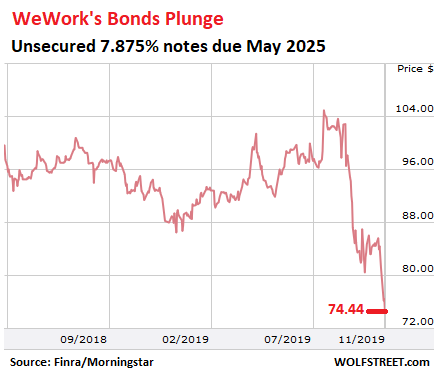

Tender Offer Didn’t Happen. Bonds Plunge to Record Low. This comes after WeWork reported a $1.25 billion loss in Q3. Second thoughts about throwing so many good billions after bad?

You’d think that by throwing billions of dollars at it, SoftBank would somehow manage to clean up this fiasco and make WeWork disappear from the headlines for a day or two, but no.

After WeWork’s IPO dream collapsed, and with the cash-burn machine operating so efficiently that it would run out of cash and face bankruptcy this year, SoftBank stepped in with a $9.5 billion bailout – a heroic effort to bail out its own prior $10 billion investment in the company by throwing good money after bad. In the process, WeWork’s valuation plunged from $47 billion to $8 billion, as decided by SoftBank.

The bailout included a $5 billion loan facility, a $1.5 billion cash investment, and a $3 billion tender offer to buy out some early investors and shareholders. This tender offer should have happened by November 6, but hasn’t happened yet, it was revealed today.

According to a letter sent to WeWork shareholders and obtained by The Real Deal, SoftBank was supposed to launch the tender offer “within five business days of the completion” of the $1.5 billion investment. WeWork made this $1.5 billion payment on October 30. So the deadline for commencing the tender offer would have been November 6.

But no tender offer was made, sources told The Real Deal:

A person close to SoftBank said the tender “is going to happen soon,” but would not provide a timeframe.

“It’s just taking a little more time than expected due to the time needed to get all the technicalities in order,” the individual said, without providing specifics.

These “technicalities” could be tricky. The Real Deal said that “the completion of the tender of is contingent on ‘the receipt of required regulatory approvals’ and the absence of litigation, bankruptcy proceedings and defaults on any debt owed, according to the letter.”

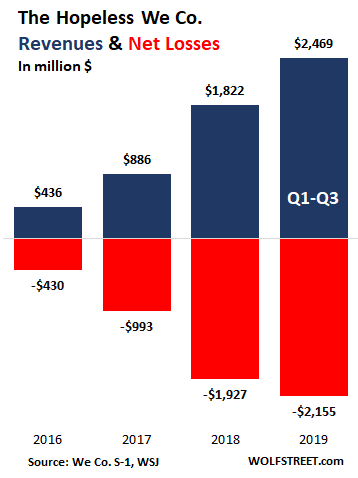

This comes a day after WeWork had reported to its debt holders a record quarterly loss of $1.25 billion for the third quarter. This loss exceeded its revenues of $934 million.

For the first three quarters of 2019, its loss ballooned to $2.16 billion, on $2.47 billion in revenues:

A double-whammy for its bonds, whereupon they hit a new record low. WeWork’s $702 million unsecured 7.875% bonds, issued in April last year and due in May 2025 – its only publicly traded securities – dropped to 74.44 cents on the dollar, down 29% from 105 in mid-August before the death spiral began. At the current price, these bonds yield 14.9%, assuming the coupon payments will be made and that the bond will be paid off — which clearly the bond holders have more and more doubts about:

Fitch rates the company CCC+ with Negative Outlook, which is in deep junk and considered “substantial risk.” Standard & Poor’s rate it one step higher, B-. Moody’s withdrew its credit rating of WeWork last year because it had “insufficient or otherwise inadequate information to support maintenance of the ratings,” and was done with it (my cheat sheet for the credit rating categories by Moody’s, S&P, and Fitch).

The original bet that investors took by buying these bonds was that WeWork’s IPO would raise so much money that it could easily keep burning cash and keep raising more cash to burn as its stock price would continue to soar and allow rich follow-on offerings so that it would have no trouble making coupon payments and eventually paying off the bonds at maturity, while continuing to burn cash.

Instead, they got the saga of the WeWork fiasco. And the prospect of those easy billions to be raised in an IPO and a series of follow-on offerings has now been replaced with the prospect of having to deal with SoftBank, which has its own problems, including massive WeWork-related losses at SoftBank and at its Vision Fund, and very nervous Saudi investors breathing down its neck.

It is ironic the Fed puts out this data, as if to show off its success, and how every time the wealth of the 1% is threatened, the Fed comes up with new bailouts, rate cuts, and other shenanigans. Read… How the Fed Boosts the 1%: Even the Upper Middle Class Loses Share of Household Wealth to the 1%. Bottom Half Gets Screwed

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

WeWork is a scam, but so are all Unicorns born in CALI

What we have here is an orchestrated effort to get Softbank to relinquish control of ARM, who makes all mobile phone CPU’s

This is another way for the HEGEMON to control Huawei

This is not about the WeWork scam, as everything is a scam.

While I concur about SillyCON valley giving birth to so many imaginary unicorns about to be slaughtered once the reality sets in and once plentiful liquidity tap dry out, doubt some kind of cabal is trying to extort Softbank to cough up ARM since Son-san already kowtow to the Fed and stopped selling chips to shady-as-hell Huawei.

Son-san is very sorry not to be able to follow through on losing more money. He is serious. He is not sure why improvement in revenue leads to ever larger losses, it is like the world has somehow gone mad. His other investments before Vision didn’t turn out this way.

This makes me wonder how much of his earlier success was due to him or someone working for him. Or perhaps, he outsourced his money making efforts to underlings, and they are failing him.

But it takes vision to lose billions, and even more vision to lose someone else’s billions. And while Son is not too bad at this, he is just a man, nothing like a system like the US government… but I’m sorry, the US debt is actually considered someone else’s assets. :)

Son-san should never, ever walk into the Saudi embassy alone.

Ouch. Nicely done.

Wondering what is main problem – does no one want to rent the space?

MCH

“…He is not sure why improvement in revenue leads to ever larger losses…His other investments before Vision didn’t turn out this way…”

Oh yes they did. Massa Son was the richest man in the world back around 2000, and lost $70B of his own money; SoftBank’s stock dropped 93% and almost went bankrupt.

Massa Son may be a lot of things, but “trusted steward of wealth” isn’t one of them. Son is a risk-junkie; an extremely high risk-junkie.

Well, to make lots of stuff… especially a mess, you need to break lots of eggs, sometime it doesn’t end up well.

Maybe he was just really lucky? Then he confuses the luck with skill, serving the sharks with their dinner!?

After all, He went at bought ARM almost right at the takeoff of mobile and embedded things which picked ARM as their preferred architecture. Back in the day, ARM was just a minnow, an IP-only provider with no wafer-making capacity, only one of many possible chip foundries that could have been used.

His downfall is because he gets confused by his wealth, the way it dissolves all problems encountered so far males it easy to believe that one ‘controls the future’ and that one is smarter than anyone else are.

This the point where the ‘actually a lot smarter than you are’-people will start smelling your honey-pot and come round with their grand visions!

He did not buy ARM “almost right at the takeoff of mobile”. SoftBank bought ARM in 2016. That at least 15 years after “the takeoff of mobile”, maybe 20, depending upon when you think mobile phones ‘took off’.

2016 is also around the time that smartphones stopped growing

Softbank didn’t get a cheap price on ARM, but never fear, it was the best investment they ever made.

Still all the drones, robots, phones, all use RISC

It’s a money-printing machine exceeding even the FED, which is why every Kleptocrat GOV is trying to steal ARM from Softbank

fajensen- Yep, these guys are basically one-trick-ponies, and when their trick goes out of style, they often don’t quit when they’re ahead; precisely because of what you say. They confuse their “some-luck and some-skill” for “all-skill”.

Peter Lynch, Magellan Fund manager was a perfect example. He was smart enough to get out at the top. Most aren’t that smart.

Well everybody is a one trick pony, and then you die, so what?

Like the guy said, “It’s better to have been a has been, then a has-not”

Most men ( think thoreau ) go through their entire lives doing nothing except obeying orders and kowtowing,

Very few men rise up and get stuff done,

But its an irony of an ignorant time, when any & every moron has a microphone to blow his horn

In his day Peter Lynch was gawd, and I still think he lives like a gawd compared to the great majority on earth ( actually Jim Simon is richer, but just keeps a lower profile – by design )

Softbank’s Son could lose 99% of his wealth, and still be a 1%-er in the gutter of that was once the USA.

Perhaps, SoftBank can partnership with the Saudi after their Aramco IPO! The IPO galore boom showing real cracks in their foundation! Soon the cash burners and IPO bubble is going to miss their bond payments and who will lend to them!

It feels like musical chairs coming soon!!

Saudi sovereign wealth fund buys a bunch of SoftBank shares, Vision fund buys a bunch of Aramco, infallible genius Jamie Dimon provides leverage to both…

Alex

A good deal of “infallible [J P Morgan’s] Jamie Dimon’s lending in the WeWork fiasco was secured by 100% restricted cash.

If you’re a J P Morcan shareholder, you like that A WHOLE LOT!

Yet JP Morgan’s stock has gone up since WeWork fiasco. What am I missing?

J P Moron – should be.

… and FED and ECB back it all up for JPM with ever more Not-QE money printing.

The risk with Saudi Investments is that, if it turns bad and goes to arbitration, one will lose an arm and a leg!

Hahaha.

Hopefully the employees of SoftBank’s companies can find a way to liquidate their holdings as well, if not, maybe they can create some patents, and put them up as collateral for a loan from JPM!

All aboard Softbank Fire Sale Express!

So… to try to get back ten billion… they lost almost ten billion more? Do these guys even know how to do simple math? Congrats! Now you lost 19.5 billions instead of just ten billions!

As Kenny Rogers said, ‘you’ve gotta know when to hold’ em, know when to fold’ em, and know when to walk away’.

It’s time for SoftBank to walk away.

Softbank executives have already stated multiple times they are “perfectly comfortable” with their debt levels and highly leveraged positions and I see no reason to doubt their assertion.

They just don’t care. At all.

They also know that they are going recoup a large chunk of that investment. But how is that even possible considering WeWork’s catastrophic accounting is all over the financial news?

Very simple: just look at the Saudi Aramco IPO.

It’s plastered all over the news, and I don’t mean the financial news: everybody is talking about it. Of course, if you read Bloomberg and other financial media they are full of cautious seasoned analysts questioning both Saudi Aramco’s real world valuation and the Kingdom’s growing budget holest, but people don’t read that stuff.

They absorb the glitzy propaganda concocted by Wall Street spin doctors and paid for by Mohammed Bin Salman about this once in a lifetime opportunity. They don’t care that even the London Stock Exchange has turned down the Aramco IPO (with its juicy fees) because the Saudi government is asking too much of a preferential treatment or that even the ruthless tycoons controlling the Hong Kong Stock Exchange have balked at the miles-long list of privileges the Saudi demand.

Softbank just needs a few months of such propaganda to wash away the bad news and people will be lining at their door for the WeWork IPO like nothing happened. Then in a month, or perhaps even a week, they’ll realize they have bought a cash burning machine with no unique technology and a terrible business model but at that point it won’t be Softbank’s problem anymore.

In Softbank corporate culture an extra $9.5 billion wasted to bring WeWork to a “successful” IPO (their metrics may be different from mine) are less than peanuts.

[They also know that they are going recoup a large chunk of that investment.]

*Falls out laughing.

Once upon a time I would have laughed with you but now, with the FTSE MIB over 23,500 and going only up and Greek 10-year bonds yielding a massive 0.5% I have learned to be careful.

Yes, WeWork is a disaster but does it really matter? All it matters is that people are ready to believe a fairytale such as how fast the Greek economy is growing or how “undervalued” Italian stocks are.

There’s far more money than common sense out there and if you can pump an asset class price high enough governments and central banks will perform acrobatics to prop it up even further. Just ask Jerome Powell.

raxadian

I’m not saying Massa Son is a rational investor (he seems to be explosively irrational), but here’s my read of his thinking (all $ rounded):

1) Before WeWork IPO went belly up, Vision Fund invested about $9.5B and Adam Neuman had absolute voting control with super-voting shares

2) WeWork IPO prospectus gets laughed off the stage; Neuman still has absolute voting control

3) Massa Son believes there is more that $10B salvage value in WeWork & pays Neuman roughly $1.7B to give up voting control & walk away (this is the famous $1B bonus + $5-700M cash to re-pay JP Morgan…)

4) Massa Son invests an additional $8B (including $3B stock repurchase) of SoftBank (not Vision Fund) money to control & turn-around WeWork

5) ASSUMING WeWork EVER DOES AN IPO FOR MORE THAN $9.5B, Vision Fund’s investment is recouped; for every dollar over $9.5B, SoftBank’s $10B “rescue investment” is reduced.

Like you, I don’t consider this rational, but Massa Son does – Son needs to protect Vision Fund investors (different from SoftBank investors) and he is doing this by putting SoftBank shareholders at risk.

For those keeping score at home: Vision Fund investors are exposed to $9.5B of WeWork risk, and SoftBank investors are exposed for another $10b.

Yours is the best explanation I have seen, and almost certainly correct.

Wework isn’t Uber, Tesla or Netflix, their business is based on renting and subrenting. They can be perfectly replaced by anyone in that type of business. They depend on how good office rentals are going. Uber can offer cheaper rides, Netflix can offer promotions, Tesla can offer upgrades, what can Wework offer to trick costumers?

Nothing, not with the hole they have in their budget.

There is noway Wework IPO is gonna go for 20 billion or a tad more, and that’s the minimun needed not to earn, but to cover the costs.

The huge problem here is that Wework rents to companies and small business not to the final customers.

What company does want to rent a place from a company that’s sinking? Is a huge risk, it means you can lose the place you are renting at any minute and that screws over your small business or company.

Tesla has their tech, Netflix has their huge library of movies and series, Uber… has an app?

What does Wework have that makes you say, this company has a future, or at least some collateral?

Wework owns NOTHING is all just rentals.

may as well, wont be able to sit for a while.

– Was Adam Neumann forced to pay back his 1.7 billion “bonus” by e.g. Softbank ?

No, he was not. That “bonus” was required for SoftBank to get (stock voting) control of WeWork from Neuman (who had super-voting stock). Apparently SoftBank did not own enough bonds to get creditor control of WeWork in bankruptcy.

Further, SoftBAnk provided about $5-6 hundred million to pay Neuman’s loans back to J P Morgan.

The NY papers claim he is looking to buy a $45M penthouse. That’s expensive even by NY standards.

The cyclical shift to private equity in the US is coming to an end. The “irrational exuberance” of WeWork is a classic sign of peak-bubble. For a decade, companies have shifted away from public scrutiny (like Wall Street), in favour of private deals with exaggerated valuations. Expect a shift back toward public deals (like Wall Street) in the 2020s. Investors will want more scrutiny and certainty.

You are probably wrong. Bad companies with too much debt often go private at a premium. In a previous age going private was one step away from going out of business, but not so much anymore. The shadow banking system is there to fund these things, and with yields in the free market at zero they can offer a real return. In ten years the S&P 500 might just be 50, and the listing covenants will probably be loosened to bring companies back to the exchange. (Including Chinese ADRs) If you are the CEO of this fund you don’t want shareholder scrutiny, you would prefer to go private, and for that you offer a better return. (CBs have prepared the way) After the S&P has it’s post monetary/political/trade deal meltdown, being private will look a whole lot better. The second point on that is the retail investor, and you might count pension funds, which are heading for the rocks as well. The moneyed players are tired of the children’s sandbox.

Another consequence of 32 years of monetary central planning, mispricing of risk, and punishment of saving and circumspection.

This feels like 2006, everything shooting straight up irrationally. I sense the smart money is dumping it all on the public. Buffets cash stash is a big clue.

Masayoshi Son, an ethnic Korean raised and living in Japan, having been discriminated by the Japanese for all his life has one thing in mind to prove himself superior to the Japanese, by achieving tremendous wealth for him.

This is the background for his concocting worldwide investment scam.

The whole business model is faulty. Even with bubble real estate prices and rents, they lose money. When a correction comes, commercial vacancies will skyrocket as they always do. Losses will snowball. Cue the sound of the anvil falling off the cliff onto Wiley Coyote’s head.

” Moody’s withdrew its credit rating of WeWork last year because it had “insufficient or otherwise inadequate information to support maintenance of the ratings,” ”

When “down grade after disaster has struck moodys” wont rate you, you in serious doo.

It’s crazy to me that Moody’s thinks this is hot garbage. But S&P gives them a B-

Seriously hard to understand that the rating agencies are still around after doing this same crap during the lead up to the housing crash.

We/They/Us never learn.

AlamedaRenter

“…Seriously hard to understand that the rating agencies are still around after doing this same crap…”

Well, consider the alternative:

1) My guess is less than 5% of the tens of millions of municipal bond investors can even meaningfully read a financial statement; of those that can, few can actually evaluate municipal (aka: political) credit risk

2) Over 50,000 states, cities, counties, municipalities, and other governmental agencies (example: mosquito districts here in FL) can and do issue muni bonds

3) A single muni bond issuer can issue several (some do hundreds) of bonds

4) No retail investor could possibly evaluate all that material, and no retail investor is willing to explicitly pay someone else to do it

5) Thus, the current 3 major rating agencies charge issuers (not retail investors) to rate their bonds

6) NOTA BENE: Federal courts have ruled “opinions” of rating agencies fall under “free speech” as opposed to “findings of fact”

It would be fantastic if somebody could come up with a business model eliminating this obvious conflict of interest…but no one has. That’s why, more-or-less, this same crap is allowed to continue: as bad as it is, it would be worse without it.

Great points and I get it.

With respect to 2, 3 and 4.

But sometimes I think that things like this would terribly complex….then I think about Google and/or Visa that can process hundreds of millions of transaction or search a minute and they seem to get to it right. Google processes something like 3.5-billion searches an hour. Visa is doing 150-million a day.

Seems like a database management issue. I’ve work with some database issues and 50K agencies times a couple hundred bonds…well…is actually a really small database.

Alameda Renter

Just to be clear: that’s 50,000 issuers with (I’m guessing here) 50-100 bonds per issuer – that’s 2,500,000 to 5,000,000 bonds (smaller issuers have many fewer bonds, larger ones have hundreds). Some of these bonds don’t trade for days on end (highly illiquid).

Governmental entities are not required to do GAAP to financial reporting – everybody pretty much makes it up (literally). With no consistency, a data base is meaningless.

Credit risk (forward looking) & financials (backward looking) are related, but are two very different concepts. Rating agencies must also factor in the local economic environment & political intent. This is pure voodoo and requires “tribal knowledge” about specific issuers.

If you figure out how to do this with pure technology (eg: search), you will make yourself a fortune.

Wolf,

On a very marginally related note (and an idea for a future post):

You mention in passing above about the withdrawn bond rating from one agency.

I have been concerned for a long time that the rating agencies torpedo (intentionally?) the accuracy of their annual downgrade/lifetime default stats by rating level, by ignoring the default outcomes of bonds once they have stopped rating them – in effect artificially reducing the numerator for default calculation purposes.

You might want to look into this since so many hundreds of billions in bonds are on the brink already.

To the extent that investors’ models assume the accuracy of the agencies’ lifetime default stats, any book cooking in this area could lead to additional major losses.

Cas127,

Agreed, this is an issue. But also, by now most or all investors who buy bonds outright (not bond mutual funds) understand what the ratings agencies are doing. Downgrades usually act as confirmation what the bond market already knew, or found out about painfully a day or two before the downgrade. Investors know that these downgrades are “reactive” rather than a warning.

Investors also know that the structural conflict of interest (bond issuer pays the ratings agency to rate the bonds to be issued) impacts the ratings, and they know that there is “ratings inflation.”

At the same time, these ratings are very useful — and the writeups are often detailed and insightful. They’re not the only factor to be considered, but one of the factors.

As bond investor, your goal would be to stay ahead of the downgrades and defaults, and not to get caught by surprise, which is not easy since these companies don’t always disclose what you really need to know.

In brief, yield trumps diligence in the era of history’s greatest all-asset bubble. As do all things, this, too, shall pass. Collapsing yields will take down valuations, which will (finally) end Greenspan’s 32-year bubble.

What a joke. Billions for a glorified office arranger. Just a scam that every slezzy financial salesman wanted in on, so they could sucker some poor mark out of their money. What next, monetize widgets and tittlywinks and sell their paper or electronic version in old folks homes or to street people? Get some Digital Mulch…anyone want to finance the IPO?

Now how long is that Digital Mulch good for?

The cyber compost is better.

I want a bit of both.

The salaried employee base at WeWork should be turning over rapidly now that the carrot of a big IPO is ruled out. Who wants to work at a place that is in severe cost-cutting mode and has no cash flow? Morale is going to hit rock bottom. WeWork should just hang it up. No use in throwing good money after bad.

As the rapacious globalist elites concentrate all wealth and power into their own venal hands, courtesy of their control over the central banks and capture of our institutions of governance, social unrest is spreading among screwed-over proles from Chile to Hong Kong. So here is some food for thought:

“People of privilege will always risk their complete destruction rather than surrender any material part of their advantage. Intellectual myopia, often called stupidity, is no doubt a reason. But the privileged also feel that their privileges, however egregious they may seem to others, are a solemn, basic, God-given right.”

— John Kenneth Galbraith

Gershom

Well said.

In the good ole’ days, this was called the “divine right of kings”. England forced King John to sign the Magna Carta in 1215, and it’s been a tough slog to defend the proposition that god did not, in fact, select [fill in name of despicable leader] to rule over, steal from, kill, rape and otherwise misbehave at the expense of citizens.

The pope, another true believe in “divine right to rule”, was furious, excommunicated King John, and stopped all English priests from conducting services.

Democratic elections certainly aren’t perfect, but try throwing the Chinese, Hong Kong, Syrian, Cuban, Saudi Arabian, or Venezuelan president out of office…or the pope

Interesting. I’ve heard people say the business culture in Korea is aggressive and shady, a bit like Wall Street. Profits, capitalism, efficiency, etc. are used to justify near anything.

It’s OK to screw your neighbor when he’s not looking, as long as you are a hard worker and exhibit some leadership.

Yes, that’s true. The Japanese elite hate him. He’s psychologically scarred. His family are extremely wealthy Korean mafia (controlling gambling, mostly) who were the source of his initial investment capital. As such, he could never, ever be employed by a Japanese bank. They keep lists of names of people they never hire. Korean Japanese are on that list. That’s why he called his company SoftBANK, a sort of revenge maneuver. Many ordinary people also hate him because he pays no tax, btw.

He has had only 2 successes really: Yahoo Japan and Ali Baba. His phone company landing exclusive rights to distribute iPhone is maybe another but his telephony service is atrocious for many (including myself when I was there).

It was amusing to watch him prop up his own share price after his disastrous losses announced recently (which he is still doing). He will spend Billions if he has to to keep the price up. Not only does his ego demand it but if the price slips too much and confidence is lost, SoftBank will collapse.

His recent result was not only a massive loss (~$6t) but his presentation was too. He vows no change to his style and to only plow forward. I doubt SB will ever earn a profit again.

In my neck of the woods there was this old building

full of old furniture.No body really knew what they did there.

We work bought it and turned into a real gem.Peeled all the old

paint and exposed the brick etc. Lifted the neighborhood

in a way.Shame they ran out of funds to do more of that.

Yes, they do spend a lot of money rehabbing old office buildings and interior spaces. That’s where in part their big cash-drain comes from.

WeSortaWork

U-Werk. We don’t.

If I understand WeWork correctly, it is a useful idea to open spaces for start-ups to work. The idea is not new since companies have offered “executive suites” to startups for decades (I worked in one in the 1990’s) and some cities and universities offer start-up/maker spaces.

Why is WeWork different? Other than the officers in the company are skimming 100’s of millions to pay executive salaries and hire a tremendous marketing team?

I’ve noticed that many companies are moving to a Home Office concept to save money. My company (not small) went from a requirement for EVERYONE to be in the office 5 years ago to a hard suggestion that everyone work from home now. Companies are trying to cut overhead so working from home achieves this. Unless you work from a $1M 2 bedroom condo with 2 babies, this may work. Companies are trying to pass overhead costs down to employees with working from home and reducing office space with visitor cubes.

In my team, 2/4 wanted to work from home. One member had a small noisy house with no office so they got an office space. The other had small kids and no space. They were not willing to sell their houses and buy a mega-mansion to work from home.

I don’t know how WeWork can work with the Corporate push to reduce overhead.

Will the trend to work from home drive bigger house purchases? Maybe. Though my 2/4 did not want to go more in debt with a bigger houses at this time in their lives.

I think the work from home trend has been reversing.

Microsoft, Amazon, and IBM are among WeWork’s largest tenants.

Is starbucks any different from any of the local coffee shops?

Yes. They have a distinctive logo and indifferent overworked personell.

Harold and JZ, these are great points.

For most companies, I see the trend to work from home is growing. The drive to reduce overhead is growing. A company that is hiring may offer trendy hip WeWork office space to lure new employees. It is hard to bring a new employee up to speed from a home office unless they already have experience (meaning older). New inexperienced hires would prefer WeWork. Corralling employees who work from home for a meeting can be like herding cats at times.

Our company is recommending experienced workers to work from home to open up office space for new hires. We haven’t moved to WeWork.

New inexperienced hires would prefer WeWork over a cheaper Executive Suites space. It is the “Starbucks” effect. Cool, hip, trendy, and most important, consistent across all sites. If you travel, the consistency and familiarity of Starbucks drives their business.

As Wolf has said, this requires low unemployment and tremendous growth in a company that is using WeWork.

WeWork and its investors bought into the myth of the decentralized office, with armies of 24 year olds working in hip cafe like environments. Sounds great in theory. In reality, most people still work as a full time employee in a cubicle in a suburban office park. The mythical 24 year old lounging on a couch somewhere creating “digital content” on his i-something doesn’t exist in enough volume to make this work.

So 6 million in revenues from 2016 was essentially a loss by 2017 the next year. The loss was glamorized into bubbling around the world and really kaputt way back in 2016. What a game.

My guess is there is drama associated with the terms of Neumann’s buyout.

Maybe the Saudis and/or Abu Dhabis want more clawback than Neumann getting literally billions for blowing up even more Saudi/Abu Dhabi billions.

Doesn’t the unicorn fiasco indicate a broader trend that will spell the death of the US stock market in ten years?

It appears there are no real companies with real profit models anymore. All the existing big companies dominate the landscape and prevent new growth. “Just give us your cheap money borrowed from the Fed”, seems to be the model for the unicorns.

The solution is obvious:

WeWork simply needs to tap into the Fed’s not QE, QE overnight repo market.

Funding problem solved.

Five Saudi banks are primary dealers.

I believe you’re referring to the Saudi government’s recent appointment of 5 Saudi banks as primary dealers for the Saudi government.

This has nothing to do with US government “primary dealers”, who are all US banks or US subsidiaries. There are about 25, and the list is easily Googled.

I may have the truth, just not the facts…

https://fortune.com/2019/10/14/fed-repo-market-crisis-saudi-arabia/

I have a theory

1) Chinese communist party has deep deep dirt on Masa Son from his time doing backroom deals with Alibaba

2) The CCP wants to disrupt the relationship between Saudi Arabia and the USA so China can ally with Saudi for the oil.

3) The CCP blackmails Masa Son into a scheme whereby he cons SA into putting billions in a company that will go bankrupt for sure in exchange for the CCP not exposing and prosecuting all of Masa’s dirty secrets

4) Masa complies and identifies WeWork as the best vector to bankrupt billions of SA money.

5) The chaos caused by the loss of Saudi wealth will cause political civil war which will result in MBS abdicating the throne.

Blue: That scenario may have some credibility but 10, 20 or even $30 Billion to the Saudis is chump change.

IMHO this may have more to do with arrogance breeding incompetence than anything else.

Just a thought

Cheers

If Khoshoggi’s killers are pumping, oh lets say 8 mil bbd, at $60 a barrel, that means about 4.8 bil per day in income. So, they make $30 bil in a week, easy.

On the other hand, if this was true, I’d still advise Mr. Son to stay out of any Saudi embassies. Most gangsters usually kill and torture not because of the money but to send a lesson to everyone else. Trump could tell the Clown Prince that, as I’m sure he’s very familiar with those sorts of people after doing a lot of of construction work in NY and NJ and running NJ casinos.

Nice Red-baiting.

It isn’t incompetence and arrogance combined into a “greater fool” play which failed, it is the nasty Chinese CCP.

Every Ponzi scheme has its legitimate expenses, used to set the glitzy stage and fancy costumes for the investors.

Just because WeWork spent their legitimate expenses on glitzy renovations and free coffee, doesn’t change the fact that the whole thing, is in fact, a Ponzi scheme.

Doesn’t get interesting until the YTW is 20%+.

I still think it goes way past that.

Wolf – Off topic, yet all the topics seem to come back to QE to some extent. I noticed that QE1, QE2, QE3, and “Not QE”, along with global central bank QE policies, are spiking with Health Care CPI costs in America. Is there a relationship between QE and Healthcare CPI? Another huge spike in Healhcare CPI is occuring with “Not QE”, just like the other spikes in 2012 and 2015/2016. I agree with one of the other reader comments, “We have built a world in which we can not afford to live in”. For example, I’m up to $23,000 per year for a family policy in which we have not used for the last five years, beyond basic checkups. I am not sure how much longer I can play this game, and it seems to me we are all becoming healthcare slaves, unless we flee the country to one which provides universal healthcare. I’d like to stay here, but not sure I can afford a $30,000 policy in 4.5 years from now (6% compounded per year). It will take the income of a $1,500,000 CD at 2% interest to cover such costs, which does not include the 2% inflation eating at the CD principle amount yearly. I guess we will all be forced into the stock market ponzi scheme soon enough, right before Wall Street crashes the system again on us for the third time in 20 years. Any articles addressing the out of control healthcare CPI would be appreciated. I do think you reach a large enough audience, that you carry weight in the financial community. I noticed your data is hitting a lot of other finacial sites, so many are noticing. Thanks for your efforts, they do make a huge difference, more than any of us can by ourselves…

Healthcare CPI chart:

https://www.zerohedge.com/s3/files/inline-images/healthcare%20inflation_0.jpg?itok=Ww0pugRD

The best thing you can do for your health is to stop reading ZeroHedge.

True , denial of reality is always good for your health

“unless we flee the country to one which provides universal healthcare.”

You could move to Netherlands which has universal healthcare, which costs just 100-150 EUR per month for ordinary citizens (completely free to foreign migrants, people with very low income or social security are partly compensated for this insurance cost). Like in many countries initially the monthly cost was much lower, healthcare premiums have risen way above official CPI almost every year and frequently common, effective treatments/drugs are eliminated from coverage. But still way cheaper than the US for a healthcare system that isn’t any worse IMHO. Sounds good?

Here’s the big trick: it isn’t healthcare insurance at all, it is just another tax. Everyone is forced to pay it (unless you are a deadbeat, foreign migrant etc.) and the real cost of Dutch healthcare is around 8000-9000 EUR per person on a yearly basis, which comes out of other taxes (income tax, wealth tax etc.); healthcare is easily the biggest part of the Dutch government budget with surging cost increases like everywhere in the developed world. But 95% of the population doesn’t want to understand this and thinks the insurance premium is the real cost (and that insurance increases track the real cost increase), and that the Dutch medical system and government are performing some magic.

Like with pensions and all the other government-mandated Ponzi schemes at some point there will be a rude awakening.

The first chart from the WSJ is beautifully symmetric! It would be an interesting experiment to removal all the numbers and letters, perhaps make the background some non-generic white, frame it suitably, and offer it for sale as art.

WeWork is actually a brilliant concept since many professionals are self-employed or have small business but don’t want responsibility of owning a loft or warehouse in cool spot in downtown location. Just don’t want to be running a small office or businesses!

Obviously, the business model is seriously flawed but is it’s financial scam?

Yes – the UK has a similar company that’s both profitable and listed. Its valued at around £1.5bn.

Wework was/is a scam because early investors invented a massive value for their shares and planned to get institutional investors (pension funds and index funds, who have a limited choice in which shares to buy) to pay them that value.

So, in America, the Land of the Lawyers who are not Free, what are the odds of a company WeWork’s size being ‘free of litigation’? Sounds like some fine print that somebody put in that the Financial Press didn’t notice.

I just had a thought that perhaps some number cruncher at Softbank just figured out that they could make more money by letting the bonds fall in price then scooping them out than by bailing out fellow shareholders? Softbank would of course be the people with the inside knowledge that Softbank wasn’t going to let the bonds go default, thus the only people who could buy those bonds confident that they were taking a risk much lower than the value of the bonds.

I keep putting tons of cash into this great white bowl, but each time I touch the silver handle, it all disappears. Maybe this next batch will be different eh?