No one knows total stock market leverage, but it’s huge and ballooning, as we see from the tidbits we’re allowed to see.

By Wolf Richter for WOLF STREET.

No one knows how much total leverage there is in the stock market. Only fragments are reported. Margin loans are reported monthly, and they provide a general idea of the trend in stock market leverage. Some types of leverage are not disclosed at all until something implodes spectacularly, such as Archegos. Other types of leverage are reported in bits and pieces, if at all, by a few banks and broker-dealers in their quarterly financial statements, if they so choose. This includes “securities-based lending.”

Some banks & brokers report securities-based lending, others don’t.

On Thursday and today, some Wall Street banks and broker filed their Q3 earnings reports and supplemental information with the SEC, and a few of them included in their supplemental filings some tidbits about their securities-based lending (SBL).

Securities-based lending is hot; people who want to cash out some of the gains in their portfolios – thank you halleluiah, Fed – but didn’t want to sell, can use their portfolios as collateral for loans by the broker, the proceeds of which can be used for anything – buy more securities, buy a house or a new vehicle, or pay for a divorce settlement.

When asset prices fall enough, the borrowers get a margin call and either have to either come up with some cash and put it into the account, or they have to sell securities and pay down their SBL balances, thereby turning into forced sellers.

Goldman Sachs didn’t disclose anything about its SBL; they’re lumped into a larger loan category.

JPMorgan didn’t disclose the amounts either but only said that in its Asset & Wealth Management division, “loans continue to be strong, up 20% primarily driven by securities-based lending.”

Bank of America disclosed its securities-based lending in a footnote: SBL balances in Q3 jumped by 25% year-over-year to $49 billion.

Morgan Stanley also disclosed its SBL balances, in the category “Securities-based lending and other,” spread over two divisions, which combined jumped 23% year-over-year to $89 billion.

Charles Schwab didn’t separate out its SBL balances, but lumps them into the category of “Receivables from brokerage clients,” which nearly quadrupled year-over-year to $81 billion.

But Wells Fargo reported that “other consumer loans,” which are primarily SBLs, declined by 18% in Q3 to $27 billion. The decline might be a side effect of the sale of its asset management business to private-equity firms GTCR and Reverence Capital Partners, announced in February this year.

No one tracks the overall outstanding balances of SBL. Each bank knows individually its exposure, you’d hope. Many banks lump them in with other loans, and there is no overall summary figure, and so no one knows how much leverage there is in the stock market in terms of these securities-based loans. But we know it’s huge and ballooning, given the amounts that are disclosed by a few banks.

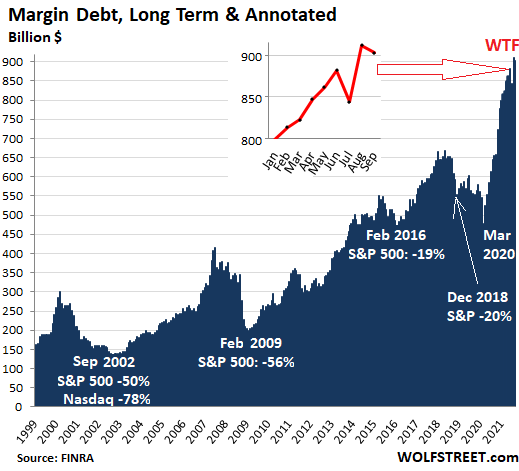

Margin Debt blows out, then dips.

Regular margin loans are reported by brokers to FINRA, which then reports them on a monthly basis, which it did today. They are the only measure of stock market leverage that is tracked. It’s an indicator of the trend in overall stock-market leverage. The tip of the iceberg.

Stock market margin debt, after spiking to another all-time high in August, ticked down in September, to $903 billion, up by 38% year-over-year, and by 61% from January 2020 before the sell-off started.

What’s important in a chart like this that spans over two decades is not the absolute level of leverage compared to back in the day, because the purchasing power of the dollar has diminished. What’s important are the trends and patterns – the steep increases before every stock market sell-off.

Spikes in margin debt don’t trigger sell-offs and they don’t predict sell-offs because they sometimes lag those sell-offs.

But leverage pumps up stock prices by creating buying pressure as borrowed money surges into the market; and when the market tanks, forced selling by leveraged investors creates selling pressure and amplifies the sell-off and triggers its own downward spiral.

The Fed has repressed interest rates to encourage borrowing, and it contributed to this spike in leverage, and to make it all work out, it inflated asset prices via $4.5 trillion in QE in 18 months as part of its official Wealth Effect policy. A few months ago, in its Financial Stability Report, while pointing at Archegos, it warned out of the other side of its mouth about the vast unknown parts of leverage among hedge funds and insurance companies.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Our economy is now like a crew of carneys hurtling through the desert in an ancient worn out school bus. The hubcaps have fallen off, all the instruments are blinking red and the oil and water have mostly leaked out. The driver (old joe) is nodding off as the clanking gets louder. The carnival boss J.POW is standing on the engine ( the hood flew off a few miles back) . He is pouring sawdust and magical mystery oil straight in to the fill spout. Then he pulls out the super special gunk ( stock market leverage) and tells the passengers “ don’t worry it’s good as new, we can drive forever.”

Good one SC!

Education AND Entertainment AND Amusement in one site!!!

I can actually visualize this……

I AM AWAITED IN VALHALLA !!!

We need Ralph Steadman to draw that scene. Thanks.

We’re missing Hunter’s wry reflections on the American Experiment.

The crooked politicians in both parties are fighting the bad fight: standing up to avoid requiring the ultra rich who bought them via money, or who hold videos of them molesting little girls, pay a fair share of taxes like your dentist or grocer. This leverage is being used to delay the inevitable crash until the parasitic banksters, Wall Streeters, and their cronies get out of those markets without losses.

This leverage and over-leveraged, US companies make it hard to believe that the collapse of China’s real estate sector, which is so huge a part of their economy will not have indirect effects in the world economy. Unless they are insane from living under such massive amounts of propaganda, after seeing these hundreds of bankrupt, real estate developers, China’s consumers may not see it as the place to invest and may not want to pay over 30 or 40 times their annual earnings to buy increasingly, defective, tofu buildings anymore.

America’s overleveraged, financial and other companies are like eggs balanced on a marrow, window sill: it does not take much to drive them off it and down.

Those huge increases in margins are from banks who offer 5-7% margin rates. You can go to a smaller brokerage for 1.5-3%. So you have to assume that those banks are getting increases in margin *despite the fact* that many of their regular users who are getting into margin will shop around and transfer to something like M1 or IB. Then you have the margin rates and amounts of leverage in crypto (which are also competing with these big banks and taking away many users).

And all these margin rates are variable – when the fed increases rates (or is about to) it’s going to be like being in crowded theater trying to get out of a single door before the forced selling begins…

Exactly.

I call it the fart in the elevator phenomena.

Those margin rates hit hardest while you are short. All shorts are done on margin (ex maybe short against the box?) Short ETFs use swaps and no idea what that costs. The expense fees make the time decay the primary factor. I have often wondered if shorting a short fund isn’t the best investment.

Ambrose Bierce,

“All shorts are done on margin”

That is not correct for all situations.

If you have enough cash in your account, and you then sell short some stocks, but less than you have in cash, there is no margin interest charged to your account. But you don’t earn interest either on your cash (what interest, hahahaha).

But if you have $100k in stocks and no cash and you sell short $20k in stocks, then you pay margin interest.

You may also have to pay the dividends on what you sold short. And some fees may also apply.

Your are not allowed to short against the box. Not for the last almost 20 years. Not with shares but you can hedge a position with options

It works great till it doesn’t work. It’s a BB on a razor blade. Step up to table and place your bets. We can all be rich. What can go wrong when the Fed and Congress are getting rich also? Come one, come all. The opportunity of a life-time is now. It’s different this time. The Fed has solved the problem of productive work getting in the way of getting rich.

A bad regulatory environment (enabling moral hazard, and dry kindling piling up in weird places) lurks beneath. I recall hearing a quote of Chuck prince, then Citi head, to Hank Paulson before the ’08 crash, I paraphrase: can’t you order us to stop this? The reference was to a competitive environment (including, legal framework) where everybody had to take the candy before the next guy does. I recall a student of mine saying he questioned the crap mortgages he was being prodded to sell to commoners, and the reply was, do you want this job or not? But on the gov side it is devilishly hard to put in good balanced frameworks with the incredible cacophony in this country. I’m so glad the Constitution happened in a different environment, because that sort of governance framework never could appear now. At least we have that.

Everything’s really going parabolic now – the DOW, crypto, Wolf’s WTF charts, etc. How many blow-off tops is a record, anyway?

To be fair, we live now in the Debt Age.

Having “lots of debt” is no longer a shock.

Debt is the new savings. The new normal. The new paradigm.

US Q3 earnings have gotten off to a cracking start this week. Expect more debt and more leverage for stocks.

The bull run is still on.

You are only an instant away from a shock. Could be giant earthquake or volcano or dirty bomb in a major city. You don’t want to get caught in an over leveraged position.

Or a pandemic…. wait. Nevermind. Those are great for the economy.

China / Taiwan one morning…

Or oops, that sw update did not work.

Last time it was Facebook, it could be the power grid or the banks next. And the downtime could last longer than a few hours also.

Earning s are a lagging indicator. But yes, it really is different this time, isn’t it?

Speaking of that…

Restaurant stocks were DOWN yesterday…

perhaps people are figuring out that no employees and higher food prices arent good.

How much to reprint your menus every week?

How much to reprint? Just put the menu on the interweb and it’s nothing more than a data entry, kind of like the Fed buying bonds. Plus you’ll rid of yourself of elderly customers.

Some local restaurants have a QR code taped to the table top. Using your mobile device, you snap the QR code and it brings you to the menu and pricing… which can change at a moment’s notice.

Then after scanning the QCR code you get the menu and quite often it is also possible to order and pay too.

Earnings?

What earnings?

50% increase in S&P since March ’09 was due to BUY-BACK SHARE programs! release from ‘reserve’ is another gimmick to increase earnings(JPM!)

Q3 earnings were to be expected. There were still tons of “stimulus” floating around from consumers.

I don’t see how that can be maintained.

Introduce “govcoin/us,” blockchain all banks, call all cash to be swapped or else goes to zero, all existing accounts immediately convert ,all assets immediately convert,all debt immediately convert. Problem solved. What say you?

Sit down, and take a laxative!

Demanding exchange of cash for electro ticks would get one a hail of buckshot between the eyes and they know this. That’s why they’re trying to quietly kill cash with every dirty trick they can find. If you convince people to walk into a jail cell on their own, you can probably get the dumbshits to close the door behind them and toss the key to you while you sit with feet up sipping megabuck mocha.

You just described a complete fantasy. Your description is absurd.

You might be called a fascist if you tried that. It’s only a label, though, shouldn’t inhibit a real technologist.

If you ove a lot of million dollars the bank has a problem…

All the gambling should be an opportunity for long term investors. Best time to buy quality assets is when there are distressed sellers who fear they are going to lose it all.

They took the gamble, they need a buyer and a value investor will do the transaction when the sell price yields an above average long term return. Fed interrupted the process in 2020, but might not this time as they are a bit in a box.

Yes, but the problem is that there have been no real value asset classes for a long time. The stock market was hardly cheap historically in March 2020.

When the trend finally reverses, buying into a “panic” low like 2020 is more likely to be the equivalent of catching a falling knife. Buying an asset as overpriced as the US stock market at a 35% discount is no real bargain.

It also depends upon what you mean by “quality assets”. I’m interested in buying individual stocks paying meaningful dividends. Problem is that the vast majority of corporate balance sheets are absolutely awful, leveraged to the gills.

Like 2008 but worse, I expect stock prices to crash making stocks look cheap, then earnings will fall even more, and then dividends will be drastically reduced or eliminated. Or whatever is paid will be paid in very reduced purchasing power.

One way or another, most people are going to lose.

When liquidity is gone it takes some real courage to jump in and a whole lot of luck to get the timing right. It’s not a crash unless people are frightened to DEATH. There should be no bids from anybody. Plus you must have been prudent enough to disobey Wall Street and move a lot of money to cash.

Just stockpiling cash until the crash. Figure if I’m patient, any losses from inflation and not capturing the current gains that would be erased will be made up for by buying the dip.

OK, buying the disaster.

All I need to know is who’ll pay this time?

Will average Joe bend over so willingly a second time?

Too Big to Fail. The 2nd act. Coming your way soon.

Too big to exist? Suffocated in it’s crib.

Yes, let’s bring Holder back to explain why the miscreants could never have guessed their actions could result in general ruin.

Kenny Logouts,

Banks can be very quick in selling the collateral – stocks are liquid and easy to sell if you don’t care what price you get. So banks can mostly protect themselves. In a huge crash, they might have some losses, but manageable.

But what will happen in this scenario is a potential wipe-out of the portfolios of heavily leveraged investors, and massive forced selling is going to hit the market. We’ve seen these periods of forced selling. They can be brutal for stock market investors. That’s where the losses are.

Not just SM Wolf, but, clearly based on RE mkt(s) since 1956 when I began to understand why dad had no work at all for six months, and he had to sell the farm and another property to be able to keep the one we lived in…

Just continuing to try to bring some perspective, eh?

Banks use your portfolio to leverage their positions.

Stocks are liquid assets, but do not trading stop if price movements are to large?

Then what if all liquidation sales continious bump the stop trading limit?

Trading doesn’t stop in a normal sell-off, unless it’s a one-day super-crash, and even then it might not stop either. We’re talking about a process that can go on for a long time, months, years, in waves, with many ups and downs.

For an individual forced seller, it might be a one-day or a two-day thing because the broker will pressure him, or do it for him. He will have to take whatever he can get for his stuff. And he might be able to sell enough and get through the day, and the next day there is a bounce, but then the day after, the crash continues, leading to more forced sales.

Generally, you start selling your best, most liquid stuff that hasn’t taken a huge hit, and then you go down the list. As you get to your less liquid stocks, you’re going to take huge losses. And some stocks become worthless and there are no bids and they stop trading and eventually disappear, and your holdings of those shares are worth zero, and when you get tired of looking at them in your account, you can ask your broker to remove them. This happens quite a bit with companies that file for bankruptcy. Someone is going to become the end-user of those shares.

The NYSE can halt trading, for days or months at a time. Liquidity is a matter of perception. If volume dries up selling a large block of shares can take a long time. Once the market perceives there is a large seller, buyers are reluctant to enter the market. (buyers want lower prices, sellers want higher prices). This is where the “block trade” comes in. Two parties agree to exchange a large number of shares, off market, which would otherwise take time to process. Rules require reporting these trades. Guarantees are asked for and given, ( due diligence). Just by ex, when China dumped a large amount of UST in the secondary market, a young hedge fund investor took the whole position. He asked for a personal audience with Bernanke, and he got it. Maybe BB wanted to know what he was doing? Details were not revealed.

‘The NYSE can halt trading, for days or months at a time. Liquidity is a matter of perception. If volume dries up selling a large block of shares can take a long time.’

The NYSE didn’t halt trading in Oct. 29. ‘Can’ it halt trading, is it theoretically possible? Sure, and Congress ‘could’ dismantle the NYSE. Anything ‘can’ happen unless it’s impossible.

As for liquidity being a matter of perception, in actuality it’s a lot like the plane running out of gas. The broker taken out by the Archego collapse may have perceived himself as liquid but the Exchange didn’t.

Taking a long time to sell? The topic is stock held on margin by the broker. In 29 at first there was the courtesy of a phone call if the stock dipped into negative territory. Today unless the average client has made arrangements to draw cash, it’s gone at the market.

In the 29 Crash, in the absence of buyers, a message boy put in a prank order for White Sewing Machine at 1.00 and got it. It had been around 40 $ weeks before. Liquidity appeared to be zero.

PS: the only time the NYSE was halted for more than a few days was at the outbreak of WWI. The (one) handful of halts for a few days have for external factors. e.g., 9/11. The only halts for selling pressures have been for hours. There was no halt at all in the record 23 % crash of 87.

@Ambrose P

“The NYSE can halt trading, for days or months at a time’

What happens when it opens? Are you willing to buy the falling knives!? Fundamentals out the window and very little or no liquidity! May Be Fed will be the ultimate buyer of ‘everything on sale ‘ right?

You’re kidding, right Kenny Logouts? The little guy’s going to pay for all of this. The IRS already has his bank account info. As long as his balance is above $600, the account is theirs for the taking. Granny Yellen, Nancy P. and company assured us it’s going to catch those wealthy tax cheats, because you know they have so many accounts with less than $1k in them.

It is crazy. However I am one of the crowd.

Before 2021 I was debt free with around 100k in assets. Now I have 420k in debt and 600k in assets….

Should I start edging closer to the door? Should I leave the game while there is still some chips on the table? Who knows how long the game will go on.

(None of my debt is callable.)

YOLO! TINA! I believe the famous quote is “you have to dance while the music is playing.” That was an odd nod to musical chairs. The man who said that never got to his chair. Well, OK, that’s overstating the case. He lost his career and had to open his golden parachute.

Sounds like you’re gambling.

I have also been spending like a drunk sailor. Borrowed against the house to buy a bunch of crap, cars, renovations, computers, etc. I am paying 2.9% on half a million dollars and in 30 years that will probably be the cost of a candy bar.

And you have to pay all that back. Smart.

Mark,

Generally speaking ,

Your leveraged assets can lose a lot of value…

Your debt will not…

And trying to walk away from the debt which cannot be repaid with asset sales means bad things in the future….

Unless, of course, Jay Powell is your uncle…

It all depend on age. In the end everyone leave everything but memories of them behind.

To have the bank representative weep of the banks loss in the funeral must be be the ultimate adaption to debt based society.

Thanks for the advice. Though I was expecting some people who might have understood some of the reasoning.

In a way Jerome Powel is my Uncle. I have debt at ~380k @ 2% and 40k @ 0% for a couple year. I figure everybody else is taking advantage of cheap money, why shouldn’t I?

I put 400k into a property that I live in the rest is in stocks that pay a decent dividend and are not US stocks. About half of it in staples like food. These stocks aren’t nearly as over valued as US stocks, but if the shit hits the fan everything cops some of the splatter.

I could liquidate the stocks tomorrow at a decent gain. The property was bought at a price less 20% less than it was 5 years ago. I don’t expect significant capital appreciation or depreciation on it but it is significantly cheaper to own that to rent at the moment.

I’m certainly not naive to the risks.

I’m still dancing. There are chairs that I could take now. Though I think this tune still has one more verse before the final chorus

People don’t want to talk about it but the courts are backed up for years. People getting traffic tickets today have a court date in 2026. Eviction proceedings are log jammed and in the event you need to stop paying mortgage debt they will take 10 years to evict you – if ever.

People are shocked at RV sales numbers but it’s simple, RVs have 30 year loans and accounting for inflation they are free right now.

This, ladies and gentlemen, is a terrifying illustration of the dearth of math skills and a debt-junkie.

*mindset

That last word was left off.

Home mortgage in USA is a subsidized rate, so if you are ready to settle down for ten years getting a 30 year mortgage on a property that you are sure you can make the payment on even in a recession will be a good proposition.

The making the payment in a recession is usually the hard part.

“But leverage pumps up stock prices by creating buying pressure as borrowed money surges into the market; and when the market tanks, forced selling by leveraged investors creates selling pressure and amplifies the sell-off and triggers its own downward spiral.”

Truer words were never said. This is the practical aspect every reader-investor should take away from this excellent piece. Nicely done.

Plus many companies are highly leveraged already. Do you really need to leverage up another 50%?

and what of all the cross collateralization and rehypothication going on?

Debt is good

War is peace. Freedom is slavery. Ignorance is strength. Saving is Punished.

Stable means increasing at a constant rate. Extremely low interest rates are moderate. Lender is slave to the borrower.

Orwellian Monetary Theory (OMT)

One of the best comments I’ve ever seen.

Consumer capitalism does take on attributes of a shark: it must keep moving, churning, eating, creatively-destructing, or it dies. When those dumb enough to be in its forced march toward ever-receding Orwellian (latest Happy-Meal-menu of) “freedom” lag, they are juiced with credit, like some sort of injected hormone that weakens the user (and the used, whichever is which). “User” is another Orwellian semantic trick.

It’s only nature naturing, the nimble taking the laggards out (with little sidewalk dice games). Oh, and nowadays, taking our biosphere out with last week’s trendy trash too. But there is no ‘out” anymore. It starts backing up into itself, devouring itself, and no time more than when the theater catches fire. Ya-hoo!!

Questions for anyone here:

Not talking about the shady banks and their possible exposure, but what methods really exist for investors to dodge their margin mistakes? Simple bankruptcy? Plus, I wonder if this borrowing behaviour is a logical result of the modern world of few real consequences?

My neighbour lost 250K back in the GFC, but not from borrowing just from following poor investment advice that didn’t fit the times. While still okay, it certainly changed his attitudes. One example of this is that he sold his spare lot with a cottage on it to make up the losses, and then did not want to buy it back at a very low price just this year. He doesn’t want to touch his capital, ever.

No unsophisticated investor should be using margin to invest. The pros, that use margin wisely, hedge their positions in the options market. This means they decide how much of a hit, in advance, they are willing to take on the downside and buy the necessary options. When the dips occur they get out of the trade with an acceptable loss. These are complicated trades and should be left to the pros.

Which sophistedcated investor keep buying stocks when the DEBT to GDP (Buffett’s indicator) is over 200%!

Only speculators!

@P

“what methods really exist for investors to dodge their margin mistakes? Simple bankruptcy?”

A margin lender will generally require collateral which will very probably be a percentage of the shares you have, hence the term ‘margin’. Usually they play extremely safe and lend maybe 50% against collateral. The absolute last thing they ever want is a capital risk just like on a house. They make their money on interest and loan fees, they may even make you pay to insure them against risk of loss, that’s their business model. When your shares drop close to 50% of their value you’ll get a phone call (yup, a margin call) saying your lender will sell all your shares unless you provide more collateral.

Technically you don’t go bankrupt, you just lose all your invested money, so long as you paid all your fees and interest, otherwise they’ll come after you for those in court, although they’ll probably charge them to your share sales first.

Lenders have no risks in margin loans, it’s a terrific earner for them, that’s why they push sales to gambling suckers. Why they push loans to all existing assets really, except small businesses where they would have to take an actual ‘risk’ to earn a living. That’s why they don’t do it.

Paulo said: “He doesn’t want to touch his capital, ever.”

—————————————-

What do mean by capital? Dollars? A dollar is like a melting ice cube; Just something conmen-bankers have devised, which they can create and use to garner real assets for themselves.

Long term, better to own a free and clear rentable cottage and lot than a bunch of “melting” dollars. Perhaps even better, to buy that rentable lot and cottage with zero down, low interest, non recourse loan ,,,,,,, holding the dollars aside as an asset. If dollars become worthless, use them to pay off the lot and cottage. If dollar becomes scarce and valuable, use them to buy cheap assets and let lot/cottage muddle through or revert to lender.

So far in 2021, has the Biden Administration,

and the Biden Federal Reserve Bank ,

made any financial / economic decisions / actions

that you would consider good for the American economy?

Would the answer to that question be a good leading indicator of future actions / decisions, and also the direction of the US economy?

Richard Greene,

“…Biden Federal Reserve Bank…”

OK, reality check. Biden hasn’t yet appointed anyone to the Fed. The Fed is run by a Republican who was appointed to that job by Trump. So you need to blame Trump for the Fed.

Nice comeback there to the Orwellian Politicians there by Wolf.

This Ancient Fart is reminded of a quote from a famous economist who is often reviled and mis-understood: “The market can remain irrational longer than you can remain solvent.”

I don’t see any good way to bet against all of the unproductive debt being used to gin up asset prices. When the music stops, I think the little guys are going to lose big.

Masked…

since 2009, central bankers have taken a pledge to disallow corrections or normal cycling of the markets and economies.

All charts are supposed to move low left to upper right.

Cycles and corrections flush excesses, the poorly financed. The Fed seems bound to save all and allow excesses to build.

The eventual flush becomes Biblical in nature.

Corrections are called corrections for good reason…..they correct.

Is there one contrarian left? The entire thing since 2009 has been a cattle drive….and this is why 12 cowboys can herd 30K of cattle.

This for h:

NO, a dozen human riders of horses CANNOT herd 30,000 cattle ”most of the time”,,, and YES indeed, your analogy is a good one.

Sometimes, YES, when all the cattle are not only hungry but thirsty and heading right at a water source, that would work, far shore…

Other times, clearly NOT even close,,, and YES indeed, your analogy for today is going to go to HECK, straight line or not!!

Thanks for your many educational posts for this old boy ( who rode horses in several ”round ups” many decades ago ) ,,, trying to figure out how to ”hedge” against the clearly crazy investment / economic environment these days…

Trump jawboned Powell in Dec of 2018…

and Trump cheered for negative rates.

Both distasteful IMO.

Trump hates interest rates as he is always the borrower…like the govt itself. And I think he hates the Fed as it put him out of business in 1981.

Biden doesnt know airplanes are flyin’ much less of the mechanics of the Fed.

Biden had a good excuse to fire Powell if he wants to. Powell said inflation was transitory and it was not. Throw Powell under the bus and then blame inflation on Trump and Powell.

I have heard they have it the way they want it with Powell and Brainard working together. Powell has market experience and Brainard is weak in this area.

Was Trump Enriched by this J Powell ” appointment ” then .

I was thinking perhaps by the Huge stimulus to the economy

just the increase to all his Real Property’s alone must have been substantial . What Part do you Give Obama as he nominated J Powell was he enriched after Trump’s appointment . Who of the 3 ( Trump / Obama / J Powell was

enriched the Most ? any chart or graph on that By Chance

Wolf…

Maybe adrift of the topic, but not entirely. It may be a revelation of the over leveraged…

October 13, 2021 ~

“The Federal Reserve Bank of New York has quietly posted the names of the banks that grabbed billions of dollars under the Fed’s emergency repo loan operations that commenced on September 17, 2019 – months before there was a COVID-19 crisis anywhere in the world.”

….

“The names of the banks and the eyebrow-raising amounts they borrowed from the New York Fed do not square with the official story at the time – that the liquidity crisis occurred because U.S. corporations withdrew large amounts from the banks in order to make quarterly tax payments. The fact that so many huge loans ended up going to foreign banks, as well as Goldman Sachs and JPMorgan Securities, suggests that this was a derivatives counterparty problem, potentially triggered by Deutsche Bank’s crisis at the time.”

Did you catch this? Any thoughts.

historicus,

The people that wrote it (name removed) are purveyors of fiction. They’re clueless about how repos work. Even the most fundamental basics. They have no idea. They didn’t even know that repos are by definition in-and-out transactions. They just added up the ins without subtracting the outs and came up with this huge gigantic ridiculous number that was total BS. But it got them a lot of clicks. I called them out on it (without naming their site) in early 2020 because I got sick of seeing that shit in my inbox. They just make up stuff to get clicks.

If you want to read financial fiction for your amusement, that’s a good place to go.

But please don’t drag their fiction BS into here.

Wolf said: “The people that wrote it (name removed) are purveyors of fiction.”

———————————–

Would you please name names so the less experienced of us know who to ignore?

Nope. But I do block people from promoting it here.

ZH, when it comes financially complicated issues such as repos, nails it. The ZH people know how repos work. This information is out there. You might not like ZH for all the other nonsense they post, but their articles on arcane financial issues are good.

So when this unnamed website produces this ridiculous fiction, I’m thinking, they can’t be that ignorant. It has got to be wilful fiction clickbait. And there is a lot of that out there.

If and when stocks fall, RE will fall as well. There’s a mountain of mortgage leverage that would blow up.

However, the Federal Reserve doesn’t seriously consider that outcome. Based on their actions (and inaction), it appears they want a strong inflation, followed by the Great Depression 2.0. They’ll achieve this through ever-increasing debt levels, ever-increasing wealth concentration, and long-term real economic structural erosion via kick-the-can policies.

It’s a great time to buy a house, the Fed says. Get a mortgage leverage out your income 10x. Don’t worry.

I really doubt that the government will allow a catastrophic crash any time soon. They realize that the economy can’t take it.

The Fed’s credit card is far from maxed out.

You don’t get a warning when the credit card is about to be maxed out. all of a sudden, foreigners start dumping their tbills, people start buying assets at any price, and you have a crack up boom followed by a collapse.

I don’t think it’s as far off as people think.

Yup, important number. Margin debt is what killed the market in 1929. Everything got way oversold due to margin calls. They put in laws to avoid this, but then, like, ‘financial innovation’ — here we are again. Oops.

My FS broker assures me they will not mark my Portfolio loan to market (never say never) The banks and Fed have this all worked out. Derivatives are written on either interest rates or currency. There is no counter party risk, esp with all the global liquidity sitting on the sidelines. You might daisy chain your hedge from a Cayman (entity) bank and when they get a margin call then the Fed sets up a offshore dollar swap line, and a repo line to swap cash for treasuries (rehypothecated from the holdings of wealthy foreign investors who were there for fun sun and a tax haven), and collateralize their position. (Nobody gets hurt). The story on Archegos is a an offshore investor running a “family” fund with no accountability. You might assume Bill Hwang lost a fortune and you might be wrong. He may have blown up his own portfolio and cashed out through offshore entities, and made money on the deal. He has to reorganize under a new shell, with some fabricated narrative about turning lunch money into a fortune buying bitcoin. Madoff would still be working if he had moved his offices to Florida? ARK? Its a problem of biblical proportions.

Massive negative wealth effect coming when this unwinds disorderly, or even orderly if that is even possible….

The weak don’t get exposed during an expansion and that’s why Powell keeps running loose policy. Even a zero real rate would crash the party now. But inflation expectations are going to bring this thing to a head.

Every signpost points to Hell but when the blood runs in the streets you’ll never know where the first bullet came from. Too much margin debt, too much interest rate repression, not enough computer chips, droughts and fires, completely screwed supply chain, Evergrande, China/Taiwan, people quitting jobs but spending up,

Too many possible triggers, too few of them known. Which straw will break the camel’s back?

All roads lead to recession/depression/deflation. What can’t go on won’t go on. Cash isn’t trash and gold is a barbaric but valuable relic. Maybe stake a little ETH at 5% while you’re at it.

@MG

On the other hand, “always look on the bright side of life!”

Everything you say, plus you forgot floods and no wind.

Nevertheless, here am I, truly ancient, drinking whisky and looking out the window at the harbour.

Just sayin’

Michael Gorback said: “The people that wrote it (name removed) are purveyors of fiction.”

—————————————-

What about about that well used road of continued dollar expansion?

I don’t think Michael Gorback said that. I think I said that :-]

Michael Gorback said: “The people that wrote it (name removed) are purveyors of fiction.”

—————————————-

What about that well used road of continued dollar creation?

On a somewhat related note, I was owed a small refund by ATT. They sent it on an ATT debit card issued by Sunrise bank. Everywhere I have tried to use the ATT debit card, it is rejected. The Sunrise bank has a number where no person is accessible. ATT refuses to send me a check, but they will replace my unusable card. And now the card expires this month.

What a perfect scam. Send out refunds on unusable debit cards which expire. Then keep the entire refund.

Big banks – ALL OF THEM – are fraud outfits. They are not legitimate businesses whatsoever, just fraudsters who are protected by paid off politicians and regulatory capture.

Just throw a magenta costume on all of them, and call it squid games.

The cashier has to hit a certain button for it to go through (and maybe enter the exact dollar amount of the card); I’ve received them also. It’s easier to use them online, the big W store for instance.

I opted to receive one instead of check for a manufacturer’s service rebate because “extended c0vld timeline!!!” — after I received it, I had to create an account to use it (of course I typed in fake personal information!).

I created an account with a pin and told every store what I was trying to do, use balance and pay the rest in cash. No store told me to do anything different than just swipe and put in pin, which got card rejected.

But thanks for letting me know there may be another way to use their unusable debit card, which is more than I got from ATT and Sunrise. I still think they are scamming their customers.

You could try making your purchase with the service desk also; the person should be more knowledgeable.

Another thing I remember from those stupid cards is making a purchase just below what the card holds—if your card holds $5, try to make your purchase $4.80 or something, and forget about the rest. I think they have to hit “credit”, but you still enter a pin. Can’t remember, but it was something screwy. A pain and yes very scammy.

Petunia,

With these kind of matters I have filed complaints with State Atty General’s offices in my state and the other state where the company existed.

I always got good results and they really changed their tune from being the bad guy to being a extremely nice guy all of a sudden when the state boys came a knocking on their doors – LOL

Don’t let them push you around!

I had the AT&T one happen. I emailed ATT several times, called them and explained that I had an issue with being forced into a contract with a third party over money owed to me by ATT and that I’d be explaining this to the Better business bureau. I’m not even sure it’s legal. I looked up Sunrise Bank on the Better Business Bureau website and the list of complaints was so long I couldn’t even scroll to the end of it. I insisted they send me a check from ATT, the company I was transacting with and not a third party. They sent the check. Things like that really irritate me.

Charming AT & T tried the same thing with me last year when I cancelled my Fibre account. I told them NO way. I filed a dispute with the FCC — they do NOT like that, Lo and Behold the refund was sent direct to my credit card in hours. It is very easy to file the dispute on line.

In the 1930s, the Americans found margin lending and share buybacks had artificially inflated the markets and this had lead to the Wall Street Crash of 1929.

What lifted US stocks to 1929 levels in 1929?

Margin lending and share buybacks.

What lifted US stocks to 1929 levels in 2019?

Margin lending and share buybacks.

A former US congressman has been looking at the data.

Sound of the Suburbs,

That’s very interesting, and can you share the US congressman’s name?

If you Google this below exactly you will find a interesting article, from MarketWatch.

“This veteran analyst hears echoes of the 1929 crash in today’s stock market, site:MarketWatch.com”

There are so many known events that can “derail” these nonsense markets, let alone all the unknown “Black Swan” events that can arise.

Those folks squawking that the market is in good shape, and others saying the Dow going to 40,000, then I have a lot of Brooklyn Bridges to sell them!

The stock market is like playing a game of double or nothing with a coin weighted 95% in your favor. The vast majority of the time , the coin comes up in your favor . But a small % of the time , it does not and you lose everything.

please delete this comment – there was an error and it posted below (it was a reply to Petunia)

Just read that bank of America issued a 3 billion dollar bond.

Also read that American banks don’t want more cash

from clients. If they already have more money than they

need why issue bonds.

Following a better-than-expected earnings report, “The bank sold 11-year fixed-to-floating-rate notes [3.25 billion] to yield 1 percentage point above Treasuries … The proceeds are earmarked for general corporate purposes.”

I’m wondering who would buy these notes?

“Blowout results from the big U.S. banks may spur even more bond issuance from the financial sector, with borrowing costs still attractive even as some market rates rise. … The bond deal comes as risk premiums in corporate debt remain low.”

If your profits are currently strong, and the risk premium is low, why not borrow and have A LOT more money than you need? Then you can leverage even bigger profits.

Bonds have a fixed maturity and the cash cannot walk out the door suddenly, as cash from a deposit can. That’s why banks sell bonds and long-term CDs. It gives them funding stability. Deposits alone can vanish overnight (run on the bank), and the bank collapses. For banks, this is a diversification of funding strategy. It’s crucial.

Wolf said: “What’s important in a chart like this that spans over two decades is not the absolute level of leverage compared to back in the day, because the purchasing power of the dollar has diminished.”

————————————————

The second part of your sentence just describes a side effect. The real reason the absolute level of leverage is unimportant is because of the huge money expansion, increased dollars created into the money supply.

Wolf said: “The Fed has repressed interest rates to encourage borrowing,”

——————————

The FED has repressed interest rates to bail out favored entities and groups. By repressing interest rates, it has allowed whole overleveraged segments of society to refinance, lowering their interest costs, increasing their cash flow, pushing up their asset prices and making them solvent. This has allowed these borrowers to spend their increased cash flow into the economy and purchase other assets.

The FED has bailed out debtors, banks and wall street at the expense of savers. They FED has made the imprudent “smart” and the prudent suckers.

Todays economy can best be called a “Baked Alaska” — Piping hot on the outside and iced cold in the center.

I think you can throw out conventional wisdom when trying to understand todays economy. The insane is now the sane.

Banks are essentially paid to borrow T-bills to put on their balance sheets through the reverse repo program.

https://www.newyorkfed.org/markets/data-hub

The federal debt has risen by 400 billion dollars in the last week, yet there’s no change to the demand for reverse repos. This and the securities lending facilitates investment banks increasing their leverage.