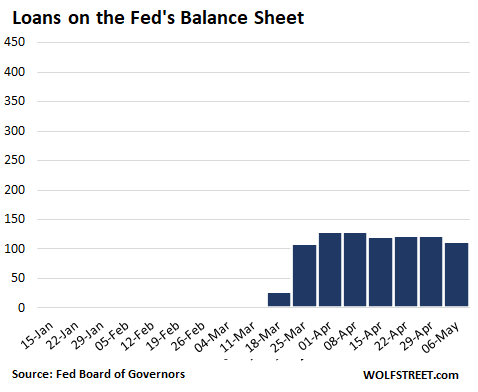

Loans to “SPVs” declined to lowest since March 25.

By Wolf Richter for WOLF STREET.

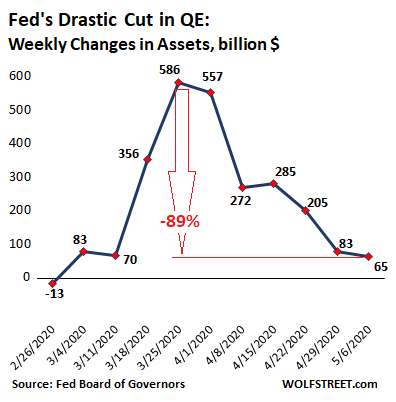

Total assets on the Fed’s balance sheet rose by $65 billion during the week ended May 6 — the smallest weekly increase since the week of February 26, when assets fell by $13 billion. And it was down 89% from peak-bailout in the week ended March 25. The chart depicts the weekly changes of total assets on Fed’s balance sheet:

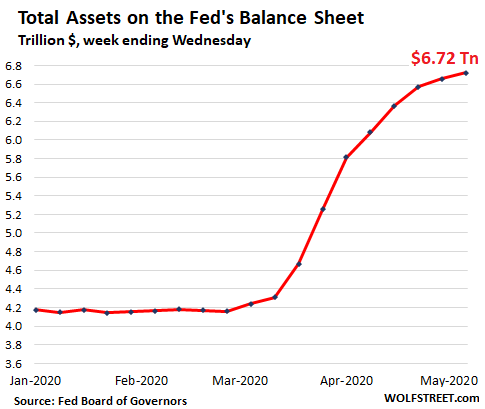

The chart below of the Fed’s total assets, now at $6.72 trillion, shows the effect of the reduced weekly QE binges: a flattening curve since peak-bailout of $586 billion in the week ended March 25:

The Fed slashed its purchases of Treasury securities. Mortgage-backed securities (MBS) and commercial mortgage-backed securities (CMBS), after falling last week, remained flat. Repurchase agreements (repos) remained essentially flat. Lending to Special Purpose Vehicles (SPVs) – through which the Fed said it would buy bonds, junk bonds, bond ETFs, etc. – actually fell, as the Fed still hasn’t bought any bonds or ETFs, junk or otherwise. But foreign central bank liquidity swaps ticked up, all of the increase being with the Bank of Japan, which now accounts for half of them.

Fed further slashes purchases of Treasury securities.

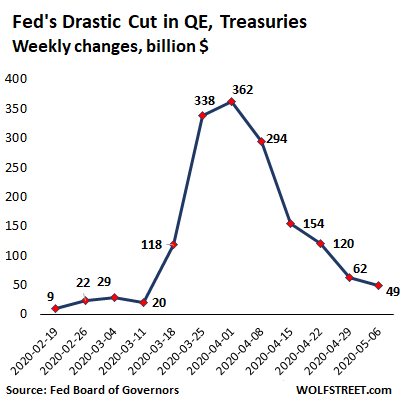

The Fed added only $49 billion of Treasury securities to its balance sheet during the week, the smallest amount since the market bailout began, down 86% from the $362 billion peak. The chart depicts the weekly changes of Treasury securities on the Fed’s balance sheet:

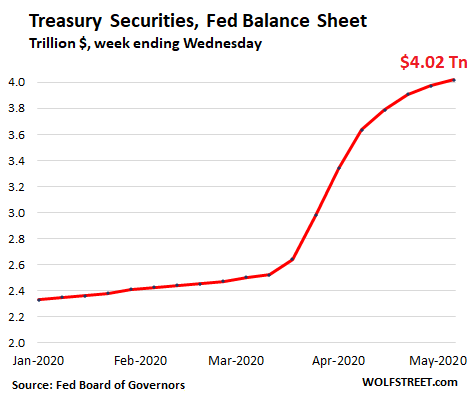

And the curve of Treasury securities has been flattening. The total is now $4.02 trillion:

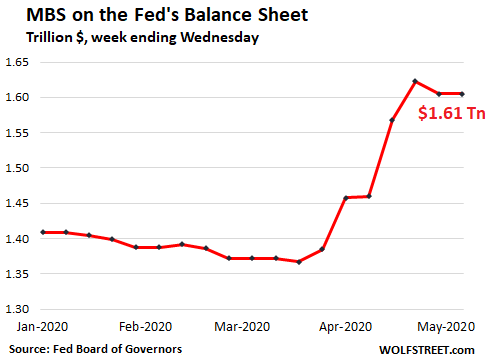

MBS purchases fell, purchases of CMBS remain small.

The Fed has slashed its purchases of government-backed mortgage-backed securities (“Agency MBS”) over the past six weeks (New York Fed transaction summary, net purchases, for the weeks ended):

- $157 billion (Mar 25)

- $145 billion (Apr 1)

- $109 billion (Apr 8)

- $58 billion (Apr 15)

- $56 billion (Apr 22)

- $38.5 billion (Apr 29)

- $30.5 billion (May 6)

The Fed is also buying government-backed multi-family “Agency CMBS” (mortgages for apartment buildings), but only in small amounts by Fed standards. It started doing this to bail out the CMBS market that had been thrown into turmoil when renters stopped making rent payments. According to the New York Fed, which does these operations, total CMBS purchased in the week ended May 6 was $3.4 billion. The CMBS are included in the MBS balances on the Fed’s balance sheet.

MBS trades take weeks to settle. The $30.5 billion in MBS the Fed bought this week will settle in May and June. But the Fed books MBS trades only after they settle, which causes the balance sheet to lag the actual trades.

Then there is the issue of pass-through principal payments. All holders of MBS, including the Fed, receive principal payments as the underlying mortgages are paid down or are paid off. With the current boom in mortgage refinancing due to historically low mortgage rates, these pass-through principal payments have swollen to a torrent.

To compensate for the pass-through principal payments and keep its MBS balance flat, the Fed would need to purchase a significant amount of MBS. If the Fed buys no MBS, the balance of MBS on its balance sheet would fall sharply.

The mix of reduced purchases, settlement dates, and pass-through principal payments caused the balance of MBS – which include CMBS – to fall by $18 billion last week and to remain flat this week, at $1.61 trillion:

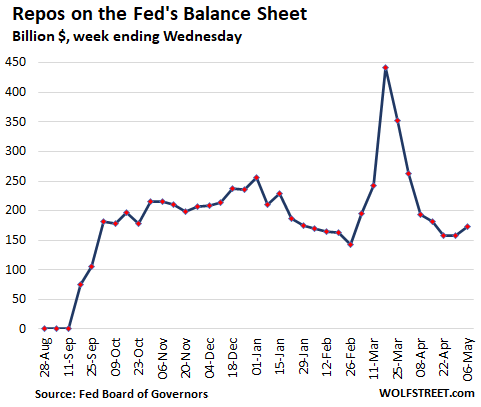

Repos languish.

The Fed has cut in half the amount of overnight repurchase agreements (repos) it offers from $1 trillion a day to $500 billion a day; and it has cut its term repo offers similarly. There has been little demand for these repos, and the majority of what is left on the balance sheet ($173 billion) are term repos from March:

“Loans” to SPVs & Primary Dealers declined.

The Fed’s multi-pronged strategy to bail out every aspect of the financial markets by buying a large variety of securities is based on loans that it extends to corporate entities it has set up, the Special Purpose Vehicles (SPVs), which then buy those assets. Via this scheme, the Fed is able in broad daylight to get around the limits imposed on it by the Federal Reserve Act. Congress, which knows what the Fed is doing, nods approvingly.

But that doesn’t mean that the Fed is actually doing what it said it might, or that it is doing it to the extent that Wall Street hoped and bet on it would. Total loans to these SPVs all combined fell again, now down to $113 billion, the lowest since March 25. The chart is on the same scale as the repo chart to allow those loans to grow into it:

These loans by category:

Primary Credit: fell to $26.5 billion from $43 billion a month ago. This Primary Market Corporate Credit Facility (PMCCF) lends to an SPV that can buy bonds directly from companies, including certain “fallen angel” junk bonds; it can also buy portions of syndicated loans or bonds at issuance. Some of the positions have unwound, and the SPV paid the associated loans back to the Fed.

Secondary credit: $0. This Secondary Market Corporate Credit Facility (SMCCF) is designed to lend to SPVs that purchase corporate bonds, bond ETFs, and junk-bond ETFs in the secondary market. None have been purchased yet.

Primary Dealer Credit Facility: fell to $15 billion from $36 billion three weeks earlier. These are the amounts the Fed lent to primary dealers to buy securities with. After the initial burst, some of the positions have been unwound.

Money Market Mutual Fund Liquidity Facility: fell to $43 billion from $53 billion a month ago. This SPV buys short-term commercial paper to bail out money-market funds.

Paycheck Protection Program Liquidity Facility: Rose to $25 billion, up from $8 billion two weeks ago. Amount that the Fed lent to the SPV to buy from the banks the government-guaranteed loans they issued to “small businesses” under the PPP program. The primary target of this SPV was Wells Fargo, which refused to participate in the PPP program because the Fed as banking regulator had imposed limits on its assets (loans), and Wells Fargo said it was bumping into this limit. The Fed then allowed Wells Fargo and other banks to offload their PPP loans to this SPV. During the second round of the PPP, Wells Fargo has successfully obtained many loans for its customers.

These loans to its SPVs show that the Fed still has not bought any junk bonds, fallen-angel junk bonds, bond ETFs, or junk bond ETFs. But the announcement in March that it might buy them, and the re-announcement last Monday that it might buy them starting in “early May” caused a huge rally in those asset classes.

The Fed’s purpose was to unfreeze the credit markets during the panic. Those markets are now steaming as investors are chasing yield. This removes the original reason for the Fed to buy those instruments. This is the effect of jawboning, and it works better than actually buying the assets – as long as the market believes it.

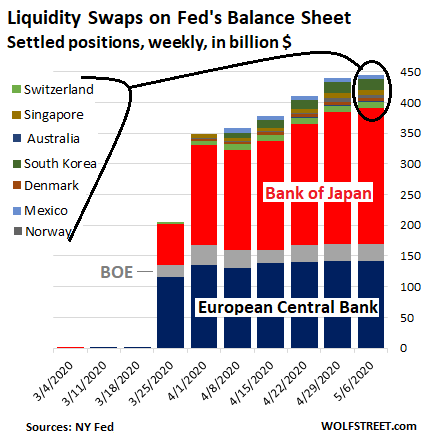

Central Bank Liquidity Swaps — half of them with Japan.

The Fed’s “dollar liquidity swap lines” with other central banks ticked up by $6 billion to $445 billion. All of that increase was with the Bank of Japan, which now accounts for $220 billion of the swaps, or nearly 50% of the total.

Swaps with the ECB, the second largest user, remained flat at $143 billion (32% of the total). Swaps with the Bank of England also remained flat at $28 billion (6% of the total).

The Fed’s swaps with the central banks of Australia, Denmark, Norway, Switzerland, Singapore, South Korea, and Mexico remained at the same relatively small level. The largest counterparty in the group is the Bank of Korea, with $17 billion in swaps.

The Fed’s swap lines with the central banks of Canada, Brazil, New Zealand, and Sweden were unused.

These swaps mature in either 7 days or 84 days. In essence, the Fed lends newly created dollars to another central bank and takes domestic currency as collateral, at the market exchange rate. When the swap matures, the Fed gets its dollars back, and the other central bank gets its own currency back. The balances by country are reported by the New York Fed.

If…

Since March 11, the Fed has printed $2.41 trillion. The purpose was to inflate asset prices across the spectrum. Surely, the Fed didn’t want Warren Buffett, one of the richest people on earth, to lose his shirt, so he and his empire had to be bailed out. The Fed also wanted to restart the chase for yield that makes investors reckless and counting on another bailout when needed. This $2.41 trillion was a gift to Wall Street and asset holders – the wealthier the asset holder, the bigger the gift.

If the Fed had spread that $2.34 trillion equally over the 130 million households in the US, each household would have received $18,535. For many households, this would have been welcome help to get through the crisis. But no. This was helicopter money for Wall Street.

I’d never imagined I’d ever see this sort of spike, though in recent years I added an upward arrow with “Debt out the wazoo” to my charts, not realizing just how factually accurate this technical term would become. Read… US National Debt Spiked by $1.5 trillion in 6 Weeks, to $25 trillion. Fed Monetized 90%

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I drop in and read these articles but my financial knowledge is weak relative to the average reader here so I rarely comment. I have questions more than insight. Can this helicopter money effectively continue ad-infinitum? Is there any chance of a correction to the financial system at the end of this (whatever this is)? As I live in the UK, is the same happening with the Bank of England here?

The BOE is following a similar program. They have an info graphic about it on their website. https://www.bankofengland.co.uk/coronavirus

The key bits in regards to this conversation are the last two headings. Lending money to companies by buying their securities and “supporting banks in lending to consumers are both for of bond buying and asset propping.

As to the long term consequences, its hard to say. One way or another the accounts have to be balanced eventually. This will either be done by sovereign debt default (like Greece post GFC), national bankruptcy (which is essentially what Iceland did after the GFC), or inflating the debt away which takes a long time but happens to an extent constantly. I hope you and your family are safe.

So Powell has gone full Elon Musk by pumping up shares and crushing shorts with nothing more than ̶l̶i̶e̶s̶ jawboning. Doesn’t he know this was the reason Twitter was created?

As a reminder, the Fed cannot send money to the people, only the Treasury can. But if the Fed and government had made some sort of arrangement wherein the people could have been sent 18k stimulus checks this probably might have significantly weakened the dollar, upsetting global markets. I do believe the Fed’s main agenda is to keep the dollar from either rising or sinking too much.

I do not recall the Congressional authorization for most if any of the acts listed above. What the Fed can or cannot do is merely an academic exercise.

agree and done for two reasons, to provide confidence to markets, and to run a trial balloon. QE was a permanent fixture, which was difficult to unwind. Nobody wants to see that again. The real problem a few months from now when the budget needs to be addressed. Congress will extract concessions (middle of campaign season) pointing out these numbers, and Feds corporate largesse, if it were spent on the unemployed, and consumers? Problem at election time the unemployment line is around the building and stocks ATH, another embarrassing situation. Right now ask yourself, who is the bigger political hack, Barr, or Powell?

sending everyone 18k would have significantly boosted GDP and surely strengthened the dollar, however The FED doesn’t print money for this purpose as it is a bank and it hates giving money away to its customers.

The growth in private debt must though eventually stop as the ability to service the debt even at very low rates of interest will be reached.

It’s simple, the higher the debt leverage, the lower the interest rate must be. Kenneth Rogoff already made the case recently that we need rates multiple percent in the negative, and why not? In an economist’s equation it all makes sense. No matter all of this may sound counter-intuitive from a free capital market point of view, but that are thoughts that are very century. And it’s true, if I can get a 30 year fixed at -3 percent, I’d happily load up on some overpriced real estate and thus contribute to our society’s prosperity.

Yaun,

I know your comment was mostly sarcasm, but for the newbies/MMT fascists…negative interest rates can cause multiple problems (besides the very big one of strongly discouraging use of the subzero’d currency at all…) – a quick to appear one is…the disappearance of money from banks (tanking the multiplier) as savers recoil from the certainty of loss and move their savings under the mattress, buried in the backyard, etc.

But, since MMT’ers believe they have unfettered rights to both your pre and post tax earnings, I’m sure they would have no problem with warrantless searches of your home, confiscation of “hidden” savings, and other post-Constitutional activities “necessary” to make MMT work and “save” the country.

Negative interest rates mean that assets become an expense and a burden. That screws up everything and totally. Rogoff is an insidious propagandist, and I want to know which hedge fund with a massive position on this pays him to spread this stuff around.

Rogoff is a communist ideologue.

The question should be why is he given such a platform to peddle his inane ideas.

His last project syndicate article is crap. All he is saying is lets tax people who have money in the bank, abolish cash and have the government control everything, naturally he considers himself as being in the class of governments apparatchiks doing the control.

The solution if any will come through a period of austerity and debt restructuring and by rewarding savers instead of punishing them. Economists have long forgotten what the purpose of an economy is, that is why they are lost in mathematical machinations pretending to validate they pet projects, we are doomed if we discard common sense and listen to expert absurdities.

Federal UE benefits of $600/week = $18K in 30 weeks.

Lisa,

The Fed can set up an SPV and lend to that SPV, and that SPV can buy junk-pots-and-pans and old BBB-rated bicycles from people, no problem ?

The Fed cannot buy corporate bonds either. So it sets up an SPV and lends to the SPV and the SPV buys the junk bonds.

Wolf,

What is your view of the legality of the Fed continuing to use the SPV circumvention of law to buy junk if Congress were to pass a law expressly prohibiting such behavior, in other words, prohibiting the Fed from purchasing junk or lending money to any SPV or similar entity that buys any quantity of any kind of junk whatsoever, even one junk bike? Of course, this Congress would never consider passing such a law so its really academic for now.

NY Geezer,

Since when does my view of legality matter to the Fed? ?

It’s not the Fed that I blame. It’s Congress. Congress could stop this. Congress could decide that these SPVs violate the spirit of the Federal Reserve Act, and hold some hearings on it, or it could start investigating and auditing the Fed and put pressure on it to quit this stuff, or it could amend the Act. But Congress — the best Congress money can buy — loves this money printing and whatever schemes the Fed comes up with.

@ Wolf –

You should blame the FED as well as Congress. The FED/Bankers/Wall Street are larcenous bastards benefitting from the theft, as well as the bought off Congress.

You could adopt the common fall back position of blaming the voter. But I know you can see through that oft quoted charade.

No ‘moral hazard’s or ‘creative destruction ‘ capatalism is dead, this is socialism for billionaires

Make Bankruptcy free and all inclusive, then nationalise banks and start again, not least set bank rate at 5%

Then sit back and enjoy

Finally might help to send a few of them to gaol

Absolutely, bloomberg was reporting that there is 4.8 trillion in cash in market funds. Clearly thee is enough savers out there to pick the pieces in a bankruptcy court, savers should be rewarded, not punished.

Capitalism is alive and well. The capitalists keep competing to acquire more capital and further fortify their positions against the serfs. Free markets are dying, yes. That is what concentrated wealth and power does – diminsh free markets. Is not the goal of every good Capitalist to concentrate wealth and power, own monopolies and suppress free markets?

From the Encyclopaedia Brittannica:

“…On January 1, 1991, the Soviet Union was the largest country in the world […] Within a year, the Soviet Union had ceased to exist…”

As Mark Twain is said to have observed, “History doesn’t repeat itself but it often rhymes”. When one studies the multiple causes of the Soviet Union collapse (political turmoil, mismanaged economy, military expense, Afghanistan, social unrest, Chernobyl disaster) one really wonders which empire will be the next to fall.

It seems to me that the USA considers itself immune to these kinds of phenomena. When I observe everything that is now going on, I am starting to have some doubts.

No empire in history has lasted forever, after all.

Those investors are like pirahna. About as smart too.

I ask me the question, why the european and japanese banks have so a huge demand for US Dollar?

Sounds like the Drug Dealer “Fed” are playing it by ear with no plan. Like a drug dealer, give the users a bit of stimulus to get by. But the users always wants more. The dealer would say “I’ll give you some stimulus next month, if you can do this job for me this month. But then They find out the dealer, like all drug dealers can’t be trusted.

Wolf I just want to thank you for being active in keeping us updated. One thing I learned from reading your articles, This financial system doesn’t make any more sense to me….

This thing now has a life of its own, and Fed was able to back off in part because situation is worse in other places. US is hot dollar destination. Rumors to the effect the EURO might crack. Takes more dollars to buy a dollar, so DXY rises, impoverishing America. The less leadership US shows the more ROW piles into off balance sheet account. Swap lines are there to keep exchange rates within reason which is why nobody is using them. They want to buy dollar assets, pump them and currency higher, buys currency derivatives, (rates are low thanks Fed) probably through US banks. Forgot what comes after pump?

Wolf Richter:

> Since March 11, the Fed has printed $2.41 trillion.

> […] the wealthier the asset holder,

> the bigger the gift.

The last thing a government wants to do

is make a decision that might trigger someone;

so, instead, it lives off inflation.

In shutting down “cheap” housing, the government:

— Increases inflation.

— Punishes “sinners”.

And so it goes, forever and always.

Great article. Thank you

Two things are certain

1. recession

2. feds will print money

The question is how do we profit of this situation without shorting any stocks. One thing I did is, took my money out of stocks. What are the good ETFs to invest once the dust settles and growth phase starts.

Vangaurd ETF for SPY is good one.

I assume oil based ETF like $USO will have a bull run after the recession. Any other specific ETFs like bonds?

Stick to non leveraged long/short index funds and investment grade corporate bond funds.

USO is an oil futures fund. Understand the concepts of rolling future contracts and backwardization/contago before you play here. I would suggest you leave this alone in general.

Good luck!

I don’t think your plan provides inflation protection, which is necessary in this money printing era.

Meant to say it does NOT provide inflation protection.

They are not printing money, they are printing debt.

Do not get it twisted, asset deflation is straight ahead.

Sounds like the Drug Dealer “Fed” are playing it by ear with no plan. Like a drug dealer, give the users a bit of stimulus to get by. But the users always wants more. The dealer would say “I’ll give you some stimulus next month, if you can do this job for me this month. But then They find out the dealer, like all drug dealers can’t be trusted.

Wolf I just want to thank you for being active in keeping us updated. One thing I learned from reading your articles, This financial system doesn’t make any more sense to me….

Sorry I messed up and reply on Marcus’ comment with this same post.

Warren’s empire is sitting on record amounts of cash – $130 billion. I think even he was hoping for cheaper asset prices to invest.

“Surely, the Fed didn’t want Warren Buffett, one of the richest people on earth, to lose his shirt, so he and his empire had to be bailed out…”

Gov’t -us- are going to have to subsidize the out of work for about

a year.Nannies ,house cleaners so many are hurting with no where

to turn.Danger all round and no health care.We either give it to them

or they will be forced to take it.Do we want our jails full and the`

various mutated viruses spreading.,Shielding the wealthy and

culling the old has been in play so far with little success.We need

a Marshall plan now.

For some citizens, the stimulus checks are going to buy Chinese junk. For some, it goes to pay down debt. For others, it keeps the lights on.

It has been consumed and money velocity

keep dropping.

They sent $1200 individual relief checks. That is helicopter money. They planned to pay the hospital costs of uninsured COVID patients at Medicare rates. One source reported a coronavirus patient’s hospital costs are $25k to $75k.

“One source reported a coronavirus patient’s hospital costs are $25k to $75k.”

Ok, that covers the first hour after admission. What were the costs after that until death/discharge?

News item today:

Former Boeing CEO David Calhoun buys Palmolive Building condo in Chicago for $2,750,000.

Carlyle Group alumnus Jerome Powell seems to be carrying on in the tradition of the “Greenspan Put”, putting an artificial floor on asset prices. (To hell with price discovery). Greenspan seemed to telegraph his monetary policy moves before he did them, Jeromey might simply be carrying on the ‘telegraph” tradition of “the Maestro”. And isn’t it trippy that Powell has millions invested with the Blackrock firm that will manage the corporate debt bailout? No doubt they will be doing more than “jawboning” in the near future regardless if there is a perceived illegality or if it violates the Federal Reserve Act.

It was the same with the trickle-down tax cut. Corporations were handed money with no incentive to bring some manufacturing back home or to provide any additional benefits for employees. It all just fueled the stock market and left nothing to show for the billions.

If that money had gone to infrastructure maybe we would have some new roads and bridges now and the corporations and banks would certainly have gained from old fashioned commerce.

Good point.

If the $1200 relief checks to individuals are a “helicopter drop”, what do we call the billion dollar relief given to corporations via tax cuts. Apple alone received about $30B to $40B in 2017 through elimination of the repatriation tax. I guess we could call Apple’s take a “monetary climax”.

As per Jamie Dimon, the Trump corporate tax cut added $3.7 billion to JPMorgan Chase’s profit last year giving them a $32.5 billion profit for the year. I would question why the corporate tax cuts were even needed at a time when the economy is in great shape (as per Trump) while the take home pay of Main Street continues to decline year over year as adjusted for inflation.

Right, so, Zimbabwean approach to money, print oodles and oodles.

14.7% working age population unemployed (I believe correct of today) for possibly 4-6months looking forward. At least. Add reduced output of all employees on furlough and those working at home.

Estimates of annual GDP contraction to be <10%. I'm sorry, how can that be?

When the confetti money settles and all these folks are still not working, where is the rest of the output going to come from?

Are the other 80% are going to make up what must be an underlying shortfall. Are they actually good to manage it by trying to make or sell whatever to a world in the same boat??

Will the apparent boyancy of the stock markets continue to convince everyone for ever?

Really??

Surely the overall contraction is going to be a lot greater. Surely the wider public won't buy what looks like a fair weather forecast for ever?

It feels like so many figures about the future are like weathermen making predictions whilst wilfully ignoring the falling barometer in the corner of the room.

I’m only commenting on US reports because I can find them. Here in the UK it’s got to be similar.

I have now.

The Bank of England look like they are expecting something along the lines of the collapse of the South Sea Company in the 1720.

How apt.

Fed’s bluff will be called and they will perform beyond market’s expectations.

Yes I believe Bank of America and Blackrock recently issued the marching orders. All stand under the Magic Money Tree! Once I was blind but now I see.

Everyone talks about $1200 checks. Everyone also forgets 2 things

1. It was $1200 per person plus $500/kid. So a family of 4 got $3400. This includes households where only 1 person worked, ie dad works, mom stays at home with the kids, they got $3400.

2. $600/week federal UE benefits which is $2600/mo, on top of state UE benefits. I’ve seen virtually no mention of this in the MSM. It’s like someone used the Men in Black memory eraser thing and this went down the memory hole. That $2600 is so generous, companies are having trouble hiring people back, since they can make more unemployed than working.

Now project the effect of that out a few months, on top of the estimated 25% of small businesses that closed and will never reopen, the ones that do, will find it hard to get employees to work because they can make more not working. This will cause even more businesses to fail and at some point, maybe 6 mos from now, when those people will want to go back to work, the jobs will be gone. Whenever government attempts to help, they only make things worse, usually much worse…. They call that the law of unintended results…..

The point of that helicopter drop, JSRG, besides political grandstanding, is to use the initial recipients as a medium to convey it to the ultimate recipients. It will cause the initial recipients to continue to pay their rent, their mortgages, their debt servicing costs, their utility bills etc., and maybe even continue their consumer spending, rather than have large groups of recently unemployed low wage people with little saved up capital defaulting en masse, cutting consumer spending, and thereby causing problems for financial markets, and for entities that have put their lobbyists to work to bring such measures into action.

I would say that most recipients, are going to skirt rent, default on debt and spend the helicopter money on a beer and drugs and party as long as possible. . But then I do not have a very high opinion of my fellow man…

All this largesse for the market is both more and faster than any help that goes to ordinary people who are and will bear all the costs. It really is truly depressing.

What can’t continue, doesn’t continue. We are just in the phase where we haven’t figured that out yet.

Perhaps we are in a lead up to an economic Dunkirk just as VE Day is commemorated.

That is well said and so true.

This is known as the “return to normal” phase. We have capitulation, fear and despair, sadly, straight ahead.

People need to brace for impact.

Fed realized it’s just poor taste to push market to new all time highs only weeks after 30 millions lost their jobs. Still, problem solved.

It’s not helicopter money, it’s helicopter soil. The Fed does not engage in plucking bad apples from the tree. It occasionally shakes the tree hoping some will naturally fall. It also tosses in some dirt to stabilize the ground, but the tree has grown too fast for pruning and there are much sour fruit hanging on overweight branches. When the latest nasty wind came through, the tree began to lean precariously over so the Fed is usuing a flying bulldozer to shovel in ground by dropping it all over the tree. Branches might actually break in this effort. It it has some success in stopping the collapse, it will be up to the orchardists (ie the government) to take control and start removing the overgrowth. But the farmer has been napping too long after his steak and pie lunch. Someone may need to give him a kick and tell him to wind up his pocket watch.

Into your analogy I would insert insect pests that bored out and consumed the heatwood of the tree.

heartwood, of course I meant to type

Don’t want to go all to the wall yet, but as I’ve mentioned the farm laborers starting blazes elsewhere, “heat wood” may indeed be correct in extreme conditions that might arise!

It is truly astonishing that Wall has the chutzpah to complain on financial media that the Fed is breaking its promise to enrich Wall Street. Wall Street has said openly that it expects the Fed to buy HY and IG in volume so that it will have the buyer it was promised when it front ran the Fed.

IS THIS REALLY A MARKET??

BTW…In order to get this soil, the field hand (Fed) had to dig a big ass hole under the barn. If the farmer does not watch his step and carry a lantern, he might just tumble in and break his neck.

It never really made sense to me why the Fed would purchase junk bonds knowing the default rate among zombie companies is going to be massive. The purchase of the bonds will not keep the zombie companies from going bankrupt and the worth of the bonds going to zero.

The people trying to front run the Fed, and jumping into junk bonds may have fallen for the biggest bull trap in history. If that is the case, the Fed will lose much of its credibility, and the bond investors their money….

That will mark the point where this thing will come unwound completely.

Well, that’s it really, isn’t it.

Which company is going to be the big-time sentinel case that fails to roll-over debt/fails to layer it’s existing bond holders with new preferential bonds?

The moment when skepticism sets more effectively.

Any ideas?

Something the FED did worked very well because the Boston Globe is reporting bidding wars in Boston. Google the article with the title:

“One thing the pandemic hasn’t changed: It’s still hard to buy a house around here”

Since I own single family rentals very close to Boston, I was a little worried, but not now.

SocalJim:

> Since I own single family rentals

> very close to Boston,

> I was a little worried, but not now.

…he said,

as Boston edges closer to Detroit.

The zombie horde is growing, trust me.

No one expects Boston prices to plunge though it will lose some ground eventually just like last time. In many parts of the country RE prices are already losing ground. Some might even plunge considering their income depends mostly on tourism.

SocalJim,

Another piece of RE propaganda that was successfully placed by the industry into the media. This falls into the category of “native advertising,” a really lucrative deal for publishers or for writers who get paid to do this, and then place the article. I get tons of those a day in my inbox.

Why worry? I mean you really don’t need people to pay their rents… right?

I hear a few cities are pushing rent amnesty out now to August. Perhaps that will catch on everywhere….

I have owned rentals for 40yrs, and I can tell you I am sure glad I sold out and am sitting on the sidelines now….

Being a landlord is going to be a nightmare going forward so long as government is telling people they do not have to pay rent. Of course you can always report the deadbeats to the credit bureaus, but then the renters tend to get mad and destroy your property…

Just curious, does the fed pay the property taxes on these real estate and apartment buildings they now own?

The Fed doesn’t own the apartment buildings. The Fed owns mortgage backed securities that are guaranteed by Fannie, Freddie (the GSEs) and by Ginnie (government agency). If a building defaults on its mortgage, it’s Fannie, Freddie, or Ginnie that have to deal with it, and the Fed receives the full principal payment for its share of the mortgage.

I just renogotiated rent in Boston at a massive discount. Dream on.

The Depression Fed game has just started. It will be a long slog not a quick painful extraction. The Fed will buy every thing before it is over. There will be no more silly talk of debt re-payment by bloated politicians . If the world demands repayment we will give them the debased fiat they demanded. It will be worthless, but they got paid. M2 money supply is rising rapidly toward deflation behavior in people. Only 4% of China’s GDP is exported to the US. What is the multiple of that 4% when it circulates as a $30 control element in your Heating/A/C unit as a $400 service call from the HVAC company. Is it possible that China may use the equivalent productivity that the $30 represents in their domestic economy because of their needs or are they fated to slaveishly make it for us? Most of my extended family, think that 90% or more of China’s GDP is for America’s consumption not 4%. It upsets them because government tv has planted a different meme in their brain pan.

The only zombies are bad fruits seeker succor from the tree. The hired farm help can be poisened, get sick, become mentally unstable, and strike out in anger. But when you’re dead, you are dead. Unemployed hands living in worker shacks can potentially become dislodged to cheaper shacks and downward to tents and cars. If conditions get so bad they may get angry and form mobs. While other hands may have taken their place in the shacks, they probably won’t burn them out. But if the shacks start to go empty as more are forced out, someone may decide to strike a match and all hell can break loose. If the fire spreads and jumps to other housing around the farm perimeter, it might be hard to douse it fast enough and losses would mount. The dead would still be dead…they don’t come back. But the aggrieved friends and families might catch a brain bug from the unburied corpses, and the torching could continue. Better hope the water buckets don’t run out.

Am I correct to say that the Fed has probably printed more money 2 months ago than perhaps its first 70/80 years of existence?

I would guess you are wrong by many miles. Max Keiser says there are 22 trillion offshored alone.

There is a lot of confusion about how much money (even just “American”) is in existence. I’ve yet to see an answer to the basic question:

How many dollars, digital and physical, are in existence, who owns them, and where are they?

And, just a statement to provoke thought:

In our American/FED system dollars, physical and digital, are often created, but must much less frequently destroyed. That’s why the huge amount of dollars keeps growing.

They are being destroyed now…. Cash burn right now is epic. Disney alone is burning 40 mil a day. Wait until commercial real estate failures and default begins, it is going to be ugly……

But the biggest cash destruction will come from falling asset values. Take the value of all the real estate in the US, and subtract 40%, what do you think that number is? In the neighborhood of 20 trillion. Then add another 15-20 trillion in the stock market value.

And that is a conservative number…. Do you really think the Fed can stop this?

Think about this …

Where is that cash that Disney is “burning” going? Is it disappearing from the system, or is it just tranfering to another entity?

And when asset values fall, does cash disappear from the system?

If you loan me $200, and I default, no money leaves the system. You loose your $200, but somebody else in the system has it. Debt destruction is not the same money destruction.

It all boils down to:

How many dollars, physical and digital, are in existence, who owns them and where are they?

CB You are confusing physical money with digital money.

Almost all the money in our system is digital debt. It is just an entry on a ledger, and a promise to pay in the future.

In the examples you give, the money is going nowhere, it is just disappearing.

When you sell something to someone and they promise to make payments, and then they lose their job and refuse to pay, where is your money?

It is gone. It never existed because it was never paid. That is what most of our money today is, it is debt that someone promises to pay in the future.

But is is still counted as if it actually existed…..

cb:

It is nice to know money never dies!

It just disappears!

Jdog said:

1.”CB You are confusing physical money with digital money.

2. Almost all the money in our system is digital debt. It is just an entry on a ledger, and a promise to pay in the future.

3. In the examples you give, the money is going nowhere, it is just disappearing.

4. When you sell something to someone and they promise to make payments, and then they lose their job and refuse to pay, where is your money?

5. It is gone. It never existed because it was never paid.

6. That is what most of our money today is, it is debt that someone promises to pay in the future. But is is still counted as if it actually existed…..”

_______________________

1. Not at all.

2. A promise to pay is money owed, not money itself, and that is a very important distinction which many people lose track of. Perhaps you are saying that much money is created via digital debt by the banking system/FED. I am not arguing against that, but that is a whole different discussion.

3. In the example I gave, you had $200 which you loaned to me. I defaulted. You didn’t get paid. You lost $200. I gained the $200. The money did not disappear or get destroyed. It changed possession/ownership.

4. Selling something on time does not create money (though it does create purchasing power, and sometimes selling power, and even pricing power). The fact that you never get paid does not destroy money. It just evidences the fact that the promise to pay was not honored. If they return to you the item, that also does not create money. It just gives you back your item. (The fact that you might thereafter sell the item for money also does not create money, though it may transfer money from the buyers to you.)

5. You are right, because selling something on time does not create money. (It can result in a transfer of money to you if the buyer actually pays you. But transfers are all we are talking about. There is no money creation or money destruction.)

6. Debt is not money. Debt is a liability.

You are right about there being a lot of confusion out there. The banking system likes it that way. Even the most basic question is, for those I know, unaswerable. That is:

How many dollars, both physical and digital, exists, who owns them and where are they?

@ WES –

actually WES, some might die or disappear, but it mostly expands. continuously. That’s why a 10 cent candy bar now costs $1.29, a $50,000 house now costs $600,000, education costs are up, health care costs are up, nominal household income is up, etc.

“Jawboning” ???? How about LYING

but what else could be expected from professional LIARS and Deceivers?

we really should stop bastardizing the language with niceties ……….

Great article Wolf…… and commentary.

Starting with the April 16 H.4.1 report, the Fed included a line item in section 2 for: Commercial paper held by Commercial Paper Funding Facility II LLC (5). It went from $0 -> $0.95B -> $2.71B -> $3.347B -> $3.948B. A drop in the bucket of the overall balance sheet for sure, but I didn’t see you mention this program in your analysis above. Any chance you are privy to a breakdown on this CPFF II vehicle? Which zombies are the Fed helping to continue to eat brains?

Yes, I don’t normally include something until it gets to some size…. meaning double-digit billions. $1 billion is less than 1/10 of 1% of the balance sheet.

I know that I will make an exception when corporate bonds and ETFs start showing up. I assume that this will also be in small numbers. So maybe I should revisit my size limitations for these new programs.

I don’t have access to data that shows which company issued the commercial paper that the Fed bought.

Watched episode of South Park from 2001 and the subject was the Airlines being financially affected by the ‘IT’ transportation machine. Untill the Govt came in and shut IT down…..LOL LOL LOL LOL

NY Fed says its going to start buying ETFs this Tuesday. (WSJ)

Kind of sad to see how off the rails things have gone. I wonder if there will be a lawsuit. I thought it would be illegal for the FED to buy anything outside of MBS and Trasuries?