The priciest markets north of the San Francisco Bay.

By Wolf Richter for WOLF STREET.

California’s “Wine Country” is typically considered to include the counties of Napa, Sonoma, Mendocino, Lake, and Solano. We’ll look at the housing markets of the two most expensive, Napa and Sonoma; and at Marin County, sandwiched between the Golden Gate Bridge and Sonoma County. Marin County is not famous for wine, but for its beauty – including the Muir Woods National Monument, Mount Tamalpais, and Sausalito – and for being a high-end cloistered bedroom community of hurly-burly San Francisco.

Sonoma County.

Back in early August 2018, while the Bay Area Housing market was still considered to be on a trajectory of endless boom, I stuck my neck out to point at the underlying dynamics that indicated the market in Sonoma County was undergoing a turning point. I was leaning on data and boots-on-the-ground observations by Thomas Stone, a Sonoma County real estate broker.

The underlying dynamics have now settled down, going from a feverish market in early 2018 to something much more subdued, and prices have come down.

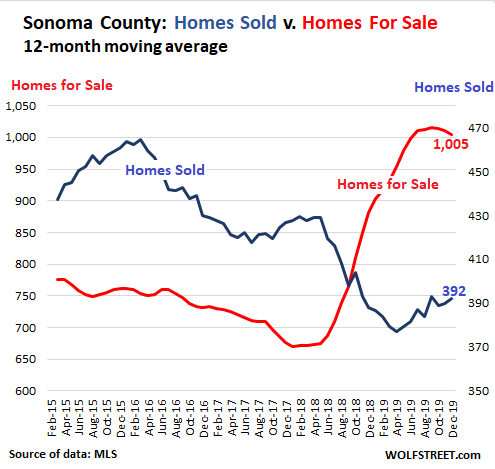

Supply has surged over the two-year period: 700 homes were for sale in December 2019 in Sonoma County, down 8.9% from December 2018, but up 72% from December 2017 (406 homes for sale).

And sales have fallen over the two-year period: 336 homes were sold in December, up 8.0% from December 2018 but down 8.7% from December 2017, and down 25% from December 2015 (450 home sales).

This data is very seasonal, with low points in the winter. The 12-month moving average eliminates the seasonality and shows the longer-term trends:

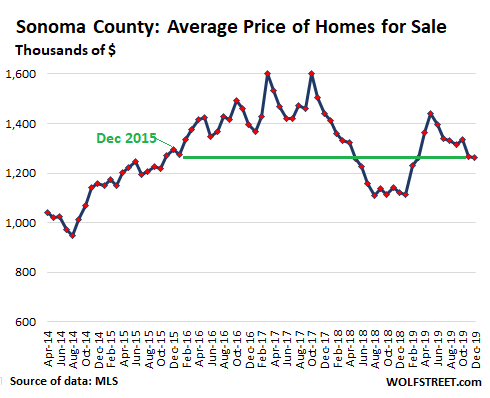

The average price of homes listed for sale went through a steep $500,000-drop between October 2017 ($1.6 million) to August 2018 ($1.1 million), then experienced a partial recovery, only to sag again, impacted by market conditions, as sellers were trying to find where the buyers are, and by the number and prices of high-end homes in the mix. The average price of homes for sale in December, at $1.26 million, was below where it had been in December 2015:

Homes remained on the market on average 72 days in December before they were either sold or pulled off the market, which was about flat compared to December 2018, but was up from 61 days in December 2017.

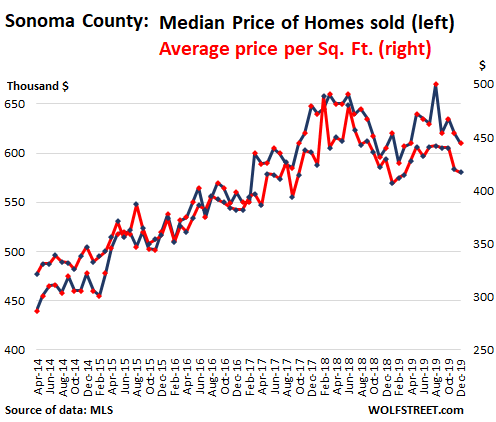

And prices of homes that have actually sold followed a similar pattern. Sonoma County doesn’t have that many transactions per month, and so data can get jumpy, influenced not only by changes in price levels but also by changes in the mix of homes that sold – for example, a greater proportion of large homes in the mix, which happened in August 2019, when the median price (half of the homes sold for more, half sold for less) spiked to $670,000 (blue line in the chart below), while the average price-per-square-foot, which eliminates the issue or larger homes in the mix, remained unchanged (red line).

Over the longer term, the median price and the average price per square foot show similar trends. In December:

- The median price, at $610,000, was down 10% from that August spike, was roughly flat with December 2018, and was down nearly 6% from December 2017.

- The average price-per-square-foot fell to $417, down 3% from December 2018 and down 4.4% from December 2017:

These prices include single-family houses and condos, but condos play only a small role, with 40 sales in December, and the median price dropped 13% from a year ago, to $345,000.

Napa County.

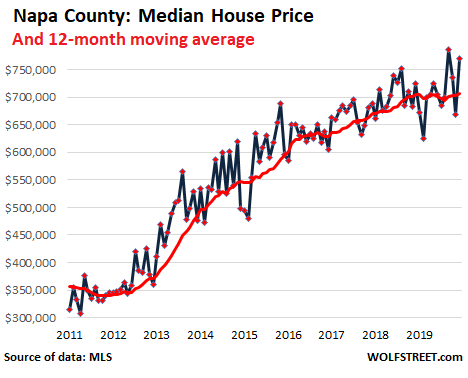

There are even fewer home sales per month in Napa County than in Sonoma County, and condos play practically no role, with zero condo sales in December (condo sales peaked in March and June with three sales each).

In December, 244 houses were for sale, down from 253 in December 2018. The average price of houses for sale, at $2.75 million, was up from $1.9 million in December 2018, with expensive homes lingering on the market and in the data for a long time. Overall, houses lingered on the market for longer, on average 88 days in December, before being sold or pulled off the market, compared to 80 days in December 2018.

And 82 houses sold, compared to 78 houses in December 2018. Because there are so few transactions in Napa County, the median price (blue line) is heavily influenced by the mix of houses sold – by a few higher-end units being sold, or by a few lower-end units being sold, entailing spikes and plunges in the median price each time. In December, the median price was $780,000. But the 12-month moving average, which irons out those spikes and plunges, at $706,000, has been flat for the past year (red line):

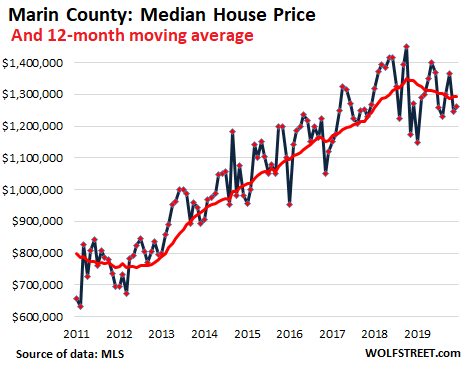

Marin County.

What is particularly interesting in Marin County is the huge seasonal variation in its inventory of homes for sale. At the seasonal peak in May 2019, there were 485 homes for sale. In September, there were still 444 homes for sale. But with the holidays approaching, homes were being pulled off the market, and by December, inventory had plunged to just 141 homes for sale – down from 175 a year earlier.

And 130 homes sold in December, up from 117 earlier. But homes lingered on the market longer, on average 77 days in December, up from 59 days a year earlier.

Year-over-year, the median price remained about flat at $1.26 million. The chart below shows the wild ride of the median price (blue line) in the low-volume environment, strongly impacted by the mix of homes that sold in each month. But the 12-month moving average has been steadily dropping since October 2018 ($1.35 million). By December 2019, at $1.29 million, it was down 4.2% from that October peak:

In Silicon Valley and San Francisco, the house prices hit a double peak – first in early 2018 and then in early to mid-2019, but have since dropped sharply, even as the Fed flooded the market with $400 billion in four months, with stocks at record highs, and with reality being pooh-pooed as irrelevant. What’s different this time… THE WOLF STREET REPORT: Housing Bubble 2 in San Francisco & Silicon Valley Has Lost its Mojo. Why?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

My sister has a house in Healdsburg ( Sonoma County) that she purchased in the last 5 years. She just missed getting it burned up this fire season. With the prospect of rolling blackouts by PG & E for at least the next 10 years she is considering selling it while fire insurance is still available. Once fire insurance is no longer affordable or available prices will take a steep dive.

Seneca

That is probably wise, although sad to hear. Many of us are in the same boat, even if folks don’t yet know it.

Last year I bought a Honda fire pump and 300′ of fire hose. We live on a river, but right next to some woods. All it takes is one idiot to get a fire going. Last May, said idiot decided to burn some brush and touched off a fire about 1.5 miles from us. It took 3-4 helicopters, 30 men, heavy equipment, and one week to put it out. I had the fire pump out and ready to go, just in case the fire turned towards our house. Anyway, getting out while it is still feasible may be wise. All those brown California hills just waiting to burn.

In BC we are developing emergency plans for all areas re: fire and earthquake. Yesterday, I attended a meeting where some pretty scary data was shared. We used to have 4 major weather events in 80 years, then 4 in 40, and now it is 4 in 20 years. Everything is speeding up. The BC Hydro spokesman said, “If you want to understand the weather future, look at California. It’s on the way”.

I wanted to add (but forgot) there is a big Condo insurance crunch already underway in Canada. Depending on claims history, some condos have seen insurance rates rise almost 700%. This has happened in Vancouver, and Ft McMurray which burned 2 years ago. Insurance rates are being adjusted as the coverage terms come up for renewal.

On Oct. 8, 1542, the Spanish explorer Juan Rodríguez Cabrillo saw smoke in the sky above Southern California while sailing off the coast.

Cabrillo’s pilot, Bartolomé Ferrelo, dutifully recorded the phenomena in the ship’s log, as the explorer christened the San Pedro roadstead “Bahía de los Fumos o Fuegos.”

Early settlers avoided the area due to the seasonal fires.

An area the size of England burned during the current Australian fire season.

What is your point?

Not even the largest fires in recent memory. 1974 and 1984 fires were even larger.

Aborigines used to start fires 300 years ago during the raining season to avoid massive fires during the dry season.

Now, with controlled burns outlawed, firebreaks outlawed and clearing brush outlawed – we wonder why there are massive fires?

“An area the size of England burned during the current Australian fire season.”

Controlled burns, firebreaks and brush clearing have never been “outlawed”, stop recycling Murdoch BS.

Australia has been in a drought for several years so there have rarely been the right conditions for controlled burns to take place.

This year is by far the most devastating fire season in recorded history in terms of impact on the population, economy, structures and wildlife. The 1974 fires burned a large area but in very remote locations. 1984 was not a major fire season.

Murdoch BS?? Wow, you don’t have to go to Australia to experience these restrictions. It can be a nightmare at the local level. I have clients that I advice to keep looking for another property because of ordinances/zoning, or subd. covenants that restrict the creation of a fire break.

It is hard for new owners to understand the danger of not having that fire break. Leaving fuel right up to the door step…

2banana,

“The point” is man made global warming is a proven fact.

I have personally experience this. The home on the sea coast of Quincy, Ma faces sea water rising 1/8 inch per year. This has been empirically confirmed by team of surveyors hired by the City of Quincy, to fight rezoning of parts of Quincy into flood zones. They mostly failed because the surveyors confirmed the rising sea level. My former house has placed into a flood zone 1 year after I sold in, because of the rising sea level.

I have also see global warming in my life time. I have noticed changes in the weather.

Banana, would you please your end comments with,

“Let not your heart be troubled”?

Thanks!……otherwise, they just seem kind of…….”incomplete”.

note to 2banana:

It’s a phenomenon.

Prices for insurance in areas directly affected by fires has increased dramatically. The state stepped in and forced the insurance companies to provide insurance at lower prices through 2021. After that it would not be surprising if insurance was unavailable in those areas.

Seneca, the agents in my office were told to make any offer contingent upon the ability to get fire insurance towar the end of 2018.

There’s always the FAIR plan, but it isn’t cheap and the coverage is not ideal.

Anyone contemplating the purchase of a home in the wine country should talk to an insurance Broker ( Not an agent, an experienced broker) before making an offer.

Broker’s deal with a variety of insurance companies and they can sometimes get you better coverage or the same coverage at a better price.

We faster the prices fall, the faster the Fed will destroy our purchasing power to prop the prices back up.

There is no where but up for prices in the long term.

I wish policy makers cared this much about the wages!

Policy makers only care about your impoverishment. When you realize this, everything will become clear to you.

AOC broke through the machine. There are a few bright lights cracking through if we can just send some more in to break up the corrupt system.

Basic human nature is to take care of yourself and those closest to you. Thousands of years of evolution have proven this out. Our environment is changing faster than we can evolve to keep up.

When you assume everyone cares about themselves and they can’t really help it, it screams that we need more control, not less, back in the hands of each individual.

Those that trust their needs to others, don’t understand human nature.

– Blame the baby boomers for pushing up real estate prices in the 1990s and early 2000s. The Millennial generation is (much) smaller and that’s why these lofty real estate prices aren’t sustainable in the long run.

– Just look at Japan. Since the peak in 1989/1990 japanese real estate prices have dropped by some 50 to 70%. In spite of massive QE by the japanese government and central bank.

@Willy2-

>Just look at Japan.

Indeed. And roughly twenty years ahead of us demographically.

if the Millennial generation is much smaller, aren’t they going to inherit a lot of precious RE later on?

In my country I see more and more twenty-somethings buying homes that one can impossibly buy on income, not even with the highest incomes in the area. It’s either inheritance money, parent piggy bank (basically also tax-free inheritance, but you receive it earlier in life) or drugs money (estimated to be a significant factor in driving up Dutch RE prices, in some parts of the country). Now that families are much smaller than in the previous generation inheriting RE can amount to a load of money (especially with older homes that should have been paid off by now).

The millennial generation (numbering 73 million ) is already bigger than the boomers (at 72 million).

Its generation X that is smaller than both.

By analyzing U.S Census data they found that in 2016 there were an estimated 71 million millennials, based on Pew’s definition of the generation which ranges from 1981 to 1996, compared to 74.1 million Baby Boomers.

https://en.wikipedia.org/wiki/Millennials

That’s probably true but will house prices keep up with the gold price That’s the question to ask I think we all know down deep that the dollar is on borrowed time only accelerated by Trumps policies of bullying adversaries as well as allies

Real estate is local but I see prices going up not down here is south california. Inventory is less than last year and prices are higher.

As i have said before, buy a house if you can afford it and plan to live in it.

If ever prices do come down, you wont qualify for a loan or the interest rate will be so high , your monthly payment will be higher.

Anyone paying attention, must know by now that the Fed is working hard to debase the currency. There was an article in the wall street journal about how the Fed is now planning to do repo directly with the hedge funds for Christ’s sake. The Fed is out of control.

Where do you invest in such a scenario?

Real estate is still the best investment out there, especially if you are already renting and plan to live in it for the foreseeable future.

Memento Mori,

Once again you are spot on. The notion that existed in certain circles of the Fed tightening and interest rates rising and inflation taking hold and Jerome Powell being his own man, was short lived. Most of these folks eventually saw the futility of it all. Some are still in denial.

But yes, the Fed will be more blatant in it’s efforts to keep things propped up than most people currently realize.

More importantly, the inflation rate for building new homes has been going at 5-10% per year for a few decades now. No such thing as low inflation as far as building new homes.

The US is also not Japan because its population is still increasing – more slowly, but still increasing, whereas Japan’s population is declining.

So, there is a floor to how low real estate prices can go in any drop, IMHO

“Real estate is still the best investment out there” – My first reaction was to scoff… then realized it may not be too far off. Everything is bubbly. I’d argue cash is the best short term investment but housing does give you the tax savings, at least until US gov’t jacks up taxes.

Note for anyone considering a purchase though… determine your local market “years to rental breakeven”. In Seattle area it is still greater than 10 years, so you better be damn confident of your job and life stability!

I have been looking at purchasing and renting out, because holding cash in strongly punished in Netherlands (minus 5% per year even assuming CPI data is correct) while RE profits are completely untaxed over here. While RE can still have positive yield, that 2-3% you can get realistically is quite low compared to the potential risk on the principal (home prices 10-20x higher than 30 years ago, with less than 2x income gains). And I also doubt the current extreme rents will stay so high after a market crash, in which case RE yield would be even lower. At some point our government will have to do something to counter our epic housing shortage, which probably means prices go down in future (the solution is simple, just politically very sensitive). But for now everyone is counting on further RE gains so they accept low or zero yield.

With cash in the bank you could lose everything above the insurance limit if there is a real market crash, but for me that risk seems pretty remote because my main bank is state-owned, so it would be difficult for them to default.

In most of the West it really comes down to finding the least bad option …

read my comment, I said if you are currently paying rent and plan to live in it, buy a house.

If you plan to rent to other people, there are different metrics you have to look at and they are not always attractive, depends where you look at, real estate is local.

@Memento:

yes I noticed the difference, in my case it would be partly for owning and partly for renting out (really big homes are at least relatively cheap like 4x the sqft for 2x the cost, but a waste of space – smaller home prices are totally nuts).

Owning is very cheap over here on a monthly basis thanks to low mortgage rates, but only if you have income; I don’t have income so I don’t get a mortgage and have to pay the full crazy price cash, unlike 99% of current buyers. And unlike a big chunk of current Dutch buyers, if the home value declines the government would not come to the rescue for me. This makes buying generally unattractive, even though the monthly cost of renting is 2-4x higher over here for the average person (with income).

My concern with RE (I do own some) is illiquidity. If (when) there is a major crunch you may have to hunker down and hold for years. Meanwhile the taxes and fees which will not have crashed continue unabated or increase.

Mortgage tax deductions was good till Trump tax ruined it at least for coastal cities.

I am in CA and my tax bill saw a hike because I no more can deduct the mortgage interest from my federal tax bill which really sucks :-(

So buying home ot save of tax is no more true at-least in expensive places

“Mortgage tax deductions was good till Trump tax ruined it at least for coastal cities.”

You mean when you stopped getting subsidized by the rest of America?

My income taxes increased 250% 2017 to 2018. In upper central US. Thank you middle-class tax breaks.

So buy a house at the top of Housing Bubble 2.0 so you can make a commission? How about #LearnToCode

1. Warren Buffet holds 125B Cash while FED is debasing it. I am sure you are smarter than Buffet.

2. There is NO “investing”, we are all currency/political speculator now. There is no more forecasting of cash flows and search for safety of margin. We just bet on directions of asset price moves driven by policies.

Yes, but we are not Warren Buffets.

He has investment opportunities that are beyond the reach of a normal middle class man. If there is a crash, he can go and buy companies at his own terms because of the vast amount of money he can raise.

If you have saved half a million on your account, who do you think really cares in the business world? That is pocket change to make a difference in any deal and also small enough to be eroded by the stealth inflation everyone is experiencing but not showing in government stats.

So what do you do with it?

At least real estate will keep up with inflation, you own it, you can add value to it if that is your thing, and you can live in it. Not so bad.

I would love to see a less risky investment with better return out there.

I don’t believe for a moment that RE will keep up with inflation over the next years.

In my country this was generally true from the early 1600’s until about 1975. Over the last years RE valuation has FAR outpaced inflation. Renters in the free market (outside social housing) now pay over 50% of their income on rent. I don’t see much room for this to keep up with inflation … more likely at some point house prices will come back to reality and/because speculators start selling. But because this is mostly decided by politics and not by economic or other factors, it is difficult to predict how long the current price surge will continue.

Read what happened with home prices in the ’30’s in the US, I remember reading about newly build trophy homes selling at 80-90% discount…

I know Wolf has had bad experiences with gold, but, for our times and conditions, it is by far the least risky investment out there, and I can cite some good company on that appraisal. If you live in Canada, the gold price has risen 18 out of the last 19 years. You will tread water with gold or possibly lose when currencies are being managed well, but when national currencies are being destroyed and real rates are negative, gold is a reliable choice. This is the “everything” (all asset) bubble. Only gold says “no,” and it is speaking clearly and audibly.

Laurence Hunt,

My, let’s say, “learning experience” was with silver, not gold. What that experience has taught me is that cycles in gold and silver are very long, stretching over many years, and outlast my patience. So if you catch the cycle right, it’s very good to you for a long time; but if you catch it wrong, it’s bad to you for very long time. Here is what I think you’re referring to:

https://wolfstreet.com/2018/09/04/my-theory-about-gold-and-silver-for-long-term-investors/

Actually, all I’m saying Wolf is that now happens to be one of those good, long cycles in gold and silver. I agree that I would not invest in this sector if the money supply and interest rates were not managed by cabals of ivory tower central bankers worldwide. The reason that value is not discernible in the everything bubble is that destroying value and misallocating capital is what these central planners specialize in. I’m with Schumpeter on how it all gets fixed. I’m a long-term optimist, at which point I’ll return to investing in the free market (when it’s free again).

Plenty of us qualified just fine in 2009… why do you think in a period of recession that rates will be higher? They never are during the crash, only possibly just before. If they do go sky high, asset prices will decline to match, then you can refinance out of it.

You should like another housing shill trying to get people to buy his overpriced shacks. I love how your only justification for RE at this point is your unwaivering faith that JPOW will prop you up indefinitely. Lets ignore that in many markets, renting is significantly cheaper than buying.

All of the housing bulls of WolfStreet of course became attached to this post like flies on sh**.

Reminder that the Sonoma Tubbs fire in 2017 destroyed 4,658 homes and killed 22 people. Its impact on upgraded building codes both within the City of San Rosa and county property along with fire insurance rates will impact the cost to rebuilt for years. Large number of homes that burned down in the hills were older and many were rented out to the wine tourist trade, those are gone and the income they generated. Large number of fire victims moved out of the area unable to afford rebuilding cost and sold their burnout lots instead.

Homelessness is a problem unlike San Francisco that cannot hide their homelessness Sonoma does a good job of keeping them out of sight in large encampments away from the wine tourist’s.

A link about rising insurance rates and housing prices. It is already underway. The market might be strong in some areas, but mortgage holders require insurance coverage. No coverage or too expensive rates = a drop in RE prices, regardless of location.

https://www.huffingtonpost.ca/entry/condo-insurance-canada_ca_5de813a3e4b0913e6f8a235c

“While not every case is as extreme, rising insurance costs can take a bite out of property values. ”

The only sure bet I make is that my insurance costs rise every year by at least 10%. This is from disasters occurring around the globe, and not where I live. There are only a few underwriters, and they don’t plan on losing money.

I can tell you Ford hand that in San Diego California.. I am looking to buy a home and lot of homes I liked are not able to get insurance because of fire hazard or very high premium

At the same time this is not yet priced in but I think it would make an impact soon

I meant first hand

Wolf,

Why not cover the CA mega counties – their ntl import is infinitely higher and I am guessing that data retrieval is about the same amt of effort.

In CA, I cover the Bay Area in greater detail a few times a year because I live here. So I covered Silicon Valley and SF in my podcast a couple of days ago. I covered the North Bay today. You’ll see this a few times a year. I pick up Southern California with my “Most Splendid Housing Bubble” series on a monthly basis, though this data (Case Shiller) is different and doesn’t provide that kind of detail.

Good article. Why is the whole comments section so scared? Calm down people. Everything will be okay.

Is that you Baron E de Rothshild ?

Fear of climate change is often worse than the disease. In fifty years they will look at the rising sea levels and say, what was all the fuss about? New tech IPOs will find ways to desalinize excess seawater and put out the fires. Co2 is vital for plant respiration. We should plant more vegetation to replace that which is burned. It is important to do something about climate change so some or all of these solutions might come about.

At the current pace in 50 years one third of the Netherlands, including the big majority of important infrastructure could be below water. We have impressive waterworks that were supposed to protect the country from flooding for the next 200 years. Those were finished one generation ago and we already know that in one generation they will offer very little protection, and there are no good alternatives. If we make the dikes higher, within 50 years or so the water will simply go under the dikes and the country will flood anyway. If sea levels keep rising (which I expect, as still nothing is done to really combat climate change and temperatures will rise far more than 1.5-2 degrees) the only real option will be to abandon the about half of the country. Some countries in e.g. Asia will fare even worse because they have no money for protective measures.

There are solutions but many of them will take a very long time to have significant effects; the only real solution is ditching the current consumption economy. Stopping the mad money printing of central banks (which fuels overconsumption and waste in general) would already go a long way in the right direction ;)

The EU/IMF is working on putting central bank authority on the problem. https://www.theguardian.com/business/2020/jan/17/head-of-imf-says-global-economy-risks-return-of-great-depression She is interested in carbon taxes which provide rebates to consumers (sounds like a corporate tax), and electricity rates to rise, (or a tariff on imported oil/LNG?) La Garde makes the case from ECB. I expect US to pull out of IMF/NATO. Trump demands Tesla build a plant here. We may have to export those cars if power rates rise.l

@Ambrose Bierce:

It is all a racket and will accomplish very little for the environment. ECB policy in practice will probably be similar to what the Dutch government is planning: raise taxes on ordinary consumers (irrespective of environmental footprint) and use it to subsidize the big energy polluters, so they can continue business as usual despite rising energy prices for almost everyone else. Dutch government is raising taxes for natural gas (which most Dutch homes use for heating etc.) and lowering electricity taxes; would be fun if the ECB forces electricity taxes up at the same time, so everything becomes much more expensive for the middle class (of course not for those that are Too Big To Comply – and in Netherlands those on the dole are shielded from increased energy cost too).

Trump pulling out of NATO? Great, let’s finally get rid of this warmonger institution. That would save us a lot of money and useless destruction.

desalination is energy expensive, hence expensive, even with 3 fold efficiency gains from current levels. it can only be indulged in in situations where energy is cheap, or if gains are considerable. which is rare when applied to large populations.

with 70 million gain in world population annually, vegetation is being lost. a soccer field worth every second. with all of current knowledge, increased forests or plant cover has not happened .

afforestation alone will provide a minor hiccup to the rate of co2 increase. every year mankind burns carbon that took a million years to sequester. decreased energy usage , 10 fold , is essential. meaning humans have to change the way they live. an impossible change till it will be forced upon us by nature.

this does not include potential methane release in the tundra and arctic. plants have no use of methane. methane is 1/200th the level of co2 and contributes upto 50 times as much to warming.

I hold to the worst case climate scenarios and I’m also a climate optimist. Climate change is the type of problem humans manage well, though not proactively. New technologies to address climate and environmental problems are literally emerging daily. My guess is that we will see the worst case scenario through about 2050, and then we will move rapidly away from carbon burning, led in large part by the oil companies themselves (oil companies are already building three prototype fusion reactors, which will be online in demonstration mode in only a few (~5) years.

With unlimited carbon-free and increasingly clean energy, we will buy ourselves at least a couple of centuries of breathing room. With lots of energy, we can desalinate seawater, pull carbon out of the atmosphere, send robots out to plant trees and protect forests, recycle our junk, and fabricate new stuff via recycling vs. mining, etc. That is, it will get MUCH worse, but then it will get rapidly better, and then we will have new problems to solve.

Through the whole process, governments and politicians will be followers, not leaders. The solutions will come out of the free market and the science labs (it will help if government invests in basic science).

Plants “respire” (breath) oxygen just like almost every living thing on earth (except for those strange single celled bugs that use sulphur and other oxidizers like in deep sea volcanic vents…where a lot of people think life started.) Plants use CO2 for photosynthesis, eventually making C-H, which parasitical living things use as food, and building material…… like us. Splitting water and producing O2 is a byproduct of photosynthesis.

But yeah, we need more plants, the ocean critters can’t do it all, and we don’t need more CO2.

Financial experts opining on scientific subjects is the stuff of comedy…..but black and tragic comedy, unfortunately. You all may be smart and educated but are woefully ignorant of even basic biology.

A big price will be paid for this, and it won’t show on any of your damned balance sheets, EVER.

If China steals more IP, California housing prices might fall like Toledo, Ohio.

It’s OK there’s always shipping containers or as the Zero Hedge article puts it “ Pod people” lifestyle for all the broke Millenials

Those pod homes sure look a bit dystopic; in reality it isn’t far removed from the situation in many Dutch cities in the fifties, with 10-30 people living in one worn-out home that today (after mortgaging to the max and upgrading) is inhabited by 1-2 wealthy boomers. When those older homes (often big canal houses etc.) come on the market they are now quickly split up again in “chicken farm” apartments because that maximizes the gain for the speculators. Before long there might be 10-30 tenants again in the building just like in the fifties; the apartments sure look a lot better now but they should, given the outrageous rents and other costs.

Container homes are fire proof aren’t they?

Or during a fire, they can double as a coffin.

if they steal more IP, don’t they have even more money to buy CA homes ? ;)

Wolf, I don’t think this is correct regarding Napa County:

“The average price of houses for sale, at $2.75 million, was up from $1.9 million in December 2018, with expensive homes lingering on the market and in the data for a long time.”

Miatadon,

It seems you read it wrong. This is the average ASKING price of homes LISTED FOR SALE – unsold inventory. This is very different from the median price of homes actually sold. The chart (2nd from the bottom) shows median prices of homes SOLD: $780,000 in Dec, with the 12-month moving average of $706,000.

A $5 million home may sit on the market for months before it sells, and so it will remain in and impact the inventory data a long time, but once it comes out of the data because it sold or is pulled, the average price of the remaining homes listed for sale drops sharply (that’s the nature of average prices). The same is true in the opposite direction: with one or two $5 million homes added to the inventory, the average price jumps. But a $500,000 home may sell in four weeks.

Napa has expensive estates, and some of them are more than $5 million. But it’s a small county with few homes listed for sale (244 in December), so pulling out a few expensive homes, or adding them to that inventory impacts the average price of homes listed for sale.

Thank you, Wolf. The number seemed too big relative to sales prices, but you explained what’s going on. By the way, I live in Napa Valley. There are several empty homes very near to where I live, rarely used by their wealthy owners. This is a phenomenon going on all over this region. And as many homes sit empty, the roads coming into the county are choked with workers coming from less costly areas to slave at the modestly-paying wine and tourism jobs.

Sssshhhhh…. don’t let Moms 4 Housing know. Or else you might be getting new neighbors soon :-)

GOOD qt, hope it happens. But break a couple windows and let them fill up with birds, bats, rats and mice. To display such excess when we have homeless is sick.

And don’t tell me it was their “hard earned money”.

r>g

Wolf, another factor may be the fear of fires and rising insurance premiums for the pricey houses. Those expensive places are more likely to be on acreage in a rural setting which would make them more vulnerable. I wonder if the difference in average prices of listed homes vs sold ones is smaller in more urban markets.

Yes, in Napa, Sonoma, and Marin fire insurance is a real issue.

If you go up Hwy 1, from 101, toward the Pacific, you climb through this steep hillside (foot of Mt. Tam), overgrown with eucalyptus trees. This is a densely populated neighborhood. You can get off Hwy 1 and drive into the neighborhood and take a look.

It is a disaster waiting to happen. If there ever is a fire (God forbid), it will race uphill, fed by these densely grown huge trees and all the shrubbery. The lanes to get out are tiny, windy, and steep, often only one-lane things. Even Hwy 1 is narrow (2 lanes), windy, and steep. People will need to evacuate well in advance or they won’t be able to get out.

I have no idea how an insurance company would assess fire risk in an area like this.

But it’s not an issue in San Francisco and the lower areas of the Peninsula (Silicon Valley).

In terms of Napa’s average price for sale, and median price sold, I think Napa is somewhat extreme in that there are very few transactions, and there are some very expensive properties, along with the much less expensive ones. It takes a long time in every market to sell a very-high-end home. It’s just that the market in Napa is so small that those few super-high-end homes that linger on the market for a long time distort the average price of all homes on the market.

“I can ask $50k for my 10 year old, broken down Chevy pickup, but where’s the buyer at that price?”

1) From x4 idiots in 80Y to x4 idiots in 20Y. Soon idiots will

fly bunch of balloons with a torch.

2) It was so cold in Alberta, even for Canadians. Oil shipment by rail was derailed.

Greta Thin-Burger with mayo : less oil is good for the climate change.

My comment was in reference to “Weather Events”. Our weather for the most part originates in the Pacific Ocean. The recent cold snap you referenced in Alberta occurred from a massive low pressure off shore, coupled with a high pressure in the Arctic.

Now here is where it might be hard to understand for climate change deniers. Climate Change happening right now is producing a jet stream flow that is in decline in velocity and prone to wander. When the jet stream sags, it allows the high pressure area to sag south with it. This used to be called a Rossby Wave. That term wasn’t sexy enough so they now call it a Polar Vortex.

BC Hydro produces electricity by…..guess it, hydro generation. Thus, they have a very very motivated reason for past weather data and accurate weather forecasting. Do they allow water to build behind dams, or do they release in anticipation of large rain events? What is the snow pack this year. And…Why? I live 50 miles from a set of 3 major dams and how they operate is of immense interest to our area.

I am also the communication leader for our area which means I run a communication centre with HF radios, a VHF repeater network, and all equipment is able to transmit data, text, and images over radio waves. It is a volunteer position. This is now being done throughout Canada because in an emergency weather event, or earthquake, a first result is the failing of cell phone coverage and landlines. This usually happens at the same time we lose power. (Like in Sonoma County this summer).

I don’t like Greata T either. She drives me nuts. However, only a fool disputes our climate is changing. Only the uninformed confuse weather with climate.

regards

I don’t think many people dispute that climate is changing. Has been since the beginning of time. What people dispute is that the climate change is caused by man. A recent science report from Finland showed that fossil fuels contribute less than 0.1% to climate. Not even statistically significant.

Have any statistically significant studies on ignorance, or wise yet willful agenda driven ignorance?

There, you have gotten a rise out of a coastal elite…in a 500sq ft apt……better enjoy it, it’s about all you have left until the second coming.

Imagine how low you have to be to not believe in climate change (despite the overhwelming science) AND feel a need to attack a 16 year old with aspergers because of it.

There are people that have not been Thunberged.

Two items I just read, that really puts the “SAME-NESS” into THIS TIME REALLY IS DIFFERENT:

1). “In a letter CFPB Director Kathy Kraninger sent to Congress today, the CFPB asked to amend the Ability to Repay/Qualified Mortgage rule (ATR/QM rule) in order to remove DTI as a qualifying factor in mortgage underwriting. This rule was created in response to the financial crisis of a decade ago as a way to prevent lending money to borrowers who might not be able to afford the loan.”

And on a similar if not 100% related note:

“Boeing is one of the few companies that uses a technique called program accounting. Rather than booking the huge costs of building the advanced 787 or other aircraft as it pays the bills, Boeing—with the blessing of its auditors and regulators and in line with accounting rules—defers those costs, spreading them out over the number of planes it expects to sell years into the future. That allows the company to include anticipated future profits in its current earnings. The idea is to give investors a read on the health of the company’s long-term investments.”

Everything is awesome!

‘That allows the company to include anticipated future profits in its current earnings.’

If your company can’t look great with that ability, you need a new accountant…

Has anyone notices that government agencies names and actions are an oxymoron of their responsibilities? The consumer financial protection board would appear to be about protecting the consumer. It seems ignoring debt levels of the public is just the opposite of protection. They should be renamed the Consumer Financial “Predatory” board. Housing must be very near its inflection point.

Have you read 1984? We’re almost there …

I think we’re closer to Brave New World with multiple classifications. We just haven’t implemented the test tube/petri dish thingy yet.

Yes, CFPB may not yet be captured, but is run by appointees that represent the thinking of those who appointed them.

What you say (agency capture), was (is?) the central thing the Econ Dept at the University of Chicago argued and I recall a book we had to read “The Logic of Collective Action” which says concentrated interests (corporations) have more and better reasons to lobby government and bend regulatory agencies to their wishes, than do individual Joe and Mary Citizen Voters…the regulatory agencies will always get captured by concentrated interests and serve them not us.

Don’t know what the solution is.

Revolution maybe?

I might have a partial solution to the Logic of Collective Action (which says corporations will beat us if we don’t figure something out):

1). Impeach and remove from office, and bar from future public office for all eternity, any Ivy League or non Ivy League Court Justice who was says Corporations people, on the grounds of gross professional and intellectual incompetence.

2). Define corporations for what they are – legal constructs – like parking ticket laws are legal constructs – and NOT people, and bar them from participation in the political process 100%, in ways shapes and forms. Including lobbying. They have ZERO political rights.

Not to wander off-subject (I did a few days ago and Wolf rightly x’d it out, heh, maybe this one, too…), but if corp.’s are ‘people’, why aren’t they registered and subject to the military draft?

May we all find a better day…

@ 91B20 1stCav (AUS) :

It sure seems like Google, Facebook, Twitter etc. etc. were drafted by the US military for social and cyber warfare operations; that is if you believe they were not started by the Deep State in the first place.

nhz-not ‘drafted’ in that their chance of becoming all-too-human cannon fodder (the ‘AUS’ in my handle tells you how I know this) is nil. Their ‘choice’, if granting your presumption, is if they wanted to receive any fat DARPA contracts, they would have to play ball on the MIC level. I agree with you, that the fallout of their choice is worldwide, and now emulated by national governments everywhere…

May we all find a better day.

Corps are one of the greatest wealth concentrating constructs developed by man. We didn’t revolt against a king, we revolted against English corporations running the king. They were hated for the first 20-30 years of this nation, but the borers (what lobbyists were called back then) did their thing, and by Lincoln’s time he feared them more than the southern army……said they had been “enthroned” and would eventually destroy the republic….we are there, Abe.

Good morning Wolf,

I had read online that there could be as many as 20 million homeowners in non- agency RMBS who have not paid a mortgage payment in years and are still in their homes. Can this be true or is this just online BS? This is suppose to be in certain states such as Hawaii and NJ. Thanks

interesting, would not surprise me …

In Netherlands more than 10% of households were severely underwater with their mortgage after the Financial Crisis. It took almost ten years for home values to recover (and overshoot) and a significant percentage is still underwater because these mortgages started at way over 100%. For most of these “owners” nothing bad happened, in some cases their rates went up a bit, in other cases part or even the complete mortgage was forgiven while people still live in their homes. In Netherlands you aren’t even registered as delinquent on the mortgage if you are one year behind in payments. At the same time, if you don’t pay rent for 3 months you are quickly evicted with no way to go.

The reason this charade continues is that in Netherlands cities have an obligation to find a new home for owners who are evicted (which apparently doesn’t apply to renters). And finding a new home in the current dysfunctional market can be extremely expensive for authorities so they prefer to paper things over with tax money.

*non-agency*. So, they are just squatting or baby sitting for private equity in the meantime. If there are no buyers at the right price or people cannot afford the rent, then I suppose allowing squatters is an option. This reminds me of the the two mothers evicted by SWAT and the Police in Oakland recently.

interesting thought, homeowners who are not paying the mortgage might be the new equivalent of squatters in the seventies/eighties, making sure the property is kept kind of safe for the banks or other “investors”. And if the banks are lucky, they can still collect some money from these non-paying “owners” later on, when they have found a real buyer (in most of Europe, maybe that would not be possible in the US when there is a new owner?).

Under Obama they kept people in their homes with section 8, and were doing stealth reintegration of middle class neighborhoods using HUD. They also placed immigrants in foreclosed homes. As Wolf notes sellers had a seasonal pullback, implies long term sellers who move in and out of the market. Makes you wonder how much excess inventory there is, families like that one in Oakland sound like long term squatters?

Nevada or So. Cal might be ground zero.

Anderson Phillips,

Hahaha. Your BS-o-meter was correctly red-lining.

Some basic numbers: There are about 81 million households in the US that own homes. About 1/3 of them own their home free and clear, so no mortgage at all. About 54 million households have a mortgage. So if 20 million households have not made a payment in years, it would mean that 40% of the households with a mortgage have not made a payment in years and would have been in default for years. This is total BS, obviously, as you correctly surmised.

And that’s TOTAL mortgages. There are not even enough non-agency RMBS out there for 20 million mortgages. Non-agency (“private label”) RMBS have been reduced to a tiny amount, compared to agency RMBS since the Financial Crisis. So this was really a ridiculous claim by someone.

Wolf, do you have numbers for corporate owned foreclosed properties?

Maybe he was trying to mean that.

I don’t off the top of my head. But it’s very small. During the mortgage crisis, about 10% of the mortgages defaulted — about 5 million or so mortgages in total. Most of them got processed fairly quickly, including in California. In some states, such as Florida, this could drag out for a long time. This was dependent on state law. Mortgages currently in foreclosure are at record lows. This includes mortgages that have been in foreclosure or in the prior stages of foreclosure for years.

I wonder how much of the Fed Repo is enabling large corporate players to hang on to these MBSes, directly or indirectly (like with derivatives)?

Similar moves are discussed in Netherlands; at the moment you can officially get a mortgage for 4.5x income (sometimes more with good career prospects etc.). But because mortgage rates are rockbottom (1.0% for 10y fixed, 1.5% for 30y fixed), 4.5x income is insufficient to buy even the cheapest homes in almost every part of the country (cheapest existing homes usually start at 7-8x income, cheapest new homes at 11-14x).

So politicians are again arguing that “in order to solve the housing crisis and unaffordability of homes in general” we should remove the cap and only look at what people can pay based on income and current mortgage rates. Bright idea, given that almost every Dutch mortgage is still 102% (basically subprime by US standards). But no problem, because the Dutch government guarantees all mortgages up to 300K (and soon even higher) against financial loss when selling, so even if prices go down nothing bad can happen . It’s great how authorities are taking good care of us :)

Interesting article, thanks! The seasonal variation here in Marin is fairly consistent year to year as sellers take their homes off the market during the slow holiday period to then re-launch in the spring. The big difference this year was the greater-than-usual amount of unsold inventory going into the holidays. We should see much of that coming back on in March.

Those sq foot numbers look a bit high, maybe not for Marin. Sq ft costs correlate directly to insurance premiums. This brings up the question of where is the service economy heading (more wage inflation?).

Phone booths. Only take up 9 square feet (when vertical). Easily moved in minutes. “Sitting is the new smoking” so a living environment that forces you to stand all the time is rather ideal. At current land prices, you only need about $4k to get your “foot in the booth”.

California is a failed State. The price of real estate is beginning to reflect that. As time goes on, the situation will continue to deteriorate. There is no hope of reversing the situation due to the Liberals hold on power, and the massive amount of unfunded liabilities.

From a different POV: living in a Chicago neighborhood on Lake Michigan I can see the accelerating pace of water levels rising.

The pace has been increasing significantly the past 3 year but this year it’s a whole new game:

The winds and floods over the Jan 11-12 weekend resulted in some epic flooding.

Lake Michigan hasn’t been this high since 1986-7, but don’t count on the lake receding.

https://www.weather.gov/lot/1011Jan2020

That is obviously a weather vs. a sea level phenomenon. However, one correlate of global warming is increased extremes, including both drought and flooding. Basically, warmer air holds more moisture, and changing climate changes where the different prevailing winds blow (or don’t).