QE ended months ago and interest rates are rising. Home prices fell in three markets, but spiked in others.

By Wolf Richter for WOLF STREET.

Potential homebuyers and speculators in Canada are now looking at rising interest rates coming their way, which is a dreadful sight with house prices at these ridiculous levels in the big markets.

As is typically the case early in rate-hike cycles, there is now a mad scramble underway to buy a house now, no matter what the price, in order to lock in the still very low mortgage rates, as prices have risen so far in recent years that even moderately higher mortgage rates move those payments out of reach.

But that mad scramble isn’t taking place in all markets. In three of Canada’s 11 largest markets – in Ottawa, Winnipeg, and Edmonton – home prices fell in December. But in the already hottest markets home prices re-surged, after having “paused” for several months.

Interest rates are already rising – but are still ridiculously low, and far below the red-hot inflation rate. The one-year yield of Canada Treasury securities has quadrupled since September 2021, to 1.05%. The 10-year Canada Treasury yield has jumped to 1.87% this morning, the highest since February 2019.

Most mortgages in Canada either have variable rates, or have fixed rates for terms typically ranging from 1-10 years. And those rates have started to rise too, but just barely.

Inflation started raging last year and in December reached 4.8%, the worst inflation rate since 1991.

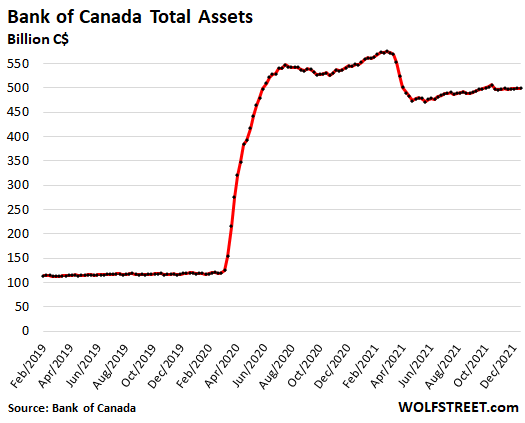

The Bank of Canada is so far behind the curve it can’t even see the curve, but it is expected to finally finally finally raise its policy rates next week for the first time in this cycle. It ended QE last year, after wagging its finger at the excesses in the housing market that resulted from its reckless QE and interest rate repression. The BoC’s total assets have been flat since October, and at just under C$500 billion, are down 13% from the peak in March 2021:

Mad scramble to lock in mortgage rates before they rise further.

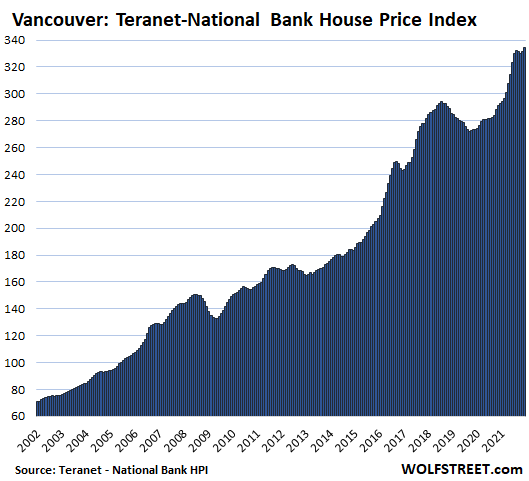

In Greater Vancouver, house prices rose 1.0% in December from November, after having been flat for three months, according to the Teranet-National Bank House Price Index, released today. Year-over-year, prices jumped 14.2%, down from the 17%-range last summer.

Vancouver’s housing market had been on a decline that started in August 2018, when the BoC’s reckless monetary policies came to the rescue to refuel the spike:

The Teranet-National Bank House Price Index is based on the “sales pairs” method. Much like the Case-Shiller Home Price Index in the US, it is a three-month moving average and compares the price of a house that sold in the current month to the price of the same house when it sold previously. In other words, it tracks how many Canadian dollars it takes to buy the same house over time, which makes it a measure of house price inflation.

The charts here are all on the same scale, and markets with less house price inflation over the past two decades have more white space above the curve.

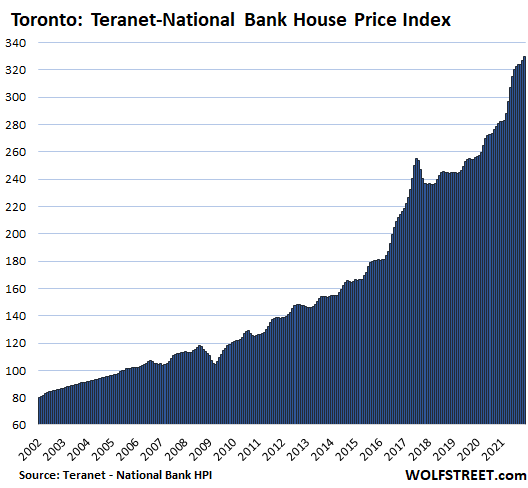

In the Greater Toronto Area, home prices rose 0.9% in December from November, and by 16.8% year-over-year:

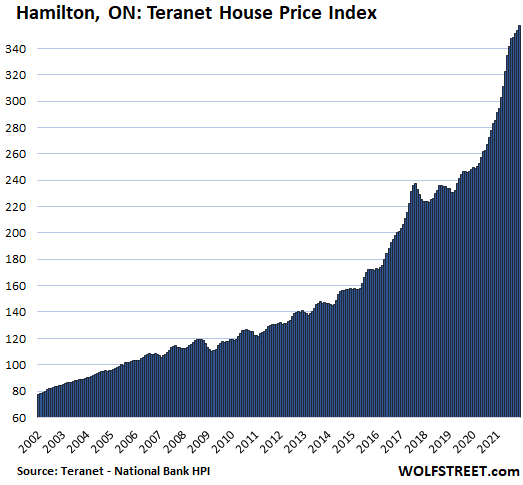

In Hamilton, Ontario, house prices jumped by 1.2% in December from November – a crazy increase but down from the even crazier increases in mid-2021 that reached 3.8% in June. Year-over-year, the index jumped by 25.4%, but that was down from the 30% spikes in July and August. Thank you, halleluiah, for the miracles of the Bank of Canada’s money-printing machine:

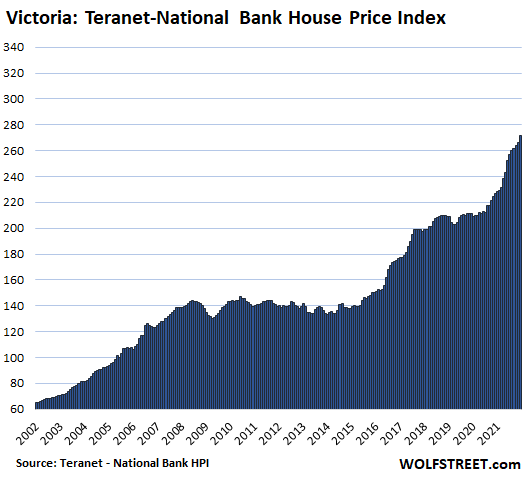

In Victoria, house prices spiked by 2.1% for the month, and by 19.7% year-over-year. From 2018 through June 2020, prices had flattened, but then the BoC started performing its miracles:

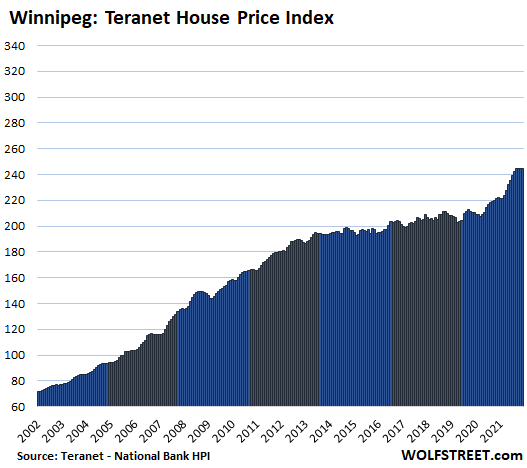

In Winnipeg, house prices declined for the month, after having been flat for two months in a row, which whittled down the year-over-year increase to 7.5%. Before the jump that started in late 2020, prices had remained about level for seven years, after the housing boom that petered out in 2013:

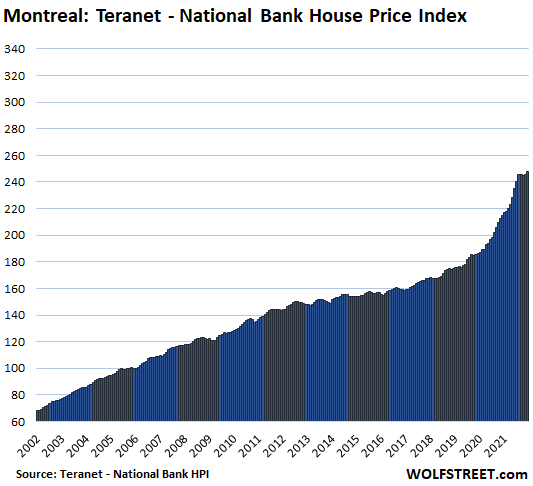

In Montreal, house prices jumped 1.1% for the month, after three months of staying put. Year-over-year, prices rose 15.6%, amid its lowest year-over-year gains all year that had maxed with a 21.6% gain in August:

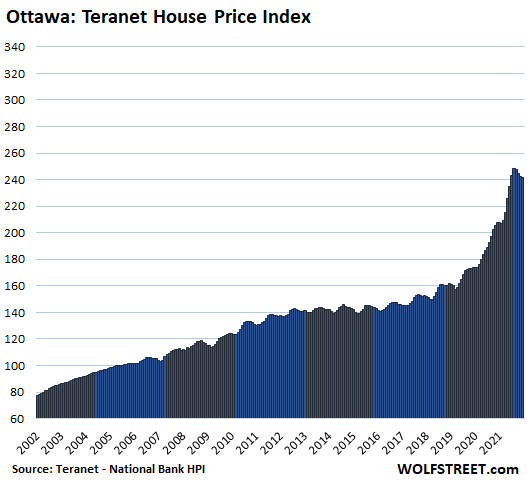

In Ottawa, house prices fell 0.3% for the month, the fourth month in a row of declines. This whittled down the year-over-year gain to 16.3%, from the peak in July of 28.9%:

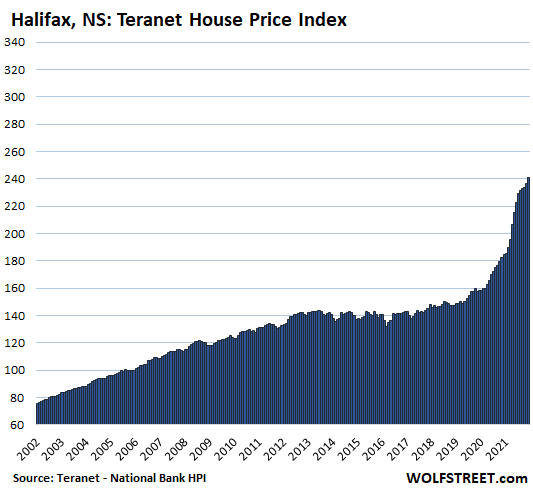

In Halifax, house prices spiked by 1.9% for the month, but that spike was just a shadow of the 5.4% idiocy spike in April. This pushed the year-over-year spike to 30.7%. A housing chart like this is just nuts:

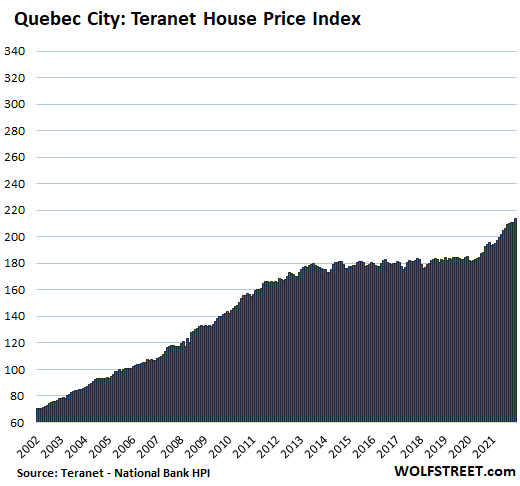

In Quebec City, house prices rose 1.1% for the month, and by 10.4% year-over-year:

Calgary and Edmonton didn’t qualify for the most splendid housing bubbles in Canada because prices have gone nowhere since the end of the bubble in 2007, which is less than splendid. Canada’s oil towns had mind-boggling housing booms through 2007, powered by the endless money of their oil booms. But the money ended, and for the following 14 years, house prices went nowhere.

In December, Calgary’s house prices – up 0.3% for the month and 8.5% for the year – were barely above their 2007 levels. Edmonton’s house prices – down 0.4% for the month and up 4.3% year-over-year – remain below 2007 levels.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

As a cash buyer is it best to sit this out and see what happens?

Depends on the currency.

I am in the uk but i am guessing that all countries will follow the same path.

I am sitting for a while longer. The problem is buyers look forwards and sellers look back. The expectation is now huge returns each year and investors are the largest group of buyers at about 20% of all homes/land. Many of these are just being left empty. This is driving the demand sky high and availability down. TINA – investors are getting better returns in housing than the stock market at these rates and tax levels. These may be the first to sell if things change, but real estate is what 12% or more of GDP now…..

“Many of these are just being left empty.”

Where? The MO in most markets in the US is buy, renovate, list for rent. Sometimes just buy and list.

And rent at a loss? That’s an interesting “investment.”

DC, renting at a loss is a tax deduction!

Renting at a loss but counting on the appreciation of the property for the profit. Plus the tax advantages of writing off everything in the world to the rental.

In the US- seaside towns, ski towns, tourist attraction towns, NYC, LA and SF. SF and NYC mostly condo units empty. Massive amounts empty in some midwestern cities like Detroit and smaller.

Domino effect in other rural areas.

You won’t read too much about it in the news and no one is tracking it. You have to go street level and ask people in other areas how much housing is empty. I’ve seen some where I am and heard of more in SF.

Depends which currency, which markets you are looking at.

But if you don’t have to buy right away and/or if this home is for investment purposes only, I would wait and see a little longer. I would get my feelers out there and see whether if any distressed seller comes my way.

That’s right

To have the luxury and advantage of being able to pay cash is greatly diminished when you are bidding against people will to take a 30yr mortgage and get it at 4% below inflation.

That is my opinion too.

Disagree. Buy for cash then cash out refinance after closing…. a seller would rather have a cash buyer who doesn’t have “underwriting” issues such as appraisals, etc., to contend with. I have bought several houses for “cash”. Every time, our offer was selected despite it not being the highest – as it was the one with the least chance of falling apart and we could provide a quick close that a “git me done” cannot. Me? 15 days. Other guy 60-90 and if VA or FHA… oh buddy.

Then we went to our favorite financial institution and took a mortgage at our leisure.

Yes, a cash buyer can take advantage of a “grow-op” house, or a house with structural damage, because insurance companies and banks generally won’t touch these. A cash offer is also more attractive than a conditional offer in a multiple bid situation. Cash is still king.

Hmm, so now with 30yrs fixed at close to 4% from my credit union. I guess this will fuel the SoCal market even more with more buyers trying to get in on the action before it’s too late?

Great…guess nothing is popping this MFing bubble anytime soon, everything end up turning into a FOMO narrative…

Non cash buyers will want to buy now to lock in a low interest rate.

Cash buyers will hold off and wait for prices to drop.

It’s a well-established pattern that I described here before: in the early phases of rising interest rates, there is a mini-surge in buying activity. Once mortgage rates hit a magic level, the buying tapers off, and when mortgage rates go beyond that magic level, it’s hard to make deals, and if a seller has to sell, prices will need to be cut. That’s how it happened in 2018. The magic level in 2018 was somewhere around 4.5%.

After the insane COVID spike, would you expect the magic number to be higher or lower this time?

My gut says lower.

I’ll guess 3.25

Thanks for that info.

People taking out loans will certainly fall into this bucket.

I am wondering about cash buyers. Do rising rates hurt 5hem.

I ask because I am getting sometimes 3 postcards or letters a day of offers to buy my 2 rental properties with cash.

Crazy

I’m guessing part of it might be offshore money funneled through a we-buy-houses-for-cash franchise posing as a person or couple. Found one a while back that had over 100 websites connected to the same server IP, each one in a different area in the US with a different “mom and pop” buyer. The one buyer I traced through corporation wiki had obscure vague connections to a company owned in part by Alibaba and Evergreen. I have a post regarding offshore stuff in Wolf’s US housing market article.

Some of the we-buy-houses companies are just grouchy old US private money- but not all of them. Some register each house as a separate LLC in Nevada.

We just went back to work after taking 2 months off. Things are booming again as buyers are jumping in to beat the interest rate rise which is just around the corner. Also, sellers are keeping their prices in line to get rid of their properties (mostly second homes) quickly before the credit crunch kicks in. Just did three condos near the downtown area. Both sellers and buyers are happy to making deals right now. Here in the Swamp, condos are doing very well if they are in a good location.

The pandemic will be winding down come the spring and therefore immigration in Canada will be increasing. Do you think this will effect home prices?

Check Nanaimo, Central Van Isle: assessments up average of 32 %, blowing away Vancouver’s and Victoria. The reason Nam was and still is much cheaper and has been ‘discovered’

Because lots of multi-sites and a very obliging planning dept. an orgy of rental / condo underway. Going to be flooding the market in 22 I think.

Fraser Valley, Greater Vancouver region. Our assessment up 38% this year. Many in the same boat.

Everyone is maxxed on their mortgages and they will need to max out again on their equity to pay for eveeything going up. This is going to get nasty very quickly.

Also nat gas just went up 15% jan.1,2022.

Wanna throw your hat in the ring on China?

They’re reducing their rates.

China has a sh*tload of problems, with their biggest RE developers in a state-controlled slow-motion collapse. RE development is a HUGE economic driver in China, and it is now fizzling. This is a very uniquely Chinese problem. And I don’t think that rate cuts in China will help much. This is just going to be a mess in China.

Also see my other comment here about this situation in China.

Funny yet, you hear Xi Jinping publicly asking Weimar Powell not to raise interest rates in the US even with inflation…funny time we live in for sure.

Its like betting against your team. Team loses you win, and if they win well it is your team. ;)

Remember that news item recently where the Chinese team met the American team in USA and were very insulting? You can’t ask for favors after doing that.

China cutting rates and urging the US not to raise too quickly. These pigs just can’t imagine getting off the high of fake, easy money. China is the world’s most prolific money printer of all. They poured more concrete in China in 3 years time than we did in 100. China is the biggest economic lie the world has ever seen. China is also a festering wound upon mother earth.

DC…you should tell us what you really think of China 😂😂

I agree with you100%.

“Mad Scramble to Lock in Mortgage Rates”

I don’t think so.

Let me fix it for you.

“Mad Scramble to Lock in a price before they go higher”

No one cares about rates with inflation running red hot.

No one cares about inflated prices to their own detriment.

If inflation is sending food prices & fuel prices & everything else prices higher and if people are taking on a mortgage that they can currently “afford” how in the world does that translate to higher housing prices. I guess I’m not following your train of thought. Are investors drooling at the prospect of being able to buy up the housing stock at higher prices?

I am just telling you what I am seeing. Seems the higher prices are being supported by equity market gains and wage increases. The bidding wars are stunning.

SocalJim is a housing pimp.

DC – please be respectful!

Yes Jim is talking his book, so what? Everybody is. But he provides insights and the reasoning that we can discuss – isn’t it why we come to the comments section?

I still remember Jim’s comment in the beginning of the 2020 – he shared the summary of some WS report that the recession will be asymmetric. Could you get this info elsewhere this early? This could make you a lot of money if acted upon.

SocalJim and people like him lead people to make extremely poor decisions about the most expensive purchase in their entire lives. Constantly pimping real estate in the most outrageous, unsustainable housing bubble in history is kind of scummy, if you ask me.

I remember these types before the last downturn:

“Real estate always goes up.”

“Prices will never drop in my state.”

“Not in my town.”

“Not in my neighborhood.”

“Not on my street.”

“Not my house.”

Then they disappear. Because they’re shills.

DC:

While, at times, I disagree with Socaljim’s opinion, I think you’re being unfair. I also recall him saying that real estate is regional… and some areas will do better than others and provides other insights from his markets of interest. Wolf allows us to use his site as a medium of idea exchange and because his opinions differ from yours doesn’t make him a “shill”.

IMHO, not every place is in a bubble. There are plenty of older properties that can be purchased for reasonable prices, but they are not located in Malibu or Martha’s Vineyard, don’t have granite counter tops and an ocean view – are not the kind of HGTV-esque property “they deserve”. They likely need somewhat extensive repairs/upgrades to meet that standard.

But many, if not most people, run from those properties like a scalded dog. It’s still in play here in North Scottsdale. “Perfect” houses are selling for ridiculous prices (one recently closed for $200K over the price it sold for only a year ago and the current seller didn’t spend a nickel on it) within hours after listing and the granny dumps are reducing prices until they can attract an investor to take them on and refurbish them.

Here’s one of my personal, anecdotal observations: Do not ever buy a house that has been a second or seasonal home. Since they are not lived in full time, they lack maintenance that would customarily come from simple observation (like the smell of mildew), are usually fixed by some “handyman” or “Idunnitmyself” who does the work “off season” without owner supervision, utilizing the cheapest materials available, and likely lipsticked to sell. If, during the open houses, the doors and windows are wide open and there’s candles burning, you know there’s problems…. you just don’t know where they are.

Most of them can’t get a high enough percentage off of the deal. Equity market gains and wage increases. The truth is, any amount they can skim from the buyer is what they ‘want to see’. Sounds familiar.

Not sure about the rest of Canada, but we haven’t had a correction in housing prices in the GTA since the early 90s. The 91/92 correction was brutal. Several of my friend’s parents lost their houses at that time. Prices only reached late 80s levels around 2005 or so in my neighborhood.

I don’t have a clue when things will correct again, but I have spoken to recent purchasers in my area, and they’re all stretched to the max. I worry that even small changes in variable rates (most people here are in those) will result in foreclosures.

Personally, I’m renting and saving up cash. I hope that my landlord isn’t overleveraged.

So @ 3.5% the house sells for 750K.

At 5.5% that same house sells for ???

Do the buyers believe that price will hold…or go up?

Depends on what typical incomes and LTVs are in your area. If you can manage to get basic data in your local area, you might be able to do some math and figure out typical levels.

Regardless, the number of distressed sellers vs distressed buyers ratio is about to shift. Prices are probably going to go down

If interest rates go up… prices will come down.

Well not according to SoCalJim, interest rates up, price goes up, everything is up..up is the only way.

Actually, as long as mtg rates remain far below inflation, as they are expected to be even after fed rate hikes, and the single family housing shortage remains, prices should go higher.

Interest rates rising will at some point cause prices to moderate if they exceed the comfort level of buyers but only if sellers are willing to accept that. There is a lag.

In my area where demand is high and money is apparantly plentiful, prices won’t drop much unless the very low inventory rises to meet demand. I see it happening but slowly.

47% of potential buyers, according to a recent poll by I forget who, said that if interest rates hit 3.5% they would be even more likely to find a home to buy.

It is changing but not all at once everywhere.

DougP,

When ( Inflation – 30MtgRates ) is less than perhaps 200bps ( the 200bps is my educated guess ), housing appreciation should slow to crawl. And if that spread approaches 0bps, you may see some real trouble in the housing market.

However, the US, and the rest of the world, has a real problem because if rates are raised to that point, growth may go quite negative. The current crop of US and global politicians do not have the backbone to bring down inflation with very high rates.

Furthermore, because so much of the inflation is from our global supply chain, the FED can not fix this alone.

That is my basecase. I might be wrong, but that is where I am.

@Harvey

Housing prices increased in the late 70s are rates kept going up from 7% to 18%.

Liquidity is what drives up prices. Maybe 18% was the pain point and banks did not believe people could pay back loans and quit loaning money?

What is the pain point now? 5%. 10%

Banks do not want to make 30 year loans at 3.5%. That is why the GSEs are the ones making 98% of all loans the past 10 years.

If you are a bank would you want to loan out money for 30 years when inflation is 4 or 5% YOY

What is a GSE?

GSEs make the loans and the FRB buys the MBSes. Capitalism free of markets at fixed price by Central committee bid. The USSR would be proud!

Thanks Mike! What does the acronym GSE stand for?

Government Sponsored Enterprise = Fannie Mae, Freddie Mac, et al.

Wolf, thank you!

Realtors and people holding would believe that prices would go up irrespective of anything.

People wanting to buy would believe that prices would come down.

jon,

You nailed it! The emotional aspect of markets. Greed and fear (or hope — which goes either way).

The real estate in the better climates was often bought on speculation and to rent out to get some type of return. (VRBO, etc)

When the interest rates go up, the convenience of a fair return on money vs an asset that needs upkeep, etc…(and is likely to also decline in price) becomes more attractive.

Interest rates going up will certainly effect the mom and pop VBRO investors. That segment may take a hit.

Specially if they can start getting a decent return on bonds. Otherwise, I know some who said they were diversifying out of the stock market to real estate. Some took out loans while others paid cash. The cash payers are retired or close to retirement and are more concerned about cash flow then the valuation of the property as they paid cash from stock gains.

“ I know some who said they were diversifying out of the stock market to real estate“

The new 60/40 retirement plan…

6 houses/4 cars…

“The new 60/40 retirement plan…

6 houses/4 cars…”

Now that’s funny!

I have to send that to my retired friends.

Okay, lets say the buyer puts 20% down. So they need a mortgage for $600,000.

With a 30 year loan at 3.5%, their monthly payment is $2,694.27

With a 30 year loan at 5.0%, their monthly payment is $3,220.93

Just play around with the PMT () function in Excel. You will see how interest rates affect house affordability.

Tom15: Correction, you asked the difference between 3.5% and 5.5%.

So if the loan amount at 3.5% is 600,000, the monthly payment is $2,694.27.

If $2,694.27 is the max payment the buyer can afford, your question is… What can the buyer afford at an interest rate of 5.5%

The answer is: $474,519.58

So you can see that a 2% increase of the interest rate dropped is loan amount from $600,000 to $474,519

If interest rates rise, eventually home prices WILL come down.

I used to think the same way. Sometimes interest rates rise because of an inflationary environment.

The currency is being devalued by the increase in the money supply. Asset prices like housing will still go up. It has happened many times in history.

Interest rates rising means people get less home with the same down payment. They may just be forced to buy a smaller home? Builders will just build smaller homes.

Obviously these charts show bubble like qualities but Some looked like a bubble 3 years ago about to pop but ample liquidity kept it going to even higher heights.

The Fed tapering will be the killer.

I know 4 people who have good jobs, Enough money for 30% down, and have been overbid on at least 10 or more houses the past year. They will buy a house even if rates hit 6 or 8%. They hate living in apartments.

The thing you’re leaving out is the effect of inflation on the buyer’s income. This has two effects: Firstly if their wages are tracking inflation, then they know that even if they take on an eye-watering monthly payment now, by next year this will be reduced as a fraction of their income to more comfortable levels. So loading up on debt today isn’t as scary as it would otherwise be.

The second thing is that they will know that buyers next year will be able to more easily afford the repayments, so nominal prices can keep rising even though nominal rates are higher.

There is sort of a time lag involved due to the time it takes for wage increase to circle around against price rises. But if you can deal with this lag then the hard truth is that real rates are deeply negative, so your mortgage is making you money.

‘They may just be forced to buy a smaller home? Builders will just build smaller homes.’

With the cost of the lot now equal or more than construction cost the answer is to put more homes on same lot sq. ft. i.e., the condo.

I am in BC Canada with the population of Paris and the land mass of France and Germany combined. We have for our size the most restrictive land use regs in the world.

Most of the province is Crown (govt) ‘in right of the people of BC’ but we can’t own it directly. Forest Code, ALR, Land Claims etc. etc.

As soon as you cross into Washington, the price of small acreages drops by at least 50%. Sure, they may be remote even off grid but they are there.

I was a realtor in the early 80’s, getting in just before the market crashed in the Vancouver suburbs. With too many realtors and too few houses for sale as well as sky-rocketing interest rates, we had to turn to that dreaded cold-calling to get listings. God, I hated that aspect of the job. Now, for the first time in a great many years, I’ve started getting cold calls from realtors as well as unsolicited offers to buy in the mail from non-realtors. Something is afoot.

You can’t get a house for 750K where I live. You mostly can’t even get a condo for that price.

Monthly payments on mortgages in the GTA are likely far higher as a % of income than people are supposed to be paying. People go to indie brokers, not banks. I worry about what sort of nonsense is going on there. As Buffett says, we’ll see when the tide goes out.

Those charts are screaming out loud one single word : Hyperinflation

No, it’s reflecting a mania supported by debt since most real estate is primarily bought with borrowed money.

The BOC isn’t about to voluntarily destroy the CAD to bail out real estate speculators any more than the FRB is going to “print to infinity” to bail out debtors and speculators participating in the US mania.

The choice to “print” and spend had been easy up to COVID because it seemed to be free.

Still, this isn’t the Weimer Republic or the Great Depression. Every central bank is still in some control of the situation and has the tools at its disposal to ameliorate medium-term to long-term inflation. It might not be pretty but it’s doable.

They all have the tools, but they have pointedly ignored them while bubbles raged for years. Having them doesn’t mean they’ll use them.

Catxman: “Every central bank is still in some control of the situation, and has the tools at its disposal to ameliorate ….inflation.”

The central bankers at the Fed in 1967 also had the tools, but it still took two decades to finally get the inflation “horse” back into the barn.

And what of the serious potential unintended consequences of using those tools?

Catxman: “Every central bank is still in some control of the situation, and has the tools at its disposal to ameliorate ….inflation.”

The central bankers at the Fed in 1967 also had the tools, but it still took two decades to finally get the inflation “horse” back into the barn. And inflation topped out in the teens. And then, like now,

The Chinese both local and foreign are still buying everything in sight in bidding wars and bully bids.

Foreign Chinese as buyers…really?

Not really foreign, as they all have Canadian passports.

Real Tony

Yep.

The Chinese are using loop holes in the Canadian laws to Launder Money.

It is very well documented.

“When the British Columbia government announced in 2018 that it would implement a publicly

accessible registry of beneficial ownership of land, hopes were high that the registry would effectively

combat the province’s money laundering problem. However, in the ensuing months, the BC government

stripped the highly touted public registry of almost all its potential power and functionality. The final

product, scheduled to be launched this fall, will likely do little to stop money laundering in BC real estate.

And, once again, Canada will have failed to show it is serious about combatting money laundering.”

for more search

cdhowe.org/sites/default/files/attachments/research_papers/mixed/Commentary_583.pdf

Many markets in the GTA like in Hamilton (where I live) there is no land for sale, and you can’t sever rural land. The balance of land is green space and development fees are $50-100K. If you want to build you have to buy a tear down. Even lake front cottages 2 hours north of Toronto doubled in value over the last two years. I would love to see a crash for my kids sake, but the bankers still have tools in their box to prop it up. Nobody up here want’s to hold bank notes.

They aren’t making any more muskeg!

…. consolidated moose pasture!

I believe when the Bank of Canada raises interest rates it actually pushes up the inflation rate as mortgage interest is included in the CPI. Rents are not.

Rents and mortgage rates are both included Canadian CPI. House prices are not, only net replacement value.

You know, it’s interesting; the graphs between Canada and US are pretty different!

US has twin towers, and Canada looks like only one half of one big mountain……..

So far and for the entire lives of these charts, owning real estate has been the smart and highly profitable thing to do. Waiting for the most splendid housing bubble to burst has been the100% WRONG thing to do.

But what do I know. I’m just a long term real estate investor, builder, developer, broker. I do know this… if I was on the wrong side of a market for 19 years, I’d do something else.

Its no secret all the Chinese started coming to Canada in 2015. One only has to look at home prices in the Chinese cities in Canada to figure out why real estate prices today are about double what they are in America in local currencies. Home prices in Canada, New Zealand and Australia are very dependent on home prices in China. Should prices collapse in China then all the margin calls come in and all the foreign real estate the Chinese own has to be sold to stave off insolvency in China.

I would think the insolvent Chinese home owners will move out to Canada and abandon the Chinese debt. I don’t think that Canada will extradite them over something like that.

Some Chinese entity will acquire the assets and pretend they are worth something; After 2008, in my local area we had homes that were empty until after 2010, and not for sale. The banks were just holding them. I’d suspect a communist country producing 400000 university graduates per year can be even more creative than that.

CCCB,

The charts mercifully don’t include what was going on in the 1990s. In Toronto, for example, house price plunged for years, and didn’t get back to their 1990 high until 20 years later.

In CT house prices peaked in 1988, dropped as much as 50%, and didn’t reach the previous high for 10 years. Yes, RE is one of the best long term assets. If you have the longevity to wait out 10 and 20 year losing streaks.

Pretty much same thing since the last 40 years as mortgage rates went from 18% to 3% in the states. That’s a one way trip. What comes next, nobody knows.

“But what do I know. I’m just a long term real estate investor, builder, developer, broker. I do know this… if I was on the wrong side of a market for 19 years, I’d do something else.”

Wait, what? Are you in Canada? Because you’re surely not talking about the US. From 2007 until 2013, some areas dropped 65%. We’re you frontin’ then, gunslinger? Puhhhleeeeeeease.

@CCCB – What is so wrong is that you are right – for my entire professional career I would have made far more money each year from owning a couple of investment properties with big mortgages than I did from doing actual work.

If I had known all this, I wouldn’t have wasted my time becoming an engineer and making useful widgets for people. And if you look at where the best and brightest graduates are increasingly going, it seems that that message is getting through loud and clear.

So what happens when all the talented hard working people are working in finance? What happens when you take some of your housing money and try to use it to find a doctor, but there aren’t any because they all became property investors?

This should never have been allowed to happen. Real wealth is the productive core of your economy, but nobody cares because you can make so much money from trading.

History teaches printing money screws up society. It makes working pointless. Can’t last.

“So what happens when all the talented hard working people are working in finance? What happens when you take some of your housing money and try to use it to find a doctor, but there aren’t any because they all became property investors?”

So at that point, doctors, engineers and other professionals will be in high demand and will command fantastic salaries. That will be an incentive for young folks to go into those fields rather than just finance.

Over simplistic I know, but you get the idea.

Agree 100%. I feel the same way, and it’s shameful what kind of behaviors have been rewarded and punished. There was this article in Toronto Life not long ago about a couple who bought for 250K and sold for 2.5M after 20 years, and even though one spouse had consistent income, it was as if they had a tax free earner in the house (cap gains in real estate aren’t taxed in Canada).

Condo prices in Edmonton are down just slightly more than ten percent in the last two years. All the price increases were in detached homes and duplexes. Apartments are down about 15 percent the last two years. Last year there were dozens of resale apartments selling in the 30 to 40 thousand price range in Edmonton much less than what a new car sells for. These are all in Canadian dollars.

Just a little reminder.

Toronto is in a blizzard condition and state of emergency this week.

60 mph winds and 25 inches of snow.

Enjoy that bubble!

Yes, and with the extra 5″ of snow, I am expanding my igloo!

The last time I was in Edmonton to visit Enbridge’s corporate office, it was -30 degrees and a 25 MPH wind. Lovely. No one was shopping real estate that day.

As always, I appreciate those charts very much Wolf.

Best,

Fixed rates rose before variable rates creating a pretty big gap, so a lot of the market is in variable rate mortgages at the moment.

That means that each 25bp increase in the bank rate is really going to take a hefty bite out of the economy and the housing market. I don’t think it will take many (plus a little lag time) before inflation is the last thing on people’s minds.

Really? I didn’t know that adjustable rate mortgages are popular these days. That could work out bad for many people.

Canadian house price statistics are bubblistic to many. Especially to the frustration of the average Canadian renter and working person/family. Wolf is informative to highlight the trend. However, there is way more is going than low interest rates, and those undercurrents are constructing those price graphs. A year ago (?), the last time Wolf reported the same observation, the same comment was noted; some might think a small Van Gogh painting is ridiculous at $40M; but it is not to that buyer. And interest rates have a smaller influence on that kind of buyer even if interest rates quadrupled again from 1% to 4%. And those undercurrents will have to fundamentally change to effect Canadian real estate prices. There is both a lot of willful blindness (to quote Sam Cooper) and intended (housing, economic, greed) policy behind those stats.

A $40Mil Van Gogh is only ridiculous if you can’t sell it for even more a few years down the road.

l understand what you are saying. And some to many homeowners could be in that position at some time; if they are job dependent to pay the mortgage which is also max’d out. That is harsh and know of families that got crushed in such scenarios.

However, anecdotally, l was about 30 years in Vancouver BC area, and watch real estate prices escalate, quadrupled. The buyers poured in. Rumoured to have average net worth of $16M. (not all of course, but many, enough). And their street gang kids were driving $500k + cars and using highway 99 as a race track. These buyers use Canada as a lifestyle, banking, and investing centre. Met some of them as neighbours; they are very wealthy people, and they had no inclination to sell, no need to sell, and they were mostly interested in buying more of everything. To quote two of them “it’s free”.

That area got too busy for me, so l moved to a quieter satellite location. And five years later that money followed me, again, and the property prices have near doubled, in that 5 years. A house down the road just sold for over asking, doubled in 5 years, bought sight unseen; owners are rumoured to be HNW people; bought it as a part time summer recreational property; at a ridiculous price, but l don’t think they give a shit what l think, such as about them jacking up my property taxes and turning this neighbourhood into a vacation destination and party house.

It is as if, one has $100M a year to spend, then a $40M on a Van Gogh is not a worry, and they don’t give a flying shit if it goes down in price, they own a Van Goth, the brag about their Van Gogh, they enjoy the Van Goth, and have no intention of selling. And next year they want buy that Rembrandt that everyone is talking about.

For some to many, Canada is more than a place to buy a house, and the price is secondary, to the other aspects of their decision. There is more going on that pedestrian price and interest rates to these Vancouver BC home prices. Read Sam Cooper’s book for a starter. The rest one has to research, to make an opinion, as there is no way the oligarchy and plutocrats wants to spell it out; they would prefer most people to say that is ridiculous. When this situation is not a ridiculously surprising event, it is intentional and it is pernicious.

Where this will end, l don’t know. As world wide both central banks and governments are spending and stimulating beyond the ability of any country to pay it back. And so are consumers, retail investors, and corporations. If Canada’s house prices are in jeopardy, then that is very likely connected to the whole wide world being in a melt down. And that will effect those dependent on jobs to cover their mortgages. But not everyone will be effected. For now we are “melting up”, and it is intentional.

I thought Canada real estate loans reset after 5 years. So while they lock in that rate and payment, if the expected devaluation occurs due to higher interest rates, wouldn’t that mean they’re screwed in 5 years? With an underwater property and higher monthly payments?

yes, this is very correct!

my guess is that most people don’t understand (or care to understand) that their mortgage will renew five times (at an unknown interest rate %) over their 30 year amortization.

keep in mind that there are LOTS and LOTS of socialists in canada…who have given up on independent thinking…i.e., government will come to the rescue for them…so just take that plunge, baby!

it really is madness.

Canada seems to have painted themselves into a similar corner to what we’ve done here. When they raise rates, it’s crash and burn, if they keep rates low, it’s crash and burn. What a cluster.

At least they have a pajama boy running things. Oh, wait….

My common sense says widespread excitement (panic buying) is not a time to buy. But if FOMO reverts viciously into a buyers’ market, it will be uncomfortable then also to buy, in a different way: fear of lacking cash. The overleveraged crowd will then lunge just as desperately for cash. Great to be able to be contrarian, but this takes time to set up.

I bought my home in ’94 just as Greenspan had started raising rates, and mine was originally a variable rate mortgage. That turned out alright, as the buy-in price was superb. Converted to a fixed rate in the post-2008 low point. Likewise I was buying stocks back in the 90s, avoiding the tech bubble (mild regret there), and that buy-in turned out good too. These things smoothed out life when the economy got stressed in ’01 and ’08 and ’20. I’m glad I did all that, bought and held, because I got those habits in place, just paying my liabilities and not too anxious to get rich.

But I don’t have a new plan, for those starting earlier who I am concerned must perhaps move further out on the risk curve to get ahead financially. The coming period seems to be fraught. I am holding lots of cash and real estate (the latter basically paid for). There WILL be opportunities.

canadians can’t “lock-in” interest rates…

all mortgages reset with new conditions (massively higher rates?) after a brief five year term.

accordingly, the canadian “rush” to “lock-in” rates is absolutely insane–unlike in the united states–where it might make sense to do so.

There are 10 year mortgages but they’re never worth taking out due to the exorbitant rate premium charged.

I am always reminded when I see crazy housing prices that someone is paying for shelter and some people can build that in a couple of hours with a chainsaw and a tarp

I’m always amazed at what a chainsaw can do to a house in less than an hour. Or a match.

I keep looking at the bubble popper, i.e. the price of oil and it’s just hit $88.40 for Brent Crude. Hopefully it will start to drop but you know what hope did….lol

I wonder how much effect homeoffice (remote working) culture will have on housing and travel in the future. I have recently seen quite a few job offers which offer remote work with some travel to different company sites, when necessary. This would enable people to work remotely from e.g. the caribbean plus travel when necessary. But I do not have any insight as to what proportion of the job market will go this way. If a substantial proportion does, then this could have some effect on housing and travel.

What is real wealth creation?

“Errrrrrr ……… that’s a hard one” the economists

Neoclassical economists have always excelled in creating wealth of the evaporating kind.

Why did they abandon neoclassical economics last time?

The wealth evaporation event of 1929 finally brought them to their senses.

They needed to find out what real wealth was.

It took them a long time to disentangle the hopelessly confused thinking of neoclassical economics in the 1930s.

This is when they invented GDP.

The real wealth creation in the economy is measured by GDP.

Real wealth creation involves real work, producing new goods and services in the economy.

That’s where the real wealth in the economy lies.

They used to think rising asset prices were creating wealth, but after 1929 they realised this was not the case.

They needed to find out where real wealth was created in the economy and they invented GDP.

This is why GDP is the thing we want to grow; it is the real wealth being created in the economy.

The futility of pumping up asset prices only to watch them collapse again.

It seems futile to me, global policymakers seem to like it.

Real estate – the wealth is there and then it’s gone.

1990s – UK, US (S&L), Canada (Toronto), Scandinavia, Japan, Philippines, Thailand

2000s – Iceland, Dubai, US (2008), Vietnam

2010s – Ireland, Spain, Greece, India

Get ready to put Australia, Canada, Norway, Sweden and Hong Kong on the list.

It wasn’t real wealth, just a ponzi scheme of inflated asset prices.

They don’t just like it, they love it.

How’s your real estate ponzi scheme, Xi?

It’s on the verge of collapse, mate.

They never learn.

Creating real wealth is only a part of the problem. The true value comes from useage over time. Once created, unless it’s booze, you can’t just store it in a bottle. So you must employ a medium which works as a storage system…i.e. money. One of the basic requirements for something to be “real money” is that it must retain a great portion of inherent value over time. The faster asset valuations increase (through speculative bids), the less that medium will be able to satisfy this basic tenet of “real money”. Result-Less desire to produce real goods and services that are longer-time related in exchange for that medium. Economic failure. Asset failure. Bank failure. Government at risk. Conclusion-A government working for its’ population might want to see the air go out some. And, thus, a government which does not work toward that goal may in fact have become an agent of a foreign enemy even if they do not realize it. Wakey, wakey.

“And, thus, a government which does not work toward that goal may in fact have become an agent of a foreign enemy even if they do not realize it. Wakey, wakey.”

Agree. At the very least, if the population which you employ as security is demoralized, and your workers are demoralised..

We got a perfect president for a 250 years empire.

Don’t worry: Trudeau will open the floodgates to money launderers and desperate “international students” who want to live ten to a room inside a basement or furnace room.

You’re looking more like US every day..

Journalist turned Finance Minister Chrystie Freeland wants to seize the bank accounts to pay for the retirements of the real estate speculators.

Regarding the pandemic era house price increases, might this not simply reflect a genuine increase in the value that homes are providing to a significant proportion of current and prospective homeowners who used to commute daily but now work from home full time.

Such folks might now be spending double the number of waking hours they did in their homes previously and making greater use of their kitchens for lunch, coffee, snacks etc., basements for home offices etc.

There is not just perception of greater value but actual savings on commuting costs (gas, parking, public transport tickets, lunch/coffee/snacks outside, dry cleaning etc.) leaving more money available to spend on housing than before.

If this shift to working from home becomes permanent, this increase in value provided to homeowners is really permanent and sustainable too meaning that house prices have reset to a permanently higher plateau than prior to the pandemic.

Couple of similar examples from the past:

Real estate in the southern US became more valuable after the invention of air conditioning since southern summer living became much more tolerable.

Land outside cities that would become suburbs became more valuable after widespread availability of automobiles and good roads or efficient public transport infrastructure.

two points in response.

first, i think the idea that most people will be working from home permanently going forward is a fantasy. it seems that hybrid (2-3 days a week in the office) is where we’re heading. that means that the house can be farther out than it was, but can’t be in the literal middle of nowhere.

second, if the demand for single family homes in the suburbs was driven by work from home, then you’d expect to see a corresponding decline in the prices of condos in the cities. we haven’t seen that in most cities. in fact, we’ve seen large increases there as well.

no, the current prices are driven by low interest rates and investors/speculators buying up housing with no intent on using them for housing.

Unfortunately, your choice of words “permanently higher plateau” was exactly the words Irving Fisher used to explain why stocks were in no danger prior to the 1929 crash.

The Chinese are money laundering through the Canadian real estate market…

Now, in the US, I read that one third of corporate residential purchases are foreign.

But the entire industry/markets are SKEWED by the central bankers keeping mortgage rates well below inflation. Unheard of in real markets…emblematic of arranged and manufactured, free market interrupted situations such as we have here and in Canada.

Why is Canada pitting one large segment of the population (renters) against another (home owners), by encouraging home price distortions? No government should be willfully dividing a population in this manner, as a direct intended result its actions.

These price rises are way too severe to be considered side-effects of policy. The charts go straight up, for years!

Divide and conquer easy peasy

The best time to buy a home is at the PEAK in the interest rate cycle. At that time prices are going to be at their lowest. If you can find a motivated seller you can get a great deal. Don’t worry about the high interest rate you’ll be paying on your mortgage. You get to refinance when the trough in the rate cycle comes. Result – low home price and low mortgage rate.

It is sad. The price of a home will go higher over the long term. The 2006-2011 U.S. housing price decline lasted about 5 years. This was probably the worst housing bust since the Great Depression. The NASDAQ 2000 sell off lasted a long time, started to regain parity, then went down with housing in 2008. The best time to buy was when foreclosures were the highest and people’s credit ratings were ruined.

Yep. A friend who was a lower income person bought a HUD foreclosures for just under $50K during last housing crises. She got in on the brief Federal credit where you got $5K if you held the house five years.

She put very little down with FHA and refinanced it after a couple of years to get rid of PMI. Her house payment was right at $400. Once it was updated with a lot of sweat equity it was a nice home.

She was lucky. In most parts of California no bank would loan towards a foreclosure. One had to pay cash for the full amount. They would not even loan with 50 – 70% down.

On top of that most banks in Ca will not give a loan less than $100K. Many don’t like to loan less than $200K.

There were a few Fannie Mae and USDA loans but very few AFAIK. From what the local banks told me, none of those would be taken on their houses. Only on specific homes that were put in the program, and those were higher priced.

I bought a 2,000 sq. ft., 3+ year old brick and Hardiplank single level, 3 bedroom house in 2011 in Texas in a great neighborhood for $62/sq. ft. There were foreclosures and HUD owned houses everywhere. I wish I could have bought a few more at that time. My daughter lives in it now.

It appears the asset bubble has finally been pricked. Wolf has done all of the heavy lifting revealing the truth of the Fed’s overstimulation. With any luck, we suckers holding cash in the face of raging inflation will be justified with lower asset prices, not just in stocks, but especially in real estate. Crashes tend to happen so quickly that most participants are like a deer in the headlights.

Instead Buy the Dip, you need to Sell the Rally.

Rest assured there will be a downward move in RE sales prices, most likely in connection with an equities bear market and a recession. Not this month, though…….maybe not this year……maybe not in ’23……..etc. But it will happen. Personally i will call it to happen in the window of ’23-’25.

Fed running negative 7% real rates makes economic calculation impossible, so people are just gambling on assets now. Going to cause a lot of people to get wiped out.

Recession and bear mkt could happen faster than any one imagine! Fed may do some ‘kakamania’ short term delay but eventually, reversion to the mean is guarateed. Once the recession hits, house of cards in housing also get hit! Most likely in early or mid 2023!

Bull and BEAR are the two faces of same coin. One cannot keep enjoying beyond it’s time (even with persistent puts) and thew Bear will growl back furiously. There will be a lot BEAR SQUEEZEs just like today!

What goes up higher & higher, with suporting fundamentals, will fall much harder than previous falls. Mr. Mkt ( in the long mkt history) never accomodates the majority, especially now, in the abscence of Fed.

The problem is the local Chinese in Canada has zero or zilch in any stock market (everything is in real estate) and the tagalongs the local Pakistani’s and Punjabs who only copy what the Chinese do also have zero or zilch in the stock market. We’ll just have to see how long the Chinese keep on buying.

The bottom is falling out. It is time to step on the gas.

Men lose their minds in herds, only to regain them one by one.

The gorilla in the room being sorely missed by DIP buyers jumping into this ‘sliding’ mkt!

Without Fed there are NO mkts either here or any where in the world! Rate cuts by China is a desperate attempt and will go no where!

Down the months the inflation may turn into DEFLATION but I don’t know the time frame. Oil hitting 86-87, once it reaches 90 or 95 will trace back b/c coming recession. This is ALL the pay back for the ‘Easy-Peasy’ money policies from Fed/Cbers since ’09! It is unwiding furiously. Of course mkts will try to be GREEN in the morning but cannot hold it by the end of the day, just like today! Once the sentiment turns into out right, fear, lookout below!

Canada is no different than everywhere else. It’s the everything bubble. Our government’s spending like mad, printing and giving away money with nothing interest rates. Savers and investors are being destroyed to keep speculators and scam artists going, who now seem to be in majority. We are still in lockdown, with people not working or pretending to work from home. Productivity is zero, and why not if you get free money. I keep thinking this will end badly, but the Bank of Canada like other Central Banks, seem to be able to postpone the day of reckoning.

true, but I would say the excess of housing price run-up in the large cities like Toronto and Vancouver has been far in excess of most U.S. cities. It’s a perfect storm (self-inflicted) of supercharged demand (high immigration quotas, lax money laundering rules, flight-capital friendly policies, homeownership FOMO fever, speculators benefitting from low-rates and not having to pay any flipping) and suppressed supply of homes that people really want (most newer condos are 1-bedroom speculator units, and slow process of approval and greenbelt have limited supply and larger units are less economic for developers).

…and as a backdrop furthering this is that people believe “cash is trash”, and fiat money is being devalued and houses are inflation proof. I’ve known a few people who bought someplace new but didn’t sell their old (rented it out instead)….this wouldn’t have happened a generation ago. As Wolf says, the central bankers have moved mountains to make speculators whole, and all these real estate buyers feel like geniuses.

Unrelated to your article.

Elon Musk lost $27 billion, Bill Gates $9.5 billion, Jeff Bezos $25 billion, Zuckerberg $12 billion and Larry Page $12 billion since January 1st. Ouch there losing it at much faster pace than they made it.

Im sure the FED will reverse course let inflation fly and bail out the Rich again more QE to follow.

I dont buy for a second the people who own this country won’t get corporate welfare again. But you go ahead and believe what you want. After 4 QE’s I believe that speaks for itself.

The FED has been responsible for every financial disaster this country has ever had. More to come but they will prop up the Rich.

Oh and currency reset is coming im suprised you havent mentioned CBDC. Thats the start of the reset. Crap dont happen over night, they start off slow. Like seatbelt laws first its a non moving violation and they cant pull you over for it but as times goes by its a moving violation.

Wow, reading most of the endless comments to this one post confirms the RE super bubble is alive and still kicking. using!! All funded courtesy of government GSE’s funded loans, not a free market. Banks that originate your loans sell them in 30 days to the GSE’s, who absorb the inevitable extraordinary losses at taxpayer expense. Gee, so everyone thinks this shell game will go one forever, huh?