Banks are trying, but demand just isn’t there.

By Wolf Richter for WOLF STREET.

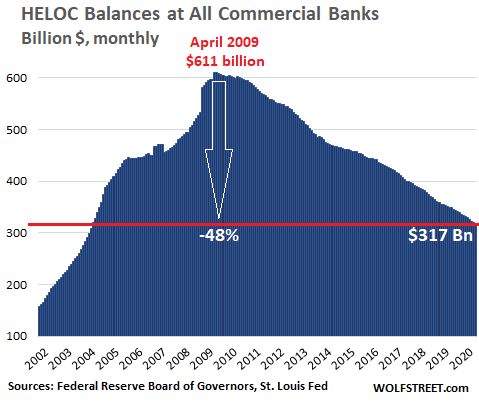

At the end of January, outstanding balances of home equity lines of credit (HELOC) at all commercial banks in the US – not including nonbanks, or “shadow banks,” we’ll get to those in a moment – fell to $317 billion, according to the data released on Friday by the Federal Reserve Board of Governors. They’ve plunged 48% from the peak in April 2009 and are now back where they’d been in April 2004. These are the balances that are actually outstanding and do not include the unused portion of the credit line:

Banks and nonbanks have been trying to get homeowners to take out HELOCs, which are credit lines secured by the home, and risks for lenders are lower than with credit cards because in case of a default, they can go after the home. Credit cards are unsecured.

For homeowners, HELOCs fill a similar function as a credit card, but borrowing costs are lower. And like a credit card, the rate is usually variable. HELOCs played a role during the mortgage crisis that triggered the Global Financial Crisis. But things are different now, and banks and shadow banks want Americans to borrow in this manner and spend the money on vacations or home improvements or a new car, or whatever. Google them and see how they’re trying.

And the Fed, which tracks these HELOC balances at the commercial banks it regulates, wants homeowners to borrow against the rising values of their homes and splurge with this money and thereby convert inflated home prices into retail sales and consumer spending and thereby into GDP growth, and into additional interest income for the banks that the Fed regulates.

When William Dudley was still president of the New York Fed, he addressed this refusal by households to do so. In a speech, he lamented this “change in household behavior” – that households have refused to turn home equity into retail sales and GDP growth, after getting burned during the mortgage crisis for having done so. And the situation, from the Fed’s point of view, has gotten more dire.

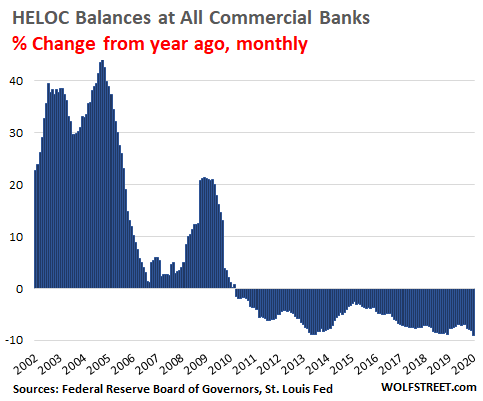

In January, HELOC balances at all commercial banks dropped 9% from January last year, the steepest year-over-year percentage decline since 2013. This chart shows the relentless year-over-year declines of HELOC balances:

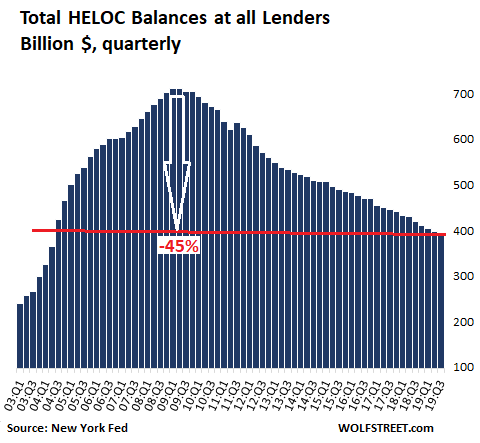

These are the HELOC balances at all commercial banks, tracked by the Fed’s Board of Governors, but do not include the balances at nonbanks, which are not regulated by the Fed. On the other hand, the New York Fed releases data on total household credit balances at all lenders, including nonbanks, on a quarterly basis. Its latest release (for Q3) shows a similar trend.

Total HELOC balances at all lenders, including nonbanks, plunged 45% from $714 billion in Q1 2009 to $396 billion in Q3 2019:

So what is going on here?

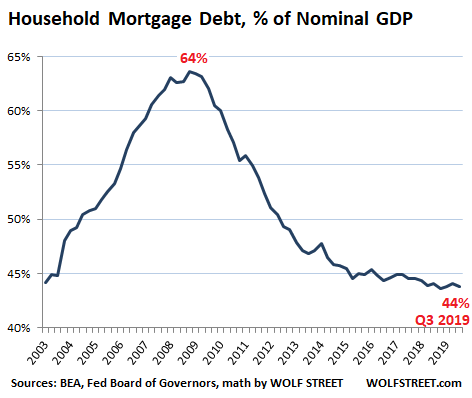

Housing-related debt fell off sharply during and after the mortgage crisis as foreclosures made their way through the system: Total housing debt had peaked at $9.99 trillion in Q3 2008, and then dropped by 16% to $8.4 trillion. In Q3 2019, it almost got back to where it had been in 2008, to $9.83 trillion.

But there are now 128.6 million households, up 9% from the 116.8 million households in 2008. Everything has grown over the 11 years, the economy, the population, incomes, consumer prices, and home prices. So the current housing debt in aggregate, compared the overall economy, has fallen from 64% of nominal GDP at the peak, to 44% in Q3 2019.

So “in aggregate,” this looks good. But this aggregate is composed of several opposing factors, including these four:

- Many homeowners have paid off their mortgages and own their homes free and clear, which has become a more attractive option for households in expensive housing markets, as the mortgage interest deduction has been further reduced, and as “risk-free” returns (Treasury securities, FDIC insured CDs, etc.) have been miserably low.

- Many other homeowners are pushing the envelope in terms of their mortgage debt and mortgage payments, struggling to make ends meet on a monthly basis. If one of the earners loses their job, the entire math gets in trouble.

- Cash-out refis have become popular again, and the risks associated with them are increasing to where regulators are trying to put some limits on them, but in terms of the mortgage debt “in aggregate,” they have not moved the needle much.

- The homeownership rate has declined from 69% in 2005-2006 to 65.1% currently, after hitting a multi-decade low of 62.9% in 2016. This means fewer mortgages and fewer HELOCs and more renters.

HELOCs are viable credit tools for homeowners, if used prudently. If not used prudently, they can contribute to a mortgage meltdown and foreclosure.

Since HELOCs are secured by the home, a default on the HELOC can trigger a foreclosure. With credit cards, this cannot happen, though the bank can sue and try to recover its loss that way.

The unused portion of a HELOC may not necessarily be there when you need it the most as the bank can freeze the HELOC when the price of the home drops, and not allow you to dip into it further. Suddenly, your credit line that you relied on is gone.

During the past housing bust, HELOCs were big contributors to homeowners being underwater with their mortgages. When homeowners could no longer make the payment, they then found out that they couldn’t sell the home either, and that foreclosure was at the end of that tunnel. And this experience is still in the collective memory of homeowners.

But the folks relying on credit cards, auto loans, and particularly student loans to accomplish their goals are now pushing the envelope again. This type of consumer credit rose to 19.3% of GDP, the highest ever. Read… The State of the American Debt Slaves, Q4 2019

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Maybe because there are fewer and fewer private single home owners that can use the value of their home as collateral for their rotating credit needs?

It’s not like there’s much of a reason for someone like invitation home or black rock or colony american to be running up an expenditure card against the value of their main assets.

I read Blackrock got out of the single family rental business last year. The articles said they sold all their interest to Invitation Homes. I personally thought their timing was really good. You can smell rent control in the air.

Blackstone not Black Rock.

so we just refied out of 2005 heloc – had converted to 30 year 5 years ago at high interest rate of 5 1/8

now our payment will go up another 300 a month but interest rate almost 2% lower

but will be paid in 15 years – via streamlined refi

only works for those with high fico’s and stellar payment history

The Moms 4 Housing incident in Oakland, where two homeless mothers and their kids broke into and squatted in a vacant home owned by a vulture fund that buys up distressed housing, should’ve served as a warning to Black Rock and its ilk. These vulture firms have used their unlimited access to nearly free “stimulus” from the Federal Reserve to hoover up distressed housing at firesale prices, then hold it off the market (and deny shelter to local communities) while the asset bubbles blown by the Fed continue to rise. It’s a lucrative racket, but as community hostility grows against these outsider vulture funds, their vacant houses will be at much greater risk of being occupied by squatters backed by local “community organizers.” So now might be an opportune time to sell off their housing “investments” before the bottom drops out of Housing Bubble 2.0.

the same is practiced by many small speculators in my area: they buy up homes and just keep them off the market, and don’t even bother renting them out (a few of them will try, asking totally outrageous prices that are 5-10x higher than the same home would cost to someone on social security). Thanks to the idiot policies of ECB the homes automatically appreciate 8-10% per year while the loan cost just 1-1.5%, easy money for vultures.

Unfortunately Netherlands got very tough anti-squatting laws after the last civil unrest around 1980, with similar causes. The government is (of course) fully protecting the speculators.

“The government is (of course) fully protecting the speculators.”

Well, the Netherlands did invent the Tulip Bubble LOL.

You are right, I live in LasVegas since ’95, we used to see housing everywhere & in the last 10 years, all you see is Appartment Complex growth & costs going up. Population boomed.

I can’t smell it in the air yet, but I sure hope you are right. Making other people buy 100% (or more) of one’s assets for them because they need shelter stinks. And maybe a law forcing the slumlord to personally do all or some high % of the maintenance, would also help?

Invitation Homes is a subsidiary of Blackstone. Invitation Homes with Blackstone original $ was buying single family homes starting in 2012.

Invitation Homes has been selling some homes the last 2 years. They did their IPO Jan 2017. Fannie Mae gave Invitation Homes a 1 Billion $ loan. I was very angered by that . Goldman Sachs was giving investment $ in still transient single family home neighborhoods& financials said something else. This was on or before 2016

This data does NOT include institutional investors such as Invitation Homes. It only includes mortgages and HELOCs held by households.

Here are some charts of home price inflation. They show that many homeowners who bought a few years or longer ago can take out big HELOCs if they want to:

https://wolfstreet.com/2020/01/28/the-most-splendid-housing-bubbles-in-america-january-update/

The numbers reported cloud the matter then.

If it doesn’t include institutional investors, then of course some of the absolute terms might be down.

My point still stands that they have taken a larger slice of the pie.

Even with those non-institutional numbers included in the reports, my theory could still apply. How many homeowners are actually landlords with more than one house? How many single homeowners are there left in the market compared to 2006?

This is in conjunction with what others have said, that it’s unlikely for the people lucky enough to have a house after 2008, are going to fall for the same trick that took so many peoples house away in 2008.

You forget that HELOCS are now non-deductible. In addition , after the first ten years, your payment triples. That’s scary. I’m paying mine down at $1000 a month toward principal, which is Chase’s choice. Right when I needed it, Chase froze my HELOC. (2010). Don’t get one. The rate is variable as well. The only way the bank won’t win is what a lot of people did in the last Recession. Pull all you can in a HELOC and then walk away when the economy tanks. It will be your down payment on the next house when prices go to the bottom.

“The only way the bank won’t win…”

Good point – the banks draft the loan agreements, they have been to every rodeo for decades/centuries, and if macroecon takes them down you will be fed to the alligators first…

Translation – those loan agreement that few borrowers read and fewer understand, shift the maximum amount of risk to the borrowers.

If supply/demand, interest rates, or whatever turns to poop the borrower is going to catch it in the neck long before the bank has to lose a penny.

People seem to forget this because Boom Bust 1 took down both borrowers and lenders…but it took down borrowers first and most completely – 8 million foreclosures in a nation with just 50 million mortgages (though 75 million SFH).

No bailout for them, but bonuses for the AIG pudding heads.

Yeah. The boom/bust limits were really pushed by the big financial crooks on that one. What a massive wealth transfer!

All saved by the “due process” and other “laws” they had been modifying for 40-50 years.

Love that Heritage Foundation and it’s many inbred spawn!

Almost makes me want to put their flag on my PU.

A spokesman for Mr. Richard Holbrooke indicated that, while he had been on the Board of Directors for years, he certainly had no knowledge regarding the company’s finances or management decisions.

So, the strategy for future defaulters during a major downturn would be:

“Fugh it!” Just stop paying your mortgages/helocs whatever and then when you are pushed move out. In other words, “consumers” are learning how to play the game just like the “biggies”! They walk away all the time from monetary obligations when it suits them….and leave devastation in their wake(s).

Tishman Speyer defaults on loans frequently when the RE market tanks. They still get access to financing and still receive awards from cities.

Walk away? NOPE….they most all have to stay in the devastation, exactly like last time, only it will be worse, maybe debtor’s prisons, like the old English “solution” (or our Great Depression) to the homeless problem……vagrancy laws?

FDR haters rule!

Excuse me…..I meant Poor Houses….debtors prisons didn’t work….require maintenance effort……come to think of it, poor houses didn’t either….for the same reason.

I think they need more think tanks for this one, and I’m sure they have them.

Question is always timing of course I’m waiting for that bottom for awhile now and not in Connecticut or Illinois

It depends. My 2010 HELOC from Wells Fargo worked out very well as a bridge loan. At the 8-year mark, I bought a new house and put the existing one on the market.

The HELOC on the old home helped me pay cash for the new one, then three months later when the sale on the old one closed, the HELOC got paid off. I didn’t need to submit any new paperwork or incur costs for that bridge loan either.

Would I be correct that when you have pay off the Chase HELOC loan, you will not be doing business with Chase any more?

More and more housing being owned by corporations like Black Rock and by foreigners?

The whole United States is becoming a great big company store where the 400 billionaire families own everything and rent it back to us at inflated prices. From hospitals to student loans to homes.

Actually, I wonder if company town might be more accurate.

Ever wonder why so many companies fairly insanely remain located in SF/NYC/LA despite costs of living 3 to 4 times ntl median?

Ever wonder how much local residential real estate might actually be buried in their books?

You may have to pay your SF employee 2x wages there, but it pulls the sting a lot if you are his landlord or your RE is pumped up by his 4x mtg no matter who his landlord actually is.

No saying this is happening…but it is the kind of heads I win, tails I win thinking that the C suite gets the big bucks for.

I have heard from a few big companies in Netherlands who are doing this (basically cornering the local market), using free money from the stock market …

In some cases it probably makes sense because our housing market is so crazy that this is probably the main problem when trying to attrackt new employees.

But what about all the needles and shit in the streets? What about all the foreigners taking over? Why are people leaving this woke hell in droves?

Damn man, get your divisive political story straight!

(not that it will help you personally in the long run….actually, it really won’t help anyone, ya know?)

Isn’t that what we had in the Middle Ages? Guess history does repeat This will only go until the people say NO MORE

BlackRock Incorporated, BLK, is up 36% since 19 August 2019. The forward dividend yield is 2.62%.

I don’t play the game and I’m Happy!

@James-

>I don’t play the game and I’m Happy!

At what rate is your 401k plan growing? Or how about your savings account interest rate? You might not be a borrower, but you’re getting screwed along with everyone else. You’d have to be medicated to be, Happy.

I’m so screwed that:

– I’ve never worked a day in my life on a farm, and yet I am fed every single day

– I’ve never hammered a single nail into a building, and yet I’ve always had somewhere to live

– I never worked in a factory, and yet I have a big screen TV, a car, multiple computers, clothing, appliances, etc etc

– I never served in the military and yet there are soldiers out there fighting for my benefit (I’m not fond of military but to simplify the argument will assume that this fighting is necessary)

– I have never made a movie or written a book and yet I have a near infinite supply of entertainment at my fingertips

– I have never been a college professor or worked in a research lab and yet my every need is taken care of better and better each year as the mankind improves its technogical capabilities

– I’ve never worked in a school and yet I was educated for free from K – 12th grade and my kids now are as well

Sometimes I feel like the USA is set up to screw me, but then sometimes I remember how good my life is when I did nothing to deserve it other than being born.

Zane,

Your pt is that technological development has improved everyone’s life…fine, agreed.

But that isn’t to say that our current government misrule does not have huge distributional consequences – mainly benefiting/insulating from the consequences of their own stupidity/corruption those in charge of the printing press and those tied into them (the political class).

Technological development is not the result of political corruption – it is an impediment to it.

Do people deserve to enjoy the fruits of their labor? Do they deserve to benefit from technological advancement and increased productivity? Or do they deserve to hit a ceiling of buying power and then be effectively told by reading between the lines that hereto all excess value you produce shall be held onto by the corporate upper echelons? Heaven forbid people spend only their take-home pay. The Fed essentially whines deflation will take over if people do not juice the economy with consumer credit. Do these people have absolutely no sense of sustainability? There is obviously a sacred cow for them however, which by neglecting the financial health of the average American reveals it. They care more for the corporate money shower (in entrenched monopolies, there are two paradigms here in zombie corp America). When the money doesn’t trickle down to consumers, money velocity just keeps on dropping, unemployment is low and yet businesses still manage to be very picky about who they hire while still generally stonewalling over offered pay, then how can they wonder why inflation has not exploded despite balance sheet growth? The cycle of money flows, old fashioned supply and demand, not a liquidity issue is what they need to recognize.

No 40k and no credit by choice. I have everything covered and a second citizenship. I will no longer a serf in America at retirement time. I wonder where you will be in six years?

You should worry about the start of the super depression around 2026.

No more reviews or replies. Enjoy life!

Wolf,

Same concern about using GDP as literal common denominator in various ratios – too easily manipulated by Keynesian governments, too subject to inflationary distortion.

I know it is close to being a universal practice – that is the problem – it contaminates everyone’s frame of reference.

And the traditional fixes (backing out supposed inflation, etc) introduce their own problems of assumption.

I wonder if the G puts out a GDP figure that excludes the G component of the G+C+I+intl surplus formula for GDP.

It would not be perfect (each of the four components has impact on the others) but a straight back out of G might provide a more honest evaluation of what is really going on in the US economy – shorn of the gvt’s ability to artificially goose GDP via things like perpetual deficit financing and money printing.

I know it is more work (I will hunt for a net G figure too…) I just hate to see standard GDP as the near universal default measure used…it simply obscures heavier and heavier G involvement in the economy and its role in things like growth, debt, etc.

Same comment as in the other thread…

I suspect if you used median nominal household income, adjusted for growth in the number households you’ll end up with a similar denominator as if you’ve used nominal GDP.

There is a factual error in the article. The claim was made that because the rate oh home ownership is down, there are fewer mortgages. This is not true. In the article it states that the number of households is up. So if someone does the math, instead of 80 million mortgages there are now 83 million mortgages. Definitely not a decrease.

Mike K,

Good lordy. Homeownership rates are down, so there are fewer mortgages than there would have been at higher homeownership rates. That’s pretty basic. The homeownership data referred to the RATIO of mortgage-debt to GDP, and why this RATIO is lower.

The text clearly points out that in absolute dollars, total household mortgage debt is near the high of 2008 because the number of US households increased over years, along with prices and everything else in absolute numbers.

Cas127,

I understand your concern about GDP, but you’re barking up the wrong tree in this case, because here it doesn’t matter whether GDP is inflated or not because it is not the absolute percentage that is important but the change over time as depicted by the charts. If GDP is inflated, it’s always inflated. So the change over time would still tell you what you need to know. Other measures, such as nominal median household incomes, would give you similar charts.

Wolf,

I am looking at the debt as percent of nominal GDP chart.

If GDP excluding Gvt has grown much more slowly than GDP including Gvt, then the debt ratio would much higher using the former measure.

I understand the point that consistent mismeasurement is okay so long as only relative comparisons across time are being made…but my point is that G contribution to GDP calculation has certainly increased over time.

And that this G component is subject to more distortionary political bootstrapping (via perpetual deficit financing/money printing/etc) than the non G components.

These political expedients have real costs over time…and do not represent the sort of honest organic growth that GDP is intended to convey.

So you really can’t compare the GDP measurement of 2000 with the GDP measurement of 2019 because there is a higher pct of non-nutritional G spending sawdust mixed in with the C, I, and net exports.

In other words, the debt numerator is real but the GDP denominator is increasingly phoney baloney (because of an increasing “cooked” G contribution over time…).

Across time we are comparing apples to cyanide swollen apples – which is going to distort ratio analysis across time too.

Maybe there is a better way to phrase it…

And to the extent that no net-of-G GDP figure is easily available – it may not matter in practical terms.

I just hate to see the Feds being able to game public perception of economic well-being for yet another decade.

And GDP as denominator is very, very, very common usage.

The government doesn’t matter. The government just changes who spends the money and who produces, not necessarily how much.

Deficit spending certainly increases the GDP higher than it would otherwise be, meaning more people employed at higher wages producing more, but I don’t see that as necessarily a bad thing.

There was a time when I thought at some point the government was going to have to raise my taxes to pay down the federal debt. But no, if I’ve learned anything, we’ll just keep getting lower taxes.

Without government spending, it is quite obvious that everyone, including wealthy tax payers, would likely be much poorer.

Your argument is invalidated by the fact that as both Wolf and I mentioned several times already, if you use nominal median household income adjusted for the growth in the number of households as the basis for the denominator you’ll basically get the same results.

Between 2006 and 2019 US median household income is up about 35% (nominal) while the number of households grew about 12%.

HELOC down 300 billion, but student loans up 600 billion And personal credit up ??? billion. Certainly not a wash but per capita must be at or lower than 2009? Will make some people want to start binging again? Thoughts.

Actually between 2009 and now student loans are up almost 1 trillion.

As a percent of the economy, all other types of personal debt have held steady or declined.

As Wolf mentions this is driving the Fed bonkers. They want the consumer to take advantage of the asset values the Fed has artificially inflated but bitten once before in the previous crisis the peasants are not cooperating.

Luckily for the Fed though corporates and governments have eaten the bait. It’s gotten so crazy in the corporate market that PIK bonds are back! If that’s not a bell that gets rung at the top of a bubble them I don’t know what is.

Those are two DIFFERENT SETS OF BORROWERS. One can blow up, and the other can do just fine, independently.

Yes but the US dollar is a lot more vulnerable now than it was in 2009

I would think the state of the American debt slaves would explain some of it. Many owe so much for cars, credit cards, and houses they can’t borrow more.

In addition, where I live, many older houses are being refurbished and flipped so there is less need of HELOCs for home improvement.

Wolf,

Simple explanation of lower HELOC during ZIRP bubble 2.0?

People *do* learn – risk aversion simply up in wake of 1.0 and some maybe even understand how brittle alleged home valuations are in face of interest rates that (hopefully) have nowhere to go but up.

Evidence – CA new home sales in Bubble 2 are about half that from Bubble 1.

A lot of people won’t put their face on a hot stove…twice.

yes, some people have learned something, probably; and much of the young generation doesn’t have enough money/income to seriously get into debt yet by buying a home … but I’m sure central banks and politicians are working on that.

Most young people know they don’t have job security and never will. They learned by seeing what happened to their parents. You need a reliable income to buy a home and few young people have it.

Some of the same dynamics at play over here in Netherlands, all four points mentioned above are present to some extent. Home ownership rate is down here as well due to more homes owned by large (mostly foreign) and small (mostly local but increasingly foreign) investors/speculators.

Mortgage debt declined slightly after the Financial Crisis and is now probably back again near all time highs, but as percentage of GDP the debt is slightly lower now. Some homeowners have been paying off their mortgages while at the same time others have been refinancing, taking out equity or leveraging up for extra speculator properties.

Total savings in Netherlands (around 380M euro) keep increasing slowly despite ECB ZIRP/NIRP policy. That’s about 20K euro for every citizen, but of course most savers have very little savings and only a small percentage has a lot. Also savings and mortgage debt (about double the total savings amount) are very unevenly distributed. Clearly ECB policy is not working as officially planned, but that only means they will double down on their stupid policies.

HELOCs were mostly banned after the FC but are starting to appear again, but from what I know you can only borrow up to 50% of the current home value (which means most Dutch “owners” get nothing). It’s probably mostly for elderly people who have paid off their mortgage in the past and now need some extra money. At the same time, any Dutch buyer with a pulse can still get a 102% mortgage when buying a new home.

correction: total savings above should be 380B (Billion), not 380M.

I don’t believe they are tax deductible anymore either, I know that’s why I didn’t take one out recently.

I’m a mortgage originator. HELOCs are available, but not at the crazy levels pre-2008. The tax change is a factor, but also banks have paired down risk. 85% ltv max at some banks, 90% at others. Not many have an appetite for investment property HELOCs, so those are very difficult to get done. Levels over 80% LTV are typically priced at Prime or higher. The math just doesn’t pencil out when compared to a cash-out mortgage. NO COST ARM rates for jumbo loans are 3% or better. 30yr rates near 3.5%. Maybe you add .125% to rate for cash-out. Most of my clients that ask for a HELOC want it as a “rainy day” line, just in case, so they get the line, but don’t borrow the funds.

Dave K, TCJA ended HELOC interest deductibility for Federal Income Tax purposed, along with capping deductibility of mortgage interest at $750k of principal.

They’re tax-deductible now only for capital improvements to the home. That change is one of several reasons why HELOCs are down, but it’s probably a big one.

– One wouldn’t want a HELOC if ones income is unstable, and middle-class incomes are increasingly unstable.

– Fees are as high as for a regular mortgage.

– Interest rates can be expected to rise, and HELOCs normally come with variable rates that can also be expected to rise.

– Residential RE prices are in bubble mode in lots of places, and can be expected to fall.

– Banksters are not to be trusted. These guys are not your friends.

A HELOC can really only be justified if the situation is an emergency because the risks are high and increasing. Taking on that kind of debt for frivilous spending is the height of idiocy. Generally speaking, if you don’t have the money, you can’t afford it, and taking out a loan against your home isn’t going to change that.

And the last thing you want to do is to pay interest to a bank if you can possibly avoid it. They’re never going to reciprocate.

I do think it’s interesting that banksters are ready to start another debt-based meltdown by pushing HELOCs and other unproductive lending, falsely believing that the risk to themselves is minimal. It will be particularly interesting to see if the crash comes before or after Social Security has been privatised and put into the stock market to maximise the fall. Speculation has it that they’ll wait on the crash until shortly after.

SS will not be privatized but a haircut on pensions and government captured retirement money will be bailed in. The state of Ohio is already cutting back promised medical care for retirees. This trend will grow.

If deficits do not matter, what will prevent the Federal government from assuming the pension obligations of the states?

Rcohn the loss of reserve currency status will change all that “ deficits don’t matter” nonsense

Bankers are not my friends?

You mean t say that the:

‘Tell us your dreams and we will help’ ads are mendacious and misleading?

As a property insurance agent before the financial crisis of 08 I sold many HO policies 80 percent first mortgage with 20 percent on a line of credit at a higher interest rate. The mortgage broker told the client to come back in six months to refinance to take out the cash or reduce the line of credit. It worked well until it didn’t work at all for them just like the liar loans. I did not see this after financial crisis.

1) The UST3M don’t move since Nov, for 4M.

2) The 10Y had a selling climax in Sep, popup and now is back to a level slightly above Sept low.

3) In the last 5M the 10Y made a round trip.

4) When the 10Y will move down, breach the Sept low, HELOC will move up.

5) For a while, all rates, from: 1M, 3M, to 1Y, to 10Y & 30Y tangled with each other in a knot, created a wild bottleneck and inverted. Soon the

trend will be clear ==> the direction of all rates will be down in a military march.

Interesting from Wolf”When William Dudley was still president of the New York Fed, he addressed this refusal by households to do so. In a speech, he lamented this “change in household behavior” – that households have refused to turn home equity into retail sales and GDP growth, after getting burned during the mortgage crisis for having done the same. And the situation, from the Fed’s point of view, has gotten more dire.”

Maybe the extra equity is just not there? Still many stagnant or underwater since purchase? What is the typical debt to property appraised value ratio for HELOC + first mortgage? Are the appraisals now actually real as compared to 12 – 20 years ago?

Might just be a better product out there. If a private home equity lender goes bust you get to keep the money and tear up the contract? The flipside of Countrywide? When a commercial bank is in trouble they demand higher rates, or call the loan, or do all those things? They have the full backing of Congress, and you have??

Can you do a piece on Canadian HELOC’s?

Marko,

I did a quick search and came up with a few articles that show overall mortgages are increasing, but the trend for Cdn HELOCS are dropping.

“However, the new regulatory report offers contrasting evidence. It demonstrates that once the components of the combined mortgage-HELOC plans are disentangled, HELOC balances contracted over the past year while mortgages grew.”

However, if you want to feel depressed I have included a link to a Global news report.

“Linda Paul, a licensed insolvency trustee with MNP, says about 25 per cent of those with a HELOC do not have a proper plan, meaning their timeline for paying off their debt ranges from “five years to never.””

https://globalnews.ca/news/5439688/home-equity-loans-vancouver-real-estate-check/

From what I can see there are two different trends. There is a large Cdn group that sees debt as normal, and a smaller group (like our family) that simply won’t go into debt, ever.

The data is somewhat outdated, but he trends are the same. I compare both US and Canadian HELOC trends with 2018 data:

https://wolfstreet.com/2018/09/20/heloc-balances-u-s-canada-house-price-bubble-risks-housing-bust/

We are one of those families. We have a HELOC but don’t plan on using the money until the next crisis, then its time to buy low. I have learned by example, that its okay to file bankruptcy, even the president does it. It is no longer considered improper to file bankruptcy, its just good business. Why would i pay off credit cards and not my home? Many knew that the financial crisis was approaching, and didn’t alert the public then, and won’t do that now. Bankers are looking for the last greater fool. My family and I are okay, and were not greedy. We can wait our turn. The last 8 years could be a repeat of the decade leading to the great depression. Everyone that reads this is more educated in this area then me, but i see correlation. The financial crisis could be compared to the 1921 depression, republicans were elected in the 1920’s in all 3 branches of government and cut regulations and taxes. Does this sound familiar? Thank you Wolfe for this information.

The people that could use low interest rate HELOCs are now renting.

The corporations that hoovered up homes so everyone can be a renter get low interest rate credit from our friend the fed.

Home owners that do not really need low interest rate loans can get “have fun credit” from a credit card at 0% that gives “free stuff” back.

This leaves the middling home owner who is too shook, too underwater or already has a HELOC.

What’s Going on Here?

They’re not taking the bait. And they’re not that fooled into believing the US economy is all that great.

That’s a good thing, but it won’t matter because the coming meltdown will take down most people whether they have a HELOC or not. The US economy is increasingly unstable, as evidenced by recent Fed actions and long-term policy. Think about it: what stable financial system requires over $100 billion in overnight liquidity injections and a $4 trillion balance sheet? Notice that the Fed did not see the need for these actions coming, but reacted to a market that suddenly required it.

Clearly they’re not telling you something very important. And they’re not going to. They want it to be a surprise.

Not a good time to be taking out feel-good loans.

Wolf listed a bunch of good reasons why people might use HELOCs less, but there might be a couple more:

– Unattractive rates. Particularly with the short end of the curve inverted, taking out a HELOC might be more costly than simply refinancing into a new mortgage.

– Interest rate risk. HELOCs are variable-rate loans. Today’s rates are historically very very low – which means they’re likely to rise over time. Better to lock in a long-term mortgage at a low rate, than risk having your budget clobbered by a rising HELOC rate.

– Hassle factor. The extra paperwork and accounting are a “time tax”; is it worth the trouble to have a mortgage and a HELOC instead of just a mortgage?

– My personal favorite was banks’ ability to screw up the paperwork during the Great Recession, and then foreclose upon everyone in sight with fraudulent paperwork.

Wisdom Seeker,

Cash-out refis and HELOCs don’t serve the same purpose.

The big difference between a cash-out refi and a HELOC is that with a HELOC you get a line of credit that sits there unused, and that you can use LATER, and you don’t pay any interest until you use it, which might years down the road. Once you use it, the balance shows up in these balances here.

With cash-out refi, you pay interest on the additional cash from day one, even if you don’t need the cash at that point.

People and businesses get lines of credit to cover variable and irregular or unexpected cash needs, or to have the cash available when an opportunity arises without paying interest until then.

So if you don’t know when you will need the cash, a HELOC is a lot cheaper than a cash-out refi.

Wolf of course you’re correct about the details, but I don’t think that matters too much to many borrowers. There’s a lot of end-use overlap between the various forms of equity lending. People who view home equity as “dead money” will tap into as much of it as they can, and won’t be paying off those loans so long as rate-repression gives them better opportunities in stocks or real estate.

From the late 90’s through 2009, I hear of many who would borrow against equity however they could (either mortgage, home equity loan or HELOC) and use it for whatever they wanted, often to invest in the stock market or pay off student loans. The home equity vehicle didn’t matter much because the house would appreciate, rates would drop and people “knew” they could refi the balance in a year or two with lower payments. The poor ones would HELOC to cut the rate on their credit card balances or student loans, the richer ones would HELOC to pull cash for toys or an investment. Either way they’d wrap it into the mortgage later. To a consumer who wants cash in their wallet to spend, the nature of the vehicle doesn’t matter too much, but rate-shopping does.

Another place one might go for “quick cash” would be a 401K loan. Those with 401K might prefer to borrow from that – and “pay themselves” the interest – rather than borrow from a lender.

First time you get bitten.

Next time you run away.

Also, unlike govt and corp debt, here people are playing with their own money so naturally they’re going to be more cautious.

I seriously think they’re maxxed everybody I know that play’s the game, is constantly buying time-shares, going on vacations, and going out to dinner and buying expensive wine.

If that money is on the table at HELOC, then it will be grabbed.

I can only think that the ‘bank’ has truly made it harder, back in the 1990’s it was just your word that you were using the money to ‘fix up the house’, now perhaps they want proof? That could definitely take the wind out of the sales, since +50% of the HELOC was always a liar-loan.

1) Can the US 3M make a round trip, from zero to 2.4% and

back to zero : yes..

2) Will the 3M go below zero : not.

3) HELOC are households unrealized funds, the last resort, not for fun.

4) Germany bend the Fed will.

5) US 10Y – German 10Y in downtrend.

6) The German 2Y in a five year trading range, 0.5% wide.

In 2016 it was (-) 0.964 and On Feb 2018 it was (-) 0.43%. That’s the range.

7) The US 2Y was 0.5% in 2016, up to 2.98% On Nov 2018 and

now in a trading range around 1.4%. US 2Y is going wild.

8) The monthly German 3M had a huge buying tail in 2016,

reaching (-) 1.527, but in the last 2Y its stable, in a box 0.4% wide,

between (-) 1.001% and 0.6%.

9) Gravity between planets and continents and interest rates…

10) J.Powell tried please the big banks, lifting rates x4 times, but

the Germans didn’t budge, The US 3m might complete its round

trip, but the US 10Y will not. It will convert to NR.

Michael

I read your posts carefully, but I really don’t understand them at all.

Since you mention it, I find his posts clear as mud.

I usually start at the end, and read back towards the beginning!

cb:

I think his posts are highly stimulating and entertaining at the least. Reading this blog for several years only has increased my stupidity about the US (global) financial system; reading Engels posts only lets me know that I’m ok. He speaks in “tongues” and that’s ok because that is what the system does anyway…..sometimes I try to relate his words and lines to some kind of “Haiku” poetry…….Love those posts, Mr. Engels!

As a cryptologist*, I have been lured into attempting to decipher Michael’s posts. Recently, I had a breakthrough, as it appears that anagrams can provide important clues.

For example, “Germany bend the Fed will” is an anagram of “A Bed Friend Lengthy Mewl”.

;>)`

*nothing could be further from the truth

Well played, I’m glad I wasn’t drinking my coffee. My interpretation is the Germany is steering so buy bonds.

Michael Engel is our Oracle.

If you look carefully, many a nail is hit on the head.

“I read your posts carefully, but I really don’t understand them at all.”

Nobody does. Why do you think the Fed is trying to recruit him ?

LOL

Recruit him?

I thought he already was the Fed’s longest serving employee.

Is it possible that home owners realize that their home is just that ,a home? A place to live with a desire to own free and clear and not a piggy bank for a want other than a need. I hope so. However it is not settling to know that the government desire is to “churn” the equity with no value placed on the emotional state that debt free ownership brings. I will resist being turned into a commodity with ever fiber of my being and maybe the data reflects this sentiment.

This has been the image pushed forever.

That a home is a piggy-bank, for free cash as you need, that you lie about the reason for the HELOC that you say your fixing up the house, but really your buying toyz or travel.

You max out your HELOC, they REPO your house, and you do it again in a few years, rinse & repeat.

Welcome to America.

People who don’t live this life style are not doing their part to keep the machine running, people who hoard cash ( save ) or bad people, the only good people are debtors & spenders

Didn’t George Carlin say that exact same thing? Except he used a few obscenities

“people who hoard cash ( save ) or bad people, the only good people are debtors & spenders”

I believe this is in the Keynesian Pledge of Allegiance.

I guess I have always been slow to learn.. I never got that message about my home being a piggy bank. Probably came from living very insecure for most of my youth and as a young adult. My dad was a compulsive gambler and when he could, he’d gamble away his pay check. My mom went to work when I was very young and we were latch kids from an early age. Never enough to eat and the only toys I can remember were at our friends houses.

When I finally got to purchase a home all I wanted to do was pay it off so I couldn’t lose it and go back to insecurity. When I married, I married a person just like me who had grown up with insecurity and poverty. We were squirrels and kept putting nuts away for winter. Ended up being a great strategy.

We have different things that bring us a ‘Quality of Life’.

For me, having a home that’s not big or fancy, but is comfortable and paid off is the foundation for my quality of life.

A few years ago, a client of mine was in the process of doing a tear-down on St Paul’s Summit avenue (home to historically notable mansions), and we were discussing homes and architecture. My client was genuinely surprised that I was quite happy with my old Sears Craftsman bungalow and did not aspire to a larger and more expensive home. I sensed that she judged my status as being lower somehow???

People should to be prudent about taking on debt. I’m with Paulo on living debt-free.

I am still trying to understand “living debt free” now that my RE taxes are more than my mortgage payment and insurance combined. My mortgage interest is just the price of remaining liquid and worth it. I could pay off my mortgage 5x over.

I agree wiht Wisdom Seeker The elimination of the deduct ability of HELOC interest is simply driving this trend. If you had a HELOC that you could roll into a mortgage and retain the deduct ability of the interest regardless of what the funds were used for , why would you not? Especially at still historically low interest rates. If you wanted to use the equity of your home ( based on advancing values for the past 10 years I would guess there is a lot of equity out there) to finance things other than capital improvements a mortgage would also be the preferred vehicle. HELOCS are not as desirable as mortgages once the interest benefit is stripped away.

I find it rather amusing that little people being prudent is “dire” for central bankers!

It’s not dire for ‘bankers’, you give them way too much credit.

The entire USA system is a ponzi based on spending what you don’t have to eat the hamburger today, that you can’t pay for tomorrow.

Like Rome, once the money becomes worthless then the farmers will quit sending stuff to the city’s to make those hamburgers.

For now, party on Garth.

I find it fascinating that in my life time we have gone from the “Ben Franklin” model of spendthrift, to the modern rich guy whose entire wealth is what it he wears or has in his pocket.

When we were kids we were told to save, and to only buy what we could afford.

Emerson said “A man is rich in proportion to what he can afford not to buy”, the truly rich man, doesn’t buy anything, and he’s happy in an empty room.

Pascal said “The Eastern man is content in an empty room, the Western man needs a room full of garbage ( today we call it gadgets ), that this is the principal difference, and problem of the Western & Eastern man”.

This monkey syndrome was exploited post 1920’s with modern advertising and marketing, by just MSM ‘snake oil salesman’; Today the system is dependent as consumerism is what 80% of the economy?

The real deal is ‘free cash’ as in the future when there are no jobs, then why work, or who does work, will probably be those in prison, in a system where its finely tuned law’s on the books that ebb&flow the needed prison population. This is fascinating because USA&Australia both began as prison colonys, and now they have reverted to such. The “Notion” of Freedom is now Orwellian, that Debt-Slavery truly is Freedom

“For now, party on Garth.”

Or,

“More cowbell Jerome”

Methinks….

From Ben Franklin, to conspicuous consumption as a means to show your value or importance. Sounds like Hollywood or advertising won the war. I was a little surprised to see Chinese consumption rates. I thought it would be different than Hong Kong or the West.

Maybe it takes remembering hard times to be wise with your money, although I know many in our area who are pretty poor and spend any extra windfall as fast as possible for ‘stuff’ that sits out in the yard in the rain.

Gotta have a plan, and even then…….

I am not ashamed to say that I only learned to be wise and very prudent after a great crisis – lost all my customers for 4 years until my particular market recovered.

I wasn’t a huge fool before that, but I certainly learned a lot then.

I also insisted on not accepting help from generous friends and family and bearing the consequences: I saw it as a test of my character and endurance.

What did the little Austrian man with the tiny moustaches say?

What doesn’t kill you makes you strong.

It also makes you keep a very sharp eye out for what is coming, and to know what is real and what is spurious…..

Those who fail to plan, Plan to Fail!

“Maybe it takes remembering hard times to be wise with your money …”

Born in 1931, seen a lot of human behavior over the years and I believe that.

Just another indication of the continued failure of Central bank policy .

Have super low to negative real and nominal interest rates in Europe ignited a CAPEX boom? Hardly;the other side of the coin of very low interest rates is very low rates of return on capital.

Super low interest rates actually are and will have the opposite effect on consumers. Among the reasons is that older consumers , who have the most equity in their houses and the greatest amount of overall assets realize that they need to save more money to make up for the very low risk free returns.

Two questions for all readers.

Will massive liquidity injections by the PBOC cure the corona virus pandemic and make people and companies consumer more when 400m are quarantined ?

Realizing that there policies are an abject failure , will the Central Banks of the world repeat the example of Rudolf Havenstein , head of the Reishbank during the early 1920s.

“realize that they need to save more money to make up for the very low risk free returns.”

Interesting isn’t it that after 20 years of mashing the big red “print”/ZIRP button with America’s forehead (to diminishing or counterproductive returns) the Fed pays attention to only one aspect of the wealth effect.

Purely coincidental that it is the aspect that results in minimizing DC’s cost to service its 105+ pct gvt debt to GDP ratio…

2008 was a desperate time. The Fed walked in voluntarily and now the door has closed behind.

HELOCs no longer tax deductible. This is probably explains most of it.

I have a HELOC, but the last time I put anything on it was in 2011 to buy a new minivan. That is the last new car I have bought, as I keep them as long as possible. Why go into debt for a depreciating asset?

With the interest only deductible for capital improvements, and I’m no longer itemizing on my tax return, I’m letting my HELOC lapse at the next renewal.

No debt slaves in my household…

“That is the last new car I have bought, as I keep them as long as possible.”

I will never understand the old car mentality. Old cars aren’t cheap. I don’t care what car it is, how well it’s built, things wear out and need replacing. On average, several $1000s a year which increases the older the car gets.

And you’re driving a 10 year old car with 10 year old tech/safety.

The sweet spot is buying 2 years old and selling around 7-8 years old. You get in after the big initial wave, but still get some value on the other side before repair costs begin to creep up.

Car safety isn’t as much of a concern, fatality rates have plateaued over the last decade.

Just,

There are plenty of ten year old Toyota’s and some other brands that just run fine. If you maintain a well designed car it can last almost indefinitely. Fifty year old Dodge Darts with V8’s sell quite well on Hemmings and they were reliable cars with almost indestructible transmissions. They do rust, but in a warm dry climate they will last, and as long as they have disc brakes, they are quite safe.

Right but the well maintain part is expensive. Tires, brakes, fuel pumps, water pumps, alternators, cost a lot of to maintain. And that’s just the things designed to wear. Now add it a transmission failing or a head gasket issue.

Constantly pumping money into an old car is not a smart financial decision.

Maybe, but I’m happy with my 2004 at 42k miles and my 1999 at 57k miles. Careful maintenance is cheaper than payments. And, one heck of a lot less jazzy electronics in the dashboard to go wrong. Then for fun there’s the 1972 Lotus and the 1966 Triumph.

The solution to the Fed conundrum of forcing us to borrow against our homes is obviousness – Negative Interest Rates. Also a tax on savings. Why am I the only one to see this?

Collapse of the banks?

Gold will do great in such a scenario whether they make it illegal or not Gold IS money and no bureaucrat or Central banker can change that fact

When NIRP is imposed…almost everything that is not “money” is money, toilet paper, booze, painkillers, bullets, canned sardines – anything that will merely hold value.

My guess is that the G holds back on NIRP because it does not really want the populace ruminating on that too much.

Still waiting on my 2011 gold to break even. It was going to $5000 but didn’t. Caveat Emptor.

NIRP is starting in Netherlands in Q2 (for now -0.5% on savings accounts over 1 million, but I guess before end of the year anything over 100K and maybe even lower). We already have a wealth tax of 1.2-1.7% per year (since 2001). Banks are experimenting how low they can go and while most savers claim they will with draw their money when rates get negative, there are no good alternatives (Gold, after a 40% euro price increase within a little more than a year??).

People are saving more because they feel problems are lurking and the NIRP will only make it worse. Of course part of the savings will (again) leak into our RE markets so they can get even more epically expensive but it won’t help. Most of the RE speculators already have too much money and they aren’t spending any of it (and certainly not locally…). And all the others are squeezed even more so they will not increase spending either.

1) HELOC are unrealized emergency funds for rainy days.

2) If US rates cont their downtrend, other assets will join them, trending down.

3) The stock markets will be down.

4) RE prices will be down.

5) The banks will not lend, because home prices will changed.

6) HELOC are down 48%. They will cont to plunge.

7) The shadow banks will be in troubles, go BK, dragging the rest

of us to the mud.

I read all this stuff and I feel down.

For years I’ve respected Alex Trebek for never hawking reverse mortgages. All those old actors selling them online were pretty cheesy. But if Alex had given in, his credibility would have swayed many to blow their own house down for cruises.

The banks huff and puff to blown your house down….live within your actual means.

Live… below….. your means.

The up and down personal economic roller coaster ride will be easier to handle if you live below your means .

“Live… below….. your means. ”

To a point!

Once you get old and have a lot, what’s the point?

There must come a point where you might as well enjoy at least your income because time is getting shorter and there are no guarantees as to how long or how healthy you have left.

Old with children makes the difference, to me.

An inheritance can compensate them somewhat for their contributions to government programs sustaining my generation, over the years.

I will freeze in the dark, go hungry, and slit my own throat before I borrow against my very modest home. That is no exaggeration.

A decade ago my life was wrecked by a devastating illness which continues to this day. I was abandoned by my partner, who sued for my home. I was too sick to work but unable to get disability for six years. As soon as I received Medicaid the state tried to revoke it for no particular reason. I was forced into bankruptcy, having cashed out my small pension.

If there had been a mortgage lien on my home, I would’ve been dead long before now, since sick people don’t survive living under bridges.

Anybody who secures a loan with a lien on their home is taking a huge risk with their life. What are the odds of a US person being able to make huge monthly payments every month for 30 years?

Even 40 years ago the odds weren’t great. But today the odds must be approaching zero.

(Every day is a struggle, but I have what I need to survive.)

Ah……..feels soooooo…..good , enjoying our greasy back beans we canned with the comfort that we don’t have to eat beans but we like em’ and even more so with a side of NO DEBT!

Irrelevant. All irrelevant.

All that matters is that central banks have said about credit/debt/money

1 whatever it takes

2 we won’t make that mistake again (referring to letting the money supply contract after 1929

credit/debt/money =asset prices

asset prices are going to do nothing but go up and it does not matter one bit what the private economy does.

I’ve been through this drill last week on here. Got the internet treatment where someone tries to find one thing i said wrong and then pretend that invalidates the whole thing. It’s typical internet style of argument. Normally deployed by the left.

But the FACT is the central banks have been, are and are going to flood the world with fiat currency, and the laws of physics dictates that asset prices have nowhere to go but up.

Get a HELOC when you DON’T need it. Then just don’t abuse it. I was able to buy a house CASH ONLY on a Monday after it was advertised on a Sunday because of my access to cash. It can be useful as long as you’re smart enough to act like a grown up.

I am president of a bank, here’s the answer:

1. Helocs RARELY go above 80% LTV. (only for highest fico borrowers)

2. THOSE borrowers can get low teaser rates on credit cards

3. HELOC rates are no longer prime minus 2% (a la 2006), rather prime Plus 2%. The rates are not great.

4. The typical borrower will cash out their first mortgage to 80%, payoff credit cards, rack them up again, then cash out again.

5. HELOCS are f’ing hard to qualify for -the underwriting is tough. In the old days, you could go to 100% ltv with a signature.

6 AND YES, tax deductibility comes up too (roll HELOC into the first)

AS long as first mortgage rates stay in the mid-3’s, people are going to take the equity out using Fannie Mae, FHA, VA, or USDA.

“Cash-out refis have become popular again”

I really don’t see much difference between a cash out refi and a Heloc ( superficial view). Maybe it’s a regulatory issue and net mortgage debt is actually going up.

I don’t like that mortgage debt as a % of GDP chart, as GDP can be faked in so many ways.

” … banks and shadow banks want Americans to borrow in this manner and spend the money on vacations or home improvements or a new car, or whatever. Google them and see how they’re trying…”

Don’t have to Google – just look in your junk email box.

Wonder how the statistics mavens use data to tailor their approach to you? I have some anecdotal evidence: Some of my colleagues and I compare our junk email and, depending on our circumstances (there’s how the data is used. “They” know our attitudes and circumstances) we get different pitches. I get offers to buy my property – not many offers for a mortgage and none for a HELOC. Others get pitches to borrow.

Which do most recommend; getting a HELOC through commercial bank or schools first federal credit union?

A spokesman for Mr. Richard Holbrooke indicated that, while he had been on the AIG Board of Directors for years, he certainly had no knowledge regarding the company’s finances or management decisions.