From crisis to crisis, and even when there’s no crisis.

By Wolf Richter for WOLF STREET.

The Fed continued to add to its heap of Treasury securities at a steady rate, thereby monetizing that portion of the US government debt. It also added to its pile of Mortgage Backed Securities (MBS). But five of its SPVs (Special Purpose Vehicles), designed to bail out the corporate credit market, expired and are on ice. Its repo positions were unwound at the end of June and remain at zero. Its foreign central bank liquidity swaps, designed to provide dollars to other central banks, have matured and fallen out of use except with the Swiss National Bank.

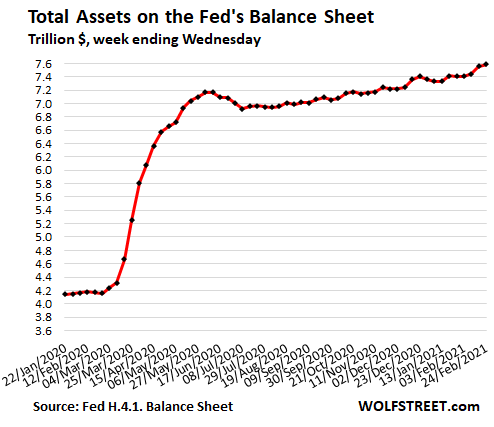

In total, the assets on the Fed’s weekly balance sheet through Wednesday February 24 rose to a new record of $7.59 trillion.

This is a mind-boggling amount of QE designed to repress long-term Treasury yields and mortgage rates – which have nevertheless been surging and sending the crybabies on Wall Street squealing for more QE:

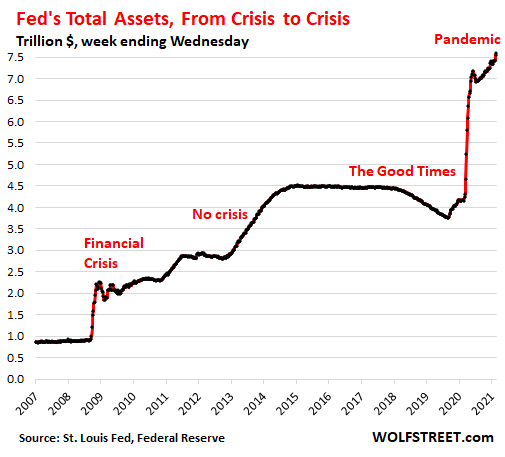

For your amusement, here’s the long-term view of how far the Fed has pushed it strategy to bail out and enrich the asset holders, treating the biggest asset holders to the biggest enrichment and creating in the shortest time span the largest wealth disparity ever, crisis or no crisis:

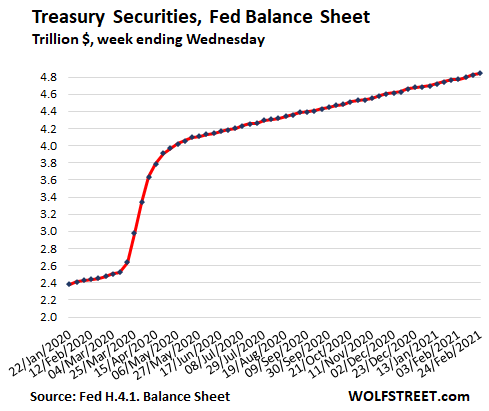

Purchases of Treasury securities do heavy lifting, hit $4.84 trillion.

The Fed has been adding around $84 billion a month in Treasury securities since the huge binge in the spring. Since the beginning of March, its holdings have nearly doubled, ballooning by $2.34 trillion to $4.84 trillion:

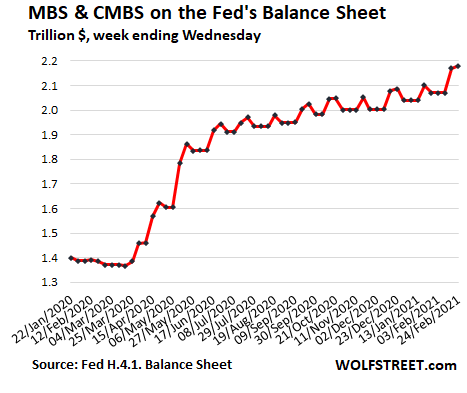

MBS zigzag higher to $2.18 trillion.

Mortgage-backed securities differ from common bonds in that all holders of MBS receive pass-through principal payments when the underlying mortgages are paid off, after the home is sold or the mortgage is refinanced. The Fed buys large amounts of MBS in the “To Be Announced” (TBA) market, to replace the pass-through principal payments and then to increase its balance. Since trades in the TBA market take months to settle, the timing differs from the pass-through principal payments, which creates the zig-zags in the chart. The Fed also sells MBS outright:

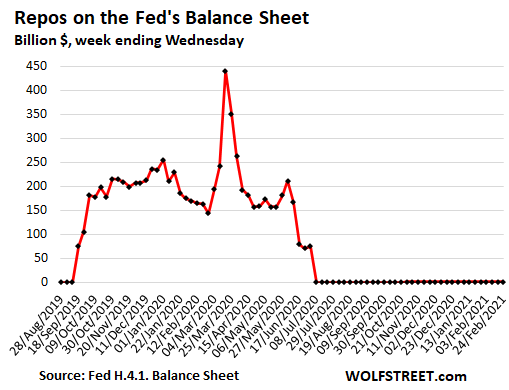

Repurchase Agreements (Repos) at zero:

The Fed continues to offer repos but has raised the rates to where there are better deals out there, and no one is taking up the Fed’s offers:

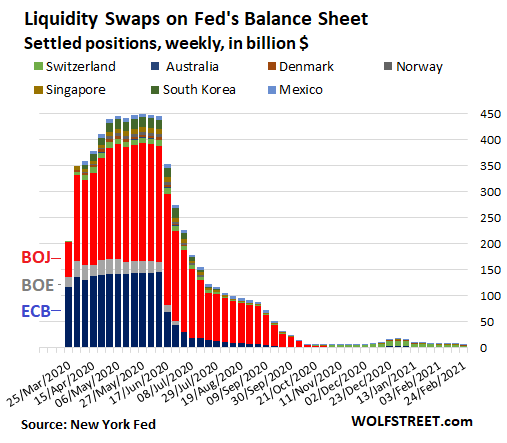

Central-bank liquidity-swaps almost at zero.

The Fed offers dollars to a select group of 14 other central banks via its “central bank liquidity swaps,” in exchange for their currency. Nearly all of those swaps have matured and were unwound. Only $6.8 billion were still outstanding, over half of it with the tiny Swiss National Bank:

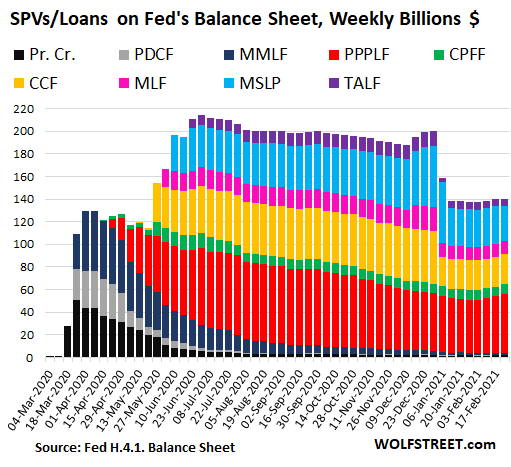

SPVs on ice, at $140 billion.

Special Purpose Vehicles (SPVs) are legal entities (LLCs) that the Fed set up and owns as a way for it to buy assets that it is not allowed to buy otherwise. Equity funding is provided by the Treasury Department, which would take the first loss on those assets. The Fed lends to the SPVs, and shows these loans and the equity funding from the Treasury in these SPV accounts.

On December 31, five of the SPVs expired – PMCCF, CCF, MLF, MSLP, and TALF – and they’re now on ice. This shut down the corporate bond buying program entirely. But the Fed had already stopped buying corporate bond ETFs in July and was only buying a smattering of corporate bonds anyway. Total amounts of the SPVs combined remain at about $140 billion, $52 billion of which are PPP loans that the Fed bought from the banks:

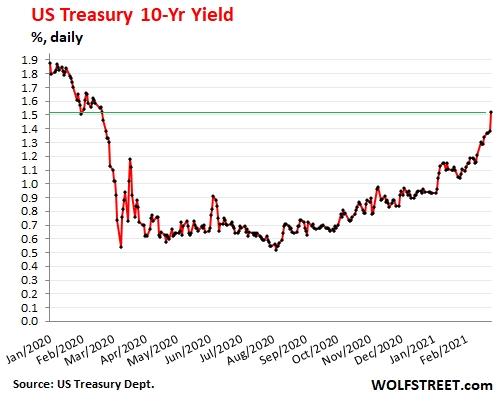

Despite massive Treasury purchases by the Fed, the 10-Year Treasury yield spiked to 1.52%:

Creating ominous rumblings in highly leveraged hedge fund circles, the 10-year yield spiked on Thursday to 1.52%, the highest in a little over a year, and nearly tripling from August, despite the Fed’s massive QE. Wall Street is not amused:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Oh well, nothing we can do about it, nevermind heh.

Looks like it is going to be a sunny day.

Automatic trading machines ( CTA models ) are shorting

T-bonds because they (foolishly) believe that the “market”

can/will react to rising inflation.

Fact is, the government sets interest rates,

even on the long end of the yield curve,

& they can’t/won’t allow higher rates.

& they can’t/won’t allow higher rates.

This is going to be the biggest short squeeze ever;

T-note rates are poised to hit zero and beyond.

How do you invest in these?

I don’t think there’s any appetite for negative interest rate here. It’s been tried in Europe and so far the result’s been ho hum.

Who gets hurt the most under a negative interest rate regime? The banks.

Who owns the Fed? The banks.

Keeping the treasury bills’ interest rates below the real inflation rate, as they are now, can only be done by monetizing more and more of the national debt as it has to be rolled over. In other words, the “Fed” has to buy enough of it that its rates remain low. Otherwise, investors may demand higher rates as they start to notice the inflation ongoing, e.g., from the (not federally owned) “Federal” Reserve banksters cartel’s bailout of the banksters by purchasing their $2 TRILLION in MBS in 2019-2020.

If they notice it, and Shadowstats’s Alternate Inflation Charts show the real annual inflation rate at 9% to 7.5% currently, and hyperinflation then begins from all the money printing (read about Zimbabwe and the Weimar Republic), the “Fed” cannot monetize all of the debt. If it tries also investors may demand even higher interest rates for all other bonds, so hyperinflation may kick off the corporate collapse prematurely as huge numbers of corporations cannot pay the interest rates demanded to roll over their gigantic debts.

This is going to be the largest squeeze of all hard working ordinary people ever;

C- note purchase power poised to hit zero and beyond.

It is just unbelievable how reckless central banks and governments have become. Parts of the economy are already overheating but $1.9T stimulus is coming (most of it has nothing to do with Covid) and central banks worldwide are still pedal to the metal while real rates are negative while having bubbles in stockmarket, housing, junkbonds, crypto and well, basically everything.

Thank you Wolf and all commenters: i swear that coming to wolfstreet is the only thing you need for making sense of the current big picture dynamics.

I’ve said it in the past: who needs a economics degree when all you need is Wolf Street? Been following for about 2 years already, and I’ve learned more here than you’d imagine. And it’s not just from Wolf: it’s from all the commenters. Google brought me here back then. We were all selected out from the Matrix. : )

Best to all of you! And thanks Wolf for your leadership!

Yes indeed!

The eye opening chart, which should be a center-point for future textbooks on the history of economics & the dollar, is ‘The Fed’s Total Assets, From Crisis to Crisis.’

One sees where the madness begins; 2009.

Dan, from a policy standpoint it all started in 1987 on October 19th when Greenspan created the now infamous PUT of flooding the markets with liquidity during the Portfolio Insurance crash that Black Monday. It was indeed a Black day since we have not had true price discovery in our financial markets since. Government interference in free markets has never been a long-term solution for anything.

It started in 1995 with the Reverse Plaza Accord where US, Japan, and Germany colluded on monetary policy. The Fed was to lower short-term rates and the other two central banks were to purchase long-term US treasuries. Japan also started QE The goal was to boost Japan and post-NAFTA Mexico export their way out of recessions. That led to an Asian currency crisis in October 1997. Hence, Japan stopped QE the following April which led to the October 1998 bear market. The Fed took up the mantle from there till 2000.

Japan restarted QE in 2002. Japan and China were big buyers of US treasuries. After Japan stopped QE in 2006 and Japan and China dumped their MBS in 2007, the next crash ensued.

There was a lot more effective QE’ing going on. After 2008, the deficits became much too large for FCBs.

Is it possible to catalog the beginning of madness?:

Or did it start with Bernanke’s speech in 2002 with his final solution: Send out the helicopters and sprinkle the earth with cash. Be sure to concentrate over the rich zip codes.

He (and Milton Friedman too) might want to reconsider whether he should have been so apologetic for the Fed because the Fed then didn’t have the wisdom to try this “obvious” solution in 1930’s.

What did work then was WW2 that was able to finally make it politically possible to pry open the wallets of the rich to finance the war and employ many people. Which also caused much improvement in USA wealth distribution that help set the economy right again.

Wolf, perhaps you could put up a long-term historical version of that graph, on a log scale, where every doubling shows up equally, not just the last few.

Looks like the historical FRED data series are TOTRA and LTOTL.

The Fed started in 1913 or so, with the balance sheet accelerating through World War 1 and stabilizing from 1917-1933. The Great Depression led only to a gentle, steady ramp upward through the end of WW2. There was stability in the Fed balance sheet from ~1945-1960 except for a tiny ripple associated with the Korean Conflict. Then in 1960 a second steady ramp upward began, which lasted for nearly 50 years, through 2008.

Amazingly enough, there were no ginormous Fed-financed bailouts during the entire Great Depression, World War 2, or all the oil/inflation crises of the 1970s.

Something did in fact change recently, in August 2008, and not for the better!!

I think history will show that the recent “printing up credit to deal with adverse economic events” is a huge mistake.

In finance, log charts only make the problem appear less terrible than it is. Never ever use log charts with things that are denominated in currency, never, ever. People need to know what’s really going on.

Nah DR, you and the others on this sub thread, or whatever the proper name these days, Are Wrong about start date :

#1 WORST OF ALL TIME,,, 1913, when the banksters, etc., were able to FED US, and somehow have kept on FED ing us since,,,,

in spite of all logic, reason, reasonable conclusions, etc., etc.

#2 1970 ish, when Nixon made some kind of ”executive decision/proclamation” to take USA off gold standard.

ALL, and I do mean ALL of the BS and degradation of USD and incomplete/incorrect wages adjustments, ETC., ETC.,,,, have followed from those two very very bad events.

Just examine closely the USA penny it took to buy a decent loaf of bread in 1900 compared with the 4 or more USD today…

Many many many equally bad and/or very bad similar examples OF INCREDIBLE degradation of USD and the delta between real/actual cost of living and lies, damn lies, and, especially, ”official” statistics regarding that degradation.

25th of February 1927, with the passage of the McFadden Act is when Pandora’s box was opened. But the scale of, and arbitrary actions since 2009 are an order of magnitude different IMO.

I learned a lot from the replies. Thank you fellow commenters.

Wrong, wrong, wrong. 1886-Santa Clara County vs. Southern Pacific Railroad Company.14th Amendmt. Equal Protection extended to corporations. Every move since came from that unnatural birth and serves but one master. Fed is just another tool to get to where this is going.

You are all wrong. It started on January 7, 1782 with the Bank of North America promoted by Alexander Hamilton – the original author of all the banking shenanigans we continue to suffer. See also: First Bank of the United States, Second Bank of the United States, Federal Reserve Bank – all private banks. The People have been snookered for centuries.

Ditto Up North… I especially like the anecdotal comments concerning financial/economic conditions from various locales.

in spite of your usual wit and wisdom on her YS,

there is nothing new or recent about the recklessness of bankers and guv mints these days…

considering that most of the wars by any name, from ”police actions” to crusades, have been at least financed if not instigated by banksters for eva and continuing, not to mention the overthrow of elected guv mints and despots, so that bankster should be advocating petals and pedals and so on now cannot be any surprise,,, especially since all such stimuli will end up in their pockets sooner and later no matter to whom such monies are sent initially

owners of central and other banks have been interfering with the democratically elected guv mint of USA at least since the founding of our country, in spite of the attempts by many early on to prevent their takeover of our financial systems; since 1913, those same folks have been degrading the USD without suffering any of the consequences incumbent on WE the PEEDONs, as has been amply commented on here…

1.9trillion$ is only the amount from the current proposed stimulus bill.

It is estimated that the current deficit ( without the 1.9trillion ) will be 2.3 trillion, so the total for 2021 will be 4.2 trillion $.

The question that I consistently ask is who is going to buy this debt at current interest rates, when any buyer is guaranteed to lose money in real terms?

Only one the FED. And when this happens , we will be on a slippery slope to a currency collapse.

“It is just unbelievable how reckless central banks and governments have become.”

Because they know when they stop doing what is responsible for bringing us to this point, it all falls apart. They are trapped.

“nothing to do with Covid” while blamed on covid is the key point.

A rush to change everything does not indicate creation which requires thought, test, planning, and consensus; but destruction.

Bonds are signalling inflation….Hurry sell Gold!

Maybe ‘when’ YCC is announced the ensuing Silver rally to $38/oz will drag Gold along for the ride; at least until DXY see’s 86 and the Monkey Hammer comes out.

Just a little reminder of what that monkey hammer looks like…

Notice the action while US & UK banks just happen to be open at the same time?

Addendum: Did you know that without Gold to hammer all these years to prop up DXY, the US Dollar would have crashed long ago. A high Gold price is the Fed’s dry powder.

u apparently have no idea of the reserves of silver around the world,,,

same mistake that those TX bros made when they tried to corner the global silver market, on and within some of us might have made some serious dough

” certainly, for sure”, a lot of that dough was hard baked,,, but most, as usual and almost always, was just ready for the oven that followed when mother RU started letting go of some of its hoard.

I believe their is still some belief in the old old saying, something like those that ignore his or her story are very likely to suffer it again…

The mistake the Hunt’s made was not appreciating that the owners of the exchange could move the goalposts unilaterally. They naively expected a fair game. Notice to all outsiders – be very, very, very careful with purchases on margin.

Lisa_Hooker,

“They naively expected a fair game” from others when they themselves were trying to corner and manipulate the entire silver market for their benefit? That’s hilarious. Not sure if you meant it to be hilarious. But given the purposeful hilarity of many of your other comments, probably you did :-]

For me, a “fair” game is one where the rules stay static until the end of the game. The Hunt’s crashed silver corner was just an early example of “dynamic rules.” That was private manipulation. The Government got into the “fixing” business when Greenspan started changing more serious rules in mid-play around the later 90’s and early 2000’s. As we can clearly see today the “rules” are now “re-fixed” with regularity.

Yeah, that’s why I don’t buy the whole stock market is reacting to inflation expectations story. It’s a bunch of psychos that actually seem to believe any day now the real economy is going to explode in a massive growth spurt. Otherwise gold would be going up way more and no one would be holding any kind of sizable bond position. Maybe they are finally dumping bonds since they figured the math out on that one and the Fed failed to pull out negative rates for the continued bond price blowout? With financial repression how are you supposed to rationally determine how to react to any of this? Every day it seems like there are fewer incentives to be sane. They’ll reap what they sow. Looking forward to a bunch of red and blue vikings frothing at the mouth and running around nyc next.

Oh I forgot, pardon me, bitcoin and houses are the only valid inflation hedges.

the biggest winner of debt money is government.

Government spending in the United States has steadily increased from seven percent of GDP in 1902 to almost 40 percent today.

Back in 1900 government spending was a modest affair. Government pensions were almost non-existent, health care was 0.26 percent of GDP, education was 1.1 percent of GDP, defense was 1.6 percent of GDP and welfare was 0.11 percent of GDP.

Over a century later in 2018 the five major functions dominate government spending in the United States. Government pensions: 6.70% GDP; health care: 7.77% GDP; education 5.32% GDP; defense: 4.20% GDP; welfare (other than health care): 2.16% GDP. That is 26 percent of GDP out of the total government spending of 34.9 percent GDP.

Back in 1900 all government programs other than pensions, health care, education, defense, and welfare amounted to 4.6 percent of GDP. Today, police, fire, infrastructure, and all the rest take 9.1 percent of GDP.

The defense establishment that sent the White Fleet around the world before World War I was tiny, compared to the defense establishment of mid century. It was about 1.25 percent of GDP.

https://www.usgovernmentspending.com/past_spending

Leonard E. Read, the founder of the Foundation for Economic Education in 1946, used to say that Americans live in a country in which various levels of government extract over 40% of their productivity, yet they call this system freedom.

“They don’t know the difference between freedom and coercion.”

I recently read an estimate that the government is responsible for 27% of income. Very close to your estimate of 26.%. Congrats

Well thought. Please extrapolate the situation in 20 more years.

For awhile now I have been wondering why joe was putting Yellen into Treasury. Clearly joe and Janet are up to no good. That is a given!

I think it is becoming more clear what Janet is planning to do. At the end of March the Treasury is planning on reducing it’s balance sheet at the Fed to less than $1 trillion from over $1.5 trillion. This means about $800 billion or so of short term US T-bills will not be renewed and will be allowed to expire.

What this means is whoever currently owns these T-Bills will not be able to safely park money at the Fed. They will have to find another home to park their unloved cash. Probably they will try depositing this cash with commercial banks. The commercial banks will probably not want the cash.

At the end of March special commercial bank exemptions for parking excess reserves at the Fed will supposedly end.

The likely upshot of this is that the commercial banks may refuse these deposits to avoid getting into trouble with their capitalization ratios with respect to their excess reserves held at the Fed. I think the commercial banks got into trouble with these ratios during the repo crisis a while back. They got the temporary special ratio exemption during the repo crisis.

Right now only Britain and the US do not have NIRP. The bank of England has said it expects (hint) NIRP later this year.

Clearly Janet wants NIRP too, but she has a problem in that all commodities are priced in USD. She can not allow the Fed’s interest rate to nominally go NIRP because it would instantly put the entire commodity market into “backwardation”!

She does not want to give this unloved cash a new home in the commodity market! She is trying to trap this money and force it into riskier financial things. Of course the owners of this cash want safety and no third party risks!

I told you she is likely up to no good!

Since the Fed can’t officially go NIRP, her moves at Treasury are designed to have the commercial banks impose negative interest rates on large deposits of USD that can’t find a home in a suddenly reduced world of US T-Bills!

Naturally foreign holders of USD will sell USD to try and find a safe harbor elsewhere reducing the value of the USD, another of her objectives!

I am still not sure exactly what the recent rise in US interest rates plays in this scenario. Maybe the markets have already sniffed joe and Janet out and we peons are only finding out after the fact.

Only time will tell if this is her plan. If it is then the commercial banks are really going to have more to be pissed off about!

When you can change the rules there is no goal.

Very deep if you consider the above like a game of soccer.

And indeed, the rules have been changed. Powell just told us that there is no inflation, but he keeps changing or doing away with the metrics that track inflation.

M2 is closely watched as an indicator of money supply and future inflation, and as a target of central bank monetary policy. On Feb 22, the Fed stopped tracking the M2 Money Supply. It’s almost as if the Fed doesn’t want to track inflation. The Fed has also tweaked it metric for gauging unemployment to make “full employment” more difficult to obtain. More justification, so that the Fed can keep on pumping QE

“Its foreign central bank liquidity swaps, designed to provide dollars to other central banks, have matured and fallen out of use except with the Swiss National Bank.”

And what might the Swiss National Bank be doing with those dollars?

“SNB Held U.S. Stocks Worth a Record $141 Billion Last Year. (Bloomberg) — The Swiss National Bank’s portfolio of U.S. equities rose to a record $141 billion as of December, reflecting a buoyant stock market.”

It’s pretty much along the lines of what Apple did with the super low borrowed money it got from the Fed, when the Fed was buying Apple’s corporate bonds. Apple used that money to by US stocks (its own stocks). Was there something in the Fed’s charter that allowed it to buy corporate bonds? Who knew?

As the 10-year yields increase, it only makes sense for investors to sell bonds and buy stocks. It appears that everything the Fed has been doing, has been favoring the stock market. Got to keep the illusion of that “wealth effect” in place, or things could get ugly for Wall Street.

Actually, higher yields should attract money into bonds, but the ugly reality of Default or Credit Risk AND Dollar Devaluation AND Inflation Risk have global investors thinking twice about buying our self-destructing Paper. Welcome to the Banana Republic of America where corruption and self-dealing are now an accepted way of governing.

“Actually, higher yields should attract money into bonds”

Actually not. If one buys bonds when rates are expected to rise, then the value of his “investment” is heading in the opposite direction. On the other hand, if one has bonds that were bought when rates were near all time lows, then he/she sells to lock in those gains.

rich

‘As the 10-year yields increase, it only makes sense for investors to sell bonds and buy stocks’

Yield on 10y is rising:

– b/c Economy is recovering?

-Inflation with economy recovering?

-inflation WITHOUT economy recovering? = STAGFLATION?

rich

‘On the other hand, if one has bonds that were bought when rates were near all time lows, then he/she sells to lock in those gains.

Only those who bought ‘individial bonds’ but NOT those MF Bond funds or ETF bonds!

They don’t call her Yellen the Felon for nothing. Per her Citadel buddies and the rest of her oligarch vulture friends- she now has grabbed over $14 million for herself.

Powell is the richest Fed Chairman ever: well over $50 million for his piggy bank.

Guessing he doesnt have his money in the bank….

the way he gooses the stock market.

We should all remember, despite the promise of our government (the Fed is now part of the government IMO) that those who pass things and dictate to us must also feel the full effect of their policies…

those in the government (and Fed) all have inflation protected futures…courtesy of us. But what of us?

Criminal behavior at best. Bernie Madoff scamming looks like small town peanuts compared to this Fed nonsense going on now.

@historicus

Sorry but I think you have got it backwards the Government doesn’t run or control the banks. The Bankers and Banks run the governments of not just the USA but the world.

Wes,

I think you are saying a lot of potentially important things here (although bank waivers can always be extended) but the density of your ideas may be leaving some of us to catch up.

Could you maybe make two or three additional posts, each focusing on a portion of your original post, and restate/expand upon the points you are highlighting.

For me, it helps if you tie upcoming changes to proposed mkt implications (ie, please elaborate/step through a bit on cause and effect).

Thanks.

I do think you might really be on to something with regard to various macro interlinkages (NIRP causing problems for commodity mkts, etc) but you have packed a lot of ideas in a short space.

WES,

In simpler terms: Starting last March, the US Treasury borrowed something like $4 trillion by issuing $4 trillion in Treasury securities. It spent some of the proceeds on stimulus programs bailouts and regular gov deficits and it parked the remaining cash in its checking account.

The Fed is the bank of the US government, so that’s where the cash sat (the US Treasury General Account is a liability on the Fed’s balance sheet). The government has now decided to spend down this balance in its checking account and bring it back to near-normal levels. “Normal” used to be in the $100-$350 billion range. In other words, the government is going to spend this cash it had borrowed a year earlier. That makes total sense.

The government already started doing this. The US Treasury General Account had peaked at $1.8 trillion in July. It is now down to $1.53 trillion. And the government is going to draw it down by another $1 trillion. That’s how it should be.

So, outside of some minor dislocations, I don’t see an issue here.

Wolf,

Can the treasury spend these funds without a corresponding appropriations bill from the Legislature? Or is it used to finance previous appropriations?

1. No.

2. Yes.

It has ongoing appropriations to spend (fiscal year started Oct 1). And now there’s the $1.9 trillion stimulus package making its way through Congress. So there will be plenty to spend over the next few months.

Non sequitur, those holding MM accounts will move further out the curve. That is the nefarious plan. NIRP was yesterday. China is shrinking credit, and even rates in the EU are showing signs of normalizing. The US central bank may be the last CB to normalize. Figure that one out you win the prize.

Wes,

I keep saying it’s a new world. Great post! I’m no longer a believer in the bubble theory……monies going to find a home, some ups and downs and moving from one spot to the next but they are up to something!

C

Where do you see this going? What is the inevitable here as we see the govt double down on QE? I see the fed as a cartoon riding a train headed straight for a brick wall while painting a fake tunnel up ahead. Yellen/Powell claim they know how to stop hyperinflation from occurring but I have a sneaking suspicion they aren’t being straight with us on a few issues…

I’m trying to understand when and what the consequences of this train wreck are going to be so I don’t get screwed again somehow like when I came of age in ‘08 as a teacher with no positions to even apply for. I just want a home for my family which is impossible here in San Diego even though my husband makes an above median salary in healthcare. Could all of the fed’s terrible band-aid moves eventually crash the over-inflated real estate market?

Thank you kindly for the education from a social science major that refused to take economics classes- I’m trying to learn now and finally someone is giving it to me straight.

LD:

I am no expert! I always seem to be behind the 8 ball!

I agree with you that the powers to be always print more money because that is the only thing they know how to do! They couldn’t fix a plumbing leak if their lives depended on it!

My guess is if the USD is devalued then the “nominal” prices of real things like real estate will go up, when priced in USD. That does not mean the value of real estate will go up. It just merely means you will need a bigger wheelbarrow full of paper money (worth less) to buy the same house!

I do know the US government can not afford to let interest rates rise because they are the biggest debtor. How they go about keeping interest rates low or even drive them negative remains to be seen. For sure we will pay the price for all of this because they sure aren’t planning on paying!

I sure don’t envy your situation. I am over 65 but I have a 24 year old son and 20 year old daughter, still living at home, so they are just a decade behind you!

Thank you for your response Wes. Maybe we should all be investing in wheelbarrows… I think you’re right about us paying the price as that’s what happened in ‘08. Wish we were making it better for your kids’ gen too..

“investing in wheelbarrows”

And don’t forget to buy a wood cook stove for burning those bundles of dollars…

Wes: thanks so much for your thoughtful posts, and thanks LD for your interest in this topic. I have been thinking about where all of this debt-out-the-wazzoo(as Wolf likes to say) ends for some time and, to be frank about it, it is scary. The only thing that I can conceive of is that the Fed and many other CB’s will find a way to destroy money (sovereign debt), just as they have created money to purchase sovereign debt. What is the least painful mechanism for this, you say? Not sure, but something like a zero coupon perpetual bond is an idea. Issued by Treasury and electronically bought by the Fed (ie. By Printing more money), these bonds pay no interest and are never paid back. Because they are worthless, the Fed does not need to account for them on its balance sheet. Treasury then uses these funds to buy and then retire sovereign debt, thereby improving the country’s balance sheet and helping to close the deficit gap. Amount could be for whatever Janet decides…$6,8,10,15 trillion. Repeat the same idea at exactly the same time and in agreed proportions amongst all sovereigns and CB’s (because all major countries are in the same (or worse) boat) and the entire world expunges alot of sovereign debt…poof. Crazy idea, you say? Maybe, but various sovereign governments, the Fed, and all CB’s have painted themselves (and us) into a terrible corner that they and we cannot get out of.

Interesting for sure. Sovereign debt is a central government’s debt. It is debt issued by the national government in a foreign currency in order to finance the issuing country’s growth and development. I do fancy the idea of a way to just make the debt vanish like a loan to a friend you never really expect to get paid back. Certainly an idea I am sure the bankers and government have looked at in detail

A guaranteed formula for the destruction of the dollar

No matter what gimmick you use – perpetual bonds, trillion dollar coins, or whatever – it is monetization. And unless the dollars are fenced in imaginary game assets like stonks, bonds, bitcoin, or WoW magic swords it begets inflation.

Dollars have to be destroyed. Most probably by destroying businesses, property, and lives and buying at $0.01 on the dollar. No safe havens will be allowed. Gold confiscation, bitcoin made illegal, property taxes increased 10 times, domestic “terrorists” imprisoned for slave labor.

If you have a variable interest rate on your debt you are screwed. If you have a fixed rate, debt jubilee. If you have no debt you are already ahead. If you are drowning in debt you are also ahead.

It might be a good idea to have sufficient debt, allocated to non-recourse hard assets, to offset about 4/5 of your dollar savings. That way if they do blow up the dollar, as they have been steadily doing for 50 years, you can use the worthless dollars to pay off your debt and you still have the hard asset.

Ahhh thank you Jacklyn this makes sense. We’ve been working on getting our debt down to $0. Almost there!

LD… good on you for trying to learn. Particularly in a field that you know is not your natural home. These topics are not easy and there are no “inevitable” answers as to what comes next.

I will say this as a former business professor, “normally” what happens when a country devalues its currency this way is that you get inflation. LOTS of inflation. So no… real estate prices do not crash because the prices of all tangible assets hold steady or go up. Moreover, people who own those assets/properties have an incentive to hold onto them… which creates shortages… which drives prices higher. If you have a 30 year mortgage on a property then you would be sitting pretty because when the inflation rate rises above the mortgage rate it is the lenders who are getting hurt rather than the borrowers.

What has been holding inflation back for the past ten years or so is the weakness in the labor markets. When people cannot ask for raises without fear of their jobs going overseas, they just don’t ask for raises… which holds the inflation rate down to a considerable degree. Wage increases were starting to hit the marketplace in 2018 and 2019 so they may come again once the economy starts to rev up following the COVID vaccination program.

Frankly, if you do not already have a home in San Diego then I would try to buy whatever I could afford right now or I would move somewhere else altogether. Finding jobs is not that difficult for teachers and medical professionals in most locations. But you may have family obligations or some other reason that ties you to that area.

I know that San Diego is a tough nut to crack house-wise… I had a friend from high school who lived there in a 1200 sq foot house that cost four times what I pay for my 1400-sq foot house in the South… and she was a medical researcher with an attorney for a husband. They moved to Bethesda, MD and are now living in a McMansion on their combined incomes… with two daughters in college no less!

Bethesda, MD prices ain’t exactly bargain basement, either. According to Zillow, “the typical home value of homes in Bethesda is $1,036,594”.

Yeah… I think she lives in some ex-burb area. I looked her up on Facebook an hour ago and her house has sort of that two-story Colonial look to it that is common in East Coast suburbia… so maybe not a McMansion. But my point is that her family’s income was able to handle that in Maryland… but not in San Diego. If I remember right her husband was a junior level prosecutor so maybe he is the one whose salary went up. Plus I think she moved to San Diego from Asia in 2007/2008 or so when housing was at a peak.

Still, I think my advice holds. Lots of places to live in America where a two-income professional family can own a nice home.

MD is the beating heart of the corrupt “Public Servant” gvt in America.

It has the most millionaires per capita in the US.

Anybody believe it is because of the crab cake industry?

Thank god for all the DC selflessness.

cas127 – right you are. I tried living in Bethesda. Lasted 6 months and ran far away.

Thank you SpencerG for the insights and advice. It is hard to leave family and we’ve made San Diego our home but I rather live somewhere on the east coast anyway. My husband wants to move to Austin. We left once before because of affordability and it didn’t work out so it’s harder to pull the trigger this time. Thanks again, so glad I found this place.

“My husband wants to move to Austin”

Austin is still cheaper than Coastal CA but it has been getting pretty expensive.

But…if you go 20 to 45 minutes north, south, east of Austin…you will pay 65% of Austin’s prices.

That is the beauty of Texas…a *ton* of developable land.

Find a job you can do remotely and move to a place with cheaper costs of living. I know this sounds dismissive, but your best years will be behind you if you try to wait this out.

Remote working is a huge opportunity to have a decent life and get out from under the thumb of rent seekers. But it won’t last – the rentier money will flow into all the places with internet connections and schools, and eventually absolutely everywhere. It is essentially what all those smart folks in the city and wallsteet spend all day trying to figure out – how to extract more from working folk.

If I was you’d I’d seize the opportunity and get established somewhere acceptable before the financial system starts front running millennials escaping the workhouse cities.

Thank you Jon, honestly I completely agree with you and I don’t think your advice is dismissive at all- it’s smart. We’ve been trying to figure out where to go (I want to go to New England, Virginia, or North Carolina, my husband likes Austin). Everything you’ve just said confirms my gut on this— to not wait it out. Thank you.

LD, I live in southern coastal North Carolina. People with serious money have pushed beach house prices in to the stratosphere. However, you can still find some screaming deals off the beach in rural Brunswick and Pender counties. Burgaw is starting to make a comeback, but house prices are still low there. Burgaw downtown has been used as a movie set.

If you must live on the water, there are still some great deals farther north on the Crystal Coast, all the way up to Harker’s Island.

If you want to live cheaply in the mountains, Franklin, NC is a lock. It is the gem capital of NC. and it’s between pricey Asheville and even more pricey Cashiers, NC.

If you cross the state line from Asheville, to Johnson City, TN, house prices drop like a rock and there are no state income taxes.

Tell your husband that migrating Californians have already pushed Austin house prices to what may be high peak levels. Hard to find a deal there.

Depends on your timeframe. I personally think buying a house nearly anywhere right now is buying at a top, but who knows?

I live in San Diego and own a SFR. No one knows what would happen but housing is hot here and is in precarious condition.

We have millions of unemployed, rental/mortgage forbearance and eviction moratorium which is basically doing extend and pretend.

If the govt keeps sending people money on monthly basis and keeps this forbearance program ON indefinitely I don’t see any risk.

Also, going by what happened to yield in last few weeks, looks like FED does not have lot of control in yield. If the interest rates rises, then it’d make expensive market very risky.

I am in San Diego since 2006 and I saw similar feeling: Home prices in San Diego can never go down because we are special!

I have no idea what the future hold but we are indeed living in interesting/precarious times.

Rich- thank you so much for taking the time to help me with your suggestions, I’ll look into those places. We don’t need to be on the coast, I’ve been looking at towns outside Charlotte like Davidson. Are you familiar with those areas? We need to be near hospitals and I love older historic homes. My husband thinks Austin will be the new Silicon Valley- believe it or not it’s actually a deal compared to what we are used to in San Diego.

I hear ya Jon- to me it appears incredibly risky here in San Diego. What I am seeing is not worth the cost, not even close. How long can this continue? I agree that it’s silly to believe it’s going to keep going up- it seems people did not learn from ‘08 but I’m afraid to stay and keep waiting because signs seem to be pointing to inflation and as SpencerG pointed out- people will continue us to hold onto their assets during those times and inventory will remain bleak.

as old guy in RE since late 1950 era, I agree totally with rnyr,,, he is in se FL, and I now back in tpa bay area FL to take care of elderly mil, who is doing great at 90!!

RE mkt in FL and CA and OR and TN has been very good to us for eva, but only with a lot of focused hard work, manual labor as we were able, and managing hired labor for all those areas.

OK, so where I want to go is for you and yours to start yesterday to make up spread sheets to actually put numbers to your dreams and plans and procedures to determine cost benefits for each and every opportunity.

As rnyr says, this certainly appears to be another top of the market as I have been through in the above states since 1956, when dad had no work for six months, and he had to sell the farm in order to keep the other city houses,,, etc…

And, to be sure, EVERY place has its pluses and minuses,,, advantages and disadvantages.

Finally, when all the brain work, etc., is done to your satisfaction, sit and make the decision in your heart,,,

just suggestions from one who has been there done that for decades,,, and Good Luck!!

LD, Davidson is a beautiful, historic town. It’s a Charlotte suburb, and one of the most expensive suburbs at that. It’s right there on Lake Norman, but Lake Norman has become pretty polluted. Still, it would be a great place to live. The college there has produced one of best pro basketball players of all time. His younger pro basketball brother, however, played for Duke before going to the pros.

If you can afford Davidson, you might want to look at Hillsborough, NC. It’s less expensive than Davidson and very much part of the research triangle. Great co-op and a growing arts scene. You can get to Raleigh, Durham or Chapel Hill in no time. You can also get more land with your house. They have probably started on the high speed line station there by now.

I got my MBA in Austin after leaving the Active Duty Navy. I will tell you one thing you need to consider… it gets HOT!!! I grew up in a waterfront town and obviously lived in them for the rest of my Navy career… and even afterwards now that I think about it. Living on the waterfront you have an expectation that the heat will die down between 2PM and 3PM in the afternoon.

Not in friggin’ Austin, Texas it doesn’t! Mowing the lawn or going for a run at 4 or 5PM was almost impossible. The heat just keeps building until near dusk because there is no ocean nearby to regulate it.

It may be a minor concern in the grand scheme of things, but take it from me that it wasn’t as minor as one might suppose.

“Yellen/Powell claim they know how to stop hyperinflation from occurring but I have a sneaking suspicion they aren’t being straight with us on a few issues…”

I tend to agree with you…for me, the Fed’s mechanism/reliability for *withdrawing/stopping* inflation from the system is a lot hazier than its ability to create inflation (print).

(As far as I can tell, the Fed thinks that by being able to pay interest to banks directly on their idle, excess reserves – and there are a ton at the Big 4 banks – it will be able to choke off lending/stop inflation at will. Hmm…maybe)

The Federal Reserve must be continuously creating currency/credit and most definitely not destroying it. If you doubt that, watch what they do when assets/securities (collateral for the currency) are in jeopardy of significantly cascading defaults.

The Treasury will crush inflation through taxation. With the 16th Amendment, they can and will tax any and all income to whatever levels necessary…you can take that to the bank.

In order to afford to buy a home my daughter and her husband moved to Texas from Orange county Ca. His employer allowed him to keep his Ca. Income while he works from home. The company has a office in Austin

“Special Purpose Vehicles (SPVs) are legal entities (LLCs) that the Fed set up and owns as a way for it to buy assets that it is not allowed to buy otherwise.”

The Fed allows the cheap borrowings that fuel the Socialist agenda of Congress. Thatcher said Socialism doesnt work because you eventually run out of other people’s money. Not so when central bankers are involved in QE and other antics.

So Congress cares not what the Fed does as long as it keeps stocks up and borrowing for money “give aways” that are mostly vote buying.

Thus when the Fed starts dealing in non federally backed securities, and is in constant violation of their mandates…

Stable Prices….promoting inflation at rates that rip 22 to 28% off the dollar (2-2.5%) in ten years.

Moderate Long Term Interest Rates…..all time lows are “immoderate” by definition…

Congress and any oversight the Fed might/should have is missing.

The Fed has no right to expand the money supply as it has ..

The Fed has no right to impose a TAX of inflation on the holders of dollars

The Fed has no right to deal in non federally backed securities.

Who do we call?

Who do we call? Ha Ha Ha. Who did you vote for? Did it matter?

Suck it up. It’s a country of arbitrary dictates now, not laws. It was fun while we were deceived. Pick you warlord and swear fealty to the death.

I remember when I had to outlaw the word “should” in the office because people kept using it foolishly instead of thinking “it is”.

I absolutely LOVE these kind of articles from Wolf. The Fed Balance Sheet articles he wrote during the QT phase are how I found his blog to begin with.

That said, I disagree with the tone. Running deficits is what governments are supposed to do in recessions/depressions (or times like these if you prefer). Central banks are supposed to burn money then. That is just basic Keynesian Economics. The CRISIS is going to come if the Congress and President cannot run balanced budgets or (“Gawdferbid”) surpluses when the economy turns around.

Hmm.

Hasn’t Keynesian economics, both in recent good and bad times been a significant factor in the current economic difficulties..?

Not really. Who is even practicing Keynesian Economics any more? We run budget deficits in bad times AND good… and tell ourselves there will be no consequences.

“Who is even practicing Keynesian Economics any more?”

The Keynesian deficit spending remedy operates as crack cocaine for politicians in the real world.

All their usual political power derives from handing out money (taking/taxing it back angers the now addicted grantees).

This creates a hopeless systemic asymmetry in the political system (deficits forever).

And the real world bears this out.

The last 50 years have been a nightmare of habitual deficit spending, with perhaps 5 or fewer of those years showing surplus.

That is how DC has taken the premier economic power on earth and turned it into a debt ridden ruin with debt to GDP being well in excess of 100%.

And now the DC Degeneracy has no option but to buy its own debt (nobody else wants it, except at interest rates that would kill ZIRP addicted businesses and DC itself).

But simply printing fiat, while driving interest rates down (temporarily), by definition creates inflation (asset or otherwise).

So DC turns its debt addiction problems into its citizens’ inflation problems…all the while lying about the process.

So…Keynesian deficit “fixes” are no such thing in the real world of slimy, sh*tbag politicians.

YES,,, absolutely YES tt,,,, and thanks for bringing that part of the basis for the ongoing degradation of the USD to the fore once again.

Stop all the various and sundry degradations, and, if necessary, ”reboot” the USD to what it was BEFORE THE FED… and most, if not all of the current financial problems go away.

Certainly NOT going to be easy/peasy, no matter which path chosen,,, but equally certainly going to happen sooner or later.

No other way than total global collapse and subsequent global war that nobody in their right mind anywhere wants to see…

Spencer…

” Running deficits is what governments are supposed to do in recessions/depressions ”

and what do they do in times of record low unemployment and record high stock prices? They do the same…and that is the issue.

The Fed never retreats or exits….it is “never the right time”.

The QE never stopped….the promise of unwinding (Bernanke WSJ July of 2009) was a falsehood.

The Fed is there for emergencies….I think there is little doubt there. But the “party on” attitude is reckless…and we will pay for idiocy. IMO.

The financial history of this nation is Fed Funds equal to or in excess of inflation. Now we can debate proper metrics of inflation measuring, but the fact remains that from 2009 on, in good times and bad, the Fed pegged Fed Funds under inflation. That is historically abnormal, and a constant thievery from the holders of dollars to prop markets and assets.

Now the Fed mints money / monetizing debt at a yearly clip of 27%. This is outside their bounds, just as the promoting of inflation and the non promotion of “moderate long term interest rates, the forgotten THIRD mandate.

I am not disputing that no one runs surpluses in good times any more. But they should. Moreover, that does not excuse them from the obligation to run deficits in the bad times. This COVID economy could be a LOT worse if the Congress and the Fed hadn’t stepped up and opened the spigots. What come NEXT is my big concern.

PS: There was plenty of QT in 2017 to 2019. From $4.5 trillion down to $3.8 trillion if I am reading Wolf’s chart right. Almost 20% in two years… that’s not bad. More like 40% if you consider that you cannot take the Fed Balance Sheet to zero assets.

Spencer

No one I know suggests the Fed take the balance sheet to zero.

“There was plenty of QT in 2017 to 2019. From $4.5 trillion down to $3.8 trillion.”………….plenty?

It was a start….and when Fed Funds got to 2% in late 2018, the stock market freaked. Trump jawboned the Fed, and Powell has been the same since.

Fed Funds, IMO, should be more formula….tied to at least equal or exceed inflation, properly measured. If not bound to the formula, fixed with appropriate magnitude to inflation.

Bernanke, when first implementing QE, said that when unemployment dropped below 6.5%, rates would normalize and roll offs and maturities would gradually provide an exit.

Never happened, even though unemployment dropped to RECORD lows (3.5%)

What the Fed does in genuine times of distress is one thing, the lack of discipline to trim sail at high winds is the issue IMO.

That .7T drawdown was a pathetic 20% reduction in the 3.5T run up following 2009. And…that was after 8 to 10 years.

Now, another enormous slug of QE, to “fix” another disaster heavily implicating DC policy/operational failures.

When you subsidize/immunize failure…you get more failure.

DC isn’t a swamp, it is a sewer.

The concept of offsetting even a tiny portion of “life or death” Covid spending with cuts elsewhere in the DC favor factory is utterly inconceivable to the kind of people who run DC.

That mentality is (and has long been) the mechanism for economic ruin in the US.

I don’t agree. Giving people printed money to buy iPhones and other foreign-made durable goods with is not a proper mandate of government.

Cas127

“DC isn’t a swamp, it is a sewer.”

Agreed

A swamp is an ecologically balanced entity. Frogs, lilies, algae, turtles, wet lands for runoff etc. Not a bad thing. But now we are going from being a swamp to a cesspool is short order, and I don’t see anything on the horizon to stop it.

“obligation to run deficits in the bad times”

The government has an obligation to balance the budget. Not support crony capitalism and self enrichment and bureaucratic growth. Nor “fix” problems of their own making by meddling in education, health, and finance and making things enormously worse.

The Constitution left most of that to the states which they can do without the expensive assistance of the federal government.

BTW, when the government “opened the spigots” whose money came out?

SpencerG says: “Moreover, that does not excuse them from the obligation to run deficits in the bad times.”

————————————————

Keynesians believe this. Other economic schools don’t. It just provides cover for previous imprudence, previous irresponsibility, previous and ongoing Banksterism, Wall Street bailouts, etc.

There was never a good time. It all was chimera of good times hence FED could never stop QE. Moreover, FED if for the rich people, so it would do what is needed to help them.

Despite QE in the last decade, the GDP could never take off

Regarding you mentioned times like these/recession/depression….it doesn’t FEEL like a recession/depression to me. It feels more like someone took the great big family cookie jar and divvied up all the cookies to a favored few, leaving some with less or nothing. I feel like someone stole something from me. Just a subjective view.

Timbers,

Not cookies…crack.

Those inflated asset holders are going to come down hard.

To lobby for another round of crack.

The problem is that these bodies model their thinking on eternal exponential growth, whereas the laws of thermodynamics don’t care what central bankers and politicians want to believe.

We should have adjusted our systems to catering for ongoing contraction decades ago, but that would have entailed inconvenience and making really tough choices. So now we’re so committed to boosting our toxic growth metrics by stealing energy and resources from the future that an adjustment to another trajectory will collapse the current leveraged to the moon system, so I’m pretty sure they won’t stop until they eventually are forced to adopt new ways of thinking in a pretty painful way for most of us.

Salt-thank you. the historic and ongoing effects of human economic systems that pay scant or no attention to the one dictated by endless TLOT on our planetary systems has resulted in belief-forms of ‘growth’ that are now gorging on our species seed corn.

Entropy is blind, deaf, and, alas, never sleeps. TANSTAAFL.

may we all find a better day.

Yeah, 91, and maybe the most alarming part is the blasé manner in which we treat our accelerating destruction of our ecosystems.

Loss of habitats, loss of biodiversity, accelerating extinctions of species, and the horrifying reductions in microfauna like insects and plankton is all papered over as we engage in ever more efficient depletion and pollution of soils, water tables and marine food stocks, and simultaneously trumpet our ability to feed ever more people on ever less nutritious and varied foods. It’s bleedin’ dystopian if you ask me.

Entropy always wins. Always.

We only live because we have evolved over 4 billion years of trial and error as steady state parasitical homeoSTATIC systems that fight entropy using the energy from the sun.

We have unfortunately created a culture that ignores this completely.

Kinda like what Carter almost begged us to realize and do? In the 70’s!

Only Prez we ever had who was a scientist.

True, but not all the time. But it doesn’t hurt to remind all the Keynes bashers that Keynes believed in balanced budgets but balanced over the cycle, not year end. The government would spend in recessions using the SURPLUS accumulated in the good times. Heard the word ‘surplus’, lately?

When did deficits cease to matter? With Reagan. Ironically, a good account of this is Stockman’s book: ‘The Triumph of Politics’ during the time Stockman was OMB director.

I say ‘ironically’ because Stockman is now a lead Keynes basher, even after telling us how

it was politicians who misused the legitimate power of the government to incur debt so they could distribute goodies all the time and thus be popular.

A few days ago someone was wondering what question they would like to ask Powell. My suggestion: “do you agree with former Fed Chair William McChesney Martin that the Fed’s job is to “take away the punch bowl just when the party gets rolling”?

Lately it seems like the keepers of the punch are more likely to spike it.

I think that is a pretty limited view of Reagan’s approach. He was facing runaway inflation… which could only be solved via a Fed-induced recession. A taxation system that was stifling growth and needed to be reformed. And a (cold) war with the Soviet Union that he fully intended to win. NONE of that was going to come cheap and ALL of it necessitated excess deficits even under Keynesian economic theory.

Stockman’s “green eyeshade” approach was of course traditional Republicanism… and what you want from your OMB Director. But Presidents have to balance priorities and Reagan did as well.

The 1981-82 recession has collapsed inflation for FOURTY YEARS now! America’s tax system is so utterly reformed that for anyone under the age of 50 you would have to explain the entire idea of “Bracket Creep” to them. Not only is the Soviet Union gone, but Reagan’s defense buildup which prompted so much of his deficit spending was Keynesian in the sense that the money was spent inside the US on defense industries (as opposed to the Obama stimulus package which subsidized China’s “green” industry to a large extent).

Reagan just ran out of time before he could address the deficit. There is only so much you can achieve in eight years. But George HW Bush carried the ball forward in the next four years… signing an agreement with Congress that cut spending and raised taxes… only to lose Republican support and fail to win re-election.

Sadly, the Baby Boomers who have run the government since then have simply not been up to the task. They look at Reagan and think that he was ONLY about tax cuts. It is almost laughable to watch Obama raise taxes 4.5 percent or Trump cut them by 2.5 percent and think they are doing anything real. Reagan took the top rate from 70% when he took office to 33% when he left office.. which is roughly where they remain today!

It really is hard to believe that Ronald Reagan was our last President with a college degree in Economics. But the results show…

SpencerG said: “The 1981-82 recession has collapsed inflation for FOURTY YEARS now!”

_______________________________________

Another ridiculous statement. Open your eyes.

And Reagan, though likable at the time, is hugely over rated in “conservative” circles. He set the stage for at least two major problems to the working class in America:

1. Deficits and debt …… with the resultant fiscal irresponsibility, FED largess and continuous inflation.

2. Immigration, with his amnesty, and all the following signals and problems.

CB, I thought I was the only conservative who does not look back fondly upon Reagan.

First, he was not a small government conservative. A good example is his signing the 1984 National Minimum Drinking Age Act, which mandated that states make the drinking age 21 or lose highway funding.

Second, he did not believe in the right to keep and bear arms.

Third, he signed the amnesty in 1986, and we were supposed to get actual enforcement in exchange. We got the amnesty, but no enforcement. Which was how it was intended, but people didn’t know it at the time.

Regan got his economics degree before Dynamic Stochastic General Equilibrium became the State religion.

“Running deficits is what governments are supposed to do in recessions/depressions (or times like these if you prefer).”

Spencer, I can find nothing wrong with the tone of the article. Running “unproductive debt”, through monetary policy, rewards asset holders and ends up penalizing a vast majority of the population. Using fiscal policy to create debt, that is backed by productive investment, could have the reverse outcome. I believe that would be more of a Keynesian approach. This article is about the Fed’s use of monetary policy through QE.

“The CRISIS is going to come if the Congress and President cannot run balanced budgets or (“Gawdferbid”) surpluses when the economy turns around.”

It is doubtful that the U.S. Government, that presides over the greatest debtor nation in the world, will ever run a balanced budget, let alone run a surplus.

I rather agree with you. I always thought that Keynes was rather naïve with his view that it would be OK to pay someone to dig a whole and someone else to fill it in a recession. It underestimates how much loss of credibility the government gets. And it is not “productive” as you say.

But the Fed’s problem is that they are the only grownups in town. John Boehner was serious about controlling the National Debt but his own party ran him out of town on a rail. Obviously it would be better if the Fed were ONLY providing “liquidity” to the markets instead of trying to fix the economy on its own. Which is why they keep calling for “fiscal policy relief.” But that is not to be for now…

Yeah, but Congress’ idea of “fiscal policy relief” is helicoptering money to people who don’t need it so they can splurge on iPhones, Pelotons, flat screen TVs, overpriced stonks, and Bitcoin.

hole not whole

“Obviously it would be better if the Fed were ONLY providing “liquidity” to the markets instead of trying to fix the economy on its own. Which is why they keep calling for “fiscal policy relief.” But that is not to be for now…”

Just the opposite. The Fed is only providing “liquidity” to the markets. That’s what QE is all about. If the Fed stopped buying trillions in MBS and Treasuries, the market would collapse. If you are a long-term Wolfe blog reader, then you know that the Fed was pouring hundreds of billions of dollars into the repo market, to protect the stock market from crashing, months before there was a pandemic. If you have any evidence that the Fed is actually supplying any “fiscal policy relief”, please post it.

By the way, a good example of fiscal policy and productive debt would be throwing money into our decaying infrastructure. What the Fed is doing is propping up asset values, and propping up asset values is monetary policy, not fiscal policy.

Even Keynes knew that once the need to stimulate with deficits was over, the stimulation should cease.

This is lost on today’s central banker.

SpencerG says: “But the Fed’s problem is that they are the only grownups in town.”

_________________________________

This is a ridiculous masterpiece. They are grownups in the sense of being master thieves.

SpencerG-…’whole’ vs. ‘hole’. Observations over my lifetime indicate the whole already were, and are now just deeper, in the hole…

may we all look up from our digging and find a better day.

Ivory tower economics theories fail continuously because they ignore actual human behavior, especially corruption at the top of the hierarchy (which bleeds down into everything).

Economists seem to think that leaders have integrity and administer honest institutions. Maybe they do someplace. Certainly not in the US. Until people are willing to face the fact we are ruled by Mafia parasites, and then organize themselves to stop the bloodsucking, no amount of turd-polishing reforms will fix the current crisis.

Wolf,

Enough room to type the trillions involved in full that have increased in the first graph with all the 0s ?

Seeing the amount of digits involved might help visualize the amounts but cause brain overload !

Regards

It’s really kind of funny. A trillion used to be a huge amount and rarely came up. Now we throw this number around casually and daily, like playing volleyball.

1 Trillion is a thousand Billions

1 Billion is a thousand Millions

one billion seconds is 32 years.

one trillion seconds is…………..320 CENTURIES!!!!!

I can remember when big projects were measured in millions, and being a millionaire was a big deal.

Not long ago, big projects were Billions, and the T word was only mentioned theoretically.

Today, you had better be a millionaire by the time you retire – you’re going to need about 2M for a typical 1960s-style middle class retirement.

Interesting, And Senator Everett Dirksen, republican from Illinois, the land of Lincoln, was instrumental in passing the ’64 civil rights act and rumored to have said a billion here a billion there and pretty soon you’re talking real money. A billion used to be a huge amount and the big bang used to be a pejorative term from the steady state universe perspective.

Hasn’t the FED talked about getting rid of the MBS for years now? While not a fan of the continued QE I grudgingly accept them buying treasuries, but the continued purchase of MBS seems like a fairly open finacial raccet for the well coñected. Does this have an end point? What is the official justification for buying more MBS instead of getting rid of them?

Fannie Mae’s stock price is 1/30th of what it was 15 years ago before the first housing bubble blew up, only to become a much wider and expensive bubble since.

So why is the stock worth less than $2 now, almost in danger of being delisted, it’s value being so little?

“What is the official justification for buying more MBS instead of getting rid of them?”

1. Bailing out holders of MBS and CMBS. They were getting in trouble in March with all the forbearance programs and eviction bans, residential and commercial.

2. Forcing down mortgage rates to inflate a housing bubble.

I don’t like QE at all, but I don’t see much of a difference between buying MBS and buying Treasuries. Unless I’m mistaken, all of the MBS that the Fed monetizes are guaranteed by the federal government. So if the Fed didn’t purchase them, and they defaulted, Congress would borrow to pay those amounts, and then the Fed would just buy the Treasury bills instead.

Am I missing something here?

RightNYer,

The Fed stated in the past during the QE unwind (2018-2019) that it wants to get rid of MBS entirely because they’re complicated to deal with in terms of monetary policy — the pass-through principal payments that are unpredictable, the way the market is set up, the fact that there is not one standardized MBS like there is a standardized 10-year T-note, etc. They were going to let them run off the balance sheet and replace them with Treasuries. And then the crisis hit.

So from a management point of view, it makes sense to let them run off (simply by not replacing the pass-through principal payments with new MBS), and never ever touch them again. But that scenario is now out the window.

Got it, thank you. It sounds like the main issue is that these are ones you really want the market to value organically.

I’m still flabbergasted that people are actually throwing tantrums about a 1.5% interest rate in a 10-year bond.

That’s essentially a negative rate bond if the FED hits it’s 2% inflation objective.

We can’t even get our savings accounts at the banks to pay us enough interest for inflation and they have the gall to cry about interest rates being too high?

Tax the rich.

A,

Yes, it’s a puny little yield. But a few months ago, they were still hoping and clamoring for a negative 10-year yield (like in Germany). That’s why they bought 10-year maturities at 0.6% yield in August. They figured they could sell them at -0.6% yield a year later. The whole calculus has been upended.

Small typo in the last section: “Creating ominous rumblings in highly leverage hedge funds circles”. Missing “d” on “leveraged”.

No need to keep this comment.

thanks for the great work, as usual.

Thanks. Two typos actually. The missing d in “leveraged” and the extra s in “funds.”

“how far the Fed has pushed its strategy to bail out and enrich the asset holders”

The ‘powers that be’ will do everything they can to maintain the status quo until it becomes untenable.

Yes, they will sink the ship through sheer hubris.

Any country whose central bank must become the Price Setter or Buyer of First Resort for its sovereign debt is technically Fiscally Insolvent. The country’s debt should trade freely in an efficient market to set price/yield BASED UPON THE REVENUE CAPABILITY OF SAID COUNTRY TO SERVICE ITS CURRENT AND NEAR-TERM DEBT & FUNDING NEEDS. The United States is no longer a solvent country where the misguided and rogue Federal Reserve is intervening daily in the price discovery mechanisms of numerous debt markets.

Potential buyers are now pondering HOW the U.S. will default on its outstanding debt, forget about the Trillions the debt python is going to disgorge in the months ahead. Dollar devaluation via inflation acquiescence and maturity extensions come readily to mind. THE FULL FAITH AND CREDIT OF THE UNITED STATES GOVERNMENT ….. give me a break! Zimbabwe or South African debt looking equally appealing. In fact, would not buy anyone’s paper in this environment.

P.S. Schwab’s trading platform locked up a few minutes ago! Katy bar the door.

David..

“Any country whose central bank must become the Price Setter or Buyer of First Resort for its sovereign debt is technically Fiscally Insolvent. ”

inflating is the only recourse…

yet the inflators (the Fed) are bound by their mandates…like stable prices..

right? And when the Fed ignores the mandates under which they are allowed to operate…who comes to halt their rogue activities?

Are they still adding long dated treasuries? To me, that should be illegal. Letting a bunch of 70 year olds borrow from 10 years in the future at fake interest rates is such selfish behavior. It’s not like they’re building hospitals and roads with that money. They’re just increasing the risk appetite of everyone else to keep the 401ks and house prices going up forever (a nicely engineered trap to prevent wage growth and increase wealth distortions). If the balance sheet never unwinds don’t we have unelected officials essentially creating and spending money? How is it even constitutional? I wish some smart lawyer would get on it.

I have what’ll probably seem like a dumb question. Right now, bonds are selling off, which is causing treasury yields to rise. That in turn is causing stocks to sell off. Gold’s selling off, too – down to $1730, which is a 6-month low.

So if everything’s selling off, where’s all the money going? Into cash?

Dogecoins.

Cryptocurrencies are down this week, too. Everything’s down this week, just about across the board. Bitcoin’s down to $48,000, from $58,000 a week ago. But of course, it’s still way up on the year.

Normally, I don’t do film reviews nor links here. But, I suggest watching the first few minutes of YouTube for Reel Histories Welcome to India (part the first) to see what humans will do to recover metals (gold in this case). It might be an eye opener on chasing those safe harbors beyond fiat or other promises.

Money can’t go into anything. Someone’s purchase is another person’s sale.

There’s a youtube from a dozen years ago where Bernanke gets grilled by Alan Grayson in regards to central banks liquidity swaps, and Ben has no idea where the money went…

Of course, this is when other countries wanted to play along with our money malarkey.

Here’s the title of the video:

Alan Grayson: “Which Foreigners Got the Fed’s $500,000,000,000?” Bernanke: “I Don’t Know.”

Treasury auction of 5yr yesterday was met with “low” demand, the volatility caused HFTs to pull back liquidity and the SHTF. The perception of rising rates and inflation puts the bond market in a bind, and if there was some chance of YCC, the Fed has to start buying everything, and Plan A is out the window. PowYellen need to alter these perceptions but so far the bond market is not getting any guidance. Maybe they want to pump yields at least in the interim to get all that money at the short end out to the long end. By that time the economic boom will look more like a bust and they can push rates down again, but it’s just possible that preogative no longer exists, or they are out of sync with global markets. Two years ago they could have normalized and turned the global deflation. What they do now is anyone’s guess.

It’s just strange because this started due to “good news” – the economy re-opening and looking strong for 2021. But that led to fears of inflation, which led to a selloff in bonds, which led to a selloff across the board. So good news was bad news for the markets. Strange.

Not really strange. American corporations are debt-leveraged to the eyeballs and many of them are just debt zombies. The Russell 2000 has no P/E because there is no net-positive E. The entire circus depends on cheap debt to keep chugging forward.

At 3% interest, American “markets” would collapse at least 50%. This is a very sickly system. Anemic growth and more borrowing are about all this old boy can handle without stroking out.

Ambrose

Fed is trapped. Either they have to bailout the bond mkt or the stock mkt, but not both. Bond mkt is vital to govt funding/spending!

By the various speeches by Powell and other FOMC members it is quite obvious that they are willing to reflation go over 2% for a while until there is havoc in the bond mkt. Apparently there is direct positive correlation of yield on 2y note with Fed Fund rate but NOT with 10 yr bond.

As the yield rises, it will be accepted as ‘good’ b/c of ‘robust’ recovering economy at 6+% GDP(?) . Bond mkt will challenge Fed and call it bluff. Selling of Bonds will go on, next week and the next until, Fed takes notice!

Deflation of equity bubble has already started. I welcome the reset either fast or slow!

Wolf:

Thanks for putting into plain talk what those SPV’s are really for!

How innocent that sounds: “Special Purpose Vehicles.”

But I get it now! They are these SPECIAL huge, heavily armed vehicles that are designed to semi covertly carry large pallets of cash directly from the Fed over to the Treasury.

Great article and exceptional comments.

I do agree inflation seems inevitable….and by that I mean interest rates will rise into a sick surprise for many in debt. However, the savings rate has been increasing of late so inflation or a downturn seems to be expected by many who do not immediately need stimulus money to stay afloat.

Question: Why on earth is there no simple means test for bigger stimulus grants (targeted) and why aren’t wealthy folks taxed back if they do make the grants universal? Do you hand out free coats to people with full closets? Doesn’t make sense to me. The money saved could then be redirected into more refined objectives like aiding entire regions that have suffered industry collapse. This might also go a long ways towards calming some of the divisive politics of the day.

The purpose of giving money to people is NOT to help out people who need it, it is to pump money into the economy that will get spent, so corporations see NO dips in revenues.

This is pure stupidity. No economist could present a coherent and honest case for doing this that was truly countered with opposing views. So they simply cut off any real debate. Have the Fed chairman testify and dont ask any real questions and allow him to lie through his teeth with no repurcussions.

Wealth effect or trickle down theory are just ‘theories’ for the bottom 90%.

How can savings rate increase when 40% of more are living from check to pay check? Many don’t have a retirement plans at all. homelessness has increased since ’09 if not earlier. Inequality in come & wealth has become worse since 2000!

Talk of surplus in savings is ‘hopium song’ of the wall st and the financial industry! Selling of bonds will continue and deflation of this 3rd largest bubble has begun, since last week. Rise in 10y yield is the trigger point and the Fed is trapped.

As much as i disagree with Wolf on the nature of QE, it’s usage and purpose is hard to justify. Today i heard they are calling on the Fed to start buying long duration because of the yield spike on the 10y. It’s pretty close to becoming a clown show at this point where every move must be approved and dictated. But it also speaks volumes as to the fragility of all this, people have panicked themselves into positions atm, levered up without any care in the world all of it resting on the idea that the Fed will dictate any move on any market from now on. It takes one little accident and the whole thing goes horrifyingly wrong across asset classes, pretty quick. Hold tight to your keyboards boys and girls.

IMHO, rise in 10y yield is the trigger point. This has risen in spite of Fed buying 120 Billions (40B in T) every month!

It takes $4.5 to produce 1$ of GDP, now. More QEs will have the least impact. They will use the same tools they have used for the last 12 yrs, b/c they know nothing else.

I’m wondering if some form of interest rate controls are on the horizon. Especially on the long rates. Given what the Fed has done to date I wouldn’t put it past these morons to try something like that. If they do this it will lead to a credit crunch the likes of which we have never seen. It will wreck the housing market.

You have to admit these “morons” are pretty good at figuring out how to kick the can down the road yet again.

I would love to see interest rates go up. I feel like 30% off a home in California would be a fair trade for the way they’ve plundered my savings.

Hey swamp creature: Do you mean interest rate controls in the sense that these morons will keep them down in a permanent way? Can you expand on that and how it would lead to a credit crunch?

Turtle: I agree about this pattern of kicking the can down the road…