“Physical occupancy” rate (tenants living in the apartment) v. “economic occupancy” rate (tenants actually paying rent).

By Wolf Richter for WOLF STREET.

A $481-million loan that had been securitized into a Commercial Mortgage Backed Security (CMBS) in July 2019 by JPMorgan Chase and is backed by 43 apartment buildings with 8,671 apartment units in 25 metros, spread over the Midwest and Southeast, has already been put on the servicer’s watchlist, according to Trepp, which tracks and analyzes CMBS.

The comments of the servicer, KeyBank National Association, on why it put the loan on its watchlist are a sign of our times when eviction bans and work-from-anywhere have changed the equation for owners of apartment buildings.

Most CMBS are backed by many slices of debt from all kinds of properties, thus providing large diversification. This CMBS – JPMCC 2019-MFP – falls into the risky category of “single borrower” CMBS, being backed by only one mortgage. And that mortgage is now causing concerns with the servicer.

When the mortgage was securitized in July 2019, investors were told that the consolidated occupancy rate across all properties was 89.5%. Even with this less than stellar occupancy rate – major renovations of the properties interfered with occupancy, it was said – the debt service coverage ratio (DSCR) was 1.42x, meaning that net operating income from the properties was 42% higher than the mortgage payments. And that sounded pretty good.

“Physical occupancy” v. “economic occupancy.”

The DSCR has now plunged to 0.86x as of the financial statements of the third quarter 2020, according to the servicer’s watchlist comments, meaning that the net operating income is no longer sufficient to cover the mortgage payments. This, according to the terms of the Loan Agreement cited by the servicer’s comments, constituted a “Debt Yield Trigger Event,” which caused the loan to be put on the watchlist.

And the occupancy dropped to 76.5% by the end of the third quarter. That’s the physical occupancy. But the “economic occupancy” – tenants actually paying rent – has dropped further, the servicer comment said.

The servicer’s comments didn’t specify that exact level of “economic occupancy” – tenants actually paying rent. But there are some clues. When the loan was securitized in July 2019, physical occupancy was 89.5%, nonpaying tenants could be evicted, and the operating cash flow was 42% higher than the mortgage payments (DSCR of 1.42x).

Now the physical occupancy rate dropped by 14.5% (by 13 percentage points), as some tenants have left, perhaps to work from anywhere, or they bought a house in the distant suburbs and became part of the land rush.

But eviction bans allow other tenants to remain in their apartments without paying rent. And net operating income from the properties plunged by nearly 40%, driven by a 14.5% drop in the occupancy rate and by an undisclosed number of the remaining tenants not paying rent.

“As a result of the COVID eviction moratorium and tenants not paying rent, the physical occupancy exceeds the economic occupancy,” the servicer notes in the comment.

At securitization, Moody’s rated seven of the nine classes of the CMBS, affecting $435 million of the $481-million deal. It gave its highest rating for CMBS, Aaa (sf), to Class A, which would be the last class to take any losses. At the other end of the spectrum was Class F, which it rated B3 (sf), six notches into junk (my cheat sheet of bond rating scales). Class F would be among the first classes to take losses.

The loan, which has remained current, matures next July, when it would have to be refinanced. But three one-year extension options in the loan agreement could put maturity out to 2024, according to Trepp.

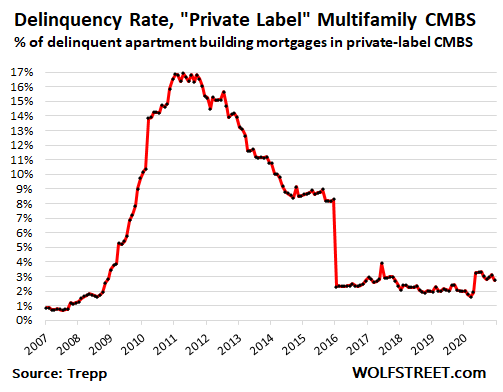

The combined effects of eviction bans and surging vacancy rates in some cities – and plunging rents in some of the most expensive cities – are beginning to percolate through the commercial real estate market. But it’s a slow process. And delinquency rates on multifamily loans remain low.

The delinquency rate of multifamily loans securitized into “private label” CMBS was 2.75% in December, according to data provided by Trepp. While that is up by about 1 percentage point from just before the Pandemic, it remains low compared to the delinquency rates of hotel CMBS (19.8%) and retail CMBS (12.9%). And it remains low compared to the delinquency rates during the Financial Crisis. In the chart, the drop in January 2016 resulted from the delinquent $3-billion loan tied to Stuyvesant Town-Peter Cooper Village in Manhattan getting paid off (delinquency data through December provided by Trepp):

The chart above tracks the delinquency rate for multifamily “private label” CMBS loans, meaning they’re not backed by the government. But they’re only a small part of the huge pile of multifamily debt. And you guessed it, for over half of it, taxpayers are on the hook. Time to take a look. Read… Who Holds the $1.65 Trillion of Apartment Building Debt amid Eviction Bans and Plunging Occupancy Rates at High Rises?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Anybody else get the personalized junk mail from Unison for what appears to be the homeowner getting a ~ 20% cash equity withdrawal in exchange for them getting a co-investment of the same amount in your property?

No monthly payments, no interest charges. Use the money for up to 20 years until you decide to sell. They share in the gain or the loss when you decide to sell. Appraisal fee up to $1250. Transaction fee 3% of their co-investment (sounds like points). The starting valuation is actually reduced by 2.5% Final home valuation by independent appraiser when selling or buying them out. They will not share in decrease in value in first 5 years. They can be bought out of deal after 5 years.

The estimated value they gave is so high it makes Zillow look like Scrooge. I’d move out within 5 minutes if they offered to buy the whole place for their price.

My question to Wolf and the commentariat here, are we in 2007 again with these offers? On the other hand, are they expecting Weimar and want cheap physical assets on the cheap? Will this be a vignette in The Big Short II and will I be sitting next to Selena Gomez?

Sounds like they make their money off the fees and sell the sliced and diced “co-equity” agreements to pension funds and to taxpayer backed funds.

Everybody sitting in their forbearing mortgaged home, who thinks they will have enough equity when forbearance ends to overcome this mess is delusional. When all these homes hit the market at once, it will be a bloodbath.

Correct again Ms Petunia

They may restructure loans or extend the repayment period.

Maybe the first ones out will. I’m going to keep my home buying cash in a no-penalty CD. I cannot believe people are putting their savings for short-term purchases into Bitcoin and stocks right now. I say to them, fear not inflation for there will be an end to forbearance!

Who’s with me?

Common sense and economic history are on your side, Turtle.

However, we are living in unprecedented times and I would not put anything past the authorities running this clown show spectacle of an economy.

Extend, pretend, and double down on what is destructive in long run rules the day, for a while. Insane behavior is seen as virtuous.

We will eventually slip slide into some long-needed but painful form of economic reset. That outcome unequivocally must and will occur.

Everything, according to Tao, is about reversal (i.e. reversion to mean, restore balance, no tree grows to the sky– “all that is presented as true will be revealed as false and all that is presented as virtuous will be revealed as fraud”).

The Bitcoin and crypto sham is one the biggest scams in history. At least a tulip bulb could be enjoyed through its beauty. Think of the pension funds who jumped into Bitcoin at $41,000. They’ve already suffered a 25% loss. How do you think that feels?

Oh, but they’re going to hold on and stay in it for the long term, right? Pffft. Once those losses accelerated and they down 60%, these idiots are going to head for the exits en masse. All crypto is WORTHLESS.

Just about all the smart people in the world (Stockman, Hussman, Jim Rogers, Jeremy Grantham, Jeff Gunlach) say the Fed owns it right now. There is no functioning price discovery. All very pessimistic on US stocks. Gunlach said he recommended 50% cash, 25% gold and finger on sell button with 25% momentum stocks if you dare play there. Maybe we really are socialist now with total government control of asset markets until the train wreck.

Depth Charge:

“Think of the pension funds who jumped into Bitcoin at $41,000”

Pension fund investments in bitcoin??

I don’t think so.

Most are “restricted” in their investments.

“Pension fund investments in bitcoin?? I don’t think so. Most are “restricted” in their investments.”

Looks like somebody should do a little bit of Googling before posting.

I expect a lot of these kind of schemes to emerge in the coming years, as so many people are going to have pension shortages and most of their “wealth” is locked up in their homes. They will be forced to accept rotten deals to be able to cover their living expenses.

A small, well maintained and paid off house is fairly inexpensive. Much cheaper than renting.

The only variable is property taxes. Which in many parts of America is a bigger expenses than the mortgage for younger buyers and always increases.

And the property tax folks don’t play the forbearance or you don’t have to pay moratorium games.

“They will be forced to accept rotten deals to be able to cover their living expenses.”

Assessors do not foreclose typically until the past due bill and the market value of the property converge. Buyers of Helocs and Rev Mos assume these are written in stone, could be called or renegotiated if the company sells the paper. There are other variables, you need a new roof and you go to the city, and they issue new (more expensive) guidelines. You throw up a tarp, or a few shingles. In tough times cities do this, and when an entire area becomes “blighted”, they implement eminent domain and sell your land to a developer. While the wealth disparity gap widens people with assets buy up desirable property.

Those who opt in will also face a lot of fine print covering the protection of that co-investment. Expect to have increased focus on repairs and maintenance to keep that property in top condition to facilitate quick transactions. Sweat equity becomes sweat preservation of eroding equity and is a hidden cost of such schemes. You don’t get any free lunch, but may have indigestion.

‘Oh, you forgot to do X, then we’ll ding your remaining value by X+, and maybe assign the remedial work to our affiliate, at a markup.’

Great article. What impact will we see in with prices of goods, stock market and general savings when the fun free times stops? Once people are required to pay for the goods rendered, either rent or student loan, what type of impact could be expected in the macro environment. The pretend and extend just got a new lease extension

Gas up 40 cents a gallon here. I thought people were talking smack until I pulled up to the pump tonight—I looked, and drove away. I will not be participating like I was the past 4 years.

Yeah at an extra 40 cents per gallon and 15 gallons to buy, that’s a whole $6.00 extra. Do that three times per month and we’re talking real money … $18.00 … Who could afford that? I thought the housing price increases pricing me out of the market and crushing my dream of owning a home were bad. But $18.00 extra whole dollars per month for gas?!? I won’t stand for it!

Hey, I don’t care. Social Security just gave me an extra $19/mnth. I’m up $1.

Ya, when that higher fuel price start making it’s way into every of the economy as oil is a base commodity it will cost you a heck of a lot more that 18 bucks.

Wow, talk about a lack of perspective. The increase is entirely dependent on location, whereas in the Bay Area this is not a big deal given the WFH and the earning of megabucks, the same may not be true for someone living in the Midwest who has to commute everyday.

It also is interesting given the reduced demand why gas would be rising at that clip. I suppose it depends on the rate, after all, it might have been a month in between refilling.

This is the kind of myopic thinking which prohibits a person from understanding the effects of inflation on household budgets and the economy as a whole.

The extra $18 per month, or whatever the figure, has to come from somewhere, and since the person likely did not magically get a raise of that amount, they will be cutting back somewhere else. Higher fuel prices = not eating out at the restaurant 4 times a month, instead cutting it down to 3. Now the restaurant has lost 25% of their revenue from that customer. If all their customers do the same, they’re now hurting. And down the line it goes….

You’re right Z. Have another $7 Starbucks.

Zantetsu, a guy/gal that “doesn’t get it”.

Also if people drive less there may be less spending on oil changes, new tires, car maintenace or even new cars.

“Also if people drive less there may be less spending on oil changes, new tires, car maintenace or even new cars.”

This is something I’ve been practicing since the oil price spike in 2007/2008. I have significantly cut my trips. I plan everything out now, even when fuel prices are low. I only do one oil change per year. Tires last 6 years.

Bicycling is very cheap and nobody on bikes give you the finger like folks in the cars!

Is that kinda like double secret probation?

“This, according to the terms of the Loan Agreement cited by the servicer’s comments, constituted a “Debt Yield Trigger Event,” which caused the loan to be put on the watchlist.”

There are other consequences, which I didn’t mention, including that the cash flow has to be put into a sweep account, and other things that protect lenders.

Eviction moratorium extended to the end of Feb.

Foreclosure moratorium extended to the end of March.

Student loan freeze extended to the end of September.

Even when the economy reopens to near pre-covid levels, I’m not sure how one engineers an orderly return of these payments. No politician wants to be the one telling 45M people that they’ve got to make SL payments again.

Your comment caused me to compare how the financial crisis 12 yrs ago with home foreclosures where handled, in part because we now have some of the same team in office now who handled that 12 yrs ago. But the situation was different. So what might be the same?

The focus of policy 12 yrs ago was not to help folks avoid foreclosure but just to slow it down so as to benefit the banks, which could not handle all of them at once. “Foam the runway” was the famous damning insider statement of what polices falsely sold as helping folks keep their home. That was never the intention. The disinterest in helping families keep their homes and the priority on bailing out investors and banks, might indicate the current team my not be interested in helping those 45M people you mention – many of them renters and home owners behind on payments.

Ignoring people while prioritizing banks and investors didn’t work out well for that team 12 yrs ago – their party went on to loss more elective offices than any other President in history.

Yet I’m not convinced they never did learn any lesions from that huge failure. What does it all mean?

If they didn’t learn from 12 yrs ago, we might have another whiplash in opposite direction again and be looking at a one termer by angry voters getting shafted on a grand scale yet again.

timbers

Good political “debt handling” observation. However, if extend & pretend becomes forgive and move on, then the moral hazard of 2009-2013 becomes the new norm with a twist.

If govt policy is to S*** on landlords and lenders, turning them into enslaved providers of lodging, the political fallout could be even worse. More likely you would see more landlord / lender bailouts, arguably justified.

“enslaved providers of lodging”

Ha ha, love the image! I can think of more than one scummy landlord I would’ve liked to put to the lash. Not sure exactly what one would have the enslaved landlord do. Mow the grass more often? Make repairs? Hoe cotton and tobacco?

Back in the real world, this ball of knotted string can not be untangled. Some problems just can not be fixed under the current system. Making everyone whole after a year of economic chaos is one of them.

Trash-Yeah, I find that funny as hell also,

Yep, same team, same playbook, but less tools in real terms.

Compared to 12 years ago, the value of the dollar has decreased, the problems though are somewhat self induced. But you can see it at the beginning of a death spiral, back rent will never be paid, mortgage forbearance isn’t forgiveness and the interest is tacked on.

None of this is good, but the temporary solution is still the best. Go with incentives that will be hard to reverse without causing massive uproar against the powers in charge. Its a recipe for disaster.

Sort of like “flatten-the curve”

It makes a lot of sense. Get whatever cash is out there by enticing buyers into a land rush, then pull out the rug with foreclosures and higher interest rates 6 months down the line.

The HAMP (Home Affordable Modification Program) allowed me to save my home.

I had sent in a Loan Mod application and it was turned down. I called the bank to ask why. The nice lady on the phone said:

“You’re up to date on your payments. You’re not showing any economic hardship” Me: “How do I do that?”

She said “Don’t make a payment for 3 months, then send in your Loan Mod app and then make a payment. You’ll be behind and that will show economic hardship.”

Me: “If I don’t make a payment for 3 months, you’ll foreclose on me.” She said “No, we don’t do that until 5 months.”

Being a naive person, I thought “My bank doesn’t want to steal my home.” and took her advice. On day 91, I heard a knock on the door. I was served a foreclosure lawsuit.

I’m so thankful for Obama’s HAMP program. It saved my home and I learned a painful, valuable lesson.

For some things like student loans, it might be possible to slowly increase payments from 0% until they reach their original amount. As long as another recession doesn’t start it could work. But, Bideen said he would push for canceling 10k worth of student loans. A scenario where you have start paying again and 10k worth is canceled at same time would help. We’ll see if he follows through. It might also be possible that for those owing more then 10k, that their payment length wouldn’t change so that monthly payments instead decrease.

Another sneaky solution is to reduce typical student loan monthly payments to a minuscule, token amount (say $25) but make entire loan sunset in 15 or 20 years (balance wiped clean no matter how much was paid back).

The optics look better that way, and the unfairness of the whole scheme is less perceptible to the public .

A small builder is building a new modest home near me. He checks in everyday but it’s all being done with various subcontractors. All these guys physically work very hard at this time of year in cold weather on a useful project. I am sure they are making a hard living. No way it’s morally right to forgive a student loan when 50% of tax payers do something useful for a living.

We already have a system in place. It’s called “bankruptcy.” Oh, your loan doesn’t qualify? So sorry you made a bad choice. LIVE WITH IT.

I wouldn’t bet that our economy will get back to pre Covid levels at least not in my lifetime anyway

The whole thing was fake pre-COVID anyway. “Stimulus” for 14 years and running. What kind of “greatest economy ever” needs stimulus?

I read a lot of financial stuff and listen to central bankers and try to read between the lines. If you listen carefully they are telling you we are not able to stop eating the seed corn or we will starve. It doesn’t take too long to eat through it. Hopefully the price of gold will shoot up to $10,000 or something to convince them they have done too much.

Politicians will always try to kick the can and the Fed has been all in ever since 2009. Covid again has caught them in a bad spot and they are going to keep going. The sad part is the deeper they dig in the more dishonest they have to be and the more corrupting to society. When millionaires are minted buying Tesla stock or bitcoin it causes more and more ponzi type behavior and hard working people get conned.

To be fair – mortgage rates in 2008 were at 6%

“And it remains low compared to the delinquency rates during the Financial Crisis.”

Yes, but it also says, “it remains low compared to the delinquency rates of hotel CMBS (19.8%) and retail CMBS (12.9%),” which are in the same credit environment as apartment CMBS.

And this is very early on in the crisis. This stuff takes time. Apartment delinquency rates are bound to rise, just as office delinquency rates are abound to rise. Landlords for now are just hanging on the best they can, and using up their reserve funds.

We are like in early 2008 at this point. Eviction moratorium is still in place. Stimulus and bailouts are just beginning. This is like a slow motion train wreck. Stay tune.

The fun starts when the FED can’t suppress interest rate any lower. I’m still waiting for the non-banks loans to go bad and for QE5 to commence.

Look at the states with problem getting unemployment benefits out to workers. Those people are desperate. I hear CA and PA are at the top of that list right now.

Wolf, this typical Extend & Pretend environment is happening at a time when the revenue streams needed to service all this stinky mortgage debt are becoming more encumbered, not less. There is no consistent signs in any economic metric, forget about the opiated activities on Wall & Broad, that points to RECOVERY OF THE ECONOMY anytime soon.

It is just the opposite with more business shut-downs threatening via a mutating Covid virus and layoffs in large and small businesses picking up steam. Vaccine results are a very mixed bag so far, not to mention a giant DELIVERY stumble going on in getting the drugs out to the public. I am not offering my arm out the window for several more quarters, too old for a mistake.

I’m never “offering my arm out the window.” I have an immune system for that.

A few months ago I would not have taken the shot, but now I would. For one thing my DNA isn’t going anywhere. Weighing the negatives, anxiety, and all the limitations it makes sense. Time for a colonscopy, how’s that gonna work? What happens when you have a heart attack? Take two aspirin? Close family member died of COPD, so no thanks. Six months on a respirator and then the dirt nap, or worse you come back with half a lung. I quit smoking (difficult) years ago, I think the Covid vaccine is going to be a lot easier, and prevent a disease whose risk factors are in multiples of those associated with using cigarettes.

Wolf,

Excellent and important post…

“And net operating income from the properties plunged by nearly 40%, driven by a 14.5% drop in the occupancy rate and by an undisclosed number of the remaining tenants not paying rent.”

I think some readers may badly underestimate the significance of such data because they don’t know enough about historical apt data to be able to put these truthfully large falls in context.

Although you would think a 40% fall in net income would be enough to wake anybody up.

And if they are counting on rent arrearages being made good…the obvious question is *how*, considering that even in “good” times a significant % struggle to make 1 month’s rent.

How are the going to catch up on 6 or 12 months worth?

I smell a “bailout” CDO (backed by DC) that securitizes this longshot arrearage “collateral”.

“And this is very early on in the crisis. This stuff takes time. Apartment delinquency rates are bound to rise, just as office delinquency rates are abound to rise. Landlords for now are just hanging on the best they can, and using up their reserve funds.”

Wolf, it implies housing market collapse is on the horizon. Since landlords couldn’t afford paying their mortgage, they have to sell the houses. If there are more houses for sale than buyers, price of housing will drop.

Does my logic make sense? I am looking to own my first house (for investment), but I am not comfortable to jump in the pool now.

8_mile_road,

Trying to time the purchase of a house that you want to live in and make your home is a very frustrating activity. Yes, do take your time; and yes, do understand that the house you live in is an expense that you need to be able to afford, and not an investment, and then just try to do what makes you happy. Life is short :-]

“and yes, do understand that the house you live in is an expense that you need to be able to afford, and not an investment”.

Wolf, this is EXACTLY what I read from “Rich dad, Poor dad” by Robert Kiyosaki. He believes housing itself is a liability, NOT an investment. BUT if this is the case, then why there are so many people buying houses for investment?

I personally believe investing in stock market is more flexible , more profitable, and less hassling. The biggest concern of stock market investment is timing. If you put 100K into stock market vs down payment of a house, chances are, your stock market portfolio does better than your house.

What do you think?

Housing is an investment is when it’s rental property.

In 2008, people didn’t stop paying because of the interest rate, they stopped paying because they lost their incomes and eventually their savings. That’s what happened to me.

If you managed to keep your job from 2008 onward, you hardly noticed anything was wrong in the economy. In fact, you did better than before because prices dropped overall.

Most people stopped paying not because they couldn’t, but because they were underwater. When they paid $350,000 and the house was now worth $175,000, they decided to stop throwing good money after bad, especially when they saw what $350,000 would then buy.

This is exactly what I did, along with many others that I know. I bought a condo in 2008 for 350k. In 2010 it dropped to190k, so I did a short sale on it, and only lost my 5% down payment (and a miniscule amount of equity). Had I been required to put a 20% down payment, I probably would not have made this decision.

Depth Charge (and others):

In the ’08-09 crash too many stopped paying mortgages because too many financial institutions refused to modify loans. You could fill a sports stadium with the amount of requests for “loan mods” by payers to their collectors during that time.

Sure set up for the gross sales of “abandoned” homes for the monied scavenger investors to vacuum up.

I agree with others that this economic mess pre-pandemic and post will not be cleaned up quickly. Too much hangover from the previous crash plus what is happening now.

Inflation?

Go grocery shopping……that will give a clue!

Social Security increases?

Some of that “enormous” increase is eaten up by the increase in Medicare deductions.

Invest in mental hospital care; that’s what will be left when this mess is on the mend.

The price of an existing home is in part based upon the materials that go into construction. Lumber and basic commodities are soaring. The salaries of the labor component of home construction (think of all the undocumented who will soon to be on the path to citizenship and demanding higher wages). So going forward it will cost more and more to build a new home. So, I’m not sure we’re going to see the crash you imagine.

Covid taught us the bottom 60% of US earners (or is it 80%?) probably don’t matter much to the US economy. They could vanish tomorrow and Blackstone group would jump in and buy their homes with Fed money at pennies on the dollar. Certainly with Biden’s new immigration policy, those in the bottom tier will feel even more stress.

I don’t see a shortage of money out there, and it’s obvious the Fed is intending to prop up asset prices for as long as it takes. The conventional notions of supply and demand don’t apply, because you have a price insensitive lender (the Fed), that keeps inflating the market.

It would be interesting if anyone who has sold a home recently, could share their experiences. Did COVID make it almost impossible, or did it go quicker than they thought?

“Covid taught us the bottom 60% of US earners (or is it 80%?) probably don’t matter much to the US economy.”

I’m sorry, but this is one of the dumbest statements I’ve ever read in my life. The stimulus to that demographic is the only thing propping the economy up.

I listened to the ECB press conference with LeGarde. She speaks Orwell type language. If you want to sum it up in a nut shell they ain’t gonna stop til they hit symmetrical 2% inflation. If the economy goes to zero they still going to be trying to hit 2% inflation.

If you know a little French history you feel like she is someone that has come back from the 1700’s solving the Government’s problem of being broke with funny money schemes. She has kind of a long neck and you would think she would remember history.

I live in SW FLA and I don’t know very few if any white people that want to do the jobs of immigrants: picking fruit/vegetables, washing dishes, busboy, maid, hard manual labor like roofing, construction, etc.

I have a neighbor who is a big DJT supporter. His contractor owns a house at our end of the block. He’s also a big DJT supporter. When this neighbor just gave his home a $75K makeover, guess who his contractor hired?

All Mexican guys. Every. Single. One.

The roofers? Mexicans

The dry-wallers? Mexicans.

The guys who installed the brick driveway? Mexicans.

The painters? Mexicans.

Window installers? Mexicans.

I could go on, but you see my point. These “America First”, anti-immigrant traitor red don the con lovers…..hire ONLY Mexicans. If you ask why, they’ll tell you: They work harder. They show up. I can pay them less.

Funny what hypocrites these people are, huh?

“I could go on, but you see my point. These “America First”, anti-immigrant traitor red don the con lovers…..hire ONLY Mexicans. If you ask why, they’ll tell you: They work harder. They show up. I can pay them less.

Funny what hypocrites these people are, huh?”

So you thought you’d take an anecdotal story about your neighbor and extrapolate to include all Republicans who you then label “anti-immigrant traitor red don the con lovers?” Do you even understand how deranged you sound? Get professional help.

No shortage of hypocrisy here, that is one USA fact, maybe even a “truth”. And they are way beyond professional help, being certifiable sociopaths like dear leader. And since there are hardly any mental facilities left, let ’em go to prison with the physical murderers, for economic murder. (I wish)

Turn around time not fast but crazy fast

House (my Mom’s) was a 60 year split in very poor condition, i.e broken boiler, termite damage, broken appliances, original driveway and walkways, in a low tier suburb of NYC.

I was thinking flipper at 300K

Sold in 3 days for 475K to a young couple who will making many trips to Home Depot and Lowe’s, wishing them well

I can’t wait to see how our nation goes from rent, mortgages,

maintenance & property taxes being optional to… What ?!

Nicer tents ?

A TARP, the kind that covers the roof and siding.

But it leaks like crazy, so you’ll need to supplement with these QE blinds, just keep adding as you want. It’s a crazy contraption, but at least you won’t get too wet.

After a few attempts I got pretty good at keeping out the weather with tarps. It helps to use two layers, nail boards around the edges, and throw an old tire in the middle to reduce flapping in a strong wind. I also found out the tarp needs to go all the way up to the peak and over the top a bit.

I am very, very grateful that now I have a solid roof these days, since I don’t do ladders and roofs anymore.

I played that game when building an off-grid home. FWIW, I learned and paid more for the tarps truckers use. They cost more but lasted much longer, with better grommets. (yeah, I even bought a grommet kit for the cheap ones). But that was in the 90’s. I have no idea what kind of garbage is being sold now. When I did roof, ELK was best shingle, back then, anyway.

Also, having high ridge top winds, you can nail boards in the middle to stop flap and secure it better if you use plenty of quality RTV under it, so the sun can’t trash it fast, which I also don’t know if they make it any more. A roofer friend taught me how to think like water, especially capillary action. (he didn’t know that term, but knew how water “thinks’.

Doubt there are many here that need that advice, maybe a small time landlord.

I was super lucky and got into a 200 unit 500 sq ft hotel style low income (under 50% of area median household) apt. Think after 10 years I’m grandfathered in, as I no longer have extensive qualifying every year, just sign under penalty of perjury my gross income. Small savings doesn’t matter anymore.

I consider myself one of the very lucky ones, after reading this article.

Forgot to mention rolled roofing, blob RTV at each roofing nail, (account for EVERY one that rolls off on vehicle used sides), but again, you have learn to “Think like water”. Also, cinder blocks are good, and you can later use them for other things like shelves, or even what they are designed for.

People joke but a $400k house will end up costing $800k with interest, taxes, insurance, upkeep, etc.

Or you could spend $500 on a great tent, use bottled water, and sh*t at a gym.

And have $799,500 pre tax dollars to spend on something else.

A bit of a jest…but made less so with each passing yr of DC insanity/stupidity when it comes to liability inflation…

The banks are in big trouble……this article multiplied across the country by a big number.

This time when they try to tarp it all up and keep the same dolts in charge the overseas value of the dollar is going to collapse.

Which will force the fed to tighten credit conditions.

Lookout grandma……that stock you bought paying 5% is about to get shredded….but they will wait……like Michael Corleone……until the capital gains tax rules are adjusted so the mob (otherwise known as Uncle Sam) gets a big cut when all the forced sales occur.

You forget that the entire world’s central banks are doing the exact same thing, and that there is a worldwide housing bubble.

Is it a good time to hold cash yet?

Gold and Silver Cash not so much And that includes ALL currencies

The worry that I have about gold is that it’s price is negatively correlated with real yields. If inflation picks up, I wouldn’t be surprised if real yields rise (anticipating much more inflation in the future) because everybody expects the Fed to be behind the curve when it happens (the Fed says so themselves!).

Ironically, cash might be the place to be when inflation picks up, because everything with duration risk (including stocks, especially the ones with high P/E) will be re-valued based on higher interest rates. Cash will lose value but not as fast as things with duration. Also consider what a couple percent rise mortgage rates will do to real estate.

Gold is a bit of a wildcard. It should suffer from higher real rates, but higher (real) rates would also lead to default risk everywhere and physical gold lacks counterparty risk and could therefore act as a safe haven, pushing the price up. But that is by no means a given.

Quality, well placed, gold producers are making immense profits and raising their dividends. They are sitting on piles of cash and relative to other fantasy sector stocks/notions are reasonably priced and undervalued (what a concept)!

For me, I will let them be my store of cash and am quite happy with their ascending dividend ‘yield control.’ Physical gold is lovely and precious global collateral/leverage.

{Note to self: Uncle Buffet showed he paid his operating ‘allegiance’ fee to those in power by feigning/shepherding a false following with that quick in and out of Barrick.}

YuShan, my only question to you: WHAT HAS GOLD AND SILVER DONE, FROM A PRICE APPRECIATION STANDPOINT, going through no less than three financial collapses since January 1, 2000??? I started buying gold at $280 per ounce and silver at $7 per ounce back in 1997 and 2003, respectively. Gold at $1863 this morn and Silver at $25.70, do the math. Don’t over-think your strategy as the barn catches fire. Just get the heck out of it.

@David W. Young

Yes that’s exactly my point. Real yields have been trending down over that period. When that trend reverses it is likely to affect the price of gold.

Didn’t you get pretty rich here as a developer/house flipper and move to Turkey? Your advice isn’t relevant for us in the US. We are stuck with coin of the realm, at least at the lower levels, wherever it goes.

I can see the day, not far into the future, when the big banks including mine, will have a bank run. The CMBS defaults and other bad paper on their books, could be the driving force. Another driving force could be negative interest rates. The news media has nothing exciting to report on now that Trump is gone and their ratings are plummeting. People lining up at banks like back in the 1931- 1932 would not be good optics but would be good for their ratings.

I see the solution will not be to close the banks like Roosevelt did but we could see the government forcing the small depositor to limit cash withdrawals to $300/week or show need if they wanted more.

Um..nobody goes to banks anymore – mostly because banks have closed all the branches. Anyways even low income people can move money between banks quickly on their phones, pay bills, do their taxes, get a loan on their refunds etc.

I hope you are never in a hurricane, flood, fire, or earthquake zone. Good luck buying anything then with your smartphone.

I learned that here in Houston during several hurricanes and recently Harvey (54″ rainstorm). The “smart” phone was only good for playing Solitaire.

On 911 out smart phone didn’t work. Just when we needed it.

Buy a Harbor Freight gel-cell battery jumper. Was $65 in 2017. Probably lousy for that, but keeps cell phone alive a long time. Bought one for sister, too. So far, so good in power outages. Even has led light you can read by.

I withdrew all my savings awhile ago Why risk being bailed in when they hardly pay anything anyway and yes , I agree that bank runs are coming

Frederick, that depends on whether you live just off the Mediterranean Sea or on the other side of the world. ;-)

I don’t think bank runs are coming. It’s unbacked fiat now. Congress can appropriate as much money as needed to citizens and Feds going to buy the treasuries with their magic computer entry. The run will be on the store like it was for toilet paper to spend it and complain about shortages and high prices. Politicians will be saying that we need to raise the minimum wage to $25 / hour.

Bank bail-ins (depositors are on hook to save banks) have already been tried out and are likely to be unleashed in a SHTF moment.

I see the government limiting withdrawals, even without a bank run. If there is no crisis then the government will create one and then use that to limit customer withdrawals so they don’t have to do what they did in 2008 in bailing out the banks for their bad investments and all the bad paper on the books which ain’t worth squat. They’ll blame tax cheats, money launderers, and drug dealers for the new emergency edict. Its called a new “Bail In” policy modeled after Cyprus.

@Swamp – that $300/week is a reason to have accounts at multiple banks. Banks are no longer paying a significant premium to large depositors.

“The news media has nothing exciting to report on now that Trump is gone and their ratings are plummeting.”

Oh man, that WAS funny!!! Thank you for making me spit ice coffee all over my laptop!! I almost choked to death. Oh gosh….man….yeah, that’s right…you’re 100% right!!

There’s nothing exciting happening in the world without that ridiculous trust fund jerk golfing, tweeting, lying, stealing and watching fox news all day long! No Sir, nothing “exciting” happening any more!!!!

With all due respect: What on earth are you talking about?

Yeah, laughed my fragile sensitive snowflake ass off, too!

Alternative; You can read all the gloom and doom at Wolf’s media empire.

(Just joking, we went through all that before)

Jamie Diamond, the CEO of JMP/Chase has a policy at his bank that it is illegal to put cash in your safe deposit box. Does he know something we don’t?

Swamp Creature,

It’s not “illegal,” meaning against the law. But the bank doesn’t want you to do it, and if you do and the money gets lost, it’s your problem, and if you falsely claim that the money got lost, it’s also your problem. This is what the Chase account agreement says (you can google it, it’s posted online):

“You agree not to use the box to store money, coin or currency unless it is of a collectable nature, and you assume all risks and hold the Bank harmless of any loss or alleged loss of said money, coin or currency.”

I used the wrong word “illegal” . But why would anyone ever put cash in there subject to that agreement. No way. And if you keep it at home, you risk getting robbed. In DC there are networks of burglars that look for easy picks. Been there.

I can think of a lot of reasons. If the money is ill gotten, or you are trying to hide it from the taxman come estate tax time, cash in a safe deposit box is one of the better options.

Lie – ability.

Cash is easy to stash my friend. Not being able to find a safe hiding place is just a failure of imagination.

Use cash, starve the banks.

No cash, no freedom.

Protip: use $50’s

Look, you are NOT a “swamp creature”, you are just a damned DC area resident….maybe. You know NOTHING about the political action there, other than from (unfortunately) fauX news. Believe me, I knew or met a lot of the REAL ones, and still know some of their offspring.

Some people forced to the bottom of a society ANYWHERE long enough often become “alternative entrepreneurs”…burglars, dope dealers, meth cookers, and such. Just be grateful you aren’t one, and hope all the goodies become spread around better here somehow, and they don’t get squashed any further.

For those interested, the major Australian banks use stronger language: “You MUST NOT store cash… ” etc etc in your SDB. They wouldn’t know of course what is in the SDB but the authorities can gain access any time they want. It’s all supposedly to do with AML/CTF. Who insures their SDB contents anyway?

Australia always seems to be ahead of the curve when crimping down on individual financial privacy.

Uncle Bob there is a quiet rumour that the guvmint has gone one better – they attach “something” to $100 notes that can be detected at a distance. Then they can drive around detecting who has got a pile of bigees hidden in the walls.

@fizee

If one really fears that the guvmint is putting funny stuff in banknotes, just put them (the banknotes I mean) in the microwave for a few seconds. That’ll make short shrift of anything electronic in them.

See, your problem is easily solved, Fizz.

You took it to right website.

Re putting currency in safe deposit boxes. I recall living in Geneva, Switzerland when the banking crisis hit and there was serious talk about banks such as UBS and Credit Suisse going bust or being nationalized when they were being scrutinized by the US Authorities. Some people pulled out all of their savings from the bank in cash (highest denomination in Swiss is 1000 CHF, ~1000 USD so a million is “only” 1000 bills fitting in a manila envelope and weighing less than 2 kilos) and putting them into safety deposit boxes. Reason was that boxes are private property and not bank property as opposed to a bank account where it was legally more uncertain to whom the money would belong after a potential default / nationalization.

The Swiss have a different approach to money in terms of gold and cash than entities such as the EU and the US. Cash and gold is highly values, reflected in their beautiful bills, small pieces of art in your hand, the practice of stashing away physical gold in big vaults is quite common and gifts of gold coins are often given for birthdays / christenings etc to kids. There was a story another UBS bank client who took out his whole physical gold savings (1 metric tonne!) and transferred it to another, private bank. UBS had to hire a whole convoy of security to pull this off but in the end delivered the gold.

Quite different from the world of freely minted, digital fiat currency around the world today and perhaps a lesson to be learned from the Swiss.

Similar to the UK in the late 90’s, the Swiss government sold off the lion’s share of their holdings of all that glitters for around $400 per oz just after the turn of the century.

They’re just another paper tiger…

The Swiss also regularly retire their currency, with full warning, after which it is valueless. I have a couple of beautiful 20 Franc notes worth nothing more than collector value.

1000 bills likely weigh 1000 grams, just under two pounds.

You can count US dollars with a scale and it is surprisingly accurate.

I meant just over 2 pounds, darn it.

Some years ago, an ETF was introduced that was holding physical cash. It was just a big safe somewhere with euro banknotes in it. But I cannot find it now. I wonder what has happened?

European banks now charge -0.5% or more on deposits above a certain limit and you are still losing your money (if above €100k) if the bank goes bust! So a physical cash ETF like that would be very interesting, provided they are properly audited etc. Should be cheap to run too. If they charge 0.1% or less, I guess many people will be interested. I certainly would be.

Btw: much better than a physical cash ETF would be a solution like Bullionvault or Goldmoney are doing for storing gold, but then for physical cash. You would be the legal owner of the banknotes, whatever happens.

Wolf, this Ain’t My Problem clause for safe deposit boxes is one reason I am heading a caravan of belligerent savers to Fargo, ND, this year. The Dakota Depository, securely run by some of my former business associates, is located very conveniently to Canada, still a country with fewer problems than the Banana States of America. Safe deposit box holdings are basically uninsured, and the armies of unemployed could be wearing vests by summer.

And I find it quite doubtful that the Bank will assume any liability for anything “of a collectable nature.”

I keep a bottle of Lagavulin on it’s side in my SDB, when I go to the bar, er bank.

It has been appreciating since prices went up on single malts, although i’ve been making withdrawals.

“Safe deposit boxes” are anything but. I will go bury my stuff on public land before I’d trust these fraudsters. The ONLY thing worth storing there is paperwork that is valueless to anybody but the owner.

Not sure why one would even want to have a safe deposit box in the US. There’s too many horror stories out there. One example: just google a story from the New York Times “Safe Deposit Boxes Aren’t Safe”.

A quote:

“There are no federal laws governing the boxes; no rules require banks to compensate customers if their property is stolen or destroyed.”

There’s a movie about the robbery of a vault with Safe deposit box at a major bank. “Italian Job” I think is the name. I guy drives up with a truck and smashed the vault and all the boxes are left on the floor opened up. After seeing that movie, I won’t leave more than a small emergency fund in them. A with dudes like Jamie Diamond saying he ain’t responsible for the contents, I’m done putting large amounts of cash in there. I’ll take my chances with the home invaders.

You are thinking too far. A bank employee can walk in and clean out your box and there would be nothing you can do. That’s the point of the article.

You are asking a fox to guard the henhouse.

You are thinking too far. A bank employee can walk in and clean out your box and there would be nothing you can do.

You are asking a fox to guard the henhouse when you put your stuff in a safe deposit box (in America that is).

@MB – correction, a bank employee can walk in and DRILL your safety deposit box. Sizeable charge for that too.

Lisa, it’s obvious you didn’t read the article.

“In the days after Mr. Poniz found his box empty, he began piecing together what had happened: Wells Fargo had apparently tried to evict another customer for not keeping up with payments, and bank employees had mistakenly removed his box instead. After drilling No. 105 open, the bank shipped its contents to a storage facility in North Carolina. After Mr. Poniz discovered the loss, Wells Fargo sent back everything it had in storage, but some items had vanished.”

Mr Poniz, the original customer, wasn’t charged. The bank made “a mistake”, but they weren’t liable.

I am not saying that there’s widespread fraud going on, not at all. But a couple of rogue employees can from time to time do this with no consequences.

That’s prudent thinking, if not contradictory to your babble above.

The real economy contracted after the last GFC. Distortions and displacements will continue shrinking the economy as this is the continuation of the GFC of a decade ago, it did not get corrected. If we don’t collapse due to this one another one then another one etc,etc will continue at shorter and shorter periods untill collapse . This is the natural end of geometric debt cycles that eventually have to fuel individual consumption plus financial assets due to non-productive consumption. When government starts handing out fiat to fuel non-productive consumption and keep assets inflated you can bet they are desperate. We are standing in a basement filled with gasoline. The spark is just a matter of a random event.

Yes, I have to agree with that.

It remains perplexing to me, to this very evening, why I never seem to end up in the fourth story solarium filled with gasoline, where I might just open a window, instead of always the basement.

Deadpool 2?

Lots of good information and interesting comments and suggestions re maintenance of wealth; however, it seems clear enough that if guv mint wants your wealth, they will get it no matter what strategy is employed.

Used to be that precious metals and good jewels were the most convenient and transportable, but, as mentioned, both can be taken fairly easily.

Read of one guy taking his wealth out of Europe long ago in form of gold sewed into his coat,, slipped and fell into the water while getting on the ship and went straight to the bottom and never seen again.

Most amusing attempt seen lately was when a house formerly owned by a big time booze smuggler during prohibition was remodeled, the new owners found bottles of rare booze built into the house!

At least that medium of wealth savings had some value no matter what happened, eh? (Though only for us imbibers!!)

Re: Jewels as a store of wealth

From lectures during a Gemology course a few years ago, the Professor revealed a few fascinating things:

– 99 % of all gems at typical retail jewelry shops are synthetic (via the drip feed method).

– For example, what is marketed as a ‘genuine emerald,’…yes…it has the exact chemical composition of an emerald but it’s a cheap synthetic mark up.

– Nature is not perfect and gives to each natural stone subtle impurities which can and should be mapped liked fingerprints for a valuable and true stone. Synthetics because of their purity lack this.

– Heirloom jewelry, your great grandmother’s for instance, is where there may be true value.

– Sometimes, with valuable jewelry, having the band resized or the settings repaired may lead to the stone(s) being ‘replaced’ unnoticed with synthetics by unreputables.

Mora,

Home jewelry shopping shows would hate it if that got around, but you may have saved a few folks that read this website.

Good and interesting info! That’s what we are all here for, no?

If it can sustain for last 10 years with no growth then it can sustain for few more decades.

Dr DOOM

[..]global earnings per share flat from 2008 levels. Put in a different way — not only are stocks divorced from the performance of the economy, they are even divorced from the profits of the companies they seemingly represent.

The incredible backdrop to the global stock-market rally — profits are flat since 2008

Marketwatch Jan 21’21

Why don’t we call the economy what it is a depression govt kicking can down the road in 2019 roughly 160 million working then we lose another say 20 million jobs when rent evictions start all hell will break loss

The eviction moratorium is great for the “Fake it till you make it” lifestyle! Btw, is there any recourse for a landlord to recover missed rents? I mean they stopped paying in May 2019. Clearly, this is not Pandemic related.

Wow! When I was getting my MBA we were taught that you diversify your portfolio in order to limit risk. But once you had 8 to 10 stocks there wasn’t much point anymore.

So a CMBS has 43 apartment buildings in it and it is at risk of default? Obviously the problem here is that they are all in a single market with a common threat. But it is still another example of “the weirdest economy ever.”

SpencerG

Just diversifying one’s portfolio without incorporating ‘uncorrelated’ assets will not shield from ravages of the bear mkts. Checkout 2000 and 2008 bears!

Looking at the numbers for the loan, it comes to $55K per unit, not a big amount anywhere in the US. The default looks like it can be entirely attributed to the economy collapsing.

If the economy can’t support apts mortgaged for $55K at under 3%. Look out below, the avalanche has started.

Biking around the middle+ hood within the surrounding busy streets, approximately 16 x 7 blocks, in St Pete this week Pet, I agree that things have changed quickly.

Just a couple of clearly overpriced houses a couple weeks ago; now several of the recently sold new and old back on the market after a year or so and many new for sale signs. Couple of old houses still in fixer upper stage, but going very slowly from what I can see.

Be interesting to watch this develop, as I have seen FL RE up and down several times since the mid 1950s when dad had no work for six months and we had to sell a nice small farm for a much smaller profit/price increase than it would have brought even a few months earlier.

Going to be a challenge for the Fed/guv mint to figure out what to do now, eh?

I live cash only a love watching everyone play a doomed game and panic! I saved and paid for everything. I owe nothing to anyone and could walk away from this S-show anytime. I warned everyone in 1987 the year 2024 should be a super depression and looks like I’m right. I live by several rules and everything has worked great! I don’t buy new cars or trucks. I pay cash or money order for everything and never used credit. yeah, no cell phone or cable but that’s fine. My taxes are extremely low. Currently I’m in stage two of a very long over due move over seas. BTW, I’ve never voted on paper but about to with my feet. I will enjoy watching the decline on TV.

What country are you going to, Randy?

for about two years the economy has been like that point in the old road runner cartoon where the coyote is suspended out over the canyon with his legs still moving but he has not begun his fall to the canyon floor. Now with these CMBS’s going bad it is like the roadrunner is stacking anvils on the coyotes head so that when he does fall he gets even more completely crushed on the canyon floor.

Further comments on the decline of home affordability in the US over time. The data is from US census data except the median 2019 home price, which comes from the Fed.

1960 median home price: $11,90

1960 median family income: $5,600

1960 20% down payment/median family income: 42.5%

1990 median home price: $79,100

1990 median family income: $29,943

1990 20% down payment/median family income: 52.8%

2019 median home price: $327,100

2019 median family income: $68,703

2019 20% down payment/median family income: 95.2%

Consider that a home is becoming less affordable for the average family, despite the increasing trend for two income earner families.

That’s what happens when you introduce credit to the system and allow almost everybody to qualify. It makes prices go bananas because assets are no longer worth what somebody can afford, but rather what they’ll agree to borrow.

Great point, DC. Same with student loans and the price of higher education.

Cheap debt drives up prices, for example homes, cars and education command a higher price because of the ability to finance. I like Charlie Munger’s saying that sometimes you have to invert the situation.

It’s not for everyone, but if you have cash you can get a good buy on a nearly new mobile home or an older car or used RV because bank financing is not available and cash buyers are rare.

“It’s not for everyone, but if you have cash you can get a good buy on a nearly new mobile home or an older car or used RV because bank financing is not available and cash buyers are rare.”

Not true. There is plentiful credit for all these items.

Random CMBS/CMBX things somewhat related to topic:

Fitch Assigns Final Ratings to 14 CMBS Risk Retention Pass Throughs

Mon 28 Dec, 2020

KEY RATING DRIVERS

Performance of Underlying Pools: Fitch reviewed each of the underlying transactions during 2020 and since the onset of the pandemic. The most recent rating actions resulted in the affirmation of 13 classes at ‘BBB-sf’ and one class at ‘BBBsf’. Six classes were assigned a Negative Outlook due mainly to higher proportions of specially serviced loans and uncertainty regarding the ongoing impacts of the pandemic….

RATING SENSITIVITIES

The Negative Outlooks on the E-RR classes in CD 2017-CD6, CSAIL 2018-CX11, CSAIL 2018-CX12, MSC 2017-H1, MSC 2018-H4 and WFCM 2017-C41 reflect the potential for further downgrades due to concerns surrounding the ultimate effects of the coronavirus pandemic and the performance concerns associated with the specially serviced loans. The Stable Outlooks on the remaining classes reflect the continued expected amortization and relatively stable performance of the majority of loans in their respective pools.

Misc crap from web:

Buyers for CMBS risk retention in 2017 were few, but enthusiastic

S&P Global Market Intelligence

For other traditional buyers of low-rated commercial real estate debt, though, risk-retention investments have held less appeal. Buyers must hold the risk-retention bonds for five years and cannot hedge or re-securitize the bonds. Investors who want more flexibility can opt, instead, to purchase low-rated debt from CMBS transactions in which sponsors held onto risk-retention slices themselves. In such deals, the low-rated, high-yield debt is freely tradable, without the requirement for a five-year hold.

Firms that bought B-pieces, as the lowest-rated portion of deals is commonly known, before the risk-retention rules went into effect have had to decide, under the new rules, whether to pursue risk-retention investments or maintain a focus on the tradable pieces from deals in which banks held the risk-retention obligation.

One factor is duration: While the risk-retention rules require a five-year hold, market participants say that in practice, selling risk-retention bonds after that period would be difficult. As a result, B-piece buyers have tended to approach risk-retention bonds as if they will have to hold them for their full 10-year lifespan.