Just because Amazon was able to succeed does not mean others will. But they’re getting showered with money.

By Jeffrey Funk, an independent technology consultant (linkedin), for WOLF STREET:

Unicorn startups are on a roll. Their share prices are up at least 50% since the pandemic started, and most have doubled and some tripled. Although profitable startups such as Zoom, Roku, and Square are up the most, even startups with large losses are doing well. Share prices for Snap, Twilio, and Pinterest are up three times, Slack’s shares have doubled, and Uber and Lyft’s shares are up 50%.

VC funding is also strong. Funding hit $125 billion in the first quarter of 2021, the highest ever. And this follows a record setting year in 2020 and in the previous five years between 2015 and 2019. Optimism about the impact of startups on productivity is at an all-time high. VC fund managers such as Marc Andreesen, founder of Netscape, are predicting a productivity boom for the 2020s.

The high funding and high share prices assume that today’s Unicorn startups will grow out of their losses. After all, Amazon achieved this. As America’s most famous money-loser, it did not turn a profit until its 10th year of existence and its profits did not cover its peak cumulative losses of $3 billion until year 16. But it is now one of the most valuable companies in the world.

If Amazon could do this, why can’t today’s money-losing Unicorn startups, which represent about 90% of Unicorn startups in 2019 and in 2020? But most of today’s money-losing Unicorns are far older than 10 years, some as old as 20 years.

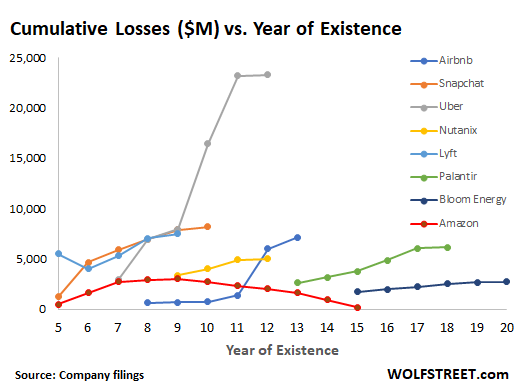

The below chart compares Amazon’s cumulative losses over time (bottom red line) with those of selected Unicorn startups. Cumulative losses are graphed vs. year of existence. In the case of the startups, the final year of data for each company is for the first quarter of 2021 and thus is only for one quarter as compared to an entire year for the other years. The losses are not adjusted for inflation.

The chart shows that several Unicorn startups have vastly exceeded Amazon’s peak cumulative losses of $3 billion in 2002. Uber’s cumulative losses have exceeded $23 billion while those of Snapchat have exceeded $8 billion, Airbnb and Lyft $7 billion, Palantir $6 billion, and Nutanix $5 billion. Bloom is close with $2.5 billion. Recent estimates for WeWork, which does not release data, put their cumulative losses at about $10 billion in March 2021.

Many of these startups have huge valuations. Snap, Airbnb, and Uber are currently valued at between $90 and $100 billion while Palantir is valued at $46 billion, Lyft at $20 billion, Nutanix at $8 billion, and Bloom Energy at $4.6 billion. In comparison, Amazon didn’t pass the $20 billion mark until 2003, after it had achieved profitability.

The losses for these startups continued to grow in 2021, partly obscured by the single quarter losses of 2021 being compared to full year losses for the previous years. Other than Bloom, all these startups are on track to add at least $1 billion to their existing cumulative losses in 2021. Uber’s 2021 data point is particularly misleading because its $100 million losses include the $1.6 billion in income from the sale of its autonomous vehicle unit. Without that sale, Uber’s first quarter losses would have been $1.7 billion or $6.8 billion on an annualized basis. $30 billion in cumulative losses by the end of 2022 is entirely possible.

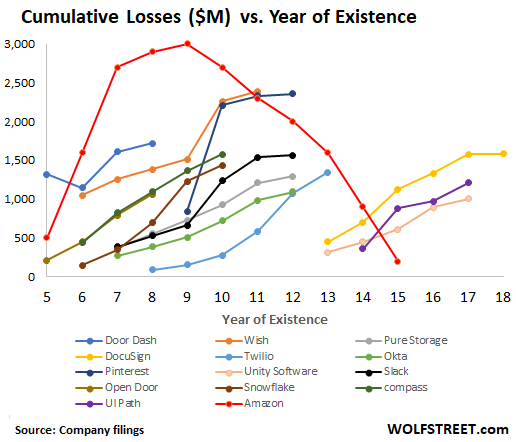

The cumulative losses for many other Unicorn startups are also rapidly growing and may well reach those of Amazon’s peak losses (in red) in the next few years. The below chart compares the cumulative losses vs. year of existence for 12 other Unicorn startups.

Six of them now have valuations greater than $50 billion: DoorDash $58 billion, Snowflake $70 billion, Pinterest $51 billion, Twilio $66 billion, Opendoor $72 billion, and Docusign $54 billion. Then there are: Okta $32 billion, Wish $7.5 billion, Compass $5 billion, Pure Storage $5 billion, Unity $30 billion, UIPath $34 billion, and Slack $26 billion.

Yet the chart suggests that only one of these startups might be on its way to profitability: Pinterest, with cost rising less than the 50% increase in revenues during the pandemic. The cumulative losses for the other 11 are still growing.

The ones on the left are a bit higher, but at least they are only in their 9th to 15th year of existence. Wish has the highest cumulative losses of the batch, reaching $2.3 billion. Door Dash, Compass, Open Door, Slack, and Pure Storage have cumulative losses between one and two billion dollars.

The startups on the right side of the chart might be in a more difficult position than those on the left because they are much older than those on the left. UI Path is in its 16th year of existence, Unity and Twilio in their 18th year, and Okta in its 20th year. Yet their losses continued to grow in 2020 and 2021 and all of them have more than $1 billion in cumulative losses. Other than Pinterest, none of the startups in this chart suggest they are close to a turnaround in cumulative losses.

In summary, Amazon is not a good model for today’s money-losing Unicorns. Just because one startup was able to succeed, does not mean that others will also succeed, particularly when Amazon had achieved profitability by its tenth year of existence. Most of today’s money-losing Unicorns are far older than 10 years, some as old as 20 years. Moreover, the cumulative losses for many of these startups still continue to rise with no turnaround in sight. Amazon’s history suggests that the biggest money losing Unicorn startups may never achieve profitability on a cumulative basis, or at least it will take so long that it doesn’t matter. By Jeffrey Funk, an independent technology consultant (linkedin), for WOLF STREET

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

All these “unicorns” are trying to corner a market and become a monopoly power difficult or impossible to dislodge. Amazon has reached such monopoly position, as have some others (not on the list here, like Microsoft, Facebook, Google). They can now set any price they want for their output.

Investors are piling money in, in hope that their horse will reach monopoly status, at which point they can skin their victims, pardon, customers, at will. See 1 above.

I wonder, how much of the investment flows are real investors with real money, and how much comes from funds that are obliged to invest somewhere, like your usual pension funds. Owners of funds (pensioners), having no idea where their funds go of course.

Which sectors can be completely cornered? Taxi riding? Fast food delivery? Document signing over internet? Seems all a bit far fetched to me.

Amazon has not reached monopoly power at all. The vast majority of Amazon profits come from the AWS service and both Microsoft and Google are gaining share, albeit from a far distance behind. Amazon has done a remarkable job in creating an unique distribution platform, but if Walmart or Target or any other ecommerce player was a better competitor, there would be no monopoly.

I think many of these unicorns will just accumulate more competitors. Palantir accumulates many new competitors who want a slice of that pie. Uber and Lyft have regional competitors and the transition to autonomous networks might actually dislodge either of them.

I am seeing a market cap for opendoor of 9.7 billion, am I missing something?

Ditto, GameTV…Amazon’s “monopoly” almost entirely rests on buyer inertia/laziness…which will evaporate once Amazon price inflation reaches a high enough level.

The huge (and hugely expensive) Amazon distribution system does give them some cost/pricing advantages…but, again, if Amazon tries to inflate pricing very much (for more attractive margins) it really, really stands out in an internet environment and buyers will migrate.

Prime provides some limited, transient lock in…but once people wise up to poor pricing, they certainly won’t pay an annual free for worse pricing.

For any pricey item, Google (although directly benefitting little) is a mortal enemy to any aggressive pricing by Amazon.

And that hypercompetitive dynamic is intrinsic to the internet.

cas127

Lot of contradictions in your post:

1) Amazon is not a monopoly, except in the opinion of guys who hate Amazon (which is perfectly ok) and have zero idea exactly what the definition of a monopoly actually is

2) Amazon market share is driven by customer demand (some of whom may indeed be lazy), but just about everybody would rather eat a dead rat than spend an afternoon at the local mall

3) After (incorrectly) anointing Amazon as a monopoly, you state that Google is a “mortal enemy” and the internet has an “[intrensic] hypercompetitive dynamic” – so which is it?

when the 1% have TRILLIONS free money to throw around

plus all that stimi they vacuumed up

well they can fund anyone

tech enemy are those still protected by 230

people need to have 3rd party arbiter to decide who gets censored

and ABILITY TO SUE SAID BIG TECH

Javert,

I did not say Amazon was a monopoly…are you unfamiliar with “ironic” quotation marks?

That said, Amazon does currently have a lot of mkt power (look at revenue levels and revenue growth).

But then I point out some of the factors that will undermine that mkt strength.

So, no contradictions.

cas127

Point taken.

I generally enjoy irony, so it’s ironic that I missed the irony.

Amazon owns online retail. Yes, many companies have their own sites and eBay, Yahoo and a few others have a small market share. Still, Amazon, like Google is the aggregator that everyone turns to, and they have massive market power. Worse, Amazon competes with its own sellers taking clear advantage of their monopoly position.

Amazon’s the price setter in just about everything they sell. In that sense they’re a monopoly.

That is what Oracle has done the past 30 years is to buy up any promising database competitor to essentially become monopoly.

Sometimes it works.

Etherium and a hundred other cryptos are competing. Two brothers in South Africa stole billions of dollars from a bitcoin exchange saying it was lost to hackers. Many billions in bitcoin have been lost to hackers or due to lost passwords.

Having worked for MySQL (loved that company) I concur.

But for the employees sometimes it doesn’t work.

ru82- this (buying competitors to eliminate them) is a sign of monopoly that the regulators are slow to respond to and in the US does not “directly”/”immediately” result in the bad/”obviously illegal” monopolistic results. In the US, the monopoly is only bad when it reduces quality or raises prices, which directly damage customers. That’s one reason why you see a lot of these startups (e.g. Amazon) come out with money-losing pricing. Then they can’t be accused of that monopolistic behavior/result.

All of these tech companies (big ones) have engaged in monopolistic practices, but it’s hard to go against them in the US legal system.

The investment case for bitcoin relies on its ability to reach monopoly position to an even greater extent. At least corporations can theoretically make a profit and a larger size helps to increase the probability that this will happen. With cryptos, the closer you get to a saturation level in the market, the more investors will be tempted to invest in competitors that have greater growth potential. After all, the dominant reason for achieving market share was rapid price appreciation. When that prospect goes away, what other reason is left to HODL?

If you graph the cumulative fees paid to bitcoin miners on a graph since 2009, you could compare bitcoin to the unicorns. If we add up all transaction fees in USD, the cumulative total is around $5 million times 400 days, or $2 billion, if the data on blockchain dot com is accurate. But if we include the coinbase block rewards, the total is closer to $20 million for 4 years, or around $30 billion. That would make bitcoin the cash burning champion, surpassing even Uber.

Good post. a lot of people don’t realize how much in fees is paid out daily.

If that velocity drops, what happens to the crypto eco system

stan65

Nice word salad, Stan. However, Amazon is nowhere near a monopoly. Last I checked, Amazon sales were <10% of total retail…and that "<10%" is inflated because it includes Amazon cloud, and I have no idea how to back that out.

JC,

You are right, Amazon is not a monopoly. My bad. But Amazon have a dominant position and whoever is looking for something they do not normally purchase, they go to Amazon . Days are long gone when Amazon’s prices were cheapest and these days there is a ton of stuff of dodgy provenance, from unknown sounding brands being littered around when you search for brand names. For example, I looked up Apple phone 11 yesterday, and with all filters properly included, the search was full of lookalikes from firms like “gunu” and “moab” and “dibl” whatever, cant be bothered to go and check the crap again.

The point I was making is that I felt that maybe one of the factors that money that is being piled into the new generation of “unicorns”, apart from being free thanks to uncle Jerome, is being piled there with hope that all these losses will pay back when the “corns” corner that particular segment and then sell cheap CCP dross at inflated prices, to dumb “consumers”, for years to come.

Total absence of transparency does not help, and the pension funds worldwide are being fleeced because a lot of that pension money is being gambled away like this. Another version of 2-20, thank you mam. When pensioners suss this out, they are too frail to fight and then they go to the big wigwam in the sky anyway.

I can’t wait for Pets-R-Us to come back from dead and give us a shining new IPO. Or SPAC if you are into newspeak.

“whoever is looking for something they do not normally purchase, they go to Amazon”

Why is that a bad thing? Isn’t it awesome for consumers?

Amazon has revolutionized shopping experience. Provided access to items that were not available locally. Saved trips to the mall and stores.

Provided a marketplace for small businesses.

Now for why people invest in unicorns, there are as many reasons as there are investors. Unless there is a good survey to find out, everything else is speculation.

“whoever is looking for something they do not normally purchase, they go to Amazon”

because they’re pretty good as a source for data. After you pick from there, don’t just buy it, use data you’ve gleaned to hunt down other sources.

You may have to go back and order it from Amazon anyway, but at least you’ve tried.

Retail includes groceries, gasoline, cars. Markets in which Amazon has tiny percentage if at all. If you look at stuff that is priced between $10 and $500 (aka mall retail) than Amazon has a much higher share so claiming that amazon has monopoly share in retail is right. Besides why would you look at total retail and not individual markets.

If DoorDash is trying to compete to force out its competitors, it’s not doing a very good job. The company overcharges its clients and rips off its poor drivers. Same for Uber, Lyft, and all the rest. Uber started out giving its drivers 80% of each fare. Drivers are now down to 40%, 30%, sometimes 20% of a fare, and that’s before auto expenses. WTF is the money going?

All this wild speculation is allowed/encouraged by our financial wizards to help mop up the trillions of excess currency they’ve printed.

That and the hope/prayer that tech will result in the next big thing for a productivity spike in our failing economy.

True, but most of these companies aren’t real tech companies at all.

Uber and Lyft are part of planned transportation where we will pay a subscription fee for transportation needs not owning a car more control over people

Ride-sharing is a great future where you will be able to pay a low subscription amount and have access to many types of vehicles. 90% of your rides will be a monopod. And it will bring clean, quality transportation to many countries that are poor (like India with 6% penetration).

But Uber and Lyft have built their brands on a two-way marketplace of drivers and riders. When drivers are replaced with autonomous cars, there will be a free-for-all of new competitors that can build scale regionally just as fast as Uber, with much lower prices. I think Uber and Lyft are terrible businesses, as they will have problems managing the conflict between drivers and autonomy.

GameTV,

From a pure physical efficiency perspective, I think rideshare only *really* provides a significant number boost when rides are literally *shared* (ie, car pooling, using optimized routing)…otherwise, Uber/Lyft are tech empowered taxi companies…where physical costs are not much reduced when the passenger is riding alone.

And note that Uber/Lyft have barely penetrated the commuter mkt…which likely accounts for 60%+ of all miles driven.

Basically, Uber/Lyft can’t make daily commutes cost effective unless riders…share.

I’ve said it before on this site, but the problem with Uber and Lyft is that each individual ride is not profitable. It’s not like Amazon, where they had to spend a ton on infrastructure and the distribution network. That’s all built out, but they don’t make money on rides.

I suspect that if they had to raise fares to what it actually costs, they would lose too much business.

Their mistake was keeping fares too low for too long. Now people have a skewed sense of what these rides should cost, and raising them will be a huge challenge.

All around the world, proper taxi companies are surviving and thriving against Uber et al. They can only survive in a city large enough to prevent the customer who was the victim of an unnoticed surge price being picked up by the same driver next week. In any smaller market, the locals all use the local taxi companies who refuse to rip off their clients in this manner. Surge pricing can only succeed when drivers do not feel they are part of the community they work in. That is, they are quite happy to rip off mugs they have no affinity with.

In the end, Uber/Lyft are just taxi services. And except for special situations, it will always cost less to drive yourself. The original ride-share model proved unworkable. There simply were not enough people wanting to car pool with a stranger for a nominal payment. Once this concept proved a failure, they should have liquidated.

“mopping up” indeed … as with a dirty proboscis!

These uh,’unicorns’ .. which I prefer to think of as pests, are as like copious Fed-laid ‘bot’ flies .. spreading nothing but economic Pestilence and Death wherever they alight!

Where’s the f’n can of Raided when you truly need it .. stuck in some neglected SEC cabinet???

What nonsense to say they’ve just printed. And it won’t be mopped up until they get some taxes to retire the paper. But since more and more money is becoming “untaxable”, lots of luck with that. I think the Fed may be able to go to their own digital currency during a crisis.

The state of the corprotocracy in the land of Absurdistan. This is all easily explained by the binary power model of governance.

There is a Cabalistic banking power in a coordinated dance with a slightly subordinate police power.

There is no independent judicial system or legislative power – that is a fantasy we were presented with at school.

The currency in which these corporations are (negatively) valued hasn’t been actual money for many decades. The declared national emergency(s) continue on. What people call “money” is emergency scrip.

Amazon was built on not paying sales tax. I wonder how Tesla TSLA would look among those cumulative loss graphs? Without the ill-deserved pollution tax credits?

Great article. Love the data.

All of these company’s business models are avoiding mandatory expenses legitimate businesses have to pay.

Airbnb – we are hotels that don’t have to pay hotel taxes or abide by health and safety laws.

Uber – we are a taxi company that doesn’t have to abide by taxi taxes or health and safety laws.

Amazon – as you said, didn’t have to pay sales taxes for a decade.

Etc.

Congress was slow passing a law requiring out-of-state sellers to pay sales tax (assuredly something to do with campaign contributions & the interstate commerce clause…).

Hardly.

It has always been if a business didn’t have a presence in a state, they don’t have to pay sales tax.

Still true today.

Amazon tried to play that all their warehouses, shipping centers and offices didn’t count because the were “re-sellers.”

They need to give mom and pop local retailers the same benefits Amazon had for ten years…..no sales tax.

That would help keep some of the profits locally instead of going to Bezo or the Walton family

You are 100% correct. If AMZN had to pay state sales taxes it would not have survived

And it literally hit a pit of gold with its AWS cloud storage business

But how easily defended is AWS in the long run, really?

Running cloud server farms (at least meat and potatoes ones) does not require rare genius that Amazon can monopolize.

Sure, the size of Amazon provides some pricing advantages but incremental cloud computing costs are pretty tiny to begin with.

If Amazon’s scale only shaves 1% off the incremental costs of Joe Blow’s Ye Olde Server Farm…the Joe Blows of the world are going to drive Amazon’s pricing power into the ground.

I don’t agree. That was true of ALL online retailers, and there’s only one Amazon. Meanwhile, ValueAmerica, Mwave, and many others have come and gone.

Actually for men’s clothing, I find Macy’s and Brooks Brothers web sites to be far superior to Amazon’s website.

Those pollution cutting tax credits have helped drive the 20% improvement in soy bean and maize productivity since 1999.

Maybe you don’t eat beef or tofu or drive a Tesla, but some of us appreciate those pollution cutting tax credits.

Great question on TSLA . I may have to dedicate some time to that

Amazon is absurdly overpriced but at least it has a cash cow (AWS) which is very profitable and maybe the building out of the network effect will really work, for them.

Uber, Lyft, Air BnB, and Door Dash are a reservation or Taxi dispatch service. Nothing revolutionary about that. Name brand recognition but no barriers to entry that I can see other than raising money.

Don’t see much difference in the rest of the group either.

CNBC had an article about the rideshares a few days ago. Having a hard time finding drivers since apparently, more of them have wised up to the low pay they were actually making. Article stated revenue share has decreased over time and many of them presumably can’t do the math to consider depreciation and maintenance costs of their car on their actual compensation.

Seems like the business model only works through a combination of low paying drivers and “investors” incinerating their cash. That’s how they undercut taxis. In a normal market, they would be a guaranteed lottery ticket selling the stock short to bankruptcy.

I think that something important is that these services, including Amazon, do provide is a better experience for the end user than previously. And that matters a lot today, which is why I believe these new entrants will be successful eventually (maybe after being acquired).

Augustus,

Mostly agree…but the rideshare companies *could* really improve bottom line physical efficiency via true ride *sharing* using computationally optimized routing and passenger matching.

Really good insights.

$23 billion in losses by a taxi ride app is incredible. Maybe they should start accepting Satoshi’s as payment?

You are being pretty charitable at that too.

“Yet the chart suggests that only one of these startups might be on its way to profitability: Pinterest…”

Yellen/Powell bucks looking for a place to die.

They will find these places, out the wazoo.

Amazon might not even have become AMAZON if it wasn’t for the ridiculously profitable Amazon Web Services. I am not convinced that the ‘growth at any cost, profits don’t matter’ brand of capitalism works unless you have a cost of capital that is essentially nil like Bexos has had access to.

The number and the market valuation of those large cap stocks which are losing money is by far and way the largest in history.

How about my favorite CHWY , an online pet food company with marginal earnings and a market cap of 30b.

Literally trillions will be lost when these stocks crash

I didnt realize Chewy had that valuation. Thanks for pointing it out. I will be looking at those financial statements and preparing for a short sale.

True technology companies are worth investing in when they are still losing money, but many of these companies are merely ecommerce sites or applications that can easily attract competition, or simply go out of usage with newer apps.

The key is to look at the true moat against competition. By the way, I think Tesla has about the weakest moat to competition of any “unicorn”. In Europe and China, the Tesla’s market share of EVs keeps getting smaller. Sure, they are still growing and will continue to grow as EVs grow, but they are a tiny player in the global auto business with massive competition coming from both established and new players. The things that are great about a Tesla car (acceleration, quiet ride, low center of gravity, no emissions, etc) are not unique to Tesla’s EV. Every new EV that hits the market will provide the same things. Tesla has maybe a small advantage in battery tech, or maybe not. But that advantage might be a 1K to 2K advantage per car, while other economies of scale and manufacturing prowess are not a Tesla advantage in the coming 5 years.

No don’t try to short anything.

Chewy….please don’t laugh, but we’ve been purchasing about $300+ a month from them since the pandemic started (mostly sacks of wild bird seed). What astounds me is that these very heavy items are shipped amazingly quickly, for free, over vast distances (from warehouses in Arizona, Nevada, Texas, Florida, etc.), to our doorstep in California. Pre-pandemic, most corporations would not ship bird seed; those that did, charged ridiculously high shipping fees.

MFG-‘ridiculously high shipping fees’, or avoiding a cause of marginal earnings?

TANSTAAFL.

may we all find a better day.

Yeah, I don’t get CHWY at all. At least the guy running it went to gamestop, a business already augured into the ground so he can’t do much worse with it.

I don’t buy much from Amazon, but they do a good job of retailing their products. I don’t use Uber, but can understand why they killed the traditional taxi business, they go anywhere and taxis don’t. Some of the others I don’t get, but I may not be the target customer.

Zillow is a good example of a platform getting worse over time. Most of the good features are being eliminated and it’s getting harder to use. They used to show the sale price of houses, now they don’t.

Isn’t Zillow selling house now?

That may be a reason they won’t show a sold price to the general public as usually a sales broker (RE agent) is only allowed to show sales comps to clients under contract.

Zillow still shows the sold price. I just checked and the first sold home I looked at it went back to 2000 and listed 4 sales prices through the years.

It may be you’re in an area where the data isn’t available, or maybe check your filters applied to the page.

They are getting worse since they started buying houses directly though. I notice they (or realtors?) play numbers games by sometimes having several entries for the same house in sold but not the ones for sale- making sales seem bigger.

Oh! You’re right, for one filter at least. just tried again using filter of “low to high” listings and the sale data disappeared. Then reappeared when I chose “high to low”. That’s interesting.

AND, unless you contract the map area it does not list the lower priced sales at all. Yep. It might become useless. Welp, that will drive buyers back to RE agents if that direction continues.

I think you just found some of the bugs they don’t even know about. This is worse than I previously thought.

I don’t buy any thing from Amazon anymore except an occasional book. I can’t stand Jeff Bazos and will not support an organization that is killing all the mom & pop businesses in the country. Same for Walmart. I don’t care if they are cheaper. I’m done with them. Same with Whole Foods which is owned by Amazon.

I hate Amazon for axing “Bosch”.

Swamp….Books should be bought from Thriftbooks. ??

Pet-Uber has zero presence in our (admittedly) rural area. Not surprising, given ‘digital divide’ and other longstanding rural invisibilities to the national population/infrastructure since the end of the REA. (Don’t care much about ridesharing, where, if you think about it, taxis were unregulated at their start as well, but eventually coming under regulation for various reasons-reasonable and reason’s everpresent handmaiden, human corruption. Uber/Lyft in CA had the economic input to political advertising in the last election to legally lock in their businesses as long as they can attract drivers who can’t initially, and fully, count their personal costs…).

may we all find a better day.

In NYC taxi owners made money, taxi drivers never did. The taxi service was limited mostly to Manhattan and the airports. If you were outside those boundaries, you were out of luck. The rest of the city used gypsy cabs and private car service (sort of uber like).

I have no sympathy for the taxi industry in NYC. I’m sure I lost it waiting for a cab in the Bronx.

Pet-so, plus ca change, plus ca meme chose…

may we all find a better day.

The Fed has bee stimulating the economy for 20 years. Grandma’s savings have somehow found their way into funding unicorns just like some predicted when it all started. US debt of $30T looks pretty manageable with total US wealth of $120T. It will not look so good if bubble bursts and wealth drops to $50T.

“US debt of $30T looks pretty manageable with total US wealth of $120T.”

The debt is especially manageable since they are effectively printing money to nullify a chunk ($8T and counting) of it as it sits dormant on the Fed’s balance sheet without the need to be serviced. And that $125T of paper wealth would be much less if we had market interest-rates on the $28T of debt without the Fed intervention.

Why didn’t previous generations run up huge debts and then print money to cancel it? Perhaps they understood in the long run, what is given by the printing press to some will be taken away by inflation for others including future generations.

Heard a theory today that house prices will force the Fed’s hand. 1) Young people going to get fed up they can’t buy a house 2). House prices are going to feed into higher rent calculations used in inflation calculations.

OS

That theory you heard is total bull s$it

1. The Fed doesn’t care whether young people can buy a home.

2. Rents will continue to lag way behind house prices.

The house next to me rents for $2,500/month. Tax assessed value $675K.

The majority of my portfolio is in AMZN, GOOGL & AMD. These allow me to sleep well at night. The thrill of a quick speculative profit is far outweighed by the pain inflicted by substantial overnight losses. New share offerings are a portfolio killer!

People used to say that about the Nifty Fifty. A lot of those companies aren’t around anymore.

Not to mention that the bigtech companies are ultimately still reliant on the credit bubble and Fed largesse. If random people and companies have less helicopter money to spend, that’s less for the tech companies.

Where are you pulling your valuations? I see on Yahoo Finance that the market cap of Compass is 4.99 billion.

Thanks. The Compass figure was a typo.

The craze will end. Shorting will be epic, but for now we have to wait. There’s no limit for madness.

I reckon all these ‘phenomina’ and others, such as Fracking, etc are all the result of an unprecedented period of incredibly low cost of capital. There are 2 ways to look at it :- 1) Is it a good thing for all the new modern businesses that have been created? 2) Are they truly viable businesses that can produce a positive return at the much higher cost of capital which has been the norm for all historical periods prior to the current ‘freak’ experience?

I liked Stockman’s article today on the hedge. Fed has ran the greatest monetary experiment in US history and the economy hardly grew, but the rich got richer and the very rich got a lot richer. Now financial assets hang on every word that comes out of Powell’s pie hole.

Some of these guys will get government bailouts. If Uber closes down is that a national security problem? If you can go two decades bleeding money maybe blood is overrated?

Ambrose-sad to say, blood has always (other than lip service) been subordinate, it’s just that the financial Ouroboros is now seriously consuming its tail…

may we all find a better day.

Someone should do an analysis on how much these companies are spending on services provided by Amazon, Google, Microsoft and Facebook. A lot of these unicorns run their tech stack on the cloud, so that means Amazon AWS, Google GCP, and/or Microsoft Azure. And for advertisement they obviously rely on those companies as well. In other words, these unicorns are joined with the big cloud companies at the hip, and when they start falling, the domino effect will be epic.

As long as investors are happy throwing their money into the bonfire though, nothing will change.

Good point. Investors also must consider the global corporate minimum tax that was agreed to by the G7. This will substantially increase tax rates on the foreign earnings of Big Tech from 3% to about 10-15%. Over 70% of earnings are reported to be foreign, so the future EPS streams are overvalued by about 10% right now. Throw in the impact of increased anti-trust enforcement, and higher interest rates, and you see a big problem for Big Tech earnings, made bigger by Big Tech valuations.

Then throw in the impact of a large general recession.

Disclosure: I have zero big tech in my portfolio.

Global corporate minimum tax = BS.

Another virtue signalling maneuver from Dems. In the end the tax dollars will find their way back to Big Tech somehow.

1) AMZN in distribution for one year.

2) Xi rule AMZN & TSLA. HSBC woke Ilan & Bezus every night. Both love space crafts, along with XI.

3) P&L : 13 out of 14 cos on the chart are trending up, losing money for years.

4) AMZN is trending down since year 9, but after 10 years, between year 5 and year 15, AMZN accumulated P&L is barely > 0, or about $300M.

5) Market cap : $1.8T (504M shares X $3,511), accumulated profit ; $300M,

or : 0.000166.

6) Share Holders Equity : $103B : $1,800B = 5.7%, better than BA & MCD.

I have a 34-year-old relative who makes $125k a year plus stock options (last year valued $75k) working from home with Uber in his pajamas.

How does he fit Uber into his pajamas?

Must be a euphemism…

Golden handcuffs. Options are amazing until tax time. Then the cycle begins again. You owe $50k so you sell options to pay this insane bill. Same problem next year but maybe bigger. Don’t get me wrong I would do it all over again. Was a member of WellPoint/Anthem in the early years and Loved/Hated the rewards

MiTurn- the stock options are the “secret sauce” of compensation.

1. let stock buybacks be legal again (in the ’80’s I think)

2. pay management with stocks/options

3. buy back enough stock to keep the stocks/options in the green

4. change executive compensation laws in 1993 to try to limit it, but it backfires- causing even more stock-based compensation

4. wash/rinse/repeat- stock market rises, management gets paid, stock market is levitated

This is probably the majority of the cause of the “bubble” in the stock market

Amazon continues to grow market share but its delivery model will never be profitable. The monthly prime subscription model in interesting but USPS, UPS Etc. will never attempt to replicate this model. Delivering unprofitable junk for free is a huge exploitable weakness not an asset IMO.

Current Inflation is the result of supply side borrowing costs increasing. The Fed continues to downplay the recent decoupling of Treasury yields and how it reflects that the Fed/Central Banks are starting to lose control of things.

I have heard a lot of warnings lately from the smartest people (Larry Summers, Noriel Rubini, Druckenmiller) that current easy policy has gone too far and is going to cause a big economic mess.

Larry Summers smartest people???????????

“Lately”? It made the mess a long time ago.

For those guys maybe it’s “lately” because it’s now so bad that their fear has overcome their greed. These guys were beneficiaries of the QE party.

Those of us who just got to watch the party through the window have been talking about kicking the can for a decade or more.

While reading this I literally ordered a tube of toothpaste on Amazon with the “swipe right” feature on the app. With Prime membership it will be here tomorrow, would have been today but it’s too late. I can’t recall the cost but I didn’t give it a moment’s thought.

If that’s not a trillion dollar idea I’m at a loss to imagine what could be possibly be.

Walter Ego. Costs matter. It’s nice that you find that valuable. It is not sustainable if there’s no profit. (which there isn’t)

My take away from this is that Amazon actually forced a change of habit and a way of doing business on the consumer. It took a relatively small market and, over a couple decades, had a major impact on not just how people buy, but how businesses are now expected to move products to consumers. This has had a profound impact on real estate, productivity, transportation, advertising, marketing, manufacture, etc. In short it impacts everyone.

I look at all those other “unicorns” and cannot see how they can create that kind of impact. Sure Uber and Lyft are a major change in ride sharing, but they’re not going to cause 60% of all trips made by individuals nationwide to be by such a service. I have yet to figure out what service Pinterest is supposed to provide. Wish is a shopping app, Twilio is a messaging app, Snowflake is a Cloud app, etc. I fail to see how any of these can impact society to the point where they will force a change of habit. Frankly, most of them will probably be overtaken by technology before they make a profit.

Correct me I am wrong , but are not people eating out more rather than having takeout.

And less takeout means less need for Doordash

From a Bloomberg article (Local Delivery Alternatives Bite Into DoorDash, Grubhub, and Uber):

“[Jon] Sewell started Chomp, a delivery service that now works with almost 200 restaurants in Iowa City and nearby Cedar Rapids. Restaurants pay commissions of 15%, and drivers earn an average of almost $20 an hour. After Chomp gained traction, friends in Fort Collins, Colo., asked for help setting up a similar service called Nosh. Last year, seeking to build on those successes, Sewell created LoCo Co-ops, a company that sells technology and know-how to restaurants interested in establishing delivery cooperatives. LoCo operates in Las Vegas, Omaha, and Knoxville, Tenn., with three more cities in the works. ‘There’s nothing that DoorDash, Grubhub, and Uber Eats do that can’t be replicated locally and operated at a much lower cost,’ Sewell says. ‘There’s no need to send all this money to a bunch of venture capital-backed firms in California and Chicago who managed to figure out how to get between restaurants and their customers.’

Pinterest is working on paid search for photos and pins. As it is now, you post a photo on Pinterest which then can be “pinned” to particular search terms. That photo or pin is then linked to a person’s blog post, Facebook page, Instagram post, YouTube video, etc. Paid search, much like the paid search on Google, will get higher placement on Pinterest.

Ok, I have to admit, I’m a bit confused by the charts above, I understand the meaning well enough. But the story doesn’t add up enough for me to quite understand. Let’s take AirBnB for example, I think that was founded in 2008/2009; so 13 years in existance.

If I look at the chart with AirBnB, it seems to imply 18 years with a cumulative loss of about $9B, is that correct? You have six dots there, which I assume represented six years of known financial data, presumably from AirBnB’s filings.

I get the message, but the charts are kind of hard for me to understand at least.

Since these companies seem to be able to sustain losses for decades, it might be possible to have a satisfying lifetime career at one. Just because the company never makes a profit doesn’t mean one’s salary checks don’t clear or the employee stock options are worthless. Stick around 25 or 30 years. Stuff your 401k and IRA. Exercise your options. Retire with a gold watch. What’s not to like? Even the investors make money. They just make it as capital gains rather than from dividends. As a bonus, the tax rate is lower.

Only old timers think that companies should turn a profit. Why should they? We’ve entered a new stage of capitalism and we should embrace it, not fight it.

Kale-so the trick now is having the ability to play musical chairs long enough to actually remain with a firm for ‘…25 or 30 years…’ ? (i know, sarc ‘on’).

may we all find a better day.

I don’t follow many of the stocks here but I do follow Okta and it seems every year they report impressively increased revenues but then net losses. That is what kept me away from Amazon in the early years.

Okta is in the secure login business. One of their features is a universal login. Accessing the universal login automatically gets you into the system’s apps. The concept behind Okta is to make sure you should have access (security aspect) but then make it easy once you’re in.

This might not sound like much, but if you’ve ever logged in to a corporate network it’s not uncommon to find yourself in a workspace offering several apps. You launch the apps from within the workspace and have to log in to each one. A system using single login is a blessing. It cuts through entering usernames and passwords.

When I used the hospital EMR I first logged into the hospital workspace. From there I logged into the EMR. What a PITA when you’re working at 3 different hospitals and you need all these logins. Single login was a blessing.

But then Okta realized this could be applied to external systems, not just an internal corporate environment. Adobe now uses Okta for customers of its Creative Cloud applications. Instead of signing in to each app, you sign in once. I use 2 Intuit apps. It would be nice to just login once. And Intuit has a significant set of business-related online products.

Opening up a new sales arena increases Okta’s growth potential. Estimates of the market for external services now run at $80 billion, whereas when Okta first IPO’d they were only looking at the internal side, estimated at $18 billion.

Otherwise I don’t see the excitement, unless there are barriers to entry.

The other name I recognize is Twilio. The CEO used to work in AWS. I don’t recall the source but they said the TWLO CEO was following the Bezos playbook. They didn’t elaborate but my reaction is it sure looks like the early Bezos playbook if you mean losing money for years. It looks like it won’t be profitable for another few years.

Yet TWLO is beloved of hedge funds. The last 13F showed one fund with almost $1B in shares that might have been over $1B before the recent sell-off. It’s also in 3 ARK funds. Shareholders include Morgan Stanley, Vanguard, Fidelity, and Blackrock.

TBH I think I do need to “learn to code” because I have no idea what some of these companies do or what makes one preferable over another.

This is the blurb on TWLO on Business Insider. I think I’m reading this correctly and have embedded a few comments.

Twilio, Inc. engages in the development of communications software, cloud-based platform, and services. Its platform consists of the following layers: engagement cloud, programmable communications cloud, and super network.

The engagement cloud software addresses use cases like account security and contact centers and is a set of Application Programming Interfaces (APIs) that handles the higher-level communication logic needed for nearly every type of customer engagement. [note overlap with Okta]

The Programmable communications cloud software is a set of APIs that enables developers to embed voice, messaging, and video capabilities into their applications. [You can add on messaging and media to existing legacy platforms]

The super network is a software layer that allows customers’ software to communicate with connected devices globally. [I have no idea what this means, unless they’re providing a remote app or maybe a universal login]

I don’t feel the magic but obviously others do.

And this is one of the easier ones to interpret. In the old days you’d look up a company and it would say “Ford Motor Company (F) mostly makes and sells cars and trucks. Some other stuff but mainly cars and trucks”.

I was in the middle of explaining modern APIs to you when the API that runs Wolf’s ads decided to reload my page. It was a beauty of an explanation too. Pity.

Delete the browsing history (all of it) in your browser. That will solve that problem.

Okta was founded in 2009 and not in its 20th year.

Okta is junk. They should be losing 100 trillion. Just coz Amazon figured out AWS (super useful infrastructure that devs love) doesn’t mean ANY of the these totally fake useless companies will ever make a dollar.

With so many financial wizard types recently predicting some very hard times as a result of the next big market downturn, it will be interesting to see just how many of these companies survive the next bear market.

I would think during times of extended economic hardship, the speculative appetite for funding these kinds of non-profitable ventures may quickly exhaust itself, or at the very least, become prohibitively expensive.

1) AMZN was founded 27 years ago, in 1994.

2) The chart cover only 10Y of accumulated P/L.

3) Add 17 more years, AMZN total P/L will be in the red.

4) AMZN is ==> “Service Merchandise” catalog warehouse online, RIP.

Micheal Engel,

Amazon started making a profit in its 10th year. By its 15th year, it had earned back all its prior losses, and therefore the cumulative losses in year 15 fell to zero, and since then Amazon made lots of money, and it now has cumulative profits, not losses.

When a bird in the hand is worth the same as the bird in the bush, you can afford to go empty-handed for a long time.

Can we stop calling them “tech stocks” and call them what they really are: Quasi-governmental surveillance and propaganda businesses.

QGSPB stonks

This is not a market view but a small money club. Buyouts happen not for strategy but for pensions. My prediction for snowflake is a giant sinkhole will appear in the centre. This collapse will instigate change in personal computer vs human interaction.

Oh, my goodness, what a great group of Financial Snowflakes that would be perfect to put into a double short ETF!! We will call it the Hot Air ETF, Losses to the Moon ETF, or the Amazon Wannabees ETF, copyright permission applied for.

The even bigger question is when did the Venture Capitalists and other start-up initial funders, pull out their money for gigantic gains??!! Probably, the vast majority of Tier One and Tier Two financing was recovered the day these turkeys went public. The greater fool theory in more than splendid fashion.

When the U.S. economy coughs up a giant hairball in the months ahead, this group of ridiculous losers will be one of the most profitable short trades in the universe. How many U.S. banks, major and regional, have their butts on the line with this group of total losers. We will soon know.