But auto sales had already dropped three years in a row — before Covid.

By Nick Corbishley, for WOLF STREET:

The finance divisions of automakers, which dominate the UK’s auto finance sector, could soon be in trouble, and the industry lobby is now badgering the government and the Bank of England for a bailout. Some 480,000 drivers have already applied for a three-month payment holiday on their car loan, reports the Finance and Leasing Association (FLA), which adds, “The FLA urges the Government and Bank of England to open up financial support schemes to all lenders, including non-banks, so that they can meet the significant current demand for forbearance and provide new lending when the economy re-opens.”

In April, new vehicle sales collapsed by 97% year-over-year, after having plunged by 42% in March, according to the Society of Motor Manufacturers and Traders (SMMT). Unlike in the U.S., British car dealerships are not considered by the government to be essential businesses and had to close during the lockdown that started in late March.

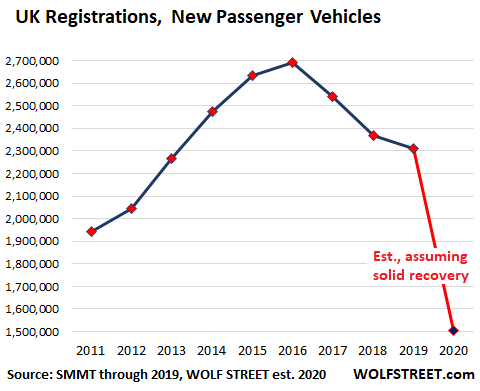

But UK auto sales already declined in the three years before Covid-19. By 2019 sales were down 14% from 2016. For the first four months of 2020, sales are down 43% according to SMMT. Given another 97% collapse in May, as dealerships remained closed, and assuming a solid recovery going forward, WOLF STREET estimates that sales for the whole year will be down around 35% (red line):

Reasons abound for the UK autoindustry’s multiyear decline, including broad consumer distrust of diesels following the endless disclosures since 2015 of industry-wide diesel emissions fraud, and stagnating consumer and business demand in the UK, due in part to the pervading uncertainty surrounding Brexit. Now, there’s Covid.

“These figures … make for exceptionally grim reading, not least for the hundreds of thousands of people whose livelihoods depend on the sector,” said SMMT’s CEO Mike Hawes.

For the UK’s auto finance sector, new business volumes in the market fell by 27% in March 2020, compared with the same month in 2019, and by 13% in Q1 2020 as a whole, according to FLA. The finance data for April and May haven’t been released yet, but given that auto sales collapsed by 97% in April and by a similar number in May, due to the lockdown, it’s unlikely to be pretty.

On Monday, June 1, dealerships will be allowed to reopen. But given the parlous state of the UK economy, with unemployment expected to surge from 3.9% in March well into double figures in the coming months, the demand for new debt-financed vehicles is likely to be weak. Many drivers — including the 480,000 on payments holiday — are already struggling to service their current auto finance arrangements.

UK motorists are even more dependent on debt for their car purchases than their American counterparts: 96% percent of all new-vehicle purchases in the UK were debt-financed (dominated by the UK’s version of leasing) in the twelve months to March 2020, according to FLA. In the US, the figure is 84.6%. The rate has risen in the UK by seven percentage points since March 2017.

The UK’s version of auto leasing — “personal contract plans,” or “PCP” — now account for 90% of all car finance deals. PCPs allow drivers to drive the car reasonable cheaply for the term of the agreement, which can be up to four years. They pay no deposit and make monthly payments that essentially cover the difference between the cost of “their” car and its predicted value at the end of the agreement (residual value), plus interest and fees. At the end of the term, the driver has a choice: return the vehicle; make a “balloon payment” for the residual value of the car and take full possession of it; or trade the car in and choose a new vehicle. Most opt for option three.

For car companies, it’s a way of churning fresh demand as finance deals end. Each time a driver upgrades to a new vehicle, the relinquished vehicle is placed on the used-vehicle market where supply is carefully controlled to ensure prices remain stable, as their residual values prop up the entire system. More and more of these used vehicles are also now being sold through PCPs.

As long as the system works, everyone appears to be happy. But what happens when the whole feedback loop stops moving, when demand slumps or collapses, when residual values are under heavy pressure, and when unemployed consumers have trouble making payments on their existing leases? This is why lobby groups such as UK Finance and FLA are badgering the British government and the Bank of England not only to expand their support of banks, but also to extend that support to non-bank lenders, including the over-stretched finance arms of the automakers. By Nick Corbishley, for WOLF STREET.

Airlines and automakers at the forefront. And it has only just begun. EU waives rules banning state aid. Ryanair, which doesn’t need a bailout, is furious. Read… It Starts: The Corporate Mega-Bailout Bonanza in Europe, Germany on Top

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

In the long run modern monetary policy is deflationary……this statement is a……what the hell moment for the fed.

As rates continue to drop and remain near zero responsible folks begin to adjust by saving more and consuming less because their retirement is at risk. If you plan to retire on a million dollars with a yield of 5%, that is a $50,000.00 per year income. At zero rates it’s zero. So one million spread over 30 years……from age 62 to 92……means you can spend only $33,000.00 per year in retirement with no extra in case you live longer.

Consumption drops and the modern fed and the wealthy all wonder what

to do next to dip into your wallet and relieve you of your savings……so they can keep running their businesses in an idiotic manner and stay in leadership.

If rates are at zero, why are you saving? Go and take out a loan.

If rates are negative – why haven’t you already taken out a loan? Take out as big a loan as you can. Keep taking out loans – what’s the downside?!?

Obviously the Fed & Central Banks will keep dropping rates into the negative as this will encourage consumers and businesses to take out loans and spend that money back into the economy.

Are you crazy? You seem to want interest rates to rise. That is a great way to choke off the economic recovery before it even gets started.

That would be a horrible mistake to make. Just like when they let Lehman Brothers go to the wall when they should have bailed them out and prevented the GFC altogether.

What a terrible error from the stupid Central Banksters.

No person,note person ,can borrow st zero interest.

Morgste rates are variable in the u.k.

Low interest rates punish savers, create asset bubbles, encourage excessive risk taking, and punish pension funds.

We will never get it but normalized interest rates is exactly what is needed.

“the used-vehicle market where supply is carefully controlled to ensure prices remain stable,”

How exactly is this done, and by whom?

Are new car manufacturers buying up/taking back used cars and then…what?

What are you saying happens to those cars?

Cars are currently basically designed to last so many miles before they wear out to the point, they are not worth repairing anymore. Usually about 200,000 miles. This means that automakers do effectively control the used market, to a large extent. This applies globally.

Right now, many automakers are also adding all kinds of “smart” junk like phone radio integration, that will no longer work after 10 years, maybe less, that will make your car feel outdated, with now useless knobs at the fingertips. More ominously, are the “driver assist” functions, which, will probably be expensive to fix, and at a certain point, you will probably be unable to get the parts, if you wanted to. If these functions don’t work, however, it’s possible that in some places, your car will fail certain safety checks, as well as, plummet the value for having broken useless car functions.

TR,

He had discussed the control of supply in the context of the UK equivalent of leasing (4 yrs, maybe 50k miles).

I’m not saying that manufacturers would not like to control used supply…but if they did I’m fairly sure that it would end up somewhere on their books (and I’m not sure that a 4 yr rental then crushing makes economic sense for anybody, including the manufacturers).

And if the cars aren’t being crushed…they are supplying some used mkt somewhere.

(If not, then the manufacturers are eating the cost…unlikely to gave been recouped in 4 yrs lease/rental)

The 200k/17 yr car lifetime is a separate issue…everything wears out.

But that is 4 times longer than the period discussed.

Cas127,

I am aware of that, I am referring to a different aspect of how automakers control the market. Which, has to be taken into account with leasing, because, the automakers control how long the cars last. This means the automakers can control almost every aspect of the market in roundabout ways; from the time it’s sold as a brand new car to the time it’s junked. They also control, roughly how much a car cost to repair a year and when. And thus influence the customers preferred lease term. These are important things to take in account.

Yes, stuff wears out, but, cars are made intentionally more expensive and difficult to repair than they need to be. Compared to everything else, cars, always seem to become, almost worthless, at a preset never changing time, right at about 200k miles; assuming, you don’t crash or abuse it. This isn’t even counting the automakers control over the parts supply chain, which, greatly impacts your ability and cost to keep your car running.

Also, he is talking about the UK, which, isn’t a democracy, the automakers can control the government’s laws on automobiles and everything related to financing.

Add all this up and yeah, automakers kinda control it all, especially in the UK. Although, they are still in competition to a limited extent with each other, to build roughly the same sets of cars for roughly the same price.

I would imagine wreckers and body repairs have something to do with it. Having a smash while on a lease can be expensive, so harvesting relatively new parts can be profitable since people would fix the car to avoid penalties, rather than write it off.

Especially since it becomes a real problem once the airbags have deployed and the crumple zones have crumpled. Here in Oz at least, getting a car roadworthy after airbag deployment is an expensive proposition, but what’s more expensive is being left holding the bill for a written off lease car.

If you know what you are doing, exporting those parts to other right hand drive nations would also be lucrative. In the former Commonwealth nations of Africa, newish parts for RHD cars going cheap would be like gold.

pcp is run by the manufacturers/importer. When the new car pcp runs out the car maker wont dump it on the British market when there is an oversupply. They will store or export them until demand is restored.

Why doesn’t the Government buy these used cars and scrap them? What are they waiting for?

They are the market makers aren’t they?!?

Covid will be the excuse that keeps on giving.

It will be used to hide all sorts of incompetence and fraud.

“I did it because of force majeure!!!”

The good news is, it will never be my fault, if I’m ever late again. CCP19 strikes again, delaying me. That dastardly coronavirus.

Excellent! I will update my being late excuses. Years ago, when asked why I was late to court, I would inform the judge: “El Niño” – alternating later, as the PC days arrived, with “La Niña” – with a brief aside in a more deferential tone of all time being some type of oscillation, now, since I was present, in forced simple harmony. Assessing correctly he was dealing with an idiot not yet hitting on all cylinders that morning, this usually worked. When pressed as to “How could this happen?”, well we all knew it was because of the “One Armed Man”.

Now the answer is simply: “Covid” (dropping the “19” so as not to be confused with a year time stamp, which the “19” is not). I like this. If Prince were still around he would eventually work this into a sign of some sort.

Any bets on when the Covid emoji arrives?

“Any bets on when the Covid emoji arrives?”

It already has, and it wears a mask, lol.

There exists a logo for the Xi virus “a unofficial name for CCP19”, could probably use that one.

It looks like Xi with snot blasting out it’s nose.

My tool kit contains a set of old Jaguar wrenches if that might help save the British E-car-nomy. Otherwise, SOL.

I would have loved to have bought a Welsh made TVR Griffith, but they do not seem to exist in real life – at least in the USA. They look cool as hell on the TVR website though, and I have seen one drive through London on YouTube.

Only one out of 25 people in the UK just write a check and pay cash for a new ride? Seriously? Nick, that’s one crazy stat! I guess the USA at one out of seven isn’t that much better.

Dad taught me, “If you can’t pay for it, you can’t afford it.” I’ll take that advice to my grave!

You have to consider that for independent contractors, contract workers and other categories leasing a car or paying it with a loan has fiscal advantages: there’s literally no incentive in paying cash in countries like Britain and France apart getting a discount on tag price.

Leases in particular are not considered a form of debt: they are a fixed monthly expense like, say, a mobile phone subscription or an utily contract. As such many countries have fiscal incentives on them, especially for independent contractors.

That’s about the same reason why Malta has become so hot among airlines over the past two/three years to register their aircraft there: tons and tons of fiscal incentives, from crazy short depreciation periods on interiors to even crazier deductions for engine maintenance, no matter where it’s carried out.

It will be fun to see what will happen to all those tax breaks now that governments worldwide face double digit budget shortfalls but cannot risk killing off whatever economy activity will be left after their genius plans.

I sense a lot of fiscal and legislative “creativity” coming up.

I’ve heard a debt counselor on TV say that vehicles are the ‘black hole of personal finance’ and to ‘never lease a car’

OK: never say ‘never’, because of course there are no doubt some attractive and rational deals out there depending on the incentives AND the requirement for a new car, e.g., sales.

It’s interesting to see the evolution of the rationale for leasing, at least in North America. The ‘sell’ began decades ago as incentive- based, almost entirely as a business expense write-off against taxes. It has ended with I would guess the majority of auto leases being taken out by people who will receive little such benefit from the scheme. At least in Canada, as leasing became common, there has been a pretty stiff crack-down on what portion is deductible. If you are just using it to get to work, not much.

Instead the dealer focuses on one thing: a lower monthly payment, or ‘more’ car for the same money. This is an aspirational, life style motive that doesn’t make financial sense.

An odd thing about the ‘more’: it’s usually entirely in the driver’s mind. There are some pretty exotic beasts even in Nanaimo now. Yesterday I parked in a rather seedy area behind an Aston Martin Rapide. So I noticed a car. Looked it up: begins at 275K Canadian.

But the TV ads showing passers-by fawning over an ‘they all look the same’ SUV?

NO ONE is looking at your auto! Only you are.

Back to leasing. It says a lot that there is a large company, Lease Busters, that for a hefty fee will get you out of your lease. There are also at any time numerous individuals offering large ‘you take over’ sums privately. One for five figures on Mortimer’s Vancouver RE Twitter last week for a Land Rover. Just take over payments of 1900 per month.

@nick kelly

Nobody buys a C$250k car. They lease it. And if you are paying $x per month you are rather driving a car that claims to cost $250k than a car that claims to cost $200k. So car manufacturers try to make the sale price as high as possible. This also makes leasing look cheaper. Finding stories about a lower total lease payment + residual payment than the sales price is not something that is hard.

Buy Some,

Doubt if your tools will help.

Your tools must be well worn out if you owned a Jaguar.

Another opportunity for the Fed to display its might and show its muscle by showering the industry with more bailout money. Meanwhile, savers/retirees get ZILCH. No interest for YOU. And now, no dividends either, looks like. I wondered how long it would take them to get around to cancelling our dividends, after all, they need that money for buy-backs.

Bank of England, not Fed.

Phase 2 re-opening in many cities tomorrow, and the new curfew due to all the riots and looting.

Bulish news is nobody talks about coronovirus anymore.

They still do, just not as the main news.

And once protesters and policemen get the virus it will be front page news again.

Rax:

Not here in the foothills of the Sierras!

Plenty of talk still of the virus…..economy trashed; mostly tourism…..from all over the world…..example: Yosemite National Park and so many other vacation/visit destinations.

Counties wondering what they are going to do when all the Gov. support monies are terminated; budgets will have huge tax shortfalls…..who or what is going to fill the gaps??????

No, it’s still major news here…..

andy,

Not quite. Lots of warnings now about a second outbreak due to people being too close together during the protests.

Part of the fun of car ownership in the UK is having to pay for car repairs due to the abysmal condition of the roads. From memory the current rule is that if a pot hole isn’t 4 inches deep then it isn’t a pot hole. With the country paying people £2500 a month to sit at home doing nothing i imagine they will need to increase the recognised pot hole depth from inches to feet.

All construction workers are now back at work in the UK, from what I see, and I should have thought road maintenance would be too, although I haven’t seen any just yet.

Actually the roads in my town, Manchester, have had massive repairs during the lockdown..not perfect but better….

The issue is huge.

From what I heard, the existence of financial arms greatly reduces the need in working capital for automakers themselves.

Here how it works : when a financed sale occurs, financial arm works like a bank. Cutomer gets the vehicle usage and a debt, financial arm gets the vehicle posession and the loan processing, but the automaker receives full instant cash from its financial arm.

Getting instant cash for the sale and paying the suppliers with many weeks delay … creates a very beneficial effect for car maker.

But I am afraid just to think about the liquidity stress for automaker when the wheel stops rolling.

So.

Like we didn’t see this one coming.

When a new car is in the way to the price of a house deposit, how else are they going to be paid for?

Even so – 97% of new car sales on PCP. Ouch.

So if someone is driving that new range rover or BMW, what it is most likely to say about them is not that they are ‘The Man’, but that they are truly all fur and no knickers.

Heart warming that :)

Tim, you just introduced me me to a new British expression. In Texas it would be “All hat, no cattle”

97% was drop in sales. But factories are closed also so not that big of a deal.

96% of new cars are financed. 90% of financed deals are pcp. So around 86.4% of new car sales are pcp. Not totally surprising. As consumer you are semi forced into them.

There is a European brand called Dacia. They are effectively Renault but made in Romania. Their cheapest model is about 9k(pounds). The equivalent from Ford or Vauxhall (GM) is 16k. Are all the silly toys worth the difference? Of course not.

These boys have been binging on the credit haven to inflate prices for years. Now they are going to get stung and I can’t wait for the demand to plunge. It’s actually rare (though I didn’t think quite as rare) to pay cash like I did 5 years ago for a second hand car.

Nick/Wolf. Are car loans securitized in the UK like the US?

Dacia fascinates me. I assume the vehicles are being sold profitably and that, in simple terms, there is a similar amount of steel, glass and plastic in, say, a Fiesta and a Sandero. Likewise, the ancillary costs (manufacturing in EU, delivery, preparation, marketing, warranty) must be about the same. The excuse ‘it is a twenty year old Clio’ doesn’t really hold water, does it?

Sandero is a bigger car than a fiesta with a smaller engine, worse suspension etc. The quality difference is noticeable when you drive it but the price difference is also very noticeable. Buying an off lease Ford/Peugeot is probably cheaper in the long run and you will have a better car. But not new. And that is what some people want

Andrew,

Yes they are, albeit not on quite the same scale as in the U.S. Many of the resulting auto loan ABS are, or at least were, highly rated. Alarms were already being sounded about the securitisation of auto loans in the UK three years ago, but it doesn’t look like they were heeded:

https://www.ft.com/content/7a343370-5ff6-11e7-91a7-502f7ee26895

Yes, concerns have actually been around for this in the UK for quite some time.

1) Fred : UK car registrations peaked in Q1 2017 @ 230M and were down to

209M in Q3 2018, or minus 21M // 21M ; 230M = 9% in less than 2Y. That sharp decline started a 1.5 years ago.

2) New car registration fell from 2.7M to 1.5M in Q1 2020,

The trend is down.

3) UK total registration was hit by : Brexit, CV19 and the oil business

collapse.

4) 90% of all new car registrations are leased. The most used cars are also leased.

5) Expired leases lead to new leases. But global recession will stop this cycle. Total UK car registrations will fall further.

The poor, the unemployed will not be qualify for loans or leasing.

6) New cars production will have to adjust and dealers will have to

drain their used cars swamp.

7) If UK gov will buy cars with lives older than cats, demand for used

cars between 1Y to 7Y will grow.

8) The bottom line : during the next recession UK car registrations

might fall from 230M below 200M to : 150M – 180M.

9) Scooters & electric bikes will do well. Local communities will cluster

together.

3) Oil business? It is not a big employer and close in skills to sea based wind mills. Which the government is supporting massively.

8) 230M? UK has a population of 60 million

9) In a lot of the UK you need a car. It is not Holland

Why would they even consider this sort of socialist solution?

This is a right-wing Tory Government under Boris Johnson – not some socialist dream led by Jeremy Corbyn!

These jokers in the auto finance industry have got to be joking.

Rely on your reserves and stop asking the Government for a handout!!

How ridiculous.

Britain is a capitalist country. If these freaks want socialism/communism – go to China!

‘PCP— now account for 90% of all car finance deals’

Fucking hell, I didn’t know the statistics were so dreadful. PCP is basically renting a car, all you pay for is the depreciation and monthly interest on the principal loan balance. It’s a way for people to ‘buy’ expensive cars that they couldn’t afford in the real world. It’s like an interest only mortgage on a property, except with an interest only mortgage you don’t pay any depreciation.

One minor correction to your article though, I believe you have to put a deposit down – usually the VAT amount of the sales price.