Commercial Mortgage-Backed Securities backed by hotel and mall properties get hit the hardest. Mall-REIT CBL failed to make bond interest payment yesterday.

By Wolf Richter for WOLF STREET.

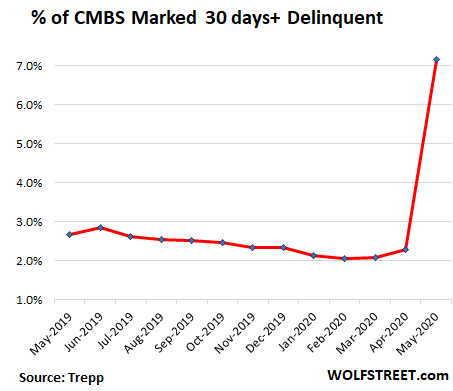

The delinquency rate for commercial mortgage-backed securities (CMBS) spiked from 2.29% in April to 7.15% in May by loan balance, according to Trepp today, which tracks securitized mortgages for institutional clients. This month-to-month spike of 481 basis points in the Trepp CMBS Delinquency Rate was the largest in Trepp’s data going back to 2009:

This 7.15% delinquency rate is composed of mostly 30-day delinquencies. The way 30-day delinquencies shot to such prominence, far above the later stages, indicates how sudden this event was:

- Delinquent 30 Days: 4.98%

- Delinquent 60 Days: 0.12%

- Delinquent 90 Days: 0.18%

- Non-Performing Matured Balloon 0.46:

- Foreclosure: 0.33%

- REO (Real Estate Owned by a lender, waiting for foreclosure sale): 1.08%

But the five biggest categories of commercial real estate – multifamily apartments, retail, offices, lodging, and industrial – had very different delinquency rates, ranging from minor to catastrophic.

Industrial CMBS: the delinquency rate ticked up to 1.82% (from 1.36% in April). This sector includes warehouses and fulfillment centers for ecommerce, which is booming and is probably one of the biggest beneficiaries of the lockdowns, as retail shifted that way. Industrial properties are a still fairly hot sector, whose delinquency rate of 1.82% was less than 1/10th the delinquency rate of Lodging.

Lodging CMBS: The delinquency rate in May shot to 19.13% (from 2.71% in April). Many hotel properties are still closed and travel has essentially shut down. The sector remains in a death spiral.

How bad is it? In California, the state has made a deal with some hotel chains that would be otherwise shut down to house the homeless during the pandemic. It remains uncertain how well this plan is working, given the number of camps I still see on the sidewalk, but at least it’s some revenues for the hotels.

Multifamily CMBS: The delinquency rate rose to 3.25% in May from 1.92% in April, according to Trepp. Apartment buildings are under some pressure as some tenants are taking a rent holiday and as many areas have imposed eviction holidays. But at least for now, tenants are still mostly paying their rents, given that stimulus payments and state and federal unemployment benefits arrived in many households.

According to the National Multifamily Housing Council’s survey of 11.4 million professionally managed apartments across the US, 93.3% of apartment households made a full or partial rent payment by May 27 (though this was down from 94.8% at the same time last year).

“Each week we see new evidence that Americans are prioritizing rent and that the work apartment firms did to create flexible payment plans is paying dividends,” the NMHC’s report said.

Publicly traded apartment REITs show similar rent payment rates in their quarterly disclosures, tracked by S&P Global Market Intelligence, which today provided the latest updates on rent collection rates for April. The REITs in this table are “Multifamily,” except Invitation Homes, which rents out single-family houses:

| Multifamily and single-family rent collections for April | ||

| AvalonBay Communities | [AVB] | 93.8% |

| Camden Property Trust | [CPT] | 94.3% |

| Essex Property Trust | [ESS] | 95.0% |

| Invitation Homes | [INVH] | 95.0% |

| NextPoint Residential Trust | [NXRT] | 95.3% |

| UDR Inc. | [UDR] | 95.5% |

| Apartment Management Investment Co. | [AIV] | 96.0% |

| BRT Apartments | [BRT] | 96.0% |

| Bluerock Residential Growth | [BRG] | 97.0% |

| Equity Residential | [EQR] | 97.0% |

| Independence Realty Trust | [IRT] | 97.3% |

| Investors Real Estate Trust | [IRET] | 98.0% |

| Mid-America Apt. Communities | [MAA] | 99.3% |

Retail CMBS: The delinquency rate for retail properties shot to 10.14% in May from 3.67% in April, according to Trepp, as landlords are having the hardest time collecting rents. Many of them have offered their tenants, whose stores were or are still closed, some leeway, such as allowing them to defer rent payments for months.

How bad is it? Rent collection rates by publicly traded mall-REITs range from terrible to abysmal. Below are the updated rent collections, released today by S&P Global Market Intelligence. Simon Property Group [SPG], the largest of the mall REITs, does not disclose this rate and is not on the list. These rates reflect percentages of April rents that REITs reported to have collected by the week ended May 29:

| Mall REITs rent collection rate for April | ||

| Tanger Factory Outlet Centers | [SKT] | 12.0% |

| Macerich | [MAC] | 26.0% |

| CBL Property Group | [CBL] | 27.0% |

| Washington Prime Group | [WPG] | 30.0% |

| Seritage Growth Properties | [SRG] | 47.0% |

| Retail Property of America | [RPAI] | 52.0% |

| RPT Realty | [RPT] | 57.8% |

| Kimco Realty Corp | [KIM] | 60.0% |

| Regency Centers | [REG] | 62.0% |

| Weingarten Realty Investors | [WRI] | 64.0% |

| Whitestone REIT | [WSR] | 64.0% |

| Brixmore Property Group | [BRX] | 66.0% |

| Cedar Realty Trust | [CDR] | 70.0% |

And it’s getting ugly. For example, #3 on the list, CBL, which has over 100 malls in 26 states, many of them serving less affluent areas, said in an SEC filing today that it has “elected to not make the $11.8 million interest payment” due on June 1 on its 5.25% unsecured notes. If CBL doesn’t make the payment within the 30-day grace period, it will be in default. CBL’s shares are down to about 26 cents. This REIT is a goner.

Office CMBS: The delinquency rate for office properties ticked up to 2.4% in May, from 1.92% in April, according to Trepp,

Looking at office REITs, a more diverse picture emerges, with rent collection rates ranging from 83% to 98%, according to S&P Global Market Intelligence, with some landlords clearly having a hard time collecting rents, and others less so, at least for now:

| Office REITS rent collection rate for April | ||

| Vornado Realty Trust | [VNO] | 83.0% |

| Douglas Emmett | [DEI] | 87.0% |

| SL Green Realty | [SLG] | 87.8% |

| Hudson Pacific Properties | [HPP] | 93.0% |

| Cousins Properties | [CUZ] | 95.0% |

| Office Properties Income Trust | [OPI] | 96.0% |

| City Office REIT | [CIO] | 98.0% |

| Equity Commonwealth | [EQC] | 98.0% |

CMBS delinquencies to set a new record in June?

The overall CMBS delinquency rate could have been worse for May and is likely to get worse for June, Trepp said.

A month ago, in its report for April, Trepp found that about 8% of the loans by loan balance missed their April payment. If 30 days later (at the end of May), all those loans would have been deemed 30 days delinquent, it would have pushed the overall delinquency rate for May to over 10%, “which would have threatened the all-time high recorded in 2012,” Trepp said.

But instead of 8%, only 4.98% were deemed 30 days delinquent. And this is somewhat in the eye of the beholder. Some loans remained in the “grace” period or in the “beyond grace” period, and were not considered delinquent, while others entered into forbearance agreements and thereby reverted to “current” without having made a payment.

But be patient, in terms of setting new records. June’s delinquencies are hanging out there. According to Trepp, about 7.6% of the loans missed their May payments but at the end of May were still less than 30 days delinquent. If they don’t revert to current via a forbearance agreement or a surprise payment, they’ll be 30 days delinquent at the end of June. And even if this happens to only part of those loans, a new record may well be set.

As far as CMBS is concerned, June is just the third month into this phase. In the wake of the Financial Crisis, the peak delinquency rate of Trepp’s index occurred four years after the Lehman shock. Now, three months into it, delinquencies are already gunning for a record.

Are the Work-from-Home-Folks Moving to Cheaper Pastures? Read… Rents in the Most Expensive Cities Drop. Oil Patch Gets Hit Too. But Massive Gains in Other Cities

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I am actually pretty surprised that supply chains held up this well.

“Industrial properties are a still fairly hot sector, whose delinquency rate of 1.82% was less than 1/10th the delinquency rate of Lodging.”

Bonds – Keep your eyes on the Bonds – Bonds now have a default risk that no one expected years ago (Well almost no one) . So, Low interest, Default Risk… and Liquidity Issues, could accelerate.. if the market de stabilizes – If the Bond Market goes “BLOOEY” then all hell breaks loose…

Tis but a scratch!

I have full faith in the feds ability to print there way out of this.

Ditto. This is a hung slider fat across the plate and lined up on the sweet spot to be taken outta the park by Jerome . Money printer go Brrrrrrrrrrr.

I recall hearing stories of Ceaușescu’s speech being met with booing and heckeling was the moment everybody knew his power was over.

With the memes that WallStreetBets is putting out making fun of J Pow, I can’t help but wonder if a similar moment is approaching for the Fed.

Cannot. It’s done.

Counterfeit their way out of it. More accurate.

FED can buy bonds but they can’t print money, jobs or income so insolvency is still on the horizon.

But, they can “digitally create money…” Jerome Brrr is handing out liquidity from space now; the problem is getting people to spend it. Europeans are NOT coming to our shores to spend this summer, and we are not headed anywhere either. I laughed at Mark Zandi’s “This will be the shortest recession in history” statement, today. He must be so drunk on Koolaid, the wagon ran his ass over…

California wants to let commercial tenants break their leases and walk away. They say, as California goes, so goes the nation. America is about to become very tenant friendly.

I was early in my rent control/regulation prediction, but I could see this coming for the last ten years.

This will also drain credit though and kill new investment. There is no future here.

Drain on credit?

The credit spigot is wide open and the stream is endless.

You really have not been paying attention.

Money is just number on a computer.

Really? Play banker for a minute please. How do you underwrite your 2MM square foot collateral with basically hundreds of month-to-month or maybe even day-to-day leases? On that basis, do you use land value less demolition costs as the valuation methodology? Over what term would you as lessor amortize any TI contributions. Right, no TI concessions. It doesn’t matter if one is paying attention if one is watching the cartoons, concession stand adverts and newsreels and not thinking about the movie. So you think the FED is going to backstop every commercial loan in Merika and maybe many outside the US? Stop paying attention to the Brrrrrr GIfs and think beyond the popular memes. Eventually, the currency gets repudiated and then what? Have you ever seen a vacant or near-vacant mall? Have you ever thought about the expenses that can’t be passed through? People that can borrow aren’t because the yield is inadequate to offset the perceived risk. So keep printing. The only people borrowing the money will be the ones who need it so bad you shuddnt lend it to them. In 1990-1994, we basically had no-bid CRE markets. Its true. The FED wont stop digging because they can’t and they won’t hit a bottom until they stop digging. But again, they cannot. They are printing not as a matter of principal, but panic desperation.

You extend and pretend, cook the books, EBITABADABADOO, money printer go brrrr like a boss and make it rain!!

What crazy logical gobbledygook are you talking about?

Amused You are the one that hasn’t been paying attention Money is Gold and nothing else

I hear you.

All of this is infuriating.

I’m glad I’m not the only one who vents.

Well in that case, we Americans can just let the Federal Reserve pay our taxes for us, right? That would be fair.

So,if corporations are people, why should they have any advantages over real people?

The smaller a business is, the greater should be their relative bailout from the Fed, that is, Jane landlady gets X$ relief for her five unit apartment house. Big commercial REIT should gets the same Xdollar amount, no more, no less, for their shopping center with five tenants.

To hell with corpeople and their special advantages.

Why would a banker lend to a borrower who has little to no income?

Seems like there are a lot of weird off the wall assumptions made about the FED’s ability to inject money into the system. As far as I know, the FED can not buy anything other than government backed securities.. They just can’t create money out of thin air and buy stuff.. So with out government backed marketable assets they can’t do much other than jaw bone. So where is all this monetization going to come from?

S’ok, we won’t need new construction investment in a lot of these sectors, especially Commercial, for a long time.

Until people go back to work – in offices, not homes – we don’t need new office towers. Until they decide to go out shopping – at malls, not online – we don’t need new stores.

There was no new investments due to NKMBYs anyway.

Nothing to lose.

There are thousands of bills proposed every year in the California legislature that never go anywhere. This is just another proposal. Until the governor signs it, it’s nothing.

And besides, you can break or renegotiate a lease in bankruptcy, no problem. That’s done routinely.

Well, there are certain realities here, if those tenants have zero ability to pay in the first place, then it wouldn’t matter even if they couldn’t break the lease.

What is going to be interesting is the unintended consequences… laws like these are never well thought out, I wonder if these could be applied by companies with less than favorable leases who wants to renegotiate… thinking may be Cheesecake factories of the world, but if they can do it, so could a Starbucks or a Chipotle… I wonder what impact it might have on franchisees like McDonalds….

It would be actually very interesting to see.

In the world I live in the natural progression of commercial real estate is From pavement to road bond and then moooooo says the cow. Pizza holes and over priced tacos and coffee do not fill the void. Money printer is still going Brrrrrrrrrrrr. Powell will print a 100 trillion to keep this fiat bitch alive and kill off 50% of the economy while printing. Jerome has to play it to the bone.Congress will applaud , the courts uses the old kings trick of lack of “standing” . The executive will be drooling on themselves between naps and their Metamucil dosing. Good grief Charlie Brown here comes Lucy with the football.

They may unwind the entire CA redevelopment agency malinvestment cycle. State abolished the agency not long ago but the overhang still exists. Some of this is (mostly low income) residential built over retail, not sure how it will play out. Without the shops and consumers spending, the promenade is a ghetto. This latest Fed Wall St bailout should produce more of franchise America, while SB dies, but where are they going to go? A reallocation, new products, lower price menus while the good RE is taken, and the property is locked up in litigation, and bankruptcy. Consumers who stop discretionary spending find they don’t miss the products, and are slow to return.

Add this to another pile of bad news/data that seems to be non stop daily so you know what this means, market rally tomorrow and in June, almost too easy to predict now at this point.

The market is toast. Retail traders suck.

^^ this type of comments, which is now probably 50% of the comments lately reminds me of the early days of the 2007 crisis: when the extent of delinquent subprime mortgage was only trickling slowly and when the Bernanke was still holding it together (and in denial) and when Cramer was still saying this:

This ain’t 2007 Dorthy, and you ain’t in Kansas anymore. The generals who fight the last war are the ones who lose…..

Trust me, I am with you on this sentiment, I am merely pointing out the absurdity of it all. Today is another perfect example, rally mode 3 days straight with more horrible data, everything is priced in right? Only thing I will say is unlike 07, Uncle Ben didn’t go as crazy as what the FED is now and act as unlimited backstop to the market. Quiet when the market is roaring back up now with utmost exuberance but even tiny bit of drop again, here comes uncle Jerome to save the day.

First, money is being destroyed by debt default much faster than all the central banks combined are able to replace it.

Second, if you look at what is really happening, the Fed is reducing its purchases not increasing them. They do not want to be stuck with worthless assets any more than anyone else.

I understand the market is continuing its irrationality, and that the perception is that the market for overvalued assets is unlimited, but I can assure you that is not reality.

The market is making some some truly absurd assumptions, and when they turn out to be false, it will have to face reality, something it has avoided doing for over a decade.

Jdog,

Most of us here know what you are saying is the absolute truth. We are just memeing away at the craziness of it all.

However, what you have said has been the truth for years and here we are still being propped up.

So we hear you, we undestand and we agree, but…

Jdog,

While I agree there is some currency that is going to be destroyed through these defaults it will not exceed all the money being printed by the Fed and central banks.

The Fed is reducing their purchases because there seems to be infinite market liquidity. Their balance sheet is still around $7 trillion and this will not be easy to unwind.

With all this currency being pumped into the markets through massive QE from all governments and central banks the market is going to go up. Unfortunately it is one of the few places that you can park your money and potentially earn a return.

I agree that this will not end well but I see inflation and you see deflation. Stocks do OK in inflation. Bonds get killed.

Gold for the long term is my pick.

Noelck

Noelck ,

Look at every loan denominated in dollars world wide. That is the real scope of dollar destruction. Not just the loans in the US.

Now look at the leverage of a defaulted loan. A loan for a commercial building with a cost of $1 mill. which had a 20% down goes into foreclosure, that $200 K bought $800K of money destruction. Leverage works both ways. Imagine the amount of Commercial real estate that is going to go vacant over the next 6 mos. It is estimated that possibly 50% of restaurants will not survive. I would imagine that number would be higher for fitness centers. How many rent a car outlets will close? How about hotels and motels? How many malls? How many department stores? And this is just commercial real estate. The amount of money destruction is astronomical. The cost of of this is being estimated at 80 trillion worldwide and that is probably conservative. The thing is most of that money will be loans made in US dollars.

It’s strange when we have little idea what only six months ahead (Christmas) in the economy will look like. I mean besides knowing the Dow will be 30K. If unemployment is still over, say 10-12%, how can this country stand it?

Dow 30K? Why, that fits right in with the announcement of Moderna’s great vaccine test results, with millions made by Moderna executives selling their holdings, and an additional issue of more shares for the public.

America. Priceless.

i once worked at the Moderna plant when it was under construction in Norwood,Mass. once in awhile they would bring in a group of investors to observe the progress. I believe their research was on rna of cancer cells. They were counting on a public that believed only drugs and treatment were the way to go. Powerful entities spend a lot of money in the media to keep this illusion going.

It’s my new toy and I’m stuck on it , Money printer go brrrrrrrrrrrr. Freaking thing is durable! It took me a year to de – tox off of Pepe the Frog.

Stand what?

There is nothing the fed money printer cannot fix.

UBI helicopter V shaped yolo recovery incoming!

“If unemployment is still over, say 10-12%, how can this country stand it?”

Wow, Mr. Lee, that sounds like you are talking about real people and whether they are surviving. I seem to remember that someone in Treasury said unemployed workers are irrelevant (in considering the status of the economy). I hear locally all the time about how already families are in food crisis and some people have still not gotten their unemployment, and are relying on relatives and community relief support to get by. That is how the country is standing it right now, and these “middleman grifter” effers political cronies are still trying to figure out how to make a profit from their misery. The country will still be here I guess, sometimes crisis brings out the best in people and I hope helps them cut out the trash causing the problems–I hope there is a lot of that going to happen.

You’ve got that right Portia

Let them eat stocks…

The U.S. can and has withstood a Revolution, the War of 1812 (Washington burned), the Civil War (barely), decades of corruption, World War 1 with Spanish Flu as a kicker, the Great Depression, World War 2, and the civil rights revolution in the 1960s leading to the riotous year of 1968 with MLK assassinated, a presidential candidate assassinated, and the ensuing election of Nixon, followed a few years later by the crisis of Watergate and the decade of stagflation.

10-12% unemployment is a big problem, but it’s not in the league of any of the above. We’ll rise to the challenge and eventually tackle it. Though I’m mindful of Churchill’s words about Americans only getting around to doing the right thing after they’ve tried everything else.

‘In the wake of the Financial Crisis, the peak delinquency rates of CMBS occurred four years after the Lehman shock.’

Yet we keep hearing a theme: ‘well it was tough but it’s over now. Time to buy into a beaten down market’

This will call for a new edition of Popular Delusions and the Madness of Crowds (approx title)

It would be less bizarre if the market valuation wasn’t already tied with Sept. 1929 before the Cov-id shut down.

Funny thing on CNBC: a survey of CFO s had a slim majority thinking we would hit the 19000 Dow low again before moving ahead, while a large minority thought the bottom was over and a steady recovery was next.

All ‘technical analysis’ does is measure sentiment. But the brains of corporate US is almost totally divided on sentiment. All that metaphysical jargon about ‘200 day moving averages, head and shoulders tops’ etc. is BS.

‘Market internals’ have run into fundamentals. It doesn’t matter what the sentiment is when the music stops.

The difference between the game of musical chairs (origin of the expression about the music stopping) is that in the game only one chair is removed at a time. In this reality a bunch of chairs will be removed.

The market seemed more scared of bernie than any longterm coronavirus fallout. If anything populist/socialist sentiment is rolling harder now than ever. Sure Biden isn’t Bernie, but how many additional AOC’s are going to show up in Congress riding the next political wave before these yay stocks rah rah rich people get it through their thick heads that the stock market is a growth delusion pinned on a dying/stagnant consumerist economy that hasn’t seen real growth in decades other than for the plutocrats.

If I hear one more “covid victim” complain about their *massively overvalued* 401k and how unfortunate they are (even though everything has bounced back already) I’m gonna snap.

“The Market” “scared of Bernie”. [rueful laugh]

No offense, rhodium, but generalizing about who is scared of Bernie misses the point. It’s pretty specific that certain political groups are the ones most scared of Bernie, as he directly threatens their income flow from their donor class. The Democrats hate Progressives with a red hot passion, as they would loathe anyone getting in between them and their lobbyists and carefully cultivated donors. As a Vermonter now, I love Bernie as a genuine human being, but politics and speech as money get in the way of anyone who has to employ people to work on their campaigns. Jeff Weaver has a lot more in common with Parscale than he would care to admit–he wants a permanent lucrative political consultant income. Bernie says he is a Democratic Socialist, but few people really look at his long, long, very active record. The panic about him is really overblown by the establishment who are panicky about losing their carefully constructed money flow, which is NOT from small donors of the general public.

It is the magnitudes of both the rate of change and the degree of change that are difficult to get to grip with.

Excellent book mention!

Extraordinary Popular Delusions and the Madness of Crowds, Charles McKay.

Link to free text for this classic historic book:

http://www.gutenberg.org/ebooks/24518

It just goes to show how the value of

any asset class can be quickly decimated.

I fear it is too late to prevent the dominos

from falling now.

If the economy fails to recover. does the dollar falter and take our government with it ?

Dollar falter? Definitely Government with it? Hopefully Can they start with that witch Pelosi and Schumer please

Well, some would say that, in many respects it depends on how other economies fare, in sovereign debt management amongst other things.

If enough go the way of Argentina (maybe soon to include Turkey and Brazil, at some point Italy) in terms of default on sovereign debt, the dollar could retain comparative value and so its reserve currency status. That alone may go a long way getting your economy through.

I appreciate there’s a lot of maybe in and around that though.

Of course people will prioritize housing more than anything, but that might mean that they are skipping some other payment, either car payment or credit cards.

I don’t know if Wolf has heard about this, but some friends told me that Wells Fargo is now suspending credit to most independent car dealership. So ABS backed by car payments might be the next domino to fall.

MonkeyBusiness,

Yeah, I saw the WF deal. WF has been pulling back from all kinds of lending: PPP, jumbo mortgages, now used vehicle financing, and who knows what all. WF’s problem is that it is bumping into the ceiling imposed on it by regulators as punishment. It’s not allowed to grow its loan book. So it stops lending in some areas in order to continue lending in other areas.

Some of this is a WF-specific issue. If you’re really worried about auto loans, you can tighten up your underwriting and only take rock-solid deals. Your risks would be minimal and you’re still making some money, but you’d make a lot fewer deals.

WF did say that it will maintain its lending with large independent dealers with which it had a long solid relationship.

It appears that their moves are fairly well calculated. They are backing off the HELOCS in realization that a lot of home equity is based on unrealistic values, and they are backing off vehicle financing due to an unprecedented glut in the market which will affect values going forward. I would expect they are also taking a cautious approach to commercial property loans..

The smart money among the banks is JP Morgan. If they are backing off lending to certain segments, you can probably be sure that those segments will be the most impacted.

That used to be the thinking. And why even risky borrowers were given AAA ratings when their mortgages were sliced/diced and sold as securities before 2009.

Not any more. With foreclosure proceedings now taking up to three years in some states, bailout programs and banks reluctant to take control of an underwater property, paying the mortgage has slipped from a priority in times of fiscal hardship.

Paying the car is now the priority. Because that will still be repoed rather quickly and a car is needed to get to work for lots of folks.

“Of course people will prioritize housing more than anything, but that might mean that they are skipping some other payment, either car payment or credit cards.”

Had a saying in my days in the auto biz…. “People will make their car payment first because you can live in your car, but you can’t drive your house.”

Measure of American decline…that saying really wasn’t common before the “old days” of 2009..

Maybe not for you younger folks cas,,, but I lived in my car at various times starting in 1960 era, and have been knowing others who have done so rather consistently since then,,, by choice.

Read about how many people, actually working folks with jobs doing exactly that right now in the bay area, and it’s very sad that an entire segment of working people cannot afford to live anywhere near where they work. And to be sure that cannot continue without serious social consequences, perhaps part of the foundational causes what we are seeing right now in many of these places.

If CMBS debt is in fact repackaged ala JP / Fed, HOW does it hit the taxpayers’ pocketbook? WHEN will any of the ongoing SPV bailouts hit the taxpayers’ pocketbook? Is that what all these protests and rallies are really about ?

The govt bails out the banks, etc, then tells taxpayers the nat’l debt is too high to give them any relief. PAYGO, etc., ad nauseum. It doesn’t matter if it has happened yet, it’s just the spiel. I think the protests and rallies are about the constant lies, myself. When people realize they’re just being strung along at their own expense and it’s killing them.

Of course it will hit their pocketbooks It’s been decimating everybodies pocketbooks since 1913 right? It’s just getting exponentially worse by the day Got Gold?

They repackage it for investors, and the worse shape it is in the higher the yield the faster it sells. ETFs buy the junk, and SPV buys the ETF and Fed buys the SPV (at 10X). Why don’t they just raise the interest rate and cut all the subterfuge. We all know government is bankrupt, put Treasury debt in various tranches, bundle it, and sell it to us at a decent rate of return, cut the dollar loose, and forget the income tax. Problem there is they would have to label the credit rating honestly, and that ruins everything.

Beardawg.

I agree, general distress has to be factor. But I doubt any of us would not feel sorry for the guy or his family.

Wolf,

Thanks Wolf. No mention of Simon Properties.

John,

It’s called Simon Property Group [SPG] – go look for it again in the Retail CMBS section, where you will find this “Simon Property Group [SPG], the largest of the mall REITs, does not disclose this rate and is not on the list.”

Or Colony Capital which defaulted a couple of weeks ago.

Wolf,

Interesting observation with the afternoon sell off of these stocks. I want to call it the California east coast sell early afternoon. Just an observation. Speculating of course.

1) There are poor Blacks, Latinos and White. Militant union riots sent good paying jobs from Johnston PA to China.

2) VIP pedigree co-op maintenance fee, on 5th Ave & 80’s NYC, cost more than 3 bdr apt rent in Harlem, but 3 bdr Harlem apartments are selling for almost $1M.

3) NYC police force is larger than the FBI. DeBilio will cut city jobs,

but not NYC police force to prevent Macy’s looting repetitions.

4) NYC retailers cannot no longer breath. Retail workers will be on furlough, or be laid off. Harlem apartments will cost less.

5) The Scots liberal imperialism took over other countries for their

own good, not just to spread Christianity. Scottish Imperialism offered better school, better hospitals, better law, better jobs and money for the poor.

6) A reciprocal ME Liberal Colonialism in colleges & online education, ME law, children hospitals, jobs and money for the poor.

7) NYC is changing for 30Y, but mayor DeBilio don’t get it.

Okay Wolf so now the $64K question?

I was on the same path as you several months ago with the big short we had on. Worked out real well for me.

Seeing all of this including some of todays all time highs I’m kinda thinking its time to put on another big short.

But the question is when will the chickens come home to roost?

Straight up everyday is just frightening….

Maybe some of your astute readers can chime in

I do respect them and you

My two cents.

People are figuring out that even if there is a second wave of virus, the economy will continue to open up. There is no turning back once things start. This is out of economic necessity. People need to eat. This also means quarter-to-quarter comps will likely start improving soon.

Also, with the Fed’s threat of never-ending money printing and interest rate suppression, there could be a lot of stock market support in the short term. Most people selling stock today don’t have the discipline to wait it out. They see their cash losing money to inflation, and they go buy something else. The reach for yield continues more than ever, with interest rates now down to nothing.

I think this can continue for a while because there are many S&P companies still down 25-50% from their highs of last year. People still see opportunity there, and that’s why we see a rotation out of overpriced tech names to “value” companies. All the money that has been going into tech has to go somewhere else.

Lots of reputable people are saying to buy gold. I don’t argue with that given all the money printing we will surely see in our future.

If you could only short Police Union Futures…these guys are headed for replacement by techno solutions.

I would not put any money on that one. Police unions are extremely powerful, as well as corrupt, and will not go down with out a very bloody fight….

This disconnect is truly frightening. But I’m staying away from shorting this until the Fed stops QE, as it did on Jan 1 through Feb. This market cannot stand on its own. The Fed has cut QE way back, but it hasn’t stopped yet. So I’m not shorting.

Even if the Fed has cut back QE to 5 billion a day, its still way above the rate they were doing from 08 to 2016.

The thing a lot of people just don’t seem to understand is you cannot replace production with a printing press. Production is wealth, printing money is not. Printing does not take the place of production.

You can print all the money you want and still end up in poverty.

As long as the Chinese still accepts US Dollar, we are fine.

Remember, you are only poor if you have no money or your money is no good.

Also even if we are printing, other countries are doing the same. I certainly don’t believe that the US is the cleanest dirty shirt out there. We have a ton of derivatives sitting out there, ready to be detonated.

Who are these “people” you refer to? I only see a handful of people that matter, and they are on the Federal Reserve Board. They obviously believe money printing is the way to go, so we have to accept that and plan accordingly.

That said, I agree with the premise of your comment. The Fed is making very bad decisions, and all signs indicate it will stubbornly continue down this path until there is a major crisis that it cannot control.

Worship of the Fed has become a religion in every sense. The problem is religion is based on faith, and not facts or understanding of science and reality.

The Fed is not omnipotent. It cannot ignore the laws of economics anymore than it can ignore physics or gravity. It may be able to postpone the inevitable, but it cannot create an alternate reality.

The Fed has created the biggest debt based bubble in history, and distorted the entire world economy to do it. It was quite a trick, but it was a trick. They have not changed the basic rules of economics. In economics as in physics, every action has an equal and opposite reaction.

Physics? I don’t agree.

The Fed prints money at will. It’s a decision made by men, not physics. As a consequence, the price of everything rises.

There will be limitations to what the Fed can do, but those limitations will NOT be dictated by physics. The limits will be put in place by people that have more political power than the Fed. Currently, I don’t see any of those people around.

If you think the Fed will act reasonably or ethically in the face of economic challenges, you are disregarding the Fed’s actions over the past 10 years.

There are more consequences to printing money than inflation, and the issue is not physics, it is economics. Economics has laws that cannot be denied the same as physics has laws. The Fed has been doing everything it can possibly do to avoid the consequences of it’s actions because they realize that when the reckoning comes, it is going to be apocalyptic. The repricing of assets is not going to be just a revision to the mean, it will carry with it the momentum of the excess of extending those valuations far beyond a normal cycle.

There is no stopping the deterioration that is now happening in the economy. It will continue and get much, much worse. To prop up the stock market while the economy crumbles is a fools errand. IMO they are simply buying time for the wealthy to liquidate while the average Joe’s pension funds and 401K’s buy them out at high valuations. After which time the Fed will liquidate and the market will reprice. As always happens, weak money will then sell out at the bottom, and strong money will repurchase their positions at pennies on the dollar. In the end, the wealthy will still own all the assets, just at a much lower cost basis….

Think you’re on the wrong track trying to equate economics with physics jpup.

Known far and wide as ”the dismal science” for a very good reason, economics is really just one more of the sorry social set of theories, more or less just opinions based on limited data.

While it may be comforting to some to theorize that various combinations of social events regarding money, etc., (as in theft of wages, etc., ) will end up with consistent results, (as in infinitely increased net worth,) as in the hard sciences of physics and chemistry, so far IMO that theory is far from proven, and enjoys the same degree of validity as the theories of the other social sciences.

“In the end, the wealthy will still own all the assets, just at a much lower cost basis….”

jdog, I call that “profit-taking” and it’s never been an accident, it’s definitely on purpose

Economics is based primarily on mathematics, and you can’t change the laws of mathematics….

As Danielle DiMartino says you can’t print jobs.

Wolf,

Forgive my incomplete comment on SPG. Simon Property Group. Always thought commercial mortgage backed securities were lumped together with other securities and used as collateral. That was some move today on SPG. Seems like you might have some sway with your return comment towards me earlier today.