Thank you, hallelujah, for the extra money, finally. But where did it go?

By Wolf Richter for WOLF STREET.

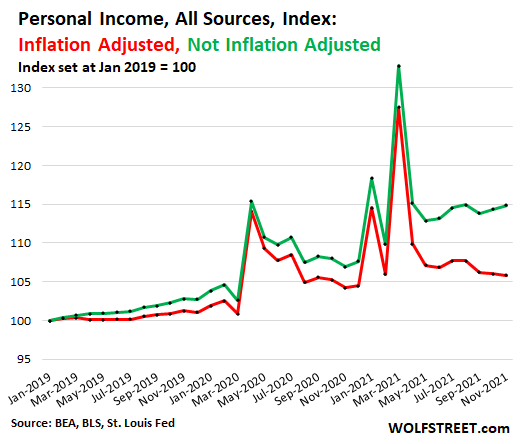

The personal income of Americans from all sources – from wages, salaries, interest, dividends, rental income, unemployment compensation, stimulus checks, Social Security benefits, etc. – jumped by 0.4% in November from October, by 7.4% from a year ago, and by 11.7% from two years ago, according to the Bureau of Economic Analysis today.

This surely makes Americans feel good. But these feel-good aspects of inflation curdle when confronted with new prices.

Adjusted for the worst inflation in 40 years, consumers’ personal income from all sources declined by 0.2% in November, the fourth month in a row of month-to-month declines, as Americans were unable to outrun this rampant inflation.

Compared to a year ago, this “real” income from all sources was up by only 1.6%, and compared to two years ago, it was up 4.5%. That includes all the income from other sources, including government transfer payments. In a moment, we’re going to strip those out.

Here’s income from all sources: not-adjusted for inflation (green line) and adjusted for inflation (red line). I set the starting point of the two indices at January 2019 with a value of 100. Note the yawning gap between income before inflation and income after inflation. That gap is going to get a lot bigger as we peel the onion.

The grotesque gyrations of personal income last year and earlier this year are a result of the various stimulus payments and special unemployment benefits. Most of these pandemic-specials have now expired:

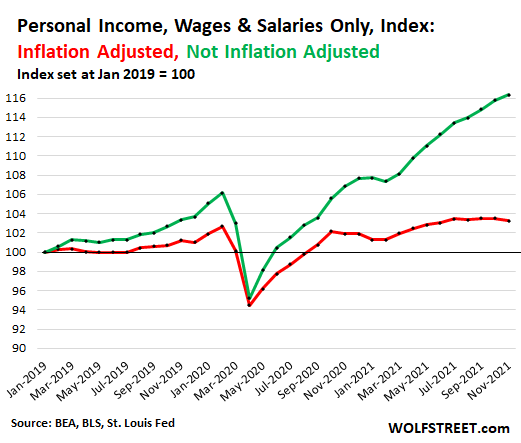

But wait… just salaries and wages.

American worker bees have received the largest pay increases in many years, finally, thank you hallelujah. In some industries, these increases were well over 10% on average. In others, not so much. The pay increases came about as companies are struggling to hire people, while people have decided for whatever reason that they don’t want to be hired under the current conditions – leaving a record 11 million job openings unfilled.

Compensation from wages and salaries in November rose by 0.5% for the month, by 8.9% year-over-year, and by 12.5% from two years ago. And that would be something to celebrate, thank you, hallelujah. But then came inflation.

Adjusted for the worst inflation in 40 years, total compensation fell by 0.2% for the month, has been roughly flat since June, was up only 1.4% from a year ago, and was up just 2.0% from two years ago.

Note the sharply widening gap between income not-adjusted for inflation (green line) and income adjusted for inflation (red line):

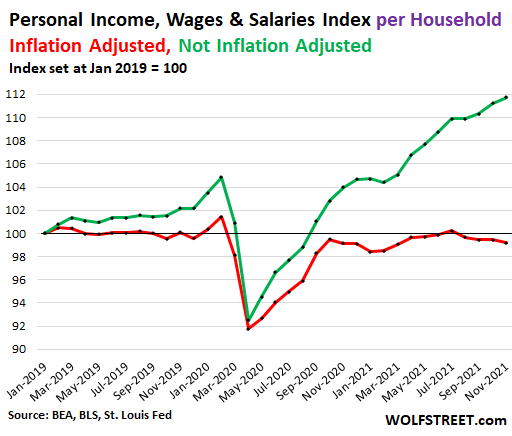

But wait… per household.

The above income indices reflect income for all workers combined. It amounts to nearly $1 trillion per month in actual salaries and wages. But the number of households is growing in the US, and so on a per-household basis, that income pie gets cut into more slices.

Not adjusted for inflation, income from wages and salaries in November on a per-household basis ticked up 0.1% for the month, and rose by 7.2% year-over-year, and by 8.7% from two years ago.

Adjusted for the worst inflation in 40 years, income from wages and salaries on a per-household basis fell by 0.6% for the month, fell by 0.2% year-over-year, and fell by 1.4% from two years ago.

In other words, inflation whittled down the purchasing power of labor; and the rising number of households feeding on this inflation-diminished income pie then whittled down the size of the average slice to where it is now below where it was two years ago, and it’s below where it was nearly three years ago.

This is the effect of inflation and population growth combined on aggregate economic data: It looks great before inflation is taken into account; it looks less great after inflation; and it looks a lot less benign on a per household basis.

But the per-household-basis – not the aggregate economic data – is what Americans are feeling and struggling with every day, and inflation is whacking those households.

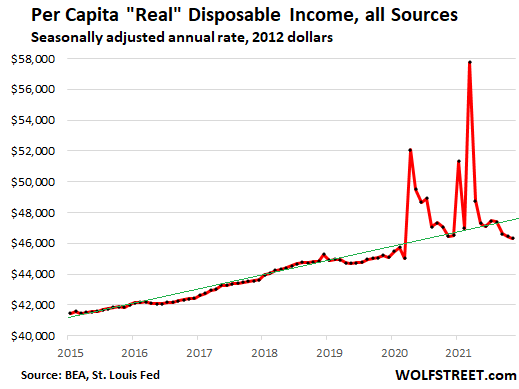

The income to be “disposed” of.

This phenomenon of inflation and population growth whittling down the individual slice of the pie during inflationary times is also showing up in the broad measure of per-capita “real” disposable income, which tracks income from all sources, including government transfer payments and income from interest and dividends, then subtracts out income-related tax payments, adjusts the remainder for inflation, and then divides what’s left by the US population.

In November, the per capita “real” disposable income from all sources dropped 0.2% for the month, was down 0.2% year-over-year, and was up only 2.5% from two years ago, having now solidly dropped below the pre-pandemic trend, thanks to the miracles of inflation:

Disposable income is what consumers can spend on goods and services, such as cars and housing and food, or they can buy stocks and other investments with it. With the worst inflation in 40 years eating up income gains, plus some, consumers have less money to spend in real terms.

But in reality, consumers can borrow to buy what they want: auto loans, credit card loans, levering up the stock market portfolio and crypto wallet, cash-out refis, etc… the opportunities to spend borrowed money to pump up GDP are endless.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

am i the only one giddy with excitement for when this collapses?

The end of the mania will ultimately have significant negative social consequences, impacting both politics and economics.

I’m fed up with it too but it’s not like asset prices will crash and everything else mostly remains unaffected.

I’m ‘negotiating’ with professional right now – got bad price on welding and good one on concrete

OK with it since my BIDEN STIMI $$ are paying excess

I’m saving in other ways which I CANNOT MENTION due to local govt rules

it’s either deductible or income making – otherwise I DON’T WANT IT

Yeah, anyone who thinks the “recession” from the mother of all crashes will only be a few quarters in duration is sadly mistaken. It’s more like life will never be the same again. Look how long it has taken to recover from the GFC. 13 years now. Hmm, 13. Lucky for some.

Agree 100%, Fat Chewer. (Good handle, BTW.)

The “moral hazard” option was just too good for even the mildly greedy to have any second thoughts AT ALL about “being ‘bad’ businessmen”, and they all jumped gleefully into “sin” with everything including the kitchen sink.

Everything since is just damage control, fighting fires, or whatever you care to call it. We have extreme wealth inequality, and other general Econ insanities…(WTF’s being the local term).

No jail for anyone except maybe some patsies hand slapped, and Madoff, who turned himself in. No mass suicides like the Great Depression, either, except for one European noble who unknowingly was feeding friends to Madoff.

How can we “recover” from something in the future, following an incident that we still can’t “recover” from?

Btw, the press doesn’t follow these “patsies”. Just like after a big robbery, they lay low till it’s out of the news and the cop’s and public’s minds.

I bet some follow up would show them living in Caribbean villas with a fat offshore bank account….for taking the fall for the higher ups who make the decisions.

As if Incorporating didn’t offer enough excessive legal protections for societal and legal wrong doing already!

Me too. We’re totally going to come out unscathed.

I know what you mean, but I’m not excited about any of this. I find it sickening, to be honest. It all could have been avoided if the Obama admin would have sent those Wall St. fraudsters to prison, and CONgress would never have bailed out any banks, instead letting them all fail and handing their assets over to the smaller, prudent banks who got railroaded. And finally, no QE. This country would be in beautiful shape right now. Instead, here we are.

Depth Charge,

You are absolutely correct. Unfortunately, ever since the (il*@*!) creation of the Fed and especially their …. interference in the economy in the 1930s, the “free market” has ceased to exist….and as of 13 months ago so too…..

OMG this is too funny. The Fed did NOTHING to counter the Depression, causing the Pres at the time I believe Harding to describe it as ‘a weak reed’ in a time of trouble.

It CAN be faulted for lowering rates slightly before the Crash, in response to plea from the British and French who were struggling with war debt and also seeing their gold draining to NY.

All accounts of life in the Depression emphasize the disappearance of money, even small change. It was something like a car motor with all parts able to work but with no liquid lubricant, so it seized up. By 34 almost ten thousand US banks had failed. There was no deposit insurance, and no help from the Fed.

The story of the Fed in the Depression is one of inaction.

Nick Kelly,

There are lot of red herrings out there these days for sure for sure, especially about the Great Depression.

The problem in the Great Depression was the total absence of government support programs, such as unemployment benefits and social security. When people got laid off, they had nothing, and stopped paying rent and mortgages, and stopped spending money, and then some landlords and banks failed, and some shops failed, putting more people of out work, and all these consumers that were laid off had lost all their income, and they stopped spending, which caused more shops and banks and companies to fail, which caused more layoffs, and more consumers lost their income and had nothing to spend, and the whole thing began cascading and feeding on itself. That’s how a recession became the Great Depression.

Government support payments, such as we’ve had for decades, but didn’t have during the Great Depression, prevent a recession from cascading and feeding on itself to become a great depression. In addition, the government can fund and pull forward infrastructure projects (highways, bridges, tunnels, rail projects, etc.) that create lots of well-paid jobs in engineering, equipment and materials manufacturing, construction, etc., plus all the secondary jobs that come with it, such as little restaurants that make sandwiches for the workers, etc. These projects keep the money flowing and provide future benefits.

But the Fed needs to stay out of this. This is the government’s role.

Nick, you know that the FED is the eternal whipping post for people. The gang that couldn’t shoot straight. No one has a better plan except to say, “free the markets”, “let them do as they please” – the markets; the oligarchs. But the bank panics in the late 19th and early 20th century, where all bank deposits were lost, is either forgotten about or people are completely ignorant of. Yep, the FED makes mistakes, and is ALWAYS walking on a tightrope, but it doesn’t compare to the absence of an activist Federal Reserve at the outset of the Depression. Easy for cranks to throw sh*t at them; but no real solution except to slam the FED and the gummnt.

@ HowNow

A central bank is an essential component of any modern economy being responsible for monetary policy, whereas the Treasury is responsible for ‘fiscal’ ie taxation policy. They need to work together for success.

Years of fiscal laxness, ie too much spending for the tax raised put pressure on monetary policy, ie higher interest rates.

Unfortunately the Fed was also too lax for years and QE-ed away it’s problems by printing money.

The question to ask is, how would the US electorate have reacted to correct fiscal and monetary policies for the last 50yrs. UK is way ahead of you guys down this one way slope. Nobody votes for taxes to equal spending unless it’s somebody else’s taxes paying for spending that suits them.

HowNow,

I don’t think anybody will argue against the Fed expanding liquidity DURING A MONETARY CRISIS, but where was the crisis from 2011 through 2020 when the Fed was expanding its balance sheet by trillions. Where is the crisis now, when the Fed is still buying MBS while housing price is going up 15% per year and employment is less than 5%?

The Federal Reserve has expanded and abused its authority, plain and simple, to the extreme detriment of younger generations and the bottom 95%.

Agree about social programs, but what caused a sudden need for them when a few years before they hadn’t been needed anywhere near as much.

Banks went under? About 10,000 went under. The Fed’s or any CB’s key job is preventing a banking crisis. Once the usual remedies of mergers etc., have been exhausted this requires an injection of liquidity.

I think the people of that era could have toughed the crash for a year or so. But then the financial system collapsed.

Re: social programs. Where would the money come from? Not the Fed in this scenario. As the crash deepened, both parties agreed the best thing was a balanced budget, so govt spending was cut, and the downturn deepened. Tax revenue collapsed.

In this environment to call for basic social programs is to call for govt to inject liquidity.

And it would have been easy. The US wasn’t mortgaged to the hilt like today. It also had so much gold and silver it could have issued significant amounts of gold backed notes, without the mere backing of the country itself.

Economists are notoriously diverse in their opinions, but I have never heard of one saying the Fed did too much in the 30’s.

Nick-perhaps a minor point, but Harding (whose Admin. certainly ranks among the top-ten most-corrupt Presidencies in U.S. history) was dead long before the ’29 crash (not familiar with the ‘weak reed’ comment, he may have made it rather than Herbert Hoover, who was Pres. in ’29 and reaped the whirlwind sown during Harding’s and the subsequent Coolidge Admin.’s).

may we all find a better day.

Ta first Cav Aus, ya it was Hoover

‘In January 1933 the three-year banking crisis brought on by Federal Reserve mismanagement of the money supply entered its final phase. This time the Federal Reserve System itself panicked. Banks were failing because they could not meet frightened depositors’ demands for cash. Statewide bank holidays spread. By March 1933 bank holidays (during which banks were not required to meet their obligations to depositors) had been declared in about half of the states. The Fed responded to these events by again raising the discount rate, making it harder for banks to meet the cash demands of depositors. From January to March the money supply fell dramatically. On March 4 the Federal Reserve Banks themselves closed. Examining this gross negligence 30 years later, Friedman and Schwartz concluded: “The central banking system, set up primarily to render impossible the restriction of payments by commercial banks, itself joined the commercial banks in a more widespread, complete and economically disturbing restriction of payments than had ever been experienced in the history of the country. One can certainly sympathize with President Hoover’s comment about that episode: ‘I concluded the Reserve Board was indeed a weak reed for a nation to lean on in time of trouble.’”

Source: Hoover Institute

For brevity I’ve skipped over this piece’s account of the previous three years in which the Fed relentlessly tightened, until the reserve banks themselves closed. Deprived of a means of exchange, the economy ground to a halt.

Wolf,

“……………………………….This is the government’s role”

ABSOLUTELY!

https://en.wikipedia.org/wiki/Taxation_in_the_United_States#/media/File:Taxes_revenue_by_source_chart_history.png

“other taxes” I assume would include dynastic wealth “estate taxes”…or “the death tax”, per those that would have to pay them.

Let’s just even things up a bit, and downsize ALL….and try for maximum energy efficiency.

D C,

Were you really surprised by President Obama’s picks for both of his Attorney Generals to lead the Department of Justice? That is why no one on Wall Street was indicted for their egregious actions.

Were you really surprised at who and where his Secretary of Treasury came from? Hint: he was President & CEO of the Federal Reserve Bank of New York. The second A.G. had served on the Board for three years under him.

The man President Obama appointed to be Deputy Secretary of the Department of Treasury was Counsel to President Clinton, and he rewrote the Gramm-Leach-Bliley-Act for Clinton after the President vetoed it initially in May 1999. Plus, the repeal of Glass-Steagall was a bi-partisan affair.

The current President served under Obama for eight years. Do you expect anything to change in the next three years under his administration?

I agree with you 100% that the USA could/should be in better shape now had a prudent response to the 2008 meltdown (much of it caused by the GLB-Act) been undertaken by Obama. Wolf is doing a great job trying to influence the officers on deck to steer the ship to calmer waters. And thank you Wolf for telling it like it is!

On the topic of inflation: my grocery bill, of which fresh fruits and veggies are the most costly portion, has shot up quite a lot in the past six months. Not a problem for me, but it certainly is for many in this nation.

The economy was already distorted enough in 2008, not even close to normal.

The “solution” to “normalize” then and now is an economic depression to clear the excess debt and unproductive parts of the economy (covering millions of jobs), back to the 1930’s. This is what everyone is trying to avoid under the delusion that there is something for nothing.

It’s a lot worse now but wasn’t even close to normal then either.

The country (and western culture generally) is in long term decline and the root cause isn’t central bank “printing”. The “printing” is a symptom of the general decay in society, a band-aid,

“ The economy was already distorted enough in 2008, not even close to normal.”

AF,

Might even go back another 10 years when everybody and their brother became day traders…

The solution is to end the rule of plutocratic kleptocracy.

Like this will EVER happen.

Yeah, it’ll be a huge party.

I hope we don’t sprain our arms patting ourselves on the back.

I shouldn’t be wishing for a collapse. I know that, but part of me does.

I’ve lived below my means and saved, foolishly thinking that was the right thing to do. Instead, a central bank has tried to force me into gambling my savings in risky investments by removing any reward for saving (interest). Many commenters here would deride me for not playing that game and staying in cash. Buy stocks! Buy real estate! Buy gold! Buy crypto! Buy farts in a jar! (see the New York Post). Perhaps I am stupid, because inflation is eating away at that savings, but my instinct will not let me gamble with it on things that are overvalued or niche.

I’m a bit angry about what’s happened. I remember in the 1990s when I had a pittance to my name and yet got a decent savings at the bank. Now I am debt free and have a bit more but get an insult when the monthly statement arrives. I know I should be a better person but if it crashes down, I will get some pleasure in watching the easy, phantom gains evaporate.

Disclaimer: the above was typed after two very large glasses of wine. And I mean large. A kitten could sleep in one of these glasses.

Merry Christmas to all of Wolf Street.

HQ – You’re not alone. Many of us have done and are doing just that…save, work hard, and manage risk.

for me, it’s less about that, as I have enough in stocks to make up for the ridiculous losses in cash. this response is really for everyone above, not just you.

i know i won’t come out unscathed from a collapse, i know it will have negative consequences, and i know it’ll not be a party. but i want the collapse to happen now before it’s my sons’ problem to clean up.

i also will get schadenfreude by a return to a society where people with skills, who are handy and self sufficient, are once again rewarded. right now those types of middle americans are endlessly derided and mocked by society and the media. i look forward to a collapse that means that parasitic bankers have to rely on these people, as the “professionals” usually can’t figure out a screwdriver.

Yes exactly Jake. I can’t say I’m happy about what is coming but I think it is necessary. My financial “powder” is dry for that time.

I just wonder if the Fed has the expertise to engineer a “soft landing.” Doubtful. The economy now reminds me of an addict who always has to have one… more… fix. And then just one more…..

To the above post, no they can’t “manage the economy” to create a “soft landing”.

One of the biggest lies in finance and economics is that central bankers magically gain some profound insight after assuming their positions.

Also, that central banks have access to some deus ex machina to magically create prosperity. It’s ridiculous yet that’s the predominant unspoken belief today.

The only actual power central banks have is mismanaging the currency. Some central banks just have joint custody (with fiscal policy) where it takes longer to impoverish the citizenry and currency holders through their foolish and counterproductive policies.

There is never something for nothing, no matter how many believe otherwise.

You’re not the only one. I feel that people on the lower rungs have already experienced a decline. A crash would return assets back to basics. If we don’t have one then housing will be out of reach for more and more. Both buying a home and renting one.

I do think that a crash in China’s economy would have to come first though. Because most of our politicians seem to be too invested in global RE to ever enact anything protect our housing stock or protect our citizens from global money parking.

@HQ

Whisky sharpens the pen better than wine!

Merry Christmas

True that old one, but it’s whisky whisky whiskey that makes you feel risky,,, and wine wine wine that makes you feel fine!!!

MERRY CHRISTMAS ( from a 50% er )

You might get your wish faster than expected. There are reports that duplicate banknotes were printed by “legitimate,” corrupt, CCP authorities with the same banknote serial numbers, so it was impossible to detect the duplicates. After laughing for about ten minutes, I realized that, since the CCP’s schemes are as original as photocopies of a photocopy, maybe this was first being done by the CCP’s bestest, best buds, US banksters? It would explain a lot.

North Korea, China and Peru are known for counterfeiting US dollars. And shipping it here.

The last demise of a large political and economic entity may have been the breakup of the Soviet Union. At the central parts, Russia there was hard times social and economic. Still it was reasonable “civilized”. Other places the red army liquidated their assets before they left and the armed fight between different groups started.

The FED is not all and everything in the USA, USA is not the Soviet Union, but be careful about you wish for. You can be in for more excitement than wanted.

The majority of jobs in red state America are government jobs. People in government, hate government. It’s all consistent with the goals of a coup, which is to leave the government in place and change the leadership. The oligarchs would take over state assets. You keep your job and the mordida works for you. Since this country is already run by a handful of oligarchs the transition would have been seamless, however the oligarchy in the US has different politics than the autocrats. So Jan 6 failed. The people would be empowered but not in a good way.

“The majority of jobs in red state America are government jobs.”

do you have a source for that? because it sounds like complete and utter bs.

You better hope the oligarchs do not start some infighting then. And that no one else try to use the opportunity for a power grab.

Geographic power centres are part of it too. The oligarchs may not unite, resulting in states breaking of.

Jake,

http// Senate Pork.org

I have a 500 page book by Catherine Belton, 2020, describing in detail what happened after the USSR broke up: the KGB took over with the head of the KGB, Putin, becoming President. This resembled an African style take- over in which they seized the assets of the state. The Bolsheviks had to seize assets from private parties, it was easier for the KGB because the state already owned them and the KGB had become the state.

It did not happen all at once and there were factions. The Putin faction first made its move on an oil shipping terminal. Others went after the oil wells, nickel and aluminum, etc. Enter ‘Aluminum Wars’ to read about a hostile ‘take over’ strewn with bodies. Around this time Putin sent his daughters to Germany.

The victors in each field are the oligarchs with Putin as Capo. He sorts out squabbles and turf claims and winners kick up. The lead members are incredibly wealthy and compete with Persian Gulf princes for London real estate in Knightsbridge. Mayfair, Belgravia. This from a country ranking GDP per capita number 57, far behind Argentina and just edged out by Romania.

Credit Suisse says Russian inequality belongs in a class of one.

Five of the oligarchs are suing Belton and publisher in UK courts.

They must believe the British courts aren’t like their own.

Forgot to include title: ‘Putin’s People’ by C Belton

Sams-your ending paragraph, regrettably, will likely be rejoindered in the wake by the execrable: “…who knew?…” amongst those who gleefully joined in a carnival of popular mayhem…

may we all find a better day.

“carnival of popular mayhem”……VERY good description 91B20…..the very first look on the face of the lady when she got shot must have been one of total bewilderment.

But I did notice one of the leaders smash a window with a chair and then scurry away to do something else, while others went through it…hope they ID, get him, and lock him up for a LONG time.

I also wonder if the Capitol cops who shot themselves posed with rioters for selfies….it appears some did.

Speaking badly about the dead is one of the social norms that almost completely vanished in me after Vietnam….you don’t seem quite as bitter, or maybe you just don’t show it.

Don’t worry, after the fed said they would taper, they again increased their balance 120 billion the past 2 weeks. 33 billion just this week. Inflation will continue to run wild

these people are deranged.

Jake W,

What Jon doesn’t know is that this is the holiday period. Bond markets are closed on two of the next six trading days. The Fed isn’t going to buy much over the next two weeks because there is no volume, and Wall Street is kind of semi-shut-down. But bonds are going to mature over the next two weeks, and so the Fed always does the concentrated buying before the holidays and then it slows, and stuff comes off the balance sheet. And it’s afterwards that you have to look at it.

Actually I do know that, thanks for assuming though. And your comment does nothing to refute my claim. They purchased what I said, if the balance sheet shrinks or they don’t purchase more in the near future is something we obviously don’t know.

It shrank at the end of November. And you didn’t get upset about it then.

Disaster and The Death of Bonds stalking the figgy pudding Wolf?

Merry Christmas :)

i guess we’ll see. the market seems to think that the end of qe will lead to a drop, maybe even a modest one, and powell will come back out and say that the fed is committed to supporting markets and restarting qe.

if that happens, they’ll all be vindicated.

The ‘magic’ of reverse repos, nobody sees it, except when you chart it. I didn’t even know they existed.

They aren’t deranged. They just don’t want to accept responsibility and admit what they’re doing. They fear the torches and pitchfork crowd. 😲

Longer they leave the larger the crowd

This headline hits home. Tuesday I was given notice that I was receiving a year end raise of 5%. Officially inflation is 6.8 to 7.2%? I’m not complaining, I still save around 35% of my salary every month so I consider myself one of the lucky ones. The true bottom line for me is how much I’m saving each month after the vultures have feasted on my carcass. Soon the house will be paid off and I might still have enough life left to gather a meaningful nest egg while avoiding the gambling casinos. We’ll see, I know these entitled scumbags are coming at me with everything they got.

@GS

Income 20shillings, expenditure 19shillings and sixpence result bliss.

Income 20 shillings expenditure 20shillings and sixpence result misery.

Mr Micawber C Dickens.

The Scottish whisky edition.

Right. They’re absolute maniacs for what they’re doing. There is ZERO justification for all this QE they are going to continue to pump for another 3 months, and Powell isn’t even questioned about it. In the face of soul-crushing inflation for the masses, this guy is going Weimar. These people are deranged.

“Soul crushing inflation?” That’s a bit hyperbolic. By all the charts listed above, in 2 years, there have been net gains in purchasing power (though miniscule). If it continues unabated, there will be something to talk about. At least the Fed and the Administration have admitted inflation is a problem. It’s a start.

According to Wolf’s response to George (below) it also appears the lowest wage earners (unskilled) have done the best during this period of wage inflation. I am glad to hear that.

I beg your pardon. Have you ever talked to a Gen Z person about buying a house, or even renting something decent without having a house full of roomies? Yes, “soul-crushing.” They have lost hope of ever affording shelter.

I do know many Gen Z’ers – my daughter is on the border of that age (renting her own home and doing fine) and my nephews / nieces are all Gen Z. Those not in college, especially those who went into trades (Ages 22 and 24 in welding and plumbing specifically) have their own rented homes and one is now buying. It is anecdotal, but it’s the data I have. The ones in college are sharing space (like I did with 3 roommates in a house in 1986), and are paying high rent for sure. Not soul crushing.

Statistical outliers mean nothing.

I forgot that you are never wrong DC. My bad. ;-)

Wolf’s charts above are statistical. I will go with that.

Mr. Wolf, thanks for the article!

Curious, do you have a breakdown of changes of wage & salaries into low-end (semi-skilled or unskilled) and high end (skilled) categories? My hunch is that real wages of unskilled workers has gone up whereas real wages of skilled workers has gone down. By unskilled workers, I mean “restaurant workers”, “plumbers”, “truck drivers” etc. By skilled workers, I mean “engineers”, “doctors”, “nurses” etc.

There are all kinds of studies and surveys out there about this. Restaurant worker pay has gone up a lot. According to a Pew survey, by 18%. But my wife, who has worked in an office the entire time of the pandemic (no WFH), has not seen an increase because the company is struggling. A software engineer I know got aged out and cannot find a job in his field, cannot even get the attention of anyone, no matter what the labor shortages. So it’s a mixed bag, as always. But some of the largest industries – retail, hospitality, transportation, warehousing, manufacturing, etc. – have seen large wage increases. Many studies have shown that the biggest percent increases were at the lowest levels of incomes. But then there are the Wall Street firms, and they implemented HUGE dollar increases on top of already hefty salaries and bonuses.

Wolf,

Suggest to your software person to remove each and every and any reference to age from their resume.

After obvious ageism rejections, etc., I did that in ’16 when I needed some work to ‘catch up’ the reserves,,, and got full time salaried work with a good company in CA.

Then, based on that work,,, worked remote for the next 3 years until fully caught up.

CA companies want skills, and I did do some homework in early ’16 to update computer skills, and then some OT when first back at work.

Yes, but that trick doesn’t work anymore.

Using LinkedIn. All data is known. A company can purchase supplemental data, such as a credit report, and get everything. All this is done by machines for preliminary vetting. Humans don’t sort through millions of resumes. Algos to that. Algos decide. In the end a human might look at the top 10 resumes that come out. You cannot hide your age anymore.

I was talking to my brother about restaurant workers recently while eating out. He lives in Canada and was telling me about some economist who claimed that people will have to accept higher menu prices so that these people can make a “living wage”.

I believe that some restaurants will be able to do that but not only a low minority. The chains will probably mostly just eliminate their servers altogether. Others will close if they don’t have that option.

Menu prices are already high enough now.

Unless the “free” money becomes semi-permanent, these workers will also have to accept whatever pay they can get, whether they like it or not just as they did before.

Augustus Frost,

I bought my first dinner in Japan the day I arrived in 1996 from a machine outside the door of a ramen restaurant. You chose from the images on the vending machine, paid at the vending machine, and then inside, the chef read the order from a screen above his work station, and fixed the ramen dish. When he was done, he put it on the counter and called out the order. My new Korean roommate took me there and walked me through the procedure. It was a one-man shop, and the roles of cashier and everything that goes with it, including counting the cash at the end of the shift, and reconciling cash and orders, etc., was automated.

This type of technology has been around for decades.

Fast food restaurants could easily switch to it, but then they would not get the opportunity for an up-sale — “would you like fries and a drink with that?” “How about an apple pie?” And that’s where they make their money.

wawa, a gas station chain on the east coast, has had coffee and sandwich orders done by kiosk for many years now. it’s much better also because the chef reading the screen has it allin front of him. there’s no risk of mishearing what someone ordered.

…the old ‘Automat’ of NYC fame, redux…

may we all find a better day.

It is an interesting point.

In the excellent book “When Monry Dies” by Adam Ferguson about 1920s Germany:

The wages of “unskilled” manual labor rose much quicker than skilled labor and did indeed match at some point.

The reason being, in a high inflation world, manual labor can negotiate salary on a daily basis and can move from employer to employer quite easily.

Skilled labor, not so much.

interesting. one difference though is that the delta between unskilled and skilled wasn’t as great then as it is now.

George can u drive a truck in all kinds of weather or unclog a toilet pompous ass every job requires a skill not a college degree

A plumber is not considered unskilled labor. Furthermore, a lot of plumbers are multi-millionaires. They make bank.

for some reason, he is equating “skilled” with “white collar.” it’s ridiculous.

He may have just made a mistake. I don’t seem to recall his name or him ever insulting tradespeople like the commenter “Outside The Box” does routinely.

Flea & Depth Charge –

The only tradesman neighbor my mother-in-law had on the hill in a wealthy peninsula neighborhood where she lived was…her plumber! He used to stop on his way down the hill in the morning to fix her plumbing! Another wealthy tradesman in that little town was the guy who put in the sidewalks, a cement contractor. His name could be seen on all the sidewalks when I lived there. Capable, clever charismatic guys, all of them….besides owning high-end real estate.

Honor Labor.

Sorry did not mean to insult anyone. Every job requires skills. By “skilled” I wanted to mean people with college degrees or white collar jobs. I am not super familiar with economics terminology.

George-mind well those terms ‘book-smart’ and ‘hands-on’ when bandied. Too often they can appear to be no more than either (a.) an aversion to a little dirt, then discounting those who are willing to deal with same, or (b.) an aversion to critically-acquiring knowledge then discounting those who are willing to do so…

may we all find a better day.

Get out of debt.

Live beneath your means.

And Merry Christmas!!!

Useless advice for those who’ve been doing those very things for years.

And to all a good night.

Doing it for years & punished.

We should have taken on a huge amount of debt, bought 20 rentals & been slum lords.

That’s the American dream…

Scrooge McDuck.

Same here….I should have bought 5 houses in 2010 instead of one. Missed that boat, for sure.

And a Happy New Year to you!

Six chapters into Big Like, and I’m hooked. Excellent writing, Wolf. I’m going to internalize those dating tips, haha.

Thanks!

Not sure about the dating tips tho :-]

A gas station near me has kept their price at $4.09/gallon for regular for three months after the price of crude dropped 20%. This inflation has hit people hard. Price gauging is rampant. People are all broke and are spending money they don’t have. All their disposable income is going for necessities while prices are rising on nearly everything. This is stagflation if there ever was such a state. The misery index has surpassed the Carter era by a mile. Inflation 13.6% + unemployment 10% = 23.6%. Carter’s topped out at 20%.

An employee owned hardware store near me has kept the price of propane low and at cost as a benefit to the community. They’ve earned loyalty because of that, and people feel better about buying other things there- even though their prices are higher on other things than some other local places.

This is a rural community and many live off grid and use propane for heat. I was an employee decision.

I = it

Wolf – I have a question. Hope you can help me understand.

I have heard the argument that fed can not raise the interest rate as gov will default/will not be able to pay for the debt. But my understanding is the following about gov debt.

Gov takes on to debt by issuing bonds. These bonds have coupon payment (i.e. similar to interest payment). Let say the gov issued/sold a bond for coupon payment which is for 3%. No matter what the future interest rate will be in the market, this will not effect the coupon payment from the gov. So in essence it is a fixed interest rate payment. If the interest rate in the market increases, it might happen that the any new bonds the gov wants to issue has to be at some what compare rate (may be higher that what it might have be couple of years ago depending on market conditions) but this does not effect the existing coupon payments that gov needs to make on the old bonds.

Am I correct in my understanding? If so, then the theory that interest rate can not rise as gov will default/will not be able to service the debt does not make sense. Yes it might cost the gov more to take on new debt but does not effect old debt.

It does not affect old debt but the old debt has relatively short maturities and MUST be rolled over with higher rates. This is why rates cannot go up.

Concerned guy,

Yes, your understanding is correct. People who say that the government will default if interest rates rise don’t know what they’re talking about. The nature of bonds with long maturities, as you pointed out correctly, is one reason.

There are other reasons. One is that the government can always borrow more to pay more interest. In addition, higher interest rates will increase income tax revenues from fixed-income investors which will pay for some of the higher interest expense. You’re talking about $50 trillion in debt that over the years is increasing in yield and taxable income… Treasury securities, MBS, ABS, savers, corporate bonds, junk bonds, leveraged loans, CMBS, CLOs…. Plus most importantly: yield fixes demand problems. If there is no demand at the current yield, there will be demand at a higher yield. Right now, there is ravenous demand, or else yields wouldn’t be so low.

“Right now, there is ravenous demand, or else yields wouldn’t be so low.”

Ravenous demand, or panic level cover from the Fed “toolbox”? Very different animals…

JeffD,

yes, there’s that. The Fed needs to stop buying and start selling its longest maturities to satisfy some of that ravenous demand at those low yields, and then sell more bonds to satisfy demand at higher yields, etc., until it satisfied demand for 10-year maturities at 5% and then at 6% and then at 7%. Because the 10-year yield should be above the rate of inflation, and then it might be a good deal again for investors — rather than being a products of financial repression.

Ravenous demand? Then how to explain the breathless acrobatics of the ‘Lender of Last Resort’ since 2008?

It IS all about keeping Leviathan propped up, lest its legs would be crushed under its own glutton weight.

Wolf, would you agree that there is a lack of transparency in what the Fed tells us? And by extension would you agree that their balance sheet might well be BS?

Gilbert,

That is nonsense for at least three reasons:

1. All securities on its balance sheet have CUSIP numbers and are tracked and are known who holds them, because interest payments are made to the holder. Just like when I buy a Treasury security, the Treasury Department knows to send me the coupon payment.

2. You cannot hide TRILLIONS of dollars in securities with CUSIP numbers. People who claim that are either ignorant or purposefully bullshitting.

3. People who claim this nonsense also don’t understand HOW the Fed operates: MARKET MANIPULATION.

Meaning pumping up the markets. You cannot pump up the market if you do something secretly. That’s why the Fed makes everything known in advance with great hoopla, in order to create hype, and it’s picked up by all the media and algos, and just saying it caused markets to move in the direction the Fed wants them to move. This is the official policy tool the Fed uses. It’s called “forward guidance” and similar.

For example, the Fed’s corporate bond buying: The Fed made all these announcements in the spring of 2020, and this created a huge amount of euphoria in the bond market and junk bond market and loan market, as investors were trying to front-run the Fed by buying those assets, which created the biggest corporate bond bubble in history.

And then the Fed actually bought next to nothing. It was hyped to buy $720 billion in corporate bonds and junk bonds and bond ETFs, and it eventually bought just $13 billion, not even a rounding error on its $8.8 Trillion balance sheet. And it stopped buying a few months after it started, and now has sold those bonds. But its hype alone – not it’s actual buying, which was minuscule – had the massive impact on the bond market that it wanted to have.

This is market manipulation pure and simple. That’s how the Fed operates. Its primary goal is market manipulation. And its primary tool in that are its announcements and Fed head talk. Doing anything in secret would have no impact.

“Its primary goal is market manipulation. And its primary tool in that are its announcements and Fed head talk.”

Which is why it thinks it can jawbone inflation down without actually raising rates or doing anything in the near term. The hubris.

Talk about towing the line, Wolf! There was a time not long ago that Congress audited the Fed’s books and we found out they had funneled money to various financial institutions around the world. Why is it that this was not shown in their balance sheet? And I for one believe they have more than one balance sheet, one for public consumption and another that is not. Unlike you, Wolf, I experienced the Vietnam War up close and personal and from that experience learned that people and institutions bend the truth so that the masses don’t get too upset.

It was shown on the balance sheet. But the recipients hadn’t been named.

Also these loans and swaps have maturities, say 30 days, and then the recipient pays them off and might get a new loan in the same amount, thereby rolling over the same amount. Some moron out there added up all the loans without subtracting the payoffs, and so the $1 billion loan rolled over 20 times became $20 billion, multiplied across the whole arrangement, which is of course braindead, but it sure as heck got a lot of clicks, and that shit is still circling around. Some sites did the same with repos in late 2019, also creating piles of BS about $15 trillion in secret repos or whatever that weren’t shown on the balance sheet. The amount of BS out there about the Fed is just stunning. These sites will do anything to get clicks.

The FED knows exactly what they are doing.

@MA

What about this one on the jawboning angle?

When JP said it was ‘transitory’ he knew it was going to be ‘hot’, now he’s saying it’s not ‘transitory’ because he knows the heat is out of it and, if wages don’t take off, he’s back to fighting recession again next year.

Just a theory but it’s what they do.

If you think inflation is bad for your paycheck, have you seen what biden wanted to do to your income tax rates…and remember, the IRS was looking at every transacting in/out of your bank account.

slight correction:

“…IRS was looking…” should have been “…IRS would have been…”

Corporate spies are already doing that, and not just your bank account :-]

Interesting claim.

It’ll be interesting to see your evidence on this.

Ohh boy…. Do you think your bank account data is private?

Javert Chip,

Start by reading the privacy disclosures from your bank. Yes, those umpteen pages in all-caps small print. They’re actually disclosing some of it. You just have to read it. That will get you started.

I make $10 billion a year and pay no tax because I’m smart. Now Biden wants me to pay 15%. He’s a socialist.

If you sell a few trinkets on Ebay and get over $600, Biden wants to tax you on that. What’s next, the IRS patrolling garage sales? Selling your used goods is not income. It was a loss. These people are deranged.

Depth Charge,

You always had to pay taxes when you sell stuff and make money on it.

But you pay taxes on income (profit), not on revenues. So if you sell something for $600 and it cost you $400 dollars, you have a gross profit of $200, and that goes into your financial accounting, and then you have some expenses too (shipping, rent, communications, etc.), and a bunch of other deductions, and what is left, if anything, is your taxable income.

It’s OK for the IRS to go after tax cheats, as long as they also go after the big ones.

The threshold for 1099 reporting has been $600 a year for years (which is what eBay will have to do). This is nothing new. That 1099 reported amount goes into your revenues. And then you deduct your expenses. And there are a lot of things you can deduct. And you pay taxes on the small profit, if any.

yes, but the difference is the $600 threshold for 1099 reporting was previously for contractors or vendors. meaning if i provide consulting services for an accounting firm and charge $1,000, they send me a 1099. that’s happened forever.

previously however, people selling things on ebay only got a 1099 if the total yearly sales were over $20,000 and (not or) there were 200 separate transactions. this exempted most hobbyists. now, if you sell $800 worth of crap from your garage before moving, you’ll get a 1099 for $800. sure, your basis is higher, and you can write that on your taxes, but if you ever get audited, the irs agent would likely demand your receipts. who has receipts for their garage crap they bought 20 years before?

i agree with depth. there was no legitimate reason for this change.

PayPal has been sending my corporation (!!) 1099s or years even though it’s a corporation and PayPal doesn’t need to send 1099s. I just don’t get what this furor is about. Sounds to me like someone is trying to rally the troops against big bad Biden. There are plenty real issues you can sock him with.

“if you sell $800 worth of crap from your garage before moving, you’ll get a 1099 for $800. sure, your basis is higher, and you can write that on your taxes, but if you ever get audited, the irs agent would likely demand your receipts. who has receipts for their garage crap they bought 20 years before?”

Exactly, Jake. Who has receipts for any household clothing or items they purchased decades before? Unable to produce them, now the government’s going to shake you down. Because it’s “guilty unless you can prove yourself innocent.” This is a disgusting overreach.

The lies and gaslighting coming out of this administration are some of the worst we have ever seen. They say in public that the wealthy are going to pay, but by their actions we see that they are going after the little guy. They want to spy on every single bank account for transactions above $600 per year. This is a police state they are aiming for.

Depth Charge,

Some basic accounting: You can estimate your costs, no problem. Just be reasonable. Generally, if you sell some stuff you’ve had for a while, your purchase costs are going to be much higher than you what get for this junk. It’s the purchase costs you deduct, not the current value. So you’d show a loss. You’d have to sell stuff that qualifies as antiques to come out ahead (where the selling price is higher than purchase costs). People use your head a little. You are hopelessly flailing around in the dark trying to hit Biden.

depth, the part to remember is that they are basically a criminal party, with a criminal mind. that’s not to say they’re actually violating criminal laws (they can’t, after all, as they are the ones writing and enforcing the law). it’s that they have a criminal mentality, the desire to get away with whatever malfeasance they can get away with, and to lie, cheat, and then reacting with righteous indignation when they are caught.

If you think they are going to start surveiling your bank account then you should stop depositing any checks in your personnal bank account. Go to another bank that you hardly use and cash the checks. It will be much harder to trace. I learned this when I was in a band and got paid in cash but sometimes with checks.

A check is an official transaction. Every check is routed via the Federal Reserve System between the two banks involved, and then the payment is routed the reverse way also via the Federal Reserve System. In the olden days, the paper check was routed that way. Now checks are scanned and the digital check is electronically routed that way. You cannot keep a check secret. If you want to hide a payment, use cash.

“You are hopelessly flailing around in the dark trying to hit…”

False, Wolf. I don’t care who is in charge, I don’t like totalitarianism, which is what this is. It’s none of the government’s damn business if I want to sell some of my used clothing, or a couch, or some old tools, or whatever. This is a gross overstep so they can look into every single financial transaction between two human beings. The fact that people like you think this is fine is SCARY.

I hate to be defending the IRS, but if you get a 1099 from ebay can’t you deduct what the goods originally cost you? Maybe you could even show a loss?

Can you find the receipt for the jacket you bought 7 years ago from Nordstrom?

If you paid by credit card, you’ve got a receipt that you can download from your bank. If you paid cash, estimate it!! But be reasonable. No problem.

And you’re going to show a loss: you bought a jacket for $200. And you sell it on eBay 7 years later for $50, you’ve got a loss of $150. And you’re not going to pay taxes on it, no matter what eBay sends you. People, you’re barking up the wrong tree.

But… Merry Christmas!! Take a few hours off from being rightfully angry.

all this is going to do is drive more commerce underground. i used to sell things on ebay when i no longer wanted them. at the time, the fees were 6% plus 3% for paypal, so a total of 9%. not bad. then they started raising the fees. now they’re anywhere from 12-15%, and since paypal is now 3.5%, it’s now 15.5-18.5%.

oh yeah, and they started charging the fees on the shipping amount, which has gone up dramatically (only the big boys get good rates from the couriers, everyone else has to pay out the wazoo).

oh, and to make matters worse, sales tax now gets on added (never mind you already paid sales tax the first time you bought it), so sale prices are depressed. it’s no longer worth it. now i just sell things locally on craigslist or i give them away. this is going to be especially true with the $600 limit and no 200 transaction minimum.

these idiots in government never learned the maxim that every action has an equal and opposite reaction.

Nailed it, Jake.

I have some Hummel figures my parents bought in the 50’s. Surprise they are worth about what the folks paid for them. Inflation based there should be a huge loss to deduct here. The cost basis should be figured at their DOD so my capitals gains are minimal, but where’s my tax deduction? Everyone is arguing over tax liabilities, when the real issue might be tax credits.

@DC

Don’t want to scare you but the US National debt is unpaid tax owed by citizens to the holders of the paper.

I expect to be off before they come calling for the money here in the UK.

The bottom 50%, not many of whom are to be found here), don’t need charts, nor do they need refereed journals to know that inflation is raging.

Question/comment Wolf,

How much of the food price inflation is a result of the food-delivery phenomenon. My city (Minneapolis) just extended an ordinance capping the fees that these companies (Uber-eats, Doordash, etc) can charge restaurants at 15% of the bill.

Years ago I was talking to someone who owned a restaurant down the street from me and he was saying that some of these services were charging 30%+ of the purchase price.

Restaurants are not high-margin businesses. The logical medium-term outcome from the ubiquity of people using these services would be for restaurants to need to increase prices to offset this huge fee. How much “food price inflation” does this ultimately result in?

I know I’ve seen pretty massive menu price increases over the past year or so even for places that don’t seem to use many/any of these services. But I fail to see how someone taking a 15% fee from every restaurant bill cannot result in higher prices for the end consumer..

Food inflation is split into two big groups: “food at home” (what you buy at the grocery store); and “food away from home” (restaurants, cafeterias, vending machines, etc.). The CPI for food at home was 6.4%; the CPI for food away from home was 5.8%.

You can check out the categories and subcategories by line-time here, including what kind of meat, etc.

https://www.bls.gov/news.release/cpi.t02.htm

We gave massive retention raises over the summer so our employees wouldn’t flee to other employers. The tea leaves have been really easy to read for a while now, and unfortunately continue to be so. I’m going to postpone our regular January raise as long as I can but know I’m in for another set of raises. On a related note, I’ll be sending out notices to all of my residential tenants the first week of January that rents will be going up but not for at least 90 days so they have time to relocate if needed. In all likelihood I’ll be raising them by the max 10% CA allows (regional CPI plus 5%). With everything costing more I talked to my insurance agent and revalued our properties as close to $400 per foot as possible. This all costs more to insure. Taxes are up, insurances are up, maintenance is up, materials are up, everything is up. Now back to wages…I’m going to let them know in that letter that they need to go to their employers and tell them this is what’s happening and ask for more money.

Nothing is good about this, not one thing. At a point in the not too distant future there will be a buyers strike where they will refuse to pay these prices anymore. It’s already happened with some construction customers.

I don’t believe you set your rents based on cost to maintain. You set them on what the market can bear. Rents are up so you help yourself to some of the action. You and all landlords would do that even if all your other costs fell.

exactly, who does this guy think he’s fooling? “Now back to wages…I’m going to let them know in that letter that they need to go to their employers and tell them this is what’s happening and ask for more money.” I’m sure that will go swimmingly. hey boss, my landlord needs a bigger cut so you need to give me a raise.

We’ve kept our rents flat for the last two years and have worked with tenants because of the pandemic. At this point we’re way below market and the CA rent control laws dictate the max we can raise rents. We’ll still be below market all said and done. I’m not trying to fool anyone. We did our part to help and skyrocketing costs mean we can no longer afford to do as much as we’ve been doing. Don’t be so judgmental and unhappy. You have no idea what we’ve done to help and continue to do so. Merry Christmas

What role do traditional banks that were brick and mortar (BofA, Wells Fargo…) play in the 10 year horizon? Was running by a local empty Blockbuster chain and got to thinking about the long term viability of the zombie banks. Haven’t the shadow and pure online players positioned themselves to replace the legacy titans?

Was thinking about the infrastructure and manpower and costs to run these powerful entities and wondered if there is a post B&M banking system waiting to close up shop on these dinosaurs?

This is one of the big questions, isn’t it? That’s what the whole crypto/blockchain/deFi crowd are “banking” on ;)

Who is “Winning” when the world prints unlimited fiat money and destroys the time/labor value of money? I’d suggest nobody as we are living in a “Financial Simulation” clusterfck, one in which the “Idiot Programmers” have at this point pushed past the point of no return, and thus ALL get to deal with the fallout in the very near future.

What is the point of no return in a zero sum game??? What the hell did anyone with an IQ bigger larger than their shoe size think would happen when aggregate money supply increased by $21 trillion since the start of 2020, including U.S., China, euro zone, Japan plus eight other developed economies???

We all know the bottom 90% is getting inflated into oblivion, yet the super rich are not “happy” either as this fantasy simulation isn’t “base” reality to anyone with an ounce of common sense, per Bloomberg:

The biggest U.S. banks are putting finishing touches on their most profitable year ever and preparing to dole out some massive bonuses, yet the usual sounds of Wall Street’s backslapping and toasts have faded.

Industry denizens describe a sense that assignments are unending, trouble is brewing and the real fun is elsewhere.

Veterans of past Wall Street booms suggest that, somehow, this one doesn’t feel so good. One reason: The wealth reeled in by elite traders and dealmakers is getting outshined by the quick riches touted by cryptocurrency fanatics, fintech whizzes and meme stocks. There’s also the gnawing realization that the financial industry is benefiting from the turmoil set off by Covid-19, stimulus efforts and a burst of market ebullience that will inevitably fade.

Do you have a link or reference to what you are quoting?

funny, i talked to some of my buddies who work at bulge bracket banks, and they said similar things. also, when I read the writings of people like druckenmiller and other billionaires, it’s almost as though they think the “elite” have overdone it this time. ultimately, if society collapses around them, their “wealth” evaporates too. i think there’s also this growing sense that the economy isn’t as healthy as the talking heads are saying.

Yeah but these are “Liberal” elitists, and either way they are deeply into philanthropy. If things collapse the privarte social safety net with suffer. The financial economy is much larger than the economy of goods and services, and that may indicate a certain cushion for the real economy. When the Fed opened up the monetary base, the question became, who owns this money? Some of it is fiscal, and Congress can appropriate money on the Feds balance sheet. So which economy do you mean? Despite shortages, there is a lot of overcapacity, and that usually gets resolved during a recession.

Capitalists. Most on here would describe themselves as capitalists, they are not, they are workers. Some might describe themselves as middle class to differentiate themselves from workers, but they are not. If you have to work you are a worker.

Now, redo all that in another article, focusing on median income figures. Since 50% of the population makes less than median income, that’s where the rubber hits the road. PS Don’t bother focusing on average income because Elon Musk alone skewed that number upward by $500 or so annually.

PS I suggest you end that article with, “Merry Xmas, and a Happy New Year”.

PS data for median annual earnings vs median hourly wages are extremely far apart. Median annual for 2019 was about $52K/yr, while doing the same calculation with median hourly wages for 2019 comes out to about $32K/yr. The first number is from BLS while the second number is from “statista research deparment”, which might explain the differnce. I actually think statista is more accurate.

PS (last one!) From Forbes: “Across the country, employees who are paid an hourly wage for their services account for 82.3 million workers 16 years and older, representing well over half (58.1 percent) of all wage and salary workers in 2019”

This helpful article does a good job of revealing the pitfall of believing government stats without appropriate critical thought — i.e., without adding in the “per household” part.

To clarify, does the per household chart include only participants in the job market? If it also includes the 38% of citizens who are not participating in the workforce, then some further analysis about them (retirees, unable to work, minors, etc.) would be useful.

For example, I am retired, so the increase in wages/salary do NOT offset my increases in living cost. Securities value increases help for now, but sub-inflation the interest rates on my interest-bearing investments nearly offsets this benefit.

Focusing just on wages seems to leave out a lot of individuals from the discussion.

The number of households here is the total number of households in the US = 127.4 million households in total.

I thought I read somewhere that the US had the same number of family households today as some time in the mid 1970s, and yet when I do some searches I see historical numbers rising over time.

Does this discrepancy have to do with the definition of household? For instance, the above reference to the family households staying the same since the 1970s may be referring to households with at least one child.

Wolf, then do your numbers refer to simply an address of a house with someone living in it regardless of “family” status?

Does this differentiation make any difference?

“I thought I read somewhere that the US had the same number of family households today as some time in the mid 1970s…”

That’s total BS. In 1975, the US had 71 million households. Today, the US has 127.4 million households.

“In 1975, the US had 71,000 households. Today, the US has 127.4 million households”

71 million I think?

Yes, thanks. Fixed.

Thomas Sowell loves to point out how misleading “household” data is. Is it 5 room mates, all with jobs? A single-income family of 6? A single tech worker in a condo? Two immigrant families? And an increase in households does not mean an increase in population. The approach is definitely flawed.

ChangeMachine, that is sort of the point that I was trying to make. What is a household and how was/is/will it be defined?

Of course the nominal number of households on paper changed. But I’m willing to bet there are fewer families with children, and way more single person households. That may have some sort of effect on the discussion.

Sheesh.

A household is defined as people living at one address. This could be a three-generation household, or a households of six roommates, or a person living solo. This is not rocket science.

From the Census Bureau: “A household includes all the persons who occupy a housing unit as their usual place of residence. … The occupants may be a single family, one person living alone, two or more families living together, or any other group of related or unrelated persons who share living arrangements.”

Household is NOT defined as “family.” Household has to do with what is in the “house” in the old Germanic sense (where this word comes from) of “home” (zuhause = at home).

Family is defined as people who have formed a family unit (couple, kids if any), and their relatives, and they could be living apart in different countries and still be a “family.”

It’s not the number of families that get counted but the number of households.

Interesting.

But how does this look in reverse next year when:

Helicopter money won’t be present

People get back to work even at lower wages

Supply goes up

Demand reverts, due to less disposable and more costly debt

2022 is going to be a delicate year.

Just how can you get demand without keeping interest rates at zero, and bribing the populace with “free” money, and the economic “multiplier” of said direct stimulus is insufficient to even pay for itself?

Yep. We are debt saturated and basically in the pop and drop cycle. Government or Fed stimulates to get pop, but as soon as heroin runs out be revert to politically new and ever lower long term real growth rate of about 1.5% and with population growth and demographics it’s less than 1% per Capita.

At least maybe the majority of people will realize from this major stimulus that command and control economies aren’t the solution for economic well being.

Lacy Hunt (former Dallas Fed guy) was interviewed by Danielle DiMartino Booth recently and he basically said government fiscal stimulus has a negative economic multiplier, with a delay, when debt levels are high.

Personally, I think it’s not purely a matter of debt levels, but of having picked the low-hanging fruit of productive government investment. Things like the interstate system and electrical grid have obvious benefits, but most government outlays are dubious at best. It gets harder and harder to productively spend each marginal dollar.

i don’t know where the line is, but i know that giving out trillions so that people can buy amazon crap, flat screen tvs, boats, luxury handbags, cars, and nfts of people’s farts is on the wrong side of that productive investment line.

One possibility is demand decreases but supply decreases even more. Think of all the young folks who are still living at home, choosing not to work, spending the day on their smartphones and all they have to spend money on is uber eats. Fewer people working at the restaurant, working at the meat processor, working in construction. Prices can keep going up.

The economy becomes bifurcated.

Rich earning and spending lots, the majority spending and earning very little.

A stock market doing the same thing, mega caps leading the indexes higher, while the rest are falling in real terms.

That itself is also ultimately unsustainable and just leads into a reversion to the mean, driven by human emotions.

Moral hazard has been encouraged to the point no one sees risk… everyone thinks bear markets are no longer, because CB stimulus.

That is exactly why it will occur.

The panic that will set in with any kind of volatile spike with all this leverage, will be enough now… greed and fear magnified the other way in equal and opposite reaction to the ignorance of risk.

“The economy becomes bifurcated…Rich earning and spending lots, the majority spending and earning very little.”

This is partly responsible for the massive increase in the median prices of houses and cars – it’s the mix. The wealthy buy the more expensive models, so the median is skewed higher.

That’s why median price is not always the best indicator of where a market is at, and why Case/Shiller was more accurate by comparing the sales of the exact same houses over time.

In some of these housing markets, prices are not up as much as the median suggests. It’s a mix problem. We’re probably going to see some wild swings in prices in the future.

Next year in reverse when:

No helicopter money to the man in the street but still grand handouts to those that have a lot.

People do not back to work, they go to the “informal” economy.

Supply do not go up. The constraints happen to be shortage of cheap energy and cheap commodities.

Demand reverts, but not prices.

2022 may be become interesting.

1) Per Capita “Real” Disposabe Income reverted to the mean, to the trend

line. The downdraft below the mean will cont because the negative momentum is great.

2) Inversion : “Real” income and NDX.

3) Fearmongering left 11 million jobs unfilled.

4) Our adversaries pay attention to American response to

fearmengering in MN. They accumulate data. So far, so good. They can cont to put a threat on us.

5) Income from wages amount to $1T/ month, but consumer

spending is about 70% of a $22T GDP. The rest is gov entitlements, black market and debt.

Michael Engel,

Your #5 is nonsense:

Total personal income = $21 trillion a year, by category:

— Total Compensation and Wages = $12.9 trillion a year, of which $10.6 trillion (“nearly $1 trillion a month) is salaries and wages only (the number I discussed).

— Proprietor’s income = $1.8 trillion a year

— Rental income = $750 billion a year

— Income from dividends and interest = $3 trillion a year

— Government transfer payments, such as SS = $3.9 trillion a year

— MINUS: contribution to government social insurance programs: -$1.6 trillion a year

5) consumer spending is about 70% of a $22T GDP. The rest is… That’s not nonsense.

6) Do I have a target on my back ?

Business consumption plus government consumption plus investment are the rest of GDP.

People have jobs now. Part of reality is, one’s rewards will fluctuate. The Fed among other things has pursued policies that spread employment to people who, in a truly free market world, would be starving and robbing you on the streets. There are lots of trade-offs, but so many commenters here implicitly think the world should be set up by some unidentified force to favor their own demographic. This is infantile, but dressed up and disguised in aging-white-guy outrage, an addiction of its own. There is a lot to be thankful for this holiday, depending on one’s baseline. But ranting (and finger-pointing at some too-obvious targets) are, based on some here, obviously in fashion. Things could be SO much worse. Meanwhile I’m doing my best and it is working OK in this environment. In the long run, we are all dead.

that’s complete nonsense. there’s no evidence whatsoever that mass printing and keeping rates at 0% does anything for employment.

if anything, it hurts employment long term, as the massive debt load and inflation puts many company’s products/services out of reach.

It only benefits the people with nothing because they already have nothing so they can’t lose more.

Despite what is being said the Fed truly do not seem too worried or too rushed at the moment.

Inflation is going to each away their debt fuelled binge as long as they can delay and jawbone minimum Interest Rate rises

except it won’t. because the debt will grow far faster than it can be inflated away. history has shown this time and time again.

if you have a bathtub you’re trying to drain, you can’t have the spigot dumping in 3 gallons a minute while you’re using a bucket to drain 2 gallons a minute.

Thanks Jake W

It looks like we will soon see

Maybe the Fed is trying to inflate away the debt as Marco suggests, but congress is foiling their plan by treating low interest rates as a blank check. Or maybe the congress is simply spendthrift and the Fed is trying to mop it up and make the best of a bad situation.

Chicken or the egg?

could be, but at this point, with troll faced janet yellen (thanks depth charge for that one) saying to “go big” because interest rates are low, it should be clear to the fed that congress will indeed treat low interest rates as a blank check.

it’d be like a parent paying their spendthrift’s kid credit card bill “just this once.” only an idiot wouldn’t realize that that would cause the kid to run the bill up again.

With my home title clear, and my business producing well, I am in an enviable position to ride this out. But that is perhaps the problem!

Those of us who are in “enviable positions” may find ourselves unable to continue in this present form in the years to come either due to our own compassionate natures when we see the suffering around us. Or due to predations of those not so well prepared.

Also, at the point of collapse, it will not matter much whose fault it all is; all that will matter is where are the resources and how can we get to them.

But yeah, MC and many happy returns! Enjoy the articles and the comments!

Property taxes just increased 10% got notice on Christmas Eve crappy present

JP printing raise Xmas temp to the highest on record.

Wolf should be required reading for all profligate legislators. You increase real wages through productivity, by putting savings back to work, or through Net Domestic Investment/GDP (which has been in the decline over the last 40 years – peaking at 1.4 in 1950 and falling to .04 in 2021).

could you run all the numbers and take out the top 10% I think it would be totally different picture Thanks for educating a lot of people….me included

This “wages and salaries.” The billionaire class is less presented in this category. Not many of them made their money off ‘wages and salaries” but through capital.

“You see, in this world, there are two kinds of people, my friend: those who’s money works for them, and those who work for their money. You work.”

Maybe it’s just the eggnog talking, but the title of this article makes me think of “Grandma Got Run Over by a Reindeer”. How about a new song….. The plebs got run over by the Fed Reserve, every year since nineteen thirteen…….. ok that’s all….

It reminded me of Britney Spears’ “Oops, I did it again,” except the FED version: “Oops, I did it again, I stole your money…”

people say that a lot, that it goes back to 1913, but the real problems are really only a little over a decade old.

@JH

You want, “We are the 99%” Amazon Xmas no1

Check it out, UK but says it for all!

It must really be bad up in Canada where 2 percent seems to be the maximum yearly pay increase and no one got stimulus money that didn’t need it unlike in America. I’ve been out at the malls and no one bought anything on the black Friday sales and no one is buying anything this Christmas season. Trudeau’s comments about interest rates sank the Canadian dollar putting more upward pressure on inflation. Canada will wither under stagflation.

1) There was a 350 pounds lineman in NYC subway. He put his

foot on a tiny Chines guy.

Instead of moving to another seat, the tiny Chinese jumped on his feet, pressed his balls on the lineman femur, forming a V shape between the guerrilla knee and hip and ==> twisted his ankle into submission.

2) USD/CNY two legs, between Mar 26 2018 and Dec 6 2021 forced

USD into submission.

3) The USD/CNY middle, between the two legs, on [B], retraced to 0.37.

4) There will be a reaction. USD will wrap a BAT on CNY and force the People Bank Of China into submission.

5) TY weekly, US10Y futures price, is going crazy. Totally unstable and volatile.

6) TY formed a Schabacker Megaghone and that’s bad news for China..

Since we have many comments including politics, ‘Obama screwed up’ etc. here is one involving the investment of hundreds of millions in the present.

Remember all the Presidential rants about ‘CHIIINAA’?

Apparently the author is capable of holding his nose if the money is right.

Via ‘The Street’

‘The Shanghai-based company has been under investigation for misrepresenting shell companies with no products and few employees as growth companies, the Washington Post reported Thursday.

Arc Capital has repeatedly helped create or finance companies with little or no revenue or customers and listed office locations that are actually P.O. boxes, according to the Post’s review of documents tied to the investigations.

Earlier this year, Arc helped create Digital World Acquisition, an investment company that has raised over $1.2 billion to conduct a merger with Trump Media and Technology Group’

A shell merging with a shell, raising money for the mission, or just for the money?

Will you people ever get over your derangement?

It’s good when the God-Emperor does it!

“God-Emperor?”

Depth Charge; “God-Emperor?”

That’s Trump’s nickname given by his supporters on 4Chan and “the Donald” on Reddit. Came along at the same time the autistic sub channel’s frog and his REEEE noise was co-opted to represent them.