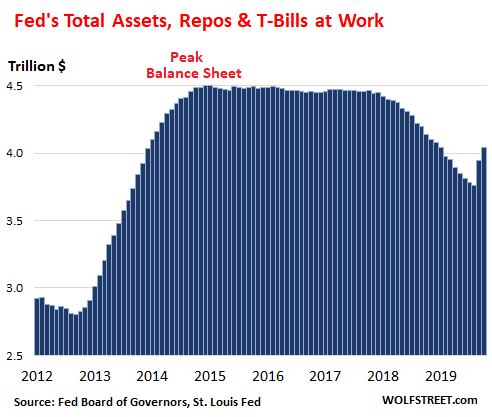

The fastest increase in assets for any two-month period since the post-Lehman freak show in late 2008 and early 2009.

Total assets on the Fed’s balance sheet, released today, jumped by $94 billion over the past month through November 6, to $4.04 trillion, after having jumped $184 billion in September. Over those two months combined, as the Fed got suckered by the repo market, it piled $278 billion onto it balance sheet, the fastest increase since the post-Lehman month in late 2008 and early 2009, when all heck had broken loose – this is how crazy the Fed has gotten trying to bail out the crybabies on Wall Street:

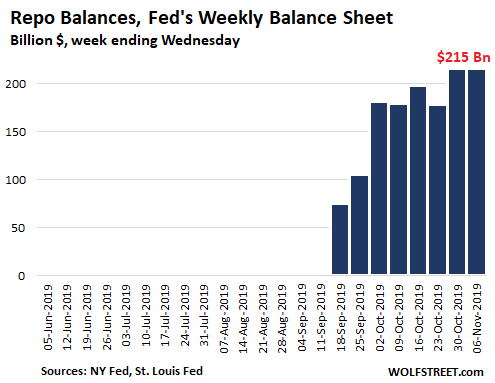

Repos

In response to the repo market blowout that recommenced in mid-September, the New York Fed jumped back into the repo market with both feet. Back in the day, it used to conduct repo operations routinely as its standard way of controlling short-term interest rates. But during the Financial Crisis, the Fed switched from repo operations to emergency bailout loans, zero-interest-rate policy, QE, and paying interest on excess reserves. Repos were no longer needed to control short-term rates and were abandoned.

Then in September, as repo rates spiked, the New York Fed dragged its big gun back out of the shed. With the repurchase agreements, the Fed buys Treasury securities and mortgage-backed securities guaranteed by Fannie Mae and Freddie Mac, or Ginnie Mae, and hands out cash. When the securities mature, the counter parties are required to take back the securities and return the cash plus interest to the Fed.

Since then, the New York Fed has engaged in two types of repo operations: Overnight repurchase agreements that unwind the next business day; and multi-day repo operations, such as 14-day repos, that unwind at maturity, such as after 14 days.

Total repos on the Fed’s balance sheet at the end of the day on November 6 amounted to $215 billion, unchanged from the prior week, and up $34 billion from a month earlier (Oct 2 balance sheet):

- $62.5 billion in overnight repos that the Fed took on Wednesday morning. These repos unwound Thursday morning. All prior overnight repos had already unwound before the date of the balance sheet.

- $152 billion in four multi-day repos – Oct 24, Oct 29, Nov 1, and Nov 5 – that had not yet unwound as the evening of Wednesday, Nov 6.

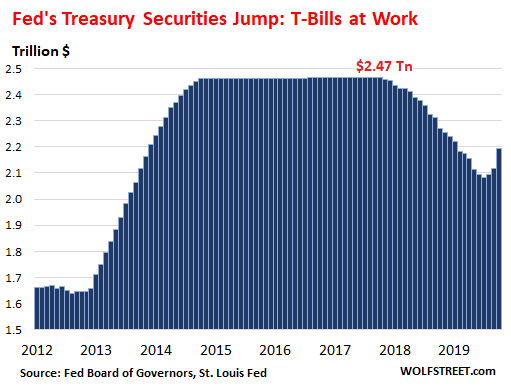

Treasury Securities jump: T-Bills at work.

During the month through the balance sheet as of Nov 6, the total amount of Treasury securities jumped by $77 billion. Most of this increase was due to the Fed’s switch to Treasury bills (T-Bills).

T-bills mature in one year or less. For the last few years, there had been no T-bills on the Fed’s balance sheet, which had been stuffed with longer maturities to force down longer-term interest rates. But this year, the Fed has abandoned that strategy. It is buying T-bills outright to raise excess reserves as part of its battle with the repo market, and it is replacing longer-dated securities that are maturing with a mix of securities that now include T-bills. And T-bills have surged from nothing to $66 billion, bringing total Treasury securities to $2.194 trillion:

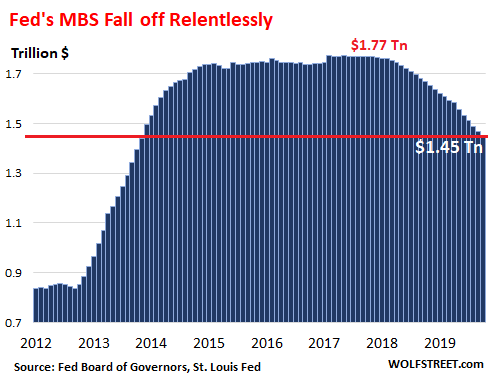

Mortgage-Backed Securities fall off

In October, the balance of Mortgage Backed Securities (MBS) dropped by $21 billion, exceeding the self-imposed cap of $20 billion per month for the sixth month in a row. At $1.45 trillion, MBS are now below where they had first been in November 2013:

Over the last six months, the Fed has shed $138 billion in MBS, exceeding its $120 billion cap for the period, and showing how intent it is in getting rid of them, even as it is loading up on T-Bills and repos.

Like all holders of MBS, the Fed receives pass-through principal payments as the underlying mortgages are paid down or are paid off. About 95% of the MBS that the Fed holds mature in 10 years or more, and the runoff is almost entirely due to these pass-through principal payments.

The Fed has stated that it wants to get rid of its MBS entirely because one, they’re awkward for conducting monetary policy; and two, they’re housing debt, and by holding them, the Fed gives preferential treatment to this debt over other forms of private-sector debt, and it said it wants to end assigning these kinds of preferences.

As expected, loading up on short-term securities, at the expense of long-term securities, has put downward pressure on short-term yields, and upward pressure on longer-term yields that have already risen, with the 10-year yield hitting 1.92% today, the highest since the end of July.

So the Fed is increasing its assets in huge post-Lehman-like leaps, with the $184 billion jump in September and the $94 billion jump in October to bail out the crybabies on Wall Street, so that the higher rates in the repo market won’t blow up some over-leveraged hedge funds or REITs that borrow in the repo market short term to cheaply fund their long-term bets.

Because indeed: Whose Bets are Getting Bailed Out by the Fed’s Repos & T-Bill Purchases? Read… What’s Behind the Fed’s Bailout of the Repo Market?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The MBS holdings and associated runoff are actually helpful rather than awkward right now (for the Fed), because it makes it possible for FRB to shift purchases from the long end (MBS) to the short end (T-Bills) without actually selling anything outright on the long end.

But personally, I’d much have preferred that FRB had never gotten into mortgage bonds in the first place.

By the way, any reference on the cited multiple reasons for FRB wanting to get rid of MBS? I did not see that specific wording in the earlier 2019/03/20 wolfstreet article, which is what google turned up.

This is all about keeping asset prices from collapsing. The Fed is a prop or crutch to that can never go away.

This year’s budget deficit is circa $1 Trillion. That is about $83 Billion a month of NEW debt hitting the market.

The Fed strangely, and not data driven at all as their claim, is buying $60 Billion a month in what is described a “non QE”.

The Fed is absorbing the deficit spending of the Federal Government. Period.

Is that their mandate? No. But who complains when they shoot stocks up to new highs each day? Certainly not the “watchers”.

And, next years projected deficit will be the same. So will the Fed be in there buying that extra $83 Billion each month?

Those who cover for the Fed say, “The Fed needs a larger balance sheet because as a % of GDP, etc. etc.”

But the Fed’s balance sheet only goes up when they buy securities, a measure previously reserved for needed injections of liquidity in special situations and banking needs.

One can deduce that perhaps this is indeed a special situation, one in which the Federal borrowing is sucking the liquidity out of the system and the Fed is compelled to offset.

But the “need” for a larger balance sheet only suggests that the “need” is a dangerous sign….the Fed is creating money to fund the government reckless spending and fund endless wars.

Using Repo to monetize government debt is full of inherent risk, on one side they monetize the intrinsic value of US Treasury paper, and on the other side cash for stock market speculators. The two are dangerously intertwined.

By keeping its darling bank control groups of billionaires from having to pay FMV repo (short term) interest rates to meet their current liabilities, through ultra low interest rate repo loans, the Federal Reserve banking cartel transfers more taxpayer money to the parasitic major banks. According to reports, this bankster subsidy rose to loans of $190 billi on a night.

If the Fed is seeking to help Wall Street (to prevent financial entities needing funds from the repo market from failing) and not the banks, it is exceeding its mandate. Thus, I would opine that it is likely that one or more of the major banks, which the Fed (since it is really a secret bank cartel, not a government agency or owned by the US government) focuses on protecting, may be short of funds, i.e., it cannot meet its current liabilities with its assets, so it is legally insolvent.

Keep in mind that each of the major bank’s net capital is reported as being about $60 to 250 billion. Thus, the $190 billion that reportedly has been needed in the repo market and the Fed has provided each night, indicates that one or more of the banks may have gone insolvent and need another bailout.

The Fed will keep this secret as it did before. See https://www.youtube.com/watch?v=dX2qvbznGKM. See also https://wallstreetonparade.com/2019/09/the-fed-is-offering-100-billion-a-day-in-emergency-loans-to-unnamed-banks-and-congress-is-not-curious-enough-to-hold-a-hearing/. See https://www.prisonplanet.com/judge-orders-fed-to-disclose-who-received-bailout-trillions.html.

If the fed is buying short term treasury notes and bills, why is long term treasury yields going up? If certain non govt entities have to buy, yet the fed absorbs all the short term treasury notes and bills, would they not instead buy long term bonds and thus drive the yields down? Are the long term yields going up because the fed is flooding the system with “not QE”, along with daily trade news hype floating risk assets, and the selling of risk off treasury bonds?

Confused

“If the fed is buying short term treasury notes and bills, why is long term treasury yields going up?”

The Fed is allowing long-term Treasuries to roll off the balance sheet when they mature, and it replaces them with a mix of maturities, including T-bills but fewer long-term securities. So the market has to absorb the long-term securities that the Fed doesn’t hold.

The Fed is also replacing its MBS, nearly all of which have maturities over 10 years, with Treasuries of mixed maturities, including T-Bills. This has the same effect – the market has to absorb the MBS that the Fed doesn’t hold.

All this removes the support under long-dated securities and allows their yields to drift up. It’s not a huge force, unlike selling those securities would be. But it’s there.

The forgotten and rarely mentioned THIRD mandate of the Fed is to “promote moderate long term rates.” The wisdom behind this is to maintain a balance between borrower and lender and to keep money flowing. Moderate means, “not extreme”, and as we sit with 4000 year lows in long rates, one can only notice the Fed ignores this mandate.

This ignorance has allowed the curve to invert.

Hold the Fed to their mandates.

In actuality the FRB ignores all these “mandates.” The FRB gives only lip service to unemployment, inflation, and, yes, “moderate long term rates.” The FRB has only one mandate, the original mandate: to be the “lender of last resort” and attempt to prevent the -ruptcy of banks. There is no corporation-ruptcy, no partnership-ruptcy, no sole proprietor-ruptcy. It’s a private club and you are not in the club.

So any stress test allows for bank to achieve a cry baby tactic?? I don’t understand how a fortress balance sheet is in jeopardy

So the Fed can’t turn off the life support, because the patient will die.

This will be permanent.

The patient will die anyway. As Ray Dalio has pointed out, the life support system is broken.

Normally when the financial economy crashes the real economy has a chance to recover. But not this time. Instead, in 2009, central banks were determined to preserve the ill-gotten gains of the financial economy, preventing the recovery of the real economy. Debt continues to increase faster than GDP, and most of the increase in GDP is in the financial economy, which produces nothing, and not the real economy, which produces everything.

For years the financial economy has continued to extract more from the real economy than it can produce. This can only reduce the real economy in real terms, which is why NIRPZIRP hasn’t helped: it does no good to put fertilizer on a parched field. The real economy can only recover if the financial economy reduces its rate of extraction, and it’s never going to do that. As the real economy declines, the financial economy has to squeeze harder.

The parasites know they are killing the host, and they have started to prepare accordingly by grabbing what they can while the grabbing is good.

I don’t trust Ray Dalio and his hand-wringing missives for one second. His writings are so contorted it gives me a headache.

Dalio did not become wealthy by being worried about poor people. Everything he says has a self-interested angle. I’ll believe him when he drops his fortune to poor people from a helicopter. Until then, hell no.

Dalio is very unconvoluted. If anything he fails to grasp some subtle points, but like most analysts his training and experience is in obsolete financial markets. This stuff now is moving way too fast, and even the Fed chief has no clue, trying to revive Repo? That will never work, and neither will NIRP in this economy. Potus and his tariffs, are laughable, Wall St is geared up for an agreement in which they will walk back all that stuff. Maybe they can go back and cancel the GD? I came in late, blessed that my head isn’t full of old school ideas.

Well how about this? Ray Dalio is from Wesport, CT. He just gave about $100 mil to the public school system. It will be matched by the State and other groups to total $300m

https://ctmirror.org/2019/04/08/after-the-donation-the-100-million-question/

In the past three years alone, the foundation, which Barbara Dalio co-founded with her husband, has donated $50 million to public education programs in Connecticut.

2 weeks ago, my wife got a job offer from Wesport public schools. They now have money. Thanks to Dalio.

Ray Dalio and Bill Gross have gotten a free ride from the financial press for too long, they always sounded like Bernie Madoff to me. Read about their weird corporate culture and TM cult affiliation. Wolf should do a writeup on them.

“Dalio did not become wealthy by being worried about poor people.”

He is not worried about them as “Poor People”.

He IS worried about them, as an important element, in the machine, that keeps him rich.

Hence when somebody like him is worried about them “Poor People” ALL is far from well with the machine/system.

Here is an ‘old school’ idea for you: you cannot ‘print’ wealth.

Correct!

The Fed has two mandates: 1) fund government deficit spending 2) inflate asset prices.

The Fed has two “tools” in their “toolbox”: 1) create a never ending gusher of new currency 2) tell the population their is no inflation, no matter how badly things spiral out of control.

The U.S. is living beyond its means and printing money to pay for out of control spending – no different than the cowardly, greedy governments that collapsed in days past. Powell has given the government a green light to spend without bounds and the government has accepted Powell’s largesse and pushed the accelerator to floor.

Anyone who can’t see the dire inflation catastrophe heading our way, like a massive meteor strike, is afraid to look up. The Fed has lied every step along this path, does anyone believe they will stop printing as we sink into an inflationary feedback loop? No! the Fed will ramp up printing in lock step with rising inflation to fund the government – same as all the other discredited money printers of the past.

Do not own currency! The courage to act – what delicious irony.

The Fed has THREE mandates.

“It is the Federal Reserve’s actions, as a central bank, to achieve three goals specified by Congress: maximum employment, stable prices, and moderate long-term interest rates in the United States””

from the official web site.

Those who continually mention only two do damage to the reality of what the Fed should be doing. IF the Fed had been held to their oft forgotten third mandate, the curve would not have inverted for starters. Why people refuse to mention this third mandate is a curiosity to me.

Moderate definition

“not extreme”.

So extreme lows in long rates, 4000 year lows in long rates, are indeed “not moderate”.

The Fed ignores this mandate of “moderate long rates”.

The Fed also promotes an inflation rate (2%) that yields price increases of 22% over ten years (compounding and aggregation).

Stable Prices? (btw, the Sept YOY core inflation was 2.4%. Anyone mention this over shot the Fed’s “target”?)

Whatever the mandate, the real purpose of the Fed is to enable politicians to get reelected by replacing taxes with slight of hand monetary policy.

Short story. There is a business in my state that is the lowest price place to purchase tires and have them installed. It’s a high volume place with a good system operating in a large 75 year old building. It doesn’t look like they waste one dollar.

It’s at the opposite spectrum of DC where it’s all hat and no cattle. Fancy buildings, $1000 per hour lawyers all feeding out of the pig trough. As some people say it’s theatre for ugly people.

Stimulus has become a crutch. And we know what happens when crutches are removed.

Bernanke promised the Fed would roll off the QE when things returned to normal and things improved. He even mentioned rates would normalize when unemployment dipped below 6.5%. Obviously, this didn’t happen.

The promises made when these unprecedented Quantitative Easings were occurring were false. And now they have become the norm, rather than an emergency measure.

I like Stockman’s analogy that the free market is like an old watch with many fragile gears making the thing work. The Fed and politicians are all the time trying to make it better with ham handed adjustments.

I suspect the Fed will eventually blow the system up with a false assumption. Let’s say 2% inflation rate. Well maybe that is not a good goal in an aging society. Japan seems to have proven this. One thing I hate about central bankers is they always take credit for good economic results. There really should be non-partisan academics that get a platform to empirically determine if Fed policy has helped or hurt the economy. Supposedly some academics have shown that Fed policy basically does not help the real economy. It’s kind of funny if that is true that the central planners for making the economy more efficient might be a very inefficient organization.

This will end badly or fail to do so.

No it WILL end badly How does this level of debt end any other way Think about it

But how will it. I keep seeing these it will end badly… But what are the specific seriesn of steps that are possible / likely as we “correct”?

specific series of steps:

1) fed saves the day again and again until big money wants out of dollar

2) dollar soars as assets are sold and markets tank.

3) dollar then tanks as those dollars are used to buy gold (and anything else real)

4) spot price of gold falls as premiums on physical blasts off

5) markets soar again but nobody cares because a haircut costs $10,000.00. US government openly monetizing debt. Helicopter money. Money money all around and still you cant afford anything….so print more!

6) gold goes no-offer

7) gold re-emerges at a much higher price. Financial markets are forever reduced in size and importance as nobody will use debt as savings or confuse savings with investing.

8)we all live happily ever after

Because it hasn’t yet. Despite all the belief it should have already.

I am concerned about the Feds duration shift. With USG bond yields rising and with the US having a $22 Trillion+ debt mountain to service even a 1/2 percent rise in debt service costs amounts to $100 billion annually. To put that in perspective, some Democrats have offered a 10% tax surcharge on million dollar plus incomes that will, supposedly, raise $635 billion in new revenue over 10 years but if debt servicing costs over that same period grow by $1 trillion instead of $635 billion in new revenue to fund this or that new benefit we will have to cut over $350 billion in existing spending to just stay even.

$23 Trillion+ ($22 Trillion is so 7 months ago)

Besides, what difference does it make, a number is just a number like any other number – just ask Dick Cheney or Paul Krugman (and that guy should know, he has a Nobel Prize so he must be smart, right?)

Modern Monetary Theory holds that the more the deficit spending, the more that money flows to the “people”…of course those people are those fully invested in stocks and got “nod” that the Fed will be overaccommodative for the foreseeable future and operate outside their mandates to stabilize prices and promote moderate long term interest rates.

Did you get the “nod” that the Fed would go rogue? Me neither, but those who “know”, who are in with the NY Fed and the powers that be are having a nice year. Free markets?

I think those words that debt doesn’t matter will go down in economic history books up there with the stock market is at a permanently high plateau or something like that.

Wolf,

I’ve always wanted to know how much money goes out to the individual countries that the US pays off to be allies?

All those UN agreements seem to have a quiet support this motion or bill on threat of funding cut off.

These UN agreements have gotten so insane now that they want to give natives compensation for disputes and forced consultations to all tribes involved in disputes. Taking the government power away that you need to consult before doing any project and adding a compensation factor. The natives love this UN resolution agreement.

Here is the link to the UN article.

http://harveyoberfeld.ca/blog/ndp-greens-adoption-of-indigenous-un-resolution-will-make-fast-ferries-fiasco-look-like-chump-change/

Hispanics everywhere should sue the Catholic Church in the international court at the Hague, for reparations after the Spanish inquisition.

No one expects the Spanish Inquisition.

“Taking the government power away that you need to consult before doing any project and adding a compensation factor.”

This has been standard operating procedure with just about all modern trade agreements: WTO, NAFTA and its successor, TPP (scuttled), and others. It’s about global corporations getting what they want and overpowering legislatures.

Example: the US Congress passed a law that required the origin of beef to be on the label so consumers knew where it came from. Canada and Mexico fought this law in the WTO, and the US lost, and the law that Congress passed and that consumers wanted, was overturned, and we still don’t know where out beef comes from. This crap is happening all over the place now.

These are mechanisms of international dispute settlements.

The UN can only spend the money it collects. Most of it goes to salaries, fancy offices, vehicles, and things like that. The rest is distributed. The budget of the UN is public and you can check it out.

While that may be true processors are not restricted from labelling their beef and everything we buy is grown and processed in Oregon or locally.

Cows are fungible. Mexican hamburger tastes the same as Kansas hamburger.

Should we start labeling our oil and copper domestic or imported?

Origin labeling is one of the fundamental things in a market economy. “Made in…” is on a lot of stuff. When I buy a steak, I want to know where the cow was “raised,” where it was “harvested,” and where the meat was processed and packed. This might impact my decision on how much I’m willing to pay, or whether or not I’m even going to buy it. The Canadian and Mexican beef industries were afraid of exactly that and wanted to keep me in the dark.

So now I don’t buy steaks unless it says where it is from — for example, “grass fed beef raised in Texas” or “grass-fed beef raised in California” sounds a lot more appealing to me than a blank. The thing is, no one is forced to put origin labels on beef, but if they’re proud of where the beef is from, they put it on the label. And I’m willing to pay a little extra for that.

this is naive in the extreme. food safety is not a given. E Coli and Prions are a real concern. I will not buy any food with China origin, Costco is selling more and more of it lately.

I think this is the current ‘populist’ backlash in US and Europe. People figured out that globalization had winners and losers with generally the further down on the food chain the bigger loser you were and the political system had become almost totally unresponsive.

Simply; are we all watching a repeat of Lehman’s Repo 105 operation designed to cover up losses; but this time involving many more actors?

The fed decided that they didn’t like an inverted yield curve, so why not just buy short bonds and let the long end run off. Voila! Normal yield curve.

Is there anything in this world that the federal reserve doesn’t think they have a right to tamper with and control?

They want to select the president. They want to fight globull warming.

They want to set the price of the stock mkt.

If the people of the US sit back and take this shit, then they will get exactly what they deserve in the end.

High stock prices and no globull warming?

Huh?

Is there anything in this world that the federal reserve doesn’t think they have a right to tamper with and control?

They delegate most tampering and control to corporations that are in on the collusion, so technically the answer is yes. Functionally the answer is a maniacal belly laugh.

hole in the net?

This repo stuff looks like a soap opera starring the FED and irresponsible sons in law and family ties with daughters who are shop-a-holics….you get the idea. There must be emotional entanglements somewhere for such waste and bail outs.

Heh. Maybe Janet Yellen’s evil twin will have an affair with Powell? Tune in tomorrow to find out!!

Wait a minute: I thought Janet Yellen and the evil twin were actually the same person with a split personality! Now you are telling me there actually two Yellen’s?

And I must have missed the episode when Jerome Powell is revealed to be Alan Greenspan’s child, long thought to have killed when he was buried by a freak avalanche of dollar bills crashing down on him.

But it’s not a U-Turn and it’s not QE so there’s nothing to worry about.

Just relax and get ready for DOW 35,000 and bigger and better bubbles.

Just relax and get ready for DOW 35,000 and bigger and better bubbles.

It is always a mistake to feed them. It only makes them hungrier.

I thought feeding them after midnight made them monsters.

If the Fed were smarter now, they’d have an optimal control algorithm to keep the equities market and housing market on average, flat. Or at least rising slightly less than inflation until the wages catch up (after years of being pummelled).

If they are listening to politics, they will drive both markets to the moon before the next election.

It is always after midnight, Bob.

If you don’t feed them you have some hope of keeping them in a cage where they might eat each other, which is good because you be crunchy and taste good with ketchup.

And ten dollar gasoline and loaves of seeded rye as well

So, I went looking for a graph of how repo rates trend. To me this would could show how hard the Fed is babying the market or leaning on them. Obviously, the Fed entered the market to steady things. Since they have this control, shouldn’t they let some of the players slip through the safety net to get the others to swim harder, or are they making it nice and safe to swim however they want.

Did not look for a graph long, but not a quick find to post a link.

The New York Fed tracks various repo rates at the close, and outliers during the day.

For SOFR, TGCR, and BGCR go to https://apps.newyorkfed.org/markets/autorates/rates-search-page?rateType=R3

Check the one you want or all three, put in the data range, and click “find.” This will give you the data in a table, and you can build charts.

Found one with a long time period:

https://tradingeconomics.com/united-states/repo-rate

SOFR as an American LIBOR is a complete fraud. They manipulate it lower by throwing billions of taxpayer dollars into the system. LIBOR is at least set according to business conditions, though lately I think they have had to track EFFR, while their expiration date is about up, so we can look forward to financial repression as far as the eye can see.

RE “LIBOR is at least set according to business conditions”

You mean rigged according to the needs of a few London banks?LOL

Just require all transactions > $1,000,000 notional to be recorded on a public exchange, publish the data and let the market decide what rates it believes and wants to use in its contracts.

I’ve heard in more than one place that our biggest bank has moved its IOER to 30Y TBonds. I would assume, if this is true, that IOER was a warm and cozy place to be and they want to stay in mom’s basement. I can’t imagine that this didn’t happen without mom’s input and approval. This signals that rates are as high as they are ever going to be.

BTW Wolf, I think the majority of MBS maturities are 10Y or less, not more.

Petunia said: This signals that rates are as high as they are ever going to be.

Yes, and Powell has indirectly said just that.

Powell said we can’t raise rates at this inflation level. We, this inflation level has remained essentially very closely what it is for a very long time and is deliberately rigged to stay their at an inaccurate, rigged low level.

IMO we now need to start thinking of these highly suppressed rates and QE as essentially being permanent. As in, like Japan.

Rate might not rise but the collateral value of those bonds may take a hit. Why would anyone buy the bottom in yields, when the secondary market has plenty of supply of better rates of return unless of course that puts a hit on the par value of new stuff, but the dollar is too high anyway, if we really want all those substandard jobs to return.

Petunia,

Currently the Fed holds $1.37 trillion in MBS that are maturing in over 10 years, see chart linked below. That’s roughly 94% of its total holdings of MBS ($1.44 trillion). Yes, it’s quite amazing…

https://fred.stlouisfed.org/series/MBS10Y

Sorry, I’m used to seeing MBS sliced and diced, I don’t remember when mortgage pools were sold and kept intact.

Re: BTW Wolf, I think the majority of MBS maturities are 10Y or less, not more.

Nope most of the MBS the Fed holds mature on 2033 or later.

Look at the VALUE of MBS the Fed has on its books. H.4.1

2. Maturity Distribution of Securities, Loans, and Selected Other Assets and Liabilities, November 6, 2019 (in millions)

OVER 10 years, 1,367,317

Total: 1,445,776**

**The current face value shown is the remaining principal balance of the securities.

Re: I’ve heard in more than one place that our biggest bank has moved its IOER to 30Y TBonds.

I assume they moved RESERVES to 30Y Treasury bonds?

I am not sure how a bank can do that. I wonder what are the transactions.

I have wondered about this all day.

Well here we are in quite a tough spot aren’t we? I mean most of us on this discussion board. We are facing even more asset inflation at the hands of the Fed central bank, but also harbor a fear of it all coming crashing down. The past couple of months have taught us that the Fed will step in and print whenever there is a liquidity problem. This means the Fed will not allow large scale asset deflation. The concept of “sound money” has been thrown into the dust bin. I admit I had hope that QE would not be used again, and that hope is now gone. What to do? There are some very smart people on this discussion board, maybe too smart for our own good. I would like to hear what you think we should do with our wealth now given recent actions of the Fed.

Practicing what I preach: Get out of the system! Live a life apart from population centers and convert your money to hard assets (land with timber on it, for example) where much of your sustenance is created on and by your own assents – as little reliant on fiat money as is reasonable.

RD, Splitting my time between Northern CA and the Northern front range of CO, the idea living among trees in a forest is hazardous to one’s health:) Seriously though, given what has transpired over the past couple of months it is hard to argue that QE is not here to stay. All I can think is to get out of cash.

Sounds like a reasonable plan to me I would add some junk silver and a dozen or so Krugerands to that and sleep pretty darn well I would love some timber acreage but where I live it’s very pricey(touristy)

Get out of the system!

Best to do it sooner, while you still have a choice, than later, when you won’t.

You can keep my things when they come to take me home.

I saw an article recently that said the US would revert back to an agrarian society in the long run because of the loss in high wage jobs or something.

Some of the comment suggestions about putting assets into productive real estate seem to support that.

Land, cattle, chickens, hay (cause you have to winter feed animals), timber and wildlife.

Low interest rates inversely cause high asset prices. If you think rates are going even lower, buy assets. If you think they are staying the same, then you can’t make a return by investing in paper. So accept risk and be a hard money lender.

“I mean most of us on this discussion board. We are facing even more asset inflation at the hands of the Fed central bank, but also harbor a fear of it all coming crashing down.”

You make an excellent point. The very same people here who swear up and down that a crash is imminent are also freaking out about inflation. Pick one or the other folks, but you can’t have both. Assets can’t inflate and crash simultaneously.

The other thing is the last “crash” wasn’t that bad. It was bad in real time since there was fear of what else would happen. But if you look back on it, 10 years later, it was a short term (2-3 year) blip in an an otherwise long term upward trend. Personally I benefited from the crash. My income didn’t suffer, and I was able to buy a lot of stuff cheap. I don’t want it to happen again, but if it did, I’d probably be no worse off than it not happening.

Personally, I will never recover from the crash, so I don’t agree with you. I do recognize that there are people, like you, who weren’t affected, but there were also people, like me, who were devastated by it.

People rarely understand that the post Great Depression banking restrictions were designed to keep banks from blowing asset bubbles. They knew, from the GD, that most of the people who were harmed were just honest folks trying to make a living. The bankers stayed rich and the innocent suffered.

By Reagan, we had forgotten that.

Same for me, Petunia: but I managed, luckily, to find a much more satisfying life in consequence.

In fact, it woke me up in the best way possible.

So many are still sleep-walking……

and no reason JSRguy to put “crash” in quotes. We are clearly still within that crisis, one which wasn’t staunched by trillions in welfare payments to the failed bankers. The proof? how about zero interest rates 11 years later.

Petunia,

Would you mind giving us your story? I always enjoy your point of view and wonder what your life experience is?

Not true according to many economists who are predicting a inflationary depression Inflation in things we need to survive ie food, healthcare etc

Inflationary deflation. I love it.

Get yourself some physical Gold and Silver and you should be good to go That’s what central banks worldwide are doing

Good time, too. Gold and silver being dumped in the last few days. The paper stuff anyway. But you know, don’t fight the FED and follow the herd.

Never understood how a little gold or silver helps.

It would seem to me that if you thought gold or silver was the answer you would put all your assets in those metals because if there is a crash a little bit won’t help you very long.

Geez, just read history…

Lael Brainard (Fed) comment today, per CNBC, concerning juicing the financial markets via changing the neutral interest rates, due to future climate change (thus reaffirming once again, the fed goal is to juice the financial markets, now due to climate change along with dozens of other manufactured reasons on their public relations list):

“For example, if prices of properties do not accurately reflect climate-related risks, a sudden correction could result in losses to financial institutions, which could in turn reduce lending in the economy. The associated declines in wealth could amplify the effects on economic activity, which could have further knock-on effects on financial markets,” Brainard said.

——-

Climate change looks to be another excuse to create more inequality, via the never ending stock markets P/E expansion via ZIRP and QE. A logical person would start reducing exposure to assets that have a high probability of financial losses from future climate change. A speculator would embrace the fed put on all income producing asset appreciation, and the speculator has a good chance of getting bailed out once again by ZIRP. Logic is not a healthy trait in a fed centrally controlled economy. I am amazed at the feds creativity to stroke further inequality, via “financial markets” and now every income producing asset one could imagine, along with art, cars, and even rare whisky booze. At some point, some elected officials are going to have to end the fed, be it ten years from now, 100 years, who knows. The feds do not seem to have any comprehension of “unintended consequences”, to the point where I question if they are unintended or not.

And I say this from someone who has levitated into the top 1% by fed engineered policies, for just owning assets tied to interest rates that now have no natural price discovery, and zero time value. This is not going to end well, for any of us, be it tomorrow of eight years from now. Not much one can do so why worry, just try to stay a step ahead and diversify in ways that exceed the feds destructive powers. Perhaps Mars will be a good place to invest in the distant future, until the fed takes over that planet too, for the sake of the poor, of course!

I hate to break it to you but we are the next Hong Kong.

Wow, tou guys are just wanting to be anxious about everything today, aren’t you?

The current “tough spot” is pretty much the same one we’ve been in forever. Loose-money inflation. Risk of a market crash, unemployment, inadequate income, not being able to save enough to retire, not being able to afford a home, missing out. Fear that the government is either incompetent, not operating with your interest in mind, or both.

Well guess what folks. Whenever the sun rises each day, most of the 7,000,000,000 people on the planet get out and work to make their lives better, and in working together they make everyone’s life better. Nature causes trouble and the greedies and the crazies need to be restrained, but by and large everyone keeps things going. (Can you believe that most successful organizations even have Democrats and Republicans working side by side?)

Now, if you have extra wealth to invest, you’re already extremely lucky, so quit whining and do your job. Yes, you too have a job to do, just like the rest of us. You have to find the people out there who are the best at helping their customers and clients, and you have to invest in them, to help them do more. You may get a share of the profits in return.

But don’t invest in businesses or people whose don’t align their interests with their customers’, who are parasites on society, who promote war or fear or broadcast lies and propaganda. And don’t lend money to those who waste it. And know this: If all you’re doing is chasing “personal returns” regardless of big-picture consequences, you’re doing it wrong. Just look at the opioid manufacturers to realize that becoming “money-rich” by destroying others isn’t worth the price.

As a conscientious investor, unfortunately the system won’t always give you the choices you’d prefer. Workers in particular often get stuck with 401K plans with terrible options. But even in a 401K plan with only 5 choices, you can always identify which is the least-worst option. Power corrupts, so don’t invest in the giant S&P500 corporations – buy the small-cap funds. They’ll earn about the same over time, and you won’t have to read the daily scandal sheet and feel bad about owning a tiny slice of the latest corporate evildoings. (Or, if you do, at least it’s on a smaller scale…)

Do what you gotta do, but then get the money out of those bad systems as soon as you can, and put it where you have more control. Freedom to pursue your own happiness is the greatest right that you have – use it. Diversify enough so you won’t get killed by a few bad choices, but not so much that you can’t keep track of how your choices are doing. Don’t try to predict the future, just let things ride. If you can’t sleep at night, wiggle out of your worst-performing investments and get back on the job: find the people out there who are doing the best job of making things better for their customers and clients, and invest in them to help them do more…

Investors hold huge amounts of power and despite what Wall Street claims, it is NOT a passive job. The more investors express our preferences for how we want the world to be, the better the world can be. The more shenanigans we tolerate passively, the worse it will be.

Back in the late ’60s I tried to get a Selective Service deferment as a “conscientious investor” but SS wouldn’t accept it. Back then you could lend your savings to a local institution where professional investors would create a portfolio of mostly local assets that would return 4-5%/yr on your savings. These local institutions were called banks. Not to be confused with what are now called banks.

My current allocation is about 10% stocks, 20% vanguard money market, 70% vg short term treasuries. Risk in long term treasuries and stocks too high for my 23 year time horizon. No debt. Limiting withdrawals to 2% annually.

The Fed is giving us a false sense of security. Once the market pukes 30% or so people are going to panic and the Fed can’t stop it til it overshoot on the downside. It’s always been that way, why is this going to be different. It’s a long way down to fair value, probably 1300 or so. No reason we can’t temporarily bust through that number. The US is the last major stock market inflated, but the air will come out.

It amazes me how much the US is moving away from a Free Market to a Managed Market. Most disturbing is how much of this “management” benefits the wealthy at the expense of the average America or even the poor. Moreover, the “people” can’t even find out who gets all this free money or why? Meanwhile the people’s representatives in Washington spend their time focusing on impeachment (a year out from an election?), legislating nothing while their public servants give money to banks and hedge funds?

Its always been that way, just more and more people falling off the wagon

Yup, for sure I know a few in the Hamptons believe it or not One guy who runs a woman’s clothing shop lives with his mom at age 40 because he can’t afford to buy or even rent a place of his own Another “ artist” who lives in an elderly gay couples garage attic because it’s free He performs “ handyman” work in exchange for his living arrangements

A little problem of having all this sponsored Fed liquity is that all this fake money is not going only to paper shit but also to hard assets, namely to housing which has been the value storage king. While the Fed and alikes, are not willing to deflate this hards assets, along with all those paper shit flying around, people are finding harder to have a home. The riots we’re seeing in some cities all around the world reflects a deep insatisfaction among young people. It wouldn’t hurt CB bankers and their friends politicians to read a little bit about history. All revolutions has something in common…

I think the risk is the demands on the private sector worker become too much. For me at 50 it was no longer worth it once I did the math.

I have friend that is 49 that is slowly killing herself in corporate life. 45 minute commutes and expense of that. All the deductions from paycheck, then the mortgage, property taxes, the slow erosion of health you start feeling trapped. When you are in really deep it’s hard to find your way out of the forest.

Suckered?

David Stockman said a year ago that there is no way the US government is going to be able to borrow an addition 1.2 trillion and the Fed run off a trillion on its balance sheet. It’s just force feeding too much into the market. Is the repo problem a sign that markets couldn’t swallow all the debt?

Indeed. Add Ambrose Evans-Pritchard to the list …

“The International Monetary Fund has presented us with a Gothic horror show. The world’s financial system is more stretched, unstable, and dangerous than it was on the eve of the Lehman crisis.”

And here is this missing $1.5 trillion. The market just printed it.

https://www.nasdaq.com/articles/fed-chair-speech-cost-investors-15-trillion-2018-10-05

Cheers,

C’mon, that’s not a serious analysis. Markest dropping an average 0,44% after Fed speeches?? The pumping that Fed has done caused a 500% gain on the SP500 since 2009. That is the truth. JPM are dishonest crooks putting out such nonsense propaganda.

Yes.

10 yield yield is just shy of 2% this morning. Looks like fears of a worldwide recession were overblown (once again).

Did you actually check out the auction results?

$39,784,731,300 is the largest every amount accepted the Treasury for 10Y.

The HIGH rate was 1.809%. But look at the LOW rate. 0.880%.

Yes 5% of the amount of accepted competitive tenders was tendered at or below that yield.

Some people (5%) were willing to buy the 10Y at almost 1% (100 points) lower. Same last Sept 11.

I think Japanese and Europe central proved you can peg interest to the floor, but that bullet is gone for at least a generation. Next bullet was buying corporate bonds and stocks. In away it is just eating the seed corn til we become France and then if we keep going Cuba.

It is a bit strange that so many people think that things will just go on forever, as long as the Fed is here to rock the cradle. The basic theory seems to be that financial history has ended at this plateau, where

we will be happily ever after. (Happy compared to a regression to the mean)

One thing to remember: deflation operates with the speed of a snake bite. A rubber balloon takes a minute to blow up and less than a tenth of a second to burst. In 1929 the gains of a year were wiped out in an hour and those of a decade were wiped out in less than a week.

A balloon half- inflated, if pricked with a pin, will not explode but will deflate slowly.

But if over-inflated, it explodes almost instantly and violently.

There are so many precarious debt dominoes right now that no physical printing could possibly catch up with their almost simultaneous collapse. (During the GFC the Fed had to farm out some printing of the $100 bill to Switzerland)

People don’t form a line to exit a theater on fire, or even one suspected of being on fire.

The move to electronic trading of everything, and the travel of news at the speed of light might make the Crash of 29 seem gradual.

But as with belief in an afterlife, even if not true, a another Crash never happening would be nice. It would be even nicer if the H-bomb is the first weapon never, ever used.

We are on the collapse arc, common to all civilisations; with some peculiarities related to our technological and complexity level, that is all.

Over-population, degradation of the resource base, pollution, over-complexity unable to sustain itself: these are the ingredients common to all collapses.

There is no escape, the only thing to debate is the timing and regional phases.

Very good point. Similar analogy could be a heavy ball on the edge of the table. Unless it’s too close, relatively small force is enough to keep it there, but once moved too far for any reason, it will not be the case any more :)

My theory is that computers will allow someone to blow up the financial world. In the old days it took time for governments to buy the paper, ink and presses to print to infinity. It took paper contracts and physical checks and processing times. In my life I might have generated a couple of million of economic activity. A trader can punch a few keys and do a multi-billion dollar trade. One person at AIG could do hundreds of billions of dollars of derivative contracts for the banks. Probably less than 50 unelected central planners created maybe $12 – 15 trillion in a few years. You can be pretty sure next time it’s going to be $50 -$100 trillion.

Party likes its 2009. I really don’t get it, unless a) Powell is head of the Trump reelection campaign – all fed chiefs support their president- b) the internals in this market are deteriorating – while new credit is piling up at a record pace – c) some banks are in trouble, allusion to JPM and one wonders if the Fed has been too much on the Treasury side of the issue, and not enough on the banks side, – quasi nationalizing the charters for QE? – if some of these banks want to get out from under, and refuse to play the Repo game – it’s alright with Fed that money has a LOTTA takers, hence the rally in NYSE stocks funded with money from foreign bourses??. And Wendy’s is gonna pay a lot to one of these banks to buy back it’s stock for them??

a) Powell is head of the Trump reelection campaign

____

Totally!!!!

Average fund rate yield by year

2019: 2.27%

2018: 1.79%

2017: 1.00%

2016: 0.39%

2015: 0.13%

2014: 0.09%

2013: 0.11%

2012: 0.14%

Yes, it is truly amazing – the lengths they must now continually go to in order to keep this debt-based, fiat money system from imploding into the deflationary Black Hole of its own creation.

Does anyone know when the US government makes good on a defaulted mortgage or student loan whether it just picks up the payments or pays out in one lump sum? I thought Wolf would know this one.

I don’t think there is such a things as defaulted student loan. They will withhold your degree or garnish wages until it is paid back.

They default when the old student dies with an outstanding loan balance and no assets.

Many older peopel officially own nothing, its simpler. Only a vindictive fool will pay money to bankrupt a stone.

This 2019 version of repo was buried in the Dodd -Frank law. Congress installed a repo auto feature for the fed post Dodd-Frank to insulate themselves from accountability . Congress got un-comfortably close to any accountability a decade ago and they made sure this would not happen again. Congress has no responsibility other than re-election and working on getting rich, very time consuming.The Creature from Jekyll Island is responsible for their constitutional duty ,ergo,repo, not that August body called The US Congress. Funny thing that the people who elect them , no matter the party, keep getting the same result. Apparently my fellow Americans can’t even agree that we ,collectively ,deserve earning a honest time value of money . Fact is most Americans can’t tell you what the requirements are for money , much less a time value for money. Money , to them,is a smart phone transaction.The certainty of growing old and infirm without a time value of money places all of us at risk .

$11.5 trillion by January?

https://seekingalpha.com/article/4303983-federal-reserve-watch-fed-underwriting-another-market?isDirectRoadblock=true

Financial Times weighs in on repo market.

https://www.ft.com/content/fe562cbe-feee-11e9-b7bc-f3fa4e77dd47

The average daily Treasury PAR Value at the DTCC GCF Repo is $48.723 billion per day for the last 250 trading days it was open. MBS average daily is $90.795 billion per day.

Since the Fed Repo is almost reaching $100 B per trading day (mostly in Treasuries), then they really have taken over the most of the repo market.

FT

Repo ructions highlight failure of post-crisis policymaking

The old ‘Greenspan put’ is now a Powell promise: fear not, the Fed is there for you

November 5 2019

FILE- In this Feb. 5, 2018, file photo, the seal of the Board of Governors of the United States Federal Reserve System is displayed in the ground at the Marriner S. Eccles Federal Reserve Board Building in Washington. On Thursday, Sept. 12, 2019, the Senate confirmed President Donald Trump’s nomination of Michelle Bowman to serve a full 14-year term on the seven-member Federal Reserve board. (AP Photo/Andrew Harnik, File)

© AP

A big failure of post-crisis financial policy was laid bare when the US repo market buckled in September.

Many have debated why the market went wrong, so fast. The Federal Reserve was so spooked that it did not wait for answers before stepping in. The central bank’s gross cumulative support for the market — which allows banks and investors to borrow cash in exchange for Treasuries and other high-quality collateral — will top $11.5tn by the end of January, according to our sums. The Fed did not just stabilise the repo market. Now, it is the repo market.

Repos were once the liquidity-providing “plumbing” of the financial system. Now, they have taken on another role because post-crisis rules demand that financial institutions hold far bigger balances of safe assets — at a time when yields on such assets are low or even negative.

The only way to comply with these rules while still eking out a profit is to squeeze each dime out of safe-asset holdings through repo market financing. Borrowers use high-speed funding flows from repo transactions to boost profitability through derivatives trading and other higher-return activities.

This transformation in repos was presaged by the equity market. The Fed’s bond-buying and interest rate-cutting programme initially supported the macroeconomic recovery. The extension of quantitative easing, however, changed its nature from an output-boosting policy into an equity-market stimulus. Yield-chasing became a market imperative, creating strong incentives for participants that hold safe assets such as Treasuries to boost returns by leveraging their positions through the repo market.

None of the new rules demanding large safe-asset holdings is necessarily wrong, but each has consequences that the Fed failed to anticipate.

At the same time that the market’s demand for repos grew, banks’ capacity to meet that demand diminished. Tougher post-crisis requirements have made big banks considerably safer, but no bank is willing to stride into the repo market if that jeopardises compliance with new intraday liquidity standards or the broader rule book.

Exposing these repo risks in such dramatic fashion would ordinarily lead participants to run for cover. Instead, the market is so vibrant that the Fed has had continuously to increase the amounts with which it supports overnight and even longer-term deals. The best explanation for this insouciance? De facto nationalisation of the market.

Desperate to keep short-term rates within its desired range, the Fed chose not to use its backstop — known as the discount window, where it provides higher-cost loans to banks, backed by eligible collateral — or other emergency-liquidity powers. Using these transparent fallbacks would have allowed the repo rate to settle in a new, orderly, and perhaps smaller marketplace. Instead, the Fed just opened its vault.

Thus, what should have been a learning experience is now a new, powerful incentive for moral hazard. Speculative bets can be made with the understanding that taxpayers, through the central bank, will bail out any bad calls. The old guarantee of the “Greenspan put” stabilising equity prices is now buttressed by a Powell promise: fear not, in the dollar-based global funding market, the Fed is there for you.

Back in the day, the central bank was supposed to be a lender of last resort, supporting banks which had no other way of funding themselves. This safety net was designed so that banks could take households’ deposits and turn them into savings that enabled wealth accumulation and loans to support growth. But after 2008, the Fed became the market-maker of last resort, lowering rates whenever equity markets trembled. Now, it is the market lender of last resort, too.

To be sure, its current repo backstop puts the Fed in a supporting role — it steps in only after primary lenders step back. Theoretically, the market could operate without the Fed, but it does not because lenders love having this backstop and the central bank is always there to provide it.

The Fed also offers reverse repos, a longstanding operation designed to keep market interest rates within the central bank’s target range, no matter the risks participants take. And now the central bank is considering making its new repo operations permanent, through a so-called standing facility. In for a penny, in for a pound — and, if you are a central bank, in forever.

But with central banks providing a backstop for both equity and funding markets, what is next? Some governors have decided that they must add digital currencies to their payment systems, not only to protect the globe from Facebook’s Libra, but also as a new tool that might better transmit monetary policy.

This could curtail lending, but some central banks have the cure for that: they will lend too, at least for projects such as sustainable energy that suit policymakers’ idea of what constitutes useful economic activity.

The market’s trains would indeed all run on time. But central bankers — not market forces — would dictate who gets on and who is pushed off.

The writer is managing partner at Federal Financial Analytics

The central bank’s gross cumulative support for the market — will top $11.5tn by the end of January, according to our sums.

Hmmm. Where did they get this huge number???

By the end of the week (Wednesday, November 6, 2019) I calculate that 2,696.14 billion has been used by the Fed for repo.

There are about 12 weeks till the end of January 2020. 13 for the reporting date Jan 5 to 6. The last 3 weeks averaged 423.415 billion per week. Assume that is the going rate, then multiply by 12 weeks and add the amount already used. That only totals $7,777.12 billion and not $11.5 trillion.

Fake news or not?

It could be. The FT author doesn’t go into the details on how it arrives at the $11.5 trillion.

The article did mention the discount window which is one of the Fed’s tools to accomplish the same task. The difference is the collateral would be subject to actual market pricing. This would interfere with the interest rate suppression of the current Federal Funds Rate. Bernanke also chose not to use the discount window in 2008 so as not to reveal the problem banks in the Federal Reserve System. I think this may be why we are seeing the Fed using the repo market and not the discount window. This is clearly a liquidity problem. Entities need cash and are swapping collateral in the short term to complete transactions and buying the collateral back at a very low interest rate charge. They don’t have enough cash and if they were to sell the same securities in the open market we would actually have price discovery. There’s a reason why the Fed doesn’t want price discovery.

Wes – thanks for the good posts!

I forgot to acknowledge the author, Karen Petrou, of the preceding article in the November 5, 2019, FT. My apologies.

Congress needs to feel some pain to get the signal to rein in spending and raise taxes. It would seem the Fed needs a mechanism to administer pain to Congress, rather than being their enabler.

We can see the drill in EU. Countries were going bankrupt and the market clearing price got too high somewhere around 7% so central bankers took over bond market to buy time for politicians to get their act together. It’s not going to happen.

A 100 year German has had their savings destroyed twice by central bankers and maybe a German central bankers could convince someone to fix the problem but politicians are mostly lawyers that live in their legal world apart from the surf’s who will run a gray market and a black market when things go haywire.

Mr. Richter, the St. Louis Fed responds to the Repo Program:

Why the Fed Should Create a Standing Repo Facility

Wednesday, March 6, 2019

monetary policy communication

By David Andolfatto, Senior Vice President and Economist, Federal Reserve Bank of St. Louis; and Jane Ihrig, Associate Director and Economist, Federal Reserve Board of Governors

The Federal Open Market Committee (FOMC) is locking down its long-run monetary policy implementation framework. We know it will consist of a floor regime characterized by an ample supply of reserve balances. We argue below that the FOMC should include a standing repo facility as a part of this framework.

Ample Reserves

Ample reserves in the present context means the minimum level of reserves necessary to permit the efficient and effective conduct of monetary policy through the use of the Federal Reserve’s administered rates, without the active management of the supply of reserves.1 Market participants are projecting ample reserves in the $1 trillion range—a level much higher than their precrisis average of approximately $20 billion. What could plausibly account for a fiftyfold increase in the necessary supply of reserves? Is the FOMC really doing all it can to minimize the necessary level of reserves in line with its 2014 Policy Normalization Principles and Plans?

Reserves as High-Quality Liquid Assets

Many commentators have pointed to post-2008 Basel III and Dodd-Frank regulations as having generated a large regulatory demand for high-quality liquid assets (HQLA), which include reserves. At first glance this explanation may seem unsatisfactory because HQLA also includes, among other things, U.S. Treasury securities.

Why should banks prefer reserves to higher-yielding Treasuries? One explanation is that Treasuries are not really cash equivalent if funds are needed immediately. In particular, for resolution planning purposes, banks may worry about the market value they would receive in the sale of or agreement to repurchase their securities in an individual stress scenario.2

Consistent with this possibility, Federal Reserve Vice Chair for Supervision Randal Quarles noted, “Occasionally we hear that banks feel they are under supervisory pressure to satisfy their [high-quality liquid assets] with reserves rather than Treasury securities.”

To quantify this liquidity consideration, a recent post on the Federal Reserve Bank of New York’s Liberty Street Economics blog suggests that the eight domestic Large Institution Supervision Coordinating Committee’s banks collectively may want to hold $784 billion in precautionary reserves to cover their immediate liquidity needs in times of stress.

Converting Treasuries to Reserves through a Standing Repo Facility

These banks would presumably not want or need $784 billion in reserves if higher-yielding Treasuries could be liquidated at a modest discount on a reliable basis in times of stress. The Fed could easily incentivize banks to reduce their demand for reserves 3 by operating a standing overnight repurchase (repo) facility that would permit banks to convert Treasuries to reserves on demand at an administered rate.4 This administered rate could be set a bit above market rates—perhaps several basis points above the top of the federal funds target range—so that the facility is not used every day, but only periodically when a bank needs liquidity or when market repo rates are elevated.

With this facility in place, banks should feel comfortable holding Treasuries to help accommodate stress scenarios instead of reserves. The demand for reserves would decline substantially as a result. Ample reserves—and therefore the size of the Fed’s balance sheet—could in fact be much closer to their historical levels.

Additional Reasons for a Standing Repo Facility

Lending to Banks in Good Standing

There are several other reasons why introducing a standing repo facility makes sense. First, as discussed here, it is a way for the Fed to lend cash to banks that are in good standing and have high-quality Treasury securities as collateral but may find themselves short of cash. Importantly, this facility would not suffer from stigma problems that make the discount window an ineffective tool in these circumstances.

Complementing Overnight Reverse Repo Facility

Second, the facility should be thought of as a complement to the existing overnight reverse repo facility, which sees take-up vary with financial market conditions. Together, these two facilities would create the standard deposit and lending tools used in typical floor-operating regimes, such as at the European Central Bank.

Eliminating Need to Estimate Ample Reserves Level

Third, the repo facility would eliminate the need, ex ante, to make a judgment about the level of reserves likely to be ample. The interest rate ceiling established by the repo facility implies that the Fed can retain interest rate control independent of any shock to reserve demand or to the Fed’s nonreserve liabilities.5

As reserves drain from the system, the point at which they become scarce would be demonstrated by a market signal: The federal funds rate and other money market rates would move up relative to the target range.

At this point, banks would start to use the repo facility, which would automatically inject reserves into the system and prevent rates from rising any further. That is, the facility would ensure there were ample reserves in the banking system and preserve interest rate control, while at the same time allowing the Fed to safely discover the lower end of “ample.”

Minimizing Payment of Interest on Reserves

Finally, apart from being consistent with the 2014 Policy Normalization Principles and Plans, a repo facility would minimize the politically bad optics of the Fed paying interest on reserves (of which a large share goes to foreign banks). It seems both wise and proper to let the Treasury directly bear the interest expense associated with the regulatory demand for HQLA.

Conclusion

Even though balance sheet normalization is well underway, we think it is never too late to introduce a repo facility. The FOMC would learn over time whether the facility is working to reduce the demand for reserves.

The FOMC could do so, for example, by permitting reserves to run off organically with the growth of currency in circulation while remaining confident that interest rate control would be maintained through the repo facility.

Notes and References

1 This definition follows from the FOMC’s 2014 Policy Normalization Principles and Plans (PDF) and its January 2019 Statement Regarding Monetary Policy Implementation and Balance Sheet Normalization.

2 This is presumably less of a concern in a collective stress scenario, in which “flight to safety” concerns would likely cause Treasuries to trade at a premium.

3 Our proposal is consistent with a remark made in the November 2018 FOMC minutes that mentions the possibility of adopting strategies that provide incentives for banks to reduce their demand for reserves.

4 We emphasize a standing facility because discretionary repo transactions were a normal part of the Fed’s open market operations prior to 2008. That is, we are not advocating practices that would be unfamiliar to the Fed.

5 The possibility of a repo facility was mentioned in the December 2018 FOMC minutes: “However, reducing reserves to a point very close to the level at which the reserve demand curve begins to slope upward could lead to a significant increase in the volatility in short-term interest rates and require frequent sizable open market operations or new ceiling facilities to maintain effective interest rate control.”

Additional Resources

On the Economy: Banks’ Demand for Reserves in the Face of Liquidity Regulations

On the Economy: Why Are Banks Regulated?

On the Economy: Bank Supervision and the Central Bank: An Integrated Mission

Posted In Banking, Federal Reserve | Tagged david andolfatto, jane ihrig, fomc, banking, reserves, repo, high quality liquid assets, treasuries, monetary policy

https://www.stlouisfed.org/on-the-economy/2019/march/why-fed-create-standing-repo-facility

Wes,

Yes, I cited and linked this article a few times, concerning the standing repo facility. In fact, in April the St. Louis Fed came out with a follow-up article that refined some of the issues in its March piece that you cited. I included and linked both here (and in some other articles):

https://wolfstreet.com/2019/09/20/fed-admits-plan-a-of-controlling-money-market-rates-fails-shifts-to-plan-b-repos-which-was-plan-a-till-2008/

Make no mistake, Treasury is very aware that the trump deficit and thus budget needs all the help it can get ASAP, as we head into a possible shutdown in a few weeks. trump’s wall doesn’t fit in the current budget, due in large to the fact that interest on the debt is making the trump budget-pie smaller and smaller. Thus treasury can play with Fed’s balance sheet to buy a little time. It’s complicated, but Wolf can explain it better ….