Just how much lower can they go? To Zero. And the ECB’s negative interest rates are driving them closer to it.

By Nick Corbishley, for WOLF STREET:

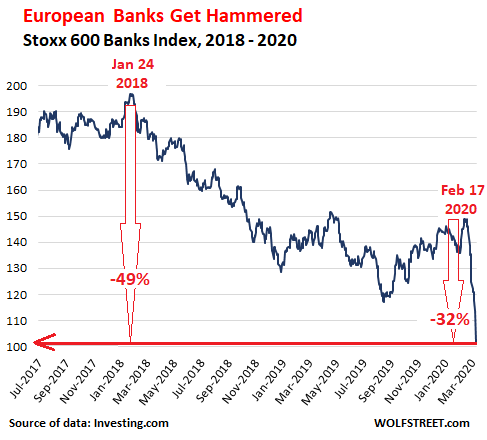

Over the past three weeks, stocks in Europe have plunged by 22.5%, their worst decline since the collapse of Lehman Brothers. The sell-off has been across the board but the worst of it has been reserved for the banking sector, whose shares have been relentlessly crushed and re-crushed for 13 years.

On Monday, the Stoxx 600 Banks index, which covers major European banks, plunged 13%. Today, after a knee-jerk bounce-back that then fizzled, the index closed essentially flat, back where it had been in March 2009. It has collapsed in a nearly straight line by 32% since February 17, when this latest Coronavirus-triggered sell-off began, and by 49% since January 24, 2018:

But it’s even worse: The Stoxx 600 bank index has collapsed by 82% since its peak in May 2007, after having quadrupled over the preceding 12 years. It was the frenzied height of the euro bubble and the sky was supposedly the limit for Europe’s biggest banks. Things got so crazy that for a brief moment in 2008, before it all come tumbling down, the Royal Bank of Scotland, now bailed-out and majority state-owned, was the world’s biggest bank by assets.

Here’s how far the shares of Europe’s largest publicly traded banks by assets fell on Monday (and in parentheses: at today’s close, since February 17):

- HSBC (UK): -4.82% (-17%)

- BNP Paribas (France): -12% (-33%)

- Credit Agricole (France): -16.9% (-42%)

- Deutsche Bank (Germany): -13.6% (-38%)

- Banco Santander (Spain): -12% (-30%)

- Barclays (UK): -9.81% (-32%)

- Société Générale (France): -17.65% (-41%)

- Lloyds Bank (UK): -8% (-24%)

- ING (Netherlands): -14% (-37%)

Today, banks in Northern Europe rebounded a tad from yesterday’s lows. But banks in Italy and Spain, having started the day in the green, closed with some big drops:

- Unicredit (Italy): -3.6% (down 10% from intraday high)

- Intesa (Italy): -2.5%

- Banca Monte dei Paschi di Siena (Italy): -6.3%

- Banco Sabadell (Spain): -7.1%

- Santander (Spain): -1%

Three of the biggest sell-offs over the past three weeks were endured by France’s three largest lenders: BNP Paribas (-33%), Credit Agricole (-42%), and Société Générale (-41%).

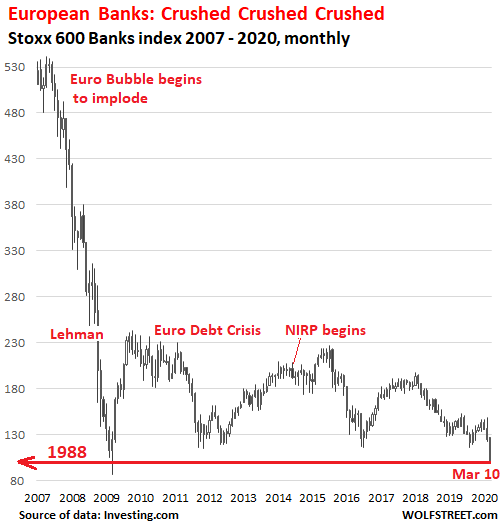

These declines in share prices, while impressive for both their speed and size, represent just one more leg down in the relentless sell-off that began in May 2007 and has dragged the Stoxx 600 82% lower, to just below where it was in January 1988.

The ECB is primarily concerned with keeping the Eurozone glued together. Unlike the Fed, whose 12 regional Federal Reserve Banks are owned by the banks and bank stocks are hugely important to the Fed, the ECB couldn’t care less about bank stocks, as long as banks themselves don’t collapse. So it has thrown just about everything it has at the problem of keeping the Eurozone glue together, including €4.7 trillion ($5.2 trillion) of newly conjured money, but with largely undesirable consequences for banks and their shares:

Here’s the handy and continuously expanding WOLF STREET timeline of some of the events that helped annihilate European bank stocks:

- In mid-2007, the euro bank bubble begins to implode.

- In 2008, the Financial Crisis hits, lighting the spark to housing market collapses in Spain, Ireland, Portugal, Greece, et al.

- In 2009, the euro sovereign debt crisis along with the Southern European banking crisis starts.

- In June 2014, the ECB’s Negative Interest Policy (NIRP), designed to solve these problems, begins decimating banks’ interest margins while also wiping out savers.

- In 2015, the Italian banking crisis resurfaces with the slow-motion collapse of Monte dei Paschi, Veneto Banca and Banca Popolare di Vicenza, and their subsequent bailout/takeover over a year later.

- In June 2016, a majority of British voters check the Brexit box, which causes the Stoxx 600 Bank index to plunge 21% in two days, the worst two-day plunge ever.

- In mid-2017, mid-sized Spanish lender Banco Popular collapses under the weight of its huge bad loan-infested balance sheet, and is taken over by Banco Santander.

- In early 2018, Deutsche Bank and other banks recommence their downward spiral.

- By late 2018, even the ECB begins to acknowledge the harm that negative interest rates does to banks’ ability to turn a profit and the risks it poses to financial stability, by encouraging banks to engage in greater risk taking and less productive lending.

- In late February 2020, COVID-19 upends the global economy, and the risks are piling up in one of the euro area’s weakest links, the banks, and particularly Italy’s banking system.

Already home to one of the highest concentrations of bad bank debt in Europe, Italy can ill afford the current shutdown of its economy that could lead to a fresh surge in nonperforming loans. The country is already either on the verge of recession, or in the very midst of one. Italy’s banking lobby, ABI, has called for a state guarantee and a 6-12 month moratorium on new, stricter EU regulations on problem loans. This would offer small firms affected by the virus-crisis the opportunity to freeze repayments or lengthen the maturity of loans.

The government has also proposed passing an emergency law that would suspend mortgage repayments for bank customers for the duration of the shutdown. Another possibility is that the government, if given the green light from the EU, pays the interest costs on behalf of its citizens.

Such measures could prove to be a life-line for struggling businesses and households. But they will also cost a lot of money, and that is one thing in short supply for Italy’s government, whose total public debt load is now equivalent to almost 140% of GDP. Just two weeks ago, as COVID-19 was gaining a foothold in the country, the European Commission warned of the “high” risks Italy faces in trying to refinance its mountain of debt. “The need to roll over sizable amounts of debt, at around 20% of GDP per year, still exposes Italy’s public finances to sudden rises in financial markets’ risk aversion,” the commission said.

Italian bond yields are already beginning to rise, albeit from an absurdly low level. The spread between the country’s ten-year bond and that of Germany’s blew out to more than 200 basis points for the first time since August. That is bad news not only for Italy’s government but also for the shaky banks in Italy and beyond that have bought huge chunks of its ostensibly risk-free debt. If the yields on that debt suddenly begin to spike as bond prices drop, it could significantly erode lenders’ capital buffers. And that is when investors begin to worry, prompting them to intensify their sell-off of bank shares.

To try to stop that from happening, the ECB may be tempted to take deposit rates, already at -0.5%, even lower. But while that may provide fiscally challenged governments with a little extra breathing space to support their stalling economies, it will also heap further pressure on banks, effectively destroying their basic business model, as bank CEOs have been loudly bemoaning. To mitigate this problem, the ECB may come up with some other magic solution, such as buying the banks’ bonds, but as with NIRP and QE-forever, the remedy will probably be worse than the disease. By Nick Corbishley, for WOLF STREET.

“If the situation of generalized panic continues, thousands of businesses, especially small ones, will first enter a liquidity crisis, then close their doors.” Read... Tourism is 10% of GDP in France, 13% in Italy, 15% in Spain. And Now it’s in Free Fall

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

How are the Canadian banks looking: TD, RY and BNS? Housing and oil patch exposure?

Cm Canadian most toxic

@Shiloh1

Rather than trying to make a deal with Russia or OPEC, Canada has decided to restrict supply by delaying every possible pipeline.

Nonsense.

This downturn will be over when Shale collapses. Oil Sands production companies are basically mining ventures, with long term debt structured in. They survived $20 dollar oil prices, they’ll survive this. Their short term output is not dependent on short term investors/financing such as Shale. Will there be belt tightening? Assuredly. Expansion delays on site? Probably. Pipeline construction delays? As few as possible. If anything this oil war provides more impetus to stop the WCS discount by currently being landlocked to US.

The pipeline wild card are the protests and civil disobedience. However, nothing like a good recession and downturn to wake people up to the importance of a pay cheque. Will Canada enter recession? Probably already has, if the truth be told. However, total debt to GDP in Canada is 88%. In the US it is 108% and rapidly climbing.

Rumour in Canada is that many pipeline protests are funded by US interests to delay pipeline construction. Many native protests are being done by non-natives which is probably fueling the rumour mill.

regards

just looking at the stoxx600 looks li,e its going lowe thru that floor

prepare accordingly

Cue the derivatives. Add another 50 billion to the Fed’s overnight Repo.

10% down is a correction.

20% down is a bear market.

David Hall,

And 49% down in two years is a crash?

And 82% down since 2007 and back to 1988 levels is annihilation, no?

Actually, annihilation would mean they are dead and gone. But since we are talking about banks in the ECB, it means bail-ins.

guess the ECB buy everything is working out well

EU banks are 30:1 levered – what possibly could go wrong

The NASDAQ crash started in early 2000 after Professor Robert Shiller published his best seller, “Irrational Exuberance.” The NASDAQ crash as described by Wikipedia in the public domain:

Between 1995 and its peak in March 2000, the Nasdaq Composite stock market index rose 400% only to fall 78% from its peak by October 2002, giving up all its gains during the bubble.

That’s just something made up in recent years by mass market financial journalists. Traditionally a bear market is any significant decline extended in time. A correction being naturally enough a reversal of a erroneous overextension. When a number is called for, it’s easy enough to state it. On his site, Wolf is free to be his own lexicographer.

US Banks (BKX) have plunged from the high at 114 in December to a recent low of 71.

Down 38%.

The collapse of speculation in so many sectors has been remarkably fast.

Spreads, the curve, industrial commodities and the stock markets.

There has to be a number of large companies and traders offside.

As in insolvent.

How long before the “discoveries” are announced?

The XLF is just 5-6% above the December 2018 low. But the ^BKX is already below the December low.

JPM is already at the discount window with its CEO breathing to a tube… BBB “IG” (collateral), long dated UST trash (collateral) and Au_79 (collateral) got pounded hard today… we’re gonna need more lube folks!

I am very curious to see if there will be a contagion from European banks that will smack other banks around the world. If we look at what Nick has put out, it basically says, the European banks are in deep shit. The respective governments may not let the banks collapse, but not collapsing doesn’t mean the shareholders and bondholders won’t get taken the the wood shed.

The crisis in the Eurozone and in particular within Eurozone banks were not addressed after 2008, and the ECB has tried every trick to solve the insolvency and illiquidity of Eurozone banks since.

Most if not all commerce in Italy has ground to a halt. An already beggared nation is going to be further corroded by this commercial closedown.

Bad debt concerning bank loans and bad debt concerning corporates is going to rocket as a result.

Add into the mix that the Spanish bank – Santander- is , i believe, the

second biggest player in the USA auto loan market, and, as reported

a while back, is suffering from an above average number of auto loans

defaulting on their first instalment. the house of cards shakes!!!!!.

Why does it seem like Santander works extra hard to make sure all of its investments are as stupid as possible?

It is waiting for a SoftBank invt.

Oh, poor Euro bankers, I hope they will get bailed out. Such an ethical and respectable bunch deserves it.

I don’t understand Italy though – they are sitting in the middle of an epidemic crisis and get exactly 0 help from their Euro-buddies. Not a single charity, not a single shipment of face masks or offer of medical help from their neighbours and welfare states that are such a great example of solidarity when a hurricane strucks some 3rd world country or when people are fleeing from war. All the Italans get – at best – is blame. I mean what would Robert Schuman think if he would see this chaos – where is the idea of a common Europe? Nowhere. The real danger is not the debt crisis, but that some Italian politican will – rightfully – say “Enough of this crap, we’re not going to take this anymore” and will trash the euro replacing it with the good old lira.

I don’t understand Italy though . . . Not a single charity, not a single shipment of face masks or offer of medical help from their neighbours

Newsweek reported yesterday that the Chinese consumer electronics company Xiaomi donated tens of thousands of FFP3 face masks to Italy’s government. It’s also getting 800,000 from South Africa.

Oh, poor Euro bankers, I hope they will get bailed out.

Not because they deserve it, which they don’t, but because it’s necessary. If the banks were required to operate as utilities rather than as high-stakes gamblers the problems would be much easier to control.

Why is it necessary?

You are not supposed to ask such questions

To preserve the cultural heritage and lifestyle of those in the financial industry. We must remember that the Italians invented banking.

The Italians didn’t invent banking. The Sumerians invented banking in the 3rd millenium BC. Pasion of Athens was the most famous banker of antiquity. Sorry.

Italy needs a trillion to weather the pandemic. The US is likely to need twenty. Guess where they’re going to get it.

There is no reason (other than politically useful illusion casting) that DC (at any moment, from either party) can not very explicitly lay out, in clear detail how the Treasury/the Fed/and the Banks are much, much more interconnected in their daily operation than the public currently understands.

It would be a good time for some of those idealized politicians expected to run the socialized Utopia to peep up.

the Banks are much, much more interconnected in their daily operation than the public currently understands.

A great deal of the order of things depends on treating whole populations like mushrooms, keeping them in the dark and feeding them manure, illuminated only with gaslight.

It will be interesting to see how banks fare with foreclosing on entire countries instead of individuals.

Prof, yup, that about sums up the heartfelt EU fraternity. Shrill shouting if someone wants to leave (UK), or do their own thing (Hungary), or just cut things back into proportion a bit (Finland, AfD). Real solidarity in times of need (not investor bailouts dressed up as such) – silence.

‘the good old lira’

That is kind of funny, especially for an Italian. The lira was a second tier currency in Italy before the euro. All real estate was priced in US$. No long term contract could be in lira, unless it had inflation clauses.

Shortly before the euro, as the lira neared collapse, Italy came out with a 500, 000 lira bank note. Imagine a 500 K dollar bill!

The idea of a return to the lira has little support in Italy and zero with its bloated, inefficient public sector, which does not want to be paid in that variety of scrip.

What the populists are threatening to do is usurp the ECB and print their own euros.

Whether these would be counterfeit is another topic.

Bank stocks have tanked because their portfolios are at risk, but the defaults haven’t hit them yet and they still haven’t recovered from the last meltdown.

If my participation in the system were more than trivial I’d be more concerned about bail-ins than bail-outs. People are going to be very unhappy about that.

Who’s tracking commercial loan defaults and bank failures here? There is reason to believe those are about to become a problem.

The FDIC website is pretty good…monthly/Quarterly reports on 30/60/90 day noncurrent loans, etc (although I’m sure plenty of game-playing, f*ckery-pokery goes on in terms of loan classification – extend and pretend, etc).

Fairly sure it is possible to filter the entire bank universe for noncurrent loans above X pct by bank (at worst, I know Financials for all bks can be downloaded and sorted via Excel).

The true biggies have so much idle capital I’m fairly sure none of them is at real risk…probably true for most of the 1 billion dollar asset banks – everyone has held an assload of federally backed debt for years (vs., you know, private sector loans…)

On the other hand, smaller banks are probably poised to get slaughtered – again (15000 in 1990, 6000 today)

You’re probably right. Particularly about the ‘true biggies’ having so much idle capital that they’re not at risk. Which could give the system some fault tolerance, at least for the present. Perhaps there’s time to shore up the system, prevent a collapse, and get on a path to recovery. Still, the whole ‘parasite killing the host’ thing needs to be reversed.

I think it is apropos that we enumerate the Fed’s available tools. I’ll start with a few:

1. Discount Rate (I will add Repo rate to this group)

2. Reserve Requirements

3. Open Market Operations

4. Interest of Reserves

https://www.stlouisfed.org/in-plain-english/how-monetary-policy-works

OK so how will this help solve the problems of massive debt overhang and the effects of the corona virus? At what point will these tools be ineffective with the impending credit freeze, if it happens? Can the Fed save everybody?

The worse things get, the closer Zimbabwe Ben Bernanke and his actual money dumping helicopter get.

Despite two decades of ZIRP created pathologies, DC is incapable of course correction and has an auto-erotic fixation on re-inflation.

Once they get the inflationary ruin they lust after…they will just call it canned-good-asset inflation and set up a market for spam-collateralized loans.

A good topic for discussion. Fed is already running 1+B REPO what does QE have to offer, while the market has already pressed rates into submission. What extraordinary measures are next; dollar devaluation? debt downgrade? off balance sheet accounting? The payroll tax cut beckons a knee jerk response, is the next crisis in US government funding?

1) BKX plunged inside 1998 trading range.

2) July 1998(H) @ 93.34 for resistance and support from Oct 1998(L) @ 54.57.

3) BKX is backing up for 3Y. Its an opportunity to buy.

4) The crybabies bankers borrow at Repo, pile assets @20%.

I like the idea to defer mortgage payments, so long as the interest is billed to taxpayers and banks are kept whole. It would be a good way to help homeowners who are trying to navigate the effects of dramatic price appreciation. It also provides some relief to banks as they continue to invest in robust risk management practices.

Bobber,

Hahahahaha… one of the funniest ones today.

The corona virus maybe self-financing. If a large enough number of the elderly die, the estate tax revenues and reduction in pension benefits can repair national government balance sheets.

Won’t help European banks but it would allow for a fresh jolt of fiscal spending the ECB keeps calling for.

Yes, lets look all of the positive effects from the coronavirus.

my 89 yr old mother in a assisted living , and not feeling well today. yep lets clear the decks of anyone over the age of 80 and lets get on with the inheritance already, extreme sarc………I am scared for her, a sitting duck…

And yet, despite the the euro gained handsomely against the dollar amidst the turbulence of the last week or so.

I just read that Italy suspended mortgage payments across the country. Did they suspend rent payments as well? If not, wouldn’t that be extremely unfair and biased, knowing that taxpayers are footing the bill ultimately? Why should a renter pay his rent and his neighbors mortgage payment?

Yes Bobber. You nailed it.

Taking it a step further, why should corporations and banks receive short term help while workers are told to report home for 2 weeks without a sick day or basic stipend?

To my very limited understanding, since 2008, the problem was, and remains to be, that the debt must eventually be paid. It’s either going to be paid by bail-ins (investors and bond holders) or by the taxpayer and general citizen (higher taxes, lower wages, and deep cuts into the various pension systems.)

The only other option was to create substantial inflation in the wider society, as a way to clear everyone’s broken balance sheets, keeping people employed (busy work with coding or whatever, it doesn’t really matter in the short term) along with importing lots of young migrants eagerly exchanging their sweat for progressively devalued script.

But this third option hasn’t worked out so well. (Why so, is another fascinating topic.)

Both remaining options, bail-in or sticking it to everyone, would reflect that the various socialist societies of Europe have aged to the point that they are quickly heading towards their end game. Those who govern just haven’t figured out how to finally transfer the patient to palliative care and gently kill it off, while avoiding popular revolt.

Unless, of course, as some have stated above, they are hoping that the Covid-19 is a deux ex machina (natura ex machina?) and will do the unpleasant job for them. It could explain why the other nations of Europe are not rushing in to help Italy save its seniors.

Nasty, brutish stuff, this struggle for money and life.

Don’t bail any banks out going forward, nationalize them and restrict private banking, period. Obviously, the bonus structures and crony corporate relationships are undermining prudence.

Whatever happened to conservative bankers, anyway? Oh right…if banks can’t fail and officers are rewarded by production numbers and skim, all prudence is lost. Of course unrestricted debt created our false prosperity to begin with, so I guess we’re all guilty by association.

Nothing like the prospect of failure and jail to sharpen the pencil of any banker or individual. I don’t mean a club Fed….but real jail time for the bad apples.

To quote Michael: “4) The crybabies bankers borrow at Repo, pile assets @20%.”

Then, have the gall to ask for the public’s help when they screw up.

Paulo, MPS stocks are 66% owned by the Italian government: look at how well it is doing. So well in fact the Italian government has been trying to get rid of it even if it means losing a big pile of money.

MPS was effectively nationalized to avoid a scandalous trial which would have laid bare what everybody not living under a rock knows in Europe: banks do not exist to make money but to stimulate economic activity.

This may sound like a great idea but remember: if you have a viable company banks will be lining in front of your door to have your business.

European banks like MPS have lent money with an abandon only matched by Thai banks in the 90’s to projects which were a disaster waiting to happen or simply money pits in the making. Bad calls and plain old bad luck happen all the time, otherwise bankruptcy codes wouldn’t be thousands of pages thick, but here we did it on industrial scale. Why?

It’s hard to explain to people from the Americas the deep ties between European banks and politics. It’s the same in Italy, Spain, France, Austria… Germany was so anxious about bailing out her sinking banking system quickly to avoid the juicy and sordid details of the deep ties between banks, politicians and export-oriented companies to be leaked to the scandal-hungry media.

MPS to say but one was notorious for lending money on a strict no-question basis to companies tied to PD politicians, but the true rot (very much like in Austria and Germany) is at local level. The most depressing part? Everybody at the ECB knows this, but they turned the other way in the name of GDP goosing.

Don’t think anything has changed. If anything banks have started to lend money with even more abandon: the absolutely ridiculous Continent-wide real estate boom would not be possible without a flood of no-strings-attached money. How long will it be sustainable without buyers is an interesting question, as is what will happen to that semi-bankrupt colossus, Deutsche Bank.

Everybody seems to bet on a bailout for the latter, but I beg to differ: the €380 million bailout of leisure airline Condor has caused a political storm in Germany. Deutsche Bank would go through that kind of money in a week or less. And on top of that there are all the scandals that have slowly turned people away: it’s exactly the same thing that happened to Mitsui Bank, once Japan’s patrician and most prestigious bank and now just a division of Sumitomo.

The average joe has no choice but to go to a central bank franchise in order to access their fiat pay for their non-fiat labor. You have to have an account so the central banks can get a cut of your labor .Banks are worthless to the average joe. Governments most basic function is to provide predatory Inital free access to their financially trapped subjects work product. Governments have failed at this.Governments want access to unlimited credit to mainly enrich their ilk. They will throw the worlds Gilets Jaunes a few crumbs every now and and then. Screw them all.

DR DOOM, basically agree but the banking stuff is a symptom rather than a cause. The basic function of the state (or govt if you prefer) is to maintain a class divided society where the few are enriched by the surplus value extracted from the many.

Anyone know what the plan is once we reach 0% interest rates (probably later this year)? Will going negative have any economic benefit?

I’m thinking we have one more leg up (there is still room for maybe 1 to 2 more cuts) and then all heck breaks loose as we reach 0%

The only thing the government can do at that point is to print massive amount of money (QE) and increase government spending???

bruce,

If you want to know why the Fed is UNLIKELY to go to negative interest rates, read this article and study the charts of the banks in the Europe. Pay attention in particular to this paragraph from the article:

“The ECB is primarily concerned with keeping the Eurozone glued together. Unlike the Fed, whose 12 regional Federal Reserve Banks are owned by the banks and bank stocks are hugely important to the Fed, the ECB couldn’t care less about bank stocks, as long as banks themselves don’t collapse. So it has thrown just about everything it has at the problem of keeping the Eurozone glue together, including €4.7 trillion ($5.2 trillion) of newly conjured money, but with largely undesirable consequences for banks and their shares”

You see, negative interest rates for long enough will kill bank stocks. And since most of the Federal Reserve System is owned and controlled by the banks, that’s not likely to happen.

The yield on the 10 Year touched .38% yesterday. The move in just the last ONE week has been bigger than the decline from 2009 to 2012 (percentage wise).

Granted rates have recovered somewhat, however it’s beginning to look like the Fed is losing control. IMO

Im thinking we MIGHT get another leg up… and then it’s a repeat of 1929/1987 market crash.

What happens when negative rates are thrust upon you?

Short-term is OK. The problem is when this turns into a permanent feature.

Also, anyone else notice real estate prices are bumping up AGAIN (Los Angeles). I assume this is b/c of lower mortgage rates from the recent rate cut.

However, it looks like the LOWEST the 30 year mortgage can go is maybe around 2.5%. Is it really possible to go much lower being the 10 year bond is already approaching ZERO??

What should we expect next? Can housing continue to go up simply b/c of massive inflation???

Paging SocalJim to the response room…

Cutting, forcing interest rates to abnormal lows, despite the central bank theories is detrimental to economic activity.

There is a reason that the average interest rate historically is circa 4%.

These self anointed “genius” central bankers who know better than free markets are the ones Hayek warned us about.

But fear not for them. They will inflate till their heads cave in…but are protected from the ill effects of their own policies by the inflation protected pensions each and everyone of them have.

Nick

Good article.

EU banks were never strong, and got walloped by the 207-9-9 melt-down & “re-capitalization” (read: taxpayers saved bank’s ass). EU bank managers (a particularly corrupt bunch), continued to weaken the banks (read: loan to knowingly corrupt businesses). Throw in more than a decade of artificially low interest rates, refusal to effectively regulate, laughable “stress tests” and huge non-performing loans, and sooner or later, you get…well, exactly what happened today.

No one in the world, investing their own money, believes EU bank financial reports. Theoretically, even with bank stock at $0.00 and all COCO’s called in, liabilities may still exceed assets.

The ECB has pushed this to the brink, and even a slight puff of financial wind may blow (lots of financial) houses down.

Negative InterestRates/RiskPremiums are

like heroin&religion — they kill the pain.

Every junkie is a setting sun.

Hmmmm – how does this work for Italian banks?

Coronavirus: Italy suspends mortgage payments amid lockdown

https://www.independent.co.uk/news/world/europe/coronavirus-italy-economy-mortgage-payments-symptoms-lockdown-latest-a9389486.html

Banks simply cannot make money in a system with zero/negative yields, flat yield curve and razor thin margins/credit spread. Bailing these banks out (or in) doesn’t take the aforementioned into account. What am I missing?

What am I missing?

The bank cartels rule the world. This is their end game, and they’re not correctly positioned for it, so things are going to get messy.