Depicted by my 13 whiplash-charts.

By Wolf Richter for WOLF STREET.

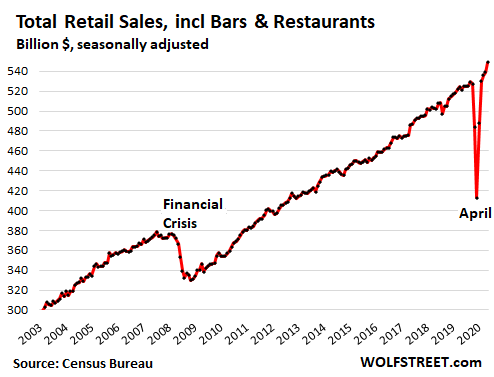

Total retail sales – sales of goods in stores and online, but not including services such as doctor’s visits, insurance, airline tickets, hotel bookings, rent, etc. – in September jumped by 1.9% from August, to a record of $549 billion (seasonally adjusted), according to the Census Bureau. Compared to September 2019, retail sales were up 5.4%.

But as we’ll see in a moment, there were huge differences between categories, from sales at clothing stores and restaurants which, though they bounced a lot, were still below where they’d been years ago; to sales at stores for building materials and garden supplies, which jumped from record to record during the crisis:

The stimulus money & things consumers no longer pay for.

There were a lot of things consumers didn’t do, such as flying – passenger traffic in the US was down 65% from a year ago – staying at hotels, going to the movies, and the like. And the money not-spent on these services got spent on other stuff. About 7% of households with a home mortgage got their mortgage moved into forbearance, and they no longer have to make mortgage payments for the forbearance period, and that money of those not-made mortgage payments got spent elsewhere. And some renters, protected by eviction bans, have stopped making rental payments and spent the money on other stuff.

Then there were the stimulus payments, starting in April, some of which are still going out to people the IRS had trouble locating. And the extra $600 a week in unemployment benefits, and the federal program for gig workers (PUA) that states had trouble processing, were sent out often way behind and in lump-sums.

The extra $600 a week was replaced in August by the extra $300 a week, which states started sending out in late August and September, also in lump-sums. In California, the first lump-sum payments of $900, covering three weeks, were sent out in early September, and more was sent later in September. After six weeks of payments in California, the federal funds have been exhausted, and those final payments are now going out, according to the California Employment Development Division.

Then there were all the folks that fraudulently obtained unemployment coverage, under one or several programs, and that money too got spent.

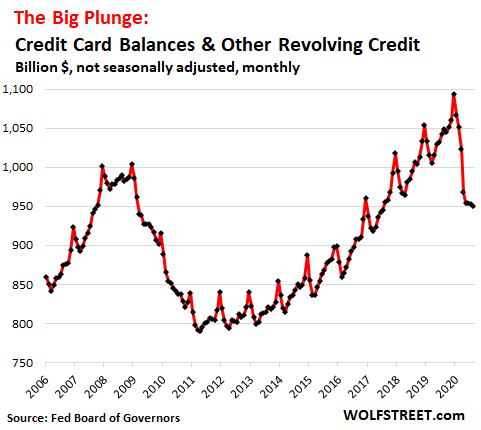

But not all these funds got spent. Some of them went to paying down credit-card debts, including the biggest plunge on record in April when the stimulus checks arrived. By the end of August, credit card balances had dropped 7% from March. Consumers who’d used their stimulus money to pay down credit cards have some room to spend more later. The paydown of credit cards essentially came to a halt in June, July, and August with the slowdown of the stimulus and extra unemployment money:

Retail sales by category.

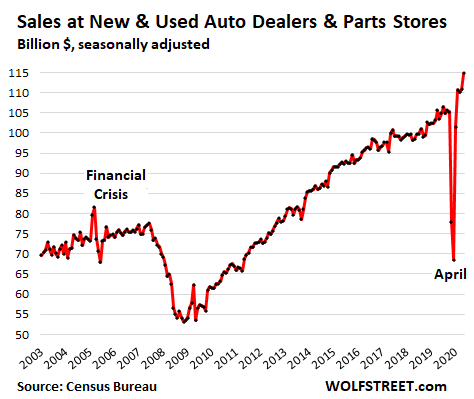

Sales at new & used auto dealers and parts stores jumped 3.6% in September from August, to $115 billion (seasonally adjusted), and was up 8.2% from September last year.

This was powered by historic price spikes of used vehicles of 6.7% in September from August, and of 15.1% over the past three months. But used vehicle retail volume, measured in the number of vehicles sold, in September was still below last year. People bought fewer used vehicles but paid more for them.

The average transaction price of new vehicles has also risen, under the dual impact of consumers buying higher-priced vehicles, particularly high-end trucks, and price increases of new vehicles. Total new vehicle sales, including fleet sales, in September were still down about 4.3% from a year ago. But retail sales were stronger year-over-year.

Sales at auto dealers and parts stores form the largest retail category, accounting for 21% of total retail sales:

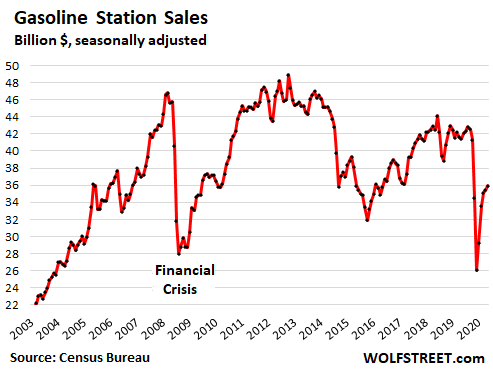

Sales at gas stations – include junk food, soda, beer, motor oil, and the like – rose 1.5% in September from August, to $35.9 billion (seasonally adjusted). Sales are impacted by the volatile gasoline prices. According to the EIA, the average gasoline price in September was down 15% from September last year, the opposite direction that used-vehicle prices took. And so, compared to September last year, sales at gasoline stations were down 13.3%:

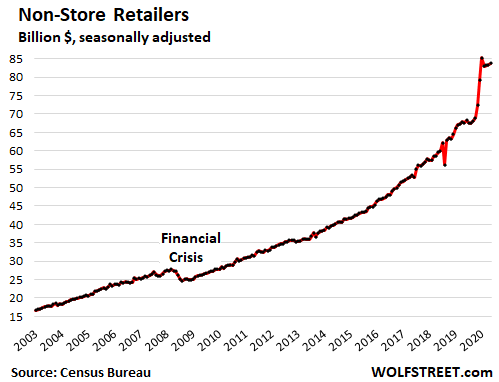

Sales at ecommerce sites and other “Non-Store Retailers” (mail-order operations, stalls, vending machines, etc.) edged up 0.5% from August, to $83.8 billion, the second highest ever, and up by 23.8% from September last year, after the huge spike during the lockdown. Despite speculations that ecommerce sales would drop sharply after brick-and-mortar stores reopened, this is not what happened:

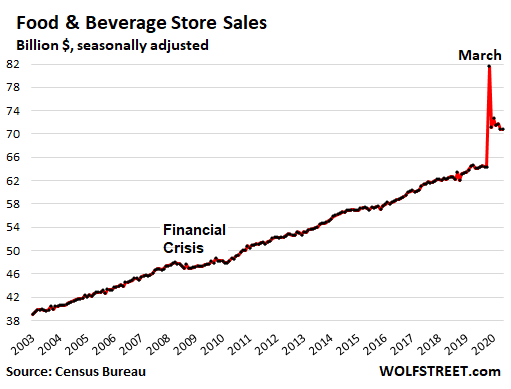

Sales at Food and Beverage Stores were flat in September compared to August, at $70.8 billion, but were still up 10.5% from a year ago, as work-at-home and study-at-home consumers are still buying for the home what they used to consume at work or at school, with spending shifting from commercial suppliers to retail channels. Nevertheless, a good part of the March spike has now been unwound:

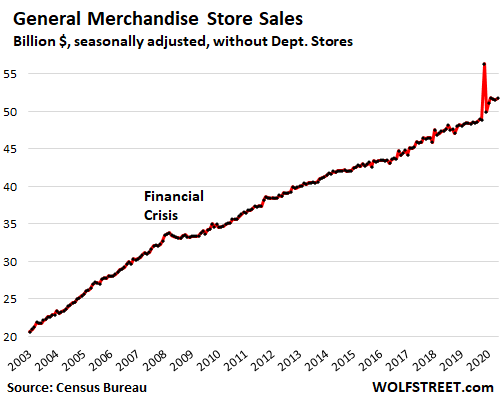

Sales at general merchandise stores (minus department stores) have essentially been unchanged for the past four months, at $51.7 billion, up 7.0% from a year ago, having unwound most of the 15% spike in March. Walmart and Costco dominate this category:

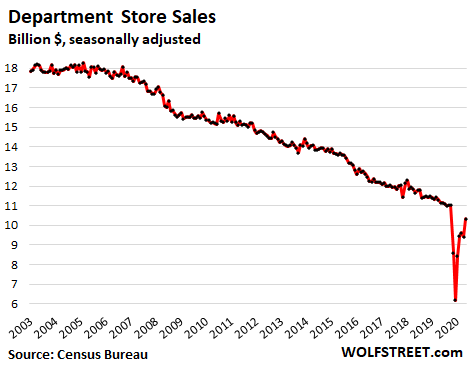

Sales at department stores jumped 9.7% in September from August, to $10.3 billion, likely boosted by liquidation sales at stores scheduled to be shuttered by numerous chains, those that filed for bankruptcy in prior months and those that are trying to avoid a bankruptcy filing by shedding stores. This does not include ecommerce sales of department store brands, just sales at brick-and-mortar stores. Year-over-year, sales are down 7.3%:

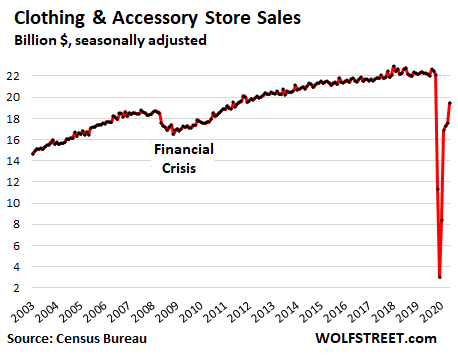

Sales at clothing and accessory stores jumped 11% in September from August, to $19.5 billion, but that was still down 12.5% year-over-year. For the two years before the Pandemic, there has been no growth at clothing stores as people were discovering how easy it is to buy clothes on line. In September, despite the big bounce and all the stimulus payments, sales at these brick-and-mortar clothing stores were back where they’d been in September 2011:

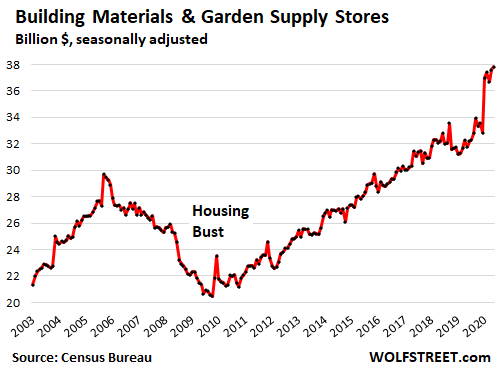

Sales at building materials, garden supply and equipment stores edged up 0.6% in September from August, and eked out a new record of $37.8 billion, up 19% from a year ago. In essence, after the blistering spike in March through May, sales have remained in the same high range.

Stores in this category include big-box stores, such as Home Depot, neighborhood hardware stores, specialized garden supply stores, etc., all supplying the new-found passion for improving the home, the backyard, and the deck, with some folks growing vegetables, fruit, and herbs at home, now that people are spending more time there, including during their adventurous staycation over the summer:

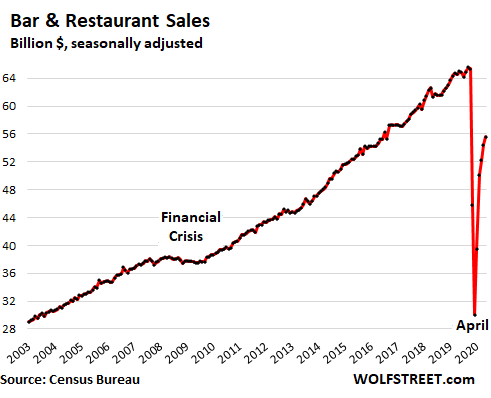

Sales at Restaurants & Bars rose 2.1% in September from August, to $55.6 billion, but were still 7.0% lower than a year ago. This includes fast-food places and drive-throughs, many of which never shut down, along with sit-down restaurants. In most cities, even indoor dining is now available, albeit with capacity restrictions. Indoor bars remain under tighter restrictions in many cities.

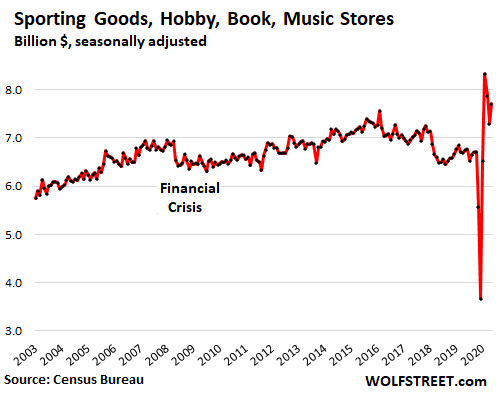

Sales at sporting goods, hobby, book and music stores jumped 5.7% in September from August, to $7.7 billion, but not enough to undo the big drops in the prior two months. Year-over-year, sales rose 14.4%:

Sales at furniture and home furnishing stores edged up a smidgen in September and thereby eked out a new record, $10.4 billion, up 4.6% from a year ago, as people, now spending more time at home, noticed that worn-out couch, or added some nice touches, or created study-at-home and work-at-home environments:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Best depression ever. I call for Covid 20 later this year. It’s like the Anti Virus companies. You know that there’s a bunch of people in the basement furiously creating new computer viruses so that AV companies can sell more and more license.

We are finally winning. Thanks China!!!

Other way around. China says, Thanks USA! Because many of these goods or their components were made in China.

With this stimulus, the US stimulates the big exporters around the world — but also globalized Corporate America, such as Walmart and Amazon. The value of imports is a negative in the GDP formula, meaning it’s deducted from GDP. So boosting imports is not the best way to boost the economy :-]

Exports are positive in the GDP formula, but nothing in the US stimulus boosts US exports.

Well US companies like the ones in the ecommerce space are winning.

That has to count for something. Amazon will probably soon become the government. That’s some serious winning. Is there even another company in the world as powerful as Amazon now? Alibaba might do a greater amount of business but they can be shutdown overnight by the CCP.

And of course the stock market will continue to skyrocket. Increasing deficit -< increasing stock market.

Berkshire probably is still a contender. Revenue of operating companies is a little lower but operating income is higher plus there is a huge investment portfolio. Market cap of Amazon might not should be 2.5 X BRK in my opinion, but that’s why it’s a market

Amazon has exactly zero power, like it never existed. In my perspective at least.

Why would they do that?

Yes buuuutt …. Trump negotiated the purchase by the Chinese of more corn and soybeans as part of Phase 1 trade deal ….

Container shipments from China to West Coast are heating up, empty containers are usually backloaded with ag products, which takes about a week and a trip to the midwest, but the sellers want them back immediately. To fill their orders China buys more ag from BRICs.

Back in 1889, a family seed farm was founded near Foxhome Minnesota. This is where my dad and I had our main wheat nursery and production, but it’s now branched out into supplying non-GMO and organically grown soy products to China, Taiwan, Vietnam and Hong Kong.

There is demand from the other side of the Pacific, as well in North America, for non-GMO food grade soybeans. These are grown under contract by farmers in the region, inspected during growth & before harvest, cleaned and packaged before being sold to the customers overseas. In 2019, over 800,000 bushels of soy was sold from Foxhome to the above four nations. I hope they surpass that this year!

China bought just under $8 billion of soybeans from the USA in 2019, and Minnesota exported over $7 billion in agricultural products last year.

Few understand that when you shop for goods made outside of America, you transfer wealth outside of America. America gets poorer, yet the stock equity owners get more wealthy. In terms of equity ownership, depending on the U.S. market, anywhere from 13% to around 35% of U.S. financial markets are owned by foreign entities. At the very least, the fed policy of “stock market inequality makes minimum wage job equality” is losing 20% of it’s “Make the Wealthy Wealthy Again” firepower to foreign interests. Not sure how this aligns with national security, etc. Imagine if the Fed just sent a $600 billion check direct to foreign governments (20% of $3trillion stock market liquidity injection). So we now have a Fed pumping up the wealth of countries that might dominate us in the future, in no small part to all the Fed “free money” policy. Printer go “Brrrrrrr”, or is that the chill down my spine? The irony…

I have tried to only spend on american made products and services. My big splurge today was that I rolled the dice and changed out all the glow plugs on my 27 year diesel Mercedes even though only one went bad. This can be risky as the tend to get stuck and break off at this age requiring the removal of the head and big repair bill. I figured if they all came out I would keep the car another 5 or more years years and give it the minor repairs it needs, and if not sell it for parts. My gamble paid off and they came out clean and since my mechanic says I have another 150,000 miles left in the engine I can drive it till the end of the petroleum age.

Apparel including footware is 19% of Chinese imports to the US. This raises US living standards. Sewing panels is not something Americans want to do, or should do. There are more productive uses of their time.

The big import from China is consumer electronics at 27%. The US was out before China was in. Last US TV Zenith 1995.

US taken out by Japan. Now Japan out with Toshiba out. Only Sony with giant screen left.

In the $169, 32 inch there is about 10$ profit.

This is not a business to chase.

Americans have this fantasy that their problems are inflicted by foreigners.

Actually they are largely self- inflicted

How does a billionaire pay $750 in 2019 taxes?

So we print up some dollars and send them to China and they give us a flat screen tv in return.

How does that make the US poorer? We have a tv and China has some paper.

The biggest export product of the US is the dollar. Costs almost nothing to produce and buys a lot of stuff. made by foreigners. What better deal do you want as a country. Now, as someone looking for a job, you hold the short end of the stick. But you can buy cheep stuff with your stimulus money, created out of nothing and gotten for free. The FED sending $600 billion to foreign governments is only to ensure the dollar will not become in short supply and gets more expensive. A dollar would buy more that way, but also those foreigners might go looking for something else to trade with than dollars. When that happens and it sticks to stay, all those who hold $$$ are scr*w*d.

Thats the catch22 the US, or actually the FED-dollar, is in. The trick is to find the amount of dollars needed to keep everybody addicted enough without killing the junkies.

At this moment it looks like the junkies are starting to look for another drug or even, may heaven forbid, go cold turkey and become sober again.

“How does a billionaire pay $750 in 2019 taxes?”

Does that include the hundreds of millions in tax credits used to pay the current tax bill?

No, I didn’t think so.

Your grade in Tax Accounting class for the Semester is an “F”.

@Suzie Alcatrez

“…How does that make the US poorer?…”

At the end of the day, these dollars will find their way back home to the US to buy things. There, these dollars are valid currency to exchange for valuable land, real estate, companies and whatnot.

So, what it comes down to at that moment, is that the US will have traded its prized possessions for a pile of flat screen TV’s.

Not my idea of a good deal.

Suzie Alcatraz…

We get the wasting asset, the flat screen.

They get the “paper”, but come to the US with that paper and buy hard assets, like resorts, our largest pork processor, grain elevators, etc.

See their game?

Yes, Yort, it’s extremely serious now on material goods, are we past the point of no return? I’m afraid China has won in the industrial sector. If you produce nothing, eventually you are nothing.

Instead of promoting human rights by our government, for instance through the Trans-Pacific Partnership trade deal, bringing up the standards of the world for labor, corporate USA had their way with demanding the lowest costs possible from foreign labor. Consumers in the USA have no idea the conditions in which the ignored laborers of the world live.

Now, we’re left with a Communist industral powerhouse and the living standards of most people forever greatly diminished, including the U.S.

In Illinois a billionaire can have his wife arrange to remove the toilets for a day, reclassify the mansion, and save $300,000 on the local property tax bill.

Suzie,

We lose our manufacturing knowledge and capabilities, which has huge value. It is NOT an even trade.

If I offer you cocaine for money, that also has the appearance of a fair trade for you.

Re: tax records. The examination has just begun despite being fought all the way to the Supreme Court ( why?)

Stay tuned for a lot more daylight. As the subject says: ‘We’ll see’.

True.

The US is a service economy. How long can the US buy foreign made goods ad nauseam while they actually produce little? This is possible because it is an advantage of having the dollar as the reserve currency but be forewarned it is only temporary. Foreign countries who make our stuff and sell it to us will soon realize as they watch the US printing trillions of dollars that the dollars they hold in treasuries will lose value and they will sell their dollars.

Who will buy these treasuries? What person would buy something that will lose value? Less and less will and soon the Fed will turn from being the buyer of last resort to the buyer of only resort.

And this is when the game gets interesting because the more treasuries the fed buys the more purchasing power people holding the dollar lose. So they will sell and the fed will buy. The death spiral cycle continues until hyperinflation. That’s when you’ll use dollars for wallpaper. Pensions. 401ks. Poof.

Is this doom and gloom? Just watch the DXY the next few years to see if the prophesy is truth or fiction.

@John Galt

‘it is an advantage of having the dollar as the reserve currency but be forewarned it is only temporary’

Why temporary? TINA!

There are three Trillions loans issued in US $, outside America. They need $$ to service their dents!

US $ is the trading and global currency for the global commerce, including petro dollars. US $ – 61%, Euro 20-30% Yen 12 % YUAN just 2%.

Russian Rubel got devalued 20% against US $, last week!

US $ is the greatest export to the World. It is the least dirty ‘shirt’ every hates but want it very badly!

I don’t have first hand experience, but have read multiple stories that people have prioritized credit cards payments and utilities over rent because of the rent amnesty and eviction pause that exist in many jurisdictions. This has likely contributed to the decline in the credit card debt, but I find it hard to believe that this is good for anyone. Who know what will happen to their credit card lifelines once their rent comes due.

If people are on the edge, I think prioritizing credit card and utilities over rent temporarily is a good idea. Credit card rates (especially for the poor) are sheer extortion. And frankly if you can’t keep up with utilities, children can be taken away from the home. Getting out from under credit debt might give some extra space for later — to actually get ahead and out from under the interest rates. And you’ve got to have utilities and food to keep your family.

I don’t know if people are truly recklessly spending rather than paying the rent. It’s possible. When nobody is being responsible with money, the poor can’t be held to higher standards, especially when NO practical money management skills are taught (and in fact are actively not taught).

It’s easy to lump everyone together. I suspect some people are being very wise, and some people are being very foolish. Naturally.

I don’t have a real feel for what’s happening to people. I wish I did. I will say, though, the housing market here, which has been soaring up and up, has started to see a sudden influx of poor people houses hitting the market (row homes in the city in unsafe areas, trailers w/ no land), and the prices are being lowered in some cases, rather quickly, even if not by much.

It feels like the beginning of the hard times have hit for some people, that have had to find new houses quickly. Although I’m sure some of these (especially unlivable properties) have been “investment” properties people are trying to unload before any downturn hits real estate.

Real Estate in generally has been rather price-gougey here IMO, and I’m not sure why. But these two markets have seen changes in recent weeks.

(I should add, poor people might not be finding new housing. They might be moving into vehicles. This was happening to some people even before all of this.)

I still really don’t understand the housing prices. Zillow is finally admitting my house MIGHT not be worth twice what I paid for it in 2016, but it seems like a reluctant admission.

A, there are now organizations in California that provide secure lots for people with cars to park and sleep in safety (YouTube video produced by Deutsche Welle).

Recently I read a story about a family in Arkansas whose trailer house burned down. The local welfare office gave them a tent. That’s it. There are also stories about families that split up with Mom & Dad sleeping in their car while kids bunk with friends/relatives.

So yes, poor people are not finding new housing. This is a fifty-foot tsunami about to hit US, while Dear Leaders of all stripes act like everything’s fine, move along, and most important, avert one’s eyes from the growing misery.

A study from UCLA/USC found if people were *able* to pay rent, they paid. So people aren’t just skipping out of rent because they won’t be evicted. That said, I imagine the people that had pay cuts & can’t pay their rent (which had been a gigantic portion of their paychecks) might also spend their new extra money on other debts & retail purchases.

Oh & the CDC eviction moratorium is based off renters’ inability to pay due to Covid, which has to be proven via a form provided by the property owner. So, if renters are still working & can pay rent but just aren’t, landlords can still evict them. Well, assuming the state hadn’t already enacted stronger tenant protections.

Another Scott,

They won’t pay back rent, so that’s a non issue for them. They’ll just move to another apartment/house/city. In places like NYC and others the courts will be backed up for years from all the delinquent tenants. In NYC it might take awhile (months at the minimum) to evict tenants even after the pandemic ends. If a tenant simply moves out after pandemic ends without a fuss, the landlords, especially smaller ones, probably won’t even file anything against them. So most of the NYC delinquent tenants will get off Scott free. Most of the non payers, could pay (once the unemployment came in), but choose not to. NYC is obviously, the extreme case, but, to a smaller extent similar cases will play out everywhere.

Curious where you got the data for “most non-paying renters could pay rent”? That’s not what I’m seeing. In fact, UCLA/USC came out with opposing data. Keep in mind that rent was already a burden for a gigantic portion of residents in big cities. It would take just a small dip in income for a family to be forced to choose between rent or food.

At the very beginning of lockdown, before the extra money was given out, many/most couldn’t pay, but, after that most could. I know in my local area, they definitely could (after unemployment kicked in). From hearing and seeing many landlords deal with many tenants, I can pretty easily spot when they are BullSh’ing on tv and online. I would be very cautious of polls, even if anonymous, where the tenants answer. NYC specifically (and maybe parts of California) have rents so high, that I could imagine there would be some people, who still couldn’t pay after unemployment, but, I doubt it’s the majority. The main legitimate issue was how long unemployment took to be given out.

It’s also important to note, that especially in NYC, alot of tenant non-payers have been employed the entire time and simply chose not to pay their rent, because, they could get away with it.

Nationwide most of those who were unemployed, were at the lower end of income bracket and the extra 600 a week (later on 300 to 400 a week), is more than they were making after also counting the original state unemployment amount.

Because of PPP loans and varying amount of unemployment benefits, alot of people’s pay has been up and down. NYC has gotten more attention, because, it’s a large severely effected single city. If you look at the huge amount of non payers in NYC, the only plausible explanation, is that alot simply chose not to pay.

If the landlord sends their claim to a collections agency then the tenant is blacklisted for years. No courts required.

I think that varies by state. None of the local landlords I know have ever dealt with that. Usually though, if a tenant falls far behind and they can’t get free money earmarked towards paying it back, they won’t ever pay it back. Ordered by a court or not. They mainly just want to get the tenant out as quickly and problem free as possible. With everything going on, especially in NYC, I’m guessing there will be a twist later on.

You are correct. I used to work for a large property management company and there are a lot of people that would rather spend their money on pot, boob jobs, new trucks, dining out, etc. than spend it on rent. They don’t care if they get behind because their plan is to move out and NOT pay the arrears. They will just move to another place and pay for a while before starting the cycle all over again. There are lots of freeloaders out there.

If I assume sales in March, April and May overall *should* have been roughly $530B, then the loss in sales is around $200B.

The subsequent *bounceback* in June, July, August and September over the $530B level is less than $30B, even discounting the likely slight growth that normally occurs over a 7 month period.

That leaves $170B still in the hole.

Ditto areas like used car sales: the recent jumps are nothing compared to the losses in March, April and May.

What is absolutely clear, however, is that employment isn’t bouncing back quickly.

So it seems like these “jumps” are more likely dead cat bounces.

One wonders what another 2-3T dollars worth of stimulus would do to these numbers. The auto sales are particularly head-scratching, as those represent big ticket items that probably won’t be enabled by a twelve hundred dollar check (or two). I wonder how much of that graph couples with waste/fraud/etc. For instance, PPP is only being routinely audited for >$2M grants (er…loans)– if ten thousand businesses “borrow” tens of thousands each (that they ultimately don’t fully need), where does the extra money go?

If you do not think $1200 will put your backside in car you cannot afford to make the payments on then you do not understand the auto finance business…

So… Service spending, biggest category, down dramatically…

Retail sales only marginally up, due to stimulus and payment deferrals…

Means there’s a big “hole” in economic activity…

And if the stimulus and deferrals end too soon …

Look out below?

Also some of the retail spending used to be corporate spending. This shift is essentially zero-sum, increasing retail, decreasing business spending.

Another aspect of payment deferrals…we were offered deferrals on almost all of our bills. If a family chose to take a deferral and pay down cc debt then all this makes sense. I don’t think this is *just* the stimulus payment + not paying rent/mortgages. I read the article, but has Wolf mention the student loans on hold? I think that’s a big chunk, right?

Spending rent and mortgage money on ‘stuff’ is like eating your seed corn. Forbearance does not mean forgiveness. I don’t understand people these days? This pandemic has been going on for 6 months. 6 months. The good times never last and this pandemic won’t last forever, either. Hopefully, it will be a learning experience for people AND Govt.

My apologies for sounding so callous. However, it can get a whole lot worse before it gets better, and it might not turn around ever given our debt levels and hollowed out economy. I don’t think people buying ‘stuff’ with rent money is an option for most of humanity. And yes, I’ve been there….losing a job and being under employed for almost 5 years. I still made our mortgage payment by hook and/or crook.

The Fed and Congress have rewarded this debt consumption and penalized savers for at least 20 years. Got a whole generation who believe that is the way. Hard to believe we were the country known for rugged individualism.

Did people learn anything from 2008? If they had they wouldn’t have bought a house after that. Or they wouldn’t have taken out a loan no matter how low the interest rate was. Did they stop doing these things?

“The good times never last and this pandemic won’t last forever, either”

I know way too many folks at the bottom rung where this truly HAS BEEN the “good times” and I’m not kidding……meanwhile my income peaked in 1997 and I see no way to raise prices on my services…..EVER.

2020 has been one of the most depressing times of my life.

Services is a major concern. That us 65% of US Economy. If Services are down, how long goods will last?!

Always remember you are not locked into anything in life. If you are on a dead end road, you can get up tomorrow and take a different path. Every situation presents opportunities.

Good one jpup, and I for one agree totally!

I know that ”this time it’s different” is likely true because of the more severe meddling of the fed and guv mint, not to mention the incredible inflation of the last few decades, but:

In my past lives, I have been very literally ”down and out” three, (3) times, and have, with some help of course, picked my life up and started over again and again and again.

Folks really need to know they can do that,,, and it certainly appears that some folks DO actually know that and continue to do that, in spite of all the negativity and ”victimology” brainwashing that the lame stream media want us all to believe.

I don’t wish it on you jdog but just one severe chronic illness is all it takes to completely wreck one’s life. “Following all the rules” and “hard work” mean nothing to a virus. The people now suffering from “Long Covid” are about to find out that society considers them to be lazy grifters that aren’t trying hard enough to “beat” the illness. They will be judged to be morally deficient and Useless Eaters.

They will be destroyed financially and socially while being dismissed by physicians and denied benefits by welfare agencies and private disability insurers.

When a person can barely get to the mailbox while being denied social and financial support, no amount of “will power”, “power of positive thinking”, or “rugged individualism” can change their path. They need doctors that believe them along with social and financial support, not platitudes and judgement.

When doctors don’t know what to do they blame the patient. The rest of society is more than happy to go along with the lie and use it to justify the denial of resources like food and shelter. This is known as “civilization” but even “primitive” cultures treat their people better than in the US.

Trailer, I hear you. My wife went through (and is still going through) a health crisis. Her problem is neurological and REAL. I have been married to her for 35 years and I can assure you she is sick and drastically changed. She is completely unable to perform the job she was trained to do but the medical establishment was unable to pinpoint the problem so they put it under the default “depression” diagnosis.

She was denied benefits, denied disability and basically sent adrift by the system. What blows me away are the people who do manage to play the system. How do they get the money and a legitimate claimant gets the heave ho?

BTW, the depression diagnosis is basically a “blame the patient” diagnosis. And yes she did get depressed and anxious as she lost her ability to function as she did before the neurological event. And before anyone judges, imagine you were once cool headed, capable and extremely cool headed under high pressure situations (she was a level 1 trauma ED nurse). Then one day all of a sudden complex issues completely confuse you, you are unable to comprehend what you are reading, unable to follow complex trains of thought, and get overwhelmed and confused by high stress situations. She obviously could no longer do her job as the risk to patients was WAY TO HIGH.

And now a person who spent years caring for others (and payed their taxes into the system) at their worst times is cast aside and told yes you can work and you are not eligible for assistance.

JPMorgan credit and debt transactions showed spending was down 5.8% compared with a year ago through the week ended Oct. 10 (according to a source I trust). Consumers spent less on services and more on retail, yet less spending in total. As far as used auto spending, the choice was risk your health on public transit, or buy your own ride. Same happened with house sales.

Such abnormal recession spending spikes will fade soon, until we print another $2 trillion in stimulus (Late January 2021???). This will work until it doesn’t, temporal at best. At some point we will get a temporary real inflation spike (and Wall Street panics, great $$$ opportunity), then back to deflation soon after as the debt trap we are spiraling down is never going to be inflationary long term…just ask Japan…

Savings rate likely plunged in September. I am bullish on the short term economy than most, but this was probably the last big up month for awhile in terms of consumption. All ready see it in October.

I think a lot of the spending is from people moving from high cost no longer desirable areas to cheaper areas. They come with plenty of money to buy less expensive houses, furniture, sporting goods with ammo, and new cars. It’s still a tale of two cities.

In my world, I find a less premium product mix at the big box store, and plenty of empty shelves at the electronic store.

None of my friends are spending and neither are we…..this is the over 65 crowd. We are just being careful and keeping houses, cars etc as is.

Travel is out and has been since the CV 19 hit.

Stock market is up and Social Security and Medicare payments are still going out.

Why on earth would the 65+ not be spending as usual?

The social security cola increase for 2021 will be 1.3%. I haven’t heard about the medicare cola yet. I suspect it will wipe out the ss cola. That’s why the retired are cautious.

I think by the time you hit retirement age a lot of your spending habits are set. There is a substantial percentage that were frugal and accumulated around a million dollar nest egg. They are frugal people and don’t know if they are going to live to 100 or not so they just keep living below their means. They most likely will die with a substantial estate and then the children will do the spending for them.

Not all 65+ year olds are in the Market. Many have SS and a megar savings or a small pension. A good number don’t even have that.

Having Medicare by itself (no $$$ medigap policy) only pays 80%. Part D drug plans are not cheap…..we pay about $5K out of pocket for my wife’s yearly prescriptions. She is pretty sick and has COPD.

Being over 65 is not all sunshine and roses.

I’m not in the Stock Market (a lot of us older folks aren’t, can’t afford to lose principle) and savings/CD’s are now paying .6 of a percent and the fed is saying rates will stay on the bottom for years. We’re hoarding our resources for an uncertain future. It’s just math.

But why would the 65+ spend less now because of COVID?

This is a joke, right? There’s basically no travel, and many people are not eating at restaurants.

People are moving for a variety of reasons, but they are moving a lot. Moving is expensive and requires purchases. People who are staying put are changing priorities and all of a sudden being a prepper is not a tin foil hat stratagy. Chest freezers were sold out since March and are now just starting to be back in stock. Gun sales are off the charts. People are buying fruit trees and gardening supplies. Camping equipment is selling out. In short, a lot of people are preparing for extended bad times and putting themselves in the position to be more self sufficient, and you have to spend money to do that. But it is for the most part a one time investment, and once done it is over…

It costs a lot of money to move so a person/family should have some pretty solid reasons to do so. Selling and/or buying has a built an agent fee that someone will be paying. Plus, the sheer costs of moving and the personal energy it takes to do so. The GD cleaning and chunking out is enough to make me weep. It’s hard to leave the familiar and comfortable. Hard.

We are one of those families that are all prepped up and rural simply because that was our preferred lifestyle choice decades ago. But let me tell you, this year is still beyond depressing. I would think people would have a better and more enjoyable life if they looked inward (I know that sounds flaky, but….) looked at themselves and chose a suitable path for their age, skills, likes, and dislikes. There are no magic safe havens. We seem to have a whole new turnover the past 3-5 years in our area. The For Sale signs have returned because the new arrivals did not fit and are moving on. One newbie about 4 km away didn’t even get his new house finished. It’s all framed up and covered with Tyvek with a For Sale sign on the road. Listed, with an agent. 4 months. I think that one set a record. We used to always have a potluck and meet and greet for new folks that moved here. Gave that up years ago.

This is a year for just getting by, imho. We are going through a once in a 100 year event. You can have all the preps in the World, and we do around our place, but it doesn’t make it any better. Luckily, our Govt and population is cooperating in keeping the pandemic at bay. The infection rate is 1.4% in the Province where I live. But we remain careful and on guard with activities and family. It’s going to be a tough winter for all of us, and really really hard for many. The lessons learned will be stern ones.

regards

While I do not want to be confused with a communist, whose financial theories and policies should exist only in fantasy, magicians’ tales, I find it amusing how a small group of middle-class/poor Americans is buying guns to protect themselves/shoot another group of middle class/poor Americans while both are unaware of the elephant in the room. All of this desperation is ludicrous and irrational.

The US and every other economy sees income/wealth being created each year from two sources: labor income from workers’ labor and income from capital via rents, dividends, increases in the value of stock, increases in the value of the trusts of the ultra-rich, etc. Labor income is, and will soon be more, heavily taxed. Capital income has largely been able to escape taxation, except for the small portion of the capital income owned by the lower and middle classes, who are not able to use the widely available schemes to avoid taxation.

It is true that the world’s economy has suffered gigantic, extremely damaging shocks. Definitely, I am very, very sorry that the small and medium businesses owned by the middle and lower classes are dying like flies.

Those individuals who are seeing their life savings disappear are sadly suffering often without any fault on their part. However, there is a GIGANTIC iceberg of wealth that still exists hidden beneath the tiny portion of wealth seen by most and whose existence the ultra-rich wish for you to never realize.

Most debts owned by most countries, persons, and individuals are not owned to extraterrestrials or to god. They are owed to the world’s ultra rich.

My work for decades has allowed me to see that vast wealth hidden carefully in trusts and foreign shell companies. There are huge fortunes out there of people who have for decades avoided paying taxes by numerous, covert tax schemes and by the covert bribery and resulting ownership of our politicians.

Those are the individuals that indirectly, secretly own the huge debts that the rest of the world, governments and individuals, are not paying now. The US constitution does not allow us just to forgive those debts, except via the statutory bankruptcy process, which “reforms” have made impractical/unavailable to most, middle-class Americans.

Thus, the problem to be solved to re-start and rescue the closing and dying portions of the economy is how to come up with the funds without more government debt creation, which the US government may soon be unable to make: pre-pandemic, it was predicted that by 2025 the US debt payments each year were going to equal its entitlement payments. That moment will probably arrive much, much sooner.

Thus, while it will not come for a few years, at some point (unless taxes are dramatically raised), the US government’s payments on its debt can be reliably forecast to take up every penny of the income that it receives in taxes, fees, etc. At that moment, theoretically, it will have to print mostly dollars in some way just to make its annual treasury bill and other payments. The ultra-rich, who are owed most of that wealth, may then lose faith in the US dollar.

Maybe, that moment will never arrive, if the economy can be induced to grow dramatically and the debt again recedes to a small portion of the GDP. Unfortunately, I doubt that is possible.

It will soon be time for some very hard decisions, which our politicians will be reluctant to make: actually forcing the ultra rich among us (who have avoided paying taxes for decades by chains of foreign trusts and foreign corporations) to pay their fair share of taxes. Since they will never consent to taxation by allowing their companies to show income or to bring their income back to the US, the only way to tax them will be via imputed income taxes, which are imposed by imputing income on wealth and then taxing that.

The “Federal” Reserve bankster cartel wants Americans to fight each other and not see the men behind the curtain working hard to steal Americans’ wealth and avoid taxation. Wake up! Open your eyes. Try to convince the EU to work with us, so the ultra-rich cannot just flee to the EU.

Require disclosure of every individual and their fortune, who is the beneficial owner (directly or via trusts, share ownership, etc.) of more than $300 million. The numbers of persons disclosed and the VAST amount of the wealth of many, many individuals will be a shock to the rest of Americans and the world.

We are like little peasants working hard to push a loaded cart, while inside the cart a gigantically fat, sumo-wrestler type (who owns most of the items in the car) does not only not help us push the cart but sits at leisure, laughs, and expects us to also push his vast, fat, lazy bulk.

This outcome was predictable at the point where we began to inject socialism into capitalism via the corporate charter and income taxes. Sadly, we no longer have a capitalist system, because of incorporation and its control over government has made it impossible for regular people to compete with corporations. When I grew up, towns were full of small businesses and business owners, who had a stake in their community. Today, those small businesses have been replace by corporate owned business, with no stake in the community, and generating no wealth for the people. If you want to see regular people thrive, then end corporate charters. They are simply another form of feudalism.

“from people moving from high cost”

Important question.

Who the hell bought their houses in high cost, now undesirable areas?

I might go along with your take on hiked retail spending due to moves, but not until someone can tell me who bought those vacated houses (thus supplying the money for the retail boost).

Important because those new CA/NYC buyers are now the ones first in line to get financially slaughtered when the illusion evaporates.

I suspect it is foreign buyers and immigrants. These groups pool money among families and tend to buy bigger and more expensive homes, and actually live in them. Also if you are in China and can get money out, they consider it better off in an overpriced empty house in the west.

There is also a bunch of real estate money being spent by the ibuyer platforms. It’s not their money they are spending, it’s all investor money, so they are not price sensitive. You better hope it’s not your pension money.

The lower interest rates have allowed people to afford to move up, and keep the same payments. It happens every time interest rates fall. Most people are financially illiterate, and never look at deferred costs or consider the long term impacts of their financial decisions.

Many keep themselves in debt at the very top of their limits, and ratchet up their lifestyle every chance they get. Then they wonder why they cannot retire and are impoverished in their later years…

Yeah, it was fun while it lasted! Now they can go live with the kids….LOL

In your honest opinion, do you think mortgage rates will ever go up? I mean meaningfully?

Spending must certainly be tanking. I have not had a single text message declaring how many ounces and which box to check, and yet the post office has made the delivery. Either they are trying to disprove the claims of incompetence or I am in the wrong area code for big buying. And I’m already stuck with unsellable blood and organs by law. Jeez!

How come total retail sales are rising but credit card balances are dropping. Must be too much stimulus.

My friend who is a loan officer says HELOC deals are off the charts. Wells Fargo is not offering HELOCs for the last three months (Fed mandate???), but smaller banks and credit unions are very very busy.

It is possible people are using home loans for funding purchases or paying down CC debt.

Idaho Potato,

That’s an interesting observation concerning HELOCs. I know Wells Fargo stopped them. Some other lenders did too. But maybe smaller lenders jumped on it. It’s not showing up in the data — at least not yet. See the weekly chart of HELOC balances below.

The other question is: if you have equity in the house and need cash, why not do a cash-out refi with today’s record-low mortgage rates? Cash-out refis are hot. So I think a lot of people are doing that.

In some states that are non-recourse, only purchase mortgages are non-recourse, and a refi mortgage can be full recourse. So that’s something to be leery of.

In Idaho HELOC rates vary widely, but there are some great deals for those with credit scores above 800.

Bank of Idaho – 3.25% pegged at Prime for 10 years. No closing costs, annual fees of $50 (waived for the first year).

Idaho Central Credit Union – fixed at 3.25% for 10 years, no annual fees.

Their loan departments are very very busy.

As a data point…

I’ve been trying to do a refi for 4 months. No cash-out, just trying to take advantage of lower interest rates.

The application goes in, with all data. Impeccable credit. And it sits there, no movement. Four different banks so far, including Navy Federal Credit Union (which at least has the courtesy to call to tell me they can’t get to it for nebulous reasons).

I think they want me to take cash out. Either that, or this entire refi thing is a scam.

I can easily afford to just pay off my mortgage. Might do that in the next few months. Maybe the loss of 6% interest will spur them on to complete a refi. If not, they’ll get nothing. We’ll see.

You should threaten them with a mortgage payoff — that’ll get them motivated to refi.

Wolf, I have been debt free for years now, but with the real possibility of some form of Debt Forgiveness or Debt Jubilee in the Untied States of America within the next decade, I am going to take out a mortgage on my next house at probably a rate of less than 3% which is at least 5 percentage points below the true rate of inflation, 8%.

DEBT AT A REAL RATE (ADJUSTED FOR REAL INFLATION) OF NEGATIVE 5%, THE SYSTEM IS PAYING ME TO BORROW MONEY, THE WORLD IS UPSIDE DOWN. I must be living in Europe, but I am not a sovereign state!!!

If a house in the neighborhood gets foreclosed or just sells at a way lower price than expected, doesn’t that drive the appraiser/ Algos to adjust all the nearby values lower? If one wants liquidity then max out the HELOC and deposit it in different bank, mattress or pm, as the E in the HELOC will soon disappear.

The only place you are going to get 3% is in something riskier. However if you agree to take a low single digit beating on your equity that is offset by something on the order of much more should prices contract, the move makes sense. Some years ago a Citi analyst said, investors will be borrowing money and putting the proceeds in a savings account. In his scenario there was a positive return. but there doesn’t need to be. You still have the collateral. You own your home and you own the equity that you borrowed. On the liability side you count the income it takes to service the debt. While RE prices rise the size of the debt shrinks. While yields rise the cost to service the debt shrinks. Then of course maybe both at the same time in a time of monetary inflation.

To be making HELOC’s in this environment is insane. Why would anyone loan money on equity that will not be there in a year?

Wolf,

Hmm…I would hope to God that smaller (under 1Bil in assets) banks have enough residual brain cells in their corporate heads to recognize that if WF/etc. have *completely* shut down HELOCs (cash out refi too?), then maybe that is a huge signal that SFH are massively overvalued, to the pt where downward revaluation is inevitable given the pandemic.

The Big Four don’t shut down entire lending sectors for giggles…the do it because they know (nuclear) winter is coming.

Ditto loan loss reserves, which brings up those disparate Q3 ones…

Of course their is always the school of thought that the Feds will step in and bail out all the banks making foolish decisions. Also, I would suspect much of the high risk loan portfolio is bundled and sold off to pension companies and mutual funds as low risk MBS.

Cas, this current surge in Single Family Home prices (SFH) is due partly to the move to exit the infected costly cities to Work From Home (WFH) and partly due to the ridiculously low mortgage rates that allow lenders no margin of error on the borrower losing his or her job in the next year which is a real possibility in America 2020/2021.

I think many of the mortgages issued in the last 6 months are going to get into trouble due to the economy experiencing a very prolonged recovery and many job losses today becoming permanent as more and more employers close their doors, esp. in the recreation/entertainment/travel/retail mall sector of the economy. The surge in home improvement sales is also temporary as a limp noodle economy will not convince everyone that this is money they will necessarily recoup upon resale.

Prices here in the Shenandoah Valley are firm close to cities (for now!!), some increases to do a purchase, but the further out you go, the prices are starting to soften. There are lots of convenience costs in living on a Covid-free mountainside. County Real Estate Taxes and personal property taxes in Virginia in 2021 are going to shock many citizens as the local governments try to recoup $Million in lost revenue from 2020.

First Quarter of 2021 should be a great time to buy a house in this crazy world we live in.

Bobber,

You are too quick to blame the victims of this crisis. All the minimum wage workers are not conspiring to impoverish the middle class. It’s the bankers doing that.

Here is how spending can be up while credit card balances are dropping. There is an entire segment of money laundering being done with credit cards. As we go cashless the spread will keep widening.

You aren’t wrong, but where are the protests against the bankers? I didn’t see any this summer, all i saw is white people and men bad.

Rather ingenious if you ask me.

I went through the last crisis and saw the protest around the world didn’t do a bit of good for the victims. Cutting the cord is the only thing they understand. That’s why people are paying off debt, canceling cable, not reading msm, moving outside cities, etc. There’s was a massive retrenching happening, covid sped it up.

“I went through the last crisis and saw the protest around the world didn’t do a bit of good for the victims. Cutting the cord is the only thing they understand. That’s why people are paying off debt, canceling cable, not reading msm, moving outside cities, etc. There’s was a massive retrenching happening, covid sped it up.”

As did I. Do you remember how they handled those protests? Thats how you can tell when something has been co opted. Look how the media treats and the reaction. I hope you are correct but with regards to people “waking” up but i don’t think we’ve reached that point yet. Things will have to get much worse.

Wolf: you aren’t kidding when you say “whiplash charts”. After looking at these charts, I scheduled an appointment with my chiropractor on Monday!!!

All things considered it does look like things will be back to normal sooner rather than later. Hopefully, that vaccine arrives early next year and the pandemic is over by summer. The work from home and flight from expensive areas will be the main things being tracked after that.

I don’t think so. If I understand things correctly the US has added more debt and less production. That seems to have been the playbook the last few decades resulting in slower and slower growth and more and more transfer payments. Once we are through this virus the overhang is going to be rough I think.

That is the normal, before, the pandemic hit, a recession was on the horizon. After the pandemic, we will see if the recession hits right away or, if the stimulus that were used to get through this pandemic and recession, will simply mean the next recession is a couple years away.

Overall, except for accelerating work from home, I don’t think the pandemic changed the direction of America, all that much.

When you say “back to normal” that statement implies things were “normal” to begin with. Debt based economies are not normal, they are abnormal and mathematically impossible to sustain long term.

That is the “normal” like it or not, for some time at least. See my comment further down.

Monthly rate above last year sounds good, but from Wolf’s first chart, looks like year to date 2020 is still about $180 billion below normal. Yes, stimulus and shifting spending created increases, but current levels could also reflect some deferred spending, which also will stop or reverse after temporary bounce …

Some of those charts look a little wanky!

I think you always have to keep in mind government goals vs. personal goals. Government likes to stimulate consumption via debt and useless economic activity to keep the nominal GDP expanding. We as individuals should think about our goals, how many goods and services do we want to labor for and invest for. It’s different for us all. Government gives us a lot of carrots and sticks to get us to be participate the way they want, but one day we will be gone and system will go on without us.

This is partly true, but, it largely is because, the way an economy is designed seems to peak and then stagnate (look at Japan). Rather than make long term structural improvements to the economy, the government, corporations, and the people; all push for slow and “steady growth”, which then levels off the standard of living for the 90%. The actual economy may be hallowed out (usually) in the meantime. This is true across the world. It’s the people’s fault as well.

This is even already happening in China, the rich top CCP members have over the last 5 years been moving factories to cheaper countries like Vietnam and others (and importing cheaper migrant workers). This was happening even before the trade war, though the trade war greatly accelerated it. At the same time in China household debt is skyrocketing.

It’s upto the people to unite and demand a better government. The divorce yourself from the community and it’s government fantasy, is a road to nowhere.

Borrow from the future to “fluff” the present. That is the game.

And the fake low rates of borrowing from that future is the great enabler.

The third mandate of the Fed that is always ignored is “promote moderate long term interest rates.”

Now, why would that be a mandate of the Fed? The wisdom is great.

Moderate means “not extreme”, up OR down. Moderate long rates prevent yield curve inversions, maintain a balance between lenders and borrowers, and prevents irresponsible and seemingly cost free creation of long term debt that unfairly burdens future generations.

If held to this third mandate, the national debt would not have ballooned to this current degree. But the “moderate long term interest rate mandate” is always and intentionally carved out of discussions via the “dual mandate” rhetoric.

Maybe it’s the wrong paradigm. If we want to reserve access to some essential assets for people who don’t have connections or great wealth, maybe we should more directly control some of that access instead of constantly manipulating money rates. Such as higher taxes on unused excess asset ownership for essential things like housing. Penalties for hoarding and keeping those units off the market.

Sometimes penalties, although not always enforced, will make people realize it’s not OK to do certain things. That their individual actions have an affect on society as a whole and that they have a responsibility. Some will do them anyway, but at least the societal values get changed and less people do it. There really are people who are incapable of normal empathy. Sometimes they just don’t care about others, but other times they really struggle with that and miss some obvious consequences of their actions. Maybe we’re living in an age of Aspergers.

No, the economy is not designed at all. The economy is a result of corporations with nearly unlimited ability to bribe politicians, doing so to make short term profits and drive share price. There is no cohesive “government” only prostitute politicians who are for sale to the highest bidder. Our policies on military intervention are not driven by public opinion or what is good for the country, they are driven by lobbying by the military manufactures who bribe Congress, high ranking military officials, and the White House. It is impossible to have “better government” when the politicians who are the government work for the corporations who are only concerned with their individual interests. Until the umbilical cord between government and corporations is cut, the US will continue to degenerate until it collapses from its own greed and corruption.

1) The unsecured credit card business is always risky.

2) The Fed cut rates. The Effective Fed Fund Rate is slightly > 0.

REPO (SOFR) is 0.001. // credit card risk premium is as high as 18%.

3) In 5Y one dollar invested today will make : 1.18^5 = $2.29 in 2025.

4) To get a one dollar in 2025 banks invest today : (1.00:1.18)^5 = $0.44.

5) The Fed stimulus save the banks. The banks cont to collect their risk

premium rate plus late fees thanks to the Fed.

6) If one dollar invested in Feb 2020 will become delinquent in Feb 2021,

the bank profit will be $0.18 on $1.00 investment, losing $0.82.

7) If in Feb 2022 the default rate will rise to 20%, in two years the banks losses will be $0.60 on each NPL dollar. Banks will lose 12 cents on a dollar. The delinquency rates will rise gradually, not from zero losses in two yeas suddenly to 20%. Their credit cards losses will higher.

8) But banks are in the credit cards business for 65 years, since 1955. They know what they are doing.

9) A dollar invested 8 years ago, in 2012, will be very profitable until 2021 :

1.18^9 = $4.44 minus a small portion of losses in 2021/22.

10) The banks will start to play defense before their profit fall, but beg

congress for additional stimulus. Their members in congress will

get it done in 2021.

For many (most?) people 2020 has been fantastic! People who kept their jobs work from home now and save hundreds of £ per month for not having to spend on fuel and expensive lunches! And people who got furloughed received money anyway and spent the entire summer on the beach!

Yes, government “debt” has exploded, but it isn’t really debt because it will never be paid back and isn’t really “borrowed” but simply printed by the central bank.

Printing trillions of money (and actually spending it!) without any apparent consequences… Record low interest rates, low inflation (except the items that are not in the CPI – paying twice as much for the same house is not inflation but “wealth creation”).

So why don’t we do this every year? Many politicians are now be pondering this idea.

I fear there will be a vaccin next year. We’re gonna need a new virus!

Excellent summary!

We do do this every year. Some years more than others.

When it comes to forbearance student loans take the cake…

Currently less than 11% of people with Federal student loans are making payments. Eleven percent! Think about that.

Source: https://www.cnbc.com/2020/10/07/less-than-11percent-of-people-with-federal-student-loans-are-paying-during-covid-19-.html

That is the biggest asset of the government. Wonder when they will take the write down.

They are moving towards autonomous driving. Five years ago I bought a new car. It has enough added safety features to qualify for an insurance premium discount. I like the back-up camera. The window tinting started to bubble in the Florida summer heat. I got it replaced with the maximum tinting allowed by law.

I noticed the price of wheat futures are up about 20% in a year. Commodities are increasing in price.

Still doesn’t substitute for driver awareness. My neighbor backed into my car. She had both a backup camera and the ultrasonic warning sensors.

You parked your car two feet too close.

It was kind of my fault. I parked on residential street where she could back into it. She had a friend in the car and was talking. Luckily it was only one door and she snuck down to the body shop and paid. Told her I would take care of mine if she took care of hers, but she wouldn’t have it.

Regarding trade with China. The US gets Flat Screen TVs, other gadgets and trinkets. The US consumer provides dollars in return. The question is, how much value do these dollars hold today, tomorrow and the next? The US may be the winner here as we obtain tangible material and China receives paper of declining value.

Not True. Those dollars sooner or later come home to roost. Chinese will bid up the price of everything with that money….including your shelters. At the end Americans are the ones who are majorly fooked. No person or country has gotten richer by consuming.

‘No person or country has gotten richer by consuming.’

Thank you for that cogent sentence. I don’t understand why folks don’t understand it. Seems like a simple concept.

Wolf, thanks for the data displays and explanations.

I think it is a reserve currency thing. As long as US government can borrow so cheaply they can run a deficit and the money gets deployed into the real economy where it earns a higher return. Seems like we are at the end of the road though as a lot of it is going into loss making enterprises.

Sorta like when the Japanese back in the 1980’s started buying up all the real estate in the US, Pebble Beach, Rockefeller Plaza, etc.

Wonder what happened to them?

“how much value do these dollars hold today, tomorrow and the next?”

A lot more than the trinkets that will be in the landfill in 10yrs…..

It’s called the Trump effect.

Quite curious to see the “whiplash” chart for gun sales.

Curious times. Very curious.

Noticing in the Last month up here on the Olympic peninsula that real estate pendings

On both building lots, land and houses have switched to “ contingent” from straight forward pendings. Is the money drying up where the hopeful buyers now have to sell something first before completing their “flee buys”?

More likely that more people who are really not in a position to move are being pressured by events to attempt to do it if they can…

The prices are outrageous. Anyone not using contingencies now, unless they do their own initial inspections and have a lot of construction experience, is a fool. I just took a close look at a house going for way too much that needs a new foundation, roof, septic and has some plumbing and electrical issues. You can’t tell by the pics.. A seller’s agent isn’t going to tell you. Buyer’s agents are clueless. A house “inspector” isn’t usually going to crawl under the house for you. Contractors are way too busy to check it for you on short notice.

As long as the rest world continues to let us stuff ourself with their productivity this can continue. Making stuff is hard and you get tired. External events outside the control of the Fed will force an accounting. Untill then. If 3.5 trillion was good then why not do more? It’s laughable at this point to be concerned about the debt we have. Tipping points are impossible to foresee but are obvious when they happen.Our concern is now focused on how to get more and the government will oblige because we need to be placated and passified untill the tipping point. Money Printer is going to bop til’ it drops. The opportunity of discipline has long expired.

Read an interesting article that kind of fits with where I think we are going. Sovereign countries were already over indebted and many will get down graded as debt to gdp numbers get worse. The marginal ones are going to get down graded to junk and will fall into the doom loop.

What’s the average and median price of a new vehicle now?

DanS86,

For new vehicles, there is only an “Average Transaction Price” (ATP), which in Q3 rose 6.5% year-over-year to $35,500. This price goes up for two reasons: price increases plus consumers shifting to more expensive models, especially high-end trucks.

Consumers have a very simple “solution” to the ever-rising cost of vehicles… simply extend the car loan length. Average new car loan today is about 72 months long.

Their is a fundamental problem with that. Vehicles depreciate, a lot.

The longer you extend payments, the more repossessions increase.

At some point it becomes financially impractical as people will not continue to pay new car payments on a old car.

Of course people are splurging on new cars. They will be living in them shortly.

$35K is more than I paid for my house in 1986.

My last house, retirement townhouse, bought in 2011 was $42K.

Vehicle purchases are like an IQ test. Only people who are really financially intellectually challenged buy new cars.

I remember reading a book 20 years ago which stated the majority of millionaires never purchased a new car until after they were already millionaires.

How to keep this new consumer society going? Idle consumers are good for the economy, workers bees with three jobs are a burden. Who saw this coming? Imagine if we end the lockdowns, terminate all jobs, and just have fun? The notion of lowering medicare to 55 is radical but how about full retirement?

You cannot keep a “consumer” economy going, that is the point. It is built on a faulty foundation and will collapse as a result. Every ponsie scheme runs its course in due time, no matter how well it is sold to the suckers….

The only kind of economy that is sustainable is a “producer” economy. At some point in the future, our consumption will have to come into line with our production.

Any data on unit sales, with regards to new and used vehicles? And what about the equivalent of “churn”, i.e. during the years measured, what percentage of sales is due to the same vehicles being resold?

1) Japan 10,000 711 stores bought 4,000 Speedy Gasoline Stations for $21B, providing gas, beer, coke, and junk food for breakfast, lunch…to every American day & night.

2) Casy is #4. MUSA is #6. Most stores are mom&pop stores,

working hard, risking their lives, providing gasoline & food in the rural areas and the inner cities.

3) Fed fads vs Gasoline stations Sales charts.

4) A buying climax @47 in 2008(H). The response #28 was in 2009(L). The trading range halfway @37.5. The 2013(H) is an upthrust. // Sept 2018(H)

was the last chance to dump gas & junk, before the 2020 slump to Mar 2020(L) @26.

5) Oct 2020 to 36 < 37.5 halfway, is another chance to liquidate before the markdown send prices lower.

6) Since WTI @40 customers can fill the tank once a month, buying less gas & junk. When WTI @100 they will fill only quarter of the tank, every week, spending more on gas & junk.

Wolf,

Some of these individual charts are *very* interesting from a historical basis…perhaps to the point of meriting individual posts, analyzing some of the charts individually in detail (if you run short of post ideas).

For one, look at gas station sales…which I have to believe are mostly made up of gasoline.

Yet, even though the post 2014 oil bust saw oil fall from $110 or so, to at least the mid $30’s (call it a 70% decline), gas station sales fell a maximum of perhaps 25%.

Hmm.

Hmm.

I’ll buy that refining margins maybe kept retail gas price up some…but not the difference between a 70% decline in oil and a 25% decline in gasoline.

Nor did Cheeto/Slim Jim sales explode…

That is just one example of some weird aspects of these individual retail sales charts, especially when viewed over multi year periods.

People seem to think that by the spring next year the virus will be gone and everything will be returning the way it was before.

What if this goes on for 5 to 10 years before we get to grips with it?

No one seems to plan for this scenario, yet it is highly probable.

Maybe at some point we will be begging for a dictator to put order and force everyone home like chinese did?

This is only the beginning, prepare for the long haul I say.

You can’t lose either way. If the virus hangs around, there will be more stimulus and free money for EVERYONE, if not, we get back to normal feeling better than ever since it’s like getting out of jail. If there’s a new virus, we get DOUBLE the stimulus.

The stock market in the meanwhile will continue to skyrocket.

The best winnings are still to come.

The virus has served the same purpose as a global recession, while clearing out overbuilt industries and businesses (mostly on main street, but some corporate bankruptcies) and providing a blueprint for new industry, all manner of virus remediation in everything from daycare to international travel. At the turn the markets will have to reallocate but it will probably be the greatest dip to buy, ever…

Realistically, if history is any indicator, these pandemics last about 3 years. The real impact is not the virus itself, but how it effects peoples psychology.

People blame lock downs for business dropping off, but it would have cratered without the lock downs, as we saw in placed that did not lock down. Most places you can go out to eat now, but many don’t because they just are not comfortable anymore. It is really hard to estimate how long that mindset will last. It is hard to enjoy yourself when you do not trust the people around you, and cringe every time someone coughs or sneezes.

Jdog,

Yes, Sweden didn’t lock down, and their economy crashed just as hard in Q2 as the US economy because people, as they saw the deaths pile up, stopped doing stuff, stopped traveling, switched to working from home, stopped going out, and businesses too cut back. And now the virus is surging again in Sweden, with cases-per-day tripling over the past five weeks.

Well, we sheeple in Melbourne have had our lockdown update and there have been some changes.

Now, for those of you that don’t know what has been going on in Victoria, Australia and in particular, Melbourne, a city of 5 million plus people, here is quick recap.

We went into lockdown sometime back in March (??) – really can’t remember it has been so long now!!!

And then we had a few brief weeks of relaxed lockdown with almost zero cases before the inept handling of the quarantine program by the State Labor government allowed the virus to escape into the community and especially aged care.

(Cases went up to around 800 a day at its worst and around 600 – 700 people in some type of aged care died as a result.)

The government imposed a curfew and a 5 kilometer travel ban along with shutting down most of the city except for ‘essential’ services. Mandatory masking and initially a one hour limit of being outside your house were imposed and only four reasons that you could go out were imposed.

The curfew was removed under threat of a court case which is still ongoing.

In my little postcode we maxed out at a total of 66 cases for a population of around 60,000 and currently have 1 active case. We went weeks and weeks without one active case.

International flights into Melbourne were stopped back in June and still haven’t resumed.

Retail except for things like food, pharmacies, gasoline, post offices, and take away food are still closed and will only partially open on 1 November.

Outdoor pools are open, but indoor pools remain basically closed. With the previous 5 kilometer travel ban, even the ocean was off limits to most people. Not that many people would be swimming there anyway with the water temp quite cool. Today the water temp is 58. (For Wolf that is about the same temp as the water in SF Bay about this time of year.)

All this is now ongoing with a total of 2, yes, 2 new active cases in the entire state and a total of 290 active cases in the entire country. 216 of those are in Victoria.

We’ve had a total of 904 deaths in total from the virus.

There have been some changes most of which are really not that important other than the travel ban has been changed. We can now go 25 kilometers away from our house. The four reasons to leave remain in place.

The actions of the state government here that favor union related activities to the detriment of small business are really digusting. The small business sector here has been decimated and put on life support with many probably unable to re-open.

Every chart is either at record highs or nearly fully recovered. I don’t get it. Why all the pessimism in the comments?

Thingy is that service sales which are 2/3 or consumer spending, are still down 7.4% from a year ago. Spending has shifted, from businesses to households (zero sum), and from services to goods (zero sum), and from making mortgage payments (7% are in forbearance) to buying goods goods (zero sum).

A few posts ago we learned the Social Security Fund sits at 2.7 trillion. In the last 3 months the gov has spent 3 trillion to keep treading water.

If you think the gov can keep doing this, there is no need for pessimism.

1) Today risk free interest 10Y @0.7 is as risky as the 10Y @15.7 was in 1981, forty years ago, under the Fed carpet protection policies.

2) If the Mach 3 Persian carpet will strike the Fed carpet ===> Repo will burst to twenty, the risk free 10Y will join NR Germany and oil will totally CRAK.

3) The Nasdaq Jan 2018(H) & Feb 2020(H) stopping actions indicate that

the Nasdaq is a system control with a positive JP feedback loop that is going to break, but we don’t know when and how to fix it. JP will sell his worthless carpet.

4) When the risk free + risk premium were @15%, in 1957, John Reed

AMEX launched a credit card, because the future is in PLASTIC, and

it’s not fair to leave all the fundamentals profit, in the next 10Y until 1967, to Mr. Bloomingdale Diner’s Club, who issued his c/c only to his rich friends, who never sat in any Greek diner.

5) Every bubble have two sides, the left and the right. Mr. Warren Buffett

bought American Express when the risk free 10Y + the risk premium

was 15%, because AXP is a good co, with good management, that can

survive more than 20 years, with an expected profit of : 1.15^20 – 1 =

16.4 -1 = $15 plus dividends, on each invested dollar, surfing on the globalism waves, along with Coke and Gillette.

6) Today China try to steal the huge Amish tomatoes, that are more expensive than Whole Food Bezus tomatoes, but China can’t because the Amish don’t watch TV and ride horse & buggies.

DOJ Sydney Powell and J.P. will protect the gov from the supreme court boomerang.

Lt. Dan, Forrest Gump, became manic depressed after Vietnam,

because he became amputated instead of dying like a hero, but during

the hurricane his spirit rejuvenated and he built a new dominant empire that lasted for decades.

Mexico Primera Liga MX replace NFL, because Mexico Kaisers don’t kneel.

Van Gogh Gump don’t discuss your art of war without stopping for oxygen.

@MarkinSF

The mortgage rates will be going up over the next year and then some. All those people who did cash-out refi’s who leveraged their homes to the max will find themselves under water. 2008/2009 all over again. Bad move.

Smarter move would be to refi into a shorter term mortgage and start paying it off faster.

True.

“The whole problem with the world is that fools and fanatics are always so certain of themselves, and wiser people so full of doubts. ”

– Bertrand Russell