“There is no justification” for continuing the purchases of mortgage-backed securities. The Fed is “misdiagnosing its impact on the housing market.” Pressure rises on the Fed to back off, in face of market craziness.

By Wolf Richter for WOLF STREET.

During the press conference following the FOMC meeting last week, Fed Chair Jerome Powell was asked by different reporters about the craziness going on in the stock market, the chaotic thingy with GameStop, corporate debt, and the housing market.

The fact that he was asked several times about the exuberant nuttiness in asset prices shows that by now everyone has picked up on it. And people are increasingly incredulous that the Fed would continue with its monetary policies in face of these markets.

Powell brushed off the GameStop thingy and gave his usual it’s-not-our-fault and it’s-never-ever-our-fault justifications for the exuberant nuttiness in the markets. The near-0% interest rates and $3 trillion in QE in just a few months had nothing to do with anything, but the drivers of the nuttiness have been the “expectations about vaccines” and “fiscal policy,” he said (transcript). “Those are the news items that have been driving asset values in recent months.”

Upon hearing this, people globally were just rolling up their eyes. And a reporter challenged him softly about the housing market – the 9% surge in prices from already lofty levels. “Are you concerned about a bubble forming there yet? And is there a price increase that you’re looking at where it might change the level of mortgage-backed securities the Fed is buying?”

That price surge “we think is a passing phenomenon,” he said. “There’s a one-time thing happening with people who are spending all of their time in their house. And they’re thinking either I need a bigger house, or I need another house, and a different house. Or a second house in some cases. So there’s a one-time shift in demand that we think will get satisfied, also that will call forth supply. And we think that those price increases are unlikely to be sustained for all of those reasons.”

He said this after having said out of the other side of his mouth, “the housing sector has more than fully recovered from the downturn, supported in part by low mortgage interest rates.

And he never responded to the question about changing – reducing – the mounts of mortgage-backed securities the Fed is buying.

Quoting Powell’s “the housing sector has more than fully recovered from the downturn,” the American Enterprise Institute Housing Center said in a presentation this week that therefore “there is no justification for continuing or increasing investment in agency MBS.”

Here are some of the points of the AEI’s presentation. It demonstrates how the Fed has gone nuts with its asset purchases and interest rate repression.

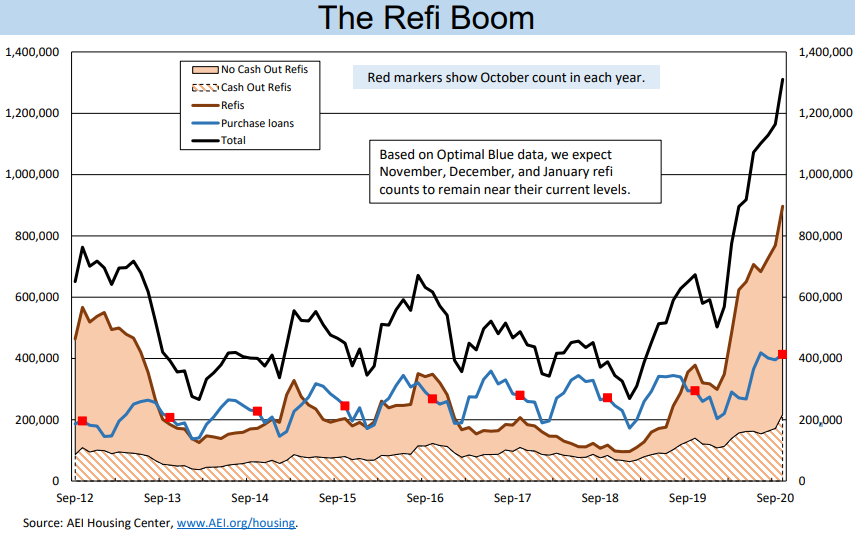

Mortgage originations and refis set new records

In 2020, an all-time record $4.04 trillion in mortgages were originated. Cash-out refis shot up 55% to a new record, and no-cash-out refis shot up 185% to a new record (shaded area). This monthly chart goes through October. The AEI says that it expects November, December, and January refi counts to remain near their October levels:

“The Fed’s Monetary Punchbowl Is Fueling Rampant Home Price Appreciation”: AEI

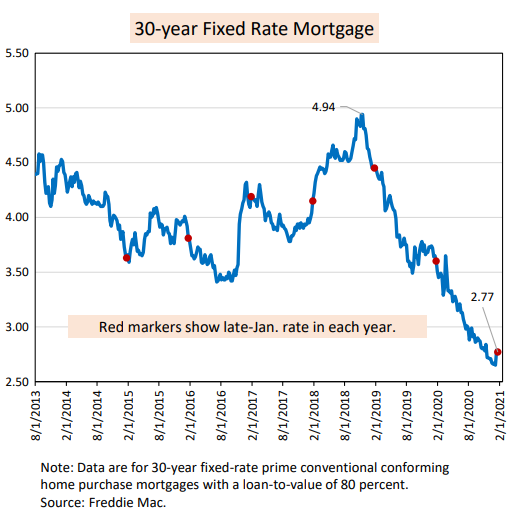

The Fed has used its monetary policy tools, including purchasing large quantities of MBS, to push mortgage rates to record lows, though they have bounced off a tiny bit in recent weeks:

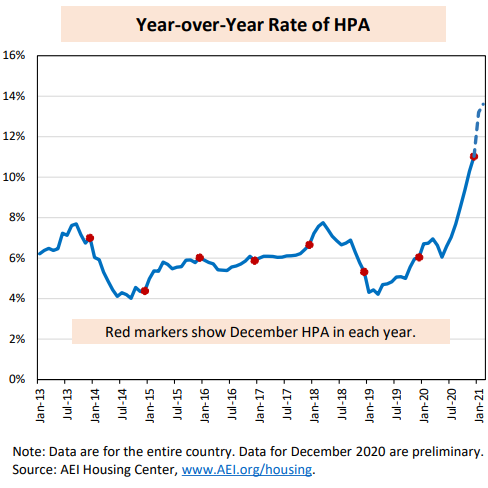

And this “monetary punchbowl is fueling rampant home price appreciation,” the AEI said. Its preliminary national Home Price Appreciation (HPA) index for December has risen to 11.0%, up from 6.0% a year earlier, “due to lower mortgage rates.” And the AEI estimates that the rate of HPA “will further accelerate over the coming months” – with the national average heading closer to 14% year-over-year:

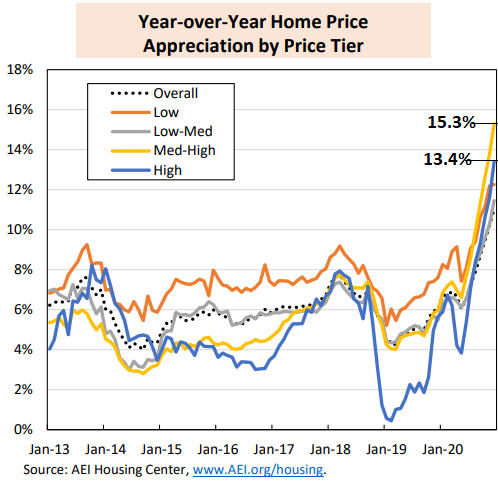

Home price appreciation by price tier: The medium-high (yellow line) and high (blue line) price tiers, “which are more dependent on the monetary punch bowl,” are showing the strongest rates of price appreciation. “This is a trend reversal, since historically the low price tier has shown the fastest year-over-year HPA”:

“The FOMC Is Misdiagnosing Its Impact on the Housing Market.”

The AEI threw cold water on Powell’s statement that the home price surge is “a one-time shift in demand that we think will get satisfied, also that will call forth supply,” and that therefore “those price increases are unlikely to be sustained.”

Home price appreciation “is exploding, with no end in sight,” The AEI says.

In the medium-high and high price tiers – “think move-up buyers” – where prices have surged the most, the default risk is relatively low due to “minimal leverage” and the “added buying power” from work-from-home. But the “arbitrage opportunity” that the shift to work-from-home offers by moving to cheaper areas that are further out in the suburbs of the same metro or moving to a less expensive metro “will likely take many years to play out.”

Default risks are higher in the low to medium price tiers – “think first-time buyers” – since they’re “much more highly leveraged” and work-from-home is less prevalent in these income categories. And in these price tiers, “affordability continues to worsen, even in places that used to be more affordable.”

And so the AEI summarizes that “there is no justification” for the Fed to continue its purchases of mortgage-backed securities.

The historic short squeeze, engineered by millions of deeply cynical small traders, exposed just how rigged the market has been. Read… THE WOLF STREET REPORT: The Stock Market Is Broken, Now for All to See

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Driving the price of shelter out of reach of the young and working class is criminal. Houses are shelter, not speculative investments. I do not say this lightly, but I am beginning to believe that nothing will change until these central bankers are punished. What they are doing is despicable, and they show absolutely no signs of abating. They’re flaunting their reverse Robinhood policies.

One wonders what will happen if the hordes of folks trapped as renters get together on Reddit and organise a mass rent strike. By the time they start cranking through evictions a lot of leveraged landlords will get taken down on cash flow.

I really think the whole Robinhood fiasco has changed things in ways we don’t quite understand yet. There is a lot of anger at the injustice in the property market and it probably just needs a spark to manifest itself.

Yes, the reddit episode with Gamestop was very much like a DDOS (Distributed Denial of Service) type action usually used to take down websites.

It turns out this can work via crowdsourcing in real life & the financial markets too.

Note, this is already done by the ‘other wise’, when the few billionaires who own most of the mainstream media have all their newspapers & TV stations they own print the same thing one morning to astroturf a ‘trend’ or a ‘national mood’ they want to push on the country.

It will certainly be very interesting to see where this goes.

Question; What percentage of American taxpayers easily filing exemption from withholding on IRS form W-4, so that you don’t have to beg for your refund, and then refusing to file any income tax return, state or federal, would so shock the system that real reforms would have be implemented?

I bet it would be less than 10% of workers.

@Delphin – don’t think that works. They’ll just print the missing money to keep US Treasury solvent, while sending the holdouts to jail. Then they’ll declare victory by noting the lowered unemployment rate (since all those jailed workers were replaced) and goosing the stock market yet again.

Home ownership is not an absolutely necessary part of a prosperous and prudent lifestyle. The Germans, Swiss, Austrians and others have a much lower home ownership rate than Americans.

That went well for a long time but it’s currently coming back to haunt them in this new globalized world. Foreign investors have been buying the apartment complexes and driving up rents beyond what folks can reasonably afford. See Berlin for example. There are millions of affordable apartments missing these days across many European cities. Add in Airbnb and whatnot.

never owned home til mid 30’s due to student loan debt and dumb choices on FREE DEBT – ie cc

took years to settle those and raise my FICO + down payment 3%

now I don’t buy unless I have 100% cash

so in current market – not interested in ‘deals’

being in hurry will cost 90% their homes due to DUMB choices

But the big tech can simply shut them off. Look what happened to Conservative media e.g. Parler.

At the end of the day, all billionaires are friends of each other and would like to look after each other.

I have always advocated that when a company screws the public, each individual file a small claim suit against that company in every small claim court in the land…that will do a great job of teaching the company a Lesson

DC…You are correct that nothing will change. This is just more of a seventy year war on the cash economy, and they are using current events to launch a cluster warhead to take out what remains of the enemy positions. Raise the price on all the things that are paid for by electronic transfers and you leave no surplus that can be withdrawn in cash. Why? To remove your ability to abstain from the economic vote. It’s like two candidates cut from different sides of the same mold which are all you can choose from. Either way, you lose. How can they force you to buy an auto filled with spy-on-you ware if you have cash in hand to buy something used that has no tracking devices? Once they destroy the cash, then they go for the metals. And by then, they’ll just dip into your accounts any time they please ’cause they’ll own the courts too. Right now, any direction you go, they will counter move before you know it is happening. This is feed lot over free grazing, and we’re all being ear-tagged.

I read a story out of China where they executed a billionaire for financial crimes. I was smiling the whole time I was reading it.

I wonder who get his billions that he left behind?

If only he held the “get out of jail free” card. Seems like they’ve got a printing press for those in the US.

I smiled reading your comment

Now you know why China is labeled “developing” country. Until the oligarchs get a full hold of the government, and remove those pesky penalties for financial crime, it will remain such.

That’s a ghastly response to someone being executed

BuySome, about the declared war on cash:

The best way to fight back is to use cash for EVERY single face to face transaction for goods and services, except in corporate stores.

Tell the store owner or clerk that you want to give them 100% of the price of the item you are buying instead of the 94% or so they get back from the credit card company, often after a long wait, subject to withholding if card is stolen etc.

Worried about virus or germs on paper money?

“Microwave it.”

Unless you are writing off the costs against your business income or for reimbursement, tell small store owners “no receipt needed.”

“Use it or lose it”

Absolutely correct IMO !!

Only error is your use of future tense with re: courts.

What used to be called, erroneously, the justice system is now called the legal system wherein the rich folks use their money to buy whatever outcome they want, while the rest of WE the PEEDONs get what we deserve (according to the rich folks.)

See Bulow and Simpson cases, well publicized examples of rich folks getting away with murdering their spouses, while anyone of the poorer folks doing so will go to jail for eva, or just be murdered/executed by the state.

I can’t help it if I am a victim of “affluenza”!!! :)

To me, it’s a 3-tier system

Uber wealthy/powerful: You walk

Rich: Slap on the wrist

Poor and the rest: Good luck

If myself and 2 friends rob 3 convenience stores tonight, we get $1000 and it’s a ‘crime spree’ resulting in 20 years in prison.

If we steal $25M from a retirement fund, it’s a “scandal” and we walk.

Too bad you can’t drop the microphone and walk off after that.

@ nodecentrepublicansleft

That level of crime in SF would not meet local guidelines for criminal prosecution. Ask locals how that’s working.

Happy-

How abouts you give a well thought out “why this is true” explanation/defense, instead of a stupid “look over here” that’s just straight out of Hannity’s $300M net worth mouth, anyway?

Nothing would change without pain.

The govt and elite would support UBI so that common joe have enough to survive and wont cause any pain on them.

If the common joe wakes up en masses with weapons then there is no stopping.

Thus it is important to keep giving common people small crumbs.

I was running around with an “assault weapon” at age 14, the old man’s Garand. Was only 8 shot but could shoot through a whole line of cars and reloaded extremely fast. Likely won WW2 for us.

However, when us kids came out of the hills and into the store to get food and drink, we would be marked as crazy idiots if we carried them around the store, or even around town. We leaned them up near the front door where the clerk could keep an eye on them for us, or behind the counter, whichever he preferred, kept the ammo in our pockets, and went back into the hills to eat.

When you grow up with guns you don’t think of them as an extension of your male members, like all these camo idiots you see running around in public today.

They are a tool, to be treated with respect, like a chainsaw or an axe, or any other dangerous tool, and not for showing off whatever it is they think they are showing off…..kinda like all those wobbly old very first bike Harley riders.

You are correct, they will NEVER change their policies. The wokefulness chick Mary Daly at San Fran Fed had proudly & wokefuly declared she is saving so many good paying jobs by “not even thinking about” thinking of changing her preferred policy of eternal ZIRP and QE.

Depth…

Right you are.

Low rates are encouraging speculation in housing. Add in VRBO etc that facilitate the rentals in vacation areas. All looking for a fair return….because fixed income has been removed as an investment avenue.

Society will suffer by the breach being built by these speculations fed by record low mortgage rates which are pumping up prices for some and pushing prices away forothers.

Not unlike college tuitions creating massive borrowing via credit just too available to purchase a product at any cost.

Remember the “Jewel Box House”? That was a concept where an older mostly utilitarian home was upgraded with expensive amenities. The working class can no longer afford to live in a tricked out garage. We all have to face the reality of our circumstances, and that includes a lot of nouveau riche. The old market, flipping shacks to sell to former middle class workers ends and the a new market begins, (upgrading mid to high) while the newly moneyed try to hold on to their vanishing lifestyle, and like always its location.

Always remember…

The central bankers that push inflation upon us ALL HAVE INFLATION PROTECTED PENSIONS…

How’s that for an arrangement.

Maybe a journalist will ask Powell if he would surrender his inflation protection?

Depends on what inflation. Certainly not housing or asset inflation. These clueless clowns wouldn’t see inflation if it hit them in the forehead.

I discarded the possibility that they practice double speak when they come out publicly in unison saying inflation is “too low”. It should be embarrassing to anyone with an intellect.

Amen!

Houses are indeed speculative investments, which is why we see what is going on and has for some time. Houses as shelter is a cute notion right?

Just like Tesla. Part one is a car company that makes cars, Part two is a speculative financial vehicle for investment purposes. Both are doing exactly what they were created to do.

In the debt expansion phase using skinny down payments and dumping money into quartz countertops and new white cabinets all works out. At some point you have got to retire and you have to figure out if the costs of maintaining and continually updating high end real estate is worth it. If you are on the fence real estate is a sell when you can, not when you have to asset.

Note typical gvt manipulation of language, “appreciation” vs. “inflation”.

In CA, where homeownership is much lower than ntl rate of 64% (approx) (CA is much closer to just 50%) the appreciation vs. inflation fig leaf is even more absurd.

You could almost feel bad for the Fed turds if they weren’t such liars.

1) Basically the Fed only has a smallish number of tools and they have been failing for two decades.

2) At this point they live every day with the country-ruining fear that was manifested in Tim Geithner’s eyes during the worst of housing bust 1.0.

The look of a man about to be ripped apart by a crowd for genocide.

This same fear is really behind DC’s new concrete and concertina, two infantry division “Brown Zone”

3) They don’t know why they have failed but they are terrified of changing course (so they haven’t, for 20 yrs).

4) “will call forth supply” is the crux of the problem and has been for two decades.

The Fed has been terrifyingly uncomprehending about why their money-printing manipulation of interest rates downward, leading to artificially soaring *existing* home prices has not led to a tsunami of *new* home building (and therefore, **employment** and **greater** affordability).

In the Fed’s conception of the Universe, people cannot see through their artifice, entire industries can be doubled by push of a button, and explicit openness of objectives/admitting catastrophic error is inconceivable.

So they have been Ahab, lashed to a whale, going to the bottom, for two decades.

It’s obvious the Fed knows exactly what it’s doing and that exponentially growing home prices is the end game. I’d suggest national rent control to help renters but let’s be real. It would get one vote from Bernie in the senate.

The objective is a powerless bottom half who will serve as Amazon shippers for the rest of their lives. All of their savings are being channeled into rents.(of various kinds). About 100 million people in the US will never save enough capital to own a home.

I’m less optimistic about a revolt of the lower classes since the young seem to be satisfied to watch the lifestyles of the rich and famous on a 3×3 screen. They’ve been trained to think tweets are real dialogue and a tiny picture of Cancun is the same as going there. The internet reinforces the notion that if you are not rich in famous you’re a loser. You have no one to blame but yourself.

Who is going to hold that mortgage paper with a sub 3% return when inflation is 4%?

Oh that’s an easy one! The Fed of course! They’ll hold those MBS nice and snug right next to the giant pile of 0.0000001% government bonds

End the FED. Greenspan, Bernanke, Geithner, Paulson, Yellin, Powell and the politicians who support them deserve nothing but scorn, and destitution. They digitize money from nothing. That allows an of extension of credit, and an extraction of interest from debtors. This “concocted from nothing” credit drives prices and provides interest earnings to the benefit of favored entities that have produced nothing. It pushes house purchasers to pay higher prices and sign their lives away to debt slavery. It is evil.

If inflation is a tax, then they also circumvent Congress…for only Congress can pass a tax in this country…not a committee of unelected bureaucrats sitting behind closed doors in oak paneled room.

Economic dictates by committee….is what? Free market capitalism or Socialism?

Here! Here! Many have been saying it for years, to deal ears.

I just read an article on Electric vehicles. It is impossible to switch the world over to electric vehicles in 20 or 30 years. You wonder why Toyota is not all on board with this? Because it’s not possible. So it makes you wonder why the mandate. Is owning a home and an automobile going to become nearly possible for middle class. Maybe we should all consider central planning has a bad economic history.

Totally convinced of that mathematical truth.

“You wonder why Toyota is not all on board with this? Because it’s not possible. “

Because Toyota’s pushing hydrogen fueled vehicles? On the other hand Toyota has supposedly developed a kick ass solid state quick charging car battery.

Note that the federal government may forbid the production of gas engines in the future. You’ll buy electric or bike it, no choices.

On a personal note, I’d gladly drive an electric car today if the government would buy me one.

Who exactly does J Powell think he is fooling at this point..after 36 Trillion of fiat printed dollars and he still denies the fact that the Fed has created the most unsustainable and dangerous bubble in economic history.

It won’t be long before all possibilities of stoking the sacrificial fires are exhausted and then………

We are putting in on a house on 5 acres near the beach … they purchased it in 2009 my offer is at 2% interest over the past 10 years even though they are asking more. I can’t justify much more than that.

My wife won’t let me buy the 20 acres with a shack in the neighboring town…. b/c I’d live in a tent, I don’t understand.

At any rate, there are distressed properties that have been on the market since precovid. They are priced roughly correct and the owners are desperate to sell because they are certain the worm will turn- and will take a lower offer.

Since my wife and I are more and more on the same page it is actually kind of fun. We both are ready to rent if we don’t get a fair price adjusted for inflation.

In the end their is always the stock market after it implodes.

My goodness my grammar is terrible

It is better than Powell’s!

I remember when Greenspan would be mumbling in front of Congress, talking in circles, and CNBC would make him out to be the Oracle Of Delphi.

That’s how the Oracle of Delphi did speak. Maybe Oracle of Omaha is a better choice?

Ahhhh, forget it, it’s all in the translation agenda, anyway.

Shiloh1:

RE: Greenspan and his annual appearance before Congress:

Read his auto-bio “Age of Turbulence”…..he confesses to staying up late at nights before the hearings thinking up words and phrase that would completely confuse Congress. It’s hilarious!

Looks fine to me

COVID may also impact the price of real estate by spooking consumers away from alternatives like renting. Fear of exposure.

I’m in old folks apts, being one myself. In fact it’s hotel style, with common hallways. Plenty of high Covid risk people here. We all wear GOOD well fitted masks religiously anywhere outside of apts, and seldom go out except to get groceries, or mail. Once every 8-9 days for me. Nobody here could buy a house. One in a while over 10 years, I’ve see “Oxygen in use” on doors, but not since Covid. Occasional ambulance/fire and alarm is about same (usually something on stove too long). Dayroom is closed, although I still see folks in vegetable garden, one at a time.

“distressed properties that have been on the market since precovid. They are priced roughly correct ”

Probably not. You have to add in materials, labor and permits which can be ridiculous. In some cases repairs would cost more than building a new house and the longer a house has been on the market the more likely it has such problems. Each repair involves an inspection which can lead to the discovery of another needed repair.

Also, septic issues are difficult in coastal areas. Some will require mini treatment plants to replace them while others won’t be allowed any and therefore won’t allow occupancy. Although, with 5 acres that is probably not as much of a problem.

I know right?

Yet the system can’t stop, it’s gone astronomical.

Parabolic, blastanomic, …. see ya in the mornin…

-k

Yeah, I was thinking with how deep they’ve dug themselves in at this point, can they really unwind? It would be like setting off a nuclear bomb. The Fed is stuck and people’s beliefs in a fair and equitable system continually die with it. If the economy collapses at this point it will be a death of morale from all the people who haven’t gotten a spot at the trough. As if we aren’t already seeing this though…

When this is done…..there will be a textbook written……all about Yellen, Bernanke and Powell. With a first chapter about Greenspan.

The title of the book will be

The greatest crime in history…….or were they really that dumb. How 4 morons destroyed US culture, families, wealth, middle class, and international posture in less than 40 years.

Here is a list of the wealth of the fifty wealthiest congress members. There are seven above $100 million and none in this list is below $10 million. It’s from 2018 so it will be even worse now.

https://en.wikipedia.org/wiki/List_of_current_members_of_the_United_States_Congress_by_wealth

Nancy Pelosi just bought $1 million call options Tesla. Do you think they are going to do anything that risks the stockmarket going down? Hahaha! Who cares that hundreds of thousands live on the streets or in their cars.

Bernie didn’t make the list, at around only $2M, no wonder they call him crazy.

“If you are so smart, why ain’t you rich?”

Ad a little Calvinism and you have the All-American mindset.

This is like maybe a little too much murder talk. Please dial it back.

No, it’s not. He’s not calling for extrajudicial killings. He’s calling for a trial and punishment within the confines of the legal system

Run along, don’t read my posts. But don’t ever tell me what to write. You sound like a narc.

You know how many tens of thousands of people the FED is responsible for killing? Have you ever heard of “deaths of despair?” Look at the homelessness epidemic, the fentanyl epidemic, etc. These are symptoms of people who have almost given up.

The FED has created this. The issues are structural, and the politicians go right along with it, ne’er breathing a word about the FED. Despicable. The entire lot of them.

MarMar,

I understand what you are saying but,

1) there is some value to understanding the depth, intensity, and the accelerating anger that has been building against DC’s grotesque incompetence and corruption for two decades,

2) without that public airing, DC will continue to live in the splendid idiot isolation of their own endless lies until,

3) DC really *is* in flames. And it won’t be *talk* of murder.

Unless you spend a little time in the DC culture, it is hard to understand just what a “media-tized” bubble of unfounded self-regard and delusions of competence they live in.

When you can print money at will, power means never having to be accountable.

I was down in front of the Capitol on Jan 6th along with 200,000+ Trump supporters mostly from flyover country. These were normal patriotic Americans who were fed up with what is happening in the Swamp and the country. They have a right to be angry. They were not loonies like they are portrayed in the media. The scene there reminded me of the last clip in the Movie “The Battle of Algiers” where the masses rose up and said enough is enough.

The Fed, Congress and the corrupt MSM are responsible for what is happening in this country and its about time someone held them accountable.

Don’t dial anything back

Count me in as a supporter of what you don’t seem to like. Keep in mind our leaders routinely violently end the lives of millions. One example: new research shows it likely a million list their lives in Indonesia, when we changed their govt in the 60’s. Never underestimate just how bad our leaders really are.

The escapades at the Capitol led to the deaths of five people, one of them a cop, and none of them via the legal system.

MarMar,

You are trying to create a false impression of who died and how they died.

1 unarmed woman shot by still unidentified federal.

1 heart attack victim with protestors.

1 stroke victim with protestors.

1 apparent crush victim with protestors.

1 federal apparently killed by thrown heavy object (assailant still unidentified, is autopsy record available?)

So four of the five casualties (2 of whom by natural causes) were there voluntarily and voluntarily engaged on the side you appear to want to otherwise condemn…but you will appropriate their deaths to create a false impression.

Those four weren’t murdered, although one may have been the victim of an unlawful killing by a federal (we hear *zero* about that).

So the honest number is *one*

Don’t play MSM games here…people are too informed (ie, we bother to Google).

Good books have already been written about the cabal behind Fed and its campaign of running US economy into the ground in service to banks and Wall Street.

Danielle DiMartino Booth’s “Fed Up” is a good place to start. She was a Fed insider and is now a Fed analyst and critic.

They go to Jackson Hole and Davos and clink glasses together, congratulating each other, and talk about how they’re going to spin things and what their future moves will be. They are quite impressed with themselves. You’d have to be mentally ill to do such thing, and I think these people are. They’re rapaciously greedy sociopaths.

Please don’t forget all the CORPORATE types that also show up in those places. This dysfunctional economy/democracy is NOT all the fault of the Fed. They just represent/help the big financial corporations. All the other corps and dynastic wealth groups have lobbyists busy corrupting our government and it’s FISCAL (not monetary) policy/law to their benefit.

Likely a bigger problem for Main Street than the Fed, popular as Fed bashing is here.

Spread the blame around to all the guilty.

Have you considered fixing the broken system

vs.

burning it all down = anarchy

“Fixing the broken”

Decades of pushback has changed very, very little about DC.

Rise of cable TV/internet has increased diversity of viewpoints allowed to be given voice…but has made the remaining dominant MSM voices *worse*, much much *worse*.

If election law rules are thoroughly gamed (where not actually broken) then in point of fact we are not living in a democracy…but merely an utterly illegitimate “something” that wears a democracy skin suit.

The longer political paths remain unchanged, despite lengthening years/decades of poorer outcomes, the more such questions are going to be raised.

Burning down a disease ridden house of ill repute is not a net loss, if it refuses to reform.

nodecentrepublicansleft

I’m afraid, the system is so corrupt, it cannot be fixed. We can start by auditing the Fed. Then abolishing it. We did OK until 1913 without it.

The legal system works for the rich and the elite and work against the middle/cass and poor.

Don’t expect your votes would change anything.

Both parties are same, taking turns to serve the same masters.

The change won’t be done by the system/govt and it can only be done by the masses and that won’t be peaceful.

Wolf, for the first time ever, there seems to be universal anger brewing in your readers comment column.

Might this be the trend of the future?

Block,

I think it is a trend for many reasons. 5 years of endless tweets. Absolute rudeness on social media by people who used to know better. Frustration with pandemic and a zillion other things. And now habit.

Our own Canada, universally ridiculed for extreme politeness, is also degrading under the onslaught. In particular, right wing comments on CBC articles are instantly anti Trudeau statements when the articles might be about anything.

People are just short tempered and it is showing up everywhere.

Be careful believing anything in any comments section, the trolls and the bots are always present. All internet forums have someone who uses two accounts to have a fake argument with him/herself for attention.

The anger is being used to secure power, though. A lot of the most contentious issues are simply too politically useful to actually resolve, see immigration.

About the US joke that we Canucks thank cash machines: NOT TRUE!

I was recently very rude to a cash machine. I was double parked, needed some cash, ran in…only to see: ‘This machine is temporarily out of service’

Well I really let er fly. My sister might have been amused at the language, but not all women. Then from somewhere inside its guts, the machine spoke! A mature but demure female voice, sounding slightly upset, said: ‘It’ll just be a minute! ‘

Just a comment on this “right wing/conservative” stuff. These movements are lead/financed by fat and fatter cats who want to stay fat cats, and/or get fatter, e.g., NO CHANGES to anything not to their benefit.

They spend a lot of time BSing the less fortunate/educated into their way of thinking. Lincoln put it best, “The current filthy rich preying on the prejudices of the people”. (yeah, I adjusted his words some so I don’t have to write the whole quote…it’s still is his same observation)

Anyway, change does happen, and I get a real laugh out of the “Duck Dynasty” conservative propaganda bunch looking like us “dirty filthy hippies” of the 60’s, and able to say previously “nasty” words, like “toilet” instead of “bathroom bowl”. Normal bodily functions are much less “dirty” and unspoken than they were before us hippies showed up.

And where would we be if the “conservatives” in say, 800AD kept things EXACTLY their way?

“Get out of the way if you can’t lend a hand”

PS: My Canadian NDP active friend isn’t totally polite when she says, “I’ll go for Citizens United when Corporations can suffer Capital Punishment”.

My zip code seen a 25.7% increase in median house prices, according to the county statistics published last week. I have one neighbor that had their property taxes go from about $8,000 to $23,000 in approximately 10 years. Most of the local natives are being forced out due to all expenses going up exponentially across the board. It has created a real unease and sense of despair for many who had been doing great 5-7 years ago. Seems cruel to me yet it is great capitalism if you remove the humanity from the equation, like has been the direction for the last 30 years. At some point, if this is what we all want, we should let the A.I. algorithms make all our choices and decisions as that should speed up our attempt to remove the last shread of humanity from our existence…and then it can remove our existence too as capitalism sees fit???

Yet nothing to see here, move along…says the Fed…

In my areas there are still vacant houses from the bust 10+ years ago – zombie houses. All part of the plan to maintain shelter prices well above what the plebs can afford to pay.

Yeah, vacant houses are an interesting aspect of all this.

Comparative lack of housing supply response has been a big part of the Fed’s ZIRP failures for 20 years.

Mainly through insufficient new builds to lower prices/improve affordability/increase employment but the mystery of increased vacancies is interesting too.

Prices soar…and immediate, effortless supply is *still* held off the mkt?

My guess is that something akin to “yield management” is going on…total housing revenues are being maximized via a lower sales volume/higher sales price approach.

But that would require a level of coordination among sellers that is almost inconceivable.

But large banks may hold so many homes in their REO inventories at this point, that they are able to calibrate limited supply additions in order to maximize sales revenues.

That would explain why so many vacant homes are held off market while leverage driven prices soar (leverage supplied by same ZIRP fed banks…another perpetual motion gerbil wheel example).

Where are you? What areas?

There are zombie houses in California as well.

If you are middle class and retirement age. Pretty easy to find nice new 1500 sq ft home for $250,000 and $2000 taxes in NC, SC and TN. If you don’t need new you can do better and get taxes to around $1000 in a decent home that just dated. Probably cheaper in Kansas , Indiana and OK.

$250K for 1500sf is a giant ripoff in the south.

Built a home in rural flyover country in 1980. Taxes on 1600 sq ft home now over 3 grand a year. Mostly to support schools and local government so it can keep water, electric and sewer updated from fed regs. Most accept that as part of living in rural area with lower tax base.

Get your state to do what CA and FL have done re: property taxes, and ASAP y.

Otherwise, no one other than the rich folks will be able to hold any RE.

Friends in both states, older retired ( 92 and 86) are only able to stay in long term houses due to stability of taxes, and many cities/counties in FL also have added additional tax reductions for elderly, widow(er)s, spouses of veterans, etc…

It’s the humane thing to do, and all states should be doing it yesterday, and let the sales taxes on legal pot, other street drugs, tobacco, and alcohol make up the difference.

And, most importantly, vote out any politician voting for any other tax increases.

A friend in TN tells me his county has had no tax increases for the last 20 years, though he says the usual municipal services seem just as good as anywhere else he has lived.

Tactical strikes win battles and lose wars. The strategic play is to take away the public credit cards at all levels, especially local governments that continually prop up a dead and rotting development scheme. You must cut down the bankers who have total control over issuing new debt and renegotiating terms on old debt. And all the owned-suits must be banned from their presence in town halls where voting on contracts and policy is carried out. Since the public is too fickle to watch every move, we might need a new branch of direct representation with power to oversee and stop….kind of like those robot policemen in The Day the Earth Stood Still. Maybe we can call it the Treason Protection Team, charged with full power to protect the citizenry and Republic from those inside enemies. Give ’em the kill switch on that printer!

ALL lobbyists gotta go, everywhere in gov’t. Even with very considerable insider knowledge about them, I was still amazed when I found out they played on the Congressional Baseball Teams.

They used to make at least some effort to hide their presence.

Liz had a good televised rant about them when a derivative law was passed that was entirely written by Citibank.

– This is based on the faulty assumption that the FED is responsible for:

1) the FED doesn’t set the level of interest rates. The FED FOLLOWS the 3 month T-bill rate.

2) the FED doesn’t lend to home owners. commercial banks do.

3) the FED doesn’t lend to investors who take out margin debt. Commercial banks do.

1) Rates are set by Federal Open Market Committee (FOMC).

2) The Fed buys MBS from the banks. This pushes down the mortgage rate the banks charge for the obvious reason that the loans are flowing onto the Fed balance sheet.

3) By reducing the cost of money to zero the Fed pushes banks into highly leveraged bets, because leverage is the only way to make money when rates are this low.

Re 3) This is the bankers excuse frequently seen now. But banks still cash in the 2.7% on every loan they just made. The rising volume compensates the drop in interest rates partially so there is no reason for the banks to fear poverty. Without significant reserve requirements each loan is mainly financed with freshly created money from the commercial bank.

Joe

“By reducing the cost of money to zero the Fed pushes banks into highly leveraged bets”

Pushes EVERY BODY into bets. Desperation investing, yield chasing etc. Misallocation of resources. Risk return ratios skewed.

They’re just middlemen for the Fed. That’s like claiming the concept of fungibility doesn’t exist. It does.

Willy2,

“The FED FOLLOWS the 3 month T-bill rate.”

Such BS. You got cause and effect mixed up. The 3-month is trying to anticipate what the Fed will do. Changes in the Fed’s policy rates are always well telegraphed by the Fed, and there are essentially no surprise cuts or hikes anymore (there used to be decades ago). So it’s easy to anticipate and react in advance of the Fed’s decision. This makes it look like the Fed is following the market if you look at it superficially and don’t pay attention to anything else.

The Fed bought over a trillion dollars worth of MBS. If the Fed sold the MBS off, mortgage rates would rise at least two percent higher. That would bring house prices down. Rule of thump is that for every percent the mortgage rate is lowered, house prices rise ten percent. The opposite could prove true on the way down.

Yep. Fed’s wealth affect becomes reality poverty affect when tide goes out. They know it too and are printing under the DC mantra that now is not the time to worry about debt. Tells me the addict is admitting they are hooked and will stop taking drugs tomorrow. Sure. I will see your name in obituary before tomorrow comes.

Old School

“The Fed’s wealth affect becomes reality poverty affect..”

Well unless you are on the housing or stock trains, you are falling behind. That is sending one sector toward poverty while elevating another sector. Not good for society to have dictates aid one group at the expense of another.

Hayek says exactly this when speaking of “central planners”….intentionally helping one group(s) at the expense of another(others)…and for 12 years central planners decided to punish savers

That’s only going to hurt the lower tier, which is one reason mortgage rates are held artificially low. People with homes with equity are using low rates to cash out, and seniors trying to get through their golden years without going broke. A lot of the venom here today is really misplaced. If this was the 30s a lot of you would be in your jalopies heading for California, not hanging around the capitol building.

“If this was the 30s a lot of you would be in your jalopies heading for California”

But they are, more and more so. Every day people show up here in well lived in vans and sedans.

Willy2,

“FED doesn’t set the level of interest rates”

C’mon man, every single fact surrounding the “need for”/effect of multiple rounds of QE refute this.

Unless you are making some Clinton/MMT level distinction between “set” and “heavily, heavily influence”

Wolf, I’d like to hear your best arguments for the FED’s actions.. Just to keep things lively in the comment section.

It sounds just like the French fiat in late 1700’s. You find printing fiat stimulates the economy, but you get trapped into printing ever greater quantities or the economy collapses until people figure out that it’s worthless paper and try to buy real stuff with it as fast as they can. Value goes to zero in a Minsky moment.

Yep, and every case of fiscal collapse caused by excessive debt and printing ultimately leads to a reign of terror.

“History doesn’t repeat itself, but it often rhymes.”

I just realized that supreme court building, white house and capitol building have all been attacked starting with Gorsuch hearing. Politicians should really stop divisive politics before things blow.

Most Americans don’t know what money is, and so don’t see the Fed banking cartel as a threat. Almost everyone I speak with is convinced that they understand money — it’s what you work for, it’s what you save. A dollar is a thing, like a car or a pineapple, but easier to trade.

It’s that belief — that money is a thing that must have been earned or created through effort somewhere — that makes the Fed threat invisible to the working man. Invisibility is the banking cartel’s vampire power.

fiat currencies issued by decree forced upon debt ridden folks sums up “Most Americans”.

So sure most see a threat. A dollar is a piece of paper that does not work “for you… it is a issuance of debt and if you have one in your pocket, two or three have been created in its place by design.

Invisibility….. oh not really.

So why is there never any protest? There’s been riot across America, but protestors never show up at the Fed. I’d love to be wrong about this, but I don’t think 5% of Americans even know what the Federal Reserve is.

I’ll take a guess from the latest statistics.

1 percent of the total population of the world have 99 per cent of everything including Antarctic.

One tenth of that one percent control the world wide banking cartel.

One quarter of that one percent of one tenth are centuries old owners of the Federal Reserve Corporation.

But don’t tell anybody

this to jil and k:

Agree with the concepts of both your comments, though I suspect you are both too generous with your percentages.

Every time I mention the Federal Reserve Bank, to any but a couple of friends, I get eye rolls or immediate eye glazing over type reactions, and not one word of the response I hope for, such as the anger from several of the clearly knowledgeable commentariat on here.

As to the global banking cartel,,, certainly it’s intent to take over the banking system of USA was the fundamental cause of the War of 1812…

As well as subsequent financial moves surrounding the establishment and demise of a ” USA national bank”, ending with the creation, after what appears at this remove to have been another engineered ”crash”, to provide/prove the immediate basis/need for the FED.

They tried Occupy Wall Street. You see how far that got.

Most people never even realized the nature of how checks were transitioned from non-negotiable orders of withdrawl demanding release of monetary (fiat cash) deposits straight into acting as a form of money themselves. The bankers understood this blindness an got away with charging fees to cash a check…as though they were not debtors obligated to pay upon demand in a reasonable time! [Imagine if you got a utility bill and sent them back less because you decided to deduct your own type “transaction fee”…boom, boom, boom, out go the lights.] Now they are sure that most don’t understand money and are replacing the check with the electrons, and they control the power plants.

They did at one branch. BLM. Very few news articles mentioned it, they just mentioned the Fed was suddenly more concerned about racial justice.

The problem is also that nobody in the MSM calls them out on this. For example, a self-proclaimed “liberal” like Paul Krugman is completely on the “inflation is good” bandwagon. This is the same guy who in 2002 argued in favour of deliberately creating a housing bubble:

“To fight this recession the Fed needs … soaring household spending to offset moribund business investment. [So] Alan Greenspan needs to create a housing bubble to replace the Nasdaq bubble.”

We all know how that ended. Many people have never recovered from that catastrophe. But hey, the guy has a Nobel price so he must be right!

The same cabal is still in charge now and they are repeating the same mistakes. The public needs to be educated on this, but the MSM are not doing it. Wolf is doing a stellar job at this. I wish he had a column in the New York Times instead of Paul Krugman. Though I’m very happy to hear that traffic to this site is increasing!

Little action will be taken by “the people” until there is a “food bubble.”

Yes, because then money printing isn’t called what it is: stealing. The money isn’t portioned out according to who is producing market priced value. Money is treated like a commodity, rather than a symbol of a debt owed for a product of value. Flooding a system with unearned money is inherently redistributionary and we know who reaps the most benefit (aka getting away with stealing) from all of this.

Money digitizing is a root of modern day slavery.

It is often cited that useful money should be: 1) fungible, 2) durable, 3) portable, 4) recognizable, and 5) stable.

Since for US dollar quality number (5) is being rapidly destroyed (as a store value) we can all agree it is only a matter of time before use as fiat currency is over.

We can debate endlessly when and how the dollar will collapse, but it eventually it will. In our lifetimes. Thank you evil Fed.

Yep. Number 5 is entirely dependent upon “limited availability”. Does not matter if it’s gold/silver, cash, sea shells, or bologna. Without agreed upon limitations to what can circulate as the coin of the realm, there is no acceptable valuation for fair trade and confidence will crash at an accelerating rate…maybe not in a straight line, but definitely curving down ever faster. The tee shirt that says “I survived the crash” will cost $500 at the last moment.

At the last moment that tee shirt will be “priceless.” But I get your drift.

There was a protest in front of a fed reserve building a while back. BLM. First time I had ever heard of one at a fed office. It seemed to have an immediate effect of promises being made. Of course, such promises will be BS, but still. People who take such care to remain invisible may be becoming visible. I was surprised.

While this has different factors at play from Bubble 2007, there are some scary similarities. The desire to get a house anywhere at any cost is mind blowing.

I analyzed some data today of year over year sales for about 75 neighborhoods in DC, Maryland and Northern Virginia. Every exurb is up in number of units sold by 15-35%. People think work from home is here forever.

I think we will see a huge backlash on the work from home. Employers aren’t going to pay the same salaries if their employees live out of the metro area. People miss the social aspect of the office. This is going to hurt big time when it falls apart.

Should be interesting.

Beautifully put. I’m seeing far more inquiries about living in Europe (where I live) or backwoods New Englands (where I came from). People are trying to build a full life around the possibility of remote work. seeing that they can work anywhere.

No one is considering what happens if they lose their job.

Well, if you live in the back woods of New England, where I once did, if you lose your day job you can cut/sell firewood, tap maple trees for sap/syrup, hunt game, raise farm animals, grow a garden, etc.

The only problem is, not many people have these skills.

True that aa,,, life skills of centuries been lost by most folks, even though their family might have recently survived several generations ONLY because they had those skills.

But IMO, the biggest problem currently is the clear preference for SO many folks, of all ages too, so don’t go there, to make their living in front of the computer or even a phone, with no manual/physical labor whatsoever.

And then they go to the gym,,, LOL!

After watching 4 older ”Old Amish” folks lift a wood cook stove onto a wagon bed at their shoulder height a few decades ago, I really understood better their clear success at maintaining a long tradition of being able to survive,,, and they appeared to be doing a fairly good job of multiplying as well.

@AA -one can always braid buggy whips. There is always a market for quality, albeit small.

– “Some scary similarities”. Spot on.

– Do you have an idea of who is buying ? People nearing retirement ? Millennilas ? People who want to cash in the risien value of their homes ? ……….. ?

One thing I haven’t seen analyzed is millennials whose student loans are in forbearance using that purchasing power to upgrade housing.

Melissa, I agree, to a point. I don’t think employers will be able to get everyone, including the people whose skills are high in demand who don’t want to be in an office 5 days a week, to come back as such. That said, I think there are a lot of lower and middle level people who are easily replaceable who will be expected to come back.

I also think a hybrid system, where people come in to the office 1 or 2 days a week, is likely for many people. This means that people could commute, for example, from Harpers Ferry to D.C. That commute would drive any sane person crazy if doing it 5 days a week, but if you only had to do it once or twice, it would be manageable.

The same goes for places like Beacon in Dutchess County, NY.

But if people, especially those whose skills aren’t that rare, think they’re going to be able to live in the middle of nowhere and NEVER come into an office, I think they’re sorely mistaken.

I think it will be a question of price. “I’ll code for less money if I can live where I want and not have to commute except for serious meetings.”

Agree 1000%

It will be very interesting to see how the WFA job scene looks like in 5 years or so after pandemic is a just a bad memory.

With evolving AI, robotics, and increasing automation impacting white collar digital work I suspect many ‘work from anywhere’ folks will be thrown under the bus.

If you are just a digital ‘hologram’ on a screen you have less skin in game and your organizational value just plummets (unless you are a highly visible overachiever willing to appear a little more often in the flesh to make the case about how valuable you are to the team).

For mostly forgotten ‘what’s his name’ 3000 miles from the action– not so much.

WFH>>>>WFA>>>>>>>>>>WPA??…….?

Wolf,

The housing market has recovered. The buying of mortgage backed securities keeps the rates down for the stock market, unemployment, covid affected businesses, treasuries on and on. So it seems buying MBS’s is the Fed’s main tool.

As our dear friend Greg reminds us,

They are the “ buyers and lenders of the last resort”

-keppered

One-off price increases are not inflationary!

How many times do I have to tell you!

Homes for sale in my family oriented coastal Southeast Florida community are flying literally off the shelf. Our community has 654 homes located in a town featuring A rated neighborhood schools. The beach is 4 miles as the crow flies. We are surrounded by two public golf courses and we have a full (with a long waiting list) boat storage facility with high speed internet and community fees of only $150 per month cable and internet included. Houses here are selling in one day with a dozen showings and cash offers in the mid 700’s. Single story ranches that have been completely redone are going for $340 per square foot. My neighbor whose home sold in one day for cash needs, new windows, new roof and AC. The frenzy is like sharks in the water nipping at it’s prey.

As a post note this retired boomer with a nearly paid off mortgage remembered vividly their first home purchase in 1984 when interest rates were 12.5%. We took a difficult cash out refi (2 brokers, no one was interested in retirees) and am putting every penny in complete home renovations. Debt to Equity 30% using cheap fed money. PS:. You still need a home to live in so it might as well be nice.

Most people can’t do this. Median home price in Florida is $285,000.

I have lived in my community for 25 years. Our house was built to Dade County code but at 25 years old it was time for some upgrades. My front door is 13 feet above sea level. I am not in a flood or evacuation zone. New widows rated 150 mph. I have had more hurricanes come near or over us than I can count The last big one to pass over (the eye) was Wilma. But Dorian as a cat 5 steered 40 miles father east and took out the Abaco’s. We are a heaven for Northeast retirees from high tax states the buy anything and everything. Donald Jr just bought two adjacent homes 2.5 miles due east for $32M. We were a sleepy beach town twenty five years ago no we are a haven for the uber wealthy.

Let us know how things are going after the next hurricane hits your community.

After the next hurricane, the homeowners ins will be more than the mortgage payment. Just ask the Andrew survivors.

Is this in Jupiter? I feel like I’ve been to this community before.

I used to like Powell….back in 2018.

Now I think he either is a liar or doesnt know what he is doing.

What will the upside down look like with inflation over 3% to the holders of mortgage paper struck at 2.8%?

Central banker = money printer

Treasury Dept = Debt management Dept

Capitol building = Mafia Headquarters

Gold= Fiat Ponzi geiger counter

They say you can tell who is a liar by watching their body language. Those of you who are behavioral psychologists may have formed an opinion on Powell.

I am not a Powell watcher but many people are and know his body language.

The things to look for in a liar are (and be aware they can be incorrectly interpreted): inconsistencies from their normal body language or mannerisms; rapid eye blinking or conversely closing eyes for long periods; fake smiles; frequently touching face; using hand gestures after speaking vs during speaking; fidgeting; staring at person they are talking to; using a higher pitched voice or increasing volume, and more.

Of course I expect a true sociopath or psychopath can defeat an earnest trained body language expert, because they simply have no compunctions or conscious.

And it is even possible that Powell and his Group Think Board of Fed Governors are truly mad in sense of being willfully detached from reality.

Watch the eyes. If they look down to answer a question, they are lying. If a right handed person looks up and to the right to answer a question, they are creating the answer–lying. If they are looking down and to the left, they are trying to remember something that actually happened and are telling the truth. Any hand movement that covers the mouth, like rubbing their nose, is a tell. Clinton touched his nose a zillion times during questioning about Monica.

Suggest to all interested in these concepts of how to discern a liar read “Talking to Strangers” by Malcom Gladwell.

He pretty much destroys the myths, etc., regarding such discernment by most folks,,, but does support the possibility of ”tells” such as mentioned only by trained professionals.

Interesting read, and based on some very unfortunate examples of lack of telling when folks were, in fact, lying

All this only works for white middle class and above. Eye contact in particular is culturally based.

Culturally based for sure. In my sub culture, prolonged eye contact means you are really driving home a point, getting mad and ready to fight or have romantic intentions. Otherwise prolonged staring just isn’t polite. And you have to look away periodically in some direction, and I don’t think it matters where.

Besides, the real manipulative (sales, etc) types read these body language books as fast as they get written. I would image there are some techniques/tips used in Wolf’s car sales book.

“The things to look for in a liar are”

Interesting list (and I’ve seen similar ones elsewhere).

Does it boil down to the fact that lying requires brain processing power/causes emotional disturbance that triggers a lack of “natural” physical coordination (so liars get subtle twitches and tics as they try to over correct physically)?

I ask because it is hard to use the list in real time conversations (people are trying to control their *own* mental/physical coordination during conversation).

But if the list basically boils down to subtle physical “herky-jerkiness” then it is easier to detect (although naturally nervous people are going to yield a zillion false positives).

And the lesson for liars?

Be a *relaxed* liar.

Watch CNN.

And politicians.

Would have been very entertaining to have had Elizabeth Holmes in the mix for COVID the past year.

Detecting lying in government employees is much easier. Are their lips moving?

They need rampant inflation; where else are they going to be able to offload all the debt they have created? They are blank faced and waiting for massive inflation to erupt, and not until the debt is largely erased by the inflation, will they bother to do anything but smile back at their critics.

I guess those who are rooting for inflation are also ASSUMING the Fed will have no response to the inflation.

If you want 2.5% inflation, do you also expect interest rates NOT to rise to that level? If you do not expect such, then you are assuming a theft arrangement at the hand of the Fed plied against the holders of dollars….a tax.

If you do expect the Fed will respond, you will be seeing a crash in the bond market which will be dramatic and geometric.

If the Fed wanted to lower the burden of debt, it would need rampant consumer price inflation and wage inflation.

What it doesn’t need – and what is counterproductive for reducing the weight of the debt – is asset price inflation because that means only one thing: more debt because assets are used as collateral for debt and higher asset prices lead to even more debt. This included corporate debt and household debts, as well as government debts.

“is asset price inflation because that means only one thing: more debt because assets are used as collateral for debt and higher asset prices lead to even more debt.”

Wolf, you are of course, correct.

Basically, it is just a variant of the debt pyramiding that RE speculators use to build “empires” (until the valuation mkt turns and all that stacked leverage works against them).

One interesting observation.

Inflated asset mkts are ripe for wealth taxes.

The G likes to set up “Heads we win, tails you lose” gerbil wheel incentive and taxation structures.

A wealth tax on ZIRP inflated equity holdings would be yet another example (see property taxes for a long existent example…accruing to benefit of localities, courtesy of Fed).

Step 1 – Fed employs ZIRP, driving its own annual interest obligations (on greater than 100% Fed debt to GDP ratio) far below unrigged mkt rates.

Step 2 – ZIRP jacks asset values (including SFH and stock mkt) way up due to manipulation of DCF calculations.

Step 3 (?) – Fed wealth tax on selected “undeserving”/”windfall” asset classes skims cream created by G’s own policies.

The self licking ice cream cone, again.

Step 3 hasn’t been discussed yet…except in terms of how “unfair” stock mkt rise is (Billionaires Profiteering during Pandemic…no mention of ZIRP role).

Step 3 hasn’t been raised yet, but it is an example of how easily the G can game the nation’s economy to its own benefit.

The mob should have stormed the Eccles Building instead of the Capitol

just as Occupy Wall Street was just a couple of blocks away from the real problem (NY FED)

The FED and Wall Street are joined at the hip.

I’m happy at this point I was smart to buy my first home at 21 (20 years ago), and slowly added rentals. Now I have a few with small mortgages, which cashflow nicely. Looking at what I did then, would be much harder to do now. Then again the economy wasn’t the same. People who worked with there hands weren’t paid as well, work wasn’t as plentiful. If you have any sort of manual labor/craft skill, you can absolutely KILL it nowadays. Nobody wants to do any physical work. Driving through my neighborhood plow trucks were clearing driveways more than people were shoveling or snow blowing themselves. Wild time to live.

Amen to all that, Dave.

I worked with my hands and retired at 57 being mortgage free for years. My electrician son just bought his 2nd home at age 37. Both are rented to cover mortgage/insurance and he lives in a suite in the basement. (Nice suite).

Now at 65, I just put in an order for materials to do the final improvement on our main house, a large covered deck that overhangs the river. Two days ago finished a reno on a bedroom. My wife looked around the other day and said, “We couldn’t live this way if you didn’t do all this work”.

Becoming a carpenter was the wisest career choice I could have made. What do carpenters build? Houses. What do tradesmen have? Connections and discounts. It all adds up in the end.

Although, I have started to take vehicles to a mechanic a while ago. Can’t do it all as we age. :-)

“the wisest career choice”

Well, it varies depending on the vagaries of DC.

Not so hot being in home construction from 2007 thru ? (note how long Fed felt it had to keep ZIRP on).

And after the inflation/tax break induced real estate boom of the 70’s…contractors were mailing bricks to DC in early 80’s in rage at what rising rates did to their business.

Don’t know about you guys but my local city taxes and fees are galloping up and upward. The City Council folk seem to think we’re all getting rich with our home values rising. Wrote many months ago how important it was to put big chunk of all that stimulus funding towards local government. It really is needed yet mostly didn’t happen. Now we’re paying the price, and the worked Fed is pouring gasoline on the raging flames of the inflation it never sees.

Being taxed out of my house as I type.

The local authorities have my house assessed at aprox 15% over the real value……and at or near the highest tax rate in the nation.

Appeal denied.

Taxing rates increase. Fair return on money decreases. Both at the hand of the govt (and yes the Fed is a pawn of the govt)

Get out while you can. If you want to prove a point, sell your house for what you think it’s worth, it will sell fast and affect the local valuations.

Having said that, this looks like Florida 2006-2008. When the whole thing crashes your house value will adjust and so will your taxes.

House assessments go down so the taxing authority raises the tax rate to compensate. Actual property tax here went slightly down in one year out of the past 15. The other 14 continued ratcheting upwards.

I donot think the RE taxes go down ever.

Property taxes will increase. Towns and cities have no other source of income. They have borrowed the money to do ANYTHING for the past 50 years. Also, underfunded pensions are coming home to roost. All those teachers, cops,firemen, and municipal workers who worked 20 years and collect a pension at full pay for the next 40 years need your money to maintain their lifestyle.

Sounds like Chicago, Crook County and surrounding collar counties.

Did anybody else see that recent Chicago Teachers Union video, “Safe”?

Roddy,

Bravo. People are waking up.

The interesting point will be when the bill for all the public pension lies really comes due (public pension fund assets completely drawn down with huge shortfalls remaining).

That can happen much, much faster than anyone thinks.

On that day, the G will have to start jacking taxes on 60 year olds without savings to pay the $70k/yr lifetime pensions of 50 yr old gvt retirees.

Unless the G closes down the internet as “insurrectionist” that will be a recipe for mass unrest (it always was, as conservatives have warned for decades).

Best solution I can think of so far…let the public pension funds clean their own dirty houses…use “internal redistribution” from highest paid public pension fund retirees (who ran the sh*show for decades) to lowest paid public pension fund beneficiaries so that any fund shortfalls are eliminated.

Who can be against redistribution?

r2/3,

Municipalities in most states, all of the dozen or so I have lived in the last 60 years or so, have the ability and use it to add to the state Sales Tax.

Some also add to the state taxes on vehicles, including trailers, etc., and on fuel, phones and other needed utilities,,, some even add taxes onto the municipally supplied services such as water, sewer, storm water, garbage collection, etc., etc.

Point is almost all municipalities have many sources of income besides property tax,,, and, of course, they want it all and they want it now.

And will absolutely take your property of any kind if you don’t pay pay pay!!!

I wouldn’t give states and municipalities a dime of stimmy money.

Having worked for local government I know how badly mismanaged they can be in practice.

Their first line of defense against fiscal shortfalls has always been raising taxes and fees rather than shrinking size and inefficiencies of government.

Problem with that is, billionaries are getting lots of free money, yet local govt has bourne cost of Covid.

Timbers,

Don’t worry…essentially impossible that billionaires are going to make it out of this without taking a hit (see my posts on incentive/tax gerbil wheel G policies elsewhere).

The G is far, far too broke (and has been for a long time) to skip over *any* conceivable source of revenues…the billionaires will just be first (well, after money printing…but once consumer inflation really bites, the G will be forced back to taxation for a while)

The dying MSM still has enough juice to whip up a good 5 minutes hate against a numerically tiny group like billionaires (especially since the MSM sees its technologically induced end and has become reflexively unconstrained…sorta like a hung man voiding his bowels)

Homeowners who make improvements, pull permits, get reassessed. In CA anyway you stay on the foundation you were given and you avoid the tax bill. I am concerned that homeowners doing Rev Mos and the like are taking under the table assessments and when the assessors get around to it, they will back tax those folks. If you were on prop 13 for half a century and your tax base is about 1/10th of your market value and you pull a RevMo at market value (plus), they might say that constitutes a reassessment. I stay away from all manner of free money.

AB,

Excellent insight.

CA is always revenue starved after one off, cap gains windfall years (systemic basket case economics will do that).

If CA is aggressive about tracking down *ex* Californians for allegedly CA sourced income…a “creative” re-interpretation of re-assessment triggers is not hard to imagine.

These things aren’t driven by logic, they are driven by political “necessity”.

Timbers,

Taxes (charged by your local G) or inflation (induced by Fed G money printing to “pay” for transfers you suggest) are just two sides of the same coin.

The G likes to pretend there are free lunches or a magic Santa Claus…there aren’t.

Why is their so much anger and talk about hurting people in the comments?

I am disabled and live on $19k a year and most of the time I live i n a Minivan, if there is anyone who should be angry it is me. But I am not. Why?

Because I am not looking for power and I am not afraid of having nothing.

All the power these bankers and corporations have over you is because of your own fear and greed. Let go and be free of it all and magically these people in power will have nothing.

This is the same reason people do not strike anymore; fear and greed.

Polish aid…..

“Because I am not looking for power and I am not afraid of having nothing.”

Any opinion on liberty and freedom? Being left alone by govt?

Having free market interest rates?

Anyone who has this much anger will not ever be free because some one will always use your emotions to control your behavior. You all will yell at a rock because it is in your way instead of just walking around it!

Being left alone by govt? What is government but you and your neighbor? Take it up with them!

Having free market interest rates? Man’s mind is not free, so why should I expect the market to be free?

Good answers Mystic. I can’t figure out how so many people are talked into hating their own government, instead of the rich and the corporations who OBVIOUSLY manipulate it to their own benefit.

Guess you are right, they probably COULD just as easily be talked into blaming a rock for whatever bothers them. Tunnel vision? Just blind? Beats me.

At least you have $19k/ year and a minivan. That makes you relatively secure (and places you in the wealthiest 10% of the world population)

So what is stopping you or anyone else from living like I do?

historicus was complaining about being taxed out of his house. So what? Sell it and live in a van!

Imagine if all of the people with these houses and cars and boats and second houses lived like I did. Imagine the good they could do with all that extra money!

But you will not change, because you are just after the same power that you are complaining about, and the cycle goes no and on…

Not everybody has the luxury of $19k/year + van. That’s why.

Btw: I have no income at all (thanks to ZIRP) and live on about €16k ($19k) per year (average of the past 10 years). That includes my rent and ~5 months per year travelling all over the world (except in 2020 of course). So I also have a wonderful life living off $19k/year and don’t need more than this.

But that doesn’t stop me from being angry because by ZIRP + inflation I get robbed from my savings that I worked hard for, in order to bail out billionaires and subsidise people who go into debt to buy garbage that they don’t need, or to subsidise other peoples mortgages. If this BS goes on for too long I will run out of money before I die.

pm and ys:

Both living styles are not only allowed in USA, but, to some extent in many other places.

Grandpa vowed to live on his $100/month SS and not touch his capital,,, to prove it could be done.

His 45′ sailboat was entirely home made by / with only his own hands, in the years before he retired, and he did all the maintenance and repairs on it many years until, finally, he thought he and his wife were too old to be safe on it in total hurricane area.

Then they went to a small village in the Rocky Mtns of NM, where his wife was from, bought an adobe, added roof, floor, windows and doors, and lived in peace until they died.

In many third world countries with that ‘meager’ wealth you would be like a king.

Polish Mystic,

Okay, I’ll take the bait and assume you’re not earning your 19K as an intern in the basement of the Eccles building. I will assume you’re for real. Heck, for all I know you’re Klaus Schwab’s personal assistant. So I’ve a couple of questions:

Are you celibate? If so, is it voluntary celibacy?

Do you have any kids? If so, do your parents, a charity, or the State raise them?

Look at this! Stephen makes up stores about me to satisfy his own greed!

Why do you want more and more and more? Don’t yo know that is how that trap you?

Why make me the enemy? I am here to help you!

You’ve concluded my life is governed by greed based only on your own theories of how others should lead their life. Good to know. And you didn’t answer my questions.

I’m not fighting with you, but as one who has read a lot of early Church history and the development of the monasteries, I curious as to whether or not you’ve worked out how you can convince others to follow your example of Christ-like minivan living.

As has been said many times, “the trick is wanting what you need, not needing what you want.”

Maybe he’s a Buddhist? Not everyone in the US is a raving lunatic Calvinist. ya know?

If you are not afraid of having nothing, you have truly achieved Freedom.

Most of my friends with multimillion dollar assets ( big homes, very expensive cars ) are sh*t scared of little things. They are indeed rats although rich rats in the rat race. I guess most of the people are like this.

I would wager that people here on this econ blog are interested in liberty, political liberty that is, not to the exclusion of moksha or spiritual freedom but preceding it. And yes, they often discuss self-control and habits (spending habits, thinking habits, and such.) Once political liberty is lost and we’re all slaves to tyrants, then it’s awfully hard to concentrate on spiritual freedom. Because your form of worship and your thoughts will also be your tyrants choice. You’ll have to go to some significant trouble to mark out any kind of space in which to pursue your freedom. If others let money and status control their lives, so be it. But we don’t have to give up everything just to prove to religious that we’re okay.

Fear due to dependence; like a child protesting against his parents’ dominance and control. In a void the dollar fiat is worthless, but in civil society it has become the sole means of surviving. Unless that changes the same cycle will continue over and over. The people will protest, but they will come to heel sooner or later, just as a pup adheres to the food from his master’s hand and obeys. The FED hasn’t stolen anything that hasn’t been given up freely.

Nuts. I never agreed to ZIRP. I never voted for anyone who endorsed ZIRP. I was never even asked my opinion. But here am I with decades of negated savings.

Polish,

In general I agree about the freedom that thrift can buy but…

What is the source of your 19K? Work or gvt disability?

Even thrift can only go so far for those who have to work to survive in an economy that is collapsing due to decades of horribly inept/corrupt public policy.

It is much easier to be mellow when work stress is largely removed…but that is a rare outcome for 95%+ of people.

Thus the rising rage.

Lumber prices are 3x from this time last year, and not exactly flying off the racks either, here anyway. I have things to build but it can wait.

Besides, I suppose most people have the herd mentality, so pumps work. I watched silver selling crazy high Monday on Ebay, coins I had bought, also this time last year, were now selling double that. It’s no wonder we see most people just going with the flow of what’s happening in the Fed and Gov.