Shares, which at peak-hype spiked 1,200% in a month, go to zero. Board of Directors goes to zero. Executives go to zero. Sales already zero.

By Wolf Richter for WOLF STREET.

Investors have been eager to plow vast sums of money into companies that offer products and services at an investor-subsidized price, the so-called cash-burn machines. They elbow into all kinds of markets and “disrupt” things. They include Uber and Lyft, WeWork, electric-scooter-rental outfits, such as Lime and Bird Rides, but also big and mature companies with thousands of employees and billions of dollars in sales, such as Netflix and Tesla, or the entire shale-oil-and-gas sector. Bedding retailer Casper is now heading for an IPO, at a price that will give its prior investors a big haircut, with the goal of getting retail investors involved in its cash-burn strategy.

But when investors get tired of funding these types of consumer subsidies, and refuse to provide more fuel to burn, than the music stops. This fate has now been finalized at the parent company of MoviePass – Helios & Matheson Analytics Inc. It said today in an SEC filing that it and its subsidiaries MoviePass and Zone Technologies each filed for Chapter 7 bankruptcy.

Everything has gone to zero, even the top executives (interim CEO and interim CFO) and the members of the Board of Directors, who all resigned, according to the filing, and there is no one left to run the place, and there is no place left to run. It will be up to the court to pick through the debris:

As a result of filing the Petition, a Chapter 7 trustee will be appointed by the Bankruptcy Court to administer the estate of the Company and to perform the duties set forth in Section 704 of the Code.

The stock scam.

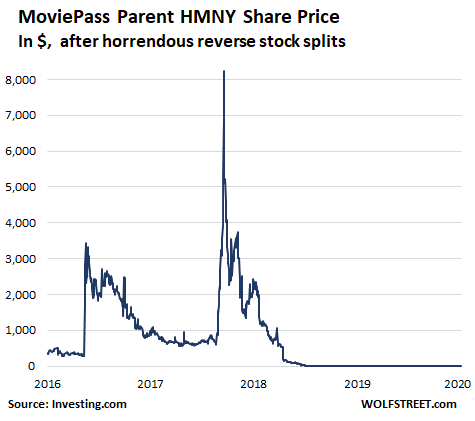

The stock [HMNY] fell 80% today from nearly nothing (fractions of a cent) to zero. Starting in August 2018, the shares went through a series of horrendous reverse stock splits to keep them dropping below $1 and to keep them from being delisted from the Nasdaq as they plunged. In February 2019, they were delisted anyway and have since traded over-the-counter.

In terms of the current number of share (following all the reverse stock splits), shares had spiked to $8,350 intraday on October 11, 2017 on all the MoviePass hype and how it would disrupt the movie theater business and the world in general. The scam artists on Wall Street got the stock to perform a miracle. Shares gained 1,200% in one month, from September 13 to October 11, 2017. But after peak-hype, shares collapsed:

At the time MoviePass offered a deal where for a fixed monthly fee of $9.95, subscribers could see a movie a day at any theater. Folks could gorge on movies, and MoviePass had to pay the theater the actual retail price of the ticket. In many cities, a single movie ticket cost a lot more then the subscription, and subscribers could see a dozen or more per month for $9.95.

It was one heck of a deal for movie-loving subscribers, funded by investors, as the company burned through cash at a blistering rate.

In the first half of 2018, the company was burning about $45 million a month subsidizing movie tickets. It then raised the subscription price to $14.95 and limited the number of movies people could see, and it said it would make money selling user data, but everyone already had this user data, and it was essentially worthless.

MoviePass wasn’t any different from other businesses whose business model calls for selling goods or services below the cost of doing so, and that constantly need new funds from investors to keep going.

The theory is that this cash-burn strategy gives them a competitive advantage over other businesses in that industry that have to make money and cannot therefore cut prices this far. With enough investor money to subsidize these companies, they can disrupt existing industries or create new niches.

But when investors get tired of throwing money at a cash-burn machine, the funds run out, and the fuel runs out, and the machine shuts down.

To avoid this fate, cash-burn machines need to entice investors by hook or crook to keep handing over their money and feel good about it. These cash-burn machines need to hold out the promise that there will always be future investors to bail them out with new money. MoviePass just wasn’t able to perform this hocus-pocus for long.

Another money-losing, cash-burning, over-hyped unicorn in a ho-hum low-tech business (bedding retailer) tries to make it out the IPO window. Read… Startup Unicorn Casper Sets IPO Price Range to Dish Out 36% Loss to Prior Investors

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

FED throwing another $400 billion at weak banks – how’d you short position work out for ya?

Apparently not all that great. I personally didn’t short but sold MA 1/2 and now it’s $20 higher per share…this is what I get for betting against insanity. Insanity is the new sanity apparently. Guess this bubble will go on for another 100 yrs perhaps…

I got out of my recent short term Nasdaq short today, made $38.71 total profit. Guess I can by a couple of beer mugs from Wolf, LOL. I got out today as the market is still somehow strong with a global pandemic, with 59% SP5000 companies in a buyback blackout this past week, and the Fed repo/QE moving down this week, yet the markets are still being held up by “something” invisible to my logic. It is the futures ramp I find amazing, relentless even with a 53% daily increase in the coronavirus infection rate. It will crash someday, yet some entity with deep pockets does not want it to crash yet.

At least you made money courtesy of Corona virus, not the beer.

Can this Corona virus “scare” really drive down the stock market?

It makes absolutely no sense to me as a very well trained Biologist, but as I see on TV ads, people are extremely ignorant when it comes to their own body….sadly.

Maybe not enough Prevegen taken?

Maybe it’s just the “reason de jour”, that we are all used to being provided with?

And what’s with this “bed thing”, like Caspar? I have a bad back and sleep fine on a 4″ thick futon on the floor that folds into 3 sections (so it fit my truck camper) that I have been sleeping on for 14 years (except for a year when I tried to make a go of it with a lady in Tucson).

Nobody is sleeping well in this stressed out culture? Even those who can drop $2K+ on a damned mattress aren’t sleeping well? Pretty weird goings on, other than the weirdness described in this article.

Yeah, btw, how is your short position, Wolf?

Why would you even ask that question?

Until the short is closed, nothing has ‘worked out’ either way. Don’t you understand that? It’s obvious. Why can’t you see that it’s obvious?

Short position is doing fine. SPY short is down 1%.

People only remember when the market is up and forget when the market is down, and then their whole perception changes. But look at a chart, and you’ll see.

And what “another $400 billion” exactly is the Fed throwing at weak banks?

https://wolfstreet.com/2020/01/23/feds-repos-drop-to-oct-level-t-bills-surge-but-mbs-fall-and-total-assets-decline-further/

Sure, but still my ongoing question is: what is the current rate of repo failure of repayment on these repos? When a repo fails on repayment with the FED it becomes indistinguishable from a small amount of QE. If the repo failure rate is only a few %, then yes these are mostly just loans, though even then a few % on $400 billion is still billions of dollars worth of “stealth” QE a day. But my real concern is that if the rate of repo failure with the current FED repo campaign is more then just a few % then really this whole program is just stealth QE.

I am willing to give the Fed the benefit of the doubt and assume the rate of repo failure is probably almost zero in the current regime, but it would be nice to be able to know that for certain to crush any lingering cynical fears that this could be a stealth QE program disguised as a loan program.

By definition there were a number of parties( banks / hedge funds which were in deep trouble. As long as these repos are rolled over these parties will survive. But if these repos are not rolled over , then the same underlying problems will be present and the entire financial system is at risk

@Rcohn

I understand that, but that isn’t what I am talking about. Repos aren’t called “loans” and are made distinct from loans because in theory unlike loans repo are collateralized enough that the both parties can just shrug and walk away if the borrower does not repay – no repercussions no one has to say or do anything. If the repo-lender (reverse-repo party) is the FED and the borrower does not repay, then the net effect is QE as the transaction has the net effect of creating a permanent liquidity injection from the Fed in exchange for bonds with respect to the non-repaying counterparty.

Now below is an extreme example but I am working with it just to demonstrate a point not suggest it is likely. Imagine if the Fed does $200 billion in repo a day. If it all gets paid back then yes it is just repo, its the “same” $200 billion every day so there is only $200 billion involved and when the Fed closes down repo operations the total liquidity the Fed has put into the system via this action is $0.

HOWEVER, lets say only 50% of it gets paid back every day and the rest is defaulted on (which we are not allowed to know about and there would be no repercussions for the counterparty). In this imaginary scenario the Fed hands out $200 billion every day, but only gets back $100 billion of this, and then it loans out another $200 billion the following day only getting back $100 billion (Again 50% default), and the next day, and the next day and the next day. In this scenario the Fed says “I am just loaning $200 billion to the market” and it is implied that it is the “same” $200 billion every day, but the reality here is that the net effect is the Fed is only lending the “same” $100 billion every day while permanently injecting $100 billion of stealth QE into the system every day just laundered through the repo program so it looks like a repo “loan” and no one besides the Fed and the counterparties receiving QE “under the table” via repo defaults knows that there is any stealth QE going on at all.

Again I don’t think the default rate is at 50%, instead it is probably closer to 0%. But the troubling thing is we don’t know what the default rate is and we aren’t allowed to know, and if the default rate is anything over 0% then there is effectively “stealth” net-QE being laundered through the Fed’s repo program as not all of that repo money comes back at the end of the repo term – the (secret) default residual becomes permanent, and then the Fed lends out the full amount the next day despite not having gotten all of it back the prior one.

Being a big fan of Doc Copper, can’t help but note it is now at $2.52/lb. I don’t know about recycling and ore quality in other parts of the world, but having had a GF in Tucson for 9 years who worked for SRK, a private, literally all over the world, S Africa local mining consulting company to all the big guys (Freeport, BHP etc) they can’t take it out of the ground in AZ for that price.

Almost nothing is built without copper.

When price was higher, and the mines in AZ running full blast, the word was China was stashing it, which makes them very smart. Maybe that is what’s in the bottom floors of those empty apts?

Anyway, industrially speaking, gold and silver are almost useless, and if it comes to barter because fiat paper is worthless?

HA HA HA! Give me Paulo’s survivalist pals .22 bricks ANYDAY.

PM nuts ARE nuts unless they just trade short term and are good at it.

How is this legal? Don’t companies have to get licenses to start and pay taxes and have accountants and send out quarterly reports?

I guess if the investors want to burn up their money, nobody wants to stop them!!! Don’t they have Moms and Dads and Sunday School and Dave Ramsey books???? What do they get out of the bonfire?

I read this morning from Bloomberg …

the company is facing probes by the Federal Trade Commission, the U.S. Securities and Exchange Commission, New York’s attorney general and four California district attorneys, the bankruptcy petition shows.

In cases like this, where a company says ‘we’re going to sell up to 300 dollars worth of goods/services for 9.95 a month’, shouldn’t the investigation have happened before they even get started?

There was never any hope of making money unless subscribers went to one movie every two months.

My local cinema chain has offered those passes for years. 21 Euro per month or as they advertise if you go more than once a month it is cheaper. But in their case i believe it is profitable.

At some point, someone needs to be able to make an actual profit somewhere. How long can this go on?

I guess as long as the people who subsidize the investors who subsidize unicorns can last.

I’m pretty sure those people are the rest of us.

It will go on until the powers that be either break something or they decide to finally pull the plug. Not sure which one will happen first. I have long stopped trying to apply logic to the illogical market.

For those of us in the real world who have to labor for a living our standard of living is in decline. As I am now about 3 years from retirement I have now pulled back on spending and focusing on saving as much as possible.

Our only choice is to starve the financial beast.

Yup by buying gold, silver and good quality rental property and getting out of fiat and paper products

?…but, I will pull out of stocks when I see the proper signals! What could go wrong? ???

The theory of low/ negative interest rates is that people will take advantage of low interest rates and increase spending. This has not happened on the Eurozone and will not happen in the US , outside of stock buybacks.

Your post is an example of the opposite , where millions of people cut back spending to save more money to make up for very low returns on their money .

PE is several steps ahead of you……the number of stocks people can invest in is dropping fast. Got $1-10M to get in on the real action?

7 out of 10 of the largest food producing conglomerates by SALES in the world are PE……might be 8 now, that info is several years old.

VC’s understand that the odds of these companies ever turning a profit.

I have been told – by a VC – that the game is to invest early – then ride along as others invest at higher valuations – then cash out — generally on an IPO but possibly sooner.

It’s called the circle jerk investment strategy and Softbank is the master of this. They are so good they don’t need a circle – they just keep jerking themselves off to higher and higher valuations using their own cash.

The suckers are slowly, oh so slowly, catching on. That’s the problem with being stupid, you lose all your money

Am I too late to get in on the funding bonanza? I am in the process of planning to market a diaper service to assisted living facilities in California of course and, possibly Arizona. Also, anyone signing up for a 6 month contract – yes, I realize these folks should not be even buying green bananas – will receive at no additional cost a double decaf latte with beyond milk skinny goat’s milk with agave syrup, shaved chocolate and bacon bits delivered every Friday and also Tuesdays, but only when the moon is blue, by Uber or Lyft. I think that I have a winner here….hopefully, I can get in on several rounds of serious funding. Act now, or be shut out forever!!!

Oops…almost forgot, we will also be marketing heavily to all WeWork locations. Only difference is their bacon bits will be vegan.

I don’t know, that sounds a little too much like it could actually be a business that at least in theory could possible turn a profit or at least break even. I think you need a pretty air-tight “business”-plan that guarantees its impossible for your business to ever be profitable no matter what (and the bigger the guaranteed losses the better) before all the “tech” VC show up to throw money at you for no good reason.

This Central Bank mirage is everywhere.

A court- approved sale of a local vacation/boat business. Accepted bid $2.6 million. Bank loan $8 million, unsecured creditors $5 million. Ergo $10 million of NOTHING.

Jacking up the nominal price of assets, begets unpayable debts.

“How long can this go on?”

As long as The Fed keeps counterfeiting, and giving their rich friends first access to the fraudulent “currency”.

I just finished this excellent synopsis of the poster child for unicorn failures, and I sat for about 5 minutes just staring into space.

Now that I have recovered from total disbelief that this company ever happened, I am thinking about that word ‘disrupter’

Selling products and services for under cost is VERY disruptive to companies that are trying run viable (i.e. profitable businesses)

I’ve been thinking of a disruptive business idea for some time now.

I have played with the idea of raising a billion or so and disrupting the coffee shop industry. This is where I sell the best coffee in the world for half the break even price. I drive all other shops in a city out of business then I raise my prices. If anyone dares to open a new coffee shop I open 3 within a block and those shops sell at half break even till the competitor is gone.

Another more blunt concept is to sell USD100 for $50. Do that until I drive the banks or the Fed or whatever the competition is (I have not worked out the details of whom I would deep six doing this)…

Then once that competition is gone then I have a monopoly on USD so I then sell the $100 for $125.

Genius – right?

I’ve got $100 to invest! Let’s do this!

“MoviePass wasn’t any different from other businesses whose business model calls for selling goods or services below the cost of doing so, and that constantly need new funds from investors to keep going.”

…

“To avoid this fate, cash-burn machines need to entice investors by hook or crook to keep handing over their money and feel good about it. These cash-burn machines need to hold out the promise that there will always be future investors to bail them out with new money.”

That is literally the definition of a ponzi scheme. There are laws against those and yet somehow there is an army of these cash-burn-[ponzi]-machines running around doing their thing in plain sight without any legal repercussions (at least not until bankruptcy, but by then lots of insiders have moved to they Caymans with other people’s money so that is too late).

Who is asleep at the switch? Who do we poke awake such that there are lawsuits, fines, and arrests to help clear these out of the system faster then waiting their natural protracted demise to clear them out of the system slowly, painfully, and with a lot of innocent (but dumb) people’s money?

Surely there is something that can be done other then waiting for all possible ponzi players to run their longest possible course of corruption and gorge themseleves as much as possible at the expense of society.

I believe Ponzi schemes pay early investors with money from later investors. I don’t think MoviePass investors received anything. The customers were the only ones who benefited.

“These cash-burn machines need to hold out the promise that there will always be future investors to bail them out with new money.”

^ Movie-Pass may have not found the “greater fool” investors they needed to pay out their earlier investors, but that is what their (unofficial but actual) business model was based on doing. Just because a Ponzi Scheme failed to enrich its creators doesn’t mean it wasn’t a Ponzi scheme, it just was a poorly run and executed one.

We don’t give bank robbers who fail to successfully rob a bank a pass on their criminality just because they are too incompetent to succeed when they actually set out to commit a crime. If the plan was innately criminal from inception, then trying to enact it is a crime even if it failed.

Bank robbers don’t know how to use the “laws of our land”…..they have been changing them a lot over the last 40-50 years, you know?

Those citizens who choose bank robbery as a profession should unite….and lobby more.

But we give a pass to bankers to steal from us all!

The pension fund managers are somewhere between totally incompetent and totally corrupt!

“Who is asleep at the switch?”

You vote for deregulation, you get no regulating…

Fools and their money are soon parted.

Regulation trying to protect all, only chokes a market out of existence. It has never protected fools from themselves or from the Ponzi schemers.

Yes, one must maintain absolute faith in those invisible hands that will guide us all to the promised land.

The last movie I saw in a theater, there was an advertisement for an AMC version of the MoviePass idea. So while the original MoviePass is dead, apparently the idea spawned copies run by the theater chains themselves.

It works for the movie chains cuz they usually make zero or break even profit on the tickets for the movies as that money goes to the movie studios/distributors. Where they get their profits are at the concession stands sales. Movie tickets become loss leaders to drive foot traffic in to sell concessions, which is where the profits are

I know the Marcus movie theatre chain has done various promotions for years, where they would attempt to get you to buy a movie “passport” which would allow you bulk see movies at a discount. It was very different than Moviepass though, they have had various promotions though, some were more similar to Moviepass.

It’s likely the movie theatre chains knew that Moviepass wouldn’t last, and thought it while bring in new people or be some other kind of promotion.

It might be possible though now that Moviepass popularized the idea for the chains to make a sustainable their chain only kind of Moviepass.

It’s important to remember that movie theatres make very little on ticket prices, they make it on the concessions.

It’s possible Moviepass was temporarily getting them extra money or maybe they accepted it to not lose customers to chains that did.

Their business model sounds vaguely like those travel agencies which fill empty rooms at a discount? $10 for unlimited movies, but put these people on standby. This stock market is a bit frothy. Squeezing unused capacity in any industry is a financially viable plan.

“A bit frothy” understatement of 2020 right there

Maybe investors will start examining some of the important policy changes that really need to be set up legally. The following link is a long read- but it’s really good to understand that yes there are some people that are putting out analysis, conclusions, and paths to counter the cash-burn machines. It won’t be easy, but it should create an alternative work that people could actually make money with the alternative processes, and engagement platforms.

https://itif.org/publications/2019/12/16/case-mostly-open-internet

I have my own theatre room, complete with about $10,000 of high end equipment. My family watches at least 1 movie each weekend, sometimes as many as three movies a week. I spend $4 to $6 for online movie rental, and about $10 on food and alchohol at home. At the commercial theater, I spend $48 on tickest ($12 x 4), and at least $50 on food and alchohol ($12 margaritas, $10 popcorn, etc). So I spend $10 at home theatre, and $100 at commercial theater. Take $90 more multiplied by 50 movies in a year (low estimate), and I “save” around $4,500 per year. We enjoy the home theatre more as the surround sound is superior to the commercial theater, the food and alchohol are more diverse, bathroom breaks and food breaks are possible without missing the movie, we do not have to travel in traffic to a theater, no worry about kids crying or sick people coughing, etc, etc, etc. I also laugh a lot at things that others seem to not find funnny, so that is a plus not being in public….ha Point being, movies at home are superior with the better equipment today, and more cost effective over time. I could stomach spending $50, but not $100. Just like cable TV today, the companies can keep raising prices while fewer people purchase their services, but unfortunately consumers now have choices, often more cost effective AND better quality. MoviePass is simply a money losing company based upon a “BlockBuster” dying industry, so logically, how could it not fail?

Very nice. The home theater. Keeps family together.

Stalin and Hitler loved home movies during the war: attendance, ahem, compulsory.

I believe that if either laughed, that was also obligatory….

$10k in high-end equipment so you can… stream highly compressed web video. Hm. I just use my iPad and sit on a fluffy pile of money, shouting “Keep printing, Jerome!” every so often.

Changemachine,

The actual resolution of movies played at movie theatres has dropped hugely over the years. Old 35mm film around since the early days of cinema have a resolution of at least 20 million pixels. There isn’t an exact pixel equivalent, because film is different than digital. Some say 35mm is equivalent to over 100 million pixels.

The last avengers movie, because of all the special effects, in an effort to save time and money reached your local movie theatre at a resolution of less than 3 million pixels. Most movies are shot digitally these days. And the 4k bluray “4k is 8.4 million pixels” version of that movie was of higher quality than the theatre. That iPad version of the top performing movie of last year is probably also greater than the picture quality of the theatre.

It’s very important to note that many movies are upscaled to fit the whole screen and aren’t really the stated resolution. That 4k bluray of avengers isn’t really 8.4 million pixels, but does have other touch-ups.

You can beat the theatre on picture quality pretty easily with a high quality led tv. OLED tvs blow the theatre away.

Beating a theatre on sound is trickier depending on if you’re willing to put speakers everywhere but a good spundbar work built-in subwoofers is most of the experience.

Overall under a $1,000 can beat the theatre. But, if you don’t want to spend that much; Those cheap Wal-Mart tvs are getting pretty competitive, picture wise, to the theatre.

The real problem is there is almost nothing to watch at the cinema. If Hollywood produced a steady stream of interesting flicks, there might be some demand. Ghost is playing at the local bargain night soon for $10/seat. We can rent it for $2.99 and make our own popcorn. To at a cherry on top, no one will be reading there phone or worse answering cellphone calls. I cant believe the multi-plexes stay in biz with $18 tix, $8 popcorn and $5 sugary drinks.

Yes. When the Arts and Humanities are looked upon as worthless degrees, it does seem to produce a dearth of culture.

“All the real talent is siphoned off into the Arts and Sciences, and that leaves the dregs to put it all together.” -Bucky Fuller

Thanks for continuing to point out these capital burning machines Wolf! The only way investors stop buying these unicorns is for the FED to stop bailing out the market every time it gets a cold(i.e. 4Q18).

I started trading stocks when I was 10 in the mid 1970’s. After college, I used the Peter Lynch principles to guide my stock picks. Today, I do not trust the stock market and the WS bankers that take companies like Blue Apron or Movie Pass public should be held accountable.

Alot of this is dependent on timing.There needs to

to be unlimited money and envy about the other guy

having made a killing on something or other. May be with the politics

and trade wars people may want to hold on to their cash

Naive comment, but aren’t there anti dumping laws? If you sell something below demonstrated (by industry norms) cost, isn’t that dumping? Competition is fine but deliberate market manipulation by dumping at below cost of manufacture is something else entirely. Countries go to battle using tariffs etc over this type of activity. “Gig economy” is wage theft AND dumping. Deliberate decimation of an industry’s incumbents by dumping (and/or using wage theft) in order to create a monopoly would surely be illegal… wouldn’t it? The “investors” would also be implicated in this activity and should have their “investments” punitively confiscated by the regulators if found engaged in this type of thing. Anyway, they certainly deserve their market induced haircuts.

Dumping is technically described as exporting goods at below cost thanks to direct government subsidies. While everybody is talking about “anti-dumping legislature”, very very little of substance is actually done by regulators, chiefly because everybody is doing it. A typical example is wine: yes, the Italian and Spanish governments heavily subsidize it (above and beyond the general EU subsidies as parte of the Common Agrarian Policy) but so do the governments of Aotearoa, Argentina, South Africa etc down to the State of California. How do you solve this problem? In the meanwhile the world is literally drowning in wine…

What MoviePass did, what Netflix, Lyft, Norwegian Air Shuttle, Delivery Hero etc are doing is technically not dumping because while we can argue until Kingdom comes about what subsidies they receive from governments, these are not direct. Much more critical all of these companies can still present themselves as in the early phases of their “disruptive business”: all businesses lose money in the early stages before turning a profit, right? This includes Netflix, which had been losing money for… how long exactly?

If private investors keep on willingly handing money at ultra-favorable conditions to your money-losing business common sense may be rolling in its grave but there’s no coercion. In fact people may be even line up to lend you money, as proven by the frankly alarming lithany of oversuscribed junk bond issues we read about weekly.

As the saying goes there’s no law against stupidity, otherwise the legal system would instantly grind to a halt.

hahahaha……the South Africa “government” subsidising anything other than failing state owned “enterprises”(south african airways, electricity supply commission (eskom), or “social security”…….fake news! a milllion taxpayers can only support the other 55 million so much….! we do make some pretty good wine though.

Agree……hollywood movies suck these days

I was surprised to see Netflix on the same list as cash burners. They burned cash for years selling cheap videos. One day they raised prices. Their subscribers stayed. They had net income of $1.87 billion TTM.

Movie Pass execs might face further liability.

In 1998 a penny stock promoter with a nationwide radio audience named Jerry Winger was indicted for his fraudulent stock promotion and trading activities. Wenger was sent to prison.

Typically it is caveat emptor – buyer beware in the stock market. People were seldom able to recover losses.

Netflix was ok when it was just a DVD service. It could even negotiate discounts for large buys of DVDs, if it agreed to delay getting them and renting them a few months after the first market release of the DVDs.

Then it started streaming online. The content owners initially gave Netflix rights to online streaming for almost nothing, cuz nobody realized that this was the next big thing. So Netflix was still OK

Now, every content owner is charging much higher fees, and some like Disney are completely withholding content they own from Netflix for their own streaming service.

So Netflix had to go into mega debt to pay for this streaming content. It is also trying to become an HBO or movie studio and producing content it owns, using even MORE DEBT.

That’s where Netflix’s cash burn debt machine started bloating up – getting caught in the Streaming Wars with the likes of Disney and Universal, etc

Just an accounting note

NFLX has reported a profit while it is bleeding cash. They do so via amortizing the videos that they produce over irrationally long periods.

Why the SEC allows this is the question

David Hall,

Yes, Netflix burned $3.26 billion in 2019. It shows an accounting profit and regularly burns more cash than just about anything else out there.

This needs to happen to more unicorns.

Fraudulently low interest rates that have no relationship to risk plus every large cap stock blowing tens of billions on buybacks has rendered fundamental investing to the dustbin.

It’s a shame that skill is no longer required for stock “investing.” Fomo MoMo bros dominate the arena with infantile btfd strategies and algos, squawking online about index ETFs like they are rooting for a football team.

RIP Peter Lynch.

He should rewrite his book and change the name from “One up on Wall Street,” to “One up on the the day.”

Off topic but can’t resist, a lot of bullshift and cash burn with this impeachment

May I substitute “caused” for “with”? Thank you.

Yes. Nothing goes to paradise in a straight line, but has anyone seen Tesla’s stock price after hours. I hope some folks caught the nearly 4 fold climb in price over the last 12 months.

I know Tesla only has 1% market share, or whatever, but i remember when Amazon had only 1% market share in book sales. Things change over time.

Tesla has amazing pull.. awesome brand appeal. Early innings.

akiddy111,

I sorted it out for you, the Tesla magic in all its glory:

Tesla’s Revenues +2%, Auto Revenue +0.7%. Net Income Plunges 25%. Without “Regulatory Credits,” it Would Have Lost $28 Million. Annual Loss Hits $862 million. Shares Spike 12%: OK, let’s look at the Tesla magic briefly…

https://wolfstreet.com/2020/01/29/teslas-revenues-2-auto-revenue-0-7-net-income-plunges-25-without-regulatory-credits-it-would-have-lost-28-million-annual-loss-hits-862-million-shares-spike-12/

Beautiful piece of writing Wolf! Your opening paragraph says it all, crisp and condensed.

Yes! And it included a piece “beginning rhyme”–when the first words of successive lines of poetry rhyme! (Full disclosure: had to look up this term)

Bedding retailer Casper is now

Heading for an IPO

People are investing in all kinds of madness because some payoff big time in this period of technological revolution.

Isn’t that the same business model as gambling at a casino?

Roddy-but so many are still “…shocked!, shocked!…” to discover that that is exactly what is going on in the financial sectors. Kudos always to Wolf for providing tout/shill-free commentary on what is transpiring.

may we all find a better day.

Fed Chairman Powell said today savers don’t have to worry about low interest rates on savings for their retirement because many who have savings also have homes that have gone up in value, and besides low income folks don’t want interest rates to rise because they benefit from all the cheap borrowing they have to do.

I think Powell trying to say to the savers with homes, that they should stop saving and take out loans against their valuable homes. Maybe invest that money into WeWork or Uber or Lyft or something.

Not saving but instead borrowing that’s why Powell likes and thinks it’s a good thing that he is punishing savers with low rates who after all have much more valuable homes now, and so they need to keep helping low income borrowers and start ups like MoviePass.

Timbers:. The irony of low or negative real interest rates is this environment creates more uncertainty in the minds of savers.

So in reaction to the increased future uncertainty, savers spend less and save more!

I think Powell is effectually saying – weather he realizes it or not – is he doesn’t want there to savers, only bowwerers. Or at a minimum, he doesn’t care about savers because he thinks they ought to be bowwerers.

The problem with monetizing the debt is the destruction of the currency. That would mean that any party who had bought the debt would own debt that had much less real value. When that starts to become apparent there will be NO buyers of the debt other than the FED.

And that is the reason why will not happen.

By golly, I’d forgotten than real estate is just an fungible and readily available as insured cash savings. And I also forgot that insured savings accounts can be reduced in value by fiat, but that housing values can only remain stable or rise. How did I forget all that?

Agreed, Timbers.

The tragedy of the Fed is its a small, obscenely overpaid, bank cartel tasked to supply cash to a Govt that always overspends, doesn’t want to tax, and can’t print by law.

Its got a near perfect 107 year history of doing so at the expense of savers’ units of measure and return – the US$, and more lately interest rates.

Its clever, and its theft by any other name.

When did your mother ever tell you to borrow and spend – never.

Neither should your Govt or your Fed.

One day it will break – when lenders work out the return offered does not compensate for risk.

It’s been a while but I’d like to remind readers that I am selling gambling debt backed securities.

LOL

If I remember correctly HMNY did not have reverse splits , but instead increase shares outstanding via private stock secondaries. The result for most shareholders was the same , but for those who bought stock in the secondaries was an almost guaranteed profit.

I saw an electronic billboard in the background of a scene in a post-apocalypse science fiction move. It read “Monetize your organs”. The Next Big Thing?

If only Wolf’s articles weren’t limited to just economics. Each article is well researched and thoughtfully presented–and then the real fun starts. Wolf street is without a doubt the best news site on the world wide web. the original article lights the fuse (howling about finance) and a chorus of (mostly) very bright and thoughtful folk round out the discussion. this kind of well rounded opinions is unique to this website. nowhere do i see such fun and intellect on display–regarding any subject. so well done Wolf for lighting the candle that gets the best and brightest off their collective arses and sharing their thoughts.

“At the time MoviePass offered a deal where for a fixed monthly fee of $9.95, subscribers could see a movie a day at any theater. Folks could gorge on movies, and MoviePass had to pay the theater the actual retail price of the ticket.”

So we’ve reached a point in the ‘investment landscape’ where you can make ridiculous claims like being able to base your business on a guaranteed loss, and still get your stock up 1200% in a month..?

This surely must be peak insanity. No wonder the Fed has to pump in 6.5 trillion in four months – and counting – to keep this sham going.

Protect yourselves – I have a feeling that within a few years people will be looking back on the wreckage and saying *what on earth were we thinking?”.

Any Japanese over the age of 50 knows the feeling.

There are a lot of idle 737s around. What if….

Lease 25 of them and keep till they are approved for flight again. Assign to a start up airline called…..uh……”BoingAir”. Also start up a travel subscription service under a different entity, we’ll call it…. well….”FlyMo”.

FlyMo will sell a monthly subscription for $650 and will allow you 3 flights per month to anywhere in the US. First it will book every ticket on BoingAir’s schedules, then move to buy up rows of seats on all the majors.

Next the parent of FlyMo and Boing….um…. “Jettage” will set an IPO (ticker JTGE) at a mere $35 per share. Millions will snap that up betting on the greater fool theory holding up again.

Figure the subscribers, and the IPO will get enough cash to burn for about 12 months before the whole thing comes apart. Now, the board and its directors and the close in managers all get huge salaries and exit bonuses just before they resign and file chapter 7.

Disclaimer: This entire scenario is a joke, and nothing like it could ever actually be accomplished. It is only a spoof on such activities.

Yet Elon Musk will likely launch such a company after selling Tesla or Space-X.

May I make a suggestion?

You monetize by taking big insurance policies on every passenger. Best to keep that part of the business plan confidential

Not such a spoof afterall?

“cash burn strategy” Lmao!./._

I’m brainstorming over a bottle of red and thinking about Movie Pass and Class Pass.

Absolutely brilliant ideas in terms of the new paradigm which is lose billions and get rich at the same time.

Elon Musk, Travis K and Adam Neumann are my idols – I have posters of them on my office wall.

Up until now I could only think of the coffee idea (sell premium coffee at a loss and drive Starbucks out of business and rule the coffee world), but now I have another idea.

Restaurant Pass. For $25 per month you get to eat as many meals as you want at my partner restaurants in your city.

Restaurants will be all over this because I pay them the full value of each meal, including all the booze and wine.

Does anyone think I will fail to sign up millions of subscribers?

But wait, say the sceptics in the audience, this is going to lose billions of dollars. Subscribers will eat out every meal and drink expensive wine and Champagne. You will lose your shirt!

To that I say … nnnnnnoooooooo…. I will lose my investors shirts – and pants and bras and suits and panties.

Because they will give me whatever I want because I will dazzle them with BS about how I will sell the data I gather on my millions of subscribers.

I will also befuddle them explaining how I will then start a food delivery company and exploit the data to ramp up a highly profitable sideline business (from the Travis playbook)

I have Elon’s former head of PR ready to come on board because he is an expert in convincing morons that useless data is worth billions, through clever placements in key media along with posts on websites using trolls.

And I intend to befriend Adam and get his advice on how I will extricate myself from this heaping pile of dung and walk away a billionaire.

Stay bloody well tuned.

I just sent a teaser message on Linkedin to Masayoshi Son and he is very excited. He’s asking for the corporate bank account number and will send over 1 billion dollars shortly

Moviepass – interesting business model – go short movie tickets and wait.

Lots of value add there, not.

Repo market – Primary dealers wont lend to it (too risky!) so Fed steps in. As long as they do that, players will arbitrage the risk free return with the Fed money.

Works until it doesnt – might take a while – but the Fed will blink first, as markets will win in the end, not the Fed.

I can imagine ClassPass und GymPass viewing the end of MoviePass with mixed feelings, if only for the sullied ..Pass suffix.

That MoviePass apparently paid full price for each visit speaks to their ineptitude. It should have been possible to translate flatrate-enabled, arguably incremental binge viewing into cheaper tickets, particularly since those discounted tickets would remain well hidden from the normal moviegoer who’s asked to pay full price. Or maybe they tried but the cinemas looked at the odd animal and decided to milk it while it still walked.

In comparison, gym subscription are usually underused outside of January, and being able to go to different gyms without additional costs is indeed compelling. So on the face of it there seems to be a real case for this model.

But this is the age of the cash burn machines as Wolf coined them so well, and things shouldn’t make too much sense. So, in my region, GymPass’s monthly cost are naturally subsidised by 50% by of course another cash burning machine – Wework.

Once again you are getting the name wrong. It is Netflakes. Please have some respect. Also check out where the genius behind the curtain of MP was a founder in the late 90’s….LOL