Are Americans finally figuring it out as they’re paying down their credit cards by record amounts? So far, $25 billion a year in lost interest income for the banks!

By Wolf Richter for WOLF STREET.

There has been a lot of commotion in banking and at the Fed about Americans having the temerity to pay down their credit cards – practically an abuse of stimulus, so to speak. In the five quarters since Q4 2019, Americans have paid down their credit card balances by $157 billion. “One of the most confounding changes in debt balances,” the New York Fed called it. Credit cards are immensely profitable for banks. The Fed has been repressing interest rates with all its might, but credit card interest has remained astonishingly high.

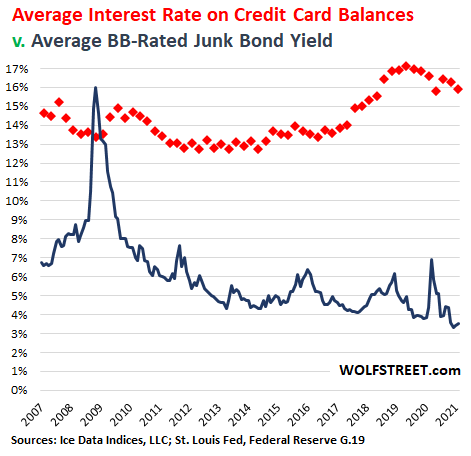

According to the most recent data from the Federal Reserve, banks charged on average 15.9% interest on credit card balances that were actually assessed interest. This is down 1.2 percentage points from the record in May 2019 (17.1%), but way above historic levels (red squares in the chart below).

By comparison, the average yield of BB-rated corporate bonds, the upper end of the junk-bond range (my cheat sheet for corporate credit ratings) has dropped to a record low of 3.2% in February, according to the ICE BofA BB US High Yield Index, and has barely ticked up since then (black line). In terms of making money off consumers that are in debt and that have run out of options, there is nothing like it out there:

Based on the average interest rate charged on credit card balances of 15.9%, that pay-down of $157 billion in credit card balances that consumers somehow engineered represents $25 billion a year in lost interest income for the banks!

That’s why banks are trying so hard to get consumers to borrow on their credit cards again. And that’s why the New York Fed, which is owned by the financial institutions in its district, finds that pay-down so “confounding.” We’re talking about $25 billion a year in banking income here.

The bank gets a fee from the merchant each time a consumer buys something with a credit card. The bank also collects interest from those consumers that carry balances on their credit cards and don’t pay them off every month. It’s this second part of the equation we’re talking about here.

The interest rate can be over 30% for consumers that cannot pay off their credit cards. If they had enough cash to pay off their credit cards at this rate, they would. But they’re stuck. Consumers that pay off their credit cards every month are often offered lower interest rates, but they don’t need to borrow on their credit cards. Banks also offer teaser rates of 0%, and then after a set period – after the consumer charged up the credit card and can no longer pay it off and is thereby stuck – the teaser rate switches to 29.9%.

Call it the credit card hustle.

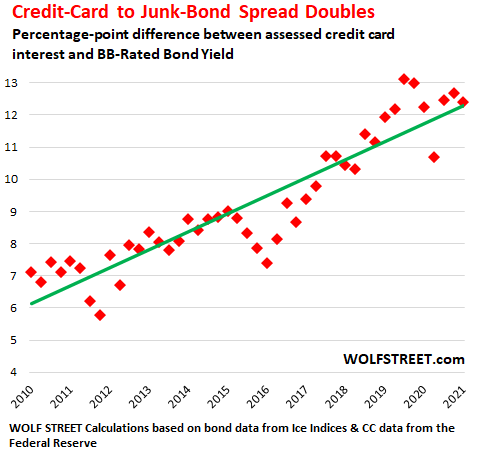

In the world of debt, “spreads” measure investor appetite for credit risk. The spread can be measured as the difference in yield between a category of corporate bonds, such as A-rated investment-grade bonds (relatively small risk of default) and Treasury securities of equivalent maturity (near-zero risk of default because the Fed can print the government out of trouble).

These spreads between higher-risk debts and lower-risk debts have narrowed and currently are near record lows. The exception is credit card interest.

The spread between credit card interest (high-risk consumer debt) and BB-rated junk bond yields (high-risk corporate debt) has widened, and over the past decade has doubled, from a difference of around 6 percentage points on average in 2010/2011 to over 12 percentage points currently.

The average BB-rated bond yield has dropped from around 7% in 2010 to 3.3% on average in early 2021. The average credit cards interest rate on balances with assessed interest has risen over the same period from around 14% on average to 16%. Hence the widening spread:

Credit cards have been carefully shielded from the Fed’s interest rate repression. That profit center is just too important for the banks.

Using a credit card to get 2% cash back or accumulate frequent flyer miles or whatever is a smart thing to do, as long as you don’t have to pay interest on the balance.

But paying off those credit cards and not having to pay the usurious interest rates is a vastly smarter thing to do. Maybe Americans are finally getting smart about the credit card hustle – hence the $157 billion pay-down.

Credit card interest will always be higher than mortgage interest because credit card debt is unsecured debt, while mortgages are secured debt. So for banks, credit cards entail bigger risks, and interest needs to make up for that risk. But not the kind of interest being charged by banks for credit cards.

The credit card hustle entails this element: When a bank charges 25% interest on a credit card, the high interest expense increases the risk of default because the borrower is unlikely to be able to pay for the interest. Charging 4% interest would cut the default risk by a huge amount. But that wouldn’t be part of the credit card hustle.

The irony is that the Fed has tried hard to repress yields on corporate debt. It is furiously repressing mortgage rates, including by buying mortgage-backed securities. It has forced down the interest rates that all types of borrowers have to pay. The Fed has moved heaven and earth to wipe out the income streams for savers and bond investors.

But at the same time, the Fed is flagellating its arms to get Americans to borrow more on their credit cards and pay this usurious interest. And instead of applying pressure to lower the interest rates banks charge on credit cards, the Fed gets upset when consumers are starting to react to the credit card hustle by paying down the amounts they owe. But for now the Fed is assuming that this is just temporary.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I’ve been thinking it’s about time the Fed starts up a CBBS purchasing program. No, not Central Bank Bull Shiet, I’m talking Credit Balance Backed Securities!

They know some folks will struggle within the new framework of permanent transitory inflation. So by reducing credit card interest rates, they’ll send a strong message of support to working families. They’ll also swallow risk on behalf of the banks.

Rejoice, the Fed’s enormous generosity is rivaled only by their balance sheet!

Credit card receivables have been securitized since the 1980’s. And auto loans too. The are called ABS, asset backed securities.

A used Tesla is now an appreciating asset, because the new self-driving software can be uploaded.

Doesn’t Tesla charge $12k for that?

2008 displayed the fragility of those backed securities.

I miss the old days…free balance transfer on CC, with no interest for 1 year on transferred balance.

Took out a HELOC and put cash in bank at 2-3% (it was 2003 or so, apologies I can’t fully remember), approved for 3 CCs with 10-20k each, no interest for 1 year on transferred balance. Pointed CCs at HELOC, sucked it all up, paid minimum without charging anything on those cards, made interest on cash at ING…all online. Autopay set up….

Got a call, and into a conversation with one of the CC representatives when they were asking if I intended to charge any NEW items…to which I said, “no”. Evidently there’s a name for folks like me in the CC industry…”freerider”. ..which I take as a compliment from an industry that shouldn’t actually exist (ability to create credit/currency is a Federal Govt charter, etc.).

Yep. There was a credit card bubble back in the 1990’s. When I was living in the UK, some clowns, Barclays probably, launched a totally new and revolutionary credit card with a holographic fish on it, where the incentive for switching was that they would pay off 20% of the credit card debt one tranferred to their bright, shiny and new card.

I renovated part of the house on 3 credit cards, dumped all the balances on them, got the 20% rebate, then paid it off the month after. They lost thousands just on little me.

LOL @ fajensen, what did they think would happen? That’s classic.

FaJensen, Good for you!!

Problem is, for each FaJensen, there are 10,000 morons who run the card up and then can’t pay the usury (it used to be called “juice”) on their balances.

Same now. For the 157b pay down, there are others running up CC balances they won’t be able to pay.

Decades of this have gone into the history books. Books no one wants to read.

And the beat goes on….

I have 2 monthly auto pays on CC, plus every 6mo truck ins, and yearly CSAA. So they stay off my back. Plus I use it every year or two. But I have noticed my nearby branch office has shrunk, the lines are long, and twice recently the ATM’s were all down and the branch was closed….on a “business day”. Brother said ATM’s were all kaput at the MAIN downtown branch after he walked 2mi to get there.

0.013% is bad enough on my “just in case” local money CD, but they are really chipping away at us.

At what point does this usury destroy itself?…..I thought several years ago but inflation may sound its epitaph unless the interest increases..my son

I am not sure that the CC are a form of usury at 15 or even 30%.

100% would be an obvious abuse though.

That’s an easy but costly micro/mini credit for consumers. Look at it as a nice luxury service. Better to have this option than not.

Now, every action has consequencies.

It would be Ok for me if the CC ads included the warning “CC are bad for your financial health”. Like alcohol or tabac.

15% in .5% world is usury. That is undeniable. Crime is something that persists until people refuse to tolerate it .

Actually, as a wage earner, I feel living in 50% world.

Different forms of taxation hit the company revenues, then personal income, then personal consumption (VAT), making 15% CC “tax” psychologically acceptable, at least for me.

There is now law that prohibits the luxury consumption, truck driving, CC usage and other non-essential spending.

Crime is something that persists until people refuse to tolerate it . It works both ways:

My grandfather died without an estate, since he had handed us, or transferred over, everything of value.

He made sure to run up his credit cards to the max to buy us building materials, tools that we needed, drilled a well, etc.

The debt died with him.

These smiling jackals hand out free pizza a college to get “kids” hooked on interest at incredible rates. That’s their goal. They’re not the worst (pay day and title loans, anybody?) but it’s still pretty sick.

The upside world.

The Fed has destroyed middle class savers by robbing them of trillions of interest payments on their savings with ZIRP with inflation at least at 4%.

And then worries about credit card debt reduction…

“the Fed gets upset when consumers are starting to react to the credit card hustle by paying down the amounts they owe. But for now the Fed is assuming that this is just temporary.”

They brought it upon themselves with the bankruptcy reform in 2005 made it much more difficult for consumers to discharge debt.

Well, that assumes that the savers are somehow entitled to risk-free return, above inflation. Is there a rule or something.

Id be happy to get interest at the rate.of inflation personally. Here in the UK you used to be able save in a bond that paid RPI +.1%. this was closed 15 years ago to new customers and the rate for those with money invested is now CPI + 0.01%.

In the US there are these ‘inflation protected’ gov bonds. Not an expert on these. Of course the problem here is that the gov tells you what the official rate of inflation is.

DOWNSIZE MORE!

There is a lot of crap ya don’t need. A dollar not spent is “almost” 100% return on your money…and drops every year:(

Still have 15 t-shirts from when the fast gas station sold 3-4 “rejects” for $10, about ten years ago..(hard to get a large, though, they seem to go fast)..and 2 pair Dickeys cheap jeans on sale from same time.

Signature Select instant coffee goes on sale…savoring a cup right now. What’s a Latte?

“…Is there a rule or something?”

Capital is really solidified labor. If you let somebody else use it, you receive a compensation.

In a rational universe, if you supply your labor, you get paid wages. If you supply the result of your labor in the form of capital, you get paid interest.

It is frightening to realize that we now live in a matrix where people seriously ask these kinds of questions.

Buy Ford bond, or Tesla bond, or Apple bond, and get your interest. Or start a business with your capital.

Why do you deserve risk-free interest? And above inflation?

Jos Oskam, Yes it is frightening.

Perhaps more frightening is a closed NJ Deli whose best revenue year was less than $40,000, goes public and attracts $100m in capital investment. I’d love to see the list of the new stockholders. Talk about a “moron list”….

The only thing to top that would be if they funded their investments on a 29% credit card!!

Oh, reminds me, you can also fund your on line betting account using your credit cards. What opportunity!!!

Andy,

‘deserves’? ‘entitled’?

In real world, real economy nobody deserves anything for free. But everyone deserves what is rightfully theirs, otherwise it’s robbery.

Capital has a cost and a price. The fed has artificially suppressed that for years. If someone wants to start or run a business they need capital (Apple bonds, Ford bonds as you say).

If the markets were functioning properly, that capital would be earning way more than what they are currently.

Fed has been creating capital out of thin air and making it available for near zero interest rate. The capital (savings) one has worked hard for has lost all its value and importance because the Fed can print as much of that as it wishes at no cost.

Do you see the robbery now?

P.S. savings are no different than bonds. Instead of lending directly to Ford, you are now lending to your bank which in turn will lend to Ford.

Follow up.

Capital has a cost – usually in the form of years of hard work, risks, discipline.

Its price, like anything else in the free market, gets determined by supply vs demand.

When someone needs capital – to start a business, to buy a car, to purchase a house – they borrow capital and pay the price for that capital in the form of interest.

When supply is low interest is high and vice versa in a free world.

Fed has interfered with this free market mechanism. It costs zero for the Fed to create capital, thanks to the Congress. Fed has flooded the market with this zero cost, near zero priced capital.

It has robbed the savers from the true price of their savings (capital).

Rule, guarantee? No. Reasonable possibility, in a sane economic world absolutely.

When central banks destroy the time value of money and interest from savings is suppressed, it thus discourages savings in ‘relatively’ risk-free investment vehicles.

As a consequence, in a desperate search for real rate of return above inflation, it encourages a shift from solid investments to speculation in riskier assets like stocks and any other speculative ‘assets’ du jour like crypto, housing, NFT, SPAC, etc.

So here we are today, in the ‘Everything Bubble’ brought to you by the Fed.

“Is there a rule or something”

As opposed to a rotted out, incompetent Government covering up its manifold policy failures by confiscating the earning power of private savings via unvoted upon money printing?

Sh*t yes there is a rule…the Fifth Amendment’s Takings Clause.

andy…

When did the Lender become slave to the borrower?

Its like you are renting an apartment, and you are wondering why the guy who owns the apartment building should get anything.

For the 20th Century until 2009, Fed Funds equaled or exceeded inflation. That is the financial history…..you use my money for something, I get paid.

The Fed works for the banks. Not you and I.

Concur, and they’re predatory too. Both of ’em.

The Fed also seems partnered with the Treasury (with a fake dealer buffer)….and bent on ruining the currency to assuage the debt load and pump GDP numbers.

2banana…

Have Fed Funds EVER been 4% below inflation? And the Fed sits on their hands as they buy MBSs ..30 yr….also at below current inflation? Ever happen? The Fed removes any historically fair return on money. They have turned Lender slave to Borrower.

This Fed is off the effing rails.

Notice the Fed wishing to help Main Street…so they press down interest rates that pump housing and stocks….but credit card balance interest rates were untouched. IF the Fed had the power (they seem to write their own powers) , lowering CC balance rates would have helped Main Street. Maybe having a fair return on savings also……imagine that!

Transitory

2banana..

“The Fed has destroyed middle class savers by robbing them of trillions of interest payments on their savings with ZIRP with inflation at least at 4%.”

And a Fed Chairman stands at the podium and declares “we are honoring our stable prices mandate” and “we are promoting a 2-2.5% inflation rate”.

HOW CAN THAT BE?

Then it runs to 4% or more and they deny it is happening. WTF

That was uncalled for.

My own 1.5% cash back CC was bought out by one of the mega banks last year, and they dropped it to about 0.8% cash back by making a huge list of complicated rules that makes you choose categories, and other children’s games. I switched to a 2% cash back card, and continue to be a “deadbeat” by paying it off monthly. If you want to win against the banking cartel, take half of their CC transaction fees via cash back (not “stuff” discounts) and never carry a balance. The banks promote inequality, like the fed, through taking advantage of those with the greatest financial needs. I am very excited that people are paying off their CCs via stimmy checks, so good for society, society!

Speaking of our phychopath Fed, billionaire Stan Druckenmiller- perhaps the most successful investor of all times, made the following comment recently at the US Marshall School of Business video (search it…this is bad news for the Fed as even the richest billionaires are shouting from the roof-tops that the Fed is screwing the poor and middle class, and enriching the billionaires at the expense of everyone else):

“I don’t think there has been a greater engine of inequality than the Federal Reserve Bank of the United States”.

The credit card companies still win.

They make 2-3% on every purchase no matter what.

In smaller grocery stores, I get 5-10% discount, when paid in cash. You have to ask for it though.

That’s good to know, as I like to pay cash too. Also, my little local supermarket owns the gas station next to it and they have a membership deal. I get a discount on my fuel purchase by buying my groceries through them. And they’re competitive pricewise regardless — for groceries and for fuel.

I feel like a winner every time I shop there!

“In smaller grocery stores, I get 5-10% discount, when paid in cash.”

That is win-win for the smaller retailer and consumer.

Besides credit card interest revenues, banks receive an appreciable income off credit card use from card interchange fees– which is a payment from retailer to banks for every retail transaction.

Although credit card users never see this fee on CC receipts, it indirectly costs them because retailer has to account for this expense in pricing goods/services.

Better than 12-25% in interest though. I’m sure that everyone reading this understands that.

I don’t begrudge them a few percent, it’s a nice convenience. It’s not like cash is free, it’s heavy, you have to lock it up, it makes a business a target for robbery, you have to hire armored car services, etc. All the marijuana businesses in Colorado would _love_ to be able to pay a few percent to a credit card company to not have to handle cash (though I’m sure the ATMs they put in those stores make them some nice bonus income).

There’s dozens of websites that will give you free advice on how to manage credit cards. NerdWallet, ThePointsGuy, all the FIRE stuff, freaking Dave Ramsey. Just like in 1990, people still took up smoking even though everyone knew it was bad for you. When offered a choice, some people will make the wrong one.

The rich guys are running scared. They can see the poor are no longer willing to sacrifice their sons to protect their assets.

I don’t think it’s that. I think Druckenmiller genuinely believes this level of wealth disparity to be dangerous to a society.

The example I use is, “Would you rather be middle class in a safe suburb of Columbus, Ohio, or would you rather be super rich in a compound with 15 foot walls in Caracas, where you can’t go for a walk at night without being worried you’ll be kidnapped?”

Don’t the rich have their own armies (private security & Police) to protect their interests? Moreover, most people are priced out of wealthy neighborhoods by design.

Modern, every stable middle class society always had “wealthier” neighborhoods.

That’s a far cry from the super rich and the poor dichotomy the Fed is creating.

Not a few Roman emperors were killed by their own guards.

The wealth disparity is dangerous…and the Fed policies sold as helping the economy merely helps real estate and stocks.

The ensuing inflation will be the final straw….and the way this govt works, I would guess they will send out “inflation compensation checks.”

It is undeniable that a certain strata has become very wealthy due to Fed policies, policies that have never been seen before.

And it is also true that the federal govt is sending out money, for free, to the other “strata” to keep them happy.

Is this how France was in 1792? It seems familiar.

This is leading to upheaval that will expand far the monetary. It’s gonna be really bumpy for the next decade.

I feel bad for the Millenials and the Gen Z who will have to live through this.

Petunia-well said. History is rife with examples of nations that too-long ignored/embraced wealth disparity finding their populations reaching a point of asking: ‘…why should i soldier???…’ (advent now of drone/slaughterbot warfare notwithstanding, it will still require a person with a rifle to hold ground…).

“…and it’s Tommy this, and Tommy that, and ‘throw him out, the lout! But he’s the ‘hero of the nation’ when the guns begin to shoot…” – Kipling.

He has every right to be concerned. As the middle class gets gutted, the masses are going to want heads. We will end up with a situation not unlike pre Bolshevik Russia or post Kaiser Germany.

While the J team might manage their way through with stimulus and endless printing, their successors won’t be so lucky.

Never going to happen. The US ruling class has learned from history and they won’t repeat the French or Russian revolutions. They killed off the unions and the rest of the “commies” in the 60’s and 70’s and their extremely well oiled propaganda machine, which starts working on its subjects in kindergarten and carries on until their untimely deaths due to overconsumption of corn-syrup and opioids will ensure that no resistance is forthcoming. The “consumers” won’t rebel until there is nothing left to consume by which time the billionaires will have left the building.

Best to keep some perspective. The vast majority of the population has never taken opiods, and the actual proportion of people who consume mainstream media and believe it is decreasing rapidly. Rebellion doesn’t just mean marching in the streets, and indeed there isn’t much point if your ‘street’ is a rural road in central Montana. It can also mean dropping out of government-regulated society, and there is a lot more of this than either the government or the media like to admit.

Historically-speaking, billionaires eventually get killed by their own security.

The uber-rich always lose in a complete collapse, essentially because they are no longer any use. The latest archeology from post-Roman Britain is interesting. In the 40 years after the Romans withdrew troops, funding, and taxes (407AD), 100% of villas became derelict, money in circulation went to zero (100% barter), and all towns and cities became unoccupied. We don’t know exactly when this happened as writing stopped also, as did pottery manufacture and coin minting, so all precise dating artifacts ceased.

Total bullshit my kids how there getting bungholled and have armed up there pissed off

@Ron What? Not using punctuation is one thing but I can’t even string this one together. It’s like Michael Engel minus list and acronyms.

Taking away the ability to save oneself to some sort of financial stability is criminal, IMO. The FED ruined the middle class and those attempting to elevate themselves to that class.

Saving was how people got ahead.

Not desperation investing, yield chasing, leveraging risks.

Once the saver got a foot hold, out of poverty, then came the investments, the house, etc.

The Fed ruined this noble and frugal route to financial stability by taking away savings rates.

Indeed, in the history of countries or even enterprises, you know that the times are tough when the upper class starts to care about the lower class…

Care about = scared of ?

“Care about” means value something fairly.

Total not caring could bring such improbable scenario:

Imagine an aircraft taking off. Inside, a costkiller convinces the pilots and the passengers that the aircraft wheels are an unnessessary weight that should be thrown instantly into the open air to save some fuel.

Under everybody’s cheering, the wheels are detached from the plane and effectively thrown away.

Several minutes later the costkiller uses his personal parachute to quit the aircraft.

Nobody thinks about the landing to come.

You’re not a “deadbeat”. You’re a “freerider”. We buy everything from sheds to tofu via Amazon and get 5% back. That’s $1K – $2K per year. Chase stinks, but this is too fun to pass up. My wife likes to redeem it on massive quantities of toilet paper and paper towels. We’re prepared for the next pandemic.

Someone might suggest a credit card debt forgiveness program. Cities and states might beg Washington for municipal tax free bond forgiveness. Homeowners will want their mortgages forgiven.

HELOC loan rates are about 3 – 12% based on one’s credit rating. Someone without long term debt and always paying off credit cards every month might qualify for the lower rates, but does not need to borrow.

There has always been a credit card debt forgiveness. It is called bankruptcy or default on CC debt.

Of course, a default will negatively affect your credit rating for a number of years. Then you can start fresh again on CC binging.

There is a video of Cracked that explains it all. Is called “Why Credit Cards Are A Scam – Honest Ads” Look for it in YouTube.

With ‘Roger?’ Some of the best, most honest commentary on the internet (they’ve done quite a few).

Timely article and as usual great piece Wolf. Guilty of over using my credit card over the past several years and stopped paying them off monthly. Got serious about getting back to frugality mid 2020. Now got a new job and have been tucking every spare dollar to get back to zero debt from the credit card cartel. At times your articles seem to be directly tuned to my particular situation. Power to the people who are already CC debt free

Wolf,

Is it possible to segregate the CC payoffs by state/region. I bring it up because in the southern bible belt, there has been a real push by religious institutions to encourage congregations to reject the use of debt. It would be interesting to see if the CC pay downs correlate to this trend.

Petunia, My sister in law who is a Baptist living in Southern California,

told me recently that they owe their financial health to their pastor there who told them to pay off their credit cards, something they should have figured out for themselves. I had an eye-opening experience when I retired and paid off my mortgage and all my credit cards and debt. The officer at Citibank which I used couldn’t understand why I wouldn’t refi my house with her bank, they all tried talking to me there but I was adamant. Why would I do such a thing at 65, and then owe interest on it again? They were also paying me 6% on a jumbo CD at that time, which is what I believe caused her to snap, screaming at me in the lobby that they were losing money on me! I had figured out their system and won, until the CD rates fell. And just outside the door in the employee parking lot, their Mercedes were all lined up in a row.

book……”Where Are the Customer’s Yacht’s”…..do a search for the book on Amazon….original book will come up…..and numerous other books reinterpreting the book……a classic that passes the “test of time”…….poignant, with some humor on the perspective of “selling of investment advice on Wall Street”…original book is is dated for that era, but the lessons are still there…..Warren Buffet and Tony Robbins have recommended it

================

Two simple rules to appy

1….GET RID OF THE DEBT

2…REDUCE YOUR MONTHLY EXPENSES

Sometime in my life I heard a (probably Zen) saying: “Happiness is freedom from want.” In our consumption-driven society it appears many/most interpret that to mean “If I have enough money to buy anything I want, I’ll be happy.” I took it to mean “To be happy, want less.” For the last week I’ve been helping out friends who farm for us bail hay; it’s boring, sometimes grueling work but I’ve had to learn a new skill–a 15 year-old kid is better at it than me–and it offers great satisfaction in doing something meaningful with my time (and they pay a little to boot).

3. Use grammar when communicating to showcase your primary education for better job prospects.

“screaming at me in the lobby that they were losing money on me!”

I hope you closed your account.

I always thought that in America, we thought happiness was freedom from tyranny.

It seems as if we are now willing to sell our souls and our liberty and sovereignty, and accept tyranny, to acquire a few bobbles and trinkets…

As a society, we have become a incredibly corrupt and unethical, and our country is disintegrating as a result.

Great to see Americans fighting back from being abused by these credit card scams. I don’t imagine when these stimulus programs were created that they imagined people would actually use it for something for their real financial health

Excellent article.

1) On average banks credit card charge is 15.9%. That’s on average.

2) The good and the ugly pay : 0%. The not bad enough pay : 25%- 30%.

3) Credit cards balances fell the most due to the stimulus support. 4)According to JPM the c/c sector have some problems.

5) SF & Houston office towers are deflating. Malls and shopping centers also have a chronic disease. Small businesses have new problems and high tech labs and fabs are being blown up every night.

6) The Fed accumulate $8T asset to provide o/n collateral in the next recession.

“On average banks credit card charge is 15.9%.”

Remember when usury was anything over 3%? And to think that some credit cards charge up to 25%!

I wouldn’t make an unsecured loan to someone I don’t know for 15.9%.

I would and there are more who do.

Check out peer-to-peer lending programs like lendingclub.com and prosper.com. Not an investment advice. Please do your own due diligence.

Readers with credit card balance might want to refinance with them and potentially get a lower rate.

How about 29%.

Haha tall about unintended consequences. The FED is like this idiot uncle that can’t do anything right, maybe the next thing they need to try is experimental mind control. How else can you make sure people will only spend with their stimulus and take out more debt and not pay down insane interest rates credit card?

Isn’t that where central bank digital currency comes in? You’ll lose your digital currency unless you spend it in a timely manner.

Pretty good article by Hussman that only thing holding up markets is belief in the Fed. That’s a sad state of affairs. It gives you asset prices staying in the 99 percentile and monetization of debt. I am betting there will be a panic sometime soon as people respond to inflation expectations.

The black swan…

and that will make the Fed cut rates to zero.

Wait….we are already there. Why would rates be zero at record high stock and housing prices?

The Fed and central bankers have set the table for a disaster.

All the “happy buttons” are pushed when there is no need. There is a need for balance and restraint, and they are nowhere to be found.

I’ve been getting CC offers by the boatload the past few weeks, including the prestigious Black cards and 100,000 bonus-point offers. Credit score has only gone up a few points recently—crazy!

Take the offerings. One might need them later and when the need is there, nothing will be offered! You should definitely go for that black card.

I find it omnious that, in Sweden, they are pushing hard to get everyone to use what I call “Swedish Credit Cards”, which are just debit cards in drag and totally stupid, no effing way I will pay a hotel in Sicily or Russia with a debit card and getting stuck with the inevitable fraud! It is bug-out time!!

Do people have a choise in Sweden with access to cash restricted ? In addition lot of companies do not accept cash over there. And you pay public transport using cash, not even the subway.

correction: You can’t pay public transport using cash, not even the subway.

I lock all my credit reports at the big 3 to protect against identity theft. A nice side effect was that I no longer get the stupid credit offers.

Brenda- get one card a year, use the card enough to meet their minimum spend, use their free bonus points then close the card before the first annual fee hits. Free money and the easiest and best revenge against big banks.

No money for credit cards when your tryin to buy a house these days.

If you believe the home price to rent chart Wolf showed last week it seems like it’s the right time to rent and not buy.

Jen smart don’t buy at top of market save buy a fixer upper go on u tube build equity rinse repeat worked for me like climbing a ladder better house each time hire a title company sell your own house u just earned 7% will end up well off get off your lazy ass

Is the Fed actually owned by private banks? Do you mean that literally or effectively? I ask because the folks at Naked Capitalism are insistent the Fed is not owned privately, not private, not owned by banks, and is a public institution and ought to be treated as such. Who pays Jerome’s salary? Maybe that’s a starter. For example, Effectively, all of Washington government is privately owned and operated. But legally it’s not, it’s a public institution.

timbers,

The 12 regional Federal Reserve Banks (such as the New York Fed) are corporations whose shares are owned by the financial institutions in their districts, and their employees, such NY Fed president and FOMC vice chair Williams, are private sector employees. These federal reserve banks pay a statutory dividend to the banks that own them. The Federal Reserve Board of Governors is a federal agency, and its employees, such as Powell, are federal employees. This is explained everywhere, including in Wikipedia and on the Fed’s own website. If anyone tells you otherwise, they’re fabricating stuff or they’re just ignorant.

Employees typically answer to the employer.

Who does Powell answer to?

Prearranged questions at hearings dont count.

Treasury Secretary and the president.

The federal reserve is privately owned just like Federal Express

The tl;dr answer is that the Fed says it is a “public” institution when it wants to expand its powers beyond their legal limits by doing things such as bailing out failing megabanks. It is a “private” institution when you ask simple and straightforward questions such as, “Exactly how much money has been loaned or guaranteed to each megabank?”, and it does not want to answer the questions.

China once did an emergency census to count the number of people who needed relief from a massive river flood and discovered that the number of ‘people’ who claimed they needed ‘free’ money vastly exceeded the number of people living there who were recorded by the tax collector in the last regular census.

An elderly black gentleman was once asked the classic philosophical question, “Is the glass half empty or half full?”. He thought about it for a moment and replied, “Are you drinking, or are you pouring?”

He gave a better answer than most “Doctors of Philosophy”, i.e. Ph. D. recipients :)

Just amazing how broken the system is when cc company can charge average of 15% interest and as high as 30% interest rate when my high yield savings account just lowered it to 0.5% interest last week. How this is not being call for it is, loan sharking is just insane. I get it, it’s not secured loans but geez, that big of a spread even for some of the higher tier cc is shouldn’t be something the general public should tolerate but here we are..

.5%$ is pretty good. I’m getting .08% on my MM savings at Wells Fargo, Wolf’s favorite bank.

Good for them. For once the middle class gets to give the banks the middle finger.

I have a feeling however, Americans will quickly return to their old ways once the economy reopens.

sadly they will have no other choice. Because the paychecks they get will not be enough to cover all their living expenses hence they take on cc debt to cover the rest. That’s why banks call them “revolvers” and milk them as if they are not poor enough. There is a video on youtube where Jamie Dimon is humiliated by a congress-lady that I think everyone should watch. “Congresswoman Katie Porter grills billionaire CEO over pay disparity at JP Morgan”.

In most of Texas, it’s all open.

We went to a local steak house Saturday night to buy my daughter and husband their 3rd anniversary dinner. The place was packed and the wait (even with our reservation) was 30 minutes. Credit cards flashed everywhere in that establishment. All the restaurants around here were jammed.

MB, I think you are right.

You’re contributing to the killing of a lot of animals eating all that steak.

“Reopens,” as though it weren’t already open. Try finding a place to park at the mall.

You probably all know the saying: “the cure for high prices, is high prices”.

The same goes for interest rates.

That’s all true…in a free market.

Are we in a free market?

The Fed has subverted the fundamental of a free market….

supply/demand price discovery.

They create FAKE demand for MBSs and Treasuries…

and all else is skewed..

For those who go online there has been, over the last 2 years, a substantial

increase in the 20-30 year age group who log on to recordings of “The Dave Ramsey Show”. And, consistently ,they hammer home the advice that the way to get financial security is to pay off your debts asap, run a tight budget, and invest the surplus, and slowly accrue capital to the point that

you can live off a 4% drawdown. It’s part of the F.I.R.E. movement i.e Financial Independence Retire Early. You could argue that this is the 20- 30 year olds rebelling against their parents attitude from 20-30 years ago, when slogans Like “shop till you drop” and “max out on your credit card” become the norm. They are rebelling against that.

Retirement is in the aggregate not a monetary thing it is a resources thing. Retirees do not require money they require real resources like food, heating and shelter, which can only be provided if there are enough non-retirees working to provide them. Hence your FIRE concept is only possible for a very small minority of the population. Unearned interest is basically financial magic – or in plain English, bullshit.

I saw one couple gloating about reaching their early retirement plans but only discreetly mentioned their government careers, likely forever safe pensions and paid-for housing during service. Oh right, I think the student loans were also “forgiven.”

Save like us! See, it’s possible if you just have advantages. Yeah, how about paying up before claiming independence.

“Retirees do not require money they require real resources like food, heating and shelter”

Well then the solution is obvious. Put the retirees in interment camps and give them those freebies.

If you let them have money they’ll just spend it on enjoying themselves. We cant allow that, even if it’s their own money.

Unearned interest is magic? In what way?

Unearned interest has a well-defined meaning and it doesn’t seem very magical.

If I lend you money at a rate of interest such that I can sit at home and drink beer and do nothing, then you have to do smething very productive with the money in order to earn enough profit to pay for my life style. If everyone in the country does what I do, i.e. wants to live off unearned interest then there is no one left to lend the money to – so expecting this system to work in the agregate is like believing in magic. It only works if there are only a few people with money and everyone else is poor and has to work for a living. Hence western developed countries love open borders, immigrants and poor people. Until they start to complain and vote, then we have to deport them and get new ones.

The thing the F.I.R.E crowd never addressed though is that the whole thing can only work if there are people spending like crazy. If everyone lives frugally, the stock market will collapse, and the bond market will be a LOT smaller.

Buyers’ strike. Deflation.

The first — “buyers strike” in this case meaning that people pay off their credit cards — if it lasts long enough, would help in forcing banks to lower interest rates on credit cards. A lot of businesses would welcome it because people could buy goods and services with the money they now blow on CC interest.

The second (a little bit of it) would be welcome to make up for the inflation we’ve had, but it’s illusory. We’re not going to get it. There have only been three quarters of deflation in my entire life, compared to something close to 200 quarters of inflation.

which makes you 50 and 3/4 years old.

Financialisation of everything and rent extraction is the basic problem, so a big roll-back of banking would be a good start.

I don’t really see why so many people here are concerned about inflation especially at the levely seen over the last 30 years. Also what is the big issue with the purchasing power of the dollar? If you have enough of them it just doesn’t mater.

“…which makes you 50 and 3/4 years old.”

Accidental math error on my part to make myself accidentally sound younger. Do it all the time accidentally :-]

This will probably not be news to the financially astute group that reads Wolf Street but I’ll toss it out there anyway. It is possible to opt out (for either a fixed period or permanently) of receiving pre-approved credit card offers by mail. Go to optoutprescreen.com for the details.

I have a good credit rating and used to receive the mailed pre-approved offers by the boatload. I opted out permanently years ago and have not missed those offers in the slightest.

Did the Fed know that the money would be used to pay down credit card balances and hurt banks?

Does the Fed know the employment numbers are disappointing because the cheap money they allow the federal govt gets doled out to potential workers to stay home, thus the lousy employment numbers?

They play the “maximum employment” game, but fund the “stay at home and dont work game.”

The Fed SKEWS everything they touch.

Housing a mess right now.

The cool thing with a crisis is that it usually exposes who they are really serving. This was true for the GFC and it is true again now. Shame on MSM for not covering this.

Also, no one seems to call them out when their obvious incongruent statements don’t connect.

For example, “The poor jobs report shows just why we need to continue flooding the market with liquidity.” No one ever stops to ask “How exactly does 0% interest help with job creation?”

They do. The theory taught in economics classes all over the U.S. in college classrooms is that low interest rates encourage “investment” which is implied to be productive investment made by businesses. Historically we can look at high growth high employment eras and see that businesses were heavily investing in their operations, so the logic goes that lowering interest rates helps recreate these scenarios because businesses will need to hire people to implement these investments. It’s called the ISLM model, and as far as I’m aware this is still the macroeconomic golden standard in neoclassical economics.

What did businesses actually do though? They bought back their stocks instead. The only trade-off acknowledged in the model is the possibility of high inflation, but since the Fed thinks that for the last 13 years inflation has been low despite qe and zirp, the econ models suggest we should just keep going. Ignore the elephant in the room that we have gotten “investment” and inflation, but it’s been due to the insatiable and mindless buying of assets. Their model worked well in the realm of the rentier economy. It did not work well in the realm of the productive economy.

Forward American dystopia. One would assume that if the Fed is not just woefully incompetent, then they know that they’re doing the work of the plutocracy by growing the rentier economy. Get plundered proles.

Low interest rates can encourage investment in things like capital improvements, new factories, etc. But employees are an operating expense. We should not be encouraging businesses to borrow to make payroll, and I haven’t seen any evidence the difference between 3% and 0% makes any real difference in either.

1) Russia was a regional power that spread from Alaska to Berlin.

2) Putin provide energy to China, US and Europe.

3) His modern submarines can sneak out of Arkhangalsk and cause troubles in US.

4) Putin is a keystone who have the power to order Tehran, Syria and Hezbollah to sit on the bench in the current events.

And yet Russia is seemingly powerless to improve their internal economy, which has been stagnant since 2008.

Probably because of restrictions on trade imposed on the country by others. Hard to compete in the international marketplace when there are concerted efforts to make trade difficult.

Remember, the Russians are the “bad guys” and guilty of this, that, and the other thing.

I think the sanctions against Russia is equal to the west shooting itself in the foot, maybe both feet. Why ? Domestic consumer industry in Russia was weak, because of western imports. Now Russia has been forced to develop and build up their domestic food and other consumer industries simply because of the sanctions. Smart, these sanctions. In addition, the US is pushing Russia and China together when the rational thing would be to do the utmost to keep them apart.

Realist,

Your comments remind me of the adage that trading partners tend to avoid shooting wars with each other.

Call me an alarmist, but I think that the present administration wants war. Doesn’t matter where…great for business and gets those patriotism juices flowing.

maybe everyone should max out their credit cards and tell them to pound sand. Had a friend that years ago when bankruptcy laws were favorable ( cap. 7). Did that on 350k. He told me you’d be surprised at deals you could get with cash. I know I know things are different now. The social media gestapo knows everything now about everyone.

Thanks to Wolf for another article that describes important trends and is not hard work to comprehend.

My post-graduate work in cognitive psychology convinced me that there are a significant portion of humans who don’t even understand percent calculations, much less compound interest.

This is why some religions considered charging interest an evil. Similar to banning alcohol, it protects a subset of humans who are extremely vulnerable due to cognitive inferiority or denial of their self-indulgence.

A friend got herself into credit card trouble five or ten years back (about 15K), and I bailed her out because I hate seeing the credit card predators eating someone’s guts out. She’s honest, but just not the type that plans logically and keeps on top of things. Bailing her out allowed her to get a college degree, so it was a productive investment.

I’m charging her 3%, which seems about the right level for the risk. The problem with a “free” society where anything goes, is a lot of people naively or ignorantly “go” to bad places.

Oh gosh. I took a capstone psychology class for what I called my hobby major ;) (psychology for anyone who doesn’t go to grad school) called human judgement and decision making. For one of our research projects I wanted to study how people perceive interest rates in order to understand why they might make poor financial decisions. I will never forget the girl in my group, who when I brought up this idea, became almost tearful and shamefully admitted that she ran up over $10k in credit card debt. It felt like she was begging not to study it. Needless to say, with the rest of the group acting confused anyway, they quickly shot it down and we studied something totally lame instead.

I’m always torn between feeling like we need to protect these people, and thinking maybe they’re just born natural prey for the financial industry and shrugging it off.

“why they might make poor financial decisions”

My understanding is that most of people on Earth make poor financial decisions because the search for the financial optimum is the least of their life concerns primarily by their family culture.

The humans still have a strong animal side within, and that side does not care at all about abstract digits sitting on the investment account.

Engin-ear,

Family culture. Two words that speak volumes!

I was raised by parents who grew up in the depression era of the 1930s. I was taught to see the big picture, think and plan ahead.

I would hope all children with parents in their lives are taught the basics of life & money. Sadly, that is not the case.

Me too, Dan. Almost all my working life I thought and planned ahead. Saved a good bit for my retirement, as passbook savings consistently paid around 4.25% (give or take) for decades.

Bankers have always profited immensely by people who are math-challenged and financially naive. That would be the majority of US population, IMO.

And that will never change.

Maybe that’s why a Rockefeller pal of Bucky Fuller’s told him;

“Why make business simple when you can make it complicated” ?

I was doing a basic financial planning session to a class of high school seniors. I tried to look up formula for the the monthly minimum payment. It was not easy to find. It turns out, most of the time it is 1% of the balance due plus fees and interest.

Which implies, even if you do not add additional charges, it will take you typically 8+ years to pay off a balance of around $1,000!

Another juicy fact! The 15% interest is for purchases. If you take a cash advance using your credit card, you are typically looking at an interest rate that is 8% to 10% more.

Somewhere out there in bankerland is a graph showing stimulant cheque hierarchy.

After mopping up the cloud of battle, and laying to rest liquidity, the CC’s balances are ripe.

There is more to the Artwork, we’re at best only half way to allocating the 5 trillion.

“If they had enough cash to pay off their credit cards at this rate, they would.”

Like 2007 (in so many ways) you can consolidate consumer debts and roll them into your mortgage (where all is forebearance) . The banks are probably breathing a sigh of relief, if the markets repeat the GFC they will not have as many bad debts to write off. In many ways the stimmies absolved them of a liability. I wouldn’t go so far as to say the powers to be want to crash this market, they do want to nip speculative finance in the bud. I am interested to see who the Fed handles the yield curve, which is ripping higher, and puts banks in a bad place, when there is no loan demand. Are they going to raise FFR, or buy longer term maturities? Or both? I believe CC rates are tied to FFR? One main advocate of MMT says raising interest rates causes inflation, and it probably does in the new paradigm. , or whenever the economy is growing it’s own money organically, yields and inflation tend to move together.

I wonder how many GameStop buyers trying to “stick it to the Man” carry CC balances.

Well you clearly don’t stick it to the man by paying off debt. Default and restart, that is an actual middle finger. Otherwise it’s just a fake front: pay some stocks, pay some crap, pay taxes and pay off gains. A consumer locked in for life.

No harm no foul if you pay off the balance every month using a card where there’s no charge for 100% payment when due.

Yes, they charge a fee of about 3% but they charge the vendor. The vendor passes that expense along to their customers. In most cases the vendors don’t discriminate; everyone pays the higher price. So I use my cash-back card and you pay cash. You’re subsidizing my cash-back feature.

Some vendors do charge extra for using credit cards, which does pare down my cash-back benefits.

However, credit cards also carry features that add value.

You are an excellent spokesperson for the banks and credit card industry. Too bad you didn’t get a promotional fee.

Credit cards are fine. But I am not going to spend my life spending more just to get points to spend towards more. $550 a year annual fee? Forget that, it’s stupid to spend so much to try to break even.

With all this talk of emissions and climate change, frivolous travel is the worst due to previously cheap tickets and just the sheer amount of checklist list itineraries. No surprise the biggest perks of credit cards now is giving you more points applicable towards more travel.

All a useless front to appear living large. Tourists are tourists, everyone can spot one. Consumption is consumption, no matter what baby carrot perks are dangled in front.

“All a useless front to appear living large. Tourists are tourists, everyone can spot one. Consumption is consumption, no matter what baby carrot perks are dangled in front.”

LOL are you aware that Wolf spent 3 years traveling around the world? It’s how he met his wife.

Shame on you Wolf for being a show-off planet-killing tourist.

Who cares if people know you’re a tourist? And how is travel “a useless front to appear living large”? A lot of people travel for fun, adventure, and to broaden their world view.

All I see in your post is envy, ignorance and sour grapes. Sounds like you could use some travel.

Consumption is 70% of the US economy. What do you plan on replacing it with?

I apologize for being someone who knows how to profitably work his way through the system.

Glad you like your cards. Glad I stopped halfway through your comment.

I deleted the rest of Michael’s comment because it violated my guideline on product promos (name, price, features, benefits, etc.).

Jos Oskam, Yes it is frightening.

Perhaps more frightening is a closed NJ Deli whose best revenue year was less than $40,000, goes public and attracts $100m in capital investment. I’d love to see the list of the new stockholders. Talk about a “moron list”….

The only thing to top that would be if they funded their investments on a 29% credit card!!

Oh, reminds me, you can also fund your on line betting account using your credit cards. What opportunity!!!

Your morning laugh from CNBC:

‘This is why Cramer worries about Elon Musk’s influence on Bitcoin.’

But wait there’s more! This piece of dreck is ‘Pro’. You have to pay to read it.

Here is one thing you can say: if the price of ‘a store of value’ dumps 20% in a week because of what anyone says about it, it wasn’t too solid to begin with.

@nick kelly

Astonishingly – Jim Cramer has yet to realize that a market mover who wishes to accumulate an asset…

…will try to *depreciate* the asset until he has finished accumulating it.

The gold guys better hope no says anything nasty about gold.

@nick kelly,

Actually they’d be delighted to have the price of gold talked down while they are still accumulating it…

People diss gold all the time. It’s one of those things substantial enough that someone saying mining hurts the environment, or something, doesn’t affect it.

Oh, you just wait. There will be a credit card notice of change in terms coming.

It will tell you that there will be a “user transaction fee” assessed at the time of each purchase, and will be included in the amount due whether paid off or paid over time. Just like the merchants get charged now.

Start to plan on how to circumvent this now.

Do you speak of theory or information about pending change of TOS?

Thank you Wolf for another excellent article!

It does give me faith in humanity to know that people are paying off usurious debt with the stimulus checks they are receiving. They seem to have the financial knowledge to know that credit card debt is one of the worst debts to have. PayDay loans are the other type of debt that is worse.

It would be far worse if people were using the stimulus as a down payment to buy more stuff on credit. Despite what the Fed thinks is best for the economy or banks.

The people who have paid off their credit cards can emerge from this pandemic in much better financial shape than before.

I don’t know what is behind the Fed plan to reward home buyers with low mortgage rates and appreciating values. Also, stock equity holders appreciating with value. If this was a properly designed control system, they would have leveled off long ago.

I don’t know why traditional savers are being punished with low interest rates during rising inflation and credit card rates are allowed to remain high.

Is this a nefarious scheme or a means to a soft landing?

Since I don’t know the endgame of the Puppetmasters, it is hard to play the game. The Free Market no longer is free so I can throw out my old college economics textbooks and try to play by some unknown rules.

It’s like a good game of Monopoly where one person has the control to dynamically change the rules of the game at any point. Would I trust that one person to be altruistic or suspect they are self-serving?

“It would be far worse if people were using the stimulus as a down payment to buy more stuff on credit.”

Worse for….whom?

In an inflationary death-spiral – those who buy on credit are quickly recognized as having made very astute decisions…

BigAl,

The sellers of stuff certainly benefit.

Good point though. If I purchase lumber now for a new fence and inflation rises, that may have been a good choice.

Even with inflated used car prices, I just overheard someone bragging that their 3 year old car that they purchased new is now worth “only” 4K less than they purchased it.

I have sadly watched too many episodes of Storage Wars where people’s stuff ends up auctioned off at pennies on the dollar after they had paid to open a storage unit.

A close family member was a hoarder of stuff that they bought on credit. Again, when they sadly passed away, the heirs had to sell mountains of stuff at pennies on the purchase price just to pay the final credit card bill.

Why would they pay the credit card bill of the deceased? A moral imperative? For an unsecured loan? Ever wonder if credit cards charge high interest to average the cost of defaults?

Lisa,

Good point. It was technically secured with a mountain of worthless stuff purchased on credit cards over time. However, the estate is legally obligated to pay off debts. The estate also included some cash and a paid-off old car.

I believe legally the CC companies could have sued the estate.

I knew the executor of the will so he was concerned that after distributing the estate to the heirs, he was liable for the CC bills and any other debts (medical, taxes, insurance, etc).

Plus, ethically I think paying off a deceased person’s debt with remaining assets is the correct thing to do. Even if you only receive pennies on the dollar for those assets.

However, if you do it right, just die with no assets of value and turn the worthless pile over to the creditors. :-)

You can’t squeeze blood from a stone and the executor is not obligated to pay off any debt from the deceased personally.

@Siab,B – Thanks Seen, you have just indicated a major modification of an old saw: “He who dies with the most toys wins.” It is obvious that: “He who dies with the most LEASED toys wins.” As usual, devil take the hindmost.

@Seen it all before, Bob

“I don’t know why traditional savers are being punished with low interest rates during rising inflation and credit card rates are allowed to remain high.

Is this a nefarious scheme or a means to a soft landing?”

Well….

a) Rising interest rates suggest that inflation is also rising – therefore, indicating that the Central Bank is failing in its mission

b) Rising interest rates tend to appreciate a currency – resulting in lower corporate profits upon foreign repatriation

c) Rising interest rates tend to lower economic activity – though whether they are any good at all in actually fighting inflation is very much open to question.

Currently, most economies in the G-20 do not offer interest rates with a positive, real rate of return. Not does this appear likely to change.

Developing/undeveloped countries that do not hold large currency reserves and are forced to balance their capital accounts – usually attempt to offer these – but with varying success.

Just to add something to the discussion that lots of people seem to be missing…

The transition from CDO to CLO works (as it does for ABS) – because there’s a pretty implicit guarantee there that the nominal value of the underlying physical asset purchased or serviced by the loan will not deprecitate in currency terms.

Do you see any evidence of physical assets depreciating *anywhere* right now?

That the loanholder cannot service the loan and will have to surrender the physical asset is of near-no importance for the Fed Res who, after all, are merely charged with perpetuating/expanding the grift.

So this really *can* go on with increasingly better-looking optics, no less…

…just don’t be surprised if all those cops who will lose their jobs as a result of defunding the police – find new ones as repo men

Seems to me that one of the hardest things for a lot of CC users to have done since the ’80’s is differentiate buying the ‘thing/service’ from buying the money to acquire the ‘thing/service’ (the broad availability of easy credit offsetting a true realization of the stagnation in wages). As the purchasing power of the dollar continues to decline (recently covered by Wolf), perhaps a significant number of folks are being flat forced to realize that they can’t afford to buy any more money, among other things…

may we all find a better day.

Wolf,

Sometimes your lack of forward-thinking amazes me ;-)

*Clearly* the solution to this problem is to *cease* quoting financing rates in Annual Percentage Yield and to, instead, quote them as Daily Percentage Yield.

Who could resist a credit card with a DPY of 0.09%!!!

(* which is, of course, an APY of ~38.9%)

Wow! Paying off credit card debt.

Is there hope for the human race after all?

That stat will drive the Fed nuts. Static debt level has no effect on demand in the economy. Only second-order has an effect ie increasing debt increases demand perhaps with a ‘multiplier’, whereas decreasing debt reduces demand, again (frighteningly possibly) with a ‘multiplier’. The very definition of ‘deflation’. They’ll be apoplectic and have to pump even more money in to cover the reduction of that arm of private debt. If they’re lucky maybe an increase in car debt or something else will balance it out. If it becomes a regular habit , they are ‘stuffed’.

Credit cards are seriously weird things.

I had a friend who ignored her card, making only final demand minor payments for ages until her balance got to £7000, then, all of a sudden, she got a letter asking her to call at an office to discuss a ‘managed’ repayment plan. She was worried, so I told her to ask them to explain what was going on. She told me the debt had been ‘transferred’ from her ‘mainstream’ bank to a small private finance company. I explained to her that they had probably ‘bought’ her debt at a discount because of her poor payment record. I had to explain to her how this could even be possible. She got it, when she finally understood that she had been charged so much interest over the years, that the bank could still make a profit even if they sold the debt for half its face value.

I told her to phone the new company and tell them she had just got a cash sales bonus of £4500 and she would pay it to them to clear the debt, otherwise she would be forced to take their managed payment plan. She was very embarrassed, but she was also amazed when they came back with a cash offer to settle for £5000 which she took and got help from her family to pay. She saved two grand, the bank was happy, the finance co was happy. There’s so much fat in the game for everybody, the banks can package these debts at half.