Junk bonds still in la-la-land as investors chase yield – risks be damned.

By Wolf Richter for WOLF STREET.

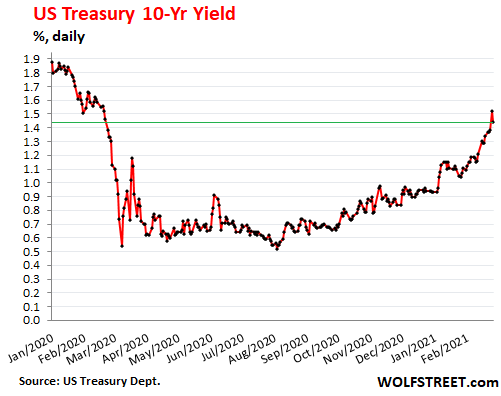

The bond market settled down on Friday. And that was a good thing for the crybabies on Wall Street that had started to hyperventilate on Thursday, when the Treasury 10-year yield, after rising for months, and accelerating over the past two weeks, had spiked to 1.52%, having tripled since August.

By Thursday, all kinds of complex leveraged trades had been coming apart, and forced selling had set in. By historical standards, and given the inflation pressures now underway, those yields even on Thursday were still astonishingly low. But Wall Street had a cow, for sure.

On Friday, the Treasury 10-year yield dropped 8 basis points, part of the 14-basis-point spike on Thursday, and closed at 1.44%, still higher than where it had been a year ago on February 21, 2020.

Yields rise because bond prices fall, producing a world of hurt – reflected in bond funds focused on long-dated Treasury bonds, such as the iShares 20 Plus Year Treasury Bond ETF [TLT]; its price is down about 16% from early August, after the 3.3% relief-bounce on Friday.

The Fed approves.

The governors of the Federal Reserve have been speaking in one voice on the rise in Treasury yields: It’s a good sign, a sign of rising inflation expectations and a sign of economic growth. That is the mantra they keep repeating.

Fed Chair Jerome Powell called the surge in Treasury yields “a statement of confidence.”

Kansas City Fed president Esther George said on Thursday: “Much of this increase likely reflects growing optimism in the strength of the recovery and could be viewed as an encouraging sign of increasing growth expectations.”

St. Louis Fed president James Bullard, one of the most passionate doves, said on Thursday: “With growth prospects improving and inflation expectations rising, the concordant rise in the 10-year Treasury yield is appropriate.” Investors demanding higher yields to offset higher inflation expectations “would be a welcome development.”

They’re all singing from the same page: They’re dovish on QE and low rates. But they’re going to let long-term rates rise, which is starting to tamp down on some of the ridiculous froth in the financial markets and the housing market.

Those Fed pronouncements on Thursday morning in support of higher long-term yields – when the markets were clamoring for the opposite, more QE but focused on long maturities to bring down long-term yields – probably also helped unnerving Wall Street.

But on Friday, the mini-panic settled back down, and that’s good because a real panic could change the Fed’s attitude.

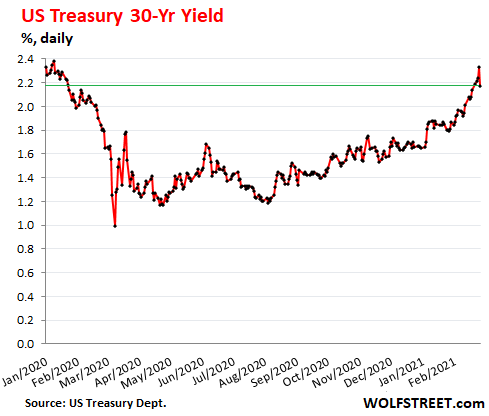

The 30-year yield on Friday dropped by 16 basis points, to 2.17%, erasing the jump of the prior three days. It’s now where it had been on January 23 last year:

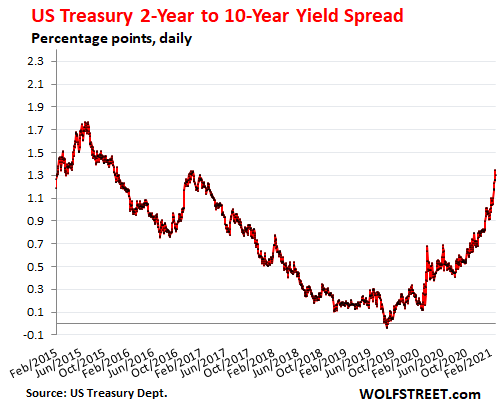

The yield curve as measured by the difference between the 2-year yield and the 10-year yield had been steepening sharply, with the 2-year yield glued in place, and with the 10-year yield taking off. On Friday, the spread between the two narrowed to 1.30 percentage points, from Thursday’s 1.35 percentage points, still making for the steepest yield curve by this measure since December 2016.

In August 2019, the yield curve by this measure briefly “inverted” when the 10-year yield dropped below the 2-year yield, turning the spread negative. The yield curve has steepened ever since in a very rough-and-tumble manner:

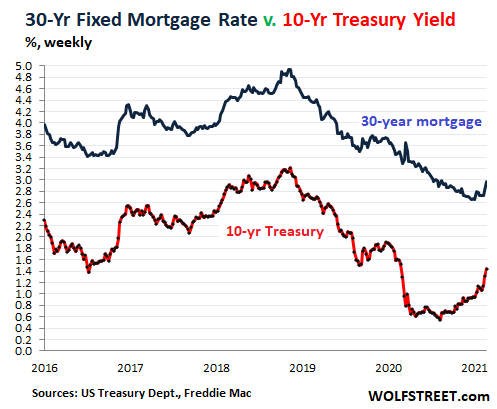

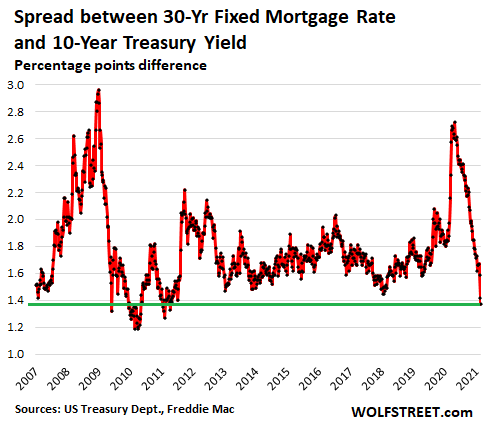

And mortgage rates finally started to follow.

The average 30-year fixed mortgage rate rose to 2.97% during the week ended Wednesday, as reported by Freddie Mac on Thursday. This does not yet include the moves on Thursday and Friday.

The 30-year mortgage rate normally tracks the 10-year yield fairly closely. But in 2020, they disconnected. When the 10-year yield started rising in August, the mortgage market just ignored it, and mortgage rates continued dropping from record low to record low until early January, whipping the housing market into super froth.

But then in early January, mortgage rates started climbing and have now risen by 32 basis points in less than two months — though they remain historically low.

Note the disconnect in 2020 between the weekly Treasury 10-year yield (red) and Freddy Mac’s weekly measure of the average 30-year fixed mortgage rate (blue):

In this incredibly frothy and overpriced bubble housing market, higher mortgage rates are eventually going to cause some second thoughts.

And that too appears to be smiled upon approvingly by the Fed. They’re not blind. They see what is going on in the housing market – what risks are piling up with this type of house price inflation. They just cannot say it out loud. But they can let long-term yields rise.

Mortgage rates have some catching up to do. The spread between the average 30-year fixed mortgage rate and the 10-year yield has been narrowing steadily since the March craziness, and at 1.37 percentage points, is the narrowest since April 2011.

The spread always reverts from extreme lows, such as this, toward the mean. It can do so in two ways, by mortgage rates rising faster than Treasury yields, or by mortgage rates falling more slowly than Treasury yields.

High-grade corporate bonds starting to feel the pain.

Yields have risen and prices have fallen across the investment grade spectrum of corporate bonds, though yields remain very low by historic measures:

AA-rated bonds yielded on average 1.81%, according to the ICE BofA AA US Corporate Index, up from the record low of 1.33% in early August (my cheat sheet for corporate bond ratings).

BBB-rated Bonds – just above junk bonds – came out of their torpor over the past two months, with the average yield climbing to 2.39%, according to the ICE BofA BBB US Corporate Index, up from the record low of 2.06% at the end of December. They, like mortgage rates had continued to fall through 2020, despite rising Treasury yields.

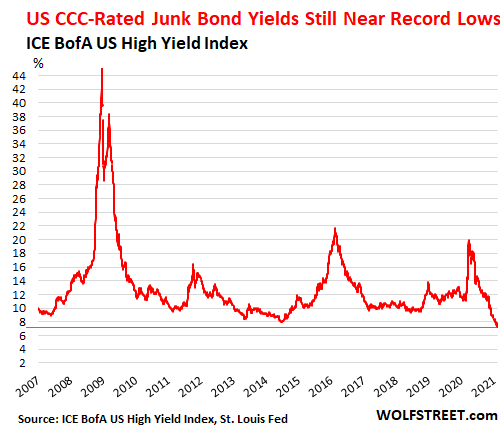

Junk bonds still in la-la-land, with yields near record lows.

BB-rated bonds – the highest-rated junk bonds – came out their torpor just over the past two weeks, and the average yield rose to 3.45%, according to the ICE BofA AA US Corporate Index, up from the record low in mid-February of 3.20%.

The average yield of CCC-rated bonds – at the riskiest end of the junk spectrum with a considerable chance of default – has barely ticked up from record lows in mid-February (7.17%) and now hovers at 7.27%. In March, the yield had shot up to 20%. During the Financial Crisis, it had spiked north of 40%.

The Fed smiles upon its creation.

The fact that the highest risk bonds still sport yields that are near record lows is a soothing sign for the Fed. It means that financial conditions are still extremely easy. All kinds of high-risk companies with crushed revenues and huge losses – think cruise lines with near zero revenues and losses out the wazoo – can fund their cash-burn by issuing large amounts of new bonds to over-eager yield-chasing investors, no problem.

So far this year, companies issued $84 billion in junk bonds, according to Bloomberg. At this pace, the first quarter will be the biggest in junk bond issuance ever. There is huge demand for junk bonds due to their higher yields – risks be damned. The yield chase is on in full force. And the overall junk bond market has ballooned to over $1.6 trillion.

For the Fed, this is one of many signs that credit markets are still super-frothy, even if Treasury yields have risen from record lows to still historically low levels. While it vowed to continue QE and not raise rates for a “while,” it’s also telling the markets in a unified voice that rising long term Treasury yields are a sign that the Fed’s monetary policies are working as intended. And those higher long-term yields are taking some of the froth off the markets, including eventually the housing market – and I don’t think that this is an unintentional side effect.

From crisis to crisis, and even when there’s no crisis. Read… Fed’s QE: Assets Hit $7.6 Trillion. Long-Term Treasury Yields Spike Nevertheless, Wall Street Crybabies Squeal for More QE

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It may be an intended effect, this reduction of the frantic housing bubble, but it still leaves me with a few questions.

There already is massive inflation, not just in housing, but in all those categories excluded in accepted CPI numbers. Real inflation, yet wages are stagnant. So, if there really is inflation, but rates need to stay crazy low to keep the wheels turning, what does that really say about the economy?

I’m purchasing posts and beams direct from a local sawmill for a project. I’m paying close to 3X what I had to pay last year. 3X. This is a direct result of the US housing surge and pandemic renovations. No big deal as I have cash in the bank, but…..but, my cash is earning zip/nada/nothing as the Fed forces consumerism upon us. I’ll be cutting back somewhere else to avoid trashing my savings.

And, what would happen if interest rates moved up to at least match ‘real inflation’. What will happen if bonds are forced to provide an honest return to the investor? Why are people still buying this crap? Is it simply what else is there to buy? 1-2%? It’s a joke. Robbery.

Finally, can this actually continue much longer? I don’t think it can? What do other commenters think?

Thanks in advance because I am dumbfounded and discouraged from this article.

In another piece Wolf said “this is the most treacherous investment environment I’ve ever seen” and that continues to stick with me.

Invest in stocks, bonds, gold, real estate, whatever, at record high prices? Seems foolish. Leave it in cash while inflation beckons? Also doesn’t seem wise.

For those that don’t have much to invest downsize and pay off debt for safety. Those with investable assets maybe acre or two of buildable lots in near rural land from major cities, some gold, cash, quantities of durable goods needed for the future, and a weapon or two for self defense.

This might not be the time to seek a good bet with stocks but the time to batten down the hatches and take profits off the table. We are living in a Everything Bizarro World unlike anything I’ve seen in my lifetime, 72 years in two weeks.

I’ve generally followed Ray Dalio’s recommendation for small investor asset allocation in the current economic environment. He identified four major asset categories: (1) cash and cash equivalents; (2) hard assets-real estate, commodities, precious metals, collectables, etc.; debt instruments; and common stock. His recommendation was to split investments 2/7 cash and equivalents, 2/7 hard assets, 2/7 debt instruments and 1/7 common stock, due to its volatility. With some tweaks, I have found this as good an investment guide as any.

I wouldn’t go near listening to Davos oligarchs like Ray Dalio- with over $14 billion plundered dollars in his pockets.

He’s desperate to be known as a “big-thinker” , and has an obscene amount of vulture capitalist loot to spend on that endeavor.

I’d be careful about listening to his advice. He was wrong big time in the eighties.

He is also one of the geniuses who lost billions in 2020 when everyone else made a killing in the market.

you failed to mention cryptos, LOL

I’m going to put crypto’s in the same asset class as Pokémon and baseball cards. Yes, you can make money off them, before they crash and we don’t know when that will happen. It will be a roller coaster along the way. Maybe they will trend again in future, but unlike most other asset classes they have no intrinsic value and could crash to nothing and stay there. Fiat despite not being directly backed, has at least the interests of major economies and other factors invested in its success.

Start a true second party ? One not owned by multi-millionaires and the legal system and regulators they have purchased? One not owned by the banks, Wall Street, and the obscene Military Industrial Complex that Eisenhower warned about?

As it stands- pull one of the two levers offered to you in elections-

oligarchs like Yellen and Powell are laughing in your face, as they and their crony vulture friends pile up their loo. They can and will prevent anyone not in their country club from earning any return on hard earned “money”.

“Start a true second party?”

To obtain positive results from that would require our easily manipulated national idiocracy to suddenly pay adequate attention to very complex issues in order to actually know what’s going on and, thereby, who to vote for. Most people don’t even know the most basic economics.

That would require for many, based upon the IQ bell curve alone, a magical rise in average intelligence and/or a magical appearance of the learned ability to think critically. It would also require smart phone delivery of those very complex issues via mobile-targeted news media since that’s where they get their news these days.

-NONE- of that is ever going to happen.

Besides, the -ACTUAL- government is not something you can vote for as statistically confirmed in a 2014 Princeton University study analyzing voting on issues versus results. Excerpts:

“In the United States, our findings indicate, the majority does not rule—at least not in the causal sense of actually determining policy outcomes.

When a majority of citizens disagrees with economic elites or with organized interests, they generally lose. Moreover, because of the strong status quo bias built into the U.S. political system [that describes the overwhelming influence of the administrative state and lobbyists – W], even when fairly large majorities of Americans favor policy change, they generally do not get it.

To be sure, this does not mean that ordinary citizens always lose out; they fairly often get the policies they favor, but only because those policies happen also to be preferred by the economically-elite citizens who wield the actual influence.”

———-

So, “The Government™” isn’t something you can actually vote for because it is, in reality, the -VAST- unelected administrative state which is present at every level of government and the unelected lobbyists who effectively own the relatively few politicians found at every level of government pretending to be in control.

But, they continue to bring people to the polls via hot button issues like abortion and gun rights…

This replying to Winston:

Sadly I must agree with what you say, almost totally:

NOT totally only because as one educated in the critical thinking you specify long ago, nothing is ever totally, just mostly, LOL.

Having taught an occupational course at two high schools 40 years ago I was appalled by the lack of ability of the students, 16 and over, to do even basic arithmetic, much less parse a sentence, both of which we were required to be able to do to get out of 7th grade in the 1950s era. These were not ”low IQ” kids, but they had been abused by the public school system they were forced to attend from age 5 or so…abused is a polite word in this case, for sure.

As to the rest of it, what you leave out is the constant overwhelming brainwashing formerly through the TV, and now apparently through the ”feeds” as you describe; that alone is the foundation on which the continuing dumbing down of the mass of ”humanity” is built, and built knowingly IMO, to the shame of the masters/oligarchy/whatever.

I will also take another path on the whole subject of ”IQ”: Unfortunately, as part of my lazy effort to earn a degree after dropping out of med school, I gave up on the hard work of learning more of actual science, and went to the ”soft sciences” and was required to study, (actually only requiring one reading of texts,) inter alia, the origins and use of the IQ.

IQ as determined by the Stanford-Binet Test, was intended as and still is only another tool of the masters to determine who were/are good candidates for various components of their machine, and, in fact, really only measured exactly that as a function of cultural indoctrination. Gardiner et alia came up with about 18 additional measurable ”intelligences”, but since those metrics did not serve the masters, those concepts went nowhere fast.

Having this discussion 40 or so years ago with a friend with high IQ, MD, PhD, etc., he was insisting IQ was all that mattered, so I suggested he go ahead and fix the motor of his XK150 himself, rather than hand that job off to a dumb wrench puller; no doubt you can predict the result.

IMHO, the pendulum is swinging back toward understanding that difference and the value of skilled trades, as I understand it now is more expensive in the SF area to call a plumber or electrician than to visit a MD, etc.

It will be interesting indeed to see how the current situation, both short and long term turns out, eh?

Wanting to start a “true political party” is an unreasonable expectation, and we all know how those turn out. All you can do is to take care of yourself and your loved ones. That alone is all you can do. Voting is much like the steering wheel on a child’s car seat. Know enough about politics and the economy to stay out of the way of war and economic disaster.

V V,

Don’t blame the kids, it’s the teachers who can’t teach the subjects that are the problem. The higher education system values “teaching” courses over hardcore knowledge in the liberal arts.

I took my degree in Computer Science, but was really an applied mathematics major. I can’t get a job teaching any kind of low level math, in any school, because I don’t have “education credits,” which are total garbage.

Most of the math and science teachers in the education system didn’t major in those subjects, but they have “education credits.” The teacher’s union are responsible for this mess.

re: “… I suggested he go ahead and fix the motor of his XK150 himself …”

Hah. Although a clever and elegant design, SU carburettors baffle even good American mechanics.

Pet,

ABSOLUTELY!

I was trying to make it clear that the kids were not dumb, just abused by the so called education system, which is, as you say, a sop to the teachers unions for way too many years now, and the system only works to ensure the union remains in charge and to hell with the kids… saw equally bad kid results earlier, back in the late 60s/early 70s when good kids of friends in bay area were graduated high school without being able to read or do any arithmetic whatsoever,,, you could guess what happened to those kids, though one did well by working very hard as a sheep herder in NZ, and eventually did learn to do enough math, etc., when he went into biz for himself…

At this point, the ”education industry” is just as corrupt as the military industrial complex and the political system, and all of them need top to bottom reorganization before we go down the tubes any more/to the bottom,,, as has been the case with every other society ever in global her and history.

Winston, that was very put. Mind if I quote you randomly?

PAULO

I always read your posts and your question to the Streeters seems sincere.

I know less than most, but what I took from Wolf’s presentation here is the Fed is seeing a glimpse

of what they intended. Though the Fed should maybe not exist, it’s what we have. The pumped markets might finally start to cool because of what the Fed is allowing to happen.

In short, things could be worse.

As long as inflation (as recognized by the Fed) moves slowly, then markets cool, housing flattens and Joe Bag-o-Donuts can buy a UST bond yielding more than a pittance. Combine that with raised min wages nationwide and things will seem more normal for most people.

If Fed instead blinks as equities stall and moves from ZIRP toward NIRP, then the Streeters (incl me) just continue to bemoan the martyrdom of being a Saver. Boo. :-(

It says the USA economy is based on increasing debt? Without the dollar scam the USA economy would definitely collapse.

If you want to make money, maybe you should turn to the crypto market, you can get up to 14%….make sure you buy the coin not just invest in a coin

Crypto is not an investment. It is an illusion. In order to be an investment, you must have an asset that actually exists, to secure the investment. In the case of crypto, no actual asset exists.

I have studied crypto’s for many hours and still do not have a clue why they exist.

They are far too volatile for transactional purposes. There is huge counterparty risk at all levels. There are backed by NO entity . The underlying value is to put it mildly impossible to determine. But they are a great gambling vehicle for those who can’t make it to their local casino

It’s quite amazing how the internet has created a platform for gambling on things that never existed before.

Company P/E ratios are higher than the long term average. Stocks outperformed real estate over the past ten years. The corrections and crashes are painful.

Short term interest rates are dirt cheap. The price of dirt is rising faster than the value of CD’s.

Property tax rates change. Assessed values are rising. One community saw a 5% increase in assessed value. HOA fees are rising. They want to repave more streets and add amenities. Maintenance and repairs are expensive. Insurance is not cheap in hurricane alley.

Average 30 yr fixed rate mortgage is 3.27% (not FHA).

Paulo,

I pretty much agree with everything you said in your post (I particularly liked “forced consumerism”, which is absolutely true and has a nice ring…I started to get images of how goose pate is made…).

This Fed “forcing” has really been going on for a very long time (nearly 20 yrs, per interest rates, using various tools) and DC has really shown very little inclination to ever stop (recent weeks’ “teeny taper” is about as brave as they get).

Whatever fundamental metrics the Fed uses to judge things have very seldom read “stop ZIRP/printing” for 2 decades and that is the underlying pathology that will kill us (basically uncompetitiveness leading to inflation overdose).

But in FedWorld addressing intl competitiveness is verboten (too politically risky) and consumer savings is the enemy (Keynesianism sees *savings* as a pathology that keeps the G’s engineered system of levers and pulleys from working properly…yeah *that’s* why (eye roll).

So you get the bayonets of ZIRP…either a force fed consumerist spend down or a blindfolded drop off into the dangerous part of town where the CCCs live.

You’re lucky that real estate prices are higher too. That will let you cover the higher lumber costs. Hopefully.

Is the local sawmill doing more business, or just passing on cost increases? Are they raising prices to compensate for loss of business? What is happening upstream? Lumber prices increase according to supply and demand if only you knew how much supply is being held off the market. In the energy sector it’s the spread between number of oil well and oil rigs. There may be a lot of oil but no rigs. In this economy if fraking ended and post pandemic economic activity ramped up we get a squeeze, but that’s probably not it right now. When demand slackens at a sawmill the workers find other jobs. That makes it tough when an order does come through even though demand in aggregate is weak. Just in time supply chains have a downside.

In the crazy construction biz for eva, and considering jumping back in with the crazy demand these days, in spite of my declaration/promise that this is my last ”retire mint”,,, just love the biz!

Bidding major wood frame apts and hotels in SoCal in late ’17, ”podium” or not,, my long time best lumber source guy , who purchased train loads almost every day, told me it would be AT LEAST six month before he could guarantee to deliver the train load I needed for a project..

And the best qualified framing sub bidding projects to us said it would be 3 years before he could start work on our job, and that only with a signed contract.

Back in the early ”oughts” rebar was rising so fast and the supply was so backed up that bids were regularly noted as, ”good for 24 hours”, and were regularly denied/re-offered even a few hours after that.

Similar with gypsum products at various times over the last 40 years or so.

Are manufacturer’s manipulating the markets for these products??

OF COURSE they are, and have been for eva.

This time is, of course, different! LOL

Vintage,

Do you know of any good websites/independent consultants that can help generate fairly detailed SFH construction “takeoff lists” itemizing materials and labor for an array of submitted design options?

I know there are the RSMeans of the world that provide somewhat geo specific pricing data but I’m looking for a more consultative approach, that would allow for sequential rounds of refinement in design and related pricing.

Basically, I’m of the opinion that there is a huge shortage of things like fourplexes and what I think of as “Simplicity Homes” – 1500 SF SFHs with cost-to-build-optimized design.

(Frankly I’m amazed that no liquidity stuffed lenders – banks or anyone – have not already affiliated with experienced builders to generate largely standardized homes along these lines…and then churned out thousands of them across the country).

The home building biz seems excessively given over to price-spiking, semi-customization at this point in time…unnecessarily hiking costs/risks to everyone…lenders, builders, and, finally, inevitably, buyers.

And it doesn’t have to be this way.

And, from the late 40’s until maybe 2000, it wasn’t.

Some of the costs may be transiently intractable (lumber) but a *lot* of the cost/price spiking seems to be self inflicted by builders’ design choices.

Am I’m just shocked that there aren’t more nationwide GC’s who focus on the lower cost, plain vanilla end of the mkt.

Most of the Builder 100 have median pricing in the $300k to $400k range for new SFH pdt.

Cas,

One of the reasons I am now fully retired is the proliferation of software that is able to ”take off” plans from CAD or even now, I believe, PDF files, and I think there are other file types now being used as well,,, and I am not up to speed on those softwares, and, being OK financially, not rich for sure, but have ”enough” to make it through the short time left in this body, the only thing I do with extra money is up the ”liquidity budget.”

So my answer is a general but qualified yes, what you seek is out there, I think…

My suggestion would be to find a motivated student of architecture or civil engineering or construction technology at the closest college or university or even perhaps a local high school. You could probably find them, with references, from their teachers. Cal Poly has an excellent program if you are near there; certainly there are other good ones around without having to go to MIT, etc.

The younger folks I have worked with in our industry the last few years have uniformly been great to work with, and mostly very helpful even though they tend to talk too fast, not to mention how fast they can type and work the computer! Not all of them have gone to college, but most have.

The fact that I worked on some of the ”beta” versions of some of these new softwares back in the late oughts, and found I was faster and more accurate, as should have been the case after more than 50 years with the paper plans, not withstanding, I do believe that the current versions are faster and of sufficient accuracy.

Paulo, I feel your pain. I’m sitting on some great lots, but I refuse to pay insanely high retail to build for myself. Lumber leads the way up in prices, but shipping costs, other commodities prices and labor costs have followed lumber prices on the way up. It’s never been more expensive to build a house.

However, if Dr. Michael Thomas Osterholm is correct, that a variant will force a fourth wave of Covid, then bond yields, along with stock market prices could drop, if this wave four produces enough of a negative market sentiment.

Unfortunately, a fourth covid wave could, once again, shut down lumber mills, infect warehouse employees and sideline overland shipping personnel. It will take even longer to get materials and appliances delivered to the job sites. That could boost building materials prices even higher, while, at the same time, there could be even greater demand for more single family houses. High single family house prices, already breaking records, could continue to break records.

I guess technology should help bring home building cost over time

Lumber may not be needed to build a home

Just Google 3d printed home

This i what we need seriously

Lumber is just an example in this case btw….

If you want lower home prices, the last thing you want is covid anything because the Fed will just open the vault again. Instead, you would want higher long-term interest and you would want the distortions in the market to be backed out. That might get you lower home prices.

For sure Wolf,

However, there are several factors in current home prices that could go away :

1. People want to live where they want to live, and not where it is still possible to build homes for a lot less,,, tons less to be clear.

2. NIMBY ism is in fact a huge deal some places, and many have had ”neighbors” ad infinitum go on and on and on to stop new housing, causing some to give up, etc.,

3. RED TAPE by any and every name is quite absurd in some places. Last new house I built in CA,,, about 30 years ago, it took six months and $22,000.00 in ”fees” from when I submitted plans for a SFR signed and sealed by a Registered Architect AND a Licensed Structural Engineer AND a licensed General Contractor; next house I built, in FL, it took 3 DAYS and $2,000.00 in fees after I submitted plans signed by a licensed General Contractor only; couple years later, built a new house in rural TN, ”fees” were $50 for septic permit and $75 for state Electric permit, including on site inspections for both.

4. The idea Cas puts forward above is good and has been done formerly for tons of housing from SoCal to FL that I have personally observed. Current houses typically have much larger roofs and entries and so forth costing about 20-25 % of total construction costs. Much more simple designs are absolutely possible.

5. The 3D printed concrete homes I have seen beta versions of certainly seem to offer a structurally sound small home for likely very much less than current pricing, which builder neighbor says is about $120/SF for basic 3/2 CBS in tpa bay area.

Lots of opportunity out there for many different modalities for housing IMO,,, actually breaking out of the often heard mantra that construction continues to proceed with basically the same methods and the same tech used since for eva,,, a thousand years or so by some thinking / commentators for the majority of the techniques/practices.

A massive dual stock market crash and housing crash will be a ton of fun for many of us to watch.

The CDC eviction moratorium order may be ruled invalid on appeal from the recent Texas decision, not all states have eviction prohibitions, and certain persons do not want massive government aid to help renters pay rent arrearages, only limited aid to small businesses, and no effective stimulus like massive, long-overdue, infrastructure spending by US government. Thus, economy may go kaput as evictions surge and millions of people get homeless and desperate.

This is on top of an inflation surge after the banksters’ (not-government-owned) “Federal” Reserve gifted $2 TRILLION plus to its banksters in exchange for mortgage backed securities that were uncollectible at anywhere near face values in 2019 to 2020, etc., etc., etc. Read about pre-revolutionary Russia or France. We are nearing the precipice and the arrogant ultra-rich banksters ignore their peril.

While a stimulus might cause more inflation, they are like people worried about a scratch on their toe while swimming as a white shark rushes at them with jaws agape. Bon apetit!

Paulo – I would be interested in hearing about the 3X hedonically-improved trees your sawmill is buying.

Blahaha.

2% CPI =300% real world

Automated trees cut, dry & transport themselves & the price reflects it. Worth every penny.

Wolf.

Sorry, but I’m still stuck on advertising being a tax write off….seems insane…right up there with Citizens United, Crypto, or any other Wall St stuff. (there, I related it to the topic)

The IRS gets less (taxpayers lose/pay) to watch commercials which pay (along with execs in media and ad agencies and all talking head compensation) for any kind of crap the TV/cable networks choose to throw together…specifically “reality shows” and “custom” “news shows”….even obviously agenda sponsored “news” content? (and the most obvious “message” reality show I’m aware of is Duck Dynasty, where education is laughed at and bumpkin stupidity and religion praised). And then there is all the psychological and demographic research ad agencies do, also in the end, tax write offs?

Over consumption is trashing the planet, and making people do it is a tax write-off!!!?????

I guess the next question would be since it is a tax write off, when a corp goes to borrow money for more advertising, is it easier and less expensive to borrow? I realize it depends on the overall financial condition, but in general would a lender allow even more debt if it is earmarked for advertising? Unlike capital equipment it’s bought, showed, and gone forever…

Am I just making a needless/stupid bunch of connections here, or is this a major part of the sheer idiocy of this “system” of ours? And I’ve ignored internet stuff, which is probably worse.

Maybe I shouldn’t even try to make sense out of this, as I can’t do anything about it, anyway, except babble here. It’s a good thing I’m well grounded in many different life experiences and biology, because this man-made cultural crap could drive people mad, likely has already. (I do notice an increase ads for “coping drugs” and sleep aids).

Everything seems fine to me….

It’s only a nightmare to people who want to save instead of spend.

Retired here on a fixed income. You are so correct.

Sorry, that was a subtle sarcastic comment that apparently got lost in translation

Ben, I understand. :) But it is getting pretty bleak for retirees on fixed incomes everywhere.

AA – I hear you. Layoff forced doing early retirement to make mortgage payments. So of course now not eligible for the current “unemployment assistance.” Then there’s the almost zero return on savings to complete the picture. Oh so equitable for older folks.

“Everything seems fine to me….”

Springtime for the Eloi.

I follow the TLT, it goes down the 20 yr yields goes up . I saw weeks ago the TLT was going to drop down to 138. I think now a move up back to the 148 to 150 level. Then? I see more down to 130 or lower. Does this mean the fed has lost control or is fixing to

All I know is the charts are a map. They be saying “buckle up”

I just follow the 10y yield.

if it exceeds 1.5% and keep going up, selling of bonds will accelerate!

Fed cannot save both bond and the stock mkt. Bond mkt is very essential to feed the Govt spending/functioning on increasing deficit and debt!

B/c they are hell-bent on creating inflation beyond 2.0% since ’09, their created inflation monster will slip out of their control, just like in late 70s-80s! It is the ‘expectation’ of inflation but inflation itself, which creates havoc. 1.9 Trillions is about to enter the economy! Plus more on the way!

Deflation os asset bubble has begun!

BTW no one rings a bell at the beginning of a bear mkt!

correction:

It is the ‘expectation’ of inflation BUT NOT the inflation itself

thanks

I agree Marmar..but what I don’t “Grok,” is why are “investors” buying Junk Bonds and higher rated bonds? Maybe I’n foolish but I’ve been investing

in REITS for 3 quarters now and knocking down 10%+ ROR. IT’S very liquid

and seems almost too easy. But I am nervous and will be putting my savings into a historic adobe home in the SOUTHWEST!

Just watch the etf ‘HYT’ the high yield Corp bond etf ($11.43) from BlackRock, the purchasing agent for US Govt/Teasury!

Total return for 1 yr = 19.9% (M*star) 3 months= 0.99%. Yield /div 8.18%’

if it starts slipping below 10, monitor it!

Part of the reason why junk bonds are not going down in price is because the stock prices of many of the underlying companies is so high , that these companies can easily raise monies via stock secondaries and do not need to turn to the bond market . The incredibly high price of the stock of these companies is allowing them to finance at what is in essence below zero rates. This makes them a better bet than Treasuries

The reason junk bond prices are not going down is because there are so many dollars in the system. That is also why stock prices are high. There are massive, steadily increasing amounts of dollars in the system. Dollars are worth very little because dollars are so plentiful. They are so plentiful because the FED digitizes them out of nothing.

The key financial question always, for those who deal with dollars and those assets denominated in them is: How many dollars are in existence, who owns them, and where are they?

The worth of a thing in dollars is the amount of dollars that may be bid for it. How much is your bank bidding for your dollars?

Uncle Warren says that the bond market is not the place to be in the foreseeable future.

If interest rate were to go up to just 5%, a lot of people will be wiped out.

In December of 2018, when Fed Funds went up to meet the inflation at the time of 2%, the Dow shed 5K in 3 weeks.

The threshold of what the stock market can handle in terms of interest rates gets lower on every stock rally.

In 2007 the stock market made an all time high of 14K, and Fed Funds were 4%.

Then, as mentioned, 2% Fed Funds knocked the market apart in December of 2018.

Now, 1.5% Fed Funds would likely do the same.

Lower and lower is the threshold of what the market can take…..and that points to its fragility.

The 27% increase in the money supply, decided by one unelected man (and his scions) at the Fed points to a lot of different problems with an untethered, unmonitored, unbound Federal Reserve.

The Constitution is clear, minting and the value of the currency lay with Congress. That is a fundamental. It can not be delegated.

“The Constitution is clear…”

Huh? What on earth is “The Constitution”?

The Constitution is the daily walk you should take for your health. The other use is archaic and should be depreciated.

Huh, the Congress says a dollar is still worth a dollar, and they run the mints right? The Fed is just creating digital numbers, what’s the issue?

Back when the constitution was written it was gold that was real money and a dollar was just an easily traded substitute. Nanke said gold isn’t money anymore and congress still allows the mints to make golden eagles officially worth $50 or whatever. The problem here is that after Nixon, people still treated dollars as a valid currency for saving. How crazy is it that we get paid now with binary digits on a computer with no minting involved!

Go to your employer and demand that they pay you in official hard currency, particularly $50 golden eagles as legal tender with the value set by congress and see what they say.

Listened to Munger last week. Read annual report. Those guys have seen it all. I think Buffet is realizing that with the Fed money printing and stuck on zero might as well buy back brk stock as there is an opportunity cost sitting on cash. Looks like he is buying it back at earnings yield of 5%.

To save people time if you use operating earnings plus look thru earnings I get $11.87 earnings per b share. Use whatever PE you think appropriate.

To save even more time, does Buffet buying back at earnings yield of 5% mean he is buying at PE of 20? Yet BRK B is selling for $248 and a P/E ration of .011.

Why doesn’t this reconcile?

The spread between Mtg paper and the 10 Year will NOT widen. The spread is getting tighter because Mtg paper is backed with actual collateral … houses. And, houses appreciate during inflation, so that collateral is getting better and better meaning default risk is decreasing. Housing will continue to climb.

Jim, that sounds a lot like wishful thinking. The data show that mortgage rates have already risen in the past 2 months. There’s real data for that! US average 30y fixed up from 2.65 to 2.97% since start of year. That’s like a 10% boost in monthly payments on any size loan.

House prices don’t appreciate when rates rise. And inflation isn’t their friend either – the last major inflation wave saw the Case-Schiller index lose ground to inflation. (See charts from 1955-1980.)

I think the “collateral value” argument goes exactly the other way. Unless workers get raises, house prices will fall if rates rise because no one can afford higher payments. On top of that, the real-world loan durations blow out when rates rise and prices fall – people can’t refi so easily.

So mortgage spreads will actually have to widen out to reflect the increased risk.

Agreed, housing appreciation will temper down as rates rise. However, there is no way housing supply will catch up with demand for many years. Assuming rates don’t rise too quickly or too high, housing will stay strong. More reasonable price inflation is welcome, which should also help bring building supply costs back down to earth.

About 1980 the inflation rate was over 10%. The Fed funds rate was over 15%. After this interest rates and inflation fell.

Bill Clinton balanced the Federal budget. The U.S. debt to GDP ratio fell during the Clinton years. Inflation was low single digits.

DH – Clinton borrowed from the Social Security trust fund to make his budget work – not from the public bond markets.

WisdomSeeker, the increase is 4%, not 10%. On a 2M home, PI goes from $6447 to $6720 with 20% down on a 30yr.

Except that the principal is money you’ll get back eventually when you sell… your actual cost of ownership is in the interest payment, which does in fact go up 10%.

To a realtor, there’s never been a bad time to own a house. If that’s true, there can’t ever be a market. Everyone will just hold on to their houses, in fact why would homebuilders need to sell a single house ever?

Why should homebuilders build houses when they can simply invest in the financial markets and get rich quick? I’ve done a bit of carpentry and pouring concrete, and it is hard work. Making money in one’s sleep is so much easier…

It’s the same for industrial production. It makes no sense to build new factories when it is more profitable to buy existing factories and financialize them into rubble.

Dear leaders used to brag about hiring half the working class to imprison and guard the other half, but that is so 19th century. Today we can all make a living selling pieces of paper to each other without even getting out of bed.

Wow, I just had a flashback to 2007. Wild.

@ SocalJim, that is absolutely wrong. Home prices go up because of easy-money policies, which are fostered by central banking idiocy. The central banks are buying up every crap-asset, including mortgage bonds, they can to avoid rates taking off and cratering prices. Rates will not stay down forever, and when they ramp up, home prices will crater as that easy money spigot is turned off. Lending standards will eventually tighten, and the idiots that bought at all time highs will be massively underwater once again.

Somewhere tonight, Alan Greenspan is sitting there and smiling.

and Volcker (RIP) rolling in is grave

Greenspan, Bernanke, and Yellen- all smiling while they wave to each other at church.

Religious.

What could be better than being on a lecture circuit where you probably get paid whether you show up or not, or say anything interesting…with a couple of inflation protected pensions in your back pocket.

“What, me worry?”

What church is that?

What church is that?

“Our Lady of Perpetual Peonage.” It’s non-denominational.

great one Rich,,,

may have to utilize it, as I have done with Unamused’s ”WE the PEEDONs”, one of his greatest summaries of the situation ever on here,,, and I try to remember to reference him, at least most of the time when sufficiently sober, a state I am trying my best to avoid these days,,, LOL

which reminds me of a conversation with a friend from 7th grade a while back in which I asked how he handled sobering up/hangover before going to work after a mid week night at the bar; he said he just went to work drunk, and was still able to do everything his job required!!!

Not that anyone should ever do such a thing, eh? LOL

The Temple of Divine Lucre!

The church of Dynamic Stochastic General Equilibrium. Ordination is required.

@Paulo,

Your post is good and represents what a good portion of investors feel including myself, and I will stay on the sidelines for awhile.

Below is from Lance Roberts and he confirmed my beliefs, along with The Traders Almanac saying about March being turbulent, – #2 is amusing to me, but true, and this market has worse odds than going to a casino – IMO.

————————————————————————-

Why Higher Rates Are A Problem

It is essential to understand the impact of rates on a heavily leveraged economy.

1) Economic growth is still dependent on massive levels of monetary interventions. An increase in rates curtails growth as rising borrowing costs slows consumption.

2) The Federal Reserve runs the world’s largest hedge fund with over $7.5-Trillion in assets. Long Term Capital Mgmt., which managed only $100 billion, nearly derailed the economy when rising rates caused its collapse. The Fed is 75x that size.

3) Rising interest rates will immediately slow the housing market. People buy payments, not houses, and rising rates mean higher payments.

4) An increase in interest rates means higher borrowing costs which lowers profit margins for corporations.

5) One of the main bullish arguments over the last 11-years remains stocks are cheap based on low interest rates. That will change very quickly.

6) The negative impact on the massive derivatives market could lead to another credit crisis as rate-spread derivatives go bust.

7) As rates increase, so do the variable rate interest payments on credit cards. With the consumer already impacted by stagnant wages, under-employment, and high costs of living; a rise in debt payments would further curtail disposable incomes. Such would lead to a contraction in spending and rising defaults. (Which are already happening as we speak)

8) Rising defaults on the debt will negatively impact banks that are still not adequately capitalized and still burdened by massive levels of bad debt.

9) Commodities, which are sensitive to the direction and strength of the global economy, will revert as economic growth slows.

10) The deficit/GDP ratio will surge as borrowing costs rise sharply. The many forecasts for lower future deficits will crumble as new estimates begin to propel higher.

Martok and Paulo –

Very good, except for one thing:

There Are No Sidelines. You can’t “sit this one out”.

“Holding cash” is every bit an “investment choice” as any other option: sometimes it works out well, but with inflation it doesn’t.

If in fact inflation is taking root, cash will be a terrible place to be, just as it was in the 1970s until interest rates actually caught up.

We small investors have a huge advantage in treacherous markets – nimbleness, the ability to quickly make significant changes to portfolios. My advice is to watch all options you have, and “do whatever is working now”, but beware of traps and don’t get locked into any particular position.

A decision not to invest is an investment decision.

The yield chasers that buy a stock for its 3% dividend will be shocked when the stock drops 4% or more….in a week.

@Wisdom Seeker,

I differ with you, however appreciate your posts here, and I actually said – “I will stay on the sidelines for awhile.”

That doesn’t mean forever, and I’m evaluating several portfolios and strategies with a wide mixture of stocks, bonds, mutual funds, ETFs, or may just go back to trading commodities and options.

I just don’t like what I see in equities, and BoFa, Cramer, Jeremy Grantham, and plenty more believe this market is perilous, and my opinions are based on what experts believe, and the many crashes from ’87 forward I experienced – but this era seems very, very similar to the 2000 dot com burst.

“Irrational Exuberance” as Greenspan said in ’96 is also here today with retail investors making up somewhere between 13-20%, with WallStreetBets on Twitter making irrational/insane “bets”, and Bitcoin (based on popularity and hype) going over 50k, and the Fed buying it’s on bonds, plus more stimulus.

It all seems to me as underrepresented series of economic events that are a recipe for disaster.

Martok, great post. I completely agree about things being ripe for a disaster. At the individual level we each decide what to own, but at the macro level the assets are already out there – so many bonds, so many stocks, so much primary credit. When the bezzle gets revealed, or opinions about the future shift, those valuations can change fast – but the numbers of shares don’t change nearly as fast. Share issuance/buybacks, bond issuance & redemption are slow.

But – Federal action on the overall supply of primary credit (“cash” is a bankster euphemism) is the only relief knob. Cash can also be devalued fast – so cash isn’t really on the sidelines, it’s part of the playing field.

My big fear is that if the Fed and Congress make a few poor choices in a row, everyone may suddenly decide to “get out of cash” at the same time. That can happen even as bond defaults soar, because the available cash is badly maldistributed. This is an Everything Bubble, so things could easily get far messier than in any crash since maybe 1929.

I don’t think anyone can know how that will play out, so we’ll all have to be very tactical. Just want folks to keep in mind that cash may no longer be a flight-to-safety escape hatch.

@Wisdom Seeker,

Nice post and you hit it right on the head as this being a “Everything Bubble”, and if the Congress and Fed make a couple bad choices in a row. We will see a 1929 collapse – IMO.

I read where UBS Warburg said to sell equities to a “Underweight” position, that was a while back, however Lance Roberts of RIA Pro said this week to sell into any short term rally this week, tighten stops, and to raise cash.

My sample portfolios of conservative, and moderate, that where pieced together carefully have taken a beating, and have left me bewildered, things are rotating and churning so fast that even the best say they don’t know what is going to happen.

And we haven’t even discussed UK’s statement of their economy being the worst in 300 years! – that will have a effect worldwide, it just hasn’t happened yet, this was announced Feb 12th, 2021

https://www.wsj.com/articles/u-k-economy-suffers-biggest-slump-in-300-years-amid-covid-19-lockdowns-11613118912

This is why I’m on the bench, however seriously thinking of going back to daytrading options, which isn’t easy, or put money into funds that do – using a small amount of cash.

IMO – this is a experiment that has never been done before, and that no one has any idea what will happen, – but it won’t end good.

Great advice and exactly what I’m doing…

WS – nimble is a trader sitting next to one of the bank’s Bloomberg terminals.

– Yields rise in a “economic expansion” and go down in “a recession”. No matter what the FED does. Yes, the 10 year yield went up but the 3 month T-bill yield kept falling. A sign that investors do see the risks (in the stock market).

– Rising rates is Always a counterweight to an economic boom. I’t’s simply part of the business cycle.

The 3-month T-bill reacts to where the market thinks the federal funds rate will be 30 to 90 days out. A freshly issued 3-month T-bill matures in 3 months. That’s the only time frame it reacts to.

Hey Wolf,

A bit off course here!

But can we have a Look at CHINESE BOND MARKET?!

I read an article recently on how the “ FRIENDLY EUROPEANS” are falling over each other to join China’s Bond market “SALE” :)

… and who can blame them, these instruments are fetching 3% !!

Something the average punter in the US bond market dreams of!

Forget the sovereign RISK!

if you’re investing in ( Junk rated corporate bonds) , who cares.

Be glad if you dedicate an article to the Chinese Bond market though. Cheers :)

Wolf,

At some point in the future, could you post longer term charts of the 1 yr and 10 yr T rates.

The Fed has been running ZIRP so long, the 5% to 8% rates of the 90’s are passing into myth.

Which is hugely dangerous, because any contemporary rise to such rates would annihilate any number of mkts now addicted to ZIRP.

And…those 7% rates were being paid by a country whose debt-to-GDP ratio was far, far lower than what it is today.

(A chart of US debt to GDP over the decades would also be useful/horrifying)

Thanks.

I don’t think the general public understands how hugely abnormal the last 20 yrs have been, from an interest rate perspective.

Wolf, I’d love to see something on the Chinese economy as well- if anyone can figure it out. I’m sure no one can- but your insights are very valuable. Seems to me the US is following and playing against the Chinese economy right now and maybe has been since 2012. At least, with housing prices in many parts of the world, and maybe, I think, the stock market as well.

Most of this is well over my head, but I find your articles give good information for someone not trained in economics.

I think some of the difficulty in assessing the economy is that much of the information we get is just inaccurate. This is a good place to find information.

I’m coming from a place of *hoping* the market crashes. The bottom part of the economy has already crashed. If the top half crashed maybe more people could find housing of whatever sort.

” Commodities, which are sensitive to the direction and strength of the global economy, will revert as economic growth slows.”

Already incorrect. The world still struggles with a pandemic…and Corn, Wheat, Soybeans, Aluminum, Copper, Lumber have done what? (hint: up more than 30%)

When cash loses its value, people buy things as a store of value. Economic activity may not have all that much to do with the prices.

historicus,

Agricultural products are in demand regardless of the economic environment, people around the world won’t stop eating!

Metals will largely benefit from the overwhelming case of the high state/s expenditure written in every country’s next 5-10 year budget DNA’s!

Note: that everyone’s investment time line is different, but if you ride the choppy waters, you’ll do great.

Precious metals like Gold and silver will always have their uses, though Silver is more likely to outdo Gold due to the really large commitments towards “ Greener” Energy sector!

Is it all a HUGE miscalculation in terms of the real cost of ( Green Energy)?!

Time will tell! As we’re borrowing from our Future incomes ( collectively).

Green energy investment is IMHO is all talk but nothing will materialize in the next 4 years.

B/c economic impact of forsaking fossil fuel is great in this ‘nascent’ recovering economy. look what happened to all the alternate energy in Texas – wind, EV vehicles, nuclear, natural gas++ Long way to go before they all become ‘economically efficient alternate to gren energy!

My proxy for them is an etf – ACES – still going nowhere!

Sunny 129

This is a replay to your comment below.

I concur with you in regards to a quick departure from fossil fuels is Not going to happen in a blink of an eye!

Nobody, and I repeat nobody is espousing a quick departure from fossil fuels for a simple reason and that is ( the oil market is THE LARGEST AND MOST LIQUID MARKET AROUND)!

Oil market is around $2 T , yup that is a T for Trillion dollar per Annum! { $1.7 Trillions }

The second largest market is Gold which comes in at roughly $170-200 billion dollars.

So yes, we’re Not going EV’s and Green overnight, regardless of MUSK’s propositions and his company’s largely inflated value.

On the other hand the whole of the NASDAQ is in need of a 30% haircut now!

So what would that do to the US Economy in the short term?

Do you think the money will immediately flow to more ( deserving sectors) of the economy?!

I for one doubt it.

There is never a correlation between what you as an individual believe and what the ( herd) seeks and believe!!

The market ultimately is like a big pond where all ( shitty light ideas and moves FLOAT to the surface) and are first to be seen by everyone and thought of as genuine ideas,

The real value however is hard to see at the outset and you need to dig deeper.

It all comes to the old adage that ( the market ultimately is a weighing machine) in the long term.

Higher rates…yes.

All the way back up to historical norms! So, higher from here, on a par with the financial history of this nation.

And what is that? Up to 2009, Fed Funds equaled or exceeded inflation.

So where would that put rates? Fed Funds around 2% now, and likely headed higher.

Call it Cloward and Piven model of breaking the financial system, or call it mere Socialism funding, but keeping rates below the inflation rate promotes…

1. Irresponsible debt creation to float the stock market

2. Irresponsible debt creation to fund Socialistic endeavors that could never be supported by taxes.

Just as Hayek noted, when central planners decide, they intend to help one sector at the expense of another. And since 2009, it is obvious who was intentionally assisted, and who was intentionally harmed. And thus we have why central planning in lieu of free market forces is harmful and unfair.

If inflation is north of 4 %, which seems likely,

the 10-year T-Notes’ real rate is -2.6 %, after inflation.

Which seems appropriate given the number of people living in tents,

unprotected, in a virtual war zone.

Look at all the armed guards on Capitol Hill;

Hugo Chavez & Chairman Xi would be ashamed to see that.

Once 10y yield is 1.5% and climbing – Watch out!

Matters little if the inflation rises slow or fast! Fed is betting on reflation trade with robust(?) economic growth in the post covid recovery – all Mary pass on vaccinations(?) and other hopium wishful thinking in the MSM/WAll St/Financial industry!

I hear the train a comin’

It’s rollin’ ’round the bend,

And I ain’t seen the sunshine,

Since, I don’t know when,

I’m stuck in Fiat Prison,

And time keeps draggin’ on,

But that train keeps a-rollin’,

On down to privation…

nice one BT,,, JC would be proud of your transliteration to the current reality from the one he was singing about and for!

Thought I heard that train a comin’

But it done got derailed

Was just the whistle wailin’

“Son, that freedom boat has sailed!”

Now you’re stuck at Hotel Prison

Where the walls are paper thin

But don’t worry ’bout feelin’ lonesome

The whole damn world is checkin’ in.

First inflation will be denied (we are here now)

Then inflation will be embraced as an achieved goal, and a sign of good economic activity

Finally the Fed will limp in with meaningless and ineffective 1/4pt hikes…

Since 2011, in the “no inflation era”, CPI up 20%. Were we really afraid of deflation?

The rate of change chart looks harmless, and they will show it to you all the time.

Remember, central bankers and most govt employees have inflation protected pensions…..what care they?

Remember the Fed is in CONSTANT violation of two of their THREE mandates under which they are allowed to operate.

Stable prices…they promote inflation (2-2.5%) which rips 22% to 28% off the dollar in ten years.

Moderate long term interest rates……moderate means “not extreme”, either way. 4000 year lows in long rates is “extremely” low. Why a “moderate long rates” mandate? So current generations can not wipe out future generations with massive low cost debt creation. Anyone sense this is going on? $20 Trillion in new national debt in 12 years.

I’m more concerned about the only part of their mandate that really matters and that they always ignore — full employment. The U6 is an ongoing scandal.

eg

” that they always ignore — full employment”

I dont think they ignore it at all…..a year ago, unemployment was 3.5%.

This is one of the big successes of the Fed. IMO.

Unfortunately, they never ever take the foot off the gas, exit, or retire.

I go to the trouble to reference the U6 and yet here you parrot the U3 right back at me?

Good grief.

There are many many job openings that are largely in technology related areas that Americans looking for work aren’t qualified for. How they are supposed to get all the education and experience (if they are even cut out for it) is beyond me.

The Fed is printing digits, not skills and knowledge. Good luck waiting for them to significantly fix employment issues. To what extent they rely on ISLM models to try to generate inflation and investment to remove “slack” the hope is that there will actually be low-skill jobs for all the low-skill Americans.

The average 30 yr fixed rate mortgage (not FHA) is 3.27, slightly lower than where it was this time last year.

They need everyone in a home that they can, Taxes on real estate will rise to heights no one is prepared for…..In SF we pay for a bunch of looney tune idiots that couldn’t run a day care center let alone a swamp infested city like this….Breed might be the most overpaid mayor in the world…..worthless and dumb

First of all I love Herr Wolf for his support of this website. Second of all the market is always right. Third of all if you use your emotions to view this market then you are wrong footed from the outset. The market is what it is. And it is composed of the trillions of transactions daily – therefore it is a continuous compilation of trades.

That is why I prefer to think of things in terms of liquidity preferences and conditional probabilities. The movement in the yield curve is clearly preferring short duration over long duration treasuries. And the short end is where the Fed has to monetize the coming stimulus wave. The curve is likely to increase (see $YC2YR in stockcharts).

Everything is a trade and you should think like a trader, rather than a philosopher if you are trading. Short term the stimulus money plus higher corporate profits in 2021 Q1 and Q2 will likely goose the equity markets ever higher. And then what? Who knows. But for now don’t fight it because you don’t believe it. That is philosophy and has no place in trading. The Hedgeye forecast is for two quarters Q1 and Q2 ’21 of higher GDP growth and inflation growth as well as robust corporate profits. After that things are likely to change world-wide. Stay nimble and watch the numbers carefully.

If 10y yield keeps climbing 1.5 and furtherm corporate earnings (beat the LOWERED bar as usual) means nothing. Bonds sell out will precede the ROUT in equities!

“he Federal Reserve runs the world’s largest hedge fund with over $7.5-Trillion in assets. Long Term Capital Mgmt., which managed only $100 billion, nearly derailed the economy when rising rates caused its collapse. The Fed is 75x that size.

h/t ria

This economy/Mkts is built on DEBT on DEBT with leverage. 20% of S&P are zombies. Many in Russel 2000 have gone up with NO earnings!

But, but this time is different, right?

Wolf,

Thank you again for your thought and facts. The market makers love this stuff. Money out of thin air. If there were no companies, what would they have, nothing! Big caps are the companies for me. The ones that pay, and buyback shares, the ones the market makers scoop up really cheap and sell to on the buybacks. I think that’s how it works, Wolf? A lot of leverage or borrowed money in this market. That is the biggest risk to me, one I don’t take. A lot of political risk coming up, market makers will be singing that for sure next couple weeks.

When the Fed buys things directly – UST’s, MBS, agency debt – how does it pay for the assets? It doesn’t send truckloads of paper currency over to the seller. I imagine it just sends over an electronic message that is registered as entry into the seller’s account. What are the mechanics of this? What legitimizes an entity’s electronic crediting messaging? Can you or I send such a credit message? What if the citizens of a country vote to delegitimize the recognition of the validity of an entity’s electonic credting capability? Is this possible?

The Fed buys these securities from its “primary dealers.” Here is the list of these broker-dealers (includes the largest US and foreign banks). These broker-dealers have accounts with the Fed. The Fed credits the money it created to their accounts in payment for the securities it buys for them.

Thanks, Wolf. But there is nothing in this transaction that is real, per se, just officially sanctioned digital crediting. Quite a lot of power for one institution to have its declaration that “now you have money” KAZAM! to be accepted as fact. Why can’t we all be able to do this, especially as the wisdom this unelected king is very much in doubt.

Crush…

Indeed. How is it that one person and his minions decide to expand the money supply of this nation by 27% in one year?

Remarkable power in a few unelected hands…and is it really in the scope of the Fed to do such?

Their primary function is to assuage liquidity issues, short term..and to behave consistent with their THREE mandates.

They are in constant violation of the second and third mandates.

The reason you can’t intervene in the fed payment system is because it is a closed system. Only recognized participants can play and they own the system literally. Also they are the only ones connected to the system literally. You are either an insider or out of luck.

Wolf,

You are leaving out the most important part…the Fed creation of money is,

1) not accompanied/tied to any incremental increase in real assets,

2) therefore the ratio of “money” to real assets simply increases,

3) creating the very definition of inflation.

We can debate the incentive/production altering results of changing interest rates by means of such changes in the money supply…but at the moment of creation of Fed “new money”…there is only inflation/debasement of existent savings.

That base dynamic cannot be restated enough and the operational minutiae of “how” more money gets created pales in significance.

I only bring it up because I think the vast majority of people care a lot more about the *impact* of Fed money creation than the specific mechanics of it.

The vast majority of what the Fed prints never reaches the money supply. It simply finances government debt.

Inflation is caused primarily by consumer debt. Every time you use your credit card, or take out a consumer loan you are creating money from thin air just like the Fed. That is the primary driver of inflation….

JDOG,

“The vast majority of what the Fed prints never reaches the money supply. It simply finances government debt.”

Aren’t you just ignoring “inflation push” one step back then?

1) The Treasury *could not* make that first step spending if there was no one to finance it. Treasury deficits have been the rule for 90%+ of the time for the last 50 years.

2) When the *Fed* has to step in to finance these habitual and/or emergency driven Treasury deficits (to avoid interest rate spikes that would trigger widespread default) the Fed is printing unanchored/unbacked incremental money out of thin air.

3) The Treasury/Fed are welded at the hip in reality (see, Yellen…but it has been the rule for decades)…there is essentially nothing the Treasury wants that the Fed won’t accommodate in practice.

If third parties (US citizens, foreign countries, etc.) think that DC’s macro policies/financial standing is/are all f*cked up and won’t buy Treasuries at less than, say, 8%…the Fed has habitually white knighted DC with printed money to keep rates at 2%.

4) This Treasury-Fed pocket pool means that for all intents and purposes, it is as if the Treasury (driven by spending policies) is really controlling money supply increases.

Jdog: Doesn’t the wages of all the government employees, contractors, etc. reach the money supply also, as these people go out and spend their wages into the economy? Also, those living on fat government pensions? I’ve always wondered how much this effects the money supply.

jdog said: “The vast majority of what the Fed prints never reaches the money supply. It simply finances government debt.”

_________________________________________________

It finances government debt that the government spends into the economy. and reaches the money supply.

If you know different please explain.

@Cas 127 – excellent points.

@Jdog, Borrowing money from the bank is not exactly the same as the Fed’s money creation ability. Banks practice fractional reserve lending. The Fed does not. And banks lend to others to buy things. The Fed does, too, but also directly buys things.

Imagine if your local bank, whose BOD was populated by RE investors, and whose managers also owned RE, decided to abandon fractional reserve lending, and to buy RE directly to increase RE demand and RE prices, and to increase the wealth of the bank’s BOD’s and managers. They would take title to a home seller’s property by keystroking numbers into the seller’s bank account. Kind of like the high school hackers who would get into the school’s computers, and change their grades from C to A. No hard work went into the grade “obtainment.” It is clearly illegitimate. But imagine if only a select few students were empowered to do this, and the grades would be regarded as legitimate. Everybody else has to achieve an A grade through hard work and stress, but these few lucky indviduals can just keystroke it in.

So why is the Fed allowed to do this? Why, for the greater good, of course. But as Wolf and many others are pointing out, it is not for the benefit of the greater good, but for the benefit of the 1%.

And so it is incumbent upon the 99% to disempower the money creation ability of the private bank.

Crush the Peasants! said: “Banks practice fractional reserve lending.”

___________________________________

Fractional reserve requirements are now zero.

This for CTP:

Thank you for this very clear explanation and examples of the current rogue behaviours of the banksters owned fed.

Been wondering how this kind of activity has impacted housing especially after we, as cash buyers, were unable to get any of the foreclosed properties owned by banks, PE, hedgies, etc., to accept our offers 5 years ago when we had to relocate to care for aged parents…

Of course it might take a while, but certainly seems to me this current situation will unravel exactly as did the crony corruption in the housing mkt and S&L biz in the 80s.

ElbowWilham:

Yes it does, the question is how much is new spending, and how much is debt service. Debt service is projected to grow to near a trillion dollars by the end of this decade and replace the military as the countries biggest expense. The money that goes to interest or maintaining existing government expenditures like wars and foreign aid, and entitlement programs, is not really inflationary, only what goes into new projects, jobs, or these latest give away programs…

Aren’t these part of ( TBTF ( TBTProsecute) BAILED OUT Banks by TARP program plus?

Fed will never let Banks go down. B.c without them Fed and therefore Govt CANNOT function. WE are beholden to Banking syatem, worldwide!

@ sunny129 –

FED will not let banks go down because FED is the banking system, NOT because Govt couldn’t function.

We are not beholden to banking system. We are their debt slaves.

“Can you or I send such a credit message?”

It is called writing a check.

Due to the political shenanigans, voting does not seem to work anymore. The fake accounting will end when people realize the (monetary) accounting is fraudulent.

Back around the turn of the century Enron was worth $70 billion. Two weeks later it was all worthless paper. Nothing real changed in those two weeks to affect the price. Only everybody realized the accounting was fraudulent and they quit buying and tried to bail out.

The fraud in the financial system (the world’s accounting system) will end when people realize that it is fraudulent. Then we will see lots of $70 billion dollar investments melt into nothing.

It is not the same thing at all. When I write a check, I have money in an account backing up the check. That money was not created on a whim, but typically the result of the money being earned through labor or other means.

I cannot write a check (legally) on an account that has no money in it, nor wire transfer money from an empty account. And I cannot say, SHAZAM!, there is now money in my account, and now in yours, too.

If the bank is willing I can promise to pay the bank some amount of money, sometime in the future, and with interest. Then, SHAZAM, there is new, unearned money in my account. I can then write a check to anyone with that money. I can even make payments to the bank with some of that new money. For a while. ;-)

The money is only as good as the resources it can buy. Therefore, from a policy standpoint Congress should pay close attention to prices. There is one resource that is in large deficit, employment of labor. And that means suppressed incomes. Suppressed incomes don’t support higher prices. Quite the contrary. And private debt is already perilously high. That’s the formula for debt deflation, which economist Michael Hudson predicts. Raising the minimum wage will help somewhat. As for bonds held by the Feds, they can be marked down to zero by next Friday.

“Raising the minimum wage will help somewhat.”

Yes! Let’s raise it to $1 million dollars per hour. Then we can all be millionaires and we will have to work only one hour per year.

Seriously though, if you want to help the working class then quit taxing wages, salaries, and tips. That’s the ball and chain on their leg.

Just as important, quit inflating away the value of their savings. And quit encouraging debt that makes the working class debt slaves.

Raising minimum wage will just increase unemployment. Walmart, Target and Amazon can only employee so many at $15.

There are many cities and states that have raised their living wages far above the national min wage. It has not led to increased unemployment. The data is pretty clear on this. This is no longer a theoretical issue. It has been done for years, and we can look at the data, instead of making up stuff.

As long as the US has limited demand for labor and unlimited supply of labor (legal and illegal immigration and offshoring), there is no real labor market at the lower end. It’s a system of wage repression. Hence the need for a minimum wage. Consumers that are paid more consume more. It’s as simple as that.

That said, I would prefer local and state living wages that are appropriate for the local price structure, rather than a federal min wage. A person working in a small town in Oklahoma doesn’t need the same minimum wage as a person working in San Francisco.

Consumers that are paid consume more as long as prices don’t go up. If prices rises match pay raises, then things equal out, except that those on fixed incomes now get to consume less.

Also for every dollar in increased income, a larger number of dollars of debt can be serviced.

Landlords and Asset Owners love any kind of inflation, minimum wage raises (and all the subsequent wage raises). Inflation is good for them.

And if open borders are enslaving a portion of the population, then the answer is to stop the open borders,

cb,

So it’s OK if executive salaries, bonus, and stock compensation packages multiply and reach tens or hundreds of millions of dollars, and are printing billionaires, and that’s not triggering any kind of inflation, and then when the pour schmuck gets a $3 an hour raise, the whole world falls apart?

I agree with your last statement. It would solve the minimum wage issue. You wouldn’t need a minimum wage.

@ Wolf – “So it’s OK if executive salaries, bonus, and stock compensation packages multiply and reach tens or hundreds of millions of dollars, and are printing billionaires, and that’s not triggering any king of inflation, and then when the pour schmuck gets a $3 an hour raise, the whole wold falls apart?

________________________________________

It’s not OK with me. A free market (and a free people) have to be vigilant against concentrated wealth and power. We have been co-opted by Corporatism, the FED, Wall Street, our political system, etc. We let concentrated wealth rule, not to mention the means to capture much of that wealth through the creation and preferred dispensation on money created from nothing. End the FED.

(That’s why I refer to Greenspan, Geithner, Paulson, Bernake, Yellen, Bush, Obama, Jamie Diamond, Goldman Sachs, Buffet, etc. in less than positive terms. Why they be given a pass if their actions have been detrimental to the fabric of the country?)