready to blow chunks!

Shields Up.

NO NO NO to all saying the net made ANY thing transactions faster:::

Decades ago, family and friends did transactions within a day,,, and sometimes the same property changed hands more than once a day,,,

and was fully ”transactioned” within hours.

Please try to get a grasp of what was happening in USA RE mkts, all over,,, but especially in FL and CA…

And then, if you really want to know where WE THE PEONS are being ”herded to” read ”The Rise and Fall of the British EMPIRE” by Lawrence James,,, that will corroborate similar RE: Roman Empire, but with a much more modern confirmation of Where WE are these days.

Sure, “IT” is ”different” this time,,, and to be sure,,, ”IT” is always at least some what different!!!

”WANTA BET??”

I would think that as boomers die off SF Houes will still be in demand but less interest in condos and townhouses. Oversupply at the lower end. Plus a lot of boomers will be leaving a lot of money to the next generation.

VintageVNvet,

I do know some RE agents and the internet has made RE transactions faster. In the past, more open houses had to be held for prospective buyers to have a good idea of the house and the neighborhood. Now it’s possible to see pictures & videos of the inside/outside as well as many other things, such as the info provided by online map services (Google/Apple maps). The map sites may show street views and local business and schools.

All the info provided online can be enough, even when there isn’t such house shortages, to better match buyers with available houses. There is less open houses and far more people have an idea of the house in question. When far more people have a good idea of the house in question, less need to come and see it. Because many people can only attend open houses on the weekend and proper open houses can only have so many people attending, this speeds up the process.

Most RE transactions aren’t with family members. As the population grows, an increasing percent of RE transactions will be with people you don’t know. As the population grows, the average person will also become poorer.

Used houses are up 17% in 2021 with mortgage rates around 3%. So real rates of -14%.

But used cars are up 37% in 2021 with auto loans around <5%. So real rate of -32%

So used cars are an even better investment than used houses …..

The last phase of bubbles is an increase in rate of change. Happens nearly every time. A blow off top. Sometimes that’s the hardest phase to resist, but it’s really a warning sign that irrational situation is occurring.

Hmmm. One thing I never hear mentioned anymore was all the delinquent mortgages that were in forebearance. What happened to those? Did all the people who claimed covid hardship not really face a loss of income and just took several months off from their house note and pocketed (blew) the money on worthless crap like cars 10% over msrp?

Those homes certainly didn’t flood the market. Seems to me like a lot of this run up is from free money helicoptered from the sky. Rates go up, wages get outpaced by inflation, the job market starts to normalize. A world of pain follows.

I like to think that for as unreasonably anti social as I am, I keep my ear to the ground. My ear only hears tales of people loading up on debt. Annectdotal evidence to be sure, but there is no resistance to over pricing. It is either ” Oh dear God, you better buy now or forever hold your nothing!” or, “Hey guy, it’s the good times! Why aren’t you having fun as well bud?”

Literally every family member I have has bought the nicest vehicle they have ever owned and bragged about only overpaying a small amount above or paying sticker price. Reminds me of when my aunt who only made money babysitting bought an escalade in 07. And then the repo man took it a year later.

I bought a new truck last year as well. New to me at least. It is about the third or fourth crappiest vehicle I’ve had. I bought the nicest truck I ever owned in 2016. Back when 5k in a used vehicle went surprisingly far. I sold it last year for a profit plus 50k miles. Buy low, sell high.

Trucker guy,

When home prices surge 30% in 18 months, no mortgage will fail. The homeowner can sell the house and pay off the mortgage and walk away with cash. Or the homeowner can get a bank to refinance the past-due mortgage with longer terms, and better rates — now that there is a huge amount of “equity” in the house. Etc.

Mortgages only get in trouble when home prices fall significantly, which means homeowners are upside down, and they cannot sell the house because they won’t get enough cash to pay off the mortgage.

A large portion of those mortgages in forbearance have already been cured either by selling the home, or by modifying the mortgage, or by refinancing the mortgage.

Twist comes when they go to refinance and rates are double the rate they had negotiated over the past 18 months. Then we have a pickle.

Do any other countries do anything like MBSs? Searched and found 2007–08 financial crisis and during the ensuing Great Recession, the Federal Reserve introduced a number of new, or unconventional, monetary policy tools. Among them were purchases of agency mortgage-backed securities (agency MBS)

Not all homeowners are willing to sell that are stuck in foreclosure. Those are:

Homeowners during refinance phase denied restructuring in underwriting due to self-employment (lack of standing), not enough income, or bad credit. Banks will not loan if the risk appetite is high. They refuse to sell because they are hopeful a lender will take their case.

Then there are some really bad apples that plan to live in the house for “free” until physically removed. They will not sell as the house will not make more then they owe on it. These individuals will flood the bankruptcy court letting the house go.

The answer to the riddle is Wolf’s last chart.

There is nothing for sale.

Remain to be see how this will evolve, a hyperinflationary event where people lose trust on the currency and withdraw all product from market or a prolonged pain where house prices stay elevated for years as inflation of wages catches up with the prices.

My bet is on the prolonged pain.

The time to be a homeowner was last year.

Welcome to renting for life.

Look at 2005 and 2006, how inventory suddenly exploded. These home are out there, but they’re not on the market, until suddenly they are.

If you’ve gotten a mortgage in the last 5 years, you would know that banks have been super strict regarding down payment and credit scores. Plus, banks dont hold the mortgages, so if things go bad, uncle Sam will be holding the bag.

I expect uncle Sam to do the right thing this time, bail out the MBS by bailing out homeowners.

Part or all their mortgage might be forgiven in such a scenario.

We are too far into this now for things to make sense.

Lunatics are running the asylum.

“…banks have been super strict regarding down payment and credit scores.”

That’s hilarious. That went out the window years ago.

Ever hear of FHA mortgages? Subprime 3%-down no problem. Government guaranteed.

But yes, banks won’t get in trouble this time. Most of the mortgages are now backed by the taxpayer.

To add to this Wolf, I have a family member who currently own 4 houses. One of which they rent out to me and my brother which works out for them since we perform all maintenance, upkeep, and improvements as well as pay rent.

With their retirement coming up I think fomo will reverse and those looking to cash out due to stock picking, retirement, cooling of RE causing fomo will list.

SocalJim brags about how successful he’s been for the last 20 years *cough* 2011 *cough* in RE like there will never be a reversal, but an ape made money during the .com era. Color me unimpressed. No salary data supports the current mania other than wild speculation and fomo from some buyer side pressure.

Actually, I have been in for more than 25 years … right out of college I started. And, the subprime loans were easy to get with next to no money down.

What I did right is I made sure I bought properties that seemed attractive if held for decades, and I also added a house only when I had enough cash positions needed to protect my properties during severe downturns because they happen from time to time. And, in 2007, when everyone was hitting the sell, I just hung on and eventually added after I was sure the bottom was in. I bought some properties low, and others high. In the long run, timing did not make that much of a difference. Dicipline did.

It took decades to build real estate wealth correctly. If you want to build wealth in than 10 to 15 years, real estate can be a big mistake.

I am seeing more house-for-sale signs in my area, but also more ‘price reduced’ signs too.

Equilibrium is setting in.

Who’s your daddy? It’s oil. We are fixing to get reminded, again,we live in the Age of Oil. Oil is our King. Stock Market,Housing Market any and all markets will be forced to kiss it’s ring and swear fealty . If Jerome does not kill inflation the King will keep liquidating untill accounts are settled. It will be ugly because the King will hurt as many as possible to achieve that end. It’s really always very simple as you start the approach to the end.

We’re getting close to bottom-rung hydrocarbon EROI sources like tar-sands. This should scare the shit out of everyone and is the most serious issue facing our species, I believe.

Regarding shale oil, the different formations seem to get depleted within 10-15 years, as I recall. The additional runway it bought us is limited and we should be building replacement energy solutions full bore (nuclear etc).

We do have large coal reserves, but that can optimistically buy us another 50-80 years using our US reserves (more including Canada), but the mining would do *enormous* environmental damage.

PS – With respect to using coal as a replacement, I am just estimating the energy needs, not the need for petrochemicals etc.

“We do have large coal reserves”

We also have a lot of Natural Gas reserves. 84 years worth at our current rate of consumption.

I have 35+ years in the oil and gas business. There is plenty of oil that has not been drilled for. Do some research. For instance, the Permian Basin in West Teas, which was thought as depleted 25 years ago, is now producing 6 million BBL of oil per day. And that’s being held back right now.

Horizontal drilling technology has opened up many old fields. The Bakkan has still a long way to go and 1/2 of it is in Canada.

I thought peak oil was supposed to be in the 1990’s.

Wha happen?

You are talking about production levels and I am talking about duration. You assert that shale allows us to squeeze more out – I agree. Look at shale production over time, broken down by geological formation. Production from Barnett and Fayetteville are petering out and Eagle Ford is flat or declining – this after about 12 years. Are you asserting that these formations are still mostly untapped?

They looked at the wrong peak! LOL

And they didn’t look in the right places….and we developed horizontal drilling with much improved tools. Seismic tech improved, etc, etc.

The people who yammered on about “peak oil” are the same crackpots who told us “your grand kids will never know what snow is.” The earth makes oil, and will continue to make oil long after human beings are gone.

Ivan: From a recent Permian article:

“The deeper drilling has found new, unconventional oil plays in some of the older strata, such as Wolfcamp, Cline shale, Strawn and Atoka formations, all located below traditional producing horizons. Targets for unconventional gas include the Devonian Woodford Shale, the Mississippian Barnett Shale, and the Permian Wolfcamp Shale. Low permeability reservoirs in the basinal deposits of the Brushy Canyon sandstone have also added significant oil production.

With over 500 rigs active and more than 30 Billion barrels of producible oil remaining, expect the Permian Basin to stay among the largest and most active hydrocarbon-producing areas in North America.

Anthony, unless my math is wrong, 30B available / 18M USA consumption per day / 365 days per year = 4.5 years worth of US consumption. And that is “among the best”, according to you. You are making my point, not refuting it.

Peter Schiff, he of Euro Pacific Capital and the host of the viral video that went “Peter Schiff was right” (about the 2008 Great Recession), refused to buy a home during the abnormal period leading up to the Great Recession. When he announced he was renting, a woman real estate agent contradicted him, saying, “housing prices never fall.” Schiff turned out to be right about that.

At some point in the next decade we may see a situation where construction exceeds demand, and the price adjusts semi-permanently. We already have a ton of construction companies out there, sawing and hammering, to construct new homes. If the demand can’t float them, they’re screwed. And more people will be living in apartments.

“housing prices never fall.”

That is such a dumb statement I just don’t know why people repeat that. All risky assets have trade-offs.

Three reasons for the drop in sales.

1. No/low inventory. You can’t sell what isn’t for sale.

2. Holidays. 10- 20% of buyers drop out of the market and a large portion of sellers pull properties off the market because of the holidays, family visits, celebrations etc.

3. Omicron. Don’t know about other places but in red Texas and Florida, people were being pretty cautious about going anywhere they didn’t have to.

Lmao. I’m in the blue part of blue California and people go wherever they please and do whatever they want. And if you don’t believe it, try finding a place to park at any shopping center or entertainment district.

4. People being priced out of the market.

CCCB,

Your second reason — “2. Holidays. 10- 20% of buyers drop…” — had little or no impact on the numbers here because the numbers are “seasonally adjusted” and account for this.

The sales figure is a “seasonally adjusted annual rates,” as I made sure to point out several times. The inventory numbers are seasonally adjusted as well. Since the holidays happen every year, the seasonal adjustments remove their effects.

What I didn’t mention – because this is seasonally adjusted data – is that people pull their homes off the market before the holidays when activity slows, and then they relist their home after the holidays. This shows up in the local MLS data which is not seasonally adjusted. Pulling the listing and then relisting it also artificially reduces the number of days the home is on the market. Nice trick.

For the West, another non-seasonal cause for weak comps would be the terrible rainy weather for most of December 2021 compared to December 2020.

Not sure the Omicron wave can be blamed, because December 2020 was also a serious COVID wave, and pre-vaccine. But there could have been higher demand for housing in December 2020 as people continued to scramble to get out of overcrowded (“COVID unsafe”) urban areas?

I’m in the DFW area, and I don’t think Omicron has slowed things down much at all.

Did someone steal your name for a day?

I think there is a difference between saying “RE will never go down….in the short run” vs “in the long run.” You have to have a time frame in mind. It might go down in the time of, say, a civil war [or WW III] but it would go back up again when everything settled back down.

After water and food, shelter is next on the survival agenda. Not crypto.

Peter Schiff permanently predicts doom and crows when, every 8 years or so, he appears right. If you want to spend actual money for this, power to you.

Aww, you’re giving away the secret to being an IYI Pundit!

Make enough different predictions – or just make the same prediction long enough – and you’re bound to be right some of the time!

With a few such “predictions” you can fool some of the people all of the time… as long as you bury all the wrong ones!

Most brilliant guy I’ve read is John Hussman. Analysis is deep and spot-on. But he’s been early and/or late (= wrong) for years and his funds’ performance is terrible!

If memory serves correctly, 2005 was peak sales and 2006 was peak price. But, with all the meddling the fed has done this time mixed with all the crazy free money policies from the White House, I’d guess this will go on for a while. Combine that with a midterm election that’s shaping up to be a shellacking for the dems and such a horribly corrupt Fed that wouldn’t even tell its blind deaf grandma to move off the tracks because there’s a train’s coming. This is such a messed up market. Something bad will happen, we all know that, but who know’s when? It will be bad when it happens, though.

Maybe not. Stuff started stalling in 2018 or early 2019. The PPP and FED bailouts have been holding it up- well, in addition to worldwide stimulus. That’s about 3 years of holding up a crippled economy. All it takes is a sentiment of the top and a few more huge margin calls on the stock market’s leverage.

“But supply always comes out of the woodwork when interest rates rise and prices stall or decline. We saw that during the housing crash: All kinds of supply sudden hit the market, with investors that owned multiple homes being among the biggest group to just let the banks worry about those houses when buyers didn’t show up.”

Awesome, thank you so much Wolf. I didn’t know that and it makes perfect sense. This is very timely for me. My realtor just talked me out of bidding on an way overpriced small rotting trailer on it’s own land. We both just *feel* it’s overdue for a correction, but this is good reasoning.. Made me feel a lot better today.

Dow steady Drop 2,084.26 last 16 days

Fed still printing

Jan 4th / 22 * 36,799.65

Jan 20th / 22 * 34,715.39

*

High 36799.65

on Tue, Jan 4

Low 34715.39

on Thu, Jan 20

Avg 36002.91

for past 1 month

NASDAQ in correction-land. I resisted the Pavlovian urge to buy the dip today, but my little oracles were screaming red for day’s close, and they were right. Now let’s see a fun-to-watch test of nerves in the bulls. Diamond hands, baby!!! To the Moon!!! Is that Lambo still in the driveway, or is it repo’d yet?

I was going to buy a couple of properties near SocalJim’s place, but then Netflix just dropped an egg, and now I have no moolah.

Sorry guys. But I’ll have to bail out.

Get Out! Scram ble!

There’s always going to be a dearth of supply when house prices are hyperinflating. The loanowners are making more on the appreciation than they are working for a living. Who would sell their house when it’s netting them $10,000 per month?

When prices turn, and suddenly all of these loanowners see their stucco sh!tboxes depreciating by $10,000 per month, there’s a mad rush to the exits. Same as it ever was.

There’s no shortages of houses for people to live in, only a shortage of speculative investments for house horny infestors – the scourge of humanity.

exactly. it’s infuriating having to explain this 100 times. there’s no such thing as a “lack of supply” independent to artificial demand. when the artificial demand dries up, the lack of supply becomes a glut of supply.

Which is why running entire economies based upon speculative bubbles is grossly irresponsible, and why the FED needs to be abolished.

agreed. i keep hearing people say that the fed had no choice because the economy was faltering, but they never stopped to think that they had cause and effect backwards. the financialization of the economy and perpetual bubbles has so misaligned incentives that we have a much less productive economy than we could have.

in america’s heyday, our best and brightest became doctors and engineers. now they go to play with money and derivatives on wall street.

” our best and brightest became doctors and engineers. now they go to play with money and derivatives on wall street.”

You’re so so right, and what a difference it has made. There’s a difference in the sorts of intelligence there, and the societal values that can emanate from that status. Preferably doctors and engineers need to have something at least related to empathy- how things feel or how things are used. Playing with numbers doesn’t rely on that kind of input from other human beings so much.

Supply is lowest at the top.

Yep

I’m seeing some of the old school landlords getting rid of their worst dogs now. Pacing it. Still overpriced AFAIC but going fast. Smart.

IMHO

All the Fed has to do is raise rates enough to drive house and stock prices down about 5-10%. There will be a mild panic with some homeowners/investors heading for the door. This will improve supply.

The Fed can then raise/lower rates slightly to keep the housing prices and supply stable and whittle away at inflation/deflation. Supply chain issues will go away with decreased demand and more workers will go back to work when their stock/BTC portfolio loses 10% and they can’t live off of it anymore. (This is already happening).

A simple control system problem. (With a million variables and inputs that could derail everything.) :-)

Other than greed, politics, and incompetence, I don’t know why this wasn’t done sooner. Wolf has been pointing this out for a long time.

I think we could have avoided the GFC fiasco in 2008 if:

1) The Fed would have reacted faster on lowering rates (people could refi before their house price crashed and they had to foreclose. Businesses would have cheaper capital to keep going and not lay off millions. The millions would have money to pay the mortgage or buy a house at a 10% discount and keep the economy going.

2) The mortgage companies would have had tighter restrictions on liar loans and proof of income. Supposedly that isn’t as big a problem now.

Just like a microburst hitting an airplane’s control system, any sudden jerk input could cause a catastrophe and not a soft landing.

Why on earth would you want to keep housing prices stable at a still absolutely insane level only 10% below today’s super extra quintuple insane level? That’s not even half of the downright bonkers pandemic spike.

I believe 10%-20% would work to stabilize prices. About the size of most downpayments + 1 year equity gains.

Most could still sell and break even. The mildly panicked will sell increasing supply.

2008 had an up to 50% drop in prices. This led to to an unstable control system where panicked homeowners walked away from their mortgages rather than try to sell at a hug loss. This created a further decrease in housing prices which was effectively a positive feedback loop causing more foreclosures. The Fed eventually stabilized this by lowering rates enough by 2012. 4 years was too slow.

Home prices have gone up well over 100% compared to wages. It needs at least a 30% correction if not more to decease the wealth gap. There isn’t much pity for investors if a good part of our population can not afford housing.

Money not gone to rent eventually goes to restaurants, clothing, hotels ect. all of which are hurting. No reason to protect one class of business people over all others.

Almost half of walk aways were from investors, who only made up 12% of buyers in the GFC.

SAIBB- re: your advice to the Fed:

You argue for better “stabilization policy.”

But to stabilize prices is to command prices. Command economies don’t work.

James Grant’s oft repeated sentiment, that the cure for high prices is high prices, leads to a better more sustainable, less error-prone outcome than central planning and control by the Fed.

Leave “stabilization” to the builders of tall buildings, and let the market sort out prices through individual exchange.

I think crony capitalism is inherently unstable.

It does not react fast enough (Current supply chain disruption is a good example) and needs some help from the Fed or the government to stabilize. Similar to if a hurricane levels part of the US, the government is sent in to stabilize and relieve the situation. Capitalism does not react fast enough (or it does with private price gouging).

The Fed needs to react with just the minimum stimulus or dampening to prevent the instability we saw during the 2008 GFC.

I see the argument that the market should weed out the dead wood and over-valued. Any interaction by the Fed may slow this.

I hear you, and agree that it would be wonderful if the government were enough omniscient to turn the right knobs and nudge the right levers just enough to avoid or repair all crises, and to help the little guy.

At least as far as Fed money creation is concerned, the fly in that ointment lies in the unintended consequences:

~unbridled federal spending,

~destruction of the purchasing power of savers, and ~societal encouragement toward indebtedness.

I’ll take the capitalists any day, even though many of them are pirates! (It appears a few outgoing administrators at the Fed were pirates themselves).

John H. And every 10 years like clockwork the markets to a face plant, sucking trillions of dollars down the rat hole. Great system that.

As long as the 30yr is this far below inflation, real estate will be well supported, IMO.

But, the amount of pyramiding that no one sees, the massive paper profits can evaporate so quickly in this most illiquid of all markets….bid to no bid in a hearbeat.

Keys in the mailbox just might happen again..

A massive destruction of wealth, the wealth that came so easy for the past several years to those set properly, is now entering a dystopic environment….

in cash lose (inflation)

in stocks lose (plus inflation loses)

in real estate, lose (plus inflation loses)

But was the wealth so easily created by money pumping really legitimate wealth?

Amen. It absolutely isn’t real wealth.

We used to call it paper wealth instead of real wealth, but now it’s not even on paper! It’s just digital wealth.

Those Digital Gains aren’t real until you sell, but now you’ve got to hold something else that may not be any better…

Time to get back to building something that produces, since that can keep up with inflation, and generate income to survive rising interest rates….

Midterm elections in November. Upset homeowners/stockholders might be bad for one of the parties.

upset young people that they are priced out of housing so the boomboys and girls can live great retirements isn’t great either.

I don’t think it matters that much. Only 56% of Americans own stocks, mostly in retirement accounts which aren’t meant to be day-traded on short-term fluctuations.

An amazingly small number of people hold any significant amount of stocks.

And homeowners don’t really care about the housing market unless they want to buy or sell.

The real deal-killer is inflation. Everyone is pissed off about it.

upper middle class people fretting about the supposed political problems that would stem from stock declines are an example of not realizing that most of america is not like them. all of their friends and family are similarly situated, with healthy portfolios, and assume that everyone else is like that too.

“Note the storm surge of homes suddenly flooding the market in 2005 and 2006 as mortgage rates surged just ahead of the housing bust:”

Wasn’t this largely due to people’s mortgage rates resetting higher? If so, the reoccurrence of this would seem to be much lower nowadays. In large part, it would be relegated to those with ARMs or at least until we find ourselves in a recession. And the FED with its QE & the Congressional money printing, will make certain any recessionary pressures are short-lived.

Which brings us to the huge change from 14 years ago, the lengths to which the government is willing to go to protect the housing market. I see no reason why loan forbearance programs et al will become all the rage again if foreclosures become a real problem again.

We are operating in a completely different environment today. The FED & governments now are hugely preemptive, and I don’t see this changing anytime soon.

Edit: “I see no reason why loan forbearance programs et al will not become all the rage again if foreclosures become a real problem again.”

Oh boy, Wolf .. talk about deals

Did a night’s gleaning for food basics .. I repeat – BASICS .. at the local BigBox. $20.00 ea. for a 20# bag of Jasmine rice and a #25 bag of Pintos. YIKES!! If this keeps up, there won’t be enough Bugs in the would to keep people fed .. Meanwhile, for the likes of KlausVader, Cardigan Bill, Soros-the-Hut and their ilk – including their toadies the Political, Managerial & Bankster classes; their STEAKS will remain cheap, juicy .. and delicious!

For Reals!

I just love it when the media gushes about how healthy the stock market is … as if most Americans are benefiting from it.

In the book “When Money Dies” Inflation broke the entire German society which before then was civil and orderly into a barbaric everyman for himself cesspool of corruption and greed. This is happening here in the US especially in our major cities on the East Coast. I see it every day. I may start keeping a diary of what I’m seeing every day. I was in DC today and what I saw would be a good trailer for a horror movie.

I know it’s completely off topic.

All the talk is about rates & housing.

What do multiple rate increases do on the production side?

Loan rates for Industrial/commercial producers?

I think they have a lot more rope to play in my brief time auditing the construction industry. With a home loan a small rate change automatically prices out large segments of the population and loan officers spend their time bending physics to eek out those extra pennies a borrower can borrow. For developers, interest expense on a loan is tertiary relative to their operating costs – materials, laborers, subcontractors, etc. When you see how much volume they go through annually in operating costs, the loan is an afterthought. Any rate hike would inevitably get baked into overhead. Not always but they’ll often use lines of credit, so they’re only drawing on the line as needed until they get paid by customers. Right now I’m seeing several not even using their lines b/c of the PPP money that infused them with free cash as we;; as the ongoing favorable demand for their product. So I guess the short of it is they are downstream, where an accumulation of enough rate hikes would softened demand for housing, and then developers would cut back or get wiped out depending on how leveraged they are in the production sense.

I have a 1975 AMC Pacer for sale with zero down at .015% APR for 8 years. Price $93,999: Mileage unknown. Buy here pay here.

Got that magical interest rate, just need that magical buyer.

Wait! You forgot to separately sell an NFT for it!

What a tragedy!

AMC went from building the Javelin muscle car to the lowly Pacer.

Well, at least they weren’t death steeds, like the other brand..

Harvey Mushman

Hey, don’t blast the Javelin. That was my 1st car. I had it when I moved here to Washington D.C. in the 70s.

It’s crazy how global markets are puking this hard over a teeny tiny bit of monetary tightening.

The Fraud Reserve is still buying $40B of treasuries and $20B of MBS for another month.

Mortgage rates, despite the recent spike, are still near 50-year lows.

If you think the market action is crazy, you haven’t found the real reason for the market action.

People in the bubble states said the same thing in 2005 when they suddenly couldn’t sell their houses for 10% over asking. “Why is the market suddenly puking when nothing’s really changed?”

It’s never clear until much later, and even then the historians get it wrong most of the time.

The rates havent even risen yet.

Inflation had about twenty six 1/4 pt upticks in the last 8 months…..

and the markets are fretting a few 1/4pt rate hikes?

I guess the world is full of 32 year old stock brokers who have had the Fed at their back their entire career…

who is left that remembers 1978 to 1983?

1/2 pt a week raises were not uncommon.

And the dollar was worth about 70% more than now.

Some people who bought in 2021 could already be in trouble. I did a search on Redfin of several locations, and median prices are down 15 to 20% from their peak. For example, my Seattle suburb touched over $1.2M median price. Now it’s below $1M.

The crazy price increases on 2021 may have evaporated already. Either that, or buyers are purchasing lower priced homes, ans there is a buyers strike for higher priced homes.

This is too large a drop to be seasonal.

The beautiful thing about falling house prices is all of the data is lagging, so when you find out that house sold for $50,000 less than you thought yours was worth, by the time you have a buyer for yours the offers are coming in at $100,000 less. “Divorce” is a common term heard at that point.

The problem with monthly housing evaluations is the different mix of houses that might get sold that particular month. You might have a month of large houses selling for 1.5 mil , one month followed by a month of small house selling at 900k. It would look as if housing dropped 600k but in really the price per foot could be going up.

We just did a 390 sq foot jr 1 bedroom condo today in a nice area near Dupont Circle, prime location. The unit was bare bones and sold for $390K after being on the market for only 9 days. So the low end is still doing well if it is well located. It’s not all gloom & doom yet.

I follow foreclosures. People in normal debt circumstances might sell their way of a foreclosure filing. People who have been sued, people who have criminal charges and drug problems, and poor dead people don’t get out of foreclosure on the low end. It doesn’t matter if they can sell because the money will go to lawyers or third parties, so they don’t bother to fight it. A few of the foreclosures I’ve tracked lately have had COVID deaths in the family, including a 30-something, but any death can set off financial disaster. While you still have a job but see trouble coming, you do a cash out refi and then default. That takes planning, but I once bought a house that went to auction in that exact premeditated way, well after 2008. They didn’t make a single refinanced mortgage payment. This still happens even in a rising market. All that said, regional foreclosures are indeed down from a few years ago.

Investors are not buying much here. I bought and flipped a (low end) place this fall in a less-than-bubbly town. Buyers weren’t picky. Their chief motivator is ridiculously high rent, doubling over the last few years, wherever they’re moving from (more bubbly urban areas). I wouldn’t do it again now. I think things are turning with the interest rates. Post-holiday/omicron inventory is gradually rising here too, judging from statewide numbers of real estate listings.

This last year I have been told that I should have escalation clauses on the houses I bid on for myself, and I have lost out to escalation offers to true first-time homebuyers who buy into that frenzy. I can wait, and I have been hoping for a big, beautiful, sudden rise in mortgage rates. There are still too many people in the world, and the cost of new building is higher than ever, but if the masses can’t pay these prices at 4%, prices will drop.

It’s hilarious when headlines say something like, “Mortgage rates skyrocket to 3.6%”. If a rate like that is viewed as a burden of galactic proportions, then the market surely will be in trouble. But news people are always so dramatic…

It looks like electronic tulips are taking a bit of a digger tonight. Doggycoins are down to 15 cents again, from a high of 75 cents, and down 32% in just a week after their brief “pop” from the DoggyCON himself. I guess we’re going to need another Tweet from his Tesla highness, but the last one didn’t even provide a week’s worth of support.

In Arizona, prices are still going up strong. Maybe because Arizona is always the last shoe to drop, it was so in 2008. Maybe because for Californians it is always cheap here (and it is).

But this time around, there is a great number of companies who moved to Arizona, for the same reason people are moving in. The diversity and the dollar value of companies and jobs who moved in is astounding. Driving around Gilbert, Chandler, Queen Creek and other areas, it’s a boom town. It is so booming, that if you think what “booming” means, then you don’t, you need to come to see to believe it. And I’ve been around for a long time, and have seen boom in Orange County CA when it was booming. This is bigger.

Even Northern Arizona (Prescott Valley and Quad Cities) are seeing more building, not exactly on the same scale, but in these areas this qualifies as something out of the ordinary.

I guess there are always pockets like this that will hang on until everything else fails. What happens then I don’t know.

But the supply of homes here is (I’ve looked at local MLS’s today) around 1 month. I don’t think it will be going back to 6 months any time soon, no matter interest rates. Before 2008, there was 10 months, which then jumped to 12 months supply. And as soon as interest rates go too high, stock market will crash and back to indefinite easing.

So comparing the years of overbuilding up to 2008 and this isn’t going to help. Even with interest rates going up, it appears very likely the prices here will still go up. How much up I don’t know. But there will be at least another 2 years of solid price increases, maybe not the 35% yoy for 2 years straight here in 85296, but likely and easily 15% each year for at least 2 years.

I chuckle when people mock those who say ‘house prices only go up’. Well they do, but maybe not in a straight line. But they do, and the Fed’s printing machine and the shifty US government assure that. Not because they like unaffordable homes, but because they overspend and frankly, they are corrupt. So they need ever cheaper money and ever more of it. Housing is just a side effect.

So folks, for those of you waiting for an epic crash, time to get real. Either accept that today’s prices very likely won’t come back and buy now, or live in a fantasy world and be disappointed when you finaly cave in and buy at even higher prices.

I am not saying this to jar you, but because sadly, the political and financial class who make these decisions isn’t working for you anymore.

Agree with your last paragraph.

Lack of water …. the unsustainability of constant expansion.

TX will have this issue also. They rely on a aquafer that is dropping, and the same river system.

Can I ask how long you have lived in Arizona?

He’s going to check his car registration and his NAR diploma and get right back to you.

It would appear from your post that you have absolutely no clue whatsoever about the housing market, neither past nor present. What you’ve penned sounds like a REALTURD fantasy novel.

Haha. No NAR diploma here. I have lived in AZ since 2012, all over the state. Like many here, I came from California and Arizona seemed ludicrously cheap to me. Over the years I have bought and sold many houses, some for profit, some for lease, and I still have about dozen rentals both in CA and AZ. I’d say I know a bit about housing market, maybe not as much as you guys. I am certainly not an armchair quarterbacker in this arena, like many who spill the beans like they mean it.

I agree NAR is a perpetual “price growth” machine and has lost all credibility long ago, especially for those of us who remember their optimism in the months leading to 2008 crash. I didn’t believe them then, and managed to buy 4 rentals for 25% of the price they go for now. Tune out NAR.

But this has nothing to do with NAR or realtors. Your anger and mockery is justified, however misdirected. Perpetual socialist state, and perpetual war state is what America is. They are by definition expensive and unsustainably so.

In America, the political class has perfected the sports approach, kind of like the NBA: there is our team and there is their team. Vote for us, not for them. Issues presented (such as all the wokeism right now, or pretending to care about Ukraine on the other side of the planet just for the pleasure of irking Russians), are generally less than relevant, but are perfect distraction for more and constant money printing.

That has been going on for many decades, but the rope to hang ourselves with is getting short. Soon, the dollar will suddenly fall, all the world’s debt will be repaid in a flash. Good for the world, but terrible for America, the world’s greatest “assembly line”, where nothing is made but plenty “assembled”, a pathetic decline for once industrial superpower. When that happens, watch for political instability, and then you will see money printing that will make this QE look like pennies.

Check back then and weep for today’s house prices….

But wait… 10yr Treasury still at a measly 1.78%. This type of action always requires sacrifices. Just what are we sacrificing to keep the fires burning? Is greed the final word?

Dawn.

The argument seems to be

*We must keep spiked prices up

*We must keep the errant policy of fake low rates subsidizing debt creation

How can that which caused the problem also be the solution and course forward? Those who push these two points are tragically illogical and expect central bankers to rescue price declines from levels that arguably never should have occurred. IMO.

“Once homes are treated as investment products, like stocks, and not as homes, there can never be” any going back to house as dwelling.

Prices will rise and fall, like stocks, but the shack as investment vehicle is a genie out of the bottle.

Yep

VRBO and the likes changed things quite a bit.

And with the increase in labor and materials, buying a property with money 4% below the inflation rate provided by the Federal Reserve, and buying below replacement cost, is a pretty solid investment….for now.

Rates sharply higher could reverse all that.

In 2006 the Fed didnt own any MBSs.

Now they own 24% of all residential mortgage paper. Why?

Rates could go up.

But I, like many others, have a 30yr fixed loan at 3%, with 28 years to go.

So what if rates go back up to 10% for a few years? I am not moving. Okay with me if my property taxes go down for a few years. Inflation will erase the loan.

It’s an interesting question. I was also thinking about this scenario.

If rates go up to 10%, the prices should go way lower. So, the bank probably will ask to repay some part of the loan to compensate?

Would be good to hear from those with knowledge.

A fixed rate mortgage is a fixed rate for a specified amount and a specified period of time. It is backed by the value of the house at the time the legal contract is signed.

There isn’t anything in the mortgage contract (at least mine) that says if the value of the collateral for the loan drops, that I have to come up with more money. Legally, I am covered.

However, mortgage and rent forbearance allowed the US government to violate allowed basic contract law. It was a national Covid emergency. I suppose if the collateral decreases and the banks are in danger of bankruptcy, the US government could bail them out by declaring an emergency again and allowing banks to collect further collateral from mortgage holders in violation of the mortgage contracts. More likely, the US government would bail out the banks with taxpayer money like in 2008.

Banks could approach mortgage holders with low interest rates and offer to allow them to buy out the loan at an amount that would be attractive to the homeowner. Banks do not want to hold 3% loans when the going mortgage rate is 10% and the savings rate is 7%.

I’m not even sure how my bank makes money with the overhead involved with a 3% mortgage. I’m sure the outsourced mortgage servicing company who has to keep records, mail statements, keep tax information, staff customer support, has to make money also.

Actually, I know Fannie owns my loan so I suspect the US government is already taking a loss on my loan after they pay the servicing company.

Also, if rates went to 10% and the value of my house dropped 70%, legally I can just walk away from my house and turn the keys over to whoever owns my mortgage. Fannie.

Over 10M mortgage holders did this in 2008-2012.

That may make short-term financial sense. The punishment would be not to be able to qualify for another mortgage for 7 years. It hurt people who walked away in 2009 and could buy another house with a loan until 2016. They missed the best time to buy a house in 2012. It was a terrible long-term financial decision unless they didn’t need a mortgage and paid with cash in 2012 during the half-off sale.

1) India most trusted ally is Putin.

2) After meeting the Iranian leader in the Kremlin, “Marine Silk Road

2022” start today in the northern Indian ocean, a drill between the Chines, Russian and the Iranian navies, shooting a blizzard of missiles at far away targets.

3) For twenty years US protected India northern border. After we left

Afghanistan India is sandwiched east & west, north & south.

4) China have naval bases in Djibouti, Sri lanka and Pakistan.

Michael Engel

‘For twenty years US protected India northern border’

Wow! News to me! How did US protect India, by supporting Pakistan with billions in aid and military weapons, for a Theological state against a Democracy!

Mr Nixon sent air craft carrier to support ( Pakistan) during 1971 Indo Pakistan war(East Pakistan getting seperated from it’s western counter part) in 1971! For the past 20 yrs, US supported Pakistan ( apparently an ally against terrorism!), which harboured Osama until 2013! The US should stop being Global police with it’s 800 military bases around the world

B/w a British diplomat was asked ‘ Who are your’ permanent’ friends?

He said ‘ we only have permanent interests’

The Energy Secretary, Jennifer Granholm was just sited for 8 separate illegal, insider stock trading violations, including Energy Companies which she overseas. She’s competing with Pelosi as the most corrupt politician in the Swamp.

That’s why we’ve heard nothing but crickets on the FED’s insider trading – because the whole administration and all of CONgress are doing the exact same thing. They’re ripping off the American people. This is a level of corruption never before seen.

Are you assuming Mr. T is no longer a politician?

Housing inventory levels may, on average, run lower in the future for several reasons.

An east coast realtor is telling me that job changes triggered a wave of inventorhy, especially in the spring. Now, she said the work from home trend has drastically cut inventory from job changes.

The 500,000 tax deduction cap for a married couple on the sale of a home is causing a drop in higher end inventory. When this cap was put in, homes were much cheaper and not many sales took a long term capital gain hit. Not anymore. More and more homes have large gains. On average the $1.5M dollar home sale costs the seller $335K in transaction costs and the capital gain tax over 500K. So, many are deciding to stay where they are and plow the $335K into a remodel instead of a house flip.

Then, there is the reverse mortage. The old practice of selling and downsizing is being replaced with the reverse mortgage, especially in higher priced areas where gains are higher than 500,000. Why pay transactions costs and the tax man … just take a reverse and hopefully the home continues to appreciate.

Rents have gone up but margins for rental owners are lagging due to increased house prices at lower echelon if buying in past few years.

Rental owners will sell / flip as market turns a bit, but not in waves. Interest rate rises will have some downward effect on prices, but not so much on the lower / middle priced inventory.

The deals, if you can afford them, will be on the $1M+ homes, which cannot be rented out profitably.

1) Netflix is down 20%.

2) US10Y will make a round trip to zero by the end of 2022.

3) JP will reduced RRP % to save the market, that’s all he can, but the smart money will park in the Fed, regardless of RRP %. Panic will send the 3Y to NR.

4) US gov debt > 100M+/ capita. Taxes are already high.

5) In the next recession there will be no pipi loans, no stimies, no checks to shingle mums with four children.

6) The DOW is a Lazer tilting up. By mid year, the DOW will be forced to escape the hot beam.

7) The RE bubble will decay.

8) SF & NYC inelastic RE will crack.

why praytell do you think there’ll be no ppp loans, stimmies or “checks?” it seems that once you’ve done it once, the political pressure to do it the next time will always be there.

@Jake W: Because there’s also pressure to not destroy people and markets with record-high inflation, methinks.

It would seem that Uncle Sam got himself into another pickle. Darned if you do, darned if you don’t. Catch-22. Et al.

9) Rent is going up, but in order to increase it further, to market value,

landlords remodel and renovate, piling debt at peak markets.

Most sfr loanowners are just riding the wave of appreciation up while they subsidize their renters or AirBnb guests. Once house prices reverse, these people will flee from housing like cockroaches in a kitchen when the lights are turned on.

Guess the Fed is stuck between a rock and a hard place? Omicron surging. I’ve never known so many people with COVID all at once. Many schools don’t have enough staff to hold class. I assume this to mean certain business will experience similar. Is a “natural” shutdown coming? And if so, won’t Uncle Sam have a harder time firing up those money dropping helicopters again? I mean, wouldn’t that pretty near guarantee that Biden succeeds Carter as the new ruler of Inflation Kingdom?

Invading Taiwan? Holy cow, that would make a great diversion for Uncle Sam, too. But I hope something so harsh would not occur.

If holding dollars is just losing money and you had a large amount of them, where else would you put them aside from homes, as in ‘safe as houses’ for it’s all we’ve known in that used domiciles go up in value (rust belt void where prohibited) and where else would you put the money if you wanted something that would hold ‘value’?

If we hyperinflate, then its gonna get crazy, imagine Socaljim crowing about a dated 1969 fixer upper 3 blocks from the beach he got $372 million for, without inspection.

I think the Fed will be successful if they avoid more than few lock limit down days on the stock market.

This is a monster bubble.

The new appointee overseaing the nation’s commercial banks is the spouse of our County Executive, Raskin. Her top priority is implementing the new Fed mandate of social justice and climate change onto the nation’s commercial bank’s lending practices.