Bond Market Smells a Rat: Inflation. So the Fed seems OK with rising long-term Treasury yields.

By Wolf Richter for WOLF STREET.

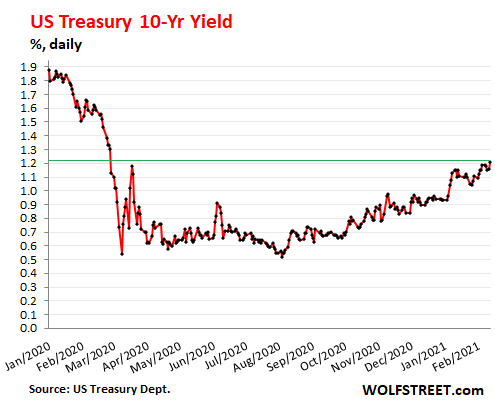

The bond market smells a rat, but the mortgage market and the high-yield bond market are holding their nose and plowing forward: The 10-year Treasury yield rose to 1.21% on Friday, the highest since February 26, when markets began their gyrations. This yield has more than doubled (+133%) from the historic low of 0.52% on August 4.

In early August, Wall Street hype mongers were still out there pushing the meme that the 10-year yield would fall below zero and be negative for all years to come, in order to entice buyers to buy at that minuscule yield. And had the yield dropped below zero, those buyers would have made some money – especially those with highly leveraged bets.

Alas, when potential buyers need to be enticed with a lower price, which is what began to happen after August 4, the price of that bond falls and therefore the yield rises, and those who’d bought at the lower yields are losing money. For example, at the most basic unleveraged level, the iShares Treasury Bond ETF [TLT], which tracks Treasury securities with at least 20 years of maturity left, fell 1.24% on Friday and is down 14.3% since August 4.

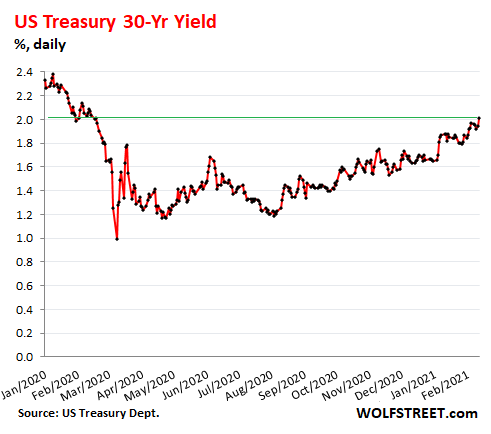

The 30-year yield rose 7 basis points on Friday to 2.01%, the highest since February 19. The yield has more than doubled from 0.99% on March 9.

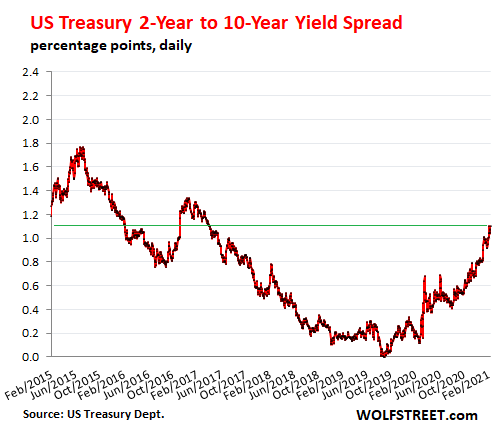

The Fed has the short-term Treasury yield locked down near zero, via its various interest rate mechanisms and Treasury purchases. Even the yield of the 2-year note is near zero, at 0.109%. With the short end near zero, and the yield at the longer end rising, the yield curve has steepened.

One of the classic measures of the yield curve, the difference between the 2-year yield and the 10-year yield, widened to 1.1 percentage points on Friday, the widest spread since April 2017. That spread had turned negative briefly in August 2019, when the yield curve “inverted” as the 10-year yield dropped below the 2-year yield.

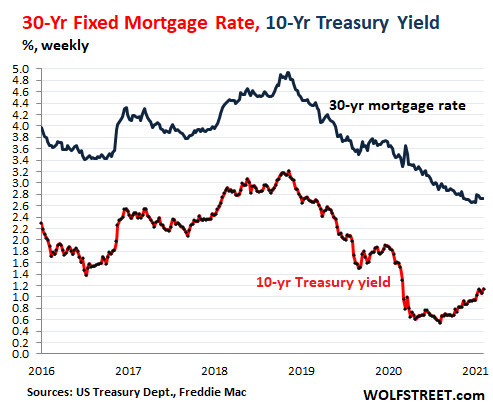

Mortgage rates went in the opposite direction, but are now having second thoughts.

The average 30-year fixed-rate mortgage rate, which generally tracks the 10-year yield, continued dropping after August 4, even as the 10-year Treasury yield was rising. Finally, in early January, it stopped dropping when it hit 2.65%, and has since ticked up a tiny bit. According to data from Freddy Mac, the weekly average as of February 11 was 2.73%.

This chart of the mortgage rate as per Freddie Mac (blue line) and the 10-year Treasury yield shows the disconnect since last summer. But as weekly numbers, they lack the movements over the past two days, when both have risen:

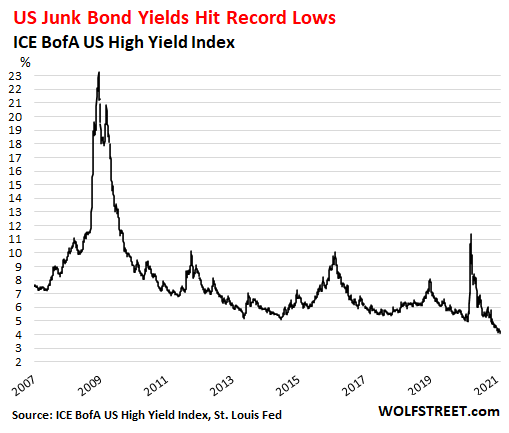

But Junk bond yields continue to drop from record low to record low.

The average yield per the ICE BofA US High Yield Index, which tracks US-issued junk bonds across the high-yield spectrum, dropped to 4.09%, the lowest in history, going from new low to the next new low, documenting every day the fabulous bubble going on in the riskiest end of the credit markets.

At the upper end of the junk bond markets, the average yield of bonds in the “BB” category (my cheat sheet of corporate bond ratings), fell to 3.19%, according to the ICE BofA BB US High Yield Index, having fallen from historic low to historic low. That’s what 10-year Treasury securities were yielding in October 2018.

But at the upper end of investment grade, average AA-rated corporate bonds have been slowly following the trend set by Treasury securities, but at a much slower pace, having risen just 25 basis points since August 4.

The Fed…

The Fed appears to be OK with rising long-term Treasury yields. Multiple Fed officials have said that if the higher long-term yields are a sign of rising inflation expectations and economic growth – rather than financial stress – they are welcome. And so they’re allowed to rise.

For the Fed, these increases in the long-term Treasury yields and the continued declines in junk bond yields and the near-record-low mortgage rates are a soothing combination, speaking of inflation and not financial stress.

If the spread of junk bonds and mortgage rates to Treasury securities were to blow out suddenly, that would be a sign of financial stress, and might be more worrisome for the Fed.

So the rat that the Treasury market is smelling is consumer price inflation. It’s gnawing its way through various layers of the economy. And the Fed has said that it will ignore inflation for a “while,” and that it will welcome an overshoot of inflation. Only when it becomes “unwanted” inflation, as Powell put it without specifying what that means, would the Fed crack down.

So maybe the Fed would crack down when inflation stays above 4% or 5% for a “while?” Once inflation has solidly set in, it’s hard to stop. That’s the rat the Treasury market is smelling, and if you’re sitting on a bond that yields 1.2% for the next 10 years, that’s not a mouthwatering item on the menu.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Watch the ten year folks as the dollar continues its demise into worthlessness.

Wouldn’t the dollar rise as interest rates in America rise?

It did once long ago when America had a strong middle class.

Going forward, I think it is safest to assume that the US won’t be granted “safe harbor” benefits by default anymore…20 yrs of more or less failed interest rate manipulation have drilled that into the head of savers around the world.

So, if some decent sized country, with a healthy economy and a healthy debt to GDP is offering 2x or 3x UST rates (not hard if 10yr is 1% or 2%), money will flow out of US, weakening the USD.

If the UST is allowed to go up by some insulting 10 or 20 bps, while a better economy’s is going up by 100 or 150 bps…the USD will still fall.

Does such a place exist?

Russia is the only place that comes to mind….

“So, if some decent sized country, with a healthy economy and a healthy debt to GDP is offering 2x or 3x UST rates (not hard if 10yr is 1% or 2%), money will flow out of US, weakening the USD.”

@Cas127,

I hear you, and agree that eventually there will be other countries that fit what you are describing, but in the near term, the most similar countries to the US, namely the EU countries and Japan, have far lower yield on similar debt. Who exactly is in position to take this role? China isn’t a candidate, they don’t respect contracts or rule of law. I think things will change but the US will probably have higher yields for their debt for some time.

Happy1,

“China isn’t a candidate, they don’t respect contracts or rule of law”

True, but 20 years of DC directed ZIRP has taken the shine off of US integrity too (Takings clause is one place that immediately leaps to mind when reflecting upon the Constitutionality of multi decade ZIRP).

Yuan is very undervalued (CCP rigs like hell to keep it so…but not forever) so it is the most obvious candidate.

Danger of seizure/currency controls is legit, but there is already a fair sized offshore Yuan mkt…and that fact works against the danger of seizure/control.

And, in the long run, it will be in the CCP’s interest to further internationalize use of the Yuan…so they will further loosen control.

It will be a race between a 8% Yuan with a 4 risk rating and a 2% USD with a 2 risk rating…huge amounts of international capital will flow to the former.

Yuan Treasuries at 8% will double in 9 yrs.

US Treasuries at 2% will double in…36 yrs.

Plenty of intl money will take that bet.

The US continues to lean more and more upon a rotting crutch.

‘So, if some decent sized country, with a healthy economy and a healthy debt to GDP is offering 2x or 3x UST rates (not hard if 10yr is 1% or 2%), money will flow out of US, weakening the USD.’

RUSSIA???

OMG: where to begin? A good place would be Wikis ‘Russian Financial Crisis 2014-2017’

It only ends at 2017 because that’s when it was written, Wiki being an online encyclopedia not a news site. Not much has changed.

Then there is the ruble. I used to spell it ‘rouble’ but apart from the single ‘r’ it’s rubble. Right now about 2 cents US. You get a WAY better deal if by slim chance you want rubles, the 2 cents is the other way round. In one famous week it lost a third of its value.

Interest? That will be paid in rubles.

If you go into a better Moscow restaurant the prices will be in US $ or euros. But it would be against the law to pay in either. Only rubles, obtained officially at a very poor rate. This is a glimpse of the way Russia hordes dollars.

The GDP per capita at well under 10K is right down there with, let’s be polite and call them ‘developing’ countries. Far behind Argentina.

Every third comment on this topic and the rest is about the huge inequality in the US.

True, but not like Russia. The economy is roughly the size of Canada’s but supporting 4 times the population. So with the average Canadian being 4 times as wealthy, Canada should have more billionaires. Russia has 4 times the number of billionaires: the oligarchs, making Russia by this measure 16 times more unequal than Canada. None of these oligarchs are the Bill Gates variety. Not one invented or developed anything. They are the survivors of the scramble for the USSR’s commodity wealth. The aluminum sector particularly but not uniquely strewn with corpses.

The saddest may be the pensioners. They survive on about 110 U$ per month and they don’t get that in US $! Not long ago a young lady on Russian TV actually laughed as she read the benefits for pensioners. It was stuff like: ‘medicines 11$’. Hopefully she still has her job.

What else did we have in the “maga” days? It’s so simple.

It’s worth a read, honest! Why complicate things? Unless your mental “software” is corrupted/prejudiced somehow? What it doesn’t show is estate tax, which IIRC STARTS at around $11M/individual. Yes there are fewer jobs, (and MANY unneeded or non-beneficial to society ones).

And that is precisely where a massive Green New Industry comes in.

https://www.factandmyth.com/taxes/eisenhower-tax-rates-90-percent.

If Interest Rates rise the Financial System implodes… They have to invent a way to create slave workers to pay back the Federal Debt. A Social salary for people with debt. Those people will have to work for free (possible) At the same time I see a Central Bank Digital Currency linked to a social score. Results. Few multinationals (monopolists) will own 90% of the goods and services. Most of the workers that will work for free to pay back the debt + a CBDC that will be programmed…Depends on your behavior you’ll be able to spend anywhere or just in some places or for some goods and/or services. With the CBDC the Central Bank will also be able to plan the inflation (Ex. you’ll have to spend your salary within 20 days or it will expire)

No way.

The dollar will rise when foreign buyers of US debt support higher interest rates in the bond market, which is already happening. Mortgage and corporate debt which are not pricing in the rise in Treasury yields offsets consumer inflation. Corporations can accomodate wage pressures. Treasury policy would be to goldilocks them, keep rates low enough to avoid funding problems, and a Fed balance sheet explosion, high enough to keep them coming back, or to allow bank credit to tighten. China is allowing their currency to rise which may be a sign they want to keep their trade competitive should the dollar firm.

Kyle Bass wrote about unprecedented Chinese money printing. Sometime ago I found statistics showing they printed more money than the US. Their economy is not slipping into oblivion in spite of them printing more money. They were able to afford to build a replica of the Eiffel Tower and many other things.

David Hall

How much of the money going into ‘productive’ economy NOT the Eiffel tower, empty cities, roads and bridges to going no where?

Nearly 1/3rd of their stated GDP is non-productive!

sunny129, that is not true that “…empty cities, roads and bridges to going no where…” I have lived here for 20 years. They build the infrasctructure and then the area gets populated. What you believe is what i used to believe. Try baidu maps street view. You can see these roads built with nothing around then four years later buildings and shops an people. That map service has snapshots of different years. I was very surprised, now impressed.

Utter nonsense. Wolf has this wrong. No one wants to commit their money on long term U.S. debt. How do we know? Treasury bills are sky high and rates are going negative. Inflation? Nonsense. You would need economic activity to generate inflation. Economic activity is falling off a cliff.

What uninformed world is Wolf living in?

No inflation? Check out lumber prices. Check out auto prices. Check out house prices. Need I go on?

Cough, cough…check out medical inflation.

Oooo, oooo! Professor, professor!!…check out education inflation.

i think the specific examples you mentioned are due to supply chain bottlenecks. With 25 Million americans currently unemployed i dont see inflation on the horizon.

“i think the specific examples you mentioned are due to supply chain bottlenecks. With 25 Million americans currently unemployed i dont see inflation on the horizon.”

Nonsense. These all existed pre-COVID.

Ppp,

If you’re waiting for incomes to rise to trigger inflation, well, personal income shot up, as wages recovered as the highly paid switched to work-from-home and government stimulus and unemployment benefits layered money on top. This does not yet include the $600 stimulus check at the end of Dec early Jan, nor the potential future $1,400 stimulus check

https://wolfstreet.com/2021/01/29/americans-cut-back-as-income-from-wages-salaries-hit-record-while-10-million-people-still-out-of-work-weirdest-economy-ever/

The fact of the matter is that inflation is sustained growth across all sectors of the economy. We’re just not seeing it. If anything, we’re becoming Japan. Relation #4 has proved to be a big disaster.

These inflation/deflation ” discussions” are always tough without us all defining terms. Prices up or down don’t necessarily indicate system inflation of deflation.

All too often inflation gets measured via the official government metric of CPI ( which has been greatly adjusted over the years to keep the index down).

More $’s created into the system in my mind creates an inflationary environment… your currency is worth less.. against a standard measure. The USD versus Bitcoin could be a measure of inflation. The USD versus the average price of a single family home could be a measure.

Take the 2% inflation target the Fed wants. Over 30 years the $ is going to be nearly cut in half in value.

Commodity prices are going up across the board. There’s a shortage of semiconductors. On what planet does that not become inflation?

We have inflation and the economy is falling off a cliff.

The “Gipper” called this an economic stew created by Carter.

Said: “It was an economic stew that is turning the nations stomach”

Check out the prices of items in the supermarket that are imported from Europe. I buy a lot of these items. They are up 15% in the last month alone. I call that inflation.

Those government CPI figures are total bulls$it. Just like their bulls$it unemployment figures.

Resturants have just opened for indoor dining in Swampland. They’ve raised their prices 10% or more to compensate for the lost business due to the pandemic.

15% is being generous on some things. I used to buy the two packs of Spanish Queen Olives at Costco. Pre-pandemic, they were $7.99, then $9.99, then $10.49, then $10.99, now $11.49. That’s 44% in one year.

RightNYer

Those prices of imported food items are probably the most accurate measure of inflation than anything coming out of the government. People like myself can afford to pay the price for these items because we are concerned about quality and health. As long as people pay these prices , they will continue to go up. I believe the average inflation in food alone now is close to 15%.

Swamp, yes.

I’m fortunate enough that I can afford to buy the food I want (especially since I’m not eating out anymore), but the levels of inflation on these types of things are insane. And while 10% of the cost increase can be explained by the Euro climbing 10% against the dollar, that doesn’t explain the rest.

A lot of it IS the devaluation of the dollar. That’s why you see it so quickly on the imported items. Labor costs and transportation are added in. Where I live people’s food budget is such a small % of their disposable income. They are very health conscious. So they pay whatever the price is to get what they want. They don’t switch to a lower cost item. In other words the price of the items is inelastic. This is the best inflation measure out there. So I’m keeping a close eye on it.

This weird bond world proves the bond market is 100% rigged.

I guess the US government will just borrow money on the short end, and the Fed will only print money at the short end!

There will be no money printed on the long end!

The long end be dammed!

Who is buying the bonds?

BlackRock that’s who.

Brought to us by our dear friends at the central bank near you.

So, if Rchon is right; “The only way to make a “real” return at current bond prices prices is to have deflation. But deflation seems to off of the table with the 10 year implied inflation rate > +2.20% .” And Blackrock is buying bonds..

Does that mean a possibility of deflation? I am assuming Blackrock is not especially altruistic.

Or if you have your money in a savings account at 0.00000001%

“So maybe the Fed would crack down when inflation stays above 4% or 5% for a “while?” Once inflation has solidly set in, it’s hard to stop. That’s the rat the Treasury market is smelling, and if you’re sitting on a bond that yields 1.2% for the next 10 years, that’s not a mouthwatering item on the menu.”

So true. Seeing my savings account monthly statement from my credit union arrive, frankly, feels like taunting now.

On another note (sorry to kill your thought processes)

The next nominee to be chairman of the Securities & Exchange Commission could have… That maybe have…a net worth between $41 million and $119 million. !

A Goldman Sachs / Vanguard wonder kid?

Born in Maryland whose daddy took him as a youth to count nickels from the vending machines. – Wikipedia

The s a lot of nickels in 64 years.

The worst things get the more they stay the same.

-K

Yep! Foxes being put in charge of all the hen houses!

Everything is now perfectly normal!

As far as inflation goes, none for me, but plenty for you! Government to borrow at “zero” short end but you have to borrow at long end!

Yep…Gary Gensler….check out his performance at the CFTC and his relationships with TBTF.

Real Treasury yields

5 year -(1.76)%

7 year -(1.39)%

10 year-(1.02)%

20 year-(.51)%

30 year-(.27)%

The only way to make a “real” return at current bond prices prices is to have deflation. But deflation seems to off of the table with the 10 year implied inflation rate > +2.20% .

So who is going to buy bonds to finance the estimated $ 4 +trillion Federal deficit . At the above negative real yields , the answer is basically ONLY the FED . And current Treasury holders will probably be the source of some additional selling because of the negative yields at current prices.So nominal yields ( inflation + real yields) are going have to go a lot higher to attract bond buyers and compensate bond buyers with positive real returns. The FED is in real bind of their making. The more that they buy , the weaker the dollar. And the weaker dollar makes all imported goods sold in dollars cost more and causes inflation in imported goods.And a weaker dollar means that foreigners will be not be buyers of Treasury and will be net sellers. A weaker dollar also means that more and more transactions will be done in other currencies , weakening the dollars status as The RESERVE CURRENCY.

There are obviously lags between Treasury yields and mortgage rates , but mortgage rates are only going higher with Treasuries at these rates.

Junk bonds have a relationship with both interest rates and with the strength of the NASDAQ. But buyers receiving only 4.91%( HYG etf) are

being compensated very little for the risk that they are taking.

Higher rates mean that a significant correction in stocks is inevitable

A $4 trillion budget deficit? But wait…we’ve been told a $1.9 trillion deficit financed spending has never ever happened before ever. Well except when we did it yesterday and the day before and the before yesterday and the day before that and….

The CBO has projected a budget deficit of 2.3t PLUS any additional deficits resulting from the stimulus bill.4t looks entirely in the ball park.

+green new deal

+student loan forgiveness

+Medicare for all

If something can not continue indefinitely, it won’t

Happy1,

Medicare for all would reduce the deficit not increase it.

@ Conan Dillion

Medicare for all would likely decrease medical costs for all (as well as quality of care in all likelihood), but would vastly increase Federal spending and therefore the deficit by any calculation from any independent party, see Obamacare as a small scale example, not remotely neutral to Federal spending.

I think that’s back to back deficits of $4 trillion. That’s $8 trillion or about $25,000 per US citizen, or maybe in the $50,000 range per tax payer.

Probably going to be paid back by financial repression. A few more years where a million bucks will get you a $10,000 nominal income.

As a Canadian, who is used to and considers it normal for a mortgage to have a term (usually max five years) before the interest rate resets, I find it almost incredible that any bank would commit to 30 years at these rates that are possibly the lowest real rates in history. (A UK banker has said ‘lowest in 5000 years’)

I assume there is a perception of a parachute or Fed emergency aid when rates rise.

The note gets sold once or twice as a mortgage securities ( yes was a no no not to long ago because of the horrible damage it did to the housing markets but now it’s full speed ahead Wall Street and waa laa.

Most aren’t looking up for a rescue parachute this time. That is if the survived the last onslaught, sad many now were to young to know of it.

nick kelly,

Most of the 30-year mortgages are dumped into the lap of Government Sponsored Enterprises, such as Fannie Mae or Freddie Mac, or government agencies such as Ginnie Mae or the Veterans Administration. Banks can securitize the remaining mortgages that don’t qualify for government backing (too big, etc.) into “private label” MBS and sell them to investors, such as pension funds.

Why is Fannie Mae stock worth 1/30th of what it was 15 years ago if the real estate bubble is bigger and vaster than then?

There is a chart out there, that shows since 2010, YOY, either 95% to 98% of all loans are bought are backed by the GSEs.

Nick your right. Very few banks are willing to give out a 30 year loan at below 3% rates. To much risk.

The mortgage lender funds their mortgages at the ten year rate and lends at the thirty year rate, that’s the spread they make. They can do this because they know the average life of a mortgage is less than 10 years. Almost all the mortgages created in year 1 will be gone in year 10. The leftovers are a very small number, insignificant amount in terms of a mortgage pool.

This isn’t entirely true. Mortgages are amortized……they front load the interest!

Additionally, loans are funded primarily from REPO until securitized. This makes the spread even greater. To top this circle of life off the loans themselves can be used as collateral in the secondary funding markets. Ask me how I know?

But you’re spot on in that things are not as they seem.

C

C,

I worked at Bear Stearns before subprime. By the time they blew up, they were funding in the repo markets, until the day no one would lend to them any more. The rest is history.

Front ending the amortization is a shady thing to do, but nothing surprises me anymore. The mortgage business is now like the used car business. Good luck out there borrowers.

The mortgages never actually last the 30 years. They usually get paid off or refinanced in 7 years, average. That’s why they track the 10 year treasury rate + 1 1/2% or so.

Yes, but if the Fed loses control of rates, and they increase steeply, housing prices will decrease such that many people will be underwater, and won’t be willing to sell.

That could happen. I got caught up in the Volcker interest rate squeeze in 1981-1983 and wound up staying in my home for 21 years before moving. It took almost that long to get into the black. Current buyers will have to wait 10 years just to break even.

This is equivalent to a huge wealth transfer, it’s just that the dummies who buy these securities think it can be unwound. Financial repression is working, but more like a spring storing tension. These people are going to get whacked in the face with the spring one of these days. Waiting for like just about a decade now…. It has to be a very tight spring after all this time.

Even the tranches going out into the first year of a mortgage pool are a death trap now.

Some smart people I am reading think assets are going to deflate later this year with stocks getting crushed and ten year back to nearly zero before Fed runs balance sheet to $30 trillion and then we are through with this cycle and then it’s inflation’s turn and rates will rise whether Fed wants them to or not. A lot of smart money people are holding gold and bitcoin in their personal accounts. Always have to have some cash as number one priority. Can’t run out of that.

PS: no doubt no one is staying in a 30 year in this 10 year period or so of constantly falling rates.

I am positing a rising rate.

Everyone does a refi to get the lower rate.

Question is: who would refi into a higher rate?

If mortgage rates were to return to the average of the last 100 years, an existing 30 yr fixed would be a prized asset which the owner would never pay off and a buyer would assume if possible. That is the trap for the lender, public or private.

A landlord would refi at a higher rate if he needs the cash for other deals and the rent covers the refi. Or someone who has more income than savings and needs the cash.

Rcohn,

This is my take of the situation.

Average people in America and most developed countries, have protection from bank failure for savings. Everybody else and those with enough money will have to find other ways to safeguard money. Right now, there is too much money in savings and investments across the world (mostly by top 10%) and as this this situation spirals out of control, there will be more scams, bubbles and eventually the rate of returns on investments should logically go negative. The treasury yields (if you see them as safe) can be a good safety asset. As those with alot of money should spread it around, bonds are seen as a safe investment. A rich person in America might have the full 250k in their savings that’s protected, after that they have to decide whether it’s a good time and what percent of holdings to put in stock market. Other than bonds there is not many options left. Precious metals would be difficult to store in significant volume for those rich enough and the precious metal vaults of the world massively sell more paper gold than they actually possess. The main remaining practical option is real estate, but that is very risky and potentially hard to manage for those rich enough. I can see many states charging special taxes for those using vacant land as investments in near future.

Who am I trying to envision with this? Anyone who has k250 to use as play money in a bank is rotating that amount or close to it as a stop gap measure against bank failure while spending that amount on a weekly if not bi-weekly living expenses. The bank is only obligated to cover maybe 12 – 14% of that FDIC insured k250.

So for most it’s a stupid non starter to store that kind of wealth in a saving institution.

As for a rich person still in the stock market casino perhaps as a hobby or kicks and giggles.

A rich person invested in bonds? Oh stop it.

A rich person invested in land and precious metals very likely.

The Gates boy the one that born after his older sister is rich and he just became the largest owner of farmland in the United States. Yes the largest acreage wise.

Your argument is directed towards upper class plebs.

Most I believe aren’t following this nonsense.

The wealthy are majority owners of Muni bonds because of their tax free status. And older people are disproportionately wealthy and also disproportionately invested in bonds. I don’t have numbers, but would bet bonds are owned by the wealthy in the same proportion as other relatively safe haven’s like gold and property.

I am not rich but heavily invested in stocks market and bitcoins.

Some real estate and pm

Btc n stock market has been great so far.

We have the fed backstop and id keep playing although I have absolutely no confidence in any of thr assets I play own including real estate

Everything is bubblicious and would come crashing down one day for sure

Till then I’d enjoy the show and even be dead before that

People who own certain kind of assets are biased usually and think it won’t come down but I am no fool.

With all due respect, are you no fool? You seem pretty confident that it’ll come crashing down after you’re dead. What makes you think it won’t be next year? Would you be able to weather a 60% drop in the value of your stocks?

Jon, I want to clarify that I didn’t mean it as an insult. I just keep getting this sinking feeling our whole foundation is on quicksand, and that no one knows what to do.

There are many potential issues with investing in real estate though, such as is your area investment worthy and is it a good time to buy or will the value soon drop. The big issue with large investors, especially out of state and foreign investors, is that they could get hit with special taxes (especially on undeveloped land). The gates family might regret those land purchases if property taxes triple and there is a large land transfer fee. For RE involving actual housing, new taxes would be more difficult to implement in ways that couldn’t be transferred to tenants, but there are ways to do that. If only large out of state owners had to pay these taxes then it would be more difficult to pass on taxes to tenants as the out of staters would have to compete with those not charging the taxes. Quite alot of things like this could happen and while America likes to have loopholes that the rich can circumvent, loopholes are easy to close. Predicting what happens next is a guessing game at this point. But RE, like the stock market, isn’t some magic money tree.

“Precious metals would be difficult to store in significant volume for those rich enough and the precious metal vaults of the world massively sell more paper gold than they actually possess.”

It’s actually very easy, even for small investors. You can buy allocated physical gold in a vault at Bullionvault, Goldmoney, Perth Mint etc. YOU have legal title to the gold itself (unlike paper gold or gold in a bank). They don’t lend it out. Bullionvault is audited daily and storage cost is very low (0.12% annually for gold).

Legal title for physical gold on the other side of the world is not gold, it is a paper receipt at best, an electronic bookkeeping entry like bitcoin at worst.

@Lisa_Hooker

No. If you pay a vault operator to store physical gold for you is is legally your gold.

If there are problems you can travel to the jurisdiction of the operator, hire an attorney to present your case, and if you get a judgement for recovery petition the local police to TRY to obtain “your” gold.

Again, you don’t have any gold – you have a “legal” claim on gold – somewhere.

The only gold I would want to hold is that which I can have in my physical possession. The hell with these paper receipts. Too many scam artists out there.

Possession is 9/10’s of the law. That saying didn’t appear out of nowhere. Let me ask you this, have the past 12 years strengthened your view of the law? Do you honestly believe we are ruled by men, or laws?

Leas a hook has this one correct YS:

If you have never been ”in custody” of law enforcement personnel, ya just cannot understand the difference between the law(s) and law enforcement systems.

It is HUGE,,, and requires a ton of money and/or lawyers/gun slingers, etc., for any individual to obtain ”justice” of any kind.

As a law student for a few months many decades ago, this was explained only by the constitutional law professor who had actually worked in the legal system for several decades before he went to law school,,, and had dedicated the rest of his years to trying to improve the USA legal system, kinda like a certain ”knight of olde who was famous for jousting with windmills.”

Been doing my best to stay out of jail since, with only mixed results: good in the ”good old boy network” of my the area of my youth where I was a known entity; not so good elsewhere.

IOW ys, there really is no way anyone should consider that they certainly/permanently own gold, or silver or real estate or really anything of any intrinsic value far far away.

Like you should never park your car in a car park, because if the car park operator goes bust you lose your car?

YuShan,

A very small investor can store actual physical precious metals in many places. The very rich could probably own their own vaults. Those in between though, have to use someone’s else’s vault though. It’s known to be a fact that the gold vaults of the world have way more paper claims for their gold then actual gold in their vaults. No matter what, they can charge huge amount to get that gold out of the vaults, if too many try to withdraw, the question is who is getting theirs? Car parking is a bad comparison, because you actually own your car. With gold vaults, you don’t, you have an IOU.

You might be asking what if I own a particular piece of gold in a vault. But, you may not realize that several others might have a paper claim to that same piece. Say you actually deposit a piece of gold, that vault may actually be selling shares of it. In general, if you don’t own the gold vault, you cannot trust the gold vault. Alot of vaults also have less gold than they claim.

There are, some actually trustworthy precious metal vaults out there, but, how do you know which one is safe?

@Thomas Roberts

“With gold vaults, you don’t, you have an IOU.”

NO. With the ones I mentioned (Bullionvault, Goldmoney, Perth Mint) you own the gold outright. Its not an IOU, it’s allocated gold. That was my whole point.

Check them out if you don’t believe me.

Aren’t you that typist from YuShan always worried what little Johnny is doing in stead of paying attention to the way the gold markets work?

There’s only “too much savings” because central banks have created so much money and made it that way.

Yes, that’s the “savings glut” for you. If there were too much savings, then why did the Fed just print $T5 to fund new government debt?

YuShan, yes. I think the definition of chutzpah should be changed from the historical “The boy who kills his parents and begs for mercy because he’s an orphan” to “The central banker who prints trillions of dollars and then says that interest rates are low because of a glut of dollars.”

YuShan,

Someone’s debt is someone’s savings. There is way too much savings (counting investments, unfortunately it’s not very well spread) and debt in the world currently.

Right now, when the actual global economy isn’t really growing the question is why should there be any returns on investments. Right now, many asset classes are being simply bid up in a bubble. Some RE is becoming legitimately more valuable, because of societal changes, however that means other land in a non growing economy should drop in value. The stock market and investments cannot forever grow faster than the actual economy.

When a person saves up money or invests, they are temporarily forgoing spending in the present in an attempt to spend the same or more in the future. The question is whether in a non growing economy that doesn’t have any need for that savings or investment, should you even get the full amount you put in back? On average, I would say no, many investments will make money, even more will lose. If you spread your money around without very careful investment and planning, you will overall lose money and if you have someone manage this all for you, you will lose even more. You can put money in the bank, but it will slowly lose value because of inflation. Even if the value stayed the same and people saved up alot for awhile, when that money actually got spent, it would lose value. Even precious metals which if invested in would always hold some value and go up quite a lot, once the selling of gold outpaced the buying, the price would crash.

Right now, most believe in Disney fairy-tales of putting away 1 dollar today will give you 10 (inflation adjusted) when you retire. But, it really shouldn’t be able to outgrow the actual economy (on average, in the long term). Instead, people will eventually get less than they put in because those who “invested” your money for decades took a bunch of it. Inflation, may hide some of it.

For the average person the only viable options I see for retirement are your family supporting you and/or transfer payments (social security, would have to be raised over time) and other benefit programs. The average person continuing to have their money put into the stock market and the such will only result in even greater income inequality. At best (my guess) one last major wave could hit US stock market. After that it will be pretty downhill for average person.

Right now, most of finance involves the average person trying to build a retirement and the rich trying to get that money and all the remaining money and assets in the world. At the same time, that money on paper grows far more massively than it actually is. The average person no longer buying into financial sccamms, would greatly help reduce income inequality.

Yesterday I had a conversation with a good friend of mine. He is a graduate of Harvard and Harvard Business School, was a drug analyst for 20 years and a stock derivative trader for over 25 years, so no one would refer to him as financially naive.

He is concerned about holding any monies in any of the large banks and is even concerned about his substantial cash balances at Treasury Direct . I tried to hold his hand and told him to worry about other things. But later I thought about this. Why is an investor who understands the financial markets better than 99% of the people on Wall St. and who has made very substantial monies worried about the very basis of our banking system . So many events have happened in the last few years that I thought was impossible that maybe his fears might just not be so ridiculous.

How many people predicted a squeeze of hundred times in GME a year ago?

How many people predicted that spot natural gas in Texas would rise 109 times in just a few days?

If you adjust yield for CPI (=1.4%), the 20-year and 30-year real yields are positive.

What you’re citing as “real yields” is based on TIPS market prices.

Just wait

The real estate would come down in due time and especially where the market is very hot )

This time is different but effects are same:)

Yes , those numbers were derived using TIPS .

But using a CPI of 1.4% is to say the least unrealistic and backwards looking and is not characteristic of your usual fine analysis.

Yes, understood. I just wanted to clarify where this came from because it was kind of confusing otherwise.

Inflation expectations among consumers is even higher than in the TIPS market. NY Fed’s consumer survey shows a 1-year median expectation of 3.03% with a 3-year median point prediction of over 4%.

Wolf,

Even taking your CPI figures that’s a lot of risk (falling bond prices) to get a measly .25 or .5% return. I still can;t understand why anyone would tie up their money for that long a period when their upside is limited and their downside is huge.

They are counting on NIRP making its US debut.

Every time we think DC couldn’t sink (the interest rate) lower…

Basically USD lenders are living with an abusive spouse, telling themselves it will never happen again as the G slips on the wife beater…

Alternatively, think of it as “Brokebuck Mountain”…”I wish I knew how to quit yuu.”

The interest rates on treasuries, investment grade and stock dividends on SP500 are approximately inflation rate. Retirees with thirty year time horizon going to be looking at about a 3% draw down including dividends and that’s assuming you don’t make mistakes. Might take 2% drawdown to make it all work out.

Breakevens are making new highs, high B/Es are not good for TIP buyers.

https://www.treasurydirect.gov/instit/annceresult/press/preanre/2021/R_20210121_3.pdf

The days of buying TIPS at auction for below par and getting 2.5 or 1.25% appear to be long gone.

“So who is going to buy bonds to finance the estimated $ 4 +trillion Federal deficit . At the above negative real yields , the answer is basically ONLY the FED”

So who is buying sub-3% mortgages? Same answer, “basically ONLY the FED.” The Fed is sitting on over a trillion dollars worth of residential mortgage backed securities. If the Fed stopped buying, mortgage rates would easily crest over 4%, and the booming single family house market sales would fall. Rule of thumb is that for every percent the mortgage rate falls, house prices rise 10%. Why wouldn’t rising mortgage rates have the opposite effect?

We are in the doom loop of fiat. Addicted to debt, Janet Yellen tells us a $2 trillion deficit is not enough, we need $4 trillion. Stock prices, house prices, college prices even car prices are all dependent on the debt bubble expanding. It’s where you always end up with fiat. It’s not that difficult. We all had rather consume than produce. Money printing gives a wealthy nation that illusion for a while.

Everyone buys until you run out of stuff to buy because you have nowhere to put it. My brother-in-law has 9 flat screen TV’s in his huge house. He can’t find a spot for another one.

Oh, he has three cars and only one is being driven.

Lucky guy!!

Anthony A,

Just for the heck of it…what does he do for a living…and in what metro.

I ask, because in Debtopolis it isn’t hard to live like a millionaire on a thousandaire’s salary.

Cas127, he’s a retired millionaire oil co. exec. living north side of Houston. He’s one of the lucky ones who got out in time.

AA,

He must have been really lucky.

From 1985 to 2003, oil industry ranged from disaster to meh.

From 2003 to 2013 was the boom. Oil went from sub $25 to $100+. This was the time when real money could be made.

Post 2014, though, pretty much downhill for oil industry, with hundreds of corporate bankruptcies. Prices fell from $100 to about $30 (excluding Covid implosion).

Oil is a very volatile industry.

That oil exec really threaded the needle.

He did 40+ years at Shell and was Sr VP of Lubricants at the end. He was a Chem Eng that developed several oils for aircraft engines then went up the line in sales and marketing. Got out when Shell sold that business in mid 2000’s.

He truly was in the right place at the right time and was pretty savvy.

re: “The only way to make a “real” return at current bond prices prices is to have deflation”

NO, the only way to return to real rates is for Congress to drive the banks out of the savings business. I.e., the velocity of circulation is destroyed as bank-held savings increase. Banks don’t lend deposits. Deposits are the result of lending. So, $15,000,000,000,000 in monetary savings is indeed frozen.

And savings flowing through the nonbanks never leaves the system in the first place. There is just an exchange in existing bank deposits in the payment’ system.

The “Taper Tantrum” is prima facie evidence (which I predicted). The FDIC reduced deposit insurance from unlimited transaction’s insurance to $250,000 (which was increased from $100,000 in 2008).

80% of all trade is done using US Dollars. Its the best option available at the moment….

1.21% ??

Much better to purchase appreciating assets; anything physical that might hold value or has the potential to appreciate.

regarding: but mortgage rates are only going higher with Treasuries at these rates.

I agree, but higher mortgage rates means lower RE prices will accordingly follow. This all makes sense if people use cash and don’t finance.

I would buy farm land in the kind of place people would choose to flee. The big push into Idaho and Montana suggests it is already happening for a variety of reasons. That it is known, indicates it is already too late for those states and folks should look elsewhere, imho.

Regards

I think I would have rather held a gold bar than a US treasury bond, over the last 20 years.

I don’t know what interest rate gold pays (I know gold doesn’t actually pay any intetest!) but since 2000, gold’s price rise (converted into an annual interest rate) has to be much higher than 20 years of US treasury interest!

“I don’t know what interest rate gold pays (I know gold doesn’t actually pay any intetest!)”

It does pay interest if you lend it out. Central banks and institutions do this. I don’t know if individuals can do this in an easy way, but of course this exposes you to counterparty risk, the avoidance of which is the whole point of owning physical gold!

If you look at the real estate prices during the great inflation of the 70s they didn’t come down despite high interest rates so I am not sure why would they crash this time.

Theoretically, if inflation is high, shouldn’t houses be a form of protection from it?

I wonder to what extent people are smelling a rat with multiple offers and very little inventory right now, what better inflation play than locking in a 30 year low mortgage on an appreciating asset?

Without having checked the actual data…. (perhaps an idea for a future Wolfstreet post?), I think in the 1970’s, houses were financed with smaller mortgages than today, so mortgage rates were probably a bit less important for affordability than they are now.

In the early 1970’s, mortgage rates (30yr) were already at about 7.5%, before big inflation started. Today they are at 2.75%. If rates go up by even a few percent, that would quickly double mortgage rates. At 2.75% housing is already unaffordable for many, so at double the rate who can buy at current prices? Unless wages double (not a chance).

Real estate as well as stock market can’t bear higher interest rate

Buying a house with an assumable mortgage was common in the late 70’s/early 80’s.

You are correct YuShan, higher rates will make it harder for people to buy current house prices.

I just don’t see rates even getting to 5% anytime soon. Last time they were above 5 was in 2009. Why will rates stay low.

Rising rates would really put the hurt on the federal government spending. Also a lot of companies have taken out huge amounts of debt to buy stocks back.

Everyone wonders how long we can stay at ZIRP. Well Japan started ZIRP in 1996 or 25 years ago. The U.S. is only at year 10. We are 15 years behind Japan.

Thus we probably need to watch Japan to know when ZIRP fails?

“what better inflation play than locking in a 30 year low mortgage on an appreciating asset?”

Sounds too good to be true. Its a trap.

Real estate prices are NOT going up because of a good economy. We’re in a DEPRESSION!!! At least here in the Swamp.

Prices are going up because of the fallout from the 2017 Tax bill which made a paid up home a good rental investment, cutting down the amount of listings, and creating other distortions in the free market. Add in the money printing, asset inflation, devaluation of the dollar, ultra low interest rates and you get this phony real estate market.

This will all come to and end for a different reason than in 2006/2007 but the results will be the same. Foreclosures, Mortgage bank failures etc.

When these people leverage their homes to the max and the prices drop 20 – 30% they will be underwater and face the same fate as those in 2008/2009. What good will that 3% 30 year Mortgage do them if they can’t sell and can’t move to a new job?

Swamp Creature, I’m not familiar with all aspects of the 2017 tax law. How did it affect rental homes? I know it negatively impacted owner-occupied homes in high property tax states.

The 2017 tax bill CORRECTED distortions in the market created by previous tax policy (SALT and excessively generous mortgage deduction).

The tax law of 2017 pushed a lot of people onto standard deduction vs itemized. People who had their homes paid off found that they could rent them out and make a nice income. The hell with selling. This cut down the number of houses that would have been on the market. Thus pushing up prices. So they made out big time. Higher income and higher prices. Rents are holding up pretty well even in the pandemic.

Right, I understand the tax deduction by effectively removing the desirability of itemizing, but I still don” see how that affects the rental market. Why would you be more likely to rent your house out under that tax regime?

Indirectly

Once you have paid off a lot of the mortgage or all of it you lose the tax advantage of the Interest deduction. The 2017 tax law accelerated this process. Pushed people onto stnd ded. So you pay off the loan. Then you need more deductions. A rental home has tax benefits, depreciation, expenses, etc to offset the loss of the itemized deductions. “Schedule E” I believe. I don’t own rental property but I can see why people would rent their houses out now more than ever. Its a good investment. The 2017 tax bill made it less advantageous to be a owner occupied homeowner (lost deductions) and better to be an absentee landloard (kept writoffs).

I may add that the 2017 tax bill was a disaster for the middle class especially those in the blue states. If you live in Maryland and went off itemized deductions and went to standard deduction your Maryland taxes skyrocketed. Offset much of the tax cuts which went to big corporations and oversea tax havens.

On the Fed level you lost your medical ded, state & local taxes ded, and charitable ded. Trump listened to those s$itheads from Goldman Sachs, Gary … , House Ways & Means Kevin Brady, Paul Ryan to draft the tax bill. This was one of the many blunders of his administration.

Happy1

Why it is it OK to change the rules in the middle of the game. People bought houses with the expectation of being able to deduct SALT taxes. The deductions were factored into the price they were willing to pay for the house. Why is it now OK to screw them over just because they happen to live in a Blue state. And for what gain ??

@ Swamp Creature

Tax laws change all the time. Just because something has existed for while doesn’t make it fair of good public policy.

Is it fair for people in low tax states to subsidize SALT and mortgage deduction that overwhelmingly benefit the top 10% in high tax locations? Is it good policy to encourage states to have high taxes knowing that the Fed will kick in to compensate? And I’m saying this as someone who is also a net loser on the SALT changes.

Best policy is low rates and few deductions. That leaves to less shenanigans and simpler taxes for everyone.

Swamp…a lot of that makes sense. Also the fact that millies are now wanting to have families and are actually buying houses. They see house prices rising and buying as an investment. i.e.

There is a lot of talk about MMT. $1000 or $2000 a month. It that happens, I doubt there will be any houses sub $300k. Why?

If a low income person suddenly gets $2k a month, why not buy a house with the $2k. They could get $300k house for $1500 a month and have 500 left to spend. Plus they will not have a rent payment anymore.

Happy1

They took away all your deductions and put you on stnd deduction. Now the new Admin is getting ready to raise your tax rates. Also, they made it easier for the IRS to do your taxes before you even lift a finger to do yours. Better make sure your numbers are correct. They’ve got all your information already. Its all in their computers for an automatic audit on everyone.

I’ve heard that BS about Red low tax states subsidizing the high tax Blue states a dozen times. Those high tax states pay way more to the Fed government than they get back in benefits.

Swamp Creature, with all due respect, of all the memes on the Internet, this is one of the most intellectually dishonest.

States don’t subsidize states at all. Nearly all of the federal spending that takes place is individual transfer payments (Social Security, Medicare, Medicaid, etc.). Wealthy people subsidize the poor, and currently working people subsidize the retired. That’s how it works, and where any of those people happen to live is irrelevant.

Too much house has taken down a lot of people in hard times. You got to make the whole nut including utilities, taxes and insurance every month for 180 to 360 months whether you have a job or not.

Swamp Creature has a very good point.

There is a motivation to hold onto a paid-off house and rent it rather than selling.

1) You won’t have to pay a large windfall capital gains on profits over 250K. It is 20%.

2) Unlike a primary home, you can fully deduct all expenses including property taxes, any interest, and repairs. You can also depreciate the house. These are all deducted from any rental income. I know most with new rentals who pay no taxes on rental income since the deductions and depreciation match the income.

3) The rental house has historically (since 2000) returned an increase in value higher than inflation. Sometimes much higher. Can that continue?

The hassles for landlords has been mostly due to the quality of renter who may not care how they treat your investment.

1) Trashed houses that cost tens of thousands in money and time to repair. That damage deposit isn’t nearly enough.

2) Recently, during Covid, renters who do not pay rent and not likely to pay back-rent without large legal expenses.

3) Even before Covid, it was costly to evict for non-payment.

4) Time and money to maintain the property. For a primary home, you live there and can stop a leak before costly damage is done. If you don’t live there, a renter may be less likely to report a costly issue for fear of rent increases. I stay busy enough repairing and improving my primary home. I’d have to pay a property manager (tax deductible) to maintain a fleet of rentals.

I’d rent to someone I know and trust. Most landlords I know, require a credit check for any tenants at a minimum.

My brother was a landlord for a decade in the early 2000’s. He said that he would never do it again because he had terrible tenants. He sold in 2006 so he just paid the windfall in taxes. If he had sold in 2011, he would have experienced massive losses.

There is a disconnect between the average price of a home and the average income a person makes. Eventually the real estate market will have to come back down to reality.

Its up to ten times annual income. Same as just before the 2008 meltdown.

Not without a lot of pain

Houses in the Swamp are going under contract for 5% or more over the appraised value in many cases. The buyer will have to kick in cash at settlement if they want the house. No more “No money down” deals. The additional cash they have to come up with doesn’t get them squat. If prices decline they will be underwater in a heartbeat. Welcome 2008 redux.

@Paulo

“Much better to purchase appreciating assets; anything physical that might hold value or has the potential to appreciate.”

Unfortunately it’s not that simple. For example in the stockmarket, returns of the past decennium were really driven by P/E expansion. When that mean-reverts, the market can come down a lot, even as profits rise.

In addition to that, corporate balancesheets are at record leverage. That helps their P/E in good times, but if they need to deleverage it works the other way.

And then there is record margin debt and people using home equity to finance stocks. etc.

In other words, there are so many layers of leverage that are stacked on top of each other. When all this goes into reverse, it will eclipse the actual real value creation of these companies.

If you look at profits over many decades, it is remarkably consistent. The biggest contributor to market returns over a limited period is really multiples expansion/ contraction.

For this reason, you cannot just say: let’s buy something “real” and I will be OK. Valuations and the amount of leverage in the system matters.

I owned real estate in CT in the late Eighties that lost 50% of its value in the early Nineties. It took a decade for market value to return to the 1988 prices. I was a Realtor. I left the market because selling homes was no different than peddling rapidly depreciating baubles like cars and electronics. Buying something “real” only works if you don’t buy near the top of a roller coaster market.

YuShan, yes, exactly. I keep hearing people say that inflation is coming and “stocks in quality companies with healthy balance sheets are good protection against inflation.”

The issue is that even the “healthy” companies with unlevered balance sheets are dependent on those that “unhealthy.”

For example, Microsoft. It makes a ton of money from its software as a service and cloud infrastructure, and its products have a relatively low marginal cost to produce. But how many of its customers are zombie companies with excessively high leverage? The same is true for Google and Facebook’s advertising revenue.

That’s the thing that tech bulls don’t seem to get. The tech companies’ fortunes are tied to the rest of the economy in the final analysis. If the economy starts raveling, big tech won’t be spared.

RightNYer

You hit the nail

People don’t understand how interconnect things are

Thanks

Recently, I saw a former top guy from Facebook explaining that from every $1 spend by these hot startups, IPOs etc that only burn money, $0.40 of that ends up at Amazon, Facebook or Google.

Also profit margins are near record levels, these will revert to mean and cut stock valuation also.

“Also profit margins are near record levels, these will revert to mean and cut stock valuation also.”

Can’t really assume that, especially given the trend is for profit margins to increase not decrease. Change in govt policy will be needed to reverse. Probably due to govt policy of wage suppression (importing cheap labor, reducing workers rights, increasing corporate power and monopoly).

Selling your home in California and moving to Montana was 30 years ago.

Yes, any physical useful item should hold its value now. I was buying old well made U.S., German tools for the last few years on Ebay. Now they are getting ultra-pricey, people are catching on.

What’s worse, the availability of many needed things may not always be so handy in a depressed economy. Toilet paper may be the last thing we’re worried about.

“The big push into Idaho and Montana suggests it is already happening for a variety of reasons.”

Prices are already topped out in these places. Buying real estate or land right now is a fool’s errand. It’s like buying at the peak in 2006, but worse.

Inflation of 4% to 5% is so last decade.

My gut tells me a better measure of inflation is the average of Housing+healthcare+cars. Maybe about 10% or a bit less which is what housing is presently rising at year over year?

Funny all three of the items that likely provide a truer account of inflation that construct called CPI – housing/healthcare/cars – the Fed has either removed from it’s inflation reporting or neutered into gobbledygook hedonic meaninglessness.

I could not agree more. Add college tuition and I agree completely, the major items that most households are spending on.

don’t forget food. people tend to need it, and it is getting more expensive too, although perhaps not as quickly as those big ticket items.

1.21% ten year treasury yield is approaching the SP500 SPY 1.40% dividend yield. Hmmm, which investment is safer?

SP500 earnings yield is around 3.1%. SP500 is about 3940, so another 1.5% by end of next week to hit magical rounded number 4,000. Then another 10% from there to to 4,400. Point being, not much meat the bone for the risk taken, as note that FT reported the Fed asked the banks last Friday to stress test the SP500 crashing 55%. 4,000 to 1,800 is a 55% drop…yet not saying it is going to happen, or even the Fed will allow it anytime soon, yet it is facinating they ask the banks to stress test a 55% collapse as that is about exactly where it should have crashed to if the Fed had not bailed out the top 1% last year.

So right now the Fed is happy to allow Crypto, TSLA, and other imaginary investments to absorb billions of the QE to keep it out to the actual stock market and the real economy, but once that falls apart and that liquidity flow goes into “real things” that people actually need, that is the point where the Fed might allow the markets to collapse as a mechanism to control the out of control inflation as they can’t raise rates, yet letting the markets collapse is a wise option IMHO, as that would cause deflation almost immediately…

Remember, the Fed works for the banks, not Wall Street or the top 1%. With the Fed and Treasury now tied at the hip and working together to give out trillions to the bottom 99%, not sure they will bail out the top 1% when they allow the markets to finally crash at the point they need it to “fix” inequality, inflation, etc. Keep an eye on J-Pow’s long $60 million portfolio as I’m sure he will get out before the music stops…not so much everyone else…

Yort,

The federal Reserve owners are not the top 1%?

Maybe that was a typo?

I think India is going to ban crypto soon. Their government probably doesn’t like the competition! They didn’t do very well getting their hands on temple gold! Don’t Indians trust their government?

India has already banned all crypto use of any kind.

On another point they did not ban Blockchain.

Silly as Blockchain technology is the weak link of crypto currency.

Although it is superior in many other applications.

Buy into the blockchain not the funny money.

Isn’t it funny how a guy creates a very good blockchain technique and says it is a currency and millions believe him.

That is what astounds me!

If you look back in history, I believe at one time shells were currency for some pacific island…until it was not.

Technology changes all the time. What if somebody else comes up with a better currency idea 3 years from now?

Nobody saw Bitcoin coming….it could happen.

I have no doubt that Powell and others belonging to the 0.1% are not voluntarily going to do anything that makes themselves poorer. That’s only human. Who cares about the 50% poor sods that get killed by inflation if the alternative is that your own stock portfolio goes down?

However, the question is for how long this is still up to them to decide. IF inflation were to run persistently hot, the bond market will force their hand. And hubris among policy makers suggests to me that there is a significant risk that they will be (much) too late to reverse and will eventually be forced to raise rates by much more than anybody now anticipates, or totally lose control.

Also, the idea that you can “inflate away” this amount of debt is a total fantasy imo. The debt erodes only slowly, but refinancing costs go up immediately with rising rates. You would have some chance pulling this off if you had a balanced budget, but deficits are only going to rise this decennium due to unfunded liabilities (entitlement spending going up massively).

Federal Reserve Chair Jay Powell: “I do want to begin by agreeing with your first point, which is the economy is far away from maximum employment and stable prices – and the balance sheet will be the size that it needs be to provide support to the economy. As you know, we’re currently buying assets. It’s a key part of what we’re doing in providing overall accommodation to the economy. That is our focus. We’re not thinking about shrinking the balance sheet, just to be clear…”

Powell gives lip service to unemployment, but he’s really just inflating asset prices. It is not the unemployed who benefit from inflated asset prices.

Inflation creates jobs. Powell said that. So we know it’s true. If we keep printing, the jobs will come.

Remember a long time ago, in an economy far far away, something called GameStop I think it was?

Imagine 100 new GameStop events every week – that’s when we will reach full employment via Powell’s program of 500,000 new day traders every month.

Powell will soon have to rent some of those off-site storage spaces to stash all the low-yield assets he’s not using.

“Inflation creates jobs. Powell said that.”

The 1970s just called. They said stagflation does not create jobs, except for demolition companies. Powell must not remember the 70s and 80s. Too many coke-fueled frat parties, Mr Powell?

Jay Powell should be arrested on domestic terrorism charges for what he’s doing and has done. I guess 300,000 homeless in CA alone isn’t enough for him. Will 600,000 be the magic number? Maybe a cool million is needed? Somebody must stop this deranged lunatic and his cabal.

You might already know this….The problem with “inflate away the debt” is that the policies that supposedly do that simultaneously encourage more debt, this defeating it’s very purpose and placing policy into a forever loop.

timbers, are you sure you understand trickle-up poverty?

Exactly. You even hear Yellen and some others in Biden’s administration say “Inflation is low, so there is never a better time to go big while borrowing costs are cheap.”

Useful Yort; thanks

Interesting theory, and not out of the question.

During Bear Mkt following GFC, S&P fell nearly 60%!

Totally agree, Yort. First inflation, then deflation.

This does not make a lot of sense. We have had inflation in the price of education, health care, stocks, automobiles, real estate, etc. whilst the 10 year UST yield has been dropping, and so the buyers of 10 year UST’s did not care aout that inflation. But they are concerned about the rising price of Blatz beer and Utz cheese balls?

It may help to start viewing inflation as the falling value of a currency.

In lieu of the general level of prices for goods and services rising.

Yes. Although I’d prefer they just correct the CPI and be honest. I know – The HORROR!

I wouldn’t believe anything the Fed says, Jerome is in panic mode, since 2008 or even to the times of Greenspan these central bankers have made mistake after mistake, dire ones, the Dollar has fallen 15% with a falling inflation rate to 1.4. There is no long term real inflation, look at the Eurozone, all there is is short term inflation from manipulations, real inflation comes from higher wages, year after year, lets not mistake their smoke and mirrors, the type of inflation people may see is oil rising (manipulation), food rising from grains, thank Trump for asking China to buy so much (China took him for a ride, they just use their treasuries), also speculation. What I am trying to convey is the Fed & Gov want to scare people into spending, the problem is people are broke, they can’t pay their rent/mortgage, or choose not to, rates are rising just like stocks are rising, doesn’t mean it’s rational or warranted, if you notice everyone is talking about the Dollar demise, it’s gonna burn & become worthless, who spread this nonsense, the ruling class of the US hold Dollars, fund their military with Dollars, if the Dollar goes so will the US, not gonna happen, the yield will collapse to join the 2 year, the vaccines will be ineffective in my opinion, give it a month & see. All in all the Fed is done, they dug their own grave, the yields rising is a sign the lost total control, they are so fearful right now because it is they who drove people into a frenzy of panic regarding inflation but it had the wrong effect, instead of spend they thought F this I’ll buy assets, like stock in hyper bubble, like commodities or whatever, this will all blow up, stocks will collapse, yields will collapse, they will never get inflation until the whole scam is flushed out with all the bad debt. In what world can you have inflation when people are jobless, in debt to their eyeballs, can’t pay rent/mortgage, car payments, loan payments, in the fullness of time people will realise, Powell & his cronies thought they are smart, just like the announcement they would buy junk bonds never came but caused a massive rush into worthless junk bonds they did to the public, they will let inflation run hot was just a sick ploy to suggest it’s coming so go spend it, It all backfired cause he made it all worse, the US taxes the world with the Dollar, the world pays for the US military & standard of living, I wouldn’t believe a word of what Powell or his colleagues say, there will be no inflation, 15% Dollar fall should have brought inflation to 5% or more, deflation was so strong it had zero effect, everything else is a massive hyper bubble, property, stocks, commodities, most people believe inflation is coming, big inflation, what Powell should be thinking now is we are F—–, simply cuz it created no spending at all. This is a view to remember, remember what I said today, even though most would disagree wait and see, the amount of propaganda & manipulation that exists is truly amazing, this whole house of cards will collapse, people should prepare, cash is the best thing to hold right now, that is why they don’t want you to.

@Jack – I enjoy your comments, but shorter sentences and paragraph breaks would be even more enjoyable and less taxing. If you would have deleted five periods the whole comment would have been a single sentence. Are you using voice to text?

PS – I am very rarely an editorial fascist. My apologies if you feel they are in order.

Lisa,

I agree and I don’t think it is fascist to make a suggestion.

The point is to communicate and the reader is 50% of that equation.

Big slugs of text are difficult to follow and often serve to bury rather than illuminate good ideas.

The is especially true for the snaky weavings of economic policy where we are all trying to ferret out the hazy implications of half spied gvt actions.

1) Bullet points provide bite size chunks of info, in a logical stepwise fashion.

2) Really.

3) Simple white space/paragraph breaks are the poor man’s bullet points. Also useful if you don’t want to read like a computer programmer.

I totally agree. I scrolled down, noted the lack of paragraphs and scrolled onward.

I don’t disagree with you, but when I get my next stimulus check it will be spent on a nice new mattress. Inflation be damned.

The 10 Year 1/15/31 TIP .00125% is priced at 112.03. This computes to a yield of -1.036% for an implied 10 year inflation of 2.46%. There’s a lot of nervous investors out there willing to pay up for inflation protection.

Wolf,

Is there some way to measure inflation vs monopoly power as the reason for the loss of the average persons buying power?

The politically correct term is not “monopoly power,” but “pricing power.” ?

The lack of “pricing power” in ecommerce has been cited as one of the reasons why CPI goods inflation has been low or negative over the years. But if you’re trying to get health insurance (CPI services inflation) in a place with only two health insurers, you’re in trouble.

About 10% of the counties in the US have a single ACA insurer so it’s much simpler there. You just pay whatever they demand.

Also Lisa, I think about half of the US has only 2 choices. Read that years ago. Probably worse now.

A few years ago, the “it” public policy thingy with NPR Radio in Massachusetts was how to slow done healthcare inflation under RomneyCare (same thing as ACA but more generous…ironic that, no?).

NPR would drone on and on with the latest most clever ideas on how to “bend the cost curve” on medical inflation. All tedious, complex, and doomed to fail.

But they never….ever….allowed these words to cross their lips or be discussed on any way – universal single payer healthcare. Their tongues would burn if they uttered them, despite it’s proven world wide success where ever it’s been used.

Who needs censorship when the media self-censors?

It is unfortunate that health care policy discussion almost always ends up being about who is going to pay. The payment problem is the smallest part, but is a good diversion from how truly awful the system is.

Clinical outcomes look bad compared to elsewhere. Even poor abused Cuba has a better infant mortality rate. We are only pieces of meat tossed onto the disassembly line. Question the doctors and be labeled a troublemaker, or follow orders and ignore the harm they are causing. Like children, patients are to be seen and not heard.

Half of us are overtreated and the other half can’t get what they need. Physicians suck at diagnosing illness. Misdiagnosis rates are shocking. If car techs were as bad, no one would drive. Iatrogenic harm is one of the top five killers, but that category is not even shown on CDC charts.

The whole system is organized for its own convenience. If patients can’t fit into the system, too bad for them. For example, when someone is sick enough for the Emergency Room, they need to rest. That means lying down. But the ER waiting room has only chairs. How is that “patient-oriented”?

I know there are physicians that do good work (to the extent they are allowed), while so many others act like patients are icky, especially the sick ones. There are not enough good doctors to go around. So a few people get good care, and the rest are just tossed aside.

The sad truth is the medical machine is rotten like so many other US institutions. Greed is good, but not for humans. The whole “pricing power” thing Mr Richter mentioned certainly plays a role.

At some point people are going to have to challenge medical machine “pricing power” and take back control of our healthcare institutions. I hope it happens soon.

The healthcare scam has me thinking of ways to screw them back. I don’t have an employers’ plan so have to buy my own on the open market. The options are few, and the price is laughable. I’ve started to think that I should liquidate my bank account, turn about half of that into precious metals and the other half into mattress money, and just claim poverty so I can get Medicaid.

I’m self-employed so I don’t get a paycheck stub weekly. I can easily go “low-income.” There’s got to be something better than paying close to $1,000 per month and getting nothing in return. Or maybe I just go naked and risk not getting care in the event of a heart attack or cancer? I don’t know what the answer is. Just thinking out loud here.

We are being played by semantics.

Historically inflation was defined as a measure of increase in money supply not increase in price level which is a consequence of the former rather than cause.

But defining inflation as an increase in price level, the government theft can carry on in a way that not one in million could spot .

I tend to agree with the Austrian school that defines inflation as government expansion of the supply of money and credit. To call price increases inflation is to confuse the symptoms with the cause, and worse, to eliminate the term to describe the cause.

Price increases are price increases. They occur for many reasons, some monetary most not.

Further, the implication is that an X% increase in the money supply = an X% increase in all prices. This is also incorrect. Massive price distortions occur at the injection points for the new money & credit, called Cantillon effects.

Those first in line for the new money & credit in effect get today’s goods and services based upon yesterday’s money supply. It takes time for those injections to ripple through the economy and cause widespread price increases. It’s a massive transfer of real goods and services from the masses to those at the front of the line…

Interesting. But, isn’t the thing about QE and ZIRP being so very bad, is that it inflates the money mostly into the procession of the rich were it remains because they spend it on things rich folks buy, and doesn’t much trickle down to impact/raise the price and items used to report “inflation”?

Yeah, and the Fed doesn’t make much mention of the massive inflation of bitcoin, houses, luxury properties, stocks, collectible cars, lumber, etc.

I see. So if the money supply were to decrease and prices continue to go up we wouldn’t have inflation. We would have???

@Memento mori

Thank you for making these much needed points. Central-bank fiat currency is the single largest act of theft from poor to rich on the planet. And it’s right in front of everyone’s faces. Yet people refuse to see it for what it is, because to do so is to draw into question the benevolence of our rulers.