High costs, working from anywhere, and sudden dislike for towers trigger large-scale shifts in the housing market. Tulsa is paying people with full-time work-from-anywhere jobs to move there.

By Wolf Richter for WOLF STREET.

The turmoil in the apartment rental scene, with rents plunging in some of the most expensive markets and soaring in some less expensive markets, thereby wringing out a portion of the price differences, appears to be rotating a bit, with plunges abating in some of the cities where they’d plunged the most, such as in San Francisco, and steepening in others, such as Boston.

These markets are facing tenants who either leave the city – now that they can work from anywhere on what they believe to be a permanent basis – or who stay in the city but move out of high-rise towers to buy a house. The soaring vacancies and plunging asking rents and incentives – “three months free” – then spur the remaining tenants to look for better deals, and churn ensues. Tenants upgrade for the same price, or rent an equivalent unit for a lot less, attested to by a surging number of lease signings in markets where rents have sharply dropped.

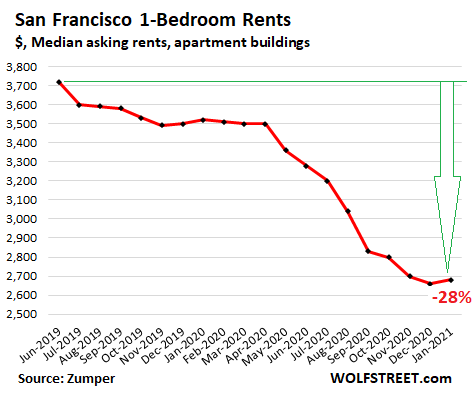

In San Francisco, still the most ludicrously expensive rental market in the US, the stunning downward spiral in rents has paused. The median two-bedroom asking rent, at $3,500 in January, was unchanged from December, after having plunged 23% from a year ago, and 30% from the peak in October 2015. The median one-bedroom rent ticked up for the first time since June 2019, by 0.8% to $2,680, but is down 24% from a year ago and 28% from June 2019:

There are now reports of vacancy rates of 30% in luxury apartment towers in San Francisco, with landlords advertising “three months free.”

During San Francisco’s dotcom bust, rents plunged by about as much, but it took twice as long – three years – from Q1 2001 through Q1 2004, and it took over a decade and another boom for rents to surpass their dotcom peak.

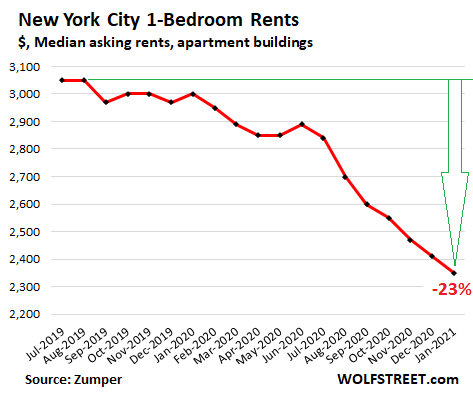

In New York City, the median asking rent for 1-BR apartments dropped 2.5% in January from December, to $2,350, and by 22% year-over-year, and by 23% from July 2019, according to data in Zumper’s Rent Report. For 2-BR apartments, rents rose 1.5% from December to $2,670, down 21% from a year ago.

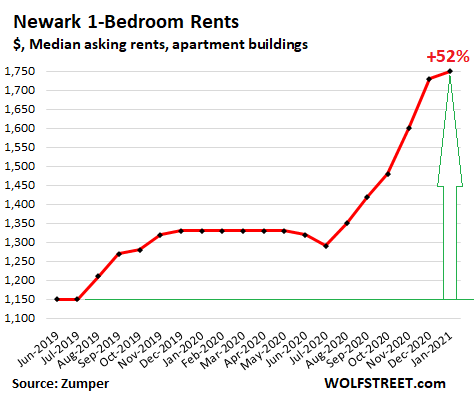

But in Newark, where some of the New York City rent refugees ended up, rents have skyrocketed by 52% since July 2019. Much of the surge took place over the past seven months.

In January, the median asking rent for one-bedroom apartments rose by another 1.2% from December, after having jumped by 8.1% in the prior month, and is up by 32% from a year ago, and by 52% from June 2019. This rent explosion has pushed Newark into 9th place of the most expensive major rental markets in the US, up from 40th place in June 2019:

These rents here are median asking rents for units in apartment buildings, including apartment towers and new construction, but not single-family houses for rent, and not condos for rent. Zumper collects this data from the Multiple Listings Service (MLS) and other listings, including its own listings, in the 100 largest markets of the US.

“Asking rent” is the advertised rent of a rental apartment, but does not include concessions, such as two months free. “Median” asking rent is the middle asking rent, with half of the asking rents higher and half lower.

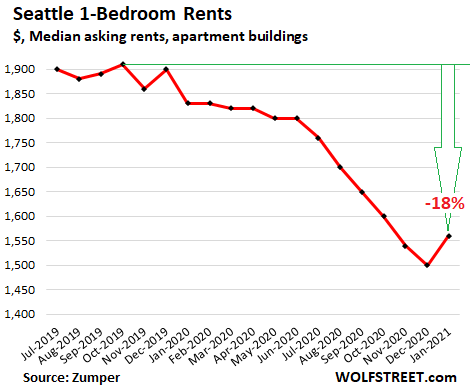

In Seattle, after spiraling down for months, the median asking rent for 1-BR apartments bounced 4.0% from the prior month, to $1,560, but was down by 15% year-over-year, by 18% since October 2019, and by 22% since the peak in May 2018: But 2-BR rents continued to decline, ticking down 0.5% from the prior month, down 12% year-over-year and down 25% from the peak in April 2016.

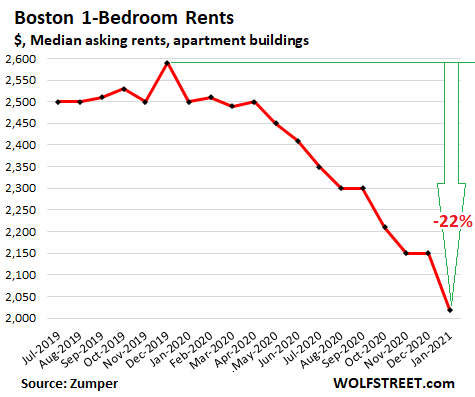

In Boston, the median 1-BR rent plunged 6.0% in January from December, to $2,020, down 19% from a year ago, and down 22% from the peak in December 2019. The 2-BR rent plunged 4.2% from December, to $2,500, down 14% year-over-year, and down15% from December 2019.

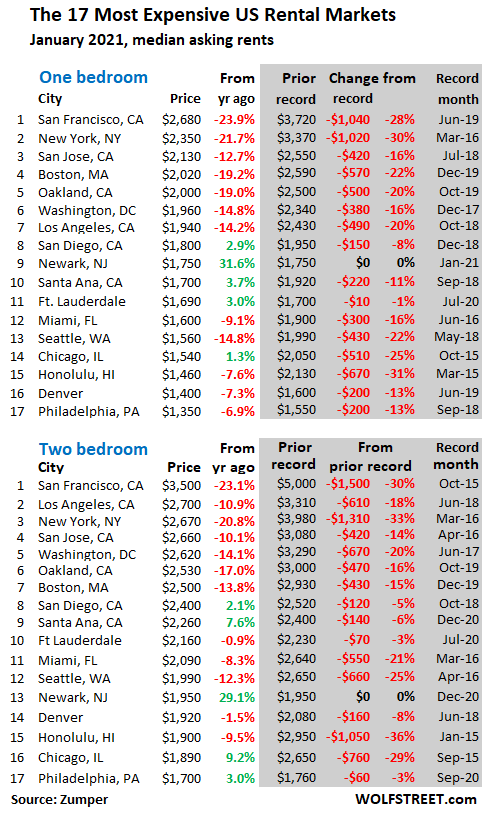

The 17 most expensive rental markets.

The shaded area in the table below shows peak rent and the changes from peak rent. The black entries in the shaded area indicate rent records set in December. 14 of these markets have experienced double-digit declines in 1-BR rents from their respective peaks in prior years, topping out with Honolulu (-31%), New York (-30%), and San Francisco (-28%). Newark, with its year-over-year jump in 1-BR rents of 32%, was catapulted into the list in December:

The 27 cities with median 1-BR rents of $900 or less.

In seven of these low-cost rental markets, the median 1-BR asking rent is below $700, with Akron, OH, being the cheapest, at $600 (-6.3% year-over-year), followed by Wichita, KS (-10.3% year-over-year), and Tulsa, OK (+4.9% year-over-year).

They pay you $10,000 cash if you move to Tulsa. The city has been through a horrible time since the oil bust of the 1980s, when oil companies moved their headquarters to Houston, leading to a permanent outflux of well-paid jobs. I was living there at the time. Now the city is trying to leverage work-from-anywhere to bring in people with full-time work-from-anywhere jobs outside Oklahoma, and people who are “self-employed outside of Oklahoma.” To do this, it is offering $10,000 cash plus other perks. And cheap housing.

In Detroit, at the bottom of this list, the median 1-BR rent shot up by 26.8% from a year ago to $900. The city’s downtown has been on a revitalization track for a decade. And there are some other double-digit gainers on this list:

| The 28 Cities with 1-BR rents $900 or less, $ & Y/Y% | |||

| 1 | Akron, OH | $600 | -6.3% |

| 2 | Wichita, KS | $610 | -10.3% |

| 3 | Tulsa, OK | $640 | 4.9% |

| 4 | Laredo, TX | $650 | -8.5% |

| 5 | Lubbock, TX | $650 | 4.8% |

| 6 | Shreveport, LA | $660 | 6.5% |

| 7 | El Paso, TX | $710 | 7.6% |

| 8 | Tucson, AZ | $730 | 7.4% |

| 9 | Albuquerque, NM | $740 | 5.7% |

| 10 | Lexington, KY | $760 | 2.7% |

| 11 | Oklahoma City, OK | $770 | 1.3% |

| 12 | Lincoln, NE | $790 | -2.5% |

| 13 | Baton Rouge, LA | $800 | 6.7% |

| 13 | Omaha, NE | $800 | -1.2% |

| 15 | Tallahassee, FL | $800 | -3.6% |

| 16 | Winston Salem, NC | $800 | 0.0% |

| 17 | Augusta, GA | $820 | 9.3% |

| 18 | Greensboro, NC | $830 | 13.7% |

| 19 | Memphis, TN | $830 | 10.7% |

| 19 | Knoxville, TN | $840 | 3.7% |

| 21 | Syracuse, NY | $840 | 5.0% |

| 22 | Bakersfield, CA | $850 | 6.3% |

| 22 | Corpus Christi, TX | $850 | 2.4% |

| 22 | Columbus, OH | $860 | 6.2% |

| 25 | Louisville, KY | $870 | 3.6% |

| 26 | Spokane, WA | $880 | 14.3% |

| 27 | Des Moines, IA | $890 | 1.1% |

| 28 | Detroit, MI | $900 | 26.8% |

The 28 Cities where 1-BR rents dropped.

Of the 100 largest rental markets, the median asking rent for 1-BR apartments rose in 67 cities year-over-year, remained flat in 5 cities, and fell in 28 cities. Among those cities where rents fell, 21 booked year-over-year rent declines over 5% and 9 booked rent declines over 10%, topped off by 8 of the usual high-dollar suspects, and by Wichita, KS, the second cheapest rental market in the US:

| The 28 Cities where 1-BR rents dropped YoY | |||

| 1 | San Francisco, CA | $2,680 | -23.9% |

| 2 | New York, NY | $2,350 | -21.7% |

| 3 | Boston, MA | $2,020 | -19.2% |

| 4 | Oakland, CA | $2,000 | -19.0% |

| 5 | Seattle, WA | $1,560 | -14.8% |

| 6 | Washington, DC | $1,960 | -14.8% |

| 7 | Los Angeles, CA | $1,940 | -14.2% |

| 8 | San Jose, CA | $2,130 | -12.7% |

| 9 | Wichita, KS | $610 | -10.3% |

| 10 | Miami, FL | $1,600 | -9.1% |

| 11 | Laredo, TX | $650 | -8.5% |

| 12 | Nashville, TN | $1,300 | -7.8% |

| 13 | Honolulu, HI | $1,460 | -7.6% |

| 14 | Denver, CO | $1,400 | -7.3% |

| 15 | Buffalo, NY | $1,050 | -7.1% |

| 16 | Minneapolis, MN | $1,300 | -7.1% |

| 17 | Philadelphia, PA | $1,350 | -6.9% |

| 18 | Akron, OH | $600 | -6.3% |

| 19 | Pittsburgh, PA | $1,080 | -6.1% |

| 20 | Madison, WI | $1,070 | -5.3% |

| 21 | Salt Lake City, UT | $1,070 | -5.3% |

| 22 | Tallahassee, FL | $800 | -3.6% |

| 23 | Chesapeake, VA | $1,090 | -3.5% |

| 24 | Plano, TX | $1,190 | -3.3% |

| 25 | Austin, TX | $1,200 | -3.2% |

| 26 | Lincoln, NE | $790 | -2.5% |

| 27 | Omaha, NE | $800 | -1.2% |

| 28 | Orlando, FL | $1,240 | -0.8% |

The 31 Cities where rents jumped between 7% and 32% YoY.

In 31 of the 100 largest rental markets, the median 1-BR asking rent soared between 7% and 32% year-over-year in January. In 21 of them, rents jumped 10% or more, with Newark on top (+31.6%). These are huge rent increases, and they run in parallel with the huge rent declines in other cities, clearly indicating that large-scale shifts in the housing market are underway:

| The 31 Cities where 1-BR rents jumped 7%-32%, YoY | |||

| 1 | Newark, NJ | $1,750 | 31.6% |

| 2 | Detroit, MI | $900 | 26.8% |

| 3 | Cleveland, OH | $1,150 | 22.3% |

| 4 | St Petersburg, FL | $1,210 | 18.6% |

| 5 | Durham, NC | $1,170 | 18.2% |

| 6 | Richmond, VA | $1,270 | 15.5% |

| 7 | St Louis, MO | $990 | 15.1% |

| 8 | Boise, ID | $1,150 | 15.0% |

| 9 | Henderson, NV | $1,300 | 15.0% |

| 10 | Providence, RI | $1,460 | 15.0% |

| 11 | Indianapolis, IN | $940 | 14.6% |

| 12 | Spokane, WA | $880 | 14.3% |

| 13 | Greensboro, NC | $830 | 13.7% |

| 14 | Virginia Beach, VA | $1,130 | 13.0% |

| 15 | Chattanooga, TN | $1,000 | 11.1% |

| 16 | Mesa, AZ | $1,020 | 10.9% |

| 17 | Memphis, TN | $830 | 10.7% |

| 18 | San Antonio, TX | $950 | 10.5% |

| 19 | Fort Worth, TX | $1,080 | 10.2% |

| 20 | Colorado Springs, CO | $1,090 | 10.1% |

| 21 | Fresno, CA | $1,100 | 10.0% |

| 22 | Kansas City, MO | $1,000 | 9.9% |

| 23 | Augusta, GA | $820 | 9.3% |

| 24 | Arlington, TX | $950 | 9.2% |

| 25 | Jacksonville, FL | $970 | 9.0% |

| 26 | Chandler, AZ | $1,330 | 9.0% |

| 27 | Tampa, FL | $1,200 | 8.1% |

| 28 | Sacramento, CA | $1,400 | 7.7% |

| 29 | El Paso, TX | $710 | 7.6% |

| 30 | Tucson, AZ | $730 | 7.4% |

| 31 | Milwaukee, WI | $1,200 | 7.1% |

The Largest 100 rental markets.

The table below lists the largest 100 rental markets, with 1-BR and 2-BR median asking rents in January, and year-over-year percent changes, in order of 1-BR rents. You can search the list via the search function in your browser. If your smartphone clips the 6-column table on the right, hold your device in landscape position:

| Rents, Top 100 Cities | 1-BR $ | Y/Y % | 2-BR $ | Y/Y % | |

| 1 | San Francisco, CA | $2,680 | -23.9% | $3,500 | -23.1% |

| 2 | New York, NY | $2,350 | -21.7% | $2,670 | -20.8% |

| 3 | San Jose, CA | $2,130 | -12.7% | $2,660 | -10.1% |

| 4 | Boston, MA | $2,020 | -19.2% | $2,500 | -13.8% |

| 5 | Oakland, CA | $2,000 | -19.0% | $2,530 | -17.0% |

| 6 | Washington, DC | $1,960 | -14.8% | $2,620 | -14.1% |

| 7 | Los Angeles, CA | $1,940 | -14.2% | $2,700 | -10.9% |

| 8 | San Diego, CA | $1,800 | 2.9% | $2,400 | 2.1% |

| 9 | Newark, NJ | $1,750 | 31.6% | $1,950 | 29.1% |

| 10 | Santa Ana, CA | $1,700 | 3.7% | $2,260 | 7.6% |

| 11 | Fort Lauderdale, FL | $1,690 | 3.0% | $2,160 | -0.9% |

| 12 | Anaheim, CA | $1,660 | 3.8% | $2,020 | 1.0% |

| 13 | Long Beach, CA | $1,600 | 0.0% | $2,020 | 1.0% |

| 14 | Miami, FL | $1,600 | -9.1% | $2,090 | -8.3% |

| 15 | Seattle, WA | $1,560 | -14.8% | $1,990 | -12.3% |

| 16 | Chicago, IL | $1,540 | 1.3% | $1,890 | 9.2% |

| 17 | Scottsdale, AZ | $1,500 | 2.7% | $1,970 | -10.0% |

| 18 | Atlanta, GA | $1,480 | 3.5% | $1,860 | 2.2% |

| 19 | Honolulu, HI | $1,460 | -7.6% | $1,900 | -9.5% |

| 20 | Providence, RI | $1,460 | 15.0% | $1,800 | 13.2% |

| 21 | New Orleans, LA | $1,420 | 1.4% | $1,700 | 7.6% |

| 22 | Denver, CO | $1,400 | -7.3% | $1,920 | -1.5% |

| 23 | Portland, OR | $1,400 | 0.0% | $1,720 | 3.6% |

| 24 | Sacramento, CA | $1,400 | 7.7% | $1,730 | 15.3% |

| 25 | Philadelphia, PA | $1,350 | -6.9% | $1,700 | 3.0% |

| 26 | Gilbert, AZ | $1,340 | 6.3% | $1,610 | 11.0% |

| 27 | Chandler, AZ | $1,330 | 9.0% | $1,560 | 11.4% |

| 28 | Henderson, NV | $1,300 | 15.0% | $1,410 | 4.4% |

| 29 | Minneapolis, MN | $1,300 | -7.1% | $1,790 | 2.3% |

| 30 | Nashville, TN | $1,300 | -7.8% | $1,450 | 0.0% |

| 31 | Richmond, VA | $1,270 | 15.5% | $1,480 | 12.1% |

| 32 | Orlando, FL | $1,240 | -0.8% | $1,390 | 0.0% |

| 33 | Charlotte, NC | $1,220 | 5.2% | $1,450 | 13.3% |

| 34 | Dallas, TX | $1,220 | 5.2% | $1,640 | 3.8% |

| 35 | St Petersburg, FL | $1,210 | 18.6% | $1,660 | 15.3% |

| 36 | Austin, TX | $1,200 | -3.2% | $1,540 | 1.3% |

| 37 | Milwaukee, WI | $1,200 | 7.1% | $1,250 | 6.8% |

| 38 | Tampa, FL | $1,200 | 8.1% | $1,370 | 2.2% |

| 39 | Plano, TX | $1,190 | -3.3% | $1,550 | -3.1% |

| 40 | Baltimore, MD | $1,180 | 2.6% | $1,340 | -4.3% |

| 41 | Durham, NC | $1,170 | 18.2% | $1,260 | 11.5% |

| 42 | Boise, ID | $1,150 | 15.0% | $1,280 | 10.3% |

| 43 | Cleveland, OH | $1,150 | 22.3% | $1,200 | 20.0% |

| 44 | Virginia Beach, VA | $1,130 | 13.0% | $1,300 | 9.2% |

| 45 | Aurora, CO | $1,110 | 2.8% | $1,430 | 1.4% |

| 46 | Fresno, CA | $1,100 | 10.0% | $1,340 | 11.7% |

| 47 | Houston, TX | $1,100 | 2.8% | $1,360 | 3.8% |

| 48 | Irving, TX | $1,100 | 0.0% | $1,440 | 0.7% |

| 49 | Chesapeake, VA | $1,090 | -3.5% | $1,200 | 0.0% |

| 50 | Colorado Springs, CO | $1,090 | 10.1% | $1,300 | 6.6% |

| 51 | Fort Worth, TX | $1,080 | 10.2% | $1,400 | 11.1% |

| 52 | Pittsburgh, PA | $1,080 | -6.1% | $1,300 | -0.8% |

| 53 | Madison, WI | $1,070 | -5.3% | $1,390 | 6.1% |

| 54 | Reno, NV | $1,070 | 3.9% | $1,430 | 10.0% |

| 55 | Salt Lake City, UT | $1,070 | -5.3% | $1,330 | -1.5% |

| 56 | Buffalo, NY | $1,050 | -7.1% | $1,160 | -14.7% |

| 57 | Raleigh, NC | $1,050 | 5.0% | $1,250 | 5.0% |

| 58 | Mesa, AZ | $1,020 | 10.9% | $1,300 | 13.0% |

| 59 | Phoenix, AZ | $1,010 | 4.1% | $1,270 | 3.3% |

| 60 | Rochester, NY | $1,010 | 4.1% | $1,200 | 8.1% |

| 61 | Chattanooga, TN | $1,000 | 11.1% | $1,140 | 14.0% |

| 62 | Kansas City, MO | $1,000 | 9.9% | $1,160 | 14.9% |

| 63 | Las Vegas, NV | $1,000 | 6.4% | $1,200 | 4.3% |

| 64 | St Louis, MO | $990 | 15.1% | $1,250 | 4.2% |

| 65 | Norfolk, VA | $980 | 6.5% | $1,100 | 10.0% |

| 66 | Jacksonville, FL | $970 | 9.0% | $1,140 | 14.0% |

| 67 | Arlington, TX | $950 | 9.2% | $1,200 | 9.1% |

| 68 | San Antonio, TX | $950 | 10.5% | $1,160 | 6.4% |

| 69 | Indianapolis, IN | $940 | 14.6% | $1,000 | 12.4% |

| 70 | Cincinnati, OH | $930 | 3.3% | $1,140 | 2.7% |

| 71 | Anchorage, AK | $910 | 0.0% | $1,150 | 4.5% |

| 72 | Glendale, AZ | $910 | 2.2% | $1,180 | 11.3% |

| 73 | Detroit, MI | $900 | 26.8% | $1,080 | 28.6% |

| 74 | Des Moines, IA | $890 | 1.1% | $940 | 2.2% |

| 75 | Spokane, WA | $880 | 14.3% | $1,130 | 11.9% |

| 76 | Louisville, KY | $870 | 3.6% | $950 | 5.6% |

| 77 | Columbus, OH | $860 | 6.2% | $1,090 | 3.8% |

| 78 | Bakersfield, CA | $850 | 6.3% | $1,100 | 12.2% |

| 79 | Corpus Christi, TX | $850 | 2.4% | $1,110 | 6.7% |

| 80 | Knoxville, TN | $840 | 3.7% | $1,000 | 5.3% |

| 81 | Syracuse, NY | $840 | 5.0% | $970 | 2.1% |

| 82 | Greensboro, NC | $830 | 13.7% | $920 | 10.8% |

| 83 | Memphis, TN | $830 | 10.7% | $880 | 11.4% |

| 84 | Augusta, GA | $820 | 9.3% | $920 | 10.8% |

| 85 | Baton Rouge, LA | $800 | 6.7% | $950 | 8.0% |

| 86 | Omaha, NE | $800 | -1.2% | $1,030 | 3.0% |

| 87 | Tallahassee, FL | $800 | -3.6% | $930 | 3.3% |

| 88 | Winston Salem, NC | $800 | 0.0% | $870 | 7.4% |

| 89 | Lincoln, NE | $790 | -2.5% | $910 | -2.2% |

| 90 | Oklahoma City, OK | $770 | 1.3% | $900 | 0.0% |

| 91 | Lexington, KY | $760 | 2.7% | $950 | 2.2% |

| 92 | Albuquerque, NM | $740 | 5.7% | $950 | 11.8% |

| 93 | Tucson, AZ | $730 | 7.4% | $980 | 11.4% |

| 94 | El Paso, TX | $710 | 7.6% | $870 | 10.1% |

| 95 | Shreveport, LA | $660 | 6.5% | $750 | 5.6% |

| 96 | Laredo, TX | $650 | -8.5% | $980 | 5.4% |

| 97 | Lubbock, TX | $650 | 4.8% | $850 | 6.3% |

| 98 | Tulsa, OK | $640 | 4.9% | $830 | 2.5% |

| 99 | Wichita, KS | $610 | -10.3% | $750 | 2.7% |

| 100 | Akron, OH | $600 | -6.3% | $740 | 4.2% |

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Unfortunately housing prices keep climbing in Seattle, distressing one of my kids to no end.

Have hope! Unless I miss my guess, and vaccinating every person on earth takes forever, nothing lasts forever. Too many companies are hugely over leveraged.

It is only a matter of time, with this pandemic pressuring them economically, until more fail. Then, when the economy recovers, since I think that many will find that working remotely is not truly practical for them, a huge number or most, probably, of those who moved far away from cities will want to move back.

Fun and profits for real estate agents, even though the real estate just purchased will plunge in value. Panicked cattle reactions in the real estate market, if it is discovered that the banks and the “Fed” hold so much real estate that they cannot foreclose upon even a fraction of it, may exacerbate the plunges.

Maybe the upcoming hyperinflation will decrease such plunges, at least concealing real value price plunges. Maybe, Uncle “Fed” wants to print dollars to conceal, and prevent realization of its losses from its bail out of the banksters by purchasing their $2 TRILLION in MBS in 2019 and 2020, and its bankster cronies’ losses.

K,

You speak the truth. For some unapparent reason Wolf has a hard on for landlords and can’t see past his nose.

Vaccines will bring the swift end to isolation and a rocketship to urban life, provided politics don’t get in the way.

We have reached a solid bottom in NY, SF and LA. Boston will rebound as well when university becomes 100% in person again by Fall.

That’s not distress, that’s FOMO, which is a relatively harmless form of envy. Distress is when you buy a house, then the price falls 40%.

Been there, done that, got the bloody T-shirt. It was the beginning of my financial trifecta disaster. Foreclosure, bankruptcy, and divorce. Fun is.

Everybody’s loading up on the big mortgage, big car payments, etc. AGAIN. Nothing was learned from last time. A neighbor just upgraded their ski boat. The $45,000 one just wasn’t doing it, they had to buy one for $100,000. I’m sure they paid cash….NOT.

Methinks we’ll be seeing lots of people losing everything again. Of course, with the shenanigans these central bankers and politicians are pulling, perhaps every debt junkie alive will get bailed out, maybe even keep all the stuff for free.

depth charge wrote

Everybody’s loading up on the big mortgage, big car payments, etc. AGAIN

just bought nice 5 year old truck $50k

my son said I should enjoy the loan payments

to which I replied – SON – you know we live within our means

and do not spend $$ we don’t have

loan amount $0

I drove 20 year old vehicles for 30 years(also used the 1 payment plan when I bought them)

pay attention woke folk

“relatively harmless form of envy”

Have to think on that one for a while.

I have empty units in the city I have never had in decades

and I’m 100% full with constant calls for people looking for inexpensive units

rents are going up and up and up on low end

but thanks for reminder – I need to give out some more notices about that very item

As do I gorby. My higher end rental units (older buildings) in a big city have been hardest hit while my lower end is holding strong.

Apartment REITs are setting up as a great buy on the next dip down in the overall market…EQR and AVB.

It can’t just be the fear of towers and elevators during this pandemic year. The other climbing locations are still offering high rises. I don’t want to insult any readers who live in high rise apartments, but I have always wondered just how people do it? Last night on our news they showed a 42 year old jerk being led away in handcuffs for running an illegal show lounge in his 3 story luxury penthouse apartment. He was fined and arrested, and an additional 77 ‘guests’ were also fined. This was in Vancouver BC. The culprit owned the suite. How would you like to be that guys neighbour? A building that size must have thousands of residents.

If it has shared plumbing or walls, never buy it.

Vancouver is the cesspool of crime, corruption, drugs and money laundering unrivaled in North America. The only way to make a living in Vancouver is to be involved in real estate or marijuana growing, on top of that you have to deal with 9 months of crappy weather and the remaining three months is smog and smoke from burning forests nearby. Absolutely unlivable.

Sounds just like Seattle. Howdy neighbor.

Seattle has some of the biggest corporations, Boeing, Amazon, Starbucks, Costco, Microsoft etc etc, what opportunities there are for working stiff in Vancouver, 1-800 got junk and lulemon?

While I’m certainly not insulted by your opinion about high rises, I do have a different perspective. I am fortunate enough to have lived in many dwellings – from the trailer park where I was born, to the McMansion that I once owned, to a ridiculous condo over the Pacific in SoCal, and my current high rise penthouse. While the high rise isn’t perfect, it is wonderful and quite private. With thick concrete walls and floor/ceiling, it’s silent inside. The staff are lovely and the neighbors are diverse. I can see 20 miles into the distance. It’s a fun place to live.

Rents are falling. Prices are rising. Building costs are rising. Taxes are rising. Maintaining is getting expensive.

Is everyone pushing the price higher blind?

Rents are falling in some cities and are rising in other cities. They rose in 63 of the top 100 housing markets and fell in 28 markets.

Wolf, it’s sad that housing price in Sacramento is going up. There is no way I can afford a 500K house with my current salary! My only debts are car and credit card payment (both are manageable).

I wonder if the price in Great Sacramento will collapse anytime soon? Or I won’t be able to get my first house!

Bobby, Hang in there. California is a boom bust state. I sold my Sacramento home in 2005. Bought a repo in Jan. 2013. It was less than half of the 2006 top. Many California state retirees here. They will go belly up when Calpers vaporizes. Rates will be moving up also. Will be major headwind. I have been watching people buy crappy 1/2 plex’s for 300k, that need work. Amazing . Delusional. You always see this at tops! Btw , I bought my 1st home here in 1979. Everyone said, “Buy now, rates are going up, you will never be able to own a home. Well, we know how that turned out. Now they are saying “Buy now, rates will never be lower. Only the faces change!

Putter, you gotta be kidding me! You said CalPer will go bankrupt, and guess what? I just started my state government job 5 months ago! Fortunately I don’t have too much money in CalPer yet.

Speaking of housing bust, I could have bought my first house today. But, I feel there is too much risk. The more expensive the house it cost, the higher the risk. Indeed, check the following link:

https://fred.stlouisfed.org/series/ATNHPIUS40900Q

If history repeats itself, I expect a bust coming up soon!

On a semi related note, there are multiple websites that provide new build data (permits, starts, completions) by metros too.

(Realpage, MultiHousing News, Yardi Matrix, etc…there is a reason why these guys are able to keep such a tight collar on supply relative to demand…they track the hell out of it…)

Here are forecasted 2021 completions by metro,

https://www.bdcnetwork.com/2021-multifamily-housing-outlook-dallas-miami-dc-will-lead-apartment-completions

Spoiler…Dallas is adding 23k units in 2021 alone…capitalism can be hot in its responsiveness.

Of relevance because the rent sanctuary cities whose prices have risen with the arrival of mega metro economic refugees, almost always have room to build…meaning that after short term upswings, the addition of new housing supply will cause rents there to settle back down.

The rent sanctuary cities as a rule are not landlocked and politically c*ck blocked the way the mega metros are.

Eventually enough out of towners, homeless who vote and ten year tourists will leave San Francisco so that we can vote for some local family oriented politicians instead of the drift-in ideological carpetbaggers that have been leading the city over a cliff for the last couple of decades.

I predict the next mayor will be a conservative Chinese.

This is an multi unit housing story. Rents are rising on single family while they fall on multi unit housing in metro NYC, Boston, and LA/OC. Thank god I never bought apartment buildings.

People are looking for alternatives to renting or buying in conventional ways.

Invest in trailer parks. Only allow people who own their trailers. They have skin in the game.

A lot of people are buying cheap land and putting single or double wides on them.

Build tiny homes but sell them as fast as you can because people end up hating them. They evolve into a “tiny compound” of sheds and other outbuildings to hold all the stuff that they can’t keep in the tiny house.

RVs are becoming popular but I suspect people will tire of them like the tiny houses. Most RVs are not well made.

Interesting comments re: alternatives.

My late twenty something physio was chatting about saving for a tiny home because of the high cost of housing and rent prices in town. I asked what she would do about plumbing, water, sewage, sceptic and related zoning issues? She said she hadn’t really thought about it.

I stopped there as I could see it was her dream alternative but it left me wondering about the not so tiny land costs, taxes, home insurance, electricity, hook ups, heating bills, garbage, future kids, homeschooling, and pets that were not likely being thought about.

“asked what she would do about plumbing, water, sewage, sceptic and related zoning issues? ”

1) Well, small houses *come* with water, toilet, and electrical.

2) If a locality has integrity, the required hookups are available on an equal basis. There may be some minor costs for adapters…but she would be saving $250k on the *house* (plus interest).

3) If the locality wants to game zoning to discriminate against lower cost housing…then the locals have much, much bigger problems than infrastructure hookups.

4) Abusive locality…drive tiny house away. Try that with a $350k hostage to political integrity.

5) Some of the objections you raised should be addressed…but they tend to pale in comparison to the huge sums saved by considering alternatives to the “sanctioned standard”

6) As ZIRP forever becomes ever more inescapable for DC to survive, housing valuation insanities are likely only to get worse. People with common sense are going to be looking at all conceivable alternatives.

usual good comment c10, good summary of situation re little housing/ mobile home, etc

neighbor builds mid range 3/2 for $120/SF, or did six months ago; concrete block and stucco (CBS) exterior, hurricane fenestrations per code, nothing fancy, but certainly serviceable

small houses I have seen are about double that, per SF

both end up having to add approximately the same costs for infrastructure. Last I heard it was approx. $12K for a septic system, water hook up $6K, electrical similar– no matter what the house size

delta, as you say, is that one can be moved easily, though it will not be convenient

and to be sure, all local guv mints are clearly focused these days on getting maximum possible taxes on anything, including all utilities at way above sales tax rates, property taxes, etc., etc.

wealth tax appears to be coming in some states,,, YIKES!

also keep in mind mobile homes appear to deteriorate at a much higher rate than even mid/low cost CBS, etc., and are always mandated to be evacuated for any major storm

Vintage,

Yep, figuring out a way to minimize home building cost/minimize captive taxation risk is going to be a major, major issue going forward.

There *are* entire books on cost effective homebuilding and web pages offer dozens of hints (some as simple as avoiding McMansion sized Sq footage and corner-Laden, convoluted frontage).

Still and all, it would be nice if a website tied everything together with detailed financial numbers and references to accommodating general contractors.

I always start from the fact that Habitat from Humanity can build sub $100k homes in a world where median new builds are going for $350k (which cost $175k in 2001).

Time to re-invent Sears Craftsman homes?

NBay,

Not a bad idea at all.

Personally, I wonder why some reasonably hungry, but prudent, regional size Bank doesn’t generate some simple, low cost house plans that it will quickly finance and provide links to general contractors who specialize in lower cost builds.

Ideally, the banks could affiliate with sizeable, low cost builders in order to fully integrate the whole simple design/fast, safe loan/low cost build process…I’m not sure why no banks do this already.

Perhaps it is excessive/real fear of bank regulation forbidding certain kinds of relationships.

But such arrangements would benefit everyone,

1) Borrowers get lower cost homes simply,

2) Banks get safe loans (less loan at risk) at scale (many more buyers at lower price pts) and

3) Builders get a high volume of steady business with assured financing.

Pretty sure Craftsman homes were delivered as a kit, with plans, and as needed, and owner built. And it wouldn’t be hard to find someone to help out as needed, or do it all if one was totally building ignorant.

Anyway, I have a couple friends still living in them. Now that we have romex and fast cheap plumbing it would be even easier.

Of course you’d be in a battle with big developers and contractors for land and utility hookups.

Lake street & Chicago avenue (8 blocks north of where George Floyd had his life ended), Minneapolis, is where my Sears home originated.

1) The foundation was delivered with blueprints (bedrooms on the left or right was one item to be decided).

2) When the owner/builder was ready, the frame work would be delivered.

3) Last delivery would be the finish work.

As I commented recently, my ‘Longfellow’ neighborhood has quite a few of them.

You hit a right note there for a idea or two.

Folks are scrambling to alternative lifestyles.

Invest in trailer parks. But only allow transient high class motor homes and recreational vehicles that pay and on their way.

“Build tiny homes”?

Zero prospects not a starter, unless you are a land owner in a alternative community ahead of the zoning curve and got a bunch of moo laa.

RV’s are becoming the shit.

And most a very well made .

Problem is they aren’t a vessel to raise the sails on and seek new horizons.

Just sayin

-k

Completed one tiny home “campground” project.

Have 2 more on the books to get started this spring.

Out here in my part of flyover, they are doing it under commercial zoning as a campground. Most of my friends were adding them

to their campgrounds the past 10 yrs as their clients age, and the youngsters just want to party.

Please Michael show us your well-documented support for the statement that people who move into tiny homes “end up hating them.” Got solid statistics to back that up U.S. wide? Nope, I doubt it as it doesn’t exist. I love it when people make overly generalized statements like they are authoritative. I have been following the tiny home movement for years and I am unaware of any authoritative support for your broad statement. In fact, having met a number of tiny home owners (and, as you may know, tiny homes come in a wide variety of forms these days, not just standard stick-built tiny homes on wheels or on foundations), spoken at several tiny home events and having been involved in several tiny home groups, the sentiments I have always heard ave been to the exact opposite of what you said. Sure, there are those who ultimately find them not to be for them long term…as there are for virtually every form of residence….and those that do largely failed to explore them adequately before going tiny. But, I am unaware of any demographic that supports your generalized statement. But, feel free to believe as you may. Hopefully, though, no one takes your comment as being reality.

In 2006 it seemed like the price of housing always went up and would never go down. I moved to Florida in 2012. There were “For Sale” signs everywhere. There were foreclosures and short sales. Housing prices collapsed. Now there are few “For Sale” signs. They are building spec homes and communities. The price of lumber went up due to pine bark beetles and Asians buying lumber shipped from North America.

Just wait until the pandemic-inspired government-mandated foreclosure/eviction forbearances expire and aren’t extended in Florida (and elsewhere). The “For Sale” signs will flourish anew.

I have a feeling this whole WFH, move to the burbs and hinterland thing is a cruel trick being played by fate on Americans. People will finish falling in to this trap and and then energy prices will skyrocket just as the grid and the internet become janky and unstable. Chaotic times will then prevail.

I live in NYC and do a reverse commute to NJ a couple days/week (in healthcare and required be in office), know Newark pretty well, and am utterly confused about the skyrocketing prices there. People of all ages moving/ed out of NYC are most certainly not relocating there–one would think they’ve, eg, headed back to parents’ or to suburban houses with yards, maaaybe to those high rises on the west side of the Hudson with spectacular views of Manhattan–nor are young people from the suburbs moving there for an “urban experience,” as there isn’t really such a thing, especially not now–Newark most certainly isn’t Oakland in any sense.

I just don’t get it…maybe someone more local can enlighten me?

When even a tiny portion of 10 million people move to a small-ish city like Newark (pop. 281,000), it has a huge impact on the apartment market.

Wolf,

I agree, and,

I know you know this…

Although the stats only come out once a yr or so (and are subject to their own sampling uncertainty) the US Census has all sorts of population measures for essentially all geo levels (from Census tract to MSA).

At some point the the BLS/job stat changes should roughly jibe with Census/population/housing changes at the city/MSA level.

So at some pt, the Zumper stats are going to have an independent reality check.

(Zumper does cough up enough identical pct yoy increases, with enough frequency to at least raise one eyebrow…perhaps in some metros their sampling is tiny and not so random)

My view is that the value of Zumper et al is not in their absolute precision (no sampling is going to be absolutely precise) but that,

1) Before them, there was essentially nothing (with free, monthly turnaround, etc) …and nothing *really* sucks in terms of consumer education and macro tracking) and

2) the *relative* placement/movement of Metro pricing is valuable in and of itself because it narrows down choice/more in depth analysis.

I only wish we had *more* real estate related pricing data (historical, sub 100 metros, etc.).

Given the outsized significance of real estate related transactional data, it is kinda annoying that it took this far into the internet Era to even get what we got.

cas127,

As I explained in the article:

Zumper does NOT use sampling. It collects data from all “for rent” ads by city for multifamily buildings. It collects this data from the Multiple Listing Services, other apartment listing services, and its own listing service. It collects something like 1 million for-rent ads every month, automatically.

There is no sampling error here. There may be other data errors, but not sampling error since this isn’t a sample. The Census and the BLS use sampling.

If 10 million people are moving into the apartment market where the hell are they?

Good lordy. Read what I wrote, which is: “When even a tiny portion of 10 million people move to a small-ish city like…”

Note the “tiny portion of”

Moving to Newark for two and only two reasons: proximity and low prices (relative to NYC). Same why some move into East New York (bed stuy, Bushwick, crown heights). This trend applies to yuppies, hipsters and younger professionals; real NYers do not partake in this activity as they know better.

Looks like the Democrats are going to ram through a spending orgy that makes the last 10 years look small. I shudder to think what’s going to happen to our currency.

You mean less than what the last chief did last year?

Dont be shy, answer ;)

First, I was not and am not a Trump fan. He was far from a fiscal conservative. Second, the original $3.2 trillion spending orgy was a bipartisan affair, and was poorly targeted and wrought with fraud. The excuse that both parties used was that they needed to do something fast.

Now, we know that most of the “stimulus” stimulated Apple and Amazon. There is zero reason to be ramming through more spending while the $900 billion from las month hasn’t even been deployed yet. Biden wants to increase the extended unemployment until September 30! At this point, we don’t even know if we need it!

The Democrats own this one entirely.

Yes, the entire concept of “measuring results” and “doing things in stages” seems wholly, utterly alien to the DC mindset.

Basically DC has a bank robber mentality.

“Grab as much as you can, as quick as you can, before anybody realizes what is going on.”

This is likely among the top three (hmm…maybe five) most hateful traits of the DC political class.

Their sociopathic persistence at it too (despite all public opposition short of violent rebellion) is also right up there.

They are very much the school yard bully in outlook (“What are you going to do about it, punk?!!”)

Cas127, yes, you summed it up perfectly. They’re despicable, hateful, sociopaths that seek to destroy everything around them, for their own enjoyment.

Apartment rents are flattening and also rising in long underpriced markets.

The Midwest rental real estate market keeps getting better. I got out too early !!

One big problem that was not mentioned yet. There is a national moratorium on evictions and foreclosures that looks likely to continue for a long time.

Many tenants will stop paying the rent.

As a landlord you still must pay real estate taxes, insurance and maintenance costs on this “rented” property while not collecting any money. Not a good time to be a landlord.

Think there is a plan to deal with exactly that. Here it is: The Bourgeoisie will be left to swist in the wind, while the BIG BOYS are bailed out like last time. More consolidation of wealth into fewer and fewer hands & financial firms. The Bourgeoisie (middle class) will become the next basket of deplorables, targeted for extinction by upward transfer of their wealth to the ruling elites.

With how terrible the news places are in America, it’s hard to keep track of exact current rules. As far as I’m aware, in most places, you can’t evict for non payment of rent, but you can evict for other things. In my local market (average Midwest city), which is a “red hot” real estate market, many of the landlords will simply use other reasons to evict. Because rent is cheaper in my area, most of the would be non payers aren’t currently a huge problem because of the extra unemployment money, if that ends though, all h*ll could break lose. Right now, once eviction starts, the evictee actually leaves with less trouble than in the past.

When the lockdowns first started in March 2020, non payment of apartment dwellers was extremely high (normal for house renters though) even among those still employed and for some local landlords everything looked pretty bleak. The situation resolved when the initial local eviction ban expired and hasn’t been an issue since. Many payed right at end of that period. Some local landlords started an eviction process when the current ban started last year using other valid reasons besides paying rent (at least 1 landlord thought this would send a message to other tenants).

Rent is roughly $625 for a 1 bedroom apartment in my area.

I’m not agreeing with the it’s not a good time to be a landlord.

Think about it.

Indeed, and per Jerome, vaccines are good for assets. More viruses gets us more vaccines which makes the stocks go up and up. Milton Friedman said “inflation was always and everywhere a monetary phenomenon.” What did he know?

I’m at the point where I hate so much what America has become that I want it to fail while I’m still young enough to help rebuild.

I’m in a somewhat similar position, I just want to know if it will start to improve, continue to get worse for awhile, or what. If it’s just gonna suck for awhile, I want to know, I’ll probably jump ship (move to another country).

America is economically and physically is better shape than people give it credit for, all the big problems are social problems. If the social problems were solved, all other problems could be easily fixed very rapidly. If the social problems aren’t fixed than there’s nothing I can do and while America should start to improve eventually, I don’t intend to spend potentially decades living through the dum dum period.

Right now, all the various identify polittics will eventually reach the point that they can’t out crazy themselves anymore and the pushback should begin. In order for some of those movements to stay alive, they have to continually out do themselves, but rock bottom, eventually comes. I might wait around for that, which hopefully, will be within the next few years and we will hopefully see what direction things are headed.

Except for a few over priced places, rents are still rising for most renters.

Renters defaulting on their rents is probably forcing up rents for those still paying.

Somebody has to pay for this!

There is little to no skiptrace left in the big cities markets.

That is in my humble opinion.

The Biden Depression is going to be long, dark and deep. After four trips around the sun, hopefully we’ll be without a central bank, without central bankers and will have a new generation of youth coming into the economy unwilling to play by the rules of the old game.

Oh please

You haven’t a idea of what ounce was and what will be come of the bankers economy. Try studying ronald regan economics for ideas what is wrong with the current state of affairs.

-k

Tulsa, my birthplace, isn’t exactly an armpit city and sure wouldn’t be on the bottom of my list to reside. But after living in Seattle for a few years I can see why people love the west coast. Don’t ever count out the west coast.

I would move to Mexico #1 if it felt safe.

Many retired spooks (all agencies) like Panama, but they can take care of themselves and their own. Still might be a good place if you go to the enclaves where they are.

I’m gonna go down with the ship where I was mostly raised and lived, and practice downsizing.