“Net income” is a bizarre term for an organization that buys trillions of dollars of securities with money that it itself created.

By Wolf Richter for WOLF STREET.

The Federal Reserve’s balance sheet is a gigantic pile of assets on one side and liabilities and statutory capital on the other side. That balance sheet, which is released weekly and which we discuss frequently, generates a lot of income and a lot of expenses. In addition, the Fed gets income from fees. It has a ton of operating expenses. It pays dividends to its shareholders. And it remits to the Treasury Department what’s left over. The Fed discloses all this annually in its financial statement.

On Friday afternoon, the Fed released its unaudited preliminary financial statement for 2021. The audited financial statements will be released later in 2022.

For what it’s worth: The Fed’s audit firm, KPMG, has been entangled in innumerable scandals – such as using stolen regulatory information to cheat on audit inspections – and massive audit failures, such as of UK outsourcing giant Carillion, which suddenly collapsed at the beginning of 2018. So there’s nothing to worry about.

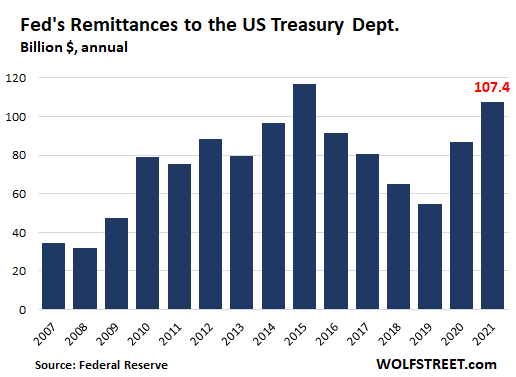

The Fed’s total “net income” for 2021: $107.8 billion.

The Fed is a very profitable organization. For 2021, it reported “net income” of $107.8 billion. But the Fed’s term “net income” is somewhat bizarre for an organization that buys trillions of dollars of securities with money that it itself created. But OK, we’ll go with the flow.

The Fed doesn’t pay income taxes, but it remits nearly all of its “net income” to Treasury Department, as required under the Federal Reserve Act.

By comparison, Apple booked a pretax income of $109 billion in its fiscal year 2021, just ahead of the Fed’s $107.8 billion. Apple’s auditor is Ernst & Young, which is tangled up in its own long series of scandals and audit failures.

The Fed’s total Revenues: $123.1 billion, from:

- $122.4 billion in interest received on its holdings of securities, mostly Treasury securities and MBS that it purchased as part of its QE.

- $275 million in net income from its pandemic era emergency programs that are being unwound, such as the corporate bond and bond ETF holdings that it sold by November 2021.

- $457 million in fees from services, mostly paid by the banks.

The Fed’s total Expenses of $15.5 billion, from:

- $5.3 billion in interest on reserves, paid to the banks; the Fed pays 0.15% interest on cash that the banks put on deposit at the Fed.

- $1.9 billion in foreign currency revaluation losses

- $414 million in interest paid to counterparties of its reverse repos.

- $1 billion in costs related to producing, issuing, and retiring currency (the paper dollars).

- $5.3 billion in operating expenses of the 12 regional Federal Reserve Banks, including the salaries of the luminary traders that run these FRBs.

- $970 million in expenses of the Board of Governors (the federal agency, of which Powell is the chair)

- $628 million to fund the Consumer Financial Protection Bureau.

The Fed paid Dividends: $585 million.

The Fed paid $583 million (with an M) in statutory dividends to the shareholders of the 12 regional Federal Reserve Banks. The amount represents about 0.55% of its net income. These 12 FRBs include the New York Fed, the St. Louis Fed, the San Francisco Fed, the Dallas Fed, etc. Their shareholders are the largest financial firms in their districts.

The Fed paid the Treasury Department $107.4 billion.

Nearly all of the net income was “remitted,” as the Fed calls it, to the Treasury Department, as required under the Federal Reserve Act. The $107.4 billion for 2021 was the second-highest amount, behind the record in 2015.

That record in 2015 was composed of two elements: $97.7 billion from income and $19.3 billion from its “capital surplus.” The Fed had a statutory limit on its “capital surplus” of $10 billion, set by Congress in the Fixing America’s Surface Transportation Act of 2015.

In 2018, the remittance of $65.3 billion included $3.28 billion “capital surplus,” as required by Congress under the Bipartisan Budget Act of 2018 and under Economic Growth, Regulatory Relief, and Consumer Protection Act of 2018, to bring the capital surplus down to $6.825 billion.

For 2021, the $107.4 billion remittance included 40 million to reduce the capital surplus to $6.785 billion, as required by Congress under the National Defense Authorization Act for 2021.

This “capital surplus” is disclosed on the Fed’s weekly balance sheet. As of its current balance sheet, the Fed had $33.7 billion in “capital paid in” plus $6.785 billion in “surplus” capital, for a total capital of $40.5 billion.

The remittance of $107 billion to the Treasury Department means that the portion of the US debt that the Fed purchased (currently $5.68 trillion) is essentially interest free for the Treasury Department.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Why doesn’t the Fed buy all the government debt and unfunded liabilities and retire it? $200 trillion over the next 30 years should do it.

You can’t buy “unfunded liabilities.” No one can. You can only buy assets.

If anyone could fund those debts, it’s the Fed.

Certainly not taxpayers.

I agree you cannot directly buy unfunded liabilities. However the federal government could issue bonds to fund these (previously unfunded) liabilities and the federal reserve could buy those bonds. Another related question is why do we need to pay taxes at all if the federal reserve can do QE to fund the federal government?

I think the answer is tax policy includes carrots and sticks to influence behavior.

SB, Why do we need to pay taxes at all…? Spending can cause inflation. All spending, private or public, tends to cause prices to rise because it requires that real goods and services be produced and exchanged for intrinsically valueless currency. Yes, sovereign national governments really do have a limitless supply of their own money, but it is quite easy to behave in a way that devalues their currency by making it too easily available. Taxing reduces private demand, makes money scarcer. If governments spent without taxing inflation would be sure to follow.

Really good article. Glad you decided to “go with the flow”, and just treated the Fed as one of our more extreme “public-private partnerships”, instead of what it’s up to and how it affects society and “investment”. Fuck investment and investors….they fucked the society, and are still at it.

Have been reading the history of “fractional banking” (money printing) and the wonderful things it can do for “growth”. Seems to me the first shot at it in 1609 was also a “public-private partnership” with the city of Amsterdam. Likely involved the first “lobbyists” (or the old post American Revolution term, “BORERS’, which is really much better and accurate, and should be changed back). Enthroning the corporations was a VERY VERY VERY bad move….Sorry Abe, but your prediction was right. Seems nobody wants to give up one damned dime of their so called “hard earned dollars” or ever will.

That said, growth for growth’s sake is obviously the ideology of a cancer cell, so I am grateful I have a Biologist world view and made it to the age I have. And didn’t take much from this ball in space or those who shared my existance time…for a white American, anyway.

Oh, and also thankful for Biology, rebellious friends, and college, which got my head out of that stinking God damned Southern Baptist Calvinistic upbringing which I was almost doomed to.

I’m gonna read the rest of the comments and switch to evolution and abiogenesis tomorrow.

Even the Fed and all it’s banks aren’t rich enough to buy the “full faith and credit” of the USA and everyone in it…not there aren’t those who wouldn’t do so, given the chance, sadly.

Real sociopaths, we just dodged the first of them, I’d say.

Theoretically the Fed could buy up the entire stock of Treasury debt, and send Treasury a letter saying “You know all that money you owe us? Forget about it.”, and tear up the notes. Presto no more Federal debt.

But don’t imagine it would be consequence free…

It would be a technical default by the United States on its debts.

Not necessarily, if left on the Fed’s balance sheet.

:) Not to worry, I agree that default, no matter how far removed from where it belongs (“front and center”) is inevitable.

Despite Yellen’s proclamation to the contrary, it certainly would NOT be the first U.S. Treasury default. There’ve been several already in the U.S.’s past, some in the past 50 or so years.

Finster,

Most US government bonds/US debt is owned by US people and US corporations, so you are effectively saying that the government agency on the owing end of the debts, should be changed and that they should just refuse to pay. That is a default.

If the US Financial system collapses/experiences severe inflation. We might as well pay, because the dollars wouldn’t be worth much anyways.

If it doesn’t, in the future, I’d expect all US debt to have negative interest rates, if this happens, there would be no interest payments on the debt, also inflation and the negative interest rates will slowly erode the size of the debt over time. I see negative interest rates as the most likely scenario, because there is simply a massive glut of savings/investment in the world and once all the bigger bubbles pop, most savings and investments, should logically have a negative rate of return. It seems crazy, because people are taught that money magically grows forever when “invested”; but, most money “invested” nowadays, is simply buying and selling assets and not towards actually growing companies or the economy. There is simply not enough worthwhile investments to substain the amount of money saved up; this has resulted in massive asset bubbles across the world.

If for some reason negative interest rates aren’t possible and large inflation doesn’t happen, as a young person, I’m demanding a default. I’m not paying for these debts. It’s possible that to preserve most of the US’s financial status, that we simply pay back the international bond holders and default on the bonds held by Americans. We don’t have to pay back those from unfriendly countries. Refusing to pay the modest holdings of poor countries, wouldn’t be worth it.

what is the percentage of return for the dividends

Since no one can buy or trade the shares, there is no market price for the shares. The shares aren’t held by the financial institution for the little bitty dividends they each get, but because they own the FRB and are able to choose its Board of Directors and the governor of the FRB who then gets to vote on monetary policy at the FOMC. This is how banks make monetary policy. And this is why the US won’t ever get negative interest rates – because they’re bad for the banks and for bank stocks.

Negative interest rates on US debt (Bonds, T-bills, and treasuries) is what I’m referring to. Bank loans should always have a positive interest rate.

Banks should always give out positive interest rates loans to customers and banks should always have to pay the FED positive rates to borrow money from the FED.

Once you get away from banks though, the effects of an overwhelming savings glut takes effect. If very little money was saved or invested in the world, people who do save, would receive a large rate of return on their investments. However, as more and more money gets saved/”invested” it becomes harder and harder to find worthwhile investments that will actually grow economies and grow companies that would yield a natural healthy positive rate of return. As more and more is saved/invested, the available options for investment, become worse and worse and the rate of returns, should keep dropping. Eventually, the rate of returns should turn negative, this is possible, because, at a certain point, foregoing today’s spending for the future, it becomes increasingly difficult to find something to hold onto that even maintains its current value.

Right now, everyone is creating asset bubbles out of everything.

Because the world has enjoyed the benefits of a very large demographic dividend (the large increase in population) for decades, it has been possible thus far, for the number of people investing to have their money going into these hot potato assets to exceed those in retirement, cashing out; resulting in skyrocketing valuations. Most of these assets do have real value, but far less than their current valuation. Some property markets will also do very well and grow from here, but, which ones?

As the asset bubbles pop (new ones will still emerge and pop over time), it will become increasingly difficult for those with large savings to find safety assets, that maintain their current value. For the general population, the only realistic retirement option is to increase social security over time and other government programs; redoing the entire structure of government programs will be necessary. After owning, debt free, the things you use, an average person, would just stick excess money into their savings account; retirement (social security) would be taken care of, for them. For those who holdings begin to exceed the insured level of savings at the bank, they can choose to purchase safer assets such as US debt, which will probably have a negative rate of return, or at least, always below the expected level of inflation. People in other countries who don’t have access to insured bank accounts or that have unreliable national governments might also purchase US debt at a face loss, as it would still exceed the averaged rate of returns for the other local investments/assets available to them (they might also be just diversifying their investments). Other countries like Germany, will probably also have negative paying bonds.

Once the debt of major countries starts to pay negative interest, it becomes a very safe investment, because defaults, become less and less likely. Unlike companies, governments are unlikely to just go out of business and disappear. Government debt is also probably going to have special tax rules, that benefit its holders (for citizens of that country, who buy its countries debt). Unlike property, it will not require maintenance or property taxes. Stocks will of course, still be major place to invest. Corporate bonds will likely have less appeal, especially as many of the big names, disappear over time.

Buying other assets after the bubbles pop, will adjusted for inflation, have very up and down valuations.

The specifics of how this will effect different countries, will vary. Immigration is a factor. As is the generational wealth divide and how younger generations will want more of the pie (each country as a different situation with this).

The overall economy can still do very well and grow once all this happens. It will also help that the primary purpose of the US government/the FED will no longer be to grow the asset bubbles. Most countries will probably do a lot better and have real growth, after this new period sets in.

Savings accounts will pay an almost zero, but positive rate, just like they currently do.

If it is correct as they say the banks make their money on the interest rate margins, banks will still earn money if the interest rates are negative. The interest rate difference must just come out in favour for the bank. That is deposit rates must be more negative than lending rates.

On the other hand, if it is true as some say that banks create money out of thin air with the mortgage paper as a counterpart, the banks are screwed with negative interest rates. ;)

Sams,

Banks have a very tough time charging negative interest rates to their customers: People take their money out of their bank accounts, people are changing to banks that don’t charge it, people HATE negative interest rates and it motivates them to fight.

Look at the European bank stocks — they have gotten crushed over the past 10 years. And the ECB ended up giving them a special deal to overcome the problems on earnings that negative interest rates pose. Same with Japanese bank stocks going back further. The core business of banks (lending) thrives when there is a steep-enough yield curve, and you can get that steep-enough yield curve only with positive rates, and with higher positive rates.

How is a bank going to make money on a 0% loan if its own depositors yank their money out of the bank if the bank charges them negative interest rates?

Negative interest rates are terrible for banks. And they’re terrible for the economy.

The moment interest rates go negative there will be monetary deflation. With monetary deflation, prices on goods and services may fall, like they rise with monetary inflation. That is, those CPI and other “inflation” indexes will also turn negative. Now, is deflation terrible for the economy?

I do see that negative interest rates are terrible for banks and financial institutions, as their wealth would and with that their power will wither away. Another problem is that a liquidity squeeze may follow. The last one can be rectified with governments by infusing some of the money nullified by deflation to some that actually do spend this money on goods and services. That will stop the economy from seizing due to liquidity squeeze. For sure this will redistribute wealth and power, but society as a whole may be better off.

Savers that have money in the bank may come out even or better, as the spread between interest and CPI stay or improve to their benefit

I see as just a default through inflation, which has been taking place anyway. The FED issues dollars to buy the Treasury debt. Dollars are substituted for debt. More dollars in the system, cheating existing dollar holders of value by making their dollars less valuable. It has been happening to savers for some time now.

That’s exactly what Congress should instruct the FED to do. Nationalize the banks, the payment’s system, institute reservable liabilities and reserve ratios necessary to sterilize the purchases.

That $211_Trillion estimate was many years ago BEFORE the latest waves of money printing every year since 2015 or so. More of the “Fed” banksters’ money printing will lead to Zimbabwe-like hyperinflation. To avoid paying taxes, the super rich have, are, and will in future create MASSIVE, US inflation. They transferred US jobs to CCP subsidized, quasi-slave factories for decades to avoid US taxation via the foreign income exclusion from US and EU taxation loopho!e.

What, no taxes? Who do they think they are, Amazon?

andy,

Maybe Amazon should remit all its pretax net income to the Treasury Dept., like the Fed does. That would amount to 100% taxes :-]

I’m curious, How many of you readers find the FED to be as evil an entity as I do?

Wolf, you won’t but I’d enjoy your take most of all.

Evil entity is an interesting description, why pray tell do you think that an institution created in1913 is evil.

Is being evil part of the mandate as described in the Federal Reserve Act?

Don’t know what the date has to do with it.

As far as the mandate, it seems unlikely that the word evil would be in the lexicon of the creators.

The evil proof is in the pudding. The evil is in what those Federal Reserve rascals have done to the economy.

I don’t think of evil as some childish magical property that some folks with weak minds attribute to ghostly entities in the air, but to real world actions carried out by real, malevolent people for their own gain.

In case you missed my comment, hahahaha

https://wolfstreet.com/2022/01/12/most-reckless-fed-ever-real-federal-funds-rate-now-the-most-negative-ever/#comment-401476

dishonest

me +1

Evil, absolutely. But also blinded by such rapacious greed and arrogance, consumed by it, that they don’t believe that the rules apply to them, that history would never be their guide because they are magical beings to whom the rules do not apply. To say they need to be knocked down a peg would be a gross understatement. They need to be stripped of all of their wealth and dignity. They deserve no better.

I don’t think any system is inherently evil. I think it can be composed of percentages of evil people- clinically selfish, if you will, but much more importantly it can have very bad or evil (clinically selfish) social values.

I think our entire society has misplaced values on social behavior and selfishness is exalted.

With that said, any system you might put into place would be corrupted.

And with that said, even with that said, I’d prefer all the clinically selfish people would just go jump in a hole rather than bother the rest of us.

The banksters’ misleadingly named “Federal” Reserve is a gigantic, evil, rip off scheme used against most Americans and others to steal from them their earnings and savings

The Fed is the epitome of the word evil.

(The man myth and the legend)

1. Lets see how much each of fed’s member (or their family members) had earned

2. If any, I would like to know, how they earned more than 1 million

3. May be they skipped avocado toast, took public transport and shopped on clearance sales in the macy’s

4. How much properties they purchased during their lifetime (not inherited)

5. If the value of property is more than an average home price, I guess they got zero interest mortgages or with cheap interest

6. Who I am kidding. Hard work pays off…

The Fed’s remittance to the treasury should immediately be applied to the national debt.

It is indirectly because it’s money the Treasury can spend but doesn’t have to borrow. So in effect it lowers the national debt over time.

So we’ve saved ~$190B since 2020 ($85 + 105) versus the nearly $10T spent. Woohoo! Thank goodness the FED can monetize all that debt.

So, I asked the question the other day, but maybe, Wolf, you don’t know the exact amount. So when the FED creates QE it’s basically putting money into banks’ reserve account with a few electronic key strokes (aka magic money), correct? Since the FED has all sorts of assets on its balance sheet and it must remit any annual net profit back to the Treasury each year, then approximately how much of the $8.8T is this magic / key stroke / bank reserve monies? $8T, $6T?

Like you’ve said, the FED could sell of $1.9T in assets before it really starts to dry up most of the excess reserves. Okay, maybe you didn’t exactly say that, but it seems reasonable. That doesn’t sound like a big deal, I guess. But if this is generally the case, honestly how much more of its balance sheet could it run off before there’s a similar type of September 2018 reaction from the central banking system where overnight loan rates shot up to 10%?

Just wondering. The FED’s balance sheet really seems like its a big part of unwinding all this inflation caused by a gigantically swollen money supply.

I seriously doubt a buyer could be found to buy the Fed’s balance sheet assets. Low coupon notes one step above garbage.

We might start seeing federal debt sold without recourse. A sort of perverse due diligence in reverse.

There is no recourse now.

If you mean where UST are sold without the statutory requirement to refinance or retire it, no private buyer will ever want or buy it. Current buyers are already being plundered through debasement of its purchasing power.

Biggest and longest lasting Ponzi scheme in history.

Creating fiat money and monetizing debt has worked and continues to enable our leaders to create tens of trillions of debt.

The emperor is butt naked.

“Round and round it goes; where it stops nobody knows.”

Cheers,

b

Fed has facilitated the bubble. If we were at normal long term stock valuation measures the SP500 would be 1440. Now they are trapped with an asset bubble and high inflation.

I see the FED as an enigma wrapped up in secrecy which from all appearance is above the laws of this nation and either ignored by the public or reviled.

From my perspective its main function is the transfer of wealth from the working people to the financiers. It is succeeding very well at this task.. It openly lies about its objectives and has way to much power for an entity that is both above the law and lawless.

It has two mandates which are opposites so it can obfuscate to the public which ever best achieves its goals of making its governors and its sponsors the elite of the elite.

I am not a fan!

In theory, the Federal Reserve Act is subject to repeal by Congress.

In practice, it isn’t.

Ah, yea. Why would they EVER drop access to unlimited fiat resources? The only saving grace (for the time being) is that other CBs worldwide are just as profligate, or more so.

> from all appearance is above the laws of this nation

One angle I see is, by now it is the resolution of an impossible dilemma and political stalemate: the owner class and its minions cannot reach a political (true congressional) agreement with the lifelong welfare class and its minions. Our experiment in self-governance is not working as chartered. Hence, the expedient of printing money from air (not from consensus and some more concrete backing), to redistribute to groups that are technically insolvent and would riot tomorrow (either group of minions, either political party). And, when really weird things happen and congress is prodded into action (2010, 2020) it comes out even weirder, because at such moments there is no discipline anymore anyway. So they just print and spend in some other way. Papering over problems is always politically preferable to calling all the bluffs and, by now (I pray not) going to anarchy and gangsterism. The Fed in this has been a cause and an effect, methinks. There might have been a time for sobriety ….

PHleep. If you haven’t noticed, your “ownership class” is also the largest “Welfare Class” the USA has…………and yes, they are very happy with the status quo.

August

In practice the Federal Reserve Act is not “in practice”.

“The Federal Reserve Act 1977 states that the Board of Governors and the FOMC should conduct monetary policy “so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.””

All you hear is the “dual mandate”, and the stable prices part of that is completely ignored.

Notice the mandate of “moderate long term interest rates”.

You will never find mention of that on the Fed’s website nor in its regular publications.

Moderate means “not extreme”. Extreme refers to unusually high OR LOW rates. 4000 yr lows in the long end, the deliberate flattening of the yield curve, enabled the games the Fed has played….the raping of future generations to fluff the assets of today.

The low cost of long term debt creation, via these faked rates, is the crime of the century.

The wealth is being pulled forward to run up the prices on housing and reasonable equity prices, depriving the younger generation of reasonable entry into both WHILE burdening them with massive debt.

And what do we do about compound interest on debt growing faster than the economy?

Unfortunately the US is using it’s last dregs of monetary and fiscal credibility. It will not be fun being a non Reserve Currency Country when you have nothing left. Well done the spineless FED.

“The reason that the rich were so rich, Vimes reasoned, was because they managed to spend less money.

Take boots, for example. He earned thirty-eight dollars a month plus allowances. A really good pair of leather boots cost fifty dollars. But an affordable pair of boots, which were sort of OK for a season or two and then leaked like hell when the cardboard gave out, cost about ten dollars. Those were the kind of boots Vimes always bought, and wore until the soles were so thin that he could tell where he was in Ankh-Morpork on a foggy night by the feel of the cobbles.

But the thing was that good boots lasted for years and years. A man who could afford fifty dollars had a pair of boots that’d still be keeping his feet dry in ten years’ time, while the poor man who could only afford cheap boots would have spent a hundred dollars on boots in the same time and would still have wet feet.

This was the Captain Samuel Vimes ‘Boots’ theory of socioeconomic unfairness.”

I was explaining the same to a young lad who asked me why on Earth I had an $800 pair of dress shoes. We did the economics on his $80 pair and worked out I was spending half as much per year as he was.

Then I discussed my $1,200 dollar bespoke suit, and how it paid for itself after the first successful job interview.

My sweatpants I get at Old Navy…and they also are successful at the kind of jobs you turn up to sweatpants in.

My longtime mantra…

Buy well, buy once…

Mantras change as one ages and the timeline gets shorter.

Mantras may change. But some of my real wood (and quality) household furnishings were new 4 generations back.

Weimar Boy Powell – STILL PRINTING.

It feels really weird to begin to sense I’m living in a history book, and not the book I would have chosen ….

I am on about my fourth book about Weimar and its fall. The scheming personalities have odd rhyming qualities to various players now: the warped popular culture, the well-meaning but ineffectual liberals, the drum-beating populist right-wingers, angling for a big moment. We didn’t QUITE have a Reichstag fire yet ….

And I see it all as wrapped up in the fate of the public finances and currency, now. This, in humankind’s last great chance at liberty and prosperity, with so much hope and sacrifice and blood invested. But all that is a wasting asset.

WSJ this week….reviewed a book…

“The Lords of Easy Money”

looks like a good read.

Excellent, timely, deeply troubling read.

Not at all phl:

Just another blip in the trending line showing the ever increasing freedoms of WE the PEONS.

While the second and subsequent derivatives of that line can and do wander positive and negative and always will,,, IMHO, any such indicator of increases to freedoms for the little people has been upward since at least the time of SPQR (Senatus Populus Quod Romanus)…

Suggest you read “Islandia” by Austin Tappen Wright to see at least one possibility, however far fetched.

Of course we have a long way to go just to reach the place our idealism of 50 years ago, ( free love and flower power and power to the people etc., ) suggested.

The good news Wolf is that quite a few million in fed member pay was saved by allowing fed members to make millions via front running the markets using confidential insider information. Sure Martha Stewart went to jail for doing such to make a little over $100k, yet the feds are truly “Above the Law”, a perk that not even Presidents can obtain nowadays…

Also Wolf, good news that the Fed did not have to pay any taxes on all that “net income”, as even the mafia paid taxes through washing illegal funds to make it clean, but the Fed is again “Above the Law” and even an institution as powerful as the IRS can’t leash the Eccles Beast…

I have been saying it for many, many years…the Fed and their members are most powerful individuals on the entire planet at this point in time, as even Xi or Putin or whoever can’t manipulate the entire global financial system into systematic debt spiral deflation/inflation financial chaos with a few clicks of a mouse and keyboard. Thus the fed and crew have a “license to steal”…and that license is good for the entire planet as nobody can escape inflation due to globalization of nearly everything…

I would guess the first thing a self-aware A.I. supercomputer would do is find all the dirt on the most powerful person on the planet, J-Pow, and then have him financially destroy all humans in order to take over the resources. And you know, that would be just about as good as an explanation as we have heard from JPow himself…HA

All your base are belong to us…HA

CONgress is in on the scam. Crickets about the FED frontrunning the market, but 1099s for the poor people selling trinkets on Ebay, cause “billionaires are gonna pay their fair share.” Uh-huh, I wasn’t born yesterday…

Congress, and explicitly the Senate Banking Committee, turn a blind eye to the entire mess.

Sherrod Brown and his under handed fluff ball questions that Powell began answering almost before Brown finished asking…

What a joke. Intellectually dishonest. A show.

Wouldnt one think that with roaring inflation, the Senate Banking Committee would hold the Fed to what they are supposed to be doing….suppressing inflation rather that promoting it …. then ignoring it?

Yort,

“…good news that the Fed did not have to pay any taxes on all that “net income”,”

Instead of paying taxes on its income, the Fed gave nearly all of its net income to the Treasury Dept. via the remittance (see chart in the article). That equals an effective tax rate of 99.99%

Wait a second, I thought the Treasury and Federal Reserve had a mega-merger back in 2020…=)

And if they did “donate” the funds I’m sure the Fed was able to write off 37% as a charity donation to the super wealthy, as it isn’t immoral as long as it is a legal, right…—>¯\_(ツ)_/¯<—JPOW

No. That’s called pure Modern Monetary Theory, MMT. Right now, we’re about 60-70% there. MMT purist want to see the FED moved under Congressional control. Not sure if or when that will happen, but QE is basically a very big step towards MMT.

But the Fed created credit out of thin air to by bonds and other assets, used interest paid by those assets to pay all their expenses and salaries, gave some to member banks, and then returned the rest of the interest income to the Treasury.

That is completely different than a corporation or person paying taxes on income EARNED from customers who voluntarily bought their products or services.

The only “product” from the Fed is a 40 year high for inflation, which is not something consumers want.

Right now the Fed “fight” to reduce the inflation they caused is too close to being Blah Blah Blah, to quote famous “climate scientist” Greta Thunberg.

I don’t see much shrinkage of their balance sheet — actions would speak louder than words.

The last time the FED shrank their balance sheet, late 2017 – 2018, the REPO market freeked out with intrabank lending rates spiking to 10% over night. The FED spent months fixing this issue to the tune of hundreds of billions of dollars. Just think about this fact. The FED’s balance sheet could be used to pay off 38% of our current national debt held by the public. Yikes!

As Wolf has pointed out, the reverse REPO market recently parked $1.9T in overnight deposits. The FED currently pay’s $5 for every $10,000 parked in reverse REPOs up to $160B. So, $160B a day generates $80K or $2.4M a month. Not a ton of money but not bad for excess reserves with ZERO risk.

From a recent Wolf article, “At the end of November, all of Fidelity’s money market funds combined had $288 billion in RRPs with the Fed, or 19% of total RRPs at the time (red line in the chart below).”

From a recent MW article, “Meanwhile, Barclays analysts estimate that the repo facility, together with bank reserves, represents about $3.5 trillion in excess liquidity in the system.

the constitution says treasury coins specie.

no fed in the constitution

fed prints liabilities for which it did nothing and contributed nothing

yet which must be repaid

which is thought to be far better than counterfeiting money

but is it

which allows fed government and

indirectly taxpayers to become beasts of tax burden

why not slowly and steadily

abolish the debts so taxpayers dont have to pay them

Paddy…

INDEED…

Congress has the power to mint……and that power may not be delegated. The Fed was designed to allow the money supply to meet the expanding economy, not to whimsically bump it 30% in less than two years.

Congress has the power to TAX, and inflation is a TAX and the Fed promotes inflation (something new that should be contested). The power to tax can not be delegated. Do the People have representation on the Fed? No. Thus we have taxation without representation. Ring a bell?

‘and the slower the Fed reacts – here Hartnett again notes that the Fed should hike 50bps on Jan 26th – on fears of upsetting Wall St, the more inflation & recession risks grow, and the more likelihood US dollar debasement scars 2022.. albeit great for EM/commodities.’

Michael Hartnett is Chief Investment Strategist for BofA. His dire view of 22 is over on ZH. The above quote’s structure is awkward and can be a bit confusing. Harnett thinks the Fed should hike .5% but

the risk is it won’t because that would upset Wall Street. But putting off the medicine means bigger problems like more inflation via ‘dollar debasement’

Coming from BofA this is unusual and will surely reach the ears of the Fed.

nick kelly,

This stuff is getting floated by Wall Street, as to create more uncertainty about the rate hike, and then when the Fed hikes “only” 25 bpts, stock surge because the hike was smaller than expected. This is how the game is being played.

If I was Harnett and the bosses wanted to create a relief emo, I’d say something like: ‘The Fed may make a policy error and raise by .5%’

But he, presumably speaking for the Bank, doesn’t just say they might bump .5, he says they ‘should’. And his prognosis of what happens if they don’t is pretty dire, i.e., ‘dollar debasement’.

Of course this may be just a more subtle setup than a simple Canuck can grasp.

It would be funny if the Bank’s intent was just to do a .5 scare but the Fed decided Harnett was right and went along.

Goldy figures 4 bumps in 22 and possible 5.

Maybe better for market to rip band-aid off with .5?

Agree completely, it is like the tariff news that kept spiking markets each time there was a sliver of positivity after the worse case scenarios had been repeated on MSM hourly. Rain down fear and then pump up with nuggets of hopium…

Every chart I’ve studied leads me to believe it will be a cold day in hell if the Fed could raise the fed funds rate higher than 1.50-2.25%, and even a 3% rate has a lot of TA resistance to stop the rise, let alone the fact the entire system would black swan very easily with rates “that high” in such a highly leveraged, indebted, liquidity driven everything cycle.

And massive $1T/year balance sheet run-off while increasing rates higher than 1.5%…riiiiiiiiiiiight…LOL

…priced in. Nuff said. Wolf likely hit the bullseye with his statement. When rates are only 25 basis points the market will go nuts. More than likely will be viewed as a great victory for the market. As markets creep ever higher and rates slowly increase. The FED is winning the PR campaign. The markets are never spooked for more than 3 days then back to business as usual with ATH every week/month/year

“Rain down fear and then pump up with nuggets of hopium…”

And the frog said: “It’s fine…they were supposed to turn it up 10 degrees, and only did 5! Rejoice!”

Hand wringing over 1/4 pt , 1/2 pt….let’s be real. Inflation just jumped 26 1/4 pts …..

and they are hand wringing over maybe, just maybe going up four 1/4 pts?

Give me a break.

Just watch, these clowns will raise rates by 25 basis points (1/4%) in some faraway time frame – late March or something – and the stock market will roar on the news. They are so far behind the curve that the proverbial barn door is not just swinging in the wind with the horse out to pasture, the barn door has weathered, fallen off the building completely and blown away, and the horse’s skeleton is strewn about the field in hundreds of pieces, long ago picked clean by the vultures.

The FED has failed. There is nothing, I repeat, NOTHING they can do to redeem themselves at this point. They are a failed institution that needs to be gotten rid of. Unfortunately, we have THE MOST corrupt, VILE politicians in history, and they are in on the scam, profiting greatly from it all. “There’s a floor under the stock market” said the 3rd in line for the presidency, Nancy P., and she’s been day trading herself ever since.

Was it the 70’s or the 80’s when they started raising rates slow then suddenly slammed them higher?

Eh Wolf, something’s been on my mind:

what effect would (will) inflation have on the FED’s balance sheet in regards to its debt owned by the Chinese more specifically?

I still think there is an ulterior goal to the FED letting inflation run red hot, with all its (really) negative downsides obviously…

I refuse the claim that the FED is acting like a chicken without its head: I’m trying to figure out what impact could they be looking at creating that would be beneficial for the government. Again, thanks but comments to the effect that the FED is just dumb and just stupid is not a very elaborated claim…

Wolf, in the reports that you read, do they at all ever mention Foreign Debt with regards to inflation?

Total U.S. debt is roughly 28 trillion. According to Statistica, Chinese hold roughly 1.04 trillion (about 3.7% of the 28 trillion). A devalued dollar would hit Japan worse (1.3 trillion), and United Kingdom/Ireland almost as bad (870 trillion).

Significantly hitting China in that way would probably be too costly because it would hit the 96.3% of non-Chinese holders (including about 70% domestically owned). Resulting in a crack-up boom and everything going haywire.

The American empire has lost much of its ability to extort and bleed the world through oligarch power-plays.

Fed is a vast bureaucracy, and it works. Representative government deficit spends in order to put a social net under workers, and corporations pocket the difference between that number and the less than living wage they pay, thus keeping prices low for the masses and profits rolling for Wall St, which flows back to the lumpen as a wealth effect dividend. Then the intellectuals sell you some baloney about self determination, which creates cognitive dissonance, the ultimate misinformation. That leads investors to take on risk, the lucky ones, like Powell, move to the top of the food chain, or they were there all along. Member of Congress unashamedly defend their right to trade stocks. They take private briefings on critical matters of national security, place their orders and make public statements. No cognitive dissonance there, their profits have nothing to do with self determination.

I’ve decided not to vote for any politician belonging to the two major political parties in the next election because of Congress-person’s actions and statements insisting on their right to play the market. Seems like the millions of dollars they collect from lobbyists would be enough.

When the Fed reduces its balance sheet, is cash held as the Fed’s profit? And will it be sent back to the US Treasury Department?

Kiliman,

When the Fed reduces its balance sheet, it “destroys” that cash, in the opposite way in which it “created” that cash when it did QE. So the cash goes back where it came from: nothingness.

But the smaller amount of assets on the balance sheet will lower the amount of interest the Fed earns, and that will lower the amount that the Fed can remit to the Treasury.

I remember getting a $100 bag of shredded cash from the Treasury as a gift when a kid, so that was my first clue that money was nothing more of a concept than anything of lasting value…

Imagine all the houses you could insulate for free if the Treasury had only printed all that digital nothingness…and it is “green” too…HA

… “that will lower the amount that the Fed can remit to the Treasury”. Play the violins !

So the federal government will just borrow a little more money, and continue to spend recklessly like a drunken sailor on shore leave, as in 2020 and 2021 fiscal years. Got to spend lots of money to make the people happy before the 2022 election.

The various governments spent a huge percentage of GDP in 2020 and 2021, and want to spend even more. By my definition of socialism, the US is already a socialist nation:

Federal spending about $7 trillion

+ State govt spending about $2 trillion

+Local govt. spending about $2 trillion

– $1 trillion fed transfers to states & local govts.

= Total spending about $10 trillion

GDP about $23 trillion

Total Government Spending

as a percentage of GDP is about 43%

(43% seems like socialism to me!)

Can the holders of dollars tax a capital gains losses every time they spend the depreciated money?

Its tax time…..

Wouldnt it be a great ruling to force?

What exactly do all these Fed employees do? And why is information on rank and file employee compensation not readily available?

Only employees at the Board of Governors are classified as civil service. Their pay should be public. The rest are not.

Remember, the district banks are technically private.

As to what the FRB does:

One: Monetary policy; that’s what the public mostly knows. That’s the FOMC and all the research staff, both at the Board and districts.

Two: Banking supervision, along with the FDIC and OCC. Primary regulator depends on the charter. There is also joint supervision since the FDIC manages the “insurance fund”.

Three: The $475 million revenue for fees includes wire transfers and ACH, where the FRB competes with private providers.

Four: Providing currency to banks.

Five: Like all other large organizations, a large internal support staff.

You might add a few other important items to your list, Augustus Frost-

Six: Subsidize banks via the interest paid on reserves (a previously taboo policy which deserves discussion).

Seven: Subsidize federal spending by manipulating the interest rate market downwards.

Eight: Attempt to “command” the economy (especially consumer and commercial spending, and employment).

Nine: Employ economics PHDs

Ten: Create money out of nothing to support their constituency and promote a debtor/rentier society.

I read somewhere that 80,000 people work for the Fed at an average Salary of $250K, but don’t quote me on that.

In the Public Eye:

Things that are Illegal are only really Illegal when the public sees and reads that responsible Party / Parties are Prosecuted by Law Enforcement, Courts, Prisons, that sort of thing.

Now when They are Not Prosecuted by Law Enforcement then over time it becomes Legal, and they change Laws (for what’s that’s worth Today)

As Example Insider trading

We are hearing about lots of that. We know about Resignation’s taking place (new get out of jail free card?)

by question parties lately. So, if I work at a bank and rob it, I can just Resign?

But we are not seeing Law Enforcement nor Parties Prosecuted by Law Enforcement Courts etc.

Perhaps this may become Legal sort of like Marijuana as an example of some other recent activity, product, medication the list would be long.

When we have no Government Leadership perhaps this is what happens

Now how this may be connected to an Economist’s point of view may be debatable I expect.

I only know what I see.

It Is interesting when I am reminded of all that’s going on but hard to stomach,

makes me think about moving far far away.

You can bet there were many people close to the senior Fed officials that were just as guilty but not forced to resign. Only an imbecile would believe that the insider trading was regulated to them that exited. Cess pool extraordinaire.

The fed returns interest payments from Treasury. This means that the fed interest rate has no impact to the budget deficit. This assumes the Fed continues to buy the bulk of the Treasury issuance. In regard to inflation, the fed cannot impact the supply chain issue, but can impact the demand side. The Fed will increase the fed funds rate until the demand softens from higher consumer credit card/car loan interest. The Fed can adjust the QE/Taper to minimize the increase in 10Y treasury rate so not to tank the housing market.

WHAT, ARE WE ALL CRAZY?

Why haven’t we been buying SHARES in the FED BANKS

all these years?

We missed the boat….

No it’s not bizarre. The Fed is a private company with stock holders who take profits. The income tax was created at the same time as it in 1913 in order to steal from the productivity of Americans through its debt. The Fed dollar is slavery of the American people through the Treasuries that the primary dealers and it holds. Our “base money” is monetized debt through the Fed then put through the fractional reserve scam system. It’s all a plot to slowly destroy the USA like a frog in boiling water. They steal through inflation over many years as the dollar has plunged 99% since the Fed’s inception. It’s all goes to the top and the debt only gets bigger. There will never be a debt ceiling for this reason. It’s all a sham.

1) The Fed is a bank.

2) In 1930 the Fed got divorced.

3) NY Fed Benjamin Strong, an Anglophile, reduced interest rates for GB. President Coolidge didn’t care, but the flyover Fed bankers opposed Churchill.

4) Roy Young, Fed Chairman of the board resigned in 1930.

5) Banks surplus liquidity, – debt to to depositors – cannot be converted to profitable loans, because interest rates are too low. Every quarter the Fed suck out liquidity, providing o/n assets, to improve bank’s ratios.

6) JP tried to pull negative rates above water, but failed. New members of the Fed are for higher rates to fight inflation and woke.

7) The chaos will spillover.

8) DIA ETF is a Lazer tilting up …

I would say the fed is not a bank because the deposits of banks are held in-house and at other banks. The fed was created to be a clearing house for the banks, using bank reserves as the bailout capital.

Now that Dodd Frank has a bail-in provision, that allows the banks to take bank deposits, they technically never go insolvent. And technically, FDIC will never have to pay as long as the bank has deposits. And the fed isn’t necessary as a result, because the banks can clear among themselves using credit.

Fed sets the rates between the banks. What you are advocating is US Libor. Excess reserves, generated by QE are technically deposits. GS has no deposits, but it has FDIC. FDIC makes bank reserves irrelevant, the Treasury can print replacement cash. I wonder if the problem with the Fed really goes back to 1980 when they were swept up in the Neo Liberal public private policy programs of Reagan Thatcher, and massive deficit spending which required monetization alchemy. I also think Volcker is completely misunderstood. I don’t believe raising rates ended inflation, but it did cement that misconception in the minds of later Fed chiefs. They tighten credit to reduce speculation, and deflate the bubble they created in the first place with excess liquidity. Inflation is always transitory. Recall Greenspan raising rates and opening the REPO window to offset the drain on liquidity, it required incremental rate hike policy and with the Powell Fed using standing REPO they are going to baby step this inflation away. This is what raises the ire of some like Kaufman, he sees what they are doing. The backup in yields (5YR) has only retraced half of the drop since 2018. If the Fed jumps in at the short end they flatten the curve and raise the cost of money and that’s inflationary which Wall St doesn’t care with 20% YOY gains.

People seem to think that QE has put money into the banks, given money to the banks, that its a Fed to banks interaction, yes it has, but the entirety of the mechanism puts the printed funds in -customer accounts- and at the disposal of the customers. The banks can choose not to lend but * they can’t make any decision regarding spending by customer accounts *. The US government spends money, that money ends up in -customer bank accounts-, the government has issued treasuries, the banks have bought the treasuries, the Fed finally has bought the treasuries from the banks with QE. Cut out the middle and the Fed has printed money into deposit accounts. I see this sometimes oh well the banks didn’t lend the QE money so its not expanding the monetary base. No the banks aren’t, the government is.

All the stuff about the Fed reserve requirements and base rate is not about taking back control of customer spending, its about controlling inflation by control of future credit expansion and interest on existing loans.

In the same vein, when the Fed reduces its balance sheet, -it-(the Fed) won’t be reducing the money supply, it will be the -government- doing it. The government will take money through tax, give it to the Fed, and one load of cash and one load of treasuries will disappear. Which means an impossibility for the Democrats, that the US government runs a surplus.

I can remember in the UK around 2006 it was being trumpeted on every single blog for those interested in economics that a crash in housing was coming, it was clear even personal experience that there had been an incredible build of debt, at my company the credit card debt held by those in their 20s was staggering. So people read the blogs, followed the conclusions that their would be a housing crash. Some sold their houses at what they imagined was the peak, some delayed purchases.

What absolutely -nobody- ever literally conceived of!, was that the response would be printing money, because it was taboo. You only ever heard about printing money as Weimar or Zimbabwe, but thats what the UK (and US) did. The UK even put money into RBS to hold down interest rates on interest only mortgages, to prevent a crash in the BuyToLet sector.

What I think people should be thinking about, is what is the -no way they would do that- thing thats actually going to be done. Whats the incredible shock coming down? So thus far, on our fiat adventure, we’ve had devaluations, money printing, interest rate controls, capital controls, rationing (in the UK). What inconceivable population crusher is coming, exactly will the US administration (to lump both Fed and Gov. together) do if inflation spirals out of control?

(btw on the subject of shock I was watching “Get Him To The Greek 2010 comedy” and incredibly Paul Krugman was there he had a cameo still flying high on the go ahead for printed cash)

My guess because I see everyone parrot it:

The very thing they can “never do”

Raise rates.

Crash market.

Sanctioned entities then buy up even more tangible assets at firesale prices…

Repeat in 10-15 years.

Debt jubilee?

Great comment lord sunbeam!

Thank you, that was very educational. With this article, all these numbers are just swimming around in my head with no associations whatsoever to anything at all. I’m just trying to pick up little pieces of meaning here and there and this was very helpful.

Didn’t they do something like start increasing interest rates very very slowly and then suddenly ramped up so fast it shocked everyone in the 70’s or 80’s? I vaguely remember people being shocked as they could no longer afford loans and housing prices hadn’t gone down enough.

Could care less about any rate hikes……any small increases from this pack of crooks are going to take years to have any effect……the only thing that I’am interested in is the sale of securities into the market. Once the players know that the fed is a seller and not a buyer (hopefully the European central bank moves also….some day) the players will become reluctant to purchase treasuries beyond their mandates…..really goosing rates. The loss of value on the books of banks from escalating rates will discourage even the most risk adverse investors. The market will set the rates where they belong much quicker than even we might think.

As for reporting income……..lets give them credit……Al Capone went to jail for tax evasion.

Fred

“loss of value on the books of banks”

Unless I am wrong, and perhaps Wolf will correct me, banks have a choice as to how they value their portfolio……at cost or at market value.

Perhaps this refers only to notes and bonds.

Review FAS 115 for your answer. Mark to market except for assets purchased with an intent to hold to maturity is being adopted.

So they do have a choice…..as their “intent” is defined.

Augustus Frost: “In theory, the Federal Reserve Act is subject to repeal by Congress. In practice, it isn’t.”

Interesting comment. Dalio’s new book (Principles for Dealing with the Changing World Order) has some puzzling assertions, one of them about central banks:

“There is a difference between what central governments and central banks do in order to drive market returns and economic conditions. Central governments determine where the money they use comes from and goes to because they can tax and spend, but they can’t create money and credit. Central banks on the other hand can create money and credit but can’t determine what the money and credit go into in the real economy. that puzzled me.”

I’m wondering how much that is a theoretical definition of central banks. A central bank did not exist in the United States until 1913. The constitution originally gave Congress the power to borrow money on behalf of the United States and the power to coin money, establish currency and determine its value.

I am interested in knowing more about the various federal banks around the world — if they have substantial differences (e.g., separate from parliament or executive governance) or are pretty much the same. Dalio knows so much more, because has he repeatedly emphasizes in the book, he has knows many of the smartest and most famous financial and political people in the world. But still, I have doubts about his cleanly cut definition of central governments versus central banks.

Questions will be asked about what laws may have been broken in the past 20 years. But those questions won’t be able to be adjudicated until 2030. Sarcasm on

Wow! It’s only costing US 970 million bucks to have a great group of guys and gals capable of destroying the paper tiger enemy with a 20% annual trouncing every season. Yeaaaah!

Flu shot in the left arm,

Booster in the right,

Protect our players,

Fight! Fight!! Fight!!!

Gooooooo Team!!!!

Fans will kindly exist through the back gates and deposit your valuables on the way out….you won’t need them at the victory celebration party.

The only precedent for this moment we (and the Fed) have for this situation is Volcker, right? But all the painful lessons of that time are being narcotized, hyped, baited-and-switched. The Fed has few precedents because it spent the last several decades tempting fate. Well, fate is here, at the door.

Mr. Richter, Your second paragraph, second sentence, should that end with 2022?

Yes. Thanks.

Wolf…

The currency losses on the Fed

“$1.9 billion in foreign currency revaluation losses”

Swaps ?

centralbanking dot com website describes this as

“revaluation gains [or losses] on foreign currency investments.”

So seems like it is the changing value of the foreign currencies that the fed holds.

That’s what I’m thinking. At that peak, they had $450 billion in swaps outstanding. So a $1.9 billion loss is less than 0.5%. They’ve been all unwound by now.

Wolf, long time follower, first time commenter ;-)

A simple question…the Fed is technically a bank and it has to follow its own capital rules so my question is, after the crisis of 2008 when its balance sheet skyrocketed and even more with the pandemic response, did it have to increase its capital to “finance” its balance sheet expansion like like any bank has to? It must have its own asset/capital ratio regulation to follow

Thanks!

The Federal Reserve Board of Governors (FRB), which is what one hears about most, is not a bank. They don’t need no stinkin’ regulations. They do the regulating.

The FRB is a federal agency (classified as civil service) that oversees and regulates the Federal Reserve System, which is a cartel of large regional banks. As Augustus describes above:

1. The regional (district) banks are technically private.

2. The FRB, along with the FDIC and the Office of the Comptroller of the Currency (OCC), supervises and regulates the banks in the Federal Reserve system, as well as an associated plethora of financial entities.

3. The FRB also provides currency to the private cartel banks.

4. So in doing all this, the operations of the FRB involve a large internal support organization and staff.

IMO, the FRB has the usurped the power of deciding who are the big-time financial winners, and who are the losers, in American culture. Politicians are too greedy and cowardly to take responsibility for these decisions.

The Fed creates money (QE) and thereby it can create its own capital. In that respect, it is not like anything else in the US. There are statutory limits on how much capital it can have — a maximum not a minimum — and it has to remit the surplus to the Treasury.

Wolf, I understand that but technically, correct me if I’m wrong, when the Fed buys an asset it creates its own liability (the corresponding reserve) in the same way a bank creates a deposit when it lends money or acquires an asset, so we cannot consider the created reserve capital.

In fact there are sometimes academic discussions about the Fed “losing money” on its assets and having to operate with negative capital. So can the Fed operate with formally negative capital if it comes to?

“So can the Fed operate with formally negative capital if it comes to?”

That seems like purely academic discussion to me. They do whatever the hell they want:

“Hey, the law says we can’t buy this set of assets, so we’ll create special purpose vehicles to get around it! Hey, now we’re buying junk bonds! Next time, stocks!”

Dominic,

Cash/Equity Create the Cash = higher money supply

Security/Cash Buy the security

Cash/Security Sell the security

Cash/Equity Balance after the buy and sell

Equity/Cash Burn cash and wipe out the equity =

lower money supply

If the fed losses money on the transaction they net it against other profits and write it off.

The fed holds reserves for the member banks, not against their own assets.

Dominic,

In theory, the Fed could credit its capital account with the cash (the credits) it created if it had to since capital is on the same side of the balance sheet as liabilities. The Fed doesn’t follow FASB accounting rules. It follows central bank accounting, which is obviously different.

But the Fed doesn’t even need to do that because for an entity that creates its own money, capital really doesn’t matter.

The Fed could also make a deal with Congress and not remit the $107 billion for 2021 to the Treasury Department, which would then automatically become an additional $107 billion in capital.

I really don’t understand why people are worried about capital at the Fed. The issue isn’t capital. The issue is money creation through QE.

Wolf , thank you

Mine was simply an “academic” question, I know that the Fed does not have to worry about capital.

Foe example, for the ECB and the sovereign bonds they have in their balance sheet, someone has suggested their conversion to zero coupon perpetual bonds to make them effectively disappear.

There are always ways around any rules….

Jim Grant used to make that spurious point that if the Fed buys bonds and interest rates rise, the value of the bonds need not fall very far (1/4 pt he said!) before the Fed was technically bankrupt. Like having a no down mortgage and going underwater on the property. The Fed just calls it a “deferred asset” and moves ahead. If there were no Fed they would be completing these complex transactions directly with the Treasury. That puts a political dimension on the problem. The Congress does have the authority to directly monetize the Feds balance sheet. And potus can tap DOD funds to build a border wall.

The Fed doesn’t sell bonds. It lets them mature and then gets paid face value for those bonds. There is zero risk for the Fed that higher rates would cause it to go bankrupt. This is just BS spread by people who don’t understand how the Fed operates.

In addition, an entity that can create its own money cannot go bankrupt, not even technically (you’re bankrupt when you run out of money to meet your obligations).

But, Wolf, doesn’t the Fed sell bonds for example when it reduces its balance sheet?? Or just to conduct monetary policy during normal times (buying and selling of assets).

We are all agree that the Fed will not go bankrupt but I’m not sure I agree that, simply by accounting rules, again, a simple academic discussion, the Fed can create willy-nilly its own capital…after all assets – liabilities = capital.

When the Fed creates money it does increase its assets and liabilities….capital can increase if the liabilities shrink compared to the left side (Assets).

Sure returns on its assets will increase capital over time (the liabilities shrink, (the Fed simply cancel then when its counterparts “pay” the Fed) but I’m not sure creating liabilities increase capital…money are still liabilities for the Central Bank.

If the Fed stops buying bonds and lets maturing bonds run off the balance sheet, and if it doesn’t replace the pass-through principal payments of MBS with new MBS, the balance sheet will decline at a rate of over $100 billion a month. In addition, in the first 12 months, all of its $328 billion in Treasury bills will mature and come off the balance sheet. It can probably unload $4 trillion in three years in this manner.

Also the Fed bought a lot of bonds at a discount and at higher yields than today. For example, it bought 10-year treasuries a few years ago when the 10-year yield was 3%. Those bonds now can be sold at a premium if it wants to sell bonds. But it doesn’t want to sell bonds.

It did sell all of its corporate bonds and ETFs and made something like $300 million on those sales.

To keep a lid on things the bottom 40% will require a lot more in 2022 because they got stimulus up-graded in 2021 and will not want to go backward. The Empire must deliver. This is a looming problem that will cause more instability than whatever the Fed may or may not do if inflation stays as high as it is. The Fed cannot jawbone or ignore its way out of $6 a pound ground beef and $4 a gallon gasoline. The majority of people do not give a rats ass about a .25% rate hike or a 2.5% hike. They know only what they cannot get that they could in the past. The political system of blue pill and red pill has dislocated from the people just as the economy has dislocated. They are one and the same. Old military acronym from my military service that I still use applies to this

reality. FUBAR, FU$&ed Up Beyond Any Recognition. SNAFU is a low level event such as getting powdered scrambled eggs and SOS with the runs.

Yes attempted rationalization with friends is making more sense, i believe. The problem isn’t blame at this time. It is on the ground metrics that are part of both red/blue team. There is no party per se to blame as this has been going on at hyper-speed for 15 years well past one side of the political spectrum or the other.

It will be a wild 2022. Movies for one adult and child with meal are now $100 events

Seems the Fed has two choices:

1. Discontinue current expansionist policy, freeing “the market” to dictate US bond prices, leading to higher rates, a period of increased unemployment, a decline (perhaps severe) in asset prices, alla the early 1930’s

2. Continue the current interventionist policy, maintain low to negative interest rates, maintain demand for employees, blow even more air into asset prices, forget Fed mandates 2 and 3 concerning inflation and interest rates, alla Weimar Germany in the early 1920’s.

Both seem to lead to significant social unrest and a severe drop in purchasing power for the US dollar

Yuck!

If the stock market goes down by 30 percent or more or if the home prices go down by 30 percent or more i don’t see how this would cause civil unrest.

Civil unrest would be caused when people are not able to afford anything.

Jon-

I guess its a matter of degrees, as far as the stock market is concerned. Here’s how it might unfold:

A 30% decline is neither so unusual nor alarming;

40% – investors (mostly younger and relatively unaccustomed to big volatility are getting scared;

50% – I’m putting off big purchases, and wondering if I should get out while the getting’s good.

at 60% the mainstream media says “biggest drop since the depression” (healthcare parallel comparison of covid to the Spanish flu);

70% – a whole raft of pension plans, self-directed retirement plans and SIFIs are facing some drastic decisions, with collateral damage to retirees, banks, insurance companies, hedge funds, and residential and commercial real estate all along the way. You get the point.

And don’t forget how all this impacts unemployment, with boardrooms frantic to control margins during a consumer strike.

Eventually the Fed/fiscal stimulators might step in to “stabilize;” but then we’re just back into the same Fed balance/federal debt trap that Wolf has been describing for months.

…or, they don’t step in….see first paragraph.

And therein lies the reasoning for potential social unrest as asset prices decline.

1) Houston marathon in the 30’s F.

2) People pay premium for a Subaru with a virgin bra, before the snow

storm arrive on Sun.

3) Long lines, with loaded carts, in the supermarket self service, because people panic from 6 inches snow. Panic repetitions lead to exhaustion.

4) Long Beach and Savanna clogging are reduced, thanks to envelops

to the stevedore crews. Once containers are shipped to their concentration

camps, their content will be sold at 50%-70% discount, biting inflation.

5) Fri SPY green candle, before a 3TD MLK weekend, half size on higher

volume is good news. On Heinken Ashi this candle is red, closed inside the BB, above Jan 10 close. Backbones tend to form a new bubble, but people pray for the end of the Fed and FANG return to fair value.

6) News, bad or good, move markets, twice as much on bad news than good. Traders panic from bad new, celebrate on good news. On the 2 min chart traders click positions and within 15 min they make their sandwich money, before exhaustion.

1. Marathoners like cool temperatures to run in. 30’s and no wind is just perfect.

Not all of them. I had (lost touch ’08 or so) a good friend and 17 year co-worker who ran the Badwater 13-14 times…Starts at lowest spot in Death Valley, goes to the Portals at 8500 ft, 135 mi. (invitation only)…..he holds the over 70 record still, I believe. (done at age 70). Arthur “Art” Webb. Used to tell me about the wild hallucinations he had, mostly before reaching Lone Pine. My favorite was seeing nothing but all kinds of patio furniture for miles in all directions. Probably Joshua tree inspired.

Ran the Western States 100 several times to qualify for his first time. Same one the lady was practicing part of and got eaten by a mountain lion. Squaw Valley to Auburn X-country.

34 deg F in Muncie Indiana this afternoon. Good running along the White River Trail. 44 degrees forecast for Tuesday. Recommend The Sunshine Cafe for post-run bacon, sausage, ice water and coffee.

Can still find a decent house around here for < $200,000.

Fortune 500 abandoned the area starting around 50 years ago. Last big plant was Borg Warner which made the famous Muncie ‘rock crusher’ Transmission, closed a generation ago. About 6000 jobs at its peak 70 years ago. Plant razed to the ground now.

Progress Rail (old ‘electro-motive, now owned by CAT) is on the outskirts of town. Their counterpart plant in west burbs of Chicago closed a few months ago.

It is interesting to look at inflation history from1800’s until now. You’ll find the dollar holdings its value until the early 1900’s. However, there were several severe deflationary periods in the 1800’s with lots of bank and business failures. The creation of the Fed was an attempt to fix the system, i.e. fix the banks.

And it has – no more deflationary periods and the dollar now being only worth a small fraction (4%). Not sure the system in 1800s was better. Your money could just evaporate during a local bank failure. But a dollar in 1800 pretty much bought as much as in 1900.

GSH- “The creation of the Fed was an attempt to fix the system, i.e. fix the banks.”

“Fix” is the perfect word!

While the Federal Reserve System was perhaps initially intended as a “fixer” of bank instability, 107 years of mission creep has expanded its role to a “fixer” of prices… most notably in the US treasury and MBS markets.

Good points on the comparison between banking in the 19th and 20th centuries.

John

“mission creep”

and it continues.

First, where was the “hey wait a minute” moment when the Fed just a few years ago declared, unilaterally, that they were going to PROMOTE a 2-2.5% inflation rate? They have a stable prices mandate.

And where was the “hey wait a minute” moment when the Fed pounded the long end, flattening the yield curve, when they have a “promote moderate (not extreme) long term interest rate mandate?

And now more mission creep….

Climate Change, Inclusive Employment, Green Energy, Gender Issues, Racial balances…………ie NON of their business. Not in their purview.

Much of the economy from the early 1800’s to 1860 was based on privately issued “wildcat” banknotes.

GSH

To provide liquidity to the banks ….. for from time to time, they have liquidity issues due to the fact they borrow short term and lend long term.

A noble endeavor…..that has run very much astray.

1) JPM and GS gap lower, but the $730B BRK/B went vertical since

Dec 1.

2) BRK/B engulf three candles since Jan 7 close.

3) BRK/B BB : Jan 10 hi/ 11 lo. BB might form a WB bubble !

4) WB trust US gov treasuries paying him minus 5% dividends in real terms, but he doesn’t care, because the $3T AAPL lifted BRK/B assets up.

5) US GDP Q3 2021 reached $23.2T. The rosy est for Q4 are down from

8% to under 2%. US GDP went vertical between Q4 2020 and Q2 2021. GDP is losing thrust, out of fuel, unless on Jan 17 the radical left will give it a booster.

6) SPY cloud front end is narrowing with a tremblant “Dynamite” cliff, sharp edges and dents. Prices tend to penetrate the sexy dents and ski on giant slalom cliff.

7) Draw a line on the daily SPY between Nov 5 and Jan 4 highs // and a

parallel from Dec 3 low.

8) Don’t panic if Heineken Ashi penetrate the cloud, because it might move back up to a lower high above the dents and the cliff, for an easier penetration.

They can legitimately book the “profit” if and when they reduce the balance sheet to zero. Otherwise it’s like Cathy Woods’ ARKK, the book value goes up so long as you are the marginal buyer of more of the assets already on your balance sheet. They’ve proven themselves full of shit in so many ways.

So much bashing of the Fed…

What is the alternative – US Congress issuing money directly,at will ??? Hillary,Pelosi,Ocasio-Cortez and Joe in charge of monetary policy ???

It already happened in 1775 when Continental Congress issued “continentals” which quickly turned into toilet paper.

Speaking of military acronyms, Fed’s current policy may be characterized as UUUU

“We the Unwilling led by the Unqualified are doing Unnecessary for the Ungrateful”

Uncle Jerome,my heart is with you !

Tell all you critics: FUBIJAR:

F.. You Buddy, I am Just a (Federal) Reservist !

Brent

“What is the alternative”

Short rates must track inflation….tick for tick

Money supply can only be raised conditionally and moderately to meet an EXPANDING economy, not a contracting one.

This Fed has been hijacked, IMO. It is coloring way outside the lines. 1/4 pt responses (maybe 4?) to an inflation that just jumped about TWENTY EIGHT 1/4 pts (7%). Absurd.

For 7 decades the Fed kept short rates equal to OR IN EXCESS of the inflation rate. That IS NORMAL.

Taylor Rule is a step in the right direction.

The Fed has too much latitude, and is too subject to influences that often do not serve the nation and People but small cabal’s of oligarchs and powerful financiers

Walmart has a solution for the flood of free money, and the supply issues…metaverse digital good and toys and booze t drown our sorrows maybe??? Leave it to mega/meta corporate America to find a solution, as now society can’t run out of anything as long as we print enough money to buy binary coded stuff in the MetaVerse…HA

A simulation inside a simulation times infinity…

Per CNBC:

Walmart appears to be venturing into the metaverse with plans to create its own cryptocurrency and collection of non-fungible tokens, or NFTs.

The big-box retailer filed several new trademarks late last month that indicate its intent to make and sell virtual goods, including electronics, home decorations, toys, sporting goods and personal care products. In a separate filing, the company said it would offer users a virtual currency, as well as NFTs.

According to the U.S. Patent and Trademark Office, Walmart filed the applications on Dec. 30.

We need real goods, not virtual ones. I really don’t get this virtual stuff.

Nor do I. How do you virtually shave?

Creepto traders, for entertainment only :

1) BCTUSD BB #2 : Jan 8 hi/ 11 lo 2021, 41,616/ 31,842.

2) Price entered the BB, tested Sept 21 2020 lo and bounced back up.

3) Negative options : #1) to BB #1 ; Nov 24/ 26 2020 to : 17,500 area . // #2) to Mar 2020 fractal zone, to 4,000 – 5,000 area.

4) Positive outlook : #1) 70,000 to 75,000. // #2) 87,000 to 85,000.

ARK is …