It’s odd to see it occur while almost every market reports record home sales.

By Daniel Wong, Better Dwelling:

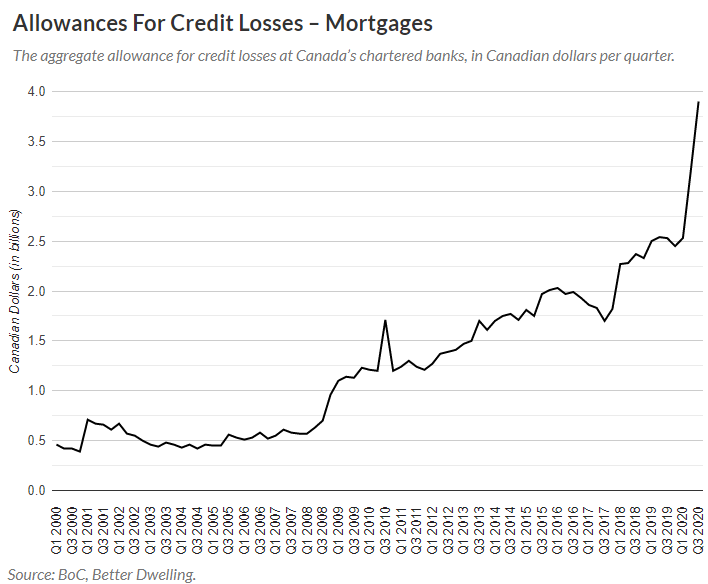

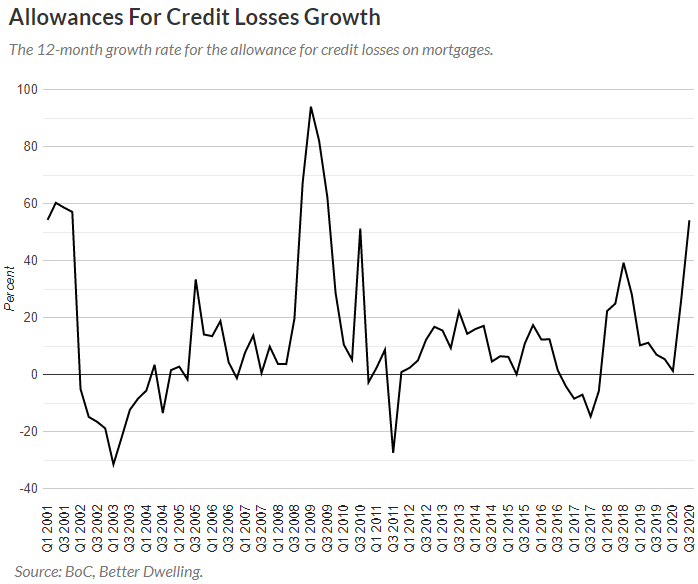

Canada’s real estate markets are booming, but lenders are preparing for mortgage losses. Bank of Canada (BoC) data shows the allowance for credit losses due to mortgages reached a record high in Q3 2020. The record was reached with the biggest surge in the annual rate of growth since the Great Recession.

Today’s data point is the allowance for credit losses, specifically for mortgages. You might have already guessed what this is – the amount banks set aside in the event of non-payment. When lenders expect a loan has become unrecoverable, they have to add more money to this pile. We’re going to be looking at the aggregate amount across all lenders.

The amount set aside for losses has climbed to a new record high, and is growing unusually fast. Allowances reached $3.9 billion in Q3 2020, up 22.01% from the previous quarter. This represents an increase of 54.11% when compared to the same quarter last year. It’s not just a record high for dollars, but also the highest rate of growth in over a decade.

Biggest Growth Loss Allowances Since Great Recession

Mortgage loss allowances at Canadian lenders grew at the fastest pace since the Great Recession. There’s been consistent growth since 2018, but the annual rate of growth has been tapering. That is, until the most recently reported quarters. Both Q2 and Q3 in 2020, showed a very large surge in growth. It was Q3’s annual growth that was the largest print since 2009 though.

Canadian mortgage lenders are preparing for record mortgage losses, but this is unusual. Large growth in this area historically occurs around market slow downs. Naturally, it’s odd to see it occur while almost every market reports record home sales. Seeing lenders prepare for a default event is great for lenders, who won’t be caught off guard. However, it’s generally bad for the borrowers that are showing signs of stress, instead of selling into a low inventory market. By Daniel Wong, Better Dwelling.

The US dollar lost purchasing power with regards to houses at the fastest rate in six years. Read… The Most Splendid Housing Bubbles in America: December Update on House Price Inflation Gone Wild

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The information below appears to conflict with the above article. Please advise.

Link: https://www.risk.net/risk-quantum/7719176/canadas-big-five-see-loan-loss-provisions-halve-in-q4

David Ribeiro,

We got apples and oranges here…

The article you linked is behind a paywall, so I cannot get all of it. But here is what is in the snippet that is before the paywall.

The article/snippet you linked is about total loans at the Big Five banks: commercial loans of all kinds, such as industrial loans, CRE loans including multifamily loans, office loans, mall loans, etc., plus consumer loans, such as credit cards and auto loans, and residential loans, such as mortgages. Mortgage loans are not detailed in the snippet.

This article here on WS is about residential mortgages only, many of which are now in forbearance.

The article here on WS is based on Bank of Canada data for ALL banks, not only the Big Five, and covers just one segment, namely residential mortgage loans. The quarter discussed is Q3, likely calendar year Q3 through Sep 30.

Canadian banks have fiscal years that end on Oct 31, so Q4 in the bank’s data goes through October 31.

The article you linked said that the Big Five banks added these amounts to their total loan loss provisions, all loans combined, by quarter:

Q2: C$10.1 billion

Q3: C$6.6 billion

Q4: C$3.2 billion

Over those three quarters, the five banks added C$19.6 billion to their total loan loss provisions. The snippet mentions nothing about mortgages.

The article on WS says that all banks in Canada combined added C$1.4 billion in loan loss provisions in the last three quarters, to reach C$3.9 billion in aggregate total.

Thanks for the clarification.

wait til 1% demand debtor prisons again

The housing markets in Canada are like bitcoin, pure speculation.

Canada sells residency to “investors” who are willing to overpay for houses(money laundering units), and are displacing Canadians. For the price of a one bedroom condo, the Canadian govt is selling out its country.

The housing market in the Maritime Provence’s of Nova Scotia, PEIsland and New Brunswick is not so great Population losses abound and lots of super deals if you don’t need to find a high paying job Taxes are high though as well as food and utilities

I think the banks know what’s coming not only to Canada but to many places On another subject new claims for unemployment were horrendous today 965k

Frederick, the housing markets in the Atlantic provinces are booming. Find some listings in Nova Scotia and look at their publicly available historical selling prices. One listing in Truro is $250k asking. Previous sale in 2008 was $119k and in 2006 was $90k. Another house in Halifax is $720k asking and sold for $250k in 2006. The only place in Canada where housing went negative is Alberta.

Not only is real estate booming in the maritime provinces, the covid death rate is about the lowest in north america. We all wear masks but no one is really afraid. Our death rate per population is a very small fraction of the Canadian average. I.E. Nova Scotia has had 65 total deaths and New Brunswick just 12.

Petunia, how do you know this, which you state so assuredly?

You cannot extrapolate Toronto and YVR markets to the rest of Canada. Seriously.

My son just bought a 2nd house. East coast Vancouver Island. Beautiful ocean view, (1 house/property distance from the beach) best part of town (45 k population). Good schools, shopping close by, sportsplex, bus transit every 1/2 hour, for $600K. He is renting out the upstairs to two ladies in their late 40s and they are happy with the rent he is charging. He dropped down $400 per month because they are simply sought after tenants. Their rent pays almost ALL of his mortgage and taxes, and he has a refurbished basement suite for himself while he is home for work on days off. They each have their own hydro and gas meters.

His finance rate is 1.4%

Will he fold and sell? Not likely. In my area I know of no foreclosures or tax sales, and building and RE sales are booming. Except for hospitality business, the economy is strong.

If this house was in Vancouver, just 80 air miles away or 2 hours drive and a ferry ride, the price would most likely be over 2 million. People do not have to live in Vancouver or Toronto except by choice. There is lots of opportunity elsewhere.

You cannot make blanket statements about the 2nd largest country in the World, absolutely diverse in geography from modified Mediterranean to the high arctic, from temperate rain forest coasts to open grass prarrie. It is like saying the SF and NYC markets are the US reality when they are not.

Canada is basically its major metro areas with a lot of space in between. Those metro areas are the ones that matter, where people work, not where they retire. House prices in Canada are obscene compared to wages. I could buy a really nice house in Palm Beach, FL for the cost of a crap shake in Vancouver.

I got interested in Canada when I moved to FL and saw all the Canadians living there. I thought all of them must be rich because they hardly work and take 6 months vacation a year.

“Canada is basically its major metro areas with a lot of space in between. Those metro areas are the ones that matter”

so canada will end up like the US, as soon as the sled dogs can drag the combatants within reach of one another?

The average Canadian is richer than the average American, hence the phenomenon of the snowbird wintering in Florida.

Paulo, the thought of Canada’s “modified” Mediterranean climate brought a broad smile to my lips and a chuckle.

Yes, Mediterranean rain forest…

Living in Nort Bay, Ontario. Toronto region is a completely different World in all aspects. Know it very well, after working there for 30 years. It is a personal choice where you are.

Although Chinese buying in a few areas no doubt juices the market, the vast majority of purchases are by Canadians. Canadians have a long history of RE obsession, developing and investing. Outfits like Brookfield are huge in the US.

And they get carried away: Cadillac Fairview went bust in NYC and the Reichmans went bust developing Canary Wharf in London’s old Dockyards.

But after the US 2008 crash individual Canadians swarmed into the US and mostly did very well.

To particulars: my niece and hubby just paid over a million for a small 100 yr old house on a 33 ft lot in Vancouver. But there are lots of Chinese in Van forcing up prices, right?

But there aren’t a lot in my town, Nanaimo, V. Isle which having been a bit of a backwater until five years ago, has been in a more violent uptick than Van for 3 years. Example: my house which we sold in August 2014 (sob) has now doubled.

Example: a very rough house which by coincidence I briefly owned decades ago, with no foundation on a 33 ft lot in a 3 out of 10 area just sold for 190K.

Example: a young couple with jobs but not careers recently paid 412 K for a 2 bed ranch on a 50 x 100 ft lot in a maybe 7 out of 10 area. I know what it costs to build one: they paid 300K for the lot.

What’s driving this: the lowest REAL interest rates in at least a century. One Brit banker has opined ‘in 5000 years’ The US ten year Treasury is at 1 %. That’s the cause of the finalization of RE.

In case anyone doesn’t know Nanaimo, this was the butt of jokes in Canada. It really isn’t a city in that it has no functioning downtown. Only the setting is nice, on a bay in the calm, inside arm of the ocean.

There is a several- thousand year old tradition of blaming outsiders or minorities for anything that goes wrong. But the greatest RE mania in modern history the Great Florida Land Boom and Bust can’t be attributed to anyone but Americans. Every one likes the idea of winning the lottery, including Caucasian Canadians. And via RE, they’ve bought a lot of tickets.

Canadians would have no obsession with real estate whatsoever but they know the Chinese will push real estate values up 30 percent a year every year until doomsday thus Canadians believe they can always sell to a Chinese buyer for huge profits.

It’s not just areas of Canada. Also parts of US, Australia, England, Hong Kong, Singapore etc. No one knows the extent of it as no one keeps close track. But it definitely has had a domino effect.

Also, no one knows the length of time that some of these “investments” are kept empty and off the market compared to how it was two decades ago.

Ground report from San Diego: Lots of Chinese buying homes here.

Canada’s GDP and unemployment numbers are all fake! Without 500 billion in gvt programs(funded by QEing and new debt)Canada’s GDP would be 50% of what it was before the Wuhan flu hitting and unemployment around 40%!

50 billion has gone to companies to pay their employees up to $875 per week via the CEWS Program so they won’t be laid off! If this gvt debt and QEing binge is halted down the tubes goes Canada’s economy and HOUSING market!

Petunia.

Yes. And Canadian Charities don’t have to disclose donors, foreign or domestic. Canada pretends to be clean, but smells like foot fungus.

K

Oh wow! an extra 1.5 billion this qtr. among 10 lenders. the sky is falling!

Meanwhile take a look at the Bank of Canada Balance Sheet and you’ll see how the BoC is gifting billions of free $$$ through its REPOs(160 billion at .20%) to buy bonds yielding a much higher rate or whatever and the interest on its Payments Canada Account(excessive reserves) of .25% on 300 billion sitting on its books.

The private banks are minting $$$ thanks to the gifts from the Crown Corporation, a taxpayer owned entity.

Wolf, checkout how Blackrock has weaseled itself into the BoC as the paid consultant on what Commercial Bonds the BoC should buy. No conflict of interest here!!! too funny. Of course, this is total conflict of interest and illegal under BoC governing rules! Now the BoC has become the ATM for banks and international financiers and hedge funds!

I would also guarantee these loan loss provisions are in the CMBS market. as housing has ripped higher across the country(though some condo markets are only slightly higher or flat) so anyone who needs to sell can dump their house for a profit.

I have been following betterdwelling for a while now and am glad to see that it’s wolfstreet approved

How does this reflect on the American Market? I don’t know, I’m just asking.

IMO, they’re almost completely disconnected. The only thing that I noticed is that the Canadian bank follows/trails the Fed almost all of the time. So if mortgage rates are low in the US, they’ll also be low in Canada.

When we had our housing collapse ten years ago, that didn’t happen in Canada.

Canada had their housing collapse 89-98

It affects markets in the US where Canadians vacation, like south FL. If the Canadians with vacation properties in the US need money, they sell their US properties. If they have extra money to spend, they might buy in the US.

If they want to exploit C$ US$ spreads they might do it in the real estate market. Right now is a good time for Canadians to sell US property, US$ is high and so are US prices.

I read this on the BBC last week: “UK house price growth 6.5% in 2020”. House price GROWTH! As if something is growing. You are just paying more for the same f*cking house! But “growth” sounds nice and positive of course.

This is how inflation is spun in the mass media and nobody ever calls them out on this. Sorry guys, you just have to go 6.5% further into debt to buy the same f*cking house!

In the news today in The Netherlands: price rise of average house increased by 11.2% in 2020. In some regions it’s 20%. But the ECB keeps interest rates negative because “inflation is too low”.

No , they keep interest rates low because raising them would blow everything up. The bad news is that will happen anyway through hyperinflation GOT GOLD?

Blow everything up. We have that happen now can we? After there’s no inflation. Anywhere. No one can see any, not at all. On that note already seeing headlines that Fed tapering anytime in the next million years would be worstest thing ever.

Food inflation has been bad for the last 5 years and only now are they talking about it. I just came from the supermarket and there is not a can of Spam on the shelf. They didn’t have any last week either. This must be the new hot item.

Spam is great! Lots of creative ways to cook it. Spam goes back a long way. I think Spam is a big seller in Hawaii.

spam, spam, spam, eggs, spam with spam

Actually I think the UK is rather tame compared to other markets (e.g. New Zealand/Netherlands). Roughly 2-3% of that rise is just inflation. Another 2-3% is due to the temporary stamp duty cut (buyers give stamp duty money to vendor instead of govt, this shows up in sale prices). So there might be about 1-2% actual rises in there, but this may just be a result of the flight of high income Londoners to cheaper areas, while the London market appears to be jammed up with a LOT of properties on the market and not getting sold (in the areas I look anyway).

The UK pretty much killed off housing speculation back in 2014 when it announced extra stamp duty on second homes, loss of interest deductibility, and new annual taxes on properties owned through ‘offshore’ structures. UK also has very strict debt to income ratios, so the interest rate cuts didn’t really have much effect on affordability.

Those insane HGTV flip shows where a run down crack shacks sells for $900,000 CD are usually filmed in Toronto.

Why wouldn’t they make large provisions for credit losses? Covid gave every company an excuse for reduced earnings. If the losses never materialize, the banks will reduce provisions and report better than expected profits in the future. For the banks, the result is either neutral or positive for the stock price.

I wonder if this was dictated by the actuary bank insurance people probability projections ie if bank loan insurance rates have risen? Inflation hits all the services that don’t supply anything concrete, except data.

Real Estate is local. There is Vancouver (off the chart prices and some of the lowest wages in Canada). The there is Calgary (low housing prices and some of the highest wages in Canada). Then there is Toronto – fueled by immigration and some speculation. The MB, Sask and Atlantic are growing but not too much and still affordable. QC is distinct :-). You can’t paint the entire country with the same brush. Very different local markets with unique risks and opportunities. .

Broadly similar dynamics, though Canada has been huffing the housing bubble paint fumes longer and more deeply.

Early on in C19, the big US banks set aside large reserves for losses as well (on all sorts of loans) and their earnings took a hit as a result.

Now we are in a phase (because accrued losses really haven’t hit yet) where some institutions are kidding themselves that C19 (thanks to DC debt orgy squared) will turn out to be “stimulative”.

This is probably the most massive example ever of market players deluding themselves that a real asset disaster (hundreds of thousands apparently killed, tens of millions having work life massively disrupted for a yr) can somehow be magically “fixed” because a collection of schmoes in DC print a mountain of green pieces of paper.

At best, DC’s actions marginally shift *attitudes* toward disaster…but they don’t undo the ultimate physical consequences of it.

For instance…what ultimately happens to the housing of the hundreds of thousands who have died?

It will hit the mkt…lowering prices in a highly overpriced, highly levered market.

What happens with huge overhang of apt rent in arrears?

“It’s like deja vu all over again.”

OR “The future ain’t what it used to be.”

Kudos to Yogi – “You’ve got to be very careful if you don’t know where you are going, because you might not get there.” – Berra unique wisdom(s).

Love the quote from Yogi Berra sam, and please continue to bring your wit and wisdom to share with us on here…

Had his rookie card, along with MM’s,,, unfortunately, as i have understood happened often, mom threw out my bag of cards when i went into Navy, which she did not like, wanting me to go into air force…

Berra really did have some of what my dad called, ”native” wisdom, for sure,,, as did many of the players and managers in those days.

it is your duty to remind your mother of her choice (tactical vs. strategic outcome) –

Btw there’s a reason why the Air Force is known as the “chair-force”.

My tour enlightened a MUCH younger version of myself of how biz/gov’t world thrives off overeducated/underqualified/ replaceable seat warmers who’s leadership quality(s) are espoused via flagrant a## kissing & (verbal) fellatio.

Senor Wolf, I apologize for the graphic metaphors…you run a high class forum and i intend no disrespect nor degradation.

Lots of hype, in the form of jawboning about treasury yields exploding, but I don’t see that playing out in USA or Canada.

Nonetheless, the Fed is playing with the yield curve and duration experiments that apparently are aimed at liquidity — does that impact loan loss stuff, sorry, but that’s above my pay grade. That’s something for an astrology expert to divine (or someone on this thread).

Powell: ” So we, we remain open to doing—you know, to, to either increasing the size of our asset purchases, if that turns out to be appropriate, or to just moving the maturities, moving to buying longer maturities, because that had—that also increases accommodation by taking more duration risk out of the market”

However, back to possible interest rates and the next housing boom, I remain loyal to Ed Yardini’s Treasury futures research which uses the 2-year Treasury as a proxy for where the 10 year will be a year from now. Hence, I see no possible path forward for rates to explode — through the process of Fed jawboning.

Furthermore, I can’t understand why the Fed would actively attack the housing market during this expanded pandemic period, and the same goes for our brothers and sisters in Canada — the central banks want liquidity and flowing markets and they will sustain that process for years.

I think it’s wise for Canada and America to demand higher loan loss limits and go back to Dodd Frank risk management, versus opening up the doors to bank chaos.

The jawboning of rates is a weird thing, the other day I was looking at FRED:

10-Year Treasury Inflation-Indexed Security, Constant Maturity (DFII10)

I was also looking at the widely distributed:

10-Year Treasury Constant Maturity Minus 2-Year Treasury Constant Maturity (T10Y2Y)

The spread there is accelerating, but it’s also offset by the lack of real inflation found in DFII10, so, in order for that spread to be meaningful, I think it’s worth looking at disinflation dynamics and stuff like treasury futures.

I’ll check my astrologist’s page on Gab and fine tune this later …

Martha Careful

With the ongoing/coming tsunami of B117 strain Covid, all over, the global economy is stuck. crawling close to the bottom. One has to modify/invent an economy, that will co-exist with the in years to come.

Forget about vacinations’ it’s effiency/efficacy, we cannot even provide needed tests kits for the virus. Distribution models are in shambles.

Will CBers providing plenty of liquidity, will solve the impending INSOLVENCY through out the Economy?Of course top 10% are exempted.

For each DEBT there is a LENDER on the otherside. Lenders have financial obligation too! There are also ‘cash’ stream recievers – pension funds, hedge funds, Mutual funds, Sovereign funds and institutional and retail investors! Wonder who will be holding the bag?

RISK won’t disappear but transferred to another willing or non-willing party! The nightmare scenerio is when there is lack of or NO BID altogether. It has happened during FLASH crash in the past, atleast for a couple of minutes!

(Been in the mkt since ’82 and witnessing the most surreal bull mkt of my life time!)

I’ve heard their counterpart housing lenders in USA are doing the same— preparing for a coming landslide of foreclosures and defaults.

But they apparently have not been publicizing it much outside their industry insider talk.

70% of US mortgage loans are Government backed. Do those loans have to be backstopped by anything other than Freddie Fannie, VA, FHA etc?

Sure, these federal agencies are final backstop when these mortgages will go bad. If I am correct, then any mortgage security losses will be made whole by such a federal guarantee. Private mortgages do not have such protections.

When deadbeat mortgage borrowers are finally foreclosed on, I think it is the lending institutions, not the FHA, VA, or whaterver, that take over the properties and have to dispose of them at whatever price the market will pay. Even at a tremendous ‘paper’ loss.

Hence, they are preparing for that eventuality.

This “record” amount set aside is peanuts for the banking cartel in Canada.

Unless oil prices go north and the USD dollar keeps dropping, besides water, there is nothing holding up Canada as a whole.

Oh yeah, get a gov’t job is like winning the lottery here.

The Canadian Railways are busy, shipping millions of tons of coal to Japan, South Korea and China.

And bringing in “Ships from Canada” containers of Chinese trickery.

I can’t believe some of the comments… like we can’t see interest rates going up or we are in a boom…. Remember, the road to the gingerbread house was full of sweeties, that is, until the kids found themselves in the cooking pot….also.. A fool and their confidence is rarely parted….

Sooooo….

1) RE prices are through the roof.

2) Loan to Value (LTV) thus gets better for the Lenders every passing month.

THRREFORE …

3) Banks need to prepare to write off losses, presumably due to foreclosures??

Sorry….the “dense-meter” just overtook my brain. If prices were stagnant / dropping and Foreclosure Moratoriums were forecasting future foreclosures, I can see Lender losses coming, but the loan collateral shows no signs of jeopardizing loan balance recovery, even if there is a 10-20% downturn.

During the GFC, housing price median) towards 30-34% according Schiller index.

The landscape of post(?) Covid is entirely and dramatically different. there will be creative extend & pretend. But Liquidity cannot solve INSOLVENCY in the long rum!